Johnson Controls: The Building Intelligence Empire

I. Introduction & The Building Controls Revolution

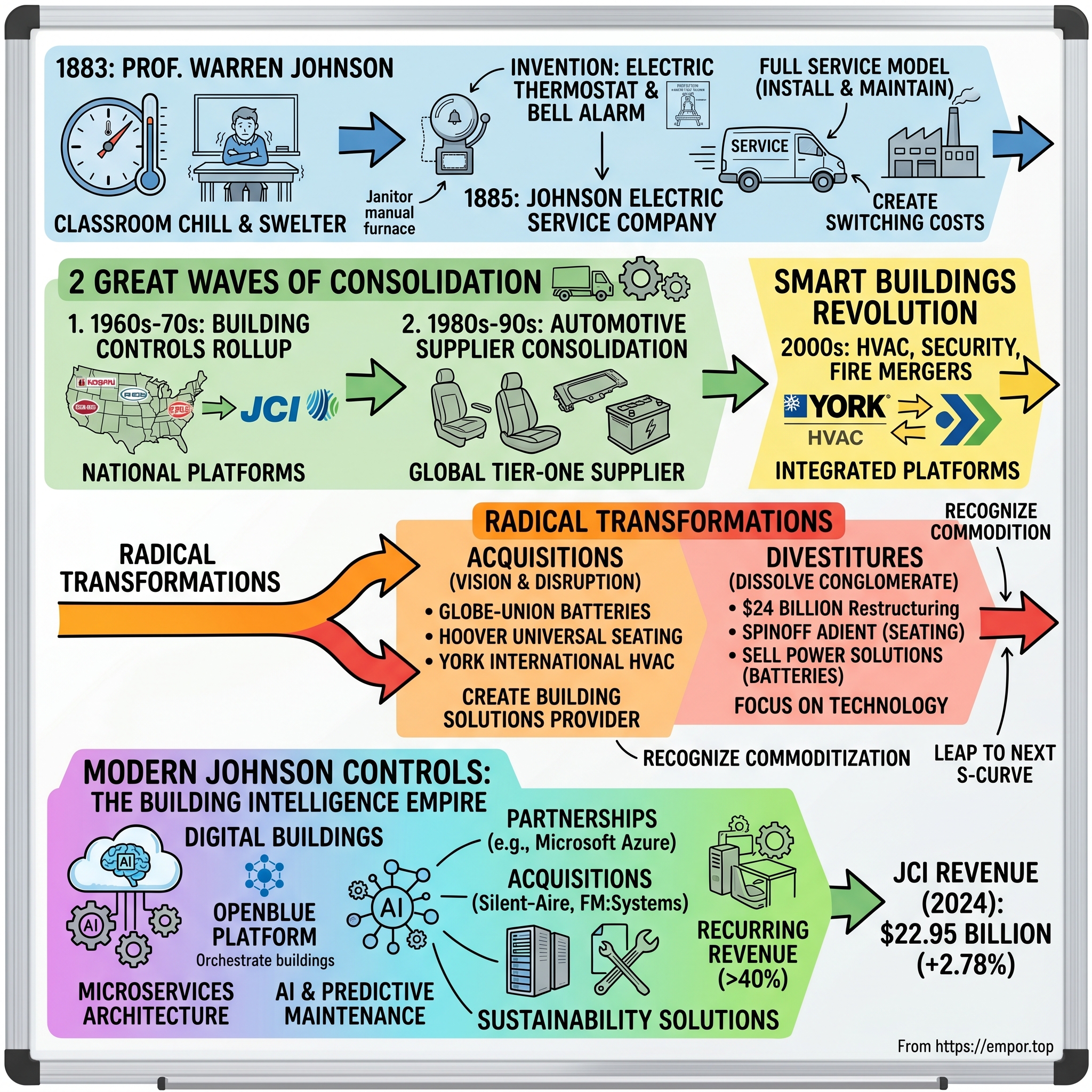

Picture a Wisconsin classroom in 1883, where students shiver through morning lessons until the janitor stokes the furnace, turning the room into a sweltering box by afternoon. Professor Warren Johnson watches his students' attention drift with the temperature swings, their learning hostage to the whims of manual heating. His solution—an electric thermostat that automatically rings a bell in the basement when temperature adjustment is needed—seems quaint today. Yet this simple invention would spawn a $27 billion global empire that now orchestrates the intelligence of the world's most sophisticated buildings.

The question that drives this story isn't just how a thermostat company survived 140 years—plenty of industrial firms have managed that feat through sheer inertia. The real puzzle is how Johnson Controls repeatedly reinvented itself at precisely the right moments: from pneumatic controls to computers, from building management to automotive interiors, from batteries to smart buildings, and most dramatically, from an American industrial conglomerate to an Irish technology platform company. Each transformation required not just vision but the willingness to destroy what came before.

Today's Johnson Controls bears little resemblance to Warren Johnson's electric service company. The thermostats are still there, buried deep in the product catalog, but they're now nodes in vast digital networks that monitor everything from air quality in Shanghai skyscrapers to energy consumption in Dallas data centers. The company that once sent technicians to manually adjust building temperatures now deploys artificial intelligence to predict HVAC failures before they happen.

This journey—from mechanical controls to digital ecosystems—offers profound lessons about industrial transformation. It's a story of brilliant acquisitions and painful divestitures, of tax inversions and political backlash, of family dynasties and corporate raiders. Most importantly, it's about recognizing when your core business is becoming commoditized and having the courage to leap to the next S-curve before it's too late.

The modern Johnson Controls emerged from three great waves of consolidation in American industry. First came the building controls rollup of the 1960s and 70s, where regional players were assembled into national platforms. Then the automotive supplier consolidation of the 1980s and 90s, creating global tier-one suppliers. Finally, the smart buildings revolution of the 2000s, where traditional HVAC and controls companies merged with security, fire, and software firms to create integrated platforms.

At each juncture, Johnson Controls didn't just participate—it led. The company's acquisition track record reads like a who's who of American industrial history: York International's century of HVAC innovation, Globe-Union's battery empire, Hoover Universal's automotive seating dynasty. But perhaps more impressive than what Johnson Controls bought is what it chose to sell. The $24 billion in divestitures between 2016 and 2019 represents one of the largest corporate restructurings in American history, systematically dismantling a conglomerate to create a focused technology company. The controversy surrounding Johnson Controls isn't just about corporate taxes or portfolio strategy—it's about the fundamental question of what an American industrial company owes to the country that nurtured it. When the company inverted to Ireland in 2016, saving $150 million annually in taxes, critics saw betrayal. Management saw survival. The truth, as always in corporate strategy, lies somewhere in between.

What makes Johnson Controls particularly fascinating is how it navigated the transition from hardware to software, from products to platforms, from ownership to orchestration. In 2024, JCI's revenue was $22.95 billion, an increase of 2.78%, modest growth that belies the radical transformation underneath. The company that once manufactured every component now focuses on the intelligence layer that makes buildings think.

This is ultimately a story about timing—knowing when to buy, when to build, when to hold, and most crucially, when to let go. It's about recognizing that in technology transitions, the companies that try to preserve their past rarely survive to see their future. Johnson Controls didn't just adapt to change; it engineered its own disruption before someone else could do it for them.

II. Warren Johnson's Innovation & Early Years (1883–1960s)

The classroom was always either too hot or too cold. Warren Johnson, teaching at the State Normal School in Whitewater, Wisconsin, noticed his students' attention wandering as temperatures swung wildly throughout the day. The janitor, stationed in the basement near the furnace, had no way of knowing when classrooms needed heat adjustment. Johnson's solution was elegantly simple: an electric thermostat connected to a bell system that would alert the janitor when temperature changes were needed. Patent number 281,884, issued in 1883, would become the foundation of a global empire.

But Johnson was more than an inventor—he was an entrepreneur who understood that the real value wasn't in selling thermostats but in solving temperature problems. In 1885, he founded the Johnson Electric Service Company in Milwaukee with a radical business model: instead of just manufacturing devices, the company would install and service complete temperature control systems. This full-service approach, revolutionary for its time, created switching costs and customer relationships that would endure for decades.

The early systems were pneumatic marvels—compressed air pushing through miles of copper tubing hidden in walls, opening and closing valves with precise choreography. Johnson's engineers became artists of air pressure, designing systems that could maintain different temperatures in hundreds of rooms simultaneously. The Milwaukee Public Library, one of their first major installations in 1898, showcased the technology's potential. Visitors marveled at reading rooms that stayed comfortable year-round without constant manual adjustment.

By the 1920s, Johnson Service Company (renamed in 1902) had evolved from a regional player to a national force. The company pioneered the "dual-duct" system that could provide heating and cooling simultaneously to different zones of a building—revolutionary in an era when most buildings still relied on opening windows for cooling. Their installation at the Bankers Life Building in Indianapolis in 1925 featured 250 thermostats controlling temperatures in individual offices, a level of customization previously unimaginable.

The company's survival through the Great Depression revealed its strategic genius. While competitors collapsed, Johnson Service Company thrived by shifting focus from new construction to retrofitting existing buildings for energy efficiency. Building owners, desperate to cut costs, discovered that Johnson's control systems could reduce fuel consumption by 20-30%. The company's service contracts, providing steady recurring revenue, proved more valuable than equipment sales during the economic downturn.

World War II transformed Johnson from a controls company into a precision manufacturer. The company's expertise in pneumatic systems proved invaluable for military applications—from submarine climate control to bomber altitude regulators. Johnson produced over two million precision instruments for the military, earning the Army-Navy "E" Award for excellence five times. This wartime experience in high-volume, high-precision manufacturing would reshape the company's capabilities permanently.

The post-war building boom created unprecedented opportunity. America was constructing office towers, schools, and hospitals at a frenetic pace, and every one needed climate control. Johnson's systems became increasingly sophisticated—the installation at Chicago's Prudential Building in 1955 featured 4,000 control points managed from a single panel, a precursor to modern building automation systems. The company's "Centerline" control system, introduced in 1959, used electrical signals instead of compressed air, marking the beginning of the transition from pneumatic to electronic controls.

But perhaps the most important development of this era was cultural. Johnson Service Company created what employees called the "Johnson Way"—a philosophy combining technical excellence with an almost obsessive focus on customer service. Service technicians were trained not just to fix problems but to understand building operations holistically. They became trusted advisors to building managers, creating relationships that lasted decades. One veteran technician recalled being summoned to the same Milwaukee office building every Tuesday for fifteen years, not because anything was broken, but because the building manager valued his insights.

The company's ownership structure during this period deserves scrutiny. Unlike many industrial firms that went public early, Johnson remained closely held by the founding family and employees through the 1950s. This allowed long-term thinking that public markets might not have tolerated. The decision to maintain large service departments, for instance, delivered lower margins than pure manufacturing but created an installed base that would prove invaluable.

By 1960, Johnson Controls (renamed in 1974, but we'll use the modern name for clarity) dominated the North American controls market with a 35% share. The company operated from 50 branch offices, employed 3,000 people, and generated $30 million in annual revenue. But more importantly, it had created a business model that was incredibly difficult to replicate: deep technical expertise, vast service networks, and switching costs that made customers reluctant to change providers.

The seeds of future transformation were already visible. Johnson's 1960 acquisition of Penn Controls, a manufacturer of electrical controls for original equipment manufacturers, signaled recognition that the pneumatic era was ending. Penn brought electrical expertise and OEM relationships that would prove crucial in the coming digital revolution. The acquisition price—$12 million, nearly half Johnson's annual revenue—showed remarkable conviction in the electronic future.

Warren Johnson died in 1911, never seeing his company's greatest triumphs. But his fundamental insight—that buildings needed intelligence, not just equipment—remained the company's north star. Every subsequent transformation, from pneumatics to electronics to digital to AI, followed the same pattern: Johnson Controls would provide not just products but complete solutions, not just installation but ongoing service, not just technology but expertise. This service-centric model, born in those Wisconsin classrooms, would prove remarkably resilient through technological upheavals that destroyed countless industrial companies.

The transition from founder-led entrepreneurship to professional management could have killed the company's innovative spirit. Instead, Johnson's successors understood that the company's true asset wasn't its patents or factories but its relationships—with customers who trusted Johnson technicians in their mechanical rooms, with employees who spent entire careers perfecting their craft, with suppliers who collaborated on custom solutions. These relationships, painstakingly built over decades, would become the foundation for expansion far beyond Warren Johnson's wildest dreams.

III. The Computer Revolution & Diversification (1970s–1980s)

The oil embargo of 1973 found Johnson Controls in an extraordinary position. While Americans waited in gas lines and thermostats were turned down to 65 degrees by federal mandate, Johnson's phones rang incessantly. Building owners, facing energy costs that had quadrupled overnight, desperately needed what Johnson had spent ninety years perfecting: the ability to control energy consumption with precision. But the company's response would transform it from a controls specialist into something entirely different—a diversified industrial conglomerate that barely resembled its roots.

The JC/80, unveiled in 1972, represented Johnson's first serious foray into the digital age. This wasn't just an upgraded thermostat—it was a minicomputer system that could manage an entire building's operations from a single terminal. The timing was fortuitous; the system launched just as energy management transformed from a convenience to a survival imperative. The JC/80's killer feature was its simplicity: building operators needed minimal training to program heating schedules, monitor energy consumption, and identify efficiency opportunities. Within three years, Johnson installed over 1,000 systems, each one generating recurring service revenue that would continue for decades.

But the real revolution came through an unexpected channel: acquisition. Fred Brengel, who became CEO in 1972, recognized that Johnson's building controls expertise, while valuable, was inherently limited by construction cycles. His solution was audacious—transform Johnson into a multi-industry powerhouse by acquiring businesses that shared certain characteristics: technical complexity, service intensity, and recurring revenue potential.

The 1978 merger with Globe-Union represented this strategy's apotheosis. Globe-Union, founded in 1911, had built America's largest automotive battery business through relentless innovation. Their manufacturing process, using pioneering automation and quality control, produced batteries with failure rates below 1%—exceptional in an industry where 5% was considered acceptable. The merger, technically structured as Johnson acquiring Globe but practically a merger of equals, doubled Johnson's revenue overnight to $600 million.

The cultural collision was immediate and jarring. Johnson's white-collar engineers, accustomed to designing custom solutions for sophisticated building owners, suddenly shared a company with blue-collar battery workers manning production lines in Milwaukee and Indiana. Globe-Union executives, who had built their careers on manufacturing efficiency and cost reduction, found themselves reporting to managers obsessed with service contracts and customer relationships. The integration took years and never fully succeeded—the businesses operated as essentially independent divisions united only by financial reporting.

Yet the strategic logic proved sound. Globe-Union's battery business generated enormous cash flow—over $50 million annually by 1980—that funded Johnson's expansion into building automation. The automotive industry's just-in-time revolution meant that battery suppliers who could guarantee delivery within hours, not days, commanded premium prices. Globe-Union's distribution network, with warehouses positioned near every major auto plant, created a moat that competitors couldn't easily cross.

The 1985 acquisitions of Hoover Universal and Ferro Manufacturing pushed Johnson even deeper into automotive supply. Hoover Universal brought expertise in injection-molded plastics and automotive seating, generating $800 million in annual revenue. Ferro Manufacturing added metal seating components and mechanisms. Suddenly, Johnson Controls could offer automotive manufacturers complete seating systems—from the metal frame to foam cushions to plastic trim—all from a single supplier.

The transformation was remarkable. In 1970, Johnson Controls was essentially a building controls company with $50 million in revenue. By 1988, it was a $2.5 billion conglomerate with leading positions in building controls, automotive batteries, and automotive seating. The company that Warren Johnson founded to regulate classroom temperatures now produced seats for Ford F-150s and batteries for General Motors.

This diversification strategy reflected the era's prevailing wisdom. Conglomerates like General Electric and ITT had demonstrated that professional management and financial discipline could successfully operate disparate businesses. The theory held that corporate headquarters could allocate capital more efficiently than public markets, moving resources from mature businesses to growth opportunities. Johnson's leaders, influenced by this thinking, saw themselves as portfolio managers as much as operating executives.

The computer revolution, meanwhile, continued transforming the controls business. Johnson's JC/85/40 system, launched in 1985, represented a quantum leap from the JC/80. Using distributed processing—a revolutionary concept where intelligent controllers throughout a building communicated with a central computer—the system could manage buildings with unprecedented sophistication. Energy consumption could be optimized in real-time based on occupancy patterns, weather forecasts, and utility rates. The system's modular architecture meant buildings could start with basic temperature control and add capabilities over time, creating upgrade paths that locked in customers for decades.

The Penn Controls acquisition from 1963 finally paid massive dividends during this period. Penn's relationships with original equipment manufacturers meant Johnson components were embedded in millions of HVAC units, refrigeration systems, and industrial controls. When these units needed service or replacement, building owners naturally turned to Johnson. This "razor and blade" model—selling components cheaply to OEMs while capturing profitable aftermarket service—generated margins exceeding 20%.

But success bred complexity. By 1989, Johnson operated through four distinct business units—Controls, Batteries, Seating, and Plastics—each with different customers, technologies, and competitive dynamics. The promised synergies rarely materialized. Building controls salespeople couldn't sell batteries; automotive purchasing managers didn't care about HVAC expertise. The corporate headquarters in Milwaukee, expanded multiple times to house growing administrative staff, became a monument to organizational complexity.

Financial engineering partially masked operational challenges. Johnson's accounting practices, while legal, pushed boundaries. The company capitalized software development costs aggressively, recognized service contract revenue optimistically, and used numerous off-balance-sheet entities for real estate and equipment financing. These techniques improved reported margins and returns on assets but obscured the true economics of increasingly disparate businesses.

Labor relations grew increasingly strained. The United Auto Workers, representing battery and seating workers, viewed Johnson's Milwaukee headquarters with suspicion. Strikes in 1981 and 1987 disrupted production and revealed deep cultural divisions. Controls engineers earning comfortable salaries struggled to understand battery workers fighting for hourly wage increases. The company that had prided itself on employee loyalty now managed through collective bargaining agreements and grievance procedures.

Environmental challenges compounded difficulties. Battery manufacturing involved lead, acid, and other hazardous materials. Johnson inherited numerous contaminated sites from Globe-Union, requiring expensive remediation. The controls business, previously seen as clean technology, faced scrutiny over refrigerants that depleted the ozone layer. Regulatory compliance costs soared while liability risks multiplied.

Yet through this turbulent period, Johnson's core controls business continued innovating. The company pioneered "intelligent buildings" that integrated HVAC, lighting, security, and fire systems through common networks. The Metasys facility management system, introduced in 1989, used open protocols that allowed equipment from different manufacturers to communicate—a revolutionary concept in an industry built on proprietary standards. This openness strategy, controversial internally, positioned Johnson as the integration platform for building systems.

The 1980s ended with Johnson Controls at a crossroads. The company had successfully diversified beyond building controls, creating a $3 billion industrial conglomerate with leading positions in multiple markets. But the complexity was becoming unsustainable. Each business required different capabilities, faced distinct competitors, and demanded specialized knowledge. The financial markets, once enamored with conglomerates, now penalized them with "diversification discounts." Activist investors began questioning why automotive batteries and building controls belonged in the same company.

The answer would come from an unexpected source: globalization. As the Berlin Wall fell and markets opened worldwide, Johnson's leadership recognized that winning globally required focus and scale. The company couldn't be a subscale player in multiple industries; it needed to be a leader in chosen fields. This realization would drive the next phase of transformation, as Johnson Controls began a three-decade journey of acquisitions and divestitures that would ultimately recreate it as a pure-play building technologies company.

IV. Global Expansion & The York Acquisition (1990s–2005)

The 1990s dawned with Johnson Controls facing a paradox: the company dominated North American markets but remained virtually unknown elsewhere. While competitors like Honeywell and Siemens built global empires, Johnson generated 85% of revenue domestically. Jim Keyes, who became CEO in 1993, understood that globalization wasn't optional—automotive manufacturers were consolidating globally, commercial real estate was internationalizing, and building standards were harmonizing across borders. Johnson needed to become a global player or risk becoming prey.

The automotive seating business led the international charge. When Honda announced plans for a new Accord plant in Marysville, Ohio, they insisted suppliers match Honda's global footprint. Johnson's response was aggressive: new technical centers in Japan and Germany, joint ventures in Mexico and Brazil, and wholly-owned facilities in Eastern Europe. By 1995, Johnson operated 75 seating plants across 20 countries, following automotive manufacturers as they globalized production.

The transformation of automotive seating from commodity to technology product enabled this expansion. Johnson didn't just manufacture seats—it engineered complete interior systems. The company's breakthrough came with the 1994 Ford Taurus, where Johnson designed an integrated cockpit combining seats, instrument panels, and door systems. This "total interior" capability commanded premium prices and created switching costs that made Johnson indispensable to automotive manufacturers.

The numbers were staggering. Automotive seating revenue grew from $1.2 billion in 1990 to $8 billion by 2000. Johnson became the world's largest automotive seating supplier, producing 25 million units annually. The company's just-in-time manufacturing capability—delivering seats to assembly lines in sequence, sometimes with less than four hours' notice—created operational dependencies that locked in customers. When General Motors attempted to dual-source the GMT800 platform seats in 1998, the complexity of Johnson's sequencing systems made switching impossible mid-production.

But the controls business transformation proved even more dramatic. Johnson's 1996 acquisition of facilities management operations from IBM and Honeywell brought something unprecedented: responsibility for complete building operations. Instead of just installing and servicing equipment, Johnson now managed entire facilities—from HVAC maintenance to security staffing to energy procurement. This "outsourcing" model transformed customer relationships from vendor interactions to strategic partnerships.

The facilities management strategy reflected profound changes in corporate real estate. Companies increasingly viewed buildings as non-core assets, preferring to focus on their primary businesses. Johnson offered to handle everything—equipment, people, contracts, compliance—for a predictable monthly fee. The value proposition was compelling: reduced costs through Johnson's scale, improved reliability through specialized expertise, and transferred risk through performance guarantees.

Marquee contracts validated the strategy. Johnson won facilities management for Microsoft's Redmond campus, pharmaceutical giant Pfizer's research facilities, and the U.S. Department of Energy's national laboratories. Each contract generated $20-50 million in annual revenue with margins exceeding those of traditional controls installation. More importantly, these contracts typically ran 5-10 years with renewal rates above 90%, creating predictable, recurring revenue streams.

The York International acquisition in 2005 represented Johnson's boldest strategic move. York, founded in 1874, had built one of the industry's most respected HVAC equipment businesses. The company manufactured everything from residential air conditioners to massive centrifugal chillers for skyscrapers. York's global footprint—manufacturing in 20 countries, distribution in 120—complemented Johnson's controls and services capabilities perfectly.

The $3.2 billion acquisition price raised eyebrows. Johnson paid 12 times EBITDA for a cyclical manufacturing business with 8% operating margins. Critics argued Johnson was overpaying for a commodity product manufacturer in a mature industry. But Johnson's leadership saw something different: the opportunity to create the industry's first integrated building solutions provider. By combining York's equipment with Johnson's controls and services, the company could offer complete building systems from a single source.

The integration strategy was sophisticated. Rather than simply bolt York onto existing operations, Johnson reimagined the entire customer experience. Building owners could now work with one company for equipment selection, controls integration, installation, commissioning, and ongoing service. Johnson's Metasys controls were embedded directly into York equipment, creating seamless interoperability. Service technicians were cross-trained on both controls and equipment, eliminating finger-pointing when problems arose.

The financial engineering behind the York acquisition deserves scrutiny. Johnson funded the purchase through a complex structure involving $1.2 billion in cash, $800 million in assumed debt, and $1.2 billion in new Johnson Controls debt. The company immediately sold York's Unitary Products Group to Barclays Private Equity for $400 million, effectively reducing the net purchase price. Johnson also negotiated an aggressive tax structure that allowed rapid depreciation of York's manufacturing assets, generating cash tax savings exceeding $200 million over three years.

Geographic expansion accelerated through the York platform. The acquisition brought major manufacturing facilities in China, India, and Mexico—countries where Johnson had minimal presence. York's joint venture with Guangzhou Refrigeration in China provided entry to the world's fastest-growing HVAC market. The Indian operations, centered in Pune, served as a beachhead for South Asian expansion. Within two years, Johnson's Asia-Pacific revenue doubled to $2 billion.

The integration revealed unexpected synergies. York's centrifugal chiller technology, when combined with Johnson's controls expertise, enabled revolutionary efficiency improvements. The YZ magnetic bearing chiller, launched in 2007, used Johnson's variable-speed drives and predictive analytics to achieve efficiency levels 40% better than conventional systems. This technological leadership allowed premium pricing even in commodity categories.

But the York acquisition also exposed Johnson to new risks. HVAC equipment manufacturing was capital-intensive, cyclical, and brutally competitive. Asian manufacturers, particularly from South Korea and China, were entering global markets with aggressive pricing. The commercial construction cycle, which drove large equipment sales, proved more volatile than Johnson's traditional controls and service business. When the 2008 financial crisis struck, York's new equipment orders collapsed 40% within six months.

The cultural integration proved equally challenging. York's engineers, proud of their company's 130-year heritage, resented absorption into Johnson Controls. The companies had different approaches to everything from product development (York favored revolutionary innovation; Johnson preferred incremental improvement) to customer service (York sold through distributors; Johnson used direct sales). Turnover among York's senior management exceeded 50% within two years of the acquisition.

Environmental regulations created both opportunities and challenges. The phase-out of ozone-depleting refrigerants required complete redesigns of HVAC equipment. Johnson invested over $500 million developing new refrigerant technologies, betting that regulatory compliance would drive replacement demand. The strategy worked—building owners facing regulatory deadlines had little choice but to upgrade equipment, driving a multi-year replacement cycle that generated billions in revenue.

The digital transformation of buildings accelerated during this period. Johnson's Building Efficiency Business introduced revolutionary capabilities: predictive maintenance using machine learning, energy optimization through real-time analytics, and remote monitoring via internet-connected sensors. The company's Panoptix platform, launched in 2004, aggregated data from thousands of building sensors to identify efficiency opportunities invisible to human operators. Early adopters reported energy savings of 15-25%, paying for the technology within 18 months.

Labor arbitrage became increasingly important to competitiveness. Johnson shifted production from high-cost locations to Mexico, Eastern Europe, and Asia. The company's Reynosa, Mexico complex employed 10,000 workers producing automotive seats at wage rates 80% below U.S. levels. Similar dynamics played out in HVAC manufacturing, with Chinese factories producing equipment at costs that made U.S. production uneconomical for all but the most sophisticated products.

By 2005, Johnson Controls had transformed into a truly global enterprise. International revenue exceeded $7 billion, representing 40% of the company total. The company operated 300 facilities worldwide, employed 140,000 people, and served customers in virtually every major market. The building efficiency business alone generated $5 billion in revenue with operating margins approaching 12%—exceptional for an industrial company.

Yet success contained seeds of future challenges. The company now operated in three distinct industries—building efficiency, automotive seating, and batteries—each requiring different capabilities and facing unique competitive dynamics. The promised synergies between businesses remained elusive. Capital allocation decisions became increasingly complex as each division demanded investment while shareholders expected returns. The conglomerate structure that had enabled growth was becoming a constraint on value creation.

The next phase of Johnson's evolution would require difficult choices. The company that had spent decades accumulating businesses would need to learn the discipline of divestiture. The transformation from diversified industrial to focused technology company would prove as challenging as any in Johnson's long history, requiring not just strategic vision but the courage to destroy what previous generations had built.

V. The Tyco Merger & Tax Inversion Controversy (2016)

The boardroom at Johnson Controls' Milwaukee headquarters was tense on January 24, 2016. CEO Alex Molinaroli had just finished presenting the most controversial proposal in the company's 130-year history: a merger with Tyco International that would relocate Johnson's legal domicile to Ireland. The tax savings were undeniable—$150 million annually—but board members understood the political firestorm that would follow. An American industrial icon, built with American innovation and nurtured by American customers, was about to become Irish.

The strategic logic extended far beyond taxes. Tyco brought world-class fire protection and security businesses that perfectly complemented Johnson's building efficiency portfolio. The combined company would offer unprecedented integration: HVAC systems that responded to fire alarms, security systems that integrated with access controls, and building management platforms that orchestrated everything seamlessly. In an era where buildings were becoming intelligent ecosystems, the merger created the industry's most comprehensive solutions provider.

But the tax inversion aspect dominated headlines. Johnson Controls would merge with Tyco in a complex transaction where Tyco technically acquired Johnson, but Johnson shareholders would own 56% of the combined company. This structure—known as an inversion—allowed the merged entity to adopt Tyco's Irish domicile and its 12.5% corporate tax rate, compared to the 35% U.S. rate Johnson faced. The annual savings of $150 million would flow directly to the bottom line, improving earnings per share by nearly 10%.

The political reaction was swift and brutal. Presidential candidate Hillary Clinton issued a scathing statement: "Johnson Controls begged the administration and Congress for help during the auto rescue, and now they want to avoid paying taxes after we saved them." She was referring to Johnson's automotive battery business receiving indirect support during the 2008-2009 automotive bailout, when government assistance to General Motors and Chrysler kept Johnson's largest customers afloat.

The criticism stung because it contained truth. Johnson's automotive business had teetered on bankruptcy during the financial crisis. Orders collapsed 45% in six months. The company eliminated 20,000 jobs and closed dozens of facilities. Without government intervention to save the automotive industry, Johnson might not have survived. Now, critics argued, the company was abandoning the country that had saved it.

Senator Bernie Sanders was even more direct: "Johnson Controls is gouging the American people. They have no allegiance to this country. Their only allegiance is to their bottom line." He proposed legislation that would block inverted companies from receiving federal contracts—a serious threat given Johnson's extensive government business managing federal buildings and military installations.

Johnson's management mounted a vigorous defense. They argued the merger wasn't primarily about taxes but about creating a global leader in building technologies. The combined company would have the scale to compete with European giants like Siemens and Schneider Electric, who enjoyed lower tax rates in their home countries. Without the merger, Johnson would remain at a competitive disadvantage, potentially becoming an acquisition target itself.

The integration challenges were monumental. Tyco itself was a complex organization, assembled through decades of acquisitions and spin-offs. The company had been led by Dennis Kozlowski, who went to prison for looting hundreds of millions from the company. Subsequent management had worked to restore credibility, but Tyco still carried reputational baggage. Its fire and security businesses, while market-leading, operated independently with different systems, processes, and cultures.

The numbers were staggering. The combined company would have revenue of $30 billion, 170,000 employees, and operations in 150 countries. Johnson's building efficiency business would merge with Tyco's fire and security operations to create a $17 billion building technologies giant. The integration required harmonizing thousands of products, consolidating hundreds of facilities, and merging dozens of IT systems.

Cultural differences proved immediately problematic. Johnson Controls, despite its global reach, remained quintessentially Midwestern—conservative, engineering-focused, and relationship-oriented. Tyco's culture, shaped by years of deal-making and restructuring, was more transactional and finance-driven. Johnson employees spoke of "customer intimacy" and "technical excellence." Tyco employees focused on "margin expansion" and "working capital efficiency."

The executive shuffle following the merger revealed underlying tensions. George Oliver, a Johnson Controls veteran who had run the automotive business, was passed over for CEO in favor of Molinaroli. Several Tyco executives departed within months, citing cultural incompatibility. The integration team, supposedly balanced between both companies, was dominated by Johnson personnel who imposed Johnson's systems and processes on Tyco operations.

Operational integration proceeded in phases. First came the combination of overlapping functions—finance, human resources, legal—eliminating thousands of redundant positions. Next, the merger of go-to-market organizations, combining Johnson's direct sales force with Tyco's distributor networks. Finally, the integration of product development and manufacturing, consolidating overlapping facilities and product lines.

The promised synergies proved elusive initially. Customers complained about confusion—who should they call for service? Which products were still available? Sales force integration created chaos as territories were reorganized and compensation plans changed. Several major customers, frustrated by service disruptions, threatened to switch suppliers. The company's claim of $500 million in annual synergies looked increasingly optimistic.

The tax benefits, however, materialized immediately. Johnson's effective tax rate dropped from 29% to 13% in the first year post-merger. The company repatriated billions in overseas cash at minimal tax cost, funding share buybacks and debt reduction. The financial engineering worked exactly as planned, even as operational integration struggled.

Regulatory scrutiny intensified. The European Commission investigated whether the merger violated competition rules, ultimately requiring divestiture of certain product lines. The U.S. Treasury Department, concerned about the wave of inversions, issued new regulations making future inversions more difficult. Johnson Controls had executed one of the last major inversions before the door effectively closed.

The workforce reductions were severe. Johnson announced 7,000 job cuts within six months of the merger, primarily in administrative and support functions. Manufacturing consolidation eliminated another 5,000 positions over the following year. Communities that had hosted Johnson facilities for decades watched as operations moved to lower-cost locations. Milwaukee, Johnson's birthplace and longtime headquarters, saw its corporate workforce shrink by 40%.

Customer reception was mixed. Large, sophisticated buyers appreciated the expanded capabilities—one company could now handle all building systems. But smaller customers found the new Johnson Controls overwhelming and impersonal. The company's Net Promoter Score, a measure of customer satisfaction, declined 15 points in the year following the merger.

The financial markets rendered a harsh verdict initially. Johnson's stock price fell 20% in the six months following the merger announcement, underperforming the S&P 500 by 25 percentage points. Investors questioned whether the complexity of integration was worth the tax savings. Credit rating agencies placed the company on negative watch, concerned about increased leverage and integration risks.

But Molinaroli and his team pressed forward with a larger transformation. The Tyco merger was just one piece of a radical portfolio restructuring. Even as they integrated Tyco, Johnson's leadership was planning the next phase: exiting the automotive business entirely to focus purely on building technologies. The company that had spent decades diversifying was about to reverse course dramatically.

The inversion controversy obscured genuine strategic merit in the Tyco combination. Fire and security systems were converging with traditional building controls as intelligence moved to the edge. Smart buildings needed integrated life safety systems that could coordinate responses to emergencies. A fire alarm that could immediately adjust HVAC systems to prevent smoke spread while simultaneously unlocking certain doors for evacuation represented the future of building technology.

Tyco's ADT security business, while consumer-facing and somewhat tangential, brought sophisticated monitoring capabilities and recurring revenue streams. The company's SimplexGrinnell fire protection business had relationships with virtually every major commercial property owner in America. These assets, properly integrated with Johnson's controls and HVAC expertise, could create unique value propositions.

The controversy also accelerated necessary changes. The political backlash forced Johnson to articulate its value proposition more clearly. The company couldn't rely on historical relationships or American heritage; it needed to compete on capabilities and innovation. This pressure, while painful, drove faster decision-making and more aggressive restructuring than might have occurred otherwise.

By late 2016, the immediate crisis had passed. Integration proceeded, synergies began materializing, and the tax savings proved real. But the Tyco merger had fundamentally changed Johnson Controls. The company was now legally Irish, culturally hybrid, and strategically focused on building technologies. The next phase of transformation—divesting the automotive business that had defined Johnson for decades—would test whether this new identity could create lasting value.

VI. The Great Portfolio Transformation (2016–2019)

The PowerPoint slide was stark: two arrows diverging from a single point. One pointed toward "Building Technologies Future," the other toward "Automotive Legacy." George Oliver, soon to be CEO, clicked to the next slide showing the financial reality—the automotive business generated 65% of revenue but only 35% of profits. The building technologies business, conversely, produced 65% of profits from 35% of revenue. The conclusion was inescapable: Johnson Controls needed to choose.

The decision to spin off the automotive seating business as Adient, announced in October 2016, represented more than divestiture—it was organizational suicide and rebirth. Johnson had spent thirty years building the world's largest automotive seating business through dozens of acquisitions and billions in investment. Now, with a keystroke, it would disappear. The 75,000 employees who designed and manufactured seats for nearly every major automaker would wake up working for a different company.

The strategic logic was compelling but painful. Automotive seating had become a brutal business—margins compressed by demanding customers, capital requirements soared as technology advanced, and competition from Asian suppliers intensified. Johnson's 2015 automotive margins of 4.5% compared dismally to building technologies' 13%. Every dollar invested in automotive seating generated returns below Johnson's cost of capital; every dollar invested in building technologies exceeded it.

The Adient spinoff, completed on October 31, 2016, created immediate value. Johnson shareholders received 0.25 Adient shares for each Johnson share owned. Adient began trading at $44 per share, creating $7 billion in market value that hadn't existed the day before. The financial engineering was elegant—Johnson kept the profitable aftermarket parts business while spinning off capital-intensive manufacturing. Tax optimization structures minimized the burden on both companies.

But the human cost was severe. Employees who had spent entire careers at Johnson Controls suddenly worked for Adient, a company with no history, uncertain prospects, and enormous debt. The Milwaukee headquarters, which had housed automotive leadership for decades, emptied as Adient moved operations to suburban Detroit. Communities that had hosted Johnson seating plants for generations lost their connection to the parent company.

The Power Solutions divestiture in 2018 proved even more dramatic. Johnson's battery business, descended from the Globe-Union acquisition forty years earlier, generated $8 billion in annual revenue. The business held leading positions in automotive batteries (30% global market share) and emerging markets like start-stop technology. But margins remained stuck at 8%, and capital requirements for next-generation lithium-ion technology were enormous.

Brookfield Business Partners emerged as the buyer, offering $13.2 billion—a price that stunned analysts. Johnson was selling Power Solutions for 11 times EBITDA, a premium valuation for a cyclical manufacturing business. The secret lay in Brookfield's financial engineering: they saw opportunities to improve working capital management, optimize the supply chain, and potentially re-IPO the business (renamed Clarios) at an even higher valuation.

The negotiations revealed Johnson's desperation to exit. When Brookfield initially offered $11 billion, Johnson countered not by demanding more cash but by proposing seller financing and earn-outs that would bridge the valuation gap. The company wanted certainty of closure more than maximum price. The final structure included $12 billion in cash and $1.2 billion in assumed pension liabilities—a crucial detail that cleaned up Johnson's balance sheet.

The speed of transformation was breathtaking. In January 2016, Johnson Controls was a $37 billion conglomerate operating in three distinct industries. By December 2018, it was an $18 billion pure-play building technologies company. The company had shed 100,000 employees, hundreds of facilities, and decades of accumulated complexity. The transformation generated $24 billion in proceeds, but the real value lay in strategic focus.

The capital allocation decisions following the divestitures revealed management's priorities. Rather than pursuing massive acquisitions or aggressive expansion, Johnson returned $3 billion to shareholders through buybacks, reduced debt by $2 billion, and invested $1 billion in digital capabilities. The company was simultaneously shrinking and strengthening, focusing resources on areas of competitive advantage. The financial markets struggled to value the new Johnson Controls. Traditional industrial analysts didn't understand software and services; technology analysts didn't appreciate the complexity of building systems. The company traded at a conglomerate discount even after eliminating the conglomerate structure. Management grew increasingly frustrated, believing the market failed to recognize the value creation from portfolio transformation.

Operational performance during this period was mixed. The Building Technologies business grew organically at 5-7% annually, respectable for a mature industrial business but disappointing for a company positioning itself as a technology leader. Margins improved from 11% to 13%, but remained below the 15%+ targets management had promised. The company blamed integration costs, but skeptics wondered if the building technologies market was simply less attractive than management believed.

The cultural transformation proved particularly challenging. Johnson Controls had three distinct cultures layered atop each other: the original Midwestern engineering culture, the Tyco deal-making culture, and the aspiring Silicon Valley technology culture. Employees joked about needing a translator to understand meetings where "building performance optimization" (Johnson-speak) met "margin expansion initiatives" (Tyco-speak) met "digital transformation journey" (tech-speak).

Yet beneath the chaos, real transformation was occurring. The company systematically upgraded its technology capabilities, hiring hundreds of software engineers and data scientists. Johnson's R&D spending shifted from mechanical engineering to software development. The company's patent filings increasingly focused on algorithms and analytics rather than physical products. This wasn't just financial engineering—it was genuine business model transformation.

The divestitures also revealed hidden value. When Adient and Clarios reported results as independent companies, their combined market value exceeded their value within Johnson Controls by $5 billion. This "reverse conglomerate discount" validated the divestiture strategy while raising uncomfortable questions about why these businesses had been accumulated in the first place.

Labor relations during the transformation were strained but not broken. Unlike many corporate restructurings that slash costs indiscriminately, Johnson's approach was surgical. The company eliminated redundant corporate functions while investing in customer-facing capabilities. Sales force headcount actually increased even as total employment fell. This selective approach maintained customer relationships while improving efficiency.

The environmental narrative became increasingly important. Johnson positioned itself as enabling the transition to sustainable buildings, with technology that could reduce energy consumption by 30% or more. This wasn't greenwashing—the company's solutions genuinely reduced carbon emissions. But the irony of an Irish-domiciled company benefiting from U.S. environmental regulations and incentives wasn't lost on critics.

By 2019, the transformation was largely complete. Johnson Controls had evolved from a $37 billion conglomerate to a $23 billion focused building technologies company. The company had shed two-thirds of its employees but doubled its market capitalization. Operating margins had expanded 400 basis points. Return on invested capital exceeded the cost of capital for the first time in a decade.

The portfolio transformation validated a controversial strategy: sometimes creating value requires destroying what previous generations built. Johnson's leaders had the courage to acknowledge that the conglomerate structure, successful in its time, no longer fit modern markets. They executed one of the largest corporate restructurings in history, navigating political backlash, operational complexity, and cultural resistance.

But questions remained. Was Johnson Controls now a technology company or an industrial company with technology aspirations? Could building technologies generate the growth and margins that justified premium valuations? Would the focus on commercial buildings prove prescient or limiting? The next phase—building a digital platform for smart buildings—would determine whether the painful transformation had been worth it.

VII. Digital Buildings & The OpenBlue Platform (2020–Present)

The timing could hardly have been worse—or better. Johnson Controls launched OpenBlue, its comprehensive digital platform, on July 31, 2020, five months into a global pandemic that had emptied office buildings worldwide. The platform, representing years of development and hundreds of millions in investment, was designed to orchestrate smart buildings. But with buildings empty and companies questioning their real estate footprints, the entire premise seemed suddenly obsolete.

Yet the pandemic accelerated the exact trends OpenBlue was designed to address. Building owners, desperate to lure workers back, needed to prove their spaces were safe. The platform promised 20-60% cost savings by optimizing HVAC performance while improving indoor air quality—suddenly a life-or-death consideration rather than a nice-to-have feature. Contact tracing, touchless controls, and air quality monitoring transformed from futuristic concepts to immediate necessities.

OpenBlue was the culmination of years of research and development, designed with agility, flexibility and scalability to enable buildings to become dynamic spaces. In leveraging the platform, customers could manage operations systemically, delivering buildings that have memory, intelligence and unique identity. This wasn't just marketing rhetoric—the platform represented a fundamental reimagining of how buildings operate.

The technical architecture was sophisticated. Rather than a monolithic system, OpenBlue used a microservices approach with different capabilities deployed as needed. The platform infused solutions with artificial intelligence, combining data from both inside and outside of buildings. A building's HVAC system could respond not just to current temperature but to weather forecasts, occupancy predictions, and energy prices.

The December 2020 partnership with Microsoft elevated OpenBlue's capabilities. Johnson Controls' OpenBlue Digital Twin integrated with Azure Digital Twins, supporting the entire ecosystem of building and device management technologies with cloud capabilities. This wasn't just a technology partnership but a strategic alliance—Microsoft's cloud infrastructure gave Johnson enterprise credibility while Johnson's domain expertise gave Microsoft entry to the massive building automation market.

The digital twin concept deserved particular attention. Every physical component—from chillers to thermostats—had a virtual replica that continuously updated based on sensor data. "Digital twins are playing an increasingly important role" in analyzing large datasets and predicting patterns to "tell our customers things they don't yet know." Maintenance could be predicted before failures occurred. Energy optimization could be simulated before implementation. The acquisitions during this period were surgical, targeting specific capabilities. Johnson Controls completed the acquisition of Silent-Aire in May 2021, with Silent-Aire specializing in the design, engineering and manufacturing of mission critical custom air handlers and modular data centers for hyperscale cloud and colocation providers. Silent-Aire's revenue for fiscal year 2021 was expected to approximate $650 million. The all-cash transaction was valued at up to $870 million, including an upfront payment of approximately $630 million and additional payments subject to earnout milestones.

The Silent-Aire acquisition revealed Johnson's strategic pivot toward data centers—the fastest-growing segment in commercial real estate. Data centers consumed 2% of global electricity and needed sophisticated cooling systems to prevent servers from overheating. Silent-Aire had grown from 30 to 3,000 employees by focusing exclusively on hyperscale data centers operated by Amazon, Google, and Microsoft. These customers valued reliability above all else—a single hour of downtime could cost millions. Johnson Controls has acquired FM:Systems in July 2023, a leading digital workplace management and Internet of Things solutions provider for facilities and real estate professionals. The base purchase price for the transaction is $455 million, plus additional payments subject to post-closing earnout milestones. FM:Systems, headquartered in Raleigh, North Carolina, had more than 200 employees and 1,200 customers, representing more than 2.4 million users across 80 countries, achieving greater than 110% average net revenue retention since 2020.

The FM:Systems acquisition addressed a critical gap in OpenBlue's capabilities. While Johnson controlled building systems, FM:Systems understood how people used buildings. Their software tracked everything from desk utilization to conference room bookings, providing insights that building operators desperately needed as hybrid work transformed office dynamics. The company's sensors could detect whether spaces were occupied, allowing HVAC systems to adjust accordingly—reducing energy consumption while maintaining comfort. The portfolio transformation continued with dramatic moves. In July 2024, Johnson Controls announced it would sell its Residential and Light Commercial HVAC businesses to Germany's Bosch Group in an all-cash transaction. The total transaction is valued at $8.1 billion, and the Company's portion of the consideration is approximately $6.7 billion. The transaction includes the North America Ducted business and global Residential joint venture with Hitachi, Ltd. ("Hitachi"), of which Johnson Controls owns 60% and Hitachi owns 40%. In fiscal 2023, the R&LC HVAC business generated approximately $4.5 billion in consolidated revenue.

This divestiture represented the final step in Johnson's transformation to a pure-play commercial building technologies company. Residential HVAC, while generating substantial revenue, diluted the company's focus on high-margin commercial solutions. The sale price—nearly 2x revenue—validated management's portfolio optimization strategy. Net cash proceeds to Johnson Controls were approximately $5.0 billion after tax and transaction-related expenses.

The OpenBlue platform evolution accelerated through 2024. Johnson Controls announced significantly expanded AI capabilities in its OpenBlue Enterprise Manager suite of digital solutions. OpenBlue now has integrated generative AI tools that proactively recommend the most impactful energy savings projects, reducing the need to analyze large amounts of building data. The system anticipates needs, like analyzing energy usage based on live weather data, to create actionable insights.

The generative AI integration addressed a fundamental challenge in building management: operators often didn't know what questions to ask their systems. "Our customers have consistently told us that one of the challenges with AI is they are unsure of what questions to ask a Generative AI chatbot about their building," said Julius Marchwicki, vice president, digital product management. "Our generative AI feature automatically constructs the right prompts that are built from our decades of experience."

Independent validation arrived in 2024 when Verdantix named Johnson Controls an IoT digital platform leader in building operations in its Green Quadrant: IoT Digital Platforms for Building Operations 2024 report. This recognition mattered because Verdantix evaluated platforms across multiple criteria including data management, analytics, integration capabilities, and vendor execution—areas where traditional industrial companies often struggled against technology natives.

The customer results validated the platform strategy. With OpenBlue Enterprise Manager guiding facility improvements, coupled with equipment upgrades and proactive services, customers are benefitting from up to 30% reduction in energy consumption. These weren't theoretical savings but measured results from operational deployments across thousands of buildings globally.

The sustainability narrative became increasingly central to Johnson's value proposition. Buildings consumed 40% of global energy and produced 36% of carbon emissions. Regulations worldwide mandated dramatic efficiency improvements—the European Union's Energy Performance of Buildings Directive required all new buildings to be zero-emission by 2030. Johnson positioned OpenBlue as the platform enabling this transition, combining hardware controls with software intelligence to optimize every aspect of building performance.

Competition intensified from unexpected directions. Technology giants recognized buildings as the next frontier for digital transformation. Google's Nest expanded from thermostats to complete building management systems. Amazon's AWS offered competing IoT platforms for building data. Microsoft, despite partnering with Johnson on Azure Digital Twins, developed its own smart building capabilities. These companies brought unlimited capital, software expertise, and platform thinking that challenged traditional building automation providers.

Johnson's response was pragmatic: embrace partnerships where beneficial, compete where necessary. The company's advantage lay in domain expertise—understanding the complex interplay between HVAC, electrical, plumbing, and structural systems that pure software companies struggled to grasp. A Google engineer might optimize an algorithm, but Johnson's technicians understood why certain buildings behaved differently on humid Tuesday mornings.

The recurring revenue transformation accelerated. Traditional equipment sales generated one-time revenue with replacement cycles measured in decades. OpenBlue subscriptions, service contracts, and software licenses created predictable monthly revenue streams. By 2024, recurring revenue exceeded 40% of total building technologies revenue, with margins significantly higher than equipment sales. This transition, while reducing reported revenue growth, dramatically improved business quality and valuation multiples.

Yet challenges remained substantial. The OpenBlue platform, while technologically impressive, required significant customer education. Building operators, often skeptical of new technology, needed convincing that digital transformation would deliver tangible benefits. Integration with legacy systems—some buildings still used pneumatic controls from the 1960s—proved complex and expensive. Cybersecurity concerns intensified as building systems connected to networks, creating potential vulnerabilities.

The workforce transformation proved equally challenging. Johnson needed to evolve from an industrial manufacturer to a technology company while retaining the field service expertise that customers valued. The company hired thousands of software engineers and data scientists while retraining existing employees in digital technologies. This cultural transformation—from wrenches to algorithms—would determine whether Johnson Controls could truly become the building intelligence leader it aspired to be.

VIII. Business Model & Competitive Dynamics

The economics of Johnson Controls' business model reveals a fundamental truth about building technologies: the real money isn't in selling equipment but in controlling the ongoing relationship with the building. A chiller might generate $500,000 in revenue once every twenty years, but the service contract attached to that chiller produces $25,000 annually—$500,000 over its lifetime with 70% gross margins compared to 20% on the equipment sale. This dynamic drives every strategic decision at Johnson Controls.

The installed base represents Johnson's most valuable asset—though it never appears on the balance sheet. The company monitors or services equipment in over 2 million buildings worldwide. Each installation creates switching costs that compound over time. When a building manager considers changing providers, they face not just equipment replacement but retraining staff, reconfiguring systems, and risking operational disruption. A study by McKinsey found that 92% of commercial buildings retain their building automation provider for over 15 years, making customer acquisition costs high but lifetime values extraordinary.

Network effects amplify these advantages in subtle ways. Johnson's Metasys platform becomes more valuable as more equipment connects to it—not just Johnson equipment but competitors' products too. This openness strategy, controversial when introduced, proved brilliant. Building owners want single-pane-of-glass visibility across all systems. By positioning itself as the integration layer, Johnson captures value even from competitors' equipment. A Carrier chiller monitored through Metasys still generates service revenue for Johnson.

The competitive landscape resembles trench warfare more than blitzkrieg. Four companies—Johnson Controls, Honeywell, Schneider Electric, and Siemens—control roughly 60% of the global building automation market. Each has strengths in different geographies and verticals. Honeywell dominates airports and government buildings through decades of relationship-building. Schneider excels in electrical integration. Siemens leverages its industrial automation expertise in manufacturing facilities. Johnson's strength lies in commercial real estate and increasingly, data centers.

Geographic dynamics create distinct competitive environments. In North America, Johnson battles Honeywell for supremacy, with each controlling roughly 25% market share. Labor relationships matter enormously—the International Union of Operating Engineers trains members specifically on Johnson and Honeywell systems, creating institutional lock-in. In Europe, Siemens and Schneider dominate, leveraging home-market advantages and EU regulatory expertise. Asia Pacific remains fragmented, with local players controlling 70% of the market but lacking the technology to compete in sophisticated applications.

The margin structure tells a story of transformation. Equipment manufacturing generates 10-15% gross margins—respectable for industrial products but unexciting for investors. Installation services produce 20-25% margins, benefiting from labor expertise and project management capabilities. But the real profit pools lie in recurring services: maintenance contracts (40% margins), software subscriptions (70% margins), and energy optimization services (50% margins). This margin ladder incentivizes Johnson to move customers from transactional equipment purchases to comprehensive service relationships.

Capital intensity varies dramatically across business lines. Manufacturing requires significant fixed investment—a single production line for commercial HVAC equipment costs $50 million. But once installed, these facilities generate cash for decades with minimal additional investment. The software business, conversely, requires continuous investment in R&D (Johnson spends $500 million annually on digital capabilities) but scales infinitely once developed. This dual model—capital-intensive manufacturing providing cash flow to fund capital-light software development—creates strategic flexibility.

The sales cycle complexity would frustrate most companies. Large commercial building projects involve multiple stakeholders: architects who specify systems, engineers who design integration, contractors who install equipment, building owners who finance purchases, and facility managers who operate systems. Johnson must influence each constituency, often years before revenue materializes. A typical high-rise project takes 5-7 years from initial design to commissioning, requiring Johnson to maintain relationships and update proposals continuously.

Vertical market dynamics increasingly drive strategy. Hospitals require 100% uptime for operating rooms and precise temperature control for laboratories. Data centers need massive cooling capacity with redundancy and energy efficiency. Schools demand simple operation and tight budgets. Each vertical has evolved its own ecosystem of specialized competitors, consultants, and regulations. Johnson's approach—dedicated teams for major verticals—trades efficiency for expertise, accepting higher costs to capture premium positions.

The technology transition creates both opportunity and threat. Traditional building automation required proprietary expertise that created moats. But as systems migrate to IP networks and cloud platforms, IT companies can potentially disrupt incumbents. Johnson's response—embracing open standards while maintaining proprietary analytics—attempts to balance accessibility with differentiation. The OpenBlue platform runs on standard IT infrastructure but the algorithms that optimize building performance remain proprietary.

Pricing power varies significantly across segments. In competitive bidding for new construction, margins compress as contractors squeeze suppliers. But in retrofit and service markets, Johnson enjoys significant pricing power. Building owners facing regulatory deadlines or equipment failures have limited negotiating leverage. The company's service price increases consistently exceed inflation, contributing to margin expansion even as equipment prices face pressure.

Distribution complexity adds cost but creates competitive advantage. Unlike pure software companies that distribute digitally, Johnson must maintain vast logistics networks. The company operates 500 branch offices globally, each stocking critical parts and housing technical staff. This infrastructure seems anachronistic in the digital age, but when a hospital's cooling system fails at 2 AM, the ability to dispatch a technician with the right part within hours justifies the cost.

The partner ecosystem extends Johnson's reach while creating channel conflict. The company works with thousands of mechanical contractors who install and service equipment. These relationships, some dating back decades, provide local market knowledge and labor capacity. But contractors also install competitors' equipment, creating complex dynamics. Johnson must balance direct sales (higher margins but limited reach) with channel sales (lower margins but greater scale).

Customer concentration risk remains manageable but notable. No single customer represents more than 2% of revenue, but the top 100 customers generate 25% of revenue. These large portfolio owners—companies like Brookfield Properties, CBRE, and JLL—have significant negotiating leverage. They demand global consistency, volume discounts, and performance guarantees that smaller customers don't receive. Losing one of these accounts would impact not just revenue but market perception.

The recurring revenue transformation fundamentally alters the business model. Traditional equipment sales created revenue spikes tied to construction cycles. Service contracts smooth revenue across economic cycles. Software subscriptions provide predictable monthly revenue with automatic renewal. This transition from cyclical to stable revenue should theoretically improve valuation multiples, though public markets have been slow to recognize the transformation.

Competitive responses vary from aggressive to acquiescent. Honeywell has matched Johnson's digital investments, launching its own Forge platform. Schneider emphasizes electrical and building system integration. Siemens leverages its industrial IoT expertise. Smaller players either specialize in niches (Automated Logic in controls, Trane in HVAC) or accept subordinate positions as suppliers to the giants. The competitive equilibrium seems stable, with each player defending core strengths while selectively attacking adjacencies.

The business model's resilience was tested during COVID-19 and proved robust. While new construction collapsed, service revenue remained stable as buildings required maintenance regardless of occupancy. The pandemic actually accelerated digital adoption as building owners sought remote monitoring capabilities. Johnson's financial performance during this period—maintaining profitability while competitors struggled—validated the recurring revenue strategy.

Looking forward, the business model must evolve to address new realities. The shift to hybrid work reduces office occupancy, challenging traditional density assumptions. Climate change increases cooling demand while regulations mandate efficiency improvements. Cybersecurity threats require continuous investment in protection. Artificial intelligence promises to automate functions that currently require human expertise. Each trend creates both risk and opportunity, requiring Johnson to balance defending existing profit pools while investing in future capabilities.

IX. Playbook: Lessons in Corporate Transformation

The Johnson Controls transformation playbook reads like a master class in corporate strategy, but with enough mistakes and reversals to keep it honest. Over 140 years, the company has executed nearly every major strategic move available to corporations: diversification, focus, globalization, retrenchment, tax inversion, digital transformation. The lessons learned—often painfully—provide a template for industrial companies navigating technological disruption.

Serial Acquisition Excellence and Integration Disasters

Johnson Controls completed over 100 acquisitions, spending more than $30 billion to assemble its empire. The company developed a systematic approach: identify strategic gaps, map potential targets, build relationships with management, wait for the right moment (usually distress), then strike decisively. The York acquisition exemplified this patience—Johnson tracked the company for a decade before executing in 2005.

But integration capabilities lagged acquisition expertise. The company excelled at financial engineering—tax optimization, working capital improvement, cost synergies—but struggled with cultural integration. The Tyco merger revealed this starkly: two years post-close, the companies still operated distinct IT systems, sales forces barely collaborated, and cultural conflicts festered. Johnson learned that successful acquisition requires not just buying assets but truly combining organizations.

The pattern repeated across acquisitions. Johnson would promise revenue synergies—cross-selling products, bundling solutions—that rarely materialized. Sales forces protected their territories rather than collaborating. Product teams resisted standardization. Customers, confused by overlapping offerings, often chose competitors for simplicity. The lesson: revenue synergies are exponentially harder than cost synergies, requiring years of patient integration rather than quarters.

Portfolio Management: The Courage to Destroy

The decision to divest automotive and battery businesses—operations that generated 70% of revenue—required extraordinary courage. These weren't failing businesses; Adient was the global automotive seating leader, Clarios dominated automotive batteries. But management recognized a fundamental truth: conglomerate structures destroy value in modern capital markets.

The divestitures followed a clear logic. First, identify businesses where Johnson wasn't the natural owner—others could generate better returns. Second, execute when market conditions favor sellers, not when forced by distress. Third, use proceeds strategically rather than simply returning cash to shareholders. The $24 billion in divestiture proceeds funded debt reduction, digital investment, and strategic acquisitions that transformed the company.

But the human cost was severe. Employees who built these businesses over decades felt betrayed. Communities that hosted facilities for generations lost their connection to Johnson. The company's identity, tied to automotive and batteries for forty years, needed complete reimagination. The lesson: portfolio transformation requires not just financial engineering but organizational psychology—helping stakeholders understand why destruction enables creation.

Tax Optimization and Regulatory Arbitrage

The Tyco inversion saved $150 million annually in taxes—real money that flowed directly to earnings. But the political backlash nearly destroyed the company's reputation. Hillary Clinton's public condemnation, amplified by media coverage, positioned Johnson as an unpatriotic tax dodger. Government contracts came under scrutiny. Employees questioned company values. Customers worried about stability.

Johnson's response—emphasizing strategic benefits beyond taxes—rang hollow because the tax benefits were so obvious. The company learned that tax optimization, while legally permissible, carries social license requirements. Actions that lawyers approve and CFOs celebrate can destroy decades of carefully built reputation. The narrow window for inversions (closing shortly after Johnson's transaction) suggests the company timed the regulatory environment perfectly, even if it underestimated the reputational environment.

Managing Conglomerate Discounts

Johnson Controls suffered from persistent conglomerate discounts—the market valued the company at less than the sum of its parts. Management tried everything: detailed segment reporting to highlight individual business performance, investor days showcasing synergies, financial engineering to improve returns. Nothing worked. The market simply didn't believe that building controls, automotive seating, and batteries belonged together.

The eventual solution—breaking up the company—validated market skepticism. Post-separation, the combined market value of Johnson, Adient, and Clarios exceeded the previous consolidated value by $8 billion. The lesson is sobering: markets are often right about conglomerate inefficiency, even when management sincerely believes in synergy potential. Fighting conglomerate discounts through communication rarely works; structural change is usually required.

Technology Transitions: From Pneumatic to Digital to AI

Johnson navigated three major technology transitions, each requiring different capabilities. The shift from pneumatic to electronic controls in the 1970s leveraged existing customer relationships while requiring new technical expertise. The company succeeded by acquiring electronic capabilities (Penn Controls) while maintaining pneumatic expertise for legacy systems.

The digital transformation of the 2000s proved harder. Software required different development cycles, talent models, and business models than hardware. Johnson's initial attempts to develop software internally failed repeatedly. Success came only through acquisition (FM:Systems) and partnerships (Microsoft) that brought native digital capabilities. The lesson: technology transitions often require buying expertise rather than building it.

The current AI transformation presents new challenges. Unlike previous transitions where Johnson could acquire leaders, no clear AI leader exists in building technologies. The company must develop capabilities internally while the technology evolves rapidly. Early efforts show promise—the OpenBlue AI features generate measurable value—but sustainable advantage remains uncertain.

Managing Through Cycles

Johnson experienced every economic cycle imaginable: depressions, recessions, booms, stagflation, financial crises, pandemics. The company developed countercyclical strategies that smoothed performance. During downturns, focus shifted from new construction to retrofit and service. During booms, capacity expanded and acquisitions accelerated. This cycle management capability—knowing when to invest and when to harvest—became a core competence.

But cycles increasingly diverge across businesses and geographies. Chinese construction might boom while American markets contract. Data centers might expand while office buildings sit empty. Managing this complexity requires sophisticated capital allocation and risk management that challenges traditional industrial companies. Johnson's response—focusing on businesses with natural hedges and recurring revenue—reduces but doesn't eliminate cyclical exposure.

The Platform Journey