ING Group: The Dutch Banking Giant's Transformation Story

I. Introduction & Episode Hook

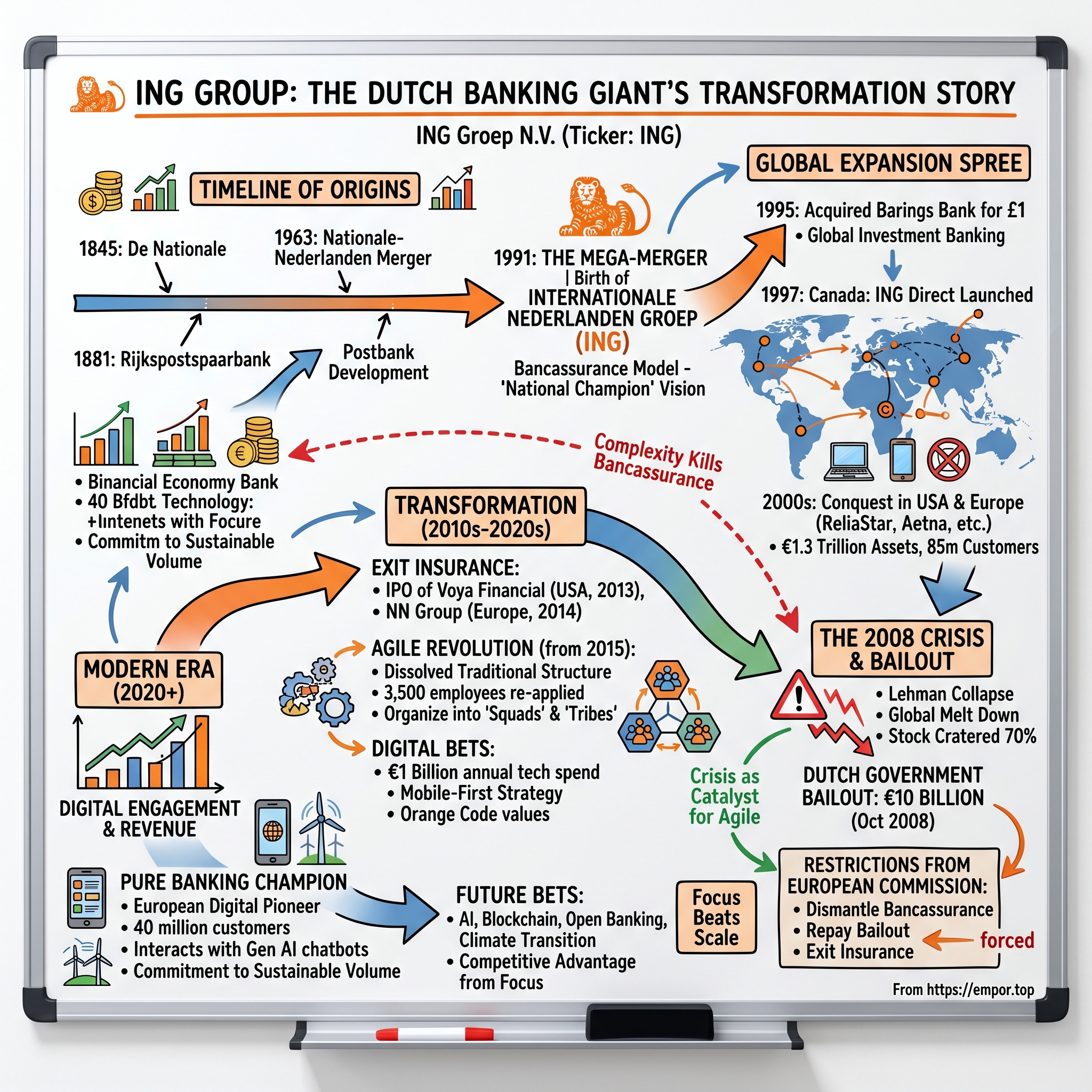

Picture this: October 2008. The global financial system is melting down. Lehman Brothers has just collapsed. Banks across Europe and America are failing daily. In Amsterdam, executives at ING Group—then one of the world's largest financial conglomerates with €1.3 trillion in assets—watch their stock price crater 70% in a matter of weeks. The Dutch government swoops in with a €10 billion bailout, but there's a catch: ING must dismantle the very empire it spent two decades building. Insurance operations? Gone. International retail banking units? Sold. The sprawling bancassurance model that defined the company? Dead.

Fast forward to today. That same company, stripped to its core, has somehow emerged as Europe's digital banking pioneer. ING serves 40 million customers across 40 countries, processes billions in daily transactions, and runs one of the most sophisticated digital banking platforms on the continent. Its market capitalization has recovered to €40 billion, making it one of Europe's most valuable banks. The company that was forced to sell its crown jewels during the crisis has reinvented itself as something arguably more powerful: a focused, technology-driven bank that competitors struggle to match.

This is the story of how a 1991 merger between a Dutch insurance giant and a postal savings bank created one of history's most ambitious financial experiments—and how that experiment's spectacular failure during the 2008 crisis paradoxically set the stage for one of banking's most successful transformations. It's a tale of visionary ambition, near-death experiences, forced reinvention, and ultimately, the power of focus in an industry that rewards scale.

The central question driving this narrative: How did ING transform from a bloated financial conglomerate that nearly collapsed into Europe's most digitally advanced traditional bank? The answer involves postal workers, insurance salesmen, a rogue trader in Singapore, Silicon Valley management techniques, and a radical bet that banking's future would be mobile-first. Along the way, we'll explore what ING's journey teaches us about building financial empires, surviving existential crises, and the surprisingly liberating power of being forced to start over.

II. Origins & The Bancassurance Vision (Pre-1991)

The year is 1845. Amsterdam is experiencing its first golden age of modern finance. A group of Dutch merchants, worried about the devastating fires that regularly consume wooden buildings and warehouses, establish De Nationale, a fire insurance company. Their timing proves prescient—the industrial revolution is about to transform risk management from a gentleman's agreement into a mathematical science. Eighteen years later, in 1863, another group of entrepreneurs launches De Nederlanden van 1845, focusing on the emerging field of life insurance. These two companies, operating in parallel for a century, would merge in 1963 to create Nationale-Nederlanden, destined to become one half of the ING story.

Meanwhile, in 1881, the Dutch government faces a different problem. Most citizens have no access to banking services. Rural communities, in particular, are cut off from the financial system. The solution? The Rijkspostspaarbank—a postal savings bank that leverages the country's extensive post office network. Every post office becomes a bank branch. Every postal worker, a part-time banker. It's a radical democratization of finance, bringing savings accounts and payment services to millions who'd never set foot in a traditional bank. By the 1960s, this postal bank has evolved into the Postbank, handling not just savings but checking accounts, money transfers, and eventually, the giro payment system that becomes the backbone of Dutch commerce.

The 1980s bring deregulation fever to European finance. Margaret Thatcher is dismantling barriers in London. France is liberalizing its markets. In the Netherlands, regulators make a fateful decision: banks and insurance companies, long kept separate by law, can now merge. The logic seems compelling. Insurance companies have massive capital reserves but limited distribution. Banks have extensive branch networks but need capital for expansion. Combine them, the theory goes, and you create a financial superpower—selling insurance through bank branches, using insurance premiums to fund loans, cross-selling products to captured customers.

Enter Jan Kalff, the visionary CEO of NMB Bank (itself a 1989 merger of the Netherlands Trading Society and the Postbank). Kalff sees the future clearly: standalone banks and insurers will be crushed by integrated financial conglomerates. He needs an insurance partner. Across town, Nationale-Nederlanden's leadership reaches the same conclusion. They need banking distribution. The courtship begins in 1990, conducted in secret meetings at neutral locations. Both companies are Dutch icons—Nationale-Nederlanden insures half the country, while NMB Postbank operates the payment system most citizens use daily. A merger would create a national champion, a financial fortress capable of competing globally.

The negotiations are complex. Who leads the merged entity? How do you value an insurance company versus a bank? What about the radically different cultures—conservative insurers who think in decades versus aggressive bankers who measure success quarterly? But the strategic logic proves overwhelming. On March 7, 1991, they announce the deal: Internationale Nederlanden Groep is born, immediately becoming the Netherlands' largest financial institution and Europe's first major bancassurance experiment. The name itself—mixing Dutch and English, combining "international" with the Netherlands—signals global ambition. The orange lion logo, derived from the Dutch royal coat of arms, projects strength and national pride.

III. The Mega-Merger & Early Expansion (1991-1999)

The morning of March 7, 1991, Amsterdam's financial district buzzes with speculation. At a packed press conference, Jan Kalff and Nationale-Nederlanden's leadership unveil their creation: ING Group, valued at 30 billion guilders (roughly €14 billion), instantly making it one of Europe's largest financial institutions. Kalff, now co-CEO alongside insurance veteran Aad Jacobs, promises nothing less than a revolution in financial services. "Customers will walk into a branch for a mortgage and walk out with life insurance, investment products, and a pension plan," he declares. The assembled journalists scribble notes, many skeptical but all recognizing the audacity of the vision.

The early integration proves chaotic. Insurance salespeople, accustomed to relationship-building over months, clash with bankers focused on quick transactions. IT systems speak different languages—literally, in some cases, with insurance mainframes running COBOL while banking systems use newer architectures. Customer databases don't sync. Products overlap confusingly. In one infamous early incident, a customer receives three different quotes for the same life insurance product from three different ING channels. But Kalff pushes forward, convinced that these are mere growing pains.

By 1993, with the Dutch integration still messy, ING makes its first major international move. They acquire Banque Bruxelles Lambert (BBL), Belgium's third-largest bank, for €3.5 billion. The Belgian market offers a perfect test case—similar to the Netherlands but without the integration headaches of the home market. ING can build bancassurance from scratch. The acquisition also brings unexpected benefits: BBL's strong corporate banking relationships and its emerging markets trading desk, which will prove crucial for ING's later expansion.

Then comes February 26, 1995—a date that transforms ING from a regional player into a global headline. Barings Bank, the 233-year-old British institution that financed the Napoleonic Wars, collapses overnight. The cause? Nick Leeson, a 28-year-old trader in Singapore, has lost £827 million betting on Japanese stock futures. The Bank of England, after a frantic weekend trying to organize a rescue, announces Barings is for sale. The asking price: £1.

ING pounces. Within 48 hours, they agree to acquire Barings for that symbolic pound, plus assumption of its liabilities. The speed stuns competitors—German and American banks are still assembling due diligence teams when ING signs the deal. Overnight, ING gains Barings' prestigious investment banking operations, its Asian securities business, and most importantly, instant global brand recognition. The financial press can't believe it: a Dutch bank nobody outside the Benelux has heard of now owns the Queen's banker.

The Barings acquisition reveals ING's emerging playbook: move fast, take calculated risks, and leverage crisis for opportunity. This philosophy drives an acquisition spree through the late 1990s. In 1997, they buy Equitable of Iowa, a U.S. life insurer, for $2.2 billion, establishing their American beachhead. The same year, they acquire Poland's Bank Śląski, betting early on Eastern European convergence. In 1999, they add Germany's BHF-Bank for €2.5 billion, gaining access to Europe's largest economy.

But the real innovation happens in Canada. In 1997, a small team led by Dutch executive Arkadi Kuhlmann launches something radical: ING Direct. No branches. No paper. No fees. Just high-interest savings accounts accessible by phone and internet. Traditional bankers mock the concept—how can you run a bank without branches? Kuhlmann's response: "Why would you want branches when you can have the internet?" Within six months, ING Direct Canada attracts 100,000 customers and C$1 billion in deposits. The savings are staggering—ING Direct operates at 30 basis points of costs versus 250 for traditional banks. Those savings get passed to customers as higher interest rates, creating a virtuous cycle of growth.

By 1999, ING has transformed from a Dutch financial conglomerate into something unprecedented: a global bancassurance platform operating in 40 countries with 60,000 employees. The company reports record profits of €2.4 billion. The stock price has tripled since the 1991 merger. At the annual shareholder meeting, Kalff, now sole CEO after Jacobs' retirement, declares victory: "We have proven that bancassurance works. We have proven that a Dutch company can compete globally. We have built the financial services company of the future."

IV. ING Direct Revolution & American Dreams (1997-2007)

Arkadi Kuhlmann stands before a whiteboard in Toronto, sketching out his vision to a skeptical board of directors. It's early 1997, and the Ukrainian-born, American-educated banker is proposing something that sounds insane: a bank with no branches, no checkbooks, no human tellers. Just a website, a call center, and one single product—a high-yield savings account. "We'll be the Southwest Airlines of banking," he insists, referring to the low-cost carrier that revolutionized aviation. "Strip away everything customers don't value, give them what they actually want—convenience and high returns—and do it at a fraction of traditional costs."

The numbers are compelling. A traditional bank branch costs $2-3 million to build and $400,000 annually to operate. ING Direct's model: zero branches, just server farms and call centers. Traditional banks need 250 basis points of margin to break even; ING Direct can profit at 30 basis points. This efficiency enables them to offer savings rates 3-4 times higher than competitors while still maintaining healthy margins. Within months of launching in Canada, the model proves itself spectacularly. By year-end 1997, ING Direct Canada has C$1.4 billion in deposits from 140,000 customers—all acquired at one-tenth the traditional customer acquisition cost.

The success catches the attention of ING's Amsterdam headquarters, particularly CEO Ewald Kist (who succeeded Kalff in 2000). Kist, a cerebral strategist who spent his career in insurance, sees ING Direct as the perfect synthesis of banking and insurance principles: low-cost distribution, actuarial precision in risk management, and scale economics. He green-lights rapid expansion. ING Direct launches in Australia (1999), France (1999), Spain (2000), and Italy (2001). Each market entry follows the same playbook: aggressive marketing, rates that traditional banks can't match, and relentless focus on simplicity.

But the real prize is America. In September 2000, ING Direct USA launches with a $100 million marketing blitz. Kuhlmann, now running the U.S. operation from Wilmington, Delaware (chosen for its banking-friendly regulations), creates a marketing sensation. The orange logo appears everywhere—billboards, subway cars, TV commercials. The tagline, "Save Your Money," becomes ubiquitous. ING Direct opens cafés in major cities—not bank branches, but coffee shops where customers can learn about online banking while sipping lattes. It's experiential marketing before the term exists.

The timing proves perfect. The dot-com bubble has burst, decimating stock portfolios. Americans are suddenly interested in safe, boring savings accounts. ING Direct offers 5% interest when most banks pay 1%. Within 18 months, they attract 1 million customers and $10 billion in deposits. By 2003, it's $20 billion. By 2007, ING Direct USA has 7.5 million customers and $80 billion in deposits, making it America's largest direct bank and the country's fourth-largest savings institution.

Meanwhile, ING's insurance operations are executing their own American conquest. In 2000, ING acquires ReliaStar for $6.1 billion, gaining massive life insurance and retirement services operations. The same year, they buy Aetna Financial Services for $7.7 billion, adding another 5 million customers. These aren't random acquisitions—they're strategic moves to build an integrated financial services platform. ReliaStar's variable annuities complement ING Direct's savings products. Aetna's 401(k) administration creates cross-selling opportunities. By 2007, ING has 45 million customers in the Americas, generating 40% of the group's total profits.

The numbers are staggering. ING's total assets grow from €400 billion in 2000 to €1.3 trillion by 2007. The company operates in 40 countries, employs 130,000 people, and serves 85 million customers globally. The stock price reaches €35 per share, up from €10 in 2000. ING ranks among the world's 20 largest companies by market capitalization. At the 2007 annual meeting, CEO Michel Tilmant (who succeeded Kist in 2004) declares: "We have built the world's first truly global bancassurance company. We are present on every continent, in every major market, with every product a customer needs."

But beneath the triumphant numbers, cracks are forming. The company's balance sheet has become impossibly complex—insurance liabilities mixed with banking assets, derivative positions spanning dozens of currencies, exposure to American subprime mortgages through securities that seemed safe but aren't. The integration between banking and insurance, always more theoretical than practical, has created a risk management nightmare. Different regulators in different countries have different requirements, making consolidated oversight nearly impossible. Some executives privately worry that ING has become too big to manage, let alone too big to fail.

V. The 2008 Crisis: Bailout & Forced Transformation

September 15, 2008, 3:00 AM Amsterdam time. Michel Tilmant's phone rings. Lehman Brothers has just filed for bankruptcy. Within hours, the global financial system freezes. Credit markets seize up. Interbank lending stops. ING's stock price, which closed Friday at €21, opens Monday at €15 and keeps falling. By September 29, it touches €8. The company that seemed invincible two weeks earlier is now fighting for survival.

The problems cascade from multiple directions. ING Direct USA, the crown jewel, suddenly can't fund itself—the commercial paper market it relies on has evaporated. The insurance operations, heavily invested in mortgage-backed securities now deemed toxic, face massive writedowns. Alt-A mortgages—one step above subprime—that ING bought for "diversification" are defaulting at unprecedented rates. The company's Tier 1 capital ratio, the key measure of banking strength, plummets toward the regulatory minimum. Credit default swaps on ING debt—essentially the cost to insure against ING's failure—spike to levels suggesting imminent collapse.

Inside ING's Amsterdam headquarters, crisis meetings run around the clock. The executive board considers every option: asset sales, capital raising, even merger discussions with healthier rivals. But events move too fast. On October 9, the Dutch government announces a €20 billion facility to shore up the country's banks. ING initially resists—taking government money means admitting weakness. But when the stock hits €5.50 on October 10, down 75% from its peak, they have no choice.

October 19, 2008: The Dutch state injects €10 billion into ING, technically purchasing preferred shares but effectively a bailout. The terms are harsh but not punitive—8.5% interest, no voting rights, but with strict conditions that will reshape ING's destiny. The European Commission, guardian of competition law, must approve any state aid. Their verdict, delivered in November 2009 after a year of investigation, is devastating: ING must divest its insurance operations entirely and sell or IPO ING Direct USA by 2013. The bancassurance model, ING's founding principle, is dead by regulatory decree.

The forced restructuring is brutal but clarifying. For the first time since 1991, ING must decide what it actually is—a bank or an insurer, but not both. The choice, perhaps surprisingly, is easy. Banking operations, despite the crisis, remain profitable. Insurance faces long-term headwinds from low interest rates and demographic changes. In November 2011, ING announces its transformation plan: become a pure-play bank, exit insurance completely, and repay the Dutch state as quickly as possible.

The divestment program becomes one of history's largest financial garage sales. ING Direct USA, the unit that revolutionized American banking, sells to Capital One for $9 billion in February 2012—a price that seems low given its $90 billion in deposits but reflects crisis realities. ING Direct Canada goes to Scotiabank for C$3.1 billion. ING Direct UK sells to Barclays for £320 million. Each sale is painful—these aren't just assets but pieces of ING's identity, businesses they built from scratch.

The insurance separation proves even more complex. Rather than sell to a competitor, ING decides to spin off its European insurance operations as a standalone company: NN Group (using the old Nationale-Nederlanden brand). The process takes three years of legal restructuring, IT separation, and regulatory approval. The North American insurance operations, rebranded as Voya Financial, go public on the New York Stock Exchange in May 2013. When ING sells its last NN Group shares in April 2016, the 25-year bancassurance experiment officially ends.

Throughout this period, ING maintains a singular focus: repay the government and regain independence. They sell profitable operations, cut costs ruthlessly, and rebuild capital ratios. The first €5 billion repayment comes in December 2009, earlier than anyone expected. Another €2 billion follows in May 2011. The final €3.5 billion, plus €3.5 billion in interest and premiums, is paid in November 2014. Total repayment: €13.5 billion, making the Dutch state a 35% profit on its crisis investment.

By 2015, ING emerges transformed. From a sprawling conglomerate with operations in 40 countries, it's now a focused European bank present in 15 countries. From 130,000 employees, it's down to 55,000. From €1.3 trillion in assets, it's at €850 billion. The empire is gone, but what remains is leaner, simpler, and surprisingly, more profitable. Return on equity, which averaged 12% during the go-go years, now consistently exceeds 10% with far less risk. The forced dismantling, traumatic as it was, has created something more sustainable.

VI. The Insurance Spinoff & NN Group Creation (2011-2016)

January 2011. Jan Hommen, ING's new CEO (appointed in 2009 to navigate the crisis), stands before employees in Amsterdam's insurance headquarters with a message nobody wants to hear: "After 20 years together, banking and insurance must go their separate ways." The room is silent. Many employees joined ING specifically for its integrated model, the promise of bancassurance. Now they must choose sides—stay with the bank or join what will become NN Group. Families who've worked together for decades will be split. IT systems integrated at enormous cost must be untangled. A corporate culture built on convergence must accept divergence.

The separation isn't just corporate restructuring—it's organizational surgery. Consider the complexity: ING's insurance and banking operations share 3,000 IT systems, 14,000 vendor contracts, and 25,000 employees who work for both divisions. The company occupies 400 buildings where insurance and banking employees sit side by side. They share cafeterias, HR systems, even corporate email addresses. Untangling this while maintaining business continuity seems impossible. Project managers estimate it will take five years and €1.5 billion.

The board appoints Lard Friese, a veteran insurance executive, to lead the separation and become CEO of the future NN Group. Friese faces an existential challenge: create a viable standalone insurance company from operations that haven't been independent since 1991. He must build separate IT infrastructure, establish independent risk management, create a new brand identity, and most critically, convince employees that NN Group has a future worth staying for.

The rebranding reveals the emotional complexity. Market research shows that "Nationale-Nederlanden" still resonates with Dutch consumers—it's their grandparents' insurance company, trusted and stable. But internationally, the name is unpronounceable. The solution: NN Group for corporate identity, with local brands maintained where valuable. The orange lion logo gets redesigned—softer, friendlier, less corporate. The tagline becomes "You matter"—a deliberate contrast to ING's increasingly digital, efficiency-focused messaging.

July 2, 2014, marks the rebirth: NN Group goes public on Euronext Amsterdam at €20 per share, valuing the company at €7 billion. It's Europe's largest IPO that year, attracting strong demand from institutional investors who see value in a pure-play insurer without banking complications. ING retains 68% ownership initially, but EU rules require complete divestment. The remaining shares are sold in tranches—25% in March 2015, another 15% in February 2016, and the final 28% in April 2016.

Meanwhile, the North American insurance operations follow a different path. These businesses—primarily retirement services and employee benefits—need scale to compete in the U.S. market. ING chooses to IPO them as Voya Financial (the name supposedly evokes "voyage" and "journey," though employees joke it sounds like a yoga studio). The May 2013 IPO prices at $19.50, raising $1.27 billion. ING's stake is gradually sold through 2016, completing the American insurance exit.

The financial engineering is impressive. Combined, the NN Group and Voya transactions generate €8 billion for ING—money desperately needed for capital buffers and government repayment. But the human cost is significant. Thousands of employees who joined a bancassurance giant find themselves in standalone companies with uncertain futures. The promised synergies—insurance agents selling banking products, bank branches distributing insurance—never materialized anyway, but the dream took 25 years to officially die.

VII. Digital Transformation & Agile Revolution (2015-2020)

Summer 2015. Ralph Hamers, ING's newly appointed CEO, returns from a pilgrimage to Silicon Valley with a radical idea. He's visited Google, Netflix, and Spotify, studying how they organize work. The traditional banking hierarchy—departments, divisions, regional fiefdoms—seems medieval by comparison. "We're going to blow up the entire organization," he announces to his stunned executive team. "No more traditional departments. We're going all-in on agile."

The transformation Hamers envisions is unprecedented in banking. Instead of traditional departments, ING will organize into "squads"—autonomous teams of nine people maximum, each with a specific mission. Squads group into "tribes"—collections of squads working on related areas. No more traditional managers. Instead, "chapter leads" provide technical expertise while "agile coaches" facilitate collaboration. It sounds like corporate buzzword bingo, but Hamers is deadly serious. He's betting ING's future on becoming a technology company that happens to have a banking license.

The physical transformation comes first. ING's Amsterdam headquarters, a traditional corporate tower with closed offices and hierarchical floor plans, is gutted and rebuilt. Walls come down. Executive offices disappear. In their place: open floors with flexible seating, collaboration spaces, and no assigned desks—not even for Hamers himself. The message is clear: the old ING is dead.

The organizational transformation proves more challenging. In June 2015, ING Netherlands dissolves its traditional structure overnight. Monday morning, 3,500 employees arrive to find they no longer have departments, managers, or even fixed job descriptions. They must apply for positions in the new agile structure—squads focused on specific customer journeys like "buying a home" or "daily banking." Many senior managers, their traditional roles eliminated, must choose between becoming hands-on squad members or leaving. Nearly 1,000 employees depart in the first year.

But something remarkable happens. Freed from bureaucracy, innovation accelerates dramatically. A squad develops a new mobile payment feature in six weeks—something that would've taken 18 months in the old structure. Customer satisfaction scores for digital channels jump 20 points. The mobile app, rebuilt by autonomous squads iterating rapidly, becomes Europe's highest-rated banking app. By 2017, 60% of all customer interactions are digital, up from 30% in 2015.

The technology investments are massive. ING spends €1 billion annually on digital transformation—more than most fintech startups are worth. They build their own cloud infrastructure, develop proprietary AI algorithms for risk assessment, and create open banking APIs before regulators require them. The bank files more technology patents than financial patents. They hire more software engineers than bankers. The IT department, once a cost center hidden in the basement, now drives strategy from the boardroom.

The "THINK Forward" strategy, announced in 2016, codifies this transformation. The goal: become the world's leading digital bank by 2020. Not just digitized—offering online versions of traditional products—but truly digital, with products that couldn't exist without technology. Like Yolt, a standalone app that aggregates all your financial accounts (even competitors') in one place. Or the blockchain-based trade finance platform that reduces transaction times from days to hours.

The cultural transformation proves hardest but most important. ING creates "Orange Code"—a set of values emphasizing speed, simplicity, and customer obsession. Traditional bankers must learn to code, at least basically. Technology staff must understand banking regulations. Everyone must embrace failure—squads are encouraged to experiment, fail fast, and iterate. This is heresy in banking, where failure traditionally meant career death.

By 2020, the transformation is largely complete. ING operates 350 squads in 13 tribes across its key markets. Product development cycles have shortened from years to weeks. The cost-to-income ratio, a key efficiency metric, drops to 50%, among Europe's best. Customer numbers grow to 40 million despite branch closures. Most remarkably, ING's market capitalization exceeds many banks with twice its assets—investors are betting on the technology platform, not just the balance sheet.

VIII. Modern Era: Pure Banking & Future Bets (2020-Present)

March 2020. COVID-19 lockdowns sweep across Europe. Banks face an existential test: can customers bank without branches? For ING, already 70% digital, the answer is an emphatic yes. While competitors scramble to enable remote work and digital services, ING's squads simply continue iterating from their homes. Mobile app usage surges 45% in three months. Digital onboarding, where new customers join without visiting a branch, increases tenfold. The pandemic doesn't disrupt ING's digital transformation—it validates it.

Steven van Rijswijk, who succeeded Hamers as CEO in July 2020, inherits a radically different bank than existed a decade earlier. The new strategy, unveiled in 2021, is telling: "Accelerating our digital transformation." Not starting, not continuing—accelerating. The ambition has grown from being Europe's digital leader to competing globally with Big Tech. ING now benchmarks itself against PayPal and Square, not just Deutsche Bank or BNP Paribas. The technology investments are massive and strategic. ING's annual ICT spending was estimated at $1 billion in 2024, comparable to many pure-play technology companies. AI, blockchain, cloud, and payments are among the key technologies under focus for the company. But it's not just about spending—it's about fundamental transformation. Since launching in September 2023, thousands of customers have interacted with ING's new gen AI chatbot, making it the first-of-its-kind real-life customer-facing pilot conducted in Europe.

The AI implementation reveals ING's sophisticated approach to technology adoption. At ING, they have a 20-step process which evaluates any AI system for 140 risks, according to Bahadir Yilmaz, ING's chief analytics officer. This isn't Silicon Valley's "move fast and break things"—it's "move fast but don't break the bank." ING sees potential in using AI and machine learning technologies in know your customer processes, client services, sustainability transition plans, pricing, marketing campaigns and fraud.

The sustainability angle particularly stands out. ING's commitment to sustainable banking has driven innovative uses of AI in environmental assessment. "We have this ambition to be a sustainable bank"—using AI to help frontline process customers see how green a deal might be and use that as a decision point. This isn't greenwashing—it's using technology to embed environmental considerations into daily banking decisions. The financial performance validates the transformation. ING posts full-year 2024 net profit of €6,392 million with total income increasing to a record €22.6 billion. Fee income has increased 11% year-on-year, following an increase in both assets under management and in customer trading activity in Retail, while fee income growth in Wholesale Banking was mainly driven by a higher number of capital markets issuance deals. The diversification away from pure interest income—critical in a volatile rate environment—demonstrates the wisdom of the digital transformation.

The number of mobile primary customers increased by 1.1 million to 14.4 million mobile primary customers, with Germany, the Netherlands, Spain and Poland especially contributing to the growth. Core lending has also grown across all markets, by €28 billion, with particularly strong growth of €19 billion in the mortgage portfolio. The deposit base has risen by €47 billion. These aren't just numbers—they represent millions of customers choosing a bank that barely has physical branches over traditional competitors.

The sustainability commitment goes beyond greenwashing. ING increased its sustainable volume mobilised to €130 billion, up from €115 billion in 2023, showing strong progress against the 2027 target of €150 billion per annum. This isn't just about ESG compliance—it's about positioning ING at the center of Europe's green transition, financing everything from renewable energy to sustainable agriculture.

IX. Playbook: Strategy Lessons

The bancassurance experiment stands as one of finance's great "what-ifs." From 1991 to 2008, ING pursued a strategy that seemed unassailable: combine insurance's capital with banking's distribution, cross-sell relentlessly, achieve global scale. The logic was impeccable on PowerPoint slides. Insurance companies generate massive float—premiums collected today, claims paid years later. Banks need capital for lending. Merge them, and you create a perpetual motion machine of financial services.

Why did it fail? Not because the strategy was wrong, but because complexity kills. Managing a bank is hard enough—interest rate risk, credit risk, operational risk. Managing an insurance company is equally complex—actuarial risk, longevity risk, catastrophe risk. Combine them, and you don't get synergy—you get chaos. Risk models that work for banking don't translate to insurance. Regulators who understand banking don't grasp insurance. Customers who trust you with their savings don't necessarily trust you with their life insurance. The promised cross-selling never materialized at scale. Worse, when the 2008 crisis hit, the complexity became toxic. Losses in one division infected the other. Regulators couldn't assess the combined risk. Markets lost confidence in the hybrid model.

The crisis management playbook deserves its own business school case study. When the Dutch government demanded ING dismantle its empire, most expected a fire sale—desperate asset dumps at distressed prices. Instead, ING played a longer game. They negotiated with Brussels for time, arguing that rushed sales would destroy value for taxpayers who'd funded the bailout. They identified crown jewels—ING Direct USA, the insurance operations—and prepared them for sale like a private equity firm prepping a portfolio company. They cleaned up balance sheets, simplified operations, and waited for markets to recover. When they finally sold, they achieved respectable prices: $9 billion for ING Direct USA, successful IPOs for NN Group and Voya. The lesson: in crisis, time is your most valuable asset. Fight for it.

The digital pioneering strategy offers a different lesson: being first matters less than being persistent. ING Direct launched in 1997, years before "fintech" existed. The model was revolutionary but also fragile. No branches meant no physical presence when customers had problems. High interest rates attracted hot money that fled at the first sign of trouble. The technology, cutting-edge in 1997, became legacy by 2007. Many competitors launched similar offerings—HSBC Direct, Citibank Direct, countless others. Most failed or retreated. ING succeeded not because they were first but because they kept investing, iterating, improving. Each country launch taught lessons applied to the next. Each technology upgrade built on the previous. By the time competitors caught up, ING had a decade of learning embedded in their operations.

The agile transformation at scale might be ING's most important contribution to management theory. How do you transform a 60,000-person organization with centuries of history into something resembling a Silicon Valley startup? Not through incremental change—that's been tried and failed countless times. ING chose shock therapy. Dissolve all departments overnight. Force everyone to reapply for new roles. Eliminate management layers ruthlessly. It was brutal, chaotic, and exactly what was needed. The lesson: organizational antibodies will kill incremental change. Sometimes you need chemotherapy, not vitamins.

The European banking challenge frames everything else. European banks face structural headwinds American or Asian banks don't. Negative interest rates for nearly a decade destroyed traditional banking economics. Regulatory burden from Brussels makes innovation harder. Language and regulatory fragmentation prevents true pan-European scale. Fintech competition is fierce, with companies like Revolut and N26 growing faster than traditional banks ever could. Yet ING thrives in this environment. How? By accepting reality rather than fighting it. They don't bemoan regulation—they embed compliance in their DNA. They don't fear fintechs—they learn from them. They don't chase global dominance—they focus on European excellence.

X. Bear vs. Bull Case

The Bull Case: ING represents the rare successful transformation of a traditional bank into a digital platform. Start with the fundamentals: a cleaned-up balance sheet, simplified structure, and clear strategic focus. The company operates in wealthy European markets with deep banking penetration but significant digital transformation opportunity. Their technology platform, built through billions in investment and years of agile transformation, creates a moat competitors can't easily cross. Traditional banks lack the culture and technology. Fintechs lack the scale and regulatory licenses. ING sits in the sweet spot—digital enough to compete with startups, established enough to be trusted with mortgages and corporate loans.

The numbers support the transformation story. Return on equity consistently exceeds 10% despite the low-rate environment. The cost-to-income ratio at 50% ranks among Europe's best. Customer acquisition costs are a fraction of traditional banks. Digital engagement metrics—app usage, digital sales, customer satisfaction—lead European peers. The €2 billion share buyback program announced in 2024 signals management confidence. Trading at roughly book value, ING offers growth potential at value prices.

The sustainability leadership creates another growth vector. As Europe transitions to net-zero emissions, trillions in capital must be redirected from brown to green assets. ING's expertise in sustainable finance, proven track record, and €150 billion commitment position them as the banker to Europe's green transformation. This isn't ESG window dressing—it's a strategic bet on where capital flows are heading.

The Bear Case: ING is a European bank, and European banking is structurally challenged. GDP growth remains anemic. Demographics are terrible—aging populations save rather than borrow. Interest rates, while no longer negative, remain historically low, compressing margins. Regulation from Brussels grows ever more complex and costly. Political fragmentation makes true pan-European banking impossible. ING may be the best house in a bad neighborhood, but it's still in a bad neighborhood.

The competitive threats are multiplying. Big Tech looms—Apple, Google, and Amazon all have payment ambitions. Embedded finance means every company can become a bank. Crypto and DeFi threaten the entire banking model. Even if ING navigates these threats, where's the growth? They're already dominant in the Netherlands and Belgium. Germany is competitive and low-margin. Eastern European expansion faces political risk. Without new markets, ING is a GDP-growth bank in a low-growth continent.

The technology leadership, while real today, faces obsolescence risk. ING spent billions building their digital platform, but what if AI makes that investment obsolete? Startups using large language models can now build in months what took ING years. The agile transformation, impressive as it was, happened once—can they do it again when the next disruption arrives? Corporate transformations have a limited shelf life. Today's innovation becomes tomorrow's legacy.

Valuation offers limited upside. At €40 billion market cap, ING trades at a reasonable but not cheap 0.7x book value. European bank multiples have been compressed for a decade—why would that change? The dividend yield of 7% is attractive but reflects limited growth expectations. Share buybacks are nice but essentially return capital that can't be profitably deployed—not exactly a growth signal.

XI. Epilogue & Reflections

The most surprising element of ING's story isn't the successful transformation—it's how the forced dismantling became liberation. Companies rarely improve by getting smaller, yet ING did exactly that. Stripped of insurance, forced to exit markets, compelled to simplify, ING discovered focus. The bancassurance empire, impressive as it seemed, was ultimately a distraction. The real value was always in the banking franchise, particularly the digital capabilities built through ING Direct. The crisis didn't destroy ING—it revealed its true nature.

What does ING's journey teach about banking transformation? First, that technology alone isn't enough. Plenty of banks have spent billions on digital initiatives with little to show for it. ING succeeded because they changed everything—culture, organization, mindset—not just systems. Second, that crisis can be catalyst. Without the 2008 bailout and forced restructuring, ING might still be a sprawling conglomerate, too complex to manage, too diversified to excel. Third, that focus beats scale. The modern ING, a fraction of its former size, creates more value than the empire ever did.

The future of traditional banks in a digital world remains uncertain, but ING offers a template. Don't try to beat fintechs at their own game—combine their agility with your advantages of trust, regulation, and balance sheet. Don't fear Big Tech—learn from their customer obsession and platform thinking. Don't resist change—embrace it so thoroughly that you become unrecognizable from your former self. The banks that survive won't be the biggest or oldest, but the most adaptable.

The orange lion that symbolizes ING has lived many lives: insurance company, postal bank, global conglomerate, crisis victim, digital pioneer. Each transformation seemed to kill the previous incarnation, yet somehow the essential spirit survived and strengthened. Perhaps that's the ultimate lesson—in finance, as in evolution, it's not the strongest that survive, but the most adaptable to change.

Looking ahead, ING faces new challenges that will test this adaptability again. Artificial intelligence threatens to commoditize the digital advantages they've built. Climate change will stress-test their sustainable finance commitments. Geopolitical fragmentation could fracture their European franchise. Yet if history is any guide, ING will adapt, transform, and emerge different but stronger. The company that began as fire insurance for Amsterdam merchants has become something its founders could never imagine: a digital platform that happens to have a banking license, serving customers who rarely visit a branch, in a world where money is mostly electronic.

The story of ING is ultimately about resilience through reinvention. It's about having the courage to destroy what you've built when it no longer serves. It's about turning existential crisis into opportunity for rebirth. And it's about recognizing that in business, as in life, the only constant is change—and the only sustainable advantage is the ability to change faster than your environment. The orange lion will surely transform again. The only question is into what.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube