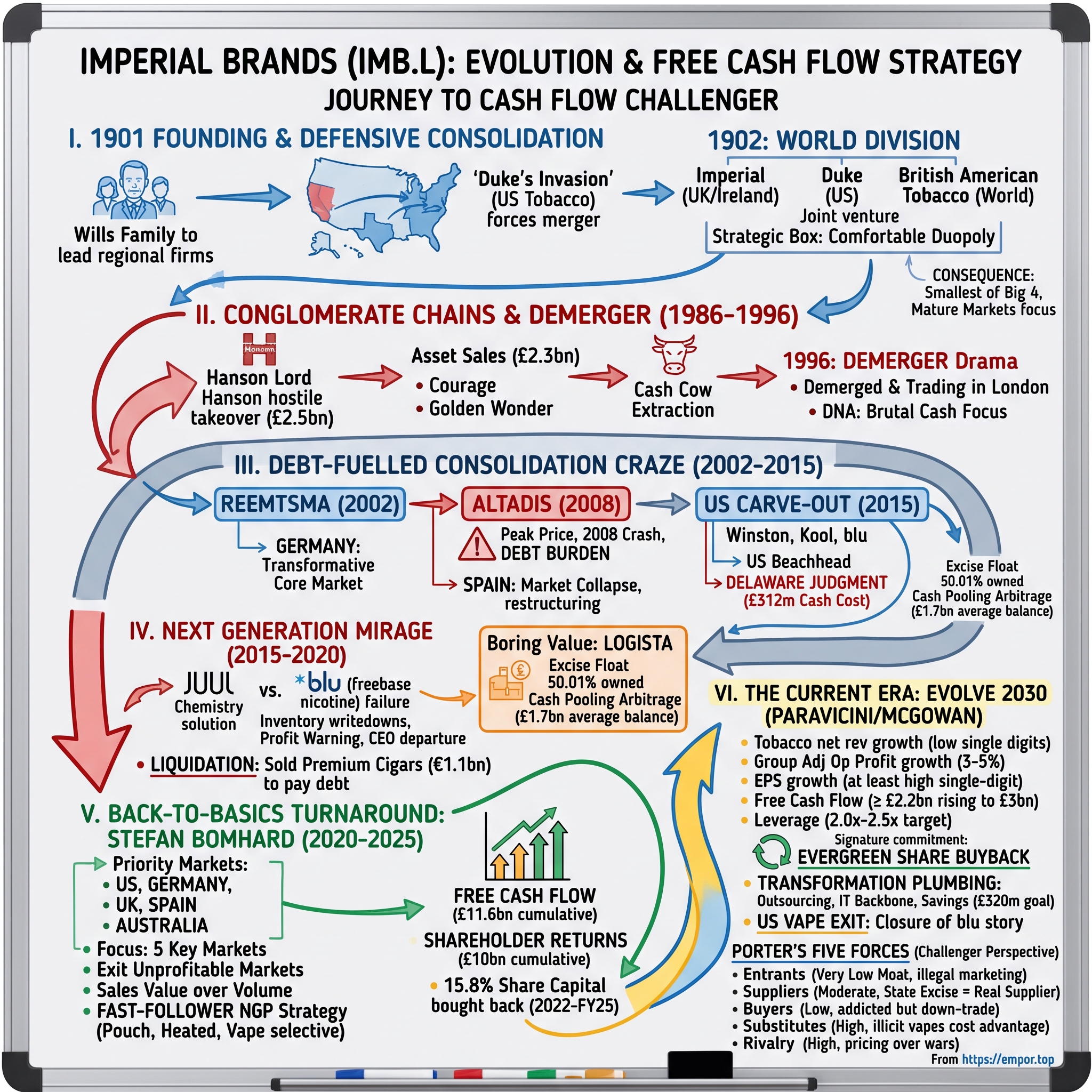

Imperial Brands: The Evolution of the Ultimate Cash-Flow Challenger

I. Introduction & Episode Roadmap

On the morning of May 12, 2026, in a presentation room in London, Lukas Paravicini stood in front of a group of sell-side analysts and did something that most chief executives of consumer companies spend their careers avoiding. He pointed at a slide showing that his company had lost market share — 60 basis points across the five markets that generate the bulk of its profit — and told the room this was not a problem. It was the plan.

"Not all basis points of market share are equal," he said.1

Sit with that for a moment. This is a company whose entire investment case, for the last five years, had been built on the promise that it would stop bleeding share. Its previous chief executive had made "we are no longer the industry's share donor" into something close to a corporate mantra. And here was his successor, seven months into the job, calmly explaining that giving up volume in the cheap end of the cigarette market was a feature rather than a bug — because the gross margin on a premium pack had drifted so far above the gross margin on a discount pack that chasing the discount consumer had become a bad trade.

Whether that is disciplined capital allocation or a convenient retrofit of the story around a disappointing number is the central question this article will keep returning to. It is genuinely hard to tell from a single half-year, and the honest answer is that we do not yet know.

Here is the hook. Imperial Brands PLC (IMB.L) is the smallest of the world's four big listed tobacco companies. It operates in an industry under permanent regulatory siege, selling a product whose volumes decline structurally every single year — management's own long-run planning assumption is a 3% to 5% annual volume decline.1 It has no global technology franchise to speak of: no IQOS, no ZYN, nothing remotely comparable. Its next-generation products business generated £368 million of net revenue in the year to September 2025 and lost £76 million doing it.2

And yet, in the twelve months to March 2026, this company generated £2.6 billion of free cash flow.1 It has committed to buying back £1.45 billion of its own stock in FY26 — roughly 5.7% of its share capital as of September 30, 2025.[^3] Add the dividend and total capital returns for the year exceed £2.7 billion.2 Since 2021, cumulative returns to shareholders have reached £11.5 billion, which management notes is around 77% of what the entire company was worth when the current strategic journey began in January 2021.1

Read that again. Over five and a bit years, Imperial has handed back to shareholders roughly three-quarters of its own starting market capitalisation — and it still exists, still grows profit, and still trades.

The thesis — and it is a thesis to be tested, not accepted — is that Imperial Brands is a study in corporate pragmatism verging on corporate fatalism. While Philip Morris International and British American Tobacco have spent tens of billions attempting to build global next-generation product monopolies, Imperial did something almost countercultural: it scaled back. It picked five markets, defended them, harvested the rest, and routed the resulting cash into its own shares at a rate that would make an LBO sponsor blink.

Underpinning it is one of the more unusual treasury structures in European large-cap equity: a majority-owned, separately listed logistics subsidiary called Logista, whose float of excise-duty cash Imperial borrows against daily.

The bear case is equally simple: this is a beautifully run liquidation. The buyback is not a sign of strength but the only remaining use for capital in a business with no future. Imperial is retiring equity because it cannot find anything better to do — and when the volume declines finally outrun the price increases, there is no second act.

Both readings fit the facts. That tension is the story.

The roadmap: the defensive consolidation of 1901 against an American invasion; the conglomerate years under Hanson and the 1996 demerger that set Imperial free; the debt-fuelled acquisition spree from Reemtsma through Altadis to the 2015 American carve-out; the vaping mirage and the leadership crisis it triggered; Stefan Bomhard's back-to-basics turnaround; and the Paravicini era now unfolding, with its "Evolve 2030" strategy and its evergreen buyback.

It starts, as so many British corporate stories do, with an American showing up and threatening to destroy everything.

II. The 1901 Founding: Defending Against the "Duke's Invasion"

In the autumn of 1901, James Buchanan "Buck" Duke stepped off a ship in Liverpool, walked into the offices of Ogden's — one of Britain's better cigarette manufacturers — and bought it. Then, according to the accounts of the period, he is said to have announced his intentions to the British trade with a bluntness that has echoed through business history: he had come to buy the market.

Duke was not bluffing, and the British had every reason to be terrified. His American Tobacco Company had spent the 1890s doing to the United States cigarette industry what Standard Oil had done to refining: mechanising production with the Bonsack rolling machine, spending ruinously on advertising, cutting prices below cost, and buying the survivors. He arrived in England with the same playbook and a war chest the British family firms could not match individually.3

And individually was precisely how the British tobacco industry existed. These were not corporations in any modern sense. They were dynasties — Quaker and Methodist merchant families, most of them, who had been rolling tobacco in the same provincial cities for a century and who regarded one another with the wary competitiveness of neighbours rather than the strategic clarity of rivals. W.D. & H.O. Wills of Bristol was the largest. John Player & Sons of Nottingham was the most famous. Stephen Mitchell & Son of Glasgow, Lambert & Butler, Franklyn Davey, Hignett Brothers, F. & J. Smith and the rest were smaller regional houses, each with its own brands, its own works, and its own profound reluctance to be told what to do by anyone.

Duke's arrival did what a hundred years of commercial logic had not: it made them arithmetic-minded. Alone, each would be picked off. Together, they had scale.

In December 1901, thirteen British tobacco and cigarette manufacturers met and merged, forming The Imperial Tobacco Company (of Great Britain and Ireland) Limited, under the leadership of the Wills family.3[^5] It was, in the truest sense, a defensive merger — a corporate lifeboat. Nobody woke up that morning wanting to share ownership with twelve competitors. They did it because the alternative was extinction.

What happened next is the part that deserves attention, because it reveals something about the character that would define this company for the next 125 years. Imperial did not simply dig in and defend. It counter-attacked — announcing plans to invade the United States, Duke's home market, and fund a price war on his own territory. It was a strategy of mutually assured destruction: we cannot beat you, but we can make winning cost you more than it is worth.

It worked. Duke, a rational monopolist above all else, recognised that a transatlantic price war would incinerate both parties' profits for years. So on September 27, 1902, the two combines stopped fighting and did something far more profitable: they divided the world.3

The settlement was elegant in its cynicism. American Tobacco surrendered Ogden's to Imperial and took the United States as its exclusive territory. Imperial took the United Kingdom and Ireland and abandoned its American ambitions, retaining only the right to buy leaf there. And everything else on Earth — every other market on the planet — was handed to a jointly owned vehicle registered in London that same year, two-thirds owned by American Tobacco and one-third by Imperial, with Duke as its first chairman. Its name was the British American Tobacco Company.3

Yes: BAT, today Imperial's largest and most direct competitor, began life as Imperial's own joint venture — the entity created to hold the rest of the world so that Imperial and Duke would not have to fight over it.

The legacy of 1902 for the modern investor is not nostalgia. It is structural, and it is arguably the single most consequential fact in Imperial's corporate life. In one afternoon, Imperial traded away the entire planet in exchange for a guaranteed, comfortable, profitable domestic duopoly. For the next seventy years it was a very rich company operating in a very small box. While BAT built the global distribution network that would eventually make it a titan, Imperial sold cigarettes to Britain and Ireland — and got extremely good at it, and extremely narrow.

Every acquisition in Section IV of this story — Reemtsma, Altadis, the American carve-out — is, in a real sense, Imperial spending the twenty-first century and tens of billions of pounds trying to buy back what it gave away in 1902. It has never fully succeeded. Imperial remains, to this day, the fourth-largest player in a four-player industry, structurally concentrated in mature Western markets. The company's own strategy documents describe it as a "challenger."4 That is a modern word for a condition set in 1902.

But before Imperial could go shopping for the world, it had to survive something arguably more disorienting than Buck Duke: becoming a line item on someone else's balance sheet.

III. Conglomerate Chains & Demerger Drama (1986–1996)

By the mid-1980s, the company that had faced down American Tobacco had become exactly the kind of business that made a certain type of investor salivate — and not in a good way.

Imperial Group, as it was then called, had done what many cash-rich businesses do when the core matures and management gets restless: it diversified. Aggressively. Into things it had no particular reason to be good at. By 1986 the group that made Player's and Wills cigarettes also owned Courage, the brewer. It owned Golden Wonder, the crisp maker. It owned hotels and catering, frozen foods, and a scattering of other assets acquired on the theory that tobacco cash had to go somewhere and somewhere might as well be everywhere.

The strategic logic was that combustible tobacco was a declining industry and the cash should be redeployed. The strategic result was that a superb cigarette business was subsidising a portfolio of mediocre also-rans, and the market noticed. Imperial Group's shares reflected the whole, not the jewel. That gap between the sum of the parts and the price of the whole is the oxygen corporate raiders breathe.

Enter Lord Hanson and Lord White.

Hanson Trust plc was the most feared acquisition machine in Britain — a transatlantic partnership in which James Hanson ran the UK and Gordon White ran America, and both operated on a philosophy of arithmetic purity. They did not believe in synergy. They did not believe in vision. They believed that most corporate assets were run badly by people insulated from consequences, and that you could buy such a company, sell the parts nobody should have owned, strip the head office to a skeleton, hold management to brutal cash targets, and pocket the difference. It was the LBO ethos in listed-company form, executed with a showman's relish.

In 1986, Hanson took Imperial Group in a hostile takeover valued at £2.5 billion — at the time one of the largest transactions in British corporate history.[^5]5

What followed was a masterclass in dismantling, and a nine-year education for Imperial's own management. Hanson sold Courage to Elders. Golden Wonder went to Dalgety. The hotels and catering business went to Trust House Forte, Ross Frozen Foods to United Biscuits, and the wholesaling arm of Sinclair & Collis to Palmer & Harvey. In total the divestments recovered roughly £2.3 billion — meaning Hanson effectively acquired one of the best cash-generating tobacco businesses in the world for a rounding error, having sold everything else to pay for it.5

And then, having stripped it, Hanson ran the remaining tobacco business as a pure cash cow — which turned out to be the best thing that ever happened to it. Under Hanson's ownership between 1987 and 1995, Imperial's productivity nearly trebled, the brand portfolio was refocused, and market share went up.[^5]

There is an uncomfortable lesson here for anyone who instinctively roots for management against raiders. Hanson was not a good custodian in any romantic sense. He was an extractor. But the discipline he imposed — no vanity projects, no diversification, no empire, relentless focus on cash conversion and cost — produced a tobacco business measurably better than the one he had bought. Imperial's modern DNA, the almost unsentimental focus on cash that defines it today, was not invented by Stefan Bomhard in 2021. It was beaten into the company by a corporate raider in the late 1980s.

The irony is that the conglomerate model then died of the same disease it had diagnosed in Imperial. By the mid-1990s investors had concluded that Hanson Trust itself was a collection of unrelated assets trading below the sum of its parts. The predator had become the prey, and Hanson, to his credit, saw it first. In January 1996 he announced that Hanson Trust would break itself into four separate listed companies: Hanson plc, The Energy Group, Millennium Chemicals — and Imperial Tobacco.[^5]5

On October 1, 1996, Imperial Tobacco Group PLC demerged and began trading on the London Stock Exchange.[^5]

For the first time in a decade — arguably for the first time ever, given the constraints of 1902 — Imperial's management controlled its own capital allocation. What it inherited was a paradox that would define the next twenty years: an exceptionally lean, highly profitable, brutally efficient cash machine, and almost nowhere to sell. A world-class operator locked in a shrinking domestic market, with a balance sheet capable of borrowing and a board that had just been handed the keys.

You can probably guess what happened next.

IV. The Debt-Fuelled Consolidation Craze (2002–2015)

Imagine you are Imperial's board in the early 2000s. You run the most efficient cigarette business in the world by unit cost. Your problem is that your home market is shrinking, your brands are barred from advertising, and your competitors — Philip Morris, BAT, and 日本たばこ産業 Japan Tobacco — are global while you are not.

You have exactly one lever. Credit is cheap, your cash flows are the most predictable on the London market, and lenders will hand you almost unlimited debt against them. So you go shopping.

Reemtsma: the deal that worked

The first move was the good one. In 2002, Imperial acquired Germany's Reemtsma for €5.8 billion.[^5] It was transformative in the most literal sense: it took Imperial from a British company with international ambitions to a genuine continental European player overnight. It delivered a dominant position in Germany — which, two decades later, remains one of the two markets that together generate roughly half of Imperial's revenue and profit2 — plus positions across Central and Eastern Europe, and a brand portfolio including West and Davidoff.

Reemtsma is the deal that quietly justifies everything. Germany today is a high-affordability market with a predictable five-year excise regime, and Imperial's German business has been one of its better performers. Not every acquisition in this section will earn that sentence.

Altadis: the €15 billion deal signed at the top of the market

By 2007, Imperial's ambitions had outgrown its caution. The target was Altadis — the merged Franco-Spanish state tobacco monopoly, itself a product of the privatisation wave, holder of Gauloises and Gitanes, half of the Cuban cigar monopoly, and something Imperial's bankers may not have fully appreciated at the time: a majority stake in a distribution business called Logista.

The deal was announced in July 2007 and completed on January 25, 2008, at €50 per share in cash — an enterprise value for Altadis of approximately €15.2 billion, or £11.3 billion at the exchange rate on completion, including Altadis' net debt and minority interests.6 (Some accounts cite figures closer to €16 billion; Imperial's own filing at completion is the number used here.)

Now look at that completion date again. January 2008.

Bear Stearns collapsed in March. Lehman Brothers failed in September. And Imperial Tobacco had just funded the largest acquisition in its history entirely with debt, at a cyclical peak, weeks before the global financial system seized. It is difficult to construct a worse-timed large-cap acquisition in modern European history without deliberately trying.

It got worse. The single largest asset Imperial bought was a commanding position in the Spanish tobacco market. Within two years, Spain suffered one of the most severe economic collapses in the developed world, with youth unemployment above 40% and a consumer utterly destroyed. Spanish smokers traded down violently, and the premium volumes Imperial had paid a premium multiple for evaporated. The company spent the better part of a decade restructuring and deleveraging under debt raised against cash flows that did not arrive as modelled.

The analytical point is not that management was stupid — the strategic logic of buying scale in Europe was defensible. The point is about how the deal was financed and when. An all-debt acquisition at a peak multiple removes your ability to be wrong. Imperial had no equity cushion and no optionality. It simply had to grind the debt down over ten years, and it did, at the cost of a decade of strategic freedom. When people ask why Imperial did not build an IQOS while PMI did, part of the answer is that Imperial spent the 2010s paying for Spain.

There is a deep irony buried in Altadis that took fifteen years to surface. The asset in that deal that has most reliably created value was not Gauloises, and not the Cuban cigars — it was Logista, the boring distribution business that came along almost as an afterthought. We will return to it, because it turns out to be the most interesting thing about Imperial's balance sheet.

The 2015 American carve-out: a beachhead with a hidden invoice

By 2014, Imperial saw an opening created by someone else's problem. Reynolds American was buying Lorillard for $27.4 billion, and the Federal Trade Commission was not going to permit it without a divestiture package substantial enough to sustain a viable third competitor in the US market.[^9]

Imperial stepped up. On June 12, 2015, it completed the acquisition of Winston, Kool, Salem and Maverick, along with the blu e-cigarette brand, certain cigar brands including Backwoods and Dutch Masters, and Lorillard's Greensboro, North Carolina manufacturing plant with roughly 2,900 employees, for $7.1 billion. The vehicle was christened ITG Brands, and it made Imperial the third-largest tobacco company in the United States overnight.78

For a company locked out of America by a treaty signed in 1902, this was the reversal of a century-old exile. It was also, on inspection, a more complicated prize than the headline suggested.

Consider what a regulatory divestiture package actually is. It is not a portfolio a seller assembled to maximise value. It is the minimum set of assets a regulator will accept to bless a deal the seller actually wants. Reynolds was not selling Camel or Newport. It was selling declining sub-premium brands it had deprioritised for years — brands that required constant promotional spending merely to hold flat share. Imperial acquired volume and a route to market, not pricing power. And blu, the asset that generated the most excitement, was about to be rendered obsolete by a technology Imperial had not noticed.

But the sharpest lesson from 2015 did not land for a decade — and it arrived in a Delaware courtroom.

When Reynolds sold those brands, it also purported to transfer the associated obligations under the historic US state tobacco settlements. Imperial's ITG Brands disputed the extent of what it had assumed with respect to Florida. Reynolds paid the state and sued. In March 2025 a Delaware judge ruled that ITG owed Reynolds $251.5 million for the Florida settlement payment.9 In December 2025, the Delaware Supreme Court affirmed the judgment, with interest bringing the total to roughly $370 million.10 Imperial paid $200 million in the first half of FY26, with the remaining $234 million due in roughly equal instalments over the following three years — a total charge of £312 million.1011

This is what "buying a divestiture package" can mean in practice. Ten years after closing, Imperial was still writing cheques for liabilities that attached to brands it bought in 2015 — and the cash cost lands in the free cash flow of a company whose entire equity story is built on free cash flow. On the half-year call, CFO Murray McGowan handled it the way a confident CFO handles a bad number: he disclosed the payment schedule explicitly, adjusted the historical charge out of underlying profit, and left the cash in the free cash flow line where investors could see it.1 That is a defensible treatment. It is also worth noting that the guided figure of "at least £2.2 billion" of FY26 free cash flow is stated including these payments — the company is not hiding behind the adjustment.1

The roll-up era left Imperial with scale, a US beachhead, and a debt load that took a decade to digest. What it did not leave was a technology strategy. And by 2015, a small startup in San Francisco was about to demonstrate exactly how expensive that omission would be.

V. The Next Generation Mirage: Vaping, Write-downs, and Leadership Crisis (2015–2020)

To understand what happened to Imperial between 2015 and 2020, you need to understand a small piece of chemistry — and the fact that a multi-billion-pound strategy was destroyed by it.

Nicotine in its natural state is what chemists call a freebase: alkaline, harsh, unpleasant in the throat at high concentrations. Every e-cigarette of the early 2010s, including blu, used freebase nicotine liquid. This imposed a hard ceiling on the product. You could not load enough nicotine into the liquid to deliver a genuinely satisfying hit, because the vapour would be too harsh to inhale. So blu and its peers delivered a mild, slow, unsatisfying dose. It was a gadget for the curious, not a substitute for a cigarette.

Think of it as trying to sell someone a replacement for espresso when your product can only ever be weak tea. You can market the tea brilliantly. You can put it in every convenience store in America. It will never be espresso.

JUUL Labs solved the chemistry. By adding an acid to convert the nicotine into a salt, JUUL lowered the pH, removed the harshness, and made high-concentration nicotine smooth enough to inhale — producing a blood-nicotine curve that actually approximated a cigarette. It was, functionally, a different product category wearing the same clothes.

Imperial did not see it coming, and the consequences compounded in the worst possible sequence. Under CEO Alison Cooper — who had joined the company in 1999 and taken the top job in 2010 — blu had been positioned as the centrepiece of Imperial's transition, pitched to investors as a high-margin additive growth engine.12 Imperial pushed blu into distribution aggressively. Then JUUL took the market, and Imperial discovered the specific horror of the consumer-goods world: a vast quantity of slow-moving inventory sitting on shelves in a category where the product spec had just moved.

Meanwhile, on the other side of the ledger, Philip Morris was pouring billions into IQOS and building a genuine global heated-tobacco franchise. Imperial was essentially absent. It had bet on the wrong horse in one category and skipped the other entirely.

The reckoning arrived in the autumn of 2019. Imperial issued a profit warning citing a "marked slowdown" in e-cigarette growth, driven by the American regulatory crackdown on vaping — wholesalers and retailers had stopped ordering and promoting the product.1213 The company had already cut its 10% dividend growth target earlier that year to fund the NGP push, which meant income investors had given up cash on the promise of a growth engine that then failed to appear. That is a particular kind of betrayal, and the market treated it accordingly.

On October 3, 2019, Imperial announced that Alison Cooper would step down once a successor was found, ending twenty years at the company and nine as chief executive.1213 The subsequent results carried substantial write-downs against NGP inventory, machinery and intangibles.

It is worth being fair about the failure, because the lazy reading is that management was foolish. The more useful reading is that Imperial made a structural error rather than a tactical one: it entered a technology category with a consumer-marketing mindset. In tobacco, the product does not change; the brand does the work. In vaping, circa 2017, the product was changing every eighteen months and the brand was worth almost nothing. Imperial optimised distribution and marketing for a product whose underlying technology was being obsoleted underneath it. Cooper's team was playing the game they knew, on a board where the rules had changed.

The final act of the old regime was the liquidation of the crown jewels. In April 2020, Imperial agreed to sell its worldwide premium cigar business, completing the transaction on October 29, 2020 for total consideration of €1,225 million.1415 It was structured as two deals: Gemstone Investment Holding took the US business — Tabacalera USA, Altadis U.S.A., the JR Cigars catalogue business and the Casa de Montecristo retail estate — for €185 million; and Allied Cigar Corporation took the rest of the world for €1,040 million, including Imperial's 50% stake in Cuba's Habanos S.A., the VegaFina brand, and the Tabacalera de García factory in the Dominican Republic.1516 Net proceeds of roughly €1.1 billion went to reducing debt.15

There is something almost elegiac about it. Habanos — Cohiba, Montecristo, the Cuban monopoly, the single most romantic asset in the tobacco world, acquired in the Altadis deal — sold for cash, to pay down the debt raised to buy it. The romance did not survive contact with the balance sheet.

That is the state of the company Stefan Bomhard walked into in July 2020: a business that had failed at technology, lost its chief executive, cut its dividend growth, sold its most glamorous asset, and had just been reminded — with unusual clarity — that it was the fourth-largest player in a four-player industry.

Which, it turned out, was the most useful thing anyone could have told him.

VI. The Back-to-Basics Turnaround: Stefan Bomhard's Strategy (2020–2025)

Stefan Bomhard did not come from tobacco, and that was the entire point.

Born in Germany in 1967, he had assembled one of the more thoroughly consumer-facing résumés in European business: Procter & Gamble, then Diageo's Burger King business, then chief operating officer of Unilever Food Solutions Europe, then chief commercial officer of Cadbury, then president of Bacardi's European region, and from 2015, chief executive of Inchcape plc — the global automotive distributor. Imperial announced his appointment in February 2020, and he took over in July.17

Look at that career and one thing jumps out: this is a distribution and brand executive, not a product executive. Burger King, Cadbury, Bacardi, Inchcape — these are businesses where you do not invent the thing, you understand the consumer, position the brand, and control the route to market. Imperial's board, having just watched the company lose a technology war it should never have entered, hired a man whose entire professional life had been spent proving that you can win without inventing anything.

Bomhard's first act was the hardest one: an honest assessment. Imperial was the smallest of the Big Four. It lacked the balance sheet and the R&D budget to fight a global, multi-billion-pound technology war against PMI or BAT. Every attempt to pretend otherwise had destroyed value.

So in January 2021, he launched a five-year plan built on the radical proposition that Imperial should do less.

The five priority markets

The core move was concentration. Imperial would focus the overwhelming majority of its tobacco resources on five markets — the United States, Germany, the United Kingdom, Spain and Australia — which together account for the substantial majority of adjusted tobacco operating profit. Everything else would be managed for cash or exited.

This sounds obvious. It was not. It meant deliberately under-investing in dozens of countries where Imperial had operations, history, and local management with ambitions. It meant telling the organisation that its job was no longer to be everywhere.

Alongside it came a shift in sales philosophy from volume to value: localised pricing, territory-by-territory shelf placement, and investment in sales force coverage and technology in the two markets that mattered most. As Paravicini would later describe it, Imperial "extended sales coverage in Germany and the U.S." and "increased significantly productivity by adding technology to that."2

And NGP was ruthlessly cut down. Exit the unprofitable markets. Stop pretending to be global. Focus selectively: heated tobacco in Southern and Eastern Europe via the Pulze device, modern oral pouches in Europe and eventually the US, vaping in Western Europe where the category was already established. The stated rule — still in force today — is that Imperial enters a market only "where the category has been created and where we have an existing route to market."1

That is a fast-follower doctrine stated out loud. It is an admission that Imperial will never create a category. It will wait for someone else to spend the money proving one exists, then arrive with brands and distribution. Whether that is wisdom or resignation depends entirely on whether the categories keep being created by others — and whether Imperial's late arrival can still buy meaningful share.

The unsung hero: Logista and the cash-pooling arbitrage

Here is the mechanism almost nobody outside the sector understands, and it deserves careful explanation because it is genuinely unusual.

Imperial owns 50.01% of Logista, a separately listed distribution business headquartered in Spain.2 Logista distributes tobacco — and increasingly a great deal else — to hundreds of thousands of retail outlets across Southern Europe. That is the boring part.

The interesting part is excise duty. In most European tobacco markets, the distributor collects the excise tax from retailers at the point of sale and remits it to the government later, on a fixed schedule. In between, that tax money — which belongs to the state, not the distributor — sits in the distributor's bank account. Because tobacco excise is an enormous fraction of the retail price, and because the volumes are vast and daily, this creates a permanent, rolling float of other people's money.

It is a structure familiar to anyone who has studied insurance. Logista, in effect, generates float — and instead of that float earning a modest return in a Spanish bank, it is loaned upward.

Through an intercompany cash pooling arrangement, Logista lends its surplus cash to Imperial Brands. The daily average cash balance loaned to the group has run at approximately £1.7 billion, and at March 31, 2026, the position stood at around £1.6 billion. The balance is volatile by design — swinging between roughly £2.6 billion and £0.5 billion across a twelve-month period, driven almost entirely by the timing of excise duty payments to governments.18

Why does this matter? Because it means a meaningful slice of Imperial's working capital is funded internally, at rates well below what the group would pay in the bond market, from a subsidiary whose minority shareholders own 49.99% of it. It lowers the group's effective cost of capital and enhances liquidity, which in turn supports the leverage the buyback depends on.

And here is where the neutral analyst has to raise a hand, because this is precisely the kind of structure an activist would put under a microscope. Imperial consolidates Logista, controls its board through a bare majority, and borrows its cash. Logista's minority holders own half of an entity whose treasury policy serves its parent's balance sheet. Imperial discloses the arrangement and the rates are subject to the usual related-party governance, and there is no public evidence of impropriety. But it is a related-party financing structure of real scale, dependent on Imperial retaining control of a listed subsidiary, and dependent on the excise-collection model in Southern Europe remaining exactly as it is. It is a genuine and durable advantage. It is not a risk-free one.

It is also not immune to the ordinary business cycle. In FY25, Logista's contribution was behind prior years — growth from tobacco price increases was offset by weakness in its long-distance transport operations.2 In the first half of FY26, Logista's adjusted operating profit declined, as reduced profit from tobacco inventory offset underlying growth.1 Logista is a real business with real cyclical exposure, not merely a treasury instrument.

The results

By FY25, the strategy had produced a genuinely consistent record. Over the five years of the plan, aggregate market share across the five priority markets improved by 48 basis points — a modest number that represents the reversal of a decade of decline. NGP net revenue grew 73%. Earnings per share rose by roughly a third. Cumulative free cash flow reached £11.6 billion, and £10 billion was returned to shareholders — equivalent to about two-thirds of Imperial's market capitalisation when the plan launched.2

The FY25 numbers themselves: adjusted operating profit of £3.988 billion, up 4.6% at constant currency, on tobacco and NGP net revenue of £8.316 billion.192 Set those two figures beside each other and the economics of this industry become vivid — Imperial converts something close to half of its net revenue into operating profit. Free cash flow was £2.7 billion on operating cash conversion of 97%; leverage finished at 2.0x, the bottom of the target range; the dividend rose 4.5% to 160.32p and adjusted EPS reached 315.0p, up 9.1%.218

But the number that explains the share price is elsewhere. Reported group revenue was £32.171 billion against net revenue of £8.316 billion.19 The £24 billion gap is excise duty and Logista's distribution turnover. Imperial is, in accounting terms, mostly a tax collector.

What does the evidence actually establish? That Bomhard did what he said he would do. Guidance was set and met, repeatedly, across five years. Share stabilised. NGP shrank to a size Imperial could afford and then grew. Debt came down and stayed down. That is a real record of execution, and it deserves credit precisely because the preceding decade offered so little of it.

What it does not establish is that Imperial has solved anything structural. Every one of those achievements is a defensive achievement. The company got better at managing decline. It did not find growth. And the man who inherited the chair would have to answer the question Bomhard never quite had to: what happens when the easy wins from fixing a broken company are gone?

VII. The Current Era: Lukas Paravicini, Murray McGowan, and the 2030 Strategy

The transition was announced on May 14, 2025, and it was as orderly as these things get. Stefan Bomhard told the board he wished to retire. Lukas Paravicini, chief financial officer since May 2021, would succeed him as CEO on October 1, 2025. Murray McGowan, the chief strategy and development officer, would become CFO the same day. Bomhard would remain on the board until December 31, 2025 and be available until May 2026 to support the transition.2021

Paravicini is a financial executive by formation — a former Nestlé man and previously CFO of Fonterra, the New Zealand dairy cooperative. McGowan joined Imperial around 2020 to run strategy and corporate development, and on the FY25 call he made a point of noting that he had personally led the development of both the January 2021 strategy and its March 2025 successor.2

Note what that means structurally. Imperial has promoted its CFO to CEO and its strategy chief to CFO. There is no outsider, no new lens, no fresh scepticism at the top. Both men authored the plan they are now executing and grading. For a business whose entire proposition is capital discipline and predictable cash return, this is arguably the ideal continuity. For a business that might one day need to admit its plan is not working, it is a governance structure with no natural dissenter. Both readings are legitimate.

Evolve 2030

The strategy was unveiled at a Capital Markets Day on March 26, 2025, and Imperial calls it "Evolve 2030."4 Paravicini describes it as "a confident evolution" rather than a break — which is accurate, and also the sort of phrase that requires interrogation, because evolution is what companies say when the strategy is not changing.

The financial architecture is precise and, to management's credit, unusually specific:

- Tobacco net revenue growth in the low single digits, NGP net revenue growth in double digits, at constant currency.

- Group adjusted operating profit growth of 3% to 5% over the strategic period.

- At least high single-digit adjusted EPS growth.

- Free cash flow of at least £2.2 billion, rising toward £3 billion by the end of the period.

- Leverage held at 2.0x to 2.5x adjusted net debt to EBITDA — and management has guided to the lower end.

- £320 million of annual cost savings by the end of the period.

- A progressive dividend, and an evergreen, always-on share buyback across the full five years.12

That last phrase is the one that matters, and it is a genuine change. Previous buybacks were announced annually and could quietly not be renewed. "Evergreen" is a commitment to a structural return of capital across a five-year horizon. McGowan reiterated it explicitly on the half-year call.1

The scale is remarkable. FY26's buyback of £1.45 billion — announced on October 7, 2025, up from £1.25 billion in FY25 and £1.1 billion in FY24 — is expected to complete no later than October 29, 2026.2[^3] In FY25 alone Imperial repurchased just over 5% of its share capital, bringing cumulative repurchases since the programme began in 2022 to 15.8%.2 By the half-year point of FY26, total buyback spend since inception reached £4.8 billion, and cumulative capital returns since FY21 hit £11.5 billion.1

Here is the honest way to describe what this is: a controlled, tax-efficient, self-funding liquidation of the equity. Imperial is buying itself out of existence, slowly, using its own cash flows, and paying shareholders to wait. That is not an insult — for a business in structural decline with no credible reinvestment opportunity, it is arguably the only rational capital allocation policy. Retaining that cash to chase a category Imperial cannot win would be worse. The 2015–2020 period is the evidence.

But it should be described accurately. Every buyback pound is a pound not invested in a future. Imperial's management is making a bet — a defensible one — that there is no future worth buying.

The transformation

The genuinely new element of Evolve 2030 is not strategy but plumbing, and it is where the near-term earnings support comes from.

Imperial is rationalising its manufacturing footprint. It announced the closure of its Langenhagen factory in Germany in October 2025, completed social plan negotiations with worker representatives, and is on track to cease production there in July 2027. In May 2026 it announced the sale of its Taiwan factory, to complete by summer 2027. Together, Paravicini said, these two actions will reduce overheads by £100 million. Manufacturing excellence programmes across the remaining plants deliver a further £25 million in FY26.1

More significant, and more revealing, is the Capgemini partnership: a long-term outsourcing arrangement under which around 400 roles transferred, alongside the continued rollout of SAP S/4HANA, Salesforce and Blue Yonder.1

Paravicini was disarmingly candid about why this is necessary. "Right now, it would be fair to say we are still playing catch-up with other consumer businesses, which started transformation years earlier," he told analysts in November 2025 — before offering an analogy about emerging economies that jumped straight from banknotes to mobile wallets, skipping the intermediate technology entirely.2

It is a good analogy and an uncomfortable admission. Imperial is a company "stitched together from many acquisitions over several decades" — his words — that in 2026 is still building the integrated technology backbone most consumer companies completed a decade ago.2 The leapfrog thesis is plausible. It is also exactly what every late adopter says. Note too that the transformation costs are being treated as adjusting items — disclosed clearly, but excluded from adjusted profit while the resulting savings will flow into it. That asymmetry is standard practice and entirely legal. It is also worth watching over a multi-year programme.

NGP today: real, growing, and small

In FY25, NGP delivered its fifth consecutive year of double-digit growth: net revenue of £368 million, up 13.7% at constant currency. Europe contributed £280 million (+8.8%), the Americas £70 million (+69.8%), and AAACE £18 million (down 30.8%). Adjusted NGP operating losses narrowed to £76 million from £79 million.19

The modern oral story is the one management most wants discussed. Zone launched in the US in 2024 and by the FY25 results had reached a 2.8% national share, available in 100,000 stores, with management targeting weighted distribution north of 85%.2 In Europe, Zone and the established Skruf brand lead the portfolio; Skruf is now the largest brand in Norway, and Zone launched in the UK on the day of the FY25 results, reaching 3% share in the independent channel within six months before rolling out to national accounts.12 In heated tobacco, the Pulze 3.0 device launched in the second half of FY25 alongside iSenzia herbal sticks. In vapour, the pod-based blu Kit range replaced the disposables that regulators across Europe have been banning.

Now the proportionality check, which management does not volunteer. £368 million of NGP net revenue sits inside £8.316 billion of tobacco and NGP net revenue. NGP is roughly 4% of the business. Growing it at 13.7% adds around £50 million of net revenue a year — against a combustible business that generates nearly £4 billion of operating profit. At this scale, NGP cannot absorb a shock in combustibles. It is not a hedge. It is an option, and a small one.

And the first half of FY26 exposed exactly how fragile the double-digit narrative is. NGP revenue growth came in below the double-digit guidance. Management attributed this to a single identifiable cause: a promotional campaign in the US over the prior year-end that worked better than expected and pulled revenue into the comparative period, costing roughly £13 million of NGP net revenue and widening losses by the same. Absent that, they said, group NGP growth would have been double digit and losses would have narrowed.1

That explanation is specific, quantified and plausible — which is the standard a good CFO should meet, and McGowan met it. But it is also the explanation of a business so small that one promotion in one country can break a group-level guidance metric. That is the actual lesson.

Then there is the decision management buried in the middle of the half-year presentation: Imperial has exited the US vapour category entirely.1 The myblu device, Paravicini said, is "a 10-year-old product... which probably does not meet the consumer needs of today, has been making a very limited contribution to the business and was loss-making."1

So ends the story that began this company's crisis. blu — the asset at the centre of the 2015 US acquisition, the engine that was supposed to power Imperial's transition, the product whose failure cost a chief executive her job — has been withdrawn from the market it was bought to conquer. Management framed the exit as a margin improvement, and in the narrow sense it is. In the wider sense, it is the formal closure of an eleven-year strategic failure, and it deserves to be named as such.

Pressed on when Imperial might re-enter, Paravicini was clear about the economics: the PMTA authorisation process remains "a lengthy, costly experience" and the US still has "a big illicit market."1 Which is a candid way of saying the legal US vape market is not currently worth the cost of entry — a judgement that may well be correct, and one that reveals how much of this industry's regulatory moat has already been breached.

VIII. Porter's Five Forces & Hamilton Helmer's Seven Powers Analysis

Strip away the narrative and ask the structural question: is this a good business, and is Imperial's position within it defensible?

Porter's Five Forces

Threat of new entrants — very low, and this is the industry's deepest moat. Not because manufacturing is hard; rolling a cigarette is trivial. Because marketing one is illegal. Advertising bans, plain packaging, display bans and the FDA's PMTA authorisation regime in the US mean that no new brand can be built. The regulations designed to destroy the tobacco industry have, in a magnificent irony, permanently protected the incumbents' existing brands from competition. Imperial's Winston and Gauloises cannot be challenged by a startup, because a startup cannot advertise.

But note the asymmetry Paravicini's own words expose: that moat protects combustibles. In NGP, the PMTA process is a barrier Imperial itself finds too expensive to cross — it just walked away from US vapour partly because of it. A moat that keeps you out is not your moat.

Bargaining power of suppliers — moderate, and misspecified. Leaf tobacco is a commodity, and Imperial's scale gives it purchasing leverage. The real supplier is the state. Excise duty determines the retail price, the affordability of the category, and therefore volume itself. Governments are a supplier with unlimited pricing power and no commercial incentive. Australia is the live demonstration: excise escalation there has been so aggressive that Imperial saw volumes decline around 50% in the first half of FY26.1 Germany, meanwhile, publishes a five-year tax plan — which McGowan explicitly described as making it "a very well-managed market."1 The difference between Germany and Australia is not consumer behaviour. It is tax policy.

Bargaining power of buyers — low, and asymmetric. Nicotine addiction produces price inelasticity that no ordinary consumer product enjoys. But the elasticity is not zero, and it does not express itself as quitting — it expresses itself as down-trading. And Imperial has just told the market that down-trading now costs it more than it used to, because the gross margin gap between the top and bottom of the price ladder has widened materially in the US, Germany and Spain.1 That is the buyer exercising power in the only way an addicted consumer can.

Threat of substitutes — high, and worse than the industry admits. The substitute is not IQOS or ZYN. It is the illicit, non-compliant disposable vape shipped from China, which pays no excise, undergoes no authorisation, and undercuts the legal product on price precisely because it bypasses the tax that constitutes the industry's moat. Imperial's own analysis attributes US volume declines primarily to illicit vape and macroeconomic pressure. When enforcement improved, Paravicini reported that industry volumes improved with it — "the enforcement, while not perfect... has made a dent."1 That is an important admission: a meaningful share of Imperial's recent volume performance depends on the enforcement priorities of a government agency, not on anything Imperial does.

Competitive rivalry — high in intensity, rational in conduct. Four large players who have all concluded that price increases beat market-share wars. This rationality is the industry's most valuable and least contractual asset. It is also visibly fraying at the bottom: Paravicini noted "growth in the deep discount segment and new brand launches" in the US, and Imperial responded by launching a new brand, Malibu, explicitly as a pricing lever — "another lever for us to balance the volume and value equation."1 Launching a fighter brand is what a rational oligopolist does when the discount end stops being rational.

Hamilton Helmer's Seven Powers

Of Helmer's seven, Imperial can credibly claim three — and the qualifications matter.

Scale Economies. Real, but regional rather than global. Imperial's manufacturing and its Logista distribution give it a unit-cost advantage over any small regional player. Against PMI and BAT, Imperial is the sub-scale one — which is exactly why it cannot fund a global NGP war. The £320 million savings programme is best read as an admission that Imperial's cost position was not as good as its scale should have delivered, because the company was assembled from acquisitions and never properly integrated.

Cornered Resource. The strongest claim here is regulatory: PMTA authorisations and grandfathered rights cannot be replicated by a new entrant at any price. Paravicini referenced Imperial's US pouch pipeline as resting on "grandfathered rights and opportunities in products with stronger strength and new flavors."1 This is a genuine cornered resource — a government-issued permission slip, unbuyable. But it is narrow, and the FDA can change enforcement priorities, as the industry was reminded when the agency signalled it might tolerate unauthorised pouch brands.1

Branding. Century-old brands with entrenched loyalty, protected by advertising bans. Real, and durable. But observe how Imperial actually monetises it: not through category-defining brand power like Marlboro, but through segment arbitrage — nurturing Davidoff and Winston at the premium end while pricing "responsibly" at the discount end. That is skilled portfolio management. It is not the same thing as pricing power.

Imperial has no Network Economies, no Switching Costs worth the name (a smoker changes brands for a few pence), no Counter-Positioning (it is the incumbent, and it is the late incumbent), and no Process Power — indeed the Capgemini partnership and the S/4HANA rollout are an explicit acknowledgement that its processes lag its peers'.

The structural verdict: Imperial operates in a genuinely excellent industry and occupies the weakest defensible position within it. Its returns come overwhelmingly from industry structure, not company-specific advantage. That is not fatal — a mediocre position in a superb industry beats a superb position in a terrible one, and the cash flows prove it. But it means Imperial's fortunes are governed by forces it does not control: excise policy, enforcement against illicit trade, and the continued rationality of three larger competitors.

Which is precisely why the company's answer has been to stop pretending it can control them, and to focus instead on the one thing it can.

IX. Playbook: Business & Investing Lessons

Don't copy the leader. The most important decision of Imperial's last decade was a decision not to do something. PMI has spent north of $10 billion building IQOS into a global heated-tobacco franchise. Imperial looked at that, assessed its own balance sheet and R&D capability, and declined. Instead it wrote down its doctrine: enter only where the category exists and a route to market already exists. Every pound not spent chasing PMI became a pound of buyback.

The generalisable lesson is that a challenger's edge is choice, not effort. Imperial's five-market focus and its fast-follower NGP posture are the same decision applied twice: narrow the front, concede the rest, compound what remains. The corollary, which Imperial's own history teaches, is that this only works if you are honest about being the challenger. The 2015–2019 period failed because Imperial tried to be a leader in vaping with a challenger's resources. The turnaround worked because it stopped.

But state the risk plainly: fast-following is a strategy that requires someone to be worth following. It works in nicotine pouches, where PMI created the category and Imperial arrived with Zone. It fails if the next category shift is one Imperial cannot buy its way into — and Imperial's own US vape exit is the proof of concept for that failure mode.

Boring assets are worth more than glamorous ones. The Altadis deal is a natural experiment. Imperial bought Cuban cigars — the most romantic asset in the industry — and a Spanish trucking-and-distribution company. It sold the cigars for €1.225 billion to pay down debt.15 It kept the trucking company, which now lends it roughly £1.7 billion a day at below-market rates.18 Fifteen years on, the boring asset is the one creating value.

The lesson generalises to treasury structure. Owning a majority of a listed, cash-rich subsidiary that sits atop a regulated float is an extraordinary financing tool. Investors screening for "conglomerate discount" or "portfolio complexity" would mark Imperial down for owning 50.01% of a listed distributor. They would be missing the point — though not entirely, because the structure's dependence on control and on Southern European excise mechanics is a genuine concentration.

M&A discipline is mostly about timing and financing, not logic. Altadis was strategically defensible and financially near-catastrophic: an all-debt acquisition completed weeks before the financial crisis, concentrated in a market about to implode. Reemtsma, six years earlier, was the same logic executed at a sane price and remains the foundation of Imperial's best market. The difference was not the quality of the thinking. It was the price paid and the cushion retained.

The 2015 carve-out adds a subtler lesson: regulatory divestitures are a real source of assets for disciplined buyers, but you are buying what a regulator forced someone to sell, not what a seller chose to offer — and the liabilities may be longer-dated than the diligence. Ten years later, the Delaware judgment was still generating cash outflows.10

Divestment is a skill, not a defeat. Selling Habanos was painful, unglamorous and correct. The corollary is uncomfortable for management: the willingness to sell good assets to fix the balance sheet is admirable, but it was only necessary because of the balance sheet decisions of 2008. Pragmatism in year fifteen is atonement for ambition in year one.

And the meta-lesson: Imperial's turnaround was not a growth story. It was a credibility story. Bomhard's achievement was setting modest targets and hitting them, repeatedly, for five years, after a decade in which the company set ambitious targets and missed them. In a mature industry, the multiple is paid for predictability. Imperial rebuilt its multiple by becoming boring on purpose.

Which raises the question every investor now has to answer.

X. Analysis: Bear vs. Bull Case & Core KPIs

The bull case

The arithmetic of the total return. This is the whole argument, and it is not a weak one. FY26 capital returns exceed £2.7 billion — dividend plus a £1.45 billion buyback — which management calculates at around 11% of market capitalisation.2 The buyback retires roughly 5.7% of the share count annually.[^3] Even with zero organic growth, shrinking the denominator at that pace produces mid-to-high single-digit EPS growth mechanically. Add 3–5% operating profit growth and you reach the "at least high single-digit EPS growth" management guides to, which is exactly what FY25 delivered at 9.1%.2

The bull case does not require you to believe the tobacco industry has a future. It requires you to believe it has a decade. Over a decade, at these return rates, the maths does the work.

Pricing power is empirically demonstrated, not asserted. This is where the evidence is genuinely strong. In FY25, price/mix of 5.4% more than offset a 1.7% volume decline, delivering 3.7% tobacco net revenue growth.192 US price/mix ran at 9.9%.2 In the first half of FY26, European pricing of 6% and US pricing of 5.7% again outpaced volumes, with AAACE excluding Australia at 6.1%.1 Volumes fell just 1.5% at the half-year — well inside the 3–5% long-run assumption. And crucially, Paravicini frames better volumes as good news for a reason worth understanding: "to get to our target net revenue of 1% to 2%, we need to price less, and that is always helpful for the consumer."1 Less price-taking means less down-trading pressure. The flywheel works in both directions.

Cash conversion is exceptional and consistent. Operating cash conversion of 97% in FY25 and 98% on a rolling twelve-month basis at the half-year.21 For a business with negligible growth capex, this is close to the theoretical maximum. The cash is real.

Management alignment has genuine teeth in one specific respect. The LTIP weights EPS growth, return on capital, free cash flow and TSR at 90%, with ESG measures at 10%. Most importantly, the EPS targets exclude the benefit of the share buyback, in line with Investment Association guidance.22 That detail matters more than it sounds. A management team paid on EPS while buying back 5% of the shares annually could hit its targets by doing nothing at all. Excluding the buyback from the EPS calculation removes precisely that loophole. This is good governance, and it should be credited.

The bear case — the activist stress test

The volume cliff. The entire model rests on price increases outrunning volume declines. That equation holds until it does not, and it is non-linear: as prices rise, affordability falls, illicit trade becomes more attractive, and volume declines accelerate — which requires more price, which accelerates the declines further. There is a point at which the flywheel reverses.

Imperial does not have to speculate about this. It has a live case study in its own portfolio. Australian volumes fell around 50% in the first half of FY26.1 That is not a decline; that is a market breaking, driven by excise escalation and the illicit trade it created. Management's response was to note that Australia is "less than 2% of our net revenue" and to resize the operation.1 Fair enough — but Australia is not an anomaly. It is a preview. The UK is on the same trajectory, which is why both are explicitly managed for value rather than share.

The illicit vape threat bypasses the moat entirely. The regulatory barrier that protects Imperial from legal competitors offers no protection at all against a product that ignores regulation. Illicit disposables pay no excise, which is the single largest component of the legal product's price. This is not a substitute competing on brand; it is a competitor with a structural 60–70% cost advantage created by tax evasion. Imperial's own commentary attributes a material portion of US volume movement to illicit vape and to enforcement against it.1 An investment case partly dependent on the vigour of customs enforcement is a fragile one.

The share number, and what changed. This is the sharpest question for the current management team, and it goes to narrative consistency. In November 2025, Paravicini told analysts: "The goal is stable market share. That's what is in our model." He described Imperial's demonstrated "capability, that agility to balance off well market share and pricing" and said he was confident Imperial could "still generate very much value out of our combustible business without losing share."2

Six months later, aggregate priority-market share was down 60 basis points, and the framing had shifted to "not all basis points of market share are equal" and a "more focused segment-by-segment approach."1

Now — is that a strategy evolution or a retrofit? The steelman for management is genuine: the gross margin spread between premium and discount really has widened, they showed the data, and harvesting share in structurally broken markets like the UK and Australia is defensible. Paravicini pre-committed to the principle at the March 2025 Capital Markets Day, saying share losses of this kind would be "consistent with running the business for sustainable value creation."1 It is internally coherent.

The bear reading is equally available: a company that spent five years making "we are no longer the share donor" its central proof point has quietly redefined the proof point in the first period where it stopped being true. When analysts pushed — twice, including a direct request for value-share data — management declined, saying value share is "more difficult to calculate" and "we don't have the means and the data to do that."1 That is a problematic answer. If the company is asking investors to accept volume-share losses on the grounds that value share is what matters, it cannot simultaneously say it cannot measure value share. The metric has been reframed toward something management does not disclose. That is exactly the kind of thing a skeptical investor should mark, and it is the single most important thing to watch over the next two reporting periods.

NGP cannot absorb the shock. At roughly 4% of net revenue and still loss-making, NGP is not a hedge against combustible decline in any meaningful sense.19 Imperial has no ZYN and no IQOS, and by its own doctrine it will never build one. Zone at 2.8% US share is a creditable start in a category where, as Paravicini noted, "the industry is investing significantly to grow the category... volume will grow well ahead of value."1 Translation: Imperial is a minor participant in a category whose leaders are subsidising growth, and it has chosen not to match them. That may protect margins. It will not build scale quickly.

The buyback is a symptom, not a strategy. An activist would frame it this way: Imperial returns three-quarters of its market cap in five years because it has nothing else to do with the money. The buyback flatters EPS, supports the shares, and consumes the capital that a genuine strategic alternative would require. And it is levered — leverage sat at 2.4x at the half-year, at the upper portion of the target range, while management guided to finishing near the lower end.1 The buyback is funded partly by debt against declining cash flows. That works while the cash flows decline gently. It compounds against you if they do not.

Risks worth naming, briefly. Excise policy is the dominant one — Germany's next five-year tax plan was under negotiation at the half-year, with McGowan expecting any impact from FY27 onward.1 The EU's revised Tobacco Products Directive is in progress and could reshape flavour rules for modern oral. The Middle East crisis, live since roughly February 2026, had not materially affected results as of May 2026, but management flagged input costs, duty-free volumes and consumer sentiment as transmission channels — and was candid that the consumer impact "is the unknown."1 Imperial has also been sued in the US over a nicotine pouch transaction, a reminder that its US pouch supply chain depends on contract manufacturing relationships rather than owned capability.23

The three KPIs that matter

Everything above reduces to three numbers. Not more.

1. Aggregate market share across the five priority markets. This is the load-bearing metric of the entire equity story, and it is now contested. It improved 48 basis points over the five years to FY25; it fell 60 basis points in the first half of FY26.21 Management says the decline is deliberate. The way to test that claim is not to accept the framing but to watch whether tobacco net revenue and operating profit growth hold up while share falls. If share declines and profit growth stays inside the 3–5% range, management was telling the truth about value over volume. If share declines and profit growth decays with it, the reframing was a rationalisation. Two or three reporting periods will settle it.

2. NGP net revenue growth. Management guides to double digits. The first half of FY26 missed, with a specific and quantified excuse.1 Watch whether the second half recovers as promised — this is a direct, near-term, falsifiable test of management's guidance discipline, and it arrives at the FY26 results. Sustained double-digit growth validates the fast-follower thesis. Persistent misses with fresh one-off explanations each time would say the transition story is not real.

3. Adjusted net debt to EBITDA. Target 2.0x to 2.5x, with a stated intention to sit near the lower end. It closed FY25 at 2.0x and stood at 2.4x at the half-year on seasonal grounds.21 This is the constraint on everything else. The buyback, the progressive dividend and the investment-grade rating all live inside this ratio. If leverage drifts up while the buyback continues, the company is borrowing to retire equity in a declining business — and that is the moment the bull case and the bear case stop being a matter of interpretation.

XI. Epilogue & Outro

Return, finally, to the 1902 treaty — because Imperial Brands has been the same company for 124 years.

In 1902, facing an opponent it could not beat, Imperial made a clear-eyed, unsentimental calculation: concede the world, keep the profitable core, take the cash. Every subsequent chapter is a variation. Hanson stripped it to its cash-generating essence and made it better. The 2008–2015 acquisition spree was the one era when Imperial forgot the lesson and tried to be something larger than it was, and it cost a decade. The vaping catastrophe was the same error in a different medium — a challenger trying to lead. And the turnaround since 2021 has been, at its heart, the company remembering what it is.

Imperial Brands does not seek to change the world. It does not claim it will win the next-generation technology crown; under Paravicini it has stated, in as many words, that it will enter only categories other people have already built. It seeks to capture, defend and efficiently distribute the cash flows of an enduring legacy industry — and then hand most of them back.

Whether that is triumph or slow surrender is not a question the financial statements can answer. Both descriptions are consistent with £2.6 billion of annual free cash flow and £11.5 billion returned since 2021. The difference between them lies entirely in a variable no one can yet observe: how long the decline stays gentle.

What can be watched is more modest, and more useful. The share number in the five priority markets is now the live test of management's credibility, because the story attached to it changed the moment it went the wrong way. The NGP growth rate is the near-term test of guidance discipline. And leverage is the constraint that governs whether the buyback is a return of surplus or a leveraged retirement of equity in a shrinking business.

The next chapter turns on execution rather than vision — the transformation programme's £320 million of savings, the Langenhagen and Taiwan closures landing in 2027, the Capgemini partnership delivering more than headcount reduction, and above all whether Zone can build durable scale in a US pouch market where the category leaders are spending to grow and Imperial has explicitly chosen not to match them.

Paravicini closed the May presentation by asking analysts to take away three things: that Imperial performed in the first half, that it would deliver its full-year guidance, and that it is transforming for tomorrow.1 The first is largely demonstrated. The second is testable in November. The third is the one that will take until 2030 to judge — and it is the only one that determines whether this is a company with a future or simply an exceptionally well-managed way to convert an ending into cash.

References

-

Imperial Brands Half Year Results 2026 — results presentation and analyst Q&A, six months ended 31 March 2026 — Imperial Brands, 2026-05-12 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Imperial Brands Full Year Results 2025 — results presentation and analyst Q&A, year ended 30 September 2025 — Imperial Brands, 2025-11-18 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

The Anglo-American Tobacco War of 1901-1902: A Clash of Business Cultures and Strategies — The Business History Conference ↩↩↩↩

-

Imperial Brands Capital Markets Day presentation — Imperial Brands, 2025-03-26 ↩↩

-

Imperial Tobacco Group PLC — Form 6-K, completion of the acquisition of Altadis — U.S. Securities and Exchange Commission, 2008 ↩

-

Imperial's 'Big' Jump to No. 3 in U.S. — CSP Daily News, 2015 ↩

-

ITG Owes Reynolds American $251.5 Million for Florida Tobacco Settlement, Judge Rules — U.S. News/Reuters, 2025-03-03 ↩

-

Imperial Brands: Trading Update — H1 2026 (Delaware settlement payment schedule) — Tobacco Insider, 2026 ↩↩↩

-

Imperial Brands PLC — Report for the six months ended 31 March 2026 — Imperial Brands, 2026-05-12 ↩

-

Imperial Brands CEO Alison Cooper to step down amid vaping backlash — The Globe and Mail/Reuters, 2019-10-03 ↩↩

-

Sale of Worldwide Premium Cigar Business — Imperial Brands, 2020-04-27 ↩

-

Update on sale of its Worldwide Premium Cigar Businesses — Imperial Brands, 2020-10-29 ↩↩↩↩

-

Cigar News: Sale of Premium Cigar Business of Imperial Brands Completed — Cigar Coop, 2020-10-29 ↩

-

Imperial Brands Appoints Inchcape's Stefan Bomhard As CEO — Nasdaq/RTTNews, 2020-02-03 ↩

-

Imperial Brands Annual Report and Accounts 2025 — intercompany cash pooling arrangement with Logista — Imperial Brands, 2025 ↩↩↩

-

Imperial Brands FY25 Results: NGP Net Revenue Up 13.7%, Americas Surges Nearly 70% — 2Firsts, 2025-11-18 ↩↩↩↩↩

-

Stefan Bomhard to retire as Chief Executive Officer of Imperial Brands — Imperial Brands, 2025-05-14 ↩

-

Imperial Brands PLC — Directorate Change — Investegate, 2025-05-14 ↩

-

Imperial Brands PLC — LTIP Performance Measures and Targets — Investegate, 2025 ↩

-

Imperial Brands Sued in US Over Nicotine Pouch Transaction — Bloomberg Law ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube