Medios AG: The Platform for Personalized Medicine

I. Introduction: The Specialty Thesis

Picture a hospital pharmacy in Berlin on a Tuesday morning. A pharmacist in a sterile gown stands inside a Grade A cleanroom — the most stringent controlled environment in pharmaceutical manufacturing, where the air contains fewer than 3,520 particles per cubic meter. She is preparing an intravenous infusion bag for a fifty-seven-year-old lung cancer patient who has an appointment at an oncology practice across the city in four hours. The bag must contain a precise dose of a chemotherapy agent calculated for this specific patient's body weight, kidney function, and treatment protocol. The drug costs roughly twenty thousand euros per dose. If the preparation is contaminated, the patient could die of infection rather than cancer. If the dose is wrong, the treatment either fails or causes catastrophic toxicity.

This is not mass-market pharmaceuticals. This is not aspirin. This is specialty pharma — the fastest-growing and highest-complexity segment of the global drug market. Oncology, neurology, autoimmune diseases, hemophilia, ophthalmology. The drugs involved are typically biologics — large-molecule proteins manufactured in living cells rather than synthesized from chemical compounds.

They require cold-chain logistics, meaning unbroken temperature-controlled storage and transport from factory to patient. A temperature excursion of even a few degrees for a few hours can render a twenty-thousand-euro drug worthless — or worse, dangerous. They often require patient-specific compounding — the preparation of an individualized dose in a sterile cleanroom by a trained pharmacist. And they are staggeringly expensive.

The economics of specialty pharma are unlike anything else in healthcare. A single dose of a checkpoint inhibitor like pembrolizumab can cost EUR 8,000 to EUR 12,000. A course of treatment for a rare blood disorder might run into hundreds of thousands of euros per year. These are not drugs that sit on shelves waiting to be dispensed. They are manufactured to order, prepared to specification, and delivered under conditions that would satisfy the quality control department of a semiconductor fabrication plant.

In Germany, the largest pharmaceutical market in Europe at roughly $96 billion as of 2024, specialty drugs now represent the fastest-growing segment. Cancer therapeutics alone accounted for more than 18 percent of total pharmaceutical revenue in 2024. Oncology spending grew 17 percent in 2023. Immunology grew 9 percent.

The structural tailwind is enormous and accelerating, driven by the shift toward precision medicine, new biologic therapies, checkpoint inhibitors, and gene therapies that require increasingly sophisticated handling, preparation, and delivery. Every new biologic approval — and the FDA and EMA are approving them at an accelerating pace — adds another drug that requires the kind of infrastructure most pharmacies simply do not have.

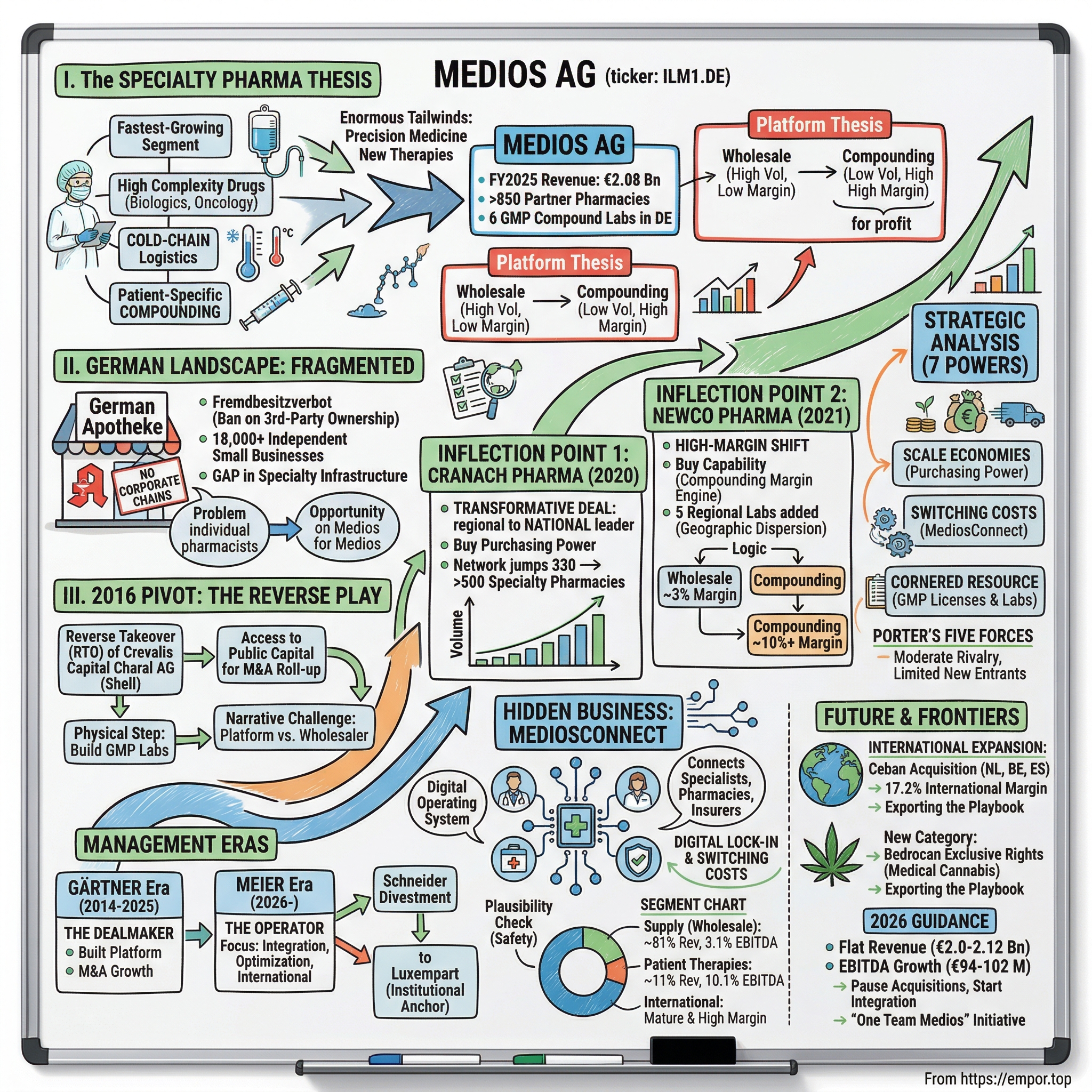

Medios AG, trading on the Frankfurt Stock Exchange under the ticker ILM1.DE at approximately EUR 13 per share, has built the infrastructure platform that makes this entire system work — at least in Germany, and increasingly across Europe.

The company generated EUR 2.08 billion in revenue in 2025, the first time it crossed the two-billion threshold, up from just EUR 133 million in 2016. That is a fifteen-fold increase in nine years — the kind of growth trajectory that in a technology company would attract breathless coverage from venture capital blogs, but in the staid world of German pharmaceutical distribution barely registers on the radar of mainstream financial media.

Medios operates approximately 850 partner pharmacies, six GMP-certified compounding laboratories in Germany, and — following a transformative acquisition — additional compounding facilities in the Netherlands, Belgium, and Spain. It is the largest specialty pharmaceutical platform in Germany and one of the largest in Europe.

The market capitalization is roughly EUR 321 million — meaning the market is valuing this business at roughly 0.15 times revenue. That ratio, which would be alarming for a tech company, makes more sense when you understand that Medios operates two fundamentally different businesses under one roof: a high-volume, thin-margin pharmaceutical wholesale operation, and a lower-volume, high-margin patient-specific compounding operation.

The wholesale business generates 81 percent of revenue at roughly 3 percent margins. The compounding business generates the remainder at margins between 10 and 17 percent. One is the engine that generates volume and purchasing power. The other is the engine that generates profit.

Understanding the interplay between these two engines — how volume feeds margin, how scale creates purchasing power, and how digital integration creates lock-in — is the key to understanding whether Medios is a commodity distributor or an irreplaceable infrastructure platform. Get this wrong and you see a low-margin wholesaler trading at a fair valuation. Get it right and you see a healthcare infrastructure monopoly hiding behind modest headline margins.

But before we can understand the platform, we need to understand the market it serves. And the story begins not with drugs or cleanrooms but with a peculiarity of German law that has no equivalent in the United States, the United Kingdom, or most other major pharmaceutical markets. It is a law that has shaped the entire structure of German healthcare, created one of the most fragmented pharmaceutical markets on earth, and — paradoxically — made Medios's existence both necessary and possible.

II. The Fragmented German Landscape

Walk into any pharmacy in Houston, Texas, and there is a reasonable chance it is owned by CVS Health, a corporation with three hundred thousand employees and $357 billion in annual revenue. Walk into a pharmacy in London and it may well be a Boots outlet, part of the Walgreens Boots Alliance empire.

Walk into a pharmacy in Berlin, and you will find something fundamentally different: a small, independently owned business run by a licensed pharmacist whose name is on the door. The shelves look similar. The products look similar. But the ownership structure — and everything that flows from it — is entirely different.

This is not an accident. It is the law.

The German Apothekengesetz — the Pharmacy Act — contains a provision called the Fremdbesitzverbot that has no parallel in most Western economies: the prohibition of third-party ownership of pharmacies.

Only a licensed pharmacist may own and operate a pharmacy in Germany. Corporations cannot own pharmacies. Private equity firms cannot own pharmacies. Hospital chains cannot own pharmacies. A single pharmacist may operate a maximum of one main pharmacy and up to three branch pharmacies — four locations in total. That is the ceiling.

The European Court of Justice upheld this ban in a landmark ruling on May 19, 2009, confirming that it served a legitimate public interest in consumer protection. The court reasoned that the personal liability of a self-employed pharmacist — whose professional reputation and legal exposure are directly tied to the quality of care provided — creates stronger incentives for patient safety than the profit-maximization imperatives of corporate ownership.

The ruling was not close. It was a clear affirmation of the German model, and it effectively ended the legal debate about whether EU single-market principles would force Germany to allow corporate pharmacy chains. They would not.

The result is a pharmaceutical market that is structurally, legally, and permanently fragmented. There are approximately 18,000 pharmacies in Germany, each an independent small business. There are no German equivalents of CVS, Walgreens, or Boots. There never will be, barring a fundamental change in law that has survived multiple legal challenges and decades of political debate.

To an American observer, this looks like an absurd anachronism — a market frozen in a pre-industrial structure by paternalistic regulation. But to a strategist looking for market inefficiencies to exploit, it looks like something else entirely: an opportunity. Because fragmentation in the pharmacy layer creates a vacuum in the infrastructure layer. If no corporation can own a thousand pharmacies and achieve scale through vertical integration, then the company that builds the horizontal infrastructure layer — the supply chain, the compounding capabilities, the digital integration — that connects a thousand independent pharmacies achieves the same economic result through a different legal structure.

For most categories of pharmaceuticals — the standard medications dispensed millions of times per day across the country — this fragmentation is merely an inefficiency. A headache tablet is a headache tablet, and an independent pharmacy can order it from any wholesaler. The three major German pharmaceutical wholesalers — PHOENIX Pharma, NOWEDA, and Alliance Healthcare — have built efficient distribution networks that serve independent pharmacies at commodity margins. The system works well enough for routine medications.

But for specialty pharmaceuticals — the biologics, the chemotherapy agents, the immunotherapies that require cold-chain handling, cleanroom preparation, and patient-specific dosing — the fragmentation creates a crisis.

An independent pharmacy serving fifteen oncology patients cannot justify the capital investment to build a GMP-certified cleanroom, which costs millions of euros and requires years of regulatory approval. It cannot negotiate meaningful volume discounts with Roche or Bristol Myers Squibb on drugs where list prices run into tens of thousands of euros per dose. It cannot maintain the specialized cold-chain logistics infrastructure required to handle temperature-sensitive biologics. It cannot hire and retain the specialized compounding pharmacists whose skills command premium salaries. It cannot invest in the quality management systems, the environmental monitoring equipment, the validated cleaning protocols, and the continuous training programs that GMP compliance demands.

The individual pharmacist is caught in a structural trap. The drugs her patients need are becoming more complex, more expensive, and more demanding of infrastructure that she cannot afford. The regulatory environment prevents any corporation from stepping in to provide that infrastructure through ownership. The pharmacist cannot scale. She cannot consolidate. She cannot invest.

This is the gap that Manfred Schneider saw.

Schneider was a pharmacist who came to Berlin in 1985 to study pharmacy and founded the BerlinApotheke am Oranienburger Tor in 1994. It was a single neighborhood pharmacy in the Mitte district of Berlin — the kind of small, owner-operated business that the Apothekengesetz was designed to protect.

He specialized first in HIV care during the epidemic years, when Berlin was one of the hardest-hit cities in Europe and specialty pharmacists were among the few healthcare providers who understood the complex antiretroviral regimens that were keeping patients alive. That experience — working with expensive, complex drugs that required careful handling and patient-specific dosing — was formative. It taught Schneider that the future of pharmacy was not in dispensing aspirin but in managing the logistics of precision medicine.

He moved into oncology as the treatment landscape evolved. From 2012, his pharmacy participated in cytostatic tenders from AOK Nordost, one of the major German health insurance organizations — meaning he was preparing and dispensing chemotherapy drugs for insured cancer patients. He was doing, at a small scale, exactly what Medios would later do at a national scale: bridging the gap between pharmaceutical manufacturers and the patients who needed their drugs.

What Schneider realized, through years of hands-on experience, was that the bottleneck in specialty pharma was not the drug itself. The pharmaceutical manufacturers could produce the drugs. The oncologists could prescribe them. The insurance companies could pay for them.

The bottleneck was everything in between: the supply chain that got the right drug to the right pharmacy at the right temperature, and the cleanroom preparation that turned a bulk drug into a patient-specific infusion bag, delivered to the oncology practice within a four-hour window. It was logistics. It was infrastructure. It was the unsexy, invisible plumbing of the healthcare system that nobody thinks about until it fails — and when it fails, a cancer patient does not receive treatment on time.

The bottleneck was infrastructure. And infrastructure, unlike drugs, could be built, scaled, and consolidated — even in a market where the pharmacies themselves could never be consolidated. This insight — that you could build the economic equivalent of a pharmacy chain without violating the law against pharmacy chains — was the founding thesis of Medios.

III. The 2016 Pivot: The Reverse Play

The path from insight to action took Schneider two decades.

In 2016, he and his team engineered the kind of corporate maneuver that would be more at home in the world of Silicon Valley SPACs than in the staid corridors of German pharmacy regulation.

They executed a reverse takeover of Crevalis Capital AG, a dormant listed shell company that had been trading at roughly EUR 0.50 per share. Crevalis had no real operations — it was a corporate shell, the kind of entity that exists on paper and on a stock exchange listing but does nothing. Through a capital increase via contribution in kind, Medios Manufaktur GmbH and Medios Pharma GmbH were folded into the listed entity, which was subsequently renamed Medios AG.

The stock began trading actively in late November 2016 at approximately EUR 7.50 per share. It was an unconventional path to the public markets for a pharmaceutical services company, but it served a very specific strategic purpose: access to capital for the M&A roll-up strategy that would define the company's trajectory over the next decade.

A reverse takeover — often abbreviated as RTO — works like this. You find a publicly listed company that has a stock exchange listing but no real operations. It is a shell. You merge your private operating company into the shell, issue new shares to the private company's owners, and — presto — the private company is now public without ever having gone through the time-consuming and expensive process of a traditional initial public offering. It is the corporate finance equivalent of a shortcut through a building rather than walking around the block. The destination is the same, but you arrive faster and cheaper.

The decision to go public so early — when the company had just EUR 133 million in revenue and was barely breaking even — reflected a calculated bet. Schneider understood that in a fragmented market with structural barriers to organic consolidation, the only path to scale was acquisition. And acquisitions required capital. Private debt markets would not fund an aggressive roll-up by a small Berlin pharmacy operation with thin margins. Equity capital from public markets would.

There was also a currency argument. A publicly listed company has something a private company does not: liquid shares that can be used as acquisition currency. Instead of paying cash for every deal — cash that the company did not have — Medios could offer its own shares to sellers, allowing them to participate in the upside of the combined entity. This is precisely what happened in the Cranach acquisition four years later.

The initial challenge was narrative. Medios was, at its founding, primarily a pharmaceutical wholesaler — a company that bought drugs from manufacturers and sold them to pharmacies, earning a thin margin on the spread.

Pharmaceutical wholesale is one of the lowest-margin businesses in the healthcare value chain. Gross margins in the low single digits. Net margins often below 1 percent. It is a volume game with commodity economics, and the market knew it. The big generalist wholesalers — PHOENIX, NOWEDA, Alliance Healthcare — had been doing this for decades, and their scale dwarfed anything Medios could offer. Competing on price in commodity wholesale against established players with vastly greater purchasing power would have been a suicide mission.

The task was to convince investors that Medios was not "just a wholesaler" but a platform for specialized care — a company that combined wholesale distribution with value-added services like GMP compounding, cold-chain logistics, and digital connectivity. The platform thesis required building capabilities that pure wholesalers did not possess and that independent pharmacies could not replicate on their own.

This is a narrative challenge that every infrastructure company faces. Amazon was "just a bookstore" until it was not. Visa is "just a payment network" that happens to be one of the most valuable companies on earth. The difference between a commodity intermediary and an essential infrastructure platform is often not visible in the business model — it is visible in the switching costs, the network density, and the barriers to replication. Medios needed to build all three.

The first step was physical: setting up the GMP laboratories. A Good Manufacturing Practice certification for pharmaceutical compounding in Germany is not a form you fill out and mail in. It requires cleanroom facilities built to exacting specifications — air filtration systems that maintain particle counts below defined thresholds, temperature and humidity controls, validated sterilization processes, comprehensive quality management systems, and trained personnel who follow standard operating procedures for every step of the manufacturing process.

Think of a GMP cleanroom as the pharmaceutical equivalent of a chip fabrication facility. The air is cleaner than a hospital operating room. Every surface is validated. Every process is documented. Every deviation triggers an investigation.

The requirements are exhaustive. Air must be filtered through HEPA systems that remove 99.97 percent of particles. Personnel must gown up in sterile suits, masks, and gloves before entering. All equipment must be validated — meaning tested and documented to prove it performs consistently within specified parameters. Raw materials must be tested upon receipt. Finished products must be tested before release. Every step of every process must be recorded in a batch record that regulators can audit at any time.

Getting certified takes years. Maintaining certification requires ongoing surveillance audits by regulatory authorities who arrive unannounced. The capital investment is measured in millions of euros.

By 2018, Medios had built its initial compounding capabilities and was generating EUR 328 million in revenue — more than doubling from two years earlier. The growth was impressive in percentage terms, but the absolute numbers told a different story. EUR 328 million in a market measured in the tens of billions was a rounding error. The company was growing, but it was still a small player in a vast market, operating primarily in the Berlin region with a limited partner pharmacy network.

The organic growth path — adding one pharmacy at a time, building one cleanroom at a time — would take decades to reach meaningful scale. The M&A path could get there in years. Schneider and the management team chose the latter. The next chapter would require a fundamentally different scale of ambition — and a fundamentally different amount of capital.

IV. Inflection Point One: The Cranach Pharma Acquisition

It was late 2020 — the second year of the COVID-19 pandemic — and most of the healthcare sector was focused on ventilators, vaccines, and ICU capacity. Cancer had not gone away, of course. Oncology patients still needed their chemotherapy, their immunotherapy, their targeted biologic infusions. But the attention of the world was elsewhere.

There is a recurring pattern in business history: the best acquisitions happen when the rest of the market is distracted. Warren Buffett's famous advice to be greedy when others are fearful applies not just to stock prices but to corporate transactions. During a pandemic, sellers become more motivated, financing markets are accommodative, and the attention of potential competing bidders is focused elsewhere. The window of opportunity is narrow and easily missed.

Matthias Gärtner, who had been guiding Medios's strategy since 2014 and was now serving as CEO, saw an opportunity to make the deal that would transform the company from a regional Berlin operation into the undisputed German market leader in specialty pharma distribution.

On November 26, 2020, Medios announced the acquisition of Cranach Pharma GmbH.

The deal was valued at approximately EUR 120.8 million, financed primarily through the issuance of 4,180,000 new Medios shares — representing roughly 20.6 percent of the post-transaction share capital — plus approximately EUR 30 million in working capital funding. The structure was elegant. By paying primarily in shares rather than cash, Medios preserved its balance sheet while giving the Cranach sellers a stake in the combined entity's future success.

The shares were subject to staggered lock-up periods of up to 24 months, aligning the seller's interests with post-merger performance. If the integration went poorly and the stock declined, the sellers would suffer alongside existing shareholders. If it went well, everyone would benefit. This alignment of incentives is a hallmark of well-structured acquisitions.

The German Federal Cartel Office approved the deal, and it closed on January 21, 2021.

The numbers tell part of the story. Cranach had generated approximately EUR 503 million in revenue in 2019, with EBITDA of roughly EUR 16.3 million. Medios was paying roughly 7 to 8 times EBITDA for a specialty pharmaceutical wholesaler — a premium to what you would pay for a generic wholesale business, but one that the strategic logic justified.

In pharmaceutical distribution, where deals typically transact at 5 to 7 times EBITDA, the premium reflected the specialty nature of Cranach's business. This was not a generic pill distributor. This was a specialty pharmaceutical platform with deep relationships in high-value therapeutic areas and a partner pharmacy network that could not be easily replicated.

What made the deal transformative was not the revenue or the EBITDA. It was the partner pharmacy network.

Before Cranach, Medios worked with approximately 330 specialized pharmacies. After Cranach, that number jumped to over 500. Think about what that means in the context of a market with 18,000 total pharmacies. Five hundred specialty pharmacies is not a majority of the market — but specialty pharmacies are a small fraction of the total, and within that fraction, Medios had suddenly captured a commanding share.

The expansion was not just quantitative — it was geographic. Cranach's network covered therapeutic areas that complemented Medios's existing strengths: neurology, hemophilia, endocrinology, ophthalmology, and rheumatology, in addition to oncology. Where Medios had been a Berlin-centric oncology specialist, the combined company was a nationwide multi-therapeutic-area platform.

The aggregation of demand changed the power dynamics with pharmaceutical manufacturers in a way that was disproportionate to the deal's headline price. When a company representing 330 pharmacies calls Roche or Bristol Myers Squibb to negotiate pricing, it is a customer. When a company representing 500-plus pharmacies calls — representing a meaningful share of the entire German specialty pharmacy market — it is a partner whose call gets returned immediately. Volume discounts, rebate structures, and preferred supply arrangements become available at scale thresholds that individual pharmacies or small networks simply cannot reach.

The Cranach acquisition was, in essence, buying purchasing power. The lower cost of goods sold that came from aggregated demand would flow through the income statement for years, improving margins on every prescription filled through the expanded network.

There is a subtlety here that is easy to miss. In most industries, buying a competitor gives you their revenue and their customers. In pharmaceutical distribution, buying a competitor gives you something more valuable: their volume. And volume, in a market where pricing is a function of aggregate purchasing power, translates directly into margin improvement across the entire existing business — not just the acquired business. Every existing Medios partner pharmacy benefited from the Cranach deal because the combined company could negotiate better pricing with manufacturers than either company could separately.

The impact on the financial trajectory was immediate and dramatic. In 2020, the year before Cranach was fully consolidated, Medios generated EUR 627 million in revenue. In 2021, the first full year with Cranach, revenue more than doubled to EUR 1.36 billion.

Pause on that number for a moment. The company had crossed the billion-euro threshold in a single acquisition — vaulting from a mid-size specialty player to a genuine platform. Revenue had grown tenfold in five years, from EUR 133 million at the time of the 2016 listing to EUR 1.36 billion in 2021. This was not the kind of organic, quarter-by-quarter growth that analysts model with spreadsheets. This was punctuated equilibrium — long periods of steady growth interrupted by step-function acquisitions that fundamentally changed the scale and competitive position of the business.

The market rewarded the vision, at least initially. Medios had been included in the SDAX index on September 21, 2020 — a milestone for a company that had been a shell company just four years earlier. The stock had reached an all-time high of EUR 42 on May 26, 2020, reflecting investor enthusiasm for the platform thesis and the M&A growth trajectory. At that price, the market was valuing the company at roughly EUR 1 billion — a significant premium to the underlying asset value, reflecting expectations of continued deal-making and margin expansion.

V. Inflection Point Two: NewCo Pharma and the High-Margin Shift

If the Cranach deal was about buying scale in wholesale — the volume engine — the next acquisition was about buying capability in compounding — the margin engine.

To understand why compounding matters so much, imagine the difference between a UPS driver delivering packages and a surgeon performing an operation. Both are essential services. Both require trained professionals. But the value created — and the margin captured — by the surgeon is orders of magnitude higher than the driver's, because the surgeon's work requires years of specialized training, regulated facilities, and cannot be commoditized or automated.

Pharmaceutical compounding occupies a similar position in the specialty pharma value chain. Taking a bulk chemotherapy drug and preparing a patient-specific intravenous infusion bag is not a matter of pouring liquid from one container to another. It requires calculating the precise dose for a specific patient based on their body weight, renal function, and treatment protocol. It requires preparing the bag in a GMP-certified cleanroom under aseptic conditions. It requires quality testing to confirm sterility and potency. And it requires delivering the finished product to the oncology practice within a window of hours, because many chemotherapy agents degrade rapidly once prepared.

The wholesale business — buying drugs from manufacturers and distributing them to pharmacies — generates margins of roughly 3 percent. Compounding generates margins of 10 percent or higher. The skill, the capital investment, the regulatory certification, and the time sensitivity all contribute to a margin structure that is fundamentally different from commodity distribution.

This margin differential is the entire strategic logic of Medios. If you are going to run a two-billion-euro pharmaceutical wholesale business at 3 percent margins, the only way to generate meaningful profits is to layer a high-margin service business on top. Compounding is that service layer. It transforms Medios from a logistics company into a healthcare manufacturing company — with the margin profile to match.

On November 25, 2021 — almost exactly one year after the Cranach announcement — Medios announced the acquisition of NewCo Pharma. The timing was not coincidental. Management had been running dual acquisition processes in parallel, and the NewCo deal was structured to close after Cranach was integrated.

NewCo was a national network of five regional compounding facilities focused on patient-specific infusion solutions for oncology and other therapeutic areas, plus associated wholesale operations. The deal was valued at approximately EUR 120 million, comprising EUR 85.2 million in cash and 924,233 new Medios shares. The German Federal Cartel Office approved the transaction on December 14, 2021, and the deal closed in the first quarter of 2022.

NewCo's financials told a compelling story. Revenue had grown from roughly EUR 91 million in 2016 to EUR 153 million in 2020, with patient-specific therapies accounting for more than 75 percent of revenue and an EBITDA margin of 8.6 percent — nearly three times the margin of a pure wholesale business.

The EBITDA margin differential bears emphasis. Medios was buying a business that generated almost three times the margin of its existing wholesale operations, in a market where margin expansion is extremely difficult to achieve organically. You cannot negotiate your way from 3 percent wholesale margins to 8 percent wholesale margins — the competitive dynamics of pharmaceutical distribution will not allow it. But you can acquire a compounding business that earns 8 percent margins and blend it into your portfolio, improving the group-level margin profile immediately.

The strategic rationale went beyond financial metrics. NewCo's five regional compounding facilities were located in northern, western, and southern Germany, complementing Medios's existing Berlin-focused manufacturing operations. This geographic dispersion mattered enormously for a product with a shelf life measured in hours rather than days. A compounded chemotherapy infusion bag prepared in Berlin cannot serve a patient in Munich — the transit time would exceed the product's stability window. Regional laboratories, positioned within driving distance of the oncology practices they serve, solve this problem through proximity.

After the NewCo deal, Medios operated six GMP-certified compounding laboratories across Germany — a network that enabled just-in-time delivery of patient-specific therapies with turnaround times as short as sixty minutes when necessary. No competitor could match this combination of national scale and regional proximity.

Consider the logistics from the perspective of an oncologist in Hamburg. A patient arrives for a scheduled chemotherapy infusion at 10 a.m. The oncologist has ordered the patient-specific preparation through the Medios system. The nearest Medios compounding laboratory receives the order, calculates the dose based on the patient's latest lab results, prepares the infusion bag in a Grade A cleanroom, conducts quality checks, packages it in a temperature-controlled container, and dispatches it to the oncology practice. The bag arrives before the patient sits down in the infusion chair. This is not FedEx delivering a package. This is a pharmaceutical manufacturing operation with a sixty-minute cycle time, producing a product with a shelf life measured in hours rather than months.

The barrier to entry was not just capital — it was the years of regulatory approval required for each facility, the trained personnel, and the established relationships with the oncology practices and pharmacies that relied on Medios's preparations for their patients' treatments. A new entrant would need to replicate not just the physical facilities but the entire network of trust, logistics, and clinical relationships that Medios had built over years.

The two major acquisitions — Cranach for wholesale scale and NewCo for compounding capability — completed the core platform. Revenue reached EUR 1.61 billion in 2022 and continued climbing to EUR 1.79 billion in 2023. Medios had achieved something the German pharmacy law was designed to prevent: a unified, scaled infrastructure platform serving hundreds of independent specialty pharmacies — without owning a single pharmacy.

The legal structure was unimpeachable. Medios did not own pharmacies. It served pharmacies. The Fremdbesitzverbot was satisfied. But the economic effect — the aggregation of purchasing power, the centralization of compounding, the digital integration of ordering and billing — was functionally identical to what a corporate pharmacy chain would achieve in a market without ownership restrictions. It was a masterclass in regulatory arbitrage: respecting the letter of the law while capturing the economics that the law was designed to prevent.

VI. Management and the Gärtner Era

Matthias Gärtner is not the profile you would expect for the CEO of a pharmaceutical company. Born in 1967, he studied computer science at the Technical University of Karlsruhe — not pharmacy, not medicine, not business administration. In 1996, he founded e.multi Digitale Dienste AG, a software company that he listed on the stock exchange in 2000 as majority shareholder and director. From 2007 to 2010, he established the Australian branch office of a European hedge fund in Sydney, responsible for selling to private and institutional investors.

The trajectory — tech entrepreneur, hedge fund executive, pharmaceutical platform builder — makes more sense when you understand what Medios actually needed at the inflection point when Gärtner became involved. The company did not need a pharmacist to run it. Manfred Schneider, the founder, already provided the pharmaceutical expertise.

What Medios needed was someone who could think like an investor, structure M&A transactions, manage a publicly listed company, and build a platform business from a fragmented collection of capabilities. It needed a dealmaker, not a druggist. Gärtner's background in tech and finance gave him the vocabulary to pitch the platform narrative to growth investors and the technical skills to structure complex share-based acquisitions.

Gärtner had been working with Medios and its predecessor entities since 2014, helping to engineer the reverse takeover and design the acquisition strategy. His background in technology gave him a natural affinity for the platform thesis — the idea that Medios could create a digital and physical infrastructure layer that connected independent pharmacies, medical specialists, and health insurers into a unified system.

The tech-executive-turned-healthcare-CEO is an increasingly common archetype in European mid-cap companies, where the digitization of traditional industries creates opportunities for leaders who understand both technology and business model design. Gärtner brought to Medios the pattern recognition of someone who had built and scaled a technology platform, applied to a market that desperately needed one.

Under Gärtner's leadership, Medios transformed from a EUR 133 million revenue company at the time of the 2016 listing to a EUR 2.08 billion platform by FY2025. He orchestrated the Cranach and NewCo acquisitions, the SDAX listing, and the company's internalization of a narrative that resonated with growth-oriented institutional investors.

His compensation was reported at EUR 647,000 — modest by the standards of a CEO running a two-billion-euro-revenue company, and structured with heavy emphasis on EBITDA performance and return on capital rather than pure top-line growth. For context, the median CEO compensation in the SDAX is several times higher. The lean compensation structure reflected a management team that owned meaningful equity and was therefore aligned with shareholders through ownership rather than pay packages.

On November 3, 2025, Medios announced that Gärtner would step down as CEO effective December 31, 2025. The Supervisory Board expressed "sincere thanks for his outstanding work and great commitment over the past ten years." The transition was orderly and planned — not the kind of abrupt departure that signals trouble. Gärtner had built what he set out to build. The next phase required a different skill set.

The successor tells you everything about where Medios is heading next.

Thomas Meier assumed the CEO role on February 1, 2026. His most recent position was CEO of Bachem Holding AG, the Swiss contract development and manufacturing organization that produces peptides and oligonucleotides for the pharmaceutical industry. Bachem is, in many ways, the kind of company that investors hope Medios will become: a specialized pharmaceutical infrastructure provider with deep regulatory moats, high margins, and a dominant market position in a niche that is too small to attract the attention of industry giants but too complex to be easily disrupted.

At Bachem, Meier had overseen sales growth of 122 percent, EBITDA expansion of 146 percent, and net profit increases of 175 percent — all achieved organically over a five-year tenure beginning in 2020. The organic growth track record is especially relevant because it suggests that Meier knows how to grow a pharmaceutical platform without relying on acquisitions — the skill that Medios needs most in its current phase.

Meier's appointment signals a shift from the M&A-driven growth phase to an operationally focused integration and optimization phase. Gärtner was the dealmaker who assembled the platform. Meier is the operator who will be expected to extract the full value from the assembled assets, optimize the cost structure, and extend the model internationally.

The pattern is common in successful roll-up stories. The founder identifies the opportunity. The dealmaker assembles the pieces. The operator integrates them into a cohesive whole. Each phase requires a different temperament and a different skill set. The danger zone — the phase where many roll-ups destroy value — is precisely the transition from assembly to integration. Acquired assets that are not properly integrated remain a collection of businesses rather than a platform, and the synergies that justified the acquisition premiums never materialize.

A new CFO, Stefan Bauerreis, joined effective April 15, 2026, replacing Falk Neukirch and completing the leadership transition. The entire C-suite has turned over within six months — a bold reset that signals ambition but also carries execution risk.

Meanwhile, the founder's connection to the company has also evolved. In June 2024, Manfred Schneider sold his entire 14.9 percent stake to Luxempart S.A., a Luxembourg-listed investment company, via a private placement. Schneider described the transaction as resolving his "shareholding succession" and praised Luxempart's "thorough analysis and deep understanding of Medios and its strategy." The sale brought a long-term institutional anchor shareholder onto the register and removed the overhang of a potential founder share sale.

The current shareholding structure reflects the company's maturation from a founder-led startup to a professionally managed platform. BMSH GmbH, the entity that sold Cranach Pharma, holds approximately 18 percent. Luxempart holds roughly 14.9 percent. Mediosmanagement GmbH, the management vehicle, holds approximately 13 percent. Institutional investors account for 26 to 31 percent of the shareholder base.

The free float is 33.7 percent — relatively thin for a company of this size, which contributes to liquidity constraints and higher-than-average price volatility. On any given trading day, the volume in Medios shares is modest by SDAX standards, and a single institutional investor building or unwinding a position can move the stock price by several percentage points. This illiquidity is both a risk and an opportunity: a risk because it amplifies volatility and discourages some institutional investors from taking positions, and an opportunity because it means the stock price can deviate significantly from intrinsic value for extended periods — creating potential entry points for patient investors.

VII. The Hidden Business: MediosConnect and Tech

Strip away the narratives about M&A strategy and platform building, and the most interesting thing happening at Medios may be the least visible: a browser-based digital platform called MediosConnect that is quietly becoming the operating system for specialty pharmaceutical care in Germany.

MediosConnect connects four stakeholders in the specialty pharma ecosystem: medical specialists (primarily oncologists but also ophthalmologists, neurologists, and other specialists who prescribe complex therapies), specialist pharmacies, health insurers, and patients.

The platform enables medical specialists to order patient-specific therapies and medicinal products from pharmacies and submit digital invoices under selective contracts — all with a few clicks rather than the phone calls, fax machines, and paper trails that still dominate much of the German healthcare system. If you have ever been surprised that Germany — one of the most technologically advanced economies on earth — still relies heavily on fax machines in its healthcare system, you are not alone. The digitization gap in German healthcare is enormous, and MediosConnect is quietly filling a corner of it.

Every prescription submitted through MediosConnect undergoes an additional plausibility check for patient safety — a layer of clinical verification that reduces dosing errors and drug interactions. When an oncologist orders a chemotherapy regimen for a patient, the system automatically checks the prescribed dose against the patient's body weight and renal function, flags potential drug interactions, and verifies that the prescribed drug is covered under the relevant insurance contract. This is not a trivial feature. Dosing errors in oncology can be fatal, and a digital safety net that catches errors before the drug is prepared adds genuine clinical value.

The platform provides real-time order status tracking, treatment course access, and customized prescription portfolios for each medical specialist. Data only needs to be entered once, flowing seamlessly across the ordering, preparation, and billing processes. In a healthcare system where the same patient information is often entered manually into five different systems — the physician's practice management system, the pharmacy's dispensing system, the insurer's claims system, the compounder's production system, and the logistics provider's tracking system — a single-entry platform that connects all four parties is a meaningful efficiency gain.

The strategic significance of MediosConnect extends far beyond operational efficiency. Once an oncology practice begins using the Medios portal to order complex chemotherapy regimens — once the doctors and nurses have integrated MediosConnect into their daily workflow, once the billing processes are connected to the health insurance systems, once the prescription protocols are customized for each specialist — the switching costs become formidable.

This is the digital lock-in that every platform company aspires to but few achieve in healthcare. Most digital health platforms fail because they ask busy clinicians to change their workflows without offering sufficient immediate benefit. MediosConnect succeeds because it is not an optional add-on — it is the mechanism through which the pharmacy receives orders for drugs that its patients need tomorrow morning. Opt out of MediosConnect and you opt out of the supply chain.

Think of it as the ERP system for specialty pharmaceutical care. Nobody switches ERP systems for fun. The retraining, the data migration, the process disruption, the risk of errors during transition — all of these create inertia that keeps users on the platform even when competitors offer marginally better terms. For Medios, MediosConnect transforms the relationship with its partner pharmacies and their prescribing physicians from a transactional one — buying drugs from whichever distributor offers the best price — to a systemic one, where Medios is embedded in the daily operational infrastructure of the practice.

Now layer the segment economics on top of the digital strategy, and the picture becomes clearer. The three segments tell very different stories about the nature of the business and its profit potential.

The Pharmaceutical Supply segment — wholesale — generated EUR 1.69 billion in revenue in FY2025, or 81 percent of the group total, with EBITDA of EUR 52.5 million at a margin of approximately 3.1 percent. This is the volume engine. It is not glamorous. The margins are thin. A 3 percent EBITDA margin means that for every hundred euros in drug sales, Medios keeps three euros before interest, taxes, depreciation, and amortization. After those charges, the actual profit on a hundred euros of wholesale revenue is barely visible.

But this misses the point. The wholesale segment is not a profit center — it is a customer acquisition channel. It generates the purchasing power that allows Medios to negotiate with pharmaceutical manufacturers at scale, and it creates the daily touchpoints with partner pharmacies that feed the higher-margin businesses. Every wholesale relationship is a potential compounding relationship. Every drug order is a touchpoint that deepens the operational dependency.

The Patient-Specific Therapies segment — compounding — generated EUR 220 million in revenue, or 11 percent of the total, with EBITDA of EUR 22.2 million at a margin of approximately 10.1 percent. This is the value engine. Every infusion bag prepared in a Medios cleanroom generates roughly three times the margin of a wholesale transaction, despite representing a fraction of the revenue.

The International Business segment — primarily the Ceban Pharmaceuticals operations in the Netherlands, Belgium, and Spain — generated EUR 169 million in revenue in its first full year of consolidation, with EBITDA of EUR 29.1 million at a margin of 17.2 percent. This is the highest-margin segment in the group, reflecting the maturity of Ceban's compounding operations and the pricing dynamics in its markets.

The margin differential between the German and international compounding operations — 10 percent versus 17 percent — deserves scrutiny. Part of the gap reflects Ceban's longer operating history and more mature cost structure. Part reflects different reimbursement rates and competitive dynamics in the Dutch and Belgian markets. And part may reflect upside potential for the German compounding operations if Meier's integration efforts succeed in bringing German margins closer to international levels. Even a 200-basis-point improvement in German compounding margins would add meaningfully to group EBITDA.

The interaction between these segments is what makes Medios more than the sum of its parts. The wholesale business brings pharmacies into the Medios ecosystem. MediosConnect digitally integrates those pharmacies with their prescribing physicians. And the compounding business captures the highest-value activity in the chain — the preparation of patient-specific therapies — at margins that are five to six times higher than wholesale. This is the flywheel that the company's investor presentations describe, and unlike many corporate flywheel claims, this one has a structural logic grounded in the physical realities of specialty pharmaceutical distribution.

VIII. Strategic Analysis: Seven Powers and Five Forces

Hamilton Helmer's Seven Powers framework provides a useful lens for evaluating whether Medios's competitive advantages are durable or temporary. In a market where the stock has declined 69 percent from its highs, the question is not academic — it determines whether the current valuation represents a buying opportunity or a fair assessment of a business with limited pricing power.

The primary power is scale economies. In pharmaceutical wholesale, the economics are brutally simple: the more volume you aggregate, the better the pricing you negotiate with manufacturers. Medios's network of 850 partner pharmacies gives it purchasing power that no individual pharmacy or small network can match. When Medios negotiates with Roche for a chemotherapy agent, it is negotiating on behalf of a meaningful share of the entire German specialty pharmacy market. The rebates and volume discounts that result flow directly to the bottom line — and they widen as the network grows. Every new partner pharmacy that joins the Medios ecosystem improves the economics for every existing partner.

This is a genuine scale economy in Helmer's sense: the unit cost of goods sold declines as scale increases, creating a structural advantage that grows over time. A competitor with 100 partner pharmacies simply cannot negotiate the same pricing as a competitor with 850. The gap is not a matter of negotiating skill — it is a mathematical function of volume.

Moreover, the scale advantage is self-reinforcing. Better pricing from manufacturers means Medios can offer better terms to its partner pharmacies. Better terms attract more pharmacies to the network. More pharmacies increase the volume further, enabling even better pricing. This virtuous cycle is extremely difficult for a smaller competitor to break into, because they cannot offer competitive pricing without the volume, and they cannot get the volume without competitive pricing. It is the classic chicken-and-egg problem that incumbents with scale love and challengers hate.

The second power is switching costs, primarily driven by the MediosConnect platform and the GMP compounding relationships. Once an oncology practice has integrated MediosConnect into its workflow — once the prescribing protocols are customized, the insurance billing connections are established, and the pharmacists have built working relationships with the Medios compounding laboratories that prepare their patients' infusion bags — switching to a competitor involves real costs and real risks. A botched transition during chemotherapy treatment is not an inconvenience. It is a patient safety issue.

The third power is cornered resource — specifically, the GMP manufacturing licenses and the physical infrastructure they represent. Getting GMP certification for pharmaceutical compounding in Germany requires cleanroom facilities meeting EU Annex 1 standards, comprehensive quality management systems, validated processes, trained personnel, and years of regulatory review.

Medios operates six certified facilities in Germany plus Ceban's European facilities. Each one represents millions of euros in capital investment and years of regulatory effort. These are not resources that can be purchased on the open market. They must be built, validated, and approved — a process that takes three to five years per facility under normal circumstances.

A competitor seeking to replicate this network would face a timeline measured in years and investment measured in tens of millions of euros — and that is before winning a single customer. During those years, Medios would continue expanding its own network, deepening its relationships, and raising the bar for what a new entrant would need to match. The cornered resource advantage grows with time, which is the hallmark of a truly durable competitive position.

It is worth noting which powers Medios does not clearly possess, because intellectual honesty about limitations is as important as recognition of strengths.

It does not have strong brand power in Helmer's sense — pharmacies do not choose Medios because of brand affinity but because of practical necessity. No pharmacist has an emotional attachment to their drug distributor. They have an operational dependency.

It does not have meaningful network effects — each pharmacy's experience does not inherently improve as more pharmacies join, except indirectly through purchasing power. This distinguishes Medios from true network-effect businesses like marketplaces or social networks, where each new participant directly improves the experience for all existing participants.

And process power — while Medios's compounding operations are competent and well-managed — is not proprietary in a way that competitors could not eventually replicate given sufficient time and capital. Medios does not hold patents on its compounding processes. The knowledge is specialized but not secret.

Now apply Porter's Five Forces to understand the competitive dynamics of the market in which Medios operates.

The bargaining power of suppliers — pharmaceutical manufacturers like Roche, Merck, and Bristol Myers Squibb — has historically been enormous. Big Pharma sets the prices for specialty drugs, and buyers have limited ability to push back. The pharmaceutical manufacturer holds the patent, controls the supply, and dictates the terms. In most categories, there is no generic alternative, no substitute product, and no negotiating leverage for the buyer.

But Medios has reached a scale where it is too important to ignore. When you represent the supply chain for a significant share of Germany's specialty pharmacy market, the manufacturer needs you as much as you need them. A pharma company launching a new oncology drug in Germany needs distribution infrastructure that can handle cold-chain logistics and reach specialty pharmacies nationwide. Medios provides that infrastructure. This does not eliminate supplier power, but it moderates it — and the moderation improves with every pharmacy added to the network.

The bargaining power of buyers — the partner pharmacies and, ultimately, the health insurance companies — is moderate but nuanced. Individual pharmacies have limited alternatives for specialty drug supply and compounding at Medios's scale. Where else would a pharmacy in Stuttgart go for patient-specific oncology compounding with same-day delivery? The practical alternatives are few.

Health insurers negotiate selective contracts that determine reimbursement rates, and Medios must operate within those constraints. The German statutory health insurance system covers roughly 90 percent of the population, and its pricing power is substantial. But the complexity and patient safety requirements of specialty pharma limit the insurers' ability to squeeze margins below the level at which quality can be maintained. You can negotiate a lower price for a headache tablet. You cannot meaningfully negotiate a lower price for a sterile compounded chemotherapy infusion without accepting a higher risk of quality failure — and no insurer wants that liability.

The threat of substitutes is remarkably low for Medios's core business. You cannot substitute a personalized cancer therapy. There is no generic alternative to a patient-specific infusion bag prepared in a cleanroom for a patient whose dosing is calculated based on their individual clinical parameters.

Digital health innovations, telemedicine, and oral oncology drugs may eventually reduce some demand for compounded infusions, but the shift will be gradual and incomplete — many biologic therapies cannot be reformulated as pills. A monoclonal antibody is a complex protein molecule that would be destroyed by stomach acid if taken orally. Until pharmaceutical science solves that problem — and it is a problem that has resisted decades of research — many specialty drugs will continue to require intravenous administration and, therefore, patient-specific compounding.

The threat of new entrants is limited by the GMP certification barriers, the capital requirements for cleanroom infrastructure, the years-long regulatory approval process, and the entrenched relationships that Medios has built with its 850 partner pharmacies and their prescribing physicians.

A well-capitalized entrant could theoretically build this infrastructure, but the time required to do so — and the fact that Medios would continue growing its network during that period — makes catch-up extremely difficult. The most plausible new entrant threat would come from a large pan-European pharmaceutical distributor like McKesson or PHOENIX deciding to build dedicated specialty compounding capabilities in Germany. This remains a possibility worth monitoring, but such a move would require years of investment and regulatory approval, and the incumbent advantage would be difficult to overcome.

Competitive rivalry is moderate. Medios's most direct competitors are hospital pharmacies that prepare cytostatics in-house, eliminating the need for an external compounder, and a handful of independent oncology pharmacies that serve specific regional markets. The large pan-European wholesalers like PHOENIX Group have specialty capabilities but lack the depth in compounding that Medios offers.

No other company currently replicates Medios's combination of nationwide specialty wholesale, GMP compounding, digital integration, and partner pharmacy network in the German market. This integrated offering is what separates Medios from both the large generalist wholesalers — who have the distribution but not the compounding — and the small specialty compounders — who have the compounding but not the distribution scale. Medios sits in the intersection, and that intersection is narrow enough that competitive intensity remains contained.

IX. The Future: International Expansion and New Frontiers

The most consequential deal in Medios's recent history may not have been Cranach or NewCo — both of which were German domestic acquisitions that expanded an existing model within a familiar regulatory environment. It may have been the purchase of Ceban Pharmaceuticals, which posed a fundamentally different question: can the German model travel?

Every successful domestic platform company faces this question eventually. The home market is finite. The playbook is proven. The question is whether the playbook works in a different country, with different regulations, different reimbursement systems, different competitive landscapes, and different cultural norms around healthcare delivery. Many companies that attempt international expansion discover, painfully, that what made them successful at home was more context-dependent than they realized.

Announced on March 18, 2024, and completed on June 6, 2024, the Ceban acquisition was by far Medios's largest transaction — approximately EUR 235 million in cash plus 1.7 million new Medios shares. The seller was Bencis Capital Partners, a Dutch private equity firm. Ceban was the market leader in pharmaceutical compounding in the Netherlands, with operations in Belgium and Spain as well.

Ceban's financials demonstrated why compounding, when operated at scale in markets with favorable regulatory frameworks, can be extraordinarily profitable. In FY2023, Ceban generated approximately EUR 160 million in revenue with adjusted EBITDA of roughly EUR 29 million — an 18 percent margin that dwarfed Medios's German compounding margins.

That margin differential — 18 percent for Ceban versus 10 percent for Medios's German compounding operations — immediately raised the question: is the difference structural, or can Medios learn from Ceban's operations and improve German margins? If even a fraction of that margin gap can be closed through operational best-practice sharing, the impact on group profitability would be substantial.

The first full year of consolidation in FY2025 confirmed the thesis: the International Business segment delivered EUR 169 million in revenue and EUR 29.1 million in EBITDA at a margin of 17.2 percent.

The Ceban deal transformed Medios from a German company into a European platform — exactly the kind of geographic expansion that investors had been hoping for but that management had been cautious about pursuing until the right opportunity appeared.

The geographic logic was deliberate. The Netherlands and Belgium share Continental European regulatory frameworks for pharmaceutical compounding that are sufficiently similar to Germany's to allow operational knowledge transfer. The pharmacists in Amsterdam and Brussels operate under regulatory principles — GMP certification, cold-chain requirements, patient-specific dosing protocols — that mirror those in Berlin and Munich. This is not a case of a company blindly expanding into unfamiliar territory. It is a case of exporting a proven model into adjacent markets where the regulatory and operational infrastructure is structurally compatible.

Spain adds a southern European market with its own growth dynamics, and with Ceban's existing local team and relationships providing the on-the-ground knowledge that a greenfield entry would lack.

The financing deserves attention, because it marked a philosophical shift for a company that had previously funded acquisitions primarily with equity. The deal was funded primarily with debt, and the impact on the balance sheet was meaningful.

Interest expense nearly doubled from EUR 10.9 million in FY2024 to EUR 19.1 million in FY2025. Net debt stood at EUR 107 million at year-end 2025, representing 1.3 times EBITDA — manageable but elevated compared to the company's historically conservative leverage. For a company accustomed to operating with minimal debt, the Ceban financing was a significant departure. The debt will need to be serviced from cash flows while the company simultaneously invests in integration and organic growth — a balancing act that will test the new management team's operational discipline.

In January 2026, Medios opened a different kind of frontier by securing exclusive distribution rights for Bedrocan medical cannabis products across Germany, Spain, Belgium, Italy, and Austria.

It is important to be precise about what this is and what it is not. This was not an entry into the recreational cannabis market — the kind of cannabis retail operation that has become ubiquitous in parts of the United States and Canada. It was focused specifically on the reimbursable, prescription segment, where medical cannabis is dispensed through pharmacies under physician supervision for conditions like chronic pain, spasticity, and nausea associated with chemotherapy. The initial agreement covers Bedrocan's EU-GMP certified production in Denmark, expanding to other facilities from January 2027.

The medical cannabis distribution deal illustrates Medios's evolving strategy: leveraging its existing distribution infrastructure — the cold-chain logistics, the pharmacy relationships, the regulatory compliance capabilities — to add adjacent product categories that share the same infrastructure requirements. Medical cannabis requires many of the same handling, storage, and distribution capabilities as specialty pharmaceuticals. The marginal cost of adding cannabis distribution to an existing specialty pharma network is far lower than building dedicated cannabis logistics from scratch.

This is the platform economics playbook in its purest form. Once you have built the infrastructure — the cleanrooms, the cold-chain trucks, the digital ordering system, the pharmacy relationships — the cost of adding the next product category is incremental. The fixed costs are already covered. Each new product category that flows through the existing infrastructure improves the return on invested capital without requiring proportional new investment. If Medios can successfully add cannabis today, gene therapies tomorrow, and personalized nutrition or compounded hormonal therapies the day after, the platform becomes more valuable with each addition — and the unit economics improve for every existing product line as well.

The 2026 guidance reflects a company in transition between growth phases. Revenue is expected at EUR 2.0 to 2.12 billion — essentially flat to modestly higher than FY2025. Adjusted EBITDA is guided at EUR 94 to 102 million, representing potential growth of up to 9.6 percent.

The flat revenue guidance is notable. After years of step-function growth driven by acquisitions — from EUR 133 million in 2016 to EUR 2.08 billion in 2025, a fifteen-fold increase — the message from new management is clear: the acquisition phase is pausing while the integration phase begins. This is a deliberate choice, not a sign of exhaustion. The pieces have been assembled. Now they need to work together.

The focus under new CEO Thomas Meier is on "One Team Medios" — an integration initiative aimed at optimizing the operations of the various acquired businesses into a unified platform, extracting synergies, and preparing the foundation for the next phase of growth. The name itself is telling. "One Team" implies that what exists today is not yet one team — it is a collection of separately acquired businesses that share a parent company but may not yet share systems, processes, culture, or operational best practices.

The risk landscape is worth cataloging with clear eyes.

The most fundamental threat would be regulatory changes to the Apothekengesetz — the pharmacy ownership ban that underpins Medios's entire model. If Germany were to allow corporate pharmacy chains, a well-capitalized player like CVS or McKesson could enter the market and vertically integrate the supply chain, rendering Medios's horizontal platform model redundant. While such changes have been discussed periodically, the political support for independent pharmacy ownership remains broad, the ECJ ruling provides strong legal precedent, and the pharmacy lobby in Germany is powerful and well-organized. This risk is real but low-probability.

Drug pricing reforms by health insurers could compress margins in the wholesale segment. The German statutory health insurance system (GKV) periodically renegotiates reimbursement frameworks, and any reduction in the spread between manufacturer prices and pharmacy reimbursement rates directly impacts Medios's wholesale margins.

The "direct-to-patient" model, where manufacturers seek to bypass the pharmacy supply chain entirely and deliver specialty drugs directly to patients or infusion centers, represents a longer-term structural threat that is more relevant in the US market than in Germany at present, but bears monitoring. If pharmaceutical manufacturers decided to build their own cold-chain delivery networks and compounding capabilities — or if they shifted to oral formulations that did not require compounding — Medios's role as an intermediary would diminish.

X. Playbook and Epilogue

The Medios story offers several lessons that extend beyond the specifics of German specialty pharma — lessons about market structure, regulatory arbitrage, and the economics of platform businesses in fragmented industries.

The first is the power of building a "synthetic chain" in a market where actual chains are prohibited. The Apothekengesetz prevents corporate ownership of pharmacies. It does not prevent a company from becoming the indispensable infrastructure provider to those pharmacies — the wholesaler, the compounder, the digital platform, and the logistics backbone all at once.

Medios built the functional equivalent of a pharmacy chain without owning a single pharmacy. The pharmacies remain legally independent, but they are operationally dependent on Medios for the most complex and highest-value aspects of their business. It is consolidation without ownership — a distinction that matters enormously for regulatory compliance and matters not at all for economic substance.

The parallel to other industries is instructive. Airbnb built the world's largest accommodation network without owning a single hotel room. Uber built the world's largest taxi fleet without owning a single car. Medios built Germany's largest specialty pharmacy network without owning a single pharmacy. In each case, the platform company captured the economics of the underlying industry without taking on the capital intensity, the operational complexity, or the regulatory burden of asset ownership. The asset-light platform model works in hospitality, transportation, and — as Medios has demonstrated — in pharmaceutical distribution.

The second lesson is the "low-margin volume feeding high-margin service" model. Pharmaceutical wholesale at 3 percent margins is not, in isolation, an exciting business. But wholesale is the customer acquisition channel for compounding at 10 to 17 percent margins. Every pharmacy that orders specialty drugs through Medios's wholesale network is a potential customer for Medios's compounding services. The volume business creates the relationships. The service business captures the value. Neither works as well without the other.

This model has parallels in other industries. Amazon Web Services generates the majority of Amazon's operating income, but it was the e-commerce business — with its thin margins and massive scale — that built the technology infrastructure and customer relationships that made AWS possible. Costco's membership model generates most of the profit, but it is the low-margin merchandise that gets customers through the door. In each case, the visible, high-volume, low-margin business is the foundation upon which the less visible, high-margin business is built. Strip away the wholesale operation and Medios's compounding business would struggle to acquire customers. Strip away the compounding business and Medios's wholesale operation would be indistinguishable from a dozen competitors.

The third lesson is about the compounding effect — in both the pharmaceutical and financial sense — of regulatory barriers to entry. GMP certification, cold-chain logistics infrastructure, and years of embedded relationships with prescribing physicians create a competitive position that strengthens with time rather than eroding.

A competitor cannot simply undercut Medios on price and win business. The competitor must first build the cleanrooms, obtain the certifications, hire the pharmacists, establish the logistics, and win the trust of oncologists who are — quite rationally — reluctant to switch the supply chain for their patients' chemotherapy to an unproven provider. This is not a market where the lowest bidder wins. It is a market where trust, reliability, and proven track record matter — because the consequences of failure are measured in patient outcomes, not just lost revenue.

For tracking Medios's ongoing performance, two KPIs matter above all others.

The first is EBITDA pre-margin for the Patient-Specific Therapies and International segments — currently approximately 10 percent in Germany and 17 percent internationally. This is the number that separates a platform narrative from a distributor reality. This metric captures the profitability of the high-value compounding business that distinguishes Medios from a commodity wholesaler. Margin expansion in these segments — driven by volume growth, operational efficiencies, and more favorable contract terms — would signal that the platform thesis is working. Margin compression would signal either competitive pressure, adverse regulatory changes, or operational inefficiency.

The second is partner pharmacy count — currently approximately 850. This is the single most important operational metric for the business. It is the fundamental measure of the network's scale and, by extension, Medios's purchasing power with pharmaceutical manufacturers. Growth in the pharmacy network drives wholesale volumes, which drive rebate negotiating power, which drive margin improvement across the entire platform. A stagnating or declining pharmacy count would be the single most concerning signal for the business model.

Watch also for the composition of the pharmacy network, not just the count. A pharmacy that generates EUR 5 million in specialty drug purchases through Medios is far more valuable than one that generates EUR 500,000. The metric to track is not just how many pharmacies are in the network, but how much each pharmacy is purchasing — the revenue per partner pharmacy, which indicates whether Medios is deepening its relationships with existing partners or merely adding marginal ones.

The company's stock has fallen roughly 69 percent from its all-time high of EUR 42 in May 2020, currently trading at approximately EUR 13. At that price, the enterprise value implies roughly 5.9 times trailing EBITDA — a valuation that prices Medios as a pharmaceutical distributor rather than as the healthcare infrastructure platform its management claims it to be.

The valuation disconnect is stark. European healthcare infrastructure companies with comparable moat characteristics typically trade at 12 to 18 times EBITDA. Pure pharmaceutical distributors trade at 6 to 8 times. Medios, at 5.9 times, is valued at the bottom of the distributor range — a market assessment that assigns zero premium for the compounding capabilities, the digital platform, the regulatory moat, or the international expansion.

Whether the valuation reflects a market that correctly sees the limits of thin-margin distribution or a market that has failed to appreciate the durability of the regulatory moat and the compounding margin engine is the central question for investors.

FY2025 results, released on March 26, 2026, demonstrated the revenue milestone — EUR 2.08 billion — but the stock fell nearly 9 percent on the day. The market's reaction was telling. Investors were not celebrating the revenue milestone. They were concerned about rising operating expenses, the interest burden from the Ceban acquisition financing, and free cash flow that declined to EUR 36.9 million from EUR 67.4 million the prior year.

The free cash flow deterioration is worth understanding. The decline was driven primarily by the Ceban acquisition's impact on interest expenses and working capital requirements, not by a fundamental deterioration in operating performance. Pharmaceutical distribution is a working-capital-intensive business — buying drugs from manufacturers and holding them until pharmacies pay creates a permanent cash drag that scales with revenue. A company that grows revenue by 16 percent in a year will see its working capital requirements grow commensurately.

The leadership transition — a new CEO, a new CFO, and a founder who has fully divested — adds execution uncertainty even as it signals professional maturation.

The personalized medicine tailwind behind Medios is real and structural. As oncology moves from standardized chemotherapy protocols toward precision dosing based on genetic profiles, tumor characteristics, and individual patient biology, the demand for patient-specific compounding will grow. Every advance in precision medicine — every new biomarker test, every new targeted therapy, every new combination regimen — makes the system more complex, not less. And complexity is Medios's competitive advantage.

As new biologic therapies enter the market — each requiring cold-chain handling, cleanroom preparation, and rapid delivery — the infrastructure that Medios has built becomes more valuable, not less. The pharmaceutical industry is moving toward greater personalization, not less. The treatments of the future will require more compounding, not less. The drugs of the future will be more temperature-sensitive, more dosing-specific, and more logistics-intensive than the drugs of today.

In this context, Medios is not just a company benefiting from a tailwind. It is the infrastructure upon which the tailwind depends. You cannot deliver personalized cancer therapy to a patient in Hamburg without someone operating the cleanroom, managing the cold chain, and coordinating the sixty-minute delivery window. As of 2026, in Germany, that someone is overwhelmingly Medios.

The story of Medios AG is ultimately a story about infrastructure — about the invisible systems that connect drug manufacturers to the patients who need their products, and about the company that figured out how to build, consolidate, and monetize that infrastructure in a market that was designed to resist consolidation.

From a single pharmacy in Berlin's Mitte district to a EUR 2.08 billion European platform with operations in five countries, the arc of Medios traces the evolution of specialty pharmaceutical care from a cottage industry of independent pharmacists to a professionalized, technology-enabled infrastructure business. The pharmacists are still independent. The law still protects their autonomy. But behind the counter, the plumbing — the supply chain, the cleanrooms, the digital ordering platform, the cold-chain trucks — belongs to Medios.

Whether the next chapter is written by Thomas Meier's integration playbook or by forces beyond management's control — regulatory change, competitive disruption, or the relentless evolution of pharmaceutical science — the platform is built, the network is in place, and the question now is what it will be worth.

XI. Further Reading

The German Apothekengesetz and the Fremdbesitzverbot (third-party ownership ban) are the regulatory foundation of Medios's entire business model. The European Court of Justice's 2009 ruling upholding the ban provides essential legal context for understanding why the German pharmacy market remains structurally fragmented and why Medios's "synthetic chain" model is necessary.

Medios AG's investor relations presentations on the Cranach Pharma and NewCo Pharma acquisitions, available through the company's IR website, provide detailed financial and strategic analysis of the two deals that transformed the company from a regional player into a national platform. The NewCo presentation in particular includes useful data on compounding economics and the geographic logic of regional laboratory placement. The Ceban Pharmaceuticals acquisition presentation, published in March 2024, lays out the international expansion thesis and the margin dynamics that made Ceban's compounding operations so attractive.

The FY2025 annual results presentation and earnings call transcript, published on March 26, 2026, documents the first full year with Ceban consolidated and the revenue milestone of EUR 2.08 billion. The segment breakdowns — Pharmaceutical Supply, Patient-Specific Therapies, and International Business — provide the granular data needed to track the margin dynamics that determine whether Medios is a wholesaler or a platform.