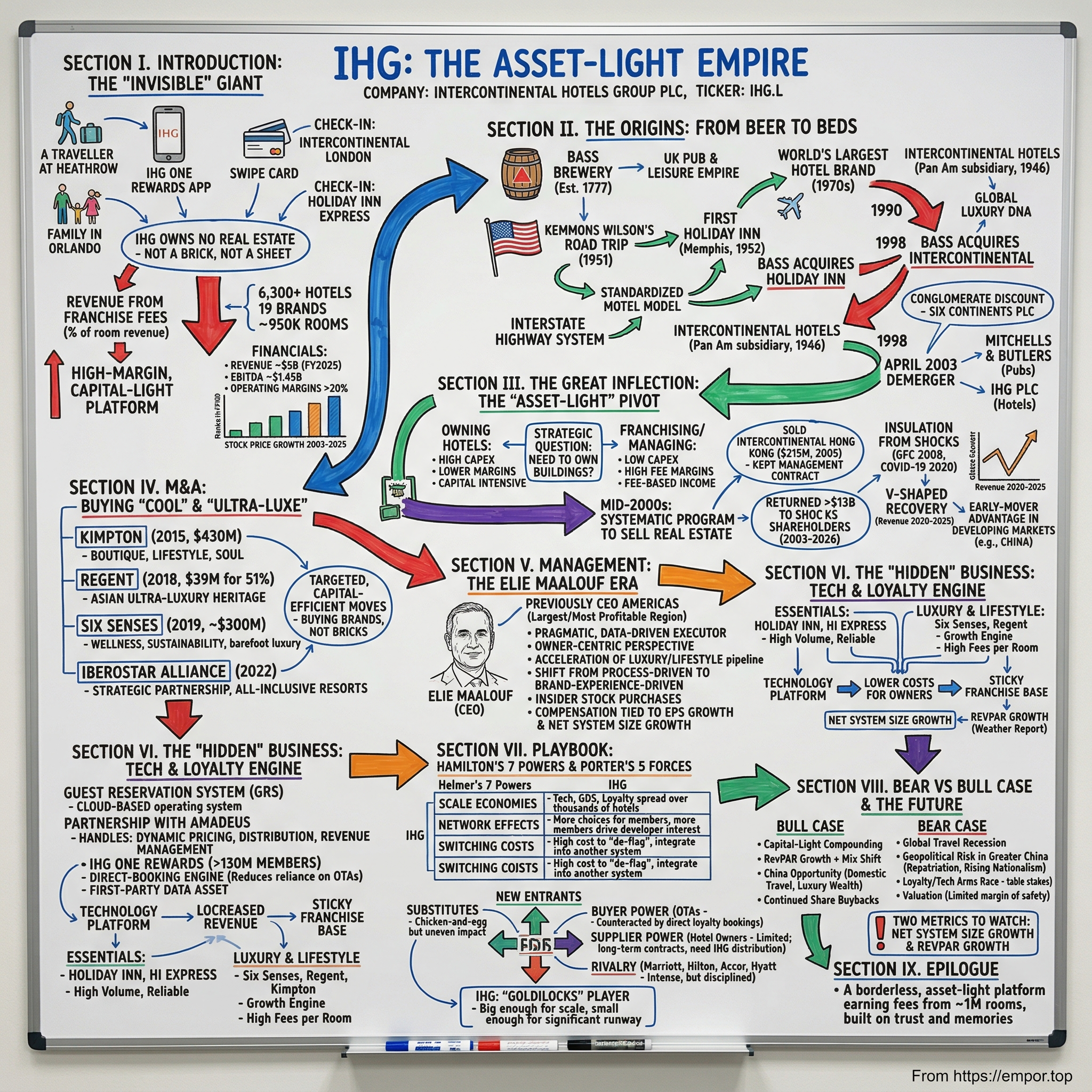

IHG: The Asset-Light Empire

I. Introduction: The "Invisible" Giant (0:00 - 12:00)

Picture this: a weary business traveler lands at Heathrow after a fourteen-hour flight from Singapore. She pulls up her phone, taps the IHG One Rewards app, and checks into the InterContinental London Park Lane before she has even collected her bag. The room key loads digitally. The concierge already knows she prefers a high floor, a firm pillow, and a late checkout.

Two days later, a family of four in Orlando checks into a Holiday Inn Express off Interstate 4, swiping the same loyalty card for a room that costs a tenth of the London suite. The kids get a cookie at the front desk. The parents get a predictable, clean, no-surprises stay with a hot breakfast included.

In both cases—the luxury traveler in Mayfair and the road-trip family in Florida—the guest walks into a building that InterContinental Hotels Group does not own. Not a single brick. Not a single doorknob. Not a single bedsheet.

And yet, IHG earned money from both stays. The company collected a franchise fee from the hotel owner in London and another from the hotel owner in Orlando—a few percent of each room's revenue, multiplied across nearly a million rooms, every single night of the year.

That is the paradox at the heart of one of the world's largest hotel empires. IHG's name sits above the doors of more than 6,300 hotels across 19 brands and over 100 countries. On any given night, roughly 950,000 rooms carry an IHG flag. Yet the company that orchestrates this global machine owns almost none of those rooms. Not the beds. Not the lobbies. Not the swimming pools. Not the parking lots.

If you tried to find IHG's real estate footprint on a balance sheet, you would find it remarkably thin for an enterprise with a market capitalisation hovering near twenty billion dollars.

This is not an accident, and it is not a recent development. It is the result of a deliberate, two-decade strategic pivot that transformed IHG from a sprawling British conglomerate—one that once brewed beer, operated thousands of pubs, and ran restaurant chains—into a high-margin, capital-light platform business that looks more like a technology franchise than a traditional hospitality company.

At its core, IHG earns money by licensing brands, managing hotels on behalf of their owners, and running a massive technology and loyalty ecosystem that connects hundreds of millions of guests with thousands of independent property owners around the globe. Think of it less as a hotel company and more as a franchise engine with a powerful loyalty currency attached—a business model that has more in common with McDonald's or Coca-Cola than with the image of a hotelier polishing brass in a grand lobby.

The business model is deceptively simple, which is part of its beauty. Hotel owners pay IHG a percentage of their room revenue—typically between three and six percent—for the privilege of flying an IHG flag and plugging into its reservation system. In return, IHG provides the brand, the booking technology, the loyalty program, the global distribution muscle, the marketing campaigns, and the corporate sales relationships. The owner provides the capital, the building, and the operating staff.

The result is a business that generates fees whether occupancy is high or low, that compounds as the system grows, and that throws off enormous amounts of free cash flow relative to the capital it consumes. When a new Holiday Inn Express opens in Bangalore or a Six Senses resort begins welcoming guests in Thailand, IHG starts collecting fees on day one without having invested a single dollar in construction.

For investors, the question that matters is whether this machine can keep compounding. The numbers suggest momentum. IHG's total revenue reached roughly five billion dollars in the fiscal year ending December 2025, with EBITDA approaching one and a half billion dollars. Operating margins sit comfortably above twenty percent on a consolidated basis, but the margins on fee income alone—the purest measure of IHG's franchise economics—are substantially higher.

The share price on the New York Stock Exchange ADR has climbed from around twelve dollars at the company's inception as a standalone entity in 2003 to above one hundred and thirty dollars today, and that figure vastly understates the total return when you factor in the billions returned through special dividends and buybacks along the way.

What makes this business so unusual is how invisible it is to the end consumer. Most travelers who stay at a Holiday Inn have no idea they are sleeping in a building owned by a local real estate investor or a regional development company, not by IHG. They assume the company behind the sign on the building is the company that owns the building. That assumption is wrong—and the gap between perception and reality is precisely where IHG's profits live.

The company has 19 distinct brands spanning the full spectrum of travel needs. At the budget end, there is Holiday Inn Express and the newer avid Hotels brand. In the midscale, Holiday Inn and Crowne Plaza. At the upper end, InterContinental, Kimpton, Hotel Indigo, and Vignette Collection. And at the ultra-luxury apex, Six Senses and Regent. This portfolio breadth means IHG can offer a hotel developer a brand for virtually any market segment and any geography, which is a powerful competitive advantage when competing for franchise signings against Marriott, Hilton, and Hyatt.

But numbers only tell part of the story. To understand where this machine is going, you first have to understand where it came from. And that story begins, improbably, with a brewery in the English Midlands, a family road trip in Tennessee, and an airline that no longer exists.

II. The Origins: From Beer to Beds (12:00 - 25:00)

In the town of Burton upon Trent, roughly one hundred and thirty miles north of London, the River Trent runs through chalky gypsum deposits that give the local water a particular mineral composition prized by brewers for centuries. This is where Bass Brewery was founded in 1777, growing over the following two centuries into one of Britain's most iconic consumer brands.

The red triangle that Bass registered as its trademark in 1876 became the first registered trademark in the United Kingdom—a symbol as recognizable in Victorian England as Coca-Cola's script would become in twentieth-century America. Édouard Manet painted it into his famous "A Bar at the Folies-Bergère." It adorned pub signs from Edinburgh to Exeter. Bass was, in every sense, a pillar of British commercial identity.

By the mid-twentieth century, however, Bass was a powerhouse searching for its next act. The brewery business was maturing, margins were thinning, and the consolidation wave sweeping British brewing meant that scale alone would not guarantee survival.

Like many large UK industrial companies in the 1960s and 1970s—think of Hanson Trust, BTR, or Tomkins—Bass began diversifying aggressively. The company pushed into pubs, leisure, and hospitality, acquiring a sprawling portfolio of properties across the United Kingdom. At its peak, Bass operated thousands of pubs, the Toby Carvery restaurant chain, and a growing collection of hotel properties. It was the quintessential British conglomerate: a bit of everything, a master of nothing.

But the move that would ultimately define the company's future came not from a British acquisition, but from an American one—and to understand it, you have to travel back to the summer of 1951.

That year, a Memphis businessman named Kemmons Wilson loaded his wife and five children into the family car for a road trip to Washington, D.C. The journey was miserable—not because of the driving, but because of the motels. Every stop was a gamble. Some were clean; some were not. Some charged extra for children; some had no air conditioning. The rooms varied wildly in quality, and there was no way to know what you were getting until you pulled into the parking lot.

Wilson, who had made his money in homebuilding and popcorn machines, was not a hotel man. He was an entrepreneur who saw a broken market and decided to fix it. When he returned home to Memphis, he famously sketched out a plan for a standardized motel chain on a legal pad, specifying everything from room size (the rooms would be large enough for a family) to amenities (every room would have air conditioning, a telephone, and a television). Children would stay free. There would be a swimming pool at every location. And the quality would be the same whether you were in Memphis, Nashville, or Miami.

He called it Holiday Inn, after the 1942 Bing Crosby film, and opened the first property on Summer Avenue in Memphis in August 1952.

Wilson's insight was brilliantly democratic, and the timing was perfect. President Eisenhower's Interstate Highway System, authorized in 1956, would soon crisscross America with 41,000 miles of high-speed roads, creating an explosion in automobile travel. Holiday Inn rode that wave with ferocious expansion, franchising aggressively and standardizing relentlessly.

By the 1970s, Holiday Inn had become the largest hotel brand in the world by room count—the "Ford Model T of hotels," as industry historians would later call it. Affordable, standardized, ubiquitous, and trusted. The Great Sign—that iconic green-and-orange neon marquee—became as much a part of the American roadside landscape as a Texaco star or a Dairy Queen cone.

By the time Bass came knocking in 1988, Holiday Inn's international operations were available for acquisition. Bass bought Holiday Inn International first, then in 1990 acquired the full Holiday Inn brand and domestic operations from Holiday Corporation for roughly $2.2 billion. It was an audacious bet for a British brewer—suddenly, Bass controlled one of the most recognizable hospitality brands on the planet, with thousands of properties stretching from Memphis to Manila.

But Holiday Inn was not the only jewel Bass would come to possess. Through a series of subsequent transactions in the late 1990s, Bass also acquired the InterContinental Hotels brand, which carried one of the most storied pedigrees in luxury travel—a lineage that traced back not to a Memphis motel, but to the golden age of aviation.

In 1946, Juan Trippe, the visionary and autocratic founder of Pan American World Airways, created a hotel subsidiary called InterContinental Hotels Corporation. Trippe's logic was elegant: Pan Am was rapidly expanding its international route network, flying glamorous passengers on its Clippers across the Atlantic and Pacific. But when those passengers landed in Bogotá, or Beirut, or Belém, there was often nowhere suitably grand to stay. Trippe wanted to ensure that the Pan Am experience extended from the aircraft to the hotel.

The first InterContinental Hotels opened in Brazil's Belém and Rio de Janeiro, and the brand soon spread to cities across Latin America, Europe, the Middle East, and Asia. These were not modest properties. They were diplomatic watering holes—the kind of places where foreign correspondents filed dispatches, where diplomats negotiated over cocktails, and where business leaders closed deals in marble-floored lobbies. The InterContinental in Geneva, the InterContinental in Nairobi, the InterContinental in Hong Kong—each carried an aura of international prestige that was inseparable from the Pan Am mystique.

When Bass acquired this brand, it inherited not just a name but a DNA of global luxury that would prove vital decades later as IHG pushed into the upper echelons of the hospitality market. The Pan Am airline was long gone by then—it had ceased operations in 1991—but the hotel brand it created lived on, carrying with it an almost diplomatic gravitas that no amount of marketing spend could replicate from scratch.

By the turn of the millennium, however, the conglomerate structure was straining under its own contradictions. Bass had renamed itself Six Continents PLC, a nod to the global reach of its hotel business, but the company still contained an enormous UK pub and restaurant empire alongside its hotel operations.

Investors struggled to value the whole, and the parts were pulling in different directions. The pubs business was capital-intensive, cyclical, and tied to the vagaries of British consumer spending and pub regulation. The hotel business, increasingly oriented toward franchising and management contracts, was generating higher returns on capital and had a compelling global growth story to tell. Analyst reports from the period reveal persistent frustration: the hotel business was being valued at a discount because it was trapped inside a pub-and-beer conglomerate.

In April 2003, the board of Six Continents made the decision that would set IHG on its current trajectory. The company demerged, splitting into two separate publicly listed entities. The pubs and restaurants became Mitchells & Butlers PLC, which still operates thousands of managed pubs and restaurants across the UK today. The hotel operations became InterContinental Hotels Group PLC, listed on the London Stock Exchange under the ticker IHG.

From its first day as an independent company, IHG held a portfolio of roughly 3,500 hotels and 535,000 rooms across nearly 100 countries, with Holiday Inn, Holiday Inn Express, Crowne Plaza, and InterContinental as its principal brands. The conglomerate discount evaporated overnight.

The demerger also forced a clarity of purpose that had been impossible within the Six Continents structure. IHG's new management team, led by CEO Andrew Cosslett who took the helm in 2005, could now pursue a hotels-only strategy without having to justify capital allocation decisions against the competing demands of a pub empire. Every pound invested, every strategic initiative, every management hour could be directed toward a single objective: building the world's most valuable portfolio of hotel brands. That focus would prove transformative.

The stage was set for one of the most dramatic strategic pivots in the history of the hospitality industry—a pivot that would transform IHG from a company that owned hotels into a company that owned something far more valuable: the right to put its name on hotels owned by others.

III. The Great Inflection: The "Asset-Light" Pivot (25:00 - 55:00)

In the spring of 2004, the newly independent IHG's management team sat in their offices in Denham, a village west of London, and confronted an uncomfortable truth. The company owned or leased a significant portfolio of hotel real estate scattered across multiple continents—some of it prime, some of it aging, all of it tying up capital that could be deployed more productively.

The question was not whether the brands were valuable. Everyone knew that Holiday Inn and InterContinental had enormous global recognition. The question was whether IHG needed to own the buildings to capture that value.

To understand why this question was so radical, you have to appreciate what the hotel industry looked like at the time. For most of the twentieth century, owning hotels was simply what hotel companies did. You built the building, you hired the staff, you managed the operations, and you kept the profits. The brand and the bricks were inseparable. The great hotel dynasties—Hilton, Marriott, Sheraton—all began as owner-operators. Conrad Hilton bought his first hotel in Cisco, Texas in 1919. J.W. Marriott opened a root beer stand in 1927 that eventually became a hotel empire. The assumption was deeply ingrained: to be in the hotel business, you needed to be in the real estate business.

IHG's leadership looked at this assumption and decided it was wrong. Or at least, it was no longer right for IHG.

The insight was simple but powerful: the highest-margin, most capital-efficient part of the hotel business is not owning rooms. It is licensing brands and operating reservation systems.

Consider the economics. When IHG owns a hotel, it captures the full room revenue but also bears the full cost of operations, maintenance, property taxes, insurance, and capital expenditure. A leaky roof, a broken elevator, a renovation cycle—these are the owner's problems. The operating margins on an owned hotel might be fifteen to twenty percent in a good year, and they can go negative in a downturn.

By contrast, when IHG franchises its brand to an independent owner, it earns a percentage of room revenue—typically three to six percent—as a franchise fee, plus additional fees for the reservation system, loyalty program, and other services. The total fee might be ten to twelve percent of room revenue. And here is the critical point: that fee income comes with almost no associated capital expenditure and minimal variable costs. The franchise fee is essentially pure margin. There is no building to maintain, no boiler to fix, no roof to replace, no labor force to manage. The brand owner earns a percentage of every room night sold, year after year, while the property owner bears the capital cost and operating risk.

Armed with this insight, IHG embarked in the mid-2000s on a systematic program to sell its owned and leased hotel properties, retain the management contracts or franchise agreements, and return the proceeds to shareholders. The strategy was labeled "asset-light," and it would become the defining strategic move of IHG's independent existence.

The most dramatic single transaction came in 2005, when IHG sold the InterContinental Hong Kong—one of the most iconic luxury hotels in Asia, commanding sweeping views of Victoria Harbour from its prime Tsim Sha Tsui waterfront location—for approximately $215 million.

The property was a jewel, the kind of hotel that defines a city's skyline. But IHG did not need to own it to profit from it. The sale crystallized the entire philosophy: sell the bricks, keep the brand, sign a long-term management contract, and let the capital flow to shareholders. The InterContinental Hong Kong continued to operate under the IHG flag, guests noticed no difference whatsoever, and IHG continued to earn management fees—but the balance sheet was suddenly lighter by hundreds of millions of dollars.

This was not a one-off. Between 2003 and the early 2010s, IHG sold billions of dollars of hotel real estate across multiple continents—properties in London, New York, Sydney, Paris, and dozens of other cities. Each sale followed the same playbook: divest the property, retain the brand and management relationship, and return the cash.

And IHG did return the cash, adopting one of the most aggressive shareholder return programs in the FTSE 100. Since the demerger in 2003, IHG has returned well over thirteen billion dollars to shareholders through a combination of ordinary dividends, special dividends, and share buybacks. That figure dwarfs the company's current market capitalisation.

An investor who bought shares at the 2003 demerger and simply held would have collected a staggering sequence of special dividends funded by asset sales: roughly $4.50 per ADR share in 2006, over $7.30 in 2007, $4.18 in 2014, and a blockbuster $11.04 in 2016. These were not ordinary dividend payments; they were the direct proceeds of real estate sales being channeled back to the people who owned the company.

Add in the regular dividends—which themselves grew steadily—and the share price appreciation from around twelve dollars to above one hundred and thirty, and the total shareholder return picture is one of the best among large-cap European companies over that twenty-plus-year period.

But the genius of the asset-light model was not just financial engineering. It was strategic insulation. When the Global Financial Crisis hit in 2008, hotel companies that owned large property portfolios found themselves in a vice. Real estate values plummeted, debt covenants tightened, and massive write-downs consumed earnings. Some hotel companies came perilously close to bankruptcy.

IHG, having already shed most of its owned properties, was far less exposed. The company's revenue declined during the downturn—occupancy rates fell across the industry, and fee income dropped as hotels took in less revenue—but IHG did not face the existential balance sheet pressures that crushed some of its competitors. There were no fire sales of prime properties at distressed prices. There were no emergency equity raises. The fee-based model provided a floor: as long as hotels remained open and guests checked in, even at lower rates, IHG earned fees.

The same dynamic repeated during COVID-19, an even more severe shock. In March and April of 2020, global hotel occupancy plunged to levels not seen since the industry's infancy. Hotels in major cities saw occupancy rates in the single digits. Business travel essentially ceased overnight. Conference centers went dark. International borders closed.

IHG reported a net loss of $260 million for the fiscal year ending December 2020, and revenue fell from pre-pandemic levels to just $2.4 billion. Those numbers were painful, but they could have been catastrophic for a company with billions of dollars of owned real estate sitting empty and generating losses.

Because IHG had already completed its asset-light transition, the company survived the crisis without a transformative restructuring, without a dilutive equity raise, and without selling trophy assets at distressed valuations. Management cut costs, preserved liquidity, suspended the buyback program temporarily, and waited for travel to return.

The recovery, when it came, was remarkably swift. By 2022, revenue had recovered to $3.9 billion. By 2023 it reached $4.6 billion, essentially matching pre-pandemic levels. And by 2025, revenue had grown to $5.2 billion, exceeding the pre-COVID peak by a comfortable margin. The V-shaped recovery was a powerful real-world validation of the asset-light thesis: when the storm passes, the fee stream comes back, because the underlying assets—the hotel buildings—are someone else's problem.

It is worth benchmarking IHG's pivot against its two most important global competitors. Marriott International, today the world's largest hotel company by room count following its transformative 2016 merger with Starwood Hotels, also operates an asset-light model. But Marriott arrived at that position through a different path—more gradual, accelerating in the 2000s and 2010s as the Marriott family ceded control.

Hilton, which Blackstone took private in the largest hospitality leveraged buyout in history—a $26 billion deal in July 2007, just months before the financial crisis—shed its owned properties as part of that private equity restructuring, eventually re-listing as a leaner, asset-light company in 2013.

IHG, by contrast, made the asset-light decision as a publicly listed company, in real-time, with public shareholders watching and questioning every step. It was arguably the first major global hotel company to commit so fully and so publicly to this model, and it did so before "asset-light" became an investor buzzword.

The timing mattered enormously. By committing early, IHG established relationships with independent hotel developers in markets like China, the Middle East, and Southeast Asia before Marriott and Hilton brought their full asset-light strategies to bear. In Greater China specifically—which would become IHG's second-largest market—the company signed franchise and management agreements in second-tier and third-tier cities that competitors had not yet reached. This early-mover advantage in developing markets built a pipeline of hotels that took years to construct and open, creating a rolling wave of new fee income that continues to arrive today.

The early commitment to asset-light also allowed IHG to build internal capabilities that would prove decisive: the franchise sales team, the owner-relations function, the technology infrastructure to support thousands of independent properties, and the legal and financial architecture to manage complex multi-country franchise agreements. These are institutional muscles that take years to develop, and IHG had a head start.

The result, by the early 2010s, was a company that looked nothing like the conglomerate that had brewed Bass Ale. IHG's capital employed had shrunk dramatically, its returns on invested capital had soared, and its free cash flow generation had become remarkably predictable. The company was earning close to half a billion dollars in annual fee revenue, with operating margins on that fee income well above fifty percent. It was, in effect, a royalty stream on global travel demand.

But IHG's leadership understood a critical vulnerability: an asset-light model only works if the brands themselves remain vibrant and desirable. Sell the buildings and keep the brand—that only works if the brand is worth keeping. And by the mid-2010s, IHG's portfolio had a conspicuous gap. It lacked a credible presence in the lifestyle and boutique hotel segments that were capturing the imagination of younger, experience-driven travelers. The company that had perfected the "reliable and efficient" hotel stay needed to learn how to be "cool."

IV. M&A: Buying the "Cool" and the "Ultra-Luxe" (55:00 - 1:25:00)

Walk into the Kimpton Hotel Monaco in Washington, D.C. on a Tuesday evening, and the scene tells you everything about why IHG wrote a $430 million check to acquire this brand. There is a complimentary wine hour in the lobby—a Kimpton signature—where hotel guests mingle with neighborhood locals over glasses of Oregon Pinot Noir and small plates from the in-house restaurant.

The decor is eclectic and playful: bold wallpaper, mismatched furniture that somehow works, a goldfish you can request for your room to keep you company. The staff wear jeans and sneakers, the general manager is on a first-name basis with half the room, and a yoga mat sits rolled up in the corner of every guest room. This is not a Holiday Inn. This is not even an InterContinental. This is something IHG had never been able to build from scratch: a genuine lifestyle hotel brand with soul, with attitude, with a point of view.

Bill Kimpton founded his eponymous hotel company in San Francisco in 1981, making it arguably the pioneer of the American boutique hotel movement—years before Ian Schrager and Steve Rubell brought Studio 54 glamour to the Morgans Hotel in New York, years before the W Hotels and Ace Hotels that would follow.

Kimpton's philosophy was rooted in San Francisco's counterculture: each property should feel unique to its city, with locally inspired restaurants, curated art installations, and a deliberate, almost defiant rejection of the cookie-cutter uniformity that defined the big chains. A Kimpton in Portland felt different from a Kimpton in Philadelphia, and that was the entire point.

By the time IHG came calling in late 2014, Kimpton operated more than sixty hotels across the United States, with a fiercely loyal following among creative professionals, tech workers, and discerning leisure travelers who would rather sleep in their car than stay at a "big box" chain hotel.

IHG announced the acquisition in December 2014 and closed it in January 2015 for $430 million. At roughly fifteen times EBITDA, it was a premium price by hospitality standards—most hotel brand acquisitions at the time transacted in the ten-to-twelve-times range. Critics questioned whether IHG was overpaying for a niche brand with limited international presence.

But the strategic logic was sound, and in retrospect, the price looks reasonable. IHG needed a lifestyle platform, and building one organically would have taken a decade—possibly longer—and carried enormous execution risk. You cannot manufacture authenticity in a boardroom. Kimpton gave IHG an instant playbook: a design sensibility, a guest experience philosophy, a pipeline of development relationships, and a team that understood intuitively how to create the kind of locally-rooted hotel experience that millennial and Gen Z travelers were increasingly seeking.

The integration was handled with unusual care, and this is where IHG deserves credit. The temptation in any large acquisition is to immediately "integrate" the target—standardize the processes, centralize the purchasing, harmonize the brand standards. IHG understood that doing so would destroy the very thing they had paid $430 million for.

Kimpton's value lay precisely in what made it different from IHG's other brands. Homogenizing it into the Holiday Inn system would have been like buying a jazz club and installing a jukebox. So IHG gave Kimpton significant creative autonomy, allowing each hotel to retain its distinctive character while plugging into IHG's reservation system, loyalty program, and global distribution network.

The combination was powerful: Kimpton's uniqueness married to IHG's scale. Since the acquisition, Kimpton has expanded internationally, opening properties in Amsterdam, Barcelona, Bali, Tokyo, and other global cities—something the standalone Kimpton, which had been almost exclusively a US brand, could never have achieved on its own.

The Kimpton deal also gave IHG something harder to quantify but equally important: organizational learning. IHG's legacy brands were built on process and standardization—the Holiday Inn brand standard manual is legendarily detailed, specifying everything from mattress firmness to bathroom tile grout color. Kimpton operated on the opposite principle: trust the local team, empower the general manager, let the property's personality emerge from its neighborhood. By acquiring Kimpton, IHG's corporate team was exposed to a fundamentally different way of thinking about the guest experience, and that thinking would eventually influence how IHG approached its broader luxury and lifestyle strategy.

But Kimpton addressed only one gap in IHG's portfolio. The company was still missing a credible ultra-luxury offering to compete with Four Seasons, Aman, and the Ritz-Carlton at the very top of the market. The InterContinental brand, while prestigious, occupied the upper-upscale space rather than true ultra-luxury. A traveler paying a thousand dollars a night for a resort villa in the Maldives expects a fundamentally different experience than even the finest InterContinental delivers. IHG needed brands that could compete at that rarefied level.

In October 2018, IHG announced the acquisition of a fifty-one percent stake in Regent Hotels & Resorts for just $39 million. Regent was a storied name in Asian luxury hospitality, founded in Hong Kong in 1970 by Robert Burns, with properties that had defined opulence across the Asia-Pacific region. The brand had faded somewhat over the decades, passing through various ownership structures and losing some of its former luster. But its DNA remained intact—a heritage of personalized, deeply attentive Asian hospitality that simply cannot be manufactured overnight.

IHG's plan was to revive Regent as an ultra-luxury brand, positioning it above InterContinental in the portfolio hierarchy, a halo brand that would signal IHG's seriousness about competing with the world's finest hotel companies.

Then, in February 2019, IHG made the move that truly turned heads across the industry: the acquisition of Six Senses Hotels Resorts Spas for approximately $300 million. Six Senses was widely regarded as perhaps the most prestigious wellness-focused luxury brand in global hospitality, with properties in locations of extraordinary natural beauty—a nineteenth-century wine estate in Portugal's Douro Valley, barefoot-luxury island resorts in the Maldives and Seychelles, mountain retreats in the French Alps, jungle hideaways in Southeast Asia.

The brand's philosophy—sustainability, wellness, and a deep connection to place—had earned it back-to-back World Best Hotel Brand honors from Travel + Leisure and accolades from virtually every other hospitality authority.

What made both the Regent and Six Senses deals so elegant from an investor's perspective was that they were themselves asset-light acquisitions. IHG was not buying real estate. It was buying management contracts, brand equity, intellectual property, and pipeline agreements. The properties continued to be owned by third parties who paid IHG to manage them.

For a combined $339 million—less than the Kimpton deal alone—IHG had acquired two ultra-luxury platforms with significant room for growth in the world's fastest-growing luxury travel markets. The capital efficiency of these deals was extraordinary: IHG was essentially acquiring the right to manage other people's hotels and collect fees from them, without buying a single room or a single parcel of land.

Consider what $339 million buys you in luxury hotel real estate: perhaps a single trophy property in a prime location. Instead, IHG used that same capital to acquire two entire brand platforms with properties across dozens of countries and a pipeline of future openings that would generate fees for decades. This is the asset-light model applied to M&A itself—buying brands and management contracts, not bricks and mortar.

The contrast with Hyatt's acquisition strategy is instructive. In late 2021, Hyatt acquired Apple Leisure Group for approximately $2.7 billion, a deal focused on acquiring volume in the all-inclusive resort segment. It was a bet on mass-market scale and distribution. IHG, by contrast, went for niche prestige with Regent and Six Senses—smaller brands with higher fee-per-room potential and stronger aspirational positioning. Different chess moves on the same board, and it will take years to know which bet pays off more handsomely.

IHG found yet another creative way to grow without writing a large acquisition check. In November 2022, IHG and the Iberostar Group—a family-owned Spanish hospitality company founded by the Fluxá family, known for its all-inclusive resorts across the Mediterranean and Caribbean—announced a strategic alliance.

Rather than acquiring Iberostar outright, IHG structured the deal as a partnership: Iberostar's properties would be co-branded with IHG brands, plugging into the IHG reservation system and loyalty program for distribution while retaining the Iberostar identity and operational expertise in the all-inclusive format. It was a capital-free way to expand IHG's presence in one of the fastest-growing niches in leisure travel, without the integration complexity and financial commitment of an outright acquisition.

The deal was signed by Keith Barr, then IHG's CEO, alongside Sabina Fluxá, Iberostar's Vice-Chairman and CEO. For IHG, it represented a new model of growth—a "system-wide" partnership that expanded the network and made the loyalty program more valuable to members, all without requiring either an acquisition premium or a traditional franchise agreement.

The Iberostar alliance also demonstrated something important about IHG's M&A philosophy. While competitors like Marriott pursued transformational mega-mergers—the $13 billion Starwood acquisition being the defining example—IHG consistently preferred smaller, more targeted moves. Kimpton for lifestyle. Regent for Asian ultra-luxury. Six Senses for wellness. Iberostar for all-inclusive. Each deal filled a specific gap in the portfolio without bet-the-company risk or the massive integration challenges that accompany billion-dollar mergers. It was M&A as precision surgery rather than blunt-force consolidation.

By the mid-2020s, IHG's brand portfolio had been completely transformed from the Holiday Inn-centric company that emerged from the Six Continents demerger. The question was whether the management team could execute on this expanded portfolio while maintaining the operational discipline that made the asset-light model work. That question landed squarely on the desk of a new CEO.

V. Management: The Elie Maalouf Era (1:25:00 - 1:45:00)

In the summer of 2022, Keith Barr, IHG's CEO since 2017, received a diagnosis that would alter the course of the company's leadership. Barr had steered IHG through the most harrowing period in the modern history of the hospitality industry—the COVID-19 pandemic—and had overseen the Six Senses acquisition, the Iberostar alliance, the launch of IHG One Rewards, and a steady cadence of capital returns to shareholders.

Barr was Australian by birth, a career hotelier who had joined IHG in 2000 and worked his way through the ranks. His style was strategic but approachable—insiders described him as someone who could hold his own in a boardroom discussion about EBITDA multiples and then walk a hotel kitchen asking the chef about plate presentation. When Keith Barr passed away in November 2023, the hospitality industry lost one of its most respected leaders, and the tributes from competitors were genuine, not perfunctory.

The succession had been carefully planned. In July 2023, IHG announced that Elie Maalouf would become Chief Executive Officer, effective immediately. Maalouf was not an outsider parachuted in from a different industry. He had spent over five years as CEO of IHG's Americas division—the company's largest and most profitable region, responsible for well over half of IHG's total fee revenue, encompassing thousands of hotels stretching from Toronto to São Paulo.

Maalouf's background reveals a great deal about what kind of company IHG intends to be going forward. Before joining IHG, he had spent more than two decades in senior hospitality and real estate roles, including positions at Rosewood Hotels & Resorts—itself an ultra-luxury brand—and various real estate development firms.

He understood the hotel business not just from the franchisor's side of the table, but from the owner's side. He knew what made a hotel developer commit tens of millions of dollars to build a property under a particular flag, because he had sat in those meetings himself. That perspective—knowing what the franchisee needs, not just what the franchisor wants—is invaluable in a business where growth depends entirely on convincing independent entrepreneurs to invest their own capital under your brand name.

The board's choice of Maalouf sent a clear signal to the market: this was not a pivot. It was an acceleration. Maalouf had overseen the Americas region during its strongest period of net unit growth, signing hundreds of new franchise agreements and deepening IHG's penetration in the US select-service market. His style is pragmatic and data-driven—less visionary speechmaker than disciplined executor.

In his early public remarks as CEO, Maalouf emphasized continuity, pointing to the luxury and lifestyle pipeline, the technology investments, and the loyalty program as the three pillars of the growth strategy. There was no dramatic "new era" proclamation. The strategy was working; the job was to execute faster.

Maalouf's compensation structure reinforces this focus. IHG's Long-Term Incentive Plan ties a significant portion of executive pay to two key performance metrics: earnings per share growth and net system size growth—meaning the net number of rooms added to the IHG system each year after accounting for hotels that leave the system. These are not vanity metrics. They are direct proxies for the two things that drive long-term value creation in an asset-light hotel company.

The insider transaction records filed with the SEC provide an additional lens into management conviction. Throughout 2024 and into early 2025, Maalouf and several board members—notably Byron Grote, the senior independent director and former BP executive—purchased IHG shares in the open market with their own money.

Maalouf made purchases at prices around $121 per ADR share. Grote was more prolific, buying at prices ranging from $92 to $127 over multiple transactions. Board member Deanna Oppenheimer made a notable $190,000 purchase at around $95 per share. These are voluntary, open-market purchases that suggest genuine conviction from the people closest to the business.

Perhaps the most important cultural shift under Maalouf has been the acceleration of IHG's luxury and lifestyle ambitions. Under Barr, the company acquired the brands—Kimpton, Regent, Six Senses. Under Maalouf, the focus has shifted decisively from "acquiring the platforms" to "filling the pipeline."

The luxury and lifestyle segment now represents the fastest-growing portion of IHG's new hotel signings. The strategic objective is explicit: luxury hotels generate substantially higher fees per room than midscale properties, so every Regent or Six Senses that opens lifts the company's blended fee-per-room metric, driving fee revenue growth even without heroic assumptions about total room additions.

The transition from Barr to Maalouf also marked a subtle but consequential cultural evolution. Insiders describe a pivot from a "process-driven" organization—one that excelled at standardizing the Holiday Inn Express check-in experience—to one that is increasingly "brand-experience-driven."

The distinction matters deeply in the luxury segment. A process-driven culture asks: how do we get the check-in time down to three minutes? A brand-experience-driven culture asks: does the Six Senses welcome ritual—the cool towel, the essential oil, the personalized greeting—create a genuine emotional connection that the guest will remember and share? Both approaches matter, but the balance has shifted as IHG's portfolio tilts upmarket.

There is one additional dimension of the management story worth noting: succession depth. IHG's smooth transition from Barr to Maalouf—in circumstances that were tragic and not fully anticipated—speaks to the quality of the board's governance and succession planning. Too many companies treat CEO succession as a crisis to be managed when it arrives. IHG, by developing Maalouf in the Americas CEO role for years before elevating him, ensured that the transition was orderly, the strategy continued without interruption, and the market's confidence was maintained. The share price barely flinched during the transition—a remarkable outcome given the circumstances.

The management story is incomplete, however, without understanding the hidden infrastructure that makes the entire franchise machine work—the technology and loyalty systems that represent IHG's true competitive moat.

VI. The "Hidden" Business: The Tech and Loyalty Engine (1:45:00 - 2:05:00)

If you want to understand why IHG's business model actually works—why thousands of independent hotel owners around the world voluntarily pay IHG a percentage of their revenue every single day—forget about hotels for a moment and think about software platforms.

Consider Shopify. Shopify does not sell products. It provides the technology platform, the payment processing, the marketing tools, and the distribution network that allows independent merchants to run their businesses more effectively than they could on their own. The merchants pay Shopify a subscription fee and a percentage of their sales. In return, they get infrastructure they could never build themselves.

Or think about it another way: IHG is to hotel owners what the App Store is to app developers. Apple does not write most of the apps; independent developers do. But Apple provides the platform, the distribution, the payment processing, and the customer base. In return, Apple takes a percentage of revenue. The developers could theoretically distribute their apps independently, but the friction and cost of doing so makes the App Store's cut worthwhile. IHG's franchise model operates on the same principle, at a different scale and in a different industry.

IHG operates on a remarkably similar logic. It does not sell hotel rooms. It provides the technology platform, the reservation system, the loyalty program, the marketing muscle, and the global distribution network that allows independent hotel owners to fill rooms more effectively than they could alone. The owners pay IHG franchise fees. In return, they get infrastructure they could never build themselves.

This analogy is not just metaphorical. IHG has invested hundreds of millions of dollars over the past decade to build a technology stack that would be recognizable to any Silicon Valley engineer.

The centerpiece is the Guest Reservation System, known as GRS, built in partnership with Amadeus, the world's leading travel technology provider. In April 2015, IHG announced this landmark partnership to develop a next-generation, cloud-based reservation platform that would replace HOLIDEX—IHG's proprietary reservation system that dated back to the 1960s and was, by twenty-first-century standards, a technological relic.

To appreciate the significance of this upgrade, consider what HOLIDEX was. Built in the era of mainframe computers and teletype machines, HOLIDEX was revolutionary when Holiday Inn first deployed it—one of the first real-time hotel reservation systems in the world. But by 2015, it was like running a modern airline on a system designed for telegram booking. It lacked the flexibility, the data analytics capability, and the cloud-based scalability that the modern hospitality industry demanded.

GRS was designed from the ground up as a cloud-native platform, modeled on the system Amadeus had built for the global airline industry. When a guest books a room at a Holiday Inn Express in Des Moines through the IHG app at midnight, that transaction flows through GRS in real time. When a travel agent in Tokyo books a suite at the InterContinental Bali through the Amadeus global distribution network, that transaction also flows through GRS.

When a corporate travel manager at Goldman Sachs or McKinsey negotiates preferred rates for fifty thousand room-nights at Crowne Plazas across twelve countries, those rates are managed and tracked through GRS. The system handles dynamic pricing, real-time inventory management, distribution to online travel agencies, direct-channel optimization, and revenue management analytics. It is, in effect, the operating system that runs every IHG-flagged hotel on the planet.

For hotel owners—the franchisees who are IHG's true customers—GRS is a massive part of the value proposition. An independent hotelier in Chengdu cannot build a cloud-based, globally distributed reservation system. A boutique hotel operator in Barcelona cannot negotiate preferred distribution rates with Booking.com or Expedia. But by joining the IHG system, they plug into all of this infrastructure instantly. The cost to replicate it independently would be hundreds of millions of dollars.

This is what makes the franchise relationship so sticky—and stickiness, as any investor knows, is the foundation of recurring revenue.

To put it in simple terms: imagine you run a small restaurant. You could handle your own bookings, manage your own website, run your own marketing, and negotiate with Uber Eats independently. Or you could join a franchise system that does all of that for you, at a scale and sophistication you could never achieve alone, in exchange for a percentage of your revenue. That is essentially what IHG offers hotel owners, except the technology is more complex, the global distribution network is more vast, and the switching costs are far higher.

IHG also functions as what might be called a "SaaS provider to its own franchisees"—it provides software-as-a-service tools for property management, revenue optimization, guest communication, and operational benchmarking. Hotel owners do not just get a sign on their building; they get an entire technology ecosystem that makes their business more efficient and more profitable than it would be as an independent operation. The deeper a hotel owner integrates into this ecosystem, the harder it becomes to leave.

Now layer on the loyalty program, and the picture becomes even more compelling. IHG One Rewards, relaunched under that name in 2022, boasts over 130 million enrolled members globally. To put that number in context, it is roughly equivalent to the entire population of Japan.

Not all of these members are active high-frequency travelers—loyalty programs always have a long tail of casual members. But the active core is enormous, and the program drives a substantial percentage of IHG's total room nights booked through direct channels.

The 2022 relaunch as IHG One Rewards was more than a name change. It represented a fundamental redesign of the program's tier structure, earning rates, and redemption mechanics, aimed at making the program more competitive with Marriott Bonvoy and Hilton Honors. The revamped program introduced more generous earning rates for higher-tier members, milestone bonuses for frequent stayers, and expanded partnerships with airlines and credit card issuers that allow members to earn and burn points outside of hotel stays. The underlying strategic goal was to make IHG One Rewards the program that travelers think of first when choosing where to stay—not an afterthought behind the larger competitors' programs.

The economics of this direct-booking engine are critical and often underappreciated. When a guest books a hotel room through Expedia or Booking.com, the hotel typically pays a commission that ranges from fifteen to twenty-five percent of the room rate. On a $200 room night, that is $30 to $50 going to the online travel agency rather than to the hotel owner.

When the same guest books directly through the IHG app or website because they want to earn or redeem loyalty points, that commission drops to effectively zero. The loyalty program is a massive direct-booking engine that reduces the entire IHG system's dependence on expensive third-party distribution. Every member added to IHG One Rewards is another guest who is more likely to book direct, more likely to choose an IHG property over a competitor, and more likely to pay a modest rate premium for the familiarity and the points.

There is a deeper strategic layer here that goes beyond booking economics. The loyalty program generates an enormous volume of first-party data—booking patterns, travel preferences, spending behavior, geographic tendencies—that IHG uses to optimize pricing, personalize marketing offers, and advise hotel owners on everything from staffing levels to renovation priorities. In an era when first-party data is becoming increasingly valuable, IHG One Rewards represents a proprietary data asset that grows more valuable with every transaction.

Now consider how these engines power IHG's two primary business segments. The first is what the company calls its Essentials segment: Holiday Inn and Holiday Inn Express. Together, these two brands account for the vast majority of IHG's global room count. They are the workhorses, the high-volume engine that funds the technology investments, marketing campaigns, and loyalty program infrastructure that benefit the entire portfolio.

Holiday Inn Express, in particular, is a franchising machine. It is a stripped-down, highly efficient hotel format—limited food and beverage, focused amenities, standardized design—that hotel developers love because it is relatively cheap to build and remarkably reliable to operate. It fills a fundamental need: a clean, predictable, reasonably priced room with a free breakfast, located near an airport, a highway interchange, or a business park. It is not glamorous, but it is enormously profitable.

The genius of the Holiday Inn Express format—and this is something that is easy to overlook—is that it is optimized not just for the guest but for the hotel owner. The limited-service format means fewer employees per room, lower food and beverage costs (breakfast is the only meal), simpler operations, and more predictable margins. A well-run Holiday Inn Express can generate occupancy rates above seventy percent consistently, with operating margins that make it one of the most attractive franchise investments in hospitality. This is why Holiday Inn Express consistently leads IHG's new franchise signings: developers build them because they work financially.

The second segment is Luxury and Lifestyle: InterContinental, Six Senses, Kimpton, Regent, Vignette Collection, and Hotel Indigo. This is the growth engine. These brands represent a much smaller share of total rooms but a disproportionate share of fee revenue growth, because luxury hotels command dramatically higher average daily rates and therefore generate higher fees per room for IHG.

A single Six Senses resort with eighty villas might generate as much annual fee revenue for IHG as a Holiday Inn Express with two hundred and fifty rooms, because the average nightly rate at a Six Senses can be five to ten times higher. The math is compelling: as the luxury portfolio grows from its current small base, IHG's blended fee-per-room metric rises, lifting total fee revenue even if the absolute number of new rooms added remains steady.

For investors trying to track this business with precision, two key performance indicators matter above all others—and everything else is noise.

The first is net system size growth—the rate at which IHG adds new rooms to its global system, net of removals. This is the single most important leading indicator of future fee revenue because each room added to the system generates fees for IHG for the life of the franchise agreement, which typically spans fifteen to twenty years. A slowdown in net system size growth does not just affect next quarter's revenue—it affects the entire future trajectory of the business. Industry observers typically watch for consistent mid-single-digit percentage growth as a sign that the franchise machine is humming. Anything above five percent is strong; anything below three percent warrants scrutiny.

The second is RevPAR growth (revenue per available room), which measures the average revenue generated per available room across the entire IHG system. For readers unfamiliar with this metric, think of it this way: if a hotel has 100 rooms and sells 70 of them at an average price of $150 per night, the RevPAR is $105 (70% occupancy times $150 rate). RevPAR combines both occupancy rate and average daily rate into a single number, making it the best proxy for the underlying demand environment facing hotels.

When RevPAR grows, IHG's fee revenue grows almost mechanically, because IHG earns a percentage of what each hotel takes in. Conversely, when RevPAR declines—during recessions or travel disruptions—IHG's fees decline proportionally. RevPAR is the weather report for the hotel industry, and IHG's fortunes are inextricably tied to it.

Together, these two metrics—system size and RevPAR—capture the franchise pipeline's health and the demand environment's trajectory. Everything else is commentary.

VII. Playbook: Hamilton's 7 Powers and Porter's 5 Forces (2:05:00 - 2:25:00)

Understanding whether IHG's competitive advantages are durable—whether this is a true long-term compounder or a well-managed company riding cyclical tailwinds—requires moving beyond the financial statements and asking a harder question: what structural forces protect IHG's ability to earn above-average returns, and how resistant are those forces to erosion?

Two frameworks are particularly useful here. Hamilton Helmer's Seven Powers identifies the sources of persistent differential returns—the structural advantages that allow a company to earn returns above its cost of capital not for a quarter but for decades. Michael Porter's Five Forces framework examines the competitive environment to determine whether industry structure supports or undermines profitability.

Start with Helmer's framework.

Scale Economies are perhaps IHG's most obvious advantage. The global distribution system—the technology infrastructure, the GRS platform, the corporate sales team, the marketing spend, the loyalty program administration—represents an enormous fixed cost base spread across more than 6,300 hotels and nearly one million rooms.

Each additional hotel that joins the IHG system adds incremental fee revenue while adding almost no incremental cost to the central platform. The marginal cost of connecting one more Holiday Inn Express to GRS is negligible. A franchisee joins IHG not because they admire the corporate headquarters, but because they cannot fill rooms on their own at acceptable rates.

They need the booking engine, the 130 million loyalty members, the corporate travel contracts, the online travel agency negotiations, the brand recognition that makes a road-weary traveler pull off the highway into their parking lot instead of the independent motel next door. IHG can offer all of this at a marginal cost that no independent hotel or small regional chain can match. This scale advantage is self-reinforcing: the larger the system, the more valuable it is to each individual hotel.

Network Effects operate on a similar flywheel logic. More hotels in the system means more geographic coverage and more choices for loyalty members, which attracts more members to the program, which drives more bookings to existing hotels, which makes the IHG flag more attractive to prospective hotel developers, which brings more hotels into the system.

This is not as explosive as the network effects that propel social media platforms—nobody joins IHG One Rewards because their friends are members—but it is powerful and durable in the B2B context. A hotel developer in Vietnam evaluating whether to flag a new property as a Holiday Inn or an independent brand will look at IHG's 130 million loyalty members and compare that to the empty CRM database of a no-name alternative. The math is self-evident.

Switching Costs are the third and perhaps most underappreciated structural advantage. Once a hotel owner has flagged their property as a Holiday Inn, signed a franchise agreement that typically runs fifteen to twenty years, installed the IHG signage, integrated into the GRS reservation system, trained staff on IHG brand standards, and begun accepting IHG One Rewards members, the cost of "de-flagging" is substantial.

It involves not just removing signage and renovating to meet a different brand's standards, but losing the IHG reservation feed (which may represent a significant share of total bookings), disrupting corporate travel accounts, alienating loyal IHG members, and navigating the legal complexity of terminating a long-term franchise agreement. These switching costs create a "sticky" franchise base with low annual attrition, meaning IHG's existing revenue stream is highly predictable and recurring.

Now turn to Porter's Five Forces.

Threat of New Entrants is low. Building a global, multi-segment hotel brand platform from scratch is extraordinarily difficult. The barriers are not about capital for real estate—this is asset-light. The barriers are brand building, technology infrastructure, loyalty program scale, and the decades of investment needed to establish trust relationships with hotel developers worldwide.

A new entrant faces a brutal chicken-and-egg problem: owners will not sign franchise agreements with an unknown brand because it cannot drive bookings, and the brand cannot drive bookings without hotels in its system. New lifestyle brands do emerge in the boutique space, but building a comprehensive global platform comparable to IHG, Marriott, or Hilton would require billions of dollars and decades of execution.

Threat of Substitutes—here we must discuss Airbnb. The short-term rental platform has undeniably disrupted certain segments of the hotel industry, particularly in leisure destinations where guests value unique, apartment-style accommodations. But the disruption has been profoundly uneven.

Business travelers overwhelmingly prefer branded hotels for consistency, security, loyalty benefits, and expense-report simplicity. The midscale segment—Holiday Inn Express territory—serves a utilitarian need that Airbnb addresses poorly: a clean room near the airport with standardized breakfast and three-minute check-in. And at the ultra-luxury end, guests are paying for full-service hospitality—twenty-four-hour concierge, spas, Michelin-level dining—that no apartment rental can replicate.

IHG's portfolio, anchored at the midscale and expanding at the luxury end, is structurally well-positioned against the Airbnb threat precisely because it occupies the segments least vulnerable to short-term-rental substitution.

Bargaining Power of Buyers is where the loyalty program pays its most important strategic dividends. The most powerful "buyers" in the hotel industry are not individual travelers but the online travel agencies—Expedia, Booking.com, and their subsidiaries—that aggregate demand and charge hotels commissions of fifteen to twenty-five percent per booking.

A hotel with a weak brand and no loyalty program is at the mercy of these platforms. IHG's 130-million-member loyalty program directly counteracts this power by driving a large percentage of bookings through IHG's own direct channels, where no third-party commission is paid.

Bargaining Power of Suppliers is modest. IHG's "suppliers" are the hotel owners who provide the physical product. These owners need IHG's brands and distribution more than IHG needs any individual property. The franchise agreements are long-term, the switching costs are high, and IHG has thousands of hotels, so no single owner has meaningful leverage.

That said, in competitive development markets—Greater China, India, Southeast Asia—where high-quality hotel developers have multiple franchise options from Marriott, Hilton, Hyatt, and Accor, IHG must compete aggressively on franchise terms and technology investment to win the best locations.

Competitive Rivalry among the major global hotel companies is intense but disciplined. The industry has consolidated dramatically, with IHG, Marriott, Hilton, Hyatt, and Accor accounting for the vast majority of branded rooms worldwide. Competition for new franchise signings is fierce, but competitors have generally avoided destructive price wars on franchise fee percentages.

The rivalry plays out through brand innovation, technology investment, loyalty program value, and geographic expansion—a structure that is inherently healthier for long-term returns than direct price competition.

To put IHG in competitive context: Marriott operates roughly 1.6 million rooms across 30-plus brands, making it by far the largest system in the world. Hilton operates about 1.2 million rooms across 22 brands. IHG, with its roughly 950,000 rooms across 19 brands, is the third largest. Hyatt, with around 300,000 rooms, is meaningfully smaller. In Europe and Asia, the French company Accor is a significant competitor, though its business model is somewhat different, retaining more owned and leased properties.

IHG's relative position is interesting: it is large enough to have genuine scale economies and a world-class loyalty program, but small enough relative to Marriott that it still has meaningful room to grow. Some investors view IHG as the "Goldilocks" player in the industry—big enough to matter, small enough to still have a long runway for system growth.

It is also worth noting an element that does not fit neatly into either Helmer or Porter frameworks but matters enormously: brand architecture. IHG's ability to offer a hotel developer a brand for almost any segment—from the $80-a-night Holiday Inn Express to the $2,000-a-night Six Senses villa—means it can capture development opportunities across the entire price spectrum. A developer who starts with a Holiday Inn Express and has a good experience with IHG's franchise support system may later build a Crowne Plaza or an InterContinental. This "land and expand" dynamic within IHG's own developer relationships is a subtle but powerful growth driver.

VIII. Bear vs. Bull Case and The Future (2:25:00 - 2:45:00)

Every investment thesis has two sides, and a clear-eyed assessment of IHG requires confronting both honestly. The company's strengths are real and well-documented, but so are its vulnerabilities. The question for investors is not whether IHG is a good business—it clearly is—but whether the current price adequately compensates for the risks.

The Bull Case rests on the power of compounding in a capital-light, fee-based model with structural tailwinds.

Consider the arithmetic. IHG has delivered consistent mid-single-digit net system size growth, meaning the installed base of rooms generating fees expands every year. Layer on RevPAR growth—driven by inflation in room rates, improving occupancy, and the secular shift toward branded hotels in developing markets—and total fee revenue compounds in the high single digits in a normal economic environment.

Now add operating leverage: IHG's cost base does not grow proportionally with fee revenue, so a significant portion of incremental revenue drops straight to the operating income line.

Finally, layer on the share buyback program. IHG returned roughly $800 million through buybacks in 2024 alone, and the share count has shrunk from approximately 181 million in 2022 to around 151 million by early 2026—a reduction of nearly seventeen percent in four years. The trifecta of organic revenue growth, margin expansion, and a shrinking share count creates a powerful compounding engine.

The China opportunity is central to the bull case. Greater China represents IHG's second-largest market after the Americas, with hundreds of hotels already open and a substantial pipeline under development. China's domestic travel market is enormous—over two billion domestic trips per year—and branded hotel penetration is significantly lower than in the United States, where the major chains dominate.

IHG has a genuine first-mover advantage among Western hotel companies in China, having entered decades ago when most competitors were still focused on North America and Europe. The Holiday Inn and Crowne Plaza brands carry meaningful recognition among Chinese domestic travelers—a valuable asset that took years to build.

The China opportunity also extends beyond the Essentials brands. As Chinese wealth grows, so does demand for luxury travel—both domestic and international. Six Senses and Regent have particular resonance in the Asian luxury market, where wellness tourism and heritage hospitality brands command premium pricing. IHG's ability to offer Chinese hotel developers a brand for every segment—from a Holiday Inn Express near a high-speed rail station to a Six Senses resort in a scenic national park—gives it a competitive flexibility that few rivals can match in this specific market.

The luxury pipeline adds another dimension. Six Senses, Regent, and Kimpton are opening new properties at an accelerating pace, each one generating fees per room that are multiples of the IHG system average. As this segment grows from its current small base, it progressively lifts the company's blended fee-per-room metric—the "mix shift" argument that acts as a margin accelerator even without heroic assumptions about total room growth.

The Bear Case is not about the business model breaking. The asset-light franchise model has proven its resilience through two severe crises. The bear case is about the external environment turning hostile.

The most immediate risk is a global travel recession. Hotels remain cyclical—there is no escaping that reality. A severe US recession would compress RevPAR as business travel budgets are slashed, conference attendance drops, and leisure travelers trade down to cheaper accommodation or cancel trips entirely. Fee revenue would decline because IHG earns a percentage of what each hotel takes in, and when hotels earn less, IHG earns less.

New hotel development would slow as owners become cautious about committing capital to construction projects in an uncertain environment, which would dampen the net system size growth that drives long-term compounding. IHG's earnings would decline, and the stock—trading at a premium multiple reflecting expectations of steady compounding—would likely re-rate lower as the market prices in a slower growth trajectory.

Geopolitical risk in Greater China is more structural and harder to hedge against. The relationship between China and Western governments has grown increasingly fraught, with trade tensions, technology restrictions, and political friction creating persistent uncertainty for companies with significant China exposure.

For IHG, the risks are multi-layered: currency controls could make fee repatriation difficult; regulatory shifts could impose onerous conditions on foreign hotel brands; rising nationalism could lead to consumer preference for domestic hotel chains over Western brands; and in an extreme scenario, travel restrictions or diplomatic tensions could directly curtail the cross-border tourism flows that luxury hotels depend on. A forced retreat from Greater China—however unlikely—would significantly impair IHG's long-term growth narrative, given the size and importance of this market to the company's pipeline.

The loyalty and technology arms race represents a different kind of risk. All four major hotel companies are pouring hundreds of millions annually into loyalty programs and technology platforms. The logic is sound, but there is a risk that loyalty programs become table stakes rather than differentiators—that travelers simply join all four programs and book on price or location, negating the competitive advantage the programs are supposed to create. If that happens, the spending becomes a cost of doing business rather than a source of advantage.

There is also the valuation question. IHG trades at roughly nineteen times forward earnings and approximately nineteen times enterprise value to EBITDA. These multiples are not extreme for quality franchise businesses, but they leave limited margin of safety if growth disappoints or the macro environment deteriorates.

For investors evaluating IHG, the assessment reduces to a judgment about durability. Can this franchise machine keep adding rooms consistently for the next decade? Can RevPAR growth persist? Can the luxury pipeline deliver the fee uplift management projects?

The two metrics to watch remain net system size growth and RevPAR growth. Together, they capture the franchise pipeline's health and the demand environment's trajectory. If both remain positive and stable, the compounding machine keeps running. If either falters, it will be time to reassess.

One myth worth addressing directly: the notion that IHG is "too small to compete" with Marriott and Hilton. This narrative surfaces periodically in analyst notes and investor forums, and it misunderstands the competitive dynamics of the industry. In branded hospitality, being the third-largest system is not like being the third-largest smartphone manufacturer—a position that typically leads to margin compression and irrelevance. Hotel franchising is not a winner-take-all market. Developers and owners want options; they want to be able to play franchise companies against each other when negotiating terms. A developer who already has fifteen Marriotts in their portfolio may actively prefer to diversify by building a Holiday Inn or a Crowne Plaza. IHG's scale is more than sufficient to deliver compelling economics to franchisees, and its focused brand architecture—fewer brands, each with a clearer identity—arguably makes it easier for developers to understand what they are buying into compared to Marriott's sprawling portfolio of over thirty brands, some of which overlap in confusing ways.

IX. Epilogue and References (2:45:00 - End)

In early 2024, IHG announced an $800 million share buyback program, continuing its two-decade tradition of returning surplus capital to shareholders. The buyback progressed through 2024 and into 2025, with the share count shrinking steadily—from roughly 181 million shares outstanding in 2022 to around 151 million by early 2026.

That reduction of nearly seventeen percent in the share base over four years is itself a powerful compounding mechanism, concentrating future earnings growth onto a smaller denominator and amplifying per-share returns even in years of modest underlying business growth.

The company's most recent audited financial results tell the story of a machine operating at full capacity. For the fiscal year ending December 2025, IHG reported total revenue of approximately $5.2 billion, up from $4.9 billion the prior year. EBITDA reached approximately $1.45 billion. Net income came in at $759 million, translating to earnings per diluted ADR share of roughly $4.87—a record.

Operating cash flow was approximately $898 million, more than sufficient to fund the company's ongoing technology investments, loyalty program costs, and dividend obligations while still leaving substantial room for share repurchases.

The balance sheet carries about $4.6 billion of gross debt against $1.1 billion of cash, resulting in net debt of approximately $3.5 billion, or roughly 2.4 times trailing EBITDA. That leverage ratio is manageable for a company with IHG's cash flow characteristics, though it bears watching in a rising-rate environment or a downturn that compresses EBITDA.

One accounting nuance deserves flagging for the careful investor. IHG's balance sheet shows a negative book value—total liabilities exceed total assets—which might alarm someone encountering the company for the first time. This is not a sign of financial distress. It is a direct consequence of the aggressive share buybacks and special dividends that have returned more than thirteen billion dollars to shareholders since 2003, effectively depleting and then inverting the equity base. Marriott has the same dynamic. The negative book value is the arithmetical shadow of massive shareholder returns, not a red flag.

A second accounting consideration: IHG reports under IFRS, not US GAAP, which means certain items—particularly around lease accounting, revenue recognition for loyalty programs, and the treatment of system fund contributions—may look different from how Marriott or Hilton report comparable figures. The system fund, through which IHG collects and spends money on behalf of franchisees for marketing and reservation services, is a significant item that flows through IHG's revenue line but is essentially a pass-through. Investors comparing IHG's headline revenue to Marriott's should be aware of this structural difference. Fee revenue, not total revenue, is the more comparable metric across the peer group.

On the regulatory front, IHG faces no material outstanding litigation or regulatory actions that would constitute a significant overhang as of early 2026. The company operates in over 100 countries and is subject to the usual web of local regulations around franchising, data privacy, labor law, and hospitality licensing, but none of these represent unusual or concentrated risk.

There is a broader point about IHG's capital allocation philosophy that bears emphasis. The company operates with a clear hierarchy: first, invest in the business—technology, brand standards, loyalty program enhancements—to protect and grow the fee stream. Second, pay a sustainable ordinary dividend that grows over time. Third, return all excess capital to shareholders through buybacks. This hierarchy is not unusual, but IHG executes it with a discipline and consistency that few FTSE 100 companies match. There is no empire-building through overpriced acquisitions, no diversification into unrelated businesses, no vanity projects. Every pound of free cash flow that is not needed to sustain the franchise machine gets returned to shareholders. For investors who value capital discipline, IHG's track record is compelling.

The insider buying pattern provides a final data point. When the people running a company—the CEO, the board members—consistently buy shares with their own money in the open market at prices above one hundred dollars per share, it signals conviction that no analyst report can replicate.

The IHG story is, at its heart, a story about what happens when a company decides to stop being all things and start being the best at one thing. Bass Brewery tried to be a beer company, a pub company, a restaurant company, and a hotel company all at once, and the result was a conglomerate discount that obscured the value of its parts.

When the hotels were finally separated and freed to pursue their own destiny—to sell the bricks, keep the brands, invest in technology, and return the excess capital—the result was one of the most successful strategic transformations in British corporate history. A company that once brewed ale in the English Midlands became a global platform business generating over a billion dollars a year in EBITDA from the licensing of brands, the operation of technology systems, and the cultivation of traveler loyalty.

What began with a Bass Ale and a Memphis motel has become something its founders could never have imagined: a borderless, asset-light platform that earns fees from nearly a million hotel rooms in over 100 countries, run by a workforce that does not clean a single room or cook a single breakfast.

IHG is not in the business of selling rooms. It is in the business of selling trust to owners and memories to travelers. Whether that business continues to compound—and at what rate—remains the open question that makes it worth watching.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube