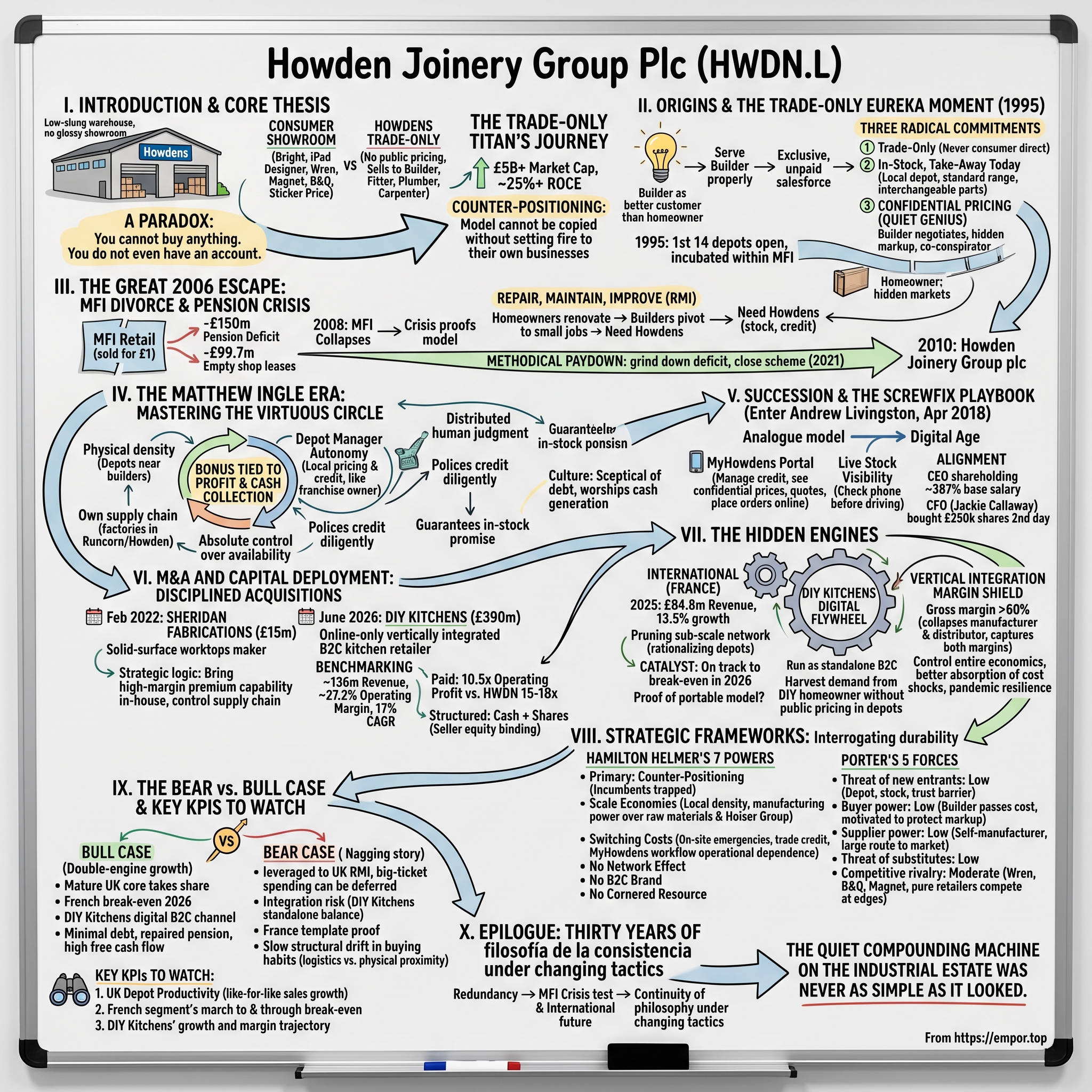

Howden Joinery Group Plc (HWDN.L): The Trade-Only Titan

I. Introduction & The Core Thesis

Drive through almost any light-industrial estate in Britain — the kind of place flanked by tyre fitters, MOT garages, and a Greggs van — and you will eventually pass a low-slung warehouse with a blue sign reading "Howdens." There is no glossy showroom out front. There are no prices in the window. In fact, if you are an ordinary member of the public who wanders in hoping to buy a kitchen, you will be politely turned away. You cannot buy anything. You do not even have an account.

And yet this company, which goes out of its way to refuse the general public, has quietly become one of the most profitable and durable businesses in the FTSE 100, with a market capitalisation comfortably above £5 billion and a Return on Capital Employed that has routinely sat north of 25%.1112 How on earth does that happen?

Here is the paradox at the heart of the story. When you decide to renovate your kitchen, you probably picture the experience the way the consumer brands have trained you to picture it: a bright showroom, a friendly designer with an iPad, a Wren or a Magnet or a B&Q with shiny worktops under warm lighting and a sticker price you can haggle down. That is the part of the industry the public sees. But the part of the industry that actually mints money is the part the public never sees at all. Howden Joinery does not sell to you. It sells to the person you hire — your local builder, your kitchen fitter, your plumber, your jobbing carpenter.

That single design decision — sell only to the trade, never to the homeowner — is the spine of this entire episode. It is, in the language of strategy, a textbook case of "Counter-Positioning": Howdens built a model that its most obvious competitors cannot copy without setting fire to their own businesses. A retailer whose entire existence depends on luring consumers into showrooms with advertised prices physically cannot pivot to a secretive, trade-only, no-public-pricing model. The moment they tried, they would alienate the very customers who pay their rent. Howdens turned the local builder into its exclusive, unpaid salesforce, its installation arm, and — crucially — its credit-underwriting partner, all at once.

Over the next four hours we are going to unpack how this happened. We will start in 1995 with a redundant kitchen executive named Matthew Ingle and a contrarian idea. We will live through the white-knuckle 2006 separation from the collapsing furniture giant MFI, and the terrifying inheritance of a £150 million pension deficit and a pile of toxic property leases that very nearly sank the whole thing.[^10] We will watch the founder hand the keys to a digital-era CEO poached from Screwfix. We will benchmark two of the most disciplined acquisitions in recent UK retail history — including the £390 million blockbuster purchase of online kitchen champion DIY Kitchens, announced just two weeks ago.45 And we will dig into the hidden, hyper-profitable engines — France, vertical manufacturing, and a digital flywheel — that will likely power the next decade.

Before we dive in, it's worth sitting with just how unusual the financial profile is, because the numbers are what force you to take the story seriously rather than dismissing it as a quirky niche operator. A Return on Capital Employed in the mid-twenties means that for every pound the company ties up in depots, factories, inventory, and working capital, it generates roughly a quarter of that back in operating profit every single year. Most retailers would be thrilled with low teens. To clear 25% consistently, across cycles, in a business that physically holds vast amounts of stock, is the kind of figure that usually signals one of two things: either an accounting illusion, or a genuinely structural advantage. In Howdens' case, as we'll see, it's the latter — and the source of that advantage is precisely the counterintuitive refusal to sell to you and me.

There's a deeper lesson lurking here for the long-term investor, which is that the best moats are often invisible from the high street. The businesses that generate the most durable excess returns are frequently the ones the public never directly interacts with — the component maker, the distributor, the trade supplier — because being out of the consumer's sightline often means being out of the consumer's price-comparison reflex too. Howdens took that principle and made it the foundation of everything.

This is a story about a company that won not through flash, but through one of the most ruthlessly aligned business models ever built in physical retail. Let's go back to the beginning — to a man who got fired, and decided the entire industry had it backwards.

II. Origins & The Trade-Only Eureka Moment

Picture a kitchen industry executive in the mid-1990s being told his services are no longer required. Matthew Ingle had spent years inside Magnet Kitchens, one of Britain's established kitchen names, when he was made redundant.[^10] For most people, redundancy is a wound. For Ingle, it was a clarifying event. Freed from the orthodoxy of the company that had employed him, he started asking a heretical question: who is actually being served badly by the way kitchens are sold?

The answer, he realised, was the builder. And the builder was the person who actually decided what kitchen got fitted.

Think about the experience of a small builder in 1995 trying to source a kitchen for a client. He walks into a consumer showroom — the same one his client might visit — and he is treated as a retail buyer. He pays something close to the retail price, which leaves him almost no margin. He waits four to eight weeks for delivery, because the showroom carries display units, not stock. When the units finally arrive, a panel is cracked or a hinge pack is missing, and now his entire job schedule has slipped, his client is furious, and he is losing money sitting around waiting for a replacement that is, itself, weeks away. The whole arrangement was built around the homeowner's leisurely shopping experience and treated the tradesperson — the person who came back to buy kitchens week after week, year after year — as an afterthought.

Ingle's insight was that this was exactly backwards. The builder was a far better customer than the homeowner. The homeowner buys one kitchen a decade, agonises over the price, and never comes back. The builder buys dozens of kitchens a year, cares far more about speed and reliability than headline price, and — this is the magic — passes the cost straight through to his own client with a markup. Serve the builder properly, and you get a repeat customer who actively wants to keep buying from you.

It's worth pausing on the psychology here, because it explains why the model is so much more than a clever distribution wrinkle. A homeowner buying a kitchen is, financially, a one-night stand. A builder is a marriage. The lifetime value of a single loyal builder — fitting kitchens week in, week out, for twenty or thirty years — dwarfs the lifetime value of any individual homeowner. And builders talk to each other. A trade that works on reputation and word of mouth means that winning over one respected local builder can pull a whole network of his peers along with him. Ingle understood that he wasn't selling kitchens; he was recruiting a distributed, self-interested, self-replicating salesforce that he would never have to put on payroll.

So Ingle built a model around three radical commitments. First, trade-only: never sell directly to a consumer, full stop. Second, in-stock, take-away today: keep the cabinets and standard doors physically sitting in a local depot, so the builder could walk in, load his van, and fit the kitchen that afternoon — no four-week wait, no slipped schedule. Third, and most subtly powerful, confidential pricing: every builder negotiates his own local discount with the depot manager, and those prices are never published. The builder buys at a trade price and quotes his client whatever he likes, pocketing a protected, invisible markup the homeowner can never benchmark against an online list.

That third pillar is the quiet genius. By hiding the price, Howdens didn't just give the builder a discount — it gave him a secret. The builder's margin became dependent on Howdens keeping that pricing opaque. Suddenly the builder wasn't just a customer; he was a co-conspirator with a vested interest in steering every client toward Howdens.

There was one more piece of design genius worth dwelling on: the product range itself was deliberately, almost stubbornly, kept simple. Rather than offering an infinite catalogue of bespoke options — the consumer showroom's instinct — Howdens standardised on a manageable range of cabinet carcasses and a wider set of interchangeable door fronts. Why does this matter? Because standardisation is what makes "in stock, take away today" physically possible. You cannot hold every conceivable bespoke configuration in a small local depot. But if the underlying cabinets are standard and only the doors vary, you can stock the components that cover the vast majority of jobs, and the builder can assemble almost any look from a finite kit of parts. The constraint that might have looked like a weakness — less choice than a high-end showroom — was actually the enabling condition for the entire speed promise.

Ingle needed capital and a corporate home to incubate this, and he found it inside the MFI Furniture Group — at the time a large, struggling consumer retail conglomerate. MFI agreed to fund the experiment, and in 1995 the first 14 Howdens depots opened their roller doors.[^10] The result was almost immediate. While MFI's consumer retail business was sliding into the structural decline that would eventually destroy it, the little trade-only offshoot grew like wildfire — a fast-compounding, cash-generative jewel buried inside a dying conglomerate.

It's one of those delicious historical ironies that the company which would later be nearly destroyed by MFI's failure could only have been born inside MFI in the first place. The conglomerate provided the patient capital, the manufacturing relationships, and the cover for a model that, in its early years, looked weird and unproven to outsiders. No standalone start-up in 1995 could easily have raised the money to open warehouses full of unsold inventory on a bet that builders would change their buying habits. The parent's deep pockets bought Howdens the runway it needed to prove the concept — and the bill for that runway, it turned out, would come due a decade later with interest.

For about a decade, that was the uneasy arrangement: a brilliant business shackled to a doomed one. Eventually, something would have to give. And when it did, in 2006, the separation would prove to be one of the most dangerous corporate manoeuvres in recent British business history.

III. The Great 2006 Escape: The MFI Divorce & Surviving the Pension Deficit Crisis

By the mid-2000s, MFI's consumer retail arm was a patient on life support. The flat-pack furniture and consumer kitchen business that had defined the brand for a generation was bleeding cash, losing relevance, and dragging down a group that, underneath, contained one of the best businesses in the country. The board faced a problem that sounds almost absurd when you say it out loud: how do you get rid of a business so toxic that someone has to be paid to take it, while keeping the hidden gem?

The answer, executed in 2006, was a kind of reverse spin-off. Rather than spinning the good business out and keeping the bad one, the group did the opposite. It sold the entire loss-making MFI Retail operation to a private equity buyer for a nominal £1 — a token sum whose only purpose was to legally transfer the burden off the balance sheet — and kept the profitable Howdens business as the surviving entity, renaming the parent Galiform plc.[^10] On paper, the bad business was gone for a pound. In reality, the price of that pound turned out to be enormous.

Here is the trap. To get the deal cleared, Galiform had to satisfy the UK Pensions Regulator, and the regulator was not about to let a fragile retail business walk away from its obligations to thousands of pensioners. So the condition of the separation was that Galiform — the Howdens side — assumed the legacy MFI defined benefit pension scheme. That scheme carried a staggering deficit of roughly £150 million, a sum that was very large indeed relative to the company's market value at the time, and the regulator gave the pension fund what amounted to "first call" on the company's assets in the event of insolvency.[^10] In plain terms: Howdens didn't just inherit a debt; it inherited a creditor that stood ahead of almost everyone else if things went wrong.

And then things went wrong. In November 2008, with the global financial crisis at full intensity, the now-independent MFI Retail business collapsed into administration.[^10] For Galiform, this was not a distant news item about a former sibling — it was a direct financial blow. Because the parent company had, in its history, guaranteed many of the leases on MFI's retail stores, the collapse triggered roughly £99.7 million in exceptional liabilities for these so-called "legacy properties," empty shops whose rent Galiform was now on the hook for, with no business inside them generating a penny.[^10] At the same time, the full weight of the pension scheme settled squarely onto Howdens' shoulders, with the dying parent no longer there to share any of it.

So here was the situation in 2008: a single trade-only kitchen distributor, freshly independent, staring down a nine-figure property liability and a nine-figure pension deficit, in the teeth of the worst financial crisis in living memory. This is the moment that would have killed a weaker business model. Instead, it became the ultimate proof of the model's resilience.

What saved them was the very counter-positioning we opened with. When the housing market crashed, big new-build projects evaporated — but homeowners who couldn't move, and couldn't afford a full new home, did the next best thing: they renovated. The phenomenon has a name in the trade: "repair, maintain, improve," and it tends to be far more resilient than new-build construction precisely because it's driven by people staying put rather than moving. When transactions freeze and prices wobble, families redirect the money they'd have spent moving into the home they already own — and the kitchen is the single most popular renovation. Builders pivoted from large builds to smaller refurbishment jobs, and for those jobs they needed exactly what Howdens offered — local stock, immediate availability, and flexible trade credit to bridge their own cash flow while they waited to be paid.

The crisis actually played to Howdens' strengths in a way that's worth making explicit, because it's the central reason the model is more defensive than it first appears. A consumer-facing showroom in a downturn faces a brutal squeeze: footfall collapses, but the expensive high-street lease and the sales staff remain. Howdens, by contrast, carried cheap industrial-estate property and a cost base that flexed with volume, and its customers actually got busier doing the small jobs that recessions create. The cash kept coming in, and management used it with discipline, systematically paying down the legacy property liabilities and pouring money into the pension hole — at times to the tune of around £2.5 million every month — until the scheme was finally closed to future accrual in 2021.10

The discipline of those years deserves emphasis because it's easy to underrate from a distance. Closing a defined benefit pension scheme to future accrual and grinding down a deficit of that size is unglamorous, multi-year, balance-sheet plumbing. There's no press release that captures the diligence of writing a £2.5 million cheque into a pension fund month after month while simultaneously honouring rent on empty shops you never wanted. But that grind is exactly what transformed Howdens from a company with a contingent existential threat hanging over it into one with a genuinely clean, low-risk balance sheet — the foundation that later made aggressive buybacks and a fat dividend possible.

Having survived the trial by fire and methodically dismantled the inherited bombs, the company performed one last act of catharsis. In 2010, it shed the awkward, transitional "Galiform" name — a name that only ever existed to mark the divorce — and rebranded as Howden Joinery Group plc, finally matching the corporate identity to the business everyone actually cared about.[^10]

The near-death experience left a permanent mark on the company's character: a deep institutional aversion to balance-sheet risk, a love of cash, and a suspicion of debt that would define its capital allocation for years. With the wreckage cleared, the founder could finally turn his full attention to perfecting the machine he had built. And perfect it he did.

IV. The Matthew Ingle Era: Mastering the Virtuous Circle

If the 2006–2010 period was about survival, the years that followed were about refinement — taking a model that worked and tuning it until it hummed. Matthew Ingle spent this era obsessing over what insiders came to call the "virtuous circle," and understanding it is the key to understanding why Howdens compounds the way it does.

Start with the physical network. Ingle's ambition was deceptively simple: put a depot within a short drive of every builder in Britain. The logic flows directly from the "take-away today" promise. That promise is only credible if the depot is close enough that driving to it is faster than waiting for a delivery. So Howdens carpeted the country with small, cheap, unglamorous depots on low-rent industrial estates — the opposite of the expensive high-street showroom real estate that consumer rivals were saddled with. Proximity wasn't a convenience; it was the entire product.

Then there is the management model, which is where Howdens gets genuinely unusual. Each depot manager is run less like a branch employee and more like a franchise owner who happens to be on the payroll. The manager has real autonomy over local pricing, over the discount struck with each individual builder, and over the credit line extended to each account. Their bonus is tied directly to the profit and the cash collection of their own depot. That last detail matters enormously. Because the manager personally feels the pain of a bad debt, they police credit with the diligence of an owner, not the indifference of a clerk. The result is a national network that behaves, at the local level, like thousands of small owner-operated businesses — each one fiercely focused on the relationships and the cash in its own postcode.

This is a subtler form of genius than it first appears, and it solves a problem that has defeated countless retail chains: the tension between scale and intimacy. Most large chains, as they grow, centralise pricing and credit decisions to control risk — and in doing so they strip the local manager of the very authority that lets them build relationships and respond to local conditions. The branch becomes a vending machine running head office's algorithm. Howdens went the other way. It pushed pricing and credit decisions down to the person who actually knows the builder, knows whether he pays on time, knows the local market — and then made that person's pay depend on getting those judgements right. It's a deliberate bet that distributed, incentivised human judgement beats centralised control in a relationship business. The trade-off is that you have to trust hundreds of managers, and you have to recruit and train people capable of running a P&L. Howdens accepted that cost because the alternative — a faceless, centralised supplier — would have forfeited the trust that is the whole point.

Now layer the confidential pricing on top, and the circle closes. Because the builder's discount is private, the builder becomes Howdens' most enthusiastic advocate. When a homeowner asks for a kitchen, the builder doesn't shop around on the client's behalf — he says, in effect, "I fit Howdens. The cabinets are good, and I can get them today." Every job becomes a sales pitch for the brand, delivered by a trusted tradesperson the homeowner is already paying to make exactly these decisions. Howdens' marketing budget is, in a real sense, the builder's own self-interest.

To make the whole thing bulletproof, Ingle insisted on owning the supply chain. The "in-stock" promise is worthless if your manufacturer lets you down, so Howdens built and operated its own large manufacturing facilities — most notably in Runcorn and at Howden itself — producing its own cabinets and doors.2 This gave the company absolute control over availability, insulating it from the external manufacturing delays that plagued rivals dependent on third parties. When you control the factory, the lorry, and the depot, you can actually guarantee the shelf is full.

A word on Ingle himself, because companies this distinctive tend to be the lengthened shadow of one person, and Howdens is unmistakably his. He was, by every account, an operator rather than a showman — plain-spoken, allergic to corporate fashion, obsessive about the unglamorous details of stock availability and depot economics, and deeply sceptical of anything that smelled of head-office empire-building. His later memoir, pointedly titled Kitchens, or Sink, captures the binary, do-or-die mentality that ran through the company's early years.[^10] That temperament left a cultural residue that outlasted his tenure: a suspicion of debt, a worship of cash generation, a contempt for vanity spending, and a belief that the depot, not the boardroom, is where the business actually happens. When you understand the man, the company's lifelong frugality and operational fixation stop looking like accidents.

By the time Ingle stepped back from the chief executive role in April 2018 after 23 years at the helm, he had built something rare: a fully optimised, cash-generative compounding machine with more than 650 UK depots, eventually taking on the role of Lifetime President as a mark of what he'd created.[^10] What he handed over was not a turnaround project. It was a finely tuned engine — one that worked so well its very excellence posed the central question of the next era. How do you improve a machine that already runs beautifully? There's a particular danger that haunts businesses inherited in pristine condition: the temptation for a new leader to justify their existence by meddling, breaking the very things that made the company great in order to leave a mark. The board's answer was to bring in someone who understood a dimension Ingle's generation had largely ignored — the digital lives of tradespeople — but who could be trusted to extend the model rather than dismantle it.

V. The Succession & The Screwfix Playbook: Enter Andrew Livingston

Succession is where great companies most often stumble. A founder-built, founder-tuned business carries its founder's instincts in its bones, and the wrong successor can spend years either breaking what worked or being too timid to change what should change. So the appointment of Andrew Livingston as chief executive in April 2018 was a genuine inflection point — and the choice was revealing.2

Howdens in 2018 was, in one sense, a masterpiece, and in another sense, oddly antiquated. It had perfected physical density and human relationships, but it was running a 2010s business on processes that hadn't fully reckoned with how tradespeople had started to live: on their phones, between jobs, checking stock and managing accounts from the cab of a van at seven in the morning. The board didn't need someone to reinvent the model. They needed someone who could drag a brilliant analogue business into the digital age without damaging its analogue soul.

Livingston was almost suspiciously well-suited to that brief. He arrived from Screwfix — the trade-focused tools and hardware retailer, part of the Kingfisher group — where he had overseen a remarkable expansion that fused physical convenience with digital ordering and click-and-collect. Screwfix's whole proposition was teaching tradespeople to order on a phone or online and pick up locally within minutes, and Livingston understood the psychology of that customer intimately: the impatience, the reliance on mobile, the way a tradesperson's day is a series of small logistical emergencies. He had, in effect, already run the playbook Howdens needed.

The neatness of the fit is almost too good. Consider what Screwfix and Howdens have in common: both sell to the trade, both rely on a dense network of local pickup points, both compete on immediacy rather than headline price, and both serve a customer who values their time more than a small discount. The difference is that Screwfix had married that trade-focused physical network to a slick digital ordering layer years earlier, while Howdens — for all its operational brilliance — had not. Livingston wasn't being asked to learn a new business. He was being asked to take a digital capability he'd already proven worked for tradespeople and graft it onto a relationship model that was, if anything, even deeper than Screwfix's. The board, in other words, hired pattern-recognition.

He moved quickly to remodel the builder's experience around digital tools — but, crucially, without touching the trade-only, confidential-pricing core that made the business special. The centrepiece was the "MyHowdens" portal, a digital platform that let builders manage their credit accounts, view their own confidential prices, generate professional-looking quotes to hand to homeowners, and place orders online.1 He paired it with live stock visibility, so a builder could check on his phone whether the local depot actually had the units he needed before driving over. These sound like modest conveniences. In aggregate, they deepened the moat: the more a builder's workflow, quotes, credit, and ordering live inside Howdens' system, the more switching to a rival means rebuilding his entire back office.

The other half of the Livingston era is alignment — how richly the people steering the company are tied to its outcome, which long-term investors should always scrutinise. Livingston's own stake tells the story plainly. His direct shareholding stood at roughly 785,594 shares, worth well over £6.5 million, equivalent to around 387% of his base salary — far above the 200% the company requires executives to hold.68 His pay is deliberately back-loaded toward performance and shares: the annual bonus caps at 200% of base salary, with 30% of it mandatorily deferred into shares for two years, and the Long-Term Incentive Plan can award up to 270% of salary, with vesting tied to Profit Before Tax and cash-flow targets.6 In other words, the bulk of his potential wealth only materialises if the company grows profit and throws off cash — exactly the metrics a long-term owner cares about.

It's worth dwelling on why a long-term investor should care about these structures rather than skimming past them as boilerplate. Incentive design is destiny. If you pay executives on revenue growth, you'll get acquisitions and discounting; if you pay them on share price over short windows, you'll get buybacks timed to vesting dates; if you pay them on returns and cash, you tend to get the patient, disciplined capital allocation that compounds over decades. Howdens' choice to tie long-term awards to profit before tax and cash flow — and to force executives to hold multiples of their salary in stock that they can't easily sell — is precisely the structure you'd design if you wanted managers to behave like owners thinking in decades rather than quarters. The fact that the CEO's personal stake is worth several times his salary means a bad year hurts his own net worth far more than it dents his cash compensation. That's the alignment a fundamental investor is looking for.

The other seat at the top changed hands more recently. In June 2025, Jackie Callaway became Chief Financial Officer, succeeding the retiring Paul Hayes, having previously been CFO of Coats Group plc.7 She signalled her conviction in an unusually direct way: on what was effectively her second day in the job, she bought 28,916 shares with £250,000 of her own money — a meaningful personal bet that, for investors reading the tea leaves, says more than any scripted statement.6 Her annualised base salary was set at £525,000, with a pro-rated 2025 total package of around £970,000, and she is required to build a holding worth 300% of salary within five years, with her own LTIP capped at 220% of salary.67

With a digitally fluent CEO and a capital-disciplined CFO now steering, the company entered a phase that would have been almost unthinkable in the Ingle era: deliberate, sizeable acquisitions. For most of its life, Howdens essentially didn't do M&A. Under Livingston, it started — and the way it did it is a clinic in disciplined capital allocation.

VI. M&A and Capital Deployment: Benchmarking the Strategic Pivots

For nearly its entire history, Howdens' approach to capital allocation was almost monastic in its simplicity. Cash went into two things: opening more depots, and expanding the company's own manufacturing capacity. Acquisitions were essentially absent from the playbook — a discipline born partly of culture and partly of the scar tissue from the MFI years, when inheriting someone else's liabilities nearly ended everything. So when Livingston's Howdens started buying companies, the interesting question for investors wasn't that they did deals, but how — and whether the famous discipline survived contact with a chequebook.

The first deal, in February 2022, was small but telling. Howdens acquired Sheridan Fabrications, the UK's largest independent maker of premium solid-surface worktops — the granite, quartz, and acrylic surfaces that sit at the higher end of a kitchen specification. The price was £15 million in cash, of which £12.4 million was allocated to goodwill.9 Sheridan was generating around £30 million of revenue at the time, which means Howdens paid roughly 0.5 times revenue and a low single-digit multiple of earnings — a notably modest price.9

For perspective on how modest that was, paying half a turn of revenue for a profitable, market-leading specialist manufacturer is the kind of price that only materialises when there's no auction frenzy and the buyer has a strategic reason to value the asset more than a financial buyer would. Howdens wasn't bidding against private equity for a trophy; it was quietly buying a capability it specifically needed, at a price set by Sheridan's standalone earnings rather than by what it would be worth slotted into Howdens' network. That gap — between standalone value and strategic value — is precisely where disciplined acquirers make their money.

But the price isn't really the point; the logic is. Howdens didn't buy a consumer brand or pay up for a flashy growth story. It bought a supply-chain capability. Solid-surface worktops are a high-margin, premium component, and historically Howdens had to source them through third-party fabricators — meaning it surrendered margin and, worse, was exposed to those suppliers' backlogs at exactly the moments demand was strongest. Bringing fabrication in-house let Howdens capture that margin itself, control its own availability, and push harder into the premium end of the kitchen market. It was, in spirit, the same vertical-integration instinct that had driven the company to build its own cabinet factories decades earlier, just applied to a new product category. Cheap, strategic, accretive — a tuck-in that strengthened the core without diluting it.

The second deal was an order of magnitude bigger, and it represented something genuinely new. On June 3, 2026 — just two weeks before this recording — Howdens announced the acquisition of DIY Kitchens, operated by Ultima Furniture Systems, for a £390 million enterprise value, structured as £292.5 million in cash and £97.5 million in newly issued Howdens shares.45 To understand why this matters, you have to understand what DIY Kitchens is: an online-only, vertically integrated manufacturer and retailer that sells high-quality, pre-assembled kitchens directly to consumers — specifically, to the kind of confident, project-managing homeowner who wants a great kitchen but is happy to organise the job themselves rather than hand it to a builder.

Now to the benchmarking, because this is where the discipline shows. In its 2025 financial year, DIY Kitchens generated revenue of about £136 million and operating profit of roughly £37 million — an extraordinary 27.2% operating margin, achieved while compounding revenue at around 17% a year over five years.45 Let that margin sink in. A direct-to-consumer kitchen retailer earning a 27% operating margin is operating at a level most retailers can only dream about, and growing fast on top of it.

So what did Howdens pay for that? About 2.87 times revenue and 10.5 times operating profit.45 Compare those numbers to the landscape around them. Traditional B2C home-improvement retailers — think Kingfisher, the owner of B&Q and Castorama — tend to trade at lower revenue multiples, around 0.5 to 0.8 times sales, but for good reason: their operating margins sit in the mid-single digits and their growth is flat to negative. You're paying a low multiple because you're buying a low-margin, no-growth business. Meanwhile, Howdens' own shares have historically been valued at something like 15 to 18 times operating profit.12 So Howdens used its own more highly-rated currency to buy a business growing at 17% with 27% margins for just 10.5 times profit. In plain terms, it bought something arguably better than itself, for less than its own multiple. That is the definition of value-accretive M&A.

There's a strategic elegance on top of the financial one. DIY Kitchens opens the door to the B2C consumer market — the homeowner who never wanted a builder in the first place — without Howdens having to put public prices in its own depots or sell directly to the public under the Howdens brand. The sacred trade-only relationship stays untouched. Howdens gets to play in two markets that would normally be in tension, by keeping them in separate boxes. We'll come back to exactly how those boxes work, because the way Howdens intends to run DIY Kitchens is itself a strategic statement.

The structuring of the deal also tells you something about the discipline involved. By paying three-quarters in cash and a quarter in newly issued Howdens shares, the company achieved two things at once. It kept the cash outlay manageable against its strong balance sheet, and — by handing the sellers equity — it bound the previous owners' financial interests to the combined company's future performance rather than letting them simply cash out and walk away. When you're buying a business whose value lives in a distinctive culture and a founder's operating instincts, giving the sellers a stake in what happens next is a quiet but meaningful way of buying their continued attention. It's the same alignment logic Howdens applies to its own executives, extended to the people it acquires.

One more piece of context makes the price look even more rational. Howdens already manufactures kitchens at enormous scale; DIY Kitchens manufactures kitchens too. Even running the two as separate front-end brands, there is obvious latent value in the shared back end — purchasing of raw materials, manufacturing techniques, capacity utilisation. A 10.5 times operating-profit price for a 17%-grower looks cheap on the standalone numbers alone; layer in even modest, carefully extracted manufacturing synergies over time, and the effective multiple paid drops further still. The art, of course, will be capturing those synergies without contaminating the thing that made DIY Kitchens special — a tension we'll return to in the bear case.

These two deals, five years apart, bracket the Livingston-era thesis: buy capabilities and growth, never vanity; pay sober multiples; protect the core at all costs. But acquisitions are only one of the engines driving the company forward. Some of the most interesting growth is happening in places most casual observers never look.

VII. The Hidden Engines: Segment-Level Analysis, France, and the Digital Vault

Ask a typical investor what Howdens is, and they'll describe a UK kitchen distributor. That's true, but it undersells the story, because beneath the mature domestic business sit several engines that don't yet show up clearly in the headline numbers — and one of them is happening across the Channel.

Start with the international segment, which today means primarily France, with smaller footprints in Belgium and Ireland. In its 2025 financial year, international revenue rose to £84.8 million, equivalent to about €99 million, representing 13.5% growth — around 12% in constant currency — over the prior year's £74.7 million.3 On a group basis that's still a small slice, which is precisely why it's easy to overlook. But growth rates in the low teens off a base that small, in a market the size of France, hint at a long runway. Of the company's 78 international depots, 65 are in France, and management has talked about a long-term ambition of around 250 depots there — roughly four times the current footprint.3

The more interesting detail is the financial inflection point. The French business has been in a deliberate, sustained investment phase — opening depots, building density, and absorbing the losses that come with a network that hasn't yet reached critical mass. In 2025 the company took a £6.1 million asset-impairment charge as part of optimising that physical network, a sign of management pruning and rationalising rather than blindly expanding.3 And here is the catalyst worth watching: management has guided that French operations are on track to break even in 2026.3 Break-even is the moment a sub-scale network stops being a drag and starts being a lever. Because so many of a depot network's costs are fixed, every pound of incremental revenue past break-even tends to flow disproportionately to profit. If France genuinely crosses that line and keeps growing, a business that has been quietly costing money turns into one that quietly makes it — and that swing isn't yet in anyone's headline forecasts.

The deeper question France answers is whether the model is uniquely British or genuinely portable, and that has enormous implications for how investors should value the whole enterprise. If Howdens is a clever distribution model that only works because of peculiarly British trade habits, then its addressable market is essentially capped at the UK and Ireland, and the stock is a mature compounder with a finite runway. If, on the other hand, the trade-only, in-stock, confidential-pricing model travels — if French builders behave enough like British ones for the virtuous circle to spin up in a market with its own large stock of housing in need of renovation — then France is the first proof point of a template that could, in principle, be rolled out across continental Europe over decades. The £6.1 million impairment and the patient, sometimes painful optimisation tell you this is hard and slow. But break-even in 2026 would be the first hard evidence that the answer to "does it travel?" is yes.

The second hidden engine is the newly acquired DIY Kitchens digital flywheel. The crucial strategic decision — and the thing that makes the acquisition coherent — is that Howdens intends to run it as a standalone business, operationally independent of the core depot network. Why deliberately keep them apart? Because they serve different customers in different ways, and merging them would damage both. DIY Kitchens captures a high-margin, often younger consumer who wants a custom, pre-assembled kitchen delivered to their door and is willing to project-manage the installation themselves — exactly the customer the trade-only model, by design, doesn't serve. Run separately, DIY Kitchens lets Howdens harvest that demand without ever putting a public price tag in a depot or giving builders a reason to feel undercut. The synergies, if they come, will live quietly in the back end — shared sourcing, shared manufacturing know-how — not in a confusing merged brand out front.

There's a generational angle to this that's easy to miss. The homeowner who happily orders a £15,000 kitchen online, watches YouTube tutorials, and either fits it themselves or hires a fitter for the labour only is a fundamentally different animal from the homeowner who hands the whole project to a trusted builder. The first type is growing as a share of the market — more confident with online purchasing, more comfortable project-managing, more price-transparent by instinct. For most of Howdens' history, that customer was simply unaddressable; the trade-only model had no way to reach them without breaking its own rules. DIY Kitchens is, in effect, a hedge against the slow drift of consumer behaviour toward self-service and online — a way for Howdens to own both the "I'll get my builder to sort it" customer and the "I'll sort it myself" customer, through two brands that never have to acknowledge each other exist.

The third engine isn't a segment at all; it's the structural reason the whole enterprise is so profitable: vertical integration as a margin shield. Because Howdens manufactures its own cabinets, doors, and now worktops, it captures both the manufacturer's margin and the distributor's margin on the same sale, rather than handing one of them to a third party. This is the mechanical explanation for why Howdens runs a gross margin north of 60%, against something like 35–40% for a typical builders' merchant such as Travis Perkins or a pure retailer.2 When your value proposition is "in stock, take away today," owning the factory isn't just a margin enhancer — it's the only way to keep that promise reliably, which means the profitability and the customer proposition are the same fact viewed from two angles.

There's a useful way to think about why that double margin is so defensible. In a normal supply chain, value is split among a manufacturer, a wholesaler, and a retailer, each taking a cut and each negotiating against the others. When external shocks hit — a timber shortage, a shipping crisis, an energy spike — that fragmented chain transmits the pain in unpredictable ways, and the party closest to the customer often gets squeezed because they can't easily pass costs on. Howdens, by collapsing manufacturer and distributor into one entity, controls the entire economics of the product from raw board to depot shelf. It can decide where to absorb a cost shock and where to pass it through, and it never has to wait on a third party's factory to honour its in-stock promise. The pandemic-era supply chain chaos was a live demonstration: businesses dependent on distant suppliers found shelves empty, while a vertically integrated operator could prioritise its own production. Owning the means of production, deeply unfashionable in the asset-light era, turns out to be a formidable advantage exactly when the world gets disorderly.

Put these together — a UK core still taking share, a French business about to flip from cost to contributor, a digital B2C arm bought cheap, and a manufacturing base that structurally protects margins — and you have a company with more growth optionality than its sleepy industrial-estate image suggests. Before we war-game the durability of all this, it's worth pausing to puncture a couple of the lazy narratives that tend to attach to a business like this.

Myth vs. Reality

The first myth is that Howdens is "just a recession-proof DIY play" that rides the housing cycle. The reality is more nuanced and, frankly, more interesting. Howdens is not immune to the cycle — a deep, sustained collapse in renovation spending would hurt it like anyone else. What makes it more defensive than a pure new-build supplier is its tilt toward repair-and-improve work, which holds up better when housing transactions freeze, plus a cost base that flexes with volume and carries no expensive showroom leases. "Recession-proof" overstates it; "recession-resilient, structurally" is closer to the truth, and the distinction matters when you're stress-testing the downside.

The second myth is that the DIY Kitchens acquisition signals Howdens abandoning its trade-only religion and chasing consumers. The reality is almost the opposite: the deal was structured specifically to avoid that. By running DIY Kitchens as a walled-off, separately branded online business, Howdens reaches consumers without ever exposing trade pricing or giving its builders a reason to feel betrayed. It's not a conversion to consumer retail; it's a way to monetise the consumer market that the core model was always, by design, leaving on the table for someone else. Read correctly, the acquisition is a defence of the trade-only model, not a retreat from it.

With the narratives cleaned up, let's put the business through the two frameworks every serious investor reaches for.

VIII. Strategic Frameworks: Hamilton's 7 Powers & Porter's 5 Forces

It's one thing to admire a business; it's another to interrogate why its advantages should persist. Let's war-game Howdens against two of the standard lenses — Hamilton Helmer's 7 Powers and Porter's Five Forces — and be honest about where the moat is deep and where it's merely a ditch.

The primary power, the one we opened the whole episode with, is Counter-Positioning. The reason this is so potent is not that rivals haven't thought of Howdens' model — it's that they can't adopt it without self-destruction. A Magnet or a Wren exists to pull consumers into showrooms with advertised prices and aspirational displays. If either tried to go trade-only and hide its pricing, it would instantly alienate the retail customers who fund its expensive high-street footprint, while lacking the decades of local trade relationships needed to replace them. The incumbent's existing business model is precisely what prevents imitation. That's counter-positioning in its purest form: your competitor's strength is the thing that traps them.

The second power is Scale Economies, which for Howdens operates on two levels. The first is local density. With well over 900 UK depots, the company can credibly claim that the overwhelming majority of British builders are within a few miles of one — and no independent competitor can replicate that lattice of warehouses, each carrying full stock, without an investment that could never earn an adequate return at sub-scale.1 The second level is manufacturing scale: Howdens' factories give it enormous buying power over raw materials and components — timber, chipboard, hinges — and over the appliances it sources from global manufacturers such as 海尔集团 Haier Group, the Chinese conglomerate that owns GE Appliances and Candy. Scale begets cost advantage, which funds either lower prices or higher margins, which funds more scale.

The third power is Switching Costs, and for a builder these are surprisingly high in ways that don't show up on a price list. Consider the on-site emergency: a cabinet door gets scratched mid-installation. The Howdens builder drives five minutes to the local depot and walks out with a free replacement, job back on track. The builder who sourced from a distant online competitor faces a delay of days or weeks, an angry client, and a stalled job. Reliability under pressure is worth more to a tradesperson than a few percent on price. Layer on the trade credit — the local, relationship-based credit line that functions as working-capital lifeblood for a small contractor — and the "MyHowdens" digital workflow where quotes, prices, and orders now live, and switching means surrendering favourable cash-flow terms and rebuilding your back office. None of these are contractual lock-ins. They're something stickier: operational dependence.

Now the Porter view, which mostly corroborates the picture. The threat of new entrants is very low: replicating Howdens demands hundreds of local warehouses, vast inventory tied up in stock to honour the take-away promise, and — least copyable of all — decades of accumulated trust with local tradespeople. The bargaining power of buyers is low, which is counterintuitive until you remember the builder isn't price-sensitive in the usual way: he passes the cost straight to the homeowner and, because his discount is confidential, he's actively motivated to keep buying from Howdens to protect that hidden markup. The bargaining power of suppliers is low, because Howdens is its own primary manufacturer, and for the third-party products it does buy — appliances, or trade tools from the likes of 株式会社マキタ Makita Corporation — its sheer volume makes it the single most important route to market in the UK, so it tends to dictate terms rather than accept them. The threat of substitutes is low: people still need kitchens, most still want professional installation, and the builder steers them to Howdens.

Where the framework is more sober is competitive rivalry, which is genuinely moderate rather than absent. Wren, Magnet, and B&Q all compete vigorously at the edges, and the consumer-facing market is crowded and promotional. Howdens' protection isn't the absence of competitors; it's that none of them occupies the same intersection of trade-only focus, instant local stock, and entrepreneurial depot-level management. The moat is real, but it's a moat around a specific castle, not the whole valley.

It's worth being explicit about which of the seven powers Howdens does not convincingly possess, because honest framework analysis means naming the absences. Howdens has no meaningful network effect in the classic sense — a new builder joining doesn't make the service better for existing builders the way a new user improves a marketplace. It has no branding power with the end consumer, who often doesn't even know their kitchen is a Howdens; the brand equity sits with the trade, not the public. It holds no cornered resource — no patent, no exclusive licence, no irreplaceable input. And process power — a hard-to-replicate way of operating — is arguable but not the core of the story. The honest conclusion is that Howdens rests on a tight, mutually reinforcing tripod of counter-positioning, scale economies, and switching costs, and it leans most heavily on the first. That concentration is a strength when those three hold and a vulnerability worth monitoring if any one of them erodes — say, if a digital-native competitor found a way to neutralise the switching costs that local stock currently creates. That distinction sets up the genuine debate: how should a long-term owner weigh the bull case against the bear case?

IX. The Bear vs. Bull Case & Playbook Lessons

Every durable business invites a confident bull story and a nagging bear story, and the honest investor holds both at once. Let's lay them side by side.

The bull case rests on what you might call double-engine growth. The mature UK and Ireland business continues to take share through steady organic depot rollouts — a proven, low-risk, self-funding form of expansion. Crucially, this is growth that requires no heroic assumptions: every new depot follows a well-worn template, opens onto cheap industrial land, and reaches profitability on a predictable timeline, which means the UK rollout is less a gamble than a known repeatable process with a finite but not-yet-exhausted runway. Simultaneously, the French business reaches its long-awaited break-even in 2026, converting years of investment losses into a high-margin growth runway just as operating leverage kicks in.3 On top of those two physical engines sits the DIY Kitchens acquisition, which bolts on a fast-growing, exceptionally profitable digital B2C channel that reaches the non-builder consumer without cannibalising the core trade brand.4 And underpinning all of it is the financial character forged in the MFI crisis: minimal debt, no expensive showroom leases dragging on returns, a pension deficit now repaired, and the kind of high free-cash-flow conversion that comfortably funds both share buybacks and a growing dividend. It's a compounder with optionality and a fortress balance sheet — the rare combination of a defensive core and several credible growth options, each of which the company can fund out of its own cash flow without ever betting the house.

The bear case is equally coherent. First and most cyclically, Howdens is ultimately leveraged to UK home renovation, and that spending is discretionary. A kitchen is a big-ticket purchase that a household can almost always defer for another year, and when confidence sags — high interest rates squeezing mortgage holders, real incomes under pressure — that deferral is exactly what happens across the whole market at once. The trade-only model proved resilient in 2008 by riding the shift toward smaller refurbishment jobs, but resilience is not invulnerability; a deep and lasting downturn would still compress volumes, and because so much of Howdens' cost base is fixed depot and factory capacity, the operating leverage that works so beautifully on the way up works just as ruthlessly in reverse. Second is integration risk: running DIY Kitchens as a standalone business is the right call strategically, but it's a genuine tightrope — Howdens must extract back-end manufacturing synergies to justify the £390 million price without smothering the distinctive direct-to-consumer digital culture that made DIY Kitchens worth buying in the first place.4 Corporate history is littered with acquirers that loved a target to death by over-integrating it, imposing the parent's processes and management layers until the nimble thing they bought becomes just another division. Third is France, where the bet is that the magic of the British builder relationship translates to a market with different trade dynamics, different builder-client buying habits, and different competitive structures. Break-even in 2026 would be encouraging evidence, but it would not yet prove the full model travels, and a stumble there would not just cost money — it would undercut the entire "this template can be rolled out across Europe" thesis that underpins the long-term growth story.3

A fourth, slower-burning risk deserves a mention: the gradual shift in how consumers and even tradespeople buy. The switching costs that protect Howdens are rooted in physical immediacy — the five-minute drive for a replacement door, the local stock a builder can see and grab. If logistics and online competitors continue to compress delivery times, and if a new generation of tradespeople grows up ordering everything to site overnight, the premium on physical proximity could slowly erode. This isn't an imminent threat; Howdens' density and trade relationships are formidable. But it's the kind of structural drift that a long-term owner should keep at the back of their mind, because moats rarely fall to a frontal assault — they silt up slowly as the terrain around them changes.

So what should a long-term owner actually watch? It's tempting to drown in the dozens of metrics a company like this discloses, but discipline means zeroing in on the few that actually move the thesis. Three KPIs carry most of the signal.

The first, and most important, is UK depot productivity — revenue and gross profit per mature depot, and like-for-like sales growth across the established estate. This is the truest test of whether the core engine is still compounding. The reason to separate mature-depot performance from total growth is that opening new depots will always flatter the top line for a while; what you really want to know is whether the existing network is getting more productive, or whether Howdens is just adding boxes to a saturating market. Healthy like-for-like growth says the model still has pricing power and is still deepening its share of each builder's spend. Stagnant or negative like-for-like growth, masked by new openings, would be an early warning that the UK opportunity is maturing faster than the headline suggests.

The second is the French segment's march to and through break-even. This is the single clearest near-term catalyst for a step-change in group profitability and, more importantly, the cleanest available test of whether the model exports beyond Britain. Watch not just the break-even milestone itself but the trajectory afterward — does French revenue per depot start climbing toward UK-like levels as density builds, or does it plateau at a structurally lower number that would imply the model is diluted outside its home market?

The third, specific to the next couple of years, is DIY Kitchens' growth and margin trajectory under Howdens' ownership. The whole financial logic of the £390 million deal rests on that exceptional combination of high-teens growth and a 27% operating margin persisting. If both hold or improve, the acquisition will look like a masterstroke and validate management's capital-allocation judgement. If the margin drifts down toward ordinary retail levels or growth stalls as integration friction sets in, it will be the first sign that the deal destroyed rather than created value. Track those three, and you're tracking the thesis itself — everything else is detail.

The Howdens story also leaves three durable playbook lessons. The first: define your true customer. Howdens' entire empire rests on Matthew Ingle's realisation that the customer wasn't the person paying for the kitchen, but the person installing it — and that serving the installer better than anyone else would make the homeowner's choice for them. The second: align incentives at the frontline. By paying depot managers on local profit and cash collection, Howdens turned thousands of branches into thousands of owner-operators obsessive about relationships and credit control — the kind of alignment that can't be bought with a slogan. The third: vertical integration is not dead. In a world of supply-chain shocks, owning your manufacturing and logistics is a profound advantage precisely when your promise to the customer is "in stock, available today."

Which brings us, finally, to what all of this adds up to.

X. Epilogue & Final Thoughts

The lasting impression of Howden Joinery is of a company that succeeded by being almost aggressively unglamorous. There was no viral product, no charismatic disruption narrative, no land-grab funded by a decade of losses. There was, instead, a single contrarian insight about who the real customer is, executed with operational discipline for thirty years, defended by a business model that competitors literally cannot copy without destroying themselves, and stress-tested by a near-death experience that left it permanently allergic to financial recklessness.

What's striking is how the company has managed to evolve without betraying that core. Under Andrew Livingston and now Jackie Callaway, Howdens has digitised the builder's workflow, pushed into France, brought premium fabrication in-house, and — with the DIY Kitchens acquisition — opened a direct-to-consumer front it had spent its entire existence carefully avoiding, all while keeping the sacred trade-only relationship intact. It is no longer accurate to think of Howdens as merely a trade-only joiner. It has become a modern, omni-channel, vertically integrated industrial business that happens to still treat the local builder as its most important customer in the world.

The through-line across thirty years is consistency of philosophy under changing tactics. The tools have changed — from paper ledgers to mobile apps, from a single domestic market to a continental ambition, from purely organic growth to disciplined M&A — but the underlying beliefs have not budged. Know who your real customer is. Align everyone, from the depot manager to the chief executive to the acquired founder, around cash and returns rather than vanity. Own the things that let you keep your promise to that customer. Treat the balance sheet as a fortress, never a casino. Those principles were forged in a redundancy, tested nearly to destruction in a financial crisis, and carried forward, largely unchanged, into a digital and international future. That kind of continuity is rarer than any single clever strategy, and it is arguably the most underappreciated part of the whole story.

The quiet compounding machine on the industrial estate, it turns out, was never as simple as it looked.

References

-

Howden Joinery Group Plc Investor Relations Hub — Howden Joinery Group, 2026-06-18 ↩↩

-

Howdens Group Annual Report & Accounts 2024 — Howden Joinery Group, 2025-02-27 ↩↩↩

-

Regulatory Announcement: 2025 Full Year Results — London Stock Exchange, 2026-02-26 ↩↩↩↩↩↩

-

Acquisition of DIY Kitchens (Ultima Furniture Systems Limited) RNS Announcement — Howden Joinery Group, 2026-06-03 ↩↩↩↩↩↩

-

Howdens Acquires Online Retailer DIY Kitchens for £390m — Financial Times, 2026-06-03 ↩↩↩↩

-

Remuneration Committee Report: Executive Shareholdings & Performance Metrics — Howden Joinery Group, 2025-02-27 ↩↩↩↩

-

Appointment of CFO Jackie Callaway and Retirement of Paul Hayes — London Stock Exchange, 2025-03-10 ↩↩

-

Director Share Transaction Disclosures for CEO Andrew Livingston — London Stock Exchange, 2026-05-12 ↩

-

Howdens Acquires Worktop Fabricator Sheridan Fabrications — KBB Review, 2022-02-04 ↩↩

-

Howden Joinery Group Plc ESG & Sustainability Report 2025 — Howden Joinery Group, 2026-03-15 ↩

-

Reuters Company Profile: Howden Joinery Group (HWDN.L) — Reuters, 2026-06-18 ↩

-

Bloomberg Stock Quote & Capital Analysis: HWDN:LN — Bloomberg, 2026-06-18 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube