Husqvarna AB: The 337-Year-Old Robotics Startup

I. Introduction: The Swedish "Everything" Company

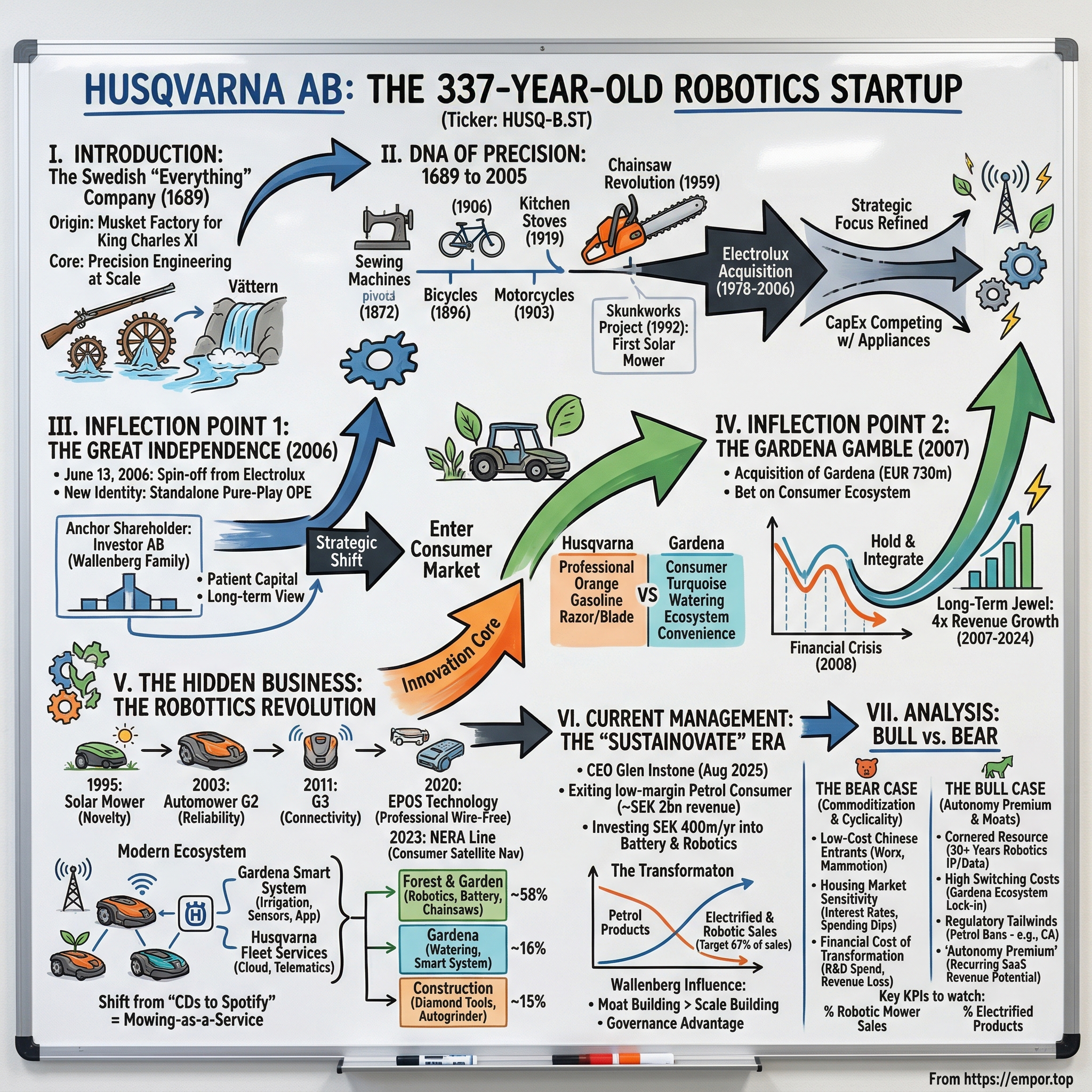

There is a factory in southern Sweden, perched beside the rapids of the Vättern waterfall, that has been making things since before the United States existed. In 1689, while Isaac Newton was still working out the implications of his Principia Mathematica, the Swedish Crown commissioned a small workshop in the town of Huskvarna to forge muskets for King Charles XI's military campaigns. Three hundred and thirty-seven years later, that same company—bearing the same name, carrying the same coat of arms—ships autonomous robots to manicured lawns in forty countries. The robots navigate by satellite, learn the contours of gardens through machine vision, and report back to a cloud platform that tells a landscaper in Frankfurt exactly how many square meters were mowed while he was eating lunch.

This is Husqvarna AB, and its story is one of the most improbable corporate metamorphoses in industrial history.

The scale of the modern enterprise is staggering. Husqvarna Group generated approximately SEK 46.6 billion in net sales in 2025, making it one of the largest outdoor power equipment companies on the planet. Its products range from professional chainsaws trusted by loggers in the Pacific Northwest to the Gardena watering systems that keep European rose gardens alive through July heat. It operates across three divisions—Husqvarna Forest & Garden, Gardena, and Husqvarna Construction—each serving distinct customers but increasingly connected by a shared technology stack built around batteries, sensors, and software.

But the real thesis here is not about size. It is about transformation. Husqvarna is arguably the purest case study in the "Innovator's Dilemma" playing out in real time among European industrials. The company is deliberately cannibalizing its own profitable gasoline-powered product lines—walking away from roughly SEK 2 billion in annual petrol consumer revenue—to bet on a future defined by autonomous robotics, battery power, and recurring software services. It is a transition from selling loud, fuel-burning tools once to building silent, software-connected ecosystems that generate revenue continuously. Think of it as the shift from selling CDs to running Spotify, except the CDs weigh forty pounds and smell like two-stroke exhaust.

The story of how a musket factory became a robotics company touches every theme that matters in modern investing: the power of patient capital (the Wallenberg family's Investor AB has been the anchor shareholder for decades), the strategic logic of M&A as moat-building rather than empire-building, and the question of whether European industrials can genuinely compete with Silicon Valley and Shenzhen in the age of autonomy. To understand where Husqvarna is going, we need to understand where it has been—and why three centuries of reinvention are not a bug in its corporate DNA, but the defining feature.

II. The DNA of Precision: 1689 to 2005

Picture the Huskvarna rapids in the late seventeenth century—a torrent of glacial water crashing down from Lake Vättern, powering a series of wooden waterwheels that drove the bellows and trip hammers of the Crown's new armory. The location was chosen for a reason that would define the company's identity for centuries: the waterfall provided free, reliable energy, and the surrounding forests offered an inexhaustible supply of charcoal for smelting. In its first years, the factory produced roughly 1,500 musket barrels annually, each one hand-forged and inspected to tolerances that were extraordinary for the era. The Swedish military was obsessed with precision—its soldiers were outnumbered by virtually every rival on the European continent, so each weapon had to work flawlessly, every time. That ethos of mechanical exactitude was baked into the Huskvarna factory from its founding, and it never left.

As Sweden's military ambitions waned in the eighteenth and nineteenth centuries, the factory did what great manufacturing enterprises do: it looked at its core capabilities and asked what else they could build. The machinery for boring musket barrels turned out to be remarkably well-suited for making sewing machine components. By 1872, Husqvarna was producing sewing machines that competed with Singer across Scandinavia. By 1896, it had moved into bicycles—a natural extension for a company that understood gears, bearings, and lightweight metal fabrication. In 1903, it bolted a small engine onto a bicycle frame and entered the motorcycle business, eventually producing racing machines that would win Grand Prix championships. Kitchen stoves followed in 1919, leveraging the company's expertise in cast iron and heat management.

This constant pivoting was not the erratic flailing of a company without direction. It was the systematic exploitation of a single core competency: the ability to engineer precision mechanical systems at scale. Every product Husqvarna touched—muskets, sewing machines, bicycles, motorcycles, stoves—required the same fundamental skills: metallurgy, tight tolerances, reliable moving parts. The brand survived because the underlying capability was transferable.

The modern Husqvarna story really begins in 1959, when the company produced its first chainsaw. This was the product category that would define it for the next half-century. Professional chainsaws required everything Husqvarna was good at—high-performance two-stroke engines, vibration dampening, ergonomic design for tools used eight hours a day in brutal conditions—and the company quickly became the gold standard among professional loggers and arborists. The iconic orange-and-gray color scheme became synonymous with reliability in the forest.

But in 1978, a fateful corporate event reshaped Husqvarna's trajectory: Electrolux, the Swedish white goods giant, acquired the company. For nearly three decades, Husqvarna operated as a division within the Electrolux empire. The Electrolux era was a mixed blessing. On one hand, it provided access to global distribution networks and manufacturing scale. Electrolux refined Husqvarna's focus toward forestry and gardening products, stripping away the eclectic portfolio of motorcycles and kitchen appliances. On the other hand, being a subsidiary of a washing machine company meant that Husqvarna's capital allocation was dictated by priorities that had nothing to do with chainsaws or lawnmowers. Investment decisions were filtered through the lens of Electrolux's core business, and Husqvarna's potential was constrained by its parent's strategic bandwidth.

What matters for today's investor is this: three hundred years of pivoting from muskets to sewing machines to motorcycles to chainsaws created an organizational muscle memory for transformation. The company had reinvented itself so many times that reinvention became part of its identity. When the time came to pivot from gasoline to batteries and from manual tools to autonomous robots, Husqvarna had a cultural advantage that no Silicon Valley startup could replicate—the institutional confidence that comes from having survived every previous technological transition since the age of flintlock muskets. And buried in the Electrolux years was a quiet project that would eventually become the company's most important product: in 1992, a small team of engineers in Huskvarna began working on a solar-powered robot that could mow a lawn by itself.

III. Inflection Point 1: The Great Independence (2006)

On June 13, 2006, the Stockholm Stock Exchange opened with a new name on the O-list: Husqvarna AB. After twenty-eight years as a subsidiary of Electrolux, the outdoor power equipment business was finally free. The spin-off had been approved at Electrolux's annual meeting in April, and Husqvarna shares were distributed to existing Electrolux shareholders on a record date of June 12. When trading began the following morning, the market was pricing a company with approximately SEK 29 billion in annual sales and the world's largest chainsaw and lawnmower business.

The moment was electric—though in a very Swedish, understated way. Bengt Andersson, who would serve as the first CEO of the independent Husqvarna, had spent years preparing for this day. The management team had been quietly building the case that Husqvarna's potential was being suppressed by the conglomerate structure. As a division of Electrolux, every capital expenditure request competed against refrigerator factories and vacuum cleaner R&D. The outdoor power equipment business was profitable and growing, but it was perpetually the second priority in a company whose identity was defined by kitchen appliances.

Independence changed everything. For the first time in decades, Husqvarna had its own balance sheet, its own board of directors, and its own stock price. Capital allocation decisions would be made by people who understood the difference between a professional-grade chainsaw and a consumer trimmer, not by executives whose primary concern was the European washing machine cycle. The strategic implications were immediate and profound.

The first realization that hit the newly independent management team was that Husqvarna was dramatically under-exposed to the premium consumer segment. The company's strength was in professional products—the orange chainsaws and commercial mowers that loggers and landscapers relied on. But the consumer garden market, where homeowners spent weekends tending their lawns and flower beds, was a much larger addressable market with different competitive dynamics. In the professional world, Husqvarna competed primarily on performance and durability. In the consumer world, brand loyalty, ecosystem effects, and retail shelf presence mattered more. The company needed a consumer strategy, and it needed one fast.

The cultural shift was equally significant. Conglomerate divisions tend to develop a particular psychology—a learned helplessness around strategic ambition, because the big decisions are always made somewhere else. Independence forced Husqvarna's leadership to think like owners rather than division managers. Every investment had to be justified on its own merits, every acquisition had to be funded from Husqvarna's own cash flows and borrowing capacity, and every mistake would be reflected directly in Husqvarna's stock price rather than buried in a conglomerate's consolidated numbers.

The Wallenberg family's Investor AB, which had been a significant Electrolux shareholder, emerged as Husqvarna's anchor owner with approximately seventeen percent of the capital and considerably more voting power through the dual share class structure. This was not incidental. The Wallenberg model of ownership—patient, long-term, engaged but not meddlesome—would prove critical in the years ahead. Investor AB's presence on the board sent a signal to management: you have the freedom to make long-term bets, but you also have a sophisticated owner who will hold you accountable for the quality of those bets. It was the corporate governance equivalent of a trust fund with strings attached—generous, but not unconditional.

The spin-off also crystallized an uncomfortable truth about valuation. As part of Electrolux, Husqvarna's outdoor power equipment business was valued at a conglomerate discount—lumped in with dishwashers and floor care products. As a standalone company, the market could assign a multiple that reflected the actual growth potential of a global leader in outdoor power. The early trading days confirmed the thesis: investors were willing to pay a premium for a pure-play in a category that benefited from rising homeownership, increasing urbanization of garden care, and a growing professional landscaping industry.

But the real strategic question was not about valuation multiples—it was about what Husqvarna would do with its newfound freedom. The answer came quickly, and it came in the form of a German garden hose company that would transform the entire group.

IV. Inflection Point 2: The Gardena Gamble and M&A Benchmarking

In the summer of 2007, barely a year after gaining independence, Husqvarna made the largest bet in its modern history. The company announced the acquisition of Gardena, the iconic German garden watering and tools brand, from private equity firm Industri Kapital. The price tag was EUR 730 million—approximately USD 964 million when including the EUR 416 million in transferred debt and pension liabilities. For a company that had been public for barely twelve months, it was an audacious move.

Gardena was, in many ways, Husqvarna's opposite. Where Husqvarna sold orange chainsaws to burly professionals, Gardena sold turquoise watering systems to suburban gardeners. Where Husqvarna's products ran on gasoline and required maintenance expertise, Gardena's products clicked together with satisfying plastic connectors and required nothing more than a functioning garden tap. At the time of the acquisition, Gardena had sales of approximately EUR 422 million and operating income of EUR 54 million, with around 2,900 employees and dominant market positions in European consumer irrigation, garden tools, and pond equipment.

The financial benchmarks were scrutinized intensely. At roughly 1.6 times sales and approximately twelve times EBITDA, Husqvarna was paying a premium that some analysts considered "top of the market." For context, comparable transactions in the outdoor equipment space at the time—think Stanley Black & Decker's various bolt-on acquisitions, or Toro's deal multiples—typically came in at lower revenue multiples. The skeptics had a point: Husqvarna was a newly public company, lever up to buy a consumer brand in a different segment, at a price that assumed continued strong performance.

And then 2008 happened. The global financial crisis hammered consumer spending, housing markets collapsed, and discretionary garden purchases—the exact category Gardena served—were among the first items cut from household budgets. Husqvarna's consolidated net sales fell from SEK 33.3 billion in 2007 to SEK 32.3 billion in 2008, with the construction segment taking the hardest hit. The Gardena acquisition, barely a year old, looked like a case study in terrible timing.

But here is where the long view matters. The Wallenberg-influenced board did not panic. They did not write down the acquisition or spin it off or engage in the kind of short-term value destruction that publicly traded companies often inflict on themselves when a deal goes sideways in its first year. They held. They integrated. They invested in the Gardena brand and its distribution network. And over the next fifteen years, Gardena became the jewel of the Husqvarna portfolio.

By 2024, Gardena was generating approximately SEK 7.8 billion in annual revenue—nearly four times the EUR 422 million in sales at the time of acquisition, even accounting for currency effects. The division had grown from a European watering company into a comprehensive smart garden ecosystem, with connected sprinklers, soil sensors, robotic mowers sold under the Gardena brand, and a smartphone app that tied everything together. The "Apple of the garden" comparison that enthusiasts used was not entirely hyperbolic: Gardena had achieved the rare feat of building consumer brand loyalty in a category—garden tools—where most products are grudge purchases treated as interchangeable commodities.

The strategic logic of the deal, which was not fully apparent in 2007, revealed itself over time. Husqvarna's professional business was a razor-and-blade model built on performance: professionals bought Husqvarna chainsaws because they were the best, and they stayed because switching costs were high in terms of muscle memory, dealer relationships, and parts compatibility. Gardena's consumer business was an ecosystem model built on convenience: homeowners bought one Gardena product, discovered that it connected seamlessly to other Gardena products, and gradually filled their garden sheds with turquoise-branded equipment. The two models were complementary. Husqvarna owned the professional's trust; Gardena owned the homeowner's loyalty. Together, they covered the entire outdoor power equipment market from the logging trail to the suburban flower bed.

The capital allocation philosophy embedded in the Gardena deal would define Husqvarna's M&A approach for the next two decades. The company did not acquire Gardena for "scale"—they did not need more chainsaw factories or additional distribution for their existing product lines. They acquired Gardena for "moat"—the deal gave them a defensible consumer brand, a product ecosystem with high switching costs, and a platform for future smart-home integration that their core professional products could never provide. This distinction between buying scale and buying moats is one of the most underappreciated aspects of Husqvarna's strategy, and it would repeat itself fourteen years later with the Orbit acquisition.

The short-term verdict on Gardena was that Husqvarna overpaid at the worst possible time. The long-term verdict is that it was a transformative deal that gave the company the consumer platform it needed to execute its robotics and battery strategy. Sometimes the best acquisitions are the ones that look worst in year one.

V. The Hidden Business: The Robotics Revolution

In 1995, at a trade show that most of the gardening world ignored, Husqvarna unveiled something that looked like a oversized hockey puck with solar panels: the Solar Mower. It was the world's first commercially available robotic lawn mower, the product of a skunkworks project that had been running inside the company since 1992. The technology was primitive by today's standards—the solar-powered unit crawled across lawns at a glacial pace, guided by a buried boundary wire that defined the mowing area. But the concept was revolutionary. A machine that could cut grass autonomously, day after day, without human intervention. The lawn would never be "mowed" in the traditional sense; it would simply always be short, maintained by a tireless robot that shaved a few millimeters off the grass every time it made its rounds.

The market yawned. In 1995, the idea of a robot doing household chores was science fiction. The Roomba was still seven years away. Smartphones did not exist. The notion that a homeowner would spend thousands of dollars on a robot to replace a weekend activity that most people considered mildly therapeutic—pushing a mower on a Saturday morning—seemed absurd.

But Husqvarna persisted. The second-generation Automower launched in 2003 with improved design and reliability. By 2009, the company had sold 100,000 units—a milestone that took fourteen years to reach but proved that a real market existed. The third generation arrived in 2011, bringing connectivity features that allowed owners to monitor and control their mowers via smartphone. Each generation was better: quieter, more capable, more reliable. The boundary wire installation—which required burying a thin cable around the perimeter of the lawn and around obstacles—remained the main friction point for adoption, but the mowing performance itself improved dramatically.

The breakthrough came in two stages. In 2020, Husqvarna launched EPOS—the Exact Positioning Operating System—for its professional mower line. EPOS used RTK (Real-Time Kinematic) satellite navigation to achieve centimeter-level positioning accuracy, enabling virtual boundaries that eliminated the need for physical boundary wire entirely. Think of it as GPS, but instead of the three-to-five-meter accuracy that tells your phone which street you are on, EPOS delivered two-centimeter accuracy that told the mower exactly which blade of grass to cut next. For professional landscapers managing dozens of properties, the elimination of boundary wire installation—which could take hours per site—was transformative.

The consumer version followed in 2023 with the Automower NERA line, which brought satellite-based wire-free navigation to residential models. And in February 2025, Husqvarna executed what it called the largest product launch in company history: thirteen new boundary wire-free robotic mowers spanning coverage areas from 600 to 50,000 square meters. The launch included, for the first time, Gardena-branded wire-free models designed for retail channels—DIY stores, garden centers, and e-commerce platforms. The new models featured "systematic mowing," which increased cutting capacity by fifty percent and could create patterned lawn designs like stripes and checkerboards. The robot mower had finally graduated from novelty to necessity.

Understanding Husqvarna's segment structure is critical for investors who want to see past the consolidated numbers. The Husqvarna Forest & Garden division, which accounts for roughly fifty-eight percent of group revenue, houses the professional chainsaw business alongside the Automower robotic mower line and the growing battery-powered product portfolio. This is where the gas-to-battery transition is most visible and most painful—the division is simultaneously managing the decline of petrol consumer products and the ramp of robotics and battery tools.

The Gardena division, at roughly sixteen percent of revenue, is the high-growth consumer platform. After the Orbit Irrigation acquisition in 2021, Gardena became the global leader in residential watering, combining European market dominance with Orbit's strong US position. The "Smart System" ecosystem—connected sprinklers, soil moisture sensors, robotic mowers, and a unified smartphone app—creates genuine switching costs. Once a homeowner has invested in the Gardena ecosystem, replacing individual components with competitor products means abandoning the integrated control and automation that makes the system valuable. This is the garden equivalent of being locked into the Apple ecosystem: each additional device makes the whole system more useful, and leaving becomes progressively more costly.

The Husqvarna Construction division, at roughly fifteen percent of revenue, is the business that analysts consistently overlook. This division makes diamond-tipped cutting and drilling tools, floor grinding equipment (including the HiPERFLOOR polished concrete system), surface preparation machines, and light demolition equipment. It serves the construction industry rather than the garden market, and its revenue profile is more stable and less seasonal than the consumer-facing divisions. Construction contributed positive organic growth of two percent in 2025 even as Gardena declined by ten percent. The division is also developing the Husqvarna Autogrinder—a self-operating floor grinder that applies the autonomous navigation technology from the Automower to construction applications. If that sounds like a niche product, consider that polished concrete flooring is one of the fastest-growing segments in commercial construction, and the labor shortage in the trades makes autonomous equipment increasingly valuable.

Perhaps the most strategically significant development is one that barely registers in the financial statements yet: Husqvarna Fleet Services. This digital platform allows professional landscapers and construction companies to track their entire equipment fleet in real time—GPS positioning, running hours, service history, and team productivity analytics, all accessible from a smartphone or laptop. The platform currently covers chainsaws, robotic mowers, hedge trimmers, leaf blowers, and other connected machines. As of early 2026, Fleet Services is offered free of charge as part of the Husqvarna professional ecosystem—a deliberate strategy to build adoption and switching costs before eventually monetizing the platform.

In May 2025, Husqvarna partnered with European landscaping providers to deploy connected robotic mower fleets under a subscription-based service model. This is the pivot that long-term investors should watch most closely. If Husqvarna can transition from selling a mower once for several thousand dollars to selling mowing-as-a-service for a monthly fee—maintaining the equipment, managing the software, providing the fleet analytics—it transforms from a cyclical hardware company into a recurring-revenue platform business. The hardware becomes, as one analyst put it, "a Trojan horse for high-margin software and service." Robotic mower net sales already reached SEK 7.2 billion in 2024, representing a substantial and growing share of group revenue. The trajectory from here depends on whether the service model gains traction with professional customers who are accustomed to owning their equipment rather than subscribing to it.

VI. Current Management: The "Sustainovate" Era

The leadership story at Husqvarna in recent years has been marked by both tragedy and transition. Henric Andersson, who became CEO in April 2020, was steering the company through the pandemic and the early stages of the strategic transformation when he took medical leave in late 2022. He passed away on February 4, 2023. The loss of a sitting CEO is always destabilizing for an organization, but the manner in which Husqvarna handled the transition revealed something important about its institutional character.

Pavel Hajman, who had been serving as acting CEO since December 2022, was confirmed as permanent CEO in May 2023. Hajman was not an outsider parachuted in to steady the ship—he was a Husqvarna veteran who had joined the company in 2014 and held leadership roles across multiple divisions. He had served as President of the Forest & Garden Division from 2014 to 2018, overseeing the professional product lines that were the company's bread and butter. He then moved into operational roles—SVP Operations Development, then EVP Global Information Services—giving him visibility across the entire organization's technology and manufacturing footprint. Before Husqvarna, Hajman had worked at Seco Tools and Assa Abloy, where he served as President of AHG Greater China, giving him international operating experience in complex industrial businesses.

Hajman's tenure was defined by execution of the strategic transformation that had been announced in the fall of 2022. The plan was bold in its specificity: exit approximately SEK 2 billion in annual sales of low-margin petrol consumer products by 2024, invest an incremental SEK 400 million per year into robotic mowers, battery products, watering systems, and professional tools, achieve cost savings of roughly SEK 800 million per year (with half reinvested), and reduce the workforce by approximately 1,000 positions—the vast majority related to the petrol-to-battery transition. The target was for sixty-seven percent of motorized product sales to come from electrified products within five years. By 2024, the company had reached forty-four percent, suggesting the trajectory was on track but acceleration was still needed.

In 2025, Hajman announced he would step down by year-end. The board moved quickly, appointing Glen Instone as CEO effective August 11, 2025. Instone's profile tells a story of its own. Born in England, forty-eight years old, a Chartered Management Accountant by training, he had joined Husqvarna in 2002—meaning he had lived through the Electrolux years, the spin-off, the Gardena acquisition, and the entire robotics evolution. He served as Group CFO before becoming President of the Forest & Garden Division, giving him both financial discipline and operational credibility. His appointment signaled continuity: this was not a board reaching outside for a transformation agent, but promoting from within someone who understood the company's complexity and had helped build the strategy he was now tasked with executing.

The management ethos at Husqvarna is distinctly non-founder, institutional, and deeply influenced by the Wallenberg ownership model. Investor AB, the Wallenberg family's primary investment vehicle, holds approximately seventeen percent of the capital but significantly more voting power through Husqvarna's dual share class structure—A shares carry higher voting rights than the widely traded B shares. The Wallenberg Foundations control roughly twenty-three percent of Investor AB's capital and fifty percent of its votes, creating a chain of influence that runs from one of Sweden's most storied industrial dynasties through to Husqvarna's boardroom.

What does Wallenberg ownership mean in practice? It means "permanent capital"—a phrase that gets thrown around loosely in investing circles but has genuine substance here. The Wallenberg family has been investing in Swedish industry for over a century through entities like Investor AB, and their time horizon is measured in decades, not quarters. For Husqvarna, this translates into the freedom to make ten-year bets on robotics and battery technology while competitors are forced to chase quarterly gasoline margins to satisfy impatient public market shareholders. The Gardena acquisition, the Orbit deal, the deliberate cannibalization of petrol revenue—none of these strategies would be palatable to a typical activist-influenced board focused on near-term earnings per share. The Wallenberg presence on the board provides the air cover for management to sacrifice short-term profitability in pursuit of long-term competitive positioning.

The Sustainovate program, launched as a formal framework, tied executive compensation to three pillars: carbon reduction (targeting a thirty-five percent absolute reduction in CO2 emissions by 2025 against a 2015 baseline, aligned with the Paris Agreement's 1.5-degree target), circular innovation (fifty circular product innovations by 2025), and people empowerment (five million customers and colleagues enabled to make sustainable choices). By 2021, the company had already achieved a twenty-seven percent reduction in emissions, suggesting the carbon target was within reach. An additional SEK 4 billion in savings was targeted through 2030, extending the transformation runway.

The second-largest shareholder, L E Lundbergföretagen AB, holds approximately 7.6 percent of the capital, followed by Handelsbanken Asset Management at around four percent. The concentrated ownership structure—with the top two shareholders controlling roughly a quarter of the equity—means that management has clear, identifiable principals to answer to, rather than the diffuse and often contradictory demands of a widely held shareholder base. This is a governance advantage that is easy to underestimate until you compare it with the strategic paralysis that afflicts many publicly traded industrials trying to manage similar transformations.

VII. The Playbook: Hamilton's 7 Powers and Porter's 5 Forces

Every great business story eventually comes down to a simple question: can the company defend what it has built? Husqvarna generates impressive revenue and holds leading market positions, but the real test is whether those positions are protected by structural advantages that competitors cannot easily replicate. Two frameworks—Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces—provide complementary lenses for evaluating Husqvarna's competitive durability.

Start with Helmer's framework. The most relevant power for Husqvarna is Cornered Resource—specifically, the accumulated intellectual property and operational know-how around autonomous mowing. Husqvarna has been building robotic mowers since 1992. That is over thirty years of patent filings, engineering iterations, failure analysis, and real-world data on how robots navigate complex terrain—slopes, narrow passages, uneven ground, garden obstacles. The company has shipped millions of Automower units across dozens of countries, each one generating data that feeds back into product improvement. When a Chinese startup enters the robotic mower market in 2024 with a slick direct-to-consumer product, it is competing against three decades of accumulated knowledge that cannot be purchased or reverse-engineered overnight. The EPOS satellite navigation system alone represents years of development in RTK positioning technology adapted specifically for the constraints of autonomous mowing—low-speed, high-precision, outdoor environments where GPS signals bounce off buildings and trees.

The second power is Switching Costs, and this is where the Gardena ecosystem becomes strategically critical. The Gardena Smart System connects robotic mowers, irrigation controllers, soil moisture sensors, and weather stations through a single app. Each device a homeowner adds to the system increases the value of the whole—the mower knows when the sprinklers are running and avoids those zones; the irrigation controller checks the weather forecast and skips a watering cycle before a rainstorm. Once a customer has invested in three or four connected Gardena devices, the cost of switching to a competitor's product is not just the price of the new device—it is the loss of all the integrations, automation rules, and usage data that make the ecosystem valuable. This is the "smart home lock-in" that technology companies have been pursuing for years, applied to the garden.

Brand is the third power, and it operates differently across Husqvarna's two primary markets. In the professional segment, the Husqvarna orange is a mark of trust earned over decades of performance in the forest. Professional loggers and arborists choose their chainsaw the way surgeons choose their scalpel—based on feel, reliability, and the confidence that the tool will not fail at a critical moment. That kind of brand loyalty is not built through advertising; it is built through tens of thousands of hours of use in extreme conditions. In the consumer segment, Gardena occupies a similar position in European garden care—the turquoise brand is the default choice for quality-conscious homeowners, and the retail distribution network (garden centers, DIY stores, e-commerce) provides the kind of shelf presence that creates a self-reinforcing visibility advantage.

Now apply Porter's 5 Forces to stress-test the bull case. The most pressing competitive threat is the Threat of Substitutes, specifically from low-cost Chinese manufacturers. Companies like Worx (owned by Positec), Mammotion, and Segway have entered the robotic mower market with aggressive pricing and, in some cases, wire-free navigation technology from launch. Segway's Navimow, marketed as the "world's first ultra-quiet borderless intelligent mower" when it debuted in September 2021, went wire-free before Husqvarna brought its consumer NERA line to market. Mammotion's Luba series offers purely autonomous navigation at price points that significantly undercut the Automower range. The question is not whether Chinese competitors can make functional robotic mowers—they clearly can. The question is whether Husqvarna's premium positioning, ecosystem effects, service network, and thirty years of reliability data are enough to justify a significant price premium as the hardware itself becomes increasingly commoditized.

Competitive Rivalry is intense and multi-directional. Stihl, the privately held German powerhouse, is Husqvarna's most direct competitor in professional forestry and gardening tools. Stihl's iMOW robotic mower line competes at similar price points, and the company is investing heavily in battery technology—a new battery factory in Romania was scheduled to open in 2025, with a target of thirty-five percent of sales from battery products by 2027. John Deere represents a different kind of threat: the agricultural machinery giant unveiled an autonomous commercial zero-turn mower at CES 2025, featuring a battery-powered system with a sixty-inch deck, GPS mapping, sensor navigation, and multiple cameras for obstacle detection. Deere's commercial release, targeted for around 2026, would bring serious competition to the professional landscaping segment where Husqvarna has been building its autonomous fleet management platform. Stanley Black & Decker, after acquiring MTD in 2021, now controls the Cub Cadet, Troy-Bilt, and Hustler brands, and its Cub Cadet XR5 3000 robotic mower has won industry awards.

The Bargaining Power of Buyers varies by segment. Professional customers—landscaping companies, forestry operations—have moderate bargaining power. They are price-sensitive but also quality-dependent, and the cost of equipment failure (a chainsaw that stalls mid-cut, a mower that damages a client's lawn) is high enough to justify premium pricing. Consumer buyers have higher bargaining power, particularly in the mass market where robotic mowers from Chinese manufacturers offer "good enough" performance at half the price.

Supplier Power is generally moderate. Husqvarna sources batteries, semiconductors, and electronic components from a global supply chain that has experienced significant disruption in recent years. The shift from gasoline engines (where Husqvarna had deep in-house expertise) to battery systems (where it depends on cell manufacturers) introduces a new supply chain dependency that did not exist a decade ago.

Threat of New Entrants is the wild card. The robotic mower market is attracting entrants from adjacent industries—consumer electronics companies, automotive technology firms, and venture-backed startups—who see autonomous outdoor robots as a natural extension of the smart home ecosystem. The barriers to entry for basic robotic mowers are relatively low; the barriers to entry for a comprehensive ecosystem with fleet management, satellite navigation, and a global service network are significantly higher.

The net assessment is that Husqvarna's competitive position is strong but not unassailable. The company's moat is widest in professional products and narrowest in consumer robotics, where Chinese manufacturers are innovating rapidly and competing aggressively on price. The ecosystem strategy—tying mowers, irrigation, sensors, and fleet management into an integrated platform—is the most promising path to defensibility, but it requires continued investment and flawless execution at a time when the company is also managing a costly transition away from petrol products.

VIII. Recent History: The Orbit Acquisition and the Battery Pivot

In October 2021, as the world was still riding the post-pandemic boom in home improvement spending, Husqvarna announced the acquisition of Orbit Irrigation for USD 480 million on a cash and debt-free basis. Orbit, purchased from private equity firm Platinum Equity, was the leading residential watering brand in North America, with net sales of approximately USD 320 million in the twelve months preceding the deal. The B-hyve smart watering platform—Orbit's connected irrigation controller—had grown from 220,000 connected devices in 2019 to 1.4 million by the time of acquisition, demonstrating the kind of adoption curve that justified a technology-inflected valuation.

The strategic logic was straightforward: Gardena dominated residential watering in Europe but had minimal presence in the United States, the world's largest market for lawn and garden products. Orbit filled that gap. The combined entity became the global leader in residential watering, with Gardena's European strength complementing Orbit's North American distribution. The deal also brought smart watering technology that could be integrated into the Gardena Smart System ecosystem, extending the connected garden platform across the Atlantic.

The valuation benchmarks deserve scrutiny. At USD 480 million for a company generating roughly USD 320 million in sales, Husqvarna paid approximately 1.5 times revenue—a multiple that looked reasonable by industrial standards but elevated by the fact that it was executed at the peak of the 2021 tech-valuation bubble, when anything with "smart" or "connected" in its description commanded a premium. Comparable smart home and IoT deals in 2021 were closing at significantly higher revenue multiples, which makes the Orbit price look disciplined by the standards of the era. But the counter-argument is that Orbit was fundamentally a hardware business with a nascent connected platform, not a high-growth SaaS company, and 1.5 times revenue for a consumer irrigation business is not obviously cheap.

The jury remains out on Orbit. The acquisition expanded Husqvarna's geographic footprint and added connected technology, but the US residential watering market proved more cyclical than expected as the post-pandemic home improvement boom faded and rising interest rates dampened housing turnover. Gardena, which now houses the Orbit business, experienced a ten percent organic sales decline in 2025—a decline that reflected both broader market weakness and the challenge of integrating a US acquisition during a period of consumer belt-tightening. The long-term value of the deal depends on whether the B-hyve platform can become the foundation for a broader smart garden ecosystem in North America, similar to what Gardena has built in Europe.

The battery pivot, meanwhile, has become the defining strategic initiative of the current era. The decision, announced formally in the fall of 2022, was to intentionally "kill" the petrol-powered consumer business. This was not a gradual phase-out or a hedge-your-bets strategy. Husqvarna committed to exiting approximately SEK 2 billion in annual petrol consumer product sales by 2024—deliberately walking away from revenue that was still profitable in order to accelerate the transition to battery and robotic products.

The mechanics of the pivot are worth understanding in detail, because they illustrate the tension between short-term financial performance and long-term competitive positioning. Petrol consumer products—lawnmowers, trimmers, leaf blowers powered by gasoline engines—were a mature business with established margins. Customers knew the products, dealers stocked them, and the supply chain was optimized over decades. Abandoning this revenue meant closing production lines, eliminating roughly 1,000 positions (primarily in petrol product manufacturing), and accepting several years of declining top-line revenue while the replacement battery and robotics products ramped.

The financial results reflect this trade-off. Group net sales fell from SEK 53.3 billion in 2023 to SEK 48.4 billion in 2024 and SEK 46.6 billion in 2025. Some of this decline was currency-related, and some reflected broader market weakness, but a significant portion was the deliberate exit from petrol consumer products. Operating margins, while improved from the trough, remain under pressure as the company invests in the new product lines that are supposed to drive the next phase of growth. The operating margin excluding items affecting comparability was 6.2 percent in 2025—respectable for an industrial company in transition, but well below the double-digit margins that would signal the transformation is complete.

The bull case for the battery pivot rests on two arguments. First, the regulatory environment is moving decisively against petrol-powered garden equipment. California banned the sale of new gas-powered lawn equipment starting in 2024, and similar regulations are advancing across Europe. Companies that cling to gasoline for too long will find themselves on the wrong side of regulatory trends, while early movers like Husqvarna will have established battery product lines and dealer networks. Second, battery products carry the potential for higher long-term margins because they are simpler (fewer moving parts, lower maintenance costs), more software-intensive (connected features justify premium pricing), and more likely to generate recurring service revenue through fleet management platforms.

The bear case is that the transition is expensive, the revenue decline is real, and the competitive landscape for battery-powered garden equipment is intensifying rapidly. Every major competitor—Stihl, Stanley Black & Decker, Deere, and the Chinese manufacturers—is investing in battery technology simultaneously. The first-mover advantage that Husqvarna built in robotic mowers may not translate to battery handheld tools, where the technology is more commoditized and the barriers to entry are lower.

IX. Analysis: Bull vs. Bear

The fundamental question for investors evaluating Husqvarna is whether the company is in the early innings of a transformation that will create enormous value, or in the middle of a costly transition that will leave it stranded between two worlds—too expensive for the mass market, too slow for the technology frontier.

The Bear Case centers on commoditization. The robotic mower market that Husqvarna pioneered is no longer a one-company show. Chinese manufacturers are shipping wire-free robotic mowers at price points that are forty to sixty percent below the Automower range, with navigation technology that is, in many cases, comparable to or ahead of Husqvarna's current consumer offerings. Segway went wire-free before Husqvarna did in the consumer market. Mammotion's products have received enthusiastic reviews from technology media. The pattern is familiar from every hardware category that Chinese manufacturers have entered: initial products may lack polish, but the price-performance ratio improves relentlessly, and within a few product generations, the "premium" incumbents find their differentiation eroding.

Beyond robotics, the cyclicality of the housing market poses a structural risk. Garden spending is fundamentally tied to homeownership and housing turnover. When interest rates rise and housing transactions slow—as they did in 2023 and 2024—discretionary garden purchases decline, and even committed gardeners defer the purchase of a multi-thousand-dollar robotic mower. Husqvarna's revenue decline from SEK 53.3 billion to SEK 46.6 billion over two years reflects this sensitivity, and there is no guarantee that the next housing cycle will be as favorable as the pandemic-era boom that inflated garden spending to unsustainable levels.

The financial cost of the transformation is also non-trivial. The company is investing an incremental SEK 400 million per year in robotics and battery products while simultaneously absorbing the revenue loss from exiting petrol consumer products. Net debt stood at SEK 11.8 billion at the end of 2025 with a net debt-to-EBITDA ratio of 2.1 times—improved from 2.5 times a year earlier but still elevated for an industrial company navigating a major strategic pivot. If the transformation takes longer than expected or the competitive environment deteriorates, the balance sheet provides less cushion than investors accustomed to fortress balance sheets might prefer.

The Bull Case is built on the "Autonomy Premium"—the idea that Husqvarna is not just selling tools but building the operating system for the smart outdoor environment. If the Automower becomes the default platform for autonomous lawn care, connected to Gardena's irrigation ecosystem and managed through Fleet Services, then the hardware is merely the entry point for a recurring relationship that generates software and service revenue for years after the initial sale. This is the razor-and-blade model elevated to a platform business, and if it works, the margins will look nothing like the six percent operating margin the company posts today.

The regulatory tailwind is real and accelerating. The global push to eliminate petrol-powered garden equipment is not a hypothetical future scenario—it is happening now, with California's ban already in effect and European regulators moving in the same direction. Every regulation that restricts gasoline-powered tools expands the addressable market for Husqvarna's battery and robotic products while stranding competitors who delayed the transition.

The Wallenberg ownership structure provides a competitive advantage that is difficult to quantify but impossible to ignore. The ability to take a decade-long view on strategic transformation—to accept short-term revenue declines and margin compression in pursuit of a fundamentally different business model—is a luxury that most publicly traded companies do not have. Stihl, as a privately held family company, has similar latitude, but Stanley Black & Decker, Deere, and the publicly traded Chinese manufacturers face quarterly earnings pressure that constrains their strategic flexibility.

On the M&A record: Gardena was a home run. The acquisition transformed Husqvarna's consumer platform, built an ecosystem with genuine switching costs, and generated returns that more than justified the 2007 purchase price despite the terrible timing relative to the financial crisis. Orbit remains an open question—the strategic logic was sound, but the execution has been challenged by market headwinds, and it is too early to render a definitive verdict.

Key KPIs to Watch: For investors tracking Husqvarna's transformation in real time, two metrics matter above all others. First, robotic mower sales as a percentage of total revenue—this is the single best indicator of whether the autonomy thesis is playing out. Robotic mower net sales reached SEK 7.2 billion in 2024, roughly fifteen percent of group revenue. If this number is not growing at double-digit rates annually and trending toward twenty-five percent or more of revenue over the next few years, the transformation story loses credibility. Second, share of electrified products in motorized sales—this stood at forty-four percent in 2024 against a target of sixty-seven percent. The pace of this metric's improvement reveals whether the gas-to-battery transition is proceeding on schedule or stalling.

A few second-layer considerations deserve mention. On the credit side, Husqvarna's improving leverage ratio (from 2.5 to 2.1 times net debt-to-EBITDA) signals financial discipline, but the absolute debt level remains something to monitor during a capital-intensive transition. On the ownership front, Investor AB's concentrated position provides stability but also means that any shift in the Wallenberg family's strategic priorities could have outsized impact on Husqvarna's governance. The dual share class structure, while common among Swedish industrials, gives the Wallenberg-controlled A shares disproportionate voting power relative to the B shares that most public investors hold—a governance asymmetry that some international investors view skeptically. On the competitive front, John Deere's entry into autonomous commercial mowing—backed by the company's massive R&D budget and existing dealer network—represents the most credible competitive threat to Husqvarna's professional robotics business and warrants close monitoring as Deere moves toward commercial launch.

X. Epilogue: The Next 300 Years

There is something deeply counterintuitive about a 337-year-old company being at the cutting edge of autonomous robotics. In the technology industry's mythology, disruption comes from garages in Palo Alto and dorm rooms in Cambridge, not from factories beside Swedish waterfalls that have been operating since the Baroque period. But Husqvarna's story challenges that mythology in a way that is worth sitting with.

The company's survival through more than three centuries of technological upheaval—from muskets to sewing machines, from motorcycles to chainsaws, from gasoline engines to satellite-navigated robots—is not an accident of corporate inertia. It is the product of a specific institutional design: concentrated, patient ownership that tolerates short-term disruption in exchange for long-term positioning; a culture of mechanical precision that transfers across product categories; and a willingness to cannibalize existing businesses when the technological direction becomes clear.

The current transformation—from petrol to battery, from manual tools to autonomous robots, from one-time hardware sales to recurring service platforms—is the latest chapter in a story that has been repeating for centuries. The tools change, the underlying logic does not. Husqvarna has always been a company that masters the dominant manufacturing technology of its era and then pivots to the next one before the old technology becomes obsolete. The question for investors is whether the current generation of leadership can execute this particular pivot with the same discipline and precision that their predecessors brought to every previous one.

The answer will not be found in quarterly earnings reports or annual revenue figures. It will be found in the adoption curves of wire-free robotic mowers, in the conversion rates of Fleet Services from free platform to paid subscription, in the pace at which professional landscapers replace their petrol fleets with battery-powered equipment managed through Husqvarna's cloud. These are the leading indicators that will determine whether Husqvarna's next century looks like its last three—a relentless succession of reinventions, each one building on the capabilities of the one before.

In the end, Husqvarna is the anti-startup. It does not move fast and break things. It moves deliberately, builds things that last, and waits—sometimes for decades—until the market is ready for what it has created. The Automower was a curiosity for fifteen years before it became a business. The wire-free navigation technology took five years to migrate from professional to consumer products. The fleet management platform is still in its free-adoption phase, with monetization somewhere in the future. This is a company that operates on a timescale that most investors cannot match, backed by owners who can.

Whether that patience will be rewarded in the age of Shenzhen speed is the central investment question. But if three centuries of history offer any guide, betting against Husqvarna's ability to reinvent itself has been a losing proposition since the days of the Swedish Empire.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube