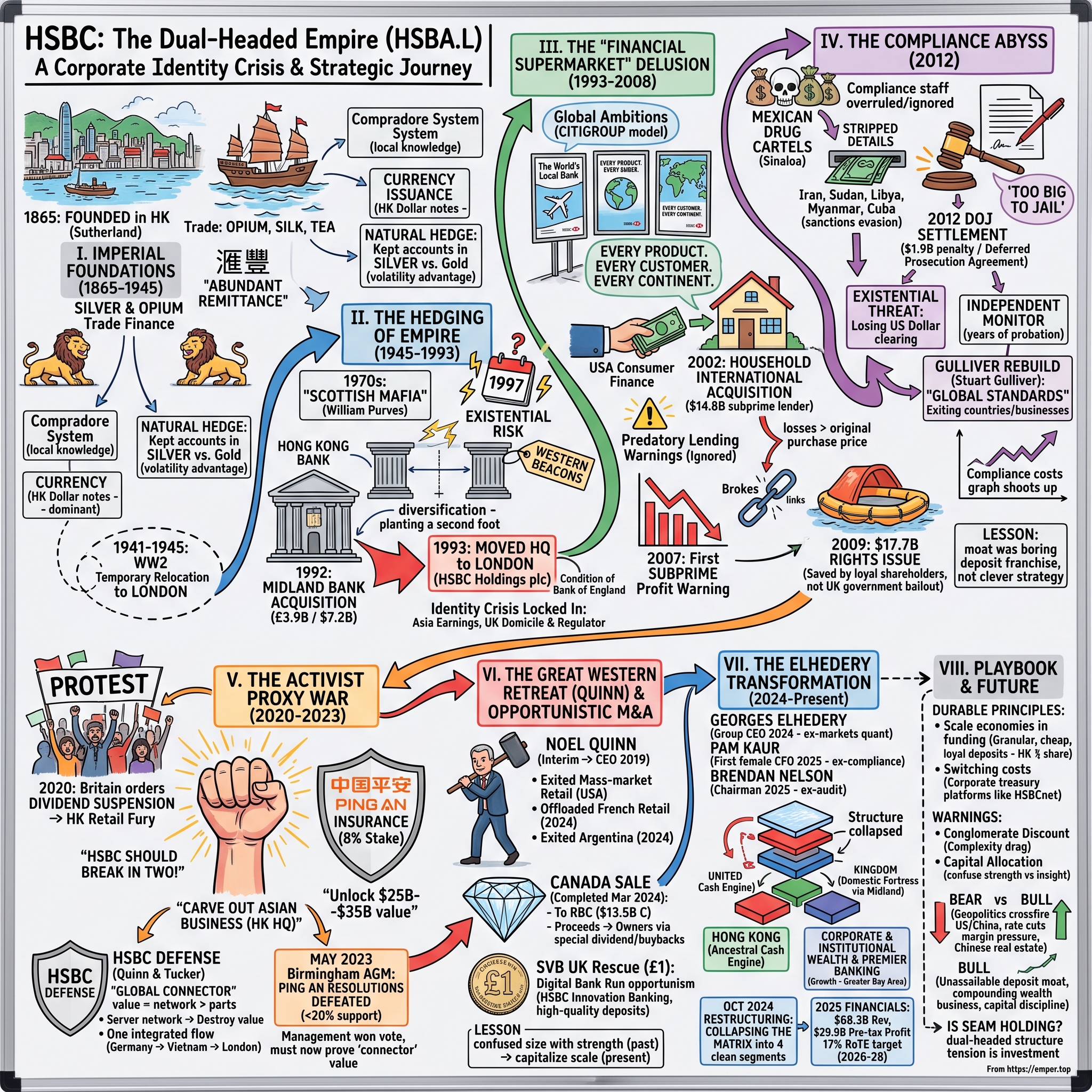

HSBC: The Dual-Headed Empire

I. Introduction & Episode Roadmap

Walk into the marble banking hall at 1 Queen's Road Central in Hong Kong and you are greeted by two bronze lions. The locals call them Stephen and Stitt, after two long-dead bankers, and for more than a century Hong Kong residents have rubbed their paws for luck before making a deposit. During the Japanese occupation of the Second World War, the lions were shipped to Osaka to be melted down for scrap; they were rescued at the last moment, returned, and one still bears the pockmarks of shrapnel from the 1941 battle for the colony. Those two scarred lions are the perfect emblem for the institution that guards them — an organization that has survived war, revolution, currency collapse, and its own spectacular mistakes, and yet has never quite decided which continent it belongs to.

That is the puzzle at the heart of this story. How did a bank founded in colonial Hong Kong in 1865 to finance the opium, silk, and tea trades of the China coast become Europe's largest financial institution — an entity that in its 2025 financial year reported roughly $68.3 billion of revenue and $29.9 billion of pre-tax profit, sitting atop one of the largest deposit bases in the world?1 And how does that bank make the overwhelming majority of its money in Asia while keeping its headquarters, its regulator, and its tax residency five thousand miles away in London?

This is the ultimate corporate identity crisis. HSBC Holdings plc trades on the London Stock Exchange under the ticker HSBA.L, answers to the United Kingdom's Prudential Regulation Authority, and yet earns the lion's share of its profits in Hong Kong and the wider Asian region. It is a British bank with a Chinese soul, or a Chinese bank in a British suit, depending on who you ask — and for the last several years, that ambiguity has been the single most contested question in global finance.

To grasp the strangeness of that arrangement, consider the mechanics of a single ordinary transaction. A German auto-parts maker sells components to a Vietnamese assembler. The invoice is denominated in US dollars. The financing runs through a trade facility booked in Hong Kong; the currency risk is hedged on a desk in London; the dollars themselves clear through New York. Four jurisdictions, three currencies, one bank — and for a century and a half HSBC has specialized in being the institution that stitches those flows together. That capability is the bank's crown jewel and, as we will see, the reason it has repeatedly refused to break itself apart even when its own largest shareholder demanded it. It is also the reason a compliance failure on one continent can threaten the entire enterprise on another. Connectivity cuts both ways.

The people now trying to resolve it are a new guard. Group Chief Executive Georges Elhedery, a former markets trader with a mathematician's temperament, took the top job in 2024 and immediately set about dismantling the sprawling matrix that HSBC had built over decades. Alongside him sits Pam Kaur, appointed the bank's first-ever female Group Chief Financial Officer.2 Together they have collapsed a bewildering structure of overlapping global businesses and geographic regions into four clean segments: Hong Kong, the United Kingdom, Corporate and Institutional Banking, and International Wealth and Premier Banking. The wager behind that reorganization is that decades of accumulated complexity have been quietly taxing the bank's returns, and that a simpler HSBC can finally be valued for the cash machine its supporters insist it is.

Over the course of this story we will trace how HSBC got here: the imperial foundations built on silver and colonial privilege; the fateful decision to hedge the 1997 handover by buying a British bank and moving to London; the ruinous American subprime adventure that nearly consumed the group; the compliance abyss of 2012, when the bank came within a whisker of losing its license to clear US dollars; the extraordinary boardroom war waged by China's Ping An Insurance to break the bank in two; and the great Western retreat that followed. It is a story about the value — and the cost — of trying to be, as HSBC's own advertising once boasted, "the world's local bank." Let us begin where the bank began: on the waterfront of a young colony, in the age of empire.

II. The Imperial Foundations: Opium, Silver, and Currency Issuance (1865–1945)

In the early 1860s, the merchants of the China coast had a problem. Trade between Europe, India, and the treaty ports of China was booming — tea and silk flowing west, cotton and, notoriously, opium flowing east — but the banking that financed it all was run out of Bombay and London by institutions with no real understanding of local conditions. When a Scottish shipping executive named Thomas Sutherland, superintendent for the Peninsular and Oriental Steam Navigation Company in Hong Kong, heard that a group of Bombay financiers planned to float a "Bank of China" with almost no shares reserved for local subscribers, he decided the merchants of Hong Kong and Shanghai should have a bank of their own.3

The result opened its doors on March 3, 1865, capitalized at HK$5 million: The Hongkong and Shanghai Banking Corporation.3 The native brand that would eventually be stamped on branches across Asia was 滙豐 — characters that translate roughly as "abundant remittance," a name chosen for a business whose entire reason to exist was moving money across the vast distances of empire. From the very first day, this was not a European bank that happened to have an Asian office. It was native to the China coast, with its head office in Hong Kong and a founding board drawn from the trading houses that actually did business there.

It is impossible to tell this origin story honestly without naming what those trading houses actually traded. The commerce that HSBC was built to finance included opium — the narcotic that Britain had forced into China at gunpoint through two wars, and whose proceeds underwrote much of the wealth sloshing around the treaty ports. Silk and tea flowed one way; silver and opium flowed the other; and a bank that could discount the bills of exchange financing that trade, advance against cargoes, and remit the profits home stood to prosper regardless of the moral character of the goods on the ships. HSBC did not invent this system. It plugged itself into an existing web of commerce and made itself the indispensable clearing house for it — a reminder that the foundations of even the most respectable modern institutions are often laid in the rough soil of their age. The bank also leaned on the compradore system, the network of Chinese middlemen who bridged the language and trust gap between foreign banks and local merchants, extending HSBC's reach far beyond what a handful of British managers could ever have achieved alone. This hybrid identity — foreign capital, local knowledge — is the original version of the "world's local bank" idea, more than a century before the slogan was coined.

That local rooting turned out to be a structural advantage of the first order, because nineteenth-century Asia ran on silver while the West was moving to gold. When the price of silver collapsed against gold in the 1870s and beyond, Western banks with gold-denominated books were whipsawed. HSBC, by contrast, kept its accounts in silver, matching the currency its customers actually used, and rode the volatility that ruined others. Think of it as a natural hedge: because both the money the bank took in and the money it paid out were denominated in the same metal its customers earned and spent, swings in the gold-silver exchange rate that devastated others simply washed through HSBC's books without breaking them. It learned early a lesson it would relearn painfully in later centuries: a bank that matches its funding to the real economy it serves is far harder to kill than one chasing yield in a market it does not understand.

The bank grew outward from Hong Kong and Shanghai in concentric rings — Yokohama, Calcutta, Manila, Singapore, San Francisco, and eventually London — building a branch network that mirrored the trade routes of the era. Each branch was less an outpost of a British head office than a node in a merchant network, financing whatever moved through its port. This geographically distributed, semi-autonomous structure would become HSBC's signature organizational form, the ancestor of the "matrix" that later chief executives would alternately praise and curse. For most of the bank's first century it was a strength: local managers who knew their markets, backed by the credit of a group that spanned the trade lanes of Asia.

The second, deeper source of advantage was political. HSBC made itself indispensable to the British colonial government, effectively acting as banker to the state in Hong Kong and, crucially, becoming the dominant issuer of Hong Kong dollar banknotes. This was no small privilege. By 1940, roughly 80 percent of the Hong Kong dollars in circulation were printed by the Hongkong and Shanghai Bank, and the note issue had swollen from HK$50 million in 1927 to HK$200 million in 1940.3 To be the printer of a jurisdiction's physical money is to occupy a position no competitor can simply buy or build — a franchise granted by the sovereign. That privilege endures today: HSBC still issues the majority of Hong Kong's banknotes, its name and one of those bronze lions printed on notes that pass through millions of hands every day. It is, in the language of modern strategy, a cornered resource, and it has been feeding the bank's reputation and low-cost deposits for a century and a half.

Then came the near-death experience. When Japanese forces overran Hong Kong in December 1941, they seized the bank's headquarters in Central and interned its senior managers; the chief manager, Vandeleur Grayburn, died in captivity. With the nominal seat of the bank under enemy occupation, the surviving group head, Arthur Morse, took the extraordinary step of relocating HSBC's head office to London for the duration of the war — a temporary, wartime London domicile that foreshadowed, eerily, the permanent one to come half a century later. When the war ended, the bank returned to Hong Kong and threw itself into financing the colony's transformation, bankrolling the mainland refugees who arrived with little more than machinery and ambition and turned Hong Kong into a manufacturing powerhouse. For investors, the lesson of this era is foundational: HSBC's deepest moat was never clever financial engineering. It was a privileged, sovereign-granted position in one specific place — and the question that has haunted the bank ever since is whether it could ever build anything as durable anywhere else.

III. The Hedging of Empire: The Midland Merger and Relocating to London (1945–1993)

By the late 1970s, the men running HSBC from the top floors of its Norman Foster-designed Hong Kong headquarters — first Michael Sandberg, later the granite-hard Scot William Purves, a decorated Korean War veteran known for his flinty candor — were staring at a single terrifying date on the calendar: 1997. Under the terms agreed between London and Beijing, sovereignty over Hong Kong would revert to the People's Republic of China. For a bank whose entire existence was bound up with a single colonial city, this was not an abstract geopolitical risk. It was an existential one. What is a Hong Kong bank worth if Hong Kong itself is about to change hands?

Purves in particular embodied the culture of the place. He belonged to what insiders half-affectionately called the "Scottish mafia" — the generations of Scots who had run HSBC since Sutherland's day — and he ran the bank with a frugality and directness that became legendary. He understood, better than almost anyone, that a bank whose fortunes were tethered to a single city about to change sovereign masters was carrying a concentration risk no amount of profitability could offset. The colony was booming; that was precisely the problem. A single political event, now scheduled and certain, could impair the entire franchise overnight. No prudent board could sit still.

The strategic answer was to diversify away from that concentration — to plant a second foot in a stable, rule-of-law jurisdiction large enough to matter. HSBC had already been shopping. It had tried and failed to buy the Royal Bank of Scotland in the early 1980s, and it had picked up Marine Midland in the United States, giving it an American beachhead. But the prize it kept circling was Midland Bank, one of Britain's historic "Big Four" clearing banks, in which it took a minority stake in 1987. Midland was a wounded giant. It had made catastrophic loans to Latin American sovereigns during the debt crises of the era, and it had compounded the damage with a disastrous foray into American banking of its own. Its share price was a shadow of its former self. For HSBC, that weakness was the opportunity — a chance to acquire a national clearing franchise at a fraction of what it would have cost in healthier times.

The endgame came in 1992 and it was pure drama. HSBC made a friendly offer for Midland in March. The following month, Lloyds Bank crashed in with a larger, hostile counter-bid, turning a quiet courtship into a public brawl. Purves refused to be outmaneuvered and, in June, put an end to the fight with a 480-pence-per-share offer, prompting Lloyds to walk away.3 The final price was roughly £3.9 billion — about US$7.2 billion — and the deal nearly doubled the group's assets, from around £86 billion to £170 billion.3 For a bank buying a struggling franchise at a discount to its former glory, the arithmetic looked shrewd.

But the real point of the Midland deal was never the price. It was structural insurance. And the price of that insurance turned out to be the bank's own domicile. Britain's regulator, the Bank of England, was not willing to let a Hong Kong-headquartered institution swallow one of the country's core clearing banks while sitting beyond its supervisory reach. The condition it imposed was blunt: if HSBC wanted to own a major British bank, it would have to establish a UK-incorporated holding company — HSBC Holdings plc — and move its group head office to London.3 In January 1993, that is exactly what happened. HSBC Holdings plc was created as the new parent, with the old Hongkong and Shanghai Bank reduced to a subsidiary, and the group's brain was transplanted from the harbor of Hong Kong to the City of London.3

It is hard to overstate the long shadow this cast. In one move, HSBC hedged its Hong Kong risk and acquired a British retail franchise — a genuine diversification win, and one that gave the group a second home market with millions of stable retail customers and a national branch network. But the deal also imported problems along with the prize. Midland was not a good bank; it was a cheap one, and integrating a demoralized, underperforming British clearer took years of patient work before it began to earn its keep. More consequentially, the move created the structural contradiction that would define the next thirty years: a bank that earned its keep in Asia, governed and regulated in Britain, with a head office five time zones from its profit center.

The deeper irony is that the hedge worked exactly as intended and yet planted the seeds of every future crisis. When Hong Kong's handover finally came in 1997, it passed without the catastrophe HSBC's board had feared, and the bank's Asian franchise not only survived but thrived under Chinese sovereignty. The insurance policy, in other words, never had to pay out on the specific risk it was bought to cover. What it did instead was reshape HSBC's entire identity and appetite. A group now headquartered in London, listed in London, and hungry to justify its new Western center of gravity would spend the following decade looking for ways to grow in the West — and that hunger would lead it, fatefully, across the Atlantic. Every subsequent chapter of this story — the American misadventure, the compliance disaster, the activist war over whether to split the bank — flows directly from the geography that the Midland deal locked in. HSBC had bought itself a hedge. It had also bought itself a permanent identity crisis, and the bill for that crisis would come due again and again.

IV. The "Financial Supermarket" Delusion: Household International & Subprime (1993–2008)

Newly domiciled in London and flush with the ambition that comes from doubling in size, HSBC spent the late 1990s and early 2000s chasing the dominant idea of the age. Everywhere bankers looked, the model to emulate was Citigroup: the "financial supermarket," a single global institution that would sell every product — retail deposits, credit cards, investment banking, insurance — to every customer on every continent. HSBC bought the dream wholesale, and it bought the marketing to match, plastering airports and magazines the world over with its famous, expensive "The World's Local Bank" campaign. The slogan was clever. The strategy behind it was about to become a cautionary tale.

The defining move came under Sir John Bond, the chairman who embodied HSBC's global-supermarket ambitions. Bond was a lifer, a man who had joined the bank as a teenager and worked his way up through Asia and the Americas over four decades, and he carried the conviction that HSBC's future lay in matching Citigroup blow for blow on the global stage. Under his "Managing for Growth" strategy the bank set out to build genuine scale in the world's largest economy, and consumer finance — lending to ordinary Americans — was the chosen vehicle.

In late 2002, HSBC agreed to acquire Household International, a large American consumer-finance company, in a deal valued at roughly $14.8 billion.4 Household was, in plain terms, a subprime lender — a machine for extending credit cards and home loans to Americans that mainstream banks would not touch. The investment thesis had a certain seductive logic on paper. HSBC controlled vast pools of cheap, sticky retail deposits in Hong Kong and Britain, funded at a near-zero cost. Household knew how to originate high-yielding American consumer loans. Marry the cheap funding to the fat yields, apply HSBC's supposedly superior risk management, and the spread would be enormous. To a board flush with confidence and eager to prove that its move to London had made it a truly global player, the logic was irresistible — which is precisely the emotional condition in which the most expensive mistakes in banking tend to be made.

There was a warning sign hiding in plain sight, and it was ethical as much as financial. Household had, shortly before the acquisition, agreed to a large multi-state settlement in the United States over predatory lending practices — the very business model HSBC was now buying into. A more skeptical acquirer might have read that settlement as a flashing red light about the quality of the company's loan book and the character of its underwriting. HSBC read it, instead, as a problem now cleaned up and priced in. That misreading would prove almost fatal.

The reality was that HSBC had bought a portfolio riddled with predatory lending and slack underwriting, and it had bought it at a moment when more disciplined players were already backing quietly away from subprime. This is the recurring pattern of the era's worst banking deals: an institution with a genuine strength in one domain — here, a fortress deposit base — convinces itself that the strength transfers to an adjacent market it does not actually understand. It did not. The credit culture that made HSBC formidable in Asian trade finance gave it no special edge in the American subprime consumer, and its confidence that it could tame Household's risk proved to be exactly the kind of hubris that precedes a fall.

The fall was historic. In February 2007, HSBC issued what is widely regarded as the first major subprime-related profit warning of the entire global financial crisis, driven by soaring losses at its American consumer-finance arm — an early tremor before the earthquake that would level the industry.5 It wrote down its subprime holdings by billions, and over the full arc of the disaster the cumulative losses tied to the Household business ran into the tens of billions of dollars.5 The very acquisition meant to prove HSBC's global-supermarket credentials instead became the largest destruction of shareholder value in its history.

By the time HSBC finally moved to wind down and shutter the bulk of the American consumer-finance business, closing its branch network and running off the toxic loan book, the cumulative damage tied to Household ran to a scale that dwarfed the original purchase price several times over.5 The lesson management would later draw — and that Ping An would one day throw back in its face — was that the West had been a graveyard for HSBC capital, while the East had quietly kept compounding.

And yet — here is the twist that reveals the bank's underlying nature — HSBC survived where others died. As Royal Bank of Scotland and Lloyds collapsed into the arms of the British state, HSBC never took a UK government bailout. It rescued itself the hard way, through a rights issue announced in March 2009 that raised roughly £12.5 billion, about US$17.7 billion, one of the largest such capital raisings London had ever seen.6 Who bought the shares that saved the bank? Overwhelmingly, its loyal shareholders in Hong Kong and Britain, drawing on the very deposit fortresses that the Household adventure had so recklessly ignored. There is a profound analytical point buried in that rescue. The thing that saved HSBC was not the clever global-supermarket strategy that Bond had pursued; it was the boring, ancient, deposit-taking franchise that the strategy had taken for granted. A bank's survival, it turns out, is determined less by the assets it chases in the good years than by the quality and stickiness of the funding it can call on in the bad ones. HSBC had both a lesson and a moat, written in the same event. It would not be the last time the two halves of the bank pulled in opposite directions — and the next crisis would not be about credit. It would be about crime.

V. The Compliance Abyss: Money Laundering and the 2012 DOJ Settlement

For most of its history, HSBC's decentralized structure had been treated as a feature, not a bug. The bank operated as a loose federation of regional franchises — Hong Kong, Britain, the Americas, the Middle East — each with a powerful local chief executive who ran his territory with enormous autonomy. Insiders called it "the matrix," and the theory was that local barons understood local markets better than any head-office committee in London ever could. In the boom years, that autonomy looked like wisdom. In 2012, it looked like something closer to negligence.

That year, a United States Senate subcommittee, followed by the Department of Justice, laid out in excruciating detail what the matrix had allowed to happen. HSBC's American and Mexican operations, investigators found, had moved staggering sums of money on behalf of Mexican drug cartels, including the notorious Sinaloa organization. Compliance staff who raised alarms about the flood of suspicious cash had been overruled or ignored. The detail that seared itself into the public imagination was almost cinematic: at some Mexican branches, launderers had reportedly built specially sized boxes to fit precisely through the teller windows, the better to slide bricks of drug cash across the counter. Beyond the cartel money, the bank had also systematically stripped identifying details from wire transfers to help clients in Iran, Sudan, Libya, Myanmar, and Cuba evade United States sanctions.

The reckoning came in December 2012. HSBC agreed to forfeit and pay approximately $1.9 billion and entered into a deferred prosecution agreement with the Department of Justice — at the time the largest penalty of its kind ever levied on a bank.[^7] But the fine, enormous as it was, was not the part that terrified HSBC's board. The truly existential threat was the one that hovered unspoken behind the negotiations: a full criminal indictment could have cost HSBC its ability to clear US dollars through the American financial system. For a bank whose entire value proposition is connecting global trade flows, losing access to dollar clearing would not have been a wound. It would have been a death sentence. That asymmetry — a modest fine set against the nuclear option of exclusion from the dollar — is precisely why the bank capitulated so completely, and why compliance stopped being a back-office afterthought and became a strategic obsession.

The settlement also ignited a political firestorm that outlived the fine itself. Critics in the United States Congress asked, pointedly, why no senior HSBC executive had been criminally charged when the bank had admitted to laundering cartel money and busting sanctions. The phrase that stuck was "too big to jail" — the uncomfortable suggestion that HSBC had been spared prosecution not because it was innocent but because indicting a bank of its systemic importance was deemed too dangerous to the financial system. As part of the deferred prosecution agreement, HSBC was placed under the supervision of an independent, court-appointed monitor who spent years embedded in the bank, scrutinizing its controls and reporting back to the authorities — an extraordinary imposition for a private company, and a daily reminder of how close it had come to the abyss. Only in late 2017, after five years of monitored probation, did the Department of Justice allow the deferred prosecution agreement to expire, and even then the reputational stain lingered.

The rebuild was sweeping and it fell to a new leadership team. The chief executive who inherited and cleaned up the mess was Stuart Gulliver, a former head of the markets business who took over in 2011 and spent much of the following decade in what amounted to a permanent restructuring — cutting businesses, exiting countries, and reorienting the entire organization around the mantra of "global standards." The theory of the old matrix, that local barons knew best, was inverted: from now on, HSBC would apply the strictest financial-crime standard it faced anywhere, everywhere. Among the executives brought in to reconstruct the bank's controls was Pam Kaur, who joined HSBC in April 2013 to lead internal audit and, later, financial-crime risk, beginning a rise that would eventually carry her to the office of Group CFO.2 Compliance headcount and spending exploded from a rounding error into a multi-billion-dollar annual line item, with tens of thousands of staff devoted to monitoring transactions and vetting customers. There is a genuine analytical irony buried here. The same global-connector model that made HSBC uniquely valuable — its ability to move money across dozens of jurisdictions — was also what made it uniquely exposed to being used as a laundry. The 2012 settlement forced the bank to prove it could police that network as effectively as it exploited it. The cost of that policing became a permanent tax on the business, a friction imposed on every legitimate corporate client, and a standing reminder that a bank as sprawling as HSBC is only ever as strong as its weakest branch. Within a few years, a very different kind of outsider would argue that the sprawl itself was the problem — and that the cure was to break the bank apart.

VI. The Activist Proxy War: Ping An's Split Campaign

The spark landed in the spring of 2020, and it landed on the streets of Hong Kong. As COVID-19 tore through the global economy, Britain's Prudential Regulation Authority ordered the country's large banks — HSBC among them — to suspend their dividends and conserve capital against the coming storm. For most of HSBC's shareholders this was a prudent, if unwelcome, precaution. For Hong Kong's retail investors it was a betrayal bordering on the sacrilegious. For generations, the HSBC dividend had been treated in Hong Kong not as a variable corporate distribution but as something close to a birthright — a reliable stream that grandmothers passed to grandchildren, as dependable as the notes the bank printed. Its sudden cancellation, decreed by a regulator in London, provoked public fury, protest, and a deep sense that the West had reached into Asian pockets.

There was a peculiarly personal dimension to Hong Kong's rage, captured by figures like Ken Lui, a Hong Kong insurance agent who organized thousands of small local shareholders into an activist bloc agitating for change. For these investors, HSBC stock was not a line in a diversified portfolio; it was a family heirloom, held for the dividend across generations, its suspension experienced as a household calamity. That grassroots fury was the tinder. What turned it into a genuine threat to the board was the arrival of a match.

Into that anger stepped one of China's most powerful financial institutions: 中国平安 Ping An Insurance, led by its founder-chairman 马明哲 Ma Mingzhe. Ping An is no ordinary shareholder — it is one of the largest insurers on earth, a sophisticated financial conglomerate managing the premiums of hundreds of millions of Chinese policyholders, and its investment arm had quietly become HSBC's largest single shareholder, amassing a stake of around 8 percent. In 2022 it went public with an audacious demand. HSBC, Ping An argued, should break itself in two — carving out and separately listing its Asian business, with a Hong Kong headquarters, as an independent entity.7 Coming from a Chinese state-adjacent institution of Ping An's heft, the proposal was impossible to dismiss as the noise of a gadfly. It had money, credibility, and a receptive audience of aggrieved Hong Kong retail holders behind it.

The case Ping An made was not frivolous, and this is what made it dangerous. Asia, the argument ran, was generating the overwhelming bulk of HSBC's profits while being forced to subsidize sluggish, low-returning Western retail operations. Free the Asian business, list it in Hong Kong, and the market would reward it with a far richer valuation — Ping An and its advisers floated numbers in the range of $25 billion to $35 billion of unlocked value. A separately listed Asian bank would also carry lower capital requirements, escape the drag of UK ring-fencing rules, and — the unspoken subtext — insulate the Asian crown jewels from the escalating geopolitical crossfire between Washington and Beijing. It was a coherent, quantified, activist thesis aimed squarely at the bank's central contradiction.

HSBC's management, led by Group CEO Noel Quinn and Chairman Sir Mark Tucker, fought back with equal conviction, and their defense rested entirely on a single idea: the "global connector." HSBC's real value, they argued, is not the sum of its geographic parts but the network that binds them.8 A multinational treasurer in Germany moving dollars to a supplier in Vietnam, financing a shipment with a letter of credit issued in Hong Kong and hedging the currency in London — that is one integrated flow running across a single bank's rails. Sever the Asian business from the Western one, management contended, and you do not create two healthy banks; you cut the international corridors that are the whole point, destroying network value that neither half could recreate alone. The connectivity, in this telling, was the moat, and Ping An's proposal was a plan to fill in the moat.

Management reinforced the argument with hard operational objections. Splitting the bank, they warned, would trigger enormous one-off costs, years of disruption, the loss of diversification benefits that lowered the group's funding costs, and a tangle of tax and regulatory complications — value destroyed today in exchange for a valuation uplift that might never materialize. To adjudicate the fight fairly, HSBC's board reviewed the structural options and concluded, unsurprisingly but with documented analysis, that a break-up would cost shareholders more than it created. Ping An, for its part, accused management of being defensive and self-interested, of protecting a London head office and a Western cost base at Asia's expense. Both sides had a point, which is what made the contest genuinely close-run rather than a foregone conclusion.

The showdown came at the May 2023 annual general meeting in Birmingham, after a bruising campaign in which HSBC lobbied its large Western institutional owners — the BlackRocks and Vanguards of the world — and worked to reassure its restive Hong Kong retail base with roadshows and town halls conducted in Cantonese. When the votes on the Ping An-aligned resolutions were counted, they were decisively defeated, drawing support well below 20 percent.9 Management had won, and won comfortably. But winning the vote settled nothing on its own. A skeptical investor could fairly point out that "trust us, the network is valuable" is an assertion, not a proof, and that a proxy defeat is not the same as a vindicated strategy. Having stared down the activist, Quinn now had to demonstrate that the global-connector model was worth more intact than in pieces — and the only way to prove it was to take an axe to the very Western operations Ping An had derided, exit them, and hand the proceeds back to shareholders. The war of words was over. The war of results had just begun.

VII. Noel Quinn's Great Western Retreat & Strategic M&A

Noel Quinn was, in many ways, the anti-showman — a Birmingham-born commercial banker who had spent decades in the unglamorous machinery of HSBC's business banking before improbably rising to the top job. Where his predecessors had chased the grand acquisition, Quinn made his name as a demolition contractor, methodically dismantling the sprawling empire that the financial-supermarket era had built. If the global-connector thesis was going to survive contact with skeptical shareholders, it needed proof in the form of capital returned, and Quinn spent his tenure supplying it.

Quinn's ascent had itself been improbable. He was named interim chief executive in 2019 after the abrupt departure of his predecessor John Flint, and he spent months auditioning for the permanent role in the most testing conditions imaginable — a pandemic, a dividend suspension, and an activist campaign all at once. That he won the job outright and then held it for five years is a testament to a temperament suited to demolition rather than empire-building: patient, unflashy, and comfortable delivering bad news. Where Bond had wanted HSBC to be everywhere, Quinn asked a colder question of every business in the portfolio — does this earn its cost of capital, and does it strengthen the network? If the answer to both was no, it was surplus.

The retreat from Western retail banking was systematic. HSBC pulled back from mass-market retail in the United States, exiting a business where it had never possessed real scale and refocusing on internationally mobile, high-net-worth clients — the sort of globally mobile customers who actually use the connector. It agreed to offload its French retail network, a perennial underperformer, to a Cerberus-backed vehicle, a deal that completed at the start of 2024 and required swallowing a painful accounting hit in exchange for freeing up capital long trapped in a low-returning franchise. And it exited Argentina, selling its operations there to Grupo Financiero Galicia in a deal that closed in late 2024, escaping a market whose chronic inflation and currency chaos made stable banking returns almost impossible and whose peso losses had become an annual embarrassment. Each disposal followed the same logic: if a business could not clear HSBC's cost of capital and had no strategic role in the connector network, it was for sale. Individually, none was transformative. Collectively, they amounted to a deliberate reshaping of the bank around its Asian and wholesale core — a de facto answer to Ping An's critique that stopped short of the break-up Ping An had demanded.

The crown jewel of the retreat was Canada. In a deal that completed on March 28, 2024, HSBC sold its Canadian banking arm to Royal Bank of Canada for roughly C$13.5 billion.1213 This was capital allocation at its sharpest. HSBC Canada was a perfectly good, profitable bank — but it was subscale in a market dominated by entrenched domestic giants, and RBC was willing to pay a premium to eliminate a competitor and bulk up at home. HSBC sold a non-core asset at a rich multiple, at a moment of strength, to a strategic buyer who valued it more. The proceeds flowed straight back to owners in the form of a special dividend and expanded share buybacks — precisely the kind of tangible return that a skeptic demanding a break-up could not easily wave away. Whatever one thinks of HSBC's strategy, the Canada sale was the clearest evidence yet that this management team could distinguish between a business it should own and one it should monetize.

If Canada showed HSBC's discipline as a seller, the other headline deal of the era showed its opportunism as a buyer — and it cost precisely one pound. The weekend of March 10-13, 2023, was one of the most frightening in recent banking history. Silicon Valley Bank in California, the lender of choice for America's technology and venture ecosystem, collapsed in a lightning-fast digital bank run, and the panic jumped the Atlantic almost instantly. Its British subsidiary, Silicon Valley Bank UK, held the operating deposits of a large slice of the country's startups, and as those companies scrambled to pull their money out on the Friday and Saturday, the very real prospect emerged that thousands of British tech firms would be unable to make payroll on Monday. Chancellor Jeremy Hunt and the Bank of England worked through the night to broker a rescue, and in a frantic, dawn auction, HSBC swooped in and acquired SVB UK for £1.1011

For that nominal sum, HSBC inherited the banking relationships of thousands of the UK's fastest-growing startups and the venture and private-equity funds behind them, complete with the kind of cheap, high-quality operating deposits that any bank covets. Rebranded as HSBC Innovation Banking, it was an organic customer-acquisition coup executed at the bottom of a crisis, with essentially no premium paid — the mirror image of the Household disaster a generation earlier, when the bank had paid top dollar for a book it did not understand. Here it paid nothing for a book everyone else was too frightened to touch, and it did so precisely because its trillion-dollar deposit base and fortress balance sheet made it one of the few institutions on earth able to absorb SVB UK overnight without blinking. Scale, in that moment, was not a burden but a weapon. Together, the Canada sale and the SVB rescue framed the capital-allocation philosophy Quinn was bequeathing to his successor: sell dear, buy cheap, and never again confuse size with strength. That successor was already in the building, and he had very different instincts about how the bank should be shaped.

VIII. The Elhedery Transformation: Collapsing the Matrix

Georges Elhedery does not fit the mold of a traditional British bank chief executive, and that is rather the point. Lebanese-French, a polyglot who reportedly speaks several languages including Arabic and Mandarin, he trained as an engineer at France's elite École Polytechnique before building his career on the trading floor, running HSBC's markets and securities-services business before a spell as Group CFO. There is a revealing detail in his biography: in 2022, while a senior executive, he took a six-month sabbatical, part of it reportedly devoted to intensive study of Mandarin — an unusual move for a banker on the CEO track, and one that signaled both personal discipline and a clear-eyed reading of where HSBC's future lay. Colleagues describe a clinical, numbers-driven operator with the temperament of a quant — someone more comfortable with a spreadsheet of capital-allocation trade-offs than a photo opportunity. When he became Group CEO in September 2024, the market understood the appointment as a signal: HSBC was done apologizing for its complexity and was going to attack it head-on.15

Elhedery moved with striking speed. Within weeks of taking over, in October 2024, he unveiled the most significant restructuring of HSBC's organizational architecture in decades.14 The historic matrix — three overlapping "global businesses" laid across five geographic regions, a structure that generated endless duplication, internal negotiation, and management layers — was to be swept away. In its place, effective from January 1, 2025, the bank would be run as four clean segments.14 Two are geographic strongholds: Hong Kong, the ancestral cash engine, and the United Kingdom, the domestic retail-and-commercial fortress acquired via Midland a generation earlier. Two are global lines: Corporate and Institutional Banking, serving wholesale trade, transaction banking, and institutional clients worldwide, and International Wealth and Premier Banking, targeting affluent individuals outside the two home markets, with particular focus on the 粤港澳大湾区 Greater Bay Area and the cross-border Wealth Management Connect scheme linking Hong Kong with Guangdong.

To run this new structure, Elhedery assembled a leadership team weighted heavily toward risk, audit, and control — a telling choice for an institution still shadowed by 2012. Pam Kaur became Group CFO effective at the start of 2025, the first woman to hold the role; her deep grounding in risk and financial-crime compliance was pitched as a credential that would carry weight with the regulators who ultimately hold HSBC's fate.2 And at the top of the board, after Sir Mark Tucker announced in 2024 that he would retire,[^17] the bank turned to Brendan Nelson — a KPMG veteran of more than 25 years and a seasoned audit-committee hand — who was confirmed as permanent Group Chairman in December 2025.16 A CEO from the trading floor, a CFO from compliance, and a chairman from auditing: the composition of the regime signals a bank whose defining ambition is no longer expansion but execution, cost control, and staying out of trouble.

What does the reshaped bank actually earn? According to the group's 2025 segment disclosures, Corporate and Institutional Banking was the largest business by revenue, contributing on the order of $27.6 billion of revenue and around $11.4 billion of pre-tax profit — the connector engine made visible.1 The Hong Kong segment generated roughly $15.9 billion of revenue and about $9.6 billion of pre-tax profit, underpinned by a commanding local deposit franchise of well over $500 billion; the sheer profitability of Hong Kong relative to its revenue reflects the near-zero cost of those sticky deposits.1 The UK contributed around $12.9 billion of revenue and roughly $6.7 billion of pre-tax profit, while International Wealth and Premier Banking, positioned as the long-term growth engine, ran at around $7.0 billion of revenue and $2.1 billion of pre-tax profit, fed by tens of billions of dollars of net new invested assets as wealthy Asian clients funneled savings into HSBC's platforms.1 The pattern is unmistakable: Asia and the wholesale network do the heavy lifting, while the UK provides ballast and wealth provides the growth option.

The 2025 results also sharpened the group's forward guidance in a way that lets investors hold management to account. On the February 2026 results call, the leadership set out a target for return on tangible equity of around 17 percent or better, excluding notable items, for each year from 2026 to 2028, guided toward mid-single-digit revenue growth by 2028, and told the market to expect banking net interest income of at least $45 billion in 2026 — a bet that even as central banks cut rates, the sheer size and structuring of the deposit book would keep the core spread engine humming.1 The bank also signaled a dividend payout ratio target of around 50 percent alongside continued buybacks. These are concrete, falsifiable numbers, and the discipline of having published them is itself a small piece of evidence about a management team that wants to be judged on delivery rather than narrative.

Wrapping the whole exercise is a hard cost target. Management has committed to roughly $1.5 billion of annual cost savings by the end of 2026, to be achieved by stripping out duplicate senior management created by the old matrix, thinning the ranks of managing directors, cutting staff costs, and leaning on automation and artificial intelligence in the back office.1 It is worth being precise about what this program is and is not. It is a structural cost-out aimed at the layers of duplicated management the matrix bred — a bank that ran three global businesses across five regions inevitably grew two or three executives where one would do. It is not, on the evidence so far, a radical shrinking of the bank's actual footprint. The strategic bet is coherent — simplify the structure, cut the complexity tax, and let the underlying earnings power show through. Whether it pays off depends on execution, and execution is exactly where a bank this size has historically stumbled; the reported 10 percent rise in operating expenses in 2025 is a reminder that gross savings can be swallowed by inflation, investment, and one-off restructuring charges before they ever reach the bottom line.1 Which raises the deeper question this whole story has been building toward: what, stripped of the narrative, are the actual sources of HSBC's advantage, and how durable are they?

IX. Playbook: Business & Investing Lessons

Strip away the drama and HSBC becomes a case study in a handful of durable business principles — and in how easily even a powerful franchise can squander them. The first and most important is the power of scale economies in funding. A bank is, at bottom, a machine for turning cheap deposits into higher-yielding assets, and the cheaper and stickier the deposits, the stronger the machine. HSBC's deposit base runs to well over a trillion dollars, and critically it is granular — millions of ordinary savers and businesses, not a handful of flighty institutional depositors — which makes it both cheap and remarkably loyal. In Hong Kong the bank commands a quarter or more of all local deposits, a share no competitor can easily contest.1 In a world of higher interest rates, a fortress of low-cost deposits is close to a license to print money, because the bank earns the spread between what it pays savers (very little) and what it earns on assets. This is the single most important thing to understand about why HSBC is worth what it is worth.

The second power is switching costs, and here the relevant asset is the global-connector network dressed in the concrete form of HSBCnet, the bank's corporate treasury platform. Picture the finance department of a multinational manufacturer. Its cash-management systems, its foreign-exchange execution, its trade letters of credit, its payroll across dozens of countries, and its supplier payments are all wired through a single bank's rails, integrated with its own accounting software and internal controls. Ripping all of that out to move to a competitor is not like switching a current account; it is like rewiring a building while the lights are on. The cost, risk, and disruption are so high that clients tend to stay for decades, and a purely domestic bank cannot even bid for the business because it lacks the cross-border footprint. This is the analytical heart of management's case against the Ping An break-up: the value is in the connections, and the connections create genuine lock-in.

The claim is credible, but an independent analyst should stress-test it rather than swallow it whole. Two caveats matter. First, lock-in is easier to assert than to measure; HSBC does not publish a clean metric for how much of its corporate revenue is genuinely captive versus contestable, so the investor is partly taking management's word. Second, the fintech era has produced a wave of specialists — in cross-border payments, in FX, in treasury software — that attack the network not by rebuilding all of it but by peeling off the single most profitable slices. HSBC's defense is that corporates value a single, regulated, deep-balance-sheet partner over a patchwork of narrow providers, and there is real evidence for that in the stickiness of transaction-banking relationships. But the moat is being probed at its edges, and "the network is valuable" must be continuously re-earned, not assumed.

The third lesson is a warning about the conglomerate discount. Sprawling, multi-line global banks have historically traded at a discount to focused domestic peers, because complexity breeds inefficiency, opacity, and management distraction — what one might call complexity drag. A pure-play domestic lender like Lloyds Banking Group is simple to model: a UK economy bet, a handful of products, a transparent balance sheet. A pure-play investment bank is likewise legible to specialists. HSBC, by contrast, asks investors to underwrite Hong Kong property, British mortgages, global trade finance, Chinese growth, and US-dollar clearing all at once, in a single security governed by two conflicting regulatory spheres. Faced with that cognitive burden, the market applies a haircut. Elhedery's collapse of the matrix into four segments is, in essence, a campaign to shrink that discount by making the bank simpler to run and easier to value — to give investors four legible businesses instead of one inscrutable blob. Whether it works is an open, testable question; simplification decreed on an org chart is not the same as simplification achieved in practice, and HSBC has announced clean new structures before, only to watch complexity quietly reassemble itself.

Finally, HSBC's own history offers a matched pair of capital-allocation lessons more instructive than any textbook. The negative benchmark is Household International: paying $14.8 billion to chase yield in an adjacent market — American subprime — where the bank had no genuine edge, and losing a multiple of that when the tide went out.45 The positive benchmark is the pairing of the Canada sale, executed at a premium to a strategic buyer, with the £1 acquisition of SVB UK at the bottom of a panic.1210 The through-line is that in banking, the acquisitions that destroy value are the ones that confuse a strong balance sheet with strategic insight, and the deals that create value are the ones that exploit a mispricing the buyer genuinely understands. HSBC has done both, spectacularly, within a single generation — which is why the current management's capital discipline is the thing most worth watching.

X. Analysis: The Investment Story & Bear vs. Bull Case

The core investment story, told neutrally, is one of transformation: HSBC is attempting to convert itself from a complex, capital-hungry global financial supermarket into a leaner, higher-returning "Eastern gateway and global connector." The 2025 results give the story some real support and some real caveats. On the supportive side, the group delivered roughly $68.3 billion of revenue and $29.9 billion of pre-tax profit, and management set out guidance for a return on tangible equity of around 17 percent or better, excluding notable items, across 2026 to 2028.1 On the cautious side, headline pre-tax profit actually fell by about $2.4 billion year over year, reported return on tangible equity came in around 13.3 percent once notable items were included, and operating expenses rose roughly 10 percent — a reminder that the "clean" numbers management prefers to emphasize sit alongside messier reported ones.1 A neutral observer should hold both in view.

For readers who want to track this business rather than take management's word for it, three key performance indicators matter above all others, and it is worth being disciplined about limiting the list to what genuinely moves the story. The first is return on tangible equity, the truest single measure of whether the bank is earning its keep on the capital shareholders have entrusted to it. The mid-to-high-teens target is credible only for as long as interest rates stay elevated, and the interesting test is what RoTE does as central banks cut; a bank that can hold a high-teens return through a falling-rate cycle is demonstrating durable earning power, while one that sags back toward its cost of equity is revealing that the recent boom was simply a gift from high rates. The second is the cost-to-income ratio, the clearest scoreboard for whether the $1.5 billion simplification program is real or rhetorical. With reported costs running near 53 percent of revenue in 2025, there is visible room — and visible pressure — to improve, and the honest way to read this metric is to strip out the flattering adjustments and watch the reported trend over several years.1 The third is net new invested assets in the wealth business, the leading indicator of HSBC's pivot from interest-rate-dependent net interest income toward more durable, capital-light fee income; every dollar of assets that a wealthy Greater Bay Area client entrusts to HSBC's platform is a dollar that generates recurring fees regardless of where rates go. Watch those three numbers — returns, costs, and wealth inflows — and you will know whether the transformation is working long before the narrative catches up.

The bull case is straightforward. If the cost program lands on or ahead of schedule, the high-margin wealth franchise keeps compounding as it harvests the vast intergenerational wealth transfer under way in the Greater Bay Area, and the bank keeps returning capital through buybacks and a heavy dividend, then HSBC becomes something close to a cash-generation machine sitting on an unassailable Hong Kong deposit moat. In the language of Hamilton Helmer's 7 Powers, the bull owns two of them outright — scale economies in funding and switching costs in the corporate network — and a third, the cornered resource of Hong Kong note issuance, thrown in for good measure. Through a Porter's five-forces lens, the barriers to entry in cross-border transaction banking are formidable, supplier and buyer power over a bank with a trillion-plus in granular deposits is weak, and the most serious competitive threat comes not from other banks but from fintech unbundling of individual services.

The bear case is where an honest analysis has to linger, because it is not primarily about earnings — it is about geopolitics, and it strikes at the bank's very structure. HSBC is permanently wedged in the crossfire of the US-China rivalry. Its regulators in London and Washington operate sanctions regimes that can directly conflict with Beijing's expectations of a bank that earns most of its money on Chinese soil, and the institution has already shown, in episodes over Hong Kong's national-security law and frozen accounts, that it can be forced to choose sides and anger someone whichever way it turns. A genuine systemic rupture — over Taiwan, over a new sanctions escalation, over Hong Kong's autonomy — would make the dual-headed structure that has defined HSBC since 1993 not merely awkward but potentially untenable, and no cost program can hedge that risk away. Ping An's break-up thesis, decisively defeated at the ballot box, was in the end an argument about exactly this vulnerability, and it has not disappeared merely because it lost a vote.

Two further risks round out the skeptic's case. The first is net-interest-margin compression, and it is the mirror image of the bull thesis. HSBC's fortune-generating deposit spread — paying savers almost nothing while earning far more on assets — works in reverse when rates fall. The mechanism is simple: the bank cannot cut what it pays on a current account below zero, but the yield it earns on loans and bonds reprices downward as central banks ease. If global rate cuts come faster or deeper than expected, the very deposit base that anchors the bull case becomes a margin headwind, which is exactly why management's guidance to defend banking net interest income at $45 billion or more is the single most scrutinized number in the story.1 The second is mainland China itself — specifically the bank's exposure to Chinese commercial real estate, a sector that has been working through a prolonged and painful downturn and that has already forced write-downs against HSBC's book. The bank's fate is bound to the health of the Chinese economy in a way that no cost program can diversify away.

An activist stress test would push harder still on governance and complexity. Is a four-segment reorganization genuinely simpler, or merely a relabeling of the same matrix with fewer boxes on the chart? Are the "notable items" that lift adjusted return on tangible equity from a reported 13.3 percent to 17.2 percent recurring in all but name — the kind of "one-off" that shows up every year?1 Is a board stacked with auditors and risk officers built to grow the bank or merely to keep it out of the newspapers? And does the relentless focus on buybacks and payout ratios reflect genuine capital discipline, or a management team out of ideas for how to grow, returning cash because it cannot find anything better to do with it? These are not rhetorical gotchas; they are the questions a serious long-short investor would actually ask, and HSBC's answers to them over the next several reporting cycles will matter more than any single quarter's profit. None of these questions has a settled answer, and that is precisely the point. HSBC is neither the pure Asian growth story its bulls imagine nor the doomed imperial relic its bears fear. It is both banks at once, and the tension between them is the investment.

XI. Epilogue & Outro

Return, at the end, to those two scarred bronze lions outside the Hong Kong headquarters. They were cast in an age when a bank founded to finance the opium trade could plausibly imagine itself the permanent financial spine of a British empire that would never set. That empire is gone. The bank spent the closing decades of the twentieth century trying to conquer the West — buying a British clearing bank, plastering the world with advertising, gorging on American subprime — only to discover, at ruinous cost, that its true moat had been in the East all along, in the cheap deposits and the note-issuing privilege and the trade corridors of the China coast.

The transition now under way is, in its way, an act of acceptance. Sir Mark Tucker and Noel Quinn began the work of shrinking the bank back toward its sources of genuine advantage — retreating from Western retail, defeating the activist who wanted to sever the halves, and proving through disposals and returns that a simpler HSBC could still generate cash. Georges Elhedery and Pam Kaur have inherited that project and pushed it further, collapsing the matrix, squeezing costs, and betting that a leaner, four-segment bank can finally close the gap between what HSBC earns and what the market is willing to pay for it.

Whether they succeed will not be decided in a boardroom or a marketing campaign. It will be decided by the numbers — the return on tangible equity as rates fall, the cost ratio as the AI and restructuring promises meet reality, the wealth inflows as the Greater Bay Area's savers come of age — and by the one variable no chief executive controls, the fraught and deepening rivalry between the two superpowers whose economies HSBC has spent 160 years connecting. Born of the nineteenth-century collision between Britain and China, HSBC remains, improbably, the bank that lives in the seam between them. Its destiny, as it always has been, is anchored in the East. The open question is whether the seam holds.

References

-

Announcement — HSBC Holdings plc Annual Results 2025 — HSBC Group, 2026-02-25 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Pam Kaur appointed Group Chief Financial Officer / Board of directors — HSBC Holdings plc ↩↩↩

-

HSBC Agrees to Acquire Household International in $14.8B Deal — The Wall Street Journal, 2002-11-14 ↩↩

-

HSBC Household subprime losses over $50B — Reuters, 2009-03-02 ↩↩↩↩

-

HSBC Reporting Archive (2004–Present) — HSBC Group Investor Relations ↩

-

Ping An calls for HSBC split with eye on unlocked value — Reuters, 2022-04-29 ↩

-

HSBC CEO Noel Quinn rejects Ping An split proposal — Financial Times, 2022-08-01 ↩

-

HSBC investors reject Ping An-backed spin-off proposals at AGM — Reuters, 2023-05-05 ↩

-

HSBC buys UK arm of Silicon Valley Bank for £1 — Reuters, 2023-03-13 ↩↩

-

HSBC acquires Silicon Valley Bank UK Limited — HSBC Group Press Release, 2023-03-13 ↩

-

HSBC completes sale of Canada business — HSBC Group Press Release, 2024-03-28 ↩↩

-

Royal Bank of Canada completes HSBC Canada acquisition — Reuters, 2024-03-28 ↩

-

HSBC to simplify structure into four business units — Reuters, 2024-10-22 ↩↩

-

Georges Elhedery's first major move: HSBC reorganization — Financial Times, 2024-10-22 ↩

-

Brendan Nelson appointed permanent group chairman of HSBC — South China Morning Post, 2025-12-10 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube