H&M Group: The Battle for the Future of Fast Fashion

I. Introduction & Episode Roadmap

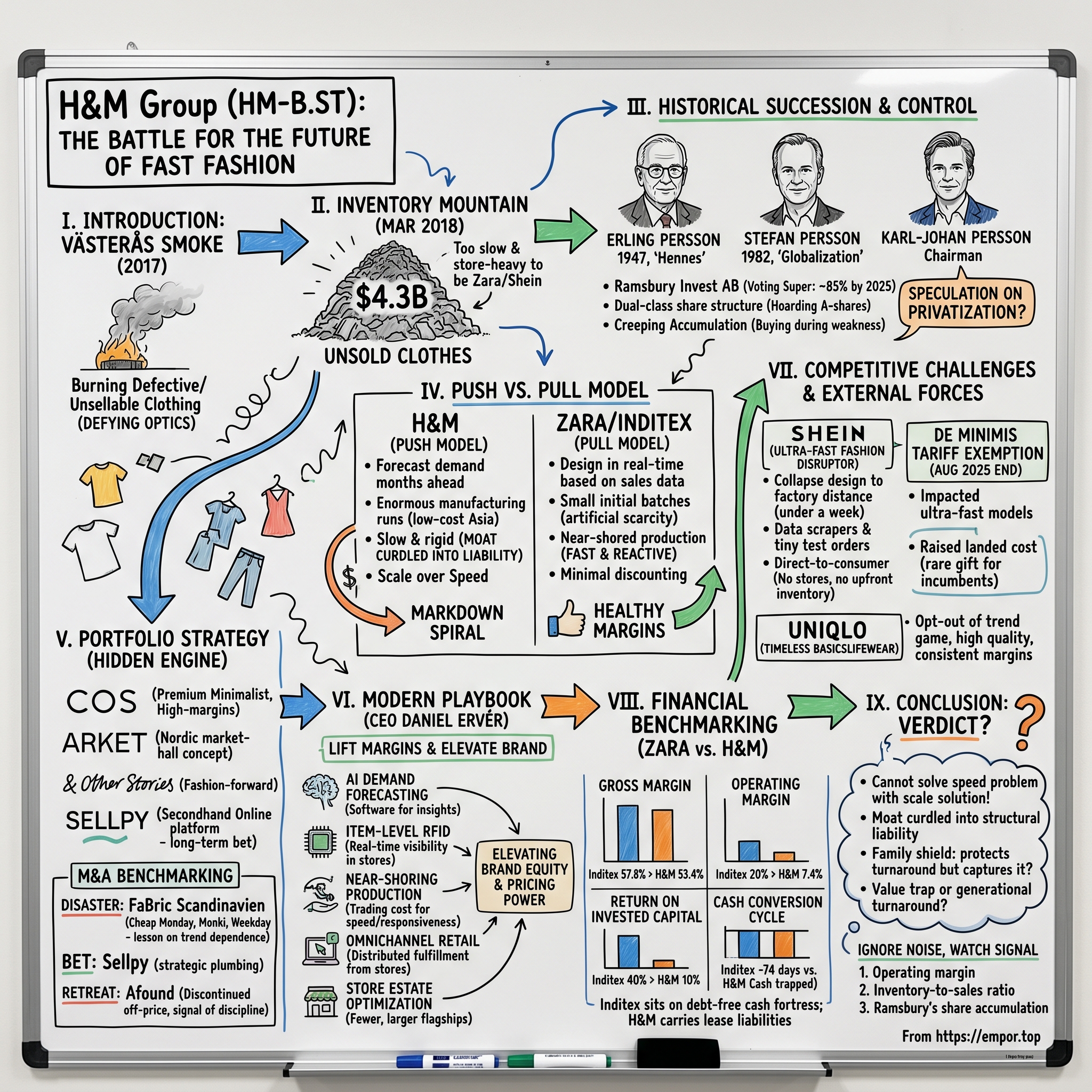

In the autumn of 2017, residents of Västerås, a quiet industrial town ninety minutes west of Stockholm, noticed something odd about the smoke rising from the local combined heat and power plant. The facility, which normally fed itself on wood pellets and recycled household waste, had begun burning something else entirely: clothing. Not rags, not factory offcuts, but garments — tens of thousands of them, defective or unsellable, fed into the furnace to keep the lights on across central Sweden.1

There was a cruel symmetry to it. Västerås is the town where, in 1947, a Swedish entrepreneur named Erling Persson opened a single womenswear shop he called "Hennes." Seventy years later, in the very same town, the global empire that shop became was incinerating its own merchandise for fuel. The company insisted the burned items were contaminated or unsafe — mildewed, chemically tainted, legally unsellable.1 But the optics were devastating, because they pointed at a truth the entire fast-fashion industry preferred not to discuss: the business of making clothes cheap and fast had become a business of making clothes that nobody wanted.

That uncomfortable fact would crystallize a few months later, in March 2018, when H&M disclosed that it was sitting on an inventory mountain worth a staggering $4.3 billion — clothes manufactured, shipped, and warehoused, but unsold.2 How does a company that began as one woman's dress shop in postwar Sweden grow into a retail colossus of more than 4,000 stores across dozens of countries, only to drown in its own product?

That question is the spine of this story. Because H&M's predicament was never really about clothes. It was about a clash of operating models — a war over the future of how fashion gets made, moved, and sold. And it is no longer a war fought with real estate and bulk purchasing. It is an algorithmic and logistical conflict, pitting H&M against Spain's Inditex, the parent of Zara; against Japan's ユニクロ Uniqlo, owned by 株式会社ファーストリテイリング Fast Retailing; and most threateningly, against China's ultra-fast-fashion disruptor 希音 Shein, a company that can take a design from sketch to shipped package in under a week with virtually no upfront inventory at all.

It helps to set the field of play. Global apparel is dominated by a handful of giants, each running a fundamentally different theory of the business. Inditex is the speed-and-scarcity champion, the company that proved a Western retailer could manufacture close to home and still beat everyone on margin. ユニクロ Uniqlo, under 株式会社ファーストリテイリング Fast Retailing, refuses to play the trend game at all — it sells timeless, engineered basics it calls "LifeWear," competing on fabric science rather than fashion fads. Shein is the digital insurgent that dispensed with stores, seasons, and forecasts altogether. And H&M sits in the uncomfortable middle: too trend-driven to be Uniqlo, too slow and store-heavy to be Zara or Shein. Much of this story is about what happens to the company caught in that middle when the ground beneath it moves.

Over the course of this episode, three themes will recur. The first is the great industrial transition underway in apparel: from a "push" model, in which a retailer forecasts demand months ahead and commits to enormous manufacturing runs in low-cost Asia, to a "pull" model, in which production is near-shored, made in small batches, and triggered in near-real-time by what is actually selling. H&M built the greatest push machine the industry had ever seen — and then watched the world pivot to pull.

The second theme is control. H&M is not a normal public company. It is a family dynasty that happens to be listed. The Persson family, through a private investment vehicle called Ramsbury Invest AB, holds a voting grip so absolute that no activist, no short-seller, no impatient fund manager can dislodge them. That shield is either H&M's single greatest strategic asset or a comfortable cushion that delayed a painful reckoning — and we will argue it is both.

The third theme is the hidden portfolio. While the world watches the flagship H&M brand, the group has quietly assembled a second engine: premium labels like COS, ARKET, and & Other Stories, and a circular-economy bet called Sellpy. These are the businesses that may hold the answer to whether H&M is a value trap or a generational turnaround. Let's begin where all dynasties begin — with the founder, and the question of who holds the keys.

II. Succession, Dynastic Control & The Ramsbury Governance Structure

To understand H&M in 2026, you have to understand that it is run less like a Swedish public company and more like a European royal house — one that has spent the better part of a decade quietly buying back its own kingdom.

The founding myth is brisk and deliberately so, because the family itself treats the old history as prologue. Erling Persson, a salesman with an eye for American retail energy, opened "Hennes" — Swedish for "hers" — in Västerås in 1947, selling affordable women's clothing. In 1968 he acquired a hunting-and-fishing apparel retailer called Mauritz Widforss, picked up its menswear inventory, and rechristened the combined business Hennes & Mauritz. The name was almost an accident of an acquisition, but the formula was intentional: fashion that looked expensive, priced so that ordinary people could buy it on impulse. Erling handed the company to his son Stefan Persson in 1982, who globalized it; Stefan handed the chairmanship through the generations until it reached the founder's grandson. What matters for investors is not the genealogy but the architecture the family built on top of it — an ownership structure engineered for permanence.

That architecture is named Ramsbury Invest AB, the Persson family's private holding company and the instrument through which they exercise dynastic control. And here is the mechanism that makes it so powerful: H&M, like many Swedish firms, has a dual-class share structure. Class A shares carry ten votes each; class B shares, the ones that trade freely on the Stockholm exchange, carry one. By hoarding the A shares and steadily accumulating B shares, the family converts a large economic stake into a near-total governance lock.

For years the family's grip sat around 57–58% of total shares and roughly 79–80% of the votes. But the family has not been standing still — it has been on a relentless, methodical buying campaign. Since 2016, the Perssons have spent more than 63 billion Swedish kronor, roughly $6.6 billion, snapping up shares on the open market, largely by reinvesting their enormous dividend stream straight back into more stock.3 By mid-2025, that creeping accumulation had pushed the family's economic stake to nearly 64% of the capital and a commanding 85% of the voting rights — up from around 35% of the capital just nine years earlier.4 In the first half of 2025 alone, Ramsbury kept hoovering up shares, and the math began to speak for itself.

This is where the speculation lives. Analysts have noticed that the family is buying fastest precisely when H&M's share price is weakest — and the stock fell roughly 9% over 2025 amid trade tensions and tariff fears, handing the Perssons a discount.4 Cross a 90% ownership threshold under Swedish takeover rules and a controlling holder can compel the remaining minority to sell, clearing the path to delisting. Several analysts have argued that at the current pace, the family could be in position to take H&M private within a couple of years — a move that would let them execute a slow, painful turnaround far from the quarterly glare of public markets.4 Chairman Karl-Johan Persson has flatly denied any such plan, insisting the family buys simply "because we believe in the company."4 Investors are entitled to weigh the denial against the checkbook.

It is worth dwelling on why this structure is so durable, because it explains a great deal about how H&M behaves. In a typical widely held public company, ownership and control are roughly proportional — own a third of the shares and you have roughly a third of the influence, and a determined coalition of outside investors can eventually force change. The dual-class system severs that link. The family can own a minority of the economics and still command a supermajority of the votes, which means that no proxy fight, no activist campaign, and no boardroom coup is possible without the family's consent — and the family will never consent. For a public-market investor, this is the single most important fact about H&M: you are buying a non-controlling, non-voting economic interest in a company that will be run, in every meaningful sense, for the family's multi-generational benefit. That can be a feature or a bug depending on whether the family's interests align with yours, but it is never neutral.

There is also a behavioral tell in how the family buys. The dividend, rather than being a return of cash to all shareholders to spend as they wish, functions for the Perssons as a recycling pump: the cash comes out as a dividend and goes straight back in as share purchases, steadily shrinking the free float and tightening the family's grip with each passing year. Every dividend H&M pays is, in part, financing its own gradual privatization. Few mechanisms reveal a controlling owner's true intentions more clearly than where they put the dividend, and the Perssons put theirs back into the stock.

Who, then, actually steers the ship today? Two men, with a deliberate division of labor. The chairman is Karl-Johan Persson — grandson of Erling, and himself H&M's chief executive from 2009 to 2020. Having run the company through the very years when the inventory crisis took root, he now sits atop Ramsbury, functioning less like a ceremonial chairman and more like the principal of a family private-equity office: deploying the dynasty's capital, buying the stock, and providing patient, long-horizon oversight of the group's strategy.

There is a quiet irony in Karl-Johan's current role that the family would prefer not to dwell on. The very decade he ran the company as CEO — 2009 to 2020 — was the decade in which the inventory crisis incubated, the markdown spiral took hold, and the digital threat went from theoretical to existential. Whatever one thinks of his stewardship, it gives him an unusually intimate understanding of exactly what is broken, and arguably a personal stake in seeing it fixed on his family's watch rather than handed to outsiders to repair. A founder's grandson presiding over the rescue of the business he helped imperil is the kind of narrative that family dynasties either rise to or are destroyed by.

The operator is Daniel Ervér, appointed president and CEO in January 2024 after his predecessor, Helena Helmersson, stepped down on the same day the company reported a surprise drop in operating profit.56 Ervér is a true company lifer. He joined H&M as a trainee in 2005, spent eighteen years climbing through the organization, and most recently ran the core H&M brand itself before getting the top job at the age of just 45.7 His mandate is unambiguous: lift margins back toward respectability, elevate the brand out of the discount bin, and finish wiring the company's digital and logistical nervous system.

The most revealing detail about Ervér is how he is paid — because it tells you exactly how the family thinks about alignment. Rather than dilute public shareholders by minting fresh equity for management, Chairman Persson reached into Ramsbury's own holdings. In February 2024, Ramsbury Invest personally issued Ervér 450,000 call options on H&M class B shares, struck at SEK 168.26, exercisable in a window three years out — with Ervér paying a real premium of SEK 11.63 per option, valued by an independent third party using Black-Scholes, so that the options carry zero cost and zero dilution to other shareholders.8 In other words, the family is sharing its own upside with the operator, on market terms, out of its own pocket. Ervér also directly holds 85,896 H&M shares, and his group package is built on a SEK 15.1 million base salary, a short-term incentive gated by an operating-profit threshold, and a long-term program tied to share price, EBIT, and sustainability targets.9

It is an elegant structure, and a telling one. The family is not preparing to sell to outsiders; it is concentrating ownership and stapling its chosen operator to the family's equity value. To understand what that operator is fighting to fix, we have to rewind to the era when H&M's model wasn't broken — it was the envy of the industry.

III. The Golden Era of Fast Fashion: Scale over Speed

Picture a high street in Manchester or Munich in 1998. The luxury houses are showing impossibly expensive coats on Paris runways, and a teenager with a part-time job has no hope of affording any of it. Then she walks into an H&M, and there it is — not the designer coat, but its spiritual cousin: the same silhouette, the same season's color, hanging on the rack at a price she can pay with a week's wages. She buys it, wears it a dozen times, and moves on. That, in a sentence, was the revolution H&M perfected: the democratization of fashion.

The genius of "cheap and chic" was that it dissolved the old hierarchy of apparel. For most of the twentieth century, fashion trickled down slowly — runway to department store to mass market over a year or more. H&M compressed that into a season and stripped out the price premium entirely. The company's designers and buyers became expert translators, reading the runways and the street, then converting high-end aesthetics into mass-market garments that captured the feeling of the trend without the cost of the original. It was aspirational and accessible at once, and for a generation of shoppers it felt like getting away with something.

But the magic trick that made the economics work happened thousands of miles from any storefront, on the factory floors of Asia. H&M, unlike a vertically integrated manufacturer, owned almost no factories of its own. Instead it built a vast sourcing network, outsourcing the overwhelming majority of its production — on the order of 80% — to a fragmented base of independent suppliers concentrated in Bangladesh, Cambodia, China, and across South and Southeast Asia. The logic was beautiful in its simplicity. By placing enormous orders with low-cost factories and committing to volume far in advance, H&M extracted rock-bottom unit costs. Spread those costs across hundreds of millions of garments and you get fat gross margins, even at high-street prices.

This was the push model in its prime, and we should be clear-eyed about how well it worked. From roughly the mid-1990s through 2010, scale was a genuine moat. The bigger H&M got, the more leverage it had over suppliers, the cheaper its yarn and fabric and labor became, and the more aggressively it could undercut smaller rivals on price while still printing money. Size begat cost advantage, and cost advantage begat size.

There was also a marketing masterstroke layered on top, one that perfectly captured the "cheap and chic" philosophy and generated the kind of attention money cannot buy. In November 2004, H&M did something the industry had never seen: it persuaded Karl Lagerfeld, the legendary creative director of Chanel, to design a roughly thirty-piece collection sold under his name at H&M prices.10 The "high-low" designer collaboration was born. Lines formed around the block; stores sold out in hours; the collection became a cultural event. And H&M had stumbled onto something profound — that it could borrow the prestige of the world's greatest fashion houses for a single drop, transfer a halo of luxury onto a mass-market brand, and pay only for a limited production run. Lagerfeld was followed by a who's-who of fashion: Stella McCartney in 2005, then Roberto Cavalli, Comme des Garçons, Versace, Balmain in 2015, and a long roster of others, each collaboration a manufactured frenzy.10 These drops did more than sell clothes; they cemented the principle that great design need not be expensive, and they kept H&M culturally relevant in a way its everyday assortment never could on its own. In hindsight, the designer collaborations were H&M's first taste of scarcity as a weapon — the same psychological lever Zara pulled every single week — even if the company would not generalize the lesson to its core operations for another decade.

This was also the era of geographic conquest beyond Europe. H&M planted its flag in the United States in 2000 with a flagship on Fifth Avenue in New York, and over the following two decades it pushed into Asia, the Middle East, and Latin America, eventually surpassing 4,000 stores worldwide. Each new market followed the same template: enter with a splash, secure the best high-street locations, and let the affordable-yet-stylish proposition do the rest.

The second pillar of the golden era was physical real estate — a land grab executed with the same conviction. H&M took the river of cash thrown off by its cheap-sourcing engine and poured it into leases: prime, high-footfall locations on the best shopping streets and in the best malls of Europe and, increasingly, North America. The strategy was to be everywhere a shopper might walk, with stores large enough and frequent enough that the brand became part of the urban furniture. In a pre-smartphone world, where discovery happened on foot and the store was the marketing, owning the corner of the busiest intersection in town was an enormous advantage. Physical scale was the ultimate competitive weapon, and H&M wielded it ruthlessly, opening hundreds of stores a year at the peak of expansion.

Here, though, is the seed of the entire drama to come. Both pillars — far-flung cheap sourcing and a sprawling leased footprint — were optimized for one thing: economies of scale in a world that moved slowly. Lock in volume six months ahead, manufacture it on the other side of the planet, ship it across oceans, and stack it high in expensive stores. The model assumed that the trend you bet on in spring would still be the trend customers wanted in autumn. For decades, that assumption held. And then a Spanish company on the Atlantic coast, and later an app on every teenager's phone, proved that you could win not by being the biggest, but by being the fastest. The collision was coming.

IV. The Great Inflection Point: The $4.3B Inventory Crisis & The Agile Shadow of Inditex

To grasp what happened to H&M, you have to hold two supply chains side by side and watch them run in real time — because they are almost philosophical opposites, two different theories of how a fashion company should relate to the future.

H&M's theory was the push. The company forecast what would sell, committed to vast manufacturing volumes in Asia roughly six months in advance, and reaped the cost savings of scale and long planning horizons. The whole system was built to be cheap, and it was cheap precisely because it was slow. A long lead time is the price you pay for low-cost, high-volume offshore production; the ocean freight, the giant order sizes, the planning lead — all of it traded speed for unit economics. As long as trends moved at the pace of seasons, the trade was a winning one.

Inditex, the Galician parent of Zara, ran the opposite theory: the pull. Founded by Amancio Ortega, Zara deliberately kept a large share of its production — roughly half — near home, in Spain, Portugal, Morocco, and Turkey, rather than chasing the lowest possible labor cost in Asia. It manufactured in small initial batches, sent limited quantities to stores, and then watched. The store data flowed back daily. If a style sold out in two days, Zara could design a response, produce it, and have it hanging in stores worldwide in as little as two to four weeks. If something flopped, the loss was tiny because the batch was tiny. Zara wasn't trying to predict the future six months out; it was trying to react to the present in real time.

This produced two effects that H&M's model structurally could not match. First, artificial scarcity: because Zara made little of any one item and rarely restocked, shoppers learned that if they didn't buy now, it would be gone — a psychological trigger that drove full-price sales and trained customers to visit constantly to see what was new. Second, and more important for the income statement, Zara almost never had to discount, because it almost never overproduced. It made what was selling, after it started selling.

It is tempting to ask why H&M simply didn't copy this. The answer reveals how deep the trap ran. Zara's speed was not a single clever tactic but an entire interlocking system — near-shored factories on standby, a logistics hub funneling everything through Spain, store managers trained to feed daily sales data back to designers, and a culture built around reacting rather than forecasting — refined over decades and embedded in physical assets and human habits. H&M's system was the mirror image, optimized end to end for the opposite goal: lowest unit cost through distant, high-volume, long-lead production. You cannot bolt speed onto a machine engineered for cheapness; you have to rebuild the machine. And rebuilding meant sacrificing the very cost advantage that justified the company's prices and protected its profits. That is the cruelest kind of strategic trap — the one where the rational short-term move (keep exploiting your cost advantage) deepens the long-term hole. For years, H&M's incremental, sensible decisions all pointed the wrong way.

Then came the smartphone, and the ground shifted under H&M's feet. The rise of Instagram in the mid-2010s collapsed the trend cycle from seasons to weeks. A look could explode globally on a Tuesday and be exhausted by the following Monday. In that world, a six-month lead time wasn't a cost-saving feature anymore — it was a death sentence. By the time H&M's Asian factories delivered the garments it had bet on half a year earlier, the moment had often already passed.

The result piled up, literally, in warehouses. Through 2017 and into early 2018, H&M's unsold stock swelled to a figure that stunned the market: $4.3 billion in inventory, equivalent to about 17.6% of the company's annual sales — far above the level a healthy fast-fashion business should carry.2 This was the push model's failure made visible. The company had manufactured for a demand picture that no longer existed by the time the goods arrived.

What followed was the vicious cycle every retailer dreads. To move the mountain, H&M slashed prices. Aggressive, sustained markdowns cleared the backlog but at a brutal cost: operating profit collapsed by more than 60% from its prior peak as the discounts gutted margins.2 Worse, the damage compounded over time. Every markdown taught the customer a lesson — that H&M's prices were negotiable, that there was no reason to pay full price when a sale was always weeks away. The brand's pricing power eroded, and a discount mentality calcified into customer behavior. The company had to keep discounting to clear stock, which trained customers to wait for discounts, which made full-price selling harder, which created more stock to clear. The push model didn't just fail to predict demand; it actively destroyed the brand equity that might have commanded a premium.

And then, as if scripted, came the public-relations gut-punch we opened with. In late 2017, news broke that the power plant in Västerås was burning discarded H&M garments as fuel.1 The company's defense — that the clothes were genuinely unsafe or contaminated and could not legally be sold or donated — was probably true. But truth was beside the point. The image of a fast-fashion giant incinerating its own product in the town where it was born became an indelible symbol of the structural waste baked into the push model. Overproduce on the other side of the world, ship it across oceans, fail to sell it, and burn the remainder. It was the entire critique of fast fashion, compressed into a single smokestack.

The inventory crisis was the inflection point — the moment the market understood that H&M's scale, once a moat, had become an anchor. But a company drowning in unsold flagship product had, almost unnoticed, been building a fleet of smaller, nimbler, higher-margin boats. To those, we turn next.

V. Brand Diversification: The "Hidden" Portfolios and Strategic M&A Benchmarking

If you walk into a COS store in London or Tokyo, you might not realize you are inside an H&M company at all. The lighting is gallery-soft, the racks are sparse, the garments are architectural and quietly expensive, and the shopper browsing the cashmere is paying two or three times what she would across town at an H&M. That deliberate distance — the fact that the customer doesn't connect the two — is the entire point. It is also one of the most underappreciated assets in the group.

As the flagship H&M brand matured and its growth slowed, management understood it needed a second engine. The answer was a portfolio of distinct brands operating at different price points and aesthetics, insulated from the discount stigma attaching to the core. Today these portfolio brands represent roughly 18–20% of group net sales, and they have been the healthier part of the growth story — expanding around 15% in fiscal 2023 before cooling to mid-single digits in fiscal 2024, with COS, ARKET, and Weekday singled out by management as the standout performers feeding group profitability.11

The crown jewel is COS — short for Collection of Style — launched internally in 2007 as H&M's bid for the premium, minimalist customer. COS sells elevated essentials: clean lines, quality fabrics, restrained design, the kind of clothing that signals taste rather than trend. Crucially, it commands far higher average order values and far healthier margins than the core brand, because its customer is buying considered pieces at full price rather than impulse-buying a markdown. COS has grown into a genuine global business, with around 247 stores worldwide, and it proves something important about the group: H&M has the institutional DNA to build a premium brand from scratch and scale it internationally.11

Alongside COS sit the other premium and lifestyle labels — ARKET, with roughly 54 stores, built around a Nordic market-hall concept of curated design, homeware, and a literal café; and & Other Stories, with around 66 stores, aimed at a fashion-forward woman with a love of detail and a higher willingness to pay.11 Then there are the younger, edgier labels acquired or built over the years — Weekday and Monki, aimed at street-style youth — and H&M Home, which extends the brand into furniture and interiors, a category with stickier customers and fatter margins than apparel. None of these will ever match the flagship's sheer volume, but that is the point. They are margin-accretive, brand-elevating, and they hedge the group against the structural pressures crushing the mass-market core. Critically, the portfolio gives H&M a laboratory: it can test premium positioning, sustainability concepts, and full-price discipline at COS and ARKET, then carry the lessons back to the flagship's elevation strategy. A conglomerate of brands is only worth the complexity if the parts teach each other something, and this is where H&M argues its portfolio earns its keep.

The portfolio strategy, however, has not been a story of unbroken success — and H&M's record as an acquirer is a genuinely instructive case study in capital deployment, with one outright disaster, one expensive long-term bet, and one disciplined retreat.

Start with the disaster. In 2008, H&M acquired a 60% stake in FaBric Scandinavien AB, a Swedish youth-fashion group that owned the cool-kid brands Cheap Monday, Monki, and Weekday, for a price in the region of SEK 560 million.12 The logic was to buy credibility with a younger, trend-obsessed consumer. It went badly. By the time H&M exercised its option to buy the remaining 40% in 2010, the brands had so dramatically underperformed that the final tranche cost just SEK 8 million — a roughly 98% collapse in implied valuation that forced the company to reverse hundreds of millions of kronor in earlier provisions.13 The aftermath dragged on for years: Cheap Monday, the skinny-jeans brand that had been the centerpiece of the deal, was shut down entirely in 2018, and Monki was eventually folded into Weekday in 2024 to stem ongoing losses.11 The lesson is the oldest one in M&A: buying someone else's cool is far harder than building your own, and a trend-dependent brand can lose its value almost overnight.

The second case is the long-term bet: Sellpy, a Swedish online secondhand platform. H&M first invested in 2015 and then took a majority stake of around 74% in 2019, betting that the future of fashion includes the resale of the clothing already in circulation.1415 Sellpy operates a full-service resale model — customers ship in a bag of unwanted clothes, and Sellpy does everything else: sorting, photographing, listing, pricing, selling, and shipping each individual item. That convenience is exactly what drove explosive adoption; Sellpy's sales reached roughly SEK 4.1 billion in 2023, up about 20% year on year, across more than twenty European markets.11 But here is the catch that every investor should internalize: the full-service model is brutally labor-intensive and structurally low-margin. Handling thousands of unique, one-off items by hand will never throw off the kind of returns a rack of identical T-shirts does. Sellpy is best understood not as a near-term profit machine but as a strategic infrastructure bet — H&M building the plumbing for a circular future it expects regulators and consumers to demand, accepting low margins today to own the capability tomorrow. That expectation is not idle: the European Union has been tightening textile and extended-producer-responsibility rules that will increasingly make brands accountable for what happens to clothes after they are sold. Owning a resale platform turns a looming regulatory cost into a potential business line — a hedge that, if the rules bite as expected, could look prescient. It is also a defensive move against the substitution threat we will return to: if customers are going to buy secondhand anyway, far better that they buy it from a platform H&M owns than from a rival.

The third case is the one that reflects best on current management: Afound. Launched in 2018 as an off-price digital marketplace, Afound was meant to be H&M's own outlet channel, a place to clear excess inventory and sell third-party brands at a discount. It never found traction; third-party brands preferred to clear their own stock through their own channels, and demand never materialized. Rather than throw good money after bad, H&M made the disciplined call to discontinue Afound in late 2024, subsequently selling the asset to the off-price platform Secret Sales.16 In a company once defined by an inability to admit a bet had failed — by literally burning the evidence — a clean, unsentimental shutdown is a small but real signal of cultural change.

That cultural change runs deeper than the M&A ledger. Under the new CEO, the entire operating model is being rewired — not to out-scale the competition, but finally to match it on speed. That is the modern playbook, and it is where the company's future will be decided.

VI. The Modern Playbook: AI, RFID, and Competing with Ultra-Fast Fashion

Just as H&M was absorbing the lesson that Zara's pull model had beaten its push model, a far more extreme predator emerged — one that made even Zara look slow. Its name is 希音 Shein, and it rewrote the rules entirely.

Shein's innovation was to collapse the distance between the factory and the consumer almost to zero. Where Zara reacts to store data in weeks, Shein reacts in days. The company uses real-time data scrapers to monitor what is trending across social media and search, then feeds tiny test orders — sometimes as few as a hundred units — directly to a tightly integrated network of factories in southern China. The factories produce on demand; whatever sells gets reordered instantly; whatever doesn't is simply never made again. Lead times compress to three to seven days, and because production is triggered only by real demand, the company carries almost no upfront inventory commitment. Then, crucially, it ships individual parcels directly to the consumer's door from China, bypassing physical stores entirely. No leases, no markdown mountains, no $4.3 billion of stranded stock — the very things weighing H&M down simply do not exist on Shein's balance sheet.

But Shein's model has an Achilles' heel, and in 2025 it was struck. The entire economics of shipping millions of individual low-value parcels from China into Western markets rested on a customs loophole: the "de minimis" exemption, which let packages valued under $800 enter the United States duty-free. That exemption was the linchpin of the direct-to-consumer ultra-fast model. On August 29, 2025, the U.S. ended it for all countries, subjecting those parcels to duties and dramatically raising the landed cost of a Shein or Temu order; in the months that followed, the volume of sub-$800 parcels entering the U.S. reportedly fell by more than half.17 For H&M, this is a rare gift from the policy gods — a structural blow to the disruptor that no amount of H&M capital expenditure could have inflicted. It does not solve H&M's problems, but it narrows the price gap and reminds investors that regulatory and trade shifts can reshape competitive dynamics overnight, sometimes in the incumbent's favor.

There is also a third competitive path worth studying, because it suggests a different answer to the speed problem: simply opt out of it. Uniqlo, the jewel of Japan's Fast Retailing, has built one of the most profitable apparel businesses on earth not by chasing trends faster but by refusing to chase them at all. Its "LifeWear" philosophy centers on high-quality, technically engineered, year-round essentials — the perfect T-shirt, the lightweight down jacket, the heat-retaining base layer — designed for longevity rather than obsolescence. Because Uniqlo sells timeless basics, it largely sidesteps the markdown trap entirely: a plain navy crewneck does not go out of style in three weeks. The result is a business profit margin north of 16% on revenue of roughly ¥3.4 trillion in fiscal 2025, comfortably ahead of H&M's profitability.18 The lesson for H&M is pointed: there is more than one way to escape the markdown spiral. You can get faster like Zara, or you can get more timeless like Uniqlo — but the one thing you cannot do is keep chasing trends slowly. H&M's elevation strategy borrows from both playbooks at once.

This is an existential challenge precisely because it attacks H&M where it is heaviest. So under Daniel Ervér, H&M has stopped pretending its legacy model can win on its own terms and started, methodically, adopting the tools its faster rivals invented.

The first is visibility. You cannot run a responsive, real-time supply chain if you don't know precisely what you have and where it is. H&M has been rolling out item-level RFID — radio-frequency identification tags — across its stores. Think of RFID as giving every single garment its own tiny radio beacon: instead of a once-a-quarter manual stock count riddled with errors, the company can know in real time exactly which size and color is sitting on which shelf in which store. That sounds mundane, but it is the foundational layer for everything else — accurate inventory data is the raw material that lets a retailer fulfill online orders from store stock, avoid needless markdowns, and feed reliable signals into demand-forecasting systems.

The second is intelligence. H&M is shifting from what we might charitably call gut-feeling buying — a designer or merchant deciding months ahead how many of something to make — toward AI-driven demand forecasting. The promise of machine learning here is to read the early sales signals, the weather, the regional differences, and the social-media chatter, and to predict demand far more accurately and far faster than a human buyer committing volume half a year out. It is, in essence, an attempt to manufacture Zara's instincts in software.

The third, and hardest, is geography. The whole point of near-shoring is to shorten the physical distance between manufacture and market so that lead times fall from months to weeks. H&M has been actively shifting a portion of production closer to its key European and American markets — to suppliers in Turkey, Eastern Europe, and elsewhere — trading some of the unit-cost advantage of distant Asian factories for the strategic advantage of speed and responsiveness. This is the most consequential and most expensive part of the pivot, because it means partially unwinding the very cost machine that made H&M rich.

Knitting all of this together is the digital channel. The RFID-enabled inventory accuracy is what makes true omnichannel retail possible — letting a customer order online and have it fulfilled from the nearest store's stock, turning the expensive store estate into a distributed fulfillment network rather than dead weight. H&M has been pushing online penetration hard, building out its app, its loyalty program, and ship-from-store capabilities, all in service of a single goal: to see demand in real time and respond to it before the goods become a markdown. The unglamorous truth of the modern playbook is that it is less about fashion and more about data — about closing the loop between what a customer wants today and what a factory makes tomorrow. The companies winning in apparel are increasingly the ones that are best at logistics and information, and H&M is, belatedly, trying to become one of them.

Finally, there is the store estate itself — the leased footprint that was once the moat and is now, in many locations, a liability. The strategy here is quality over quantity: closing underperforming, commoditized stores while opening fewer, larger, experiential flagships. In practice that has meant shutting roughly 190 weaker locations while opening around 80 new-concept stores designed to be destinations — better designed, more localized in their assortment, and meant to give shoppers a reason to come in that a phone screen cannot replicate.11 The goal is to make the physical store an asset again rather than a fixed cost dragging on returns.

Whether this turnaround succeeds is ultimately a question of competitive structure — of moats won, lost, and contested. So let's put H&M on the analyst's whiteboard and run it through the two frameworks that matter.

VII. Hamilton's 7 Powers & Porter's Five Forces Analysis

Hamilton Helmer's framework asks a single question of any business: what is the persistent source of differential returns — the thing that lets you earn more than your cost of capital while competitors can't copy it? Run H&M through it and you get a portrait of a company whose old powers have eroded and whose new ones are still under construction.

Start with scale economies, historically H&M's signature power. For decades, sheer purchasing volume gave it a genuine cost edge in yarn, textiles, and bulk garment production — the more it bought, the cheaper it bought. But scale economies are only a moat if scale itself confers advantage, and the inventory crisis revealed the brutal truth: scale tied to a slow, rigid supply chain is not an asset but a liability. When the trend cycle accelerated, H&M's vast committed volumes became vast committed mistakes. The power hasn't vanished, but it has been severely disrupted; being big no longer guarantees being profitable.

Next, process power — the ability to do something operationally that rivals cannot easily replicate even if they know how it works. This is Zara's defining power, embedded in two decades of organizational learning about how to design, manufacture, and distribute in two-to-four-week cycles. It cannot be bought off a shelf; it lives in routines, supplier relationships, and information systems built up over years. H&M conspicuously lacks this power, which is precisely why it is spending billions on RFID, AI, and logistics automation trying to build it. The hard question for investors is whether process power can be acquired through capital expenditure, or whether — by its nature — it must be earned slowly through experience. The honest answer is that H&M is years behind and the gap is not trivially closed.

Then there is brand, which for H&M is a genuinely double-edged story. The company possesses enormous global mindshare — almost everyone knows what H&M is and roughly what it stands for. But brand as a power means the ability to charge a premium for an identical good, and years of relentless discounting did real damage to that ability, training a generation to wait for the sale. The entire premiumization push — COS, ARKET, the experiential flagships, the elevation of the core — is fundamentally an attempt to rebuild brand power that markdowns corroded. The portfolio brands, tellingly, hold more pricing power than the flagship precisely because they were kept clear of the discount stigma.

The most intellectually interesting power in this story belongs not to H&M but to its disruptor: counter-positioning. Shein occupies a business model that H&M cannot copy without destroying itself. By manufacturing on demand at the factory gate and shipping single parcels directly to consumers, Shein sidesteps the entire multi-billion-dollar apparatus of physical retail — the very apparatus H&M is contractually locked into through long-term leases. If H&M tried to fully replicate Shein's model, it would have to write off its store estate and torch its existing cost structure; the incumbent's assets become the prison. That is counter-positioning in its purest form: the disruptor's model is attractive specifically because the incumbent can't follow.

There is one power H&M might still be able to build, and it is worth naming because the bull case depends on it: a form of brand and process power concentrated in the portfolio rather than the flagship. COS, with its full-price discipline and premium positioning, behaves like a business with genuine pricing power — a small but real moat the flagship lost. If H&M can replicate the COS playbook across more of the group and drag the core brand upmarket toward it, the company could assemble a defensible position not by beating Shein at speed but by retreating to a part of the market where speed matters less and taste matters more. That is a narrower, more achievable ambition than out-Zara-ing Zara, and it is essentially the strategy management has chosen. Whether it is enough to move the consolidated numbers is the open question.

Now Porter's Five Forces, which maps the structural attractiveness of the industry H&M competes in — and the verdict is sobering, because fast fashion is one of the harder industries in which to earn durable returns.

Rivalry among existing competitors is extremely high. H&M is squeezed from every side: Zara dominates the premium-fast segment above it, Shein and 拼多多 Pinduoduo's Temu dominate the ultra-cheap digital segment below it, and Uniqlo flanks it with high-quality basics that win the customer who has tired of disposable trends entirely. Being caught in the middle, undifferentiated on speed, price, or quality, is the most dangerous position in retail — it is the strategic equivalent of fighting a three-front war. Worse, much of this rivalry plays out on price, the most value-destructive axis of competition there is, because a discount is instantly matchable and leaves no lasting advantage behind.

The threat of new entrants is high. Social media has demolished the old barriers to entry; a micro-brand with a viral TikTok and a drop-shipping arrangement can reach millions without a single store or a forecasting department. The capital intensity that once protected incumbents has inverted into a burden.

The bargaining power of buyers is effectively absolute. Consumers face zero switching costs and infinite choice. Loyalty in fast fashion is thin to nonexistent; the shopper goes wherever the price-and-trend combination is best this week.

The bargaining power of suppliers, by contrast, is low — a rare point of comfort. H&M sources from thousands of fragmented factories across Asia and North Africa, none of which has meaningful leverage over a buyer of H&M's scale. The company can play suppliers against one another almost at will.

The threat of substitutes is high and rising. The explosive growth of secondhand apps like Vinted and Depop offers consumers a genuine alternative to buying new fast fashion at all — directly cannibalizing primary demand. It is no accident that H&M bought Sellpy; owning a piece of the substitute is one of the few rational hedges against it.

Add it up and you have an industry of high rivalry, low entry barriers, all-powerful buyers, and credible substitutes — structurally tough — in which H&M's traditional powers have weakened while its new ones remain unproven. The financial statements show exactly what that costs.

VIII. Financial Benchmarking & Capital Efficiency

Numbers can be numbing, so let's frame this section around a single idea: two companies sell broadly similar clothes to broadly similar customers, and yet one is a far better business than the other. The gap between them is the entire investment thesis, and it is enormous.

Begin with gross margin — the share of each sales dollar left after the cost of the goods themselves. In fiscal 2024, Inditex posted a gross margin of 57.8%, against H&M's 53.4%.1920 A four-and-a-half-point gap may not sound dramatic, but in retail it is a chasm, and the reason traces directly to everything we have discussed. Because Zara near-shores, makes small batches, and reacts to demand, it sells the vast majority of its goods at full price. Because H&M forecasts, overproduces, and discounts, it surrenders margin to markdowns. The supply-chain philosophy shows up, dollar for dollar, in the gross line.

The gap widens dramatically by the time you reach operating margin — what's left after running the stores, the staff, the logistics, and the overhead. Inditex operated at roughly 20% EBIT margin in fiscal 2024; H&M was mired around 7.4%, having quietly abandoned its long-standing 10% margin target under the weight of currency headwinds and markdown pressure.1920 Think about what that means: out of every hundred kronor of sales, H&M keeps barely seven as operating profit, while Inditex keeps twenty. The same revenue produces nearly three times the operating profit at the Spanish rival. That is not a small efficiency gap; it is two different qualities of business.

The single metric that captures it all is return on invested capital — ROIC, the truest measure of how much profit a company squeezes from every dollar of capital tied up in the business. Inditex generates an outstanding ROIC in the high-30s to around 40%, while H&M languishes near 10%.19 To translate: for every dollar of capital deployed, Inditex earns roughly four times the return H&M does. A business compounding at 40% on capital is a wealth-creation machine; one earning 10% is barely clearing its cost of capital. This single comparison explains why the two companies trade at such different valuations and why investors treat them as belonging to different leagues despite competing on the same high streets.

What drives that ROIC chasm is the most elegant concept in retail finance: the cash conversion cycle, and Inditex runs a negative one — on the order of negative 74 days. Here is the magic, in plain terms. Because Zara's inventory turns over so fast, it sells the clothes and collects cash from customers before it has to pay the suppliers who made them. The suppliers are, in effect, financing Zara's growth for free; the faster Inditex grows, the more cash it generates from working capital. H&M experiences the mirror image. With slower-moving inventory — that stubborn 15–17% inventory-to-sales ratio — its cash sits trapped in warehouses, in shipping containers crossing oceans, and on store shelves, paid for long before it sells. One company's growth funds itself; the other's growth consumes cash. Same industry, opposite physics.

The balance sheets complete the contrast. Inditex sits on a debt-free cash fortress of roughly €11.5 billion, which lets it self-fund massive logistics and technology upgrades out of its own pocket, with no lender's permission required.19 H&M, by contrast, carries meaningful leverage — a debt-to-equity ratio around 1.4x — much of it in the form of lease liabilities on its enormous physical footprint. Those leases, the same store estate that was once the moat, now show up as fixed obligations that must be serviced in good times and bad, constraining flexibility precisely when the company most needs it to fund its turnaround.

A word of fairness is due, though, because the picture is not static. Under Ervér, H&M has run a determined cost-reduction program, and operating profit has been recovering off the crisis lows even as the company quietly retired its long-held 10% margin ambition.21 The leverage figure also deserves a footnote of caution for the careful reader: a large share of H&M's reported debt is lease liability, an artifact of the accounting rules (IFRS 16) that put the present value of future store rents onto the balance sheet as debt. This is not the same as borrowing billions from a bank to fund losses; it is the capitalized cost of operating thousands of physical stores. It is real — those rents must be paid — but it overstates how "leveraged" the company is in the conventional, solvency-threatening sense. The comparison to Inditex's cash fortress still holds directionally, but the gap in financial risk is narrower than the headline debt-to-equity ratio implies. The gap in financial quality and flexibility, however, is exactly as wide as it looks.

So the financial picture is unambiguous: H&M is the structurally weaker of the two great European fast-fashion houses, and the weakness is not cosmetic — it is rooted in the operating model. The investor's real question is not whether the gap exists today, but whether it can be closed tomorrow. That brings us to the verdict.

IX. Conclusion & The Acquired Playbook

Step back from the spreadsheets and the supply-chain diagrams, and the H&M story resolves into a single, durable lesson — the kind worth carrying to other companies and other industries. You cannot solve a speed problem with a scale solution. H&M built the most formidable scale machine fast fashion had ever seen, and from roughly 1995 to 2010 that machine was spectacularly profitable. But the machine was optimized for a slow world, and when retail flipped to a real-time, algorithmic pull model, the same scale that had been a moat curdled into a structural liability. The asset became the anchor. That inversion — moat into millstone — is one of the most important patterns in business history, and H&M is now a textbook case of it.

The second lesson is about the family shield, and it cuts genuinely both ways. The Persson family's commanding voting control through Ramsbury Invest is, on one reading, H&M's single greatest asset. It insulates management entirely from activists, short-sellers, and the tyranny of quarterly earnings. That insulation is exactly what a multi-year, capital-hungry, margin-sacrificing turnaround requires — the freedom to spend years and billions rewiring a supply chain without being fired for the dip in profits it causes along the way. Few public companies could attempt what H&M is attempting; the family shield is why it can. But the same shield has a darker reading: it was the comfortable cushion that let management tolerate a broken model for too long, and that may yet let the family take the company private at a depressed price, capturing the upside of a recovery that public shareholders funded the cost of. The shield protects the turnaround and, potentially, captures it.

Before the verdict, it is worth puncturing a few consensus narratives that cloud this story, because the popular version of H&M is wrong in several instructive ways.

The first myth is that H&M is simply a cheaper, lower-quality Zara — two versions of the same business separated only by price. The truth, as this entire story argues, is that they are operational opposites. Zara is a speed company that happens to sell clothes; H&M was a scale-and-cost company that happens to sell clothes. They look like twins on the high street and behave like different species in the warehouse. Confusing the two leads investors to assume H&M can simply "try harder" to match Zara's margins, when in fact closing the gap requires rebuilding the company's industrial core.

The second myth is that the Persson family's relentless buying is an unambiguous bullish signal for ordinary shareholders — insiders buying, after all, is supposed to be good news. The reality is more double-edged. The family is buying with the apparent intention of eventually owning the whole thing, and a controlling owner who wants to take a company private has every incentive to do so at the lowest possible price. The same buying that signals long-term conviction also signals that minority holders may one day be bought out near a cyclical low, capturing little of the recovery they helped finance. Insider conviction and minority interest are not always the same thing.

The third myth is that fast fashion is a dying category, doomed by sustainability backlash. The data says otherwise: the explosive growth of Shein and Temu shows demand for cheap, trend-driven clothing is not shrinking — it is migrating to whoever serves it fastest and cheapest. H&M's risk is not that the category dies but that it loses share within a category that is very much alive. The sustainability pressure is real and rising, but it functions less as a death sentence and more as a cost and a competitive variable — one that, through Sellpy and its circularity investments, H&M is at least attempting to turn to its advantage.

The fourth and most important myth is that H&M's problem is its brand. It is tempting to look at the discount-bin reputation and conclude that a marketing refresh and a few designer collaborations would fix things. But the brand damage is a symptom; the disease is the operating model. The markdowns that corroded the brand were forced by the overproduction that the push supply chain made inevitable. Fix the supply chain — make less, react faster, discount less — and the brand recovery follows. Treat the brand without fixing the supply chain, and the markdowns return. This is why the entire turnaround thesis rests on logistics and sourcing, not on advertising.

So which is it — value trap or generational turnaround? The honest answer is that the evidence points both ways, and that is precisely what makes H&M interesting rather than obvious. The bear sees a structurally disadvantaged middle child, out-margined by Zara above and out-priced by Shein below, in a brutal industry, weighed down by leases and leverage, earning a third of its best rival's operating margin. The bull sees something subtler: a company that has already proven it can build premium brands customers pay full price for — COS is not a hope, it is a 247-store fact — and that has the patient capital and managerial alignment to execute a slow pivot most public companies could never attempt. The success of COS and the strategic logic of Sellpy show the group has the DNA to win in premium and in circularity, not just in cheap. If Daniel Ervér genuinely near-shores the supply chain, rebuilds the brand's pricing power, and the family takes the company private to finish the job away from public scrutiny, H&M could re-emerge as a leaner, far more profitable private giant.

Two second-order risks deserve a place on any watch list. The first is concentration of dependence: this turnaround is effectively a bet on one man, Daniel Ervér, executing a multi-year operational rewiring, backed by one family's patience. That is a powerful alignment when it works and a single point of failure when it doesn't — a leadership stumble or a fracture in family resolve would matter more here than at a diffusely owned peer. The second is the shifting trade landscape. The end of the de minimis exemption helped H&M by hurting Shein, but the same tariff turbulence cuts both ways: H&M sources globally, and a world of rising duties, reshoring pressure, and currency swings raises input costs and complicates the very near-shoring pivot the company is betting on. The company that lives by global sourcing can also be whipsawed by the politics of it.

For the investor watching from outside, the noise is endless but the signal is narrow. Ignore the quarterly sales headlines and the store-opening press releases, and watch a very small number of things. First, the operating margin — the single cleanest gauge of whether the turnaround is real, because it captures markdown discipline, brand recovery, and cost control all at once; the journey from 7.4% back toward double digits is the thesis, quarter by quarter. Second, the inventory-to-sales ratio — the direct readout on whether the push model is actually becoming a pull model; falling, well-controlled inventory means the supply-chain pivot is working, while another bloat means it isn't. And third, the pace of Ramsbury's share accumulation — because the family's checkbook is the clearest available signal of the endgame, and the rate at which they approach the threshold for compulsory buyout will tell you more about H&M's future ownership than any management statement will.

Everything else is commentary. The clothes will keep changing with the seasons. The question that won't change is whether a seventy-nine-year-old Swedish scale machine can learn to move at the speed of a phone screen — and whether the family that owns it will let the public come along for the ride.

X. Outro

The deepest research on this story lives, as it usually does, in the primary documents rather than the headlines. For the supply-chain pivot, the margin trajectory, and the portfolio-brand disclosures, the richest source is H&M Group's own Annual and Sustainability Report and its quarterly interim reports, alongside the company's investor-relations archive of presentations.21[^22] For the competitive benchmark that frames the entire debate, Inditex's full-year results filings lay out the margin and capital-efficiency gap in the company's own numbers.20 And for the question that hangs over everything — whether the Perssons intend to take their kingdom private — the trail runs through Ramsbury Invest's own regulatory disclosures and the steady drumbeat of share-purchase filings that no press release can spin. Read those three sources together, and the battle for the future of fast fashion stops being a slogan and becomes a set of numbers you can actually watch move.

References

-

Swedish Power Plant Burns H&M Clothes Instead of Coal — Bloomberg, 2017-11-24 ↩↩↩

-

H&M, a Fashion Giant, Has a Problem: $4.3 Billion in Unsold Clothes — New York Times, 2018-03-27 ↩↩↩

-

H&M Family Owners Buy More Shares, Fueling Buy-Out Speculation — Reuters, 2018-05-30 ↩

-

H&M's Hennes & Mauritz Billionaire Family Quietly Moves Brand Toward Private Ownership — Fortune, 2025-06-09 ↩↩↩↩

-

H&M Reports Surprise Operating Profit Drop; CEO Steps Down — Reuters, 2024-01-31 ↩

-

H&M CEO Helena Helmersson Steps Down; Daniel Ervér Appointed — Bloomberg, 2024-01-31 ↩

-

Daniel Ervér Appointed New President and CEO — H&M Group, 2024-01-31 ↩

-

Ramsbury Invest AB Issues Call Options to CEO and CFO of the H&M Group — Ramsbury Invest AB / Cision, 2024 ↩

-

H&M Celebrates 20 Years of Designer Collaborations — H&M Group, 2024 ↩↩

-

Annual and Sustainability Report 2024 — H&M Group, 2025-03-27 ↩↩↩↩↩↩

-

H&M Acquires the Company Behind Cheap Monday, Weekday and Monki — H&M Group, 2008 ↩

-

H&M Buys Remaining 40 Percent of Fabric Scandinavien — WWD, 2010-11-24 ↩

-

H&M Group Continues to Invest in Sellpy — H&M Group, 2019-10-10 ↩

-

H&M Takes Control of Secondhand Platform Sellpy to Boost Circular Credentials — Financial Times, 2019-10-10 ↩

-

Etsy, eBay and Shein Reel as De Minimis Tariff Exemption Ends — Fortune, 2025-08-29 ↩

-

Fast Retailing Results for FY2025 and Estimates for FY2026 — Fast Retailing Co., Ltd., 2025-10-09 ↩

-

Inditex Full Year 2024 Results (PDF) — Inditex S.A., 2025-03-12 ↩↩↩

-

H & M Hennes & Mauritz AB Full-year Report 2024 — H&M Group, 2025-01-30 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube