Haleon plc: The Titan of Science-Led Self-Care

I. Introduction & Episode Roadmap

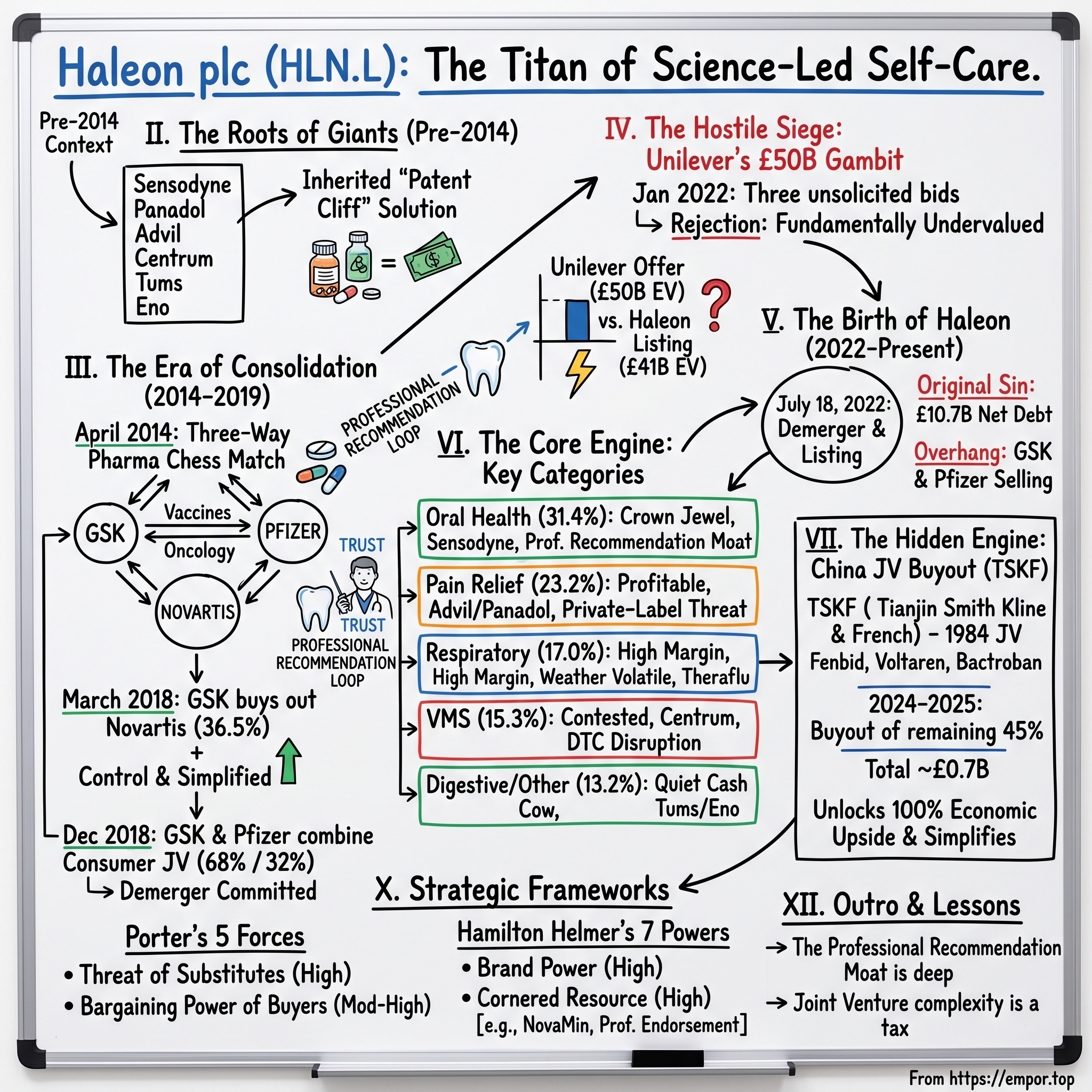

Picture a London trading floor on the morning of July 18, 2022. After years of corporate maneuvering — asset swaps, joint ventures, a hostile takeover siege, and an internal civil war among shareholders — a new ticker flickered onto screens across the City: HLN. By the end of that first session, a company almost nobody had heard of two years earlier carried a market value north of £30 billion, making it the largest public listing in Europe in more than a decade.1 It owned no blockbuster drug, no patent cliff to fear, no oncology pipeline to nurse. What it owned instead was the inside of your bathroom cabinet: the Sensodyne by the sink, the Advil in the medicine drawer, the Centrum on the kitchen counter, the Tums in the glovebox.

This is the story of Haleon plc — and it is a strange one, because Haleon was not built in a garage or dreamed up by a visionary founder. It was assembled, like a corporate Frankenstein's monster, from the discarded consumer divisions of three of the largest pharmaceutical empires on earth: GSK, Novartis, and Pfizer. For decades these brands lived as profitable afterthoughts inside drug companies obsessed with the next molecule. Then, in a roughly eight-year sequence of chess moves between 2014 and 2022, they were swapped, merged, fought over, and finally cut loose to stand alone.

Here is the central tension we want to wrestle with. On one reading, Haleon is the dream business — a defensive, high-margin consumer staples machine with brands so trusted that dentists and doctors recommend them by name, throwing off cash like clockwork through booms and recessions alike. On another reading, it is a heavily indebted spin-off, loaded with more than £10 billion of borrowings on its first day of trading, dependent on the British winter for its cold-and-flu profits, and quietly losing the bottom shelf to Walmart's own-brand ibuprofen. Which is the real Haleon? That is the question that should animate every long-term investor looking at this name.

Our roadmap runs the full arc. We will start in the pharma laboratories where these brands were incubated, then walk through the dizzying three-way consolidation that fused them together. We will relive Unilever's audacious £50 billion lunge in January 2022 and the boardroom rejection that followed. We will examine the demerger itself and the "original sin" of leverage that came with it, the slow clearing of the GSK and Pfizer share overhang, and the unit economics of the five categories that actually generate the cash. We will spend real time on the underappreciated China engine, on management's incentives and credibility, and finally run the whole thing through an activist stress test, Porter's Five Forces, and Hamilton Helmer's 7 Powers. Let's begin where all of it began — inside the giants.

II. The Roots of Giants (Pre-2014 Context)

Walk into any pharmacy in any country and you are standing inside a museum of acquisitions. The Sensodyne tube traces back to Block Drug Company of Brooklyn, which formulated a toothpaste for sensitive teeth in 1961; the brand passed to GlaxoSmithKline in 2001. Panadol, the paracetamol that much of the Commonwealth reaches for instinctively, was developed by Frederick Stearns & Co, a Sterling Drug subsidiary, back in the 1950s. Advil — branded ibuprofen — launched in the United States in 1984 under American Home Products, later Wyeth, later Pfizer. Centrum, the multivitamin that sits in tens of millions of American kitchens, came up through Lederle Laboratories. Eno, the fruit-salt antacid that fizzes in glasses across India and Latin America, was concocted by a Newcastle pharmacist named James Crossley Eno in the 1850s.

The point is not the trivia. The point is that none of these products were born inside a consumer-goods company. They were all born inside, or absorbed by, pharmaceutical companies — and they stayed there for a reason. For most of the twentieth century, the over-the-counter (OTC) drug aisle was the steady, unglamorous cousin of the prescription business. Drug companies kept it around because it solved a very specific financial problem.

That problem has a name: the patent cliff. A prescription blockbuster enjoys roughly a decade of monopoly pricing, then falls off a cliff the moment generics arrive — revenue can collapse 80% or more within a year of patent expiry. Pharmaceutical R&D is a brutal, boom-and-bust casino where a single drug can make or break a decade, and the failure rate in clinical trials runs staggeringly high. Against that volatility, a portfolio of toothpaste and headache tablets is a financial sedative. Consumer health brands don't go off-patent in any meaningful sense — Sensodyne in 2014 sold for the same reason it sold in 1974 — and the cash flows are smooth, predictable, and recession-resistant. People keep brushing their teeth in a downturn. The OTC division was, in effect, the drug company's bond portfolio: low excitement, low risk, always paying its coupon.

So why did the giants eventually want out? Because by the early 2010s the two businesses had become culturally and operationally incompatible. Selling oncology drugs is a game of clinical data, regulatory affairs, and physician detailing over timelines measured in decades. Selling toothpaste is a game of brand marketing, retail shelf placement, and fast-moving consumer-goods (FMCG) instinct measured in quarters. One business thinks like a scientist; the other thinks like Procter & Gamble. Running both under one roof meant the consumer brands were perpetually starved of management attention and capital, treated as a sideline by executives whose careers were made or lost on drug approvals. The friction was real, and the logic of separation grew louder every year. The only question was who would untangle the knot first — and in 2014, the answer turned out to be a complicated three-way trade.

III. The Era of Consolidation (2014–2019): The Three-Way Pharma Chess Match

In April 2014, GSK and Novartis announced a deal so intricate it read less like a transaction and more like a diplomatic treaty. This was not a simple buy or sell. It was a three-part swap designed to let each company double down on what it did best and shed what it didn't. GSK agreed to buy Novartis's vaccines business (excluding flu); GSK sold its own marketed oncology portfolio to Novartis for up to $16 billion; and — the part that matters for our story — the two companies folded their respective consumer health divisions into a single joint venture, with GSK holding 63.5% and Novartis 36.5%.2 The combined consumer business became the world's largest by some measures overnight, pairing GSK's oral-care and respiratory strength with Novartis's OTC brands like Voltaren and Excedrin.

Pause on the elegance of it. Each company used the others' weaknesses to sharpen its own focus. Novartis wanted to be a pure prescription-drug powerhouse and was happy to step back from consumer; GSK wanted vaccines and was willing to lead the consumer venture. Nobody had to write an enormous net cheque, because the assets largely paid for each other. This was financial engineering in service of strategic clarity, and it set the template for everything that followed: in this corner of the industry, the path to value was simplification through combination.

But a 63.5/36.5 joint venture is an awkward thing to own. Minority partners get a say without bearing full responsibility; profits leak out to a co-owner who may not share your strategy; and selling, restructuring, or eventually spinning off the business is far harder when someone else holds a third of it. By 2018, GSK's new chief executive, Emma Walmsley — herself a former L'Oréal and consumer-health executive who understood these brands intimately — decided to take control. In March 2018, GSK agreed to buy out Novartis's entire 36.5% stake for $13 billion, roughly £9.2 billion.2

Was that a good price? Let's benchmark it the way Ben and David would. The $13 billion paid for 36.5% implied a total enterprise value for the venture of around $35.6 billion. Against annual sales of roughly $7.8 billion, that put the deal at about 4.5 times revenue. Set that next to the comps: Johnson & Johnson's consumer segment was generally valued around 4 times sales in this era, while Reckitt Benckiser had paid a punchy 5.5 times when it bought Mead Johnson's infant-nutrition business in 2017. So GSK was paying a full price, but not an insane one — and crucially, it was buying control right before the next, larger move. With Novartis out, GSK suddenly owned 100% of the cash flows and 100% of the strategic steering wheel. The verdict here is that this was disciplined, deliberate consolidation: GSK paid up for clean control precisely because it knew what it wanted to do next.

What it wanted to do next was bigger. In December 2018, GSK announced it would merge its now-wholly-owned consumer business with Pfizer's consumer healthcare unit into a new joint venture, with GSK holding 68% and Pfizer 32%.3 If the Novartis combination created scale, the Pfizer combination created dominance. Pfizer brought the American crown jewels into the fold — Advil, the leading branded ibuprofen; Centrum, the leading multivitamin; and Caltrate, the leading calcium supplement. Overnight the combined entity became the unambiguous number-one over-the-counter consumer health company in the world and, critically, the leader in the United States, the single most lucrative consumer-health market on earth.

And buried in the announcement was the line that made Haleon inevitable. GSK committed, explicitly, to demerge the combined business and list it as a separate, publicly traded company within three years.3 This was not a vague aspiration; it was a clock. Both parents wanted out — Pfizer to fund its pharmaceutical ambitions, GSK to focus Walmsley's new "biopharma" GSK on vaccines and specialty medicines. The consumer business had finally been assembled into its final form. The only thing left was to set it free. But before it could walk out the door on its own, someone tried to buy the whole thing out from under it.

IV. The Hostile Siege: Unilever's £50B Gambit & The Rejection (January 2022)

Over the Christmas holidays of 2021, while most of corporate Britain was switched off, a small group of executives at Unilever were quietly assembling one of the most audacious bids in recent FMCG history. The target was the GSK-Pfizer consumer healthcare joint venture — the soon-to-be-Haleon — and Unilever's logic was seductive. Its own portfolio of mayonnaise, soap, and tea was growing sluggishly; bolting on a high-growth, high-margin health-and-wellbeing business could, in one stroke, reshape the company toward the categories investors actually prized.

Unilever did not make one offer. It made three, each higher than the last, across late 2021. The final proposal, revealed publicly in mid-January 2022, valued the business at £50 billion — structured as roughly £41.7 billion in cash and £8.3 billion in Unilever shares.4 It was a colossal number, one of the largest attempted acquisitions in British corporate history. And GSK's board, chaired and led on the consumer question by Emma Walmsley, rejected it. Not reluctantly, not as a negotiating posture — unanimously, and bluntly. The board stated that all three proposals "fundamentally undervalued" the business and its prospects.4

Let's war-game both sides, because this is where the investment case gets genuinely interesting. At £50 billion against 2021 sales of about £9.6 billion, Unilever was offering roughly 5.2 times revenue and around 21 times operating profit. That is a rich, strategic-buyer price — a full turn or more above where GSK had bought out Novartis just three years earlier. From GSK's seat, accepting would also have triggered an enormous, tax-heavy cash transaction and handed shareholders a slug of Unilever stock that they might not want. Rejecting it preserved the cleaner, tax-efficient demerger path and bet that public markets would reward the standalone business over time.

Here is the uncomfortable scorecard, viewed from 2026. When Haleon finally listed in July 2022, it opened at a market capitalization of roughly £30 billion. Add the roughly £10.7 billion of net debt it carried, and the implied enterprise value was about £41 billion.15 And by the middle of 2026 — four years on — Haleon's standalone enterprise value still sits in the neighborhood of £41 to £43 billion. In other words, on an enterprise-value basis, the public market has still not matched the £50 billion that Unilever was waving in GSK's face. A skeptic could argue GSK overplayed its hand, turning down a premium it has yet to recreate.

But the bull rebuttal is equally sharp, and it comes from Unilever's own shareholders. The moment the bid leaked, Unilever's stock fell about 7%, wiping billions off its value as investors recoiled. The most pointed attack came from Terry Smith of Fundsmith, one of Unilever's largest holders, who calculated that at £50 billion the deal implied a return on capital employed of just 5% — a value-destroying use of money by his math, and evidence that Unilever's management had "lost the plot."6 The market, in real time, judged that Unilever was overpaying. So which was it — did GSK leave £9 billion on the table, or did it dodge a deal so dilutive that the acquirer's own investors were in open revolt? The honest answer is that both can be true at once: the price may have been too high for Unilever to justify and higher than Haleon has since achieved on its own. With Unilever publicly ruling out any increase by January 19, 2022, the siege lifted, and GSK turned back to the plan it had committed to all along.[^8]

V. The Birth of Haleon: Demerger, IPO, & Parent Exits (2022–Present)

The name itself was a clue to the awkward birth. "Haleon" — a coinage stitched together from "hale," an old English word for good health, and "leon," evoking strength — was a brand-new word for a company with century-old products. On July 18, 2022, the demerger completed. GSK shareholders received one Haleon share for each GSK share they held, and the new company listed on the London Stock Exchange under HLN.L, with American depositary receipts trading on the NYSE under HLN.1 At a stroke, a sprawling collection of bathroom-cabinet brands became an independent, FTSE-100-scale public company — and, as Bloomberg noted, Europe's biggest listing in over a decade.1

But a spin-off is rarely a clean birth, and Haleon arrived with what we'll call its original sin: debt. To compensate the parents who were letting it go — and to optimize the tax and capital structure of the separation — Haleon was loaded with roughly £10.7 billion of net debt on day one.5 Against its earnings, that worked out to a leverage ratio of about 3.0 times net debt to EBITDA. For a stable consumer-staples business, 3.0x is heavy but survivable; the cash flows are reliable enough to service it. The problem was timing. Haleon was born in mid-2022, at the exact moment central banks began the most aggressive interest-rate tightening cycle in forty years. A company that might have refinanced cheaply in 2021 now faced a structurally higher cost of capital, and every analyst note for the next two years circled back to the same question: how fast can they pay this down?

There was a second weight on the share price, more technical but just as real: the overhang. GSK and Pfizer did not vanish at the demerger. GSK distributed most of its stake to its shareholders but retained a residual holding, and Pfizer walked away owning 32% of the new company. Markets hate a known seller. When everyone can see that two enormous shareholders intend to dispose of billions of pounds of stock, the share price sags under the anticipated supply — buyers simply wait for the next block to come cheap. Clearing that overhang became one of the defining sagas of Haleon's first two years.

Management and the parents handled it with discipline rather than a fire sale. GSK sold down its position in a series of placements and, in May 2024, disposed of its final remaining shares, exiting completely.7 Pfizer, meanwhile, executed a patient, programmatic reduction, trimming its 32% stake to roughly 22.6% by late 2024 — selling into strength, often with Haleon itself buying back chunks of the stock to support the price. Each block placed and absorbed removed a brick from the wall of supply hanging over the shares. The analytical takeaway is that the overhang was a temporary technical drag, not a fundamental flaw — and as it cleared, the market could finally value Haleon on its operating merits rather than on the fear of the next seller. So what, exactly, were those operating merits? To answer that, we have to open the cash machine and look at the gears.

VI. The Core Engine: Proportionality, Market Structure, & Unit Economics

Here is the single most important thing to understand about Haleon: not all of its revenue is created equal. The company reported total revenue of £11.03 billion for 2025, with organic growth of 3.0% and an adjusted operating margin of 22.9%.8 But that headline number is a blend of five very different businesses, some of which are extraordinary franchises and some of which are ordinary commodities dressed in branding. The investment case lives or dies on the mix, so let's walk the five categories in order of how much they matter.

Oral Health — the crown jewel. At 31.4% of revenue, roughly £3.46 billion in 2025, oral health is both the largest category and the best one.8 Its engine is Sensodyne, marketed as the world's number-one dentist-recommended brand for sensitive teeth, alongside parodontax for gum health and Polident/Poligrip for denture care. This category grew organically by around 8% in 2025 — roughly double the company average — and it is where Haleon's true pricing power lives.8 Why? Because sensitive-teeth toothpaste is not a commodity. It is a quasi-medical product with a specific, demonstrable function, recommended by a professional, purchased repeatedly by a customer who has found relief and is terrified to switch. We will return to this "professional recommendation" mechanism, because it is the heart of the whole thesis.

Pain Relief — profitable but exposed. At 23.2% of revenue, about £2.56 billion, pain relief is anchored by Advil in North America and Panadol across the Commonwealth and emerging markets.8 These are powerful, beloved brands with enormous margins. But here the analytical knife comes out: the active ingredients — ibuprofen and paracetamol — are off-patent chemical commodities that any generic manufacturer can produce identically and cheaply. When you buy Advil over store-brand ibuprofen, you are paying purely for the brand, the trust, and the packaging. That is a real moat, but a softer one than Sensodyne's, because the substitute on the shelf next to it is chemically identical and often half the price. Pain relief is where the private-label bear case has the most teeth.

Respiratory Health — high margin, high volatility. At 17.0% of revenue, roughly £1.87 billion, respiratory health sells Theraflu, Otrivin nasal sprays, and Flonase allergy relief.8 The margins are excellent. The problem is that demand for cold-and-flu products depends on something no executive can control: the weather and the severity of the season. In 2025, an unseasonably warm winter and a weak global cold-and-flu season hammered the category, and respiratory revenue fell sharply on a reported basis.8 This is the single most cyclical part of Haleon, and it is a recurring source of earnings volatility that the bears rightly fixate on. A business that needs people to get sick to hit its numbers carries a structural unpredictability that no amount of brand strength fully cures.

Vitamins, Minerals & Supplements (VMS) — fragmented and contested. At 15.3% of revenue, about £1.69 billion, VMS is led by Centrum and Caltrate.8 During the pandemic, consumers stockpiled vitamins, and the category boomed; the post-COVID normalization has since slowed it to a crawl. More worrying structurally, VMS is the category most exposed to disruption. It is highly fragmented, with low barriers to entry, and a wave of direct-to-consumer digital brands has been chipping away at the legacy multivitamin with sleek packaging, subscription models, and influencer marketing. A teenager's idea of a vitamin brand today is more likely to be an Instagram gummy than a Centrum tablet. This is the category an activist would most want to question.

Digestive Health & Other — the quiet cash cow. At 13.2% of revenue, roughly £1.45 billion, this segment holds Eno and Tums, antacid brands that are about as stable and cash-generative as consumer products get.8 Unglamorous, high-margin, sticky, and dominant in their markets — these are the brands that simply keep paying.

Now zoom out to the competitive battlefield, because Haleon does not operate alone. Its closest mirror was Kenvue Inc., the consumer health business Johnson & Johnson spun off in 2023 with about $15.4 billion in revenue and crown jewels in skin health (Neutrogena, Aveeno) and oral care (Listerine). In a landmark consolidation, Kenvue was acquired by Kimberly-Clark in mid-2026 for $48.7 billion — a deal that reshaped the entire sector and put a fresh public-market price tag on a Haleon-like asset.[^11] Beyond Kenvue, Haleon fights Procter & Gamble head-on in oral care, where P&G's Crest and Oral-B generate more than $5.5 billion; Reckitt Benckiser, whose health division (Nurofen, Strepsils) does around £6 billion; and the OTC arms of Bayer AG and Sanofi S.A., each multi-billion-dollar competitors in pain and allergy.

So how does Haleon actually win against this murderers' row? The answer is the mechanism we flagged earlier, and it deserves its own spotlight: the professional recommendation loop. A traditional consumer-staples company persuades you to buy through advertising — it shouts at you on television until you reach for its brand. Haleon does that too, but it has a second, far more durable weapon inherited from its pharmaceutical DNA. When more than 90% of dentists recommend Sensodyne to patients with sensitive teeth, or when a doctor suggests Voltaren gel for an aching joint, the brand is not competing on a supermarket shelf — it is being prescribed, informally, by a trusted authority. That endorsement creates an enormous psychological switching barrier. A consumer told by their dentist that a specific toothpaste will stop their nerve pain is not going to gamble that relief on a 40%-cheaper store brand. This is the difference between liking a brand and trusting it with your health, and it is structurally impossible for a private label to replicate, because no retailer's house brand comes with a dentist's blessing. That single mechanism is what separates Haleon's best categories from its commodity ones — and it is also the cornerstone of the moat analysis we'll formalize later. But the most interesting recent test of Haleon's strategy didn't happen in a London boardroom or an American supermarket. It happened in Tianjin.

VII. The Hidden Engine: China Joint Venture Buyout (TSKF)

In 1984, while most Western companies were still tiptoeing around the newly opening Chinese economy, a venture was quietly established in the port city of Tianjin under a mouthful of a name: 中美天津史克制药有限公司, the Sino-American Tianjin Smith Kline & French Laboratories, Ltd., known to everyone in the industry simply as 天津史克 TSKF. It was one of the earliest Sino-foreign pharmaceutical joint ventures, a marriage between a Western drug maker and Chinese state-owned partners at the very dawn of China's reform era. Four decades later, it would become the stage for Haleon's single most important modern capital-allocation decision.

TSKF is not a sideshow. It contributes roughly 40% of Haleon's total revenues in China — and China is one of the largest and fastest-growing self-care markets on the planet, with an aging population that will spend more and more on health every year.[^12] What TSKF manufactures and distributes reads like a roll call of Chinese household names. There is 芬必得 Fenbid, the ibuprofen pain reliever that is one of the best-selling OTC analgesics in the country. There is 扶他林 Voltaren, the diclofenac anti-inflammatory gel that Chinese consumers reach for on aching joints and muscles. And there is 百多邦 Bactroban, the mupirocin antibiotic ointment that sits in millions of Chinese first-aid kits. These are not niche imports; they are category leaders, built over decades inside a venture with deep local manufacturing and distribution roots.

For years, though, Haleon only owned a slice of this engine, with the rest held by its Chinese state-owned partners. That is the classic joint-venture problem we saw with Novartis, transplanted to China: profits leaking to a co-owner, strategic decisions requiring a partner's sign-off, and a structural cap on how much of the upside Haleon could ever capture. So in a two-step move announced in September 2024 and completed through 2025, Haleon bought out the remaining 45% it didn't own from its partners, 天津医药集团 Tianjin Pharmaceutical Group and 天津达仁堂集团 Tianjin Pharmaceutical Da Ren Tang Group.[^12] The price came in two tranches — roughly RMB 4.465 billion for a 33% stake and RMB 1.623 billion for a further 12% — for a combined total of around £0.7 billion.[^12][^13] By June 2025, the acquisition was complete, and TSKF became a wholly owned Haleon subsidiary.[^13]

Why does this matter so much for a £40-billion-plus company spending less than a billion? Because it is the purest expression of Haleon's entire playbook. The same logic that drove the Novartis buyout in 2018 drove the TSKF buyout in 2025: corporate simplification is accretive. Owning 100% eliminates the profit that used to leak to partners, unlocks supply-chain and manufacturing efficiencies that a shared venture made awkward, and — most importantly — hands Haleon the full economic upside of China's demographic wave rather than a partial claim on it. It is real optionality on the fastest-growing major self-care market in the world, bought at a price that looks modest against the strategic prize. The skeptic's caveat is fair: China carries geopolitical and regulatory risk, and a wholly owned subsidiary concentrates rather than diversifies that exposure. But on the merits of the transaction itself, this was the company doing exactly what it says it does — buying out complexity to own the cash flows outright. The question, then, is whether the people running Haleon can be trusted to keep making calls this disciplined.

VIII. Current Management, Incentives, & Credibility

The man who has steered this business through all of it is Brian McNamara, and his résumé tells you why GSK trusted him with it. Before taking the helm of the GSK Consumer Healthcare business in 2016 — the role that became Haleon CEO — McNamara built his career inside the FMCG-pharma hybrid world that Haleon embodies, with senior stints at Novartis and a foundational training at Procter & Gamble, the West Point of consumer-goods management. He is not a charismatic founder spinning a vision; he is a professional operator, valued for consistency, supply-chain rigor, and the unglamorous discipline of running a global brand portfolio. In an industry where the product is trust, having a steady, low-drama executive is arguably a feature, not a bug.

His financial counterpart changed in late 2024. Dawn Allen was appointed Chief Financial Officer in November 2024, succeeding Tobias Hestler. Allen arrived with roughly 25 years of experience spanning Mars Inc. and Tate & Lyle plc, with a reputation built specifically on large-scale corporate transformation and margin optimization — precisely the skill set a company trying to expand margins while paying down £8-plus billion of debt would want in the CFO chair. And in the boardroom, the chair passed at the start of 2026: Vindi Banga succeeded Sir Dave Lewis as Chair on January 1, 2026, after Lewis stepped down at the end of 2025.9 Banga's pedigree is almost poetically fitting — he spent 33 years at Unilever, the very company that tried to buy Haleon in 2022, rising to lead Hindustan Unilever and run Unilever's global foods business. Bringing that depth of FMCG credibility onto Haleon's board signals where the company sees its identity: not as a pharma orphan, but as a consumer-goods champion.9

Now, the part that separates rhetoric from reality — incentives. On paper, Haleon's pay structure is built to force long-term alignment. The CEO is required to hold shares worth 500% of base salary, and the CFO 300%, and crucially these holdings must be maintained for two years after the executive departs — a design meant to stop a leader from juicing short-term numbers and cashing out. Compensation is tied to three metrics that, helpfully for investors, are exactly the right ones: organic revenue growth, adjusted operating profit, and cumulative free-cash-flow conversion. That last one matters enormously for a debt-laden company — it rewards turning accounting profit into actual cash, which is what pays down borrowings.

So has management earned credibility, or just designed nice slides? The evidence so far is genuinely mixed-to-positive, and we should hold it to the standard of behavior over time rather than press-release adjectives. On the positive side, the execution on cost has been real. Haleon ran a productivity program targeting around £300 million of annual savings, and the proof is in the margin: adjusted operating margin expanded to 22.9% in 2025, up from 22.3% in 2024, even as a brutal collapse in high-margin respiratory sales and persistent input-cost inflation were dragging the other way.8 Expanding margins into those headwinds is hard, and it suggests the cost discipline is more than a talking point.

The tougher test was the quality of growth, and here analysts pushed hard. Through 2024 and into 2025, the central challenge on earnings calls was whether Haleon's organic growth was real — driven by customers buying more units (volume) — or merely the optical result of pushing through price increases that customers grudgingly absorbed. Price-only growth is fragile; it eventually meets the limit of what shoppers will pay before they defect to private label. To management's credit, they were transparent about the issue and pointed to a return to positive volume/mix as 2025 progressed, rather than hiding behind a single blended growth number.8 That is the right way to handle a hard question — concede the distinction, then show the data turning. The lingering doubt, which no investor should wave away, is durability: positive volume in a single year is encouraging, but the franchise has to prove it can hold volume and price together through a full cycle, especially in the commodity-exposed pain and VMS categories. Which is exactly the kind of pressure a skeptical investor would apply — so let's apply it deliberately.

IX. Activist Stress Test & The Bear vs. Bull Case

Imagine a sharp long/short fund — call it an Elliott-style activist — building a position in Haleon and preparing a slide deck for management. What would they attack? Two things, primarily.

First, portfolio complexity. The activist's pitch is brutally simple: Haleon is two companies wearing one trench coat. There is the magnificent business — oral health and the better pain brands, with structural pricing power and the dentist-recommendation moat — and then there is the mediocre business — fragmented, low-growth, disruption-prone VMS and therapeutic skin health. Why, the activist demands, do you keep dragging down your multiple by holding the mediocre half? Haleon has shown it can prune; it sold ChapStick to Suave Brands in 2024 for about $430 million, a clean divestment of a non-core asset.10 The activist would say: do that, but ten times bigger. Aggressively divest VMS and skin health, become a focused pure-play in oral care and pain, and let the market re-rate the remaining jewel upward. Management's counter — that scale across categories provides distribution leverage and that VMS rides the same aging-demographic tailwind — is reasonable but not unassailable, and this is the most legitimate strategic critique on the table.

Second, capital allocation. Haleon bought back over £1 billion of its own shares across 2024 and 2025, even while carrying a debt pile that stood around £8.5 billion. The activist's objection is sequencing: in a world of structurally higher interest rates, every pound spent buying back stock is a pound not spent retiring debt that now costs real money to service. Buybacks at a full valuation, the critique goes, smell less like value creation and more like supporting the share price during the parent-overhang sell-down — financial defense dressed as capital return. Management would argue that near-100% free-cash-flow conversion lets them do both at once: deleverage and return cash. The honest assessment is that they have, in fact, been doing both — but the activist is right that the balance is a live judgment call, and at higher rates the case for tilting harder toward debt paydown strengthens.

With the stress test on the table, let's lay out the two cases cleanly.

The Bull Case. First, the brand moat is structurally unique. The dentist-and-doctor recommendation loop — the professional endorsement that no private label can buy — gives the best categories a defensibility ordinary consumer staples lack. Second, the wholly owned China engine. Taking full control of TSKF positions Haleon to capture 100% of the upside as an aging Chinese population spends ever more on self-care, optionality that few Western consumer companies possess. Third, the cash machine. With free-cash-flow conversion running near 100%, Haleon can deleverage, grow its dividend, and buy back stock simultaneously — a financial flexibility that compounds quietly over years.

The Bear Case. First, private-label erosion. Retail giants from Walmart to Boots are pouring resources into their own-brand ibuprofen, paracetamol, and vitamins, and on chemically identical products the only thing standing between Haleon and the store brand is marketing spend — a war that gets more expensive every year. Second, weather and flu volatility. Too much of Haleon's high-margin profit rides on the severity of the respiratory season, and as 2025 showed, one warm winter can erase a category's growth overnight. Third, the innovation question. Haleon's "innovation" is overwhelmingly line extensions — a new Sensodyne Pronamel Active Shield variant, a reformulated gel — rather than genuine breakthrough discovery. It is a marketing and reformulation machine, not a molecule-discovery machine, which caps how much organic growth it can manufacture from new science rather than from price and incremental volume.

To referee this debate properly, we need a framework — two of them, in fact.

X. Strategic Frameworks: Porter's 5 Forces & Hamilton's 7 Powers

Let's run Haleon through Hamilton Helmer's 7 Powers first, because it cuts straight to the durability of competitive advantage.

Brand Power (High). This is Haleon's most obvious source of strength. Sensodyne, Advil, Panadol, and Centrum carry decades of accumulated consumer trust, and that trust translates into low price elasticity in the premium categories — customers will pay up rather than experiment with their health. The caveat, as the bear case noted, is that brand power is strong in oral health and weak in commodity pain, so this "power" is unevenly distributed across the portfolio.

Cornered Resource (High). Here is the most interesting and most defensible power. The professional recommendation loop — the fact that the overwhelming majority of dentists recommend Sensodyne and that doctors steer patients toward specific Haleon brands — functions as a cornered resource that competitors cannot simply buy their way into. Layered on top is genuine proprietary product technology: the NovaMin calcium sodium phosphosilicate formulation in certain Sensodyne products, for instance, is a patented physical mechanism for repairing tooth surfaces, not just a marketing story. That combination of professional endorsement plus protected formulation is the closest thing Haleon has to an unassailable moat.

Scale Economies (Moderate). Haleon's enormous global manufacturing footprint and an R&D budget exceeding £250 million per year give it cost and capability advantages that small challengers and generic manufacturers cannot match. But "moderate" is the right grade, because in consumer health scale does not compound infinitely the way it does in, say, semiconductors — a regional generic maker can still produce cheap ibuprofen competitively.

Switching Costs (Moderate-High). For a casual purchase, switching costs are near zero — you might grab a different antacid on a whim. But for chronic conditions, they spike. Once someone with genuinely sensitive teeth finds the toothpaste that stops the nerve pain, the perceived risk of switching to an unproven alternative is high, and they stick. The depth of the switching cost is therefore a direct function of how medical the use case is.

Now Porter's Five Forces, which frames the competitive pressure rather than the firm's advantages.

Threat of Substitutes (High). This is the dominant force and the core of the bear case. Generic, store-brand chemical equivalents — identical ibuprofen, identical paracetamol, identical multivitamins — sit on the same shelf at a fraction of the price. In the commodity categories, the substitute is not merely comparable; it is molecularly the same thing. This single force is the biggest structural threat to Haleon's pricing power.

Bargaining Power of Buyers (Moderate-High). The "buyers" here are the giant retail consolidators — Walmart, Walgreens, Boots, Amazon — who control access to the shelf and the customer. Their leverage is real and growing, and their own private-label ambitions make them competitors as well as customers. The countervailing force is that they must stock Haleon's power brands; a pharmacy that didn't carry Sensodyne or Advil would lose customers. So the relationship is a tense mutual dependence rather than outright retailer dominance.

Threat of New Entrants (Low). Building a globally trusted healthcare brand from scratch requires hundreds of millions in sustained marketing, decades of accumulated consumer trust, and navigation of strict pharmaceutical regulation across every market. The DTC vitamin upstarts can nibble at the fragmented edges of VMS, but no new entrant is going to build the next Sensodyne quickly. The regulatory and trust barriers that make this industry slow-moving are, for an incumbent, a feature.

Put the two frameworks together and a clear picture emerges. Haleon's defenses are genuinely formidable in oral health — cornered resource, brand power, and switching costs all stacked together — and progressively weaker as you move toward the commodity end of the portfolio, where the high threat of substitutes and powerful buyers bear down. The company is not uniformly moated; it is a barbell of brilliant franchises and contested commodities. The investment question is whether the brilliant end keeps growing fast enough to outweigh the contested end. That framing, in turn, dictates exactly what an investor should watch.

XI. Playbook, Lessons, & Key KPIs to Track

Step back from the details and two durable lessons emerge from the Haleon story — lessons that travel well beyond this one company.

The first is the professional recommendation moat. The most valuable insight in the entire Haleon case is that when you sell consumer goods, the deepest and most defensible moat is often not the end-consumer's affinity for your brand, but a trusted intermediary's professional endorsement of it. A celebrity ad campaign can be outspent; a logo can be copied; a price can be undercut. But a dentist's recommendation, repeated across millions of appointments, builds a form of trust that competitors cannot buy and private labels cannot fake. Any business that can insert itself into a professional's recommendation — a doctor, a dentist, a mechanic, an architect — owns something far stickier than advertising can ever produce.

The second is the complexity tax of joint ventures. Twice now — buying out Novartis in 2018 and the TSKF partners in 2024–2025 — Haleon and its predecessors have demonstrated the same truth: shared ownership imposes a hidden tax in the form of leaked profit, divided strategy, and constrained flexibility, and paying to eliminate that complexity is reliably accretive to long-term value. Corporate simplification is not glamorous, but it compounds. The lesson for investors is to watch how a company treats its partial ownerships — the willingness to pay up for clean, 100% control is often a marker of disciplined management thinking in decades, not quarters.

So what should a long-term investor actually track? Resist the temptation to drown in metrics. Three KPIs capture the essence of whether the thesis is working.

First, organic revenue growth — and specifically its composition. The headline growth number, which management targets in roughly the 4–6% range, matters less than the split between volume and price. Growth driven by customers buying more units is durable; growth driven purely by raising prices is borrowed from the future, because it eventually pushes shoppers toward private label. Watching whether positive volume/mix sustains — rather than relying on price — is the single best read on whether the brand moat is genuinely holding.

Second, adjusted operating profit margin. With a target of holding above roughly 22.5%, this number is the scoreboard for whether the £300 million productivity program is genuinely offsetting input-cost inflation and the periodic gut-punches of a weak respiratory season. A margin that keeps grinding higher despite headwinds, as in 2025, is evidence of real operational control; a margin that slips would signal that pricing power and cost discipline are losing the tug-of-war against commoditization.

Third, free-cash-flow conversion and the leverage ratio. For a company born with the original sin of £10.7 billion in debt, the speed of deleveraging is existential. The target investors should watch is net debt to EBITDA falling below roughly 2.5 times, powered by free-cash-flow conversion near 100%. This single relationship tells you whether the cash machine is real and whether management is winning its race against a higher cost of capital. If conversion stays high and leverage keeps falling, the balance sheet stops being a worry and starts being a weapon for dividends and buybacks. If it stalls, every other strength is compromised.

XII. Outro & Epilogue

The arc of Haleon is, in the end, a story about focus. For a century, the world's best self-care brands lived as profitable afterthoughts inside drug companies whose hearts were elsewhere — tolerated for their steady cash, starved of attention, treated as a hedge against the casino of pharmaceutical R&D. It took an intricate decade of asset swaps, a contested £13 billion buyout, a transformative merger with Pfizer, a hostile £50 billion siege from Unilever, and finally a debt-laden demerger to carve them out into a single, focused, independent company. Whether GSK was wise to reject Unilever's premium remains genuinely debatable — the public market has not yet matched that price — but what is no longer debatable is that these brands now have an owner whose entire reason for existing is to nurture them.

What comes next rests on a demographic tailwind that is about as reliable as forecasts ever get: the world is aging, and aging populations spend more on health, on pain, on supplements, on the daily maintenance of bodies that need more upkeep. Haleon sits directly in that current, with a wholly owned engine in the world's largest aging society and a portfolio of brands that professionals recommend by name. The risks are equally real — the commodity shelf below the premium brands, the warm winters that erase a season's profits, the absence of breakthrough innovation, and a debt load still being worked down in a higher-rate world. Haleon is neither the unblemished compounder its supporters describe nor the fragile, over-levered orphan its critics warn of. It is something more interesting: a barbell of genuinely moated franchises and genuinely contested commodities, run by operators whose discipline will be tested not in any single year, but across the long, unglamorous decades that consumer health is measured in.

References

-

GSK spins off Haleon in Europe's biggest listing in a decade — Bloomberg, 2022-07-18 ↩↩↩↩

-

GSK to acquire full ownership of Consumer Healthcare joint venture — GSK Press Release, 2018-03-27 ↩↩

-

GSK and Pfizer to combine consumer healthcare businesses — GSK Press Release, 2018-12-19 ↩↩

-

GSK response to Unilever unsolicited proposals — GSK Press Release, 2022-01-15 ↩↩

-

London Stock Exchange Haleon PLC LSE:HLN Company Page — London Stock Exchange, 2026 ↩↩

-

Unilever unlikely to raise £50 billion GSK Consumer bid, investors say — Wall Street Journal, 2022-01-18 ↩

-

Appointment of Vindi Banga as Chair — Haleon / Investegate, 2025-11-10 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube