Harvia: Healing with Heat

I. Introduction: The "Hidden" Global Champion (0:00 – 0:10)

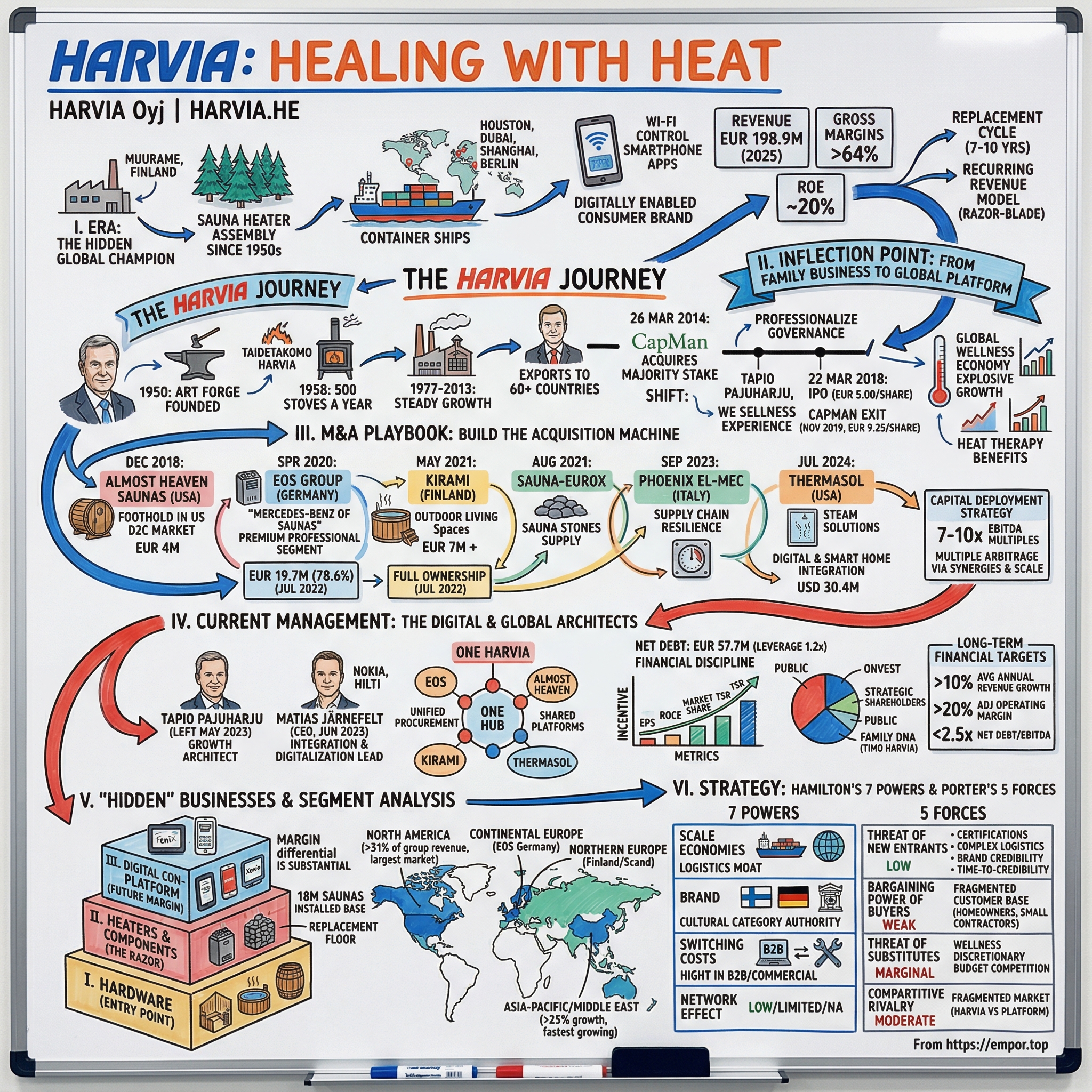

There is a factory in Muurame, a small town just outside Jyväskylä in central Finland, where workers assemble sauna heaters the way their predecessors have done since the mid-1950s—steel casings, heating elements, stone compartments, the same fundamental architecture that has made the Finnish sauna a cultural institution for centuries. But something has changed. The heaters rolling off the line today are not destined for Finnish lake houses. They are being packed into shipping containers headed to Houston, Dubai, Shanghai, and Berlin. Some carry touchscreen control panels with Wi-Fi connectivity. Others are bundled with smartphone apps that let a homeowner in Connecticut preheat their backyard sauna from the office. The company that makes them, Harvia Oyj, has taken one of the oldest wellness traditions on earth and turned it into a global, publicly listed, digitally enabled consumer brand.

Most investors have never heard of Harvia. The sauna industry does not feature in the same conversations as cloud computing, artificial intelligence, or electric vehicles. And yet the numbers demand attention. Revenue reached a record EUR 198.9 million in 2025, growing at over thirteen percent. Gross margins run above sixty-four percent—territory more commonly associated with software companies than manufacturers of steel appliances. Return on equity sits around twenty percent. The company commands more than twenty percent of the global sauna heater market, making it the clear leader in an industry where the top five players collectively hold less than half the total share. The installed base of roughly eighteen million saunas worldwide creates a replacement cycle—heaters need swapping every seven to ten years—that functions as a form of recurring revenue, not unlike the razor-blade model but with stone-filled steel instead of cartridges.

Harvia listed on the Nasdaq Helsinki in March 2018 at EUR 5.00 per share, giving it a market capitalisation of roughly EUR 93.5 million. The stock peaked near EUR 60 during the pandemic-era wellness boom in 2021, fell sharply as post-COVID demand normalised and European energy prices spiked, and trades today at around EUR 35—a market capitalisation of approximately EUR 655 million. The company has been on a seven-times journey from IPO price to current levels, yet the most interesting question about Harvia is not where it has been but what it is becoming: a vertically integrated wellness platform with a growing digital layer, an expanding North American footprint, and a disciplined acquisition machine that has drawn comparisons to Constellation Software in the spa world.

This is the story of how a Finnish family forge became a private equity transformation story, then a public market compounder—and why the ancient art of heating rocks might be one of the most defensible businesses in European consumer goods.

II. The Inflection Point: From Family Business to Global Platform (0:10 – 0:35)

In 1950, a metalworker named Tapani Harvia opened a small workshop in Jyväskylä called Taidetakomo Harvia—"Art Forge Harvia." The initial business was decorative ironwork and hearth doors, the kind of artisanal metalcraft that sustained small Finnish workshops in the post-war years. Sometime in the mid-1950s, Tapani built a wood-burning sauna stove for his own use. Neighbours noticed. By 1958, the forge was producing roughly five hundred stoves a year. The sauna business had found its founder.

Over the following decades, the company grew steadily but unremarkably. The 1970s oil crisis boosted demand for wood-burning heaters. In 1972, Tapani relocated to a purpose-built factory in Muurame—the same site where Harvia operates its headquarters today. His son Risto took over as CEO in 1977 and would run the business for the next thirty-six years. Electric heaters were added in the 1980s as Finnish urbanisation made wood-burning impractical for apartment saunas. Exports to Central Europe, Russia, the United States, and Asia began in the 1990s. By the early 2010s, Harvia generated roughly EUR 47 million in annual revenue with around three hundred employees, exporting to over sixty countries. It was a successful, conservative, family-run Finnish industrial company—profitable, respected, and firmly in its comfort zone.

Then, on 26 March 2014, everything changed. CapMan, one of Finland's leading private equity firms, announced the acquisition of an eighty percent majority stake in Harvia from the founding family through its Buyout X fund. The Harvia family retained approximately twenty percent and continued in management roles, but control had passed to professional investors with a very different ambition for the business.

The CapMan playbook was straightforward but transformative. First, clean up the balance sheet and professionalise the governance structure. Second, shift the strategic narrative from "we sell heaters" to "we sell a wellness experience"—expanding the product range beyond core heaters into complete sauna rooms, accessories, control electronics, and steam solutions. Third, build the management infrastructure needed for international scale. Tapio Pajuharju, a consumer goods executive with experience running the cosmetics company Lumene, joined the board in 2014 and became CEO in June 2016, replacing the last family member in the top role. His mandate was to prepare Harvia for a public listing and the aggressive growth phase that would follow.

The IPO came on 22 March 2018, when Harvia's shares began trading on the Nasdaq Helsinki at EUR 5.00 apiece. The company issued 9 million new shares, raising approximately EUR 45 million in gross proceeds, while CapMan retained roughly 69.5 percent at listing. The market's initial reaction was polite but unenthusiastic. Analysts valued Harvia as an industrial manufacturer—a maker of metal stoves—and assigned it a multiple that reflected that perception. What they missed was the "wellness" tailwind that was about to transform the entire industry.

The global wellness economy was entering a decade of explosive growth. Heat therapy—long a staple of Finnish and Germanic cultures—was gaining mainstream scientific credibility through researchers and public health advocates. Podcasters and biohacking influencers amplified the message: regular sauna use was associated with cardiovascular benefits, stress reduction, improved sleep, and longevity. The sauna was no longer a Nordic curiosity. It was becoming a global wellness essential. And Harvia, freshly professionalized by CapMan and armed with IPO capital, was perfectly positioned to ride the wave.

CapMan's exit was staged over the following eighteen months. They sold shares in tranches through 2019, with the final 12.3 percent stake—roughly 2.3 million shares—sold to Finnish investment company Onvest Oy in November 2019 at EUR 9.25 per share, nearly doubling the IPO price. The PE firm had done its job. What happened next would be up to the public market and the acquisition machine that Pajuharju was about to build.

III. The M&A Playbook: Did They Overpay? (0:35 – 1:00)

The first deal came just nine months after the IPO, and it signalled exactly where Harvia was headed. In December 2018, the company acquired the business operations of Almost Heaven Saunas, a forty-year-old manufacturer based in Renick, West Virginia, for approximately EUR 4 million on a debt-free basis. Almost Heaven was the largest traditional sauna maker serving the American consumer market, known for its barrel saunas and cabin-style units—the rustic, Instagram-friendly products that were gaining traction with health-conscious American homeowners. The company had grown from about USD 3.5 million in revenue in 2014 to roughly USD 9 million by 2017.

On paper, EUR 4 million for a sub-ten-million-dollar revenue business looks modest. But the strategic value was far greater than the price tag suggested. Almost Heaven gave Harvia three things it could not easily build organically: a domestic US manufacturing base, an established direct-to-consumer distribution channel, and an American brand identity in a market where "Finnish sauna" was an exotic concept but "backyard barrel sauna" was something a suburban dad in Colorado could picture next to his grill. The US sauna market was—and remains—enormously underpenetrated compared to Finland or Germany. Roughly twenty million American households have the income to support a sauna purchase. Almost Heaven was the foothold from which Harvia would attack this market.

The second acquisition was bigger and bolder. In the spring of 2020, Harvia acquired a roughly 78.6 percent stake in EOS Group, a German manufacturer of premium sauna solutions, for EUR 19.7 million—part of a total debt-free enterprise value of EUR 25.5 million for the full company. EOS was, in the words of one industry observer, the "Mercedes-Benz of saunas." Founded over seventy-five years ago and based in Driedorf, Germany, EOS served the professional segment—hotels, spas, fitness centres, commercial wellness facilities—with premium heaters, gas-powered units, steam generators, and advanced electronic control systems manufactured to exacting German engineering standards.

EOS filled a critical gap in Harvia's portfolio. The core Harvia brand was strongest in the residential mid-market. EOS opened the door to the high-end professional segment, where margins are higher, relationships are stickier, and the installed base creates long-term maintenance and replacement revenue. The control electronics were particularly valuable—EOS's Xenio system was the industry standard for commercial sauna installations, embedding Harvia's technology into the operating infrastructure of hotels and wellness centres worldwide. Harvia completed its ownership of EOS in July 2022, acquiring the remaining German shares for EUR 19.0 million at the same EBITDA multiple as the original deal—a disciplined approach that avoided the valuation creep that often afflicts staged acquisitions.

In May 2021, Harvia moved into an adjacent category with the acquisition of Kirami, Finland's leading still-water hot tub manufacturer, for EUR 7 million at closing plus up to EUR 4 million in performance-based deferred consideration. Kirami was a pioneer in wood-heated hot tubs—a product category that was exploding during the pandemic as homeowners invested in outdoor living spaces. Was this "di-worse-ification"—the dreaded PE-backed brand extension into an unrelated category? The strategic logic suggested otherwise. Kirami's customer was Harvia's customer: the same wellness-oriented homeowner who bought a sauna also wanted a hot tub. The cross-selling opportunities through Harvia's distribution network were immediate. And the product shared enough manufacturing DNA—steel fabrication, wood components, heating elements—that operational synergies were real.

The pattern continued. In August 2021, Harvia acquired Sauna-Eurox, one of the world's largest suppliers of sauna stones, for undisclosed terms—vertical integration into a critical consumable component. In September 2023, Phoenix El-Mec, an Italian manufacturer of electromechanical timer switches (a key component in basic Harvia heaters), was brought in-house for supply chain resilience. And in July 2024, the most significant recent deal: ThermaSol, a US pioneer in steam solutions founded in 1958 and headquartered in Round Rock, Texas, acquired for USD 30.4 million. ThermaSol brought not just steam technology but digitally connected controls with Wi-Fi integration and smart home compatibility—the kind of digital layer that transforms a commodity appliance into a connected wellness platform.

The overarching capital deployment strategy deserves analysis. Harvia has consistently paid between seven and ten times EBITDA for its acquisition targets—reasonable multiples for niche industrial businesses in fragmented markets. It then scales these businesses through its global distribution network, applies its manufacturing and procurement expertise, and extracts synergies that effectively "arbitrage" the multiple down. The EOS acquisition, for instance, generated at least EUR 2.2 million in annual synergies by 2024. ThermaSol is targeted for EUR 1.7 million in annual synergies by the end of 2027. These are not transformative deals that bet the company. They are disciplined tuck-ins that compound over time—a playbook that shares more with Constellation Software's approach to vertical market software than with the leveraged buyout model that created Harvia in the first place.

IV. Current Management: The Digital & Global Architects (1:00 – 1:20)

When Tapio Pajuharju announced in November 2022 that he would leave Harvia the following May—citing a desire for "new challenges outside Harvia"—the company faced a succession question that would define its next chapter. Pajuharju had been the growth architect: the CEO who took a family business through private equity transformation, IPO, and a string of acquisitions that tripled revenue from EUR 62 million at the 2018 listing to a peak of EUR 179 million in 2021. His departure meant Harvia needed someone who could shift the emphasis from "acquiring growth" to "integrating and digitising what we've built."

The board's choice was revealing. Matias Järnefelt, announced on 28 March 2023 and installed as CEO on 1 June 2023, came not from the sauna industry but from the intersection of technology and industrial distribution. Born in 1974 and educated in industrial engineering and management, Järnefelt spent fourteen years at Nokia—including roles as Director of Corporate Strategy and Global Head of Sales for Nokia Gear—before moving to Hilti, the Liechtenstein-based premium power tools and construction technology company, where he spent eight years rising to Head of Northern Europe and Managing Director of Great Britain. At Hilti, he ran a business that shares striking structural similarities with Harvia: premium-branded hardware sold through a professional distribution network, with an increasing digital services layer wrapped around the physical product. The message was clear: Harvia's next phase would be about technology, integration, and global commercial execution, not about deal-making.

Järnefelt's management philosophy centres on "One Harvia"—a programme to integrate the fragmented collection of acquired brands, factories, and distribution networks into a unified operating platform while preserving the distinct identities that made each brand valuable. EOS remains the premium professional brand. Almost Heaven retains its rustic American identity. Kirami keeps its outdoor lifestyle positioning. ThermaSol brings its digital steam heritage. But behind the scenes, procurement is being centralised, supply chains are being rationalised, ERP systems are being harmonised, and the digital control technology is being developed as a shared platform across all product lines.

The financial discipline is reflected in the balance sheet. Net debt stood at EUR 57.7 million at the end of 2025—a leverage ratio of just 1.2 times adjusted EBITDA. That is conservative for a company that has been on a seven-year acquisition spree. It means Harvia retains significant capacity for further M&A without needing to raise equity, while maintaining the financial flexibility to weather cyclical downturns in the housing and renovation markets that inevitably affect demand.

The CFO, Ari Vesterinen, provides institutional continuity in the finance function. The broader management board spans a dozen executives covering regional operations (Northern Europe, Continental Europe, North America, Asia-Pacific), product development, manufacturing, and marketing—reflecting a business that has outgrown its family-firm origins and now operates as a genuinely global enterprise with roughly 700 employees.

The incentive structure tells investors what management is optimising for. The 2023-2025 long-term incentive plan—which concluded with 13,823 shares transferred to participants in March 2026—was weighted fifty percent on earnings per share, thirty percent on return on capital employed, and twenty percent on market share gains. The new 2026-2028 plan, announced on 2 April 2026, shifts the targets toward total shareholder return, revenue growth, EBIT margin, and CO2 emissions reduction—signalling a management team that is thinking about both profitability and sustainability as the business scales. The maximum payout of 77,924 shares across up to thirty-three participants represents meaningful skin in the game without excessive dilution.

Ownership remains concentrated in strategic hands. Onvest Oy, the Finnish investment company that acquired CapMan's final stake, is a significant shareholder. WestStar, Nordea Funds, and Evli Fund Management provide institutional anchoring. Tiipeti Oy, linked to Timo Harvia—a member of the founding family who serves as Head of Innovation and Technology on the management board—ensures that family DNA persists in the business seventy-six years after Tapani Harvia lit the first forge.

Harvia's long-term financial targets remain ambitious: ten percent average annual revenue growth, adjusted operating margin above twenty percent, and net debt to EBITDA below 2.5 times. The 2025 results showed revenue growth of 13.5 percent and an adjusted operating margin of 19.6 percent—just shy of the twenty percent threshold, a miss that caused the stock to dip despite the strong top line. Closing that margin gap while funding continued expansion is the central challenge for Järnefelt's tenure.

V. The "Hidden" Businesses & Segment Analysis (1:20 – 1:40)

Harvia reports as a single segment, which means investors must dig into the product categories and geographic splits to understand where the value actually sits. The company's internal organisation, however, reveals a multi-layered business with distinctly different growth profiles and margin characteristics.

The first layer is the hardware—sauna rooms, hot tubs, barrel saunas, infrared cabins. These are the "entry point" products that bring customers into the Harvia ecosystem. A homeowner renovating a bathroom, a hotel developer designing a wellness floor, or a suburban American dad building a backyard retreat—all start with the physical structure. This layer is capital-intensive to ship (sauna rooms are bulky), moderately cyclical (tied to construction and renovation activity), and carries healthy but not spectacular margins. It is the top of the funnel.

The second layer is the "razor" in the razor-blade model: heaters and components. Every sauna needs a heater. Every heater needs sauna stones. Every installation needs ventilation components, lighting, and accessories. And critically, every heater needs replacing roughly every seven to ten years, because the extreme thermal cycling—heating to 80°C or higher, cooling, reheating, over thousands of sessions—eventually degrades the elements and the stone chamber. With an estimated eighteen million saunas installed globally, this replacement cycle creates a floor under Harvia's revenue that is largely independent of new construction activity. The customer who bought a sauna in 2016 will need a new heater by 2024 or 2025, regardless of whether the housing market is booming or busting. And when they replace, they tend to trade up—choosing a better heater with smarter controls, which lifts average selling prices over time.

The third and most strategically significant layer is the digital control platform. This is where Harvia's future margin expansion lives. The company's Fenix touchscreen controllers for residential saunas feature Wi-Fi connectivity, learning algorithms that optimise heating patterns based on usage habits, and integration with the MyHarvia 2 mobile app—allowing users to start and monitor their sauna remotely. For commercial installations, the EOS Xenio control system is the industry standard, managing multiple sauna rooms, steam generators, and environmental parameters from a centralised interface. ThermaSol's acquisition in 2024 added digitally connected steam shower controls with smart home integration.

Think of this digital layer the way Apple thinks about iOS relative to the iPhone hardware. The physical sauna is the device. The control unit is the operating system. And the app is the interface that creates ongoing engagement, data collection, and the potential for future software-based services. A "dumb" heater with a mechanical timer is a commodity. A connected heater with a touchscreen controller, remote access, and usage analytics is a platform. The margin differential between these two propositions is substantial, and the share of connected products in Harvia's mix is growing steadily. Industry research suggests that forty-four percent of sauna buyers now express demand for smart sauna systems—a proportion that is only going to increase as younger, more digitally native consumers enter the market.

The geographic revenue split reveals another dimension of the story. North America has emerged as Harvia's single largest market, contributing roughly thirty-one percent or more of group revenue in 2025. This is remarkable for a company that had essentially zero US presence before the Almost Heaven acquisition in 2018. The build-out has been methodical: Almost Heaven provided domestic manufacturing and a consumer brand, ThermaSol added steam technology and digital controls, and Harvia's own heater range has been distributed through an expanding network of US dealers, contractors, and online channels. Continental Europe—anchored by the EOS brand in Germany—and Northern Europe (the traditional Finnish and Scandinavian heartland) contribute the bulk of the remainder, while Asia-Pacific and the Middle East are the fastest-growing region, up over twenty-five percent in 2025.

The "aftermarket" opportunity deserves special emphasis because it is the element of Harvia's business that most closely resembles a recurring revenue model. Sauna stones need periodic replacement. Heaters degrade and require service or replacement. Control units can be upgraded. Accessories are consumed and replenished. For a company with the dominant market share in installed heaters, the aftermarket creates a revenue stream that is predictable, high-margin, and growing in line with the installed base—which expands every year as new saunas are built and old ones are maintained. This is not a SaaS subscription, but the economic characteristics—high retention, low customer acquisition cost, predictable demand patterns—share more with software than with traditional capital equipment sales.

VI. Strategy: Hamilton's 7 Powers & Porter's 5 Forces (1:40 – 2:00)

The fundamental question for any investor in Harvia is whether the company's market position is protected by durable competitive advantages or merely reflects first-mover status in a niche that competitors could erode. Hamilton Helmer's Seven Powers framework helps structure this analysis.

The most powerful advantage is Scale Economies, and they operate primarily through distribution. A sauna heater is a heavy, bulky object filled with stones. Shipping it from a factory in Finland to a distributor in Texas is expensive. Harvia's global distribution network—built over decades in the Nordic market and expanded through acquisitions in the US and Germany—amortises these logistics costs across a volume base that no smaller competitor can match. A regional manufacturer in, say, Estonia can make a perfectly adequate heater, but it cannot get it to a customer in Seattle or São Paulo at a cost that competes with Harvia's containerised global supply chain. This logistics moat is particularly acute for the heavier, bulkier product categories: complete sauna rooms, barrel saunas, and hot tubs. In these categories, shipping economics effectively limit competition to companies with continental-scale distribution.

Brand is the second significant power, and it manifests in a culturally specific way. In the global sauna market, "Finnish" is the ultimate quality signal. It carries the same category authority that "Swiss" carries in watches or "Italian" carries in luxury fashion. Harvia is not just Finnish—it is one of the oldest continuously operating Finnish sauna companies, with seventy-six years of heritage. For a hotel developer in Dubai specifying a spa installation, or an American wellness enthusiast researching their first home sauna, the Harvia brand conveys authenticity that non-Finnish competitors struggle to replicate. The EOS brand extends this authority into the German-speaking professional market, where "made in Germany" carries its own engineering cachet. Harvia effectively holds the two strongest origin-story cards in the industry.

Switching Costs are low for individual consumers—a homeowner replacing a heater can theoretically choose any compatible brand—but materially higher in the B2B segment. Hotels and commercial wellness facilities that have specified Harvia or EOS equipment are integrated into the company's design software, maintenance protocols, and control systems. A resort chain that has standardised on EOS Xenio controllers across twenty properties does not casually switch to a competitor's control platform, because that would require retraining maintenance staff, recertifying installations, and replacing integrated control hardware. This is the same lock-in dynamic that drives enterprise software retention, except the "software" is embedded in physical infrastructure.

The powers Harvia arguably lacks are worth noting. There is no meaningful Network Effect—one sauna owner's use does not make the product more valuable to another. Counter-Positioning is limited; larger industrial conglomerates could theoretically enter the sauna market, though none has found the niche attractive enough to justify the investment. Process Power is difficult to assess from outside, though the manufacturing expertise accumulated over seventy-six years in a specialised product category is not trivially replicable.

Porter's Five Forces reinforce the picture. Threat of New Entrants is low for reasons that are deceptively powerful. Sauna heaters involve fire safety certifications, electrical safety compliance across multiple jurisdictions, and complex logistics for heavy goods—barriers that are individually manageable but collectively formidable. A new entrant must simultaneously develop product expertise, obtain multi-country certifications, build a distribution network, and establish brand credibility in a market where the category leader has been operating for over seven decades. The capital intensity is modest compared to heavy industry, but the time-to-credibility is long.

Bargaining Power of Buyers is fragmented and weak—exactly the market structure that supports pricing power. Harvia's customer base consists overwhelmingly of individual homeowners, small contractors, independent sauna dealers, and boutique hotel developers. No single customer represents a material share of revenue. There is no "Walmart of saunas" that can dictate terms. This fragmentation allows Harvia to maintain premium pricing while growing volume—a combination that is extremely difficult to achieve in markets with concentrated buyer power.

Threat of Substitutes exists at the margins. Home exercise equipment, spa memberships, cold plunge pools, and general wellness spending compete for the same discretionary budget. But the sauna itself—as a category—has been gaining share of the wellness wallet, not losing it, driven by the scientific evidence and cultural momentum discussed earlier. Within the sauna category, the most relevant substitution risk is between electric and infrared saunas, where Harvia competes in both formats and is therefore hedged against any shift in consumer preference.

Competitive Rivalry is moderate. The market is highly fragmented—the top five players hold only about forty-six percent combined share. Key competitors include KLAFS (German, luxury and commercial focus), TylöHelo (Swedish-Finnish, broad range), SAWO and Tulikivi (Finnish niche players), and various regional manufacturers. But the fragmentation itself is a form of protection: no competitor has the scale, distribution, or brand portfolio to challenge Harvia across all product categories, price segments, and geographies simultaneously. They compete in pieces. Harvia competes as a platform.

VII. The Bear vs. Bull Case & Playbook (2:00 – 2:10)

The bear case for Harvia begins with the post-COVID demand hangover. The pandemic unleashed a wave of home improvement spending—backyard saunas, hot tubs, home wellness installations—that pulled forward years of demand into 2020 and 2021. Revenue peaked at EUR 179 million in 2021 before declining to EUR 150.5 million in 2023 as the boom normalised. The question bears ask is whether the 2021 peak represented the "true" demand level or an aberration, and whether the recovery to EUR 198.9 million in 2025 is sustainable or merely a restocking cycle.

Energy prices add a layer of concern. An electric sauna heater consumes significant electricity—a typical residential session uses six to nine kilowatt-hours. The European energy crisis that followed Russia's invasion of Ukraine made sauna operation meaningfully more expensive for consumers in Germany, Finland, and other key markets. While energy prices have normalised from their 2022 peaks, they remain elevated relative to pre-crisis levels, and any future energy shock would directly impact consumer willingness to use (and therefore buy) electric saunas. Wood-burning heaters are partially hedged against this risk, but they face their own regulatory pressures in some European markets due to particulate emissions concerns.

The correlation with the luxury housing market is the third bear pillar. Saunas are disproportionately installed in higher-end homes. When mortgage rates rise and housing construction slows—as it did across Europe in 2022-2023—new sauna installations decline. The replacement cycle provides a floor, but new construction activity drives the growth rate. A prolonged housing downturn would cap Harvia's expansion regardless of the wellness trend.

Finally, the adjusted operating margin of 19.6 percent in 2025—just below the twenty percent long-term target—suggests that the business has not yet demonstrated the margin expansion that the acquisition strategy was supposed to deliver. Elevated capex of EUR 14.8 million in 2025 (versus roughly EUR 3-6 million in prior years) raises questions about whether the company is entering a phase of higher investment that could pressure free cash flow.

The bull case rests on structural forces that are difficult to reverse.

The global wellness megatrend is not a fad. Heat therapy's health benefits are increasingly supported by peer-reviewed research, and the cultural adoption of sauna practice is expanding far beyond its Nordic and Germanic roots. The US market—where Harvia now generates its largest share of revenue—remains massively underpenetrated. Finland has 3.3 million saunas for 5.5 million people. Germany has an estimated six million. The United States, with seventy times Finland's population, has a fraction of the installed base. If even a small percentage of the twenty million US households with sufficient income adopt home saunas, the addressable market dwarfs anything Harvia serves today.

The digital services layer represents the next margin frontier. As connected products—Fenix controllers, MyHarvia app, ThermaSol smart steam—grow as a share of the product mix, average selling prices rise and the potential for recurring digital services revenue emerges. A connected sauna generates usage data, enables predictive maintenance alerts, and creates opportunities for premium subscription features. None of this is material revenue today, but the infrastructure is being built.

The replacement cycle provides downside protection that most growth stories lack. Eighteen million installed saunas worldwide, with heaters that degrade every seven to ten years, create a demand floor that is independent of new construction activity. And replacement buyers trade up—choosing smarter, higher-priced products—which lifts average selling prices through the cycle.

Harvia's balance sheet gives it optionality. At 1.2 times net debt to EBITDA, the company has meaningful capacity for further acquisitions. Management has stated it is "prepared to act swiftly on M&A" if the right opportunity emerges. The fragmented competitive landscape provides a deep pool of potential targets—regional sauna manufacturers, specialty component makers, digital wellness technology companies—that could be acquired at seven to ten times EBITDA and scaled through Harvia's global distribution, exactly as the playbook has delivered for the past seven years.

For investors tracking Harvia's performance, two KPIs matter most. Organic revenue growth at constant exchange rates strips out the effects of acquisitions and currency movements to reveal the underlying demand trend—the company reported 14.4 percent organic growth at comparable exchange rates in 2025, a strong signal. Adjusted operating profit margin measures whether the business is converting revenue growth into the profitability improvement that the long-term targets promise—the twenty percent threshold is the line to watch, and Harvia's 19.6 percent in 2025 shows the company is close but not yet there.

VIII. Epilogue (2:10 – 2:15)

Harvia is the kind of company that the Acquired podcast was made for: a business that dominates a niche so thoroughly that most investors do not even know the niche exists, generates returns on capital that would embarrass many technology companies, and was hidden in plain sight for seventy years before a private equity firm saw the potential and a public listing revealed it to the world.

The journey from Tapani Harvia's art forge to a EUR 655 million publicly listed wellness platform spans three distinct eras. The family era—1950 to 2014—built the product expertise, the Finnish heritage, and the manufacturing base. The private equity era—2014 to 2019—professionalised the operations, expanded the ambition, and prepared the company for global scale. The public era—2018 to present—has funded a disciplined acquisition programme that transformed a heater company into a vertically integrated wellness platform with brands spanning four continents, products ranging from hand-forged stones to Wi-Fi-connected touchscreen controllers, and a digital layer that is only beginning to be monetised.

The stock trades at roughly 35 euros, down more than forty percent from its pandemic-era peak and still far from the all-time high near sixty euros reached in 2021. Whether the market is right to discount the wellness boom as a one-time event, or wrong to underestimate the structural adoption of sauna culture in the world's largest consumer markets, is the central investment question. The replacement cycle keeps ticking. The rocks keep heating. And somewhere in Muurame, the factory that Tapani built seventy-six years ago keeps shipping heaters to places he never imagined.

Top References

- Harvia Oyj Annual Reports (2018–2025), available at harviagroup.com

- Harvia Q4 2025 results announcement, 12 February 2026

- CapMan press releases: Harvia acquisition (March 2014) and exit (November 2019)

- Harvia IPO prospectus, March 2018

- Acquisition announcements: Almost Heaven Saunas (December 2018), EOS Group (March 2020, July 2022), Kirami (May 2021), Sauna-Eurox (August 2021), Phoenix El-Mec (September 2023), ThermaSol (July 2024)

- Long-term incentive plan 2026-2028 announcement, 2 April 2026

- Global Sauna and Steam Room Equipment market research reports

- Harvia company history and brand information at harviagroup.com

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube