The Gym Group: The Low-Cost Disruptor of the High-Street

I. Introduction: The "Budget" Revolution (00:00 – 00:12)

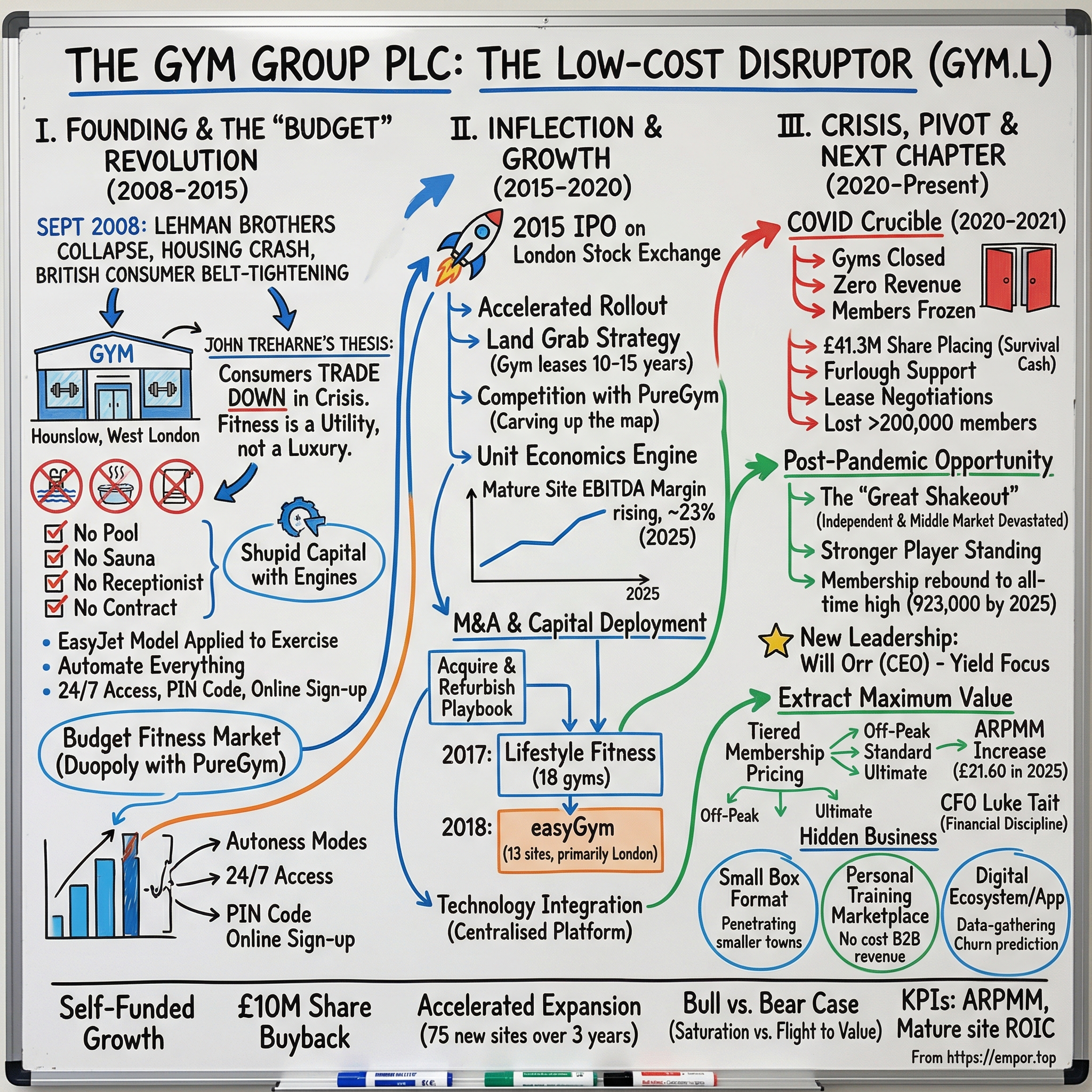

September 2008. Lehman Brothers had just collapsed. Northern Rock had already been nationalised. House prices were in freefall, credit markets were frozen, and the British consumer was about to enter the most sustained period of belt-tightening in a generation. And in Hounslow, West London, a former squash player named John Treharne was opening the doors to a new kind of gym—one with no swimming pool, no sauna, no towels, no juice bar, no receptionist, and no contract. The membership cost less than a takeaway curry. The doors were open twenty-four hours a day, seven days a week. You signed up on a website, received a PIN code, and walked in whenever you wanted.

It was, on the surface, a terrible time to start a consumer business. But Treharne had a thesis that the financial crisis would prove correct: when household budgets shrink, consumers do not stop spending. They trade down. The thirty-something professional paying £80 a month for a Virgin Active membership with a pool she never used was not going to stop exercising. She was going to find somewhere cheaper. And if that somewhere was clean, well-equipped, and available at five in the morning before the school run, she would not miss the sauna one bit.

That insight—that fitness was not a luxury but a utility, and that the traditional gym industry was wildly overcharging for it—became the founding thesis of The Gym Group. Strip away everything the customer does not value. Automate everything that can be automated. Keep the squat racks, the treadmills, the free weights, and the classes. Lose everything else. It was the EasyJet model applied to exercise: unbundle the product, lower the price, fill the capacity.

Eighteen years later, The Gym Group operates 260 locations across the United Kingdom with 923,000 members. Revenue reached £244.9 million in 2025. The adjusted EBITDA margin—the metric management watches most closely—hit twenty-three percent and is climbing. The company is listed on the London Stock Exchange, trades at around 179 pence per share with a market capitalisation of roughly £315 million, and has just announced an accelerated expansion plan to open seventy-five new sites over the next three years. It sits alongside PureGym as one of the two dominant players in the UK's budget fitness market—a duopoly that emerged from the wreckage of the pandemic, which destroyed much of the competition they once had.

This is the story of how a crisis-era startup became a toll bridge on the British high street, why the most important thing about a gym is not the equipment but the software, and what happens when a "land grab" business finally matures into a cash-generating machine.

II. Founding Context: The End of the "Middle Ground" (00:12 – 00:30)

To understand why The Gym Group worked, you have to understand what the British fitness market looked like before it arrived. In the early 2000s, the gym industry in the UK was stuck in an uncomfortable middle ground. At the top end, operators like David Lloyd and Virgin Active offered a full-service experience: swimming pools, tennis courts, spas, restaurants, crèches, and personal trainers in matching polo shirts. Membership ran to £80 or £100 per month, typically locked in with twelve-month contracts and hefty cancellation fees. These were lifestyle clubs for affluent families—think suburban country club with better parking.

At the bottom end, local council leisure centres offered basic facilities at subsidised rates, but the experience was often dispiriting: ageing equipment, limited opening hours, changing rooms that had not been refurbished since the 1980s, and queues for the one working treadmill during peak hours. There was no middle option—no clean, modern, well-equipped gym that a normal person could afford without a significant monthly commitment.

John Treharne had seen this gap before. Born in 1954, educated in economics at University College London, and a former England squash international, he had opened his first gym chain—Dragon's Health Clubs—in 1991, growing it to twenty-two clubs before floating the company in 1997 and selling it in 2000. He understood the physical fitness business intimately: the unit economics of a square metre of gym floor, the seasonal membership curves, the relationship between equipment investment and retention. What he did not yet have was the technology to strip out the cost structure that made gyms expensive.

By 2007, that technology existed. Online payment processing was reliable. Building access control systems—swipe cards, PIN pads—were cheap and proven. Broadband internet was ubiquitous enough to support a fully digital sign-up process. Treharne recognised that these tools, combined in the right way, could eliminate the two biggest cost centres in a traditional gym: the front desk staff and the sales team. If every member signed up online and entered via an automated access system, you did not need receptionists. If there were no contracts to negotiate and no cancellation fees to dispute, you did not need a sales force. If you did not serve food or drinks, you did not need catering staff. A traditional gym might employ thirty to forty people per location. Treharne's model needed six or seven.

The first Gym Group site opened in Hounslow in 2008, followed quickly by Guildford and Vauxhall. Membership was priced at £15 to £20 per month—roughly a quarter of a mid-range gym and less than a fifth of the premium operators. There were no contracts: sign up today, cancel tomorrow. The gyms were open around the clock. And from the very first day, one hundred percent of memberships were sold online. There was no paper. There was no till. There was, by design, almost no human interaction unless a member wanted it. Treharne was not building a gym chain. He was building, as one early investor described it, "a software company with squat racks."

Bridges Ventures, a social impact-focused fund, backed the company from inception. The timing of the launch—into the teeth of the worst financial crisis in eighty years—proved paradoxical. The recession drove consumers to trade down from expensive gyms, accelerating the adoption of the budget model. And the crash in commercial property values meant that Treharne could negotiate extraordinarily favourable lease terms on the high-street and retail park units that traditional retailers were desperate to vacate. The very conditions that made 2008 terrifying for most businesses made it the perfect moment to launch a low-cost gym chain.

III. Inflection Point 1: The 2015 IPO and the "Land Grab" (00:30 – 00:55)

By 2013, The Gym Group had grown to forty sites. Bridges Ventures sold its majority position to Phoenix Equity Partners for approximately £50 million, valuing the company at £90-100 million. Phoenix brought fresh capital and a clear mandate: accelerate the rollout. The budget gym market was still in its early stages, and the competitive dynamics were classic land-grab territory—whoever secured the best locations first would hold them for decades, because gym leases typically run ten to fifteen years with options to extend.

The primary rival was PureGym, founded in 2009 by Peter Roberts with a virtually identical model: low cost, no contract, twenty-four-hour access, technology-enabled operations. By 2015, PureGym had grown slightly faster and was already the larger of the two chains by site count. But the market was big enough for both. The UK had roughly six thousand gyms serving about nine million members at the time, with private sector penetration well below comparable European markets. The opportunity was not to steal share from each other but to convert the vast population of non-gym-goers into members by making fitness affordable for the first time.

On 12 November 2015, The Gym Group debuted on the London Stock Exchange at 195 pence per share, giving the company a market capitalisation of approximately £250 million. At the time, it operated sixty-six sites with roughly 363,000 members. The IPO raised £125 million, primarily through the sale of existing shares by Phoenix Equity Partners and Bridges Ventures. The pitch to institutional investors was straightforward: the UK could support hundreds more budget gyms, each site followed a predictable economic ramp from cash-draining opening year to cash-generating maturity by year three, and the company had the operational playbook to replicate this unit economic model at scale.

The unit economics are worth understanding in detail, because they are the engine of the entire business. A new Gym Group site typically costs between £1.5 million and £2.5 million to build out, depending on location and size—covering equipment, fit-out, technology installation, and initial working capital. In its first year, a new gym is almost always loss-making. Membership builds gradually as local awareness grows. By year two, most sites reach breakeven. By year three, a well-performing site generates site-level EBITDA margins that make it a "cash cow"—generating cash flow that funds the next wave of openings. The company reported mature site return on invested capital of twenty-seven percent in 2025, and thirty percent excluding thirteen sites operated in partnership with local authorities. These are exceptional returns for a business that requires real physical assets and significant upfront capital.

The competitive dynamics with PureGym in those early years were surprisingly cooperative. Rather than competing for the same street corner, the two chains tended to carve up the map—PureGym taking one side of a city, The Gym Group taking the other. This was not a formal agreement but a practical recognition that cannibalising each other's locations would be value-destructive for both operators. The real competition was not between budget gyms but against the traditional operators whose members were quietly trading down, and against the vast pool of non-gym-goers who had never considered membership because the price had always been too high.

In the years following the IPO, The Gym Group expanded aggressively. From sixty-six sites at listing, the network grew to 128 by the end of 2017 and 175 by the end of 2019. But the truly interesting strategic question was not how many gyms they opened—it was how they chose to supplement organic growth with acquisitions.

IV. M&A & Capital Deployment: The easyGym Benchmark (00:55 – 01:25)

In June 2017, The Gym Group completed its first significant acquisition: eighteen gyms from Lifestyle Fitness, primarily in the Midlands and North of England, for £20.5 million in cash. The sites generated revenues of £11.1 million and site EBITDA of £3.45 million—implying a purchase multiple of roughly six times site EBITDA. The deal was notable for its geography: it filled gaps in the map where organic expansion would have taken years. It was also notable for its playbook: acquire sites operated by a weaker competitor, strip out the old branding, refurbish the equipment, plug the location into The Gym Group's proprietary technology stack—online membership, automated access control, app integration—and watch the margins improve as the more efficient operating model takes hold.

The second and more scrutinised deal came in July 2018, when The Gym Group acquired thirteen easyGym sites for a base consideration of £20.6 million, plus up to £4.1 million contingent on lease extensions for two locations. EasyGym was a budget operator that had launched under the "easy" brand (the same licensing umbrella as EasyJet and EasyHotel) but had struggled to achieve the scale needed to compete. The sites generated revenues of £12.9 million and site EBITDA of £4.3 million in the twelve months prior to completion, putting the base purchase multiple at roughly 4.8 times site EBITDA. Eight of the thirteen sites were in London, making this effectively a land grab for premium urban locations that would have been extremely difficult and expensive to build organically.

Was £20.6 million the right price for thirteen gyms? The answer depends on the comparison. A brand-new Gym Group site cost £1.5 to £2.5 million to build—so thirteen organic sites would have cost roughly £20 to £32 million in capex alone, plus two to three years of ramp-up losses before each reached maturity. The easyGym sites came with existing members, existing cash flow, and immediate revenue contribution once converted to The Gym Group's operating model. At £1.6 million per site on the base price, the acquisition was cheaper than building from scratch—and faster, which matters in a land-grab market where the best locations are finite.

The "acquire-and-refurbish" playbook that emerged from these deals became a template. The Gym Group takes a site operated by a weaker competitor, replaces the signage, upgrades the equipment where needed, integrates the membership base into its app and billing system, and applies its labour-light operating model to immediately reduce costs. The technology integration is the critical step: once a site runs on The Gym Group's centralised platform, it benefits from the same automated access control, digital marketing, churn prediction algorithms, and centralised procurement as every other site in the network. The margin improvement from this conversion is typically rapid and significant.

A broader look at capital allocation reveals a company that learned discipline the hard way. In the years immediately following the IPO, the emphasis was on growth at virtually any cost—open sites, fill the map, establish the brand. Return on capital employed was a secondary consideration. The acquisition multiples on Lifestyle Fitness (six times EBITDA) and easyGym (4.8 times) were reasonable, but the pace of organic expansion meant that aggregate capital returns were diluted by the drag of immature sites ramping up. It was not until the post-COVID era—when the management team changed and the strategic emphasis shifted—that capital allocation became genuinely disciplined, prioritising returns over raw site count. The current management targets thirty percent mature site ROIC and insists that every new opening clears a minimum return hurdle before capital is committed.

The combination of organic builds and bolt-on acquisitions grew the portfolio from 66 sites at IPO to 175 by the end of 2019. But what happened next would test the business model in ways that no amount of strategic planning could have anticipated.

V. Inflection Point 2: The COVID Crucible (01:25 – 01:45)

On 20 March 2020, the British government ordered every gym in the country to close its doors. For a business with 175 sites, 794,000 members, and a cost structure built on high fixed costs—leases, equipment financing, maintenance contracts—the order was an existential threat. Revenue went to zero. Not reduced. Not impaired. Zero. Members could not enter the buildings. Memberships were frozen. The tills stopped.

What followed was thirteen months of intermittent closure spread across three national lockdowns. Gyms in England reopened briefly on 25 July 2020, closed again on 5 November for a second lockdown, and shut once more in January 2021 for a third. The final reopening came on 12 April 2021. During this period, The Gym Group lost over 200,000 members—membership fell from 794,000 to 578,000—and posted a net loss of £36.4 million in 2020, followed by a further £35.4 million loss in 2021.

The survival mechanics were brutal but effective. In April 2020, management raised £41.3 million through a share placing at 150 pence—a significant discount to the pre-COVID price—diluting existing shareholders but providing the cash needed to survive extended closure. The company's revolving credit facility was extended from £70 million to £100 million. Furlough support from the government covered a portion of employee costs. Lease negotiations with landlords reduced or deferred rent obligations. Every discretionary expense was eliminated. In July 2021, as gyms reopened and membership recovery accelerated, a further £30.3 million was raised to fund an ambitious plan to open forty new sites over the following eighteen months—a bet that the pandemic would prove to be not just a crisis but an opportunity.

That bet proved prescient, because the pandemic's most lasting impact was not on The Gym Group itself but on its competitors. The "middle market"—independent gyms charging £30 to £50 per month, lacking the scale to negotiate lease deferrals or the brand recognition to rapidly rebuild membership—was devastated. Hundreds of independent operators closed permanently. Council leisure centres, already underfunded before the pandemic, emerged in even worse condition. The competitive landscape that existed in February 2020 was fundamentally altered by April 2021.

The Gym Group and PureGym—the two operators with the strongest balance sheets, the deepest operational capabilities, and the lowest cost structures—emerged from the pandemic as the last major players standing in the budget segment. The "Great Shakeout" handed them a structural gift: a market with fewer competitors, more available locations (vacated by failed operators), and a consumer base that was more price-conscious than ever. By the end of 2022, membership had surpassed pre-COVID levels at 821,000. By 2025, it reached 923,000—an all-time high.

The pandemic also provided an unexpected validation of the operating model. A business with a thirty-person staff per location would have faced an enormous wage bill during closure, even with furlough support. The Gym Group's labour-light model—six or seven employees per site—meant that the fixed-cost base was dominated by rent and equipment, both of which could be negotiated or deferred. The same automation that made the business efficient in normal times made it resilient in crisis. The software company with squat racks survived a zero-revenue environment that would have killed a traditional gym operator within months.

VI. Current Management: The "Next Chapter" Strategy (01:45 – 02:10)

In January 2023, Richard Darwin—who had served as CEO since 2018, leading the company through COVID and the subsequent recovery—stepped down. Founder John Treharne returned as Executive Chairman on an interim basis, running the business while the board searched for Darwin's successor. The choice they made signalled a fundamental shift in what The Gym Group wanted to be.

Will Orr joined as CEO in September 2023. His background was not in fitness, nor in property, nor in operations. Orr had spent his career in brand-building and consumer data. He served as Managing Director of Times Media Limited, the publisher of The Times and Sunday Times, where he oversaw digital transformation and subscription growth. Before that, he held senior roles at the RAC and British Gas, part of Centrica—large consumer-facing businesses where the strategic challenge was not acquiring customers but maximising the lifetime value of the ones you already had. He brought an MBA from London University, thirty years of marketing and data experience, and a worldview shaped by subscription economics rather than real estate development.

The appointment sent a clear message: The Gym Group's era of "build as many gyms as possible" was giving way to an era of "extract maximum value from the gyms you have." This was not a subtle shift. Under Darwin, the company had prioritised site count—growing from 63 to 229 gyms. Under Orr, the emphasis moved to yield: revenue per member, retention rates, tiered pricing, and margin optimisation. The language of the company changed. Annual reports began talking about "member experience," "data-driven engagement," and "brand equity" rather than "pipeline" and "openings."

The most visible manifestation of this shift was the introduction of tiered membership pricing. Where The Gym Group had historically offered a single price point per location, it now operates three tiers: Off-Peak (from £15.99 per month with restricted hours), Standard (from £19.99 for single-gym 24/7 access), and Ultimate (from £24.99 for multi-gym access and additional perks). Prices vary by location—central London gyms charge meaningfully more than regional ones. This tiering is a classic yield management technique borrowed from airlines and hotels: segment the customer base by willingness to pay, and capture more revenue from those who value flexibility without alienating the price-sensitive majority.

Average revenue per member per month—ARPMM—climbed to £21.60 in 2025, up four percent year over year. That may sound modest, but in a business with 923,000 members, every penny of ARPMM improvement drops almost directly to the bottom line. The operating leverage in this model is extraordinary: once a gym is built and staffed, the marginal cost of serving an additional member is close to zero. Higher yield per member flows through at near-100 percent incremental margin.

Alongside Orr, CFO Luke Tait—who joined in October 2022 from Nando's, where he had served as Group CFO—brought financial discipline sharpened at SSP Group (the Upper Crust and airport food operator) and Compass Group. Tait's focus has been on "self-funded growth": ensuring that expansion capex, technology investment, and shareholder returns are all funded from operating cash flow without further equity dilution. The company generated £38.3 million in free cash flow in 2025 and announced a £10 million share buyback programme in January 2026—the first meaningful return of capital to shareholders since the IPO.

The management incentive structure reflects the strategic shift. The company's key performance metric is "Group Adjusted EBITDA Less Normalised Rent"—essentially, the cash profit after accounting for the true economic cost of occupying the property. This metric reached £56.7 million in 2025, up nineteen percent year over year. By tying incentives to this measure rather than raw site count or revenue, the board has aligned management with the kind of profitable, capital-efficient growth that compounds shareholder value. Mature site ROIC of twenty-seven percent—thirty percent excluding workforce-partnership sites—demonstrates that when executed well, each new gym creates significant value.

Institutional shareholders dominate the register—about seventy-four percent of shares are held by institutions, led by Liontrust Asset Management at roughly nine percent. Founder Treharne remains Chairman but holds a relatively modest economic stake. The free float is eighty-five percent. In March 2026, the company announced an acceleration of its expansion plan: seventy-five new sites over three years, up from a previous target of fifty, with at least twenty planned for 2026. At an expected thirty percent ROIC per new site, the maths on self-funded growth are compelling—provided the company can maintain the operational discipline that makes the unit economics work.

VII. The "Hidden" Business: Segments & Initiatives (02:10 – 02:30)

The Gym Group appears from the outside to be a simple business: build gyms, sell memberships, collect monthly fees. But beneath the surface, there are several revenue streams and operational innovations that rarely feature in analyst conversations yet contribute meaningfully to the economic moat.

The "Small Box" format, launched in November 2019 with the first site in Newark, Nottinghamshire, is perhaps the most strategically significant. A standard Gym Group site occupies a large commercial unit—typically a former retail store or warehouse—in a town or city with sufficient population density to support thousands of members. But the UK has hundreds of smaller towns, with populations of ten to seventy-five thousand, where a full-size gym is not economically viable. The Small Box format scales down the concept: a smaller footprint, lower rent, reduced equipment investment, but the same technology stack, the same brand, and the same operating model. The result is a gym that can be profitable in markets that PureGym and other full-size competitors cannot economically serve.

This matters because the budget gym segment has already saturated many of the UK's major cities. London, Manchester, Birmingham, Leeds—the obvious locations have been taken. Future growth depends on penetrating secondary and tertiary markets where the population density is lower but the competitive environment is also far more favourable. Industry data shows that budget gym presence in towns of ten to seventy-five thousand population more than doubled between 2019 and 2024. The Small Box format positions The Gym Group to lead this expansion wave.

The Personal Training marketplace is another hidden business that inverts the traditional cost structure. In a conventional gym, personal trainers are employees. The gym pays their salaries, manages their schedules, handles their payroll taxes, and absorbs the risk if they underperform or leave. The Gym Group does none of this. Instead, personal trainers operate as independent contractors who pay The Gym Group a rental fee for access to the gym floor and its members. The PT sets their own prices, manages their own client relationships, and runs their own business. The Gym Group collects a predictable stream of rental income with zero employment cost, zero scheduling complexity, and zero liability. Think of it as a "marketplace" model embedded within a physical space—the gym provides the platform (foot traffic, equipment, brand credibility) and the PTs provide the service, paying for the privilege. It is, in effect, a recurring B2B revenue stream hidden within what looks like a consumer business.

The digital ecosystem ties everything together. The Gym Group's app is not just a tool for opening doors—though that is its most visible function. It is a data-gathering engine that tracks member behaviour: visit frequency, time of day, duration, class attendance, and engagement with in-app content. This data feeds machine learning models that predict churn risk—identifying members who are visiting less frequently or whose engagement patterns match historical defection profiles. The operations team can then intervene with targeted communications, promotional offers, or personalised content designed to re-engage at-risk members before they cancel. Average member tenure now stands at approximately eighteen months, which in a no-contract, cancel-anytime business represents a meaningful achievement. The app also enables targeted upsells—promoting the Ultimate tier to Standard members who visit multiple locations, or surfacing personal training offers to members who consistently train at peak hours.

The technology investment extends to the infrastructure layer. The Gym Group partnered with Ensono to build an Azure-based e-commerce platform that achieved 99.99 percent availability during the critical January-February 2023 peak period—when gym sign-ups surge as part of the annual New Year resolution cycle. In an industry where the front door is a PIN pad and the sales counter is a website, technology reliability is not a nice-to-have. It is the entire customer acquisition funnel. A five-minute outage during peak sign-up hours means lost members who may never return.

VIII. Strategic Analysis: 7 Powers & 5 Forces (02:30 – 02:50)

The question any long-term investor must answer about The Gym Group is whether its competitive position is genuinely durable or merely a function of being early to a trend. Hamilton Helmer's Seven Powers framework helps distinguish between temporary advantage and structural moat.

The primary power is Scale Economies, and they operate at multiple levels. With 260 sites, The Gym Group amortises its central technology stack—the app, the billing system, the access control platform, the data analytics—across a base that no new entrant can match without equivalent scale. National marketing campaigns, which drive brand awareness during the critical January sign-up season, cost roughly the same whether you have fifty gyms or three hundred, but the revenue they generate scales with footprint. Equipment procurement at volume secures better pricing from manufacturers. And the operational know-how—how to fit out a site efficiently, how to negotiate leases, how to optimise staffing levels—compounds with every gym opened. A new entrant building their first ten sites faces per-unit costs that The Gym Group long ago optimised away.

The second power is a Cornered Resource, though it requires some unpacking. The resource is not equipment or technology—both are commodity inputs. The resource is real estate. Prime high-street and retail park locations with the right combination of size, accessibility, footfall, and planning permission are finite. The UK's planning system underwent a significant change in September 2020, when Use Class D2 (Assembly and Leisure) was merged into the new Class E (Commercial, Business and Service). This means that conversion from retail to gym—or vice versa—can now occur without planning permission, significantly expanding the addressable property pipeline. But the best locations are still scarce, and The Gym Group's existing portfolio of 260 long-term leases represents a real estate footprint that a competitor cannot replicate without years of site-by-site negotiation. Each lease signed is a location locked away from the competition for a decade or more.

Process Power is the third relevant Helmer power. The labour-light operating model—roughly six to seven employees per gym, with no front desk staff and no in-house sales force—produces a cost structure that traditional operators cannot match without fundamentally redesigning their businesses. Full-year like-for-like site cost increases were limited to just one percent in 2025, despite broader inflationary pressures on wages and energy. This operational efficiency is not the result of a single innovation but of thousands of small process optimisations accumulated over eighteen years of running automated gyms. A traditional operator trying to replicate this model would need to retrain staff, redesign workflows, rebuild technology systems, and overcome institutional resistance to automation—a multi-year transformation that most incumbent management teams are unwilling or unable to execute.

Porter's Five Forces paint a complementary picture. Threat of Substitutes is genuinely high—people can run outdoors for free, buy a Peloton bike, follow YouTube workouts, or simply stop exercising. The pandemic proved that many gym members could survive without a gym, and the home fitness trend surged during lockdowns. But TGG combats substitutes through "social friction" (working out among others is motivating in a way that a spare bedroom is not), equipment variety (no home setup replicates a full commercial gym floor), and sheer affordability—at £16 to £20 per month, the price barrier to maintaining membership is lower than the cost of most home fitness subscriptions.

Barriers to Entry are rising, not falling. The capital cost of building a gym has increased with construction inflation. The best locations are increasingly occupied. The two dominant operators—TGG and PureGym—have built brand recognition, technology platforms, and supplier relationships that a new entrant would need years and hundreds of millions of pounds to replicate. PureGym, backed by KKR and Leonard Green, operates 420-plus UK sites and plans to nearly double again by 2030. The scale gap between the duopoly and any potential new entrant is widening every year.

Bargaining Power of Buyers is limited by the consumer nature of the business. Individual members have no negotiating leverage. Churn is a risk, but it is managed through low pricing, convenience, and the behavioural nudges enabled by the app. Bargaining Power of Suppliers is similarly modest—equipment manufacturers and landlords face a competitive market, and TGG's scale gives it procurement leverage. Competitive Rivalry between TGG and PureGym is real but disciplined. Both operators understand that irrational price competition would destroy value for both. The market is large enough—UK fitness penetration is still only about seventeen percent including the public sector—that both can grow without needing to take share from each other.

IX. Playbook: The Business Lessons (02:50 – 03:10)

The first lesson from The Gym Group's story is the discipline of subtraction. In most consumer businesses, the instinct is to add features: a new product line, a premium tier, an adjacent service. The Gym Group's founding insight was that the most valuable thing you can do is remove things that the customer does not value and that the operator pays for. A sauna costs tens of thousands of pounds to install, requires constant maintenance, increases energy bills, takes up floor space that could hold squat racks, and is used by a small minority of members. Removing it does not reduce the value proposition for ninety percent of the customer base—it reduces the price, which is what that ninety percent actually cares about. Every time a suggestion is made to add a new amenity—a cafe, a shop, a spa treatment room—the correct response is: "Does this reduce our cost per member or increase our revenue per member? If neither, we do not do it." That discipline is harder to maintain than it sounds, particularly as a company scales and new managers arrive with ideas about "enhancing the experience."

The second lesson is that in budget fitness, the competitive advantage is not price—it is efficiency. Any operator can lower prices. The question is whether you can operate profitably at that price point. The Gym Group's technology stack, its labour-light model, its centralised procurement, and its data-driven churn management collectively produce a cost structure that allows healthy margins at price points that would bankrupt a traditional gym. The winner in budget fitness is not the operator that charges the least. It is the operator that spends the least per member served while maintaining acceptable quality. This is why adding a sauna would hurt the business: it would increase the cost per member without a proportionate increase in the price the budget-conscious customer is willing to pay.

The third lesson is the power of technology as a deflationary force. Automation replaces labour. Data replaces intuition. Centralised systems replace local improvisation. The Gym Group's technology investment—the app, the access control, the billing platform, the analytics engine—has allowed it to scale from one site to 260 without proportionally scaling its headcount. The company employs roughly 1,837 people, including headquarters staff. That is approximately seven per gym on a blended basis, and fewer per site once you exclude the 200-odd central employees. In a traditional gym operation, labour costs can consume twenty percent or more of revenue. At The Gym Group, the number is substantially lower, and the gap widens with each site added because the technology platform's cost does not scale linearly with the portfolio.

The final lesson concerns pricing power in a business perceived as "low cost." The conventional wisdom is that budget operators have no pricing power—that they compete solely on being cheap and any price increase will drive members to an even cheaper alternative. The data suggests otherwise. Average revenue per member per month increased four percent in 2025, with no material impact on churn. The introduction of tiered pricing—Off-Peak, Standard, Ultimate—created an upward migration path that did not exist when every member paid the same flat fee. Members who value multi-gym access or peak-hour flexibility self-select into higher tiers, increasing yield without requiring the company to raise base prices aggressively. At £20 per month, The Gym Group is still so far below the traditional gym industry's pricing that it has significant room to optimise yield before it bumps against the ceiling of customer price sensitivity.

X. The Bull vs. Bear Case (03:10 – 03:25)

The bear case begins with saturation. The UK budget gym market has grown enormously over the past fifteen years, with PureGym now operating 420-plus sites and The Gym Group at 260. How many more locations can the UK realistically absorb before cannibalisation becomes a real problem? PureGym plans to nearly double its footprint by 2030. The Gym Group has announced seventy-five new sites over three years. At some point, opening a new gym in the next town over starts pulling members from your existing location rather than adding new ones. The Small Box format addresses smaller towns, but these markets are inherently limited in scale.

Energy costs remain a structural concern. A gym requires significant electricity for lighting, HVAC, and equipment—twenty-four hours a day, seven days a week. The energy price shocks of 2022-2023 demonstrated the vulnerability: operating costs excluding depreciation jumped twenty-five percent in the first half of 2023. Management has since implemented optimisation programmes that limited like-for-like cost increases to just one percent in 2025, but energy price volatility remains a risk that cannot be fully hedged.

The "Planet Fitness threat"—the US budget gym giant with over 2,500 locations—is often cited in bear analyses, though there is no current evidence of UK market entry plans. More relevant is the competitive threat from PureGym itself, which has deeper pockets (backed by KKR and Leonard Green) and a significantly larger UK footprint. In any head-to-head market, PureGym's scale advantages in procurement, marketing, and brand recognition are difficult to overcome.

The balance sheet carries more leverage than the headline numbers suggest. Total debt including IFRS 16 lease obligations stood at £409.7 million at the end of 2025, against equity of £141.7 million. Stripping out the lease liabilities—which is the more economically meaningful way to assess a property-leasing business—non-property net debt was £59.3 million at a leverage ratio of just 1.0 times. But the lease obligations are real commitments, and in a scenario where membership drops significantly (as it did during COVID), those fixed lease payments do not disappear. The company's ability to survive future shocks depends on maintaining the membership volumes and yields that service these obligations.

The bull case is anchored in two structural tailwinds.

First, the "flight to value." The UK cost-of-living crisis has accelerated the structural shift from mid-priced gyms to budget operators. Consumers who previously paid £40 to £60 per month for a gym with a pool and sauna are trading down to £20-per-month operators that provide ninety percent of the workout experience at a third of the price. This is not a temporary phenomenon driven by a single economic shock—it is a permanent behavioural shift, similar to what happened in air travel when EasyJet and Ryanair proved that budget did not mean inferior. UK private sector gym penetration reached 11.4 percent in 2024, with the total market (including public sector) at 16.6 percent as of 2026. Both figures are still below mature European markets, suggesting meaningful headroom for continued growth.

Second, the "moat of the last man standing." The pandemic permanently removed a layer of competition from the market. Independent gyms that closed in 2020-2021 are not coming back. Their locations are available for acquisition or new builds. Their former members need somewhere to go. The Gym Group and PureGym have inherited a market structure that is more favourable than the one they built—a duopoly with high barriers to entry, disciplined pricing, and a growing addressable market.

The valuation provides context. At 179 pence, The Gym Group trades at roughly 7.2 times enterprise value to EBITDA—a reasonable multiple for a growing, cash-generative consumer business with improving margins. The company has turned profitable on a statutory basis (net income of £7.4 million in 2025), initiated a share buyback, and is guiding to results at the upper end of analyst expectations for 2026. Year-to-date revenue growth is running at nine percent.

For investors tracking the business, two KPIs matter most. ARPMM (Average Revenue Per Member Per Month) captures the yield story—the company's ability to extract more revenue from its existing base through tiered pricing, retention improvements, and ancillary revenue streams. At £21.60 and growing, this is the metric that determines whether The Gym Group is a value compounder or a volume-dependent commodity. Mature site ROIC measures the quality of capital deployment—whether each pound invested in a new or existing gym generates attractive returns. At twenty-seven percent (thirty percent excluding partnership sites), this metric validates the unit economics that underpin the entire growth story. If ARPMM stalls or ROIC declines, the investment thesis weakens regardless of how many new sites are opened.

XI. Epilogue & Closing (03:25 – 03:30)

In a business textbook, The Gym Group would sit comfortably in the chapter on disruptive innovation. It entered at the bottom of the market with a product that incumbents dismissed as "too basic." It used technology to deliver that product at a cost structure the incumbents could not match. And it gradually moved upmarket—through tiered pricing, brand investment, and operational excellence—while the incumbents struggled to respond. The premium operators could not match the price. The independents could not match the technology. The council leisure centres could not match the experience. And so the market shifted, permanently, toward a model that John Treharne sketched out in an office in Hounslow in 2007.

Where the company goes from here depends on execution. The accelerated plan to open seventy-five new sites over three years—at least twenty in 2026—will test whether the self-funded growth model can scale without compromising returns. The yield optimisation strategy will test whether a budget brand can sustainably raise prices in a market where consumer affordability is the core value proposition. And the leadership transition—from a founder-chairman to a brand-specialist CEO—will test whether the culture of operational discipline that built the company can survive the institutional evolution that scale demands.

The Gym Group started with a simple question: what would happen if you made going to the gym as easy and cheap as buying a coffee? Nearly two decades later, 923,000 members—more people than live in the city of Liverpool—answer that question every month. The squat racks and the software keep working.

Top References

- The Gym Group Annual Reports (2015–2025), available at tggplc.com

- The Gym Group FY2025 Preliminary Results, March 2026

- UK Active / Leisure DB State of the Fitness Industry reports

- Health Club Management coverage of UK budget gym expansion

- Bridges Fund Management case study: The Gym Group IPO (2015)

- Phoenix Equity Partners investment profile

- Use Class E planning changes (September 2020): implications for gym property pipeline

- PureGym expansion strategy updates (2025-2026)

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube