GSK plc: The Pure-Play Biopharma Transformation

I. The Hook & The Miels Mandate

On the morning of January 1, 2026, Luke Miels walked into the chief executive's office at GSK's headquarters on the South Bank of the Thames, and for the first time in nearly a decade, there was almost nothing left to break apart. The consumer business was gone. The joint ventures were being untangled. The litigation that had once threatened to swallow tens of billions of pounds of shareholder value had been settled. After the long, grinding, high-drama tenure of Dame Emma Walmsley, the decks were finally clear. What Miels inherited was not a turnaround project but something rarer in large-cap pharmaceuticals: a company that had finished reinventing itself and now simply had to prove the reinvention was worth it.12

The numbers he took charge of were substantial. GSK closed 2025 with £32.7 billion in turnover, up 7% at constant exchange rates, led by a Specialty Medicines division that grew 17% to £13.5 billion.1 Core earnings per share rose 12% to 172 pence, the company threw off £4.0 billion of free cash flow, and the board reaffirmed a target that has become the single most-quoted sentence in every GSK investor deck: total sales of more than £40 billion by 2031.1 That is the mandate. Cross £40 billion in six years, from a base that took a Victorian laxative maker, a New Zealand milk-powder importer, and a Philadelphia apothecary the better part of two centuries to build.

Miels is an unusual person to hand that mandate to, and the choice tells you something about how GSK's board now thinks. He is not a scientist and not a lifer. An Australian by background, he spent years at AstraZeneca — the very peer GSK's compensation committee benchmarks against — before joining GSK in 2017 as president of global pharmaceuticals, and he built his reputation as a commercial operator who could take a promising molecule and turn it into a franchise.3 By the time he was named CEO designate in 2025, he had run the commercial engine behind GSK's oncology and specialty push and carried responsibility for both medicines and vaccines. The board did not pick a discovery visionary. It picked a closer.

That choice frames the central conflict of the whole GSK story, and it is a brutally specific one. GSK's most reliable cash machine is its HIV business, and the crown jewel of that business is dolutegravir — the integrase inhibitor at the heart of blockbusters like Tivicay and Dovato. Dolutegravir's core composition-of-matter patent expires in the United States in April 2028 and in Europe in July 2029.4 When a small-molecule drug loses patent protection, generic competition does not nibble at it; it detonates it. Prices can fall 80% or more within a year or two as generic manufacturers flood in. A division that generated £7.7 billion in 2025 — nearly a quarter of the entire company — is staring at a cliff that arrives roughly two years into Miels' tenure.1 The £40 billion target and the 2028 patent cliff are on a collision course, and everything GSK does between now and then is, in one way or another, about surviving that collision.

So the thesis of this story is not "GSK is a great company" or "GSK is doomed." It is that GSK is the purest large-cap case study we have in the perils and the payoffs of strategic refocusing. Over roughly fifteen years it deliberately dismantled a sprawling, low-margin, diversified conglomerate — consumer brands, generics, a globe-spanning footprint — to become a hyper-focused, high-margin, R&D-driven specialist in vaccines and long-acting therapeutics. The question this article tests, section by section, is whether the scientific moats GSK built along the way — its adjuvant chemistry, its long-acting injectable HIV franchise, its rebuilt oncology pipeline — are deep enough and durable enough to outrun the patent cliffs its own past keeps generating. To understand whether the machine works, you have to understand how strange and how old its component parts really are.

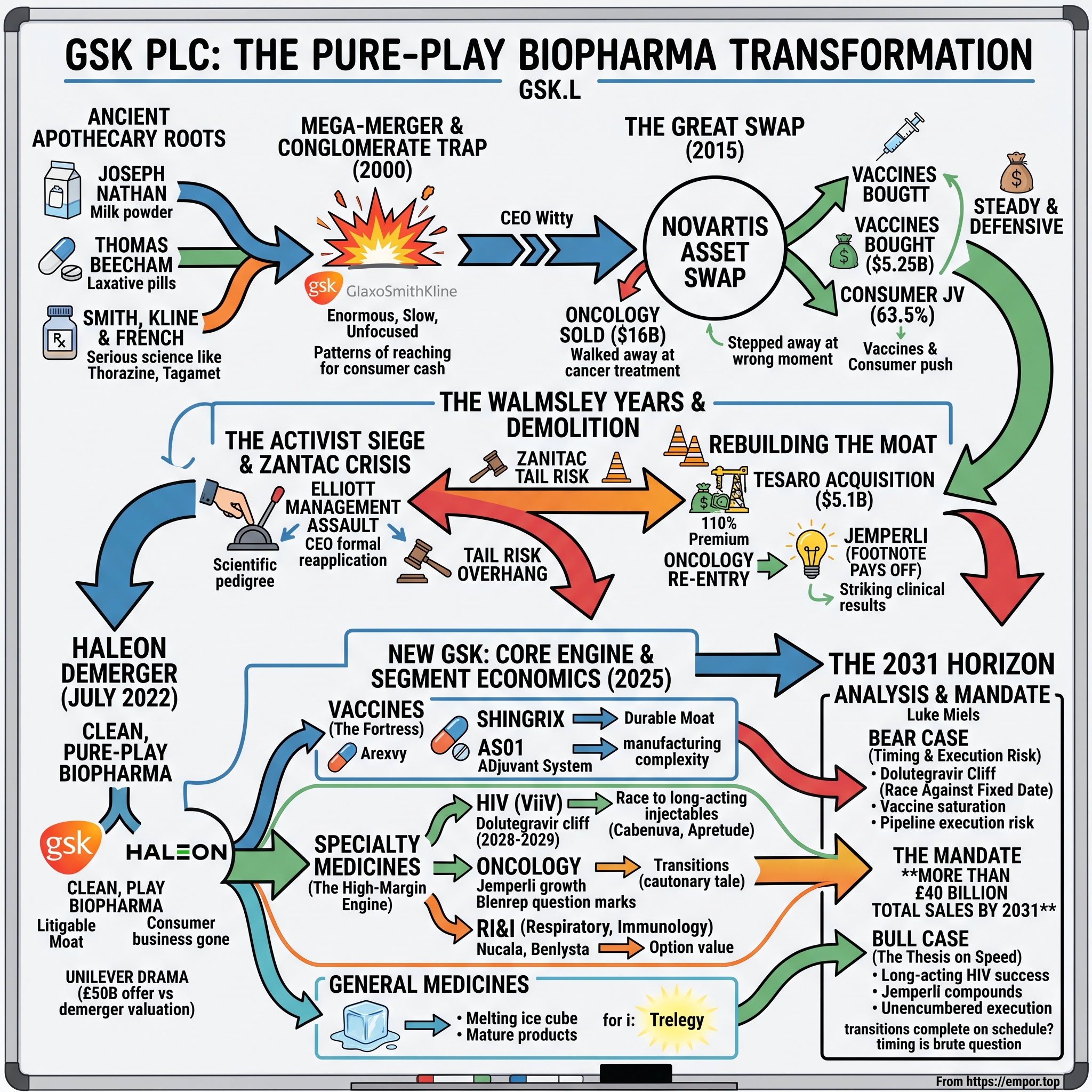

II. The Ancient Apothecary Roots

Every origin myth in pharmaceuticals eventually arrives at a chemist's bench, but GSK's arrives at three of them, on three continents, separated by decades — and, improbably, at a dairy in New Zealand. The modern company is the product of a family tree so tangled that GSK itself has periodically struggled to narrate it cleanly. The two great trunks are Glaxo Wellcome and SmithKline Beecham, and each of those is itself a merger of mergers. It is worth pulling the branches apart, not for antiquarian pleasure, but because the DNA of each explains a recurring habit of the company: an instinct, whenever the science got hard, to retreat toward the comfortable cash flows of consumer products.

Start with the milk. In 1873, Joseph Nathan, a London-born trader, set up a general merchant business in Palmerston North on New Zealand's North Island. The firm's breakthrough came not from medicine but from dried milk: Joseph Nathan & Co. began importing and processing skimmed milk powder, and in 1906 it registered a brand name derived from the Greek word for milk, gala. The original coinage was "Galactos"; trademark constraints forced a truncation, and the name that emerged was Glaxo. The product was infant formula, and the marketing was pure Edwardian genius: "Glaxo builds bonny babies" became one of the most recognizable slogans in the British Empire. From dried milk the firm moved into vitamin D — a natural adjacency, since rickets was the childhood scourge that fortified milk could prevent — and from vitamins into pharmaceuticals proper. During the Second World War, Glaxo built a penicillin manufacturing plant in Britain, and a milk company became, almost by accident, a drug company. The lineage matters because it planted the first seed of an idea that would haunt GSK a century later: that nutrition and consumer health and medicine all belonged under one roof.

Now the laxative. In 1848, a farm laborer turned entrepreneur named Thomas Beecham opened a shop in Wigan, Lancashire, selling a compound of aloes, ginger, and soap pressed into a pill and sold as a remedy for digestive complaints. Beecham's Pills were, in clinical terms, a laxative of no great sophistication. In commercial terms, they were a phenomenon. Beecham understood something most of his contemporaries did not — that a cheap, repeatable consumer product could be scaled almost without limit through advertising. He poured money into print, blanketing Victorian newspapers with Beecham's copy until the brand became a household name, and the cash the pills generated funded the firm's slow migration into proprietary and, eventually, prescription medicines. Beecham was, in the language of modern strategy, running a consumer-staples playbook a century before the phrase existed: a branded, habitually purchased, low-cost product throwing off cash to fund a move up the value chain.

The third bench was in Philadelphia. In 1830, John K. Smith opened a drugstore there; in the following decades the business joined with Mahlon Kline and others to become Smith, Kline & French — SK&F. This was the branch where the serious science lived. In the early 1950s, SK&F licensed and commercialized chlorpromazine under the brand Thorazine, a drug that did nothing less than transform psychiatry, emptying the back wards of asylums and making outpatient treatment of psychosis conceivable for the first time. Then, in 1976, SK&F delivered one of the defining commercial achievements in the history of the industry: Tagamet (cimetidine), the first of the H2-receptor antagonists for ulcers. Tagamet did not just treat peptic ulcers; it replaced surgery for millions of patients, and it became the first medicine in history to exceed $1 billion in annual sales — the original blockbuster, the drug that taught the whole industry what a true franchise could be worth. (Tagamet's success also drew a competitor's response that will reappear, darkly, later in this story: a rival H2 blocker called ranitidine, sold as Zantac.)

There is a fourth strand worth naming, because it supplied GSK's respiratory backbone. The Wellcome side of the family — founded by two American pharmacists, Henry Wellcome and Silas Burroughs, who built Burroughs Wellcome in Victorian London — was a research powerhouse in its own right, home to Nobel-winning scientists and, crucially, to the asthma and antiviral chemistry that would later underpin franchises like the Advair/Seretide inhaler dynasty and, indirectly, the HIV heritage that flowed into ViiV. When Glaxo absorbed Wellcome in 1995, it was not just buying scale; it was buying the respiratory and antiviral DNA that still generates a large share of GSK's revenue today. The pattern across all four strands is the same: each was, at its peak, a focused innovator, and each lost some of that focus as it grew and merged.

These three streams braided together over the back half of the twentieth century — Beecham and SmithKline Beckman merging into SmithKline Beecham in 1989, Glaxo absorbing Wellcome into Glaxo Wellcome in 1995 — and then, in 2000, they converged in one of the largest transactions the sector had ever seen. Under CEO Jean-Pierre Garnier, Glaxo Wellcome and SmithKline Beecham combined in a deal valued at roughly £115 billion, creating the world's second-largest pharmaceutical company and christening it GlaxoSmithKline. On paper it was a colossus. In practice, the mega-merger exposed what might be called the conglomerate trap. The combined entity was enormous, slow, and internally political; its marketing budgets dwarfed its breakthrough output; and its research pipeline, spread thin across too many therapeutic areas and too many legacy fiefdoms, struggled to produce the caliber of new molecules its scale demanded. GSK entered the twenty-first century with the balance sheet of a giant and the metabolism of a bureaucracy — and a pattern, inherited from its milk-and-laxative ancestors, of reaching for consumer cash flows whenever the drug pipeline disappointed. It would take two more decades, and a great deal of pain, to break that pattern. The breaking began under a soft-spoken doctor named Andrew Witty.

III. The Conglomerate Trap & The Great Swap

Andrew Witty took over as chief executive in 2008, and he did so at the worst possible moment for a big pharmaceutical company: on the leading edge of the industry's great patent cliff, as a generation of nineties-era blockbusters marched toward expiry and the R&D engines that were supposed to replace them sputtered. Witty was a GSK lifer, thoughtful and diplomatic, and his instinctive response to the drought was defensive. If the high-risk, high-reward business of inventing breakthrough small molecules was failing to pay off reliably, then the answer was to diversify away from that risk — to build a broader, steadier, more geographically spread portfolio anchored in things that did not live or die by a single Phase III readout: consumer healthcare, established brands in emerging markets, generics, and vaccines.

Witty was, by temperament, a builder of systems rather than a swashbuckler. He restructured GSK's research into smaller, semi-autonomous units meant to behave more like biotech startups, tied their funding to milestones, and championed "open innovation" — partnerships, patent pools for neglected tropical diseases, and tiered pricing in poor countries that won him genuine admiration as one of the more socially thoughtful executives in the industry. He was knighted for services to the economy and to public health. But admiration is not the same as returns, and beneath the reformist rhetoric GSK's core problem persisted: too few genuinely new, high-value molecules were emerging from the pipeline relative to the sheer amount being spent, and the ones that did emerge too often landed in crowded, price-pressured categories rather than in the frontier areas where pricing power and durability live.

It was a coherent philosophy, and in retrospect a costly one, because it led Witty to make a decision that would define GSK's competitive position for a decade: he stepped away from oncology at the precise moment oncology was about to become the most valuable therapeutic battlefield in medicine. The vehicle for that retreat was one of the most intricate transactions the industry has ever executed — the 2015 three-part asset swap with Novartis, which completed in March of that year.[^5]

Unpacked, the swap had three moving parts, and each one is a strategic decision in its own right. First, GSK sold its marketed oncology portfolio to Novartis for approximately $16 billion in cash, with the potential for up to $1.5 billion more contingent on a clinical milestone.[^5] Second, GSK bought Novartis's vaccines business — everything except the influenza franchise — for an initial $5.25 billion plus royalties, a deal that brought in the meningitis B vaccine Bexsero and meaningfully deepened GSK's vaccine bench.[^5] Third, the two companies pooled their consumer health portfolios into a joint venture, GSK Consumer Healthcare, in which GSK held a 63.5% controlling stake.[^5] Read together, the three legs point in one direction: away from the high-stakes, winner-take-all world of cancer drugs and toward the high-volume, defensively steady worlds of vaccines and consumer brands.

The consumer joint-venture leg deserves a note of its own, because it set up the drama of the following decade. By combining GSK's and Novartis's consumer brands into a single controlled venture, the 2015 swap created — almost as a byproduct — the scaled consumer-health champion that would eventually become Haleon. Novartis retained a large minority stake it would later sell down and out, giving GSK full control and, ultimately, the clean asset it could demerge. In other words, the transaction that hollowed out GSK's oncology position simultaneously assembled the consumer business whose separation would define the Walmsley years. The swap was not one decision; it was three, braided together, and their consequences would play out on completely different timelines.

For the vaccines side of the ledger, the logic was sound and the payoff would eventually be enormous. Vaccines are a genuinely different business from small-molecule pharmaceuticals — they are biologically complex, extraordinarily hard to manufacture at scale and quality, and therefore far harder for generic competitors to copy than a pill. Consolidating a global vaccines franchise gave GSK a platform with structurally better defensibility than the oral drugs it was becoming known for. The Bexsero acquisition, and the manufacturing and adjuvant know-how that came with the Novartis assets, would help set up the vaccine powerhouse GSK became.

But the oncology divestiture is where the story turns, and it is worth being clear-eyed about what happened. In 2015, selling a modest, sub-scale oncology portfolio for $16 billion in cash looked like shrewd portfolio pruning — take a full price for assets where you lack scale, and redeploy into areas where you have an edge. What GSK could not have priced, or chose not to, was the revolution about to break over cancer treatment. Within a year or two, the checkpoint inhibitors — Merck's Keytruda, Bristol Myers Squibb's Opdivo — would begin transforming oncology from a graveyard of incremental therapies into the industry's single most valuable and fastest-growing market, ultimately producing individual drugs with annual sales larger than GSK's entire vaccine division. By selling out of oncology in 2015, GSK did not just take a price; it forfeited its option on the biggest value-creation event in modern pharmaceuticals and left itself, in the words of its later critics, entirely naked in cancer just as cancer became the game. The full cost of that decision would not become visible until a new CEO tried, at great expense, to buy the company back into the arena Witty had walked away from.

IV. The Consumer Separation & The Unilever Drama

When Emma Walmsley was named to succeed Witty in 2017, the reaction across the pharmaceutical establishment ranged from skepticism to open derision. Walmsley was not a scientist. She had spent seventeen years at L'Oréal, the French cosmetics giant, before joining GSK in 2010 to run the consumer healthcare business — she was, in the eyes of a research-obsessed industry, a marketer of shampoo and toothpaste being handed the keys to a company whose future supposedly depended on molecular biology. The idea that a consumer-packaged-goods executive should lead one of Britain's two great drug houses struck many analysts as a category error. It is one of the quiet ironies of this story that the executive installed to preside over GSK's consumer-heavy structure would become the one to dismantle it entirely.

To understand Walmsley, understand what L'Oréal teaches. She spent nearly two decades in a business obsessed with brands, consumer behavior, distribution, and ruthless portfolio management — deciding which products to back, which to kill, and how to allocate marketing capital for maximum return. That is not drug discovery, but it is exactly the skill set a company needs when its central problem is not "can we invent things" but "have we built a bloated, unfocused portfolio that destroys value at the edges." Walmsley's critics saw a marketer out of her depth in molecular biology. Her defenders — and the eventual record — saw a disciplined capital allocator brought in precisely to make the hard portfolio decisions that a lifelong scientist, emotionally attached to every research program, might flinch from. Her tenure would test which reading was right, and the answer turned out to be more favorable to her than the 2017 consensus allowed.

Walmsley moved on two fronts at once, and they pulled in opposite directions, which is what made her tenure feel like a decade of controlled demolition. On one front she began preparing the eventual separation of the consumer business. On the other, she recognized the gaping hole Witty had left in oncology and set out to fill it — fast, and, her critics would argue, recklessly. The instrument was the $5.1 billion acquisition of Tesaro, announced in late 2018.5

The Tesaro deal is a case study in what it costs to rebuild a moat you have already sold. GSK paid $75 per share in cash, a price that represented roughly a 110% premium to where Tesaro's stock had recently traded — more than double the market value of the company, with no rival bidder forcing the price up.5 The immediate market verdict was withering: GSK's own shares fell around 8% on the announcement as investors digested the sheer size of the premium.5 The headline asset, Zejula, was a PARP inhibitor for ovarian cancer that faced ferocious competition, most obviously from AstraZeneca's Lynparza, and critics argued GSK had grossly overpaid to reverse Witty's 2015 exit — paying a fortune to re-enter a market it had walked out of for cash three years earlier. It looked, at the time, like an expensive act of strategic remorse.

Why pay a 110% premium with no competing bidder? The uncomfortable answer is that GSK was negotiating from weakness, not strength. Having exited oncology entirely in 2015, it had no platform, no commercial oncology infrastructure of consequence, and a narrowing window to rebuild before the field consolidated around a handful of scaled players. When you need to be in a market and the seller knows it, you pay the price the seller names. That is the deeper lesson of Tesaro, and it is a governance lesson as much as a strategic one: the 2015 divestiture did not just lose an option, it destroyed GSK's negotiating position for re-entry, converting what should have been a buyer's market into a seller's market with GSK as a captive buyer.

Buried inside the Tesaro portfolio, however, was an asset almost nobody was pricing: an unapproved, early-stage anti-PD-1 monoclonal antibody then known by its development code and later branded Jemperli (dostarlimab). In 2018 it was a footnote — one more checkpoint inhibitor arriving late to a crowded party dominated by Keytruda and Opdivo. Whether that footnote would eventually justify the whole $5.1 billion was, at the time of purchase, entirely unproven. Hold that thought; the payoff comes several years later, and it reframes the entire deal.

While Walmsley was buying her way back into oncology, the consumer business she had once run was becoming the center of the highest-stakes corporate drama of her tenure. In late 2021, Unilever — the Anglo-Dutch consumer-goods conglomerate — approached GSK with a series of proposals to buy GSK Consumer Healthcare outright, culminating in an offer valued at approximately £50 billion in cash and stock.6 GSK's board, chaired by Sir Jonathan Symonds, rejected it, declaring publicly that the bid "fundamentally undervalued" the business and its prospects.6 Unilever walked away shortly afterward under pressure from its own shareholders, who balked at the price and the strategic logic.

Rather than sell, GSK chose to demerge. In July 2022, the consumer healthcare division was spun off as an independent, separately listed company on the London Stock Exchange under the name Haleon — home to Sensodyne, Panadol, Advil, Centrum, and a stable of other household brands.[^10] The demerger was, in one sense, the culmination of everything the previous fifteen years had been building toward: GSK was finally, cleanly, a pure-play biopharmaceutical company. But the market's valuation of the newly independent Haleon delivered an uncomfortable verdict on the board's earlier decision. Haleon began trading at a market capitalization in the region of £30 billion and settled well below the £50 billion Unilever had been prepared to pay in cash and stock only months before.

The optics were painful, and the criticism was pointed: the board had turned down a rich, largely-cash offer for the division, only to watch public investors value that same business at a substantial discount to the rejected bid on its very first day of trading. There is a more charitable reading — that a demerger let GSK shareholders retain the upside in a good business rather than cashing out at a single fixed price, that the Unilever bid's large stock component was itself of uncertain and possibly deteriorating value, and that a straight sale would have triggered an enormous tax bill that the demerger avoided. On this reading the board did not reject £50 billion of certain value; it rejected an offer whose real, after-tax, risk-adjusted value to GSK shareholders was a good deal lower than the headline. The honest verdict sits in between: the demerger was defensible, but the board's public claim that £50 billion "fundamentally undervalued" the business looked, within months, like exactly the kind of overconfident assertion an independent analyst should be skeptical of when management is talking its own book.6 The episode fed a narrative that would soon crystallize into a full-blown governance crisis: that GSK's board, and its non-scientist CEO, were leaving value on the table and needed to be forced to do better. An activist was already circling.

V. The Activist Siege & The Zantac Hangover

By the time Haleon rang the opening bell, Emma Walmsley had already survived an assault on her job that most CEOs do not walk away from. In 2021, Elliott Management — the New York hedge fund run by Paul Singer, and perhaps the most feared activist investor on the planet — had built a multi-billion-pound position in GSK and gone public with a scathing analysis of the company's long underperformance. Elliott's central argument cut straight at Walmsley's legitimacy. The fund noted that GSK's total shareholder returns had lagged badly behind peers, and above all behind its natural British rival AstraZeneca, whose science-led resurgence under Pascal Soriot had become the template for what a focused, R&D-driven pharma could achieve. Elliott's most provocative demand was that Walmsley should be required to formally reapply for the CEO role of the post-demerger "New GSK," and that the board should recruit directors with genuine, world-class scientific and drug-development pedigree — the implication being that a marketer had no business running a drug-discovery company.7

The AstraZeneca comparison was the sharpest blade in Elliott's argument, and it is worth understanding why it stung. In 2014, AstraZeneca had fought off a $118 billion takeover approach from Pfizer, with CEO Pascal Soriot staking his credibility on an audacious promise: that AstraZeneca's own pipeline, particularly in oncology, would deliver more value than Pfizer's cash. Over the following years he made good on it, as drugs like Tagrisso and Imfinzi turned AstraZeneca into one of the great pharma growth stories of the decade and its share price left GSK's far behind. Here were two British pharma giants of similar heritage and similar size, and one had bet on science and won while the other had diversified into consumer goods and stagnated. Elliott did not have to invent a narrative; it simply had to point across the Thames. The implicit charge was devastating precisely because it was concrete: GSK's underperformance was not bad luck, it was a choice, and the person who made the choice was a marketer.

What followed was a masterclass in activist defense, and it is central to any honest assessment of Walmsley's record. Rather than capitulate, the board dug in. It rallied its major institutional shareholders behind the existing strategy, moved to strengthen the board's scientific credentials, and leaned hard on the elevation of R&D leadership — most visibly the promotion of Tony Wood, a seasoned drug-development scientist, to Chief Scientific Officer, directly addressing Elliott's charge that the company lacked scientific depth at the top.7 Walmsley kept her job, the demerger proceeded on the board's terms rather than the activist's, and Elliott's campaign faded without securing its headline demand. For an investor weighing management credibility, this is a genuine data point in Walmsley's favor: faced with the most formidable activist in the business, she and the board held the line and executed the strategy they had committed to. Whether that strategy was the right one is a separate question — but they delivered what they said they would.

Elliott, however, was the manageable crisis. The existential one was chemical, and its name was Zantac. Recall that Zantac (ranitidine) had been the H2-blocker that raced against SK&F's own Tagamet decades earlier and went on to become one of the best-selling drugs in the world. Its problem emerged long after its commercial heyday: allegations that ranitidine molecules can degrade over time — potentially accelerated by heat and storage — into NDMA, a compound classified as a probable human carcinogen. Beginning in 2019 and 2020, regulators pulled ranitidine products from the market, and a wave of American litigation followed, with tens of thousands of plaintiffs alleging that Zantac had caused their cancers.

For GSK shareholders, the Zantac litigation was, for a stretch of 2022, a genuine near-death experience for the equity — not because the company was insolvent, but because the tail risk was unquantifiable. In the summer of 2022, as key U.S. court decisions loomed and plaintiffs' lawyers floated damages theories running into the tens of billions of dollars, GSK's share price fell hard, and the litigation overhang wiped out an enormous slice of the company's market value — well over £30 billion at the trough, as investors simply could not price a liability with no visible ceiling. This is the defining feature of mass-tort risk for a pharmaceutical investor: it is not that the eventual bill is necessarily catastrophic, but that until it is bounded, the market cannot value the business at all, and the uncertainty itself destroys the stock.

It is worth separating myth from reality here, because the Zantac panic became a case study in how markets misprice legal tail risk. The consensus narrative in mid-2022 held that GSK faced a potential liability so large it could threaten the company's dividend and its investment-grade standing. The reality that emerged over the following two years was more prosaic: the scientific link between properly stored ranitidine and cancer proved far harder to establish in court than the early plaintiffs' theories suggested, several bellwether cases went GSK's way, and the eventual settlement figure landed at a small fraction of the tens-of-billions damages that had been floated at the trough. The lesson for investors is not that mass-tort risk is fake — it is real and occasionally ruinous — but that markets, unable to price an unbounded number, tend to price the worst plausible headline rather than the probable outcome. Those who could stomach the uncertainty were, in hindsight, paid for holding a risk that turned out to be bounded. Those who could not had already sold at the bottom.

GSK's resolution strategy was therefore about buying certainty as much as buying peace. Through 2023 and 2024 the company won several important trials and saw the scientific basis of the plaintiffs' claims challenged, gradually shrinking the perceived tail. Then, in October 2024, GSK announced a comprehensive settlement of up to $2.2 billion to resolve roughly 80,000 cases — approximately 93% of the product-liability claims pending against it in U.S. state courts — and separately settled with a major plaintiff to clear related exposure.8 Crucially, the settlement involved no admission of liability.8 For a company that had briefly faced an unbounded, tens-of-billions liability, capping the state-court exposure at a known, financeable number was arguably worth more than the absolute size of the check. It converted an existential, un-valuable risk into a line item. With the Zantac overhang systematically cleared and Haleon gone, GSK entered 2025 as something it had not been in its entire modern history: a clean, focused, litigation-light biopharmaceutical company whose value would finally be decided by the performance of its drugs. Which brings us to the engine itself.

VI. The Core Engine: Segment-Level Financials & Proportional Economics

To understand GSK today, forget the corporate history for a moment and look at how the £32.7 billion of 2025 turnover is actually generated, because the shape of that revenue is the whole investment case in miniature.1 The company reports in three buckets. Specialty Medicines is the largest and fastest-growing at £13.5 billion, roughly 41% of the total. General Medicines — the legacy inhalers and established products — contributes £10.0 billion, about 31%. And Vaccines delivers £9.2 billion, around 28%.1 The critical thing to notice is the direction of travel: Specialty grew 17% in 2025 while General Medicines shrank 1%, which means GSK is steadily transforming from a legacy-heavy company into a specialty-and-vaccines company with every passing quarter.1 The mix is migrating toward higher margins and higher defensibility. That is the strategy working in real time — but the same mix shift also concentrates the company's fortunes on a smaller number of high-stakes franchises, each with its own cliff.

The financial character of the modern GSK is worth stating before diving into the segments, because it is what gives management room to maneuver. In 2025 the company converted its £32.7 billion of turnover into a 12% rise in core earnings per share to 172 pence, generated roughly £8.9 billion of cash from operations and £4.0 billion of free cash flow after investment, and paid a dividend of 66 pence with guidance to raise it to 70 pence in 2026.1 Those are the numbers of a business with genuine pricing power and disciplined cost control — a far cry from the low-margin conglomerate of a decade earlier. But free cash flow of £4 billion is also a constraint: it is enough to fund a steady stream of bolt-on deals and a growing dividend, but not enough to buy GSK's way out of the dolutegravir cliff with a single transformational acquisition without stretching the balance sheet. The cash statement, in other words, is exactly consistent with the "disciplined bolt-on" strategy — and it also explains why that strategy is less a philosophy than a necessity.

The High-Margin Engine: Specialty Medicines

Within Specialty, the dominant force is HIV, run through ViiV Healthcare — the specialist joint venture GSK formed in 2009 to house its HIV assets. ViiV generated £7.7 billion in 2025, up 11%, making it comfortably the single largest profit contributor in the entire group.1 And in early 2026, its ownership was simplified in a way that matters for how investors should read GSK's future cash flows. Pfizer, one of the original partners, exited its economic interest: in a transaction announced in January 2026 and completed in April, ViiV issued new shares to Japan's 塩野義製薬 Shionogi for $2.125 billion and cancelled Pfizer's holding, with Pfizer receiving $1.875 billion and GSK taking a special dividend. The result is a clean two-shareholder structure — GSK holding 78.3% and Shionogi 21.7% — which means a larger share of ViiV's economics now flows through to GSK.9 It also, not incidentally, removed a put-option liability that had sat on GSK's balance sheet.9

Here is where the central conflict of the whole company lives. ViiV's franchise was built on dolutegravir, the oral integrase inhibitor sold in Tivicay and, combined with lamivudine, in the two-drug regimen Dovato. Dolutegravir is a marvel of efficacy and tolerability — but its U.S. composition-of-matter patent expires in April 2028, and its European protection in July 2029.4 Think of what that means mechanically: a product line responsible for the bulk of a £7.7 billion division will, starting in 2028, face generic copies priced at a fraction of the branded product. In small-molecule pharmaceuticals, that is not a headwind; it is a cliff, and it arrives barely two years into Luke Miels' tenure.

To feel the weight of that date, picture what a patent cliff actually does. A branded small-molecule drug typically holds close to 100% of its market until the day protection lapses; within a year of generic entry, it can lose 80–90% of its revenue as pharmacies automatically substitute cheaper copies and payers mandate the switch. There is no gentle glide path — it is a wall. For a molecule generating billions, that means several billion pounds of high-margin revenue can evaporate over a handful of quarters. This is the single most predictable and most destructive event in the pharmaceutical business, and every major drugmaker organizes its strategy around outrunning its own cliffs. GSK's April 2028 date is not a surprise or a risk that might materialize; it is a scheduled demolition, and the entire question is what GSK can build to replace the revenue before the wrecking ball swings.

ViiV's answer — and it is the most important strategic bet in the company — is to move patients off daily oral pills and onto long-acting injectables before the cliff hits. The lead products are Cabenuva, a treatment regimen dosed as infrequently as every two months, and Apretude, a pre-exposure prophylaxis (PrEP) injection that prevents HIV infection. Both are anchored by cabotegravir, a molecule with patent protection extending toward 2031, and GSK is developing even longer-interval formulations — dosing as infrequently as twice a year — to extend the runway further.4 The logic is elegant: convert a patient from a generic-vulnerable daily pill to a proprietary injection administered in a clinic, and you do two things at once. You move them onto a molecule with years more patent life, and you erect a switching cost that a generic pill simply cannot overcome — because the "product" is now bundled with a clinical administration workflow that patients and providers are reluctant to abandon. Whether this conversion happens fast enough, and at high enough margins, is the single most important operational question at GSK, and no amount of management confidence settles it in advance; it will be settled by the conversion data over the next several years.

It is worth pausing on why ViiV exists as a separate structure at all, because it explains why HIV has been GSK's most resilient franchise. GSK spun its HIV assets into a dedicated joint venture in 2009, giving the business its own management, its own commercial focus, and its own singular mission — an unusually clean example of a large company deliberately creating a focused sub-unit rather than letting a franchise get lost inside a sprawling org chart. That focus produced dolutegravir, the two-drug regimen strategy (treating HIV effectively with fewer drugs and fewer long-term side effects than the traditional three-drug cocktails), and now the long-acting pivot. The ViiV model is, in miniature, the argument for the entire "focus" thesis that this whole article examines: a smaller, dedicated unit repeatedly out-innovated the larger, more diffuse competition. Whether GSK-as-a-whole can replicate that focus at scale is the open question; ViiV is the proof of concept.

The other Specialty story is oncology, and here the Tesaro footnote finally pays off. GSK's oncology sales reached £2.0 billion in 2025, growing an eye-catching 43%.1 The engine of that growth is Jemperli (dostarlimab) — the once-obscure anti-PD-1 antibody that arrived, almost unnoticed, inside the 2018 Tesaro deal.10 Jemperli has established itself first in endometrial (uterine) cancer, where it has moved into front-line combination use, and it has produced striking clinical results in mismatch-repair-deficient (dMMR) tumors — a genetically defined subset of cancers, most notably in colorectal cancer, where Jemperli-based treatment has in some trials produced complete responses without the need for surgery. The scientific significance is real: a treatment that can, for a defined patient group, dissolve tumors without an operation is the kind of result that reshapes clinical guidelines. That said, an honest ledger notes that at £2.0 billion, GSK's oncology franchise remains a fraction of the scale of Merck's or Bristol Myers Squibb's checkpoint businesses; Jemperli is a genuine success and a partial vindication of the Tesaro price, but it has not yet made GSK an oncology powerhouse. It has made GSK a credible oncology participant, which — given where the company stood in 2016 — is itself a meaningful recovery of lost ground. The wildcard is Blenrep, the multiple-myeloma therapy GSK pulled from the U.S. market in 2022 after a confirmatory trial disappointed, and which the company has been working to bring back on the strength of newer combination data — a reminder that GSK's oncology hand still contains as many question marks as aces.

The third and quietest pillar of Specialty is Respiratory, Immunology & Inflammation (RI&I), which grew 18% to £3.8 billion in 2025 — the fastest-growing sub-segment in the company after oncology.1 This is where GSK is quietly building its next franchise, and it deserves attention precisely because it gets so little of it. The anchor products are Nucala, a biologic for severe eosinophilic asthma and, increasingly, for COPD, and Benlysta, the first drug ever approved specifically for lupus — a notoriously difficult autoimmune disease where GSK holds a genuine first-mover position. What makes RI&I strategically important is that these are biologics, not small molecules: like vaccines, they are hard to copy, and their patents and manufacturing complexity give them more durable protection than the oral inhalers of General Medicines. The Aiolos and Bellus acquisitions were bets designed to feed exactly this pipeline. If the HIV franchise is the cash cow facing a cliff and vaccines are the fortress, RI&I is the option value — the part of GSK that could, if the late-stage pipeline delivers, become a third growth engine by the time the £40 billion target comes due.

The Cash-Flow Fortress: Vaccines

If Specialty is the growth engine, Vaccines is the fortress, and its keystone is Shingrix, the shingles vaccine that delivered £3.6 billion in 2025, up 8%.1 Shingrix is the closest thing GSK has to a structural near-monopoly, and understanding why is essential to understanding the whole company's competitive moat. Shingles is caused by the reactivation of the chickenpox virus in older adults, and Shingrix prevents it with an efficacy of roughly 97% — a figure that is simply in a different league from anything a competitor has fielded. The reason it works so well is not the antigen alone but GSK's proprietary AS01 adjuvant system.

An adjuvant deserves a plain-English explanation, because it is the crux of GSK's most defensible advantage. A vaccine's antigen is the piece of the pathogen that teaches the immune system what to attack. An adjuvant is a separate chemical "amplifier" mixed in alongside it — it provokes the immune system to respond far more vigorously than it would to the antigen alone. Here is the strategic point: the antigen in many vaccines is relatively easy for a competitor to replicate, but a sophisticated adjuvant system like AS01 is fiendishly difficult to formulate, source, and manufacture at scale. One of its key ingredients, QS-21, is derived from the bark of a Chilean soapbark tree, and the supply chain and chemistry around it are a genuine barrier to entry. So even a rival that copies the antigen cannot easily match Shingrix's clinical performance, because it cannot easily match the amplifier. That is a durable moat — though not a permanent one, since Shingrix's growth increasingly depends on lower-margin international markets and on re-vaccination dynamics as the initial wave of U.S. adoption matures.

Beyond Shingrix, the vaccines fortress rests on a broad and unglamorous base of franchises that individually rarely make headlines but collectively throw off dependable cash: the meningitis portfolio anchored by Bexsero and Menveo — the very assets the 2015 Novartis swap brought in, now grown into a multi-billion-pound business — plus pediatric and travel vaccines that most competitors cannot economically replicate. Meningitis vaccines grew in 2025, a reminder that the Novartis deal's vaccine leg, whatever the sins of its oncology leg, compounded into real value over a decade.1 This is the underappreciated character of a vaccine business: it is less about any single blockbuster than about a portfolio of hard-to-manufacture biologics, sold largely to governments and public-health systems on multi-year cadences, that competitors cannot easily disrupt because the barriers are industrial as much as scientific. Building a sterile, high-yield vaccine plant and validating it with regulators takes years and hundreds of millions of dollars before a single dose ships. That is the fortress — not a moat around one product, but a moat around an entire manufacturing capability.

The cautionary tale within Vaccines is Arexvy, GSK's vaccine against respiratory syncytial virus (RSV). In 2023, GSK won the race to market with the world's first RSV vaccine for older adults, and for a season it captured the lion's share of a brand-new market — a genuine first-mover triumph. But Arexvy's 2025 numbers tell a sobering follow-up story: sales of roughly £0.6 billion, growing just 2%.1 The deceleration is the direct result of competition arriving fast and hard — Pfizer's Abrysvo and Moderna's mRNA-based mRESVIA turned RSV from a GSK monopoly into a three-way war — compounded by shifting and narrowing U.S. recommendations on who should be vaccinated and how often. Arexvy is the reminder that being first is not the same as being defensible: without an AS01-class moat and with well-funded rivals, even a pioneering launch can stall within two years. It is a useful check on any assumption that GSK's vaccine science automatically translates into durable franchises.

The Legacy Portfolio: General Medicines

General Medicines is the past GSK is slowly outgrowing: £10.0 billion in 2025, down 1%, a portfolio of mostly mature respiratory inhalers and established products under steady generic and pricing pressure.1 The standout exception is Trelegy, a once-daily triple-therapy inhaler for COPD and asthma that combines three active ingredients in a single device. Trelegy generated £3.0 billion in 2025 and grew 13% — a striking outlier in an otherwise flat-to-declining segment.1 Its success shows that even in a commoditizing category, a genuinely differentiated delivery format (three drugs, one inhaler, once a day) can still command volume and margin. But Trelegy is one bright product in a division whose overall trajectory is gently downward, and its own device patents will not last forever. General Medicines is best understood as a slowly melting ice cube of cash flow — useful for funding the transition, not a source of future growth. The company's future rides on Specialty and Vaccines, which is precisely why the strategic lessons of the last decade are worth codifying.

VII. The Playbook: Key Strategic and Investing Lessons

Step back from the quarter-to-quarter numbers and GSK's modern history offers a set of transferable lessons — the kind of durable strategic principles that outlast any single drug or CEO. Three stand out, and each is anchored in a specific, expensive episode we have already walked through.

Lesson one: rebuilding a divested moat is brutally expensive. In 2015, selling the oncology business to Novartis for $16 billion in cash looked like disciplined portfolio management — take full value for a sub-scale asset and redeploy.[^5] Three years later, GSK paid $5.1 billion for Tesaro, at a 110% premium, largely to buy its way back into the very market it had exited.5 The lesson is not simply "don't sell oncology." It is that in industries defined by long innovation cycles and winner-take-most economics, corporate "focus" decisions can quietly destroy enormous option value. The oncology GSK sold in 2015 was small; the oncology it was locked out of turned into the industry's most valuable arena. When you divest a position in a major, fast-evolving market, you are not just selling today's cash flows — you are selling the option to participate in whatever that market becomes, and that option can be worth far more than the price you receive. Buying it back, if you can at all, means paying the market's price after the value has already been revealed.

Lesson two: in vaccines, the adjuvant is the moat. The Shingrix story generalizes into a principle about where competitive advantage actually sits in vaccine design. The antigen — the visible, headline component — is often the least defensible part, because competitors can identify and replicate it. The durable advantage lives in the harder-to-copy layer: the adjuvant chemistry, the manufacturing process, the specialized supply chain. In the language of Hamilton Helmer's 7 Powers, GSK's AS01 platform functions as a Cornered Resource — a preferential access to a coveted asset (here, decades of accumulated adjuvant know-how and a locked-up specialty supply chain) that rivals cannot easily obtain at any price. The investing lesson: when analyzing any product-based moat, ask which layer of the product is actually hard to copy. If the answer is "the visible, marketed part," the moat is shallow. If it is a process or resource buried three layers down, the moat may be deep. Arexvy, tellingly, lacked that buried layer against mRNA competitors, and its franchise eroded.

Lesson three: long-acting formulations are a switching-cost engine, not just a convenience. ViiV's pivot from daily oral HIV pills to multi-month injectables is usually described in terms of patient convenience, but the strategically important effect is economic. Once a patient is established on an injection administered in a clinician's office — with the appointment cadence, the provider workflow, and the reimbursement plumbing all built around it — the cost of switching back to a generic daily pill is high for everyone involved. The generic competitor may have an identical molecule and a far lower price, but it cannot easily dislodge a patient who has been moved into a different treatment paradigm entirely. Long-acting delivery, in other words, converts a molecule-level competition (which generics win on price) into a workflow-level competition (which incumbents can win on inertia). It is one of the most elegant defensive maneuvers in pharmaceuticals — provided the conversion happens before the patent cliff, not after. That single proviso is what separates GSK's bull case from its bear case.

Notice that all three lessons rhyme. Each is, at bottom, a lesson about the difference between the visible surface of a business and the durable layer beneath it. Divesting oncology looked like selling cash flows; it was really selling an option. A vaccine's antigen looks like the product; the real moat is the adjuvant nobody sees. A pill and an injection look like two delivery formats; they are really two entirely different competitive games, one fought on price and one fought on workflow. The through-line of GSK's modern history — and the discipline it demands of an investor analyzing it — is to keep asking where the actual defensibility lives, and to refuse to be satisfied by the version of the story that sits on the surface. That discipline is exactly what the bull-versus-bear debate over the next five years will require.

VIII. Analysis: The Bear vs. Bull Case & The 2031 Horizon

Luke Miels inherits not just a strategy but an incentive structure engineered to make him think like the AstraZeneca operator he once was. GSK's executive pay, overseen alongside CFO Julie Brown, is benchmarked directly against a global peer set led by AstraZeneca, features U.S.-style long-term equity plans designed to reward multi-year outperformance, and carries an unusually demanding post-employment shareholding requirement — Miels is expected to hold shares worth 7.25 times his base salary, and to keep holding a large portion of that even after he leaves.4 The design intent is transparent: bind the CEO's personal wealth to GSK's long-run share price so that the temptation to juice short-term numbers ahead of the 2028 cliff is blunted. Whether incentive design translates into good judgment is, of course, unproven — but the structure at least points in the right direction.

Miels' own track record, and that of the team, has so far favored disciplined, mid-sized "bolt-on" deals over transformational gambles — a deliberate contrast to the Tesaro-era swings. The pattern is visible in three transactions: Affinivax in 2022, for up to $3.3 billion, which brought GSK a novel vaccine platform (the Multiple Antigen Presenting System, or MAPS) aimed squarely at Pfizer's dominance in pneumococcal vaccines;12 Bellus Health in 2023, for roughly $2.0 billion, which secured camlipixant, a late-stage candidate for refractory chronic cough;11 and Aiolos Bio in 2024, for up to $1.4 billion, which added a long-acting anti-TSLP antibody for asthma.[^15] Each is a targeted attempt to fortify a specific pipeline — vaccines, respiratory, immunology — without betting the company. The strategy is coherent. The risk, which we will come to, is that a string of mid-sized clinical bets can fail just as expensively as one large one, only more quietly.

The Competitive Frame: Five Forces and Seven Powers

Viewed through Michael Porter's five forces, GSK sits in a structurally attractive but pressured position. Barriers to entry are high — the capital, regulatory, and scientific requirements to field a vaccine or an HIV franchise are enormous — which protects incumbents like GSK from new entrants. Buyer power, however, is significant and rising: GSK sells into concentrated, price-sensitive buyers such as government health systems, U.S. pharmacy-benefit managers, and large payers who negotiate hard, particularly on vaccines and legacy inhalers. Supplier power is mostly low, with the sharp exception of specialty inputs like the soapbark-derived QS-21 adjuvant, where GSK has worked to secure and control supply precisely because it is a chokepoint. The threat of substitutes is the patent cliff in another guise — generic dolutegravir is the ultimate substitute, identical in molecule and cheaper in price. And rivalry is intense and well-funded across every franchise: Merck and Bristol Myers in oncology, Pfizer and Moderna in RSV, Pfizer in pneumococcal and increasingly in long-acting HIV.

Helmer's 7 Powers sharpens the picture of where GSK's advantages are real. Its clearest powers are Cornered Resource (the AS01 adjuvant platform and cabotegravir's fresh patents), Scale Economies (in vaccine manufacturing and the fixed cost of global clinical trials, where GSK's size is a genuine advantage), and Switching Costs (the clinic-administered long-acting franchises and the provider networks built around them). What GSK conspicuously lacks is Network Economies — nothing about GSK gets more valuable as more customers use it — and its Branding power, strong in consumer health, largely departed with Haleon. The honest read is that GSK's moats are real but narrow and franchise-specific: deep around Shingrix and long-acting HIV, shallow-to-absent around General Medicines and, increasingly, RSV.

The Bear Case

The bear case is disciplined and largely reduces to timing. The dominant risk is the 2028 dolutegravir cliff: if ViiV cannot convert enough patients onto long-acting injectables before generic dolutegravir arrives, the entry of cheap generics will gut the margins of a franchise responsible for well over a fifth of group revenue, and it will do so on a timeline that leaves little room to recover.1 The conversion is a race against a fixed date, and the bear notes that clinic-administered injectables face real-world friction — reimbursement, patient adherence to appointments, provider capacity — that could slow adoption below what management assumes.

The second pillar of the bear case is vaccine saturation and price war. Shingrix's high-margin U.S. growth is maturing, pushing the franchise toward lower-margin international markets, while Arexvy's stall demonstrates that GSK's vaccine science does not guarantee durable share once well-funded rivals arrive.1 The third is pipeline execution risk: the Affinivax, Bellus, and Aiolos bolt-ons are late-stage bets that can still fail in Phase III or stumble in regulatory review, and a cluster of such failures would not only cost the purchase prices but would puncture management's credibility on capital allocation at the worst possible moment. A skeptical long/short investor would add a fourth, quieter concern: GSK has repeatedly reached for expensive M&A to paper over pipeline gaps, and the market will be watching closely for any sign that the "disciplined bolt-on" era gives way to another Tesaro-style lunge if the organic pipeline disappoints.

The Bull Case

The bull case is the mirror image, and it hinges on the same variables breaking GSK's way. First, the long-acting HIV transition succeeds: ViiV moves the treatment and PrEP markets onto injectable cabotegravir before 2028, locking in patients behind switching costs and fresh formulation patents that extend the franchise's protected life toward and beyond 2031 — converting a looming cliff into a multi-decade annuity.4 Second, Jemperli compounds: dostarlimab entrenches itself as a standard of care in front-line endometrial cancer and expands into the dMMR colorectal, gastric, and other tumor settings where its data are strongest, turning the Tesaro purchase from a punchline into one of the better-value oncology deals of its era.10 Third, unencumbered execution: with Zantac capped at a financeable number and the consumer business gone, GSK can direct essentially all of its £4.0 billion-plus of annual free cash flow toward high-margin biopharma R&D and shareholder returns, rather than toward litigation reserves and conglomerate overhead.18

There is also a governance and capital-allocation stress test that a sharp-eyed activist would run, and it is worth stating plainly because it cuts against the clean-story narrative GSK's investor relations prefers. First, management credibility on M&A is a mixed record, not a spotless one: the same company that overpaid spectacularly for Tesaro and rejected a £50 billion cash-and-stock offer for the business it then floated at a discount is now asking investors to trust its "disciplined bolt-on" framing. The bolt-ons look sensible today, but the institutional temptation to make a large, cliff-covering acquisition if the organic pipeline wobbles is real, and shareholders should treat any pivot back toward big M&A as a warning, not a rescue. Second, the £40 billion target itself invites scrutiny: round-number, long-dated sales goals are a classic device for anchoring a narrative, and the honest question is whether the target is driven by identifiable products with defined timelines or by an aspiration working backward from a headline. On the evidence, GSK has at least named the "15 major launches" it is counting on through 2031 — but naming launches is not the same as landing them, and a genuinely independent observer keeps the burden of proof on the company. Third, the benchmarking of pay against AstraZeneca is double-edged: it aligns incentives, but it also frames the entire GSK story as a catch-up race against a rival that has, for most of the last decade, simply executed better on science. Being paid to close a gap is an admission that the gap exists.

The synthesis a fundamental investor should hold in mind is that the bull and bear cases are not competing stories about different companies — they are the same story with different assumptions about speed. Does the long-acting conversion outrun the patent clock? Does the oncology pipeline mature before the HIV base erodes? Can RI&I and the vaccine base grow fast enough to absorb the dolutegravir shock? GSK does not need a miracle; it needs its transitions to complete on schedule, and it needs to do so while a better-executing peer sets the benchmark for its own pay. The £40 billion 2031 target is management's assertion that they will. It is an assertion, not a fact, and it should be treated as a hypothesis to be tested against evidence quarter by quarter — not accepted because the company is confident.

The KPIs That Actually Matter

For all the complexity, an investor can track whether GSK is winning with a very short list of metrics. First, the ViiV long-acting conversion rate — the share of HIV revenue coming from injectable cabotegravir-based regimens (Cabenuva, Apretude) versus oral dolutegravir. This single ratio is the most direct measure of whether GSK is defusing its biggest bomb before it goes off. Second, Arexvy's global RSV market share — the cleanest read on whether GSK's vaccine franchises can hold ground against Pfizer and Moderna, or whether first-mover launches keep eroding into price wars. Third, oncology pipeline milestones — the cadence of Phase III readouts and approvals for Jemperli combinations and for camlipixant, which together will show whether the specialty pipeline is compounding or stalling. Watch those three, and you are watching the whole thesis.

IX. Epilogue & Outro

There is a strange symmetry to the arc that ends on the South Bank of the Thames in 2026. A company whose oldest ancestors sold a laxative made of aloes and soap, and dried milk marketed to build "bonny babies," has spent the last decade methodically stripping away everything that made it resemble those origins — the consumer brands, the household names, the comfortable low-margin cash flows its Victorian founders would have recognized — to become a pure-play biopharmaceutical specialist betting its future on adjuvant chemistry and long-acting molecules. The conglomerate that Jean-Pierre Garnier assembled in 2000, that Andrew Witty diversified, that Emma Walmsley dismantled through a decade of activist sieges, litigation panics, and boardroom drama, has arrived at last as the focused machine its strategists always said it should be.

Luke Miels inherits that machine with a clear runway and an unforgiving clock. The structure is clean, the litigation is bounded, the strategy is set, and the incentive plan ties his fortune to the outcome. What remains is the only thing that was ever really the point: whether GSK's R&D engine — its vaccine science, its HIV franchise, its rebuilt oncology pipeline — can produce enough new value fast enough to outrun the patent cliffs its own history keeps manufacturing. The 2028 dolutegravir expiry is the first and largest test, and it arrives before Miels has finished his second full year. The £40 billion target hangs on the far side of it, in 2031, as both a promise and a dare. The next five years will not be decided by the elegance of the strategy, which is genuinely elegant, but by the brute question of timing — whether the moats GSK spent a decade building are deep enough, and were finished in time, to hold the line while the old cash cows quietly go generic. That is the wager. The evidence will arrive one conversion rate, one trial readout, and one vaccine season at a time.

References

-

GSK delivers strong 2025 performance and re-affirms long-term outlooks — GSK, 2026-02-04 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Luke Miels appointed CEO designate for GSK — GSK, 2025-09-17 ↩

-

Factbox: Who is GSK's next CEO Luke Miels? — Reuters, 2025-09-17 ↩

-

GSK plc Annual Report 2025 — GSK Investor Relations, 2026-03-01 ↩↩↩↩↩

-

GSK to acquire Tesaro for $5.1 billion to rebuild oncology pipeline — Reuters, 2018-12-03 ↩↩↩↩

-

GSK rejects Unilever's £50bn bid for consumer health unit — Financial Times, 2022-01-15 ↩↩↩

-

How Emma Walmsley fought off Elliott Management and reshaped GSK — Bloomberg, 2022-07-15 ↩↩

-

GSK agrees to settle 93% of Zantac state court cases for up to $2.2 billion — Reuters, 2024-10-09 ↩↩↩

-

GSK, Pfizer and Shionogi agree on changes to ViiV Healthcare shareholding — GSK, 2026-01-20 ↩↩

-

GSK plc Annual Report 2024 — GSK Investor Relations, 2025-03-01 ↩↩

-

GSK to acquire BELLUS Health for $2.0 billion — GSK, 2023-04-18 ↩

-

GSK to acquire Affinivax for up to $3.3 billion — GSK, 2022-05-31 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube