Greggs plc: The Sausage Roll Hegemony

I. Introduction & Episode Roadmap

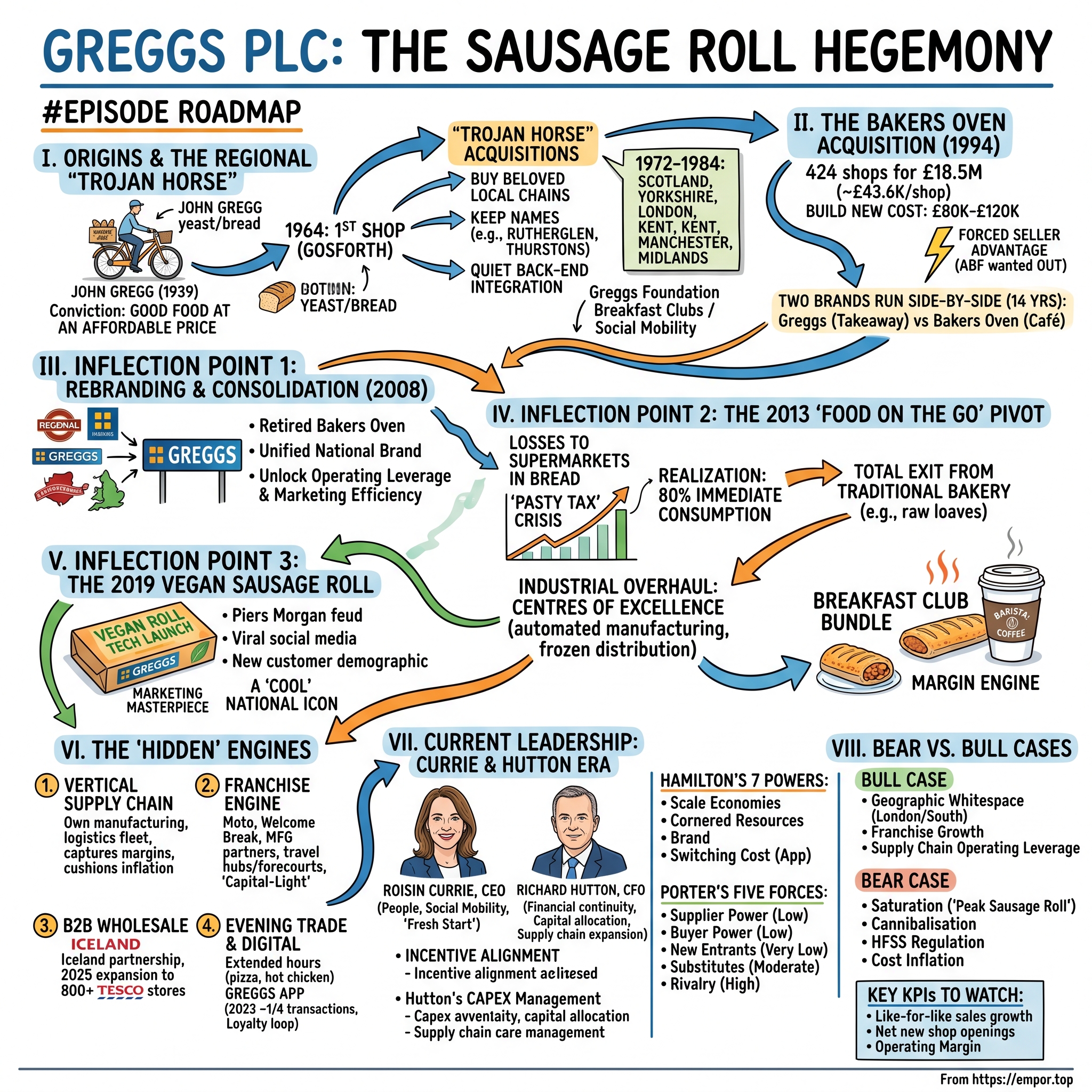

Picture a man on a bicycle in 1939, pedalling through the terraced streets of Gosforth on the northern edge of Newcastle upon Tyne. In his basket are yeast, eggs, and bread, and he is delivering them door to door to the working families of England's industrial North East. His name is John Gregg. He has no factory, no shops, no brand recognition beyond his own neighbourhood. He has a bicycle and a conviction that ordinary people deserve good food at a price they can actually afford.

Now fast-forward eighty-seven years. That bicycle round has become a publicly listed company on the London Stock Exchange generating over £2 billion in annual sales, operating roughly 2,600 shops, and — this is the part that still startles people — overtaking McDonald's as the United Kingdom's single most popular destination for breakfast.[^8] The sausage roll, a humble cylinder of seasoned pork wrapped in flaky pastry, has become a national icon. When a politician wants to look like a man of the people, he is photographed clutching a Greggs bag. When the company launched a vegan version of its signature product, it became front-page news and triggered a celebrity feud. How did this happen?

Here is the thesis, and it is the most important idea in this entire episode: Greggs is not a bakery. Or rather, calling Greggs "a bakery" is like calling Amazon "a bookshop." The truth is that Greggs is four or five businesses stacked on top of one another and disguised as a friendly high-street shop. It is a vertically integrated industrial food manufacturer that produces the majority of what it sells. It is a temperature-controlled logistics network with its own fleet. It is a tech-enabled digital loyalty platform with millions of app users. It is a franchise royalty engine bolted onto petrol forecourts and motorway services. And it is a B2B wholesale supplier sitting inside supermarket freezers. All of that machinery hums beneath a brand so beloved that the British public treats it as a kind of national treasure.

This is the story of how a regional bakery became a manufacturing-and-logistics powerhouse — and how it pulled off the rarest trick in retail, which is to become more profitable precisely because it stayed cheap.

Here is the roadmap. First, the origins and the regional "Trojan Horse" acquisition strategy that let Greggs conquer Britain piece by piece in the 1970s and 1980s. Second, the landmark 1994 acquisition of Bakers Oven and the bold 2008 decision to consolidate everything under one name. Third, the two great pivots — the 2013 reinvention as a "food-on-the-go" business and the 2019 vegan sausage roll that became a marketing masterpiece. Fourth, a deep dive into the hidden engines: vertical integration, franchising, wholesale, and the digital flywheel. Fifth, the modern guardians, chief executive Roisin Currie and chief financial officer Richard Hutton, and their capital-allocation playbook. And finally, the strategic analysis through Hamilton's 7 Powers and Porter's Five Forces, plus the bull and bear cases for the years ahead.

Let's start with the bicycle.

II. Origins & The Regional "Trojan Horse" Strategy

The early Greggs story is an origin myth almost too on-the-nose for a value brand. John Gregg founded his business in 1939, the year Britain went to war, delivering eggs and yeast by bicycle to the households of Gosforth.[^8] The North East of England in that era was a place of shipyards, coal pits, and heavy engineering — hard physical labour, modest wages, and a deep cultural premium on getting good value for your money. You did not waste. You did not show off. You fed your family well and you did not overpay. That ethos was not a marketing slogan invented in a boardroom; it was simply the water Greggs swam in. And it would prove to be the most durable competitive asset the company ever built, because it could never be replicated by a chain that arrived later trying to act working-class.

When John Gregg died in 1964, his son Ian Gregg took over and opened the first dedicated Greggs shop in Gosforth. The company that had been a delivery round became a retailer. And here is where the story gets genuinely interesting from a strategy standpoint, because Ian Gregg confronted the central problem of every regional retailer who dreams of national scale: how do you get big, fast, without bankrupting yourself building from scratch?

The slow way is organic. You find a high street, sign a lease, fit out a shop, hire and train staff, and then spend years — years — earning the trust of locals who have their own bakery they have used since childhood. Do that one shop at a time across a country and you will be dead before you finish. Ian Gregg looked at that math and made a decision that would define the company for the next half-century. Greggs would not build. Greggs would buy.

But it would buy in a very specific, very clever way. This is what we'll call the Trojan Horse strategy. Rather than march into a new region under the Greggs banner and trigger the resentment that outsiders always trigger, Greggs would acquire a beloved local bakery chain and keep its name, its shopfronts, and its regional identity entirely intact.[^15] To the customer in Glasgow or Leeds or Kent, nothing changed. Their favourite local baker still had the same sign over the door. What changed was invisible: behind the scenes, Greggs slowly absorbed the supply chain, the procurement, the recipes, and the logistics, harvesting the cost advantages of scale while leaving the brand love undisturbed.

The campaign unfolded across two decades. In 1972, Greggs acquired Rutherglen in Glasgow, planting its flag in Scotland.[^15] In 1974 came Thurstons in Leeds, which gave rise to "Greggs of Yorkshire" and a foothold in the populous textile-and-industrial belt.[^15] Then came the masterstroke year of 1976, a multi-region sweep that landed Broomfields in London, Bowketts in Kent, Tooks in East Anglia, and Price's in Manchester — four distinct regional businesses bought in a single coordinated push, each one a ready-made distribution beachhead in a part of Britain Greggs had never touched.[^15] In 1984, Braggs in the Midlands filled in another gap on the map.[^15]

Why keep all these names for so long? Because Ian Gregg understood something that MBA-driven acquirers routinely forget: brand equity is local, and ripping out a trusted local name to impose a foreign one destroys value you paid good money to acquire. A customer in Kent in 1980 did not want "Greggs from Newcastle." She wanted Bowketts, the bakery her mother used. By keeping the banner and quietly integrating the back end, Greggs got the best of both worlds — economies of scale on the inside, local affection on the outside. It is a strategy of patience, and it bought the company the one thing money usually cannot buy: time to grow trust.

That patience, that community-first instinct, was never abandoned. It echoes today in the company's social-mobility programmes and the Greggs Foundation breakfast clubs that feed schoolchildren across the country — initiatives that current chief executive Roisin Currie treats not as charity bolted on the side but as a continuation of the founding promise.[^13] The bicycle round, in other words, never really ended. It just got a logistics fleet.

By the early 1990s, though, Greggs had a structural weakness that all the regional charm in the world could not fix. It was strong in the North and patchy everywhere else. To become truly national, it needed scale in the South — and it needed it fast. The opportunity, when it came, arrived as a fire sale.

III. The Bakers Oven Acquisition: The Southern Crusade

In 1994, a phone was ringing inside Associated British Foods, the industrial giant that owned Allied Bakeries. ABF had made a strategic decision that would turn out to be Greggs' great good fortune: it wanted out of retail baking. Running shops was a fiddly, labour-intensive, low-margin distraction from what ABF really wanted to do, which was to operate enormous industrial flour mills and sell wholesale. Retail baking was a business it had drifted into and now wished to shed. And when a large conglomerate decides it no longer wants something, it does not always sell patiently for top dollar. It sells to clear the decks.

The asset on the block was Bakers Oven, a chain of 424 shops concentrated precisely where Greggs was weakest — the South of England and the Midlands.[^15] For Greggs, this was the missing piece of the entire national jigsaw, suddenly available from a motivated seller who valued speed and certainty over squeezing out the last pound. Greggs moved, and in 1994 it acquired Bakers Oven for £18.5 million.[^15]

Let's sit with what that number actually meant, because the genius of this deal is in the arithmetic. Four hundred and twenty-four shops for £18.5 million works out to roughly £43,600 per shop.[^15] Now compare that to the alternative. To build a single new bakery storefront on a British high street in that era cost somewhere between £80,000 and £120,000 in capital expenditure — and that was before you added lease premiums and before you spent the years required to build local brand equity from a standing start. Greggs, in a single transaction, acquired prime, high-footfall retail real estate at roughly half the cost of building it new, and it skipped the years of brand-building entirely because the shops already had customers walking through the doors.

This is the forced-seller advantage in its purest form, and it is one of the great recurring lessons in business history. When a large, well-capitalised seller is desperate to exit a category for strategic reasons rather than financial ones — when the asset is perfectly good but simply doesn't fit the seller's plan — a disciplined buyer can acquire quality at a discount that bears no relationship to the asset's intrinsic worth. ABF was not selling because Bakers Oven was failing. It was selling because milling was the future for ABF. Greggs read that asymmetry correctly and pounced. Overnight, the deal nearly doubled Greggs' estate and solved its single greatest structural weakness — its thinness in the South.[^15]

But Greggs did not immediately stamp its own name on the new shops, and here the strategic discipline shows again. For fourteen years, Greggs and Bakers Oven ran side by side as two distinct brands serving two distinct purposes. Bakers Oven became the more premium, sit-down café format — a place to linger over a coffee and a cake. Greggs remained the high-velocity grab-and-go takeaway brand, optimised for speed and value. Two propositions, two price points, two atmospheres, one supply chain humming beneath them both.

It was a sensible structure for its time. But a multi-brand empire carries a hidden tax that compounds quietly year after year — the tax of fragmentation. And by the late 2000s that tax had grown too large to ignore.

IV. Inflection Point 1: Rebranding & Brand Consolidation (2008)

By 2008, if you had drawn a map of the Greggs empire and colour-coded it by brand, you would have produced something that looked less like a coherent company and more like a patchwork quilt sewn by a committee. There was Greggs. There was Bakers Oven. There were the lingering ghosts of Thurstons, Braggs, and the other regional names absorbed over the decades.[^15] Each carried its own signage, its own local quirks, its own subtle differences in range and presentation. To the romantic, it was charming heritage. To the operator trying to run a modern national business, it was a slow-motion disaster.

Consider what fragmentation actually costs. You cannot run a national television advertising campaign when your shops carry five different names, because every pound you spend building awareness of "Greggs" does nothing for the Bakers Oven across town. You cannot enforce uniform national pricing or a coherent product-innovation pipeline when each banner has its own legacy assortment. You cannot build a single, instantly recognisable brand identity — the kind that lets a customer spot your shop from across a railway concourse — when the brand changes depending on which region the customer happens to be standing in. Fragmentation is the enemy of operating leverage, and operating leverage is the entire game in food retail.

So the leadership team made a bold and genuinely risky call. It would retire every remaining regional brand — including the surviving 165 Bakers Oven shops — and unify the entire estate under a single name: Greggs.[^15]

Why was this dangerous? Because in the South of England, "Greggs" carried baggage. It was perceived as a Northern, low-cost, slightly downmarket brand — fine for a builder's bacon roll, perhaps, but not the sort of place a Home Counties professional thought of as their bakery. The Bakers Oven name, by contrast, had spent years building a softer, more café-like image in exactly those Southern markets. Retiring it risked telling millions of loyal Southern customers that their pleasant local café was being replaced by a cheap Northern takeaway chain. In brand terms, it was a deliberate act of demolition, and demolition is always easier to get wrong than right.

But the payoff justified the risk, and it unlocked everything that came afterward. A single national brand meant Greggs could finally spend marketing money efficiently — every advertising pound now reinforced one name across the entire country. It meant a streamlined supply chain feeding one standardised range rather than a tangle of legacy assortments. And it meant the company could forge the iconic blue-and-orange identity that is now recognised instantly across Britain, the visual shorthand for fast, warm, affordable food.

Consolidation, in short, was the precondition for scale. You cannot industrialise what you have not first standardised. And industrialisation — turning Greggs from a network of bakeries into a manufacturing-and-distribution machine — was about to become the entire strategy. The trigger would be a crisis.

V. Inflection Point 2: The 2013 "Food on the Go" Pivot

In the years around 2012 and 2013, Greggs was quietly losing a war it had been fighting for decades, and it was losing it to an enemy that had become almost impossible to beat: the supermarket. The traditional heart of a British bakery's business — selling loaves of bread, scones, flour, and the sort of cakes you take home for tea — was in structural decline. The big grocers had turned bread into a loss-leading commodity, baking it in-store and selling it at prices a high-street baker simply could not match. Why would a family trek to Greggs for a loaf when the same loaf sat at the front of every Tesco and Asda for less?

Meanwhile, the high street itself was hollowing out. Footfall was cratering as shoppers migrated to out-of-town retail parks and, increasingly, to the internet. Margins were being squeezed from every direction. And then, in 2012, the government delivered an almost comic insult to injury: the so-called "pasty tax," a proposal to levy VAT on hot takeaway baked goods that landed squarely on products like the freshly baked sausage roll. The political backlash was so fierce that the policy was largely reversed, but the episode crystallised something — Greggs was operating in a category under pressure from supermarkets, from the high street's decline, and now from the taxman.

And then the company found a number that changed everything. Buried in its own customer data was a statistic that should have been obvious but somehow wasn't: roughly 80% of customers were buying Greggs products for immediate, on-the-go consumption — eaten within minutes, often before they had even left the street — and only a minority were buying to take home for later. Greggs had been thinking of itself as a bakery, a place where you bought provisions. But its customers had already decided it was something else entirely: a place where you grabbed lunch. The company was fighting the supermarkets in the take-home-bread war when it should have been fighting the sandwich shops and coffee chains in the food-on-the-go war — a market it was already, accidentally, winning.

This realisation set off a radical reset, and the executives who drove it included two figures who will dominate the back half of this story: Richard Hutton, the chief financial officer, and Roisin Currie, then the retail director. The decision they helped make was breathtaking in its decisiveness. Greggs would exit the traditional bakery market entirely. It would stop selling raw loaves of bread, stop selling baking flour, stop selling the complicated celebration cakes. It would pivot one hundred percent of its business to food on the go — sandwiches, sausage rolls, bakes, savouries, and crucially, coffee.

Now, walking away from a category you have been in since 1939 is the kind of move that gets discussed endlessly and executed almost never, because it means deliberately killing revenue you currently have in hand. But the pivot was not just a merchandising change; it demanded a complete industrial overhaul of how Greggs made and moved its food.

The old model — bake everything fresh in regional in-store bakeries — was charming and hopelessly inefficient. The new model was industrial. Greggs began closing down its scattered regional in-store baking operations and consolidating manufacturing into a small number of giant, highly automated "centres of excellence." The logic here is the logic of the modern food industry, and it is worth understanding in plain terms. Imagine building one enormous, robotically run factory whose sole job is to make every sausage roll sold in the entire United Kingdom. That single facility produces them at a scale and unit cost no in-store bakery could approach, freezes them raw, and ships them out daily to thousands of shops, where they are baked fresh on-site in ovens throughout the day. The customer still gets a hot sausage roll straight from the oven — the romance survives — but the economics behind it have been completely transformed. The skilled, expensive craft of making the pastry moves to the factory; the shop simply finishes the bake. Cost per unit plummets; consistency soars; freshness is preserved.

And then came the move that turned the pivot into a footfall machine: the Breakfast Club. Greggs began offering a hot bacon or sausage roll paired with a fresh, barista-style coffee for a single low bundle price — the kind of deal that undercut every coffee chain and every supermarket meal deal in the country. Think about the strategic elegance of this. Coffee is one of the highest-margin products in all of food retail; the marginal cost of a cup is pennies. By using a cheap, freshly baked roll as the hook and a high-margin coffee as the profit engine, Greggs manufactured a morning habit. It gave commuters a reason to walk in before lunch, doubling the number of times each shop could sell to the same customer each day. This is the daypart logic that would later become a central growth lever — wring more transactions out of the same four walls.

The pivot worked, and it reframed the entire company. Greggs was no longer a bakery competing with grocers. It was a food-on-the-go operator competing with sandwich shops and coffee chains, armed with an industrial cost base they could not match. All it needed now was to become culturally irresistible. That moment arrived, improbably, in the form of a vegan sausage roll.

VI. Inflection Point 3: The 2019 Vegan Sausage Roll

For all its commercial success, Greggs entered 2019 carrying a perception problem that money alone had never quite solved. In the eyes of much of the media — and in the eyes of a certain kind of affluent Southern consumer — Greggs was a guilty pleasure. It was where you went for a cheeky, slightly shameful treat, the food equivalent of a confession. It was cheap, it was a bit naughty, and it was emphatically not aspirational. That perception capped the brand. It meant whole demographics walked past the door.

In January 2019 — timed precisely to coincide with "Veganuary," the now-annual campaign encouraging people to try a plant-based diet for the month — Greggs launched a vegan version of its most iconic product. A sausage roll with no sausage, the meat replaced by a Quorn-based filling, wrapped in the same flaky pastry. On paper, this was a minor line extension. In practice, it became one of the most studied pieces of brand marketing in recent British history.

The masterstroke was in the framing. Greggs did not present the vegan sausage roll as a worthy, slightly apologetic health product for a niche audience. It presented it like a technology launch. The company sent samples to journalists packaged in a sleek box that deliberately parodied the unveiling of a new iPhone — the vegan roll nestled in moulded packaging, accompanied by a mock "tech spec" sheet describing the product in the breathless language of a gadget reveal. It was funny, it was self-aware, and it was exactly the kind of cultural wink that signalled Greggs understood the joke about itself. A value bakery treating a Quorn sausage roll like the launch of a flagship smartphone is inherently absurd, and Greggs leaned all the way into the absurdity.

Then came the gift that no marketing budget can buy. The broadcaster Piers Morgan, a man who has built a career on performative outrage, tweeted his disgust, branding Greggs "PC-ravaged clowns" for daring to make a vegan product. The tweet went viral. And rather than retreat into corporate blandness, Greggs' social-media team fired back with a perfectly judged, dry, self-assured reply — "Oh hello Piers, we've been expecting you" — that read as the confident comeback of a brand entirely comfortable in its own skin. The exchange detonated across the internet. Free, national, top-of-the-news coverage poured in. A celebrity had inadvertently become the launch's unpaid hype man, and Greggs had played the moment flawlessly.

The financial results were extraordinary. The vegan sausage roll sold out in shops across the country within hours of launch. More importantly, it became the spark for a banner year: Greggs reported a like-for-like sales surge of 13.5% in 2019, an exceptional figure for any food retailer and a number that would have been the envy of every competitor on the high street.[^15] But the deeper victory was strategic, not financial. The launch reached straight into a demographic that had long ignored Greggs — affluent, health-conscious, often Southern and urban — and gave them a reason to walk through the door for the first time. And it completed the brand's transformation from "guilty pleasure" into something far more valuable: a self-aware, beloved, genuinely cool national icon, a company so comfortable with its own identity that it could joke about itself and win.

The vegan sausage roll, then, was the moment Greggs stopped apologising for what it was and started celebrating it. With the brand now culturally bulletproof, we can finally lift the floorboards and examine the machinery underneath — the hidden engines that actually make the money.

VII. The "Hidden" Engines & Growth Initiatives

Walk into a Greggs and you see a shop. What you do not see is everything that had to happen for that sausage roll to be warm in your hand at that price — and that invisible apparatus is where the real strategic story lives. Greggs is a case study in how the most durable competitive advantages are usually the ones the customer never notices. Let's open up four of them.

The vertical supply chain. Here is the fact that separates Greggs from almost every other retailer on the high street: it manufactures the majority of the food it sells, and it owns its own distribution fleet to move that food.2 Most retailers are, at heart, middlemen — they buy finished products from suppliers and resell them, which means their margins are forever at the mercy of those suppliers and their costs rise and fall with someone else's pricing decisions. Greggs is the opposite. By owning the factories that make its savouries and the temperature-controlled lorries that deliver them, Greggs captures the manufacturing margin and the distribution margin that competitors hand to third parties. This is the "hidden business" — an industrial food manufacturer operating at enormous scale, sitting inside what looks like a chain of bakeries. The strategic payoff becomes most visible in bad times. When raw-material costs spike — when the price of pork, or wheat, or energy lurches upward — a conventional retailer simply eats the supplier's price increase or passes it to customers. Greggs, controlling its own production, can absorb inflationary shocks, find efficiencies inside its own four walls, and protect its value proposition when rivals are forced to raise prices. In an industry of thin margins and volatile commodities, owning the supply chain is not a cost; it is a shield.

The franchise engine. For most of its history Greggs grew by signing its own leases on expensive high-street property — paying the rent, fitting out the shop, carrying all the capital cost and all the risk. But high streets are exactly where footfall has been declining, and prime leases are expensive. So Greggs built a second growth engine that flips the economics entirely. Rather than open every shop itself, it partners with franchise operators who run Greggs outlets in locations Greggs cannot easily reach — partners such as EG Group (the business built by the Issa brothers), the motorway-services operators Moto and Welcome Break, and the forecourt group MFG.4 Across this network, franchise partners operate hundreds of Greggs locations in petrol stations, motorway service areas, and travel hubs.4 The magic is in who pays for what. The franchise partner provides essentially all of the capital expenditure to build and fit out the shop, while Greggs supplies the food, the brand, and the systems — and collects a highly profitable royalty and supply stream in return. This is the closest Greggs gets to a capital-light business: growth funded by someone else's balance sheet. And it deliberately shifts the company's geographic footprint away from the declining high street and toward the places where Britain actually travels — the forecourts, the service stations, the transport interchanges where a hungry traveller has nowhere else to turn.

The B2B wholesale business. For years Greggs ran a quiet, clever side business: an exclusive partnership with the frozen-food specialist Iceland to sell Greggs-branded frozen bakes that customers could finish baking in their own ovens at home.3 It put the Greggs brand inside the supermarket freezer aisle, reaching people in moments — a Saturday-night-in, a party spread — when they would never have visited a shop. Then in 2025 Greggs made the strategic decision to break that single-retailer exclusivity, rolling out Greggs-branded frozen products into more than 800 Tesco stores and tapping a vastly larger consumer base than Iceland alone could provide.3 It is a low-capital, high-reach extension of the brand: Greggs earns wholesale revenue from shoppers who buy its food without ever setting foot in a Greggs.

Evening trade and the digital flywheel. The final two engines are about squeezing more value out of assets Greggs already owns. The first is time. Historically a Greggs emptied out after lunch; the afternoon and evening were dead hours in shops that still had to be lit, staffed, and rented. So Greggs extended trading hours and built an evening proposition — pizza slices, hot chicken, sharing boxes — designed to capture the dinner and snack occasions that used to walk straight past. By 2025 this evening trade had grown to account for nearly a tenth of company-managed shop sales, incremental revenue extracted from real estate the company was already paying for.[^15] The second is data, through the Greggs App. By 2025 the app was being scanned in roughly a quarter of all transactions, with the company reporting that app-driven loyalty had become a central engine of repeat visits.1 The mechanism is simple — a "buy nine, get one free" loyalty loop — but the strategic value is profound. Every scan tells Greggs who is buying what, when, where, and how often, turning an anonymous cash transaction into a rich stream of customer data that informs everything from product development to where the next shop should open. The app is the closest thing a sausage-roll business has to a switching cost: once a customer is nine stamps deep, the rational move is to come back.

Four hidden engines, then — manufacturing, franchising, wholesale, and the digital-and-evening flywheel — all working in concert beneath the friendly shopfront. Running this increasingly complex machine requires a particular kind of leadership, and that brings us to the two people steering it today.

VIII. Current Leadership: The Currie & Hutton Era

The person running Greggs today did not arrive through the conventional retail-chief route of merchandising and store operations. Roisin Currie came up through people. She joined Greggs in 2010 as group people director — the head of human resources, in older language — at a company about to undertake the most disruptive industrial transformation in its history.[^13] That timing matters. The 2013 pivot, with its factory consolidations and store-format overhaul, was as much a human challenge as an operational one, and Currie was in the room for it. She rose to retail and property director, taking ownership of the shops and the estate, and in 2022 she was appointed chief executive of the entire company.[^13]

Currie's defining quality as a leader is a conviction that the workforce is the strategy, not a cost to be minimised. The clearest expression of this is the "Fresh Start" programme, which actively recruits people who face the steepest barriers to employment — including ex-offenders and others rebuilding their lives. This is not corporate window-dressing. The business logic is real: people given a genuine second chance by an employer who believed in them tend to stay, and in an industry where staff turnover is a chronic and expensive plague, loyalty and retention are a direct competitive advantage. It is also a clean continuation of the founding ethos — a company born serving working-class communities now creating opportunity within them. In 2025 Currie was awarded a CBE for services to the hospitality industry, formal recognition of both the commercial turnaround and the social-mobility agenda woven through it.[^13]

On the alignment question that long-term investors always ask — does the chief executive have skin in the game? — Currie holds a direct stake of roughly 0.03% of Greggs.[^15] Her total remuneration package runs to approximately £1.8 million, a structure built from a base salary, an annual bonus that can reach up to 150% of salary, and long-term incentive plans whose payouts are tied directly to multi-year targets for earnings per share and return on capital.[^15] The design is conventional but sound: the bulk of the upside is contingent on the metrics that actually matter to owners — profitable growth and disciplined use of capital — rather than on revenue for its own sake.

If Currie is the company's heart, Richard Hutton is its financial spine, and his tenure is remarkable for its sheer length. Hutton has served as chief financial officer since 2006 — a span of two decades — and his association with the company stretches back further still, making him a true Greggs veteran.5 He has been the financial mind behind essentially every major capital-allocation decision of the modern era, from integrating the regional acquisitions and Bakers Oven through to funding the current supply-chain expansion. Continuity of this kind in a CFO seat is rare and valuable: it means institutional memory of what worked, what didn't, and what every previous cycle of capital spending actually returned.

Hutton's recent challenge has been managing the largest capital-expenditure cycle in Greggs' history. To support the company's ambition of a far larger store estate, Greggs has been building out new mega-distribution hubs — major facilities at Derby and Kettering — to give the supply chain the capacity to feed a national network of thousands of shops. Capital expenditure peaked in 2025 at roughly £287.5 million, an enormous outlay for a company of Greggs' size, and the strategic question for investors is whether that spending front-loads years of future growth or simply weighs on returns.[^15] Hutton's stated discipline is to bring spending back down now that the peak has passed, steering capital expenditure toward roughly £200 million for 2026 as the big infrastructure projects complete.[^15] The pattern Hutton has run for years is a virtuous one when it works: invest heavily in capacity during the build phase, then harvest the operating leverage as the new capacity fills, generating excess cash that Greggs has historically returned to shareholders through ordinary and special dividends.

Hutton, like Currie, is aligned through a substantial personal shareholding backed by performance-based long-term incentives. In late 2025 he exercised and retained a significant portion of a 15,769-share award that vested under the company's long-term plan — the kind of "exercise and hold" behaviour that signals continued confidence rather than a cash-out.5

Two leaders, then: one who treats people as the engine of performance, one who treats capital as a resource to be deployed with patience and recovered with discipline. The question for the rest of this episode is whether the business they steer is genuinely defensible. For that, we turn to frameworks.

IX. Framework Analysis: Hamilton's 7 Powers & Porter's Five Forces

Strip away the brand affection and the cultural cachet, and ask the cold question a serious investor must ask: what actually stops a competitor from doing to Greggs what Greggs did to the high-street bakers it replaced? Hamilton Helmer's 7 Powers framework gives us a vocabulary for durable advantage, and Greggs possesses an unusually clean set of them.

The foundational power is scale economies, and for Greggs this is not abstract. The decision to consolidate production into a handful of giant, automated centres of excellence — the factory that makes millions of sausage rolls a week and freezes them for national distribution — drives the unit cost of manufacturing down to a level that a small independent bakery or a regional competitor cannot physically reach. This is the heart of the entire model. When you make sausage rolls by the million and your rival makes them by the hundred, your cost per unit is in a different universe, and that gap funds either fatter margins or lower prices, whichever the competitive situation demands. It is the power from which most of the others flow.

The second is what Helmer calls a cornered resource, and Greggs holds two. The first is its proprietary, temperature-controlled distribution fleet — the cold-chain logistics network that no rival can simply rent into existence. The second is its accumulated estate of prime locations, especially the travel-hub and forecourt leases secured through franchise partners, which occupy the high-footfall sites a latecomer would struggle to acquire at any price. These are assets that took decades and enormous capital to assemble.

The third, and the one the public feels most directly, is brand. Greggs has achieved the genuinely rare status of a national treasure — a brand that connotes trust, warmth, and what we might call unapologetic value. The strategic beauty of this particular brand is counter-cyclical: because Greggs is positioned as the smart, affordable choice, it tends to perform better when the economy weakens and consumers trade down from pricier lunch options. A recession that wounds premium competitors can actually send customers toward Greggs. Few brands have a moat that widens in a downturn.

The fourth is a modest but real switching cost, embodied in the app and its loyalty loop. It is not the iron lock-in of enterprise software, but the buy-nine-get-one-free mechanic and the accumulated convenience of a saved payment and order history create just enough friction to nudge a wavering customer back through the door rather than into the Pret next door.

Now flip to Porter's Five Forces, which examines not the company's powers but the structure of the industry it sits inside — and the picture is strikingly favourable.

The bargaining power of suppliers is low, and this is the direct dividend of vertical integration. Because Greggs makes most of its own food and buys its raw inputs — wheat, pork, coffee — in vast national volumes, it negotiates from a position of strength and can lock in multi-year hedging contracts to smooth out commodity volatility. It is not at the mercy of suppliers because, for most of its value chain, it is the supplier.

The bargaining power of buyers is low in practice, even though in theory a customer can eat absolutely anywhere. The reality is that no competitor matches Greggs on the specific axis that matters to its core customer: a freshly baked, hot lunch at its particular price-to-quality ratio. The customer has infinite choices and yet, for that specific need, no real substitute.

The threat of new entrants is extremely low, and this is perhaps the single most important point for a long-term investor. To replicate Greggs, a new entrant would have to build a national, vertically integrated cold-chain logistics network, construct industrial bakeries, and assemble thousands of prime locations — a multi-billion-pound capital barrier that no rational entrant would attempt. The moat here is not cleverness; it is the sheer, daunting cost of recreating the machine.

The threat of substitutes is moderate and is the force Greggs must watch most carefully. Supermarket meal deals and the giants of fast food — McDonald's chief among them — offer real alternatives for the lunchtime pound. Greggs' answer is product differentiation: hot, freshly baked food beats a cold, pre-packaged sandwich, and that sensory difference is the wall it defends.

Finally, the intensity of competitive rivalry is high. Greggs competes against Pret a Manger, the rapidly expanding bakery chain Gail's, Subway, and the entire supermarket food-to-go apparatus — and that field is getting more crowded, not less.2 But Greggs has carved out an insulated "value sweet spot." Pret and Gail's compete at a premium price point; the supermarkets compete on cold, packaged convenience. Greggs sits in the middle — hot, fresh, and cheap — a position that is genuinely hard to attack from either direction. Whether that sweet spot stays insulated as rivals expand is precisely the debate that defines the bull and bear cases.

X. Bear vs. Bull Cases

Every great business eventually runs into the same question: is the story still in its early innings, or is the easy growth already behind it? For Greggs, that question crystallises into a clean bull-versus-bear debate, and an honest investor has to hold both sides at once.

The bull case begins with a single number: the company's long-stated ambition of pushing well beyond its current estate toward a vision of around 3,500 shops.2 The argument is one of geographic whitespace. For all its national fame, Greggs remains under-penetrated in exactly the markets with the most people and the most spending power — the South of England, and London in particular, where the brand historically lagged, plus the travel hubs and forecourts that the franchise model is purpose-built to capture.2 If Greggs can do in the South what it long ago did in the North, the runway is years long.

The second pillar of the bull case is operating leverage from the supply chain. The enormous 2025 capital expenditure that built the Derby and Kettering hubs was, in this reading, the painful front-loaded investment that pays off for a decade.[^15] Those hubs were sized not for today's estate but for a much larger one. As store count climbs toward the 3,500 vision and capital expenditure falls back toward £200 million, the fixed cost of that new infrastructure spreads across far more shops and far more volume — and that is the classic recipe for margin expansion.[^15] You build the big factory once; you fill it for years.

The third pillar is daypart and channel expansion. The evening-trade push, the hot-food and sharing ranges, the growth of delivery, and the deepening digital loyalty loop all extract incremental revenue from real estate Greggs already controls.[^15] Every new occasion — breakfast, lunch, afternoon, dinner, the freezer aisle at home — is more sales per square foot without a corresponding increase in rent.

The bear case is just as coherent, and it has a memorable name: peak sausage roll.[^10] The first worry is saturation and cannibalisation. The drive toward 3,500 shops invites the very risk that has dogged other expansion-hungry chains — what we might call the Pret problem, where you open so many outlets in such close proximity that new shops simply steal sales from existing ones rather than generating fresh demand. At some point on the map, the next Greggs cannibalises the last Greggs, and like-for-like growth stalls even as the store count keeps rising.

The second bear worry is regulatory and cultural: the slow tightening of the screws around unhealthy food. Britain has been steadily building out restrictions on the promotion and advertising of products high in fat, sugar, and salt — the HFSS regime — and consumer awareness of ultra-processed foods has been rising in tandem. A pastry-and-savoury business is squarely in the firing line of both, and a sustained shift in either regulation or public sentiment could pressure demand for exactly the products that define the brand.

The third bear worry is the one that threatens the value model from underneath: cost inflation. Greggs' entire proposition rests on offering hot, fresh food cheaply, which means it operates on tight, value-led margins with limited room to raise prices without breaking the promise. Rising minimum wages — a structural reality for a large, labour-intensive employer — combined with commodity and energy volatility in pork, wheat, and power, all press on those margins simultaneously.2 Vertical integration cushions the blow better than rivals can manage, but it does not make Greggs immune. The bear's question is simple: what happens to a value brand when the cost of delivering value keeps climbing?

So which KPIs actually let an investor adjudicate this debate over time? Three matter above all. The first is like-for-like sales growth in company-managed shops — the single cleanest read on whether the core proposition is still winning customers organically rather than just adding stores. The second is net new shop openings, both directly operated and franchised, the truest gauge of how much of the 3,500-store runway is actually being converted. And the third is operating margin, the scoreboard on which the entire bull-versus-bear argument is settled — the place where supply-chain operating leverage and cost inflation fight it out in real numbers. Watch those three, and the rest of the noise mostly fades.

XI. Outro & Playbook Lessons

Step back from the sausage rolls and the celebrity feuds and the freezer aisles, and Greggs offers a handful of lessons durable enough to outlast any single quarter.

The first is that vertical integration can be a genuine moat. In an age that worships outsourcing and the asset-light model, Greggs went the other way — it bought the factories and the lorries — and that ownership is precisely what protects its quality, defends its margins through inflationary shocks, and lets it innovate at a speed competitors cannot match. Sometimes the most contrarian thing a company can do is own the boring, capital-heavy middle of its value chain.

The second is the power of self-aware brand marketing. Greggs never tried to be something it wasn't. It did not chase the premium positioning of Pret or Gail's. It embraced its identity as the value champion of the British high street and used humour, confidence, and cultural fluency to turn that identity into affection. The vegan sausage roll worked not because it was a health product but because it was funny — a brand secure enough to laugh at itself and invite the whole country in on the joke. Authenticity, it turns out, scales.

The third is the discipline of pragmatic M&A. Buying Bakers Oven at roughly £43,000 per shop — half the cost of building new — was a low-risk, highly accretive asset acquisition that bought Greggs decades of organic real-estate growth in a single stroke, by reading a forced seller's strategic motivation correctly and acting decisively.[^15] Great deals are usually not about paying a fair price for a great asset; they are about paying a cheap price because the seller's reasons for selling have nothing to do with the asset's worth.

From a man on a bicycle delivering yeast in 1939 to a £2-billion industrial, logistical, and digital food machine wrapped in a beloved national brand, Greggs stands as a masterclass in operational excellence and patient transformation — a company that grew up by getting bigger on the inside while staying exactly what it always was on the outside.

References

-

Greggs Q1 2026 Trading Update — London Stock Exchange, 2026-05-12 ↩

-

Can Greggs hold its own in the fiercely competitive food-to-go market? — The Grocer, 2025-07-15 ↩↩↩↩↩

-

Guess what's coming to ever-expanding Greggs — Financial Times, 2025-04-20 ↩↩

-

Greggs unveils new franchise partners in forecourts expansion — British Baker, 2024-11-12 ↩↩

-

Director/PDMR Shareholding: Richard Hutton — Investegate, 2025-11-04 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube