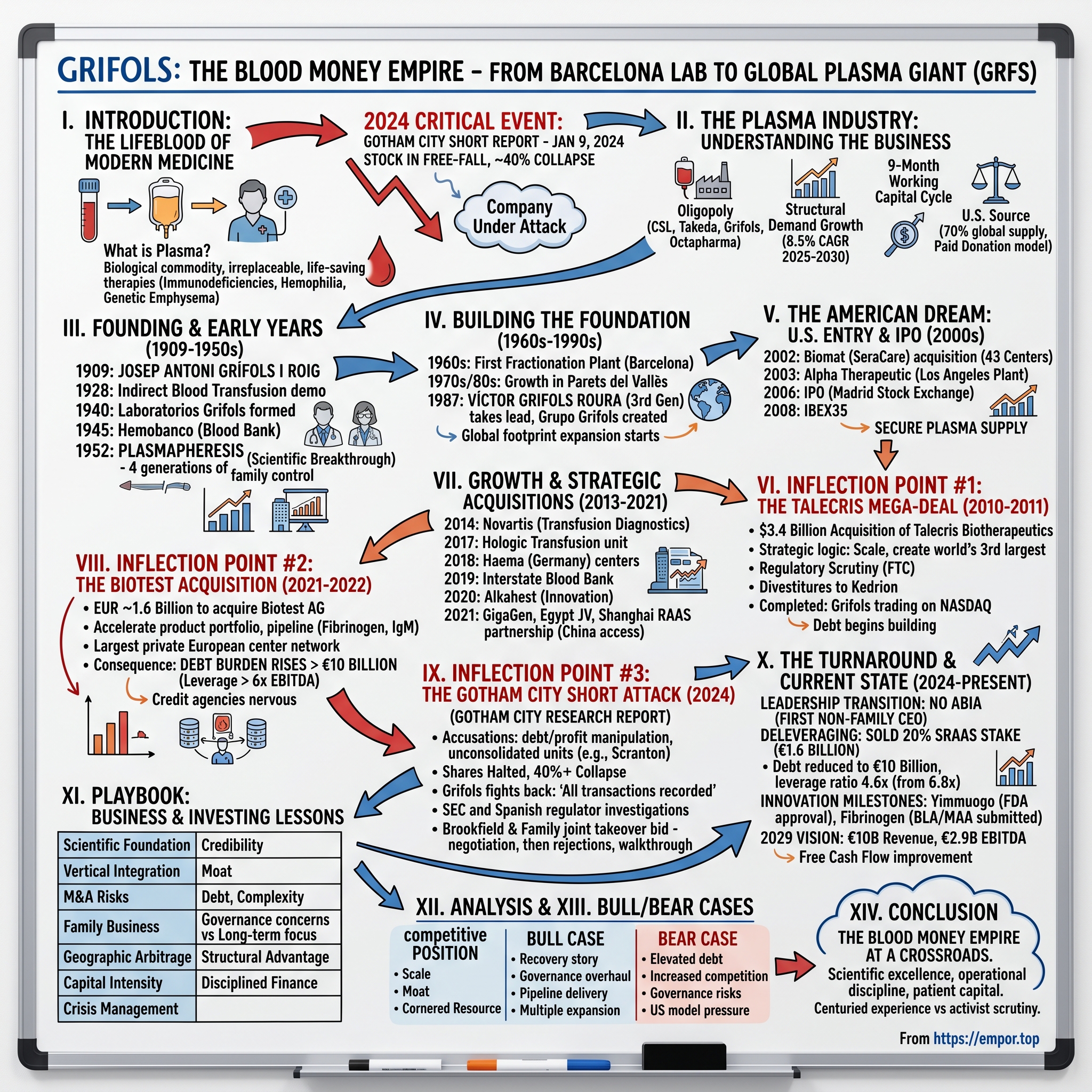

Grifols: The Blood Money Empire — From Barcelona Lab to Global Plasma Giant

I. Introduction: The Lifeblood of Modern Medicine

Picture the scene: It's January 9, 2024, on a cold Madrid morning. Trading screens across Europe flash crimson as Grifols, Spain's pharmaceutical crown jewel, enters free-fall. After a delayed trading start that stretched 90 minutes, the stock finally opened—down 40% in one of the most dramatic collapses in European healthcare history. In Barcelona's Grifols headquarters, executives scrambled to respond to a devastating report from an obscure New York short-seller named Gotham City Research, which accused the 115-year-old family company of manipulating its debt and profit figures.

But this is not a story about a company in decline. It's a story about one of the most remarkable family businesses in pharmaceutical history—and one of the most misunderstood industries on Earth.

Grifols is a global healthcare company that since 1909 has enhanced the health and well-being of people around the world. A leader in essential plasma-derived medicines and transfusion medicine, the company develops, produces and provides innovative healthcare services and solutions in more than 110 countries.

Here's what makes Grifols fascinating: human blood plasma—the straw-colored liquid that carries blood cells through your body—is one of the most valuable commodities on the planet. It cannot be synthesized, replicated, or manufactured in a lab. Every liter must come from a human donor. And from this biological raw material, companies like Grifols create life-saving therapies for some of the most devastating conditions known to medicine: primary immunodeficiencies, hemophilia, genetic emphysema, and neurological disorders.

A pioneer in the plasma industry, Grifols has the largest network of donation centers in the world, with approximately 400 centers across North America, Europe, Africa and the Middle East, and China through a partnership with Shanghai RAAS.

The economics are extraordinary. The global plasma fractionation market size was estimated at USD 35.79 billion in 2024 and is projected to reach USD 58.24 billion by 2030, growing at a CAGR of 8.5% from 2025 to 2030. Yet this is a market controlled by fewer than five major players—and Grifols commands one of the largest positions, making it both a defensive healthcare asset and a leveraged bet on the structural growth of immunology treatments.

This episode covers four generations of the Grifols family, from a Barcelona laboratory in 1909 to a NASDAQ-listed multinational. We'll explore transformational acquisitions that created billions in value—and billions in debt. We'll examine the ethical complexities of paid plasma donation, the scientific innovations that created an industry, and the existential crisis of 2024 when everything the company had built seemed on the verge of collapse.

The plasma industry offers something rare in modern business: an irreplaceable product with structural demand growth, massive barriers to entry, and only a handful of companies with the capability to serve the market. That combination makes Grifols one of the most interesting—and misunderstood—healthcare companies in the world.

II. The Plasma Industry: Understanding the Lifeblood Business

Before diving into Grifols' story, understanding what makes the plasma industry so unusual—and so defensible—is essential.

Plasma is the liquid portion of blood, the pale-yellow fluid that remains after removing red cells, white cells, and platelets. It contains hundreds of proteins with vital therapeutic applications. But here's the critical insight: these proteins cannot be manufactured synthetically. Despite decades of research and billions in investment, no one has found a way to replicate the complexity of human plasma proteins in a laboratory.

Plasma-based drugs are vital for many forms of therapy. Only a few providers are active in the markets since the production and approval of such products is very time consuming and cost intensive.

The therapies derived from plasma are among the most essential in medicine. Grifols produces immunoglobulins for patients with primary and secondary immunodeficiencies, albumin for intensive care and liver disease patients, Factor VIII for hemophilia A, Alpha-1 antitrypsin for genetic emphysema, and specialized hyperimmune immunoglobulins that prevent rabies, tetanus, and other diseases after exposure.

The production process—called plasma fractionation—transforms raw plasma into finished pharmaceutical products through a series of complex purification steps. It takes approximately 9 months from plasma donation to final product, creating enormous working capital requirements. Immunoglobulins held 63.21% of the plasma fractionation market share in 2024, reflecting their broad therapeutic footprint.

What makes this industry structurally fascinating is the raw material constraint. In particular, manufacturers depend on blood plasma donations from the general public, which are insufficient in Europe as a whole.

This creates an extraordinary geographic arbitrage. Just over 3 million people in the U.S.—predominantly low-income adults—provided around 70% of the world's plasma in 2019. That's because the U.S. is one of only five countries worldwide that allows pharmaceutical corporations to compensate donors, and it permits relatively high donation frequencies.

The paid-donation model is ethically controversial, raising questions about exploitation of economically vulnerable populations. "There's a lot of the controversy around plasma versus blood donation is that it preys on the poor." Yet without the U.S. supply system, there would simply not be enough plasma to meet global medical demand.

The United States is an outlier for other reasons as well, including the frequency of donations that are allowed in the United States, which is two per week, separated by at least two days. Those are the guidelines. Whereas most other advanced countries that do allow this, it's usually once a week or sometimes even every other week.

This dependence on U.S. plasma creates both opportunity and risk for companies like Grifols. On one hand, controlling collection infrastructure provides significant competitive advantage. On the other, it creates exposure to U.S. regulatory changes and public health dynamics—as the COVID-19 pandemic demonstrated when donation volumes collapsed temporarily.

The market structure reflects these dynamics. With nearly 33% of the total, CSL Behring held the highest market share in 2021. The company operates over 300 plasma collection centers and is focused on boosting its R&D capabilities. Grifols accounted for a share of 17–19% of the plasma fractionation market in 2022.

The competitive landscape presents a classic oligopoly structure: CSL Behring (Australia) leads with approximately one-third of the market, followed by Takeda (Japan), Grifols (Spain), and Octapharma (Switzerland), with smaller players like Kedrion rounding out the field. These five companies control the vast majority of global plasma production—and maintaining that position requires massive capital investments in collection infrastructure, fractionation capacity, and regulatory capabilities.

For investors, the plasma industry offers an unusual combination: essential therapies with growing demand, structural supply constraints that limit competition, and a competitive moat built on decades of infrastructure investment and regulatory expertise. The question is whether Grifols' debt-fueled expansion strategy has positioned it to capture this growth—or created excessive financial risk.

III. Founding & Early Years: The Birth of a Scientific Legacy (1909–1950s)

The story begins not in a gleaming laboratory or corporate boardroom, but in a modest Barcelona clinic during the twilight of Spain's constitutional monarchy. Grifols began in 1909 when hematologist and scientist Josep Antoni Grífols i Roig founded a clinical analysis laboratory in Barcelona: the Instituto Central de Análisis Clínicos, Bacteriológicos y Químicos, a precursor to Laboratorios Grifols.

Over a century ago, doctor and homeopath Josep Antoni Grifols Morera enthused his son with a passion for science in the family's Barcelona home. It was here that young Josep Antoni Grifols i Roig later built his laboratory, and ultimately his business, with the help of his own sons.

To appreciate what Grifols i Roig achieved, consider the state of blood medicine in 1909. Blood transfusion was essentially experimental—dangerous, unreliable, and limited to direct arm-to-arm transfers between donor and patient in the same room. The concept of stored blood was barely understood. Sterility was a constant battle against infection and contamination.

In Spain, Grífols i Roig patented the first instrument for carrying out indirect blood transfusions, the transfusion flebula. This innovation allowed blood to be collected, stored temporarily, and transferred without requiring the donor and recipient to be physically present together—a fundamental breakthrough that would eventually enable modern blood banking.

In the 1920s Josep Antoni took full charge of the laboratory, which was mostly dedicated to clinical analysis and the manufacture of vaccines at the time. On 23rd May 1928, Dr. Grifols i Roig demonstrated for the first time in Spain that blood could be donated, stored, and then transferred to a patient without the donor and recipient both being present.

The Spanish Civil War (1936-1939) and World War II created enormous demand for blood products while simultaneously destroying much of Europe's medical infrastructure. In this challenging environment, the Grifols family took a transformative step.

The formal establishment of Laboratorios Grifols in 1940 by Josep Antoni Grífols i Roig and his sons, Josep Antoni Grífols i Lucas and Víctor Grífols i Lucas, marked a significant turning point. The company's founding by three family members—father and two sons, spanning two generations—established a pattern that would persist for over eight decades.

By 1940, amid the postwar recovery, Grifols i Roig and his sons, Víctor and Josep Antoni Grifols i Lucas, formally founded Laboratorios Grifols, expanding into plasma processing and freeze-dried products. In 1945, they launched Hemobanco, Spain's inaugural private blood and plasma bank, which utilized freeze-drying techniques to preserve donations and one of the earliest such facilities in Europe.

Then came the scientific breakthrough that would eventually define the company's destiny. In 1952, for the first time in the world, the results of a systematic application of the plasmapheresis technique in humans was published in the British Medical Journal thanks to a study led by Josep Antoni Grífols i Lucas.

Plasmapheresis revolutionized plasma collection by allowing donors to give plasma while retaining their red blood cells. Plasmapheresis is a procedure which allows blood cells and platelets to be injected into a patient after the plasma has been extracted from the original blood donation. Because the body takes only two days to regenerate its plasma compared to 90 for whole blood, plasma donations can be more frequent and provide larger quantities of the fluid without putting the donor's health at risk.

This technique—developed by a small Barcelona laboratory and published in the world's most prestigious medical journal—remains the foundation of the global plasma industry today. It enabled the shift from whole-blood donation to dedicated plasma collection, creating the supply dynamics that would fuel an entire pharmaceutical industry.

The 1952 publication in the British Medical Journal established Grifols' scientific credibility on the global stage. But commercial success would require something more: the ability to scale production, enter international markets, and integrate vertically from collection to finished products. That transformation would take decades—and multiple generations of Grifols family leadership.

IV. Building the Foundation: Growth Under Family Control (1960s–1990s)

The decades following the plasmapheresis breakthrough were years of patient construction, as the Grifols family built the industrial and organizational infrastructure needed to compete globally.

Grifols opens its first plasma fractionation plant in Barcelona. This marked the transition from research to manufacturing—from discovering how to collect plasma to actually processing it into therapeutic products at scale.

The 1970s and 1980s brought significant expansion. Grifols opens a new production plant in Parets del Vallès (Barcelona). The plant includes sections for plasma fractionation, manufacture of parenteral solutions, and scientific instrumentation.

The generational handoff—always a crucial test for family businesses—came in the late 1980s. Control of the company is handed down to the entrepreneur Víctor Grifols Roura, a process that finishes in 1987. The holding company Grupo Grifols is created, uniting the commercial company and clinical diagnostic, plasma-derived medicines, and parenteral solutions production companies.

Víctor Grifols Roura, grandson of the founder and son of one of the original co-founders, represented the third generation of family leadership. His tenure would span the company's transformation from a Spanish pharmaceutical company into a global plasma powerhouse.

A pioneer in the biomedical industry, he led the company's growth from its roots in Barcelona to becoming an international leader in the sector. After earning degrees in pharmacy and chemical sciences, he joined the company founded by his father, Dr. Josep Antoni Grífols i Roig, and held key positions such as Technical Director, CEO, and, later, Chairman of the company.

International expansion began in earnest in the late 1980s. The company opened its first subsidiary in Portugal in 1988, marking the beginning of what would become a global footprint spanning more than 110 countries.

Yet despite these achievements, Grifols remained fundamentally a European company through the 1990s—respected for its scientific heritage but lacking the scale to compete with global giants like Baxter or emerging Australian powerhouse CSL. The company needed something transformational.

That transformation required access to the single most critical resource in the plasma industry: American donors. The United States, with its unique regulatory framework permitting paid plasma donation, supplied the vast majority of global plasma. Any company serious about becoming a global leader would need a significant American presence.

The challenge for a family-controlled Spanish company was how to achieve that expansion without losing control or taking on excessive financial risk. The answer would come through a series of increasingly ambitious acquisitions that would fundamentally reshape Grifols—and ultimately create both enormous value and existential danger.

V. The American Dream: U.S. Entry & IPO (2000s)

The new millennium brought a strategic pivot that would define Grifols' future. The family leadership understood that controlling plasma collection infrastructure—particularly in the United States—was essential for long-term competitive positioning.

Grifols acquired its first group of plasma donation centers (43 in the U.S.) in 2002, taking over the company SeraCare, now known as Biomat.

Forty-three centers represented a substantial foothold, but building a globally competitive position would require far more. The following year, Grifols acquired Alpha Therapeutic Corporation-Mitsubishi, including its plasma fractionation plant in Los Angeles, California.

The Alpha Therapeutic acquisition was strategically significant beyond its collection centers. A Los Angeles fractionation plant gave Grifols manufacturing capability on American soil—crucial for serving U.S. healthcare customers and reducing dependence on transatlantic logistics.

These acquisitions established the template that would guide Grifols' expansion strategy for the next two decades: use acquisitions to build vertical integration across collection, manufacturing, and distribution, with particular emphasis on securing plasma supply in the United States.

Going public became essential to fund this expansion. Grifols began trading on the Madrid stock exchange in 2006 and was listed on the IBEX35, the exchange's benchmark index, in 2008.

The Madrid listing provided access to public equity markets while maintaining the dual-class share structure that kept control firmly in family hands. The Grifols family retained voting control through B shares, while public investors could participate in the company's growth through non-voting shares.

This structure—common among European family businesses but controversial among governance advocates—allowed the family to pursue long-term strategies without short-term market pressure. It also meant that public shareholders were essentially along for the ride, with limited ability to influence management or strategy.

By the late 2000s, Grifols had established a meaningful U.S. presence and demonstrated its ability to integrate acquisitions. Revenue was growing, margins were healthy, and the family had maintained control while accessing public capital.

But the company remained the fourth-largest player in a market dominated by CSL, Baxter (which would later spin off its plasma business to Shire, subsequently acquired by Takeda), and Talecris Biotherapeutics. To join the top tier, Grifols would need to make a transformational bet.

That bet would come in 2010—and it would nearly double the company's size overnight.

VI. INFLECTION POINT #1: The Talecris Mega-Deal (2010–2011)

In June 2010, Grifols announced a deal that stunned the plasma industry: a $3.4 billion acquisition of Talecris Biotherapeutics, the North Carolina-based plasma company that had been separated from Bayer in 2005.

On June 6, 2010, Grifols agreed to acquire Talecris for approximately $3.4 billion in stock and cash. Grifols, headquartered in Barcelona, Spain, develops and manufactures human blood plasma-derived products, with facilities in Barcelona and Los Angeles. Talecris is based in Research Triangle Park, North Carolina, and also specializes in the development, manufacture, and worldwide sale of blood plasma-derived products.

The strategic logic was compelling: combining Grifols and Talecris would create the world's third-largest plasma company, with leading positions in key products and dramatically enhanced scale in the U.S. market.

But the deal immediately attracted regulatory scrutiny. According to the FTC, Grifols and Talecris currently have approximately 8.4 percent and 22.8 percent of the U.S. Ig market, respectively, and their merger would leave only three meaningful manufacturers with nearly all U.S. Ig sales. In the market for albumin, the companies have U.S. market shares of approximately 13 percent each, and the acquisition would leave only four significant competitors. In the market for pdFVIII, Grifols and Talecris have 23 percent and 3.6 percent of the U.S. market, and after their merger there would be only three main competitors.

The Federal Trade Commission challenged the merger as anticompetitive. The FTC required Grifols, S.A., a manufacturer of plasma-derived drugs, to make significant divestitures as part of a settlement allowing Grifols to acquire a leading plasma-derived drug manufacturer, Talecris Biotherapeutics Holdings Corp. It resolves FTC charges that Grifols' proposed acquisition of Talecris would be anticompetitive and would violate federal antitrust laws.

The required divestitures were substantial. The FTC's order requires Grifols to sell the Talecris fractionation facility in Melville, New York, and Grifols' plasma collection centers in Mobile, Alabama, and Winston-Salem, North Carolina, to Kedrion S.p.A. Kedrion, an Italian plasma company, became a new entrant in the U.S. market as a result.

According to the FTC, Grifols and Talecris currently have approximately 8.4 percent and 22.8 percent of the U.S. plasma derived products market, respectively, and their merger would have left only three meaningful manufacturers with nearly all U.S. sales. The other two major manufacturers of plasma derived products are Baxter and CSL.

After a grueling year of regulatory review, the deal finally closed. Barcelona-based blood-plasma products company Grifols said it completed its acquisition of Talecris Biotherapeutics, based in Research Triangle Park, N.C., after the Federal Trade Commission approved the deal earlier this week.

In 2011, Grifols acquired the North American company Talecris Biotherapeutics, making Grifols the third-largest manufacturer of plasma-derived medicines in the world.

The acquisition transformed Grifols' market position. With the acquisition of Talecris Biotherapeutics in 2011, Grifols began trading on the NASDAQ. Dual listing in both Madrid and New York gave the company access to U.S. investors while enhancing its profile as a global healthcare company.

The integration generated substantial synergies from combining the companies' plasma collection networks, optimizing manufacturing operations, and consolidating sales and marketing functions. But the deal also required significant debt financing—beginning a pattern of leveraged expansion that would eventually create severe financial strain.

The Talecris acquisition demonstrated both Grifols' strategic ambition and its ability to execute complex transactions. It also established a precedent: growth through M&A, funded substantially by debt, with family control maintained throughout.

VII. Growth & Strategic Acquisitions (2013–2021)

The post-Talecris years brought continued expansion across multiple fronts, as Grifols sought to diversify its portfolio, strengthen its innovation capabilities, and extend its geographic reach.

Grifols acquired Novartis' blood transfusion diagnostics unit, based in Emeryville, California, in 2014. It was a part of Chiron, which had been acquired by Novartis in 2006. This acquisition expanded Grifols beyond plasma-derived medicines into the complementary diagnostics market, where blood banks and transfusion centers require sophisticated testing equipment.

Grifols grew its transfusion medicine business with the acquisition of Hologic's transfusion unit in 2017, leading the company's creation of reagents and instrumentation based on NAT (nucleic acid testing) technology.

Collection infrastructure remained a priority. In 2018, Grifols acquired the German company Haema and its network of donation centers and, in 2019, Grifols grew its network of donation centers further with the addition of Interstate Blood Bank Inc.

Innovation investments accelerated through partnerships and acquisitions. Following a major equity investment in 2015, Grifols acquired the remaining shares of Alkahest in 2020 to help enhance the company's discovery research and development to identify therapies based upon an understanding of the human plasma proteome.

In 2021, the company acquired the remaining capital of GigaGen, a U.S. biotechnology company specialized in recombinant polyclonal antibodies—a potential next-generation technology that could complement or eventually replace some plasma-derived products.

Geographic expansion continued as well. In 2020, Grifols signed an agreement with Egypt's National Service Projects Organization to establish a joint venture building the first integrated platform for sourcing and producing plasma medicines in Africa and the Middle East—demonstrating the company's ambition to extend beyond its traditional markets in North America and Europe.

But the most significant strategic move of this period involved China. Grifols built a partnership with Shanghai RAAS, one of China's largest plasma companies, creating a channel for albumin distribution into the world's largest single-country market for plasma products. China accounts for over 50% of global albumin consumption, making this relationship strategically vital.

By 2021, Grifols had transformed from a regional Spanish company into a genuinely global player with operations spanning collection, manufacturing, diagnostics, and research. The company operated approximately 400 plasma donation centers worldwide, maintained leading positions in key product categories, and had established footholds in high-growth emerging markets.

Yet this growth came at a cost. Each acquisition added to the debt burden, and the integration challenges grew more complex. The family had maintained control, but the balance sheet was increasingly stretched. Then came an opportunity that seemed too good to pass up—but would prove nearly fatal.

VIII. INFLECTION POINT #2: The Biotest Acquisition (2021–2022)

In September 2021, Grifols announced its second transformational deal: the acquisition of Biotest AG, a German plasma company with deep European roots and a promising innovation pipeline.

Grifols has agreed to acquire the entire share capital of Tiancheng (Germany) Pharmaceutical Holdings AG - a German company that holds 89.88% of the ordinary shares and 1.08% of the preferred shares of Biotest AG- for EUR 1,091 million.

The transaction values Biotest's capital at approximately EUR 1,600 million (Equity Value) and its market value at EUR 2,000 million (Enterprise Value).

Founded in 1946, Biotest AG specializes in hematology, clinical immunology, and intensive care medicine.

The strategic rationale was multi-dimensional. The acquisition of Biotest AG enables Grifols to accelerate and expand its product portfolio, increase the availability of plasma therapies for patients, own the largest private European network of plasma centers with 87 centers, and drive revenue growth and margin expansion.

Furthermore, it enables Grifols and Biotest to jointly increase the global availability of plasma-derived therapies for the benefit of patients, while allowing Grifols to strengthen its position as the industry's leading European company by improving and complementing its operational, industrial and scientific capabilities: Owning the largest private European network of plasma centers (87 centers: 29 Biotest and 58 Grifols). Leading fractionation capacity with more than 20 million liters of plasma annually.

Beyond scale, Biotest brought critically important pipeline assets. As part of a broader pipeline, Biotest is leading clinical trials on plasma-derived fibrinogen (BT-524) to treat congenital and acquired disorders. These include the Adjusted Fibrinogen Replacement Strategy (AdFIrst) study in patients with high blood loss during spine surgery and abdominal surgery for treatment of pseudomyxoma peritonei (PMP). Biotest is also conducting a clinical trial on plasma-derived IgM concentrated (Trimodulin, BT-588) for the treatment of patients with severe community-acquired pneumonia (sCAP).

The fibrinogen program would later prove especially valuable—but that vindication lay years in the future.

The merger was cleared within the one-month deadline of first-phase merger control. Plasma-based drugs can be replaced by biotechnologically produced pharmaceuticals in a few cases only. Nevertheless, there will still be sufficient alternative providers to choose from after the merger since in addition to Grifols and Biotest, the leading company CSL Behring (Australia/USA), Octapharma (Switzerland) and Takeda (Japan), among others, are active in the markets.

Grifols today announced the completion of the acquisition of 100% of the share capital of Tiancheng (Germany) Pharmaceutical Holdings AG, a German company that holds 89.88% of the ordinary shares and 1.08% of the preferred shares of Biotest AG, a European healthcare company specialized in innovative hematology and clinical immunology. Grifols completed the acquisition of Biotest on April 25, 2022.

But the Biotest deal had a significant consequence that the optimistic projections obscured: it dramatically increased Grifols' already substantial debt burden. Combined with the working capital demands of the plasma business—where inventory takes months to convert into finished products—the balance sheet became increasingly stretched.

By turning to an outsider to run the business, the family is attempting to reverse its fortunes and spur a rebound in its shares, which skyrocketed in the decade to 2020 before tumbling 40% on concerns over the slump in business and Grifols SA's debt-fueled acquisition binge in the US and Asia.

The company's debt following the two major acquisitions exceeded €10 billion—an enormous sum for a business generating revenues of approximately €6.5 billion. Leverage ratios pushed above 6x EBITDA, levels that made both investors and credit agencies increasingly nervous.

Still, the family maintained confidence. The synergies would materialize. The pipeline would deliver. Cash flows would improve. Debt would come down.

Then came January 2024.

IX. INFLECTION POINT #3: The Gotham City Short Attack Crisis (2024)

The crisis arrived without warning. On January 9, 2024, Gotham City Research—a New York-based short-seller with a history of targeting European companies—published a devastating report accusing Grifols of manipulating its financial statements.

New York-based Gotham accused Grifols of manipulating its debt and profit figures by consolidating earnings of units it doesn't control.

After the report, Grifols shares were halted in early European trading on Tuesday as the opening auction saw a huge trading imbalance for almost 90 minutes, with millions of shares on offer and little buying interest. Once the stock finally opened more than 40% lower, it immediately began pushing higher, rallying as much as 34% from an intraday low.

The same day Grifols dropped as much as 43%, General Industrial Partners reduced its short position in the blood plasma company to 0.06% from 0.6%, a regulatory filing showed.

The market reaction was brutal, and the trading pattern outraged many investors. "This is wild and people are really not happy with Gotham's behavior," said Mathias Lascar, sales trader at Makor Securities. "We see investors saying: 'you can't say it's worthless, and buy it back at 8 euros.'"

Haema and Biotest Pharmaceuticals Corp., two businesses Grifols acquired in 2018, are owned by Scranton Enterprises BV, an investment vehicle controlled by former executives of the firm including members of the founding family.

Grifols immediately fought back. The Spanish company's shares rose as much as 13% in Madrid trading on Wednesday as the Barcelona-based company pushed back against the Gotham allegations. It said all the transactions mentioned in the short seller's report were recorded and presented to regulatory authorities in Spain and the US. "There's no new information that can be considered hidden," Grifols said in a filing. The company also said its board fully backs Chief Executive Officer Thomas Glanzmann after Gotham questioned his independence from the family that controls Grifols. In a statement, it threatened legal action against Gotham "for the significant financial and reputational damage" done to the company and its stakeholders.

Grifols SA sued Gotham City Research over a report alleging the company has overstated profit and misstated its accounting.

"Unlike other short sellers, defendants crossed the line with their attack on Grifols by knowingly making false and misleading statements in furtherance of a single illegal purpose: to manipulate the value of Grifols' stock for their own monetary gain," Grifols said in its suit.

The legal battle proceeded through U.S. courts with mixed results. But not everything in Grifols' lawsuit will be heard. The court dismissed its accusations of unjust enrichment and unlawful interference, stating that many of Gotham's remarks were expressions of opinion rather than verifiable falsehoods. In short, the judge found that much of the report was protected by the First Amendment.

Gotham City, for its part, welcomed the partial dismissal. In a statement, the firm said it was pleased that "the vast majority of Grifols' claims" had been thrown out. It defended its report as a protected form of analysis, adding: "We remain confident in the integrity of our research and stand by our work."

Regulatory investigations followed. The U.S. Securities and Exchange Commission looked into the matter but ultimately took no enforcement action. Spanish regulators initiated their own proceedings, targeting both Gotham City and Grifols itself.

In the chaos, a potential exit emerged. Brookfield and the Grifols family "have reached an agreement to evaluate a possible joint takeover bid to acquire all" the shares of the company and take it private, the Barcelona-based firm said in a regulatory filing Monday.

Brookfield and the Grifols family, who are working together to potentially take the company private, have yet to present a formal offer to the Grifols board and are waiting to complete their due diligence, the people said. Any proposal could give the company an equity value of around €8 billion ($8.9 billion), the people said.

Brookfield Asset Management is asking banks to line up about €9.5 billion ($10.6 billion) of debt for its potential take-private deal for Spanish pharmaceutical producer Grifols SA, according to people with knowledge of the matter.

But negotiations dragged on for months. In November 2024, Brookfield made a formal offer. Grifols' board of directors on Tuesday rebuffed Brookfield's potential buyout offer, recommending management reject the non-binding bid that it argues "significantly undervalues the company's fundamental prospects and its long-term potential."

Brookfield, which telegraphed interest in the acquisition earlier this week, suggested it would pay 10.50 euros per A share and 7.62 euros per B share in the company, valuing Grifols at 6.45 billion euros (about $6.8 billion) overall, according to a securities filing.

Brookfield Asset Management Ltd. is preparing to walk away from a plan to acquire Grifols SA over disagreements on valuation. The Spanish company's billionaire founding family said it won't support any new bid to take its namesake drug-maker private. New York-based Brookfield decided to end months of negotiations, which were disclosed publicly in July, after failing to reach an agreement with the board of Grifols on the price, according to people familiar with the matter.

The Gotham attack and failed Brookfield negotiation marked perhaps the most turbulent period in Grifols' 115-year history. The stock had lost billions in market value. The family's control was being questioned. The debt burden loomed larger than ever.

Yet beneath the chaos, something else was happening: operational execution was actually improving.

X. The Turnaround & Current State (2024–Present)

While the headlines screamed crisis, Grifols' management was quietly executing a turnaround that would eventually vindicate the company's fundamental strategy.

Leadership transition played a crucial role. Raimon Grifols and Víctor Grifols Deu transfer their respective responsibilities to Abia and will remain as advisors in a transition period until May 31, 2024. The moves conclude a meticulously planned corporate governance evolution that began in 2022 to separate ownership from company management.

José Ignacio (Nacho) Abia Buenache has been serving as Grifols Chief Executive Officer since April 2024 and as board member since February of the same year. Prior to joining the company, he was President and Chief Executive Officer of Olympus Corporation of the Americas for more than a decade, based in Pennsylvania. Concurrently, he held senior executive roles at Olympus Corporation, including Executive Officer and Chief Operating Officer (COO) and Chief Strategy Officer (CSO). He brings more than two decades of experience in the Medical Technology and Life Sciences industries, having spent equal time in both the United States and Europe.

The appointment of a professional CEO from outside the family—the first in company history—represented a significant governance evolution. Only CEO Nacho Abia will have executive functions for the company, a change that follows a swift and successful transition. The move further strengthens the company's corporate governance, marking a clear separation between the Board and the daily management of Grifols, and concludes a long-term transition plan. The change was approved by the Board and is effective immediately. It is the final step of a long-term management transition plan initiated in 2022.

Deleveraging became the top priority. Through a share purchase agreement Grifols has sold a 20% equity stake in SRAAS to Haier Group for RMB 12.5 billion (approximately EUR 1.6 billion). Grifols and SRAAS extend their exclusive albumin distribution agreement over the next 10 years, and SRAAS has the option to prolong it through 2044.

The €1.6 billion from the SRAAS transaction—completed in June 2024—went entirely toward debt reduction. Grifols retains a significant 6.58% economic stake in SRAAS as well as a seat on its Board of Directors.

Financial results began to demonstrate the turnaround. Key financial highlights include a 10.3% increase in full-year revenue to EUR 7,212 million, with a notable 13.6% growth in the fourth quarter. Adjusted EBITDA rose by 19% in Q4, reaching EUR 526 million, and the full-year adjusted EBITDA was EUR 1,779 million. Net profit saw a significant improvement, almost tripling to EUR 157 million for the year.

Leverage ratio in 2024 declined from 6.8x in the first quarter of 2024 to 4.6x by the end of 2024 (4.5x at constant currency).

The leverage ratio improvement—from 6.8x to 4.6x in a single year—demonstrated the combined impact of EBITDA growth, the SRAAS proceeds, and improved working capital management.

Innovation milestones added to the positive momentum. Global healthcare company, Grifols, announced on June 17, 2024 that its subsidiary Biotest has garnered its first FDA approval with the intravenous immunoglobulin (Ig) therapeutic, Yimmugo, which Grifols hopes to launch commercially in the United States in the second half of 2024.

BT524 will likely enter regulatory authorization processes in Q4 2024 starting in Europe and the United States. It would be the first FC approved for an AFD indication in the U.S. in a global market with an estimated potential of USD 800 million.

The fibrinogen program advanced steadily. Grifols today announced it has submitted a Biologics License Application (BLA) for its new potential fibrinogen treatment to the United States Food and Drug Administration (FDA). The European equivalent, a Marketing Authorization Application (MAA), was submitted for several countries in October 2024. Grifols expects to begin treating patients in Europe starting in the second half of 2025, with rollout in the U.S. planned for the first part of 2026.

Most recently, The new therapy, commercialized as Prufibry® in Germany, is approved for both congenital and acquired fibrinogen deficiency and is expected to be available to patients in Germany by the end of 2025. Germany is the first European country to grant marketing authorization for the company's fibrinogen concentrate, following a decentralized regulatory procedure with Austria and Spain expected to follow in 2026.

The company laid out ambitious long-term targets. Grifols will focus on accelerating the execution of its strategic plan, stressing financial discipline, operational excellence, innovation, cash flow improvement and deleveraging. By 2029, halfway through its 10-year ambition, Grifols forecasts revenue of EUR 10 billion, EBITDA of EUR 2.9 billion and cumulative cash flow pre-M&A of EUR 3.5+ billion.

The latest results showed continued progress. Group net profit increased to EUR 177 million, close to 4x the figure reported in H1 2024. Free cash flow before M&A improved by EUR 182 million year on year. Leverage ratio decreased to 4.2x, with liquidity standing at EUR 1.4 billion.

The dividend, suspended since the Biotest acquisition, returned. The company declared a EUR 0.15 per share dividend payment supported by continued underlying earnings and free cash flow generation momentum.

What had seemed like an existential crisis eighteen months earlier had transformed into a compelling recovery story. The debt remained elevated but manageable. Cash flows were improving. The pipeline was delivering. And family control had been maintained while bringing in professional management.

XI. Playbook: Business & Investing Lessons

Grifols' 115-year journey offers several insights for business observers and investors:

The Scientific Foundation Matters

The 1952 plasmapheresis publication in the British Medical Journal established credibility that persisted for decades. Grifols' scientific heritage—spanning four generations of family leadership—created trust with regulators, healthcare providers, and patients that could not be easily replicated. First-mover advantages in industries with long regulatory approval cycles can persist for generations.

Vertical Integration Creates Moats

By controlling collection, fractionation, and distribution, Grifols insulated itself from raw material volatility and created barriers that new entrants cannot easily overcome. Building approximately 400 plasma centers requires billions in capital, years of regulatory approvals, and operational expertise that competitors simply cannot acquire quickly.

M&A as Growth Engine—With Risks

Talecris transformed Grifols from regional player to global powerhouse. Biotest added critical pipeline assets and European infrastructure. But each acquisition added debt, integration complexity, and execution risk. The strategy worked—until it didn't, during the 2024 crisis when leverage became existential.

Family Business Dynamics Cut Both Ways

Family control enabled long-term strategic thinking that public shareholders might never have tolerated—such as maintaining high R&D spending during difficult periods or pursuing acquisitions that diluted near-term returns. But it also created governance concerns that short-sellers exploited, and raised questions about related-party transactions that damaged credibility.

Geographic Arbitrage Can Be Structural

The U.S. paid-donation model creates a regulatory moat around American plasma supply. Companies without significant U.S. collection infrastructure simply cannot compete for global immunoglobulin demand. This advantage is unlikely to change given the ethical complexity of paid donation and Europe's insufficient voluntary supply.

Capital Intensity Requires Disciplined Finance

Nine-month inventory cycles, massive collection infrastructure, and specialized manufacturing facilities create enormous working capital requirements. Managing leverage through cycles is essential—and Grifols learned this lesson painfully during the 2024 crisis.

Crisis Management Matters

The Gotham attack could have destroyed Grifols had management panicked. Instead, the company fought back legally while simultaneously executing operational improvements. The Brookfield negotiation provided optionality without giving away control. And the governance changes—bringing in professional management while maintaining family oversight—addressed legitimate concerns while preserving strategic continuity.

XII. Analysis: Competitive Position and Investment Framework

Porter's Five Forces Applied to Grifols

Threat of New Entrants: LOW

Building a competitive plasma business requires billions in capital, decades of regulatory expertise, and an established collection network. The approximately 400 centers that Grifols operates took decades to build. New entrants face massive fixed costs, long approval timelines for fractionation facilities, and the challenge of recruiting donors in an established market. The only realistic path to scale is through acquisition—but few attractive targets remain, and existing players have deep pockets for competing bids.

Bargaining Power of Suppliers: LOW-MODERATE

The primary "suppliers" are plasma donors, who have limited bargaining power individually. However, donor recruitment costs have increased as competition for suitable donors intensifies. Regulatory constraints on donation frequency and location create local monopolies for established centers.

Bargaining Power of Buyers: MODERATE

Hospital systems and healthcare providers are sophisticated purchasers, often negotiating through group purchasing organizations. But plasma-derived medicines have limited substitutes for most indications, and switching between suppliers creates regulatory and clinical complications. Payer concentration in the U.S. creates some pricing pressure, but the essential nature of these therapies provides protection.

Threat of Substitutes: LOW-MODERATE

Recombinant alternatives have captured some market share in coagulation factors, and emerging gene therapies may eventually reduce demand for certain plasma products. But immunoglobulins—the largest product category—have no synthetic alternatives for most indications. The complexity of plasma proteins makes full substitution unlikely for decades.

Competitive Rivalry: MODERATE-HIGH

Five major players compete intensively for market share, but rational pricing has generally prevailed given the oligopoly structure and high fixed costs. Capacity additions create periodic overcapacity, but structural demand growth (8-9% annually for immunoglobulins) typically absorbs new supply.

Hamilton's 7 Powers Framework

Scale Economies: Significant. Fractionation facilities operate most efficiently at high utilization, and collection networks achieve density economies in donor recruitment.

Network Effects: Limited. Plasma is a commodity raw material without meaningful network effects.

Counter-Positioning: Moderate. Grifols' vertical integration from collection to manufacturing creates a business model that simpler competitors cannot easily replicate.

Switching Costs: Moderate-High. Healthcare providers develop clinical experience with specific products and face regulatory documentation requirements when switching.

Branding: Moderate. Physician and hospital familiarity with specific brands creates preference, but this is weaker than consumer brands.

Cornered Resource: High. The approximately 400 plasma centers represent a cornered resource that took decades to build and cannot be easily replicated.

Process Power: Moderate. Manufacturing expertise and yield optimization create cost advantages that compound over time.

Key Metrics to Track

For investors monitoring Grifols' ongoing performance, three metrics deserve particular attention:

-

Leverage Ratio (Net Debt / EBITDA): The single most important metric for assessing financial risk. Grifols targets below 4x; the current ratio of approximately 4.2x represents significant progress from the crisis-era 6.8x but remains elevated versus global healthcare company averages. Watch for continued deleveraging toward 3.5x.

-

Biopharma Revenue Growth at Constant Currency: This metric strips out FX noise and reflects underlying demand for Grifols' core products. Double-digit growth indicates strong market positioning; mid-single-digit growth would suggest competitive or pricing pressure. The current 11%+ rate is healthy.

-

Free Cash Flow Conversion: The ratio of free cash flow to adjusted EBITDA indicates how effectively EBITDA growth translates into deleveraging capacity. Given the capital intensity of the business, conversion rates of 15-20% are reasonable; higher rates would indicate improving operational efficiency.

Myth vs. Reality

Myth: Grifols is primarily a Spanish company. Reality: Over 60% of revenues come from the United States and Canada. Spain represents only about 5% of sales. Grifols is a global company headquartered in Barcelona.

Myth: The Gotham report uncovered financial fraud. Reality: Regulatory investigations found no fraud. The U.S. SEC took no enforcement action. While certain transactions with related parties created legitimate governance concerns, the fundamental accounting was not materially misstated.

Myth: Paid plasma donation is inherently exploitative. Reality: The ethics are genuinely complex. Without the U.S. paid-donation system, there would be insufficient plasma to meet global medical demand. However, the system's concentration among lower-income donors and high-frequency donation protocols warrant ongoing scrutiny.

XIII. Bull Case and Bear Case

The Bull Case

Grifols emerges from its 2024 crisis as a fundamentally stronger company. The governance overhaul—separating family ownership from professional management—addresses the concerns that short-sellers exploited. The balance sheet deleveraging continues, with the leverage ratio declining steadily toward the 4x target.

The pipeline is delivering: Yimmugo's FDA approval validates the Biotest acquisition, and the fibrinogen program represents a potential $800 million market opportunity with first-mover advantage in the U.S. If FDA approval follows German marketing authorization, Grifols could have a differentiated growth driver just as deleveraging completes.

The plasma industry's structural tailwinds persist. The immunoglobulins segment dominated the market in terms of revenue share of 63.2% in 2024 and is anticipated to grow at the fastest CAGR of 9.1%, fueled by its widespread use in treating immune deficiencies, autoimmune diseases, and neurological disorders. The increasing prevalence of these conditions, particularly among aging populations, has significantly boosted demand for immunoglobulin therapies.

Grifols trades at a significant discount to peers despite comparable market positioning and superior growth rates. As deleveraging completes and the Gotham overhang fades, multiple expansion could provide meaningful upside beyond operational improvement.

The Bear Case

The debt remains elevated, and any operational stumble could reignite concerns about financial sustainability. Interest expenses consume significant cash flow that could otherwise fund growth or shareholder returns. Rising rates since 2022 have increased financing costs.

Competition is intensifying. CSL Behring continues to expand capacity, Takeda is optimizing its plasma business, and Octapharma is growing aggressively. If industry pricing weakens due to overcapacity, Grifols' highly leveraged balance sheet would magnify the impact on equity returns.

Family control creates ongoing governance risk. The dual-class share structure limits public shareholders' ability to influence management or strategy. Related-party transactions between Grifols and family-controlled entities like Scranton Enterprises may continue to generate controversy, even if they're properly disclosed and executed at arm's length.

The U.S. paid-donation model could face regulatory or reputational pressure. If political attention focuses on plasma donor exploitation, collection volumes could decline, increasing costs and reducing supply. Any material disruption to U.S. supply would impact the entire industry—but Grifols' concentration in U.S. collection creates particular exposure.

Recombinant and gene therapy alternatives represent long-term substitution risk for certain product categories. While immunoglobulins appear safe from synthetic substitution, coagulation factors face competitive pressure that may intensify.

XIV. Conclusion: The Blood Money Empire at a Crossroads

More than a century after Josep Antoni Grífols i Roig opened his Barcelona laboratory, the company bearing his name stands at an inflection point.

The crisis of 2024 is fading into memory. The stock has recovered from its January lows. The balance sheet is strengthening. The pipeline is delivering. Professional management is in place. And the fundamental drivers of the plasma industry—aging populations, expanding diagnostic capabilities, growing immunological disease prevalence—continue to generate structural demand growth.

Yet the challenges remain formidable. The debt, though declining, still weighs on returns. Competition shows no signs of weakening. Governance questions linger. And the ethical complexities of an industry built on paid plasma donation from economically vulnerable populations continue to invite scrutiny.

For the Grifols family, the path forward requires balancing the long-term thinking that built the business against the financial discipline that markets demand. For investors, it requires distinguishing between the noise of short-seller attacks and the signal of fundamental business performance.

What seems clear is that the plasma industry's unusual characteristics—an irreplaceable product, massive barriers to entry, structural demand growth, and consolidated supply—create value that will persist regardless of short-term volatility. The question is whether Grifols, with its century of experience and global infrastructure, can capture its share of that value while managing the leverage that two decades of aggressive expansion created.

In the end, the blood money empire's future depends on the same qualities that built it in the first place: scientific excellence, operational discipline, and the patient capital that family businesses can deploy when public markets lose faith. Whether that formula remains viable in an era of activist investors and short-seller scrutiny is the question that Grifols' next chapter will answer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube