Grupa Pracuj: The Toll Bridge of European Talent

I. Introduction & The "CEE Tech Darling" (0:00 – 0:07)

Somewhere in Warsaw, right now, a human resources manager at a Polish bank is logging into a piece of software to review sixty-three applications for a compliance analyst role. She does not think about which company built this software. She does not compare alternatives. She simply opens eRecruiter, the same tool she has used every working day for the past six years, scrolls through AI-ranked candidate profiles, and schedules her interviews. The job was posted on Pracuj.pl—the same platform where this bank has posted every open role since 2005. The candidates found the listing on Pracuj.pl because that is where Polish professionals go when they want a new job, the same way Americans go to Indeed or Germans go to StepStone. This HR manager is, without realising it, a captive customer of one of the most quietly dominant technology businesses in Central Europe.

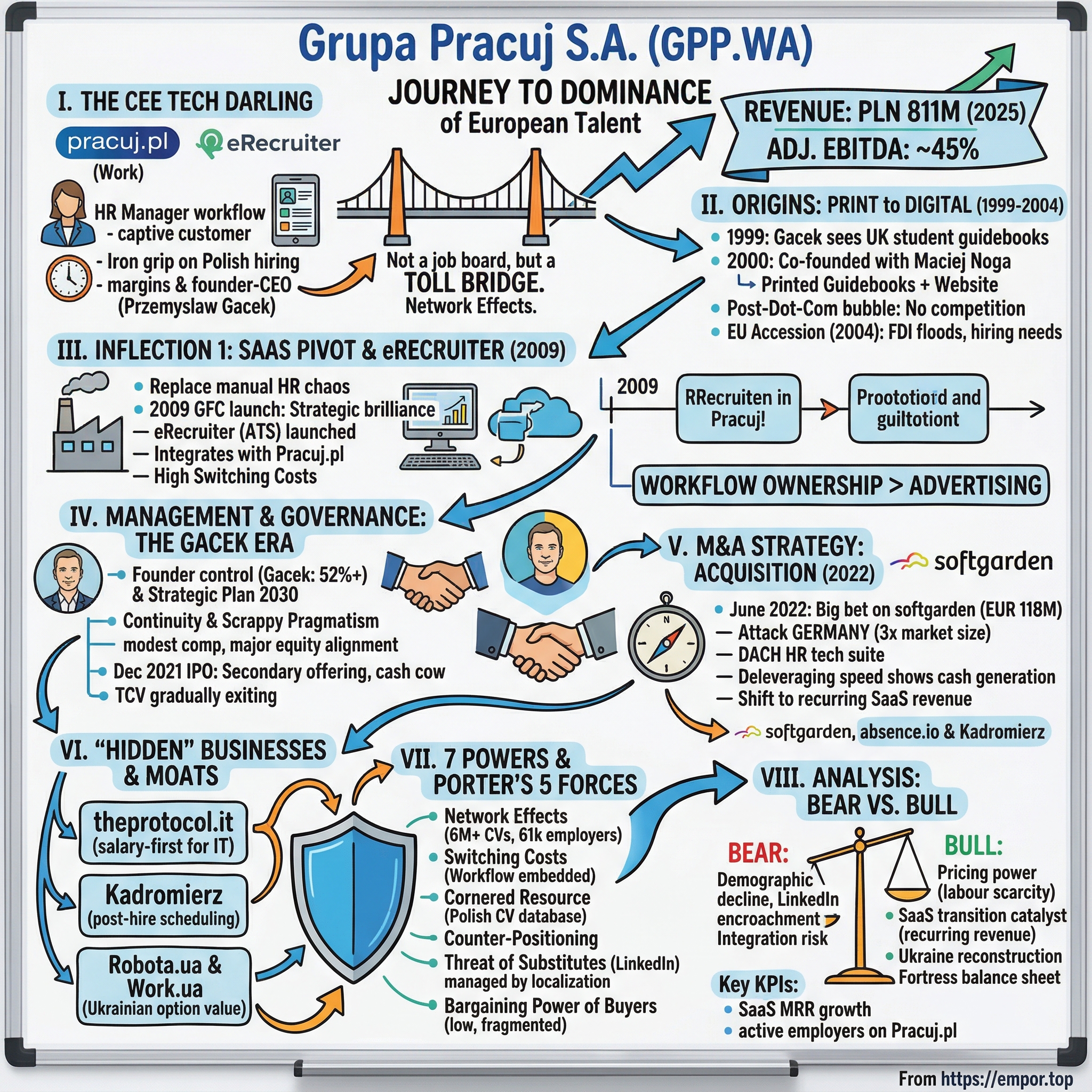

Grupa Pracuj S.A. is not a household name outside Poland. It does not have the brand recognition of LinkedIn or the global ambitions of Recruit Holdings. What it has is something arguably more valuable: an iron grip on the professional hiring workflow of an entire country, margins that would make most SaaS companies blush, and a founder-CEO who has been running the business for a quarter of a century with no apparent interest in selling.

The numbers tell a story of quiet dominance. Revenue reached PLN 811 million in 2025, with adjusted EBITDA margins around forty-five percent at the group level. In the core Polish business—Pracuj.pl alone—those margins historically ran closer to seventy percent. Return on equity sits at forty-seven percent. Free cash flow conversion is consistently excellent. The company carries almost no debt. And it trades, as of April 2026, at roughly PLN 41 per share—barely half its December 2021 IPO price of PLN 74, despite the business being meaningfully larger and more profitable than it was at listing.

The thesis on Grupa Pracuj is deceptively simple. This is not a job board. It is a toll bridge. Almost every white-collar hire in Poland must cross it. The company has spent two decades building network effects so deep that competitors—including LinkedIn and Indeed—have failed to dislodge it. And management is now executing a deliberate strategy to transform what the market prices as a "classified ads" business into what should be priced as a recurring-revenue software platform. The gap between those two valuations is where the story gets interesting.

This is the journey from a student guidebook in post-Communist Warsaw to a PLN 2.8 billion listed company that owns the hiring infrastructure of Central Europe—and the audacious bet on Germany that could either double the story or dilute it.

II. The Origins: Print to Digital Transition (0:07 – 0:17)

The year was 1999, and Przemyslaw Gacek was finishing his studies at Columbia University in New York, splitting time between classes in international public affairs and an internship at a London consulting firm. In London, he stumbled across something that would change his life: a publishing house that produced glossy employer profile guidebooks for university students, paired with a companion website where graduates could browse job listings. The concept was simple—bridge the gap between employers hungry for young talent and students about to enter the workforce. Gacek looked at this model and saw not a British business to admire, but a Polish business to build.

He returned to Poland and, in 2000, co-founded what would become Grupa Pracuj with Maciej Noga. "Pracuj" means "Work" in Polish—blunt, functional, impossible to forget. The initial product was a hybrid: printed guidebooks profiling employers, distributed on university campuses, paired with a nascent website called Pracuj.pl. It was the kind of bootstrapped, analogue-meets-digital operation that defined early internet businesses in Central and Eastern Europe.

The timing was both terrible and perfect. Terrible because the dot-com bubble had just burst, and internet businesses globally were being written off as fantasies. Perfect because the very same crash meant there was virtually no competition. Internet penetration in Poland stood at roughly fourteen percent when Pracuj.pl launched. LinkedIn did not exist. Indeed did not exist. Monster.com had no meaningful presence east of Berlin. The entire professional labour market of a thirty-eight-million-person country was essentially uncontested digital territory.

Poland itself was in the midst of a historic transformation. The post-Communist economy was professionalising at extraordinary speed. Foreign direct investment was flooding in—especially after EU accession in 2004—and every multinational setting up a Warsaw office needed to hire local talent. But the infrastructure for matching employers with candidates barely existed. Newspaper classifieds were the norm. Recruitment agencies served the top end but were expensive and slow. For the vast middle market—mid-career professionals, regional employers, growing Polish companies—there was nothing efficient.

Pracuj.pl filled this vacuum. The website grew steadily through the early 2000s as internet penetration climbed and as the print guidebook business faded in relevance. By the mid-2000s, the balance had tipped decisively toward digital. Gacek made the critical decision to invest everything in the website rather than trying to sustain the print operation. The print business was killed. Pracuj.pl became the sole focus.

What happened next was a classic network effects flywheel. As more employers posted jobs on Pracuj.pl, more candidates registered. As the candidate pool grew, employers had even more reason to post exclusively on Pracuj.pl rather than splitting budgets across multiple channels. By the time potential competitors woke up to the opportunity, the flywheel was spinning too fast to catch. Poland's largest job board had become Poland's only job board that mattered. More than six and a half million CVs sit in the Pracuj.pl database today. Over sixty-one thousand employers actively use the platform—a record. In 2025, roughly 762,000 job offers were published on the site. When a Polish professional types "praca" (work) into Google, Pracuj.pl is the first result, every time.

But Gacek understood something that many marketplace founders miss: owning the traffic is not the same as owning the customer. A job board is, at its core, an advertising business—cyclical, transactional, and vulnerable to any platform that can aggregate listings more cheaply. To build something durable, he needed to go deeper. He needed to own the workflow.

III. Inflection Point 1: The SaaS Pivot & eRecruiter (0:17 – 0:35)

Picture the hiring process at a mid-sized Polish company in 2008. The HR manager posts a job on Pracuj.pl. Within days, two hundred applications flood into a shared email inbox. The manager prints the best CVs, passes them to the hiring manager in a manila folder, schedules interviews via phone calls, and tracks candidate status in an Excel spreadsheet taped to the side of her monitor. Feedback from interviewers arrives as hallway conversations. Offer letters are Word documents emailed back and forth. The entire process is manual, error-prone, and invisible to anyone trying to measure hiring effectiveness.

Grupa Pracuj's management looked at this chaos and saw an opportunity far more valuable than selling job postings. If they could build software that replaced the email inbox, the Excel tracker, and the manila folder—software that managed the entire recruitment workflow from application to offer—they would transform their relationship with employers from transactional to embedded. A job posting is a one-time purchase. Workflow software is a subscription.

In 2009, in the depths of the Global Financial Crisis—when most companies were cutting R&D budgets—Grupa Pracuj launched eRecruiter. The timing was counterintuitive but strategically brilliant. During a recession, HR departments face pressure to do more with less. An affordable cloud-based tool that automated candidate management, interview scheduling, feedback collection, and compliance documentation was exactly what stretched HR teams needed.

For those unfamiliar with the category, an Applicant Tracking System—or ATS—is to recruiting what Salesforce is to sales. Think of it as a CRM specifically designed for hiring. Every candidate who applies for a job becomes a record in the system. Every interaction—email, interview, assessment, reference check—is logged. The hiring manager can see the entire pipeline at a glance: how many candidates are at each stage, where bottlenecks exist, and how long the process is taking. Compliance features ensure that data handling meets local labour law requirements—a particularly important consideration in Europe, where GDPR and national employment regulations create real legal exposure for companies that manage candidate data carelessly.

The genius of eRecruiter was not the software itself—ATS products existed globally. The genius was the integration with Pracuj.pl. When an employer posted a job on Pracuj.pl and used eRecruiter, the applications flowed seamlessly into the ATS. Candidate data populated automatically. Communication templates were pre-built. The two products became a single workflow. And once an HR team had spent months configuring eRecruiter—setting up their hiring stages, building their template library, training their managers, accumulating years of candidate history—switching to a competitor's ATS meant abandoning all of that institutional knowledge. The switching costs were enormous, not because of contractual lock-in, but because of operational dependency.

By the third quarter of 2025, eRecruiter had grown to 2,270 active employer clients, with monthly recurring revenue of PLN 4.3 million—growing at roughly ten percent year over year. Combined with HRlink—a complementary ATS acquired from media group Agora in January 2024 for PLN 6.2 million—Grupa Pracuj now controls over fifty percent of the paid ATS market in Poland. An AI Assistant launched in 2024 analyses applications, generates candidate summaries, and recommends process improvements, further deepening the product's value proposition and stickiness.

The strategic transformation was profound. Grupa Pracuj had moved from selling advertising impressions—a model where revenue evaporates the moment an employer decides to stop hiring—to selling infrastructure that HR departments depend on regardless of hiring volume. The subscription revenue from eRecruiter does not disappear when the economy softens. If anything, it becomes more valuable during downturns, when HR teams need to process more applications per open role with fewer resources.

This shift from classified advertising to SaaS also had significant implications for how the market should value the business. Public markets typically assign job board companies multiples of eight to ten times EBITDA—roughly in line with other media and advertising businesses. SaaS companies with strong retention and recurring revenue command fifteen to twenty times EBITDA or more. The more of Grupa Pracuj's revenue that shifts into the SaaS column, the wider the gap between its current valuation and what a pure-play SaaS company would command. Management has explicitly targeted fifty percent of revenue from HR software by 2030, up from approximately twenty-seven percent today. That transition is the single most important valuation driver for the next five years.

IV. Management & Governance: The Gacek Era (0:35 – 0:50)

In an industry littered with founder exits—where the typical pattern involves building a marketplace, selling to private equity, and moving to a beach—Przemyslaw Gacek is an anomaly. Twenty-six years after co-founding the company, he remains CEO and controls 52.37 percent of the shares through his holding vehicle, Frascati Investments. This is not a hired-gun manager running someone else's company. This is a founder with majority control, no financial need to sell, and a strategic plan that stretches to 2030.

Gacek's background shaped his approach. The Columbia education and London consulting exposure gave him a pattern-matching framework that his Polish peers lacked in the early 2000s. He saw what worked in mature Western markets and adapted it for a country that was rapidly converging toward European norms. But he never lost the scrappy pragmatism of a founder who built a business from university campuses and printed guidebooks. Colleagues describe a management style that is conservative on capital structure—the balance sheet carries almost no debt—but aggressive on product development. The decision to launch eRecruiter during a financial crisis, when every instinct says to hunker down and protect margins, is characteristic.

In 2024, Gacek was named EY Entrepreneur of the Year in Poland—recognition that came a quarter century into his tenure, at an age (estimated late forties based on his 1999 graduation) when most founders have either cashed out or burned out. He is a member of the Young Presidents' Organisation, a peer network that provides the kind of cross-industry perspective that helps founder-CEOs avoid insularity. His total disclosed compensation is approximately PLN 729,000—modest by any standard, let alone for the CEO of a publicly listed technology company. The real alignment is in the equity: at the current share price, his stake is worth roughly PLN 1.5 billion.

Co-founder Maciej Noga moved from operational leadership to the chairmanship of the Supervisory Board, an arrangement that preserves founder DNA in governance without creating the dysfunction of two CEOs. Noga holds 8.35 percent of shares through a family foundation and has built a parallel career as a venture investor through Pracuj Ventures and Ataraxy Ventures, which has created a useful deal pipeline—the March 2025 acquisition of Kadromierz, a workforce scheduling tool, originated from Pracuj Ventures' portfolio.

The executive team beneath Gacek reflects institutional depth rather than revolving-door instability. CFO Gracjan Fiedorowicz has been with the company since 2007 and architected the 2021 IPO. COO Rafal Nachyna has been aboard since 2005 and runs the core Polish and Ukrainian operations. Neither is a recent hire parachuted in to prepare for an exit. The continuity is unusual for a tech company of this size and matters because the current strategy—transforming from classified advertising to SaaS—requires patient, multi-year execution rather than quarter-to-quarter optimisation.

The December 2021 IPO on the Warsaw Stock Exchange was structured as a pure secondary offering—no new shares were issued by the company. Existing shareholders, primarily TCV (a US growth equity firm that had acquired a roughly thirty percent stake in 2017 at an estimated EUR 400 million valuation) and minority portions from the founders, sold 15.1 million shares at PLN 74 apiece, raising PLN 1.12 billion. The message was clear: this was a cap table clean-up and liquidity event, not a fundraising exercise. The business generated more than enough cash internally to fund its ambitions.

TCV has been gradually reducing its position since the IPO—from roughly sixteen percent post-listing to 6.73 percent as of mid-2025. John Doran, a General Partner at TCV, remains on the Supervisory Board, providing Silicon Valley perspective on SaaS metrics and product strategy. The gradual nature of TCV's exit—selling in tranches over four years rather than dumping the entire position—suggests a deliberate effort to avoid disrupting the share price, though the stock has nevertheless fallen significantly from its IPO level.

The Long-Term Incentive Plan is tied to the 2025-2030 strategic targets: PLN 1.4 billion in revenue, forty percent-plus adjusted EBITDA margins, and a fifty-fifty revenue split between classifieds and HR software. In December 2025, the company completed a buyback of 225,782 shares at PLN 58 per share—earmarked for the incentive programme. Stock-based compensation totalled roughly PLN 13.5 million in 2024, a modest 1.8 percent of revenue, suggesting management is not diluting shareholders excessively to pay itself.

V. M&A Strategy: The softgarden Acquisition (0:50 – 1:10)

In June 2022, Grupa Pracuj made the biggest bet in its history. The company announced the acquisition of softgarden, a Berlin-headquartered cloud-based talent acquisition suite, for approximately EUR 118 million—purchased from Investcorp, the Bahrain-based alternative investment firm, which reportedly achieved a three-times return on its investment. For a company that had spent two decades building dominance in a single country through organic growth and small tuck-in deals, this was a fundamentally different kind of move. This was not about defending Poland. This was about attacking Germany.

To understand why Germany matters, consider the arithmetic of addressable markets. Poland has roughly seventeen million employed workers. Germany has forty-five million—nearly three times as many—in an economy where employers spend significantly more per hire on recruitment technology. The DACH region (Germany, Austria, Switzerland) represents the largest HR technology market in continental Europe. By acquiring softgarden, Grupa Pracuj was not just adding a product line. It was effectively tripling its total addressable market overnight.

softgarden itself was founded in 2003 by Dominik Faber and Stefan Schuffler in Saarbrucken before relocating to Berlin. The product suite includes an ATS, a multiposting tool that distributes job listings to over 1,200 job boards simultaneously, career website builders, employer branding tools, and analytics. An adjacent product called absence.io—bundled into the deal—provides absence management, time tracking, and digital personnel files to roughly 2,300 small and mid-sized businesses in the DACH region. At the time of acquisition, softgarden served approximately 1,700 employer clients with around 140 employees.

The purchase price of EUR 118 million implied a multiple of roughly fifteen to eighteen times trailing EBITDA. Was this expensive? In isolation, the number looks steep. But context matters. Comparable US-based SaaS HR tools—Greenhouse, Lever, iCIMS—were transacting or being valued at twenty times EBITDA and above during the same period. Recruit Holdings, which owns Indeed and Glassdoor, trades at a perpetual premium to every HR tech peer on the planet. Against those benchmarks, Grupa Pracuj paid a meaningful discount for a growing, subscription-based business in a market nearly three times the size of its home territory.

The deal was funded with PLN 368 million in debt—the first time Grupa Pracuj had taken on significant leverage. But the deleveraging speed tells you everything about the company's cash generation. Net debt fell from PLN 277 million at the end of 2022 to PLN 133 million at the end of 2023, and to just PLN 52 million by the end of 2024. Within two years of the acquisition, the company had paid down most of the acquisition debt from operating cash flow alone. By the end of 2024, the net debt to EBITDA ratio stood at 0.16 times—essentially debt-free again.

The German operation has performed well, though not without headwinds. In 2024, softgarden's SaaS client base grew to 1,817—up nearly twelve percent year over year—with monthly recurring revenue reaching PLN 7.82 million, up fourteen percent. The German segment's operating profit surged to PLN 21.6 million, more than tripling from PLN 6.1 million in 2023, as the integration delivered cost synergies and the revenue base scaled. By the third quarter of 2025, SaaS clients had reached 1,878 with MRR of PLN 8.4 million. The German economy itself was in recession through much of 2025, which suppressed hiring volumes and kept top-line growth muted. But the subscription nature of the revenue meant that softgarden's client base remained sticky even as the broader market contracted. When German hiring eventually recovers, the revenue uplift should flow through at high incremental margins against a now-optimised cost base.

A new "Light Touch" self-service model, powered by an AI chatbot, was launched to target smaller German SMEs—the vast Mittelstand—who cannot justify the cost of a full enterprise ATS implementation. This is the kind of product innovation that turns a good acquisition into a great one: using the acquired technology platform to access customer segments the original business could not reach.

The strategic logic of softgarden extends beyond revenue arithmetic. The acquisition shifted Grupa Pracuj's revenue mix materially toward recurring SaaS. Before the deal, the company was overwhelmingly a Polish classified advertising business with an emerging SaaS side project. After the deal, SaaS revenue—eRecruiter plus softgarden—became a significantly larger share of the total. The combined group's annualised SaaS MRR (including the subsequently acquired Kadromierz) now runs at roughly PLN 161 million—a meaningful and growing portion of group revenue, with retention rates and growth characteristics that look nothing like a cyclical advertising business.

VI. "Hidden" Businesses & Segment Data (1:10 – 1:25)

Beyond the headline businesses of Pracuj.pl and the SaaS platforms, Grupa Pracuj operates a constellation of smaller brands that rarely attract analyst attention but play critical strategic roles. Together, they form a moat that is wider and deeper than a casual observer might assume.

The most intriguing is theprotocol.it—a recruitment platform launched in 2021 specifically for the IT sector, built on a "salary-first" transparency model. In Poland, as in much of Europe, salary information has traditionally been omitted from job postings. For IT professionals—a community with high demand and low tolerance for opacity—this was a persistent frustration. Niche competitors like No Fluff Jobs and Just Join IT had gained traction in the Polish developer community precisely by requiring employers to disclose salary ranges. theprotocol.it was Grupa Pracuj's defensive response: a purpose-built platform for tech talent that features salary transparency, filtering by tech stack and specialisation, and remote work preferences. It is cross-promoted with Pracuj.pl but operates as a distinct brand, allowing the company to compete on two fronts—the broad professional market with Pracuj.pl and the high-value tech niche with theprotocol.it—without diluting either brand's positioning.

Kadromierz, acquired in March 2025 for PLN 20 million from Pracuj Ventures (co-founder Noga's investment vehicle), is a workforce scheduling and working time management tool. Think of it as a digital shift planner—the kind of software that a restaurant chain or retail operation uses to manage hourly workers' schedules, track attendance, and ensure compliance with labour regulations. With monthly recurring revenue of PLN 687,000 growing at forty-six percent year over year as of the third quarter of 2025, it is the fastest-growing SaaS product in the portfolio. More importantly, it represents Grupa Pracuj's first step into the "post-hire" market—managing employees after they have been recruited—which the company estimates is a EUR 3.5 billion addressable opportunity in Europe, roughly ten times larger than the pre-hire market where it currently dominates.

Robota.ua and Work.ua constitute the Ukrainian segment—and they represent the most unusual "option value" in the portfolio. Grupa Pracuj has owned Robota.ua since 2006. In May 2025, the company increased its stake by acquiring an additional 29.4 percent from co-founder Andriy Borovyk for $7.64 million, bringing total control to 76.7 percent of Robota International and 52.7 percent of Work Ukraine. The combined Ukrainian platforms serve over five million monthly visitors with approximately one hundred thousand active job offers.

The Ukrainian business has remained operational and profitable throughout the war—a testament to the resilience of both the platform and the Ukrainian labour market, where the need to match workers with employers has, if anything, intensified. In 2024, the Ukrainian segment generated roughly PLN 52 million in revenue, growing twenty-six percent year over year. According to the FY2025 results, the Ukrainian business was a key driver of the seventeen percent net profit growth, with pricing increases of thirty-five percent in local currency reflecting both inflation and the platform's pricing power. When—not if—large-scale reconstruction begins, the demand for organised labour matching in Ukraine will be enormous. Grupa Pracuj owns the dominant infrastructure. Whether this option value materialises in 2027, 2028, or later depends on geopolitics that no financial model can predict. But the optionality is real and was acquired at a trivial cost relative to the group's market capitalisation.

The segment breakdown reveals the architecture of the business. Poland remains the cash cow: approximately seventy percent of group revenue, generating EBITDA margins that historically exceeded seventy percent before the softgarden acquisition diluted the blended figure. Germany contributes roughly nineteen percent of revenue, with margins improving rapidly as the softgarden integration matures and the fixed-cost base is leveraged. Ukraine contributes about seven percent but punches above its weight in growth terms. The remaining four percent comes from smaller brands and new initiatives.

What matters most for valuation purposes is the revenue mix shift. In 2021, before the softgarden acquisition, virtually all of Grupa Pracuj's revenue came from classified job advertising and Polish ATS subscriptions. Today, approximately twenty-seven percent of revenue is recurring SaaS. The 2030 target of fifty percent would represent a fundamental transformation in the business's character—and, if achieved, should command a fundamentally different market multiple. The company is not asking investors to take a leap of faith on an unproven strategy. It is showing them a predictable glide path, executed by a management team that has been in place for over a decade, funded entirely by internal cash flow.

VII. The Playbook: 7 Powers & Porter's 5 Forces (1:25 – 1:45)

The question every serious investor must answer about Grupa Pracuj is whether its dominance is durable or fragile. Network effects in marketplace businesses can be powerful, but they can also erode quickly—ask anyone who remembers Craigslist's dominance of classified advertising before Zillow, Indeed, and dozens of vertical attackers unbundled it. Hamilton Helmer's Seven Powers framework provides a useful lens for stress-testing the moat.

The most obvious power is Network Effects, and they are unusually strong. Pracuj.pl operates a classic two-sided marketplace: candidates go where the jobs are, and employers post where the candidates are. With sixty-one thousand active employer clients and six and a half million registered CVs, the platform has reached a density where the cost of not being on Pracuj.pl exceeds the cost of being on it. A large bank in Warsaw posting a compliance analyst role cannot afford to skip Pracuj.pl—the probability of missing the best candidates is simply too high. Similarly, a mid-career professional updating their CV will register on Pracuj.pl first because that is where the most relevant opportunities appear. This flywheel has been spinning for over two decades and shows no sign of slowing. AI-powered recommendations now drive fifty-three percent of all "Apply" clicks on the platform, further increasing match quality and reinforcing the incentive for both sides to stay.

Switching Costs represent the second major power, and they operate at the software layer rather than the marketplace layer. eRecruiter and softgarden are embedded in the daily workflows of HR departments. Once an employer has configured their hiring stages, built their communication templates, trained their recruitment team, and accumulated years of candidate history within the ATS, switching to a competitor means starting from zero. The data is portable in theory but not in practice. The institutional knowledge—which interview questions work, which sourcing channels produce the best candidates, how long each stage typically takes—exists within the system. Ripping it out and rebuilding it in a new tool is a project that most HR directors will avoid unless they have an overwhelming reason to change.

The third power is a Cornered Resource: Grupa Pracuj's proprietary database of millions of Polish-language CVs. This is not a resource that LinkedIn or Google can easily replicate. The CVs are structured in Polish, tagged with Polish-specific job categories and qualifications, and enriched with behavioural data from years of interactions on the platform. Scraping this data is technically difficult and legally prohibited under European data protection regulations. Building an equivalent dataset from scratch would require years of market presence and the critical mass of employer clients needed to attract candidate registrations. It is, in effect, a data moat that deepens every year.

Does Grupa Pracuj have Counter-Positioning? Arguably, yes. The company is using the extraordinary cash flow from its dominant Polish classified business to fund lower-return investments in SaaS (eRecruiter, softgarden, Kadromierz) and geographic expansion (Germany, Ukraine). A pure-play classified competitor cannot afford to make these investments because it does not have the margin cushion. A global SaaS player like LinkedIn lacks the local market knowledge and regulatory expertise to compete effectively in Poland. Grupa Pracuj occupies a strategic position that neither type of competitor can easily attack.

The powers the company lacks are worth noting. There is no significant Branding advantage beyond Poland—softgarden is a respected but not dominant brand in Germany. Process Power is difficult to assess from the outside, though the AI integration and product development velocity suggest meaningful operational capability. Scale Economies exist in the traditional sense—the fixed costs of running Pracuj.pl are spread across a growing revenue base—but they are not the primary source of competitive advantage.

Turning to Porter's Five Forces, the picture reinforces the strength of the position. Threat of Substitutes is the most frequently cited risk, and LinkedIn is the substitute that comes up in every analyst conversation. But the reality is more nuanced than the headline suggests. LinkedIn's penetration in Poland remains materially lower than in Western European markets. The platform is effective for senior-level and international roles but less relevant for the bread-and-butter mid-career hiring that constitutes the bulk of Pracuj.pl's volume. Pracuj.pl's deep integration with Polish labour law compliance, its Polish-language AI recommendations, and its ATS integration create a user experience that LinkedIn's global platform cannot match locally. The IT niche—where LinkedIn is strongest—is addressed by theprotocol.it. The threat is real but manageable.

Bargaining Power of Buyers is structurally low. Grupa Pracuj's client base is highly fragmented—sixty-one thousand employers, none of whom individually accounts for a material share of revenue. A big bank may negotiate a volume discount, but the average SME takes the published price. This fragmentation gives the company remarkable pricing power: average recruitment project prices increased 4.8 percent in 2024, with minimal evidence of churn. In Ukraine, prices rose thirty-five percent in local currency. When seven out of ten employers in your market report difficulty filling positions, the platform that delivers candidates can name its price.

Bargaining Power of Suppliers is essentially irrelevant—the "suppliers" are the candidates who register for free, and the cloud infrastructure providers whose costs are declining.

Threat of New Entrants is moderated by the network effects and switching costs already described. A well-funded new entrant could theoretically build a competitive job board, but attracting the candidate base away from a platform with six and a half million CVs and two decades of brand recognition would require a marketing spend disproportionate to any realistic return.

Competitive Rivalry is intense at the margins—No Fluff Jobs in IT, OLX in blue-collar, LinkedIn in senior roles—but Pracuj.pl's position in the core professional market remains unchallenged. The closest listed peer, Epam Systems or Allegro, does not compete directly. In Germany, softgarden competes against Personio (a well-funded HR platform targeting SMBs) and enterprise players like SAP SuccessFactors, but its Mittelstand focus and competitive pricing carve out defensible space.

VIII. Analysis: Bear vs. Bull Case (1:45 – 2:00)

The bear case for Grupa Pracuj begins with demographics—and it is a serious argument. Poland's population has been declining for six consecutive years, from a peak of 38.5 million in 2012 to roughly 36.5 million today. The total fertility rate stands at 1.16—one of the lowest in Europe, and well below the 2.1 replacement level. The working-age population is projected to shrink by 2.1 million by 2035. A job board's revenue is ultimately a function of hiring volume, and if there are fewer people to hire, the ceiling on that revenue shrinks. This is not a cyclical headwind that will reverse. It is a structural trend that will define the Polish labour market for decades.

LinkedIn's encroachment is the second bear pillar. While Pracuj.pl's position is currently dominant, LinkedIn's product has been steadily improving its Polish-language capabilities, and younger professionals are increasingly accustomed to the platform's global network. The risk is not that LinkedIn displaces Pracuj.pl overnight, but that it gradually siphons off the highest-value segment—senior professionals and tech workers—leaving Pracuj.pl with the less profitable mid-market. theprotocol.it addresses the tech segment, but whether it can hold the line against a platform with LinkedIn's resources and global brand remains uncertain.

Integration risk on the German acquisition deserves mention. softgarden is performing well by the numbers, but the German economy has been in recession, suppressing hiring volumes. The true test of the acquisition will come when German hiring recovers and management must demonstrate that softgarden can grow revenue significantly—not just maintain margins—in a competitive DACH market where Personio and SAP are formidable incumbents. The "Light Touch" self-service model is promising but unproven at scale.

Finally, there is the valuation gap risk. The bull case depends on the market re-rating Grupa Pracuj from a classified advertising multiple to a SaaS multiple as recurring revenue grows. But markets can remain stubborn. If the SaaS transition takes longer than expected, or if margins compress during the transition, the re-rating may not materialise, and investors will be left with a slow-growing classified business trading at what turns out to be a fair price.

The bull case, however, is built on structural advantages that most bears underestimate.

Start with pricing power. The demographic argument—fewer workers means less hiring—actually cuts both ways. When labour is scarce, employers compete more fiercely for candidates, and the platform that delivers those candidates becomes more, not less, valuable. Seven out of ten Polish employers already report difficulty filling positions. In a tightening labour market, the incentive to invest in recruitment technology—better job postings, more sophisticated ATS tools, employer branding—increases. Grupa Pracuj's average revenue per employer can grow even if the total number of employers stays flat, because each employer is willing to pay more for access to a shrinking talent pool. The 2024 data supports this: pricing up nearly five percent with minimal churn.

The SaaS transition is the primary valuation catalyst. Markets value job boards at eight to ten times EBITDA. They value SaaS businesses with strong retention and recurring revenue at fifteen to twenty times. Grupa Pracuj currently trades at roughly twelve times EBITDA—between the two categories. As SaaS revenue grows from twenty-seven percent toward the fifty percent target by 2030, the blended multiple should drift toward the SaaS benchmark. The company does not need to become a pure SaaS business for the re-rating to occur—it just needs to demonstrate consistent progress on the mix shift.

The Ukraine reconstruction catalyst is speculative but potentially transformational. Grupa Pracuj owns the dominant hiring platforms in a country that will need to mobilise millions of workers for the largest reconstruction effort in European history since the Marshall Plan. The platforms are operational, profitable, and growing even during wartime. The increased stake acquired in May 2025 demonstrates management's conviction in this optionality.

The balance sheet is a fortress. Net debt to EBITDA of 0.16 times means the company has enormous capacity for further acquisitions, buybacks, or simply riding out a prolonged downturn. Free cash flow of PLN 263 million in 2024 provides ample room for the proposed PLN 3.00 per share dividend for 2025—the highest in the company's history—while still funding organic investment and tuck-in M&A.

For investors tracking this story, the KPIs that matter most are two. First, SaaS MRR growth rate—the combined monthly recurring revenue of eRecruiter, softgarden, and Kadromierz, which currently runs at approximately PLN 13.4 million per month. This is the purest measure of progress on the transition from classified advertising to recurring software revenue. Second, active employer client count on Pracuj.pl, which stood at a record 61,500 in the third quarter of 2025. This metric captures both the health of the network effect and the company's pricing power: if the client count holds steady or grows while revenue per client rises, the flywheel is intact. A third metric worth monitoring—though less frequently disclosed—is softgarden's net client additions in DACH, which will determine whether the German bet is scaling or stalling.

IX. Epilogue & Playbook Lessons (2:00 – 2:10)

The playbook lesson from Grupa Pracuj is deceptively simple, and it applies far beyond HR technology: do not just build the marketplace—build the software that manages the marketplace. Pracuj.pl alone would have been a successful classified advertising business, generating strong margins and throwing off cash. But it would have been vulnerable to the same forces that disrupted newspaper classifieds globally. By building eRecruiter on top of Pracuj.pl, and then acquiring softgarden to replicate the model in Germany, Gacek transformed a transactional advertising platform into an embedded infrastructure business with subscription economics. The job board is the top of the funnel. The ATS is the lock.

The capital allocation lesson is equally instructive. Grupa Pracuj used the extraordinary margins from a dominant local position—seventy percent-plus EBITDA margins in the core Polish business—to fund a strategic acquisition in a larger, more stable market. The softgarden deal was financed with debt that was repaid within two years from operating cash flow. No equity dilution. No fundraising roadshow. Just a disciplined deployment of internally generated capital into a higher-growth, higher-TAM opportunity. This is the kind of capital allocation discipline that compounds over decades.

And then there is the broader lesson about local champions beating global giants. LinkedIn is one of the most powerful professional platforms ever built, backed by Microsoft's limitless resources. Indeed, owned by Recruit Holdings, is the most visited job site on earth. Neither has been able to dislodge Pracuj.pl from its dominant position in Poland. Why? Because Grupa Pracuj owns the workflow, not just the traffic. The ATS integration, the Polish-language CV database, the local labour law compliance, the twenty-five-year brand recognition—these create a local advantage that no global platform can replicate without committing resources disproportionate to the Polish market's size. For investors looking beyond Silicon Valley for compounding businesses, this pattern—local workflow dominance defended by switching costs and network effects—repeats across emerging and mid-market economies worldwide.

Grupa Pracuj trades today at roughly PLN 41 per share, down forty-five percent from its IPO price, in a market that seems unable to decide whether it is looking at a legacy classified ads business or an emerging SaaS platform. The company itself is not confused. The 2025-2030 strategy—PLN 1.4 billion in revenue, fifty-fifty revenue split between classifieds and software, forty percent-plus adjusted EBITDA margins—is the roadmap of a management team that knows exactly what it is building. Whether the Warsaw Stock Exchange catches up to that vision is a different question. The toll bridge, meanwhile, collects its toll.

X. Outro & Reading List (2:10 – 2:15)

- Grupa Pracuj S.A. 2021 IPO Prospectus—a goldmine of CEE labour market data, industry sizing, and competitive analysis

- Annual and interim reports available at ir.grupapracuj.pl

- YPO profile of Przemyslaw Gacek (2024)—rare biographical detail on the founder's early career and motivations

- TCV investment announcement (June 2017)—context on the pre-IPO growth equity phase

- Fosway 9-Grid 2025 for European HR Technology—industry positioning of eRecruiter

- AIM Group coverage of CEE online recruitment markets

- Reuters coverage of FY2025 results (April 2026)—latest financial performance and strategic outlook

- Impact of AI on recruitment matching: Grupa Pracuj reports that AI-powered recommendations now drive fifty-three percent of Apply clicks on Pracuj.pl, with roughly ten percent of job posting content AI-generated—a leading indicator of how recruitment platforms will evolve over the next five years

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube