Games Workshop Group PLC: The Fortress of Miniature Wargaming

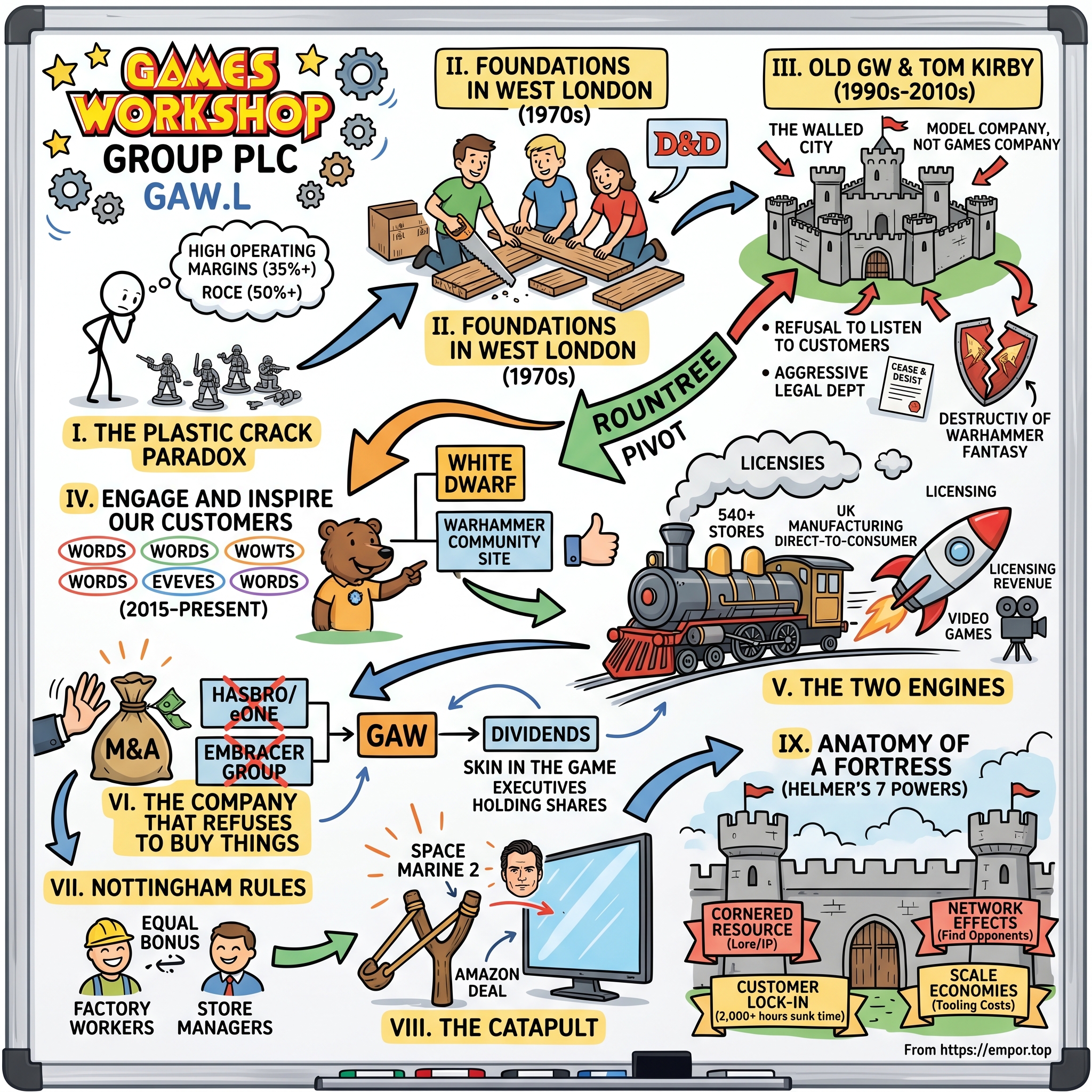

I. The Plastic Crack Paradox

In December 2024, the keepers of the FTSE 100 Index — the roster of the hundred most valuable companies on the London Stock Exchange, a club populated by oil majors, global banks, pharmaceutical titans, and mining conglomerates — quietly admitted a new member. It did not drill for crude in the North Sea. It did not underwrite mortgages or refine copper. It made, of all things, little grey plastic soldiers. The company was Games Workshop Group PLC, headquartered not in the glass towers of the City of London but in an unglamorous industrial estate in Lenton, on the western edge of Nottingham.1

Pause on the strangeness of that. The FTSE 100 is supposed to be the commanding heights of the British economy, and here was a firm whose flagship product was a box of unassembled, unpainted miniature warriors that a customer then had to glue together and paint by hand over many evenings. The hobby's own devotees have a nickname for their habit, half affectionate and half confessional: "Plastic Crack." You buy one kit, you assemble it, you paint it, and somehow you are back at the store three weeks later buying three more. It is an addiction modelled in polystyrene.

Now look under the hood, because this is where a curious investor's eyebrows go up. Games Workshop has run operating margins north of 35% — the kind of profitability you associate with enterprise software, not injection-moulded toys.[^2] Its return on capital employed has at times exceeded 50%, meaning that for every pound the company tied up in its factory, its tooling, and its stores, it spun out more than fifty pence of operating profit a year.[^2] Software companies dream of those numbers. A "toy company," by every received notion of the toy business — thin margins, brutal retail middlemen, fickle Christmas demand — should not be able to print them.

So the thesis of this episode is that the conventional labels are wrong. Games Workshop is not a toy company. It is not a video game publisher, though video games made from its worlds have lately sold in the millions. What it actually is, is a vertically integrated, direct-to-consumer lifestyle hobby business that owns three things almost no one else in its category owns together: the intellectual property of an entire fictional universe, the factories that physically manufacture the universe in plastic, and the local community hubs — over 540 of its own stores — where new recruits are inducted into the hobby for free.[^2] Control all three, and you have built something that looks less like a manufacturer and more like a fortress.

Here is the roadmap for how we get there. First, we trace the company's transformation from a fan-hostile, isolationist regime into the community-first machine it is today — a near-death cultural experience followed by one of the great corporate turnarounds in modern British business. Second, we examine why this company flatly refuses to do mergers and acquisitions, and we benchmark that refusal against multi-billion-dollar M&A disasters in the toy and gaming world that vaporised shareholder capital. Third, we open up the "hidden engine": a small but explosively growing licensing business whose economics are so good they almost don't look real. And finally, we run the whole enterprise through the strategic frameworks — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — to understand exactly why the walls of this particular fortress are so hard to scale.

To understand how a company gets to be this weird and this profitable, you have to go back to a flat in West London in the 1970s, where three friends were sawing wooden boards in their spare time.

II. Backgammon Boards in a London Flat

The origin story of Games Workshop is almost aggressively humble. In 1975, three friends — John Peake, Ian Livingstone, and Steve Jackson (the British Steve Jackson, not to be confused with the American game designer of the same name) — founded a small enterprise hand-crafting wooden boards for traditional games: backgammon, chess, mancala, the kind of thing you might find in a craft fair. They worked out of a flat, with a workshop sensibility and almost no capital. The name was literal: it was a workshop where games were made.

The pivot that mattered came not from woodworking but from importing. Across the Atlantic, a former insurance underwriter named Gary Gygax had co-created a game called Dungeons & Dragons, a fantasy role-playing system that let players become characters in an unfolding story narrated by a "dungeon master." It was strange, it was niche, and it was about to detonate across the hobby world. Livingstone and Jackson recognised what they were looking at. They secured the rights to distribute Dungeons & Dragons in the United Kingdom, becoming the conduit through which an entire generation of British teenagers discovered tabletop role-playing.

That importing business did two things that would define the company forever. First, it forced Games Workshop to build retail and mail-order infrastructure — the unglamorous plumbing of catalogues, fulfilment, and eventually shops, which taught them that the relationship with the end customer was an asset worth owning directly. Second, in 1977 they launched a magazine called White Dwarf, ostensibly to support role-playing games. White Dwarf was, in modern language, content marketing decades before the term existed: a publication that built community, taught the hobby, and — crucially — created a captive channel to sell readers the next thing they didn't yet know they wanted.

But the founders soon noticed where the real money and the real passion lived. It was not in the rulebooks. It was in the miniatures — the small metal figurines that players used to represent their characters and monsters on the table. A sculptor and entrepreneur named Bryan Ansell was producing these through a venture called Citadel Miniatures, and Games Workshop drew Citadel into its orbit. This was the foundational insight of the entire enterprise: rules can be photocopied, but a beautifully sculpted, tactile object that a customer paints with their own hands is something they will pay for again and again. Games Workshop was, even then, learning that it was in the model business.

From that realisation came the games that still drive the company today. In 1983, the company launched Warhammer Fantasy Battles, a mass-combat tabletop wargame set in a grim medieval-fantasy world of warring empires, undead legions, and chaos gods. Then, in 1987, came the masterstroke: Warhammer 40,000: Rogue Trader, which took that grim sensibility and flung it into a far future of interstellar war — genetically engineered super-soldiers in power armour, malevolent alien races, and a galaxy-spanning human empire ruled by a corpse-god on a golden throne. The tagline that would come to define the setting captured its whole tone: "In the grim darkness of the far future, there is only war." Warhammer 40,000 — "40K" to the faithful — would become the crown jewel.

By the early 1990s the founders were ready to move on, and a corporate chapter began. In 1991, an executive named Tom Kirby led a management buy-out, taking control of the company from its founders and beginning the long work of professionalising what had been a freewheeling hobbyist outfit. The capstone came in September 1994, when Kirby floated Games Workshop on the London Stock Exchange, turning a Nottingham model company into a publicly traded one. The float gave the company permanent capital and a public scorecard. It also handed Kirby an enormous amount of room to run the business exactly as he saw fit — and how he saw fit would, over the next two decades, very nearly strangle the thing he had built.

III. The Walled City: Old GW and the Foil of Tom Kirby

To appreciate the turnaround that defines the modern Games Workshop, you first have to sit inside the strange, defensive world of "Old GW," and that world was built in the image of one man. Tom Kirby ran the company as chief executive and later as executive chairman across roughly two decades, and he held a corporate philosophy so contrarian that, reading the old annual reports today, you are not always sure whether you are looking at iconoclastic genius or slow-motion self-sabotage. For a long stretch it was the former. By the end it was unmistakably the latter.

Kirby's central article of faith was a single sentence he repeated in various forms: Games Workshop was "a model company, not a games company." On the surface this sounds like harmless brand positioning. In practice it was a doctrine with teeth. If you are a model company, then the quality of your rules — whether the game is balanced, whether it is fun to play competitively, whether tournaments are well-supported — is secondary. What you are really selling is the plastic and the experience of building and painting it. Everything else is a marketing expense to move models. Kirby genuinely believed the gameplay was the loss-leader and the miniatures were the product, and he organised the entire company around that conviction.

From that root grew a second, more corrosive principle: a proud refusal to listen to anyone outside the building. Kirby wrote, in black and white in annual reports, that Games Workshop did not conduct market research and did not ask its customers what they wanted, on the theory that the company understood the hobby better than the hobbyists did. There is a version of this that is admirable — the Steve Jobs "people don't know what they want until you show them" school. But Kirby took it to an isolationist extreme. The company had effectively no social media presence. Staff were discouraged or outright banned from interacting with fans on internet forums. And the legal department developed a reputation for aggression, firing off cease-and-desist letters at fan creators, animators, and small independent retailers who, in most cases, were doing nothing but evangelising the hobby for free.

Picture the absurdity from the customer's side. Here was a company with one of the most devoted fan bases in any consumer category — people who would happily spend hundreds of pounds and hundreds of hours inside its worlds — and its default posture toward those people ranged from silence to litigation. The fortress had pulled up its drawbridge and was pouring boiling oil on its own most loyal subjects. The community came to call it "Old GW" with real bitterness, a shorthand for a company that seemed to resent the very enthusiasm that sustained it.

For years the financials masked the rot, because the underlying IP was so strong that it could absorb a great deal of mismanagement. But by the early 2010s the cracks were structural. The share price stagnated. Margins drifted downward. The company leaned ever harder on price increases to hit its numbers — raising the cost of boxed kits year after year — which worked in the short run and poisoned customer goodwill in the long run. A hobbyist who already felt ignored now felt gouged. Cash flow tightened. And the cost of starting the hobby crept so high that the funnel of new recruits began to narrow, the slow-acting poison for any business that depends on continually replacing churned customers.

Then came the act that, more than any spreadsheet, symbolised the dead end. In early 2015, the company blew up Warhammer Fantasy Battles. Not quietly retired it — destroyed it, literally, inside the fiction. In a storyline known as "The End Times," the entire thirty-year-old Warhammer Fantasy world was annihilated, its setting shattered to make way for a new game built on different commercial logic. Whatever the internal rationale, the message the core fan base received was that three decades of lore, of armies they had collected and characters they had loved, had just been wiped off the map by the company that sold it to them. It was a creative and commercial nadir, and it alienated the very veterans who anchored the community. The walled city had finally turned its weapons on its own founding myth.

The remarkable thing is what happened next. Because at almost exactly the moment Old GW reached the bottom, the man who would invert nearly every one of Kirby's principles took the chief executive's chair.

IV. Six Words That Rebuilt a Company

On January 1, 2015 — the same window in which Warhammer Fantasy was being detonated — Kevin Rountree became chief executive of Games Workshop. He was not a charismatic outsider parachuted in to save the company, and that turns out to be the whole point. Rountree was the former chief financial officer, a Nottingham man who had come up inside the building, an accountant by training who understood the company's cash flows intimately and, just as importantly, understood exactly how badly the company had alienated the people who loved it. He inherited a business in structural decline with an angry, estranged fan base and a stock the market had largely stopped believing in.5

Rountree's first move was not a new product or a price cut. It was a sentence. He rewrote the company's internal mission statement, and the substance of the change came down to six words: the company would exist "to engage and inspire our customers." Read that against Kirby's doctrine — no market research, no listening, the customer as someone to be sold to rather than served — and you see how quietly radical it was. For the first time in a generation, the official, stated purpose of Games Workshop put the customer's experience at the centre rather than treating it as an afterthought to moving plastic. Mission statements are usually corporate wallpaper. This one was a reversal of two decades of philosophy, and Rountree meant it operationally, not rhetorically.

The first test arrived almost immediately, and at first it looked like a disaster. In July 2015, the company launched Warhammer Age of Sigmar, the new fantasy game built on the ashes of the world it had just destroyed. In an effort to make the game frictionless for newcomers, the designers stripped out the points system — the mechanism by which players build balanced armies of equal value before a match — and removed structured "matched play" rules entirely. The competitive veterans, already raw from the destruction of the old world, revolted. A game with no points system felt, to a serious player, like a sport with no agreed way to keep score. The backlash was loud and immediate.

Here is the hinge of the entire turnaround. Under the old regime, this is precisely the moment the company would have gone silent, dismissed the critics as a vocal minority, and pressed on, secure in the conviction that it knew better. Rountree did the opposite. He listened. In 2016, Games Workshop released the General's Handbook, which added points values and a proper matched-play framework back into Age of Sigmar — and it was built substantially on the feedback the community had been screaming into the void. The product got better because the company let its customers help fix it. More than the financial recovery that followed, that act of listening was the cultural Rubicon. The fortress had lowered its drawbridge, not to surrender, but to let the citizens back in.

The institutional expression of that new openness was the Warhammer Community website, which became the daily heartbeat of the new Games Workshop.6 Where Old GW had banned staff from talking to fans, New GW hired community managers whose entire job was to talk to fans. The company embraced social media, started posting daily — painting tutorials, lore deep-dives, sneak peeks at upcoming models, behind-the-scenes studio content, and a steady stream of self-deprecating jokes that signalled, more than any press release could, that the humans inside the building were hobbyists too. The relationship flipped from antagonistic to collaborative. Customers who had been treated as marks to be litigated against were now treated as partners in the hobby, and they responded with exactly the loyalty that posture invites.

Rountree also went after the structural problem Kirby's price hikes had created: the cost of getting in the door. Under the old regime, assembling a starter army could run to hundreds of pounds, a wall that turned curious newcomers away before they ever painted their first model. Rountree introduced curated boxed sets — the "Start Collecting!" range and later "Combat Patrol" boxes — that bundled a coherent starter army at a discount of roughly 30% or more versus buying the same kits individually. The strategic logic was pure funnel economics: lower the price of the first hit, get the hobbyist building and painting and emotionally invested, and let the lifetime value take care of the rest. It was the precise inverse of squeezing existing customers harder on price.

And then there were the ghosts. Games Workshop's back catalogue was full of beloved "specialist games" that Old GW had mothballed — Blood Bowl, the gleefully violent fantasy-football game; Necromunda, the gang-warfare skirmish game set in the underbelly of a hive city; Epic, the mass-scale version of 40K. These had cult followings of older, high-spending collectors who had grown up with them. Rountree's company brought them back, often in lavish new editions. This was a brilliant piece of low-risk, high-margin capital allocation: the worlds and the fan demand already existed, the development risk was modest, and the target customer was a nostalgic veteran with disposable income and an empty shelf to fill. You were not creating demand from scratch; you were re-opening a tap that the previous management had needlessly turned off.

For investors, the lesson of the Rountree pivot is almost embarrassingly simple, and that is what makes it powerful: a company sitting on a genuinely irreplaceable asset had spent two decades actively repelling the people who wanted to give it money, and a turnaround consisted, in large part, of simply stopping. The product engine had always been world-class. The cultural operating system around it had been the bottleneck. Fix the culture, and the financial renaissance follows — which is exactly what happened next.

V. The Two Engines: Core and Licensing

Walk through the numbers that the cultural turnaround produced and you start to understand why the market eventually dragged this Nottingham model company into the FTSE 100. In the decade from 2015, Games Workshop's revenues roughly tripled and its profits grew by something on the order of tenfold.[^2] That is not the trajectory of a mature toy company harvesting a stable franchise; it is the trajectory of a business that had been operating with a hand brake on for twenty years and finally released it. But the headline figures hide a more interesting structure underneath, because the modern company runs on two very different engines bolted to the same chassis.

The larger engine is the core business: designing, manufacturing, and selling the physical miniatures and the hobby products around them — paints, brushes, rulebooks, modelling tools. In the 2024/25 financial year, core revenue came to £565.0 million, the overwhelming majority of the company's top line.[^2] What makes this number remarkable is not its size but how it is earned, because Games Workshop does almost everything itself, in a way that runs against every instinct of modern manufacturing orthodoxy.

Consider what the textbook would tell you to do. You have a high-value branded product and cheap labour available across Asia; you outsource the manufacturing to a contract producer in a low-cost jurisdiction, you go asset-light, and you pocket the margin. Games Workshop does the reverse. It designs, tools, and injection-moulds its plastic miniatures at its own facilities in Nottingham, in a high-cost developed economy, and it has steadily added factory and warehouse capacity there rather than offshoring.[^8] The reason is control. When the entire value of your product rests on the crispness of the detail in the plastic — the rivets on a tank, the filigree on a suit of power armour — and on absolute consistency batch to batch, owning the factory is not a cost to be minimised but the thing that protects the brand. Vertical integration here is a quality moat dressed up as a manufacturing decision.

The second piece of the core engine is the retail network: over 540 Warhammer stores spread across the world.[^2] But to call them "stores" undersells what they actually are. A standard retailer exists to convert demand that already exists into a transaction. A Warhammer store exists to manufacture demand. Walk into one and you will typically find a member of staff teaching a newcomer — very often a child or a teenager, very often for free — how to assemble a model, how to paint it, how to play a first game on the tables that occupy a large share of the floor space. The store is a customer-acquisition funnel disguised as a shop. Its job is to take curious foot traffic and convert it, patiently, into a high-lifetime-value hobbyist who will spend for years or decades. The four walls are a recruitment centre for the hobby, and they happen to also sell paint.

Now to the second engine, which is far smaller in absolute terms but tells you something profound about where the business is heading. This is licensing: the business of letting other companies — video game studios, board game makers, apparel firms, and now film and television producers — pay Games Workshop for the right to use its worlds and characters. In 2024/25, licensing revenue reached £52.5 million, up a startling 69% from £31.0 million the prior year.[^2] That growth rate, on its own, would make the segment interesting. What makes it extraordinary is the margin.

Licensing is as close to pure profit as a real business gets. When a games studio pays Games Workshop a royalty to make a Warhammer video game, the company does not have to buy steel tooling, mould any plastic, ship any boxes, or staff any stores to earn that money. The intellectual property already exists; it was paid for long ago in the writing of forty years of novels and rulebooks. The incremental cost of letting one more partner build on top of it is close to nothing. In practice the segment runs at something approaching a 100% operating margin — high-velocity cash flow that lands on the income statement with almost no capital expenditure and almost no working capital tied up behind it.[^2] It is the rare line item where the marginal pound of revenue is very nearly a marginal pound of profit.

Hold those two engines side by side and the shape of the company comes into focus. The core business is the fortress: capital-intensive, physical, slow to build, and almost impossible for a rival to replicate, throwing off the bulk of the cash. The licensing business is the catapult mounted on the fortress wall: tiny by comparison today, requiring almost nothing to operate, and capable of launching the brand into the minds of hundreds of millions of people who have never set foot in a hobby store. The question of what Games Workshop does with all the cash those engines generate is where the story turns genuinely unusual — because the answer is, emphatically, "not what everyone else does."

VI. The Company That Refuses to Buy Things

In the modern playbook of corporate growth, there is one move that managements reach for above almost all others when they have cash and ambition: they buy other companies. Acquisitions promise instant scale, new capabilities, a bigger empire to preside over, and a story to tell investors about transformation. Games Workshop looks at that playbook and, as a matter of stated policy, declines to open it. Its approach to mergers and acquisitions is essentially zero. It does not buy other companies, on the explicit theory that acquisitions dilute the culture it spent so much pain rebuilding, distract a small management team from the work of making and selling miniatures, and almost always represent a worse use of capital than simply doing more of what already works.[^3]

To a certain kind of growth investor this sounds like timidity. To understand why it is closer to wisdom, you only have to look across the toy and gaming landscape at the companies that did reach for the M&A lever, and watch what it did to them.

Start with Hasbro, the American toy and games conglomerate behind Monopoly, Transformers, and Dungeons & Dragons. In 2019, hungry for "content creation capacity" — the ability to turn its toy brands into films and television — Hasbro acquired the entertainment studio Entertainment One, known as eOne, for roughly $4 billion. The logic was fashionable: own the pipes that turn intellectual property into screen content. The execution was a catastrophe. By 2023, having concluded that the acquisition no longer fit its strategy, Hasbro sold eOne's film and television business to Lionsgate. The headline price was around $500 million, of which roughly $375 million was cash, with Lionsgate also assuming production financing loans.78 Read those two numbers together: roughly $4 billion paid, roughly half a billion recovered four years later. A multi-billion-dollar shareholder bonfire, lit in pursuit of exactly the "content capacity" that Games Workshop instead acquires by simply licensing its IP to others and collecting cheques.

Then there is the cautionary tale of Embracer Group, the Swedish gaming roll-up that for a few years embodied the opposite of the Games Workshop philosophy. Embracer pursued growth through relentless, debt-fuelled acquisition, hoovering up studios and intellectual property — including, famously, the rights to Tolkien's Middle-earth — on the theory that scale and a vast IP library would compound into something great. Then a roughly $2 billion investment deal collapsed, the debt came due, and the strategy detonated. Between June 2023 and 2024, the restructuring that followed cost something on the order of 4,500 jobs and shut down dozens of studios, with beloved development houses extinguished and projects cancelled. In April 2024, Embracer announced it would break itself apart into three separately listed companies.9 The roll-up that had been assembled with borrowed money had to be dismantled to survive. It is hard to imagine a sharper illustration of why a debt-free company that grows organically might sleep better at night.

The contrast extends east, to the giants of Asian gaming. Companies like 腾讯控股 Tencent and 网易 NetEase have spent enormous sums acquiring or taking stakes in game studios around the world, buying their way to the IP and the talent they want to control. Games Workshop inverts the entire relationship. It does not pay studios for access to worlds; it makes studios pay it for the privilege of building on the world it already owns. When the flow of money between an IP owner and the industry's biggest spenders runs toward you rather than away from you, you are sitting in a structurally enviable seat — and you reach it not by spending billions but by having spent four decades building something no amount of money can buy after the fact.

So if Games Workshop does not deploy its cash on acquisitions, where does it go? The answer is a capital-allocation framework so disciplined it borders on the ascetic. The company runs a clean, debt-free balance sheet with no structural hedging — no clever financial engineering, no leverage juicing the returns.[^2] It calculates the cash it actually needs and refuses to hoard a penny more. The required buffer is defined with almost monastic precision: roughly three months of operating expenses — on the order of £85 million — plus about three months of tax, plus the planned capital expenditure for tooling and factory expansion, plus the money set aside for employee bonuses.[^2] That is the reserve. Everything the business generates above that line is treated as belonging to the shareholders and is returned to them as dividends.

The discipline here is the part worth dwelling on, because it is so rare. Most companies hoard cash "just in case" — building war chests that, conveniently, also fund the empire-building acquisitions that destroy value. Games Workshop does the opposite. It does not keep money it cannot justify. If it has an exceptional quarter, it does not sit on the windfall; shareholders are liable to receive a special dividend within weeks. The dividend is not a residual afterthought paid out of what is left over. It is the default destination for capital, and the burden of proof falls on any pound that wants to stay inside the company rather than on any pound that wants to leave. It is one of the purest expressions of a "return it unless you can prove you'll compound it better" philosophy in the public markets — and it works only because the underlying business needs so little capital to keep growing. That same philosophy, it turns out, runs straight through how the company pays its own people.

VII. Nottingham Rules: Incentives and Culture

If you wanted to find the headquarters of a FTSE 100 company, you would not naturally look where Games Workshop sits. There is no marble lobby in Mayfair, no glass tower with the company's name backlit against the London skyline. The nerve centre is in Lenton, an industrial part of Nottingham, co-located with the factory and the warehouse — the place where the plastic actually gets moulded and the boxes actually get packed.[^8] That geography is not an accident or a cost-saving compromise; it is a statement of identity. This is a working company run by people who think of themselves as makers, and the culture that flows from that self-image shapes everything from executive pay to how the rank and file share in the spoils.

Start at the top, with Kevin Rountree's own incentives, because they are unusually well-aligned for a public-company chief executive. For the 2024/25 financial year, Rountree received total remuneration of approximately £4.41 million, built on a comparatively modest base salary of £726,000.[^2] In an era of eye-watering CEO packages, the base is almost restrained, and the bulk of the pay is performance-linked rather than guaranteed. But the genuinely interesting mechanism is not the size of the package; it is the rule governing what the executives must do with the variable part of it.

Games Workshop's executive directors are required to take at least two-thirds — 67% — of their annual performance bonus and use it to buy company shares on the open market, with their own bonus money, at the prevailing price.[^2] And once bought, those shares must be held for a minimum of three years. Sit with the design of that for a moment. It means an executive cannot simply collect a bonus in cash and walk away; a majority of that bonus is converted into ownership, at market price, and locked up. It forces management to eat its own cooking — to become substantial long-term shareholders whose personal wealth rises and falls with the same shares the public owns. Rountree himself held 21,965 shares, worth on the order of £3.5 million, a meaningful personal stake that ensures his interests and the outside shareholder's interests point in the same direction.[^2] This is "skin in the game" not as a slogan but as a binding contractual mechanism.

Then comes the part of the culture that, more than any other, explains the loyalty inside those Nottingham walls — and it sits at the opposite end of the hierarchy from the executive suite. Games Workshop runs a profit-sharing scheme, and the word that matters in describing it is "equally." In 2024/25, the company distributed £20.0 million in profit-share bonuses among its workforce — and the distribution was made on an equal basis across the rank and file: the factory workers running the moulding machines, the warehouse staff packing the boxes, the store managers teaching children to paint.[^2] When the company has a great year, the person packing the boxes shares in the upside on the same footing as far more senior colleagues.

Think about what that does to the texture of the place. £20 million spread broadly and equally across a workforce is a serious sum per head, and it lands not as a discretionary favour from on high but as a structural feature of working there: the company wins, you win, and your share is not determined by your rank in the org chart. It is hard to overstate how powerful that is for morale, retention, and the kind of discretionary care that shows up in product quality. It also, not incidentally, tends to make trade union organising a hard sell — it is difficult to rally workers against management when management has built equal upside-sharing directly into the deal. The Nottingham working-class ethos is not marketing; it is wired into the cash flows.

Step back and you can see the architecture of the whole thing. The customer is served — engaged and inspired, in the language of the mission statement — which drives the revenue. The employees share in the resulting profits equally, which drives the loyalty and the quality that keep customers coming. And the shareholders, including the executives forced to become shareholders, collect the surplus as dividends. Customer, employee, owner: three constituencies that most companies treat as locked in zero-sum tension, wired here into a single reinforcing flywheel. And the newest, fastest-spinning part of that flywheel is the engine we have so far only glimpsed — the one that is about to put Warhammer in front of an audience a thousand times larger than any hobby store could reach.

VIII. The Catapult: Licensing, Space Marines, and Amazon

For most of its history, Games Workshop's worlds lived where the company made them: on tabletops, in rulebooks, and in the imaginations of a devoted but finite community. The catapult that is now flinging those worlds into the mainstream consciousness is licensing, and to understand why the segment's revenue leapt 69% in a single year, you have to look at one product that detonated in the autumn of 2024.

In September 2024, a video game called Warhammer 40,000: Space Marine 2 launched, developed by Saber Interactive and published by Focus Entertainment.4 It was a third-person action game that put the player inside the armour of a Space Marine — one of those genetically engineered super-soldiers at the heart of the 40K mythos — wading through tides of alien monsters. It was, by any commercial measure, a phenomenon. The game sold two million copies in its first twenty-four hours, and within roughly three months it had surpassed five million copies sold.10 For Games Workshop, which earns a royalty on each of those sales without having written a line of the game's code or spent a pound on its marketing, the hit single-handedly drove the surge in licensing revenue.[^2] It was the licensing model working exactly as designed: someone else takes the development risk and the capital outlay, and Games Workshop collects a high-margin royalty on a runaway success.

But Space Marine 2, for all its scale, was a video game — a product aimed largely at people who already had some awareness of the brand. The deal that has the potential to change the company's trajectory altogether aims at everyone else: the hundreds of millions of people who have never heard the phrase "in the grim darkness of the far future."

In December 2024, after a long and genuinely fraught negotiation, Games Workshop finalised an agreement with Amazon to develop films and television set in the Warhammer 40,000 universe.[^6] The word "fraught" is doing real work there. By multiple accounts the deal nearly collapsed, and it nearly collapsed over a single issue: creative control. Games Workshop, having spent four decades and one near-death cultural experience learning exactly how much its fan base cares about the integrity of the lore, refused to hand its universe to a studio that might reshape it for mass appeal. The company insisted on extensive creative veto power over how its world would be depicted on screen — the right to protect the canon from being diluted, sanitised, or simply gotten wrong. That a small Nottingham model company could stare down one of the most powerful media and technology businesses on earth, and win meaningful creative authority, is itself a measure of how much leverage genuinely irreplaceable IP confers.

The human face of that protection is Henry Cavill. The actor — a lifelong, openly obsessive Warhammer hobbyist who has spoken publicly about painting his own miniatures — attached himself to the project as both star and executive producer. His role is not merely to draw an audience. It is to serve as the creative bridge between Amazon's commercial machinery and Games Workshop's intensely protective fan base, a credible signal to the faithful that the adaptation is being shepherded by someone who actually understands and loves the forty-year-old canon rather than someone treating it as interchangeable content. In an IP this beloved and this easy to get wrong, a trusted steward is not a nice-to-have; he is risk insurance made flesh.

The structure of the deal reveals the strategy underneath it. The agreement grants Amazon exclusive rights to the Warhammer 40,000 universe for film and television, with an option to later license the Warhammer Fantasy and Age of Sigmar universe as well — but that second universe is gated on the commercial success of the first.[^6] This is a sensible, optionality-laden design: prove the model with the crown-jewel setting, and only then extend it to the secondary one. Management has indicated that the first productions are expected to reach screens in the window of roughly 2027 to 2029.[^6] For Games Workshop, the financial character of all this is the now-familiar magic of the licensing engine: a potential multi-decade royalty stream, with the entire capital cost of production — the budgets, the sets, the visual effects, the marketing — borne by Amazon, not by Nottingham.

It is worth being clear-eyed about the asymmetry here, because it is the whole investment case for the segment in miniature. If the adaptations fail, Games Workshop has risked very little real capital; the downside is largely a brand-reputation question, mitigated by the creative controls it fought so hard to win. If they succeed, the prize is enormous and self-reinforcing — not just the royalty cheques, but a wave of newly minted fans who, having met the Space Marines on a screen, walk into one of those 540-odd stores to meet them in plastic. The screen adaptation is, in a sense, the most powerful customer-acquisition funnel the company has ever had access to, and it is being built almost entirely with someone else's money. To understand why all of this holds together so durably, it helps to put the whole enterprise under the lens of formal strategy.

IX. Anatomy of a Fortress: 7 Powers and Five Forces

Strip away the plastic and the lore and the Nottingham charm, and what makes an investor's pulse quicken about Games Workshop is the durability of its competitive position. The frameworks built to diagnose exactly that — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — are unusually flattering when pointed at this company, because it happens to stack several distinct, mutually reinforcing advantages rather than relying on any single one. Let us walk the walls.

The deepest of the powers is what Helmer calls a cornered resource: control of a coveted asset that produces outsized returns and that rivals simply cannot obtain. For Games Workshop, the cornered resource is the intellectual property itself — the worlds, the iconography, and above all the lore. No competitor can legally make a Space Marine, a Chaos Daemon, an Ork, or any of the hundreds of other entities that populate these universes. And crucially, the moat is not just legal but temporal. The lore is forty years deep, accreted across hundreds of novels, rulebooks, codices, and interlocking character arcs. Even if a rival could somehow ignore the trademarks, it could not manufacture four decades of accumulated narrative and the emotional attachment fans have formed to it. You cannot speed-run history.

The second wall is customer lock-in, and in this hobby the switching costs are unusually, almost physically, high. Consider a hobbyist who has spent something like $2,000 and hundreds of hours assembling, converting, gluing, and painting a 2,000-point army of Space Marines. That investment is not just financial; it is sunk time, accumulated skill, and emotional attachment. To switch to a competing miniatures system — whether a rival wargame or the model kits of a company like 株式会社バンダイナムコホールディングス Bandai Namco Holdings — would mean abandoning the painted army, relearning a new rules system, and walking away from the local community that plays the game they already know. The physical assets, the rules knowledge, and the social network are all locked to the Warhammer ecosystem. Few consumer products bind a customer with that many simultaneous tethers.

That social dimension points to the third power, network effects, which in tabletop wargaming are real and badly underappreciated. This is an inherently social, multiplayer hobby; a beautifully painted army has no purpose unless you can find an opponent to play against. The value of being a Warhammer player rises with the number of other Warhammer players nearby. And because Games Workshop commands the dominant share of the high-end miniature wargaming market — on the order of 70% or more — the default game at any given local hobby shop, club, or kitchen table tends to be Warhammer. A newcomer choosing a system to invest in rationally picks the one with the most opponents available, which is the one that already has the most opponents, which deepens the lead. The network compounds.

The fourth and fifth walls are about manufacturing, and they are why even a well-funded rival struggles to compete on the product itself. Scale economies show up in the brutal economics of injection moulding. Producing a multi-part plastic miniature to Games Workshop's fidelity requires high-precision steel tooling — moulds that can cost tens of thousands of dollars each to cut. That is an enormous up-front capital barrier that an independent competitor, serving a fraction of the market, cannot easily justify or amortise. But once the tooling exists and the volume is there to spread its cost, the marginal cost of stamping out another plastic sprue is measured in pennies. High fixed cost, trivial marginal cost, large volume to spread it over: that is the textbook recipe for a scale advantage, and it lets Games Workshop offer detail at a price a sub-scale rival cannot match. Layered on top is process power — the decades of hard-won institutional knowledge in engineering hyper-detailed, multi-part plastic sprues that fit together cleanly and do not warp. That know-how is not written down in any manual a competitor could buy; it lives in the accumulated experience of the design and tooling teams, and it cannot be acquired quickly at any price.

Run the same business through Porter's Five Forces and every arrow points the same comforting direction. The threat of new entrants is very low, blockaded by both the tooling-cost barrier and the un-replicable depth of the lore. The bargaining power of buyers is low, because the customers are passionate, relatively price-inelastic hobbyists emotionally invested in the worlds — which is precisely the dynamic Games Workshop abused under Old GW's price hikes and now wields more carefully. The threat of substitutes is lower than it first appears: video games and other entertainment compete for leisure time, but they do not substitute for the specific, meditative, tactile, social experience of building and painting a physical model and playing it across a table with a friend. And the intensity of competitive rivalry is muted, because in high-end miniature wargaming Games Workshop operates less like one combatant among many and more like a benevolent monopolist setting the terms of the category.

The honest caveat, and the reason this section is analysis rather than a victory lap, is that fortresses can still be undone — usually not by a frontal assault on the strongest wall but by a flanking move that makes the wall irrelevant. So before we leave the strategic high ground, it is worth turning to face the threats that a thoughtful skeptic would raise, and the upside a believer would counter with.

X. Bull, Bear, and the Things That Could Change the Story

Every fortress has a postern gate, and for Games Workshop the bear case starts at the one technology genuinely capable of routing around its manufacturing moat: 3D printing. The logic of the threat is straightforward and, on its surface, alarming for a company whose scale advantage rests on expensive steel tooling. If a hobbyist can buy a high-resolution home resin printer — an SLA machine that cures liquid resin layer by layer into finely detailed objects — and download or design model files, then in principle they can bypass the entire Games Workshop supply chain. The tooling barrier that keeps competitors out becomes, from this angle, irrelevant to a customer who can simply print at home. For a business that earns its margins on physical plastic, that is the threat that deserves to keep management awake.

The counter-argument is more robust than the threat first suggests, though it is not airtight. Resin printing remains, for now, a meaningfully worse consumer experience than buying a boxed kit: liquid photopolymer resin is toxic and requires careful handling and ventilation, the process is messy, post-processing is fiddly, and the whole thing demands a level of technical commitment that the convenience of walking into a store and buying a clean injection-moulded kit does not. Just as importantly, Games Workshop's intellectual property protection acts as a powerful defence at exactly the point of community: printing pirated copies of GW designs is a copyright violation, and the company can and does enforce a "GW models only" norm on the tables of its own stores and at its official events, denying printed armies access to the social heart of the hobby. The network effect and the IP, in other words, defend the manufacturing moat that the technology threatens. Still, an investor should watch this honestly: printing technology improves every year, and convenience gaps have a way of closing.

The second strand of the bear case is valuation, and it is the more immediate risk. Following its ascent, the stock has traded at premium multiples — a price-to-earnings ratio in the region of 25 to 30 times.23 A multiple like that prices in continued excellence and leaves little margin for disappointment. It means the market is already paying for the turnaround to keep compounding and for the new licensing catalysts to land. If the Amazon adaptations stumble creatively, or if a stretch of core product releases underwhelms the community, or if growth simply decelerates from its torrid recent pace, a stock priced for perfection can correct sharply even without anything fundamentally breaking in the business. Premium quality and premium price are not the same thing, and the gap between them is where shareholder risk lives.

Turn the page to the bull case and the geography of the opportunity opens up. The most concrete lever is global underpenetration. Games Workshop's strength has historically been concentrated in the United Kingdom, parts of Europe, and pockets of North America, while vast, wealthy markets — much of East Asia, and large stretches of North America beyond the existing strongholds — remain lightly penetrated relative to their potential. A hobby this culturally portable, with this much accumulated content to draw newcomers in, has a long runway simply by planting more recruitment-centre stores in places it has barely touched.

The grander bull argument is the one we have already seen taking shape: the prospect of a Disney-scale royalty flywheel. If the screen adaptations succeed, Warhammer crosses over from a beloved niche into mainstream cultural property, in front of an audience measured in the hundreds of millions rather than the millions. Mainstream awareness drives new hobbyists into physical stores; a larger installed base of hobbyists deepens the network effects, increases the value of the licensing IP, and feeds the core business — which funds more stores and more worlds, which feeds the next adaptation. The screen deal is not just a royalty line item; it is potentially the largest top-of-funnel the company has ever had, financed largely by someone else.

For an investor trying to cut through all of this, the noise resolves into a small number of things genuinely worth tracking. The first is the trajectory of licensing revenue — the segment is the highest-margin, fastest-growing, most asymmetric part of the company and the clearest read on whether the IP is successfully escaping the tabletop; its growth rate is the single most informative number in the report. The second is core revenue growth alongside the store count, taken together, because that pairing reveals whether the underlying hobby is still recruiting new participants or merely harvesting existing ones — the health of the funnel, not just the till. Those two readings, more than any single quarter's profit figure, tell you whether the flywheel is still turning. Everything else — the margins, the dividends, the ROCE — has tended to follow when those two are healthy.

XI. What the Toy Soldiers Teach

There is a lesson in Games Workshop that runs directly against the grain of the last quarter-century of business fashion, and it is worth stating plainly. The prevailing wisdom has told companies to go asset-light: outsource the factory, rent the cloud, own the brand and the customer relationship and let someone else, somewhere cheaper, make the physical thing. Games Workshop did almost the opposite and built a compounding machine out of it. It owns its factory in a high-cost country. It owns its stores. It owns its intellectual property outright. And by controlling all three at once, it created something that no asset-light competitor and no deep-pocketed acquirer has been able to dislodge. Vertical integration, the supposedly obsolete strategy, turns out to be very much alive when the thing you are integrating is irreplaceable.

The deeper lesson belongs to Kevin Rountree, and it is not really about plastic at all. The achievement of the turnaround was the recognition that a great business is a system of aligned constituencies, and that the previous regime had broken the alignment by treating customers as adversaries. Rountree's quiet genius was to wire the three constituencies back together: customers engaged and inspired rather than gouged and ignored, employees sharing equally in the profits their work generates, and shareholders — including the executives compelled to become shareholders — receiving the disciplined return of every pound the business cannot productively reinvest. Each group's gain reinforces the others. That tripartite flywheel, far more than any single product or even the irreplaceable lore, is what turned a Nottingham model company into a member of the FTSE 100 — and it is the part of the story that any founder or investor, in any industry, can learn from.

References

-

FTSE UK Index Series Quarterly Review December 2024 — London Stock Exchange ↩

-

The Nottingham Toy Soldiers: Games Workshop's Turnaround — Financial Times ↩

-

Hasbro Completes Sale of Entertainment One Film and Television Business to Lionsgate — Hasbro, 2023-12-27 ↩

-

Lionsgate Closes eOne Acquisition for $375 Million — Variety, 2023-12-27 ↩

-

Embracer Group Announces Intention to Transform into Three Standalone Publicly Listed Entities — Embracer Group, 2024-04-22 ↩

-

Warhammer 40,000: Space Marine 2 Surpasses 5 Million Copies Sold — KitGuru, 2024-11 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube