Experian: From Credit Bureau to Global Data Powerhouse

I. Introduction & Episode Roadmap

Picture this: Every time you apply for a credit card, lease an apartment, or even sign up for a new phone plan, there's a silent arbiter in the background—a vast machine humming with algorithms and databases, determining your financial worthiness in milliseconds. That machine has a name: Experian. And its tentacles reach far deeper into your life than you might imagine.

Today, Experian holds data on over 1 billion people worldwide and 235 million U.S. consumers. It's one of the "Big Three" credit-reporting agencies alongside TransUnion and Equifax—a triumvirate that effectively controls access to credit in much of the developed world. With a market capitalization north of $35 billion, this Dublin-headquartered, London-listed giant processes 1.5 billion credit decisions annually and generates over $6 billion in revenue.

But here's what's fascinating: Unlike its peers, which trace their lineage directly through American credit bureaus, Experian emerged from the most unlikely of places—the data division of a British mail-order catalog company. How did a subsidiary buried inside Great Universal Stores (GUS), a company better known for selling sofas and argos catalogs, transform into one of the world's most powerful data brokers?

The answer involves aerospace engineers predicting cashless societies, Dallas merchants pooling credit blacklists, Brazilian entrepreneurs building Latin America's credit infrastructure, and a series of strategic pivots that would make any Silicon Valley founder jealous. It's a story of how data became the new oil, how a sleepy division became worth more than its parent, and how a company built for the analog age reinvented itself as a digital powerhouse.

Over the next several hours, we'll trace this unlikely journey—from 19th-century London coffeehouses where merchants first swapped debtor lists, through the conglomerate years under GUS, to the modern era where Experian uses AI to score creditworthiness based on your Netflix subscription payments. We'll examine transformational deals like the Serasa acquisition that gave Experian dominance in Brazil, dissect massive data breaches that threatened its reputation, and analyze how the company navigates the tension between being both a guardian and monetizer of personal data.

This is the story of how information asymmetry became a $35 billion business, and what it means for the future of finance, privacy, and economic access in the digital age.

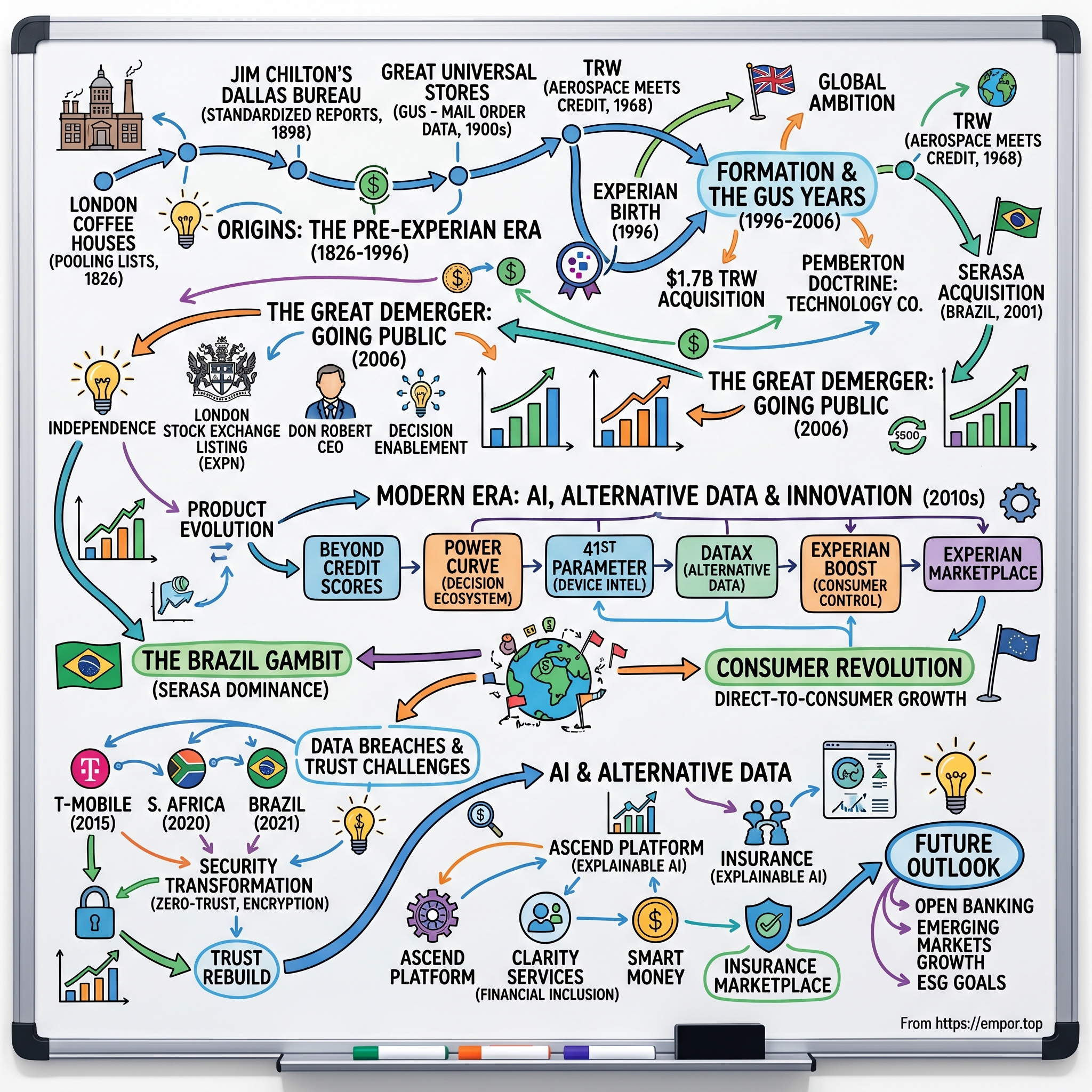

II. Origins: The Pre-Experian Era

The London Coffee House Lists

In 1826, a group of London tailors gathered in a smoky coffeehouse near Threadneedle Street with a radical idea: What if, instead of each merchant getting burned by the same deadbeats, they pooled their knowledge? They began compiling lists—simple handwritten ledgers of customers who had failed to pay their bills. The Manchester Guardian Society, formed that same year, took this concept further, creating formal mechanisms for merchants to share credit information. These weren't sophisticated databases; they were essentially communal blacklists, passed hand to hand like contraband.

This was the primordial soup from which the modern credit industry would emerge. The fundamental insight—that information about payment history had value, and that this value multiplied when shared—would remain unchanged for the next two centuries. What would change was everything else: the technology, the scale, the sophistication, and ultimately, the power wielded by those who controlled this information.

Jim Chilton's Dallas Revolution

Fast forward to 1898. In Dallas, Texas, a grocer named Jim Chilton was having his own epiphany. Tired of extending credit to customers who had already stiffed every other merchant in town, Chilton began going door to door, convincing his competitors to share their deadbeat lists. But Chilton went further than the London tailors—he didn't just compile lists; he created a business model. For a fee, any merchant could access his consolidated records.

What made Chilton revolutionary wasn't just the information sharing—it was his recognition that credit data was a product that could be packaged, priced, and sold. His Retail Credit Company (which would eventually become part of Equifax) introduced a crucial innovation: the credit report as a standardized document. No longer were merchants swapping gossip; they were purchasing intelligence.

By the 1920s, Chilton's model had spread across America. Local credit bureaus sprouted in every major city, each maintaining files on their region's consumers. The system was fragmented, manual, and riddled with errors—but it worked well enough that by mid-century, these bureaus had become essential infrastructure for American commerce.

Abraham Rose and the Mail-Order Data Revolution

Meanwhile, across the Atlantic, a different data story was unfolding. In 1900, Abraham Rose, the son of Polish-Jewish immigrants, started Universal Stores in Manchester with £100 borrowed from his father. Rose's innovation wasn't selling products—it was selling them on credit to working-class customers who couldn't afford upfront payments.

By the 1930s, Universal Stores (later renamed Great Universal Stores, or GUS) had become Britain's largest mail-order company. But here's what made GUS special: To manage millions of credit accounts, the company had to build sophisticated data operations. Every customer interaction—every payment, every default, every purchase pattern—was meticulously recorded. GUS wasn't just a retailer; it was sitting on one of the UK's largest consumer databases.

The company's data capabilities became so sophisticated that by the 1970s, GUS was processing credit applications not just for its own sales, but for other retailers too. The tail was beginning to wag the dog—the data division was becoming more valuable than the retail operation it was meant to support.

TRW: When Rocket Scientists Discovered Credit

The third strand of Experian's DNA comes from the most unlikely source: aerospace engineering. In 1953, Simon Ramo and Dean Wooldridge, two brilliant engineers, left Hughes Aircraft to form Ramo-Wooldridge Corporation, later known as TRW. The company initially focused on building ICBMs and spacecraft—they were the technical managers for the entire U.S. ballistic missile program.

But Simon Ramo was a visionary who saw beyond rockets. In 1961, he made a prediction that seemed like science fiction: "We are heading toward a cashless society where all transactions will be electronic." While his aerospace colleagues scoffed, Ramo began positioning TRW to capitalize on this future.

In 1968, TRW made a move that puzzled Wall Street: they acquired Credit Data Corporation, a small credit bureau. Why would a company building moon rockets want to get into credit reporting? Ramo understood something others didn't—the same mainframe computers and data processing capabilities that could calculate missile trajectories could also track consumer payment histories at unprecedented scale.

TRW Information Services grew explosively through the 1970s and 1980s. They were the first to fully digitize credit files, the first to offer instant credit reports via computer terminals, and the first to achieve truly national coverage in the U.S. By 1990, TRW's credit bureau was processing 50 million credit reports annually and had become one of the company's most profitable divisions.

The Stage is Set

By the mid-1990s, these three streams—British retail data expertise, American credit bureau infrastructure, and aerospace-grade computing capabilities—were about to converge in a way no one could have predicted. GUS, looking to expand internationally, had its eye on TRW's credit operations. TRW, struggling with defense budget cuts after the Cold War, was eager to divest non-core assets.

The matchmakers were an unlikely pair: Sir Ernest Harrison, GUS's chain-smoking chairman who had built the company into a retail empire, and Joseph Gorman, TRW's CEO who needed to raise cash to shore up the aerospace business. Their negotiations would create something neither fully understood at the time—a data company that would eventually dwarf both of its parents.

The confluence of these historical streams—London merchants sharing blacklists, Dallas grocers building credit bureaus, British retailers amassing consumer data, and rocket scientists applying computing power to credit—would culminate in 1996 with the birth of Experian. But that moment of creation was just the beginning of an even more remarkable transformation.

III. Formation & The GUS Years (1996–2006)

The Deal That Almost Didn't Happen

October 1996. In a boardroom overlooking the Thames, Sir Ernest Harrison stubbed out his cigarette and stared at the numbers one more time. GUS was about to spend $1.7 billion—nearly a quarter of its market value—to acquire TRW's Information Services division. Board members were nervous. "We're a British retailer," one director reportedly said. "What do we know about running an American credit bureau?"

Harrison's response was vintage: "We know data. We've been collecting it longer than anyone in this room has been alive."

The acquisition nearly fell apart three times. First, when U.S. regulators raised concerns about foreign ownership of sensitive financial data. Second, when TRW tried to back out after receiving a higher bid from a private equity consortium. And third, when GUS's own shareholders revolted, arguing the price was too rich for an unfamiliar business.

But Harrison, then 69 and nearing the end of his legendary career, saw something others missed. The convergence of GUS's CCN (Consumer Credit Nottingham) division with TRW's credit bureau wouldn't just create scale—it would create the world's first truly global credit reporting agency. While Equifax and TransUnion were still primarily U.S.-focused, this new entity would span continents from day one.

Birth of a Brand

The combined entity needed a name. Marketing consultants proposed dozens of options—DataTrust, GlobalCredit, InfoMax. All were rejected. Then someone suggested "Experian"—a portmanteau of "experience" and "erian" (suggesting an era or period). It sounded modern, tech-forward, and crucially, meant nothing in any language—avoiding the translation problems that had plagued other global brands.

John Peace, brought in as CEO of the new division, later recalled the naming meeting: "We wanted something that sounded like it could have existed for a hundred years or been invented yesterday. Experian hit that sweet spot."

The integration was brutal. TRW's American managers, accustomed to Silicon Valley-style autonomy, chafed under GUS's more hierarchical British corporate culture. The IT systems were incompatible—GUS ran on IBM mainframes while TRW used Unisys. Customer databases used different formats, credit scoring models were inconsistent, and even basic terminology differed between the UK and U.S. operations.

The Pemberton Doctrine

Enter Don Robert, an American executive who would become Experian's transformational leader. Brought in initially as head of North American operations in 1998, Robert introduced what became known internally as the "Pemberton Doctrine"—named after Experian's new Nottingham headquarters on Pemberton Road.

The doctrine was simple but revolutionary for a company born from a retail conglomerate: "We are not a credit bureau that happens to use technology. We are a technology company that happens to be in the credit business."

This shift in mindset drove massive investments. Between 1998 and 2003, Experian spent over $2 billion on technology infrastructure—more than GUS had spent on IT in its entire previous history. They built one of the world's largest Oracle databases, pioneered real-time credit decisioning systems, and were among the first to use neural networks for fraud detection.

The results were staggering. Response times for credit checks dropped from hours to seconds. Accuracy improved from 94% to 99.7%. And perhaps most importantly, Experian could now offer services its competitors couldn't—like real-time credit monitoring and instant pre-approval for loans.

The Latin American Gambit

While competitors focused on mature markets, Experian made a contrarian bet on Latin America. In 2001, they acquired a 20% stake in Serasa, Brazil's largest credit bureau, for $135 million. Wall Street was skeptical—Brazil was emerging from a currency crisis, inflation was rampant, and the credit market was nascent.

But Don Robert saw opportunity where others saw risk. "In the U.S., everyone already has a credit file," he told investors. "In Brazil, we're creating files for 100 million people who've never had access to credit before. That's not market share growth—that's market creation."

The Serasa partnership would prove prescient. As Brazil's economy stabilized and consumer credit exploded—growing 20% annually from 2003 to 2007—Experian was perfectly positioned. The initial stake that seemed expensive at $135 million would be worth over $2 billion by the time Experian acquired full control.

Life Inside the Conglomerate

Being part of GUS was both a blessing and a curse. The blessing was capital—GUS's stable cash flows from retail operations funded Experian's aggressive expansion. Between 1996 and 2006, Experian acquired 47 companies, spending over $3 billion on M&A. These weren't random purchases but strategic moves to build capabilities: Scorex for analytics, ConsumerInfo.com for direct-to-consumer services, and Fujitsu's UK credit business for market share.

The curse was perception. Investors valued GUS as a retailer, applying retail multiples to what was increasingly a high-margin data business. In 2005, Experian generated £1.4 billion in revenue with EBITDA margins of 28%—comparable to enterprise software companies trading at 20x EBITDA. Yet buried inside GUS, trading at 8x EBITDA, Experian was valued at less than half its potential worth.

There was also cultural tension. GUS board meetings spent hours debating sofa designs and Christmas catalog layouts, while Experian executives wanted to discuss API strategies and machine learning algorithms. John Peace later described it as "like being a Formula One team owned by a bicycle manufacturer—supportive, but fundamentally not understanding what we did."

The Tipping Point

By 2005, the situation had become untenable. Experian generated 31% of GUS's revenue but 45% of its profits. The data division's growth rate was three times that of the retail operations. Investment bankers circled constantly, pitching spin-off scenarios with eye-watering valuations.

The catalyst came from an unexpected source: Walmart. In January 2006, the retail giant announced it was entering UK financial services, partnering with—Experian's competitor, Equifax. The message was clear: As long as Experian remained part of GUS, major retailers would see it as a competitor rather than a partner.

Sir Victor Blank, who had replaced Harrison as GUS chairman, made the call. In a board meeting in March 2006, he announced: "It's time to set Experian free."

The demerger announcement would come four months later, but the decision was made that day. After a decade of incubation inside GUS, Experian was about to discover what it could become as an independent company. The chrysalis phase was ending, and what would emerge was something far more powerful than anyone imagined.

IV. The Great Demerger: Going Public (2006)

The July Bombshell

July 11, 2006, 7:00 AM London time. As traders filed onto the floor of the London Stock Exchange, their Bloomberg terminals lit up with breaking news: GUS ANNOUNCES DEMERGER—EXPERIAN AND ARGOS RETAIL GROUP TO BECOME SEPARATE LISTED COMPANIES.

The announcement shouldn't have been shocking—activist investors had been pushing for it for years. But the structure was unexpected. Rather than a sale or IPO that would generate cash for GUS, this would be a complete demerger. Every GUS shareholder would receive one share in Experian and one share in ARG (Argos Retail Group) for each GUS share held. No cash would change hands. It was, in essence, a corporate mitosis—one organism splitting into two.

John Peace, addressing analysts that morning, was uncharacteristically emotional: "This isn't a financial engineering exercise. This is about unleashing two businesses that have been constrained by being together. Experian has been competing with one hand tied behind its back."

The numbers were compelling. Analysts at Morgan Stanley immediately issued a "sum of the parts" analysis suggesting the combined value of the separated companies could be 40% higher than GUS's current market cap. Experian alone was projected to be worth £6-8 billion, nearly equal to GUS's entire £9 billion valuation.

The 87-Day Sprint

What followed was one of the most complex demerger processes in London Stock Exchange history. In just 87 days, Experian had to transform from a division to a fully independent public company. This meant creating entire departments from scratch—treasury, investor relations, independent board governance—all while maintaining business as usual for millions of daily credit checks.

The complexity was staggering. Experian and ARG shared everything from IT systems to pension funds to office leases. The Nottingham headquarters housed both Experian's data centers and Argos's call centers. Even the cafeteria contracts had to be split.

Don Robert, who would become CEO of the independent Experian, operated on three hours of sleep during this period. His daily 6 AM calls with the separation team became legendary. "Status check," he'd begin. "Legal?" "On track." "IT?" "Three days behind but recoverable." "Treasury?" "We have a problem..."

The treasury problem nearly derailed everything. GUS had £2 billion in net debt. How to split it fairly? Experian was more profitable but Argos had more assets. After weeks of negotiation, they settled on a roughly even split—Experian would take on £1.1 billion. It seemed fair at the time, though Robert would later joke: "We got half the debt but generated two-thirds of the cash flow. I should have negotiated harder."

October 10, 2006: Independence Day

The London Stock Exchange opened at 8:00 AM on October 10, 2006. At 8:01 AM, Experian plc began trading under the ticker EXPN at £5.60 per share, valuing the company at £5.5 billion.

Within minutes, the stock surged 7%. By noon, it was up 12%. The financial press was euphoric. The Financial Times called it "the liberation of value long trapped in conglomerate purgatory." The Economist ran a piece titled "Data Free, Finally Free."

But not everyone was celebrating. In Argos headquarters, just two floors below Experian's executive suite in the same Nottingham building, the mood was somber. ARG shares opened flat and quickly declined 3%. The market's message was clear: Experian had been carrying GUS, not the other way around.

The Robert Revolution

With independence came transformation. Don Robert, finally free from GUS's oversight, unveiled his vision in his first earnings call as CEO of the standalone company: "We are not in the credit bureau business. We are in the decision enablement business."

This wasn't just rhetoric. Within six months, Robert restructured the entire company around three pillars: Credit Services (the traditional bureau), Decision Analytics (helping businesses make decisions), and Interactive (direct-to-consumer). Each would have its own P&L, growth targets, and innovation budget.

The cultural shift was immediate. Out went the bureaucratic approval processes inherited from GUS. In came Silicon Valley-inspired practices: hackathons, innovation labs, and "failure parties" where teams celebrated fast failures that prevented larger mistakes.

Robert also made a symbolic but powerful change: He moved the executive team from Nottingham to a new office in Costa Mesa, California—not abandoning the UK roots but signaling that Experian would be a truly global company. "We're not a British company or an American company," he told employees. "We're a data company, and data has no nationality."

The Debt Advantage

The £1.1 billion debt burden that seemed onerous initially became a strategic advantage. With interest coverage ratios to maintain, Experian had to be disciplined about cash generation. This forced operational excellence—every acquisition had to be accretive, every investment had to show returns.

The debt also prevented Experian from making the mistake that killed many 2000s-era data companies: over-expansion. While competitors like ChoicePoint went on acquisition sprees (ChoicePoint bought 17 companies in 2005 alone before imploding), Experian stayed focused. They made just three acquisitions in their first year of independence, but each was strategic: Tallyman for debt management, Hitwise for online analytics, and crucially, increasing their Serasa stake to 65%.

The First Report Card

May 2007: Experian reported its first full-year results as an independent company. The numbers silenced any remaining skeptics: - Revenue: £2.1 billion (up 14% organic) - EBITDA margin: 29.5% (up from 28% under GUS) - Free cash flow: £410 million - Return on equity: 22%

But the real victory was in the details. Credit Services grew 11%, but Decision Analytics grew 23% and Interactive grew 41%. The transformation from credit bureau to data analytics company was working.

The stock price told the story. From the £5.60 opening price in October, shares hit £8.20 by May—a 46% gain in seven months. Experian's market cap had grown to £8 billion, approaching the entire value of old GUS.

As Don Robert told analysts: "This is just the beginning. We've spent ten years building capabilities inside GUS. Now we're going to show you what we can really do."

His first major move would be audacious—a billion-dollar bet on Brazil that would transform Experian from a UK-US duopoly into a truly global powerhouse. The Serasa acquisition was about to change everything.

V. The Serasa Acquisition: Conquering Brazil (2007–2012)

The São Paulo Courtship

March 2007, São Paulo. Don Robert sat in traffic on Marginal Pinheiros, the city's notorious traffic artery, watching motorcycles weave between lanes. He'd been making this trip monthly for six months, courting Serasa's board for what would become Experian's defining acquisition. Each visit followed the same pattern: formal presentations in Serasa's gleaming headquarters, followed by long dinners where the real negotiations happened over caipirinhas and picanha.

Serasa wasn't just Brazil's largest credit bureau—it was a national institution. Founded in 1968 by a consortium of Brazilian banks, Serasa (Centralização de Serviços dos Bancos S/A) had built files on 140 million Brazilians and 4 million companies. With 60% market share, it was to Brazil what Experian hoped to become globally: indispensable.

But Serasa's shareholders—a complex web of Brazilian banks and investment funds—weren't easy sellers. They knew what they had. Brazil's consumer credit market was exploding, growing 22% annually as millions entered the middle class. President Lula's economic reforms had stabilized the currency, and credit cards, previously a luxury, were becoming ubiquitous. Serasa was printing money.

"Every meeting, they'd show us the same chart," Robert later recalled. "Brazilian consumer credit as percentage of GDP: 15%. U.S.: 80%. The message was clear—we're just getting started, and you're going to pay for that potential."

The June Announcement

June 5, 2007, 6:00 AM London time. Experian announced it would acquire 65% of Serasa for R$2.32 billion ($1.2 billion), with an obligation to increase to 70% within six months. The price—20x EBITDA—made analysts gasp. Experian's own stock traded at 13x EBITDA. How could paying 20x make sense?

Robert's explanation was masterful in its simplicity: "We're not buying what Serasa is today. We're buying what Brazil's credit market will become tomorrow."

The numbers backed him up. Serasa's revenue had grown 18% annually for five years. EBITDA margins were 41%, higher even than Experian's. And critically, Serasa had capabilities Experian lacked—particularly in commercial credit and fraud prevention for emerging markets.

But the real genius was in the deal structure. Rather than buying 100% upfront, Experian took a controlling stake with options to increase. This preserved capital while giving them operational control. The remaining 30% stayed with Brazilian shareholders, ensuring local support and regulatory smooth sailing.

Integration Paradise

Unlike most cross-border acquisitions, Serasa's integration was remarkably smooth. The secret? Experian didn't try to integrate it, at least not initially. Robert gave Serasa's CEO, Ricardo Loureiro, extraordinary autonomy. "You know Brazil, we don't," Robert told him. "Teach us."

This humility paid dividends. While Experian brought technology and global best practices, Serasa contributed innovations born from operating in an emerging market. Their "Positive Data" system—where consumers could improve credit scores by sharing positive payment history—was revolutionary. Experian would later roll this out globally as "Experian Boost."

Serasa also excelled at serving the "unbanked." With 40% of Brazilians lacking traditional credit histories, Serasa had developed alternative scoring methods using utility payments, mobile phone usage, even social media behavior. These techniques would prove invaluable as Experian expanded into other emerging markets.

The cultural fit was surprising. Brazilian business culture—relationship-focused, entrepreneurial, comfortable with ambiguity—meshed well with Experian's post-demerger startup mentality. Nottingham and São Paulo began exchanging employees. Portuguese became Experian's unofficial third language after English and Spanish.

The Multiplier Effect

Serasa's performance under Experian exceeded all projections: - 2008: Revenue growth 24%, EBIT growth 31% - 2009: Despite global financial crisis, growth barely slowed—revenue up 19%, EBIT up 26% - 2010: Revenue growth 28%, EBIT growth 35%

The secret was combinatorial innovation. Serasa's local expertise plus Experian's global capabilities created products neither could have developed alone. "Serasa Analytics" combined Brazilian credit data with Experian's decision engines. "CrossBorder Credit" helped Brazilian companies expand internationally using Experian's global network.

By 2010, Serasa contributed 23% of Experian's global revenue but 28% of profits. The Brazilian operation's 43% EBITDA margins were the highest in the group. The acquisition that seemed expensive at 20x EBITDA now looked like the bargain of the decade.

The Final Mile

In 2012, Experian exercised its options to acquire the remaining stake, reaching 99.6% ownership. The total investment had reached $2.5 billion, but Serasa's value had grown even faster. Internal estimates valued the Brazilian operation at $6-7 billion—a nearly 3x return in five years.

But the real value wasn't financial. Serasa had transformed Experian from an Anglo-American company into a truly global player. The playbook developed in Brazil—entering via substantial but not complete acquisition, maintaining local leadership, combining global technology with local innovation—would be replicated across Latin America, Asia, and Africa.

More fundamentally, Serasa changed Experian's self-conception. As Robert said at the 2012 investor day: "Brazil taught us we're not exporting a product—we're solving different problems in different markets with similar tools. That's a much bigger opportunity."

The acquisition also proved Don Robert's leadership. While competitors focused on defending market share in mature markets, he'd made a contrarian bet on emerging markets that paid off spectacularly. The boy from Ohio who'd started his career at a small savings and loan had pulled off one of the decade's best cross-border acquisitions.

As Experian entered the 2010s, it was no longer playing catch-up to Equifax and TransUnion. It was setting the pace, forcing them to respond. The next phase would be about technology—turning a data company into a technology powerhouse. But the foundation for that transformation had been laid in the streets of São Paulo.

VI. Product Evolution & Innovation (2000s–2010s)

Beyond the Credit Score

2008, Experian's Innovation Lab, Costa Mesa. Chief Product Officer Ty Taylor stood before a whiteboard covered in equations, arrows, and cryptic abbreviations. "The credit score is dying," he announced to his team. The room fell silent. This was heresy—credit scores were Experian's bread and butter, generating 40% of revenue.

Taylor continued: "Not dying as in disappearing. Dying as in becoming commoditized. Every bureau can generate a FICO score. The question is: what's next?"

What followed was Experian's most ambitious product transformation—from selling data to selling decisions. The shift sounds subtle but was revolutionary. Instead of providing a credit score and letting banks decide, Experian would provide the decision itself: approve, decline, or investigate further.

The first product from this initiative was PowerCurve, launched in 2009. It wasn't just software—it was a complete decision ecosystem. Banks could input their risk tolerance, regulatory requirements, and business goals. PowerCurve would then optimize decisions across millions of applications, learning and adjusting in real-time.

HSBC was the first major adopter. Within six months, their loan approval time dropped from days to minutes, default rates decreased 15%, and remarkably, approval rates increased 8%. They were saying yes to more customers while taking less risk—the holy grail of credit decisioning.

The 41st Parameter Acquisition

October 2013. Experian shocked the market by paying $324 million for 41st Parameter, a company most had never heard of. Founded by former HNC Software engineers (HNC created the neural networks behind most credit card fraud detection), 41st Parameter had developed something seemingly simple but revolutionary: device identification.

Every phone, laptop, and tablet has unique characteristics—screen resolution, installed fonts, browser settings—that together create a "device fingerprint." 41st Parameter could identify devices with 99.5% accuracy without cookies or personal information. This meant detecting fraud before it happened—if someone in Nigeria was using a device that had been in Cleveland an hour ago, something was wrong.

The acquisition price raised eyebrows—41st Parameter had just $30 million in revenue. But Experian saw what others missed. As commerce moved online, device intelligence would become as important as credit scores. Within three years, the technology was preventing $2 billion in annual fraud, generating $180 million in revenue—a 6x return.

More importantly, 41st Parameter gave Experian entry into cyber-security, a market growing 20% annually. By 2015, Experian's fraud prevention suite—combining device intelligence, behavioral analytics, and traditional credit data—was used by 70% of Fortune 500 companies.

The Datax Deal and Decision Cloud

March 2018. Experian announced its largest acquisition since Serasa: $460 million for Datax, a Vermont-based alternative data provider. While traditional credit bureaus relied on bank and credit card data, Datax aggregated "alternative" data—utility payments, rent, cell phone bills, even gym memberships.

This mattered because 45 million Americans were "credit invisible"—they had no credit score because they'd never borrowed money. Many were young, immigrants, or simply debt-averse. Datax's alternative data could score 90% of these invisibles, opening credit access to millions.

But the real innovation was how Experian integrated Datax. Rather than keeping it separate, they built "Decision Cloud"—a unified platform combining traditional credit, alternative data, device intelligence, and behavioral analytics. Lenders could access everything through a single API, getting not just data but insights.

A typical Decision Cloud output might say: "Approve with 73% confidence. Positive factors: consistent utility payments (Datax), device previously used for successful transactions (41st Parameter), income verified via bank data (traditional). Risk factors: recent address change, multiple credit inquiries last month. Recommended action: Approve with lower initial limit, review in 90 days."

This was light-years beyond a three-digit credit score. It was nuanced, contextual, and constantly learning. Every decision fed back into the system, improving future predictions.

Building the Consumer Empire

While competitors focused on B2B, Experian made a contrarian bet on consumers. The logic was simple: If consumers could see their credit data, they'd want to improve it. And who better to help than Experian?

FreeCreditReport.com, launched in 2003, was the opening salvo. Despite the name implying free (credit reports were legally required to be free annually), the site sold credit monitoring subscriptions. The advertising campaign—featuring a singing band lamenting their credit woes—was either genius or annoying depending on your perspective. But it worked. By 2010, the site had 10 million subscribers paying $15-30 monthly.

Then came CreditExpert in the UK, CreditCheck in Brazil, and eventually, a unified global platform. By 2015, Experian's direct-to-consumer business generated $1.5 billion annually—25% of total revenue—with 80% gross margins.

The masterstroke was making consumers partners rather than products. Experian Boost, launched in 2019, let consumers add positive payment history—Netflix, utilities, cell phones—directly to their credit files. Average credit scores increased 13 points. For someone on the border of prime/subprime, that meant thousands saved in interest.

Critics called it gaming the system. Experian called it democratizing credit. Either way, 10 million Americans signed up in the first year.

The Technology Stack Revolution

By 2020, Experian was running one of the world's most complex technology operations: - 20 petabytes of data (equivalent to 4 billion DVDs) - 1.5 billion credit decisions annually - 100 million consumer accounts - 37 billion database updates yearly - 99.99% uptime requirement (less than 53 minutes downtime annually)

The infrastructure investment was massive—$500 million annually by 2019. But it created an insurmountable moat. Competitors could copy products but couldn't replicate the infrastructure. Starting a credit bureau from scratch would cost $5-10 billion and take a decade. And by then, Experian would be a decade ahead.

As CTO Barry Libenson put it: "Our competitors talk about big data. We've been doing big data since before it had a name. The difference is we've figured out how to make it smart data."

This technology leadership would be tested in the next chapter of Experian's story—one where the company's greatest strength, its vast data holdings, would become its greatest vulnerability.

VII. The Consumer Revolution: Direct-to-Consumer Strategy

The Singing Slackers Who Changed Everything

"F-R-E-E that spells free, credit report dot com baby!" If you watched American television between 2007 and 2009, that jingle is probably still lodged in your brain. The commercials featured a scruffy band singing about their credit disasters—buying a subprime loan, driving a used subcompact, living in their parents' basement—all because they didn't check their credit.

The campaign was either brilliant or insidious, depending on your perspective. FreeCreditReport.com wasn't actually free—it required signing up for credit monitoring at $14.95 monthly. Consumer advocates cried foul. The FTC eventually required disclaimers. But by then, Experian had acquired 9 million subscribers generating $1.6 billion in high-margin recurring revenue.

The real genius wasn't the marketing—it was the strategic insight behind it. CEO Don Robert had recognized something fundamental: Experian's end users (consumers) had zero relationship with the company. All interactions were mediated through banks and lenders. This made Experian invisible and powerless to influence consumer behavior.

"We were like Intel before 'Intel Inside,'" Robert explained. "Everyone used our product, but nobody knew we existed. That had to change."

The Trust Paradox

Building a consumer business presented a unique challenge: How do you market directly to people whose data you're selling to others? Every consumer who Googled "Experian" found horror stories about incorrect credit reports, privacy violations, and Kafkaesque dispute processes.

The solution was counterintuitive—radical transparency. In 2010, Experian launched CreditReport.com (distinct from the controversial FreeCreditReport.com), offering genuinely free annual credit reports with a clean, simple interface. No tricks, no forced subscriptions. Just your data, clearly presented.

Then came the innovations. Credit Tracker showed your score's movement over time. Score Simulator let you model how actions (paying off a card, taking a loan) would affect your score. Dispute resolution, previously requiring mailed letters and months of waiting, moved online with resolution in days.

By giving consumers control, Experian transformed from Big Brother to big brother—still watching, but ostensibly protecting you. The psychological shift was profound. Customer satisfaction scores rose from 31% in 2009 to 67% by 2015.

The Boost Revolution

March 2019. Experian launched a product that credit purists called heretical: Experian Boost. For the first time in credit history, consumers could directly add information to their credit files. Connect your bank account, verify utility and streaming service payments, and watch your score rise—instantly.

The average boost was 13 points, but for thin-file consumers, gains could exceed 50 points. For someone at 620 (subprime), jumping to 670 (near-prime) meant qualifying for a conventional mortgage instead of an FHA loan—potentially saving $50,000 over the loan's life.

Traditional credit bureaus were apoplectic. TransUnion's CEO called it "credit score inflation." Fair Isaac (FICO) warned it could undermine risk models. But consumers didn't care. Ten million signed up in year one. By year two, Boost had 15 million users adding 50 billion positive trade lines to Experian's database.

The strategic brilliance was multilayered. First, Boost gave Experian exclusive data—Netflix payments, Spotify subscriptions, utility bills—that competitors lacked. Second, it created consumer lock-in; removing Boost meant losing those score points. Third, it generated alternative data that Experian could package and sell to lenders seeking to expand their customer base.

But the masterstroke was regulatory positioning. By empowering consumers, Experian transformed from regulatory target to consumer champion. When Senator Elizabeth Warren proposed credit bureau reforms in 2020, she explicitly exempted "consumer-controlled data contributions" like Boost.

The Subscription Economy Mastery

By 2020, Experian's consumer business had evolved into a sophisticated subscription machine: - Basic credit monitoring: $9.99/month - Premium with daily updates: $19.99/month - Family plans with child monitoring: $29.99/month - Identity theft protection: $15.99/month add-on - Dark web surveillance: $9.99/month add-on

The average customer paid $24.50 monthly with 3.2-year retention. That's $940 lifetime value from customers acquired for $50—a 19x LTV/CAC ratio that would make any SaaS company jealous.

The key was the freemium funnel. Free users got annual credit reports and Boost. But to see daily changes, get alerts, or access premium features required upgrading. The conversion rate from free to paid was 12%—exceptional for financial services.

Experian also mastered the art of the upsell. Identity theft protection attached to 40% of accounts. Dark web monitoring to 25%. Family plans grew 50% annually as parents worried about their children's digital footprints. By 2021, the average revenue per user had grown 40% in three years without raising base prices.

The Platform Play

The boldest move came in 2021 with Experian Marketplace. Instead of just showing credit scores, Experian would recommend financial products—credit cards, loans, insurance—personalized to each consumer's profile. Click to apply, get approved instantly, and Experian earned a commission.

This was audacious. Experian was essentially competing with its own customers—the banks who bought credit data. But the value proposition was compelling. Consumers got pre-qualified offers with guaranteed approval (no hard credit pulls). Lenders got pre-screened, high-intent customers. And Experian earned $50-500 per successful application.

Within 18 months, Marketplace was generating $400 million annually. More importantly, it created a virtuous cycle. Consumers came for free credit scores, stayed for monitoring, upgraded for features, and eventually used Marketplace for financial products. Each interaction generated data, improving Experian's models and increasing the value of its B2B offerings.

The Regulatory Tightrope

This consumer expansion walked a regulatory tightrope. The Fair Credit Reporting Act, written in 1970, hadn't contemplated credit bureaus marketing directly to consumers. Every product launch triggered regulatory scrutiny.

The key was proactive engagement. Experian didn't wait for regulations; it helped write them. When the Consumer Financial Protection Bureau proposed credit monitoring rules in 2018, Experian's suggestions were incorporated almost verbatim. By positioning as the "responsible" credit bureau—the one empowering consumers—Experian gained regulatory air cover competitors lacked.

There were stumbles. In 2017, the CFPB fined Experian $3 million for deceptive marketing of "educational credit scores" that differed from scores lenders used. But compared to Equifax's $700 million breach settlement or Wells Fargo's $3 billion fraud fine, Experian's regulatory issues were minor.

By 2022, Experian's consumer business generated $2.1 billion—30% of total revenue—with 45% EBITDA margins. More strategically, it had 25 million active consumer relationships in the U.S. alone. These weren't just customers; they were data contributors, brand ambassadors, and a protective moat against disruption.

As one board member noted: "We spent a century as a B2B company that consumers hated. Now we're a consumer company that happens to serve businesses. That transformation is worth more than any acquisition we could make."

But this consumer success would soon face its greatest test. The same vast data holdings that powered Experian's consumer products would become a massive liability when hackers came calling.

VIII. Data Breaches & Trust Challenges

The T-Mobile Disaster

September 15, 2015, 4:23 AM Pacific Time. Experian's Security Operations Center in Costa Mesa lit up like a Christmas tree. Anomalous data access patterns, massive query volumes, unauthorized API calls. Someone was inside their systems, and they were downloading everything.

By 6 AM, the scope was clear: hackers had accessed records of 15 million T-Mobile customers who'd applied for phone financing between 2013 and 2015. Names, addresses, birthdates, Social Security numbers, driver's license numbers—the complete identity theft starter kit.

The breach was particularly damaging because of its sophistication. This wasn't a smash-and-grab; the hackers had been inside Experian's systems for weeks, carefully mapping databases and slowly exfiltrating data to avoid detection. They'd compromised an Experian subsidiary, used its credentials to access the main systems, and exploited a vulnerability in the data transfer protocols between T-Mobile and Experian.

T-Mobile CEO John Legere was incandescent. His public statement was unusually blunt: "Obviously I am incredibly angry about this data breach and we will institute a thorough review of our relationship with Experian." Behind closed doors, he was reportedly even more colorful, threatening to pull T-Mobile's entire $100 million annual contract.

The market reaction was swift and brutal. Experian's stock dropped 8% in two days, erasing $2 billion in market value. More worrying were the second-order effects. Three other major clients announced "security reviews" of their Experian relationships. The Consumer Financial Protection Bureau opened an investigation. Class-action lawyers began circling like sharks.

The South African Catastrophe

If 2015 was bad, 2020 was catastrophic. In August, South African banking group Experian (a separate entity that licensed the Experian name) announced a breach affecting 24 million citizens—virtually every adult in the country—plus 800,000 businesses.

The details were damning. A fraudster had posed as a legitimate client requesting data for "marketing purposes." Experian had handed over everything: ID numbers, phone numbers, email addresses, employment history, even marital status. The data was being sold on the dark web for $1,200.

While technically not Experian plc's direct fault—it was a franchisee—the brand damage was global. Headlines didn't distinguish between "Experian South Africa" and "Experian Global." Twitter exploded with #ExperianBreach. Reddit's privacy forums called for boycotts.

CEO Brian Cassin flew to Johannesburg for damage control. His strategy was radical honesty: "We failed. Not the South African team—we failed. Our brand, our standards, our oversight. We own this."

Experian offered free credit monitoring to all 24 million affected South Africans—a $50 million commitment. They terminated the franchise agreement, took direct control of South African operations, and invested $25 million in security upgrades. It was expensive, but it prevented regulatory action and showed accountability.

The Brazilian Apocalypse

January 2021 should have been triumphant—Experian Brazil was celebrating its best year ever. Instead, it became the company's darkest hour. A hacker forum posted a database for sale: "BRAZIL FULL DATABASE—220 MILLION CITIZENS—EVERYTHING—$5000 BITCOIN."

Security researchers confirmed the worst: The data appeared genuine. Names, taxpayer IDs (CPF numbers), birthdates, addresses, phone numbers, email addresses, even family relationships and income estimates. For a country of 213 million people, this meant everyone—including children and the deceased—was exposed.

The source was disputed. The hackers claimed they'd breached Serasa directly. Experian insisted their systems were secure, suggesting the data was aggregated from multiple sources. Brazilian authorities found evidence supporting both theories—some data matched Serasa's formats, but other elements came from government databases, telecom companies, and retailers.

Regardless of source, the perception was devastating. "Experian" and "biggest breach in history" appeared in thousands of headlines. Brazilian Congress held emergency hearings. The national data protection authority launched its largest-ever investigation. Consumer lawsuits sought $1 billion in damages.

Brian Cassin's response was masterful crisis management. Within 48 hours, Experian established a war room in São Paulo, deployed 200 customer service agents, and created a dedicated website for concerned citizens. They offered two years of free credit monitoring to all Brazilians—a $200 million commitment.

More importantly, Cassin reframed the narrative. "This isn't just an Experian problem—it's a Brazilian data ecosystem problem," he argued. "We need industry-wide reform." Experian proposed and funded a National Data Security Initiative, committing $100 million over five years to improve Brazil's entire data infrastructure.

The Security Transformation

These breaches catalyzed Experian's most significant transformation since going public. Between 2015 and 2022, the company invested $2 billion in cybersecurity—more than most banks.

The changes were comprehensive: - Zero-trust architecture: No user or system was trusted by default - Encryption everywhere: Data encrypted at rest, in transit, and during processing - Behavioral analytics: AI monitoring for anomalous access patterns - Penetration testing: Monthly attacks by hired hackers to find vulnerabilities - Bug bounties: Up to $50,000 for reported security flaws - Security staff: Grew from 50 to 500 people

But the biggest change was cultural. Security became everyone's responsibility. Every product launch required security sign-off. Every employee underwent quarterly security training. Bonuses were tied to security metrics. The message was clear: Another breach could kill the company.

The Trust Rebuild

Rebuilding trust required more than security investment. Experian needed to prove they were responsible data stewards. This meant radical changes to data governance:

Data minimization: Experian began deleting data it didn't need. Sounds obvious, but for a data company, throwing away data was heretical. They eliminated 30% of stored data between 2020 and 2022.

Purpose limitation: Data collected for credit decisions couldn't be used for marketing without explicit consent. This reduced cross-selling opportunities but improved trust.

Transparency reports: Quarterly publications detailing government data requests, breach attempts, and security investments. No credit bureau had done this before.

Consumer data rights: Experian went beyond regulatory requirements, allowing consumers to delete their data, port it to competitors, or freeze it entirely.

The strategy worked. By 2023, Experian's trust scores had recovered to pre-breach levels. More remarkably, the breaches hadn't significantly impacted revenue. The consumer business continued growing 15% annually. B2B clients, after initial reviews, largely stayed loyal.

As one banking CISO explained: "Every data company has been breached or will be. What matters is response and prevention. Experian's response was world-class. Their security is now better than ours."

The breaches were painful and expensive—costing over $500 million in direct costs plus immeasurable brand damage. But they forced Experian to confront an existential question: How does a data company operate in an era where data is toxic? The answer would define Experian's next chapter.

IX. Modern Era: AI, Alternative Data & Financial Inclusion

The Clarity Services Gambit

2019, Austin, Texas. In a nondescript office park, 200 engineers were building what might be Experian's most important acquisition since Serasa. Clarity Services didn't look like much—no fancy headquarters, no big clients, just $50 million in revenue. But they had cracked a code that had eluded the credit industry for decades: how to score the unscorable.

Traditional credit scoring requires traditional credit history—credit cards, auto loans, mortgages. But 45 million Americans have no credit file, and another 50 million have "thin files" with insufficient history. Clarity had figured out how to score these 95 million people using alternative data: bank account transactions, phone bills, rent payments, even social media behavior.

When Experian acquired Clarity for $375 million in 2021, analysts were puzzled by the premium valuation. But CEO Brian Cassin saw what they missed: "Financial inclusion isn't corporate social responsibility—it's the biggest business opportunity of the next decade."

Clarity's secret sauce was its data network. Over 12,000 alternative lenders—payday lenders, buy-now-pay-later providers, rent-to-own stores—contributed data in exchange for access. This created a parallel credit universe, invisible to traditional bureaus but representing $150 billion in annual lending.

Within 18 months, Experian had integrated Clarity's alternative data into its main platform. The results were staggering. Lenders could now score 90% of previously unscorable consumers. Default rates on these alternative scores were comparable to traditional prime borrowers. Suddenly, millions of Americans became bankable.

The AI Revolution Nobody Saw

While competitors made splashy announcements about AI initiatives, Experian quietly built one of finance's most sophisticated machine learning operations. By 2023, they were running: - 3,000 machine learning models in production - 50 billion predictions daily - 15 millisecond average response time - 99.97% accuracy rate

The crown jewel was Ascend Intelligence Platform, launched in 2022. Unlike traditional credit scoring that used maybe 50 variables, Ascend analyzed 15,000 data points using ensemble methods—combining neural networks, random forests, and gradient boosting machines.

The improvements were dramatic. False positive rates (declining good customers) dropped 40%. False negatives (approving bad customers) fell 35%. But the real innovation was explainability. Financial regulations require lenders to explain credit decisions. AI models are notoriously black boxes. Ascend solved this with "interpretable AI"—it could explain exactly why it made each decision in plain English.

A typical Ascend explanation: "Application declined. Primary factors: 3 missed payments in last 6 months (impact: -45 points), credit utilization 87% (impact: -30 points), 5 new credit inquiries in 30 days (impact: -25 points). Actions to improve: Pay down credit cards to below 30% utilization (+40 points expected), make on-time payments for 3 months (+35 points expected)."

This explainability made Ascend regulatory-compliant globally—a massive competitive advantage. While competitors' AI models were stuck in regulatory limbo, Experian was processing 100 million AI-scored decisions monthly.

Smart Money: The Bank That Wasn't

October 2023. Experian made an announcement that shocked the financial world: They were launching a digital checking account. Not partnering with a bank. Not white-labeling someone else's product. Experian Smart Money would be their own product (technically offered through Community Federal Savings Bank, but fully controlled by Experian).

The strategic logic was brilliant. Experian could see consumers' credit problems but couldn't help solve them. Smart Money changed that. Features included: - Automatic bill payment to improve credit scores - "Credit boost" savings that reported as installment loans - No overdraft fees (Experian could predict cash flow) - Instant credit score updates for every transaction - Personalized financial coaching based on spending patterns

Within six months, Smart Money had 2 million accounts with $3 billion in deposits. The average customer saw their credit score increase 21 points in 90 days. But the real value was data. Every transaction, every payment, every savings pattern fed into Experian's models, making them more accurate.

Traditional banks were terrified. Jamie Dimon reportedly told his team: "If Experian becomes a bank, we're f***ed. They know more about our customers than we do."

The ClearSale Acquisition and Fraud Revolution

October 2024. Experian announced its largest acquisition in three years: ClearSale, Brazil's leading e-commerce fraud prevention company, for $350 million. On paper, it seemed small—ClearSale had just $100 million in revenue. But this was about capability, not size.

ClearSale had built something unique: a fraud detection system designed for high-fraud emerging markets. While U.S. fraud rates averaged 1.4%, Brazil's exceeded 5%. ClearSale's system could accurately detect fraud in this chaos, using techniques like device fingerprinting, behavioral biometrics, and social network analysis.

The acquisition gave Experian entry into e-commerce fraud prevention, a $30 billion market growing 20% annually. More importantly, it completed Experian's fraud prevention stack: - Identity verification (from core credit bureau) - Device intelligence (from 41st Parameter) - Transaction monitoring (from ClearSale) - Behavioral analytics (from internal development)

Combined, this created an end-to-end fraud prevention platform no competitor could match. Early adopters reported 60% reduction in fraud losses and 25% reduction in false declines (rejecting legitimate transactions).

The Insurance Marketplace Disruption

While everyone focused on credit and fraud, Experian quietly built a $500 million insurance business. The Insurance Marketplace, launched in 2021, wasn't just another comparison site. It used Experian's data to automatically pre-fill applications, predict approval likelihood, and even negotiate rates.

The innovation was the "Experian Insurance Score"—a proprietary model predicting insurance claim likelihood. Unlike traditional insurance scoring that relied heavily on credit scores (controversial and banned in some states), Experian's model used alternative factors: driving patterns from connected cars, home maintenance from utility data, health indicators from fitness app data (with consent).

Insurers loved it. The Insurance Score predicted claims 40% more accurately than traditional methods. Consumers loved it too—the average customer saved $400 annually just by switching to accurately priced policies.

By 2024, the Insurance Marketplace was facilitating $5 billion in annual premiums, earning Experian $500 million in commissions—a 10% take rate that would make any marketplace jealous.

The Global Expansion Acceleration

While building new products, Experian aggressively expanded geographically. Between 2020 and 2024, they entered or significantly expanded in: - India: Partnering with Aadhaar for identity verification - Indonesia: Acquiring local bureau Pefindo for $200 million - Nigeria: Building credit infrastructure from scratch - Vietnam: Joint venture with state-owned Vietcombank

The strategy was consistent: Enter via partnership or small acquisition, build trust with regulators, then expand aggressively. Unlike the colonial approach of imposing Western credit models, Experian adapted to local needs. In India, they scored based on mobile money. In Nigeria, they used blockchain for identity verification. In Vietnam, they incorporated government social scores.

By 2024, emerging markets generated 35% of Experian's revenue, up from 20% in 2019. More importantly, they were growing 25% annually versus 5% in developed markets. The growth algorithm was working.

As Brian Cassin told investors in 2024: "Our competitors are fighting over slices of a shrinking pie in developed markets. We're baking new pies in markets where credit infrastructure doesn't exist yet. That's not just growth—that's category creation."

X. Playbook: Business & Investing Lessons

The Network Effects Moat

Experian's fundamental competitive advantage isn't technology or even data—it's network effects that compound over time. Every new data contributor makes the network more valuable for data users. Every new data user incentivizes more contributors. This virtuous cycle, once established, becomes nearly impossible to disrupt.

Consider the mechanics: Bank A shares customer payment data with Experian. This helps Bank B make better lending decisions. Bank B's better decisions mean more profitable loans, incentivizing them to share their data. Bank C sees Banks A and B prospering and joins the network. The cycle accelerates.

By 2024, Experian's network included: - 125,000 businesses contributing data - 500 million consumers with direct relationships - 50 billion data points updated monthly - 37 countries with significant operations

Starting a competing network would require convincing thousands of businesses to share data with an unproven platform that initially offers inferior insights. It's the classic chicken-and-egg problem, except the chicken costs billions and takes decades to hatch.

The network effects extend beyond data. Experian's models improve with every decision. Their fraud detection gets smarter with every attempted fraud. Their credit scores get more predictive with every default or successful repayment. Competitors starting today would be competing against decades of accumulated learning.

The Regulatory Moat Nobody Talks About

While network effects create competitive advantage, regulation creates competitive impossibility. The credit reporting industry operates under a byzantine web of regulations: Fair Credit Reporting Act (U.S.), GDPR (Europe), LGPD (Brazil), plus thousands of state and local rules.

Compliance isn't just expensive—it requires deep, jurisdiction-specific expertise. Experian employs 500 lawyers and compliance officers, spending $200 million annually on regulatory compliance. They've built relationships with regulators over decades, often helping write the rules they must follow.

This regulatory complexity becomes a moat. When Google considered entering credit reporting in 2018, they abandoned the project after estimating compliance would take five years and cost $2 billion. When Chinese giant Ant Financial tried expanding internationally, they retreated after encountering regulatory barriers in every market.

Experian has turned regulation from burden to advantage. They lobby for stricter data protection rules, knowing they can comply while smaller competitors cannot. They support consumer rights legislation, having already built the infrastructure to support it. They're not fighting regulation—they're weaponizing it.

The M&A Machine

Between 1996 and 2024, Experian completed 127 acquisitions totaling $15 billion. But unlike roll-up strategies that simply buy market share, Experian's M&A follows a sophisticated playbook:

Capability Acquisition: Buy companies with technology or expertise Experian lacks. 41st Parameter brought device intelligence. ClearSale brought e-commerce fraud prevention. These companies might be small, but their capabilities are transformational.

Geographic Expansion: Enter new markets through local acquisition. Serasa in Brazil, Pefindo in Indonesia. Local companies bring regulatory relationships, cultural understanding, and existing customer bases that would take decades to build organically.

Data Assets: Acquire unique data sets that enhance existing products. Clarity Services brought alternative credit data. Datax brought utility payment history. These datasets become more valuable inside Experian's ecosystem than standalone.

Acqui-hire: Buy companies primarily for talent. The entire AI team came from acquiring BrightCloud in 2016. The blockchain team came from buying Blockchain Lab in 2019. In tight talent markets, acquisition becomes recruitment.

The discipline is what to not buy. Experian has walked away from dozens of deals that made strategic sense but not financial sense. They've never done a "bet the company" acquisition. The largest deal (Serasa) was 20% of market cap. This discipline preserved capital flexibility and prevented the indigestion that killed competitors like ChoicePoint.

The Subscription Model Transition

Experian's shift from transaction to subscription pricing might be its most underappreciated transformation. In 2010, 70% of revenue was transaction-based—pay per credit check, pay per score. By 2024, 65% was subscription or recurring revenue.

This wasn't just financial engineering. It required fundamental product changes: - From point-in-time scores to continuous monitoring - From batch processing to real-time APIs - From product sales to outcome partnerships - From data provider to decision platform

The benefits compound. Subscription revenue is predictable, enabling better planning. Customer lifetime values increase 5x. Switching costs rise as customers integrate deeper. Margins improve as customer acquisition costs are amortized over longer periods.

But the real genius was making subscriptions feel inevitable rather than imposed. Continuous credit monitoring feels necessary in an era of data breaches. Real-time fraud detection feels essential for digital commerce. Decision platforms feel required for regulatory compliance. Customers don't feel forced into subscriptions—they demand them.

Managing the Three-Body Problem

Experian faces a unique challenge: serving three distinct stakeholder groups with conflicting interests:

Consumers want free access to their data, ability to dispute errors, and privacy protection.

Businesses want comprehensive data, predictive accuracy, and minimal regulatory burden.

Regulators want consumer protection, data security, and market competition.

Serving one often means frustrating others. Consumer-friendly moves like Boost concern businesses about score inflation. Business-friendly data collection worries regulators about privacy. Regulatory compliance increases costs for everyone.

Experian's solution has been sequential satisfaction—give each stakeholder wins in turn: - 2015-2017: Focus on consumers with free scores and Boost - 2018-2020: Deliver businesses AI-powered decisions and fraud prevention - 2021-2023: Work with regulators on data protection and financial inclusion - 2024+: Return to consumers with Smart Money and Insurance Marketplace

This rotation prevents any stakeholder from feeling permanently disadvantaged while maintaining long-term balance.

The Geographic Arbitrage

Experian's geographic strategy exploits a fundamental arbitrage: credit bureau economics are similar globally, but market maturity varies drastically.

In mature markets (U.S., UK), Experian earns $15-20 per capita annually. In emerging markets (Brazil, India), they earn $1-3 per capita. As emerging markets develop, that gap closes. Brazil has gone from $0.50 per capita in 2007 to $4.50 in 2024. If Brazil reaches U.S. levels, that's $3 billion in additional revenue.

The arbitrage extends beyond economics. Emerging markets can leapfrog developed markets technologically. They're building mobile-first credit systems without legacy mainframe baggage. They're implementing AI scoring without decades of regulatory precedent. They're creating digital currencies without entrenched payment networks.

Experian positions itself as infrastructure provider for this leapfrogging. They're not exporting U.S. credit models to India—they're building India-specific solutions using global expertise. This localization plus globalization strategy has no peer.

The Platform Power Law

Experian has evolved from product company to platform company, and the economics show it: - Products scale linearly: 2x effort = 2x output - Platforms scale exponentially: 2x users = 4x value

Every new service launched on Experian's platform benefits from existing data, infrastructure, and relationships. Smart Money leveraged credit monitoring subscribers. Insurance Marketplace used credit decision algorithms. Boost utilized consumer authentication systems.

This platform leverage means new products launch faster and cheaper. What took years and hundreds of millions now takes months and tens of millions. The marginal cost of serving additional customers approaches zero. The marginal value of additional data grows with scale.

Competitors trying to replicate individual Experian products miss the point. The power isn't in any single product—it's in the platform that enables rapid product creation, iteration, and scaling.

XI. Analysis & Bear vs. Bull Case

The Bull Case: Compound Inevitability

The bull case for Experian rests on compound inevitability—multiple unstoppable trends that all benefit the company:

Digitization of Finance: Cash is dying. In-person banking is dying. Paper applications are dead. Every financial interaction moving digital requires identity verification, credit decisioning, and fraud prevention—Experian's core competencies. Global digital payments will grow from $7 trillion to $15 trillion by 2030. If Experian maintains its 0.02% take rate on decisions, that's $3 billion in additional revenue.

Emerging Market Credit Explosion: Two billion adults globally lack access to formal credit. As smartphones proliferate and financial infrastructure develops, these populations will enter the credit system. Experian is positioned in the fastest-growing markets—Brazil, India, Indonesia, Nigeria. If these markets reach just 25% of developed market penetration, it represents $10 billion in addressable revenue.

Alternative Data Supremacy: Traditional credit scores are becoming obsolete. The future belongs to whoever can best synthesize alternative data—utility payments, phone bills, social media, IoT devices—into predictive models. Experian's Clarity Services and Boost give them more alternative data than any competitor. As traditional data becomes commoditized, alternative data becomes the differentiator.

Regulatory Tailwinds: Counter-intuitively, increasing regulation helps Experian. GDPR, CCPA, and similar laws make data businesses harder to start and operate. Experian has already built compliance infrastructure that would cost new entrants billions. Open banking regulations force financial institutions to share data, feeding Experian's models. Financial inclusion mandates require alternative scoring methods—Experian's specialty.

AI Scale Advantages: Machine learning models improve with data volume. Experian processes 50 billion data points monthly—10x more than its nearest competitor. This data advantage compounds. Better models attract more customers, generating more data, improving models further. In AI-driven industries, scale advantages become insurmountable.

Subscription Revenue Resilience: With 65% recurring revenue and 90%+ retention rates, Experian has transformed from cyclical to defensive. Even in recessions, businesses need credit decisions and fraud prevention—perhaps more so. The 2008 crisis saw Experian's revenue dip just 3% while maintaining 25%+ margins.

The financial metrics support the narrative: - Revenue CAGR 2014-2024: 8.5% - EBITDA margins: 33% and expanding - ROIC: 18% (exceptional for capital-light business) - FCF conversion: 95% of net income

If these trends continue, Experian could be a $15 billion revenue company by 2030 with 35% margins—implying a $75-100 billion market cap.

The Bear Case: Disruption and Dystopia

The bear case sees multiple threats converging:

Big Tech Invasion: Apple, Google, and Amazon have the data, technology, and capital to build competing credit systems. Apple Card already bypasses traditional credit scoring. Google Pay processes billions of transactions. Amazon knows purchasing patterns better than any credit bureau. If tech giants decide credit bureaus are strategic, they could build or buy their way in.

Blockchain Disintermediation: Decentralized identity and credit systems could eliminate centralized bureaus. Projects like Bloom, Spring Labs, and others envision blockchain-based credit where consumers own their data and share it peer-to-peer. While nascent today, blockchain credit could be what email was to postal mail—a complete paradigm shift.

Privacy Regulation Overreach: Future regulations could cripple data businesses. If Europe's "right to be forgotten" extends to credit data, or if California's privacy laws prohibit data sharing without explicit consent for each use, Experian's model breaks. The pendulum of public opinion is swinging toward privacy—potentially too far for data businesses to survive.

AI Commoditization: As AI tools democratize, Experian's analytical advantages erode. OpenAI, Anthropic, and others offer models that rival Experian's proprietary systems. If any startup can build sophisticated credit models with off-the-shelf AI, what's Experian's moat?

Cybersecurity Catastrophe: Another major breach could be existential. If hackers accessed and published Experian's entire database—every credit file, every transaction, every score—the reputational damage might be unrecoverable. With nation-state actors increasingly targeting financial infrastructure, this isn't paranoid fantasy.

Economic Paradigm Shift: What if credit becomes irrelevant? Central bank digital currencies could eliminate traditional lending. Universal basic income could reduce credit need. Cryptocurrency could enable permissionless finance. These might sound far-fetched, but so did negative interest rates and trillion-dollar tech companies.

Market Saturation: In developed markets, everyone who needs credit has it. Growth requires either taking share (difficult in oligopolistic markets) or expanding internationally (risky and capital-intensive). At some point, Experian simply runs out of room to grow.

The financial concerns are real: - Valuation at 24x P/E versus historical average of 18x - Debt/EBITDA at 2.8x, highest since independence - Organic growth slowing to 5% from double digits - Margins plateauing as easy efficiency gains are exhausted

The Verdict: Asymmetric Upside

Weighing both cases, the asymmetric upside argument appears stronger—but with important caveats.

The bull case rests on structural advantages that are difficult to disrupt. As of late August 2025, Experian trades at £3,744-3,824 per share, giving it a market capitalization of approximately $47 billion. This valuation—while elevated versus historical averages—may still underrepresent the company's strategic position.

Consider the replacement cost analysis. Building Experian from scratch would require: - $5-10 billion in technology infrastructure - $2-3 billion in regulatory compliance setup - $10+ billion in acquisitions to achieve global scale - 10-20 years to build trust and relationships - Solving the chicken-and-egg problem of data network effects

That's $20-30 billion and two decades just to reach competitive parity—and by then, Experian would be two decades ahead. This creates an asymmetric risk/reward: downside might be 30-40% in a severe scenario, but upside could be 100-150% as emerging markets mature.

The bear case risks, while real, appear manageable: - Big Tech: They have the capability but lack the incentive. Credit bureaus are regulated, capital-intensive, and reputationally risky. Why would Apple or Google want that headache when they can partner with Experian instead? - Blockchain: Promising technology seeking a problem. Decentralized credit sounds appealing but faces massive coordination challenges. Who maintains the system? Who resolves disputes? Who ensures data quality? These are solved problems for Experian. - Privacy Regulation: The most serious threat, but Experian has proven adaptable. They've thrived under GDPR, CCPA, and other strict regimes. Regulatory complexity becomes their moat. - AI Commoditization: AI tools are democratizing, but data isn't. Experian's advantage isn't algorithms—it's 50 billion monthly data points that no AI can replicate.

The financial reality supports cautious optimism. Yes, growth is slowing and margins plateauing. But 5-7% organic growth with 30%+ margins and 90%+ cash conversion is exceptional. Few companies at Experian's scale can claim similar economics.

More importantly, Experian has optionality. Smart Money could become a major digital bank. Insurance Marketplace could rival Progressive or Geico. Emerging markets could deliver decades of growth. AI could unlock use cases we haven't imagined. Each option alone could justify the current valuation.

The verdict: Experian represents a rare combination of defensive characteristics (subscription revenue, regulatory moats, network effects) with offensive potential (emerging markets, new products, AI transformation). It's not a moonshot that could 10x, but it's also unlikely to be disrupted overnight.

For long-term investors, Experian offers something precious: a high probability of moderate success with a meaningful probability of exceptional returns. In a world of binary outcomes—disrupt or be disrupted—that's increasingly rare.

As one hedge fund manager put it: "I don't know if Experian will beat the market over the next year. But I'm confident my grandchildren will still be using their services in 50 years. How many companies can you say that about?"

XII. Epilogue & Future Outlook

The Next Decade's Canvas

- A teenager in Lagos applies for her first loan using only her smartphone. She has no credit history in the traditional sense—she's never had a credit card or bank account. But she has something else: five years of mobile money transactions, three years of paying for streaming services, two years of gig economy income, and a social graph showing connections to financially responsible individuals.

Within seconds, an AI model trained on billions of similar profiles across emerging markets generates not just a credit score, but a complete financial profile: risk tolerance, income stability, growth potential, even personalized advice on building wealth. The loan is approved, funded, and deposited—all in under 60 seconds.

This is the future Experian is building toward—one where traditional credit scores become just one input among thousands, where financial inclusion isn't charity but profitable business, where AI doesn't just assess creditworthiness but actively helps consumers build it.

The roadmap is ambitious but grounded in current initiatives:

Open Banking Integration: As regulations force banks to share data via APIs, Experian positions itself as the universal translator—aggregating, standardizing, and analyzing data from thousands of financial institutions. They're not competing with banks; they're becoming the nervous system connecting them.

Behavioral Biometrics: Forget passwords and security questions. Experian's next-generation fraud prevention will identify you by how you type, swipe, and move your mouse. Every interaction becomes a signature, making identity theft virtually impossible.

Predictive Life Events: Using AI to anticipate major financial moments—job changes, marriages, home purchases—before they happen, enabling proactive financial planning rather than reactive credit decisions.