Equinor: The Sovereign Energy Transition

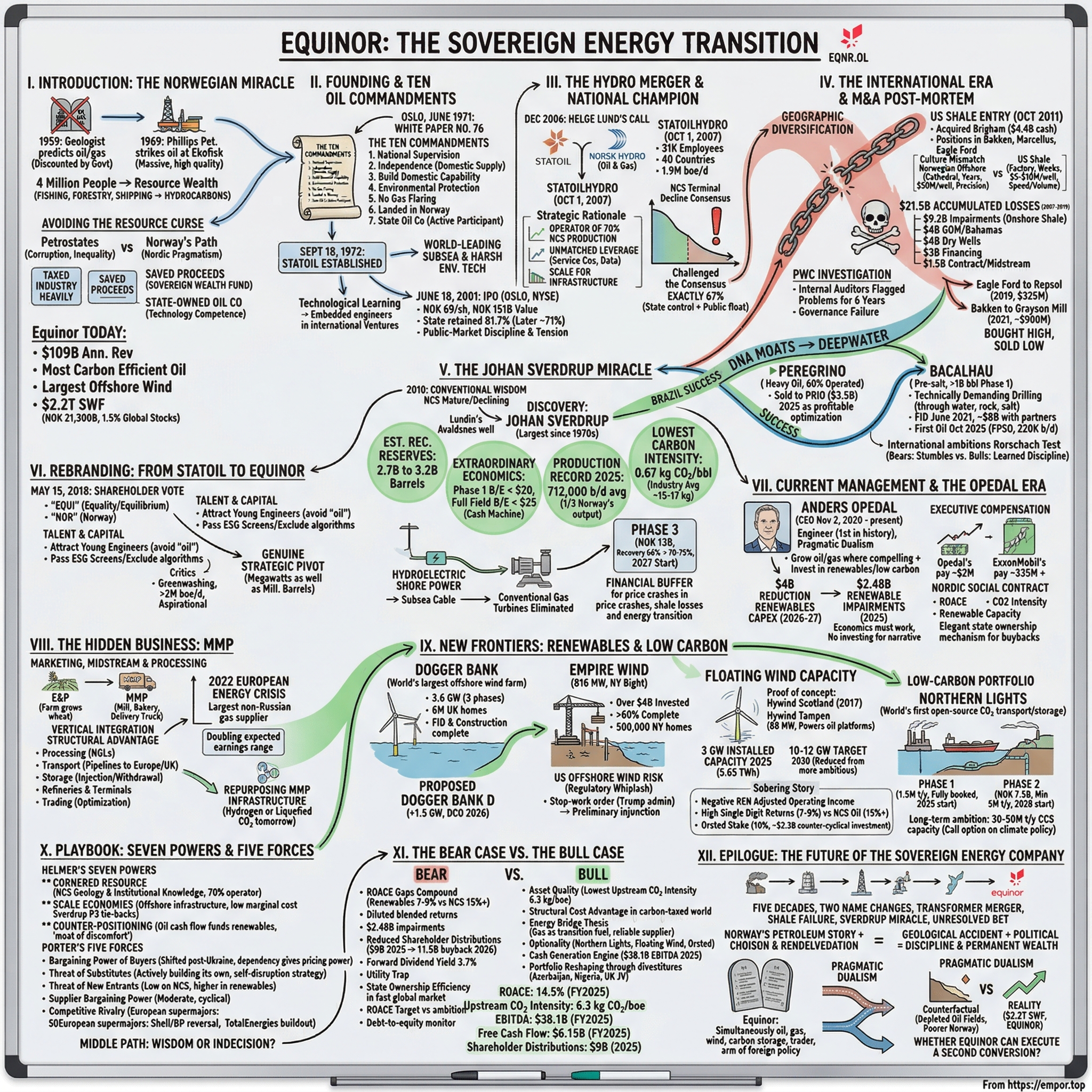

I. Introduction: The Norwegian Miracle

In 1959, a Dutch geologist named Friedrich van Dixhoorn sent a letter to the Norwegian government. The Groningen gas field had just been discovered in the Netherlands, and van Dixhoorn believed similar geological formations extended beneath the North Sea into Norwegian waters. The Norwegian government's response was polite but unequivocal: the Ministry of Foreign Affairs declared in a press release that "the chances of finding oil or gas on the Norwegian continental shelf can be discounted." They could not have been more wrong.

A decade later, on Christmas Eve 1969, Phillips Petroleum struck oil at Ekofisk — a massive field in the Norwegian sector of the North Sea that would eventually yield more than three billion barrels of oil equivalent.

Norway, a country of four million people whose primary industries were fishing, forestry, and shipping, suddenly found itself sitting atop one of the world's great hydrocarbon provinces. The discovery was not just large — it was geologically exceptional. The chalk reservoir at Ekofisk contained high-quality crude oil under conditions that, once the engineering challenges were solved, would make it one of the most productive fields in the world.

What happened next is arguably the most successful exercise in national resource management in human history.

Most countries that discover enormous petroleum reserves succumb to what economists call the "resource curse" — the paradox where natural wealth leads to corruption, inequality, Dutch disease, and long-term economic stagnation. Nigeria, Venezuela, Angola, Iraq — the list of petrostates that squandered their endowments is long and depressing.

Norway looked at that list and decided, with a kind of Nordic pragmatism that borders on stubbornness, to do the opposite. Where other countries spent their oil windfalls on current consumption — subsidized fuel, bloated civil services, vanity infrastructure — Norway taxed the industry heavily, saved the proceeds in a sovereign wealth fund, and built a state-owned oil company designed to maximize not just revenue but national technological competence.

The vehicle they built to execute that vision is Equinor ASA, formerly Statoil — a company that today generates roughly $109 billion in annual revenue, operates the most carbon-efficient oil production in the world, manages the largest offshore wind portfolio of any oil major, and serves as the financial engine behind the Norwegian Government Pension Fund Global. That sovereign wealth fund has grown to approximately $2.2 trillion — roughly NOK 21,300 billion — and now owns about 1.5 percent of every publicly listed company on earth. Its 2025 return of 15.1 percent generated approximately $248 billion in profit in a single year.

Equinor trades on the Oslo Stock Exchange under the ticker EQNR.OL at approximately NOK 368 per share, with a market capitalization of roughly NOK 917 billion. The 52-week trading range — from NOK 226 to NOK 422 — reflects the volatility inherent in a company whose fortunes are tied to global commodity prices, European energy policy, and the pace of the energy transition.

The Norwegian state owns exactly 67 percent of the company, a level maintained by law since 2009. The remaining third trades freely, listed on both Oslo and New York. The stock carries a beta of negative 0.67 — meaning it tends to move inversely to the broader market, a characteristic that makes it a natural portfolio hedge during periods of market stress but an underperformer during risk-on rallies.

The thesis for understanding Equinor is deceptively simple: this is the canary in the coal mine for the entire global energy transition. If the world's most sophisticated, best-capitalized, lowest-carbon oil company — backed by the patient capital of a sovereign owner — cannot successfully pivot from hydrocarbons to renewables, then no oil company can. And if no oil company can, the energy transition will be built entirely by new entrants rather than incumbents, with enormous implications for capital allocation, employment, and geopolitics.

To understand how Equinor arrived at this crossroads, you have to go back to 1971 and a set of principles so foundational that Norwegians still call them "commandments."

II. Founding and the Ten Oil Commandments

The scene is Oslo, June 1971. The Storting — Norway's parliament — is debating White Paper No. 76, and the mood in the room is more cautious than euphoric.

Ekofisk has been producing for barely a year. The money is already flowing. Foreign oil companies are circling, eager to negotiate concessions. The temptation to simply open the taps and collect royalties — as dozens of developing nations have done before and since — must have been enormous.

But the parliamentarians have been watching what oil wealth has done to other countries, and they are determined to avoid the same fate.

The committee chair is Rolf Hellem of the Labour Party, and the document under consideration will become one of the most consequential policy frameworks in modern economic history. The result was a set of ten principles that became known internationally as the "Ten Oil Commandments" — a phrase that captures both their moral weight and their lasting influence.

The commandments were not suggestions. They were the philosophical constitution of Norwegian petroleum governance.

National supervision and control of all continental shelf operations. Petroleum discoveries exploited to make Norway as independent as possible of foreign crude supply. New industry developed on the basis of petroleum — meaning the wealth should build domestic capability, not just fund consumption. Environmental protection explicitly mentioned alongside industrial development. No flaring of gas except during testing periods. Petroleum to be landed in Norway, not shipped directly from offshore platforms to foreign ports. And, most critically for this story, the establishment of a state oil company to ensure the government was not merely a regulator collecting royalties but an active participant in every level of the industry.

What made the commandments remarkable was not any single provision but the totality of the framework. In an era when most oil-producing nations were signing away their resources to international majors in exchange for royalties and signing bonuses, Norway insisted on building domestic capacity from the ground up. The commandments enjoyed cross-party support — a rare consensus in Norwegian politics that has endured for over five decades.

That state oil company was Den norske stats oljeselskap AS — Statoil — established on September 18, 1972. Its founding was not universally popular. Norsk Hydro and Saga Petroleum, the existing Norwegian oil companies, viewed Statoil as an unwelcome competitor backed by the state's regulatory power. International majors like Phillips, Shell, and Exxon saw it as resource nationalism with a Scandinavian accent. Even within the Labour Party, there were debates about whether a state company could be operationally competent in a technically demanding industry dominated by American and British engineers.

The answer took about fifteen years to become clear.

And when it did, the answer was emphatic.

Statoil's early years were defined by a deliberate strategy of technological learning. Norwegian engineers were embedded in international joint ventures, absorbing subsea engineering techniques, deepwater drilling expertise, and project management methodologies from established majors. The company invested heavily in R&D — particularly in the harsh-environment offshore technologies required to operate in the North Sea, where hundred-foot waves, sub-zero temperatures, and extreme water depths made every drilling campaign an engineering ordeal.

By the late 1980s, Statoil had developed proprietary capabilities in subsea processing, multiphase flow technology, and harsh-environment platform design that were genuinely world-leading.

For non-specialists, subsea processing is the ability to separate oil, gas, and water on the seabed floor — hundreds of meters below the surface — rather than bringing everything up to a platform for processing. Multiphase flow technology allows oil, gas, and water to be transported simultaneously through a single pipeline over distances of dozens of kilometers without separating first. These sound like incremental engineering improvements, but they are not. They fundamentally change the economics of offshore development by reducing the need for expensive surface infrastructure. A field that would require a full platform under conventional methods can instead be developed with a simple subsea "tie-back" to an existing facility — at a fraction of the cost and time.

The Ten Commandments had demanded that oil build national competence. They delivered.

The next inflection came on June 18, 2001, when Statoil completed its initial public offering on the Oslo Stock Exchange and the New York Stock Exchange. The IPO priced at NOK 69 per share, valuing the company at approximately NOK 151 billion — roughly $16 billion. The state retained 81.7 percent, later reducing to approximately 71 percent through secondary sales in 2004 and 2005.

The IPO gave Statoil something it had never had before: public-market discipline.

Quarterly earnings calls. Analyst scrutiny. Institutional investor expectations. The constant pressure to deliver returns on capital employed. The requirement to publish audited financial statements, explain capital allocation decisions to skeptical fund managers, and justify executive compensation to proxy advisory firms. These forces reshaped a state-owned enterprise into something more hybrid: a company with the strategic patience of a sovereign owner and the operational intensity of a publicly listed corporation.

That dual nature — part state instrument, part commercial enterprise — remains the defining characteristic of Equinor today. It also created an inherent tension that every CEO since has had to manage: a state owner with a multi-generational time horizon can tolerate investments that take decades to mature, while public shareholders want returns now. Finding the equilibrium between those two mandates would become the central leadership challenge of the company — and the source of both its greatest triumphs and its most expensive mistakes.

III. The Hydro Merger and the National Champion

In December 2006, Statoil's CEO Helge Lund made the phone call that would define the next chapter. Lund, a McKinsey-trained strategist who had taken the top job in 2004 at the unusually young age of forty-one, proposed a merger with Norsk Hydro's oil and gas division — a deal that would consolidate the Norwegian Continental Shelf under a single national champion.

The logic was compelling but not without controversy.

Norsk Hydro was Norway's other great industrial company, with roots stretching back to 1905 and a diversified portfolio spanning oil, gas, aluminum, and hydroelectric power. It was a source of deep national pride — the company that had electrified Norway through hydropower and built a world-class aluminum industry. Merging its petroleum operations into Statoil would create a company of unprecedented scale on the Norwegian shelf, but it would also end Hydro's century-long identity as an independent energy company.

The political debate was intense. Critics argued that concentrating the entire Norwegian petroleum industry in a single state-controlled entity created excessive risk and reduced competition. Supporters countered that the fragmentation of Norwegian shelf operations across multiple companies was preventing the kind of coordinated infrastructure investment that the basin needed to maximize long-term recovery.

The European Commission approved the deal on May 3, 2007. The Storting followed on June 8. Under the merger terms, former Statoil shareholders received 67 percent of the combined entity while Norsk Hydro shareholders received 33 percent — a split that coincidentally mirrored the state's ownership target for the merged company.

Operations under the combined entity — temporarily branded "StatoilHydro" — began on October 1, 2007, bringing together approximately 31,000 employees, operations in roughly forty countries, and combined production of about 1.9 million barrels of oil equivalent per day.

The strategic rationale proved exactly right. The merged company became the operator of approximately 70 percent of all Norwegian continental shelf production — a dominance that gave it unmatched leverage in negotiations with service companies, unparalleled operational data across hundreds of wells, and the scale to invest in ambitious infrastructure projects that smaller operators simply could not fund.

To understand the significance of that 70 percent figure, consider the analogy of a railroad. Operating the majority of tracks in a region does not just give you more trains — it gives you control of the network itself. Scheduling, maintenance, capital allocation, and technology deployment decisions for the entire Norwegian shelf effectively flow through Equinor's project management apparatus. Smaller operators on the shelf — Aker BP, Lundin (now Aker BP after their merger), and various international joint venture partners — operate within a system that Equinor largely defines.

That scale mattered enormously for what came next. The Norwegian Continental Shelf was widely believed to be in terminal decline by the mid-2000s. Production had peaked in 2004 at roughly 4.5 million barrels per day and was falling steadily.

The consensus — shared by energy analysts, investment banks, and even some within the company — was that Norway's best years as a petroleum province were behind it. Every major field — Ekofisk, Statfjord, Gullfaks, Troll — was mature and declining. The remaining prospects were smaller, more technically challenging, and more expensive to develop. Conference presentations routinely showed production curves declining steadily toward irrelevance by the 2030s.

This is a pattern worth recognizing, because it recurs throughout petroleum history. Mature basins are written off, exploration budgets are cut, and the remaining resources are assumed to be small and uneconomic. Then someone drills in the right place with better technology, and a basin that was "dead" suddenly produces more than it ever did. The North Sea was about to provide the most dramatic example of this pattern in modern memory.

The merger gave the combined company the resources and the institutional mandate to challenge the consensus of decline.

And in 2010, they found something that proved it spectacularly wrong. But first, the company had to survive its most expensive lesson.

Helge Lund's tenure delivered 11.2 percent annual shareholder returns, outperforming the industry average by 2.3 percentage points annually over a decade. The name reverted from StatoilHydro to Statoil following a 2009 shareholder vote, integration having been largely completed. Norway had its national champion, and that champion controlled the most productive and profitable offshore acreage in the world.

The Norwegian state's ownership settled at exactly 67 percent through the merger mechanics — a level it has maintained ever since. This was not accidental. The government wanted enough control to set strategic direction but enough public float to impose market discipline. It was, in hindsight, a remarkably sophisticated piece of governance design. The 67 percent stake made the government the ultimate "cornerstone investor" — too large to be outvoted, too invested to walk away, and too visible to allow mismanagement without political consequences.

IV. The International Era and the M&A Post-Mortem

With the Norwegian shelf consolidated, Statoil turned its attention outward. The company's leadership believed — not unreasonably — that a world-class offshore operator should be able to replicate its North Sea success in other basins. The strategy was geographic diversification: reduce dependence on Norway, build a global portfolio, and demonstrate that Statoil's engineering capabilities could generate returns anywhere.

The logic felt unassailable at the time. Norway's production was declining. The company had world-class offshore engineering talent with excess capacity. Oil prices were high and rising. The global exploration frontier was expanding into deepwater Gulf of Mexico, pre-salt Brazil, and — most fatefully — US shale. Why limit a company with $100 billion in enterprise value to a single, mature basin?

The strategy was sound in theory. In practice, it produced the most expensive lesson in Norwegian industrial history.

The centerpiece of the international expansion was the entry into US shale. In October 2011, Statoil acquired Brigham Exploration for $4.4 billion in cash — paying $36.50 per share for a company focused on tight oil production in the Bakken formation of North Dakota's Williston Basin. The company also assembled positions in the Marcellus shale of Appalachia and the Eagle Ford shale of Texas.

The timing could hardly have been worse. Statoil entered the US shale play at the peak of the "land grab" — the frenzied period from 2008 to 2012 when international majors, flush with cash from high oil prices, competed aggressively for acreage in America's emerging unconventional basins.

The competition for leases was intense, prices were inflated, and the operational realities of shale were poorly understood by most international entrants. BHP Billiton had paid $12.1 billion for Petrohawk the same year. Shell was pouring billions into the Permian. It felt like a gold rush, and like most gold rushes, the late arrivals paid the highest prices and earned the worst returns.

The fundamental mismatch was cultural and operational.

Norwegian offshore operations involve multi-billion-dollar platform installations, five-year development timelines, and engineering tolerances measured in millimeters. The decision cycle is measured in years. A single well might cost $50 million or more. Every decision is reviewed, modeled, and stress-tested before capital is committed.

US shale is a manufacturing business — drill, frack, produce, move to the next pad, repeat thousands of times across vast acreage positions. The decision cycle is measured in weeks. Wells cost $5 to $10 million each. Speed and volume matter more than precision. The companies that won in shale were lean, fast-moving independents like EOG Resources and Pioneer Natural Resources that made hundreds of decisions per month, not large bureaucratic organizations that made a dozen per year.

Think of the difference between building a cathedral and running a factory. The skills that make an engineer brilliant at designing a subsea production system in three hundred meters of freezing North Sea water are largely irrelevant when the task is optimizing frack schedules across a hundred wells in North Dakota.

The numbers tell the story with brutal clarity. Between 2007 and 2019, Statoil and its successor Equinor accumulated approximately $21.5 billion in losses on US operations.

The breakdown is worth examining in detail because it reveals the breadth of the failure. The $9.2 billion in impairments on onshore shale assets represents the direct write-down of the value of Brigham and other shale acquisitions — the acknowledgment that the assets were worth far less than what was paid. The $4 billion in Gulf of Mexico and Bahamas write-offs reflects a separate set of exploration bets that failed to find commercial quantities of oil. Another $4 billion went to dry wells and related costs — the drilling equivalent of burning cash. Three billion dollars in financing costs accumulated as the company borrowed to fund operations that were not generating adequate returns. And roughly $1.5 billion disappeared into contract losses and midstream asset write-downs.

Norwegian media called it the biggest industrial scandal in the country's history — approximately NOK 200 billion in destroyed value. The political fallout was significant in a country where the state owns 67 percent of the company and petroleum revenues fund the national budget.

A PricewaterhouseCoopers investigation, commissioned by Equinor's board and published in October 2020, found that the business case for the US shale entry was "marginal and relied on upsides that were not realized." More damningly, the report revealed that internal auditors had flagged problems for six years, but management failed to act on their warnings. The failure was not just strategic — it was a governance failure, a breakdown in the internal checks that should have forced a course correction years before the losses reached catastrophic levels.

The exit was prolonged and painful.

The Eagle Ford position was sold to Repsol in 2019 for $325 million — a fraction of the invested capital. The Bakken position — 242,000 net acres producing approximately 48,000 barrels per day — was sold to Grayson Mill Energy for roughly $900 million, closing on April 27, 2021.

Compare those exit prices to the $4.4 billion paid for Brigham alone, and the magnitude of the value destruction becomes visceral. Equinor bought high, operated at a loss, and sold low — the trifecta of bad capital allocation.

The contrast with Brazil could not be starker. While the US shale adventure was destroying billions, Equinor's Brazilian operations were quietly demonstrating that the company's deepwater engineering DNA could generate returns outside Norway — when deployed in the right geological and operational context.

Peregrino, a heavy oil field offshore Brazil where Equinor held a 60 percent operated interest, produced reliably for years. In May 2025, Equinor sold the asset to PRIO, Brazil's largest independent oil and gas company, for $3.5 billion including contingent payments — a profitable exit that represented genuine portfolio optimization rather than the fire-sale disposals that characterized the US retreat.

The crown jewel is Bacalhau — a massive pre-salt field in the Santos Basin with estimated recoverable reserves exceeding one billion barrels in Phase 1 alone. For readers unfamiliar with Brazilian offshore terminology, "pre-salt" refers to oil deposits trapped beneath a thick layer of salt several kilometers below the ocean floor. Reaching these reservoirs requires drilling through deep water, then through rock, then through a salt layer that can be two kilometers thick, then through more rock to reach the oil. It is, by any measure, among the most technically demanding drilling operations on earth — and precisely the kind of engineering challenge at which Equinor excels.

The final investment decision came in June 2021, committing approximately $8 billion alongside partners ExxonMobil and Petrogal Brasil. The FPSO — 370 meters long with production capacity of 220,000 barrels per day — delivered first oil in October 2025. Bacalhau validated what the US shale debacle had called into question: Equinor could execute complex deepwater projects internationally, provided the geology matched their engineering strengths.

The lesson is one that many integrated oil companies have learned at enormous cost: operational excellence in one domain does not automatically transfer to another. Equinor's offshore DNA — patience, precision, massive capital deployment over long timelines — was perfectly suited to Brazil's pre-salt plays and catastrophically mismatched to US shale's manufacturing-speed economics.

The US and Brazil experiences, taken together, form a Rorschach test for the company's international ambitions. Bears see a company that consistently stumbles outside its Norwegian comfort zone — the US shale impairments as Exhibit A, with the Orsted stake and Empire Wind as potential Exhibits B and C. Bulls see a company that learned from its most expensive mistake, exited positions that did not fit its competencies, doubled down on those that did, and now applies that discipline to its renewable expansion. The truth, as usual, is more nuanced than either narrative. But the $21.5 billion in US losses remains scar tissue that shapes every international investment decision the company makes today.

V. The Johan Sverdrup Miracle

By 2010, the conventional wisdom about the North Sea was well established: the basin was mature, production was declining, and the remaining opportunities were marginal fields requiring heroic engineering and high oil prices to be economic. The glory days of Ekofisk, Statfjord, and Troll were behind Norway. The future was managed decline.

Then Lundin Petroleum drilled the Avaldsnes well in a part of the central North Sea that had been extensively explored for decades. Everyone assumed the area had been picked clean. The well was almost an afterthought — a low-probability prospect in a basin that most geologists considered thoroughly understood.

And everything changed.

The discovery, later combined with an adjacent find called Aldous Major South, turned out to be a single enormous structure named Johan Sverdrup — after Norway's first prime minister. With estimated recoverable reserves of 2.7 billion barrels (some estimates reaching 3.2 billion), it was the largest find on the Norwegian Continental Shelf since the 1970s and one of the largest offshore discoveries anywhere in the world in the twenty-first century.

The economics were extraordinary. Phase 1, which began production in October 2019, achieved a break-even price below $20 per barrel — at a time when most new offshore developments globally required $40 to $60 per barrel to justify the investment. Phase 2, adding over 220,000 barrels per day of capacity, had a break-even below $30. The full-field break-even sits below $25 per barrel.

For non-oil specialists, "break-even" means the oil price at which the project generates zero profit after all operating and capital costs. At any price above that threshold, every additional dollar flows directly to the bottom line. At a break-even below $25 and a Brent crude price that has averaged well above $70 for most of the past five years, the profit margin on every barrel from Johan Sverdrup is enormous.

To put those numbers in context: even during the worst oil price crash of the past decade — when Brent crude briefly traded below $20 in April 2020 — Johan Sverdrup was generating positive cash flow. It is, in the most literal sense, a cash machine that runs in virtually any price environment.

The field reached peak capacity of 755,000 barrels per day and produced a record 260 million barrels in 2025 at an average rate of 712,000 barrels per day.

That is roughly one-third of Norway's entire oil output from a single field — the third-largest on the Norwegian Continental Shelf. To appreciate the concentration: Equinor's total equity production across all assets worldwide was 2,137 thousand barrels per day in 2025. Johan Sverdrup alone accounted for more than a third of that figure. No other single asset in Equinor's portfolio comes close to matching its contribution to cash flow and production.

Perhaps the most remarkable statistic is its carbon intensity: 0.67 kilograms of CO2 per barrel. The global industry average is approximately 15 to 17 kilograms per barrel.

How is this possible? The answer is hydroelectric shore power. On a conventional offshore platform, gas turbines burn natural gas to generate the electricity needed to run pumps, compressors, and processing equipment. Those turbines are the largest source of greenhouse gas emissions in offshore oil production. At Johan Sverdrup, Equinor eliminated them entirely by running a subsea power cable from the Norwegian mainland — where virtually all electricity is generated by hydroelectric dams — to the platform. The oil is produced using renewable electricity, making it roughly twenty-five times cleaner per barrel than the global average.

There is no other large-scale oil field anywhere in the world that comes close. This is not a marginal improvement. It is a categorical difference — the kind of advantage that becomes increasingly valuable as carbon costs rise globally.

In July 2025, Equinor approved Phase 3 — a NOK 13 billion investment targeting an additional 40 to 50 million barrels through eight new wells. The goal is to push the recovery rate from approximately 66 percent to 70 to 75 percent, with production starting in the fourth quarter of 2027. TechnipFMC was awarded a NOK 5.3 billion integrated contract for the work.

Sverdrup's significance extends beyond its own economics. The discovery provided Equinor with the financial buffer it needed to survive the 2014 oil price crash, absorb the US shale losses, and begin investing in offshore wind and carbon capture. Without Sverdrup, the energy transition strategy that defines Equinor today would have been financially impossible. It is, without exaggeration, the most important legacy asset in the modern history of the European oil industry. Production is expected to decline 10 to 20 percent from its plateau beginning in 2026, but Phase 3 signals Equinor's intent to squeeze every recoverable barrel from this field — and the economics justify every dollar spent doing so.

VI. Rebranding: From Statoil to Equinor

On March 15, 2018, the board of directors of Statoil ASA proposed something that would have been unthinkable a decade earlier: dropping "oil" from the company's name.

The proposal went to a shareholder vote at the annual general meeting on May 15, 2018. The government, holding its 67 percent stake, supported the change. All five employee unions backed it. The resolution passed by a wide margin, and the new name — Equinor — became effective the following day.

The name was a deliberate construction. "Equi" from equality and equilibrium — a nod to the balanced approach between traditional energy and renewables. "Nor" from Norway — the company's identity, heritage, and strategic anchor.

The rebranding cost an estimated $30 million, covering everything from platform signage in the North Sea to business cards in thirty countries. The company had already been renamed once — from StatoilHydro back to Statoil in 2009 — making this the second identity change in a decade. For a company that prides itself on long-term thinking, the name instability was ironic. But the strategic rationale was different from the 2009 change, which was about simplification. This one was about transformation.

CEO Eldar Saetre, who led the company from February 2015 through the rebranding period, offered a rationale that went beyond environmental signaling. The name change, he argued, was fundamentally about talent and capital.

The talent argument was straightforward. The best young engineers in Norway — and globally — were increasingly reluctant to join a company with "oil" in its name. University recruiting had become measurably harder. The cognitive dissonance of working for "Statoil" while developing offshore wind farms was creating friction that the old brand could not resolve.

The capital argument was more subtle but equally important.

Institutional investors were beginning to apply ESG screens that automatically excluded companies with "oil" or "petroleum" in their names from certain index funds and mandates. The exclusion criteria were crude — sometimes literally based on keyword searches of company names rather than actual emissions profiles or transition strategies — but the capital flows affected were real.

A company called "Statoil" would be screened out by algorithms that a company called "Equinor" would pass through. It sounds absurd, and in many ways it was. But in asset management, where trillions of dollars are allocated by systematic strategies that apply rigid inclusion and exclusion criteria, naming conventions have real financial consequences. Equinor needed to signal to asset allocators that it was something different from a pure-play oil company, even if the underlying production profile had not yet fully transformed.

Critics dismissed it as greenwashing. Oil Change International and environmental groups pointed out that the company was still producing more than two million barrels of oil equivalent per day with no plans to stop. Removing "oil" from the name, they argued, was cosmetic surgery on a business model that remained fundamentally petroleum-dependent.

There was also a shareholder proposal at the same AGM requesting a full transformation from fossil fuels to renewable energy. It was not adopted. The juxtaposition was telling: the company was willing to change its name but not, at that point, willing to commit to a fundamental restructuring of its asset base. The rebranding was aspirational, not operational.

But the rebranding also coincided with a genuine strategic pivot that would, over the following years, give the new name substantive meaning. Capital deployment began shifting — slowly at first, then more meaningfully — from barrels of oil to gigawatts of power. The Hywind Scotland floating wind farm, the world's first commercial installation of its kind at 30 megawatts, had been operational since 2017. Dogger Bank, which would become the world's largest offshore wind farm, was in advanced development. The name change was not the strategy. But it was the public declaration that the strategy had changed — that the company's M&A playbook was now measured in megawatts as much as in millions of barrels.

Whether the rebranding was premature, appropriately timed, or overdue depends on one's view of the energy transition timeline. What is indisputable is that it forced a conversation — internally and externally — about what kind of company Equinor intended to become. The new CEO who took over two years later would be tasked with answering that question.

VII. Current Management and the Opedal Era

Anders Opedal took over as CEO on November 2, 2020, inheriting a company in the middle of a pandemic, an oil price collapse, and the still-unresolved aftermath of the US shale debacle. He was fifty-two years old, and he was the first engineer to lead the company in its history.

That fact is more significant than it might appear. Opedal's predecessors had been lawyers, management consultants, and finance executives — leaders who thought in terms of strategy, capital allocation, and stakeholder management. The engineer's appointment signaled a shift toward operational pragmatism: a recognition that Equinor's next chapter would be defined not by grand pronouncements but by the grinding, technically complex work of actually building wind farms, drilling carbon storage wells, and optimizing oil production simultaneously.

Opedal holds an engineering degree from NTNU in Trondheim and an MBA from Heriot-Watt University in Edinburgh. He began his career at Schlumberger and Baker Hughes — the oilfield services companies where engineers learn the physical realities of drilling and production before ascending to corporate strategy. He joined Statoil in 1997 and rose through petroleum engineering, chief procurement officer, head of the company's NOK 300 billion project portfolio, country manager for Brazil from 2017 to 2019, and finally executive vice president for technology, projects, and drilling.

His leadership style has been described as "pragmatic dualism" — a willingness to grow oil and gas production where the economics are compelling while simultaneously investing in renewables and low-carbon technologies, and a readiness to cut spending on either side when the numbers do not work.

Under Opedal, Equinor achieved record production of 2,137 thousand barrels of oil equivalent per day in 2025 — up 3.4 percent year-on-year — while simultaneously advancing the world's largest offshore wind farm and the world's first commercial carbon storage facility. That ability to execute on both fronts simultaneously is the operational manifestation of pragmatic dualism.

But the pragmatism cuts both ways. In late 2025 and early 2026, Opedal announced a $4 billion reduction in renewables and low-carbon capital expenditure for 2026 and 2027, drawing sharp criticism from environmental advocates who had positioned Equinor as a transition leader. The company also took $2.48 billion in impairments on renewable assets in 2025, primarily related to US offshore wind synergies and revised price assumptions.

Opedal's response was characteristically blunt: the economics had to work. Investing in renewables for the sake of narrative — to look good in ESG rankings while destroying shareholder value — was precisely the kind of decision-making that had led to the US shale debacle. If returns on renewable projects were inadequate, capital would be reallocated to higher-returning opportunities, including oil and gas.

His compensation reflects the unique hybrid nature of the company — and the unique constraints of Norwegian corporate governance.

Total pay in 2024 was approximately NOK 22 million — roughly $2 million. His base salary sits at approximately NOK 9.1 million, with an annual variable component targeted at 25 percent of base salary (maximum 50 percent) and a long-term incentive at 30 percent. His compensation was increased by approximately NOK 1 million for 2025, aligned with government bonus guidelines. Six Equinor executives earned above NOK 10 million in 2025.

For context, ExxonMobil's CEO earned more than $35 million in 2024 — roughly seventeen times Opedal's total.

The gap is not accidental. Norwegian corporate governance norms, reinforced by the state's 67 percent ownership, impose explicit constraints on executive pay that would be unthinkable in Houston or London. There are no stock option packages worth tens of millions. No golden parachutes. No retention bonuses that dwarf base salary. The entire compensation philosophy is rooted in the Nordic social contract: executives are well-paid professionals, not plutocrats.

Opedal operates, as one analyst put it, "more like a high-level civil servant with commercial authority than a traditional CEO." Low relative salary, but massive geopolitical influence — the man effectively controls Europe's most important non-Russian energy supply.

His compensation is tied to three categories of performance metrics: ROACE (return on average capital employed), CO2 intensity reduction, and renewable capacity growth. The structure embeds the strategic tension at the heart of the company: deliver hydrocarbon returns today while building the clean energy business of tomorrow, and do both while reducing the carbon intensity of every barrel produced.

The government's 67 percent ownership stake is maintained through an elegant mechanism. When Equinor conducts share buybacks — $5 billion in 2025, reduced to $1.5 billion for 2026 — the state redeems and cancels a proportionate number of its own shares at each annual general meeting, ensuring the percentage remains exactly 67 percent regardless of how many shares are repurchased from public shareholders.

The Norwegian state is simultaneously a dividend recipient benefiting from high oil prices, a climate policy actor committed to aggressive emissions targets, and a sovereign wealth fund manager holding $2.2 trillion in global equities including positions in companies that compete with Equinor. No other major energy company operates under this degree of strategic complexity — and no other CEO must navigate it.

VIII. The Hidden Business: Marketing, Midstream and Processing

The segment that generates the most revenue at Equinor is not exploration and production. It is Marketing, Midstream and Processing — MMP — the division that processes, transports, stores, and trades oil, gas, LNG, electricity, and carbon emission rights across global markets.

MMP is Equinor's least understood and arguably most valuable asset. While E&P gets the analyst attention and renewables gets the headlines, MMP is the trading powerhouse that captures the spread between wellhead prices and delivered prices — the margin embedded in the physical infrastructure and commercial relationships connecting Norwegian gas fields to German living rooms and British power stations.

Think of it this way: if E&P is the farm that grows the wheat, MMP is the mill, the bakery, and the delivery truck.

Equinor does not just pump gas. It controls the processing plants that separate natural gas liquids from dry gas. It operates the pipeline infrastructure that moves gas from the Norwegian shelf to Continental Europe and the UK. It manages the storage facilities that allow gas to be injected during low-demand periods and withdrawn during peaks. It operates refineries and terminals. And it runs the trading desks that optimize the timing and pricing of every molecule sold.

The segment generated the largest share of the company's revenue — roughly $106 billion in 2023 alone. Most casual observers of Equinor assume the company's revenue comes primarily from pumping oil and gas. In reality, the majority flows through MMP's trading and logistics operations.

The segment's importance became unmistakable during the 2022 European energy crisis. When Russia curtailed pipeline gas supplies following the invasion of Ukraine, European gas prices spiked to historic levels. Equinor, as the largest non-Russian supplier of pipeline gas to Europe, sat at the exact center of this supply crunch. MMP's trading desks captured massive spreads as European utilities scrambled to secure supply at any price. Total company revenue in 2022 reached $148 billion — compared to $97 billion in 2024 and $109 billion in 2025. MMP's quarterly adjusted operating income guidance was raised from a range of $250 to $500 million to $400 to $800 million — a doubling of the expected earnings range.

This vertical integration creates a structural advantage that pure-play producers cannot match. A company that only produces gas sells at the wellhead price. Equinor captures the wellhead price plus the processing margin plus the transportation margin plus the storage margin plus the trading margin. In a stable market, these incremental margins are modest. In a volatile market like 2022, they are enormous.

The analogy is a farmer who also owns the grain elevator, the flour mill, the bakery, and the delivery trucks. In a normal year, most of the profit comes from the farm. But in a year when grain prices spike, every link in the chain captures an amplified margin — and the integrated operator earns multiples of what the pure-play farmer does. That is exactly what happened to MMP in 2022.

It is worth noting that Equinor's total net income fell from its 2022 windfall of $28.6 billion to $5.19 billion in 2025, despite revenue recovering to $109 billion. The decline reflects the normalization of European gas prices from their 2022 crisis peaks — a reminder that MMP's extraordinary 2022 profitability was driven by exceptional market conditions rather than structural improvements.

In March 2026, Equinor announced that MMP would be split into two separate segments effective early 2027: Trading and Marketing, led by Irene Rummelhoff, and Midstream, Processing and Infrastructure, led by Geir Soertvedt. The restructuring reflects recognition that the trading operations and the infrastructure assets have different risk profiles, capital requirements, and strategic trajectories — and that investors deserve clearer visibility into each.

The restructuring also hints at future optionality.

The physical infrastructure that moves methane molecules today — pipelines, processing plants, terminals — could, in theory, move hydrogen molecules or liquefied CO2 tomorrow. Natural gas pipelines can be converted to carry hydrogen blends, and potentially pure hydrogen, with relatively modest modifications. LNG terminals can be adapted for hydrogen or ammonia import and export. Storage facilities can be repurposed for hydrogen buffering.

That repurposing potential is currently unpriced by the market but increasingly relevant as European hydrogen policy takes shape. If the European hydrogen economy develops as policymakers envision, Equinor's MMP infrastructure could become as strategically important for clean energy distribution as it currently is for natural gas.

IX. New Frontiers: Renewables and Low Carbon

On a patch of the North Sea roughly 130 kilometers off the northeast coast of England, 277 wind turbines are rising from the water in what will become the world's largest offshore wind farm.

Dogger Bank — named for the submerged sandbank that has been a fishing ground since the Viking age and a naval battlefield in both world wars — represents Equinor's most ambitious bet on the energy future. The location is not accidental: the shallow waters and consistent wind patterns over Dogger Bank make it one of the best offshore wind sites in the world, and Equinor's decades of North Sea operational experience translate directly into the ability to install, maintain, and operate turbines in these challenging conditions.

Total capacity across three phases will reach 3.6 gigawatts. Each phase contributes 1.2 gigawatts. The project is a joint venture with SSE Renewables and Vargronn, with Equinor as lead operator. Phase A delivered first power in October 2023 and reached commercial operations in 2024. Phase B achieved commercial operations in 2025. Phase C is targeted for 2026. When fully operational, Dogger Bank will generate enough electricity to power approximately six million UK homes. A proposed fourth phase — Dogger Bank D — would add another 1.5 gigawatts, with the development consent application expected between July and September 2026.

Across the Atlantic, Empire Wind 1 — an 816-megawatt project in the New York Bight, located 15 to 30 miles south of Long Island — represents Equinor's most important and most politically fraught US renewable investment.

Over $4 billion has been invested. The project is more than 60 percent complete. First power is expected in late 2026 or early 2027. When operational, it will supply electricity to approximately 500,000 New York homes.

But the path to completion has been anything but smooth. On December 22, 2025, the Trump administration issued a stop-work order affecting the project. Equinor responded by filing for a preliminary injunction, and Judge Carl J. Nichols granted it on January 15, 2026, allowing construction to resume. An earlier Bureau of Ocean Energy Management stop-work in April 2025 was also resolved.

The regulatory whiplash illustrates a risk that is unique to US offshore wind: the projects require billions of dollars in upfront capital, take years to build, and are subject to federal permitting decisions that can change with each administration. For a company accustomed to the regulatory stability of Norway — where energy policy enjoys cross-party consensus and licensing decisions are rarely reversed — the US political environment introduces a category of risk that is fundamentally different from geological or engineering risk.

Beyond the flagship projects, Equinor operates nearly half of the world's installed floating wind capacity — a distinction worth pausing on. Floating wind is to conventional offshore wind what deepwater drilling was to shallow-water drilling: the technology that unlocks the next frontier. Fixed-bottom turbines require water depths of roughly 60 meters or less. Floating platforms can operate in depths of several hundred meters, opening vast new geographic markets — the US West Coast, the Mediterranean, Japan, South Korea — where conventional offshore wind is physically impossible. Hywind Scotland, operational since 2017, was the proof of concept. Hywind Tampen, at 88 megawatts, powers the Snorre and Gullfaks oil platforms, using wind energy to reduce the carbon intensity of oil production itself.

Total installed renewable capacity at year-end 2025 reached 3 gigawatts, with renewable power generation of 5.65 terawatt-hours — up 25 percent year-on-year. The target is 10 to 12 gigawatts by 2030, reduced from earlier, more ambitious projections. To put 3 gigawatts in context, that is enough to power roughly two million homes — significant, but still a small fraction of the energy generated by Equinor's oil and gas portfolio.

The renewables segment financials tell a sobering story. The REN segment has reported negative adjusted operating income in recent quarters — a "capital sink" that absorbs billions in investment while generating returns in the high single digits, compared to the 15 to 20 percent or higher returns available from Norwegian Continental Shelf oil production. The fundamental question for investors is whether the renewable portfolio will eventually generate returns that justify the capital deployed, or whether it will remain a structurally lower-return business that dilutes overall profitability.

That reduction in the 2030 target reflects a broader industry reckoning. In late 2025 and early 2026, Equinor cut renewables and low-carbon capex by $4 billion for the 2026 to 2027 period. The company took $2.48 billion in impairments on renewable assets — predominantly US offshore wind — where supply chain inflation, higher interest rates, and slower permitting pushed costs well beyond original assumptions. Equinor is not alone: Orsted wrote down billions on US projects in 2023, and BP has retreated dramatically from its renewable commitments.

Speaking of Orsted: in December 2024, Equinor completed the acquisition of a 10 percent stake in the Danish offshore wind giant for approximately $2.3 billion, becoming the second-largest shareholder after the Danish state. Opedal called it "a counter-cyclical investment in a leading developer" — buying into the world's largest offshore wind company at a moment of peak sector pessimism. Whether this proves to be a brilliant contrarian bet or another international overreach in the mold of Brigham Exploration will not be clear for years.

The low-carbon portfolio centers on Northern Lights — the world's first open-source commercial CO2 transport and storage facility, jointly owned by Equinor, Shell, and TotalEnergies in equal thirds. The concept is straightforward but revolutionary: industrial emitters capture their CO2, liquefy it, ship it to an onshore terminal at Oygarden in western Norway, and Northern Lights pipes it to injection wells beneath the North Sea for permanent geological storage. Think of it as the "landfill of the future" — but instead of burying garbage, you are burying carbon dioxide kilometers below the seabed.

Phase 1, with capacity of 1.5 million tonnes per year, completed its first CO2 injection in August 2025. The facility is fully booked — every tonne of its annual capacity has been committed to customers — which itself is a significant commercial milestone for a technology that many skeptics dismissed as economically unviable.

Phase 2 received final investment decision in March 2025 with a NOK 7.5 billion investment, expanding capacity to a minimum of 5 million tonnes per year with expected operations in the second half of 2028. Customer agreements already cover 900,000 tonnes annually from Stockholm Exergi, with additional volumes expected from Denmark and the Netherlands in 2026.

The long-term ambition is 30 to 50 million tonnes of CO2 equivalent in CCS capacity by 2035. If European carbon prices rise to levels that make CCS economically essential — and the direction of EU policy suggests they will — Equinor owns critical infrastructure for a multi-billion-dollar industry that does not yet fully exist. It is an option on climate policy itself.

X. Playbook: Seven Powers and Five Forces

Hamilton Helmer's Seven Powers framework, applied rigorously, reveals that Equinor possesses three genuine structural advantages — an unusually strong position for any company, and particularly remarkable for one in a commodity industry where competitive moats are notoriously difficult to sustain.

The most unambiguous power is the cornered resource. The Norwegian Continental Shelf is not open to all comers. Operating licenses are awarded by the Norwegian government through a process that heavily favors Equinor, which operates 70 percent of all Norwegian production.

The specific acreage — Johan Sverdrup, Troll, the remaining NCS portfolio — represents some of the highest-margin, lowest-carbon oil production on earth. No competitor can replicate these assets. They are geological endowments controlled by a company with sovereign backing to retain them indefinitely.

The cornered resource extends beyond geology to institutional knowledge: forty years of North Sea operations have built organizational capability that cannot be purchased or poached. It must be built over decades. A new entrant to the Norwegian shelf would need not just a license but decades of operational experience in some of the harshest conditions in the global oil industry. The resource is cornered by both geology and institutional history.

The second power is scale economies in offshore infrastructure.

Equinor's subsea production systems, pipeline networks, and processing facilities on the Norwegian shelf represent billions of dollars of installed infrastructure. Each incremental barrel produced through existing facilities incurs minimal marginal cost — the platforms are already built, the pipelines already laid, the processing capacity already installed.

A competitor developing a new field in the same basin bears the full cost of greenfield infrastructure, while Equinor can often tie back new wells to existing facilities at a fraction of the cost. Johan Sverdrup's Phase 3 — connecting new wells to existing infrastructure for NOK 13 billion to recover 40 to 50 million additional barrels — is the textbook example. The cost per incremental barrel is dramatically lower than any greenfield development.

The third power is counter-positioning. Equinor uses the enormous cash flows from its oil production to fund construction of a renewable energy portfolio. This is a strategy that smaller pure-play renewable developers cannot replicate — they lack the cash flows — and that larger oil majors have been reluctant to pursue with comparable commitment. Shell has declared it sees no "competitive advantage" in renewables. BP slashed its renewable investment by 70 percent and abandoned climate targets. Equinor occupies the uncomfortable middle: still growing oil production while building the world's largest offshore wind farm. The discomfort is the moat. Competitors who refuse to tolerate the contradiction cannot follow Equinor's path.

Now apply Porter's Five Forces.

The bargaining power of buyers has shifted dramatically since 2022. Before Russia's curtailment of gas supplies, European buyers had multiple suppliers and significant negotiating leverage. Today, Equinor is the largest non-Russian supplier of pipeline gas to Europe — a position of extraordinary strategic importance. Germany and the UK are structurally dependent on Norwegian gas in a way they were not five years ago. This dependency provides pricing power reinforced by geopolitics rather than market dynamics alone.

The threat of substitutes is the most intellectually interesting force, because Equinor is actively building the substitute. Offshore wind, hydrogen, and carbon capture are not threats to Equinor's business — they are Equinor's business, or at least the business Equinor intends to become.

This self-disruption strategy is rare in corporate history and inherently unstable. Clayton Christensen wrote extensively about why incumbents fail at self-disruption: the existing business is too profitable, the new business is too risky, and the organizational culture optimized for the old model fights the new one at every turn. Equinor's bet is that its offshore engineering capabilities, project management discipline, and patient sovereign capital give it a structural advantage in managing this transition that other incumbents lack. The jury is still out.

The threat of new entrants is low on the Norwegian shelf — license requirements, capital intensity, and Equinor's incumbent advantages create effectively insurmountable barriers. In renewables, the threat is higher: offshore wind is competitive and growing, with Orsted, Iberdrola, RWE, and well-capitalized newcomers all vying for seabed leases and power purchase agreements.

Supplier bargaining power is moderate and cyclical. Offshore service companies — rig operators, subsea contractors, fabrication yards — wield significant pricing power during periods of high activity, as the NOK 5.3 billion TechnipFMC contract for Sverdrup Phase 3 illustrates.

Competitive rivalry among European majors is intense but differentiated. TotalEnergies remains the most committed to its renewable buildout among the European supermajors, still targeting 100 gigawatts by 2030, though it trimmed its renewable capex from $5 billion to $4.5 billion in 2025. Shell has tilted decisively back toward oil and gas, with its CEO explicitly questioning whether the company has a "competitive advantage" in renewables. BP has executed the most dramatic strategic reversal in the sector — slashing renewable investment by 70 percent, abandoning climate targets, and taking a $5.4 billion write-down on green assets.

Equinor's middle position — cutting renewable spending but maintaining flagship projects and unique capabilities in floating wind and CCS — sets it apart from peers who have chosen more binary strategies. Whether this middle path represents strategic wisdom or strategic indecision is the question that divides the analyst community. The pragmatists argue that Equinor is doing what the physics and economics demand: producing low-carbon oil profitably while building renewable capacity at a pace that actual returns justify. The skeptics argue that the middle path delivers neither the pure-play oil returns that energy investors want nor the clean energy growth that ESG-focused investors require.

XI. The Bear Case vs. The Bull Case

The bear case begins with simple arithmetic. Norwegian Continental Shelf oil projects generate returns on capital employed of 15 percent or higher. Offshore wind projects, even well-executed ones, currently deliver returns in the high single digits — perhaps 7 to 9 percent in optimistic scenarios. That is a meaningful gap — and in capital allocation, gaps compound.

As the company shifts capital from oil to renewables — even at the moderated pace now planned — the blended return on capital must decline. Capital expenditure in 2025 reached $14.4 billion, with an increasing share directed toward lower-return renewable projects. Free cash flow fell to $6.15 billion from $7.93 billion in 2024 and the windfall $26.4 billion of 2022. The concern is what equity analysts call the "utility trap": a company that once generated oil-major returns gradually transforming into an entity that generates utility-like returns, while retaining the commodity price volatility and political risk of an oil company. The $2.48 billion in renewable impairments in 2025 reinforces this fear — if even Equinor, with its decades of offshore experience and sovereign backing, cannot generate acceptable returns in offshore wind, the argument for continued capital deployment weakens.

The shareholder returns trajectory tells its own story. The 2025 buyback program was $5 billion. For 2026, it was slashed to $1.5 billion — a 70 percent reduction. The quarterly dividend, at $0.39 per share, continues to increase by $0.02 per share annually, but the total return package is shrinking.

Total shareholder distributions in 2025 were $9 billion — comprising $5 billion in buybacks and approximately $4.93 billion in dividends. For 2026, with buybacks reduced to $1.5 billion, the total distribution will be roughly half of the prior year's level. For investors who own Equinor as an income stock — and at a trailing yield of approximately 8 percent, many do — the direction is concerning.

The forward dividend yield, stripped of the buyback component, is approximately 3.7 percent — a level that makes Equinor competitive with utilities but unremarkable among energy majors.

There is also the state ownership question. Can a company 67 percent owned by a government — a government simultaneously pursuing aggressive climate targets, collecting petroleum revenues, and managing a $2.2 trillion investment fund — ever be truly efficient in a competitive global renewable market?

State-owned enterprises historically struggle with the speed, risk tolerance, and entrepreneurial flexibility that emerging industries demand. The US shale experience provides an uncomfortable data point: when Equinor ventured outside its North Sea comfort zone into a fast-moving, entrepreneur-driven American market, the result was $21.5 billion in losses. Offshore wind is also a competitive, fast-evolving market where agility matters — and a company that runs decisions through Oslo ministerial channels may not move fast enough.

The ROACE target of greater than 15 percent — already under pressure at 14.5 percent for FY2025 — may prove incompatible with an aggressive renewable buildout. Something will have to give: the return target, the renewable ambition, or the dividend. The balance sheet provides some cushion: net debt stood at $28.4 billion against equity of $40.4 billion at year-end 2025, with a debt-to-equity ratio of 0.83. But the trajectory of rising net debt — up from $24.2 billion in 2024 — deserves monitoring.

The bull case starts with asset quality. Equinor's upstream CO2 intensity of 6.3 kilograms per barrel of oil equivalent is the lowest among the major integrated oil companies — less than half the global industry average of 15 to 17 kilograms. By 2030, the target is 6 kilograms — a level that Equinor is already approaching, having achieved a 34 percent reduction from its 2015 baseline by the end of 2025.

In a world where carbon costs are rising through emissions trading schemes, border adjustment mechanisms, and direct carbon taxes, the lowest-carbon producer has a structural cost advantage that grows every year. Every dollar-per-tonne increase in the effective carbon price disproportionately penalizes high-emission producers while barely affecting Equinor. This is not a theoretical advantage. The EU Emissions Trading System is expanding in scope and ambition, and the direction of global carbon pricing policy is unambiguously upward.

The second bull argument is the "energy bridge" thesis. Europe needs natural gas as a transition fuel while renewable capacity scales. Equinor is the continent's most reliable, most politically acceptable, and most geographically proximate supplier. The post-Ukraine reconfiguration of European energy supply has elevated Equinor from important to essential. That essentiality provides pricing power, demand visibility, and political goodwill that translate directly into commercial advantage.

The third argument centers on optionality. Northern Lights, if European carbon prices reach levels that make large-scale storage economically mandatory, represents a call option worth potentially tens of billions. Floating wind technology, in which Equinor has more operational experience than any competitor, becomes increasingly valuable as development moves into deeper waters. The Orsted stake provides exposure to the world's leading offshore wind developer at what may prove to be a cyclical trough. None of these options are fully priced into the current equity valuation.

FY2025 financials show the scale of the cash generation engine: $109 billion in revenue, $20.6 billion in operating cash flow, $6.15 billion in free cash flow, and $9 billion distributed to shareholders through dividends and buybacks. The company generated EBITDA of $38.1 billion, supporting operating income of $27.4 billion. The balance sheet remains robust, and the dividend yield — trailing at approximately 8 percent — provides a floor under the stock even in bearish scenarios.

Equinor has also been actively reshaping its portfolio through disciplined divestitures. In addition to the Peregrino sale, the company exited Azerbaijan for $745 million and Nigeria for up to $1.2 billion. In the UK, Equinor combined its offshore oil and gas operations with Shell to form "Adura" in December 2025, a joint venture that pools assets for more efficient management. These moves signal a strategic focus on the Norwegian Continental Shelf and select high-conviction international positions — a narrowing of scope that contrasts with the expansionary ambition that led to the US shale losses.

For tracking Equinor's ongoing performance, two KPIs matter above all others.

The first is ROACE — return on average capital employed — currently 14.5 percent against a target of greater than 15 percent. This single metric captures whether Equinor is deploying its enormous capital base effectively across both hydrocarbons and renewables. A sustained decline below 12 percent would signal that the renewable buildout is diluting returns without compensating growth. A sustained reading above 15 percent would confirm that the "pragmatic dualism" strategy is working.

The second is upstream CO2 intensity — currently 6.3 kilograms per barrel of oil equivalent, targeting 6 kilograms by 2030. In a world of rising carbon costs, this metric is increasingly a proxy for long-term unit economics.

A rising intensity would signal portfolio degradation — perhaps the addition of higher-emission assets or the decline of Johan Sverdrup's ultra-clean production. A falling intensity signals that the production base is becoming more efficient and more resilient to carbon pricing — the kind of structural advantage that compounds over decades. Equinor has already achieved a 34 percent reduction from its 2015 baseline, with a target of 50 percent net reduction in Scope 1 and 2 emissions by 2030, of which 90 percent is to come through absolute reductions rather than offsets.

XII. Epilogue: The Future of the Sovereign Energy Company

The journey from Ekofisk to Sverdrup spans five decades, two name changes, one transformative merger, one spectacular international failure, one miraculous discovery, and an ongoing, unresolved bet on the future of energy.

Norway's petroleum story began with a geological accident — oil happened to be beneath Norwegian waters — and was shaped by a political choice to manage that accident with extraordinary discipline. The Ten Oil Commandments, the creation of Statoil, the sovereign wealth fund established in 1990, and the 67 percent state ownership maintained to this day — these are not the policies of a country that got lucky. They are the policies of a country that decided, with deliberate intent, to convert a finite natural resource into permanent national wealth.

Consider the counterfactual. If Norway had followed the path of most petrostates — spending the windfall, failing to build domestic competence, allowing international majors to capture the lion's share of the value chain — there would be no sovereign wealth fund, no Equinor, no floating wind industry, and no Northern Lights. There would be a smaller, poorer Norway with depleted oil fields and nothing to show for them. The distance between that counterfactual and the reality is the measure of how much the Ten Commandments accomplished.

Equinor is the instrument of that conversion. It is simultaneously an oil company, a gas company, a wind company, a carbon storage company, a commodity trader, and an arm of Norwegian foreign policy.

It employs engineers who drill wells three kilometers beneath the seabed and technicians who maintain wind turbines a hundred meters above the ocean surface. It operates trading desks in Stavanger that price natural gas for German industry and project management offices in New York that navigate US federal permitting. It publishes an annual Energy Perspectives report that models global energy scenarios through 2050 with an intellectual honesty that most oil companies would find uncomfortable.

The contradictions are real. A company producing 2.1 million barrels of oil equivalent per day cannot credibly claim to be a "pure" energy transition play. A company that built the world's first commercial floating wind farm and the world's first commercial carbon storage facility cannot credibly be dismissed as a fossil fuel company engaged in greenwashing.

Equinor exists in the uncomfortable space between those narratives — the space where the actual energy transition is happening, messily, expensively, and with no guarantee of success. Anders Opedal's "pragmatic dualism" is not a marketing slogan. It is a description of reality: the world needs both more hydrocarbons and more renewables, simultaneously, for at least the next two decades. The question is whether a single company can deliver both without being torn apart by the contradictions — and whether its shareholders will be patient enough to find out.

The $2.2 trillion sovereign wealth fund provides one kind of validation. That fund exists because Norway extracted petroleum, taxed it heavily, invested the proceeds globally, and resisted the temptation to spend the windfall on current consumption. It is the world's most successful conversion of natural resource wealth into permanent financial capital.

Whether Equinor can execute a second conversion — from petroleum producer to integrated energy company — is the question that will define the next two decades.

The financial resources are enormous: $109 billion in revenue, $20.6 billion in operating cash flow, and the backing of a sovereign owner with a multi-generational time horizon. The engineering capabilities are proven: from the harshest conditions of the North Sea to the deepest waters of Brazil's pre-salt, Equinor has demonstrated repeatedly that it can execute technically complex projects at scale. The strategic position is unique: the largest non-Russian gas supplier to Europe, the lowest-carbon oil producer among the majors, the operator of the world's largest offshore wind farm, and the builder of the world's first commercial carbon storage facility.

The only oil major that actually acts like an energy company is also the only one whose success or failure will be measured not in quarterly earnings but in generational outcomes.

XIII. Further Reading

The "Ten Oil Commandments," formally rooted in Stortingsmelding nr. 76 (1970-1971), is the foundational document of Norwegian petroleum governance. The ten principles established in this parliamentary report remain the philosophical architecture supporting Equinor's unique position as a state-controlled commercial enterprise operating in global commodity markets.

The PricewaterhouseCoopers investigation report on Equinor's US onshore operations, published in October 2020, provides the definitive post-mortem on the US shale debacle. The report's finding that internal auditors flagged problems for six years before management acted is essential reading for anyone interested in institutional governance failures at state-owned enterprises.

Equinor's annual Energy Perspectives report offers the company's internal view of global energy supply and demand scenarios through 2050. The document is notable for its intellectual honesty — presenting scenarios in which oil demand declines significantly alongside scenarios in which it remains robust — and provides the analytical foundation for the "pragmatic dualism" strategy that defines the Opedal era.

The Johan Sverdrup field development plan, available through the Norwegian Petroleum Directorate, documents the technical and economic parameters of the discovery that transformed Equinor's strategic options. The break-even economics, carbon intensity figures, and recovery rate targets provide the factual basis for understanding why this single field has been so consequential for the company and for Norway.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube