Eurocell: The Circular King of the British Building Site

I. Introduction: The "Unsexy" Compounder (0:00 – 10:00)

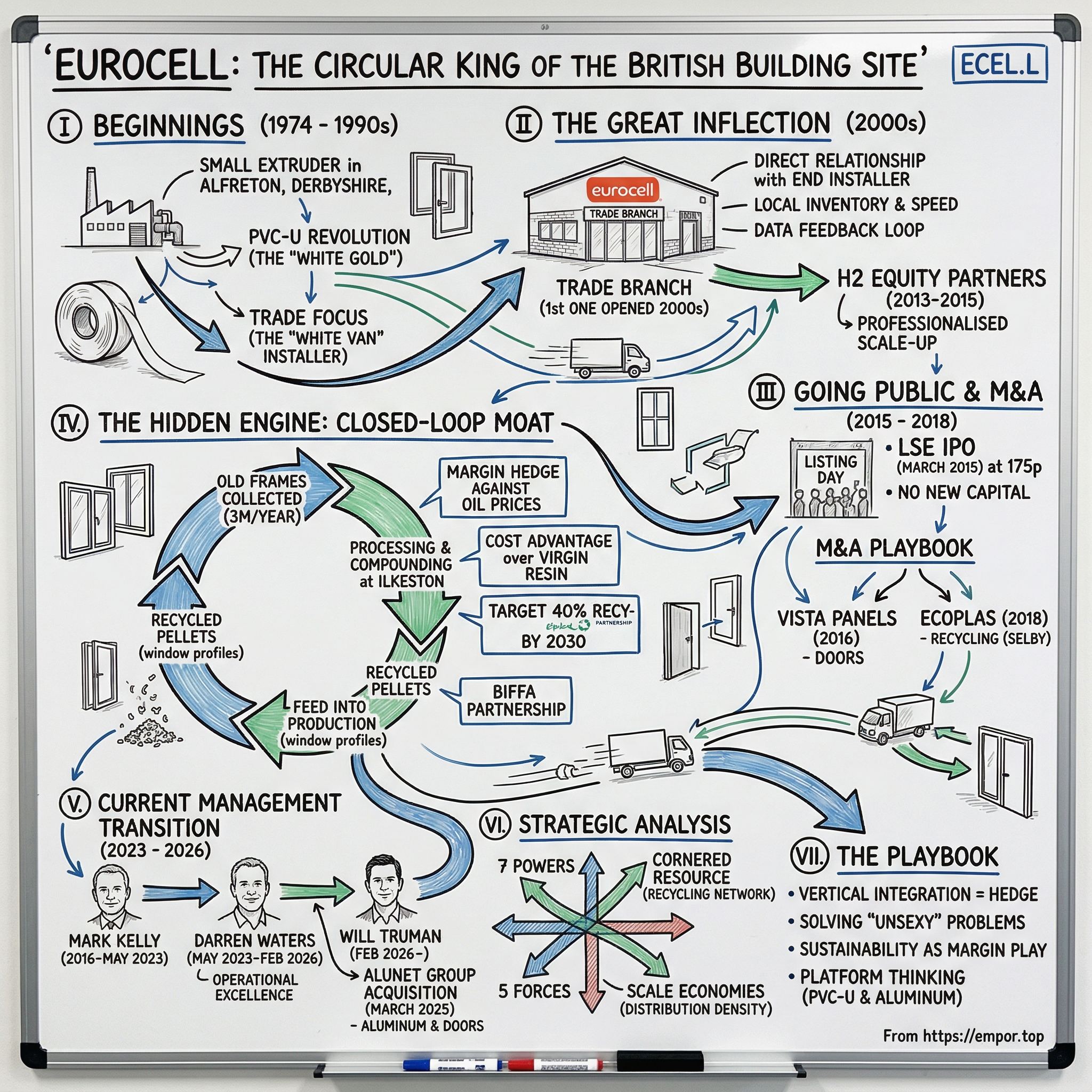

There is a factory in Alfreton, Derbyshire—a town of about eleven thousand people wedged between Nottingham and Sheffield—where machines run twenty-four hours a day, seven days a week, turning white powder into long ribbons of hollow plastic profile. The product these machines spit out will eventually become a window frame, a length of guttering, or a fascia board screwed beneath someone's roof line. It is, by most measures, one of the least glamorous manufacturing operations in Britain. And yet, if you wanted to find one of the most elegant vertical integration stories on the London Stock Exchange, this is exactly where you would start.

Eurocell plc makes PVC-U building products. Windows, doors, rainwater goods, roofline, conservatories—the unglamorous essentials that keep British homes weathertight. Say "PVC window" at a dinner party and watch the room's eyes glaze faster than a double-glazed unit. But here is the thing investors keep missing: Eurocell is not really a manufacturing company. It is a logistics business, a recycling business, and a retail franchise wrapped inside an industrial shell. The manufacturing is almost incidental—it is the scaffolding that holds a much more interesting structure together.

Consider the full picture. Eurocell extrudes its own profiles. It fabricates its own doors. It recycles old PVC-U window frames at industrial scale—processing roughly thirty-six thousand tonnes of post-consumer waste a year—and feeds that recycled material straight back into its production lines, replacing expensive virgin resin derived from oil. Then it sells the finished product through its own network of more than two hundred trade branches, bypassing the builders' merchants entirely and going direct to the "white van" installer who actually fits windows for a living. From rubbish bin to factory floor to shop counter, Eurocell controls the entire chain. No one else in the UK PVC-U market does this.

The company listed on the London Stock Exchange in March 2015 at 175 pence per share, giving it a market capitalisation of roughly £175 million. As of April 2026, the shares trade around 112 pence—below the IPO price—despite the fact that the business has doubled its branch count, built the UK's largest PVC-U recycling operation, and posted revenue north of £400 million. At an enterprise value of around £229 million, the market values Eurocell at barely 4.4 times adjusted EBITDA. Either the market is right that this is a business in structural decline, or it is spectacularly wrong about a compounder hiding in plain sight.

This is the story of how a small Derbyshire extruder built an "Apple Store" for guttering, turned rubbish into a competitive moat, and found itself navigating CEO upheaval and a sluggish housing market at the very moment that new government regulations could force millions of British homeowners to replace their windows. It is a story about the power of the unsexy.

II. Origins & The PVC Revolution (10:00 – 25:00)

To understand Eurocell, you have to understand the material that made it. PVC-U—unplasticised polyvinyl chloride—arrived in the United Kingdom as a German import. Companies like VEKA and Rehau had been manufacturing window profiles on the continent since the 1960s, and when British builders first encountered the stuff, the pitch was irresistible: a window frame that never needed painting, never rotted, and lasted decades. Compared to the softwood timber frames that had defined British housing for centuries, PVC-U was a revelation.

The adoption curve was staggering. In the early 1970s, double glazing penetration in UK homes sat at roughly sixteen percent. By the end of the 1990s, it had surged past sixty percent. The industry called it "White Gold," and with good reason—a window that cost thirty pounds to manufacture could retail for three hundred. Margins were extraordinary, and the market attracted every kind of operator, from legitimate manufacturers to door-to-door salesmen whose aggressive tactics became a national punchline.

It was in this environment that Eurocell was founded in 1974, a small plastics extrusion business set up in Alfreton to make PVC-U components. The early years were modest. Eurocell was one of dozens of small extruders feeding the double-glazing boom, turning out lengths of profile that window fabricators would cut, weld, and glaze into finished units. There was nothing particularly distinctive about the operation—it was a component supplier in a commodity market.

The first meaningful strategic pivot came when Eurocell's management recognised the difference between selling components and selling systems. A component supplier ships raw profile to anyone who will buy it. A system supplier designs the entire profile system—the geometry of the chambers, the gasket channels, the reinforcement slots—and licenses fabricators to build windows using that proprietary design. Think of it the way Intel works: the end customer never sees the chip inside, but the computer manufacturer has to build the entire machine around Intel's architecture. Owning the system design meant fabricators had to buy Eurocell's ancillary products—gaskets, beading, trims—to complete the window. Lock-in, not through contracts, but through engineering.

The second critical insight was about customer selection. The double-glazing industry in the 1980s and 1990s was split between two channels. The "Retail" channel meant selling directly to homeowners, often through door-to-door sales forces notorious for high-pressure tactics and bad debt. The "Trade" channel meant selling to independent installers—small businesses with a van, a couple of employees, and a steady stream of jobs from word-of-mouth referrals. The retail channel offered higher margins per unit but came with enormous sales costs, reputational risk, and boom-bust volatility. The trade channel was less flashy but far more resilient, because home maintenance never stops—gutters leak, fascia boards crack, windows fog up, regardless of what the economy is doing. Eurocell chose the trade channel, and that choice would prove foundational.

A management buyout in 1988 gave the company independent momentum. By 1991, Eurocell had launched its first branded building products range, moving beyond pure window profile into roofline, rainwater goods, and cladding—the full suite of plastic products that wrap the outside of a British home. In 1998, Tessenderlo Holdings, a Belgian chemicals group, acquired a seventy-five percent stake, bringing industrial-scale capital and operational discipline. By 2003, Tessenderlo owned the business outright. But Eurocell's most important idea was still germinating—and it had nothing to do with manufacturing.

III. The Great Inflection: The "Apple Store" of Guttering (25:00 – 45:00)

Picture a typical British building site in the early 2000s. A small installer—call him Dave—needs a length of white fascia board, a bag of fixing clips, and maybe a replacement section of guttering. His options are limited. He can drive to Travis Perkins or Jewson, the big builders' merchants, where building plastics occupy a neglected aisle between the timber racks and the plumbing supplies. The staff rarely know the difference between a round-line and a square-line downpipe. Or Dave can phone a distributor, place a minimum order, and wait for delivery. Neither option is fast, convenient, or particularly helpful.

Eurocell's management looked at this situation and asked a deceptively simple question: what if we opened our own shops? Not glossy consumer showrooms, but no-nonsense industrial units on trading estates, stocked exclusively with building plastics, staffed by people who actually understood the product, and open at seven in the morning when Dave starts his day. The concept was the Eurocell Trade Branch—a dedicated specialist outlet that sold nothing but building plastics and related accessories, direct to the trade installer.

The first branches opened in the early 2000s, and the impact was immediate. Suddenly, Eurocell had something none of its competitors possessed: a direct relationship with the end installer. When Dave walked into a branch every week to buy fascia board, the branch manager learned what Dave needed, what colours were selling, which new products Dave's customers were asking about, and which competitor products were causing problems. This intelligence flowed upstream into product development and inventory management in a way that was impossible for a manufacturer selling through third-party merchants. It was a feedback loop that compounded over time—the more branches Eurocell opened, the more data it gathered, and the more precisely it could tailor its product range and service levels.

The model also solved a distribution problem that most investors overlook. PVC-U profiles are long, bulky, and expensive to ship. A five-metre length of fascia board is awkward to handle and costly to deliver in small quantities. By positioning branches close to where installers work, Eurocell could hold inventory locally and offer rapid availability—often same-day collection. For a builder working on a two-day job, the difference between getting a part this morning and getting it on Thursday is the difference between staying on schedule and losing money. Speed became a competitive weapon.

By the time H2 Equity Partners entered the picture in September 2013, Eurocell had grown to roughly £150 million in sales with over nine hundred employees and a branch network that was still in its early rollout phase. H2 was a Netherlands-based mid-market private equity firm that saw exactly what the branch network could become. They acquired Eurocell from Tessenderlo and immediately went to work with management, identifying eight key strategic initiatives aimed at doubling EBITDA. The target was ambitious. Within eighteen months, it was achieved.

The private equity era did what good PE does: it professionalised the scale-up. Systems were standardised. Branch openings were accelerated. The back office was streamlined. And critically, H2 injected the discipline of measuring branch-level economics with granular precision—tracking each location's sales ramp, contribution margin, and return on invested capital. This data-driven approach to unit economics would form the cornerstone of the story Eurocell told when it was time to face the public markets.

IV. The 2015 IPO & The M&A Playbook (45:00 – 1:05:00)

On 4 March 2015, Eurocell plc debuted on the main market of the London Stock Exchange at 175 pence per share. The listing was structured as a sell-down rather than a capital raise—H2 and selling management shareholders offloaded approximately 52.4 million existing shares for total proceeds of around £91.7 million. No new equity was issued for the company's balance sheet. The message to the market was clear: this business generates enough cash internally to fund its own growth. The IPO merely needed to create liquidity for the private equity sponsor to exit.

At listing, Eurocell operated roughly 160 branches. The roll-out thesis pitched to institutional investors was straightforward: the UK could support at least 250 specialist building plastics outlets, possibly more. Adding fifteen to twenty branches per year would compound revenue growth reliably, because each branch served a local catchment of trade installers who, once habituated, rarely switched. Each new location cost relatively little to open—these were leased industrial units with small teams—and followed a predictable maturity curve: losses in year one, breakeven in year two, attractive returns thereafter. It was an execution play, not a speculative bet. H2 retained approximately 37 percent of shares post-listing, subject to a 180-day lock-up, before selling their final stake in March 2017. The full PE cycle—entry to exit—ran roughly three and a half years, a textbook value creation and realisation.

With the company now public, management turned to bolt-on acquisitions—small, targeted deals designed to fill specific gaps in the product offering or value chain. The philosophy was deliberately conservative: no "transformational" mergers, no leveraged mega-deals, just tuck-in margin plays that could be immediately cross-sold through the existing branch network.

The first move came in March 2016 with the acquisition of Vista Panels, a Wirral-based manufacturer of composite and PVC-U entrance doors. The price was £6.7 million for a business generating approximately £14 million in revenue with over a hundred employees. What made the deal elegant was that Vista had been Eurocell's sole supplier of entrance doors for a decade and was already a significant consumer of Eurocell profile. Bringing it in-house was pure vertical integration: Eurocell now controlled the manufacture, pricing, and distribution of composite doors through its branch network. Composite doors were one of the fastest-growing segments in the fenestration market, driven by homeowner demand for front doors that looked like timber but required no maintenance. By owning the manufacturing, Eurocell captured margin that had previously sat with a third-party supplier. Did they overpay at £6.7 million? At less than half of Vista's annual revenue and with an immediate cross-sell channel of 160-plus branches, the arithmetic looked compelling from day one. Doors became a meaningful category in the branch network, contributing to same-store revenue growth in the years that followed.

But the most consequential acquisition in Eurocell's history came two years later, in August 2018, when the company bought Ecoplas—the UK's largest independent PVC-U recycler, operating near Selby in North Yorkshire. If Vista was about vertical integration forward into product, Ecoplas was about vertical integration backward into raw material. To understand why this deal mattered so much, you need to understand the economics of PVC resin.

Virgin PVC resin is a commodity derived from oil and chlorine. Its price swings with petrochemical markets and global supply chains. For a company like Eurocell, whose single largest input cost is resin, these swings create margin volatility that is difficult to hedge and impossible to control. A spike in ethylene prices can erase an entire quarter of margin improvement overnight. Recycled PVC is fundamentally different. The feedstock—old window frames ripped out during renovations and demolitions—exists in abundance across the UK, because the millions of PVC-U windows installed in the 1990s are now reaching the end of their twenty-five to thirty-five year service life. Collecting this material, processing it, and compounding it into pellets produces a raw material that is chemically almost identical to virgin resin but sourced from a domestic waste stream rather than a global commodity market. The cost dynamics are completely different—and more importantly, they are more stable and more favourable.

By combining Ecoplas's Selby facility with its existing recycling operation at Ilkeston (developed from the 2009 acquisition of Merritt Plastics), Eurocell created the largest PVC-U recycling capability in the UK. The contrast with industry peers is instructive. Epwin Group, the closest listed competitor, operates Profile 22—one of the UK's larger PVC-U profile systems—but lacks recycling at comparable scale. German-owned competitors like VEKA and Rehau have deep resources and global reach, but neither operates a vertically integrated branch network or a meaningful closed-loop recycling operation in the UK. Eurocell was quietly assembling a value chain that no single competitor matched end to end.

V. The "Hidden" Engine: The Closed-Loop Moat (1:05:00 – 1:25:00)

Walk into Eurocell's recycling facility at Ilkeston and the first thing you notice is the scale of the operation. Mountains of old window frames—white, faded cream, the occasional woodgrain effect—are stacked in the yard, having been collected from demolition contractors, window installers, and waste management companies across the country. Inside the plant, the frames are fed into industrial shredders that reduce them to chunks. Automated sorting systems then separate the PVC from glass, metal reinforcement bars, rubber gaskets, and other contaminants. The cleaned PVC granulate is washed, dried, and fed into compounding extruders that melt it and produce uniform pellets—chemically almost indistinguishable from virgin resin—ready to be shipped to Eurocell's profile extrusion lines and turned into new window frames.

Think of it like aluminium recycling, but for plastic. Melting down old Coke cans to make new Coke cans requires far less energy than smelting bauxite ore. The same principle applies here: reprocessing old PVC-U frames requires far less energy and cost than synthesising virgin PVC from petrochemical feedstocks. The difference is that while aluminium recycling is a mature, commoditised industry, PVC-U recycling at this scale in the UK is dominated by one player.

The trajectory of Eurocell's recycling operation tells the story of a side project that became a strategic engine. When the company first began recycling around 2009, recycled content represented a modest fraction of total resin consumption. By 2018, the year of the Ecoplas acquisition, the figure had reached approximately seventeen percent. By 2021, it was twenty-seven percent. By 2023, recycled content in rigid profiles hit thirty-two percent, with the plants processing eighteen thousand tonnes of recycled material into profiles and a further seventy-three hundred tonnes into other products or sold externally. In 2025, the combined operation processed thirty-six thousand tonnes of post-consumer waste, with recycled content at thirty percent of total resin input—the slight dip from thirty-two percent reflecting the addition of the Alunet Group's aluminium products to the group's overall denominator. The target is forty percent by 2030.

To put this in tangible terms, Eurocell diverts approximately three million old frames from landfill every year. PVC-U is extraordinarily durable—it does not biodegrade—which means every frame that goes to landfill sits there essentially forever. The environmental case for recycling is obvious. But what makes this operation strategically significant rather than merely virtuous is the margin impact.

When virgin resin prices spike—as they did during the pandemic supply chain chaos—a manufacturer buying one hundred percent virgin resin absorbs that cost directly into its gross margin. Eurocell, by sourcing thirty percent of its resin from a domestic waste stream with completely different cost dynamics, has built a natural hedge. When virgin prices rise, the gap between virgin and recycled input costs widens, and Eurocell's margin advantage over competitors grows. When virgin prices fall, the advantage narrows but does not disappear, because recycled material still avoids the logistics costs associated with importing resin from global suppliers.

The closed-loop model also creates a virtuous cycle with the branch network. When Eurocell's branch customers remove old windows to install new ones, those old frames can be collected and returned into the recycling stream. The installer buys new product from a branch, removes the old product from the homeowner's house, and Eurocell collects the old product for recycling into the next generation of new product. This is a genuine circular economy operating as a business model, not a marketing slogan.

The company's partnership with Biffa, one of the UK's largest waste management firms, has expanded this collection capability further, diverting over eighty-five tonnes of domestic PVC-U from landfill with rollout to additional regions planned for 2026. And in a consolidation move announced with the 2025 results, the Selby recycling site will close by end of 2026, with all recycling concentrated at an upgraded Ilkeston facility following approximately £2.6 million in capital investment. The expected annualised savings are around £1.5 million from 2027 onward—a small number in absolute terms, but indicative of the relentless operational tightening that characterises the business.

The flagship product of this circular philosophy is the Modus profile system. Manufactured using co-extrusion technology—think of it like a two-layer sandwich, where recycled material forms the structural core and virgin material provides the smooth, colour-fast outer surface—Modus contains fifty percent post-consumer recycled content. The result delivers U-values as low as 0.7 W/m²K in triple-glazed configurations, comfortably exceeding the forthcoming Future Homes Standard. The installer cannot tell the difference between a Modus profile and one made entirely from virgin material. The homeowner cannot tell the difference. But Eurocell's margin is materially better.

The business reports in two segments that reveal this integrated structure. The Profiles division sells extruded profiles to large window fabricators—the "Intel Inside" model, where Eurocell's system design is embedded in windows carrying the fabricator's brand. In 2024, this segment generated approximately £146 million in third-party revenue at an adjusted operating margin of around thirteen percent. The Building Plastics division encompasses the trade branch network and smaller product categories, generating roughly £212 million in third-party revenue. Together, these segments create a business that participates in both the wholesale and retail ends of the market, with the recycling operation sitting behind both as a shared cost-advantage engine that competitors simply do not have.

VI. Current Management: Leadership in Transition (1:25:00 – 1:40:00)

The story of Eurocell's leadership over the past three years reads like a corporate soap opera—and the instability matters, because in a business built on operational execution, leadership continuity is not a luxury. It is a prerequisite.

Mark Kelly served as CEO from 2016 through May 2023, guiding the company through the pandemic, the branch expansion past two hundred locations, and the critical Ecoplas acquisition. Kelly was a steady-hand operator who built credibility with the market through consistent delivery against targets. When he announced his retirement in early 2023, the succession appeared orderly.

Darren Waters was appointed CEO Designate in April 2023 and formally took the role on 11 May 2023. On paper, he was an ideal fit. Waters had spent more than twenty years in building products. He served as CEO of Tyman's UK and Ireland division for nine years, overseeing a programme of acquisitions, divestments, and manufacturing consolidation into the company's Wolverhampton facility. Before joining Eurocell, he had been Chief Operating Officer and Managing Director of the Concrete and Kevington division at Ibstock plc—one of the UK's largest brick manufacturers. He knew building products intimately. He knew the UK construction supply chain. He knew how to run factories and squeeze efficiency from industrial operations.

Waters immediately signalled a shift in emphasis. Where Kelly had focused on aggressive branch expansion—adding fifteen to twenty locations per year—Waters pivoted toward what he called "Operational Excellence." The strategic review he led in 2023 produced a five-year plan targeting £500 million in revenue and £50 million in operating profit by December 2028, implying a target operating margin of ten percent compared to the roughly six percent the business was delivering at the time. The plan emphasised margin improvement through cost reduction, recycling expansion, and more disciplined capital allocation rather than raw branch count growth. A £4 million cost savings programme was identified and delivered from the first half of 2025, split evenly between branch restructuring and operational efficiencies.

Waters also oversaw the largest acquisition in company history. In March 2025, Eurocell completed the purchase of the Alunet Group for £29 million upfront, with up to £6 million in contingent consideration tied to performance. The deal brought in four Dewsbury-based businesses spanning residential aluminium windows and doors (under the "Aluna" brand), premium solid-core timber composite doors, and two aluminium garage door operations. This was not just a product line extension—it was a strategic hedge against the single biggest substitution threat facing PVC-U. By offering both materials through the same distribution infrastructure, Eurocell was neutralising the risk that aluminium's growing appeal among architects and homeowners could erode its core market. In its first ten months under Eurocell ownership, Alunet delivered £46.7 million in sales and £4.8 million in adjusted operating profit, comfortably ahead of the acquisition plan.

Then came the shock. On 9 February 2026, Eurocell announced that Darren Waters had stepped down as CEO "by mutual agreement" with immediate effect. No detailed explanation was provided. The shares fell approximately seven percent on the news. The speed and opacity of the departure—less than three years into a five-year strategic plan—raised immediate questions about what had gone wrong behind closed doors.

The board moved quickly, appointing Will Truman as CEO on the same day. Truman had been a non-executive director who had been named CFO Designate just three months earlier, in November 2025, to succeed the retiring Michael Scott. His elevation to the top job instead was a battlefield promotion. Scott, the incumbent CFO, agreed to postpone his retirement and continue in role while a permanent finance director is recruited.

The board's incentive structures remain anchored on Return on Capital Employed and Earnings Per Share growth—designed to reward efficient capital deployment rather than top-line empire building. In terms of shareholder returns, the company has been active: a £15 million buyback was completed in 2024, repurchasing 10.7 million shares, followed by a further £5 million buyback in 2025. Total capital returned to shareholders in 2025 reached £11.4 million—buybacks plus a dividend that has grown steadily from 5.5 pence in 2023 to a proposed 6.4 pence for 2025. At the current share price, that dividend yields roughly 5.7 percent. Chairman Derek Mapp presides over a board that has demonstrated willingness to make decisive moves, for better or worse. Whether the decisive move of replacing the CEO mid-strategy proves to be the right one remains to be seen.

VII. Strategic Analysis: 7 Powers & 5 Forces (1:40:00 – 2:00:00)

Strip away the corporate narrative and ask the fundamental question: does Eurocell have a durable competitive advantage, or is it just a well-run commodity manufacturer? Hamilton Helmer's Seven Powers framework provides a useful lens.

The strongest power Eurocell possesses is a Cornered Resource in the form of its recycling feedstock network. The old-frame collection infrastructure—relationships with thousands of demolition contractors, waste handlers, and installers across the UK—took nearly two decades to build. It is not protected by patents or regulations, but it is protected by something equally effective: the sheer difficulty of replication. A new entrant would need to simultaneously build collection logistics, processing capacity, and downstream manufacturing to make the economics work. Eurocell processes thirty-six thousand tonnes annually from a supply base that grows every year as more 1990s-era windows reach end of life. The resource is renewable, domestic, and increasingly abundant—a rare combination.

The second significant power is Scale Economies, specifically in distribution density. With 215 branches covering England and Wales, Eurocell has achieved a geographic density that creates meaningful logistics advantages. Products flow from central manufacturing to regional hubs to local branches at lower per-unit cost than a competitor operating twenty or fifty locations. More importantly, for most trade installers, there is a Eurocell outlet within a reasonable drive. A new entrant opening its first ten branches would face higher per-branch logistics costs and would struggle to match the geographic convenience that keeps installers loyal. This is the same density-based scale economy that makes route-based businesses like Cintas or Waste Management so difficult to dislodge—except here the "route" runs through every trading estate in England.

There is also a meaningful element of Switching Costs, though it operates at the fabricator level rather than the branch level. Window fabricators who adopt the Eurocell profile system invest in tooling, training, and workflow optimisation specific to that system's geometry. Switching to a competitor's profile means re-tooling, re-training, and re-certifying—a costly and disruptive process that fabricators undertake only reluctantly. Not an impregnable barrier, but meaningful inertia that slows customer defection.

The powers that Eurocell arguably lacks are instructive too. There is no obvious Network Effect—one installer using Eurocell does not make the product more valuable to another. Counter-Positioning is limited; competitors could theoretically replicate the branch model, though none has done so at comparable scale after two decades. Branding power is modest in consumer terms; Eurocell is respected in the trade but not a household name, so premium pricing power is constrained.

Turning to Porter's Five Forces, the picture is nuanced. Bargaining Power of Buyers varies dramatically by customer type. Large housebuilders purchasing at volume have significant leverage—they can and do negotiate aggressively. But the branch network's genius is that it primarily serves thousands of fragmented small installers, none of whom individually accounts for a material share of revenue. Dave the builder buying fascia board has essentially zero bargaining power. He cares about availability and convenience, not extracting the last penny of discount. This fragmented customer base is inherently less powerful than a concentrated one.

Bargaining Power of Suppliers is mitigated by the recycling operation. By sourcing thirty percent of resin internally from recycled material, Eurocell has reduced its dependence on virgin resin suppliers and the petrochemical markets they track.

Threat of Substitutes is the most interesting force at work. Aluminium is the premium alternative—it offers slimmer sightlines, a contemporary aesthetic, and a perception of quality that PVC-U struggles to match at the high end. The Modus system was Eurocell's product-level response, delivering flush aesthetics that mimic the aluminium look while retaining PVC-U's cost advantage. But the Alunet acquisition was the more definitive strategic answer: if you cannot beat the substitute, sell it alongside your core product. Timber is a less relevant threat—its share of the UK window market has been declining for decades and shows no signs of reversal.

Competitive Rivalry is intense but fragmented. VEKA, Rehau, Deceuninck, Liniar, and Epwin all compete for fabricator business. But rivalry is moderated by the fact that Eurocell competes on a different dimension than most peers. While competitors fight primarily on profile specifications and price to fabricators, Eurocell also competes on distribution convenience and cost advantage through recycling. The competitive battle is not fought on a single playing field.

Threat of New Entrants is low. The capital requirements for extrusion equipment, the time needed to build a branch network, and the difficulty of establishing recycling infrastructure create substantial barriers. The UK PVC-U market is mature and consolidating, not growing—which further deters new investment. Eurocell holds approximately twenty percent of the UK rigid PVC profile market and roughly twenty-five percent of the roofline market. These are not dominant positions, but in a fragmented industry they represent meaningful scale.

VIII. The Playbook: Lessons for Investors & Operators (2:00:00 – 2:20:00)

If there is a single lesson that Eurocell's story teaches, it is that vertical integration is not just a strategy—it is a hedge. A "pure" manufacturer is at the mercy of its distribution partners, who control pricing and customer relationships. A "pure" retailer is at the mercy of its suppliers, who control product availability and input costs. By owning the factory, the recycling plant, and the shop, Eurocell can manage inventory, pricing, and margins across the entire value chain rather than being squeezed at a single choke point. When construction demand softens—as it did through 2023 and 2024, with organic volumes falling—the company can absorb the blow across multiple points in the chain. The branches can promote higher-margin products. The recycling operation can offset rising resin costs. The profiles division can adjust production schedules without waiting for a distributor to relay demand signals. Resilience, in this model, is structural rather than accidental.

Consider the counterfactual. If Eurocell were just a profile extruder selling through Travis Perkins and Jewson, it would have no control over how its products are merchandised, no direct relationship with the end installer, and no pricing flexibility at the point of sale. If it were just a trade retailer buying profiles from third-party manufacturers, it would have no control over input costs, no recycling margin advantage, and no proprietary product differentiation. The integration of manufacturing, recycling, and distribution creates a business that is more than the sum of its parts—and more defensible than any individual piece.

The second lesson is about the power of solving unglamorous problems. "Where does a builder buy a piece of trim at seven in the morning?" is not a question that excites venture capitalists or technology analysts. But it is a question that generates hundreds of millions of pounds in annual revenue for the company that answers it best. Eurocell's branch network succeeds because it solved a mundane logistics problem—getting the right building plastic to the right tradesperson at the right time—better than the generalist builders' merchants could. The builders' merchants carry fifty thousand product lines across a hundred categories. Eurocell carries one category and knows it exhaustively. In a world obsessed with platform businesses and digital disruption, there is something refreshingly durable about a company that wins by being the most convenient place to buy a downpipe.

The third lesson concerns sustainability as a margin play. The corporate world is full of ESG initiatives that cost money without generating returns—tree planting programmes, carbon offset purchases, glossy reports that no one reads. Eurocell's recycling operation is the opposite. It generates a direct, measurable cost advantage by replacing expensive virgin resin with cheaper recycled material. It reduces exposure to commodity price volatility. It creates a marketing advantage with environmentally conscious specifiers. And it positions the company favourably for tightening environmental regulations. If an ESG initiative does not improve the economics of the business, something is probably wrong with the initiative. Eurocell's closed-loop model demonstrates that genuine circularity and genuine profitability are not just compatible—they reinforce each other.

A related insight concerns what the Alunet acquisition reveals about strategic thinking. The conventional narrative has always framed Eurocell as a "PVC-U company." By acquiring an aluminium and composite door manufacturer, management signalled that Eurocell is a fenestration distribution and manufacturing platform, not a single-material business. The branches do not care whether they sell PVC-U windows or aluminium doors—the logistics are the same, the customer relationships are the same, and the cross-sell opportunity is identical. Platform thinking is what separates Eurocell from competitors who remain defined by a single material or a single position in the value chain.

For investors tracking Eurocell's ongoing performance, the key KPIs to watch are not headline revenue or earnings, which are heavily influenced by cyclical construction demand and acquisition effects. Two metrics cut closest to the structural health of the business. First, like-for-like branch revenue growth—the organic demand trend at existing locations, stripped of new openings and acquisitions. This is the purest signal of whether the branch model is gaining or losing wallet share with its core installer customer base. Second, recycled content as a percentage of total resin input—currently thirty percent, targeting forty percent by 2030. Every percentage point of progress translates directly into margin resilience and widening competitive advantage. A third metric worth monitoring is ROCE, which the board uses as a key performance target in its long-term incentive plans. At 11.2 percent for 2025, it remains well below the 17.2 percent achieved in 2021. The trajectory will reveal whether the current strategy is genuinely improving capital efficiency or merely growing the top line.

IX. The Bull vs. Bear Case & Epilogue (2:20:00 – 2:40:00)

The bear case for Eurocell starts with the cycle. The UK housing market has been sluggish for the better part of two years. High mortgage rates have suppressed housing transactions, and when people do not move, they are less likely to undertake major home improvements like window replacements. Private housing RMI output fell roughly four percent in 2024, and while forecasts suggest modest recovery in 2025 and 2026, these are tepid numbers for a business whose branch network depends on steady renovation activity. Organic volumes fell two percent in 2025, with general RMI sales through the branches declining six percent. The UK construction labour market faces its own challenges—the industry estimates it needs nearly three hundred thousand additional workers over the next five years. If the installers are not there to fit the windows, the quality of Eurocell's products becomes irrelevant.

Leadership instability compounds the concern. Three CEOs in three years—Kelly, Waters, Truman—is not the kind of continuity that inspires confidence in execution. Waters's abrupt departure in February 2026, with no public explanation, raises unanswered questions. Truman is an unproven CEO who was originally recruited for the CFO role. He may prove excellent, but investors are betting on potential rather than track record. The five-year strategy—£500 million revenue, £50 million operating profit, ten percent margins by 2028—was Waters's plan, and its credibility is inevitably diminished by his departure. The non-underlying charges associated with the ongoing IT systems replacement—approximately £13 million over 2024 to 2027—add execution risk during a period when management bandwidth is already stretched by the CEO transition and Alunet integration.

There are also structural questions about the PVC-U market itself. Aluminium's share of the UK fenestration market has been growing, driven by architectural trends favouring slim frames and contemporary aesthetics. The Alunet acquisition addresses this, but integration risk is real—combining four acquired businesses with different cultures, systems, and customer bases into Eurocell's operations is a multi-year project. And while thirty-nine percent of UK homes were built before 1944, meaning massive renovation demand exists in theory, translating that theoretical demand into actual spending requires consumer confidence and disposable income—both of which remain constrained.

The bull case, however, is anchored by something more concrete than hope.

The Future Homes and Buildings Standard was published on 24 March 2026, with new Part L 2026 regulations going live on 24 March 2027 after a twelve-month transition period. These regulations mandate seventy-five to eighty percent lower carbon emissions for new homes compared to 2013 standards—the most significant uplift to building energy requirements in over a decade. While the standard is technology-neutral, the tightening U-value requirements make high-performance glazing effectively essential for compliance. Eurocell's Modus system comfortably exceeds the new requirements. This is not a speculative tailwind—it is published regulation with a defined implementation date. Every new home built after March 2027 will need windows that meet these standards, and a significant portion of the existing housing stock will face increasing pressure to upgrade as energy efficiency requirements tighten across the broader regulatory environment.

Beyond regulation, there is the replacement cycle. The millions of PVC-U windows installed during the 1990s boom are now twenty-five to thirty-five years old and approaching end of life. This creates a dual demand surge: homeowners need new, higher-specification windows, and the old frames entering the waste stream feed directly into Eurocell's recycling operation. The company benefits from both sides of this cycle—selling the new product and recycling the old one. No competitor in the UK market is positioned to capture both sides of this equation.

The valuation provides a significant margin of safety for those who believe the cycle will turn. At 112 pence, the shares trade at roughly 4.4 times adjusted EBITDA and 0.3 times revenue. The dividend yield sits at approximately 5.7 percent and has been growing. Management has been actively buying back shares—returning a combined £11.4 million to shareholders in 2025 and £21.2 million in 2024, equivalent to roughly fourteen percent of the market capitalisation in a single year. Net debt of £22.1 million represents just 0.7 times EBITDA—conservative leverage by any standard—and free cash flow of £34.2 million in 2025 comfortably covers the dividend, funds branch openings, and leaves room for further bolt-on acquisitions. If management delivers even a portion of the five-year plan, the earnings power of the business could look dramatically different from current levels.

The recycling moat continues to widen. The consolidation at Ilkeston will improve efficiency. The Biffa partnership is expanding the collection network. Every incremental percentage point of recycled content widens the cost gap with competitors relying on one hundred percent virgin resin. And the Alunet acquisition has transformed Eurocell from a PVC-U pure-play into a multi-material fenestration platform—reducing single-material risk while leveraging the same distribution infrastructure.

Is Eurocell the "last man standing" in UK PVC-U manufacturing? That framing is probably too dramatic. VEKA and Rehau are not going anywhere—they have global scale and deep resources. But Eurocell may be the only company in the sector that has assembled all the pieces—manufacturing, recycling, distribution, and now multi-material capability—into a single integrated platform, listed on a public market at a valuation that implies the market sees none of it. The building site does not care about share prices. Dave the builder will show up at seven tomorrow morning needing a length of fascia board, and Eurocell will be there to sell it to him. Whether the stock market eventually notices is a different question entirely.

X. Top Links & References (Post-show)

- Eurocell Annual Reports (2015–2025), available at investors.eurocell.co.uk

- Eurocell FY2025 Preliminary Results, Investegate, 19 March 2026

- H2 Equity Partners case study: Eurocell (h2ep.co.uk)

- Future Homes and Buildings Standard, published 24 March 2026 (UK Government)

- Eurocell recycling and closed-loop sustainability information (eurocell.co.uk)

- Eurocell CEO departure announcement, 9 February 2026 (Sharecast, The Business Desk)

- Eurocell Alunet Group acquisition announcement, March 2025 (Investegate)

- SureSpec specification tool launch (Fenestration News, 2025)

- Eurocell and Biffa recycling partnership expansion (Fenestration News, 2026)

- Construction Products Association forecasts, Summer 2025

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube