Diploma PLC: The Value-Add Compounder

I. Introduction: The Best Company You've Never Heard Of

Somewhere in an industrial park outside Chicago, a technician is pulling low-voltage cable through the ceiling of a half-finished data center. The cable arrives not on a standard spool but inside a patented carton system that eliminates the need for a second pair of hands. Across the Atlantic, in a muddy quarry in Queensland, a mechanic is tearing apart a hydraulic arm on a two-hundred-ton excavator. The replacement seal kit arrived overnight, custom-assembled, with installation instructions specific to the serial number of that machine. And in a hospital lab in Oxford, a pathologist is loading reagents into a diagnostic analyzer, never once wondering who supplies the consumables that keep the machine humming—or how profitable that supply chain really is.

None of these people have heard of Diploma PLC. Almost no one in the general investing public has. And that is precisely the point.

Over the last two decades, this London-headquartered group of businesses has delivered a total shareholder return that dwarfs most of the technology darlings that dominate financial headlines. From a sleepy mid-cap trading around 80 pence per share in the early 2000s, Diploma entered the FTSE 100 index and, as of early 2026, commands a market capitalization approaching eight billion pounds. The stock has compounded at roughly 20 percent annually for two decades—a performance record that would make it the envy of any Silicon Valley growth fund, achieved by selling seals, wires, and lab pipettes.

The thesis on Diploma is deceptively simple. This is not a distributor, at least not in the way that word is typically understood. Diploma is a value-add specialist. Every business it owns sits at the intersection of three powerful characteristics: the product is mission-critical to the customer, the cost of the product is trivially small relative to the cost of downtime, and the technical knowledge required to spec, source, and deliver the product creates a moat that Amazon, or any generalist wholesaler, cannot cross. Diploma calls this the "Value-Add" model. Investors who have studied the company closely call it something else: a legal license to print money.

The story of how Diploma arrived here—from a 1930s hardware concern to a decentralized compounding machine generating 22 percent operating margins and 25-plus percent returns on invested capital—is a masterclass in strategic patience, disciplined capital allocation, and the power of buying boring businesses brilliantly. It is a story that begins, improbably, with tea.

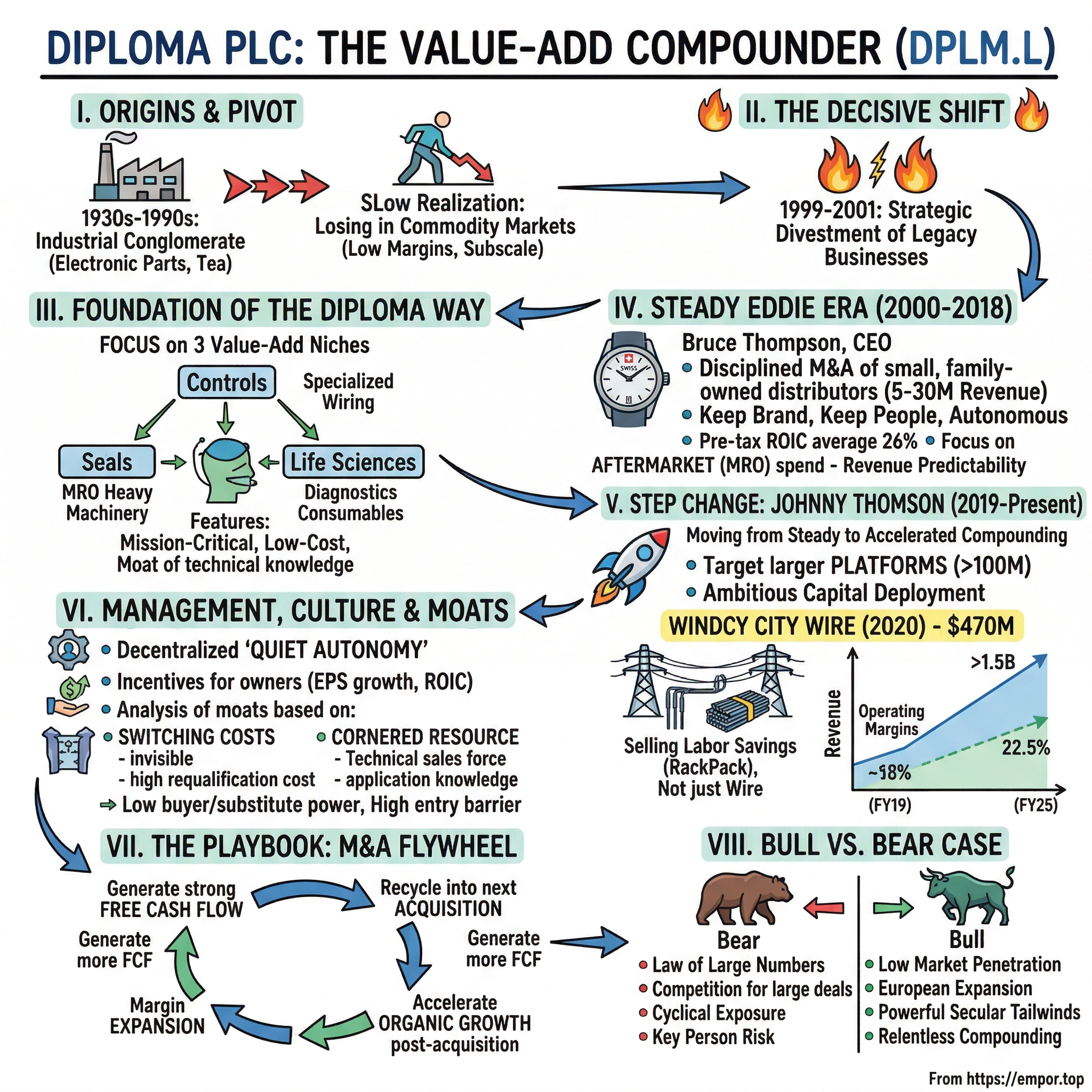

II. The Origins and the Pivot

In 1931, a small group of British industrial entrepreneurs incorporated a business in London. The company that would eventually become Diploma PLC spent its first several decades as a thoroughly unremarkable participant in the UK's post-war industrial economy. It was, for lack of a better term, a conglomerate—though a modest one by the standards of the era. By the time it listed on the London Stock Exchange in 1960, its portfolio included electronic component distribution, building products, and special steels. At one point, it was even involved in tea distribution. This was classic mid-century British business: a collection of loosely related activities held together more by accident of history than strategic logic.

The turning point came in the late 1980s and 1990s, and it was born not from a moment of inspiration but from a slow-dawning realization that the company was losing. Electronic component distribution was becoming a commodity business—a race to the bottom on price where scale was the only advantage, and Diploma did not have enough of it. Building products faced similar pressures. The margins were thin, the competitive dynamics were brutal, and the company was subscale in every market where it competed.

What followed was one of the most decisive strategic pivots in modern British business history, even though it happened so quietly that almost nobody noticed. Between 1999 and 2001, Diploma systematically divested every business that did not fit its emerging vision. The electronic component arm, SEI Macro, was sold in 1999. The building products division, Robert Lee, went in 2000. The special steels business, Henry Whitham, followed in 2001. In the space of three years, Diploma essentially liquidated its entire legacy portfolio. It was the corporate equivalent of burning the ships.

What remained—and what management chose to build upon—were three specific niches where Diploma had discovered something remarkable: businesses that looked like distribution from the outside but functioned like highly specialized consulting firms from the inside. These niches were Seals (aftermarket hydraulic seals for heavy machinery), Controls (specialized wiring and interconnect solutions), and Life Sciences (diagnostic and surgical consumables). In each case, the product itself was inexpensive—often just tens or hundreds of pounds—but the consequences of getting it wrong, or getting it late, were catastrophic. A wrong seal could shut down a mining operation. A wrong cable specification could compromise the fire safety of an entire building. A wrong reagent could invalidate an entire batch of diagnostic tests.

This insight—that value-add distribution in mission-critical, low-cost categories creates extraordinary pricing power and customer stickiness—became the foundation of what Diploma calls "The Diploma Way." The old Diploma was a portfolio of businesses. The new Diploma was a cohesive philosophy: find the places where technical expertise, rapid delivery, and application knowledge matter more than price, and then compound returns by reinvesting every pound of free cash flow into acquiring more of these businesses.

The metric that captured this philosophy was not revenue growth—it was Return on Invested Capital. Diploma did not want to be big. It wanted to be excellent. That distinction would prove to be the single most important strategic choice in the company's history, and the foundation upon which everything that followed was built.

III. Inflection Point 1: The "Steady Eddie" Era (2000–2018)

Bruce Thompson took the helm as CEO in 1996, and for the next twenty-two years, he ran Diploma with the quiet intensity of a Swiss watchmaker. There were no dramatic press conferences, no splashy investor days, no attempts to "disrupt" anything. Thompson's genius was recognizing that the boring businesses Diploma owned could generate extraordinary returns if managed with surgical discipline—and if the company remained patient enough to let compounding do its work.

The model Thompson perfected was elegant in its simplicity. Diploma would identify small, family-owned distributors—typically generating between five and thirty million pounds in revenue—that occupied the same value-add niche the parent company prized. These were businesses started by an entrepreneur who understood a specific technical domain: hydraulic seals for Caterpillar equipment, specialty fasteners for aerospace applications, or diagnostic consumables for veterinary labs. The founders were often in their fifties or sixties, ready to monetize a lifetime of work but deeply protective of the culture they had built.

Thompson's pitch to these founders was straightforward and, by all accounts, genuinely delivered: sell to Diploma, keep your brand, keep your people, keep running the business. Diploma would provide the balance sheet for growth—better credit terms, larger inventory, capital for warehouse expansion—while the founder would continue to operate with near-total autonomy. The price was typically five to seven times EBITDA, a multiple that reflected the small size and limited liquidity of these businesses. Over approximately thirty transactions during Thompson's tenure, this formula was applied with remarkable consistency.

The result was a financial profile that made Diploma one of the most capital-efficient industrial companies in Europe. Pre-tax return on invested capital averaged 26 percent during the Thompson era—a figure that placed Diploma in the same rarefied territory as luxury goods companies and software businesses, achieved by selling rubber rings and copper wire. Operating margins settled into a band around 18 to 20 percent, well above the single-digit margins typical of traditional distribution.

Why did this work so well? The answer lies in the nature of the end demand. Thompson deliberately targeted businesses focused on maintenance, repair, and overhaul—what the industry calls "aftermarket" or "MRO" spend—rather than businesses tied to new capital projects. This distinction is critical. When a company is building a new factory or a new mine, it shops aggressively on price. Procurement departments run competitive bids, squeeze suppliers on margin, and treat distribution as a commodity. But when that same company has a two-hundred-ton excavator broken down in a quarry, losing fifty thousand pounds a day in lost production because of a fifty-pound seal, the procurement dynamics change completely. The customer does not want the cheapest seal. The customer wants the right seal, delivered overnight, with technical confirmation that it will fit the exact machine model and serial number.

This is the core insight that powered the Thompson era: mission-critical, low-cost products sold into aftermarket channels create a business with the revenue predictability of a subscription model and the pricing power of a monopoly. Thompson did not invent this insight—he inherited the DNA from Diploma's surviving businesses—but he was the first leader to recognize it as a repeatable formula and build an acquisition machine around it.

Paired with Thompson was CFO Nigel Lingwood, who joined in 2001 and remained until 2020. Together, they formed one of the longest-serving and most effective CEO-CFO partnerships in UK public company history. The duo operated with a skeleton corporate staff—Diploma's head office in Charterhouse Square, London, never employed more than a few dozen people—and maintained an almost fanatical focus on capital discipline. Dividends grew steadily, but the primary use of free cash flow was always the next acquisition. By the time Thompson retired in 2018, Diploma had transformed from a company worth a few hundred million pounds into a multi-billion-pound compounder with an unbroken track record of profitable growth.

The succession, however, did not go smoothly. The board initially hired an external candidate, but the appointment lasted only a matter of months. Whether the issue was cultural fit, strategic disagreement, or something else entirely was never fully aired in public. What mattered was what happened next: the board moved quickly to appoint Johnny Thomson, who would prove to be not just a continuation of the Thompson legacy but a dramatic acceleration of it.

IV. Inflection Point 2: The Johnny Thomson "Step Change" (2019–Present)

Johnny Thomson arrived at Diploma in February 2019 with an unusual profile for a CEO of an industrial company. He held a Master of Arts in English Literature and Political Science from Glasgow University—not exactly the typical CV for someone running a business that sells hydraulic seals and fire alarm cable. But Thomson's career had been forged in the demanding operational environment of Compass Group, the world's largest contract foodservice company, where he had served as Group Chief Finance Officer and, before that, as Managing Director of the Brazilian operation. He understood what it meant to run a decentralized, multi-site business across geographies and cultures. He understood capital allocation. And he understood that Diploma's conservative balance sheet, while admirable in its prudence, was also a form of strategic underperformance.

Thomson's diagnosis was blunt: Diploma had a world-class operating model but a mid-cap mentality. The company was acquiring businesses at a rate of two or three per year, spending twenty to thirty million pounds annually on deals. The pipeline of potential acquisitions was enormous—the fragmented market of specialty distributors across North America and Europe contained literally thousands of targets. But Diploma was moving too slowly, constrained by a self-imposed conservatism that treated any deal above fifty million pounds as recklessly large.

Thomson's strategic shift was not to change the model but to change the scale at which it operated. He called it moving from "steady" to "accelerated" compounding. The operating principles remained the same: value-add positioning, decentralized autonomy, mission-critical end markets. But the capital deployment would become dramatically more ambitious. Diploma would move from buying ten-million-pound bolt-on businesses to acquiring hundred-million-pound "platforms"—larger businesses that could themselves become beachheads for further bolt-on acquisitions in new geographies.

The proof of concept came in September 2020, in the middle of a global pandemic, when Diploma announced the acquisition of Windy City Wire Cable and Technology Products for approximately $470 million. For a company that had built its reputation on cautious, bite-sized deals, this was an audacious bet—nearly doubling Diploma's presence in North America in a single transaction.

Windy City Wire, founded in 1994 and headquartered in Bolingbrook, Illinois, was a distributor of low-voltage wire, cable, and related technology products serving the security, access control, CCTV, fire alarm, and home automation markets. On the surface, it looked like a wire distributor. But the reason Thomson was willing to pay approximately twelve times EBITDA—nearly double the multiples Diploma had historically paid—was the same reason that made every great Diploma acquisition work: Windy City Wire was not selling wire. It was selling labor savings.

The company's signature innovation was the RackPack system: a patented cable packaging and transportation solution that eliminated the need for traditional cable spools. Instead of requiring two or three installers to manage heavy spools on a job site, the RackPack allowed a single technician to stage, store, and pull cable from a compact carton system. In a construction industry facing chronic labor shortages and rising wage costs, this was not a nice-to-have—it was a competitive weapon. Contractors who used Windy City Wire's system could complete installations faster, with fewer workers, and with fewer safety incidents. The cable itself was a commodity. The system around it was proprietary, patented, and deeply embedded in the workflows of thousands of low-voltage integrators across the United States.

Analysts questioned the price. Twelve times EBITDA was rich by Diploma's standards. But Thomson's bet was that Windy City Wire was not a one-time earnings stream—it was a growth platform. The data center construction boom, driven by cloud computing and artificial intelligence, was creating explosive demand for low-voltage infrastructure. The security and access control market was growing at high single digits annually. And Windy City Wire's proprietary system gave it pricing power and customer retention rates that commodity wire distributors could only dream of.

The deal was funded through a combination of equity—Diploma raised approximately £190 million through a share placing of up to 10 percent of its issued capital—and new debt facilities, including a $170 million term loan and a £135 million multicurrency revolving credit facility. The blended interest cost was just 2.2 percent, a reflection of the credit markets' confidence in Diploma's balance sheet.

The result validated Thomson's thesis. Windy City Wire became the cornerstone of Diploma's Controls segment, which by fiscal year 2025 had grown to represent approximately 55 percent of group revenue. More importantly, the deal proved that Diploma could execute large transactions without losing the decentralized culture that made its model work. Rich Galgano, Windy City Wire's founder, remained engaged with the business, and the management team stayed intact.

Thomson continued the acceleration. By the end of fiscal 2025, Diploma had invested over £1.3 billion in more than forty acquisitions over five years. The company's revenue had grown from approximately £550 million in fiscal 2019 to over £1.5 billion, while operating margins expanded from around 18 percent to 22.5 percent—a counterintuitive result, since rapid acquisition typically dilutes margins. At Diploma, the opposite occurred, because each acquisition brought businesses with structural pricing power into a group that provided operational support without imposing bureaucratic cost.

The most recent results, for the first quarter of fiscal 2026, showed 14 percent organic revenue growth—a figure that demonstrated the model was not just acquiring growth but generating it internally. Thomson's Diploma was not just bigger than Thompson's Diploma. It was, by almost every financial metric, better.

V. Management, Incentives, and Culture

The question that every serious investor should ask about a serial acquirer is this: what happens when the founders leave? Diploma's answer to this question is, arguably, its single most important competitive advantage—and it is rooted in a culture so deliberately unglamorous that it almost defies description.

Johnny Thomson runs Diploma with a corporate staff that remains remarkably lean for a FTSE 100 company. The head office at Charterhouse Square in London functions more as a holding company than an operating headquarters. There are no mandates to rebrand acquired businesses under the Diploma name. There are no shared ERP systems imposed from the center. There are no corporate "integration playbooks" of the type that management consultants sell for millions of pounds. Instead, Thomson and his team focus on three things: capital allocation, talent development, and strategic direction.

The Managing Directors of Diploma's individual businesses are the real operators, and the incentive system is designed to make them behave like owners. Each MD has end-to-end accountability for their business—revenue, margins, inventory, customer satisfaction, and talent. They are incentivized through a combination of base salary, annual bonus, and participation in the group's Performance Share Plan, which ties long-term compensation to two metrics that matter most: earnings per share growth and return on adjusted trading capital employed. This is a crucial design choice. Many industrial companies incentivize on revenue growth alone, which encourages empire-building and margin-dilutive acquisitions. Diploma's system rewards profitable growth and capital efficiency, which means that an MD who grows revenue at 5 percent but improves margins by 200 basis points is rewarded more generously than one who grows revenue at 15 percent through price-cutting.

The result is tenure. In an era when the average CEO lasts less than five years and the average business unit leader changes every three, Diploma's Managing Directors routinely stay for ten, fifteen, or even twenty years after their businesses are acquired. This is not because they are locked in by golden handcuffs—most have already received their acquisition payout. It is because the culture of autonomy and accountability is genuinely attractive to the kind of entrepreneurial personality who built these businesses in the first place.

Thomson has described the Diploma culture as "quiet autonomy"—a phrase that captures both its power and its invisibility. Acquired businesses keep their names, their brands, their customer relationships, and their local identities. A customer of Hercules Aftermarket in Australia may never know that the company is part of a London-listed FTSE 100 group. A contractor buying cable from Windy City Wire in Illinois has no reason to think about a holding company in Charterhouse Square. This invisibility is deliberate. It preserves the local, entrepreneurial, "small company" feel that customers value, while providing the financial firepower and strategic guidance that only a multi-billion-pound group can offer.

Thomson has also professionalized the M&A function in a way that Bruce Thompson never did. Under the previous regime, deal-sourcing was largely opportunistic—driven by personal networks and broker introductions. Thomson has built a dedicated M&A team that systematically maps the landscape of value-add distributors across North America, Europe, and Australasia, maintaining a pipeline of hundreds of potential targets at any given time. This has reduced the company's dependence on deal flow from intermediaries and increased its ability to be proactive—approaching founders before they formally put their businesses up for sale.

The skin-in-the-game alignment extends to Thomson himself. His compensation is heavily weighted toward long-term equity, and the Performance Share Plan ensures that his personal wealth is tied to the same metrics—EPS growth and ROIC—that drive value for shareholders. It is worth noting that Diploma does not pay a particularly generous base salary by FTSE 100 standards. The real wealth creation comes from the equity component, which only vests if the compounding machine delivers.

VI. The "Hidden" Engines: Segment Deep Dive

Walk into a Caterpillar dealership in Perth, Western Australia, and ask who supplies the aftermarket seal kits for the fleet of excavators working the Pilbara iron ore mines. The answer, more often than not, is a Diploma business—specifically, Hercules Aftermarket, which operates what amounts to a hidden global franchise in one of the most quietly lucrative niches in industrial distribution.

Hercules supplies an extensive range of sealing products and custom kits to customers repairing heavy machinery and hydraulic equipment. The business model is almost comically simple: when a hydraulic cylinder on a piece of heavy equipment develops a leak, the machine goes down. Every hour it sits idle costs the operator thousands of pounds in lost production. Hercules provides next-day delivery of the exact seal kit required—custom-assembled, with technical specifications matched to the machine's make, model, and serial number, along with installation instructions and quality assurance. The individual seal might cost fifty or a hundred pounds. The machine it goes into might be worth five million. The customer does not shop around.

The Seals segment, which accounts for approximately 30 percent of group revenue, is Diploma's cash cow—a business with the predictability of a utility and the margins of a luxury goods company. The aftermarket orientation means that demand is driven not by new equipment purchases but by the installed base of heavy machinery already in the field. Every excavator, every crane, every hydraulic press that has ever been sold will eventually need new seals. And as the global fleet of heavy equipment grows and ages, the aftermarket opportunity only expands. FPE, another business within the Seals segment, extends this model into industrial sealing and fluid power, serving manufacturing and process industries across Europe and Australasia.

The Controls segment, now Diploma's largest at roughly 55 percent of revenue, is where the growth story is most compelling. Windy City Wire anchors the segment's North American operations, but the portfolio extends well beyond low-voltage cable. Peerless, a specialist in high-performance fasteners for the aerospace industry, supplies components that go into commercial aircraft, military platforms, and space launch vehicles. These are not commodity fasteners—they are precision-engineered, certified to exacting specifications, and often sole-sourced by aerospace OEMs. Once a specific fastener is qualified for use in an aircraft program, the switching costs for the manufacturer are prohibitive. Requalification can take years and cost millions.

The Controls segment is also Diploma's primary exposure to two of the most powerful secular growth trends in the global economy: data center construction and defense spending. As hyperscale cloud providers and AI companies race to build computing infrastructure, the demand for low-voltage cabling, cable management systems, and interconnect solutions has exploded. Windy City Wire's patented RackPack system positions it at the center of this build-out. In defense, rising NATO budgets and the rearming of Western militaries have driven increased demand for aerospace-grade fasteners and specialized wiring harnesses. Spring Solutions, acquired to support growth in UK and European defense markets, is one of several recent additions that have expanded Diploma's exposure to this theme.

Life Sciences, at approximately 15 percent of revenue, operates on a different but equally powerful economic logic. The businesses in this segment supply specialized diagnostics instruments and surgical equipment to hospitals, veterinary clinics, and research laboratories. The classic "razor and blade" model applies: once a Diploma business places an analyzer or an instrument in a lab, the recurring revenue from consumables—reagents, test kits, calibration fluids—creates an annuity stream that can last for the lifetime of the equipment. Alpha Laboratories, acquired to enter the UK's in vitro diagnostics market, exemplifies this strategy. The sale of the instrument is almost a loss leader; the real value is in the decade-long consumables contract that follows.

The newest strategic thread running through all three segments is the European expansion initiative. Historically, Diploma's businesses were concentrated in the UK, North America, and Australasia. Continental Europe—with its fragmented landscape of thousands of small, family-owned technical distributors—represents an enormous whitespace opportunity. Recent acquisitions such as Haagensen in Denmark and Swift Aerospace, which extends reach into European aerospace fastener markets, signal that Thomson is applying the proven UK and US playbook to new geographies. With only 16 percent of revenue currently coming from continental Europe, the runway for expansion is long.

VII. The Playbook: M&A and Capital Deployment

Diploma deploys virtually all of its free cash flow into acquisitions. This is not a dividend growth story or a buyback story. It is a compounding story, and the fuel for the compounding engine is disciplined M&A.

The mechanics of the flywheel are straightforward. Diploma's existing businesses generate strong free cash flow—conversion consistently exceeds 100 percent of adjusted operating profit, meaning the businesses throw off more cash than they report in earnings thanks to favorable working capital dynamics. That cash is recycled into the next acquisition. The acquired business, plugged into Diploma's balance sheet and supported by its capital, typically accelerates its own organic growth—management has historically guided to mid-to-high single digit organic growth post-acquisition. That organic growth, combined with the margin expansion that comes from Diploma's operational support, generates even more free cash flow. And the cycle repeats.

The multiples Diploma pays have evolved alongside its ambition. During the Bruce Thompson era, the typical deal was struck at five to seven times EBITDA—a range that reflected the small size and limited competitive tension around these transactions. Many were proprietary deals, sourced directly from founders through personal relationships, with no auction process and no investment bank driving up the price. Under Thomson, the average has crept higher: bolt-on acquisitions still trade in the six to eight times range, but platform deals—the larger, more strategic transactions that provide beachheads for future bolt-ons—can command ten to twelve times.

The natural question is whether Diploma is overpaying. The answer requires understanding what happens after the acquisition. A business bought at eight times EBITDA that subsequently grows organically at 8 percent annually effectively sees its acquisition multiple compress to five or six times within a few years. And because Diploma's operating model improves margins over time—through better purchasing, shared technical knowledge, and access to a broader customer base—the post-acquisition returns consistently exceed the group's cost of capital. In fiscal 2024, Diploma invested £293 million in seven acquisitions at an average of six times EBIT and reported a return on adjusted trading capital employed of approximately 17 percent across the acquired portfolio. In fiscal 2025, six additional deals were completed for £92 million at an average of eight times.

The comparison to peers is instructive. Halma, often cited as Diploma's closest UK-listed comparable, operates a similar decentralized, acquisition-driven model but focuses on safety, environmental, and medical technology rather than distribution. Bunzl, the other frequently mentioned comparator, is a pure-play distributor but operates in lower-margin, more commoditized categories—PPE, cleaning products, foodservice packaging. Diploma sits between them in strategic positioning but increasingly above them in financial quality. Diploma's operating margins at 22.5 percent exceed Halma's and dramatically exceed Bunzl's single-digit margins. All three trade at similar earnings multiples—roughly thirty-five to forty times forward earnings—but Diploma's faster growth rate arguably makes its valuation the most justified.

The critical filter that separates Diploma from a generic roll-up strategy is what management calls the "Value-Add" test. If a target business could be disintermediated by Amazon or a commodity wholesaler—if the customer cares primarily about price and availability rather than technical expertise and application support—Diploma will not buy it. The test is simple: does this business require a "white glove" technical sell? Is the salesperson more of a consultant than an order-taker? Are the products specified into a customer's process in a way that creates switching costs? If the answer to any of these questions is no, the deal does not get done.

This discipline is what prevents Diploma from succumbing to the most common disease of serial acquirers: diworsification. Every acquisition must reinforce the core value-add positioning. Every acquisition must be capable of generating returns above the group's cost of capital within the first year. And every acquisition must fit within one of the three established segments, building density and scale in markets where Diploma already has competitive advantage.

VIII. Strategy Analysis: Hamilton's 7 Powers and Porter's 5 Forces

To understand why Diploma's competitive position is so durable, it helps to examine the business through the lens of two frameworks that sophisticated investors use to assess the quality and sustainability of a company's moat.

Hamilton Helmer's 7 Powers framework identifies seven distinct sources of persistent competitive advantage. Diploma's primary power is Switching Costs—and the nature of these switching costs is worth understanding in detail, because they are simultaneously invisible and almost insurmountable.

Consider the lifecycle of a hydraulic seal in a mining excavator. When the equipment manufacturer designs a new machine, an engineer specifies the exact seal required for each hydraulic cylinder. That specification includes material composition, dimensional tolerances, operating temperature range, pressure rating, and chemical compatibility. The seal is then qualified through a testing process that can take months. Once qualified, the specification is locked into the machine's bill of materials. For the life of that machine—which might be twenty or thirty years—every replacement seal must match the original specification. The cost of switching to a different seal vendor is not the price difference between the seals themselves. It is the cost of requalification: the engineering time, the testing, the risk that a new seal might fail in the field and bring a multi-million-pound machine to a halt. No rational procurement manager will take that risk to save a few pounds on a seal.

The same logic applies to Windy City Wire's low-voltage cable installations. Once a building's fire alarm system or access control network is wired with a specific cable type, replacing it would mean ripping out walls and ceilings—a cost that dwarfs the original cable purchase by orders of magnitude. The cable is literally embedded in the structure.

Helmer's framework also identifies Cornered Resource as a source of competitive advantage, and Diploma possesses this in the form of its technical sales force. These are not traditional salespeople. They are application engineers who understand the customer's equipment, processes, and operating environment at a level of detail that takes years to develop. A Hercules sales representative does not simply take orders for seals—they advise customers on which seal material will perform best under specific operating conditions, help troubleshoot equipment failures, and sometimes design custom seal configurations for unusual applications. This expertise is a cornered resource because it is embodied in people, not systems. It cannot be replicated by an e-commerce platform or a call center. It takes years of on-the-job training to develop, and once developed, it creates a relationship of trust and dependency between the sales engineer and the customer that is extremely difficult for a competitor to break.

Porter's Five Forces analysis reinforces this picture of structural advantage. The bargaining power of buyers is low, precisely because the products are mission-critical but represent a tiny fraction of the customer's total cost. A seal that costs fifty pounds is protecting a machine worth five million. A cable harness that costs a few hundred pounds is a rounding error in the budget of a data center that costs hundreds of millions to build. Customers simply do not have the incentive to negotiate aggressively on price, and the technical complexity of the products means that most procurement departments lack the expertise to evaluate alternatives even if they wanted to.

The threat of substitutes is equally muted. A specific hydraulic seal cannot be replaced with a "generic" alternative without risking equipment failure. A fire-rated cable that has been specified to meet a particular building code cannot be swapped for a cheaper alternative without violating the code and potentially invalidating the building's insurance. The products Diploma sells are, in many cases, defined by regulatory or engineering specifications that have the force of law.

The threat of new entrants is moderated by the same dynamics. A new competitor entering the aftermarket seal market would need to build a catalog of tens of thousands of SKUs, develop the technical expertise to match seals to specific equipment applications, establish overnight delivery capability in multiple geographies, and earn the trust of customers who depend on product quality for the safety of multi-million-pound assets. The capital required is modest, but the time and expertise required are not. This is not a business that a well-funded startup can disrupt with a better app.

One additional dimension of Diploma's strategic positioning deserves attention: its resilience in a high-interest-rate environment. Unlike many serial acquirers that fund growth with leverage, Diploma maintains a conservative balance sheet. Net debt stood at less than one times EBITDA, and the company's strong free cash flow generation means it can fund a significant acquisition program from internal resources, supplemented by modest borrowing. In a world where higher rates have punished highly leveraged business models, Diploma's capital-light, cash-generative profile is a source of genuine antifragility. The company does not just survive in a tighter monetary environment—it thrives, because higher rates raise the hurdle for competitors who depend on cheap debt to fund their own acquisitions, while leaving Diploma's internally funded model largely unaffected.

IX. Conclusion: The Bear vs. Bull Case

Every investment thesis has two sides, and Diploma's extraordinary track record does not make it immune to legitimate questions about its future.

The bear case centers on the law of large numbers. A company generating £1.5 billion in revenue and approaching eight billion pounds in market capitalization cannot grow as easily as one generating £200 million. The universe of acquisition targets that meet Diploma's stringent value-add criteria is, by definition, finite. As the company moves up the size spectrum—from ten-million-pound bolt-ons to hundred-million-pound platforms—it faces more competition from private equity firms and other strategic acquirers, potentially driving multiples higher and returns lower. There is also a cyclical dimension to monitor. Diploma's Controls segment, now its largest, is meaningfully exposed to US construction activity and, increasingly, to the data center build-out cycle. If data center construction decelerates—whether due to overbuilding, technology shifts, or a pullback in hyperscaler capital expenditure—the growth narrative could face headwinds. And at roughly thirty-five times forward earnings, the stock's valuation leaves limited room for execution missteps.

There is also the key-person question. Johnny Thomson has been the architect of Diploma's step change, and the company's strategic ambition is closely associated with his leadership. While the decentralized model means that individual businesses can operate independently of the center, the capital allocation function—the engine of the compounding machine—is concentrated in the hands of a small group at headquarters. Succession planning, as the company learned during the brief post-Thompson transition, is not trivial.

The bull case is equally compelling. Diploma's penetration of its addressable market remains tiny. In North America, the company has identified a landscape of thousands of specialty distributors, many of which are family-owned and approaching generational transitions. The European market is even more fragmented. If Diploma can replicate even a fraction of the density it has achieved in the UK across these geographies, the growth runway extends for decades. The secular tailwinds are powerful: data center construction, defense rearming, the aging of the global heavy equipment fleet, and the increasing complexity of building systems all drive demand for the exact type of value-add distribution that Diploma provides. And the compounding mathematics are relentless. A company growing earnings at 15 to 20 percent annually, funded primarily by reinvesting its own cash flow, does not need the market to rerate. It just needs time.

For investors tracking Diploma's ongoing performance, two KPIs matter above all others. The first is organic revenue growth, which measures the health of existing businesses independent of acquisitions and is the truest indicator of whether the value-add model is working. Management has targeted mid-to-high single digit organic growth, and the recent 14 percent print in Q1 fiscal 2026 suggests the model is firing on all cylinders. The second is return on adjusted trading capital employed, which captures the efficiency of capital deployment—both organic investment and M&A—and ensures that growth is generating returns above the cost of capital. As long as these two metrics remain strong, the compounding flywheel is intact.

Diploma PLC is not the kind of company that will ever generate headlines. It will never announce a moonshot project, never make the front page of a tech blog, never become a meme stock. It is, by design, invisible—a company that has built extraordinary wealth for its shareholders by doing unglamorous things with extraordinary discipline, in markets that most investors never think about. The seals, the wires, and the pipettes will never be exciting. But for those who understand the power of mission-critical positioning, value-add moats, and patient compounding, Diploma represents something rare in public markets: a business that is both easy to understand and almost impossible to replicate.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube