Domino's Pizza Group plc: The Ultimate Toll Road on Every Slice

I. The Business That Hides in Plain Sight

Picture a Friday night in any British suburb. It's raining, because it's Britain. A family of four has decided that nobody is cooking tonight. Someone opens an app, taps through a pizza, a side of garlic bread, a 1.25-litre bottle of cola, and watches a little animated tracker crawl across the screen as their order moves from "prep" to "bake" to "out for delivery." Twenty-odd minutes later a driver hands over a stack of warm boxes at the door. The family eats. The brand they remember is Domino's.

Here is the trick worth sitting with for a moment: almost none of the money that family just spent goes to the company you might think of as "Domino's UK." The franchisee who owns that local store paid for the driver. The franchisee paid for the rent, the ovens, the staff. And yet Domino's Pizza Group plc — the London-listed company trading under the ticker DOM.L — made money on the dough ball, on the cheese, on the tomato sauce, on the cardboard box, on the app the family ordered through, and on a royalty skimmed off the top of the sale itself. It made money without owning the store, hiring the driver, or signing the lease.

This is the central paradox of Domino's Pizza Group, and it's the reason this is one of the most interesting case studies in European retail economics. DPG is not really a restaurant company. It is a vertically integrated logistics, manufacturing, and technology platform that happens to lease a world-class American brand name. It is a food factory that runs three industrial-scale facilities producing dough and processing ingredients. It is a software business that builds and maintains one of the highest-converting e-commerce platforms in UK retail. And it is the holder of an exclusive, perpetual licence to one of the most recognised quick-service brands on earth, for the UK and Ireland.

The big question we want to answer is deceptively simple: how do you build a business that makes money every time someone in the UK eats a slice of pizza, without having to pay for the flour, the cheese, or the drivers yourself?

The answer is a story with genuine drama in it. Because for all the elegance of the model, the last decade nearly broke it. Between 2018 and 2021, DPG fought a brutal three-year civil war with its own franchisees — the very partners the entire model depends on — that froze store openings completely while the rest of food delivery exploded around them. Meanwhile, management went on an overseas adventure into the Nordics that ended with them literally paying buyers to take businesses off their hands, including one country sold for a single Norwegian krone. And running alongside that catastrophe, the same company pulled off one of the cleanest, most disciplined M&A trades in the FTSE 250 — a German joint venture that returned nearly six times its money with almost no operational risk.

So this is a tale of two companies inside one ticker: the serene, compounding cash machine at home, and the accident-prone empire-builder abroad. How those two characters fought, who won, and what the survivor looks like today is the arc of this episode.

Here's our roadmap. We'll start with how an American brand landed in Britain and got carved into a separate public company. We'll open up the two "hidden" businesses inside DPG — the commissary supply chain and the digital platform — that turn pizza into a toll road. We'll live through the franchisee civil war and the freeze that nearly killed the compounding engine. We'll benchmark the company's split personality in M&A, the German triumph against the Nordic disaster. We'll watch the return to discipline through the Irish consolidation. And we'll meet the management team running the modern, reset company, and stress-test the whole thing through the frameworks investors actually use. Let's get into it.

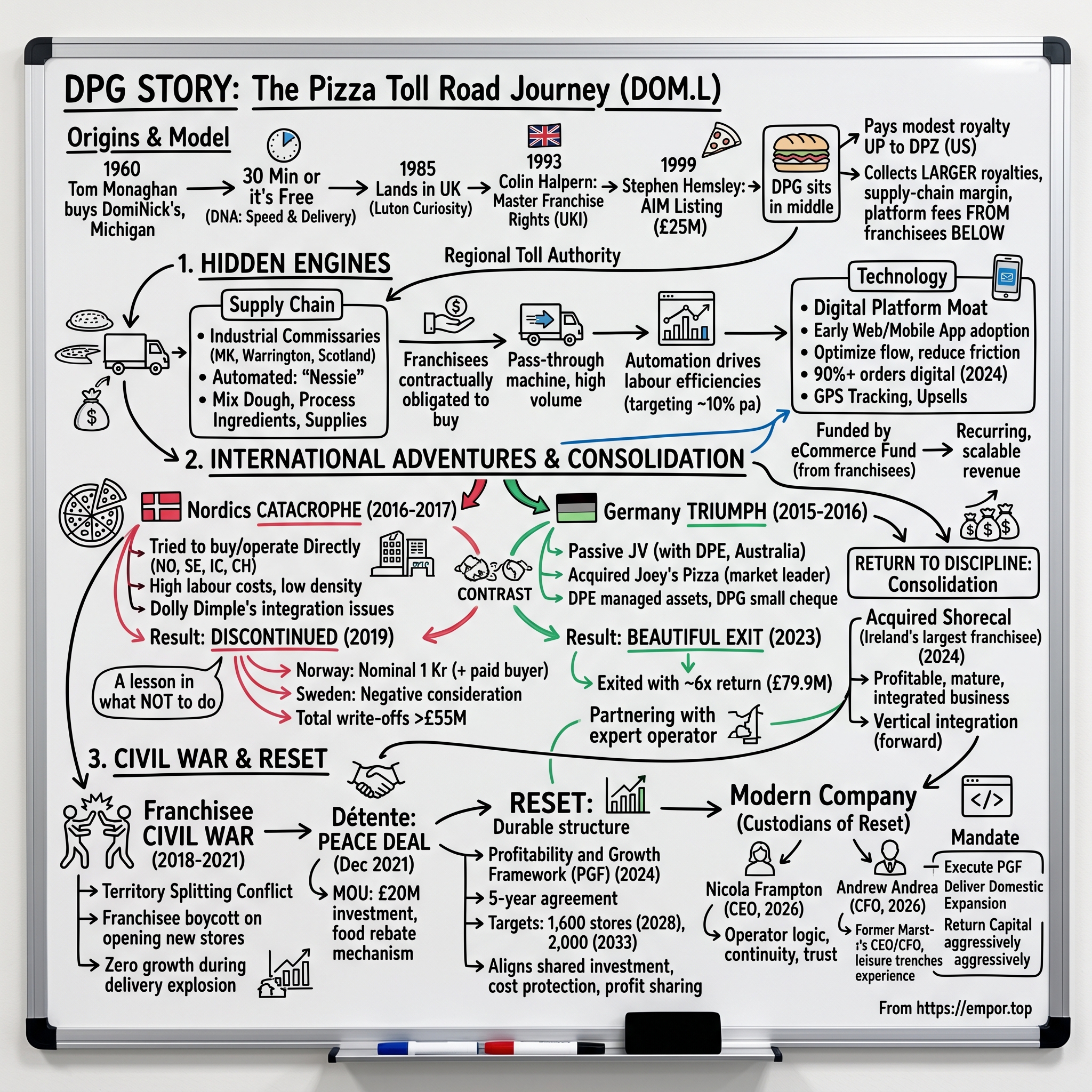

II. Origins and the Master Franchise Model

Every great franchise story starts with a founder who turned a simple operational promise into a religion. For Domino's, that man was Tom Monaghan, who with his brother James bought a single struggling pizzeria called DomiNick's in Ypsilanti, Michigan, in 1960 for a few hundred dollars. James, famously, traded his half of the business to Tom for a used Volkswagen Beetle within a year — one of the more expensive cars in business history, given what the company became.

Monaghan's genius wasn't the pizza. It was the realisation that a pizza company is actually a delivery company that happens to make pizza. He stripped the menu down to almost nothing, standardised everything, and built the entire operation around speed. The legendary promise — "30 minutes or it's free" — was the original operational algorithm, a constraint that forced every other decision in the business: store placement, oven design, route density, dough consistency. (The guarantee was eventually retired in the US in the 1990s after safety concerns about drivers racing the clock, but the obsession with speed it instilled never left the system.) That obsession is the cultural DNA that eventually crossed the Atlantic.

The brand landed in Britain in 1985, when the first UK Domino's store opened its doors in Luton, just north of London. For most of the decade that followed, it was a curiosity — a small American import in a country that still thought of pizza as a sit-down restaurant occasion rather than a thing you summoned to your sofa. The British takeaway market belonged to fish and chips, Indian, and Chinese. Pizza delivery was a culture that had to be built almost from scratch.

The pivotal commercial move came in 1993, when the entrepreneur Colin Halpern, working alongside his brother Gerry, acquired the master franchise rights for the UK and Ireland. This is the moment to understand, because it's the structural foundation of everything that follows. Halpern didn't buy a chain of pizza shops. He bought the right to be Domino's across an entire territory — the exclusive, long-dated licence to operate and sub-franchise the brand in the British Isles. That is a fundamentally different and far better asset than owning restaurants. It's the difference between being a tenant and being the landlord of an entire district.

The man who turned that licence into a compounding machine was Stephen Hemsley, who joined in 1998 and would become the defining figure in DPG's history — first as CEO, later as a long-serving chairman whose shadow stretched across decades of the company's life. Hemsley understood that the value wasn't in operating stores; it was in building the infrastructure that every store would be forced to depend on, and in taking the whole thing public to fund the build-out. In 1999, Domino's Pizza UK & IRL listed on London's Alternative Investment Market — AIM, the junior market for smaller, growing companies — at a market capitalisation of roughly £25 million. To put that in perspective: a company that would later spend years as a FTSE 250 constituent worth well over a billion pounds began its public life valued at less than the price of a few London townhouses.

Why did the model work so well in Britain specifically? Several forces lined up. The UK is densely populated and heavily suburbanised, which is exactly what a delivery business needs — lots of households packed into tight delivery radii, so each store and each driver can serve more customers per shift. Britons adopted credit and debit cards early and enthusiastically, which made remote, cashless ordering frictionless. And the broader cultural drift toward convenience food, toward the night in rather than the night out, gave delivery pizza a structural tailwind for two decades.

But the real engine sat in the contract itself: the Master Franchise Agreement with the US parent, Domino's Pizza, Inc. — the Michigan-based, NYSE-listed company known to investors as DPZ. Under that agreement, DPG pays the American parent an ongoing royalty as a percentage of sales. In exchange, DPG holds exclusive territorial rights to the UK and Ireland on a long-term, effectively perpetual basis, with the right to sub-franchise the entire region to local store operators. So DPG sits in the middle of a sandwich: it pays a modest royalty up to DPZ in America, and it collects a much larger stack of royalties, supply-chain margin, and platform fees from the hundreds of franchisees below it. It is the regional toll authority on a road the Americans built.

That middle position — owning the infrastructure, renting the brand, and sub-letting the territory — is the foundation everything else is built on. And the first place DPG turned that structural advantage into a genuine moat wasn't in the kitchen. It was on the internet.

III. The E-Commerce Turn: Technology as a Platform Moat

It's hard to remember now, but ordering a pizza used to be a genuinely chaotic experience. The "menu" was a grease-spotted paper flyer shoved through your letterbox, or a fridge magnet you'd half-lost. Ordering meant a phone call — on a Friday night, that meant a busy signal, a teenager taking down your address by hand, a misheard postcode, and a wait of indeterminate length with zero visibility into whether your food was being made or had been forgotten entirely. The whole thing ran on hope.

Domino's, both in the US and at DPG in the UK, made an early and consequential bet that the future of this business was digital, and that being first and best online would compound into an unassailable lead. DPG was among the earliest UK food brands to launch web ordering in the early 2000s, at a time when most takeaways still treated the internet as a novelty. The logic was clean: every order that moved from a phone call to a web form was an order that was cheaper to take, more accurate, and — crucially — captured as data the company owned.

The real inflection point came in the early 2010s with the mobile app. This is where DPG stopped thinking like a restaurant chain with a website and started thinking like a technology company that sold pizza. The difference shows up in how they treated the app: not as a digital menu, but as a product to be relentlessly optimised. They attacked friction at every step — saved addresses, saved payment details, one-tap reordering of your "usual." They pioneered real-time GPS-style delivery tracking, that little progress bar that turned the anxious dead time of waiting into a weirdly compelling experience. And they engineered the upsell into the flow of the order itself: the "add garlic pizza bread for £2.99?" prompt that appears at exactly the moment of maximum hunger and minimum resistance. Each of those nudges, multiplied across millions of baskets, lifted the average order value in a way no human phone operator ever could.

The results were staggering in their completeness. What began as a novel channel became, by 2024, more than 90% of all system orders flowing through DPG's digital platforms.[^1] Think about what that means competitively. The company isn't guessing what its customers want — it knows, order by order, what every household buys, when, how often, and what makes them come back. That data feeds the loyalty engine, the promotions, the menu decisions, and the marketing spend. An independent pizzeria, or even a rival chain without that digital depth, is effectively flying blind by comparison.

Then came the threat that, in theory, should have undone all of it: the delivery aggregators. The rise of Deliveroo, Just Eat, and Uber Eats in the mid-to-late 2010s created a new layer between restaurants and customers — platforms that owned the demand, owned the data, and charged punishing commissions for the privilege of access. For most restaurants, the aggregators were a Faustian bargain: more orders, but a hollowing-out of the direct customer relationship and a permanent tax on every sale.

DPG resisted them for years, and the reasoning was strategic, not stubborn. The company's entire moat was the direct relationship — the app, the data, the loyalty loop. Handing that relationship to a third party would have meant renting back its own customers and surrendering the very asset that made the business special. So Domino's held the line, betting that its own delivery network and its own app were good enough that it didn't need the middlemen.

But strategy has to bend to reality, and the reality was that the aggregators had trained an entire generation of customers to start their food search inside those apps. To never appear there was to be invisible to a growing slice of demand. So DPG eventually integrated with the aggregators — but on its own terms, framing them strictly as a source of incremental customers: people who would never have come to Domino's directly, captured at the margin, while the core, high-value relationship stayed locked inside DPG's own platform. The discipline in that distinction — defend the direct channel, use the aggregators only to mop up demand you couldn't otherwise reach — is the difference between a brand that controls its destiny and one that becomes a commodity supplier to someone else's app.

The digital platform is one of the two hidden engines that make DPG so much more than a pizza company. To understand the other, we have to go behind the storefront entirely, into the factories.

IV. The Hidden Engines: Vertical Supply Chain and the Internal SaaS

If you want to understand why DPG's financial model is so much better than a normal restaurant's, you have to stop thinking about pizza and start thinking about toll roads. A normal restaurant makes money once — when it sells a meal — and bears all the costs and risks of doing so. DPG built something different: a structure where it collects a fee at multiple points along the journey of every single pizza, while the franchisee carries the operational weight. There are two of these toll booths, and neither one looks like a restaurant at all.

The first and largest is the supply chain. DPG doesn't just license the brand to its franchisees — it manufactures and distributes the food they sell. The company owns and operates a set of highly automated Supply Chain Centres, the industrial commissaries at Milton Keynes, Warrington, and West Lanarkshire at Cambuslang in Scotland. These are not kitchens; they are food factories. They mix and portion dough into the standardised dough balls that go to every store, process and pack the cheese, blend the tomato sauce, prepare the meat toppings, and supply the cardboard boxes and consumables.

Here's the part that makes it a toll road rather than a wholesale business: franchisees are contractually obligated to buy essentially all of these core ingredients and supplies from DPG. They cannot shop around for cheaper cheese. They cannot source their own dough. The franchise agreement makes DPG the sole supplier for the inputs that matter. So every time a franchisee opens a new store, or an existing store sells more pizzas, DPG's supply-chain revenue grows automatically — with zero cost to acquire that customer, because the customer is captive by contract. This is what makes the supply chain a high-volume, pass-through machine with effectively no customer acquisition cost. The franchisees do the selling; DPG sells to the sellers, and it's the only shop in town.

This is also where some of the most interesting recent strategy lives, because DPG has been pouring capital into automating these facilities. The marquee example is the deployment of robotics — including an automated system nicknamed "Nessie" at the Scottish operation and investment at the Warrington facility — aimed at squeezing labour out of the dough-and-distribution process. The financial logic management has set out is targeting roughly 10% annual labour-cost efficiencies from automation, against a payback period of three to four years on the capital spent. Think about what that does over time: in a business where the supply chain is the single biggest cost line, automating the factory floor doesn't just cut cost once — it compounds, year after year, widening the margin between what franchisees pay DPG and what it costs DPG to produce. The cheese stays the same; the labour to handle it keeps falling.

The second hidden engine is subtler, and it looks a lot like a software-as-a-service business hiding inside a pizza company. Remember that more than 90% of orders flow through DPG's digital platform. Someone has to build, run, and continually upgrade that platform — the app, the loyalty engine, the payment gateways, the order-routing systems. DPG does, and it funds the work through a central eCommerce Fund that the franchisees pay into as a percentage of their sales. In other words, the franchisees collectively bankroll the technology that drives their own orders, and DPG operates it as a shared service.

Under the new Profitability and Growth Framework that took effect in January 2025, the franchisees' contribution to that eCommerce Fund increased from 0.75% to 1.0% of system sales, with DPG itself adding a further 0.25%.[^2] That might sound like a small number, but apply it to a system generating well over a billion pounds in sales and it becomes a substantial, recurring, software-like revenue stream dedicated to keeping DPG's digital moat in front of everyone else's. It has exactly the characteristics investors prize in SaaS: recurring, contractual, scaling automatically with the size of the network, and funding a product that gets harder to compete with every year.

When you put the segments side by side, the shape of the real business becomes clear. The supply chain is the largest single revenue contributor — typically in the region of £420 million to £440 million a year — which tells you just how much of DPG's top line is actually industrial food processing and distribution rather than retail.[^1] Sitting on top of that is the genuinely high-margin layer: the royalties and franchise fees, collected as a percentage of the system's total sales, which have run north of £1.4 billion annually.[^1] These are the cleanest, most cash-generative pounds in the entire model — money that arrives simply because pizzas were sold, with almost no incremental cost attached. And then there's a growing slice of direct corporate-store retail revenue, which stepped up meaningfully after DPG took full control of its Irish operations in 2024 — a deal we'll come to shortly.

So the toll road has two main booths and a high-margin royalty skim layered over both. It is, on paper, close to an ideal business. Which makes what happened next all the more remarkable, because the people who depended on that toll road — the franchisees — got angry enough to shut the whole thing down.

V. The Great Franchisee Civil War (2018–2021)

A franchise system runs on a delicate truth that's easy to forget when the cash is flowing: the franchisor and the franchisee are supposed to be partners, but their interests are not perfectly aligned. The franchisor wants more stores, more sales, more volume through the supply chain. The franchisee wants their store to be profitable. Most of the time those goals point the same direction. And then, occasionally, they collide head-on. Between 2018 and 2021, they collided so violently that they nearly broke the compounding machine.

The root of the conflict was a growth tactic called "territory splitting." Under the management of the era, DPG wanted to drive the store count higher — more stores meant more dough balls sold, more royalties collected, more system sales. The fastest way to add stores was to carve up the delivery territories of existing franchisees and drop new stores into zones that established owners considered theirs. From head office, this looked like efficient market densification: shorter delivery times, better coverage, more capacity. From the perspective of the franchisee who had spent years and serious capital building up a territory, it looked like the company was inviting a competitor to set up shop in their back garden and calling it strategy.

The timing made the grievance combustible. Franchisees were simultaneously being squeezed from two directions on cost. Successive increases in the National Living Wage drove up their single largest controllable expense — labour — because a pizza store is, at the end of the day, a building full of people making and driving food. At the same time, the ingredient prices coming down the supply chain from DPG were rising. So franchisees faced a vice: higher wages, higher input costs, and now head office wanted to split their territories and cannibalise their sales on top of it. They argued, with real numbers behind them, that territory splitting gutted store-level return on investment — that you cannot ask an operator to accept lower sales per store and higher costs and keep investing in new locations. The maths simply didn't work at the kitchen level.

So the franchisees did something a fragmented, dependent group rarely manages to do: they organised. The Domino's Franchisee Association, representing the overwhelming majority of UK store owners, coordinated a collective response — a freeze on opening new stores. And because franchisees, not DPG, are the ones who actually build and open stores, this was a devastatingly effective weapon. For more than three years, new store growth in the UK ground essentially to a halt. The single most important driver of DPG's long-term value — the relentless addition of new stores feeding the supply chain and royalty engine — simply switched off.

The strategic damage went beyond the frozen store count. This was precisely the window in which food delivery was being utterly transformed by the aggregators, when demand was exploding and the landscape was being redrawn. And there sat Domino's, the category's most powerful brand, locked in litigation-heavy internal gridlock, unable to expand, pointing its energy inward at its own partners instead of outward at the market. Every year the stalemate dragged on was a year of ground ceded. The market noticed; the shares spent much of the period under a cloud.

The resolution required a change in tone at the top and a recognition that you cannot win a war against the people who run your business. Under interim leadership, DPG negotiated a historic peace deal, announced in December 2021 as a memorandum of understanding with the franchisee body.[^3] The terms were a genuine compromise, and they're worth understanding because they reveal what it actually takes to re-align a franchise system. DPG committed £20 million of investment into digital platforms and marketing over three years — putting real money behind shared growth rather than just demanding it.[^3] The company introduced a food-cost rebate mechanism, a way of cushioning franchisee margins when ingredient inflation spiked, directly addressing the cost squeeze that had detonated the conflict. In return, the franchisees agreed to end the boycott, the two sides set a target of opening 45 or more new stores a year, and they agreed to unify national marketing campaigns again.[^3] The Financial Times reported the détente as the end of a dispute that had hung over the company for years.1

The deeper lesson — and the thing management clearly internalised — was that a one-off peace treaty wasn't enough. Trust that has been broken needs a durable structure, not a handshake. So the temporary memorandum was developed into something permanent: the Profitability and Growth Framework, a five-year agreement reached with franchisees in December 2024 and commencing in January 2025.[^2] The PGF institutionalised the alignment — locking in the profit-sharing logic, the cost protections, and the shared investment in technology — and attached long-term ambition to it, with targets of reaching 1,600 stores by 2028 and 2,000 stores by 2033.[^2]

The civil war is the most important episode in DPG's modern history because of what it proves about the model's one true vulnerability. The supply chain, the technology, the brand licence — none of it matters if the franchisees are losing money, because the entire toll road runs on their willingness to keep building and operating stores. While management was learning that lesson the hard way at home, it was simultaneously learning a far more expensive version of it abroad.

VI. Capital Allocation and M&A: A Tale of Two Strategies

Here's the puzzle that defines DPG's most controversial decade. The UK business is a cash gusher — a capital-light, high-margin machine throwing off more free cash flow than it can reinvest at home. That's a wonderful problem, but it is still a problem, because cash that can't be deployed at high returns has to go somewhere, and the somewhere a management team chooses tells you almost everything about its judgement. DPG made two big overseas bets in roughly the same window, with diametrically opposed structures, and the results could not have been more different. Studied together, they form one of the cleanest natural experiments in capital allocation you'll find on the London market.

Start with the masterpiece: Germany. In 2015 and 2016, DPG wanted exposure to the large, under-penetrated German pizza-delivery market. But — and this is the crucial bit — it did not try to operate Germany itself. Instead, it partnered with Domino's Pizza Enterprises, the Australian-listed master franchisee known as DPE, which was already one of the most capable Domino's operators on the planet. Together they formed a joint venture, nicknamed Daytona, to acquire Joey's Pizza, then Germany's leading delivery chain, in a deal that valued the target at up to roughly €79 million.

The structure is the whole story. DPG took a passive 33.3% stake and contributed an initial equity investment of only about £13.8 million.[^5] DPE — the expert operator with the local muscle and the operational know-how — ran the assets. DPG essentially wrote a relatively small cheque, lent its brand-side expertise, and let a world-class partner do the hard, risky work of integrating and operating a foreign business. It was a bet on someone else's competence rather than a bet on its own.

And it paid off beautifully. In June 2023, DPG exercised a put option — a pre-negotiated right to sell its stake back to its partner — and exited the German JV for total proceeds of £79.9 million, comprising £70.6 million for the equity plus £9.3 million in loan repayment, on top of the market-access and royalty-type fees it had collected along the way.[^5] Run the basic arithmetic that any investor would: a roughly £13.8 million equity investment turned into £70.6 million of equity proceeds. That's close to a six-times return on the equity, generated with minimal operational risk and almost none of management's own attention, because the partner carried the load.[^5] This is what disciplined international expansion looks like — find a market you believe in, then rent the operational mastery you don't have rather than pretending you do.

Now the catastrophe, and the reason the German trade looks so wise in hindsight: the Nordics. In almost exactly the same era, between 2016 and 2017, DPG pursued the opposite philosophy. Instead of partnering, it tried to directly buy and operate a cluster of northern European markets — Norway, Sweden, Iceland, and Switzerland. It started with minority stakes costing around £24 million, then spent roughly a further £16.1 million buying its way to majority control across Sweden, Norway, and Iceland, layered on about £4 million for a Norwegian chain called Dolly Dimple's, and committed roughly £26.8 million to take its Icelandic position up to around 95%. This was empire-building in its purest, most hands-on form: DPG would own these markets directly and run them itself.

Almost everything that could go wrong, did. The Nordic markets had punishingly high labour costs, particularly Norway and Sweden — which is poison for a delivery model that is fundamentally a business of paying people to make and drive food. There was none of the supply-chain density that made the UK work; without a thick network of stores close together, you can't run efficient commissaries or tight delivery routes, so the unit economics never cohered. The Dolly Dimple's integration created severe friction — bolting a different local brand onto the Domino's system proved far harder than the spreadsheet suggested. And aggressive local competitors didn't roll over for the new foreign owner. DPG was trying to run a high-labour, low-density retail operation directly, in markets where it had no structural advantage — the exact inverse of the dense, infrastructure-rich cash cow it ran at home.

By October 2019, the board faced facts and declared the international operations discontinued, drawing a line under the experiment to stop the cash bleed — the directly operated international business was running an underlying operating loss of around £20 million in 2019 alone. What followed was a series of exits so painful they have become a textbook illustration of what it costs to admit a mistake.

Norway went first. In early 2020, DPG agreed to dispose of its Norwegian operations for a nominal consideration of one Norwegian krone — a fraction of a penny — and even then it had to put money in, paying around £7 million to the buyer to fund ongoing losses through to completion, ultimately booking a disposal loss in the region of £10.8 million.[^6] Read that again: the company paid someone to take the business away. Sweden followed in 2021, sold for a negative consideration of roughly €2 million — once more, DPG paid the buyer to assume the operation.[^7] Iceland was disposed of in 2021 for £13.7 million, crystallising a loss on disposal of around £7.3 million.[^8] The Swiss operations were the last to go, with completion in August 2021 marking DPG's full and final exit from directly operated international markets.[^9]

Tally it up and the total write-offs and exit charges across the Nordic adventure exceeded £55 million — and that headline number understates the real cost, because it omits the years of management attention, the opportunity cost of capital tied up in losing markets, and the distraction during the very period when the franchisee war was raging at home. This is the "diworseification" trap that the investor Peter Lynch named: a strong core business destroying value by diversifying into things it has no business doing. The lesson DPG paid tens of millions of pounds to learn is stark and worth carrying out of this episode: running a dense, infrastructure-backed cash cow in a market you understand is a completely different game from operating high-labour retail directly in foreign territories where you have no edge. Owning the moat at home does not mean you can build one abroad.

Chastened by the Nordics and enriched by Germany, DPG emerged with a clear new philosophy about where its cash should go. And the first big test of that philosophy came not in some distant market, but right next door.

VII. The Return to Discipline: Consolidating Ireland

After the Nordic bonfire, DPG's M&A strategy underwent a complete personality transplant. Gone was the appetite for greenfield international adventures, for buying minority stakes in distant markets and hoping to learn how to operate them. In its place came a much narrower, much more defensible idea: in-market consolidation. Don't go somewhere new and unfamiliar. Go deeper into the markets you already understand, where the supply chain already exists, where the brand is already established, and where you already know exactly how the economics work. Buy profitability you can see, not potential you have to imagine.

The target that embodied this new discipline was Shorecal Limited, the largest Domino's franchisee across Northern Ireland and the Republic of Ireland. Shorecal wasn't some speculative platform in a foreign culture — it was an established, mature, highly profitable operator running 34 of the 99 Domino's stores on the island of Ireland, already plugged into DPG's system, already buying from DPG's supply chain, already running on DPG's technology.[^10] In other words, DPG knew this business intimately, because it had been supplying and supporting it for years. There was no integration mystery, no operational culture shock, no foreign labour market to decode.

In a deal announced in March 2024, DPG acquired the remaining 85% stake in Shorecal that it didn't already own, for €72 million, structured as 61% cash and 39% in new DPG shares, and additionally repaid €19.9 million of Shorecal's outstanding debt.[^10] The share component is itself a tell about discipline — by paying part of the price in equity, DPG aligned the sellers with the future of the combined business and conserved cash, rather than levering up for a purely cash deal.

Strategically, the contrast with the Nordics could not be sharper, and that's exactly the point. Where the Nordic markets were high-cost, low-density, foreign, and loss-making, Shorecal was a profitable, mature business fully integrated into DPG's existing infrastructure. By moving from being the supplier-and-royalty-collector for these Irish stores to being the outright owner of them, DPG captured 100% of the retail economics — the full margin on every pizza sold, not just the slice it took at the supply-chain and royalty toll booths. It vertically integrated forward into ownership of a piece of its own network, precisely where the economics were proven and attractive. This is what a mature, disciplined capital-allocation framework looks like in practice: a company that has learned, expensively, the difference between buying a business it understands and buying a story it doesn't.

The Shorecal deal also tells you something about who now runs DPG and how they think. The reset company is more cautious, more focused on its home territories, and more willing to deepen rather than broaden. Which brings us to the people charged with carrying that philosophy forward.

VIII. Current Management: The Custodians of the Reset

Every company that survives a near-death experience eventually faces a question of stewardship: who do you trust to make sure it never happens again? For DPG, after the franchisee war and the Nordic disaster and the long, grinding work of resetting the franchisee relationship, the answer that emerged was telling. Rather than reaching for a celebrity outsider with a turnaround reputation, the board reached inward, for the person who already knew where every body was buried and every dough ball was made.

That person is Nicola Frampton. She stepped in as interim CEO in November 2025 and was confirmed as permanent chief executive on March 31, 2026.2 What makes her appointment significant is precisely that she is not a parachuted-in stranger. Frampton had served as DPG's Chief Operating Officer for over four years before taking the top job, which means she lived through the back half of the franchisee reset and the Shorecal integration from the operational driver's seat. She knows the franchisees personally. She understands the supply-chain automation programme not as a slide in a board pack but as a set of machines in real factories. In a business whose single greatest vulnerability is the relationship with its franchise partners, putting an operator who has spent years managing exactly that relationship in charge is a deliberate bet on continuity and trust over disruption and reinvention.

Her incentives are structured to keep her focused on the long game. Frampton holds a direct shareholding of roughly 0.008% of the company, valued at around £56,830 — a modest absolute stake, but the more important detail is the shape of her pay. Her compensation package, in the region of £528,820 for FY25, is heavily geared toward performance, with close to 90% of the potential reward tied to long-term incentives rather than fixed salary. Those incentives run through the Long-Term Incentive Plan and a Deferred Share Bonus Plan, vehicles designed to bind her personal wealth to multi-year shareholder returns and to the store-opening targets at the heart of the Profitability and Growth Framework. In plain terms, she gets meaningfully rich only if the share price and the store count both go the right way over years, not quarters — which is exactly the alignment shareholders should want from someone running a long-duration compounding machine.

Frampton also brings outside boardroom weight that's worth noting. She serves as a Non-Executive Director and chairs the Remuneration Committee at Frasers Group plc, the FTSE 100 retail empire built by Mike Ashley. That role gives her direct, current exposure to high-level corporate governance and pay design at one of the more aggressive operators in British retail — useful experience for a CEO whose own job is partly about keeping a fractious, incentive-sensitive network of franchisees pointed in the same direction.

Alongside her sits a new chief financial officer, Andrew Andrea, who joined the board as CFO on March 16, 2026. Andrea's background is a deliberate fit for DPG's reality. He is the former CFO and later CEO of Marston's plc, the pubs and brewing group — which means he has spent decades running highly operational, estate-heavy, hospitality and leisure businesses where margins are thin, labour is the swing factor, and physical operations matter enormously. That is precisely the texture of DPG's world: factories, logistics, stores, and the unglamorous grind of operational efficiency. A pure financial engineer would be the wrong hire for a company whose value comes from running food factories well and keeping store-level economics healthy; an operator-CFO who has lived in the leisure trenches is the right one.

The mandate this pair share is unambiguous, and it's the inverse of the empire-building that nearly came undone. Execute the Profitability and Growth Framework and keep the franchisee relationship aligned. Deliver the domestic store expansion, marching toward 1,600 stores by 2028 on the way to 2,000 by 2033. And return capital aggressively — through dividends and consistent share buybacks — funded by the core UK and Ireland cash engine rather than gambled on foreign adventures. It is, deliberately, a less exciting story than the one that came before. After the decade DPG just had, less exciting is the entire point.

Having met the company, lived through its crises, and met its custodians, we can now do what investors actually need: stress-test whether the moat is real, and where it might leak.

IX. Framework Analysis: 7 Powers and Porter's Five Forces

Let's put DPG under two of the most useful lenses in business strategy and see what holds up. Hamilton Helmer's 7 Powers framework asks where a company's durable advantage actually comes from. Michael Porter's Five Forces asks how attractive the underlying industry is and where the pressure points sit. Run DPG through both and the picture is consistent: a genuinely powerful core with a couple of real soft spots.

Start with Helmer's powers, because this is where DPG is strongest. The dominant one is scale economies, and it lives in the supply chain. When you are processing and distributing dough, cheese, sauce, meat, and packaging for well over 1,300 stores from a handful of automated commissaries, you buy raw ingredients at a scale no independent pizzeria and few rival chains can approach. A single store buying mozzarella pays one price; a network buying it by the multi-thousand-tonne pays another entirely. That cost gap, widened further by the automation programme squeezing labour out of the factories, is a structural advantage that compounds as the network grows — every new store makes the supply chain a little more efficient, which makes the whole system a little harder to compete with.

The second power is network effects, expressed through the marketing and data flywheel. DPG runs a National Advertising Fund financed at 4.0% of system sales, pooling the marketing muscle of the entire network into a single war chest. The larger the store count, the bigger that pool, the more national advertising it can buy, and the lower the marketing cost per individual order — while the digital platform simultaneously gathers more data with every transaction, sharpening targeting and promotion. More stores feed more marketing and more data, which drive more orders, which support more stores. It's a self-reinforcing loop that a sub-scale competitor simply cannot spin up.

The third power is a cornered resource: the exclusive, perpetual Master Franchise Agreement for the UK and Ireland. There is exactly one Domino's licence for this territory, and DPG holds it. No amount of capital or cleverness lets a competitor acquire it, because it isn't for sale. This is the bedrock under everything else — the legal right to be Domino's in the British Isles.

The fourth power is switching costs, and here the analysis has to be honest about who's switching. For consumers, switching costs are only moderate — loyalty points and saved app preferences create some stickiness, but a hungry customer can tap a different app in seconds. The far higher switching costs sit with the franchisees, who have sunk millions in capital into store builds and fit-outs and are locked into multi-year franchise agreements. That's a double-edged power: it makes the network stable and durable, but — as the civil war demonstrated — it also breeds resentment when those locked-in partners feel squeezed, which is why the PGF's profit-sharing logic matters so much to keeping the power benign rather than explosive.

Now Porter's Five Forces, which surface where the industry pressure actually comes from. The threat of new entrants is low: anyone can open a pizza shop tomorrow, but nobody can quickly replicate national scale, a roughly 20-minute average delivery, automated commissaries, and a proprietary mobile technology stack built over a decade and funded by tens of millions of pounds. The barrier isn't making pizza; it's building the machine around the pizza. The bargaining power of suppliers is low, because DPG flips the usual dynamic — as a near-monopsony buyer of cheese, flour, meat, and packaging for the whole UK system, it dictates terms to its vendors rather than the other way around.

The forces that bite are on the demand and partner side. The bargaining power of franchisees is medium-to-high — the 2018–2021 boycott proved they can collectively bring growth to a standstill, and while the PGF has institutionalised a more balanced settlement, the structural tension never fully disappears. The threat of substitutes is high: every other quick-service brand — McDonald's, KFC — and every independent restaurant now sits one tap away on the same delivery aggregators, so a household choosing dinner has near-infinite alternatives. And rivalry is high, with Papa John's, Pizza Hut, and a long tail of local independents all fighting for the same Friday-night order.

Net it out and the framework view is coherent: DPG's powers are deep and durable on the supply, scale, and licence dimensions — the toll-road economics are real — but the model is genuinely exposed on the demand side, where substitutes and rivalry are fierce, and on the partner side, where franchisee power is a permanent variable to manage rather than a problem that's been solved. That balance of structural strength and real vulnerability is exactly what makes the investment case worth arguing both ways.

X. The Playbook: Business and Investing Lessons

Step back from the specifics and DPG offers a handful of lessons that travel well beyond pizza. These are the transferable principles an investor or operator should carry out of this story.

First: the royalty toll road, paired with vertical integration, is about as good as business models get. Slicing a royalty off the top of system sales is wonderful on its own — it's high-margin, recurring, and scales without capital. But DPG layered the commissary supply chain underneath it, so the company captures margin not just on the final sale but on the dough, the cheese, the sauce, and the box that go into it. Stack a royalty skim on top of a captive supply chain on top of a platform fee, and you get a capital-light compounding machine where the franchisees fund the store builds, carry the operating risk, and DPG collects at every stage. When you find a business that gets paid multiple times along a value chain it doesn't have to fund, pay attention.

Second: operator alignment beats greenfield heroics. The single starkest lesson in this entire story is the Germany–Nordics contrast. Same company, same era, same pool of cash — and a roughly six-times return where it partnered with an expert operator, against tens of millions in losses where it tried to operate foreign markets itself. The principle is general: if you don't possess local operational mastery, rent it through a joint venture or a partnership rather than convincing yourself you'll learn it on the job. Humility about what you don't know how to do is worth real money.

Third: a franchise is a partnership, not a dictatorship. You cannot run a healthy franchise system if your franchise partners are losing money, no matter how strong your brand or how clever your supply chain. The three-year boycott is the permanent reminder that the franchisees hold the ultimate veto — they're the ones who build and run the stores — and that growth extracted at their expense isn't growth, it's a loan against future conflict. Aligning incentives through a durable structure like the PGF isn't soft corporate citizenship; it's the precondition for any structural growth at all.

Fourth: vertically integrate the moat itself. By owning dough production and the logistics that move it, DPG guarantees absolute product consistency — a Domino's pizza tastes the same in Luton as in Lerwick — and simultaneously builds the toll road that captures margin at every step. Control of the physical inputs is both a quality mechanism and a profit mechanism. When the thing that makes your product consistent is also the thing that makes you money, you've integrated in the right place.

These lessons all point in the same direction, which is also where the investment debate lives: a powerful, focused core, deliberately defended after an expensive education in what not to do. So how should an investor weigh it?

XI. Bull, Bear, Myth, and the Numbers That Matter

Let's end where an investor would: with the two-sided argument, the consensus narratives worth checking, and the short list of metrics that actually tell you whether the machine is working.

The bull case is a story about focus and cash. DPG has resolved into a pure-play UK and Ireland operator — no more foreign distractions, no more cash bleeding into Nordic firesales. Its franchisee network is, for the first time in years, contractually aligned under a five-year framework that ties everyone to shared growth and shared profits. Its margins are protected on two fronts: the food-cost rebate mechanism cushions franchisees through inflation, and the supply-chain automation programme is structurally lowering the cost of the largest expense line in the business, with that targeted 10% annual labour efficiency compounding over time. And because the core throws off more cash than it can reinvest at home, the company can return capital steadily through dividends and buybacks while still funding the march toward 1,600 and then 2,000 stores. It's a serene, cash-generative compounder doing the boring thing well.

The bear case is a story about saturation and the squeeze. The UK is not an infinite market; a footprint already past 1,300 stores marching toward 2,000 inevitably runs into diminishing returns, with each new store more likely to split an existing territory than to open virgin ground — the very dynamic that lit the civil war. Food-cost inflation is a persistent adversary, and rebates that protect franchisees protect them by transferring cost or margin away from DPG, so the squeeze doesn't vanish, it just moves around the system. And there's a longer-term demand worry: in a cost-of-living-conscious Britain, the supermarket private-label pizza — a £3 chilled margherita you bake yourself — is a real substitute at the value end, and a structural trade-down in consumer behaviour would pressure the volumes the whole toll road depends on. Layer on the high substitute threat and intense rivalry from the Five Forces analysis, and the bear has plenty to work with.

A couple of myths worth checking against that consensus. The first is the lazy framing that "Domino's is a restaurant chain," which the whole architecture of this business contradicts — it's an industrial supply-chain-and-technology business that licenses a brand, and valuing it as a restaurant misreads where the margin and the moat actually sit. The second is the narrative, popular during the dark years, that the franchisee relationship was a permanent structural flaw. The reality is more nuanced: the relationship was genuinely broken under one approach to growth and has been deliberately re-engineered under another, but it remains a variable to be managed in perpetuity, not a problem stamped "solved." Believing either extreme — that the conflict was fatal, or that it's permanently behind them — misses the truth that franchisee alignment is an ongoing discipline, not a one-time fix.

If you strip everything down to the metrics that genuinely matter for tracking this company, three stand out, and they map directly onto the three things that can make or break the model. The first is system sales growth combined with new store openings against the PGF targets — because the entire compounding engine runs on more stores selling more pizzas, and the cadence of openings is the cleanest read on whether the franchisee peace is actually translating into growth. The second is the supply chain margin, which is where the automation thesis either shows up or doesn't; if the robots are delivering, this is where you'll see the cost of the largest segment falling relative to its revenue. And the third is franchisee store-level profitability and the health of the relationship, harder to read from a single number but visible in the openings cadence, the tone of franchisee commentary, and whether the rebate mechanisms are keeping operators willing to invest. Watch those three and you're watching the load-bearing walls of the business.

Domino's Pizza Group remains one of the most instructive case studies in retail economics precisely because it contains both a near-perfect business and a near-disastrous decade inside the same ticker. It shows how a capital-light toll road on top of a captive supply chain can compound beautifully — and how the same management, flush with cash from that machine, can torch tens of millions chasing markets it never understood. It shows that the deepest moat in the business, the franchisee network, is also its most dangerous fault line. And it shows a company that paid an expensive tuition, learned the lesson, and came back to do the one thing it was always best at: standing in the middle of every pizza sold in Britain and Ireland, collecting at every toll booth along the way.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube