Dunelm Group plc: The King of the English Home

I. The Curtain Stall That Conquered a Nation

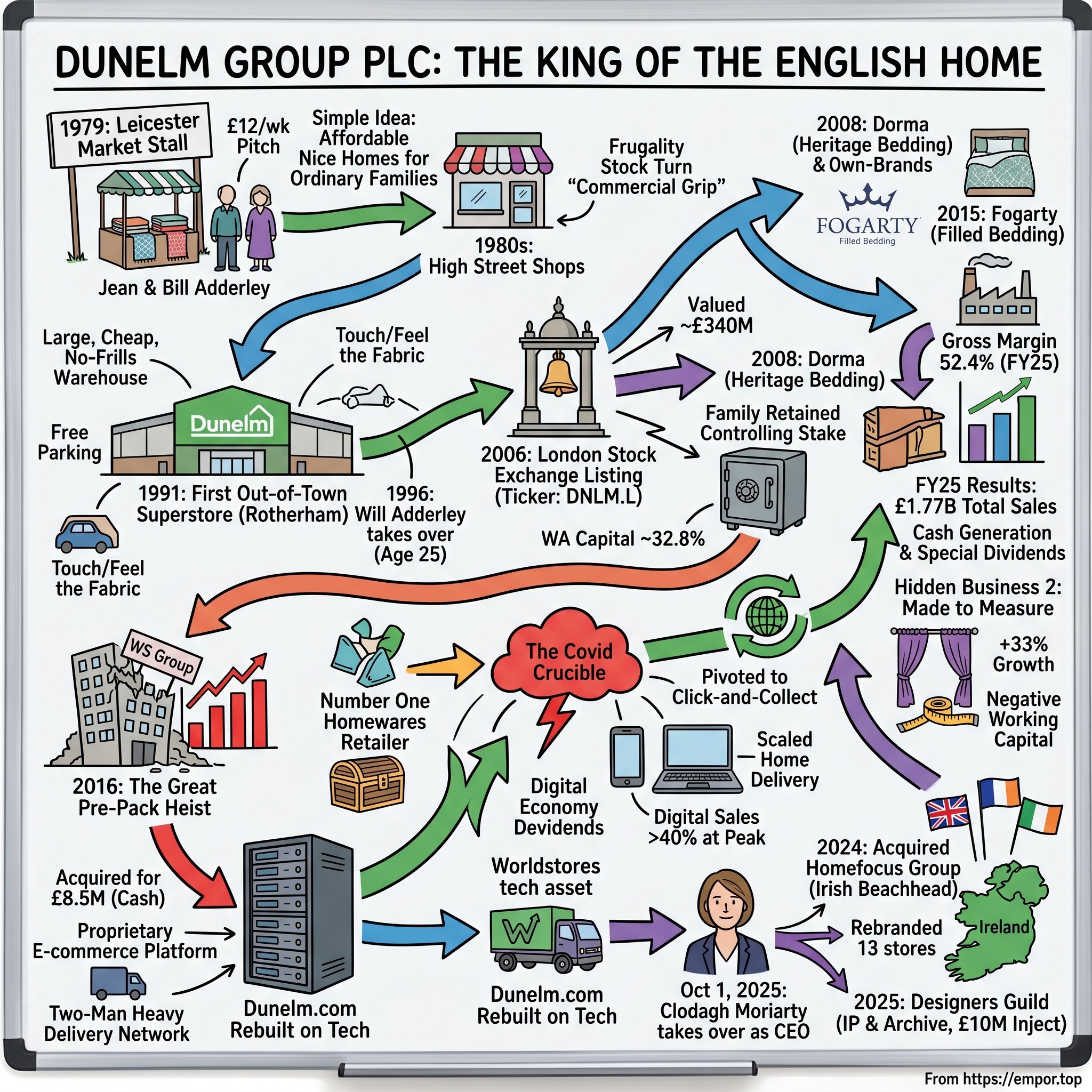

Picture a market hall in Leicester in 1979. The air smells of frying onions and damp wool. Stallholders shout over one another, hawking everything from socks to saucepans, and somewhere in the middle of that din, a woman named Jean Adderley is selling curtains — not designer curtains, not anything fashionable, just plain, ready-made "seconds" that the textile mills of the East Midlands could not sell at full price. Her husband Bill kept the books and humped the stock. The pitch fee was £12 a week. There was no brand, no logo, no grand plan, just a simple, almost stubborn idea: ordinary British families wanted to make their homes nice, and nobody was serving them at a price they could actually afford.

Forty-seven years later, that curtain stall has metastasised into Dunelm Group plc, the undisputed number-one homewares retailer in the United Kingdom. In its 2025 financial year, Dunelm rang up total sales of £1.77 billion, up 3.8% on the prior year, and held the largest single share of a fragmented £25-billion-plus UK home market.1 It operated more than 200 stores, generated an industry-leading 52.4% gross margin, and threw off so much cash that it has handed shareholders special dividend after special dividend on top of its ordinary payout.1 The market valued the whole thing at north of £2 billion.2

Here is the paradox that makes Dunelm worth a deep dive. Over the same four decades, the British high street became a graveyard. BHS collapsed. Woolworths vanished. Debenhams was liquidated. House of Fraser limped into a rescue. Even John Lewis — the cooperative cathedral of middle-class British retail, the company whose "Never Knowingly Undersold" promise was practically a national institution — was forced to suspend its staff bonus and scrap that very pledge. The entire department-store model that had defined British retailing for a century was dying. And yet here is a company that sells the most boring products imaginable — duvets, cushions, curtain poles, scatter rugs, kitchen utensils — out of giant sheds on the edges of provincial towns, and it has done nothing but grow.

So what is the secret? The lazy answer is "they're cheap." But cheap is not a strategy; cheap is a race to the bottom that Amazon, the Chinese platforms, and a thousand discounters will always win. The real Dunelm story is far stranger and far more interesting than discount retail. It is a story about a frugal family that listed on the stock market but never really let go of the wheel. It is a story about a £8.5 million corporate heist that bought one of Britain's most expensive e-commerce technology stacks for pennies on the pound. It is a story about a quietly brilliant manufacturing operation hidden inside a curtain shop, and a portfolio of heritage brands bought for almost nothing and squeezed for margin. And it is, most recently, a story about a generational handoff — from the founding family to a digital-native chief executive poached from one of Britain's biggest supermarkets.

This is the anatomy of one of the highest-quality, most underrated retail operators in the Western world. We'll travel from that Leicester market stall to an out-of-town superstore revolution, through a stock-market listing that minted a family fortune, into the audacious 2016 acquisition that gave Dunelm its digital engine, inside the high-margin businesses most investors never notice, and finally into the boardroom where the Adderley family — still sitting on roughly a third of the company — has just handed the keys to a new chief executive named Clodagh Moriarty. Let's get into it.

II. The Leicester Stall and the Market DNA

To understand Dunelm, you have to understand the world that made it. Leicester in the late 1970s was a textile town in slow decline. The hosiery and knitwear mills that had clothed the Empire were being undercut by cheap imports, and the warehouses of the East Midlands were stuffed with overruns, off-cuts, and "seconds" — perfectly serviceable fabric that, for one reason or another, couldn't be sold at full price through the proper channels. Bill and Jean Adderley looked at that glut of cheap textiles and saw not a problem but an arbitrage.3

The genius of the original Dunelm pitch — the name came from "Dunholme," a nod to the family's roots — was that it solved a real problem for real people. A ready-made pair of curtains from a department store was an expensive, intimidating purchase. The Adderleys took the same product, stripped out the markup, and sold it off a market stall to the kind of customer the department stores barely noticed: the working family furnishing a council house or a starter home, who wanted their front room to look respectable without taking out a loan to do it. The first stall did well enough that they took a second, then a third, and by the early 1980s Dunelm had graduated from market pitches to small high-street shops.

But the high street was never the natural home for this business, and here we arrive at the first cultural trait that still runs through Dunelm's DNA today: an almost pathological frugality. The Adderleys ran the operation the way you run a market stall even after it stopped being one — count every penny, turn the stock as fast as humanly possible, never get caught holding inventory you have to mark down, and treat rent as the enemy. In retail, gross margin gets the headlines, but it's stock turn and markdown discipline that quietly determine whether you live or die. A business that sells its inventory many times a year at full price will crush a business that sells fewer times and discounts the rest, even if the second one charges higher prices. The Adderleys understood this in their bones. They called it, in later years, "commercial grip," and it is not an exaggeration to say it is the single most important inheritance the modern company carries from its founders.

The second defining move came in 1991, and it was a quiet revolution. Dunelm opened its first out-of-town superstore in Rotherham — a big, cheap, no-frills warehouse on a retail park, miles from the expensive high street.3 To appreciate why this mattered, you have to think about the economics of retail space. A high-street shop is small, dear, and constrained; you pay a fortune in rent per square foot, and you can only stock so much. An out-of-town shed is enormous, cheap per square foot, has free parking, and lets you put the entire range — every curtain, every duvet, every cushion — under one roof where the customer can touch it, compare it, and load it into the car. For a category like homewares, where people genuinely want to feel the fabric and see the colour in real light, the superstore format was almost unfairly well-suited. It gave Dunelm scale, low occupancy costs, and a shopping experience the department stores couldn't match without bulldozing their flagship buildings.

By the mid-1990s the formula was proven, and the founders did something many family businesses never manage: they got out of the way at the right moment. In 1996, Bill and Jean's son, Will Adderley, took over day-to-day running of the business at the age of just 25.3 Will was not a flashy retail showman. He was, by all accounts, a details man — a operator obsessed with systems, ranges, and the relentless rollout of the superstore model across the country. Under his hand, Dunelm institutionalised the family's lean ethos and turned a regional chain into a national one, opening superstore after superstore across the Midlands, the North, and eventually the whole of Britain. The market-stall instincts — value first, stock turn above all, rent as the enemy — were now baked into a scalable operating machine. The next question was how to fund the expansion and what to do with the value the family had created. The answer would take Dunelm to the London Stock Exchange.

III. Going Public and the Master-Brand Playbook

On the morning of October 4, 2006, Dunelm rang the bell at the London Stock Exchange. The market-stall curtain business that Bill and Jean Adderley had started with a £12 weekly pitch fee floated as a public company valued at roughly £340 million.3 For a family that had spent a quarter of a century counting pennies in Leicester, it was a staggering validation. But the most revealing thing about the IPO was not the valuation — it was the structure. The Adderleys sold only a slice. They kept the overwhelming majority of the shares, and they kept control.4

This was a deliberate and, in hindsight, deeply consequential choice. A family that retains a controlling stake after a flotation is making a statement about time horizon. Public markets are a machine for converting long-term businesses into quarterly anxiety; the pressure to hit the next earnings number, to chase a fashionable acquisition, to financial-engineer the share price, is relentless. By keeping their hands firmly on the tiller, the Adderleys insulated Dunelm from that pressure. They could keep running the business with the patience of owners rather than the nervousness of hired managers — opening stores when the economics made sense, not when an analyst wanted to see a growth story, and saying no to the kind of empire-building deals that have destroyed so much shareholder value in retail. We'll see the fruits of that discipline again and again.

With public-market capital behind it, Dunelm now made the strategic move that would define its product economics for the next two decades. In 2008, it bought the worldwide intellectual-property rights to Dorma — a heritage British bedding brand with genuine pedigree in luxury sheets and bedlinen — for around £5 million.3 On the surface this looked like a minor bolt-on. In reality it was the opening move in a playbook that Dunelm has run, with variations, ever since.

Here is the logic, and it's worth slowing down on because it's the engine of Dunelm's famous margins. Most retailers are, at bottom, distributors. They buy branded products from manufacturers at wholesale, mark them up, and sell them on. The problem is that the brand owner captures most of the value and dictates the price, leaving the retailer fighting for a thin slice of margin against every other shop selling the identical item. When Dunelm bought Dorma outright, it flipped that relationship. Instead of being a distributor of someone else's brand, it became the owner. It brought Dorma's design in-house, controlled the entire supply chain, and — crucially — sold the brand exclusively through its own stores. Nobody else could stock Dorma. That exclusivity did three things at once: it gave shoppers a reason to choose Dunelm over a rival, it raised the average value of each item in the basket because a "brand" commands more than a nameless equivalent, and it captured the manufacturer's margin and the retailer's margin in a single business. You buy the cow instead of paying for the milk, and then you're the only shop in town that sells beef.

The Dorma deal worked so well that Dunelm simply ran it again. In 2015 it acquired Fogarty, a specialist in "filled" bedding — pillows, duvets, the unglamorous but enormous-volume heart of any bedding business.3 Same logic, different category. Filled bedding is something every household buys and replaces; owning the leading brand in it gave Dunelm control over one of its highest-turnover product lines, from design through to the shelf. Over time this brand-ownership strategy would expand until the great majority of everything Dunelm sells carries one of its own labels — a structural source of margin we'll return to in detail.

Somewhere in the middle of all this, a quiet milestone passed that captured how far the curtain stall had come. By around 2012, Dunelm had overtaken John Lewis to become the largest specialist retailer of home furnishings in the UK.3 Think about what that meant. A no-frills value chain selling out of retail-park sheds had just dethroned the most prestigious name in British middle-class retailing in its own core category. It was the clearest possible proof that the low-overhead, own-brand, value-specialist model was not merely cheaper than the department-store model — it was structurally superior. The department stores carried enormous fixed costs, sprawling ranges, and city-centre rents; Dunelm carried cheap space, a focused range, and brands it owned outright. In a war of attrition, the structure wins.

But for all its physical strength, the Dunelm of the mid-2010s had a glaring weakness, and Will Adderley knew it. The world was going online, and Dunelm was a digital laggard. Solving that problem would require either years of painful, expensive in-house development — or one of the most opportunistic acquisitions in modern British retail history.

IV. The Great Pre-Pack Heist

By 2016, Dunelm had a problem that money alone couldn't quickly fix. It was a physical juggernaut — hundreds of superstores, a dominant share of the UK home market — but online it was an also-ran. E-commerce accounted for well under a tenth of sales, and the gap between where Dunelm was and where retail was heading widened by the month.3 Building a modern online business is not as simple as putting up a website. It means a transactional platform that can handle millions of customers, an inventory system that knows in real time what's in every store and warehouse, a delivery operation — and for a company that sells wardrobes, sofas, and beds, that last part is brutal. Two-man heavy-furniture delivery, where a crew carries a flat-pack wardrobe up three flights and into a bedroom, is one of the hardest, most capital-intensive logistics problems in retail. Building all of that from scratch would have cost tens of millions of pounds and taken years Dunelm didn't have.

And then, as if on cue, a gift fell into Dunelm's lap — though it arrived disguised as somebody else's catastrophe.

The somebody else was WS Group, the parent of three online brands: Worldstores, a sprawling home-and-garden marketplace; Achica, a members-only flash-sale site for furniture and homewares; and Kiddicare, a baby-products retailer. On paper WS Group was substantial, turning over around £100 million a year. The trouble was that it was haemorrhaging cash. It was the classic mid-2010s e-commerce story: a business that had raised mountains of venture capital, spent it building genuinely sophisticated technology, and then discovered that growth without profit is just an expensive way to go bankrupt. Goldman Sachs and a roster of other blue-chip backers had poured well over £30 million into WS Group, and a large chunk of that money had gone into exactly the things Dunelm desperately needed: a state-of-the-art proprietary e-commerce platform and a purpose-built two-man heavy-furniture delivery network that the company had developed under the internal name of its "Fleet" project.

Here is the brutal beauty of what happened next. In November 2016, WS Group ran out of road and was pushed into a "pre-pack" administration. For readers who haven't encountered the term, a pre-pack is a peculiarly British insolvency mechanism, and understanding it is the key to the whole deal. In a normal administration, a failing company is put into the hands of an insolvency practitioner who tries to keep it running while finding a buyer — a slow, value-destroying process during which suppliers flee and customers vanish. In a pre-pack, the sale is negotiated and agreed in advance, in secret, and executed the instant the company formally enters administration. The business changes hands in a single, pre-arranged transaction, leaving the old debts and liabilities behind in the husk of the failed company. It is legal, it is controversial — critics argue it lets buyers cherry-pick the good bits while creditors eat the losses — and for an opportunistic, cash-rich acquirer, it is the closest thing in business to a perfectly legal heist.

Dunelm was that acquirer. When WS Group entered administration, Dunelm stepped in and bought the entire business and its assets — the technology, the delivery network, the brands, the lot — out of administration for just £8.5 million in cash.[^5] Let that number sink in. A technology and logistics platform that venture capitalists had spent the better part of £30 million building was acquired for less than a third of what it cost to create, with all the loss-making baggage stripped away in the insolvency.

The headline price, though, understates the true outlay, and it's worth being precise because the cleverness is in the details. On top of the £8.5 million purchase price, Dunelm injected roughly £15 million of working capital to keep the acquired operations running and paid around £3 million in transaction fees, bringing the all-in cost to somewhere near £26.5 million.[^5] Even at that fuller figure, the maths is extraordinary. Against WS Group's roughly £100 million of sales, Dunelm paid an all-in multiple of about a quarter of one year's revenue for a business whose underlying technology had cost its previous owners nearly double that to build. In a world where loss-making e-commerce platforms routinely changed hands for multiples of revenue, Dunelm bought one for a fraction of book cost.

But the price is only half the story. The genius was in what Dunelm did with the pieces. It had no interest in running a baby-products chain or a flash-sale website for their own sake; it wanted the engine. So it ruthlessly pruned. The non-core Achica flash-sale brand was sold off to BrandAlley in 2018.3 Kiddicare was wound down and integrated. And then came the real prize: Dunelm took its own entire online operation, Dunelm.com, and rebuilt it on top of Worldstores' proprietary technology platform. The acquired tech stack didn't sit beside Dunelm's business — it became Dunelm's business, the digital nervous system of the whole company.

This is the move that changed Dunelm's trajectory, and it's the first great lesson of the whole story. By buying distressed digital assets for their underlying infrastructure rather than their failing brands, Dunelm leapfrogged years of in-house IT development in a single transaction. Overnight, it acquired the capability to do next-day delivery, click-and-collect, automated inventory management across stores and warehouses, and — through the Fleet network — the ability to deliver heavy furniture into people's homes. It plugged a multi-channel operating system into a business that had been, weeks earlier, a digital laggard. Will Adderley had found a way to buy time, and in retail, time is the one thing you can never manufacture. The full payoff for that foresight, however, wouldn't become visible until the entire country was ordered to stay home.

V. The Covid Crucible

In March 2020, the British government did something no peacetime administration had ever done: it ordered every non-essential shop in the country to close its doors. For a retailer whose entire identity was built around enormous physical stores where customers came to touch the fabric and feel the cushions, this was, on its face, an extinction-level event. Dunelm's 170-plus superstores went dark overnight. The single channel that had carried the business from a market stall to market leadership was, with no warning, simply switched off.

This was the stress test, and it's the kind of moment that separates companies that got lucky from companies that built something real. A Dunelm that had still been a digital laggard in 2020 — a Dunelm that had never made the Worldstores acquisition — would have been in genuine peril, with its sales channel closed and no meaningful way to reach customers. Instead, the foresight of 2016 paid off in a way that even Will Adderley could not have fully anticipated when he bought a bankrupt furniture website four years earlier.

Because the technology was already there, Dunelm could pivot almost instantly. It launched a nationwide click-and-collect service in a matter of days, turning its shuttered stores into makeshift fulfilment hubs where customers could order online and pick up from the car park. It scaled home delivery dramatically, leaning on the very heavy-furniture network it had acquired out of administration. The platform that had been built with somebody else's venture capital, and bought for a song, was suddenly the thing keeping the entire company alive. While pure-play online rivals strained against the limits of their logistics and high-street competitors sat locked out of their own stores entirely, Dunelm had both the digital front end and the fulfilment muscle to keep selling.

The results were dramatic. Digital sales, which had been a single-digit afterthought just a few years earlier, surged to more than 40% of the business at the peak of the pandemic disruption. More importantly, Dunelm didn't merely survive the crisis — it used it to take share. With many competitors hobbled, and with locked-down households suddenly pouring money and attention into the homes they were now spending every waking hour inside, Dunelm captured customers it might otherwise never have reached. The pandemic, which should have been the curtain stall's funeral, instead became its coming-of-age as a genuine multi-channel retailer.

There is a deeper lesson here for investors, and it's about the nature of resilience. The Worldstores deal looked, in 2016, like a clever piece of opportunistic capital allocation — a bargain, a bit of arbitrage. What Covid revealed was that it had also been a profound act of risk reduction. By building a second channel before it was forced to, Dunelm had inadvertently bought itself an insurance policy against the most extreme retail shock in living memory. The best capital-allocation decisions often look like value plays at the time and only later reveal themselves as existential hedges. With its multi-channel model now battle-tested and its market share enlarged, Dunelm emerged from the pandemic stronger than it went in — and ready to lean harder into the parts of its business that the casual observer never sees.

VI. Inside the Hidden Businesses

Walk into a Dunelm superstore and your eye goes to the obvious things: walls of cushions, stacks of duvets, aisles of crockery and curtain poles. What you don't see — what almost no shopper or even many investors register — is that the most interesting and most profitable parts of Dunelm are hiding in plain sight. There are two of them, and together they explain why this company earns margins that the rest of the retail world can only envy.

The first hidden business sits behind an unassuming desk near the curtain section, where a member of staff helps a customer choose fabric and takes the measurements of their windows. This is Made to Measure — Dunelm's bespoke, custom-made curtains, blinds, and shutters service — and it is a small masterpiece of business design. In the 2025 financial year, Made to Measure grew by an extraordinary 33%, making it one of the fastest-growing parts of the entire company.1 To understand why management is so excited about it, you have to look at the economics, which are close to perfect.

Consider how a normal retail product works. Dunelm buys inventory, ships it, warehouses it, and puts it on a shelf, where it sits — tying up cash and risking obsolescence — until someone buys it, and even then the customer might return it. Now consider a made-to-measure curtain. The customer chooses the fabric and the dimensions, pays up front, and only then is the product manufactured, cut precisely to the measurements of their specific windows. Think about what that does to the economics. There is no inventory risk, because nothing is made until it's sold. There is no markdown risk, because a curtain cut to fit one family's bay window is worthless to anyone else and so never needs discounting. And because the customer pays before the product exists, the business runs on negative working capital — Dunelm collects the cash before it spends a penny making the goods. It is, in effect, a business that customers finance themselves.

The margins on all this are exceptional, and the reason is the second piece of the puzzle: Dunelm doesn't buy these curtains and blinds from a supplier — it makes them itself. The company owns and operates a dedicated curtain and blind manufacturing facility in Leicester, the same city where Jean Adderley once sold curtain "seconds" off a stall, and it has added a purpose-built facility to make custom shutters.1 This vertical integration cuts out every middleman between the fabric and the customer's window, so the margin that would normally be shared across a manufacturer, a wholesaler, and a retailer is captured in a single business.

And here is the part that should make a long-term investor sit up. This is a business that the great low-cost disruptors of global retail simply cannot touch. The likes of 拼多多 Pinduoduo — the parent of Temu — and 希音 Shein have rewired the economics of cheap consumer goods by connecting Chinese factories directly to Western doorsteps, and they are a genuine threat to anyone selling commodity homewares on price. But a made-to-measure curtain is not a commodity that can be shipped in bulk from a distant warehouse. It requires a local human to advise the customer, to measure the windows accurately, to manufacture to bespoke dimensions, and often to fit the finished product. It is local, it is service-intensive, and it is fundamentally a physical-presence business. The very things that make it operationally hard are the things that make it defensible. No app sliding products across an ocean can replicate a person standing in your living room with a tape measure.

The second hidden business is less a single department than a quiet fact about everything on the shelves: the overwhelming majority of what Dunelm sells, more than 70% of its total range, consists of its own proprietary, own-brand products.1 This is the grown-up, company-wide version of the Dorma and Fogarty playbook we saw earlier. Most of those cushions and duvets and dinner plates aren't third-party brands that Dunelm distributes; they're Dunelm's own labels, designed in-house and made to its specification.

The strategic leverage this provides is enormous, and it is the single most important reason Dunelm sustains a gross margin of 52.4% — a figure that improved further in its most recent year and stands far above what a conventional reseller of branded goods could ever achieve.1 When you own the brand and control the design, you capture the manufacturer's margin as well as the retailer's, exactly as we saw with Dorma. But there's a second, subtler benefit that matters enormously in an inflationary world: pricing and supply-chain control. A retailer that distributes other people's brands is at the mercy of those brand owners' price increases. A retailer that designs its own products can re-engineer them, switch suppliers, tweak materials, and manage costs directly, insulating its margins from external inflation in a way a pure reseller never can. Own-brand isn't just a margin story; it's a control story, and control is what lets Dunelm hold the line on price when its costs rise.

These two hidden businesses — bespoke manufacturing and pervasive own-brand — are the quiet machinery beneath the value-retail surface. They're also a useful corrective to the lazy view of Dunelm as "just a cheap homewares shop." The cheap homewares are the front door; the margin and the moat are in the rooms behind it. With that machinery humming, the question for management became what to do with all the cash it generated — and how to keep growing a company that already dominated its home market.

VII. Modern Capital Deployment and Strategic M&A

By the mid-2020s, Dunelm faced the pleasant problem of the genuinely dominant company: it was the clear leader in its home market, throwing off more cash than it could sensibly reinvest in its core business, and it needed new avenues for growth that wouldn't compromise its discipline. The way it answered that question in 2024 and 2025 tells you almost everything about how this management team thinks — patient, opportunistic, and allergic to overpaying.

The first move was geographic, and it was the first time in Dunelm's history that it planted a physical flag outside the United Kingdom. In November 2024, Dunelm acquired Homefocus Group, an Irish retailer trading as Home Focus at Hickeys, picking up 13 stores across the Republic of Ireland — six of them in Dublin — along with an online business.56 Ireland was a shrewd choice for a first overseas step. It shares a language, broadly similar consumer tastes, and a retail culture close enough to Britain's that Dunelm's range and brand could travel without wholesale reinvention, yet it's a distinct market where Dunelm had no presence to cannibalise.

What's revealing is the format. The Hickeys stores were small — generally under 10,000 square feet — and service-oriented, a world away from Dunelm's vast British sheds.6 Rather than trying to airlift the giant superstore model into a new country, Dunelm used the existing smaller footprints as a low-risk way to introduce Irish consumers to its core value-homewares proposition and to learn the market before committing serious capital. It was a beachhead, in the truest sense: a small, defensible foothold from which to expand. And expand it did. By October 2025, Dunelm had completed the rebranding of all 13 stores to the Dunelm name, converting its acquired foothold into a genuine Dunelm presence in a new country within a year of the deal.7 For a company that had spent its entire life as a purely British operator, the smooth, fast integration of an international beachhead was a meaningful proof point.

The second move was stranger and, in its way, more clever. In April 2025, Dunelm acquired the intellectual property and design archive of Designers Guild — one of the most respected luxury names in global interior design, founded by the formidable Tricia Guild in 1970 and known for bold, painterly fabrics and wallpapers that sit at the opposite end of the price spectrum from Dunelm's everyday value range.8 The price was not disclosed, but the structure was reported to involve Dunelm injecting around £10 million of cash, partly to repay director loans and stabilise the business.8

On the surface, a value retailer buying a luxury design house looks like a category error — the kind of vanity acquisition that destroys value. But look at how the deal was structured and you see the same disciplined Dunelm mind at work. This was not a straightforward takeover; it was a "license-back" arrangement. Dunelm took ownership of the thing it actually wanted — the brand and the vast, decades-deep design archive — which it can mine to create exclusive, mass-premium product lines for its own stores, raising the ceiling of what a Dunelm shopper can buy. But it then licensed the Designers Guild brand back to the company's existing management, led by Tricia Guild herself, so they could carry on running their independent luxury business as before.8 Dunelm got the asset it valued — the IP and the archive — without having to take on the unfamiliar, low-margin headache of running luxury boutiques.

And the price, set against the prize, was vintage Dunelm. A net injection of roughly £10 million against a brand reportedly turning over around £40 million in sales implies an acquisition multiple of about a quarter of one year's revenue.8 That is the same fractional multiple Dunelm paid for the Worldstores technology platform a decade earlier — and it is a fraction of the 1.5-to-3-times-sales multiples that globally recognised premium consumer brands typically command. Once again, Dunelm bought a valuable, hard-to-replicate asset from a position of strength, at a price set by the seller's distress rather than the asset's true worth. It is the Dorma playbook, the Worldstores playbook, and the Hickeys playbook, all rhyming: own the IP, structure the deal cleverly, and never, ever overpay. The discipline that produced these deals is not an accident of one clever executive — it is cultural, and that culture was about to be tested by the biggest leadership change in the company's history.

VIII. The Sainsbury's Handoff

On October 1, 2025, a quiet but profound transition took place at the top of Dunelm. Nick Wilkinson, who had run the company as chief executive for seven highly successful years — overseeing the Worldstores integration's maturation, the Covid surge, the Irish entry, and the Designers Guild deal — stepped down. In his place arrived someone who had never sold a curtain in her life, but who had spent fifteen years inside the engine room of one of Britain's biggest retailers: Clodagh Moriarty.[^10]1

The choice of successor was itself a strategic statement. When a founder-influenced retailer reaches for a leader, it can pick a safe internal continuity candidate or it can pick someone who signals where it wants to go next. By choosing Moriarty, Dunelm's board signalled, unmistakably, that the next chapter would be about digital scale and technology — the very capabilities that the Worldstores deal had bolted on a decade earlier, now to be driven by a leader whose entire career had been built on them.

So who is Clodagh Moriarty? She is, to start with the basics, an Irish national — a nice symmetry given Dunelm's freshly planted Irish beachhead — with an INSEAD MBA and an early career at the elite strategy consultancy Bain & Company, the kind of pedigree that produces rigorous, analytically minded operators.[^10] But the heart of her CV is the decade and a half she spent at J Sainsbury plc, where she rose to become Chief Retail and Technology Officer. In that role she oversaw an enormous canvas: digital and technology across the Sainsbury's empire, store operations, and the integration of the Argos general-merchandise business and the Nectar loyalty programme.[^10] This is a leader who has wrestled with multi-channel retail at a scale far larger than Dunelm's, who understands loyalty data and e-commerce logistics in her bones, and who has run technology not as a support function but as a core driver of a retail business. For a company that has decided its future is about pushing digital from a large minority toward half the business and beyond, it is hard to imagine a more on-the-nose hire.

The structure of Moriarty's pay package is worth examining, because executive compensation is where a board reveals what it actually wants. Her base salary was set at £825,000, positioning her around the median for a FTSE 250 chief executive — neither lavish nor stingy.1 On top of that sits an annual bonus worth up to 150% of salary and long-term incentive awards worth up to 225% of salary, the usual architecture of modern executive pay.1 The interesting part is what those incentives are tied to. The performance metrics are heavily weighted toward earnings per share growth — reportedly around 80% — with the remaining fifth tied to specific sustainability targets such as reducing plastic packaging, sourcing responsibly grown cotton, and launching circular take-back services for old textiles.1 An incentive scheme that is four-fifths driven by EPS is a board telling its chief executive, in the bluntest language available, that the job is to grow the actual per-share earnings of the company — not revenue for its own sake, not store count, not vanity metrics, but the bottom-line value that accrues to each share. It is precisely the kind of ownership-minded yardstick you'd expect from a company where the founding family still owns a huge slug of the stock.

That alignment is reinforced by the shareholding requirements. Moriarty is required to build and hold shares worth at least 200% of her salary, and to smooth her transition she received roughly 550,000 buyout shares to compensate for the Sainsbury's incentives she forfeited by leaving — with the catch that she must retain two-thirds of all vested shares for as long as she works at Dunelm.1 The message is consistent from top to bottom: this is a company that wants its leaders to think and feel like owners, because its largest owners are still very much in the room.

Which brings us to the family. The most important fact about Dunelm's governance is that, even after going public two decades ago and even after handing operational control to a series of external chief executives, the Adderleys never let go. Sir Will Adderley — the son who took the reins in 1996, now knighted — remains on the board as Executive Deputy Chairman, and through the family's WA Capital vehicle the Adderleys own around 32.8% of the company.14 That stake survived a notable manoeuvre in September 2024, when WA Capital placed 4.9% of the company's shares, raising roughly £114 million — a partial monetisation that, far from signalling a retreat, simply trimmed an overwhelming holding to a merely dominant one while putting some liquidity in family hands.4

The division of labour between Adderley and Moriarty captures the central balancing act of the modern Dunelm. Will Adderley's role is to be the keeper of the flame — to safeguard the frugal, customer-first, commercial-grip culture that his parents built on a market stall and that he spent his career institutionalising. Moriarty's role is to drive the digital and operational transformation that will carry the business into its next phase. It is the family-executive balance in its purest form: world-class outside management running the company day to day, with a deeply invested founding family in the boardroom acting as the guardian of strategy and culture and the ultimate check on capital discipline. Rounding out the senior team are chief financial officer Karen Witts, who joined in 2022 and brought heavyweight FTSE finance experience, and chairman Alison Brittain, the former chief executive of FTSE 100 hospitality group Whitbread, who took the chair in 2023.1 It is, by any measure, an unusually credentialed board for a company that still, at heart, sells duvets out of sheds.

With the leadership settled and the strategy set, the question for an investor becomes the analytical one: just how durable is Dunelm's advantage, and where are the cracks?

IX. The War-Game: Powers, Forces, and the Shape of the Moat

Strip away the narrative and look at Dunelm as a competitive system, and the durability of its position comes into focus. The cleanest way to do this is through two frameworks long-term investors lean on — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — not as a box-ticking exercise but as a way to locate exactly where Dunelm's advantage lives and where it's vulnerable.

Start with the Powers. The most obvious is scale economies. As the largest homewares retailer in the UK, Dunelm buys in volumes no domestic competitor can match, which gives it superior terms from its suppliers and the ability to design and source own-brand products at costs a smaller rival simply cannot reach. Scale also transforms the economics of the expensive bits of modern retail — the proprietary technology platform, the two-man delivery fleet, the national logistics network. Those are largely fixed costs, and spreading them across £1.77 billion of sales means each individual order carries a far smaller slice of the overhead than it would at a smaller competitor.1 The bigger Dunelm gets, the cheaper each unit of its operation becomes, and that is the textbook definition of a scale advantage.

The most interesting Power, though, is counter-positioning — the situation where an incumbent literally cannot copy a challenger's model without damaging its own existing business. Dunelm enjoys this in two directions at once. Against the traditional department stores and high-street retailers, its out-of-town, low-rent, big-shed format is something they cannot replicate, because doing so would mean abandoning the expensive city-centre flagships that define them; John Lewis cannot become Dunelm without ceasing to be John Lewis. And against the pure online players — the Wayfairs of the world, or a minimalist design retailer like 無印良品 MUJI — Dunelm offers exactly what they structurally lack: physical stores where you can touch the product, click-and-collect convenience, and local services like measuring, fitting, and assembly. An online-only competitor can't match the physical touch-and-feel without building a store estate and abandoning the asset-light model that is its entire reason for existing. Dunelm sits in a sweet spot that hurts to attack from either side.

The third Power is what Helmer calls a cornered resource — a unique asset a competitor can't acquire on equal terms. Here it's the combination of the vertically integrated Leicester manufacturing for made-to-measure products and the exclusive ownership of heritage brands like Dorma, Fogarty, and now the Designers Guild archive. A rival can build a curtain shop, but it can't easily build Dunelm's bespoke-manufacturing capability or buy brands that Dunelm already owns outright and sells exclusively. Layered on top is the fourth and gentlest Power — brand — the decades of accumulated trust that have made Dunelm the default name for value homewares in British households. It's a real asset, though a more modest one; trust in a value retailer is durable but rarely commands a price premium.

Now run the Five Forces, which test the attractiveness of the industry Dunelm operates in. Competitive rivalry is genuinely high — IKEA, Next's enormous home division, Wayfair, the supermarkets' homeware ranges, and a long tail of specialists all compete for the British shopper — but Dunelm owns the value-specialist niche more completely than any rival owns its own patch. The threat of new entrants, by contrast, is low: to challenge Dunelm head-on, a newcomer would need to replicate a national estate of 200-plus superstores, a proprietary logistics and delivery network, bespoke factories, and a custom-built technology stack, a combination requiring prohibitive capital and years of execution. The threat of substitutes is also low in the deepest sense — people will always need bedding, towels, and curtains; these are household necessities, not discretionary fashion that can simply go out of style.

The two forces worth watching most closely are the bargaining powers. Buyer power is moderate: individual shoppers face low switching costs and can defect to a cheaper rival for a commodity cushion, which is a real constraint — but the made-to-measure service and the exclusive own-brands raise switching costs and build retention precisely where it matters. Supplier power is low, and this is one of Dunelm's quiet structural strengths: because of its scale, Dunelm is frequently the single largest customer of the factories it buys from, which inverts the usual relationship and hands Dunelm the superior negotiating position. A supplier that depends on Dunelm for a large share of its order book is in no position to dictate terms.

Put it all together and the picture is of a business with a genuinely multi-layered moat — scale, counter-positioning from both flanks, a cornered manufacturing-and-brand resource, and an industry structure that favours the entrenched incumbent. It is not invulnerable; the buyer-power and rivalry forces are live, and we'll come to the threats. But the architecture of the advantage is unusually well-built. The practical question for an investor is how that architecture translates into the handful of numbers actually worth watching.

X. The Playbook and the Numbers That Matter

If you distil the Dunelm story into transferable lessons, four stand out — and each is really a window into how this particular management mind works.

The first is the pre-pack technology arbitrage: the willingness to buy distressed assets not for their failing brands but for the valuable, heavily capitalised infrastructure buried inside them. The Worldstores deal is the canonical example, but the pattern of mind — separating the asset you want from the liabilities you don't, and letting someone else's distress set your purchase price — runs through everything Dunelm buys. The second is own the IP, don't just distribute it: the discipline of acquiring high-equity consumer brands and pulling design in-house to capture the manufacturer's margin on top of the retailer's, the mechanism that more than anything else produces that 52.4% gross margin.1

The third lesson is the one that matters most to a long-term shareholder: Dunelm is, underneath the retail story, a capital-return machine. Its capital policy is almost monastic in its discipline. It reinvests what the business genuinely needs, maintains a deliberately conservative balance sheet — management targets net debt of around 0.2 times earnings, and the company has operated close to that, carrying modest leverage rather than the aggressive debt loads that have sunk so many leveraged retailers — and then returns essentially all the surplus cash to shareholders.1 It does this through a steady ordinary dividend topped up by regular special dividends whenever the cash builds beyond what the business needs, including a 35p special dividend declared with its FY25 results, matching the prior year's special payout and lifting the total ordinary-plus-special distribution to 79.5p per share, with a further special distribution declared alongside its early-2026 interim results.1[^11] The philosophy is the antithesis of empire-building: grow the core sensibly, refuse to overpay for anything, and hand the excess back rather than torch it on diversification. In a sector littered with retailers who borrowed heavily and diversified into oblivion, Dunelm's refusal to do either is itself a competitive advantage.

The fourth lesson is the family-executive balance we've already seen in action — the demonstration that a company can hand day-to-day control to world-class outside managers like Moriarty while keeping the founding family deeply involved as the guardian of culture and the ultimate enforcer of capital discipline. The 32.8% Adderley stake is not a relic; it is the mechanism that keeps the whole system honest.4

So what should an investor actually watch? Resist the temptation to track everything; for Dunelm, two or three numbers carry most of the signal. The first is gross margin. At 52.4% it is the single clearest expression of the entire own-brand, vertical-integration thesis; if that margin holds or expands, the moat is intact and pricing power is real, and if it erodes materially, it is the first sign that the low-cost disruptors or input-cost inflation are getting through the defences.1 The second is the mix and growth of the high-margin specialist businesses — above all the Made to Measure operation, which grew 33% in FY25 and which embodies the negative-working-capital, zero-inventory-risk economics that the disruptors cannot copy.1 As long as that engine keeps compounding, Dunelm is moving toward its highest-quality revenue, not away from it. The third, for those who want a single proxy for whether the digital transformation is working, is the digital share of sales — the metric that will tell you whether Moriarty is succeeding in pushing the business from its current large-minority online mix toward the half-and-half model the company aspires to. Those three — margin, specialist-business growth, and digital penetration — are the dials that matter. Watch them, and you are watching the thesis itself.

XI. Bull, Bear, and the Verdict of the English Home

Every quality business is a wager on the future, and Dunelm is no exception. Lay the two cases side by side.

The bull case is a story of compounding strengths. Under Clodagh Moriarty's technology-first leadership, Dunelm pushes its digital sales decisively higher — past the half-of-the-business mark — capturing the structural shift online while its physical estate, far from being a liability, becomes the click-and-collect and service backbone that pure-play rivals can't match. The Irish beachhead, having proven the format travels, becomes a template for measured international replication, opening a long runway of growth beyond a UK market Dunelm already dominates. And the high-margin specialist businesses — Made to Measure above all — keep compounding at the kind of rates that mechanically lift the whole company's margin and quality of earnings, because every pound of bespoke-curtain revenue is worth more, and carries less risk, than a pound of commodity-cushion revenue. Stack those together and you have a dominant, cash-generative, owner-aligned business with multiple independent vectors of growth and a capital-return machine handing back everything it doesn't need.

The bear case is equally coherent, and a serious investor should sit with it. The first threat is macroeconomic and largely outside management's control: Dunelm sells into the British home, and the British home is hostage to the housing market and the consumer's mood. A severe UK recession, a frozen housing market with few transactions, and stretched household budgets would all hit furniture and big-ticket homeware demand at once, because people who aren't moving house aren't buying new curtains, and people worried about their jobs defer the new sofa. Dunelm has navigated downturns before, and its value positioning is a partial hedge — in hard times, trading down to a value specialist can actually help — but it is not immune to a genuinely deep consumer slump.

The second threat is the structural one we've already flagged: the ultra-low-cost global supply-chain platforms. 希音 Shein and 拼多多 Pinduoduo's Temu have demonstrated an ability to deliver commodity goods to Western consumers at prices that defy belief, by collapsing the distance between a Chinese factory and a Western doorstep. On entry-level home décor — the scatter cushions, the cheap throws, the £4 storage baskets — they can undercut even Dunelm, and they could erode margins at the value end of the range over time. This is precisely why the made-to-measure and own-brand strategies matter so much: they are Dunelm's answer to the disruptors, the parts of the business that an app shipping boxes across an ocean cannot replicate. The bear would argue the disruptors nibble at the bottom of the range faster than the specialist businesses can grow at the top; the bull would argue Dunelm is deliberately retreating from the commoditisable and advancing into the defensible. Both can be true at once, and which dominates is the central tension in the investment case.

There are quieter risks worth naming too. A founding family controlling roughly a third of the votes is a double-edged sword — it has been the guarantor of discipline and long-term thinking, but concentrated control always carries governance considerations, and the interests of a dominant family shareholder will not always be identical to those of minority investors. The leadership transition itself, however well-credentialed the successor, is an execution risk: cultures forged on market stalls do not always survive contact with executives raised in FTSE 100 boardrooms, and the Adderley-Moriarty balance is a hypothesis still being tested. And the international expansion, promising as the Irish start has been, is unproven beyond a single small, culturally adjacent market; replicating it further afield is a different and harder problem.

Weigh it all, and what you are left with is not a verdict but a character study. Dunelm is a company that began as the humblest thing imaginable — a stall selling curtain off-cuts in a Leicester market — and that has, through nearly half a century of relentless frugality, opportunistic dealmaking, and refusal to overpay or overreach, become the quiet king of the English home. It bought its digital future out of someone else's bankruptcy for the price of a London townhouse. It hides some of the best margins in retail behind a tape measure and a curtain rail. It owns the brands it sells, makes the products it owns, finances its growth with its customers' upfront cash, and hands the surplus back to its shareholders rather than chasing the diversifications that have buried so many of its peers. And it has just placed the wheel in the hands of a technologist while the founder's son watches from the boardroom, guarding a culture that still, after all these years, runs on commercial grip. Whether that combination compounds for another decade or finally meets a disruptor it cannot out-flank is the open question. But few retailers in the Western world have built a machine this well-engineered for the world it actually lives in.

References

-

Dunelm Group plc FY25 Preliminary Results — Dunelm Group plc / London Stock Exchange, 2025-09-09 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Dunelm Group plc Share Price and Analysis — London Stock Exchange ↩

-

Dunelm Group plc Investor Relations / Corporate History — Dunelm Group plc ↩↩↩↩↩↩↩↩↩

-

Will Adderley's WA Capital sells 4.9% stake in Dunelm Group plc — Financial Times, 2024-09-12 ↩↩↩↩

-

UK's Dunelm buys Home Focus at Hickeys chain — RTÉ News, 2024-11-20 ↩

-

Dunelm acquires Home Focus at Hickeys to enter Ireland — Insight DIY, 2024-11-20 ↩↩

-

Dunelm completes integration and rebranding of Irish Hickeys stores — Home of Direct Commerce, 2025-10-15 ↩

-

Dunelm acquires Designers Guild IP and design archive — Retail Gazette, 2025-04-28 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube