Diageo: The Hangover of Premiumisation and the Drastic Dave Turnaround

I. Introduction & Episode Roadmap

Picture the scene inside Diageo's Great Marlborough Street headquarters in London on a grey morning in February 2026. In the executive suite sits a man who has been in the CEO chair for barely eight weeks, about to do something the company had not done in living memory. Sir Dave Lewis — the retailer the British press nicknamed "Drastic Dave" during his rescue of Tesco — was preparing to tell the owners of Johnnie Walker, Smirnoff, Tanqueray, Baileys, Don Julio and Guinness that their dividend was being cut in half. For a company that had raised or held its payout for decades, this was heresy. For Lewis, it was arithmetic.

How did the undisputed titan of global spirits — a business with brands so iconic that "Johnnie Walker" is practically a synonym for Scotch — end up here? A company whose shares once traded like a bond proxy for the world's rising middle class had watched its valuation slide toward ten-year lows, absorbed a multi-billion-dollar inventory crisis in Latin America, taken more than a billion dollars of write-downs on trophy acquisitions, and burned through the top of its C-suite at a rate that would embarrass a Silicon Valley startup: three chief executives in less than three years.

This is not a story about a broken brand. Diageo's liquid is as good as it ever was, and a bottle of aged Scotch remains one of the most defensible consumer products on earth. It is a story about what happens when a beautiful moat meets a brutal balance sheet — when the very economics that make premium spirits so profitable in the good years turn into an operational trap in the bad ones.

Four threads run through everything that follows. The first is the physics of premiumisation — the central alcoholic-beverage thesis of the 21st century, "drink better, not more," and what happens to a business built on it when inflation forces consumers to drink cheaper, or not at all. The second is the working-capital paradox: aging Scotch for a decade or two builds an almost impregnable barrier to entry, but it also locks billions of dollars of cash inside oak barrels that cannot be sold for years. The third is the M&A engine — the genius of the Don Julio–Bushmills swap set against the eye-watering multiple paid for Casamigos and the eventual write-down of Ryan Reynolds' Aviation Gin. And the fourth is channel visibility: the deceptively simple gap between "sell-in" (shipments to wholesalers) and "sell-out" (what consumers actually buy), a gap wide enough to hide a crisis inside a multi-billion-dollar business.

Our posture throughout is that of an independent analyst, not a cheerleader. Management says Lewis can fix this. The interesting question is not whether they say it, but what evidence supports it — and what would prove it wrong. Let us start where Diageo started: with a brewer, a lease, and a very long time horizon.

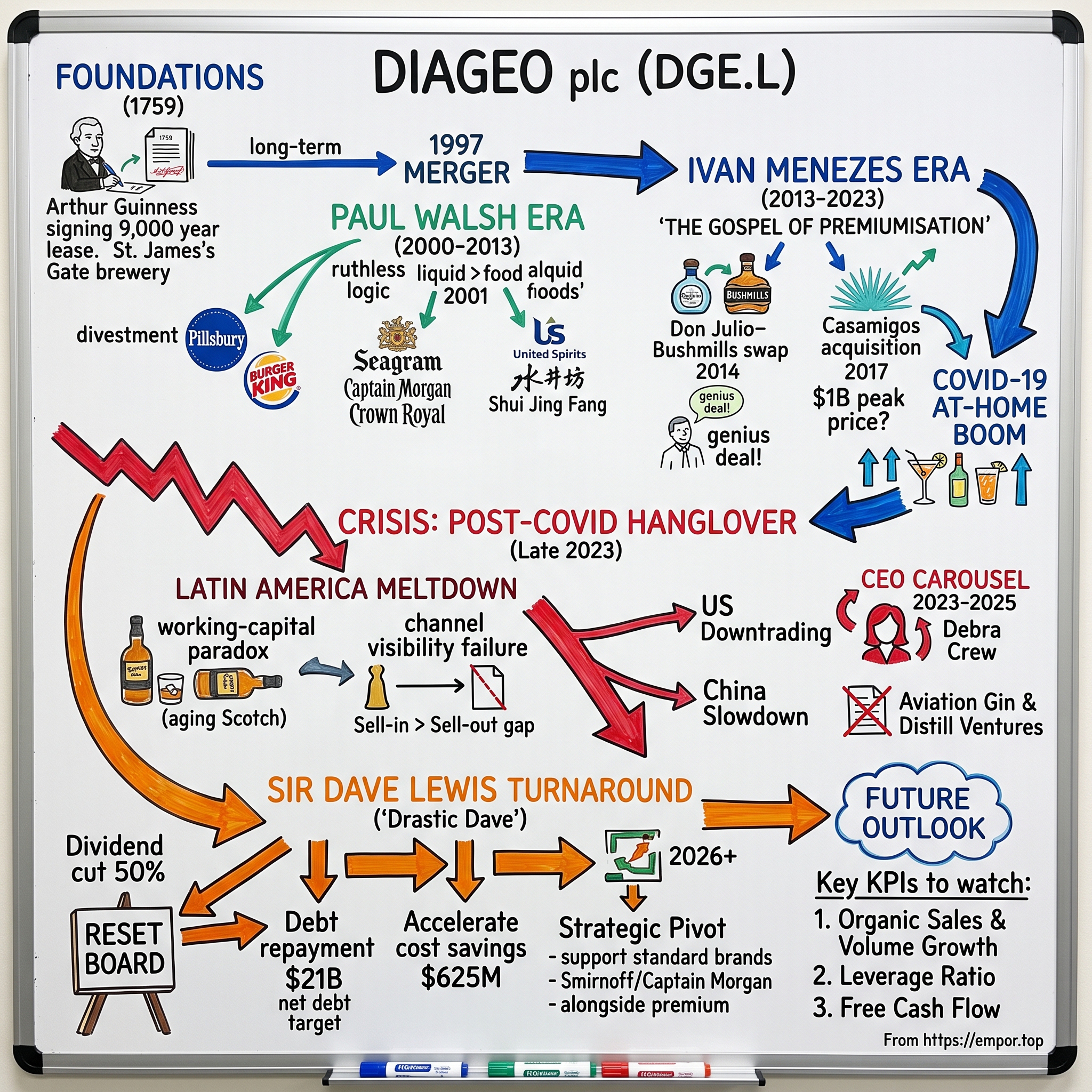

II. The Brewery and the Merger: Foundations of a Global Empire

In 1759, a 34-year-old brewer named Arthur Guinness walked into a disused, four-acre brewery at St. James's Gate in Dublin and signed a lease. Not a ten-year lease, or a fifty-year lease. A nine-thousand-year lease, at a fixed rent of £45 a year.1 It is the kind of decision that reads today either as lunatic overconfidence or as the single greatest real-estate deal in the history of alcohol — a founder so certain his black porter would outlive him by centuries that he priced the option accordingly. He was right. St. James's Gate still brews Guinness today, and that improbable act of long-termism is the spiritual DNA of the modern company: patience as a competitive weapon.

Fast-forward through two centuries of empire, war and consolidation, and by the 1990s the British drinks industry was a chessboard of sprawling conglomerates. Two of the biggest were Guinness plc — by then far more than a brewer, having absorbed the Distillers Company and its Scotch whisky treasure — and Grand Metropolitan, a hotel-to-food-to-drinks empire that owned Smirnoff vodka, J&B whisky and Baileys Irish Cream. In 1997 the two merged to create a single behemoth. The new company needed a name that belonged to no existing brand, and it landed on something almost comically grand: Diageo, stitched together from the Latin dia (day) and the Greek geo (earth) — roughly, "every day, everywhere in the world."

The merged entity was, at first, a bit of everything. Alongside the spirits sat Burger King and the Pillsbury food business — the Doughboy and the whisky under one roof. It took the arrival of Paul Walsh, who became chief executive in 2000, to impose a ruthless logic on the sprawl. Walsh, a Lancashire-born accountant by training, made a simple bet that defined Diageo for a generation: liquid is a better business than food. Premium spirits carried fatter margins, aged rather than spoiled, and enjoyed pricing power that a hamburger could only dream of. So he sold. Pillsbury went to General Mills; Burger King was offloaded to private equity. Diageo would be a "pure-play" drinks company.

Having cleared the decks, Walsh went shopping. In 2001, Diageo and rival Pernod Ricard jointly carved up the drinks empire of the collapsing French conglomerate Vivendi, buying the Seagram spirits and wine business for $8.15 billion in total — with Diageo taking the larger share, around $5 billion.2 The prize brands that flowed to Diageo were Captain Morgan rum and Crown Royal Canadian whisky, two mass-market workhorses that instantly gave the company category scale and, just as importantly, leverage over the distributors and retailers who decide which bottles sit on the shelf. Bargaining power in spirits is not won bottle by bottle; it is won by controlling so much of the back-bar that a distributor cannot afford to say no to you.

Walsh's final act was to plant flags in the markets where the next billion drinkers would emerge. Diageo took control of United Spirits, the dominant Indian liquor company, and bought into China's baijiu category through the premium producer 水井坊 Shui Jing Fang — a bet that as Asia's middle class grew richer, it would trade up from local spirits toward international brands, or at least toward premium versions of its own. These were long-dated wagers on demographics, and like Arthur Guinness's lease, they would take years to prove out. Some are still being litigated by events today. What Walsh handed to his successor was a company of unmatched scale and enviable brands — and a strategic thesis that his successor would take from a bet to a gospel.

III. The Ivan Menezes Era: The Gospel of Premiumisation (2013–2023)

When Sir Ivan Menezes took the top job in 2013, he did not so much change Diageo's strategy as canonise it. Menezes — Pune-born, IIM-Ahmedabad and Kellogg-educated, a soft-spoken operator who had run Diageo's North American business and served as chief operating officer — believed with near-religious conviction in a single idea: that the future of alcohol was not more drinking, but better drinking. "Premiumisation" became the word that Diageo's entire machine was tuned to serve.

The logic was seductive and, for a decade, largely correct. Around the world, a growing middle class was trading up — from unbranded spirits to branded, from standard to premium, from premium to super-premium. A consumer who used to buy a bottle of ordinary blended Scotch might now reach for Johnnie Walker Black; the one who bought Black might reach for Blue. Each step up the ladder carried disproportionately more margin. In an industry where volume growth is capped by biology and public health, price-mix — selling a richer blend of more expensive products — was the growth engine that mattered. Menezes reoriented marketing dollars, innovation and sales incentives toward the top of the range and toward North America, the single most profitable spirits market on earth.

Nowhere was the premiumisation thesis vindicated more spectacularly than in tequila — and nowhere was Diageo's dealmaking sharper. In late 2014, the company executed what remains one of the most value-accretive portfolio swaps in the history of spirits. It handed the venerable Bushmills Irish whiskey brand to Mexico's Casa Cuervo, and in return took 100% ownership of Don Julio, the super-premium tequila — plus a net cash payment of $408 million flowing to Diageo.3 Read that again: Diageo gave away a slow-growing category and was paid to take a fast-growing one. Bushmills was a fine brand in a sleepy corner of the market; Don Julio sat at the front of a wave that was about to become a tsunami. Trading category maturity for category momentum, and pocketing cash for the privilege, is about as good as capital allocation gets.

Then came the deal that critics could not stop talking about. In June 2017, Diageo agreed to buy Casamigos — the tequila co-founded by George Clooney and his friends — for up to $1 billion: $700 million upfront and a further $300 million tied to hitting performance targets over a decade.[^4] The howls were immediate, because on the trailing numbers the price looked absurd. Casamigos was young and small, and the headline figure implied a multiple in the region of 20 times sales, versus an industry norm closer to four to six. Was Diageo paying a billion dollars for a celebrity's dinner-party anecdote?

Here the analysis has to be honest in both directions. The earn-out structure was genuinely clever: by tying a third of the price to future performance over ten years, Diageo kept the founders financially motivated to keep the brand hot rather than cashing out and walking away — the classic failure mode of a celebrity acquisition. And commercially, Casamigos delivered, blowing past the one-million-case threshold by 2020 and becoming a genuine pillar of Diageo's tequila portfolio. For several years, the "20x" deal looked like a masterstroke. But — and this matters for what comes later — a price that is justified by permanent hyper-growth becomes a liability the moment the growth stalls. The bill for peak-cycle multiples is not paid at signing; it is paid at the next downturn.

That downturn was still years away, and before it arrived came the greatest sugar-high in the industry's modern history. When COVID-19 lockdowns shuttered bars and restaurants in 2020, the conventional wisdom was that alcohol sales would collapse. The opposite happened, at least in the premium tiers. Stuck at home, flush with stimulus cash and with nowhere to spend it, consumers turned their kitchens into cocktail bars. Demand for ultra-premium Scotch and tequila surged; people who might have nursed a cheap beer at a pub were now buying $60 bottles to mix Old Fashioneds on Zoom calls. Diageo posted double-digit organic growth and record operating margins, and premiumisation looked not merely validated but unstoppable.

It was, in hindsight, a trap dressed as a triumph. The at-home boom pulled forward demand, inflated inventories across the supply chain, and — most dangerously — convinced almost everyone that a temporary spike was a permanent step-change. Menezes's gospel had never been more popular. But the very conditions that made it look infallible were about to reverse, and the company's plumbing was not built to see it coming.

IV. Inside the Business: Segment-Level Data & Economic Drivers

Before we walk into the crisis, it is worth opening the hood and understanding what actually generates Diageo's cash — because the shape of the profit engine explains why the downturn hit where it hit. Diageo is not one business; it is a collection of very different businesses wearing a single logo, and their economics diverge more than most investors appreciate.

Start with geography. In the fiscal year ended June 2025, North America was the crown jewel, contributing roughly 40% of net sales and an even more disproportionate share of operating profit — this is the market where premium American whiskey, tequila and Crown Royal earn their fattest margins.4 Europe followed at around 24%, Asia Pacific at 18%, and Africa and the Latin America & Caribbean (LAC) region at roughly 9% each.4 The concentration matters: when North America sneezes, Diageo catches pneumonia, because no other region can carry the profit load. A business this dependent on one market's disposable income is, by construction, a leveraged bet on the American consumer.

Now slice it by category. Scotch is the single largest at about 22% of net sales, anchored by the Johnnie Walker empire; beer, driven overwhelmingly by Guinness, is around 18%; tequila (Don Julio and Casamigos) about 13%; and vodka, chiefly Smirnoff, roughly 8% — with the remaining share spread across gins, liqueurs like Baileys, rum, and the fast-growing ready-to-drink category.4 But these percentages hide wildly different underlying machines.

Consider the Scotch moat. Whisky is the ultimate delayed-gratification business. Spirit distilled today cannot legally be sold as a 12-year-old until it has spent twelve years asleep in oak; the 18-year-old you buy in 2026 was made when the iPhone was brand new. This is a textbook example of what strategist Hamilton Helmer calls a "cornered resource": no competitor, however well-funded, can conjure a genuine 15-year-old single malt in less than fifteen years. The barrier to entry is time itself. But time is also the trap. Every barrel maturing in a warehouse is cash that has been spent and cannot be recovered until the liquid is bottled and sold years later. Diageo must forecast demand more than a decade in advance and lay down inventory accordingly. Guess high and you drown in unsold whisky; guess low and you have no premium stock when demand arrives. The moat and the millstone are the same object.

Tequila runs on a different but equally unforgiving clock — an agricultural one. The blue agave plant takes seven to ten years to mature before it can be harvested for tequila. That long lead time creates a violent boom-and-bust commodity cycle: when demand runs ahead of planting, agave prices spike and margins get squeezed; when growers over-plant in response, a glut arrives years later, prices collapse, and the market floods with cheap tequila that ignites retail price wars. A brand like Casamigos, priced at the premium end, is exposed on both sides — cost pressure when agave is scarce, and pricing pressure when it is abundant and rivals undercut.

And then there is the beer exception. Guinness is, economically, the odd one out — and, lately, the quiet hero. Its operating margin is lower than a bottle of aged Scotch, but it is gloriously cash-generative because it turns over fast: brew it, ship it, drink it, repeat, with none of the decade-long capital lock-up of brown spirits. Guinness dominates the UK on-trade, has enjoyed a genuine cultural resurgence, and has extended into the fast-growing non-alcoholic segment with Guinness 0.0. In a portfolio full of slow-aging, capital-hungry assets, Guinness is the one that spins the cash register quickly — which is exactly why, as we will see, it became a strategic pawn when the balance sheet came under strain.

Put together, the picture is of a company whose greatest strengths — aged inventory, premium positioning, geographic concentration in America — are also precisely the sources of its fragility when the macro environment turns. The engine is magnificent. It is also, in the wrong conditions, a machine for trapping cash and amplifying bad news. In late 2023, the wrong conditions arrived.

V. The Post-COVID Hangover and the Latin American Meltdown

On July 5, 2023, Diageo lost its leader in the most shocking way imaginable. Sir Ivan Menezes, the architect of the premiumisation era, died suddenly following complications from surgery, at the age of 63. Just weeks earlier the board had lined up Debra Crew — a former US Army officer turned consumer-goods executive who had run PepsiCo and Reynolds American businesses before joining Diageo — as his successor. Crew was thrust into the top job under the worst possible circumstances: no honeymoon, no managed handover, inheriting a company that still looked, on the surface, to be firing on all cylinders.

The surface lasted four months. On November 10, 2023, Diageo issued a trading update that detonated the stock. Management disclosed that performance in the Latin America & Caribbean region — around a tenth of group sales — had turned "materially weaker," and that organic net sales there were now expected to fall by more than 20% in the first half of fiscal 2024.5[^7] The shares dropped roughly 14% in early London trading, wiping billions off the market value in a session.5 For a company that had spent a decade cultivating a reputation for reliability — the FTSE 100's dependable compounder — the profit warning was a credibility earthquake.

What had actually gone wrong is the analytical heart of this entire story, because it was not really about Latin America. It was about the gap between what Diageo could see and what was true. During the post-pandemic boom, Diageo kept shipping high-margin Scotch and other premium spirits into LAC wholesalers — "sell-in." Those wholesalers kept reordering, and Diageo read the reorders as a signal of healthy underlying consumer demand. But the reorders were an illusion. On the ground, high interest rates and stubborn inflation had hammered Latin American consumers, who did exactly what economically squeezed drinkers do: they downtraded, abandoning premium imported Scotch for cheaper local beer and spirits. Consumer "sell-out" had quietly rolled over months earlier.

The result was a mountain of unsold premium liquor sitting in distributor warehouses — inventory that had been booked as Diageo revenue on the way in but now had to be worked back down, throttling future shipments to a trickle. The company was, in effect, flying with a broken instrument panel: it lacked real-time visibility into what distributors were actually selling to end consumers, so it mistook a channel filling up for a market growing. When the channel finally choked, the correction was sudden and violent precisely because the warning signs had been invisible on Diageo's dashboards.

Here is where an independent read has to part company with the initial management narrative. In the immediate aftermath, the explanation leaned heavily on macro forces — inflation, rates, a tough Latin American consumer — factors outside the company's control. All of that was true. But it was not the whole truth, and arguably not the important part. Rival multinationals sold into the same Latin American economies without blowing up so spectacularly. The distinguishing failure at Diageo was internal and controllable: an over-reliance on sell-in metrics, thin real-time visibility into distributor sell-out, and inventory discipline loose enough to let the channel bloat unnoticed during the boom. Blaming the weather is easy when the roof has been leaking for months. On subsequent calls, management increasingly acknowledged the execution dimension — but the initial framing, macro-first, cost the leadership a measure of trust it would spend the next two years trying to earn back.

The deeper problem was that the LAC blow-up was not an isolated regional accident. It was the first crack in the premiumisation edifice — the first hard evidence that when the macro turns, "drink better" can flip to "drink cheaper" faster than a decade-long distribution machine can react. And the crack was about to spread to the one market Diageo could least afford to lose.

VI. The CEO Carousel and the Speculative M&A Write-downs

If Latin America was the warning shot, the following eighteen months were the body blow — because the same downtrading dynamic migrated north into the United States, the profit engine that carries the whole company. The trouble was most visible, and most poetic, in the very brands that had defined the boom. Casamigos, the celebrity tequila bought at a legendary multiple, watched its volumes come under pressure as rivals slashed prices and the American consumer, squeezed by inflation, thought twice about a premium bottle. The fragility that critics had warned about in 2017 finally showed itself: a celebrity premium commands attention on the way up, but it offers little protection when a category turns promotional and shoppers start comparing price tags.

China compounded the pain. As the Chinese economy sputtered and property-driven consumer confidence sagged, demand for imported ultra-premium Scotch weakened, and Diageo's premium baijiu brand, 水井坊 Shui Jing Fang, struggled against entrenched, state-linked national champions like 贵州茅台 Kweichow Moutai and 五粮液 Wuliangye — companies that dominate the Chinese white-spirits pantheon in a way no foreign brand can easily dislodge. Two of Diageo's biggest long-dated growth bets, India aside, were now headwinds rather than tailwinds.

The financial reckoning landed with the fiscal 2025 results, published on August 5, 2025. Reported operating profit fell 27.8%, driven by a wave of exceptional charges.4 Diageo booked roughly $1.4 billion of exceptional operating items, dominated by impairments — including about $458 million written off across its Distill Ventures incubator investments and $231 million against Aviation American Gin.4 The Aviation write-down was the symbolic gut-punch. This was the Ryan Reynolds gin that Diageo had bought in 2020, at the peak of the celebrity-brand craze, for up to $610 million — $335 million upfront plus as much as $275 million in performance-linked earn-outs stretched over a decade.6 Five years later, the company was conceding that a chunk of that value was never coming back.

The analytical lesson is not that celebrity brands never work — Casamigos genuinely did, for years. It is about when and at what price they were bought. The Aviation and Distill Ventures write-downs are, in effect, a receipt proving that Diageo paid peak-cycle prices for speculative, early-stage premium bets on the assumption that pandemic-era momentum was permanent. When the assumption broke, the accounting caught up. Impairments are backward-looking confessions: they mark the gap between what management once believed a brand was worth and what the market will now bear.

Underneath the write-downs, the harder problem was the balance sheet. Net debt swelled to $21.9 billion by June 2025, pushing leverage to 3.4 times net debt to adjusted EBITDA — above the top of the company's own 2.5x–3.0x comfort zone.4 Leverage is insidious in a downturn: as EBITDA falls, the ratio rises even if the absolute debt holds steady, and a business that funded buybacks, dividends and pricey acquisitions during the boom suddenly finds its financial flexibility evaporating exactly when it needs room to invest through the cycle. Diageo still generated real cash — free cash flow of about $2.7 billion in FY25 — but a growing slice of that was spoken for by interest and a progressive dividend the company had promised never to cut.4

Something had to give, and in July 2025 it was the CEO. Debra Crew stepped down by "mutual agreement" after just two years, the shortest tenure of any Diageo chief executive, with the shares languishing near decade lows.7 Chief Financial Officer Nik Jhangiani — a seasoned drinks-industry finance executive who had joined from Coca-Cola Europacific Partners — stepped up as interim CEO while the board hunted for a permanent leader.7 Two CEOs in two years, a profit engine misfiring, a billion in write-downs, and a debt pile pressing against its ceiling. The board needed someone whose entire reputation was built on exactly this kind of mess.

VII. The Sir Dave Lewis Turnaround: "Drastic Dave" Resets the Board

On November 10, 2025 — two years to the day after the Latin American profit warning that started the unravelling — Diageo announced its answer.[^10] Sir Dave Lewis would become chief executive on January 1, 2026.1[^10] To anyone who had followed British business over the previous decade, the choice was a statement in itself.

Lewis is not a spirits man. He is a turnaround man. He spent 28 years at Unilever, climbing from graduate trainee to run global personal care and major regional divisions — a marketer and operator schooled in one of the world's toughest consumer-goods academies. But his reputation was forged at Tesco. In 2014, Lewis became the first outsider ever to run Britain's biggest retailer, taking the wheel just as the company confessed to a £250 million accounting scandal and stared down collapsing margins and a wounded balance sheet. Over the next six years he did the unglamorous work: he cut costs to the bone, rebuilt supplier trust, restored the balance sheet, and dragged Tesco back to health. The press dubbed him "Drastic Dave," and it was not entirely a compliment — but the turnaround worked. After leaving Tesco in 2020, he chaired the healthcare group Haleon through its 2022 spin-out from GSK.8 Diageo hired the man precisely for the trait his nickname captured: a willingness to do the painful, unpopular thing quickly.

He did not keep the market waiting. On February 25, 2026, in his first major results announcement — the interim figures for the six months to December 2025 — Lewis reached for the most sacred cow in Diageo's investor relations playbook and slaughtered it. He cut the interim dividend to 20 cents per share, down from 40.50 cents a year earlier: a halving.9 For a stock long owned by income investors as a reliable, ever-rising payer, this was the "kitchen-sinking" move of a new CEO clearing the decks — taking the pain early, on his own terms, and resetting expectations to a level he could actually beat.

The logic was cold and, on an independent read, largely defensible. A company carrying 3.4x leverage into a demand downturn cannot keep shovelling cash out the door to appease income funds while its balance sheet corrodes; that is the road to a forced deleveraging on someone else's timetable. By cutting the dividend, Lewis freed up cash to attack the roughly $21.7 billion net debt pile and drive leverage back toward the target range.9 Alongside the cut, the board scrapped the old progressive policy entirely, replacing it with a 30–50% payout ratio and a minimum floor of 50 cents per year — a far more flexible framework that ties returns to actual earnings rather than to a promise made in better times.9 Management also announced the sale of Diageo's stake in East African Breweries to Japan's アサヒ Asahi Group for estimated net proceeds of about $2.3 billion, a disposal expected to shave roughly a quarter-turn off leverage on completion in the second half of 2026.9 Selling a fast-growing African beer asset to pay down debt is telling: when a deleveraging is urgent enough, even good businesses get sold.

Beneath the headline dividend cut sat a three-pronged operational reset. First, cost: Lewis inherited and expanded the "Accelerate" programme, targeting roughly $625 million of savings over three years — raised from an earlier $500 million goal — carved out of supply-chain inefficiency, marketing spend and, most painfully, corporate overhead, including job cuts reaching into United Spirits in India.49 Second, structure: Lewis moved to strip out layers, reorganising the top of the company and thinning the regional management tiers that had slowed decisions and, arguably, helped hide the LAC inventory build in the first place.10 A flatter organisation is not just a cost play; it is a visibility play. Third, and most heretically, strategy: Lewis signalled a willingness to challenge the sacred cow of premiumisation-at-all-costs, redirecting marketing and pricing support back toward high-volume standard brands like Smirnoff and Captain Morgan to meet downtrading consumers where they actually were, rather than where the strategy deck wished they would be.10

That last shift is the most consequential, because it is a partial repudiation of the Menezes gospel. For a decade, Diageo's answer to every question was "trade the consumer up." Lewis's early moves suggest a more pragmatic reading: premiumisation is a tailwind in expansions and a headwind in squeezes, and a resilient portfolio needs a strong volume base to catch consumers on the way down. Whether he can execute that pivot without cannibalising the premium mix that drives Diageo's margins is the open question on which his entire tenure will turn. The strategy is credible on paper. The evidence will take years to arrive.

VIII. Playbook: Business & Investing Lessons

Step back from the specifics of one drinks company and Diageo's ordeal offers a set of lessons that travel well beyond the liquor aisle. The first is the elasticity of premiumisation. Moving consumers up the value chain is one of the most powerful growth levers in all of consumer goods — but it is not a one-way ratchet. It works brilliantly when incomes are rising and confidence is high, and it works in reverse, sometimes violently, when inflation bites. Worse, it acts as an amplifier on the downside: a business optimised for the top of the range has the most to lose when consumers retreat to the bottom of it. The defensive antidote is portfolio balance — retaining genuine strength at accessible price points so that a downtrading consumer trades within your house rather than out of it. Diageo, having spent a decade celebrating its super-premium tilt, is now rediscovering the value of Smirnoff.

The second lesson is the sell-in versus sell-out illusion, and it is the most operationally important idea in this entire story. In any business that reaches customers through wholesalers and distributors, the metric that is easiest to measure — shipments into the channel — is a dangerously lagging and manipulable proxy for the metric that actually matters: consumption out of the channel. A channel can absorb inventory for months, flattering revenue and masking a demand rollover, right up until it can't. Real-time digital visibility into end-consumer sell-out is not a luxury analytics project; in a distributed consumer business it is a core risk-management requirement. Diageo learned this the hard way, and any investor evaluating a wholesale-distributed company should ask, bluntly: how do you know what your distributors are actually selling, and how fast do you find out?

The third lesson concerns the limits of celebrity and brand hype. Casamigos, Aviation, the whole wave of famous-founder spirits — they command enormous initial attention and, therefore, enormous acquisition multiples. Sometimes, with the right structure and genuine product-market fit, they pay off; the Casamigos earn-out is a fair template for aligning founders through the awkward post-sale years. But celebrity is a customer-acquisition tool, not a durable moat. Long-term brand equity is built on distribution depth, pricing discipline and real product differentiation, and a brand bought at 20x sales has priced in perfection. When you pay peak-cycle multiples for momentum, you are underwriting the assumption that the momentum is permanent — and momentum, almost by definition, is not.

The fourth lesson is about turnaround credibility and payout discipline. There is a seductive but destructive instinct, common among mature blue-chips, to protect a progressive dividend at all costs — to treat an unbroken payout record as sacred even as leverage climbs and the underlying business weakens. That instinct is how balance sheets get destroyed one "we couldn't possibly cut the dividend" at a time. The healthier path, counterintuitive as it feels, is often a decisive cut executed by a credible new leader who can absorb the reputational hit and redirect the cash to repair. A dividend cut announced by an outgoing management under duress reads as capitulation; the same cut announced by a "Drastic Dave" in his first quarter reads as a reset. The action is identical; the credibility of the actor is what changes the market's interpretation.

Which raises the meta-lesson that binds them all: even the deepest moats — and Diageo's are genuinely deep — cannot protect a company from poor inventory discipline and an over-leveraged balance sheet during an economic transition. Great assets can survive bad management for a long time, which is precisely why bad management can hide in them for a long time. The structural analysis that follows tests just how deep those moats really are.

IX. Structural Analysis: Hamilton Helmer's 7 Powers & Porter's 5 Forces

To judge whether Diageo can actually recover, we need to separate the durable from the fragile — to ask which of its advantages are structural and which merely felt structural during a boom. Two frameworks help: Hamilton Helmer's 7 Powers, which catalogues the sources of persistent competitive advantage, and Michael Porter's Five Forces, which maps the pressures bearing down on industry profitability.

Start with Helmer. Diageo's single strongest power is its cornered resource: the maturing inventory of aged Scotch. As established, no amount of capital can compress the calendar — a 12-year-old whisky requires twelve years, full stop — and Diageo's warehouses of aging stock represent a lead measured not in market share but in decades. This is as close to an unassailable advantage as consumer goods offers, and crucially it is rival-proof: even a competitor with infinite money cannot buy their way past time. The caveat, familiar by now, is that this resource is also a balance-sheet weight, and its value depends on forecasting demand a decade out — a skill Diageo demonstrably fumbled in the recent cycle.

The second power is scale economies. Diageo's portfolio is so broad and so deep that it is a near-mandatory partner for distributors and on-trade accounts worldwide. A bar that wants Guinness, Johnnie Walker, Tanqueray, Smirnoff, Baileys and Don Julio finds it far simpler to deal with one dominant supplier than to assemble the same range piecemeal — and that bundling drives lower per-unit costs in distribution, marketing and shelf negotiation. The bigger the bundle, the harder it is to say no. The third power, tightly related, is brand and share of mind: Guinness, Johnnie Walker and Tanqueray occupy consumer mental real estate that took centuries to build and cannot be replicated with an advertising budget. When a drinker orders "a gin and tonic" and pictures a specific green bottle, that is an asset no newcomer can manufacture quickly.

Where the moat thins is switching costs, which Helmer would rate low to moderate. For the retail consumer they are essentially nil — nothing stops a shopper from reaching for a cheaper bottle next to the Johnnie Walker, which is exactly the downtrading vulnerability that mugged Diageo in Latin America and the US. Switching costs are more real in the on-trade, where commercial bars depend on Diageo for credit terms, marketing support, staff training and reliable delivery of a full portfolio — a relationship that is stickier than a supermarket shelf. But it is a moderate power, not a deep one, and it does not protect the crucial at-home consumer at all.

Now Porter. The threat of new entrants is low at the top of the market: the capital cost of building global distribution and laying down years of aging brown-spirits inventory is prohibitive, which is why the industry's giants have stayed the giants for generations. But the threat of substitutes is genuinely high and rising — this is the force that should worry Diageo most. Consumers are drifting toward ready-to-drink cocktails, local craft distilleries, and, increasingly, toward drinking less alcohol altogether, whether for health or generational reasons. The rise of the sober-curious younger drinker is a slow-moving but potentially structural threat to volume that no moat around premium Scotch fully addresses; Diageo's push into Guinness 0.0 and Tanqueray 0.0 is a direct, and so far encouraging, response.

Bargaining power of buyers sits at medium-to-high: consolidated supermarket chains and mega-distributors wield real pricing leverage and can promote house brands, yet they cannot easily delist Diageo's anchor names without angering their own customers, which caps how hard they can squeeze. And competitive rivalry is intense and margin-eroding — Diageo battles Pernod Ricard, Brown-Forman, Campari Group and the luxury-drinks arm of LVMH, all fighting for the same back-bar space and all capable of igniting the kind of tequila and Scotch price wars that turn premiumisation's tailwind into a headwind. Netting it out: Diageo's supply-side moats (cornered resource, scale, brand) remain formidable and largely intact, but the demand-side forces (substitutes, weak consumer switching costs, downtrading) have strengthened materially — which is precisely why a business with such deep advantages could still stumble so badly.

X. The Investment Case: Bull vs. Bear and Key KPIs

So where does this leave a long-term investor trying to underwrite Diageo from here? The honest answer is that this is a genuine two-sided debate, and the resolution hinges on a small number of measurable things. Rather than drowning in metrics, focus on three KPIs that together tell you whether the Lewis turnaround is real or rhetorical.

The first is organic net sales and volume growth, watched together. Price-mix can flatter a top line for a while, but if volumes keep falling, the company is simply raising prices on a shrinking base — a strategy with a hard ceiling, especially amid downtrading. The signal to watch is stabilisation and then recovery in the volumes of the core engines — Scotch and tequila in North America — accompanied by price-mix that reflects genuine premium demand rather than desperate list-price hikes. The interim results to December 2025 showed organic net sales still declining, down 2.8%, with North America under real pressure from stretched disposable income; the inflection has not yet arrived.9

The second KPI is the leverage ratio, net debt to adjusted EBITDA. This is the single cleanest scorecard for whether Lewis is winning his central battle. It stood at 3.4x at the June 2025 year-end, above the 2.5x–3.0x target range, and the entire architecture of the dividend cut, the Accelerate cost programme and the East African Breweries sale is aimed at driving it back inside that band.49 Watch the trajectory over the coming years: steady progress toward 3.0x and below would validate the strategy; a stalled or rising ratio, whether from weak EBITDA or further disappointments, would suggest the deleveraging plan is being outrun by the business's decline.

The third is free cash flow generation. Cash, ultimately, is what pays down debt and funds the brand investment that keeps the moats maintained. FY25 free cash flow came in around $2.7 billion, and management has pointed to a target of roughly $3 billion a year going forward.4 Hitting that number consistently would give Lewis the ammunition to deleverage and reinvest simultaneously; missing it would force uncomfortable trade-offs between the balance sheet and the brands.

The bull case runs like this. Lewis is a proven operator doing exactly what proven operators do: cutting costs decisively, resetting the dividend to a sustainable level, selling non-core assets, and deleveraging with discipline. The Latin American inventory overhang, being a channel problem rather than a demand-destruction problem, normalises over time. North American consumer weakness proves cyclical, not permanent, and premium demand recovers as inflation eases. And Guinness — genuinely resurgent — together with the non-alcoholic range, proves Diageo can capture modern wellness and moderation trends rather than being run over by them. In this reading, the current valuation near decade lows is the market extrapolating a cyclical trough as though it were structural, and the deep moats reassert themselves.

The bear case is equally coherent, and it is not merely the mirror image. Its sharpest edge is that downtrading is structural, not cyclical — that a generation drinking less and paying more attention to price permanently impairs the high-margin super-premium sales on which Diageo's profitability was rebuilt. Layer on aggressive price competition from Pernod Ricard, Brown-Forman and Campari, which could turn tequila and Scotch into value-destructive price wars, and the margin structure erodes further. And the debt itself becomes the trap: a heavy interest burden on more than $20 billion of net debt constrains the very brand-marketing reinvestment that sustains share of mind, creating a slow bleed where underinvestment begets share loss begets weaker cash flow. An activist looking at Diageo would press hardest on exactly these pressure points — the portfolio complexity across hundreds of SKUs, the peak-cycle acquisition record, the overhead that Lewis is only now attacking, and whether the board moved fast enough on any of it.

The intellectually honest conclusion is that the bull and bear cases are separated less by narrative than by data that has not yet been printed. The three KPIs above are how an investor keeps score without taking management's word — or the skeptics' — on faith.

XI. Epilogue & Outro

Return, finally, to that February morning and the man cutting the dividend. The symmetry is almost too neat: a retailer famous for rescuing a supermarket accounting scandal, now standing over the spirits industry's most storied portfolio, reaching for the same instruments — cost, cash, candour — that worked at Tesco. Can Drastic Dave do for Johnnie Walker and Smirnoff what he did for the weekly grocery shop? Nobody knows yet, and anyone who claims to is selling something.

What the story does make clear is where the answer will not come from. It will not come from the brands, which remain magnificent, nor from the moats, which — cornered inventory, scale, share of mind — remain among the deepest in all of consumer goods. Arthur Guinness's nine-thousand-year lease is intact. The 18-year-old Scotch aging in the warehouses is exactly as rival-proof as it always was. The failure that brought Diageo to a decade-low valuation was not a failure of assets. It was a failure of execution: of inventory discipline, of channel visibility, of capital allocation at peak-cycle prices, and of a strategy so enamoured of its own premiumisation gospel that it could not see consumers walking down the price ladder until the warehouses were already full.

That is the enduring lesson, and it is a humbling one for anyone who believes a great business is a self-driving one. The best consumer companies do not win on marketing narrative alone. They win, or lose, on the unglamorous disciplines beneath the brand: knowing what your distributors are actually selling, laying down the right inventory for demand a decade away, refusing to overpay for momentum, and keeping the balance sheet strong enough to invest through a downturn rather than retreat into one. Diageo forgot some of that during the boom. Whether Sir Dave Lewis can rebuild it — brick by unglamorous brick — is now the only question that matters, and it will be answered not in press releases but in the leverage ratio, the volume trend and the cash flow, quarter after quarter, for years to come.

References

-

Sir Dave Lewis appointed Diageo plc CEO — Diageo plc, 2025-11-10 ↩↩

-

Seagram's Wines and Spirits Sold for $8.15 Billion — Wine Spectator, 2000-12-19 ↩

-

Diageo swaps Bushmills for Don Julio — Food Dive, 2014-11-03 ↩

-

2025 Preliminary Results, year ended 30 June 2025 — Diageo plc, 2025-08-05 ↩↩↩↩↩↩↩↩↩↩

-

Diageo Warns on Profit, Hit by a Sharp Slowdown in Latin America — Bloomberg, 2023-11-10 ↩↩

-

Diageo to acquire Aviation Gin and Davos Brands — Diageo plc, 2020-08-17 ↩

-

Diageo CEO Debra Crew to Step Down, CFO Nik Jhangiani Appointed Interim — Reuters, 2025-07-16 ↩↩

-

Diageo appoints Dave Lewis as CEO — The Spirits Business, 2025-11-10 ↩

-

Diageo 2026 Interim Results: Six Months Ended 31 December 2025 — Diageo plc, 2026-02-25 ↩↩↩↩↩↩↩

-

Diageo Faces Hard Premiumisation Headwinds as Consumers Downtrade — Food Dive, 2024-07-31 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube