Deutsche Bank: The Rise, Fall, and Redemption of Germany's Banking Giant

I. Introduction & Episode Roadmap

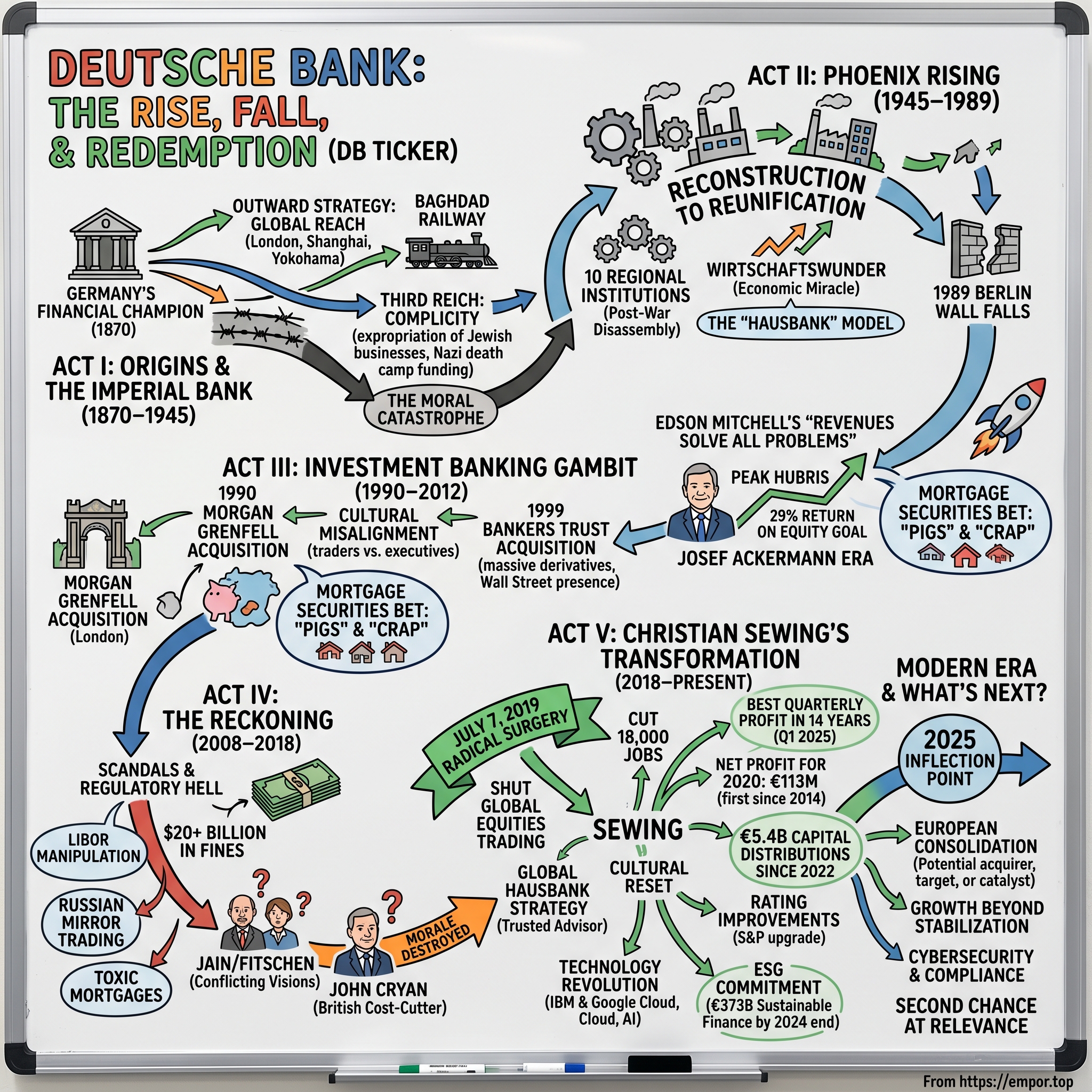

Picture this: A gleaming glass tower in Frankfurt, once the symbol of German financial might, now trading at €15—a mere fraction of its €112 pre-crisis peak. Inside, Christian Sewing, the son of a Westphalian farmer, sits where titans of European finance once commanded a global empire. The year is 2018, and Deutsche Bank, Germany's largest financial institution, teeters on the edge of irrelevance. How did a bank founded to finance German trade become Wall Street's most controversial player, only to nearly destroy itself in the process?

This is the story of Deutsche Bank—a 154-year saga of ambition, overreach, and perhaps the most dramatic attempted comeback in modern banking history. It's a tale that spans from financing the Baghdad Railway in the Ottoman Empire to laundering Russian oligarch money through mirror trades. From being Hitler's banker to becoming the fourth-largest financial management firm globally. From a conservative German Hausbank to a casino capitalist that racked up $20 billion in regulatory fines.

The central paradox haunts every chapter: How could an institution so fundamental to German economic identity—the bank that rebuilt post-war Germany, that financed the Wirtschaftswunder, that stood as Europe's answer to Wall Street—fall so spectacularly? And more importantly, can it rise again?

What makes Deutsche Bank's story particularly compelling isn't just the scale of its rise and fall, but what it reveals about the modern financial system itself. This is ultimately a story about culture—what happens when conservative German banking DNA collides with Anglo-Saxon casino capitalism. It's about the price of transformation, the cost of ambition, and the question that every global bank must answer: Can you be both a trusted local institution and a global investment banking powerhouse?

Over the next several hours, we'll trace Deutsche Bank's journey through three distinct acts. Act One: The Imperial Bank that helped build modern Germany, survived two world wars, and emerged from the ashes of the Third Reich. Act Two: The investment banking gambit that transformed a German commercial bank into a Wall Street player, culminating in the hubris of the Josef Ackermann era. And Act Three: The reckoning—a decade of scandals, leadership chaos, and Christian Sewing's radical surgery to save the patient.

We'll explore the key inflection points that changed everything. The 1999 Bankers Trust acquisition that injected Wall Street DNA into Frankfurt's bloodstream. The 2007 mortgage securities bet that nearly brought down the bank. The 2015 annus horribilis when Deutsche posted a €6.7 billion loss and faced existential questions about its survival. And the pivotal July 7, 2019 restructuring when Sewing shut down global equities trading and cut 18,000 jobs in a last-ditch effort to save the institution.

This isn't just a story about one bank. It's about the transformation of global finance itself—from relationship banking to algorithmic trading, from local trust to global reach, from prudent lending to synthetic CDOs. Deutsche Bank's journey is, in many ways, the story of modern capitalism's excesses and attempts at redemption.

So buckle up. We're about to embark on a journey that takes us from Bismarck's Berlin to Putin's Moscow, from the trading floors of London to the courtrooms of New York, from the heights of financial engineering to the depths of regulatory hell. This is Deutsche Bank's story—and it's far from over.

II. Origins & The Imperial Bank (1870–1945)

The gaslight flickered in a modest Berlin office on a cold January evening in 1870. Georg von Siemens, a 30-year-old banker with ambitious eyes, spread out maps of the world across his desk. Railway lines, shipping routes, telegraph cables—the sinews of a new global economy were being laid, and Germany was barely at the table. While British banks financed the Empire's trade from London and French banks dominated continental finance from Paris, the newly forming German nation lacked a financial institution capable of competing on the world stage. Siemens had a vision: Deutschland needed its own champion.

On March 10, 1870, with the personal approval of Prussian King Wilhelm I, Deutsche Bank came into existence. The founding document was audacious in its simplicity: "to transact banking business of all kinds, in particular to promote and facilitate trade connections between Germany, other European countries and overseas markets." The initial capital of 5 million thalers—modest by London standards—represented the collective bet of Berlin's merchant elite that Germany could build a global financial powerhouse from scratch.

What distinguished Deutsche Bank from its inception wasn't just ambition but strategy. While other German banks focused on domestic industry, Deutsche Bank looked outward. Within two years, it had established a presence in Shanghai (1872), becoming one of the first Western banks in China. By 1873, it opened in London, planting its flag in the heart of global finance. This wasn't gradual expansion—it was a sprint to relevance.

The early decades read like an adventure novel. Deutsche Bank financed the Northern Pacific Railroad across the American frontier, underwrote bonds for the Ottoman Empire's Baghdad Railway (a project that would reshape Middle Eastern geopolitics), and established branches from Yokohama to Constantinople. By 1876, it was issuing Chinese government bonds. By the 1890s, it controlled significant stakes in American railways and South American infrastructure. The conservative Prussian bank had become, improbably, one of the world's most aggressive international financiers. The 1929 merger with Disconto-Gesellschaft created Germany's largest bank—a colossus that would soon face history's darkest test. When Adolf Hitler rose to power in 1933, Deutsche Bank didn't resist. By 1934 it dismissed its three Jewish management board members, Oscar Wassermann, Theodor Frank, and Georg Solmssen, men who had helped build the institution into a global force. By the end of 1938, it had been involved as an intermediary and lender in at least 363 cases of expropriation of Jewish-owned businesses.

But the bank's complicity went far deeper than dismissals and expropriations. Through its branch in Katowice, Deutsche Bank loaned the funds used to build the Auschwitz camp and the nearby IG Farben facilities. Executive member Hermann J. Abs was also a member of the board of directors of IG Farben, the parent company of the Buna plant in Auschwitz-Monowitz, which produced synthetic rubber and exploited forced laborers, with turnover running to 5 million marks a month by spring 1943. Between 1942 and 1944, Deutsche Bank purchased 4,446 kg of gold from the Reichsbank, of which 744 kg came from Holocaust victims.

The scale of this moral catastrophe cannot be understated. This wasn't passive acquiescence but active participation in genocide. The same institution that had financed railways across continents now provided banking facilities for the Gestapo. The bank that had helped build global trade networks now processed gold extracted from the teeth of murdered Jews. When the full truth emerged decades later, Deutsche Bank disclosed in 1999 that it funded the construction of the Nazi death camp at Auschwitz, a revelation that nearly derailed its planned merger with Bankers Trust.

After Germany's defeat in 1945, the Allies understood that Deutsche Bank's power needed to be broken. The bank wasn't just complicit in war crimes—it had been integral to the Nazi war machine's financial infrastructure. The reckoning was swift and severe, setting the stage for one of the most remarkable institutional resurrections in business history.

III. Phoenix Rising: Reconstruction to Reunification (1945–1989)

The courtroom in Frankfurt was silent as the Allied Control Council pronounced its verdict in 1948. Deutsche Bank would cease to exist as a unified entity. Like Germany itself, the bank would be divided—split into ten regional institutions, a financial dismemberment designed to prevent any single German bank from ever again accumulating such dangerous power. The executives who had overseen loans to Auschwitz were gone, some imprisoned, others barred from banking. The institution that had once spanned continents was reduced to fragments.

Yet even in division, the DNA of Deutsche Bank proved resilient. By 1952, the ten regional banks had consolidated into three major institutions: Norddeutsche Bank AG in Hamburg, Rheinisch-Westfälische Bank AG in Düsseldorf, and Süddeutsche Bank AG in Munich. Each operated independently, but old relationships endured. Former Deutsche Bank employees, those untainted by Nazi collaboration, began quietly coordinating across the artificial boundaries. They shared a vision: Germany would need a strong bank to rebuild, and that bank would rise from Deutsche's ashes.

The pivotal moment came in 1957. With Germany's economic miracle—the Wirtschaftswunder—in full swing, the Allied authorities permitted what many thought impossible: the three successor banks merged back into Deutsche Bank AG. Hermann J. Abs, controversial for his wartime role but undeniably brilliant as a banker, returned as chairman. It was a decision that would haunt the bank's reputation for decades, but it also brought back the institutional knowledge and relationships that would fuel Germany's post-war economic explosion.

The reborn Deutsche Bank faced a different world. American banks dominated global finance, the British Empire's financial architecture was crumbling, and Germany itself was divided by the Iron Curtain. Abs and his successors crafted a strategy that would define the bank for the next three decades: Deutsche Bank would become the house bank—the Hausbank—to German industry. It would take equity stakes in major German corporations, sit on their boards, and provide patient capital for long-term growth. This wasn't Anglo-Saxon shareholder capitalism but something distinctly German: capitalism with deep, interlocking relationships.

The 1959 decision to enter retail banking marked a cultural revolution. For 89 years, Deutsche Bank had served corporations and governments. Now it would serve ordinary Germans, offering personal loans and savings accounts. Branch offices sprouted across West Germany—from 50 locations in 1957 to over 500 by 1970. The bank that had once financed railways in America now helped German families buy their first Volkswagens.

International expansion resumed, but cautiously. The 1970s saw Deutsche Bank return to the world's financial capitals: Milan (1977), Moscow (1978), Tokyo (1979). But this wasn't the swashbuckling expansion of the imperial era. These were careful, calculated moves, often following German corporations as they expanded abroad. The bank was building what would later be called "Deutschland AG"—the interlocking network of German companies, with Deutsche Bank at its center, that would dominate European business.

Then came November 30, 1989. Alfred Herrhausen, Deutsche Bank's visionary chairman, sat in his armored Mercedes in Bad Homburg, heading to work. A sophisticated bomb, triggered by a light beam, tore through the vehicle. Herrhausen, who had been pushing for debt relief for developing nations and had grand visions for reunifying Germany's economy, was killed instantly. The Red Army Faction claimed responsibility, but conspiracy theories abounded. Some saw it as a warning to Germany's financial elite. Others suspected darker forces opposed to Herrhausen's reformist agenda.

Nine days later, the Berlin Wall fell.

The assassination and the Wall's collapse created a strange duality at Deutsche Bank. The institution faced both its greatest opportunity—the reunification of Germany and the opening of Eastern Europe—and a stark reminder of its vulnerability. Herrhausen's successor, Hilmar Kopper, would need to navigate both. As East and West Germany rushed toward reunification, Deutsche Bank prepared for its own transformation. The conservative Hausbank model had served it well, but the 1990s would demand something different. The age of global investment banking was dawning, and Deutsche Bank would either adapt or be left behind.

The stage was set for the most audacious gamble in the bank's history.

IV. The Investment Banking Gambit (1990–2002)

Hilmar Kopper stood in the London offices of Morgan Grenfell on a gray December morning in 1989, just weeks after Herrhausen's assassination. The venerable British merchant bank, founded in 1838, was hemorrhaging money and reputation after a series of scandals. For Deutsche Bank, it represented something else entirely: a gateway to the Anglo-Saxon financial world. "We're not buying a troubled bank," Kopper told his skeptical board back in Frankfurt. "We're buying centuries of relationships and a seat at the table of global finance."

The £950 million acquisition of Morgan Grenfell, completed in 1990, was more than a purchase—it was a declaration of intent. Deutsche Bank would no longer be content as Germany's dominant bank. It wanted to compete with Goldman Sachs, Morgan Stanley, and Merrill Lynch on their own turf. But this meant embracing a culture antithetical to everything Deutsche Bank had represented: aggressive trading, enormous bonuses, and a winner-take-all mentality.

The cultural fault lines appeared immediately. Morgan Grenfell's London traders, accustomed to seven-figure bonuses, clashed with Deutsche Bank's Frankfurt executives, who believed in modest salaries and long-term employment. The British bankers mocked German bureaucracy; the Germans were appalled by British excess. One Morgan Grenfell trader famously expensed a £1,000 lunch, causing apoplexy in Frankfurt where executives ate sandwiches at their desks.

But the real transformation came with the $10.1 billion acquisition of Bankers Trust in 1999—the largest bank takeover in history at that time. Deutsche Bank disclosed its funding of Auschwitz construction during these merger negotiations, nearly derailing the deal when New York City Comptroller Alan Hevesi threatened to block it. The bank's chairman Rolf-Ernst Breuer was forced to publicly acknowledge "ethical and moral responsibility" for its Nazi-era crimes.

Bankers Trust brought something Morgan Grenfell couldn't: a massive derivatives operation and a presence on Wall Street. It also brought Edson Mitchell, a larger-than-life American who became head of global markets. Mitchell was everything Frankfurt feared and London admired—brash, brilliant, and compensated at levels that would make a German board member faint. His 1999 compensation reportedly exceeded $30 million, more than the entire management board of many German companies.

Mitchell transformed Deutsche Bank's trading operation into a powerhouse. He recruited aggressively from American banks, offering guaranteed bonuses that broke all precedent. He established the principle that producers—traders who made money—were kings, while everyone else was overhead. The trading floor in London became a gladiatorial arena where only profit mattered. Mitchell's motto, displayed prominently on the trading floor: "Revenues solve all problems."

Then tragedy struck. On December 22, 2000, Mitchell died in a plane crash at age 47. The Learjet he was piloting crashed on approach to a Maine airport in poor weather. With him died not just a brilliant banker but also the most powerful advocate for the American way of banking within Deutsche. His death created a power vacuum that would define the bank's next decade.

Into this vacuum stepped Josef Ackermann, who became CEO in 2002. The Swiss-born Ackermann was an unlikely revolutionary—a precise, disciplined executive who spoke in carefully measured sentences. But he harbored ambitions that would have shocked Deutsche Bank's founders. At his first investor presentation, he made a promise that would haunt the bank: Deutsche would achieve a 25% return on equity, matching the profitability of the best American investment banks.

Deutsche Bank's October 2001 listing on the New York Stock Exchange—the first after the 9/11 attacks—symbolized this new era. The bank that had once epitomized German financial conservatism now answered to American investors demanding American-style returns. The pressure to deliver those returns would drive decisions that would nearly destroy the institution.

The bank strengthened its U.S. presence by purchasing Scudder Investments in 2002 and expanded in Europe by acquiring Rued Blass & Cie and the Russian investment bank United Financial Group in 2005. Each acquisition brought new cultures, new risks, and new pressures to generate returns that would justify Ackermann's ambitious targets.

The transformation was remarkable and terrifying. By 2002, Deutsche Bank had become the fourth-largest financial management firm globally, with over €1 trillion in assets under management. Its trading revenues rivaled those of Goldman Sachs. Its bankers were closing deals from Silicon Valley to Shanghai. But beneath the surface, a dangerous dynamic was building. The conservative German bank had acquired the apparatus of American investment banking without fully understanding its risks. The traders in London and New York operated in a different universe from the relationship bankers in Frankfurt. The risk models that worked for commercial lending were being applied to complex derivatives that few truly understood.

As one former executive would later reflect: "We thought we were buying expertise. We were actually buying a culture that would consume us."

V. Peak Hubris: The Ackermann Era (2002–2012)

Josef Ackermann's morning routine never varied. The CEO of Deutsche Bank would arrive at his Frankfurt office at 6:30 AM, review overnight trading positions from New York and Asia, then video conference with his top lieutenants in London. On one particular morning in early 2007, the head of trading in London had spectacular news: the bank's proprietary trading desk had just placed a $25 billion bet on American mortgage securities. It was the largest single position in the bank's history. Ackermann's response was telling: "Make sure we can explain this to the board."

The Ackermann era represented Peak Deutsche—a decade when the bank seemed unstoppable, when its ambitions knew no bounds, when a German bank seriously contemplated merging with Citigroup to create the world's first trillion-dollar financial institution. The 2003 discussions with Citi, though ultimately blocked by the German government who feared losing a national champion, revealed the scale of Ackermann's vision. He didn't want Deutsche Bank to compete with Wall Street; he wanted to dominate it.

The numbers were intoxicating. Revenues soared from €20 billion in 2002 to €40 billion by 2007. The investment banking division, once an afterthought, generated over 70% of group profits. Deutsche Bank traders were the kings of European credit markets, the dominant force in foreign exchange, and increasingly powerful in the mysterious world of structured products. The bank's derivatives book, with a notional value exceeding €50 trillion, was larger than the GDP of the entire world.

But it was in the American mortgage market where Deutsche Bank made its most fateful decisions. Between 2004 and 2008, the bank underwrote and sold $32 billion of mortgage-backed securities to clients, marketing them as safe investments suitable for pension funds and insurance companies. What clients didn't know was that Deutsche Bank's own traders were simultaneously betting against these same securities, buying credit default swaps that would pay off when the mortgages failed. Internal emails later revealed traders calling the securities "pigs" and "crap" while selling them to unsuspecting clients.

The most controversial figure of this era was Greg Lippmann, the head of mortgage trading who became famous as the real-life inspiration for a character in "The Big Short." Lippmann had convinced the bank to let him bet against the housing market even as other divisions were selling mortgage securities. By 2007, his team had built a massive short position that would eventually generate billions in profits. When asked about the ethics of betting against products the bank was selling, Lippmann reportedly shrugged: "That's how markets work."

The culture had transformed completely. The Frankfurt headquarters, once the undisputed center of power, became increasingly irrelevant. Real decisions were made in London and New York, where traders earning eight-figure bonuses wielded more influence than board members. The compensation committee meetings became surreal exercises in justification. How to explain to German shareholders that a 28-year-old trader earned more than the CEO of Siemens? Ackermann's solution was simple: don't explain, just deliver the returns.

The bank's risk management, once legendary for its conservatism, became a box-ticking exercise. Risk managers who raised concerns were labeled "business preventers." The Value at Risk models, which supposedly captured the bank's maximum possible losses, were based on historical data that assumed housing prices could never fall nationwide. When one risk manager pointed out this flaw, he was told the models had been approved by the regulators and that was sufficient.

In 2007, as cracks appeared in the mortgage market, Deutsche Bank faced a defining moment. The bank could have reduced its exposure, taken losses, and preserved its reputation. Instead, it doubled down. The Leveraged Super Senior trades—synthetic CDOs that would later result in massive losses—were approved despite internal warnings. The trades were so complex that even the bank's own risk committee didn't fully understand them. One board member later admitted: "We were assured by very smart people that the risks were hedged. We didn't know what questions to ask."

When the financial crisis hit in 2008, Deutsche Bank initially seemed to weather it better than peers. Unlike UBS or Citigroup, it didn't need a government bailout. Ackermann famously declared that accepting state aid would be "shameful." The bank even reported a profit in 2008, a feat that seemed to vindicate the universal banking model. But this was largely an illusion, built on accounting treatments and one-time gains that masked deeper problems.

The real cost of the Ackermann era wouldn't become clear until years later. The aggressive expansion had created a sprawling, unmanageable institution with operations in 70 countries and over 100,000 employees. The focus on trading had alienated traditional German corporate clients. Most damaging of all, the pursuit of profits above all else had created a culture where bending rules became normalized, where compliance was seen as an obstacle to overcome rather than a principle to uphold.

By 2012, as Ackermann prepared to step down, Deutsche Bank appeared successful by conventional metrics. It was Europe's largest investment bank, a top-three player in global foreign exchange, and a powerhouse in derivatives. But beneath the surface, time bombs were ticking: regulatory investigations, toxic assets, and a culture that had lost its moral compass. The bill for a decade of excess was about to come due.

VI. The Reckoning: Scandals & Regulatory Hell (2008–2018)

The email arrived at 3:47 AM Frankfurt time on December 23, 2008. "Merry Christmas," it read, "We're under investigation by the DOJ for our mortgage securities business. Delete nothing. Preserve everything." Within hours, FBI agents were in Deutsche Bank's New York offices, seizing computers and filing cabinets. The age of reckoning had begun.

What followed was a decade of investigations, scandals, and fines that would transform Deutsche Bank from predator to prey. The numbers alone stagger the imagination: over $20 billion in fines and settlements, more than 7,000 external lawyers and consultants crawling through every transaction, every email, every chat message. By 2015, the bank employed more compliance officers than traders—a complete reversal of the Ackermann-era priorities.

The mortgage securities investigation that began that December morning would culminate in a $7.2 billion settlement with the U.S. Department of Justice in 2017. The investigation revealed a pattern of deception that shocked even hardened regulators. Deutsche Bank had knowingly packaged defective mortgages into securities, with internal communications showing employees joking about the poor quality. One trader's chat message became infamous: "These bonds could blow up at any time. Still, until then, we make money."

But mortgages were just the beginning. The LIBOR manipulation scandal erupted in 2013, revealing that Deutsche Bank traders had systematically rigged the benchmark interest rate that underpinned trillions in financial contracts. The bank paid €227 million to UK regulators and $2.5 billion in total fines globally. The investigation uncovered a culture where manipulation was routine, with traders requesting specific LIBOR submissions to benefit their positions as casually as ordering coffee.

The Russian mirror trading scandal, uncovered in 2015, was perhaps the most damaging reputationally. Deutsche Bank had facilitated $10 billion in suspicious transactions, allowing Russian clients to convert rubles into dollars through simultaneous trades in Moscow and London. The scheme was so blatant that compliance officers had raised red flags for years, only to be overruled by senior management focused on revenues. One Moscow trader, when asked about the suspicious patterns, reportedly said: "It's Russia. Everything is suspicious."

The Leveraged Super Senior trades scandal revealed another dimension of the rot. Traders had hidden up to $3.3 billion in gap risk—potential losses that weren't properly accounted for in the bank's risk models. When the trades finally unwound, they contributed to massive losses that nearly brought down the bank. Internal investigations revealed that multiple layers of management knew about the hidden risks but chose to ignore them to protect bonuses.

Leadership during this period became a revolving door of crisis management. Anshu Jain and Jürgen Fitschen's co-CEO structure (2012-2015) was a disaster of conflicting visions. Jain, the investment banker who had built the trading empire, couldn't accept that the model was broken. Fitschen, representing traditional German banking, lacked the authority to force change. Board meetings became battlegrounds, with German labor representatives clashing with international investors over the bank's direction.

The annus horribilis came in 2015. Deutsche Bank posted a staggering €6.7 billion loss, its first annual loss since 2008. The share price collapsed to €8, down 90% from its peak. Credit default swaps on Deutsche Bank's debt—essentially insurance against the bank's failure—spiked to levels suggesting genuine concern about survival. The German government privately discussed contingency plans for a bailout, though publicly maintained confidence.

John Cryan's appointment as CEO in July 2015 brought hope for reform. The British banker, known for his dour demeanor and cost-cutting prowess, immediately announced radical changes: 18,000 job cuts, withdrawal from 10 countries, and a promise to create a "boring" bank focused on traditional banking. "We must reduce complexity," Cryan declared. "Deutsche Bank has become too difficult to manage."

But Cryan's medicine proved too bitter for an organization in denial. His brutal honesty—publicly stating the bank was "not profitable enough" and had "serious operational challenges"—destroyed morale without delivering quick results. The investment bankers resented his dismantling of their empire. The Germans found him too Anglo-Saxon. The board grew impatient with losses that continued despite the restructuring.

By early 2018, with the share price still languishing and no clear path to profitability, the board had seen enough. Cryan was unceremoniously dumped, despite having three years left on his contract. The search for a savior led to an unexpected choice: Christian Sewing, a lifetime Deutsche banker who had started as an apprentice in 1989. The son of a Westphalian farmer would attempt what Swiss investment bankers and British cost-cutters had failed to achieve: saving Deutsche Bank.

The decade of reckoning had extracted a terrible price. Beyond the financial costs—the billions in fines, the collapsed share price, the destroyed reputation—was the human toll. Thousands of careers ended, retirement savings evaporated, and the proud institution that had helped rebuild Germany lay in ruins. The question was no longer whether Deutsche Bank could dominate global finance, but whether it could survive at all.

VII. Christian Sewing's Transformation (2018–Present)

Christian Sewing's first all-hands meeting as CEO, held in the Frankfurt headquarters on April 9, 2018, was unlike any in Deutsche Bank's history. No grand vision, no promises of glory, just brutal honesty from a man who had spent his entire career at the bank. "We have lost our way," he said simply. "We tried to be something we're not. It's time to remember who we are." The investment bankers in London and New York, watching via video link, knew what was coming. Sewing knew that half-measures wouldn't work. Previous CEOs had promised transformations while protecting sacred cows. On July 7, 2019, Sewing unveiled a restructuring so radical that even veteran bankers were shocked. The restructuring of Deutsche under Sewing is usually traced back to July 7, 2019, when he unveiled a sweeping plan to reshape the firm, including the radical decision to shut down its equities franchise. The bank would exit global equities sales and trading completely—not scale back, not restructure, but shut down entirely. Deutsche will cut 18,000 jobs for a global headcount of around 74,000 employees by 2022.

The morning of the announcement, employees in the equities division arrived to find their access cards deactivated. Security guards handed them boxes for their personal belongings. In London, entire trading floors were cleared within hours. It was brutal but necessary—Sewing believed that anything less decisive would be seen as weakness. "We tried to be everything to everyone," he told the board. "That ends today. "The strategy he unveiled went beyond just cutting equities. Sewing called it the "Global Hausbank" model—returning to Deutsche Bank's roots as a trusted advisor to businesses while maintaining selective strength in capital markets. "It meant an overhaul of the entire bank in terms of discipline, in terms of focus, in terms of business setup, in terms of cost management," he later explained. The bank would create a Capital Release Unit—essentially a "bad bank"—to wind down €74 billion of unwanted assets. Adjusted costs would be cut by a quarter to €17 billion.

The transformation faced immediate skepticism. Goldman Sachs called it "very deep" but warned that "DBK's structural challenges, as we see them, fall into three categories: the absence of a high-return platform, elevated funding costs, and uncertainty around the scope of its IB business." Citi termed the plan "optimistic," noting that "Restructuring charges of €7.4 billion (c12% of tangible equity) are heavier than anticipated, but spread out over 4 years. Management intends to fund this from existing resources, so there is no capital raise. This may yet prove optimistic."

But Sewing had advantages his predecessors lacked. As a lifetime Deutsche banker who started as an apprentice in 1989, he understood the institution's culture intimately. He had served as chief credit officer from 2010 to 2012 and deputy chief risk officer for a year, giving him deep knowledge of where the bodies were buried. Most importantly, he had credibility with the German staff who felt alienated by foreign CEOs and the German corporate clients who had been neglected during the investment banking obsession.

The pandemic could have destroyed the restructuring. When COVID-19 hit in early 2020, with Deutsche Bank in the middle of its most radical transformation, many predicted disaster. Instead, something remarkable happened. The trading businesses that remained after the equities exit performed brilliantly, generating windfall profits from market volatility. More importantly, the crisis validated Sewing's balanced approach—while pure investment banks suffered, Deutsche's diversified model provided stability.

Deutsche's net profit attributable to shareholders for 2020 was 113 million euros, compared with a 2019 loss of 5.7 billion euros. It was the bank's first annual profit since 2014—modest but symbolically crucial. The momentum continued in 2021, with the German lender quadrupling profit to 2.4 billion euros in 2021 versus 2020, recording its best result in a decade.

The numbers told a story of gradual recovery. Revenue grew from €24 billion in 2020 to €25.4 billion in 2021, then accelerated. The investment bank, despite losing equities, saw revenues rise 28% from the 2019 low. The corporate bank, long neglected, returned to growth. Even the troubled private bank achieved profitability. By 2023, the transformation was gaining credibility—S&P upgraded the bank's rating in December, the first of what would become five rating improvements in 2024.The most dramatic transformation came in the investment bank. Investment Bank net revenues grew 15% year on year to € 10.6 billion in 2024, with revenues € 2.4 billion, up 30% on the prior year quarter in Q4 2024 alone. This wasn't the reckless growth of the Ackermann era but focused expansion in areas where Deutsche Bank had genuine competitive advantages. Origination & Advisory revenues grew by 61% to € 2.0 billion, and Deutsche Bank's share of a growing global fee pool increased by approximately 50 basis points to 2.3%.

The "Global Hausbank" strategy was working. "We have a very successful investment bank, but an investment bank that is not dominating the bank anymore," Sewing explained. "This bank needed to drive on four cylinders, not only one, and that is what we have achieved." The balance was crucial—investment banking generated strong returns without overshadowing the rest of the institution.

But challenges remained formidable. The bank faced €2 billion in Postbank litigation costs in 2024, a painful reminder of past mistakes. The cost-income ratio, while improving, remained stubbornly high. And the share price, despite recovering from its lows, still traded at a massive discount to book value—a sign that investors remained skeptical about the sustainability of the turnaround.

VIII. Modern Era & Current State (2020–2025)

The morning of March 24, 2023, Christian Sewing watched his Bloomberg terminal with a mixture of disbelief and quiet fury. Deutsche Bank's credit default swaps had spiked to crisis levels, the share price was crashing, and social media was ablaze with speculation about the bank's imminent collapse. The trigger? Credit Suisse's rescue by UBS the previous weekend had sparked contagion fears. But Sewing knew something the market didn't: Deutsche Bank had never been stronger.

"It was on the weekend of March 24, 2023 – when the cost of insuring Deutsche Bank bonds against default had rocketed and its crashing share price had shaved more than €1.5 billion from its value – that Christian Sewing knew the bank he led had turned itself around. Two things told him. One, as chief executive, he had access to data right across the institution that no one on the outside and few on the inside could see. That gave him confidence in his bank, even as the rescue of Credit Suisse by UBS the previous weekend was throwing the sector into turmoil."

Within 48 hours, the panic subsided. Deutsche Bank's fundamentals—strong capital ratios, improved profitability, reduced risk—reasserted themselves. The episode became a perverse validation of Sewing's strategy. The bank that had once been the epicenter of every financial crisis was now merely caught in the periphery of someone else's problems. The numbers from 2024 and early 2025 tell a remarkable story of recovery. Investment Bank net revenues grew 15% year on year to € 10.6 billion in 2024, driven by growth across the franchise. The fourth quarter alone saw revenues of € 2.4 billion, up 30% on the prior year quarter. But this wasn't the reckless expansion of old—it was disciplined growth in areas of genuine strength.

The first quarter of 2025 brought validation that the transformation was sustainable. "We are very happy with first-quarter results which put us on track for delivery on all our 2025 targets. Our best quarterly profit for fourteen years, achieved through revenue growth combined with lower costs, demonstrates that our Global Hausbank strategy is working well." The bank reported profit before tax of € 2.8 billion for the first quarter of 2025, up 39% year on year, driven by 10% growth in net revenues and a 2% decline in noninterest expenses.

Most importantly, the return metrics that had been dismal for so long were finally recovering. Post-tax return on average tangible shareholders' equity (RoTE) was 11.9%, up from 8.7% in the prior year quarter and in line with the bank's full-year 2025 target of above 10%. For a bank that had struggled to generate any returns for years, achieving double-digit RoTE was transformational. The capital returns story became the clearest evidence of transformation. Deutsche Bank announced plans for € 2.1 billion in further capital distributions to shareholders in 2025. The bank has received supervisory authorization for further share repurchases of € 750 million so far in 2025 and plans to propose 2024 dividends of € 1.3 billion, or € 0.68 per share, at its Annual General Meeting in May 2025, up 50% from € 0.45 per share for 2023. These measures would increase cumulative capital distributions to shareholders to € 5.4 billion since 2022, in excess of the € 5 billion goal in the bank's transformation program launched in 2019.

For a bank that couldn't pay dividends for years during the crisis era, returning over €5 billion to shareholders in just four years represented a stunning reversal. The 50% dividend increase year-over-year sent a clear message: Deutsche Bank was no longer fighting for survival but competing for investor capital.

The cost discipline that Sewing implemented was bearing fruit. The bank targeted a cost-income ratio below 65% for 2025, a level that would have seemed impossible during the Cryan era. More importantly, the costs being cut weren't muscle but fat—the bank continued to invest in technology, controls, and revenue-generating businesses while eliminating inefficiencies.

Rating agencies, those stern judges of banking credibility, were finally believers. Five rating improvements in 2024 alone validated the transformation. S&P's upgrade in December 2023 was particularly significant, recognizing not just improved metrics but structural change in how the bank operated.

Yet challenges remained formidable. The European banking sector still faced structural headwinds—negative rates for years had damaged profitability, American banks dominated capital markets, and the German economy struggled with stagnation. Deutsche Bank's share price, while recovered from crisis lows, still traded at a significant discount to book value, suggesting investors remained skeptical about long-term value creation.

The competitive landscape had also shifted dramatically. While Deutsche Bank was restructuring, American banks had grown even more dominant. JPMorgan's investment banking revenues alone dwarfed Deutsche Bank's entire investment bank. In Europe, BNP Paribas and Barclays had gained market share while Deutsche was retrenching. The question wasn't whether Deutsche Bank had stabilized—it clearly had—but whether it could grow from this new, smaller base.

Most critically, the cultural transformation remained incomplete. While Sewing had changed the tone at the top, turning around an institution with over 80,000 employees took time. The bank still faced occasional compliance lapses, evidence that the risk-taking culture of the past hadn't been entirely exorcised. The challenge was maintaining discipline while competing aggressively—walking the tightrope between prudence and profit.

As 2025 progressed, Deutsche Bank stood at an inflection point. The crisis era was definitively over, the restructuring largely complete. What came next would determine whether Deutsche Bank could reclaim its position as a European champion or would remain a cautionary tale of imperial overreach. The foundation Sewing had built was solid, but the superstructure remained to be constructed.

IX. Playbook: Lessons from the Brink

Deutsche Bank's journey from near-death to recovery offers a masterclass in both how to destroy a financial institution and how to resurrect one. The lessons are written in billions of losses, thousands of ruined careers, and ultimately, in the grinding work of transformation. For investors, executives, and students of financial history, Deutsche Bank's playbook reads like a manual of what not to do—until the final chapters.

The Dangers of Cultural Misalignment in M&A

The Bankers Trust acquisition in 1999 stands as one of the most destructive deals in banking history—not because of the price paid or the assets acquired, but because of the cultural poison it injected into Deutsche Bank's bloodstream. When you acquire an institution, you acquire its culture. Deutsche Bank thought it was buying expertise; it bought a trading mentality that would ultimately consume the acquiring institution.

The lesson is stark: cultural due diligence matters more than financial due diligence. Bankers Trust brought a winner-take-all mentality, a focus on short-term profits, and a casual relationship with rules that metastasized throughout Deutsche Bank. The German executives never truly controlled the Anglo-Saxon trading culture they imported. Instead, that culture controlled them, driving decisions that would cost tens of billions in fines and nearly destroy the institution.

Why "Too Big to Fail" Doesn't Mean "Too Big to Suffer"

Deutsche Bank learned that systemic importance provides no immunity from consequences. The bank avoided a government bailout in 2008, but the price of that independence was a decade of suffering. Being too big to fail meant regulators scrutinized every transaction, prosecutors pursued every violation, and markets punished every misstep more severely than they would for smaller institutions.

The approximately $20 billion in fines and settlements Deutsche Bank paid represents more than just financial penalties—it's the cost of believing that size provides protection. Every major violation, from LIBOR manipulation to Russian money laundering, was magnified by Deutsche Bank's systemic importance. Regulators made an example of the bank precisely because it was too big to fail.

The Cost of Regulatory Violations

The numbers are staggering but the true cost goes beyond money. The $7.2 billion DOJ settlement for mortgage securities, the $2.5 billion in LIBOR fines, the endless investigations—these created a perpetual crisis atmosphere that made normal business impossible. Talented employees left, clients defected to competitors, and the share price collapsed.

But perhaps the most insidious cost was the destruction of institutional confidence. When compliance becomes a daily crisis rather than a background function, when every email might become evidence, when regulators are permanently embedded in your offices, the organization becomes paralyzed. Deutsche Bank spent years in this purgatory, unable to move forward while constantly relitigating the past.

Importance of Risk Management and Compliance Infrastructure

The transformation under Sewing revealed a profound truth: risk management isn't a cost center but a profit center. By 2024, Deutsche Bank employed more compliance officers than it had traders at the peak of the Ackermann era. This wasn't bureaucratic bloat but necessary infrastructure for a global bank.

The bank learned that risk management must be embedded in the business, not imposed upon it. The old model—where risk managers were seen as "business preventers"—created an adversarial dynamic that encouraged circumvention. The new model makes risk management a partnership, where business heads own their risks and compliance provides tools rather than obstacles.

Leadership Continuity vs. Transformation Needs

The revolving door of leadership from 2012 to 2018—Jain/Fitschen, then Cryan, then Sewing—illustrates the tension between continuity and change. Each leadership change reset the strategic clock, confused employees, and delayed necessary decisions. Yet bringing in outsiders like Cryan also failed because they lacked institutional knowledge and credibility.

Sewing's success suggests that transformation requires an insider-outsider paradox: someone with deep institutional knowledge but willing to challenge institutional orthodoxy. As a lifetime Deutsche banker, Sewing had credibility with German staff and regulators. But his willingness to shut down entire businesses showed he wasn't captured by institutional inertia.

Managing Stakeholder Expectations During Multi-Year Turnarounds

Deutsche Bank's transformation took seven years from the depths of the 2015 crisis to achieving sustainable profitability. Managing stakeholder patience over such a timeline requires extraordinary communication discipline. Sewing's approach—under-promise and over-deliver—rebuilt credibility incrementally.

The contrast with Ackermann's era is instructive. Ackermann's promise of 25% return on equity created expectations that drove destructive behavior. Sewing's more modest targets—10% RoTE by 2025—were achievable and sustainable. The lesson: in turnarounds, credibility matters more than ambition.

The Challenge of Maintaining Talent During Restructuring

Cutting 18,000 jobs while trying to compete in talent-intensive businesses like investment banking creates an impossible dynamic. The best people have options and leave first. The mediocre stay and hope to survive. Deutsche Bank's solution was selective protection—identifying core businesses and protecting key talent there while cutting aggressively elsewhere.

But the deeper challenge was psychological. How do you motivate employees when the share price has collapsed, when media coverage is relentlessly negative, when competitors are poaching your best people? Sewing's answer was purpose—returning Deutsche Bank to its roots as a "Global Hausbank" gave employees something to believe in beyond just financial metrics.

The Hidden Costs of Complexity

At its peak, Deutsche Bank operated in over 70 countries with more than 100,000 employees. The complexity wasn't just operational but cognitive—no one truly understood the entire institution. Risks emerged from interactions between businesses that no one fully comprehended. The Leveraged Super Senior trades that helped bring down the bank were approved by committees that didn't understand what they were approving.

Sewing's radical simplification—exiting entire businesses, withdrawing from countries, reducing products—wasn't just cost-cutting but complexity reduction. A simpler bank is a more manageable bank. The lesson for all financial institutions: complexity is a risk that doesn't appear on any risk report but can destroy you nonetheless.

The Path Dependency of Strategic Choices

Every strategic choice creates path dependencies that constrain future options. Deutsche Bank's decision to become a global investment bank in the 1990s created constituencies—traders, bankers, investors—that made reversal extremely difficult. Even when the strategy was clearly failing, these constituencies fought to preserve it.

Breaking path dependency requires crisis. Only when Deutsche Bank faced existential threat in 2018-2019 could Sewing make radical changes. The lesson is sobering: sometimes organizations cannot change until they have no other choice. The art of leadership is recognizing the need for change before crisis makes it mandatory.

X. Bear vs. Bull Case

The investment case for Deutsche Bank in 2025 presents a fascinating study in contrasts. After one of the most dramatic destructions of shareholder value in banking history, the bank now trades at a fraction of book value despite demonstrating operational improvement. The bear and bull cases are equally compelling, reflecting genuine uncertainty about whether Deutsche Bank's transformation is sustainable or merely a temporary reprieve.

Bear Case: The Structural Pessimist's View

The bear case begins with European banking's structural challenges. European banks face a toxic combination of negative rates (until recently), aggressive regulation, fragmented markets, and competition from better-capitalized American rivals. Deutsche Bank, as a prime example of European banking's struggles, cannot escape these sector-wide headwinds. Even with perfect execution, the bank operates in an environment that structurally disadvantages it versus American competitors.

The interest rate environment, despite recent ECB hikes, remains challenging. While rising rates initially helped margins, the ECB is likely to cut rates again as European growth slows. Deutsche Bank's renewed profitability depends partly on the rate environment remaining favorable. A return to negative rates would devastating for a bank that has finally achieved sustainable returns.

The litigation tail risks, while reduced, haven't disappeared entirely. Deutsche Bank's history means that every regulatory investigation, every compliance lapse, every market downturn brings renewed scrutiny. The bank paid €2 billion for Postbank litigation in 2024—a reminder that ghosts from the past continue to extract costs. What other skeletons remain in the closet?

Competition from US banks in investment banking remains overwhelming. Despite Deutsche Bank's recent growth, its investment banking market share remains a fraction of JPMorgan, Goldman Sachs, or Morgan Stanley. These American giants have scale advantages, technology investments, and client relationships that Deutsche Bank cannot match. In a business where scale matters, being subscale is a permanent disadvantage.

German economic stagnation poses particular risks. Deutsche Bank's renewed focus on being a "Global Hausbank" ties its fortune to Germany's economic performance. But Germany faces structural challenges: an aging population, dependence on manufacturing in a digitalizing world, energy costs from the Ukraine war, and political paralysis. If Germany stagnates, can Deutsche Bank thrive?

The share price discount to book value reflects persistent skepticism. Despite operational improvements, Deutsche Bank trades at approximately 45% of tangible book value. This suggests markets don't believe the bank can sustain returns above its cost of capital. The discount becomes self-fulfilling—making it harder to attract talent, retain clients, and compete for deals.

Cultural transformation remains incomplete. While Sewing has changed the tone at the top, turning around an 80,000-person organization takes a generation. The occasional compliance lapses, the continued complexity, the struggle to generate consistent returns—all suggest the cultural transformation remains a work in progress.

Finally, the bear case rests on competitive dynamics. While Deutsche Bank was restructuring, competitors were growing. BNP Paribas, Barclays, and even smaller European banks gained market share. In America, JPMorgan's investment bank alone generates more revenue than all of Deutsche Bank. The competitive gap hasn't narrowed; it's widened.

Bull Case: The Transformation Believer's View

The bull case begins with tangible evidence of transformation. Deutsche Bank has achieved €30 billion in capital efficiency measures—real, measurable improvements in how the bank operates. The cost base has been reduced from €39 billion at peak to sustainable levels. The bank has returned to consistent profitability after years of losses. These aren't promises but delivered results.

The diversified revenue streams finally work as intended. Unlike pure investment banks that suffer in market downturns, Deutsche Bank's four-pillar model—corporate banking, investment banking, private banking, and asset management—provides stability. The 2025 first quarter results showed all four businesses contributing to profit growth. This diversification, long a weakness, has become a strength.

Deutsche Bank's strong position in German corporate banking provides a competitive moat. As Germany's Hausbank, Deutsche has relationships with the Mittelstand—Germany's mid-sized industrial champions—that American banks cannot replicate. These relationships, built over decades, provide stable revenues and cross-selling opportunities.

The investment banking momentum is building. Despite exiting equities, the remaining fixed income and advisory businesses are gaining share. The 30% revenue growth in Q4 2024 and 15% full-year growth show that focused investment banking can succeed. Deutsche Bank doesn't need to compete with JPMorgan across all products—it needs to excel in selected areas.

Management credibility under Sewing has been restored. Unlike previous CEOs who over-promised and under-delivered, Sewing has consistently met or exceeded targets. This credibility creates a virtuous cycle—investors believe in the strategy, employees believe in the leadership, and clients believe in the bank's stability.

The capital return story is compelling. €5.4 billion returned to shareholders since 2022 demonstrates that Deutsche Bank can generate excess capital. The 50% dividend increase and continued buybacks show management confidence. For value investors, a bank trading at less than half of book value while returning significant capital presents an attractive opportunity.

Technology investments are beginning to pay off. While less visible than trading revenues, Deutsche Bank's investments in digital banking, process automation, and data analytics are improving efficiency and customer experience. These investments, painful during the restructuring, position the bank for the digital future.

The regulatory relationship has normalized. After years as a regulatory pariah, Deutsche Bank's relationship with supervisors has stabilized. The five rating upgrades in 2024 reflect not just improved metrics but improved regulatory confidence. This normalization reduces both costs and uncertainty.

The Balanced View: Probability-Weighted Outcomes

The reality likely lies between these extremes. Deutsche Bank has clearly stabilized and returned to profitability, but whether it can generate returns above its cost of capital consistently remains uncertain. The bank faces structural headwinds but has also demonstrated operational resilience.

The key variables to watch are: - European interest rates and economic growth - Market share trends in investment banking - Success in cost reduction initiatives - Ability to grow fee-based revenues - Any new regulatory or litigation surprises - Success in technology transformation

For investors, Deutsche Bank represents a classic "option on recovery" trade. If Sewing's transformation succeeds, the stock could double or triple from current levels just by returning to book value. If the transformation fails, further value destruction is possible but limited given how much has already been destroyed.

The bear case is backward-looking, focused on past failures and structural challenges. The bull case is forward-looking, focused on transformation progress and future potential. The truth is that both cases have merit, making Deutsche Bank one of the most interesting and controversial investment cases in global banking.

XI. Epilogue: What's Next?

As Deutsche Bank enters the final year of its 2025 transformation plan, the institution stands at a crucial juncture. The emergency surgery is complete, the patient has stabilized, but the question remains: can Deutsche Bank thrive rather than merely survive? The answer will determine not just the fate of one bank but potentially the future of European banking itself.

The 2025 Inflection Point

The year 2025 represents more than just the end of Sewing's transformation plan—it's a moment of truth for the entire strategy. The bank has promised to achieve a return on tangible equity above 10%, a cost-income ratio below 65%, and revenues around €32 billion. Early indicators suggest these targets are achievable. The Q1 2025 results, with 11.9% RoTE and the best quarterly profit in fourteen years, provide confidence.

But meeting 2025 targets is just the beginning. The real question is what comes next. Sewing has stabilized the bank, but stability isn't a strategy. Deutsche Bank needs a vision for growth beyond 2025, a narrative that excites investors, attracts talent, and differentiates it from competitors. The "Global Hausbank" positioning works for stabilization but may not inspire growth.

M&A Scenarios in European Banking Consolidation

European banking consolidation, long predicted but never realized, may finally be approaching. The combination of Credit Suisse and UBS, while forced by crisis, broke a psychological barrier. European regulators, previously hostile to cross-border mergers, now recognize that European banks need scale to compete globally.

Deutsche Bank could play multiple roles in this consolidation. As an acquirer, it could absorb smaller German banks or expand into adjacent markets. A merger with Commerzbank, long speculated, would create a German national champion but face political and execution challenges. Cross-border deals with banks like Société Générale or even distressed Italian banks could provide growth but carry integration risks.

As a target, Deutsche Bank's improved operational performance and cleaned-up balance sheet make it more attractive. An American bank seeking European presence might view Deutsche as a platform for expansion. Or a larger European bank might see opportunity in Deutsche's corporate banking franchise and selectively strong capital markets capabilities.

The most likely scenario may be Deutsche Bank as a consolidator of specific capabilities rather than entire institutions. Acquiring boutique advisory firms, specialized trading desks, or wealth management operations could provide growth without the complexity of large mergers. This "string of pearls" approach would align with Sewing's philosophy of controlled, manageable expansion.

Technology Transformation Imperatives

The technology challenge facing Deutsche Bank—and all traditional banks—is existential. Fintech companies, neo-banks, and technology giants are disaggregating the banking value chain. Deutsche Bank must transform from a bank that uses technology to a technology company that does banking.

The cloud migration, while expensive and complex, is just table stakes. The real transformation involves artificial intelligence, machine learning, and data analytics. Deutsche Bank's vast data assets—decades of client relationships, transaction patterns, market behaviors—represent untapped value. But extracting that value requires capabilities the bank is still building.

The partnership versus build decision looms large. Should Deutsche Bank develop proprietary technology or partner with technology companies? The bank's recent partnerships with Google Cloud and others suggest a hybrid approach. But managing these partnerships while maintaining competitive differentiation requires sophistication that traditional banks often lack.

Cybersecurity represents both a cost and an existential risk. As banks digitize, they become more vulnerable to cyber attacks. Deutsche Bank, given its history and importance, is a prime target. Investment in cybersecurity is non-negotiable, but it's a cost that doesn't directly generate revenue—a challenging dynamic for a bank still focused on cost reduction.

ESG and Sustainable Finance Opportunities

Environmental, Social, and Governance (ESG) considerations have moved from periphery to center of banking strategy. Deutsche Bank's target of €500 billion in sustainable financing by 2025 represents both an obligation and an opportunity. The bank has reached €373 billion by end-2024, suggesting the target is achievable.

But sustainable finance is more than just green bonds and ESG loans. It's about fundamentally reimagining the role of banking in society. Deutsche Bank's history—particularly its Nazi-era involvement—makes this transformation especially important. The bank must prove it can be a force for positive social impact, not just profit generation.

The challenge is balancing ESG commitments with commercial reality. Many of Deutsche Bank's traditional clients—German industrial companies—face difficult transitions to sustainability. Supporting these transitions while maintaining profitability requires nuanced judgment. Too aggressive on ESG risks alienating clients; too lenient risks regulatory and reputational damage.

Climate risk is becoming credit risk. Deutsche Bank must assess not just the immediate creditworthiness of borrowers but their resilience to climate change. This requires new models, new expertise, and new ways of thinking about risk. The banks that master climate risk assessment will have competitive advantages; those that don't face potentially catastrophic losses.

The Leadership Succession Question

Christian Sewing's contract runs through 2026, but succession planning must begin now. The next CEO will inherit a stabilized but not yet thriving institution. They'll need different skills than Sewing—less crisis management, more growth generation. The choice will signal Deutsche Bank's direction for the next decade.

An internal candidate would provide continuity and institutional knowledge. Several of Sewing's lieutenants have emerged as potential successors, having proven themselves during the transformation. But internal candidates might lack the fresh perspective needed for the next phase.

An external candidate could bring new energy and ideas but risks disrupting the fragile stability Sewing has achieved. The failed external hires of the past—particularly John Cryan—serve as cautionary tales. Any external candidate would need to understand German culture, European banking, and Deutsche Bank's unique position.

The ideal might be an internal candidate with significant external experience—someone who understands Deutsche Bank but isn't captured by it. This combination of insider knowledge and outsider perspective could provide the best foundation for growth beyond stabilization.

Final Reflections

Deutsche Bank's journey from 1870 to 2025 encompasses the entire arc of modern capitalism—from industrial revolution to financial revolution to digital revolution. The bank has been protagonist and antagonist, hero and villain, creator and destroyer of value. Its story is Germany's story, Europe's story, and in many ways, the story of global finance itself.

The transformation under Christian Sewing proves that even the most troubled institutions can recover with determined leadership, clear strategy, and disciplined execution. But recovery isn't redemption. Deutsche Bank must still prove it can create sustainable value, serve society positively, and justify its existence in a rapidly changing financial landscape.

The challenges ahead—technological disruption, climate transition, demographic change, geopolitical uncertainty—are formidable. But Deutsche Bank has survived the Franco-Prussian War, two World Wars, hyperinflation, division, reunification, and its own near-death experience. This resilience, hard-earned through crisis, may be its greatest asset.

As investors evaluate Deutsche Bank in 2025 and beyond, they're not just assessing financial metrics but judging whether one of history's most important financial institutions can write a final chapter worthy of its complex legacy. The story isn't over. In many ways, it's just beginning again.

XII. Recent News

Q2 2025 Performance and Market ReactionThe second quarter of 2025 delivered further evidence of Deutsche Bank's operational momentum. Net profit attributable to shareholders reached 1.485 billion euros ($1.748 billion) in the second quarter, versus a 1.2 billion forecast from Reuters. The bank more than doubled its first-half 2025 profit before tax to €5.3 billion, demonstrating sustained improvement across all business lines.

The results showed both strength and challenges. In fixed income and currencies, the bank posted a "strong" 11% revenue bump driven by higher net interest income in financing and increased volatility and client activity in foreign exchange. However, Deutsche Bank's origination and advisory division logged a second-quarter revenue decline of 29% to 416 million euros, citing "market uncertainty" and noting an overall "postponement of some material transactions into the second half of 2025."

Market reaction was decisively positive. Following the announcement, Deutsche Bank's stock price surged by 7.11% in pre-market trading, reflecting investor optimism. The bank, with a market capitalization of $70 billion, has demonstrated remarkable momentum, delivering a 128% return over the past year. The shares reached their highest level since April 2015, a clear vote of confidence in Sewing's strategy.

Management Changes and Strategic Appointments

In March 2025, Deutsche Bank announced significant management board changes to prepare for the next phase of growth. The appointments signal a shift from crisis management to growth generation, with new leaders brought in to drive expansion in key areas. These changes, while maintaining continuity under Sewing's leadership, bring fresh perspectives to critical business lines.

Regulatory Developments and Capital Management

The Common Equity Tier 1 (CET1) capital ratio was 14.2% at the end of the second quarter, up from 13.8% in the first quarter of 2025. The quarter-on-quarter development reflected strong organic capital generation through retained earnings which more than offset deductions for Additional Tier 1 (AT1) coupon payments and dividends. At its Annual General Meeting on May 22, 2025, Deutsche Bank announced its intention to maintain a CET1 ratio within an operating range of 13.5% to 14.0% while adhering to its commitment to a 50% payout ratio.

The bank's capital strength enabled continued shareholder returns. The bank has completed the majority of its current € 750 million share repurchase program and has sought supervisory approval for a second share repurchase program in 2025. This would, if approved, enable capital distributions in excess of the € 2.1 billion completed or anticipated in 2025 from dividends and share repurchases under the current program.

Market Share Gains and Competitive Positioning

Despite challenges in certain areas, Deutsche Bank continued to gain market share in key businesses. The bank maintained its number one ranking in Germany for investment banking and won multiple industry awards, including Europe's Best Investment Bank from Euromoney. These accolades, while symbolic, reflect genuine improvement in competitive positioning.

The Fixed Income and Currencies business, in particular, showed remarkable resilience. Record revenues in Q1 2025 followed by strong Q2 performance demonstrated that Deutsche Bank's focused approach—competing selectively rather than universally—was working. The bank doesn't need to beat JPMorgan everywhere; it needs to win in chosen markets.

Strategic Initiatives and Technology Investments

The operational efficiency program achieved significant milestones. At the end of the first half of 2025, cumulative savings either realized or expected from completed efficiency measures grew to € 2.2 billion, approximately 90% of the program's expected total savings. More importantly, Deutsche Bank delivered RWA reductions of a further € 2 billion during the quarter, predominantly through two securitization transactions. As a result, cumulative RWA equivalent benefits from capital efficiency measures reached € 30 billion, the high end of the bank's year-end 2025 target range of € 25-30 billion.

Industry Recognition and ESG Progress

Deutsche Bank's transformation gained external validation through multiple channels. Rating agencies continued their positive reassessments, industry surveys showed improved client satisfaction, and talent retention improved markedly. The bank's ESG initiatives, particularly in sustainable finance, positioned it as a leader in the transition to a low-carbon economy.

The cumulative sustainable financing volume approaching €400 billion demonstrated that ESG wasn't just compliance but a business opportunity. German corporate clients, facing their own energy transitions, increasingly turned to Deutsche Bank for advice and financing. This alignment of social responsibility with commercial opportunity represents the best of the "Global Hausbank" strategy.

XIII. Links & Resources

Official Deutsche Bank Resources - Annual Reports and Investor Presentations: investor-relations.db.com - Quarterly Financial Data Supplements and Earnings Reports - Sustainability Reports and ESG Frameworks - Historical Archive and Timeline

Key Books on Deutsche Bank History - "Dark Towers: Deutsche Bank, Donald Trump, and an Epic Trail of Destruction" by David Enrich (2020) - "The Deutsche Bank and the Nazi Economic War Against the Jews" by Harold James (2001) - "A History of Deutsche Bank 1870-1995" by Lothar Gall et al. - "The Nazi Dictatorship and the Deutsche Bank" by Harold James (2003)

Regulatory Filings and Settlement Documents - U.S. Department of Justice Settlement Documents (2017) - LIBOR Manipulation Investigation Files - European Central Bank Supervisory Reviews - BaFin (German Federal Financial Supervisory Authority) Reports - SEC Form 20-F Annual Filings

Industry Analysis and Research Reports - Moody's, S&P, and Fitch Rating Reports - Euromoney Banking Surveys and Rankings - IMF Financial Sector Assessment Program Reports - Bank for International Settlements Working Papers

Documentary Recommendations - "The Big Short" (2015) - Features Deutsche Bank's role in the mortgage crisis - "Inside Job" (2010) - Examines the 2008 financial crisis - Various investigative documentaries by German broadcasters ZDF and ARD

Academic Papers on European Banking - "The Political Economy of European Banking Union" - Multiple authors - "Deutsche Bank's Transformation: A Case Study" - Various business schools - "Regulatory Capture in European Banking" - Academic journals - "The Cost of Being a Global Systemically Important Bank"

Journalist Investigations and Exposés - Financial Times Deutsche Bank Investigation Series - Wall Street Journal coverage of regulatory violations - Der Spiegel investigations into German banking - New York Times coverage of money laundering scandals

Historical Archives and Primary Sources - Deutsche Bank Historical Institute Archive - German Federal Archives (Bundesarchiv) - U.S. National Archives (OMGUS files on post-war Germany) - Contemporary newspaper coverage from 1870-present

Competitor Analysis Resources - JPMorgan Chase Investor Relations - Bank of America Annual Reports - European Banking Authority Comparative Analysis - Coalition Greenwich Competitive Analytics

Industry Data and Market Intelligence - Dealogic Investment Banking League Tables - Refinitiv Banking Analytics - Bloomberg Terminal Resources - S&P Market Intelligence

Regulatory and Compliance Resources - Basel Committee on Banking Supervision Publications - European Banking Authority Guidelines - Federal Reserve Supervisory Assessments - Financial Stability Board Reports on SIFIs

Technology and Innovation Resources - McKinsey Global Banking Annual Review - Deloitte Banking Industry Outlooks - Fintech Partnership Case Studies - Digital Banking Transformation Reports

Climate Transition and ESG Imperatives

Deutsche Bank's September 2025 update to its Transition Plan maintained the bank's commitment to net zero goals, demonstrating that ESG considerations have become central to strategic planning rather than peripheral compliance exercises. Chief Sustainability Officer Jörg Eigendorf framed this commitment not just as "societal responsibility but also as part of a prudent risk management practice as well as a business opportunity".

The implementation has moved beyond rhetoric to operational integration. The bank implemented Divisional Carbon Budgets in the corporate bank and investment bank, integrating these carbon budgets into the compensation program for the Management Board. This linkage between executive compensation and climate goals represents a fundamental shift in how banks incentivize behavior—environmental performance now directly affects leadership remuneration.

Deutsche Bank achieved a 79% reduction in Scope 1 and 2 emissions, and a 45% reduction in Scope 3 emissions (other than financed emissions) since 2019, though managing financed emissions remains the primary challenge. The bank's €118 billion corporate loan portfolio represents 93% of financed emissions, with its €166 billion European residential real estate portfolio accounting for 7%.

The approach to high-emitting clients reveals the nuanced challenge facing all banks in the energy transition. Deutsche Bank outlined its strategy to systematically reduce financing of carbon intensive activities while growing financing for transition activities, including engaging with high-emitting clients to support their decarbonization and reviewing engagement with clients unwilling or unable to transition—with responsibly phasing out high-emitting assets as a last resort.

Technology Infrastructure Revolution

The technology transformation under Chief Technology, Data and Innovation Officer Bernd Leukert represents more than modernization—it's a fundamental reimagining of Deutsche Bank as a technology company. The bank focused on three major pillars: Cloud, AI and Talent, closely linked and underpinned by the vast amounts of data flowing through the bank daily.

In May 2025, Deutsche Bank announced a strategic agreement with IBM granting access to IBM's comprehensive suite of software solutions, including IBM's business and IT automation stack, advanced hybrid cloud products, and the watsonx AI portfolio. Tony Kerrison, Deutsche Bank's Head of Group Technology Infrastructure, called IBM "a natural partner for Deutsche Bank's ambitious technology transformation," noting their solutions help "modernize, simplify and strengthen our technology infrastructure".

The cloud migration has delivered tangible benefits. The migration of 17 financial reporting systems, including the strategic general ledger, resulted in data processing improvements of up to 50% and reduced recovery time by a factor of 16-20. In collaboration with Google Cloud, Deutsche Bank developed solutions allowing classic on-premise applications like the Autobahn FX electronic trading platform to benefit from hybrid-cloud solutions.

The AI adoption has been particularly aggressive. Over 11,000 colleagues completed AI Foundations training, with no technical background required. The Technology, Data and Innovation division runs a central programme to lay the foundation for safe AI adoption, including technical and operational standards, guardrails, and an AI platform with scalable shared services to prevent different areas from implementing similar solutions.

The Digital Customer Revolution

The transformation extends beyond back-office technology to customer-facing innovation. Deutsche Bank's app will be comprehensively renewed in 2025 and supplemented with further digital services. "Our customers expect a modern and fully digitized offering, but at the same time want the possibility of personal advice via the access channel of their choice. By completing more and more simple banking transactions digitally, we can concentrate fully on advising our customers through personal contact", explained the bank's retail leadership.

The Personal Banking division continues a "major efficiency transformation" begun in 2021, closing 400 branches since 2021, including 125 in 2024. While closing smaller branches, the bank is adding new formats and technologies, increasing capacity to advise via video and telephone, and adding private banking centers, modern ATMs and community events to remaining branches.

China and International Expansion

Deutsche Bank's position in China demonstrates how the "Global Hausbank" strategy works in practice. Deutsche Bank China successfully implemented the new foreign currency cross-border liberalization framework at branches in Shanghai, Beijing, and Guangzhou, becoming the first European Union bank to fully implement reforms under SAFE's "1+6" foreign currency policy framework.

Under the new framework, eligible corporations can complete cross-border transactions by simply submitting payment instructions, with processing times reduced from several days to just minutes, greatly improving liquidity management and operational speed. Rose Zhu, Deutsche Bank China Chief Country Officer, noted this "strengthens our ability to deliver local execution, risk control, and compliance capabilities for multinational clients, helping them manage cross-border operations and treasury functions in China more efficiently".

2025 Target Validation and Market Response

The second quarter 2025 results provided crucial validation of the transformation trajectory. Net profit attributable to shareholders reached 1.485 billion euros in Q2, versus a 1.2 billion forecast from Reuters, with the bank more than doubling first-half 2025 profit before tax to €5.3 billion. The momentum continued from Q1, where net profit reached 1.775 billion euros, up 39% year-on-year and above analyst expectations of 1.64 billion euros.

The bank maintained its CET1 capital ratio at 13.8% while achieving a post-tax return on tangible equity of 11.9%, exceeding its 10% target for 2025. This achievement of double-digit returns represents a watershed moment—proof that the transformation has delivered sustainable profitability.