Datagroup SE: The Mittelstand's IT Engine

I. Introduction: The Hidden Backbone of German Industry

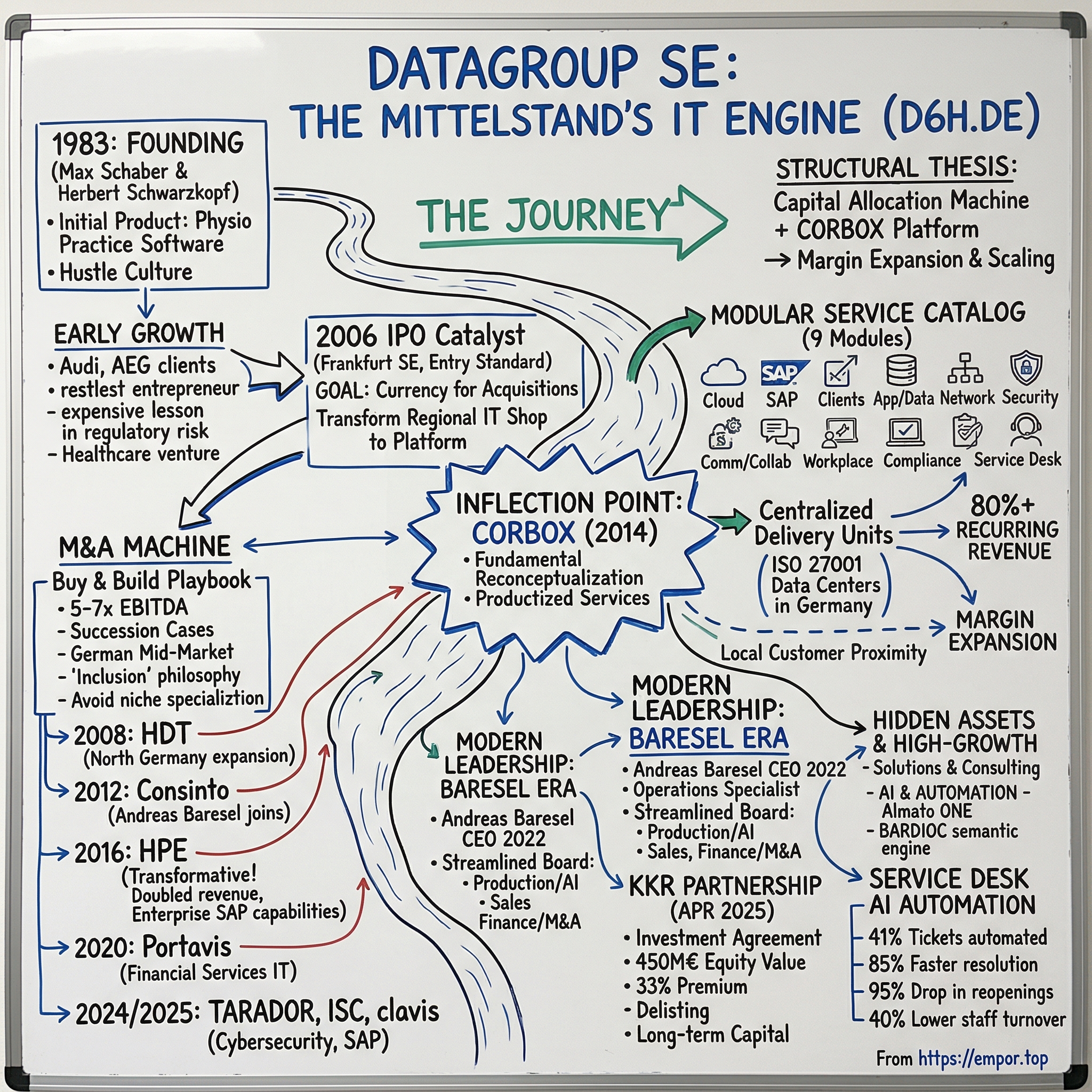

Somewhere in the rolling hills of Baden-Württemberg, about twenty minutes south of Stuttgart, sits a sleek, Hugo-Häring Prize-winning office building in the small town of Pliezhausen. No neon logos. No campus shuttles. No kombucha bar. Just a quiet headquarters running one of the most effective capital allocation machines in European IT services. This is Datagroup SE, and if you have never heard of it, that is sort of the point.

While the world fixates on Silicon Valley's latest AI darling or the next trillion-dollar hyperscaler, something equally consequential is happening in the heart of Europe. Germany's famed Mittelstand—the vast ecosystem of roughly 3.5 million small and medium-sized enterprises that collectively form the backbone of Europe's largest economy—is undergoing a generational digital transformation. These are the companies that make the precision bearings inside your car's transmission, the chemical coatings on solar panels, the specialized pumps in municipal water systems. They are world-class at what they do. What they are decidedly not world-class at is running their own IT infrastructure.

That gap—between industrial excellence and digital immaturity—is the trillion-dollar opportunity. And Datagroup has spent two decades positioning itself as the company that fills it.

The numbers tell a compelling story. Revenue has grown from roughly thirty million euros at its 2006 IPO to over 560 million euros in fiscal year 2025. The company has completed more than thirty-four acquisitions. Over eighty percent of its revenue is recurring, locked into long-term service contracts. EBITDA margins have expanded from the low teens into the mid-teens, a trajectory that speaks to the operating leverage inherent in productized services. And in April 2025, KKR—the legendary private equity firm—signed an investment agreement valuing Datagroup at approximately 450 million euros in equity, offering a thirty-three percent premium to the prevailing share price.

But the financial metrics, impressive as they are, only tell half the story. The real thesis on Datagroup is structural. This is not merely an IT company that happens to be growing. It is a capital allocation machine purpose-built to roll up one of the most fragmented service markets in Europe. Every time a sixty-five-year-old founder of a regional IT firm in Bavaria or Saxony decides to retire—and there is no heir waiting in the wings—Datagroup's phone rings. They acquire the company at a reasonable multiple, migrate the customers onto their standardized CORBOX service platform, and watch the margins expand. Rinse. Repeat. Scale.

Think of it as the Constellation Software playbook, transplanted to the German IT services landscape. Or, if you prefer an American industrial analogy, a baby Danaher for digital infrastructure. The question is not whether the model works—nearly two decades of compounding have answered that. The question is how far the runway extends, and whether the company can keep its disciplined culture intact as it enters a new chapter under KKR's wing.

To answer that, we need to go back to the beginning—to a twenty-seven-year-old mechanical engineer in 1983 who just wanted to be his own boss.

II. Founding and The IPO Catalyst

The year was 1983. The personal computer revolution was barely underway in the United States, let alone in the Mittelstand heartland of Southern Germany. IBM had released its PC only two years earlier, and the idea that every mid-sized manufacturer would someday need an IT department was still the stuff of science fiction. Into this nascent market stepped Max Hans-Hermann Schaber, a freshly minted mechanical engineering graduate with a co-founder named Herbert Schwarzkopf and a company called Datapec Gesellschaft für Datenverarbeitung mbH. The name—a portmanteau referencing the personal computers beginning to appear on desks—was about as glamorous as the business itself.

Their first customer was a physiotherapy practice. Their first product was custom software to help that practice manage its appointments and billing. It was, by any measure, a modest beginning. But Schaber was not chasing a grand strategic vision. In his own words: "I only wanted to be self-employed." That honest pragmatism—the absence of messianic founder mythology—would prove to be a recurring theme in Datagroup's culture. This was never a company built on hype. It was built on hustle.

Within three years, that hustle had produced roughly eighty to one hundred employees and about ten million deutschmarks in revenue. Early clients included Audi and AEG—serious industrial names that lent credibility far beyond what the company's size would suggest. Through the late 1980s and into the 1990s, Schaber proved himself a restless entrepreneur. He ran Datapec like an incubator, founding more than ten companies across diverse verticals. One was a computer trading company that reached nearly one hundred million deutschmarks in turnover with six international branches—essentially an early e-commerce operation before anyone called it that. Another was KIS, a healthcare software venture that partnered with Hewlett Packard and Andersen Consulting to develop one of the first hospital information systems built on relational database technology, predating Oracle in that niche.

Not every bet worked. The healthcare venture, despite landing thirty-six hospital customers, ran headlong into a wall when German hospital financing reforms froze capital expenditure budgets. KIS was eventually sold to Jenoptik under, by Schaber's own admission, unfavorable terms. It was an expensive lesson in regulatory risk—and in the peril of building a business dependent on a single sector's willingness to spend. The scar tissue from that experience would later inform Datagroup's deliberate choice to avoid deep industry specialization in its acquisition targets.

By the early 2000s, Schaber had consolidated his various ventures under the Datagroup umbrella and was running what was essentially a regional IT system house—selling hardware, providing some services, managing relationships with mid-sized companies across Southern Germany. Revenues were respectable but not remarkable. The company was profitable but capital-constrained. And Schaber could see the writing on the wall: in a world where Dell and Lenovo would commoditize hardware margins to near zero, a company that primarily resold PCs and servers had a limited shelf life.

The answer was the 2006 IPO. On September 14 of that year, Datagroup listed on the Entry Standard segment of the Frankfurt Stock Exchange, issuing one million new shares. The company was generating around thirty million euros in revenue at the time—tiny by public market standards. But Schaber was not listing to cash out or to generate a vanity headline. He was listing to gain access to a currency: publicly traded stock. In the fragmented German IT services market, where hundreds of small firms operated with revenues between five and fifty million euros, the ability to use equity as acquisition consideration was a superpower. Cash-strapped private companies could not compete. Larger listed competitors like Bechtle and Cancom were playing a different game, focused more on hardware distribution and larger enterprise deals. Datagroup had found a seam.

The IPO was the inflection point that transformed a regional IT shop into an acquisition platform. Within two years, Datagroup made its first significant deal—HDT Hanseatische Datentechnik GmbH in 2008, which expanded the company's footprint from its Southern German base into the north, eventually becoming Datagroup Hamburg GmbH. The flywheel had started to turn.

What made this particularly clever was the timing. Germany's IT services market was—and remains—extraordinarily fragmented. Unlike the United States, where decades of consolidation had produced a handful of dominant systems integrators, Germany's market reflected the Mittelstand ethos of independence and regionalism. Hundreds of small IT firms had deep relationships with local businesses, providing everything from helpdesk support to SAP administration. But these firms faced a common problem: their founders were aging, and their businesses were too small to attract institutional buyers. The succession crisis that would define German business demographics for a generation was already visible to anyone paying attention. Schaber was paying attention.

III. The Inflection Point: CORBOX

Picture a typical Mittelstand company in 2012. Let us say it is a precision machinery manufacturer in the Ruhr Valley, employing four hundred people. The company makes the best hydraulic presses in Europe. Its engineers are world-class. Its IT department, however, consists of three overworked generalists who spend their days fighting fires—resetting passwords, patching servers that should have been replaced years ago, and struggling to keep an aging SAP installation from collapsing. The company's CEO knows IT matters, but it is not core to what makes the business special. What the CEO wants is simple: make the IT work, keep it secure, do not surprise me with the bill.

This was the universal pain point that Datagroup identified, and CORBOX was the answer.

Formally introduced in 2014, CORBOX represented a fundamental reconceptualization of how IT services could be delivered to mid-sized companies. The insight was almost embarrassingly simple in retrospect: every Mittelstand company needed roughly the same ten to twelve IT services. Cloud hosting. Cybersecurity. SAP management. A helpdesk. Network management. Workplace services for laptops and mobile devices. Collaboration tools. Compliance monitoring. The specifics varied at the margins, but the core menu was remarkably consistent across industries and company sizes.

Before CORBOX, most IT service providers—including Datagroup's own acquired companies—delivered these services through bespoke consulting engagements. Every customer got a custom proposal. Every contract was negotiated from scratch. Every delivery team reinvented the wheel. This approach had the virtue of flexibility but the vice of non-scalability. Labor utilization was unpredictable. Margins were inconsistent. And most critically, the business could not grow faster than it could hire and train consultants.

CORBOX flipped the model. Instead of bespoke consulting, Datagroup created a modular catalog of nine standardized service modules, each with precisely defined quality features, service levels, and pricing. A customer could select Cloud Services, add SAP Services, layer on Security Services, and bolt on a Service Desk—all from a standardized menu. Think of it as the difference between a custom-built house and a well-designed modular home: the customer gets high quality and some customization, but the provider gets repeatability and scale.

The nine modules that comprise CORBOX today are Cloud Services covering multi-cloud solutions from enterprise private to hyperscaler to sovereign cloud options; SAP Services for optimizing on-premise, cloud, or hybrid SAP landscapes; Application and Data Management for software support, development, and data platform operations; Network Services spanning connectivity across workstations, locations, and data centers; Security Services including a twenty-four-seven Security Operations Center with vulnerability management and endpoint detection; Communication and Collaboration built around Microsoft 365 management; Workplace Services covering client management, mobile devices, and virtual desktops; Compliance Services handling IT compliance reporting, identity management, and license management; and a Service Desk providing round-the-clock user support with certified processes.

The architectural elegance of CORBOX lies in how it combines local customer proximity with centralized delivery. The customer-facing relationship manager sits close to the client, understands their business, and speaks their industry language. But behind the scenes, the actual service delivery is handled by centralized, highly efficient supply units—one for the Service Desk, one for data center operations, one for SAP services, one for enterprise applications. These centralized units operate from ISO 27001-certified data centers located entirely within Germany, a critical selling point for Mittelstand companies increasingly concerned about data sovereignty and GDPR compliance.

The impact on Datagroup's business model was transformative. Before CORBOX, the company was valued—to the extent the market paid attention—as a hardware distributor with some services attached. After CORBOX, as recurring service revenue climbed past eighty percent of the total, the market began to re-rate the company as a managed services provider. The valuation multiple expansion that accompanies a shift from project-based to recurring revenue is one of the most powerful forces in business, and Datagroup rode it beautifully.

By fiscal year 2023/2024, the power of the CORBOX model was fully visible in the order book. The company reported record order intake of fifty million euros in combined new business and cross-selling—thirty-three new customer contracts worth twenty-six million euros and fifty-two cross-sell and upsell transactions worth another twenty-four million. These are not one-time project wins. They are multi-year service agreements with predictable revenue streams and high switching costs.

The genius of the model becomes even clearer when you understand how it interacts with Datagroup's acquisition strategy. When Datagroup acquires a small IT firm with, say, twenty million euros in revenue and a collection of bespoke customer relationships, the first thing it does is begin migrating those customers onto CORBOX. The customer gets a better, more standardized service with clearer SLAs and twenty-four-seven support. The acquired company's employees get access to centralized tools and training. And Datagroup gets margin expansion as the labor-intensive bespoke delivery model gives way to the platform-leveraged CORBOX model. It is an elegant arbitrage—buying at a low multiple based on the target's standalone economics, then improving those economics through platform integration.

CORBOX transformed Datagroup from a company that made acquisitions into a company that had a system for making acquisitions productive. That distinction is everything in the buy-and-build world.

IV. The M&A Machine: The Buy and Build Playbook

There is a particular type of deal that Datagroup has mastered, and it starts not in a boardroom but at a Stammtisch—the regular table at a local restaurant where German business owners gather to drink beer and discuss the world. The owner of a twenty-person IT company in Rosenheim or Bremen has been running his firm for thirty years. He built it from nothing, knows every customer by name, and has a team of loyal engineers who have been with him for decades. He is sixty-two years old. His children became doctors or lawyers. There is no successor.

This is the "succession case," and in Germany, it is not an edge case—it is the dominant dynamic in small and medium-sized IT services. The German demographic cliff, combined with the Mittelstand's cultural emphasis on founder-led businesses, has created a rolling wave of companies that need a new home. The founders do not want to sell to a faceless multinational that will gut the team and relocate the operations. They want a buyer who will preserve the culture, keep the employees, and continue serving the customers with care.

Datagroup has built its entire acquisition strategy around being that buyer. The company's stated criteria are remarkably specific: German-headquartered IT service providers serving the mid-market, with annual revenues between five and fifty million euros, strong recurring revenue streams, skilled technical workforces, regional customer relationships, and—critically—a non-specialized industry focus. They want generalists, not niche specialists, because generalist IT service providers are the easiest to integrate onto the CORBOX platform.

The integration philosophy itself is distinctive. Datagroup uses the word "inclusion" rather than "integration," and the distinction matters. Acquired companies are maintained as independent operating units under the Datagroup umbrella. They keep their names, at least initially. They keep their teams. They keep their customer relationships. A formalized process called "100 Days Datagroup" provides a structured but gentle onboarding that allows the acquired firm to continue normal operations with minimal disruption during the transition period. Over time, the acquired company's customers are migrated onto CORBOX, the back-office functions are consolidated, and the acquired team gains access to Datagroup's centralized delivery infrastructure. But the front-office identity and customer intimacy are preserved.

This approach directly addresses the single biggest risk in IT services M&A: customer attrition. When a company's IT service provider gets acquired, the natural instinct of the customer is fear. Will my contact person change? Will the service deteriorate? Will they raise prices? By maintaining the acquired firm's identity and team, Datagroup neutralizes these concerns. The customer barely notices the transition—until they realize their service has actually improved because their provider now has access to a twenty-four-seven SOC, enterprise-grade data centers, and a standardized service management framework they never had before.

The financial mechanics of the deals are equally disciplined. While global consulting giants like Accenture or Capgemini routinely pay twelve to fifteen times EBITDA for "hot" technology acquisitions, Datagroup operates in the decidedly unsexy five to seven times EBITDA range. The targets are not glamorous. They do not have proprietary AI models or viral consumer products. They have reliable service contracts with Mittelstand companies that need their SAP systems to work and their employees' laptops to turn on in the morning. The boring nature of these businesses is precisely what keeps the multiples low—and what makes the post-acquisition economics so attractive once the CORBOX platform does its work on margins.

Since the 2006 IPO, Datagroup has completed more than thirty-four acquisitions, a pace of roughly two per year. The deals have ranged from small tuck-ins to transformative transactions. The 2008 acquisition of HDT Hanseatische Datentechnik expanded the geographic footprint northward. The 2012 acquisition of Consinto GmbH—at the time the largest deal in company history—brought not just mid-sized IT consulting capabilities and its own data center, but also a future CEO: Andreas Baresel came to Datagroup through the Consinto transaction. The 2020 acquisition of a sixty-eight percent stake in Diebold Nixdorf Portavis GmbH added roughly two hundred employees, about sixty million euros in annual revenue, and a foothold in financial services IT, serving marquee clients like Hamburger Sparkasse and Hamburg Commercial Bank.

But the deal that truly put Datagroup on the map was the 2016 Hewlett Packard Enterprise transaction. On September 1 of that year, Datagroup took over approximately 330 SAP and application management specialists from HPE's German operations. The deal came with a guaranteed revenue volume in the "three-digit million euro range" over sixty-four months—more than five years of contractually committed revenue, with an option to extend for another twenty months.

The HPE deal was transformative on multiple dimensions. Financially, it roughly doubled Datagroup's revenue base and provided a long-duration revenue stream that de-risked the income statement. Strategically, it gave Datagroup enterprise-grade SAP capabilities that would have taken years to build organically. And reputationally, it proved that a mid-sized German IT service provider could credibly take over operations from one of the world's largest technology companies—and deliver. The market took notice. Revenue jumped from 175 million euros in fiscal 2016 to 224 million in fiscal 2017 and 273 million in fiscal 2018, with EBITDA margins expanding simultaneously.

The HPE deal also revealed something important about Datagroup's strategic positioning. Large multinational IT companies periodically shed regional service operations that are profitable but not strategic to their global ambitions. These "orphan" business units are too small for the parent to care about but too large for most regional players to absorb. Datagroup sits in the sweet spot—large enough to credibly operate enterprise-grade services, small enough that these deals move the needle on growth.

More recent acquisitions have reflected an evolution in the playbook. The 2024 acquisition of TARADOR GmbH, a cybersecurity service provider, added capabilities in one of the fastest-growing segments of IT services. The acquisition of ISC Innovative Systems Consulting AG, also in 2024, brought roughly fifty SAP specialists and twelve and a half million euros in revenue with a low double-digit EBIT margin—a classic bolt-on that strengthened the SAP practice. And in 2025, the acquisition of clavis continued the steady cadence.

What investors should recognize about the M&A machine is that it is not just a growth strategy—it is the growth strategy. Organic growth for an IT services company serving the German Mittelstand is structurally limited to the low-to-mid single digits. The market is mature. Customer budgets grow slowly. Pricing power is real but modest. The way to compound at double-digit rates in this environment is through disciplined, repeatable M&A combined with operational improvement of acquired assets. Datagroup has proven it can do both.

V. Modern Leadership: The Baresel Era

The transition from founder to professional manager is one of the most perilous passages in corporate life. The founder's vision, relationships, and institutional authority are irreplaceable—until they must be replaced. The history of European Mittelstand companies is littered with cautionary tales of brilliant founders who held on too long, or successors who lacked the credibility to maintain the culture.

Datagroup navigated this transition with unusual grace. In March 2022, Max Schaber stepped back from the Management Board and moved to the Supervisory Board, handing the CEO title to Andreas Baresel. The move was not abrupt. Baresel had been on the Management Board since October 2018, serving as Chief Production Officer—the executive responsible for the operational heart of the business. Before that, he had been running Consinto GmbH, the IT consulting firm he led before it was acquired by Datagroup in 2012. In other words, Baresel spent a decade inside the Datagroup ecosystem before taking the top job. He knew the culture, the people, the customers, and the integration playbook intimately.

Baresel's profile is telling. He is not a sales-driven, charisma-forward CEO of the type that often leads growth-stage technology companies. He is an operations and integration specialist—someone who understands how to take disparate IT service organizations and make them work together efficiently within a common framework. For a company whose core competency is acquiring and integrating IT firms, this is exactly the right skill set. The CEO of a buy-and-build platform does not need to be a visionary. He needs to be a systems thinker who can maintain discipline as the organization scales.

Under Baresel's leadership, the management structure has been refined for the next phase of growth. In 2024, the company reorganized its top management, creating two new divisional board positions alongside the statutory Management Board. Mark Schäfer, who joined in 2019 from a CISO role at T-Systems International, took responsibility for Production, IT Service Management, Governance Risk and Compliance, and—crucially—AI-based automation. Alexandra Mulders, with Datagroup since 2010, took charge of the Sales division with a mandate focused on organic growth and full-service outsourcing contracts. The statutory board was streamlined to two members: Baresel, responsible for Finance, M&A, Investor Relations, and service portfolio strategy; and Dr. Sabine Laukemann, responsible for Organization, Legal, Human Resources, Corporate Communications, and ESG.

This structure signals a maturation in how the company thinks about its growth levers. Rather than having a single CEO who does everything, the organization now has dedicated executive ownership of the four pillars that matter most: operations and automation, sales and organic growth, M&A and capital allocation, and organizational development. It is the kind of structure you see in well-run industrial conglomerates, and it is appropriate for where Datagroup sits in its lifecycle.

The governance alignment between management and ownership deserves particular attention. The Schaber family, through HHS Beteiligungsgesellschaft mbH, held 54.4 percent of Datagroup's shares as of 2025. This is not a widely held company with dispersed ownership and the attendant agency problems. This is a controlled company where the founding family's economic interests are overwhelmingly aligned with long-term value creation. The incentive structure has historically focused on EBITDA margin expansion and recurring revenue growth—the metrics that drive intrinsic value—rather than vanity top-line targets or short-term earnings per share management.

The KKR investment agreement, announced in April 2025, adds a new dimension to the governance picture. Under the deal structure, HHS transferred its 54.4 percent stake to Dante Beteiligungen SE, the KKR acquisition vehicle, with HHS and KKR becoming indirect fifty-fifty shareholders of the bidding entity. This means the Schaber family is not cashing out. They are rolling their equity into the new structure and partnering with KKR for the next chapter. The public purchase offer of fifty-four euros per share—later increased conditionally to up to fifty-eight euros at higher acceptance thresholds—was funded entirely with equity from KKR's funds, not debt.

The KKR partnership is significant for several reasons. First, it removes the quarterly reporting pressure of public markets and gives management the freedom to invest in longer-term transformation initiatives—including larger acquisitions and geographic expansion—without worrying about near-term earnings dilution. Second, it provides access to KKR's operational improvement playbook, a proven methodology for driving efficiency and growth in platform companies. Third, the all-equity funding means Datagroup is not being loaded up with leverage, a common criticism of private equity deals in the services sector. The company enters private ownership with a net debt to EBITDA ratio of approximately 2.2 times—elevated from the 1.7 times at fiscal year-end 2024, but hardly distressed territory for a business with eighty percent recurring revenue and strong cash conversion.

The delisting process was initiated in December 2025, marking the end of Datagroup's run as a public company. For long-term shareholders who rode the journey from thirty million euros in revenue to over five hundred sixty million, the returns were substantial. For the company itself, the transition to private ownership may prove to be the catalyst that unlocks the next phase of growth—larger deals, faster integration, and an accelerated push into AI-driven service delivery.

VI. Hidden Businesses and High-Growth Initiatives

Peel back the consolidated financial statements of any successful roll-up and you will find businesses within the business—units and capabilities that the market either misunderstands or overlooks entirely. Datagroup is no exception.

The core of the enterprise is the Managed Services segment, powered by CORBOX. This is the cash cow—predictable, high-retention, margin-rich. When a Mittelstand company signs a CORBOX contract, they are typically committing to a multi-year engagement covering the full spectrum of their IT infrastructure needs. The switching costs are enormous. Once a company's SAP landscape, cloud infrastructure, security monitoring, and helpdesk operations are running on Datagroup's platform, the cost and disruption of migrating to a competitor are effectively prohibitive. This is not a hypothetical moat—it is an operational reality confirmed by the company's consistently high renewal rates and the fact that customer satisfaction rankings from Whitelane Research placed Datagroup among the top performers in Germany for nine consecutive years.

Alongside the managed services cash cow sits a Solutions and Consulting segment that often gets lost in the narrative. This division encompasses IT consulting, custom software development, robotic process automation through the Almato brand, mobile and app development, and industry-specific solutions. It also includes one of Germany's leading SAP Business One consulting practices, focused specifically on SMEs. While this segment generates lower margins than the recurring managed services business, it serves a critical strategic function: it is the tip of the spear. Consulting engagements are how Datagroup develops new customer relationships and demonstrates capabilities that can later be expanded into full CORBOX managed services contracts. The consulting-to-managed-services pipeline is one of the underappreciated growth engines in the business.

But the most compelling hidden asset is what is happening on the automation front. When Datagroup acquired Almato GmbH in 2018, it was buying a specialist in robotic process automation—software robots that can handle repetitive, rule-based tasks faster and more accurately than human operators. In 2020, the company merged Almato with its mobile solutions unit to create a dedicated AI and automation division with approximately 120 employees. The division developed the Almato ONE platform, which enables automation through RPA, digital assistants, intelligent applications, ready-made software robots, and machine learning services.

The real breakthrough, however, came with the Service Desk. For any managed IT services provider, the service desk is simultaneously the most critical customer touchpoint and the most labor-intensive cost center. Thousands of tickets per day—password resets, software installation requests, hardware troubleshooting, access permissions—each requiring a human agent to triage, categorize, and resolve. It is the kind of repetitive, pattern-based work that AI was born to handle.

Datagroup deployed its proprietary BARDIOC platform—a semantic data engine with an integrated reasoning capability designed for company-specific retrieval augmented generation systems and automated decision-making—to attack this cost center. The Almato Classifier uses machine learning to automatically categorize incoming tickets, and BARDIOC's AI reasoning engine handles resolution for an increasing share of routine requests. The results reported by the company are striking: within six months of deployment, forty-one percent of all service desk tickets were automated. Resolution times accelerated by eighty-five percent. Ticket reopenings—a key quality metric indicating whether the initial resolution actually solved the problem—dropped by ninety-five percent. And staff turnover in the service desk, historically one of the highest-churn roles in IT services, fell by forty percent.

These numbers, if they hold at scale, have profound implications for the business model. The service desk is one of the largest cost lines in a managed services P&L. Automating forty percent of ticket volume does not just save labor costs—it fundamentally changes the unit economics of every CORBOX contract. Each new customer added to the platform generates incrementally higher margins because the fixed cost of the AI-driven service desk infrastructure is spread across a larger base. This is the kind of operating leverage that the market has not fully priced into the current valuation—though admittedly, with the KKR take-private underway, the public market's opinion is becoming moot.

Mark Schäfer, the divisional board member responsible for Production and AI-based automation, represents the company's commitment to this transformation. His background as former CISO at T-Systems International gives him credibility in both the security and operational technology domains—two areas where AI automation intersects most naturally with managed services delivery.

Another dimension worth noting is Datagroup's public sector exposure. The company serves large public institutions and has developed a "Defense Cloud" for aerospace and defense customers, hosted geo-redundantly and entirely within Germany. In a European political environment increasingly focused on digital sovereignty and the risks of depending on American hyperscalers for critical infrastructure, a German-operated, ISO 27001 and C5-certified cloud service has obvious appeal. The NIS2 directive and BSI compliance requirements are driving a new wave of public-sector IT procurement that plays directly to Datagroup's strengths.

VII. The 7 Powers and Competitive Position

To understand whether Datagroup's advantages are durable, it helps to apply Hamilton Helmer's Seven Powers framework—the analytical toolkit that asks not just whether a company has an advantage, but whether that advantage is the kind that gets stronger over time.

The primary power at work is switching costs, and they are formidable. When a Mittelstand company outsources its IT infrastructure to Datagroup's CORBOX platform, the integration is deep. SAP landscapes are migrated and optimized. Cloud workloads are moved into Datagroup's certified data centers. Security monitoring is routed through their Security Operations Center. Collaboration tools are configured and managed. Helpdesk processes are tailored to the customer's specific environment. Unplugging from this web of dependencies is not merely expensive—it is operationally terrifying. For a four-hundred-person manufacturer whose core competency is hydraulic presses, the prospect of simultaneously migrating SAP, cloud, security, and helpdesk services to a new provider is the stuff of boardroom nightmares. The switching costs are not just financial; they are cognitive and organizational. This is what Helmer would call "entrenched" switching costs—the kind where the customer's internal processes have co-evolved with the provider's systems.

The second power is process power. Datagroup's ability to acquire, include, and operationally improve IT service companies is a proprietary capability built over decades and thirty-four-plus transactions. The "100 Days Datagroup" integration framework, the CORBOX migration playbook, the centralized delivery model—these are not things a competitor can replicate by hiring a few integration specialists. They are organizational routines embedded in the company's culture, systems, and institutional memory. A well-funded competitor could certainly attempt to build a similar roll-up platform, but they would face years of learning curve and the inevitable integration mistakes that Datagroup has already made and learned from.

Counter-positioning is also at play, though more subtly. The large global IT services firms—Accenture, Capgemini, T-Systems—could theoretically move downmarket to serve the Mittelstand. But doing so would require them to fundamentally restructure their delivery models, which are optimized for large enterprise engagements with high day rates and complex, bespoke solutions. Sending a team of expensive consultants to a two-hundred-person auto parts manufacturer in rural Baden-Württemberg does not fit their economic model. Datagroup's cost structure, local presence, and CORBOX productization make it economically viable to serve customers that the large players find unprofitable to pursue. This is a classic counter-positioning dynamic: the incumbents can see the opportunity but cannot rationally pursue it without cannibalizing their existing business model.

Scale economies are emerging but not yet dominant. As Datagroup grows, its centralized delivery units—the Service Desk, the data centers, the SOC—become more efficient on a per-customer basis. The AI automation of the service desk amplifies this effect. But the company is still relatively small compared to the addressable market, so the scale advantages are more about internal efficiency than about market-level economies of scale that would deter competitors.

Turning to Porter's Five Forces, the competitive landscape reveals several structural advantages. The bargaining power of buyers is constrained by the critical nature of IT services. A Mittelstand company can negotiate on price, but it cannot walk away from IT support without paralyzing its operations. The threat of new entrants is moderated by two factors: the Mittelstand's deep cultural preference for established, trusted providers over new and unproven ones, and the capital requirements of building the centralized delivery infrastructure needed to offer competitive service levels. The bargaining power of suppliers is limited because Datagroup's key inputs are human talent and commodity technology infrastructure—neither controlled by a small number of suppliers. Rivalry among existing competitors is real but differentiated; the market is large enough that Datagroup, Bechtle, Cancom, and Computacenter can coexist without destructive price competition, each serving somewhat different segments and geographies. The threat of substitutes—such as companies bringing IT back in-house—is low and declining, as the complexity and security requirements of modern IT infrastructure make DIY approaches increasingly impractical for mid-sized firms.

Where Datagroup ranks on the competitive landscape tells this story clearly. The 2025 Lünendonk List, the definitive ranking of German IT service providers, placed Datagroup seventh among the nation's leading firms. The Lünendonk list covers ninety-four IT service providers with collective German revenue of 34.3 billion euros—a vast market in which Datagroup's five hundred sixty million represents less than two percent. The fragmentation is both the challenge and the opportunity: there are decades of consolidation runway ahead.

The company's competitive position is further buttressed by its customer satisfaction track record—ranked eighth in the December 2023 Whitelane Research study with seventy-seven percent general satisfaction, and top-ranked for customer satisfaction for nine consecutive years. In a relationship-driven market where contracts are renewed based on trust and performance rather than lowest price, this reputation is a compounding asset.

VIII. The Playbook: Lessons for Investors and Founders

Every great business story contains lessons that extend beyond the specific company, and Datagroup's two-decade journey from a regional PC reseller to a five-hundred-sixty-million-euro managed services platform offers several.

The first lesson is the enduring power of unsexy niches. The global technology narrative is dominated by consumer-facing platforms, artificial intelligence, and frontier innovation. But the vast majority of enterprise IT spending goes to prosaic, essential services—keeping systems running, data secure, employees productive. Companies that dominate these "boring" categories often compound more reliably than their glamorous counterparts because they face less competition for talent, less pricing pressure from fashion-driven demand shifts, and less disruption risk from the next technological paradigm. Datagroup understood early that being the best at running a Mittelstand company's SAP system was more valuable than being mediocre at something sexier.

The second lesson is that capital allocation is the ultimate CEO skill in a mature market. When organic growth is structurally limited to low single digits, the only way to compound at attractive rates is through disciplined deployment of capital—buying the right businesses, at the right prices, and integrating them effectively. Max Schaber grasped this when he took the company public in 2006, and Andreas Baresel has continued to execute the playbook with precision. The thirty-four-plus acquisitions since the IPO have maintained remarkable consistency in target profile, valuation discipline, and integration methodology. There have been no empire-building splurges at inflated multiples, no ill-conceived diversification into adjacent markets, no chasing of "transformational" mega-deals. Just steady, disciplined execution of a proven formula.

The third lesson is that productizing a service is the only way to scale human capital. Every professional services firm eventually hits a wall: growth requires hiring, hiring requires training, and training takes time. The only way through this constraint is to reduce the amount of human judgment required per unit of revenue—not by cutting quality, but by standardizing delivery so that each professional can serve more customers at a higher and more consistent quality level. CORBOX is the embodiment of this principle. It transforms what would otherwise be a bespoke consulting relationship into a repeatable, platform-leveraged service delivery model. The AI automation of the service desk takes this logic to its next level, substituting machine intelligence for routine human labor.

How does Datagroup compare to the pantheon of great roll-up stories? Constellation Software, the Canadian vertical market software acquirer, is the gold standard—a company that has compounded shareholder value at extraordinary rates through relentless, disciplined acquisition of small software businesses. Datagroup shares Constellation's discipline and niche focus but operates in services rather than software, which inherently carries lower margins and more labor intensity. Danaher, the American industrial conglomerate, pioneered the Danaher Business System for operational improvement of acquired companies; Datagroup's CORBOX integration playbook serves an analogous function, albeit at a much smaller scale. The comparison to these titans is flattering but premature—Datagroup has proven the model works but has not yet demonstrated it at the scale that would put it in the same conversation.

What makes Datagroup's story particularly instructive for European founders and investors is the demonstration that world-class capital allocation and operational excellence are not exclusively American phenomena. The German Mittelstand tradition of patient, long-term business building—often dismissed as stodgy by Silicon Valley standards—can produce remarkable compounding when combined with a sophisticated acquisition strategy and a willingness to invest in operational systems.

IX. The Bear vs. Bull Case

Every investment thesis has its vulnerabilities, and intellectual honesty demands that we examine Datagroup's with the same rigor we applied to its strengths.

The bear case begins with talent. Germany's IT labor market is among the tightest in Europe, with tens of thousands of unfilled technology positions nationwide. For a company that derives its revenue from human-delivered services, the "war for talent" is not a cliché—it is an existential constraint. Every acquisition brings new customers, but those customers require engineers, consultants, and service desk agents to serve them. If Datagroup cannot attract and retain enough skilled professionals to staff its growing portfolio of contracts, the engine stalls. The company's employee count of roughly 3,500 to 4,000 people across twenty-five locations represents a workforce that must grow with the business. This is not a software company where marginal revenue comes with near-zero marginal cost.

The AI automation initiatives partially address this concern—automating forty-one percent of service desk tickets meaningfully reduces the labor intensity of delivery—but the service desk is only one component of the cost structure. SAP consultants, cloud architects, and security specialists cannot yet be replaced by machine learning. Until they can, talent remains the binding constraint.

The second bear concern is balance sheet risk. Goodwill of 182 million euros represents thirty-four percent of total assets as of fiscal year 2024—a direct consequence of thirty-four acquisitions. In a downturn scenario where acquired businesses underperform, goodwill impairment charges could materially impact reported earnings and book value. The equity ratio of 28.6 percent is adequate but not conservative, and net debt rose from 155 million euros at fiscal year-end 2024 to 176 million by the third quarter of fiscal 2024/2025, pushing the net debt to EBITDA ratio from 1.7 times to 2.2 times. Under KKR's ownership, the temptation to accelerate acquisitions with debt financing could push leverage to uncomfortable levels, though the all-equity structure of the KKR deal itself provides some reassurance on this front.

A third concern, more nuanced, is concentration risk. While Datagroup serves hundreds of customers, the loss of a single large contract—such as the kind of multi-year, nine-figure engagement inherited from the HPE deal—could create a meaningful revenue gap. The company does not disclose individual customer concentration in sufficient detail to fully assess this risk, which is itself a red flag for rigorous investors.

There is also the broader competitive question. Germany's IT services market may be fragmented today, but the forces of consolidation are accelerating. Bechtle and Cancom, both larger and better-capitalized, are pursuing their own acquisition strategies. International players like Computacenter are expanding their German operations. And the hyperscalers—Amazon Web Services, Microsoft Azure, Google Cloud—are increasingly offering managed services that compete with portions of CORBOX's value proposition. Datagroup's defense is its customer intimacy and local presence, but these advantages could erode as cloud-native services become more sophisticated and self-service.

Now, the bull case.

The German digital gap is real and enormous. McKinsey and other research firms have consistently documented that German Mittelstand companies lag their American counterparts by roughly a decade in cloud adoption, IT automation, and digital process transformation. This is not a market where IT spending is declining—it is a market where IT spending is being restructured, shifting from capital expenditure on owned infrastructure to operating expenditure on managed services. Datagroup sits at the exact intersection of this secular trend. Every year that a Mittelstand company decides to stop running its own servers and outsource to a managed services provider, Datagroup's addressable market expands.

The regulatory tailwind is equally powerful. The EU's NIS2 directive, Germany's BSI requirements, and the broader GDPR enforcement framework are making IT compliance increasingly complex and costly for mid-sized companies. The do-it-yourself approach to cybersecurity and compliance that many Mittelstand firms have relied on is becoming untenable. Datagroup's Security Services module, operated from German data centers with C5 cloud security compliance, is precisely what regulators are demanding and what CISOs are recommending.

The KKR partnership unlocks a new category of growth. As a public micro-cap, Datagroup was limited in the size of acquisitions it could pursue. Under KKR's umbrella, with access to the firm's capital, relationships, and operational resources, Datagroup can credibly pursue larger transactions—potentially including the kind of international expansion into Austria and Switzerland that the DACH region represents. The stated ambition of entering "the next league" is more than marketing language; it reflects a genuine step change in the company's M&A firepower.

The AI-driven margin expansion story may be the most underappreciated element of the bull case. If the service desk automation results—forty-one percent ticket automation, eighty-five percent faster resolution—can be replicated across the full customer base and extended to other service delivery functions, the impact on operating margins could be transformative. A two-to-three percentage point improvement in EBITDA margins on a five-hundred-sixty-million-euro revenue base translates to meaningful incremental cash flow—cash flow that can be reinvested in further acquisitions or used to delever the balance sheet.

For investors tracking this story from the outside—and with the delisting underway, "outside" is increasingly the only vantage point—two KPIs matter above all others. The first is the recurring revenue percentage, which measures the stability and predictability of the revenue base and currently sits around eighty percent. Any meaningful decline in this metric would signal that the CORBOX model is losing traction or that new customer acquisition is tilting toward lower-quality project work. The second is EBITDA margin, which captures both the operational leverage of the platform model and the success of the AI automation initiatives. The trajectory from eleven percent in 2016 to sixteen percent in 2023 tells a story of compounding efficiency; a stall or reversal would demand investigation. A third metric worth watching is the net debt to EBITDA ratio, which will reveal whether the KKR era brings disciplined leverage or the kind of balance sheet aggression that has undone other PE-backed services platforms.

Is Datagroup the "Baby Danaher" of German IT? The comparison is aspirational but not yet earned. What Datagroup has demonstrated is that the playbook works: disciplined acquisition, platform-based integration, margin expansion through standardization, and now AI-driven automation. What it has not yet demonstrated is the multi-generational compounding and operational perfection that defines true industrial greatness. The KKR chapter will be the test.

X. Epilogue and Final Reflections

In the spring of 2025, as KKR's investment agreement was announced and the delisting process began, a chapter closed on Datagroup's life as a public company. But the underlying story—the one about a fragmented market, a disciplined acquirer, and a secular digital transformation—continues to unfold.

The most recent financial results tell a story of steady execution. For the first nine months of fiscal year 2024/2025, ending June 2025, revenue grew 9.3 percent to 416 million euros, with organic growth contributing roughly eight percentage points. EBITDA reached sixty-one million euros, up from fifty-eight million in the prior year period. Full-year guidance was confirmed. The acquisition of clavis in early 2025 added another building block to the platform, and the TARADOR cybersecurity acquisition in late 2024 reflected the company's recognition that security services will be an increasingly important growth vector.

On the technology front, the BARDIOC semantic data platform and Almato automation tools represent what may be the company's most important strategic asset for the next decade. The shift from human-delivered to AI-augmented IT services is not a future possibility—it is happening now, inside Datagroup's service desk, with measurable results. The forty-one percent automation rate achieved within six months of deployment is a proof point, not a projection. If that number reaches sixty or seventy percent over the next several years, the labor economics of managed IT services will be fundamentally transformed, and Datagroup will have a cost advantage that no amount of acquisition spending by competitors can replicate.

The broader significance of Datagroup's story extends beyond the company itself. It is a demonstration that Europe—and Germany in particular—can produce capital allocation excellence of the kind more commonly associated with American conglomerates. The Mittelstand model of patient, founder-led business building, when combined with a sophisticated acquisition platform and a willingness to invest in operational technology, can generate the kind of compounding returns that attract even the most selective global investors. KKR's decision to partner with the Schaber family, rather than simply buying them out, is an implicit acknowledgment that Datagroup's culture and methodology are worth preserving.

From the Hugo-Häring Prize-winning headquarters in Pliezhausen, looking out over the Swabian hills, the view has not changed much since Max Schaber first set up shop nearby in 1983. The buildings are nicer. The revenue is about eighteen times larger. The team has grown from a handful of founders to nearly four thousand professionals. But the essential proposition remains what it has always been: making technology work for the German Mittelstand, one company at a time. In an industry obsessed with disruption and reinvention, there is something quietly powerful about a business that just keeps doing the same thing—only better, and at ever-greater scale.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube