Currys plc: The Bricks, Clicks, and Moats of Europe's Electricals Giant

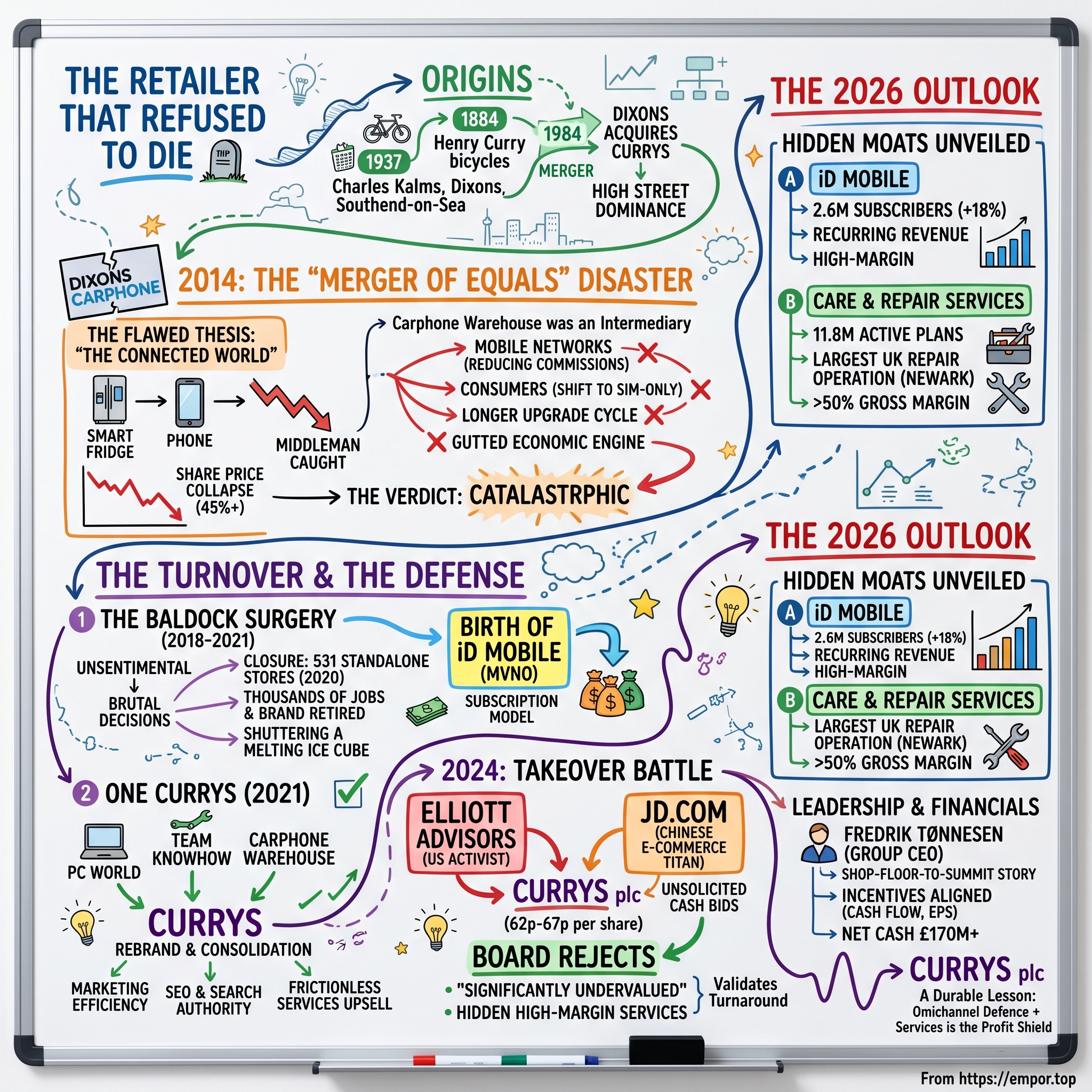

I. Introduction: The Retailer That Refused to Die

Picture the graveyard of consumer electronics retail. It is a crowded place. Circuit City, once the second-largest electronics chain in the United States, liquidated in 2009. Comet, Britain's number-two electricals retailer, collapsed into administration in 2012, taking nearly 7,000 jobs with it. RadioShack filed for bankruptcy twice. Best Buy, the American giant, charged into Europe with great fanfare in 2008 and retreated in humiliation by 2012. The thesis was simple and seemed unstoppable: 阿里巴巴 Alibaba in China and Amazon in the West would commoditise every box with a plug, strip the margin out of selling televisions and laptops, and leave the high-street electricals retailer as roadkill on the information superhighway.

And yet, here in the middle of 2026, one legacy British bricks-and-mortar electricals retailer is not merely surviving. It is generating cash, paying dividends, buying back its own shares, and trading on the London Stock Exchange under the ticker CURY.L with the strongest balance sheet in its modern history.

That company is Currys plc. And its story over the last decade is one of the most underappreciated turnarounds in European retail—a tale that runs from a Victorian bicycle workshop in Leicester, through a £3.8 billion "merger of equals" that turned out to be a catastrophic bet on a melting ice cube, through the brutal closure of 531 stores in a single stroke, all the way to early 2024, when the company found itself the prize in a three-way takeover brawl. On one side stood the elite American activist fund Elliott Advisors, waving cash. On another, circling quietly, was the Chinese e-commerce titan 京东 JD.com, hunting for a European logistics footprint. And in the middle stood a board of directors who looked at both suitors and said, in effect: you are insulting us.

The remarkable part is that the board turned out to be right. Within weeks of both bidders walking away, Currys upgraded its profit guidance. By the time we reach mid-2026, the company has just announced full-year adjusted profit before tax of around £191 million, up roughly 18% year on year, and finished its financial year with more than £170 million in net cash.1 The opportunists who tried to buy the company on the cheap missed the very thing the board insisted they were missing: a high-margin, recurring-revenue services engine hiding inside what everyone assumed was a doomed box-mover.

Here is the roadmap for how we get there. We will start with the surprisingly tangled roots of Currys and Dixons, two retail dynasties that merged decades ago. We will dissect the 2014 Carphone Warehouse merger as a near-textbook case study in overpaying for a business model about to be structurally gutted. We will walk through the near-death of the mobile business and the decisive, write-off-heavy surgery that followed. We will examine the 2024 defence—the brilliant divestment of the Greek business and the rejection of hostile foreign bids. We will go inside the two hidden moats: the iD Mobile network and the Care & Repair subscription machine. We will meet the incoming Group CEO, Fredrik Tønnesen, who started on the shop floor in Norway as a twenty-year-old. And finally we will run the whole thing through Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. Let's get into it.

II. Succinct Origins: From Leicester Bicycles to High Street Dominance

Every great retail empire seems to begin with a single restless founder and a workshop, and Currys is no exception. In 1884, in the back garden of a house in Leicester, a man named Henry Curry began building bicycles.16 This was the height of the British cycling boom, when the safety bicycle had just democratised personal mobility and every market town wanted a maker. Curry's machines were good, the business grew, and the Curry family did what successful retailers always do: they followed their customers' changing desires. As the twentieth century arrived, the workshop that sold bicycles started selling the new wonders of the age—radios, gramophones, and eventually the domestic appliances that would electrify the British home during the interwar years.

Notice the pattern, because it repeats across the entire history of this company: Currys was never really in the business of any single product. It was in the business of selling whatever piece of consumer technology was new, exciting, and slightly intimidating to the ordinary household. A radio in 1925, a washing machine in 1955, a television in 1965, a laptop in 1995, a smart speaker in 2018—the products changed, but the proposition stayed identical. Come to us, we will explain this baffling new device, we will sell it to you, and we will help you when it breaks.

Some fifty miles to the south-east, the second half of our story was beginning. In 1937, a young man named Charles Kalms opened a small photographic studio in Southend-on-Sea and gave it a name plucked, essentially at random, for its memorability: Dixons.16 Kalms—and later, far more consequentially, his son Stanley Kalms—rode the postwar photography boom and then a relentless wave of expansion into high-street consumer electronics. Calculators, video recorders, hi-fi separates, and eventually the personal computer all flowed through Dixons' stores. Stanley Kalms in particular was a ferocious, detail-obsessed merchant who built Dixons into a genuine retail juggernaut and a fixture of the British high street.

The two dynasties collided in 1984, when Dixons acquired Currys.16 On paper it was a takeover; in spirit it was the consolidation of two of Britain's great electricals names under one roof. Over the following two decades the enlarged group sprawled into a multi-brand empire—Dixons, Currys, and the big-box computing specialist PC World, plus a powerful Nordic arm in Elkjøp—that dominated British electricals retail for a generation.

Why does any of this dusty corporate genealogy matter to an investor looking at the company in 2026? Because of what all that history physically built. More than a century of expansion left Currys with three legacy assets that are almost impossible to recreate from scratch today. The first is real estate: an enormous estate of out-of-town, retail-park superstores—exactly the cheap, high-square-footage, easy-to-park-at locations that pure-play e-commerce startups cannot conjure into existence. The second is a national logistics and delivery network capable of getting a refrigerator into a kitchen and carrying the old one away. And the third, which we will return to in depth, is Europe's largest electronics repair operation, in Newark, Nottinghamshire. These are not relics. They are the modern logistical moat. An Amazon can undercut you on the price of a box; it cannot easily install your oven, repair your laptop in-house, or let you walk into a physical store and hand back a dud television. Those scale advantages, accumulated over 140 years, are the foundation everything else in this story is built on—and they are exactly what the company nearly squandered in 2014.

III. The Mega-Merger: Dixons Retail and Carphone Warehouse

In May 2014, the executives of Dixons Retail and Carphone Warehouse stood before the press to unveil a deal they described in the most exhilarating terms the English language permits in a merger announcement. It was a £3.8 billion combination, structured as an all-share "merger of equals," that would create Dixons Carphone—a new champion of British retail spanning more than 500 Currys and PC World stores and roughly 2,000 Carphone Warehouse outlets, with management promising £80 million a year in cost synergies.9 Sir Charles Dunstone, the charismatic founder of Carphone Warehouse, would chair the combined group; Dixons' Sebastian James would run it as chief executive.

The narrative was seductive, and it had a name: "The Connected World." The grand thesis went like this. Every appliance in your home was about to get smart. Your fridge would talk to your phone, your heating would learn your schedule, your washing machine would order its own detergent. In this coming world, the argument ran, you could no longer separate the hardware from the connectivity. The company that sold you the smart device (Dixons) and the company that sold you the data contract to connect it (Carphone Warehouse) belonged under one roof, bundling hardware and connectivity into one seamless purchase. It was, on a whiteboard, a beautiful vision.

So did they overpay? Here the analysis gets interesting, because in the narrowest accounting sense, they did not. This was an all-share, roughly 50/50 merger in which the former shareholders of each company ended up owning half of the combined entity. No cash changed hands. No control premium was paid. By the textbook definition, nobody overpaid for anything.

And yet this was one of the most value-destructive deals in modern UK retail history. The reason is that the price of a no-premium share merger is set by the relative valuations of the two sides—and the Carphone Warehouse side was being valued as a high-growth, high-multiple business at the precise moment its core economic model was about to collapse. Dixons was effectively swapping half of its resilient, cash-generative electricals and Nordic operations for half of a business whose revenue rested on a foundation that was about to dissolve.

To understand why, you have to understand what Carphone Warehouse actually was. It was an intermediary—a middleman. It did not own a mobile network. It sold you a phone bundled with a 24-month contract from EE, Vodafone, or O2, and in return the network paid Carphone a fat commission for every customer it signed up and locked in. That commission was the entire economic engine. And right around 2014, three things happened to that engine, all at once. First, the mobile network operators looked at those commissions, decided they were paying a fortune to a middleman for customers they could acquire directly, and began ruthlessly cutting third-party retail commissions. Second, consumers grew wise to the maths of the expensive 24-month bundle and shifted en masse toward cheap SIM-only deals, where there was no handset subsidy and almost no commission to be had. Third, smartphones simply stopped improving fast enough to justify an upgrade every two years; people held onto their phones for three years, then four, lengthening the upgrade cycle and starving Carphone of churn. The middleman was being disintermediated from three directions simultaneously.

There was, in fairness, a warning written on the wall in letters anyone could read. Carphone Warehouse had spent the prior years in a joint venture with America's Best Buy, which had bought a 50% stake in Carphone's retail business in 2008 with grand ambitions for European expansion.17 By 2012–2013, Best Buy had concluded that European electricals retail was a brutal, low-margin slog, and it sold its half back to Carphone at a steep discount before retreating across the Atlantic. When the most sophisticated big-box electronics retailer on earth has just looked at this exact market and fled, paying to get out, that is information. The Dixons Carphone architects chose to read it as opportunity.

Contrast the trajectory with the 2016 merger of France's Fnac and Darty, which combined a cultural-goods retailer with an electricals specialist and built a stable, scaled omnichannel operator that broadly held its value. The difference was the quality of the assets being combined. Fnac-Darty merged two businesses selling things people would keep buying. Dixons Carphone bolted a structurally declining commission stream onto a healthy retailer.

The verdict came fast and it was merciless. Within roughly three years of the merger, the combined company's share price had collapsed by more than 45% as the mobile division's profits evaporated and a string of profit warnings shredded management credibility.16 The "Connected World" never arrived in the form anyone had imagined; the smart fridge did not need a Carphone Warehouse contract. Dixons had traded half of a good business for half of a melting ice cube—and now someone was going to have to walk into that meltwater and clean it up.

IV. The Inflection Points: Shuttering Standalone Stores and the Death of the Mobile Contract

In April 2018, a man named Alex Baldock walked into the chief executive's office at Dixons Carphone and inherited a slow-motion catastrophe. Baldock was not a legacy insider; he came from outside, having run the online white-goods retailer Shop Direct, and he arrived with the unsentimental eye of a turnaround operator rather than the loyalties of a long-serving lifer. What he found on the books was an electricals business that was fundamentally sound and a mobile business that was, in his own characteristically blunt framing, broken—burning cash at a rate that could not continue and dragging the entire group's valuation into the gutter.

For his first eighteen months, Baldock did what new CEOs do: he studied, he tested, he tried to make the mobile business work within its existing shape. It did not work, because it could not work. The economics were not cyclical; they were structural. You cannot reform your way out of being a commission-collecting middleman when the parties paying the commission have collectively decided to stop. By late 2019 and into 2020, Baldock had reached the conclusion that defines his entire tenure: the standalone Carphone Warehouse store had to die.

This was not a trim. In early 2020, Currys announced it would permanently close all 531 standalone Carphone Warehouse stores across the United Kingdom.16 Think about the courage—or the desperation—that decision required. These were 531 leases, thousands of jobs, and a brand that had been a fixture of every British high street for three decades. Closing them meant absorbing a brutal, write-off-heavy hit to near-term earnings: redundancy costs, lease exit costs, stock liquidation, the whole grim arithmetic of retreat. The market would punish the reported numbers. Baldock did it anyway.

The logic, once you see it, is clean. Those standalone shops were small-format, high-rent, low-footfall units sitting on expensive high streets, selling a product—the bundled mobile contract—whose margin had been gutted. Every one of them was a fixed cost attached to a dying revenue line. Meanwhile, Currys already operated a fleet of enormous, cheaper-per-square-foot superstores out on the retail parks, where customers were already coming to buy televisions and laptops. So rather than sell phones in 531 expensive little boxes, Baldock folded the entire mobile offer inside the big stores he already owned and was already paying for. The marginal cost of selling a phone next to a fridge was close to zero. The marginal cost of selling it in a dedicated high-street unit was a lease.

But closing the stores solved only half the problem. The deeper issue was the business model itself—the dependence on other people's commissions. And here Baldock made the move that turned a defensive retreat into a genuine strategic asset. Instead of continuing to sell other networks' contracts for a shrinking cut, Currys would become a network operator itself. It leaned hard into iD Mobile, a Mobile Virtual Network Operator, or MVNO.

It is worth slowing down on what that actually means, because it is the hinge of the whole turnaround. An MVNO is a phone company that does not own any physical network. iD Mobile rents wholesale capacity on the Three UK network and then sells mobile plans to consumers under its own brand, billing the customer directly every single month. The difference from the old Carphone model is profound. Under the old model, Currys made a one-time commission when it signed you up for someone else's contract, and then the relationship—and all the recurring revenue—belonged to EE or Vodafone. Under the MVNO model, the customer is Currys' customer. The monthly payment is Currys' revenue. The relationship is direct, recurring, and high-margin, and it renews month after month after month. Currys had stopped being a middleman taking a one-off finder's fee and become a principal collecting a subscription. That single shift, born out of a crisis, planted the seed of one of the two hidden engines we will return to later. But first, the company had to stop confusing its own customers.

V. The Rebrand and Consolidation: "One Currys"

If you had walked through a British retail park in 2019 and tried to map the company's brand architecture, you would have come away dizzy. There was Currys, the electricals name. There was PC World, the computing name—often literally bolted onto the same building as "Currys PC World." There was Carphone Warehouse for mobile. And there was Team Knowhow, the somewhat awkwardly named banner for installation, support, and repair services. Four brands, four logos, four advertising identities, four sets of customer expectations—all ultimately owned by the same company, selling to the same customer, often inside the same store. It was a museum of past acquisitions, and it was costing the company dearly in ways that did not show up cleanly on any single line of the income statement.

In 2021, Baldock's team swept the whole confusing edifice away. Every consumer-facing identity—Currys, PC World, Carphone Warehouse, Team Knowhow—was collapsed under a single unified brand: Currys.16 The group even renamed itself at the corporate level, retiring "Dixons Carphone plc" in favour of "Currys plc" in September 2021. One name. One promise. One front door.

The strategic value of this move is easy to underrate because it sounds like a marketing exercise, but it operates on three distinct levels, each of which feeds the bottom line. The first is raw marketing efficiency. A company running four brands is, in effect, paying four times to build awareness, splitting its advertising budget across identities that compete for attention with one another. Consolidate to one brand and every pound of marketing spend now reinforces a single name, and every store format can be standardised, simplified, and run more cheaply.

The second level is more subtle and, in the modern era, arguably more important: search. When you fragment your web presence across multiple domains—currys.co.uk, pcworld.co.uk, carphonewarehouse.com—you fragment your search-engine authority. Google rewards domains with depth, traffic, and link authority by ranking them higher in organic results. By funnelling everything onto currys.co.uk, the company concentrated its entire digital gravity into one domain, sharply boosting its organic search rankings. In a world where the battle for a customer often begins with a Google search for "cheap washing machine," ranking on the first page against Amazon is worth a fortune in advertising the company no longer has to buy. The rebrand, in other words, was partly an SEO strategy wearing a marketing costume.

The third level is the one that matters most for the long-term economics, and it sets up everything in the back half of this story. A single, simple relationship with the customer makes it dramatically easier to sell that customer the second, third, and fourth thing. When a buyer thinks of "Currys" as one coherent entity rather than a confusing federation of sub-brands, the path from buying a laptop to also buying a protection plan, a credit agreement, a setup service, or an iD Mobile contract becomes frictionless. Every additional attachment deepens the relationship and lifts the lifetime value of that customer. The rebrand was the plumbing that let the high-margin services flow. And it was that services profitability—still largely invisible to most investors—that would soon make the company a takeover target, just as it cleaned up its balance sheet in spectacular fashion.

VI. Divestments and the Great Takeover Battle of 2024

The first move in the drama of 2024 was actually made in the closing months of 2023, and it was a masterstroke of capital recycling that, in hindsight, looks almost prescient. In November 2023, Currys agreed to sell its Greek and Cypriot business—trading under the venerable name Κωτσόβολος Kotsovolos—to Greece's state-backed electricity giant, Δημόσια Επιχείρηση Ηλεκτρισμού Public Power Corporation, known as ΔΕΗ PPC, for an enterprise value of €200 million, or roughly £175 million.4 The deal completed in early 2024, delivering net cash proceeds of around £156 million.14

On its own, this was simply a sensible piece of portfolio pruning. Kotsovolos was a fine business—in fact, it was a successful, market-leading one—but it was sub-scale relative to the group's core, and PPC, which was trying to build an ecosystem of energy and connected-home services, was willing to pay a full price for it. Selling a good asset to a buyer who values it more than you do is the essence of disciplined capital allocation. But the timing transformed a good decision into a brilliant one. That injection of cash, landing right at the start of 2024, effectively wiped out the company's remaining net debt and left it sitting on a clean balance sheet with a cash cushion—precisely the financial armour a company wants when a raider is about to kick down the door.

And the raider was already lacing up its boots. The attacker was Elliott Advisors, the European arm of Elliott Management, one of the most feared and sophisticated activist investors on the planet. Elliott had run the numbers on Currys and seen what value investors see: a company whose shares were trading at an absurdly depressed forward price-to-earnings multiple of around 5.5 times—a valuation that implied the market believed Currys was a structurally dying business with no future. To Elliott, that gap between the depressed share price and the underlying cash generation was a layup. In February 2024, it launched an unsolicited cash bid of 62 pence per share, valuing Currys' equity at roughly £700 million, and within days sweetened it to 67 pence per share, or about £757 million.2

Then the story acquired a second, far more exotic suitor. Almost simultaneously, the Chinese e-commerce titan 京东 JD.com confirmed it was in the preliminary stages of evaluating its own cash takeover of Currys.3 JD.com's interest had a completely different logic from Elliott's. Elliott wanted to buy cheap, fix, and flip. JD.com wanted something strategic and almost impossible to build organically: an instant European footprint—Currys' retail-park stores, its national logistics network, its repair infrastructure, its supplier relationships, and its millions of customers—as a beachhead for Western expansion. Suddenly a sleepy British electricals retailer was the object of a transcontinental bidding tension, courted by Wall Street's sharpest activist and one of Asia's largest internet companies at the same time.

The board's response, under chairman Ian Dyson, was unambiguous and, to many observers at the time, surprisingly defiant. They rejected every proposal flatly, declaring that the bids "significantly undervalued" the company and its real assets, and recommended shareholders take no action.5 This was not posturing. The board's conviction rested on the very thing the market was ignoring: that beneath the cyclical, low-margin hardware business sat a portfolio of high-margin, recurring-revenue services—the mobile network, the protection plans, the repair operation—that no 5.5x earnings multiple could possibly capture. Crucially, major institutional shareholders backed the board's stance rather than grabbing the quick cash, with significant holders signalling they wanted a great deal more than Elliott was offering—chatter coalesced around a floor closer to £1 billion, in the high-80s to mid-90s pence per share.

Then came the validation, and it was almost anticlimactic in its decisiveness. Both suitors walked away. JD.com announced in March 2024 that it would not make an offer.3 Elliott, after what it described as multiple rebuffed attempts to engage the board, also abandoned its pursuit.13 The activist and the internet giant both blinked. And here is the part that vindicated the board completely: within weeks of the bidders' retreat, Currys upgraded its full-year profit guidance. The standalone company, run by its existing management, was demonstrably worth more than the opportunistic exit on offer. The board had stared down two of the most formidable buyers in global finance and won—not with financial engineering, but by simply being right about what the business was worth. The question that lingered was who would steer this newly confident company into its next chapter.

VII. Modern Leadership and Shareholder Alignment

The answer arrived, with a twist of irony, in June 2026. Alex Baldock—the man who had spent eight years dismantling the conglomerate, closing the 531 stores, killing the legacy brands, building iD Mobile, fending off Elliott, and restoring the balance sheet—announced he was leaving. And he was not leaving for a quiet retirement or a rival electricals chain. He was departing to run Boots, the iconic British pharmacy and health-and-beauty chain, in the autumn of 2026.15 It was, in a sense, the ultimate testament to a turnaround completed: a CEO who had so thoroughly fixed his company that he could hand it over and walk into one of the biggest jobs in British retail.

The question of who would succeed him was where the board made a statement about the company's soul. They did not hire a flashy outsider or a celebrity retailer. They reached down into their own Nordic business and promoted Fredrik Tønnesen to Group Chief Executive, effective August 3, 2026.6 And Tønnesen's biography is the kind of detail that tells you something real about a company's culture.

Tønnesen joined Currys' Nordic division, Elkjøp, in 2005—as a twenty-year-old sales assistant standing on the shop floor in Norway, selling appliances to customers face to face.15 He did not parachute in from a consultancy or a business school. He sold the boxes. Over the following two decades he climbed every rung: managing director for Norway, then Chief Operating Officer for the Nordics, and from March 2023, Chief Executive of the entire Nordics business—a region responsible for roughly 40% of group revenue.6 In that role, he orchestrated a dramatic profit recovery as the Nordic market normalised after the pandemic's distortions, proving he could run a major P&L through a difficult cycle. His promotion to Group CEO is, in the purest sense, a shop-floor-to-summit story, and it signals continuity rather than rupture: the board is betting that the operational discipline that fixed the Nordics is exactly what should now be scaled across the group.

The way Currys structures its executive pay reveals how seriously the company takes the alignment between management and long-term owners—a question that matters enormously to any fundamental investor, because incentives quietly shape every decision a leadership team makes. Tønnesen's base salary as incoming Group CEO is positioned in the £900,000 to £1,000,000 range, with a standard annual bonus and a Long-Term Incentive Plan set, for the transition period, at an elevated 300% of base salary.[^8] His CFO partner, Bruce Marsh, appointed in 2021, draws a base of £506,900 and—more tellingly—personally holds 911,973 ordinary shares, a stake worth over £1 million, which means his own net worth rides on the same share price as every outside shareholder's.[^8]

But the truly instructive part is the structure of the incentives, because the metrics a board chooses to reward are a confession of what it actually believes drives value. Currys weights its long-term plan toward three things: Cumulative Free Cash Flow at 40%, Relative Total Shareholder Return at 30%, and Adjusted Earnings Per Share growth at 30%.[^8] Read that mix carefully. The single largest weighting is on cash generation, not on revenue growth or empire-building. For a company that nearly destroyed itself chasing a grand merger narrative, rewarding management above all for turning operations into hard cash is a deliberate course correction. On top of that, both the CEO and CFO must maintain a personal shareholding worth at least 250% of base salary, and must keep holding shares for a mandatory two-year period after they leave the company.[^8] That post-employment lock-up is the detail that separates genuine stewardship from short-term box-ticking: it forces executives to care about the durability of their decisions long after they have stopped collecting a salary. With leadership aligned and the balance sheet repaired, we can finally open the hood on the two engines that make this whole machine run.

VIII. The 'Hidden' Recurring-Revenue Engines

Here is the central misunderstanding that defined Currys' valuation for years, and the one that the takeover battle exposed. The market looked at Currys and saw a cyclical hardware retailer—a company that sells televisions and laptops on razor-thin margins, whose fortunes rise and fall with consumer confidence and the upgrade cycle. That perception is not wrong, exactly. It is just radically incomplete. Because bolted onto that low-margin hardware business are two high-margin, recurring-revenue engines that behave almost nothing like a box-mover, and that most investors were valuing at close to zero.

First, let's frame the company's two-region structure, because the engines sit inside it. Currys operates two primary segments. The UK and Ireland business is the legacy core, generating roughly £5.3 billion in annual revenue. The Nordics business—Elkjøp—generates roughly £3.4 billion and occupies a near-monopoly market position across Norway, Sweden, Denmark, and Finland, a genuinely enviable competitive structure in markets where Amazon's presence is far weaker than in the UK.7 Now, the engines.

The first hidden engine is iD Mobile, the MVNO born from the wreckage of the Carphone disaster. By mid-2026, iD Mobile had quietly scaled to 2.6 million subscribers, growing roughly 18% year on year—a growth rate that would make a Silicon Valley subscription startup proud.1 It generated over £719 million in revenue at an operating margin of around 5.9%.[^8] Now, 5.9% may not sound thrilling until you place it next to the operating margin on the hardware business, which runs at a paper-thin 2–3%. iD Mobile is roughly twice as profitable as the core retail operation, and—this is the crucial part—its revenue is recurring. Every one of those 2.6 million subscribers pays Currys every single month, automatically, with low churn and almost no incremental cost to serve. This is, in economic substance, a subscription business with software-like characteristics: high gross margin, recurring billing, and a customer base that grows by capturing people who walk into a Currys store to buy a phone anyway. The reason it stayed hidden is simply that it was buried inside the financials of a company everyone had pre-labelled as a dying retailer. Investors do not look for a high-margin subscription network inside a TV shop, so they did not see one.

The second hidden engine is the services moat—the constellation of Care & Repair and Repair & Protect plans. By mid-2026, Currys was managing approximately 11.8 million active consumer protection plans: extended warranties, maintenance subscriptions, accidental-damage cover, and the like.[^8] Eleven point eight million. That is a recurring-revenue book the size of a substantial standalone insurance business, attached to a retailer.

And it is anchored by something genuinely difficult to replicate: the repair operation in Newark, Nottinghamshire. The Newark customer repair centre is the largest facility of its kind in Europe, a vast campus staffed by some 1,100 colleagues—including hundreds of in-house engineers—processing on the order of three million products a year across returns, repairs, and recycling, running effectively around the clock.12 Let that sink in as a competitive fact. When you buy a laptop from an online-only marketplace and it dies, you are on your own—you ship it back into a void, or you fight a manufacturer's warranty line. When you buy that same laptop from Currys, you can walk into any store for an immediate replacement, or have it repaired under a subscription plan by engineers the company employs directly. That service—Currys calls its premium tier its "Most Valuable Service"—carries gross margins exceeding 50%, a figure from a different universe than the 2–3% on the hardware itself.[^8]

This is the strategic heart of the entire company, so it is worth stating plainly. The hardware is not really the product. The hardware is the customer-acquisition vehicle—the reason a human being walks through the door or lands on the website. The actual profit is made on what attaches to that hardware: the protection plan, the repair subscription, the credit agreement, the mobile contract. Sell a laptop at a 2% margin and you have made almost nothing. Sell that same customer a multi-year protection plan at a 50%-plus margin, an iD Mobile contract that bills monthly, and a setup service, and you have transformed a commodity transaction into a durable, high-margin relationship. The hardware price war that everyone assumes will kill Currys is, in fact, survivable precisely because the company does not depend on making money on the hardware. That insight is what the board understood and the bidders did not—and it is what the analytical frameworks confirm.

IX. Framework Analysis: Hamilton's 7 Powers and Porter's Five Forces

Strategy frameworks can be a lazy way to dress up a narrative, but applied honestly they force you to distinguish what is genuinely durable about a business from what merely sounds impressive. Run Currys through Hamilton Helmer's 7 Powers and Porter's Five Forces and a clear picture emerges: this is a company with two or three real powers, several outright weaknesses, and a competitive position that is defensible rather than dominant. Let's be rigorous about which is which.

Start with Helmer's powers. The strongest is Scale Economies. As the outright market leader in both the UK and the Nordics, Currys commands enormous purchasing power over the global technology OEMs—Apple, Samsung, Sony, HP, and the rest. That scale translates into better wholesale pricing, priority access to constrained stock during product launches, and co-marketing contributions from manufacturers eager for prime shelf space. A smaller competitor simply cannot match the buying terms, which means Currys can either undercut on price or pocket a wider margin at the same price. This is a real and durable advantage.

Switching Costs rank as a medium power, and they live entirely in the services ecosystem we just dissected. A customer with an iD Mobile plan, a Currys credit account, and three active Care & Repair plans is not going to casually drift to a competitor; unwinding all of that is a genuine hassle, and each additional attached service ratchets up the friction of leaving. This is not the iron lock-in of enterprise software, but it is real, and it compounds with every product the company attaches.

Cornered Resource also rates as medium, and it is the Newark repair hub combined with the out-of-town retail-park real estate. It is, for all practical purposes, impossible for a new entrant to assemble a physical repair-and-trade-in network of this scale in the UK today—the land, the planning permissions, the trained engineers, and the logistics took decades and a great deal of sunk capital to build. A competitor cannot simply buy this; they would have to recreate it brick by brick.

Then there is Counter-Positioning, and here we have to be honest rather than flattering—this power runs against Currys, not for it. For years the pure-play online retailers, Amazon and the UK's AO.com, were the ones doing the counter-positioning, attacking Currys' high-rent physical stores with an asset-light online model the incumbent could not easily copy without cannibalising itself. Currys has largely neutralised that attack by converting its stores into fulfilment nodes for click-and-collect, turning the once-feared real estate into a last-mile asset that lowers shipping costs. But "neutralised an opponent's power" is not the same as "possesses a power." This is a draw the company fought its way to, not a moat it enjoys.

Now Porter's Five Forces, which sharpens the picture further. The Threat of New Entrants is very low—replicating a national omnichannel supply chain, a fleet of superstores, a logistics network, and a repair operation is so capital-prohibitive that essentially no one is going to attempt it. The Bargaining Power of Suppliers, by contrast, is high: marquee OEMs like Apple and Dyson have such powerful direct consumer pull that Currys cannot afford to drop them from its shelves. That said, the relationship is genuinely two-sided—Currys' volume makes it an essential distribution partner, so the power is balanced rather than one-way. And then there is Competitive Rivalry, which is very high and is the single force that defines the company's economics. Currys faces relentless price competition from Amazon and from manufacturers selling direct to consumers, and that rivalry is exactly what keeps hardware operating margins pinned at 2–3%. This is the force that makes the entire services strategy not just clever but existential. Strip out the high-margin services and you are left with a business competing on price against the most efficient logistics company on earth—a fight with no winners. The services division is what lets Currys lose the hardware price war on any given television and still come out ahead on the customer. Which brings us to the lessons.

X. Playbook: Business and Strategic Lessons

Step back from the specifics and Currys offers a small handful of durable lessons that travel well beyond electricals retail.

The first is that the omnichannel defence is real—but only if you actually use the physical assets, rather than merely owning them. For a decade, the consensus held that bricks-and-mortar stores were pure liabilities, dead weight to be shed as fast as possible. Currys proved the more nuanced truth: a store is a liability if it is only a place to display products, but it is an asset if it doubles as a local distribution hub, a click-and-collect point, a returns desk, and a face-to-face service centre. The same square footage that looks like a cost on a spreadsheet becomes a last-mile fulfilment advantage that an online-only rival has to spend enormous sums to replicate. The lesson is not "stores good" or "stores bad"—it is that the function you assign to an asset determines whether it is dead weight or a moat.

The second lesson is the cruellest, and it is written in the wreckage of the 2014 merger: never buy a business whose revenue depends on intermediation commissions that a more powerful party can cancel overnight. Carphone Warehouse's entire economic engine was a stream of commissions paid, at their discretion, by the mobile networks. When those networks decided to stop paying, there was no business left to defend—and it took Currys five years of painful write-downs and the closure of 531 stores to unwind a mistake that was, in retrospect, visible at the moment the deal was signed. The middleman with no structural lock on either side of its market is always living on borrowed time.

The third lesson is the one the company now lives by: services are the profit shield, and you cannot survive on commoditised hardware alone. The discipline is to treat the hardware sale not as the goal but as the customer-acquisition cost—the loss-leader that buys you a relationship—and to make the actual money on the attach rate of credit, insurance, repair, and connectivity. A retailer that internalises this stops fighting a losing war on box prices and starts competing on the depth and stickiness of the relationship, where it can actually win.

And the fourth lesson belongs to the boardroom: when your shares are trading at cyclically depressed levels and an opportunist arrives with cash, the right response is to trust your own unit economics—if, and only if, those economics are genuinely robust. Currys' board held the line against Elliott and JD.com not out of ego but because they could see the cash flow the market was ignoring. Holding out paid off handsomely. But the lesson carries a warning label: this strategy works only when the underlying cash generation is real. A board that rejects a fair bid while sitting on a deteriorating business is not being brave; it is destroying value. The judgement is everything.

XI. Bear vs. Bull Case, Myth vs. Reality, and the KPIs That Matter

Let's war-game both sides honestly, because a turnaround this complete invites both over-enthusiasm and reflexive skepticism.

The bull case starts with the balance sheet. Currys entered the second half of calendar 2026 with more than £170 million in net cash—the strongest financial position in its modern history, transformed from the debt-laden conglomerate of the mid-2010s.1 Adjusted profit before tax of around £191 million for the financial year, up roughly 18%, came in ahead of prior guidance and consensus, evidence that the operational momentum is real rather than a one-off.1 The two recurring engines—iD Mobile and the protection-plan book—continue to grow and structurally insulate group profit from the cyclicality of hardware retail, group like-for-like sales rose 4% over the year, and the company has been returning cash to shareholders through dividends and buybacks while still building its cash pile.1 On top of that, the bull points to the incoming CEO: Tønnesen ran the Nordics, the group's most operationally efficient region, and the bull thesis is that the "Elkjøp playbook" of disciplined execution will now be scaled across the UK business that has historically been the laggard.

The bear case is equally coherent and should not be dismissed. The competitive rivalry we flagged in the Porter analysis is not going away: Amazon and direct-to-consumer manufacturer channels exert relentless, structural downward pressure on hardware margins, and there is no version of the future in which selling televisions becomes a fat-margin business. In the Nordics, the bull's prized near-monopoly faces aggressive price competition from the regional discounter Power, whose willingness to dump on price can compress margins across the whole market. And there is genuine execution risk in the leadership transition: however smooth the succession, a new Group CEO inheriting a turnaround at its peak inherits the risk that the easy wins are already banked. Layer on the macro—the British consumer remains vulnerable to spending freezes if inflation, rates, or employment turn—and you have a business whose hardware demand could soften meaningfully in a downturn, even if the services book holds.

It is worth puncturing one myth directly, because it shaped the company's valuation for years. The myth is that Currys is "just" a doomed bricks-and-mortar box-mover being slowly eaten by Amazon, deserving of a low-single-digit earnings multiple. The reality, as the takeover battle and the subsequent profit upgrades demonstrated, is that Currys is a low-margin hardware retailer wrapped around a high-margin, recurring-revenue services and connectivity business that the market systematically under-valued—which is precisely why two of the world's most sophisticated buyers tried to take it private at 5.5 times earnings, and why the board was right to refuse. But the inverse myth—that Currys has somehow "become a subscription company"—is equally false. The hardware business is still the large majority of revenue, it is still brutally competitive, and the services engines, impressive as they are, sit on top of a cyclical foundation. The truthful framing is a hybrid: a commoditised hardware base whose survival is underwritten by genuinely attractive services economics.

For an investor trying to cut through all of this, the discipline is to watch a small number of things rather than drown in the full income statement. Three key performance indicators capture the heart of the thesis. The first is iD Mobile subscriber growth—the cleanest single proxy for the high-margin recurring engine; as long as that subscriber base keeps compounding, the highest-quality part of the business is intact. The second is the size and renewal of the consumer protection-plan book—the active-plan count and its trajectory tell you whether the services moat is widening or eroding. And the third is free cash flow generation, which is both the metric management is most heavily incentivised against and the ultimate test of whether a low-margin retailer is actually creating value or merely churning revenue. Hardware like-for-like sales matter for the cyclical pulse, but it is these three—connectivity subscribers, the protection book, and cash conversion—that reveal whether the durable, defensible Currys is strengthening or fading.

XII. Epilogue

There is a neat symmetry to where this story lands. It began in 1884 with a man building bicycles in a Leicester garden—a single merchant selling the era's most exciting new technology to ordinary households and helping them when it broke. One hundred and forty-two years later, the company that grew out of that garden has shed a bloated, multi-brand conglomerate structure, survived a near-fatal merger, fought off two of the most formidable acquirers in global finance, and emerged as a lean, cash-generative, services-first omnichannel operator—doing, at its core, exactly what Henry Curry did: selling people technology they don't fully understand, and being there when it goes wrong.

And the man now taking the helm embodies that continuity better than any strategy slide ever could. Fredrik Tønnesen started his Currys career in 2005 as a twenty-year-old standing on a shop floor in Norway, selling appliances one customer at a time. In August 2026 he becomes Group Chief Executive of an LSE-listed company spanning the UK, Ireland, and the Nordics. In an age of celebrity outsider CEOs and private-equity flip artists, Currys chose the person who had sold the boxes himself—a wager that the deepest understanding of a retail business comes not from a spreadsheet but from the shop floor. Whether that wager pays off is the next chapter. But it is a fitting one for a company whose entire turnaround was, in the end, about remembering what it had always actually been good at.

References

-

Currys FY 2025/26 Trading Update — Currys plc, 2026-05-19 ↩↩↩↩↩

-

UK electronics retailer Currys rejects Elliott's improved £757 mln proposal — Reuters, 2024-02-27 ↩

-

China's JD.com says it will not make an offer for Currys — Reuters, 2024-03-15 ↩↩

-

Currys agrees to sell Greek unit Kotsovolos to PPC for 175 mln pounds — Reuters, 2023-11-03 ↩

-

Currys board recommends shareholders reject hostile bids — Financial Times, 2024-02-19 ↩

-

Currys names Nordics chief Tønnesen as group CEO — RTÉ, 2026-06-03 ↩↩

-

Carphone Warehouse and Dixons unveil £3.8 billion merger — Yahoo News UK / PA, 2014-05-15 ↩

-

Currys plc Results, Reports & Presentations — Currys plc Investor Relations ↩

-

Currys plc share price and market analysis — London Stock Exchange ↩

-

Behind the scenes: Currys repair centre — InternetRetailing, 2023-10-04 ↩

-

Elliott walks away from Currys takeover — Retail Gazette, 2024-03-18 ↩

-

Currys completes sale of its Greek business Kotsovolos following approval — Retail Week, 2024-03 ↩

-

Currys names shop-floor veteran as new boss as Baldock exits for Boots — Retail Gazette, 2026-06-03 ↩↩

-

Dixons Retail and Currys plc corporate history — Wikipedia ↩↩↩↩↩↩

-

Best Buy completes acquisition of 50% of Carphone Warehouse retail — Best Buy Co. Inc. Form 8-K, SEC, 2008-05 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube