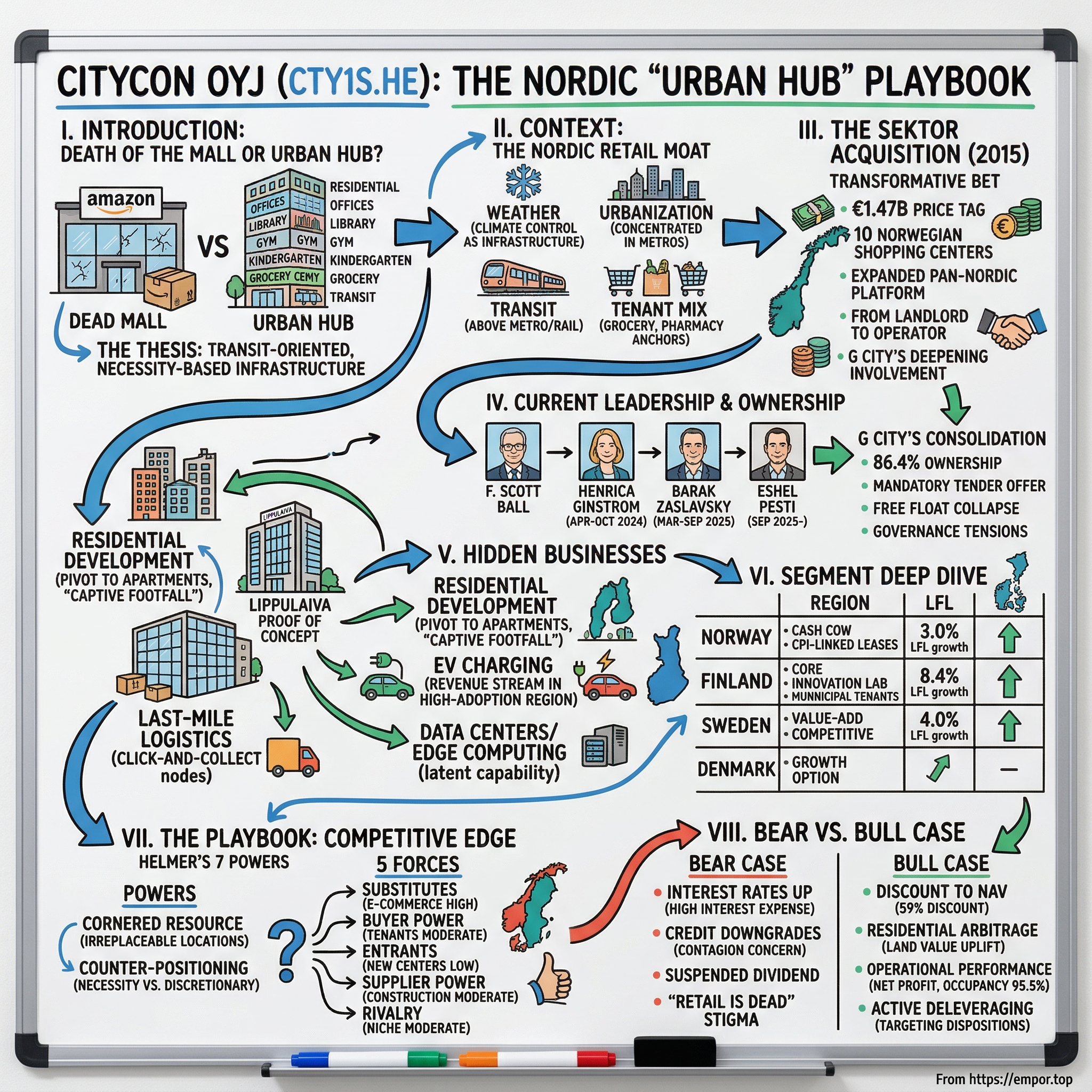

Citycon: The Nordic "Urban Hub" Playbook

I. Introduction: The Death of the Mall, or Is It?

There is a genre of YouTube video that has quietly become one of the platform's most addictive rabbit holes: the Dead Mall Tour. Some filmmaker walks through an echoing, half-lit American shopping center — a JCPenney sign hanging crooked, a food court with exactly one operating Sbarro — and the comment section fills with nostalgia and fatalism. Retail is dead. Amazon won. The mall is a relic of the Boomer era, destined for demolition or conversion into a warehouse for the very e-commerce companies that killed it.

Now picture a different scene. It is February in Helsinki, minus fifteen degrees Celsius outside, snow piled along the sidewalks. A mother pushes a stroller through automated glass doors into a gleaming, warm, LED-lit atrium. She drops her child at a municipal kindergarten on the second floor, picks up a prescription at the pharmacy next door, grabs groceries from K-Supermarket on the ground floor, and — before heading home to the apartment tower directly above her — pauses for coffee at a café overlooking an indoor plaza where teenagers are studying at tables operated by the city library. She never stepped outside. She never needed to.

This is not a mall. This is what Citycon Oyj calls an "Urban Hub." And the distinction matters enormously for anyone trying to understand why physical retail in the Nordics is not just surviving but actively attracting institutional capital in 2026.

The thesis is straightforward once you see it: Citycon is not a shopping mall company. It is a transit-oriented, necessity-based infrastructure play disguised as a retail landlord. Its centers sit on top of metro stations. Its anchor tenants are grocery stores, pharmacies, and healthcare clinics — not fast fashion chains vulnerable to Amazon. Its newest developments include hundreds of residential apartments built directly above the retail podium, creating what management calls "captive footfall" — residents who shop downstairs not because of marketing but because of gravity.

Founded in Finland in 1988, listed on the Helsinki exchange a decade later, and transformed by a massive Norwegian acquisition in 2015, Citycon has spent the last several years executing one of the most interesting pivots in European real estate: from passive landlord collecting rent checks to active developer building mixed-use urban nodes that blur the line between shopping center, apartment complex, transit hub, and municipal service center. Along the way, it has navigated a change of controlling shareholders, a revolving door of CEOs, a string of credit downgrades, and a share price that trades at a staggering discount to the replacement cost of its assets.

This is the story of how a "boring" Finnish property company ended up sitting on one of the most defensible portfolios in European retail — and why the market still cannot decide what it is worth.

II. Context: The Nordic Retail Moat

To understand Citycon, you first have to understand why retail real estate in the Nordics operates under fundamentally different rules than in the United States — or, for that matter, most of continental Europe.

Start with the weather. For roughly five months of the year, much of Scandinavia is genuinely inhospitable to outdoor activity. Temperatures regularly dip below minus ten. Daylight in December lasts fewer than six hours in Helsinki, fewer than five in northern Norway. In this context, enclosed, climate-controlled spaces are not luxuries — they are infrastructure. Nordic shopping centers function as de facto public squares, places where communities gather because the alternative is staying home in the dark. This is a cultural reality that has no real parallel in Texas or California, and it creates a floor of demand that has nothing to do with the quality of the retail offer inside.

Next, consider urbanization patterns. The Nordic countries are among the most urbanized in Europe, with populations heavily concentrated in a handful of metropolitan areas: Helsinki, Oslo, Stockholm, Copenhagen. These cities were built around robust public transit systems — metros, trams, commuter rail — rather than the car-dependent suburban sprawl that defines American retail geography. A shopping center located directly above a metro station in Helsinki or Oslo is not analogous to a strip mall off a highway exit in Ohio. It is more analogous to Grand Central Terminal — a piece of transit infrastructure that happens to contain retail, visited by tens of thousands of daily commuters whether or not they intend to shop.

Then there is the tenant mix, which is where Citycon's model diverges most sharply from the American mall archetype. In a typical US regional mall, the anchor tenants are department stores — Macy's, Nordstrom, JCPenney — surrounded by fashion retailers, electronics stores, and food courts. The entire model depends on discretionary spending, on consumers choosing to visit because they want something rather than because they need something. When Amazon made it easier to buy clothes and electronics from a couch, the model collapsed.

Citycon's centers are anchored by groceries. K-Supermarket, Prisma, Lidl, and Tokmanni in Finland. Coop, Rema 1000, KIWI, and NorgesGruppen in Norway. Management estimates that eighty to ninety percent of footfall is driven by necessity-based visits: buying food, picking up prescriptions, visiting a doctor, dropping off children at daycare. Fashion and discretionary retail exist in these centers, but they are supplementary — drawn by the foot traffic generated by grocery anchors rather than generating it themselves. Grocery e-commerce penetration in the Nordics remains below ten percent, far lower than general retail, which means the digital substitution threat that gutted American malls barely applies to Citycon's core traffic drivers.

The company's origins reflect this infrastructure-first positioning, even if the founders did not articulate it in those terms. When four Finnish institutional investors — insurance company Sampo Pension, state energy firm Imatran Voima, construction company Rakennustoimisto A. Puolimatka, and the Finnish postal bank Postipankki — established Citycon in 1988, they were assembling a portfolio of urban retail properties in the Helsinki metropolitan area during a period when the city's metro system was still being extended. The locations they secured — directly adjacent to or integrated with transit nodes in dense, high-income catchment areas — are the same locations that form the irreplaceable core of Citycon's portfolio today. You cannot build a new mall on top of the Helsinki Metro. Those sites were claimed decades ago, and Citycon owns them.

The company listed on the Helsinki Stock Exchange in March 1998 and was renamed Citycon Oyj in April 2002. For its first fifteen years as a public company, it was a solid but unremarkable Finnish landlord — steady rental income, modest growth, the kind of stock that pension funds owned and forgot about. It took a transformative acquisition to turn it into something more ambitious.

III. The Great Consolidation: The Sektor Acquisition

In May 2015, Citycon's management team walked into a conference room and announced a deal that would fundamentally alter the company's scale, geographic footprint, and strategic identity. The target was Sektor Gruppen, a privately held Norwegian shopping center portfolio owned by three family entities — Joh Handel Eiendom, Varner Invest, and K&S Holding. The price tag: approximately 1.47 billion euros on a debt-free basis. It was, by a wide margin, the largest transaction in Citycon's history.

What did 1.47 billion euros buy? Ten Norwegian shopping centers scattered across the country's major cities — Oslo, Bergen, Stavanger, Trondheim, Skien, Sarpsborg, and Elverum — all anchored by the same necessity-based grocery tenants that defined Citycon's Finnish portfolio: Coop, Rema 1000, KIWI, NorgesGruppen. The implied cap rate on the deal was approximately 5.2 percent, meaning Citycon was paying roughly nineteen times net operating income for these assets. In the zero-interest-rate environment of 2015, with the European Central Bank in full quantitative easing mode and Norwegian property yields compressing alongside every other asset class in the developed world, this looked broadly in line with market pricing. In hindsight — after the ECB began hiking rates aggressively in 2022 — it looked expensive. But that is the nature of real estate acquisitions: you buy at the yields available, not the yields you wish existed.

The financing structure revealed just how aggressive the bet was. Citycon funded the deal through a three-part cocktail. First, a 604-million-euro rights issue in July 2015 — the largest equity raise in company history — with the Canada Pension Plan Investment Board participating as a cornerstone investor, lending credibility and capital simultaneously. Second, 222 million euros drawn from a 400-million-euro bridge facility arranged by Danske Bank and Pohjola Bank. Third, approximately 671 million euros of existing Sektor bank debt assumed by Citycon. The combined effect pushed the company's loan-to-value ratio above fifty percent, a level that would later constrain its financial flexibility.

Was it a winner's curse? The honest answer is: it depends on the time horizon. In the short term, the deal saddled Citycon with a heavy debt load at what turned out to be the tail end of a historically cheap financing environment. When interest rates eventually rose, the cost of carrying that debt increased meaningfully — by 2025, Citycon's weighted average interest rate had climbed to just over four percent, and annual interest expense consumed roughly 45 percent of net rental income. That is a significant burden for a company whose entire business model depends on the spread between rental yields and borrowing costs.

But zoom out, and the strategic logic looks more compelling. The acquisition doubled Citycon's geographic footprint overnight, transforming it from a Finnish landlord with some Swedish exposure into a genuinely pan-Nordic platform. Norway, with its oil-supported economy, high consumer spending, and CPI-linked lease structures, gave Citycon a cash-generating engine that would prove resilient through multiple economic cycles. The Norwegian assets consistently delivered higher net rental income per square meter than the Finnish portfolio, and their inflation-linked rents provided a natural hedge against the rising cost environment that eventually arrived.

More importantly, the deal forced a cultural transformation. Sektor had been run as a hands-on operating business by its family owners, with deep relationships with tenants, active management of tenant mix, and a focus on center-level performance that went far beyond passive rent collection. Absorbing this operational DNA pushed Citycon from "landlord" to "asset manager" — a shift that would prove essential when the company later pivoted to the Urban Hub strategy. You cannot execute a mixed-use development program — building apartments, integrating municipal services, managing complex construction projects — with a passive landlord mentality. The Sektor integration taught Citycon how to operate, and that operational capability became the foundation for everything that followed.

The deal also marked the deepening involvement of Gazit-Globe — the Israeli-founded, globally diversified property platform led by Chaim Katzman — which had first acquired a significant stake in Citycon back in 2004 and would eventually become its controlling shareholder. The Sektor acquisition aligned perfectly with Katzman's long-stated philosophy: buy irreplaceable urban retail assets at discounts to replacement cost, hold for the long term, and focus on necessity-based "boring" retail in stable democracies. It was exactly the kind of deal that Gazit-Globe's playbook called for — big, transformative, and oriented toward assets that would be impossible to replicate.

IV. The Current Leadership: The Henrica Ginstrom Era and Beyond

Leadership at Citycon has been anything but stable in recent years, and the turbulence tells a story about the tensions between operational ambition and controlling-shareholder influence that define the company today.

The chapter begins with Henrica Ginstrom. Born in 1983, Finnish, educated with dual master's degrees — one in technology from Aalto University, one in economics from the Hanken School of Economics — Ginstrom joined Citycon in 2011 after a stint at PricewaterhouseCoopers' transaction services practice. She was, in every sense, an internal veteran. Over a decade at the company, she rotated through commercial leadership in Norway during the critical post-Sektor integration period, ran investor relations and communications, and was named Chief Operating Officer in 2018 when F. Scott Ball, an American real estate executive, took over as CEO.

Her appointment as CEO, effective April 1, 2024, was widely read as a signal. Ball had been a financial engineer — focused on capital structure, dispositions, and navigating the debt markets. Ginstrom's elevation suggested the board wanted the next phase to be about operational execution: delivering the Urban Hub developments, extracting value from the mixed-use pipeline, managing the complex construction and leasing programs that the strategy demanded. She knew the assets. She knew the tenants. She knew the Norwegian market intimately. On paper, it was the logical succession.

Then, six months later, she was gone. On October 8, 2024, Citycon announced that Ginstrom had stepped down "by mutual agreement." No public explanation was provided. No forward-looking rationale. Just a terse press release and the appointment of an interim arrangement. The abruptness shocked observers and raised immediate questions about what had happened behind closed doors. The most plausible interpretation — supported by the subsequent trajectory of events — is that her departure was driven by strategic disagreements with the controlling shareholder regarding the pace and direction of the company's transformation.

To understand that dynamic, you need to understand Chaim Katzman and G City. Katzman, born in Israel and trained as a lawyer, moved to South Florida in 1979 and spent the next four decades building Gazit-Globe — renamed G City around 2022 — into a global platform of grocery-anchored retail properties spanning Brazil, Northern Europe, and North America. His philosophy is deceptively simple: find irreplaceable urban retail assets in stable democracies, buy them at discounts to replacement cost, hold them forever, and focus relentlessly on necessity-based tenants that generate foot traffic regardless of economic conditions. It is a philosophy that maps almost perfectly onto Citycon's portfolio — which is precisely why Gazit-Globe first acquired a roughly 33 percent stake in the company back in 2004, and why Katzman himself became Chairman of Citycon's board in 2010.

What changed in 2024 and 2025 was the intensity of G City's control. In November 2025, G City crossed the fifty-percent ownership threshold, acquiring 14.2 million additional shares and pushing its combined voting rights — held through G City Ltd, subsidiary Gazit Europe Netherlands BV, and Katzman personally — to approximately 57.5 percent. Under Finnish securities law, crossing fifty percent triggered a mandatory public tender offer. G City offered four euros per share, a 35.8 percent premium to the October 31 closing price of 2.95 euros. After a 0.20-euro-per-share equity repayment was distributed to shareholders in January 2026, the offer price was adjusted to 3.80 euros.

The tender period ran from January 2 through March 6, 2026. Approximately 49.9 million shares — representing 27.2 percent of outstanding equity — were tendered. When the dust settled, G City held roughly 158.5 million shares, or 86.4 percent of all shares and voting rights. The free float collapsed to under fourteen percent. The squeeze-out threshold under Finnish law is ninety percent — meaning G City is tantalizingly close to being able to force remaining minority shareholders to sell.

The ownership consolidation has had cascading effects. Three CEOs cycled through in eighteen months: Ginstrom from April to October 2024, Barak Zaslavsky from March to September 2025, and the current CEO, Eshel Pesti — previously CEO of G City Europe — who took over in September 2025. CFO Hilik Attias is also aligned with G City. The management team is now effectively a subsidiary operation, executing the parent's strategic vision rather than operating with independent board oversight in the traditional Nordic governance sense.

For long-term investors, this leadership instability and ownership concentration create a genuine governance question. On one hand, the "owner-operator" model that Katzman champions has a long track record of value creation in real estate — concentrated ownership can enable faster decision-making, longer time horizons, and willingness to invest through cycles rather than optimizing for quarterly earnings. On the other hand, minority shareholders are now exposed to the credit profile and strategic priorities of G City itself, a relationship that has already had material financial consequences, as the credit rating trajectory makes painfully clear.

V. Hidden Businesses: Beyond the Storefront

Walk into a Citycon property today and the retail floor tells only part of the story. The more interesting narrative is happening on the floors above, in the parking structures below, and in the digital infrastructure threaded through the walls.

The most significant strategic shift in Citycon's recent history is the pivot to residential development — building apartments directly on top of its retail centers. The concept is elegant in its simplicity: Citycon already owns land in the most desirable, transit-connected urban locations in the Nordics. That land is currently valued by the market as depressed commercial retail, but its actual utility — proximity to metro stations, surrounded by dense urban populations, zoned for mixed-use development — makes it worth premium residential prices. The arbitrage between how the market values the land (retail) and how residents value the land (home) is the core of the opportunity.

Lippulaiva, Citycon's flagship development in Espoonlahti (part of the greater Helsinki metropolitan area), is the proof of concept. Opened on March 31, 2022, Lippulaiva is a 150,000-square-meter mixed-use complex that integrates approximately 44,000 square meters of commercial space — roughly a hundred shops, cafés, and restaurants anchored by K-Supermarket, Prisma, Lidl, and Tokmanni — with more than 560 residential apartments in towers ranging from four to fourteen stories. Two hundred and seventy-five of those units were developed by Citycon itself; the remainder were built by development partners including Hausia. The complex sits directly on top of a Helsinki metro station that handles approximately 14,000 daily commuters. It houses the 2,900-square-meter Espoonlahti regional library, operated by the City of Espoo. It contains a Pilke kindergarten, an Elixia fitness center, and a Terveystalo medical clinic — Finland's largest private healthcare provider.

Beneath the surface, Lippulaiva features 170 geothermal wells drilled three hundred meters into Finnish bedrock, forming one of Europe's largest geothermal heating and cooling systems for a commercial building. The property earned LEED Gold certification and became the world's first building to receive a Smart Building Gold certificate. It is, in the fullest sense of the phrase, a city in a box.

The term "captive footfall" that management uses to describe the residential component is not marketing fluff — it describes a genuine economic dynamic. When five hundred families live in apartments directly above a grocery store, pharmacy, and kindergarten, those families generate retail demand with zero customer acquisition cost. They do not need to be advertised to. They do not need to be lured with promotions. They need milk and diapers and prescriptions, and the most convenient place to get those things is the elevator. This creates a baseline of foot traffic that is essentially weather-proof, recession-resistant, and immune to e-commerce competition.

Management has identified more than 300,000 square meters of additional residential building potential across the Nordic portfolio, spread across approximately twenty potential projects with total capital expenditure estimated at around two billion euros and roughly 590,000 square meters of gross leasable area. More than half of the planned development capital is directed toward residential. The next major project, RE:Liljeholmen in Stockholm, envisions expanding an existing 48,000-square-meter center to approximately 118,000 square meters of mixed-use space: roughly 120 apartments, 30,000 square meters of offices, a 14,000-square-meter hotel, and 6,000 square meters of public space, with construction expected to run through the late 2020s.

Below ground level, Citycon's parking structures represent another underappreciated asset. The company has committed to deploying EV charging infrastructure across all of its properties, transforming parking garages from cost centers into revenue-generating energy hubs. In a region where electric vehicle adoption is among the highest in the world — Norway leads globally in EV market share — this is not a marginal opportunity. It is a structural revenue stream that grows in proportion to the energy transition.

The properties also serve increasingly as last-mile logistics nodes. Rather than competing with e-commerce, Citycon's urban locations function as click-and-collect and micro-fulfillment points, turning the supposed existential threat into a complementary revenue source. When a consumer orders groceries online from a retailer operating inside a Citycon center, the center itself becomes the distribution point. The building earns rent regardless of whether the consumer walks in or drives through.

Finally, there is the unpriced optionality of data center and edge computing. Citycon's properties — located in dense urban areas, connected to robust power grids, equipped with fiber infrastructure, and in some cases cooled by geothermal systems — possess exactly the physical characteristics that edge computing operators seek. The Nordic countries rank among the world's most attractive data center markets thanks to cool climates, cheap renewable energy, and political stability. Citycon has made no public announcements in this space, but the latent capability is there, waiting to be monetized if and when management chooses to pursue it.

VI. Segment Deep Dive: The Nordic Map

Citycon operates twenty-eight shopping centers plus one additional property across four countries. Each geographic segment plays a distinct role in the portfolio, and the financial profile of each tells a different story about risk, return, and strategic priority.

Norway is the cash cow. The ten centers acquired through the Sektor deal — Stovner Senter, Linderud Senter, Kolbotn Torg, and Liertoppen in the Oslo region; Oasen in Bergen; Kilden in Stavanger; Solsiden in Trondheim; Herkules in Skien; Storbyen in Sarpsborg; and Kremmertorget in Elverum — generate the highest net rental income per square meter in Citycon's portfolio. Norwegian leases are typically linked to the consumer price index, which means rents escalate automatically with inflation — a feature that proved enormously valuable during the inflationary spike of 2022-2023. The Norwegian economy, buoyed by oil and gas revenues and sovereign wealth fund stability, supports consumer spending levels that exceed those of Finland and Sweden. Three non-core Norwegian centers were divested in 2024 as part of the broader portfolio rationalization, but the remaining assets are firmly positioned as core holdings.

Norway's like-for-like net rental income growth in the first nine months of 2025 came in at three percent — the lowest of Citycon's geographic segments, but this reflects the maturity and stability of the portfolio rather than weakness. These are fully leased, fully optimized assets generating steady, inflation-protected cash flows. The Norwegian krone denomination does introduce currency risk for euro-reporting Citycon, but it also provides diversification away from the eurozone.

Finland is the core — the historical heartland and the innovation lab. Citycon's nine Finnish centers, including Lippulaiva and the company's flagship Iso Omena complex in Espoo (which also serves as corporate headquarters), represent the most advanced expression of the Urban Hub concept. Finland is where Citycon has the deepest management expertise, the longest tenant relationships, and the most ambitious development pipeline. The integration of municipal services — libraries, kindergartens, health clinics — into retail centers is most developed here, creating tenant relationships backed by sovereign-grade municipal credit quality on leases that often run ten to fifteen years or longer.

Finnish like-for-like net rental income growth was the strongest in the portfolio at 8.4 percent in the first nine months of 2025, reflecting both the operational excellence of the core Finnish assets and the ongoing lease-up of Lippulaiva as the complex matures. The Finnish segment also includes Rocca al Mare in Tallinn, Estonia — a legacy Baltic asset that operates under broadly similar dynamics.

Sweden represents the value-add opportunity — and the greatest source of both growth potential and risk. Citycon operates six centers in Sweden, including Kista Galleria in Stockholm's technology district (where the company acquired the remaining minority interest in early 2024 to take full ownership) and the RE:Liljeholmen development. Sweden is Citycon's most competitive market, with a deeper pool of institutional property investors and more liquid transaction activity than Finland or Norway. The Swedish commercial property sector was rocked by the SBB crisis of 2023-2024, when that company's aggressive leverage and opaque corporate structure led to a dramatic loss of market confidence that colored sentiment across the entire Nordic property sector. Citycon's Swedish portfolio delivered like-for-like net rental income growth of four percent in the first nine months of 2025 — solid but reflective of the more challenging competitive environment.

Denmark is the smallest segment — just two centers — functioning more as a growth option than a core portfolio pillar. Copenhagen's strong demographic fundamentals and high urbanization rates make it an attractive market, but Citycon's Danish presence is more opportunistic than strategic at this stage.

Across the full portfolio, total net rental income for fiscal year 2025 reached 209.2 million euros, with like-for-like growth of 5.4 percent. Average retail rents climbed 3.3 percent year-over-year to 27.70 euros per square meter. Tenant sales grew 1.7 percent while footfall increased 2.0 percent — modest but positive in a macroeconomic environment characterized by consumer caution. The occupancy rate held at 95.5 percent, consistent with the company's historical range above ninety-five percent and indicative of the limited supply of competing space in Citycon's micro-markets.

VII. The Playbook: 7 Powers and 5 Forces Analysis

The intellectual framework for evaluating Citycon's competitive position requires two lenses: Hamilton Helmer's 7 Powers, which explains why the company can sustain abnormal returns, and Michael Porter's 5 Forces, which maps the structural threats to those returns.

Start with Helmer. The most potent power Citycon possesses is the Cornered Resource — its physical locations. This cannot be overstated. You cannot build a new shopping center on top of an existing Helsinki Metro station. You cannot replicate the Lippulaiva site. You cannot construct a competing retail complex at Kista Galleria's exact position within Stockholm's technology corridor. These locations were secured decades ago, when Nordic cities were still building out their transit infrastructure. The planning permissions, the physical integration with rail and metro systems, the established pedestrian flows — all of these create a resource monopoly that no competitor can replicate at any price. In Helmer's terminology, this is the purest form of Cornered Resource: the asset itself is unique, non-reproducible, and generates demand that is location-specific rather than brand-specific.

The second relevant power is Counter-Positioning. While global retail real estate peers — particularly American REITs and European operators like Unibail-Rodamco-Westfield and Klépierre — were still anchored to the discretionary fashion model that Amazon was systematically dismantling, Citycon pivoted to a mixed-use, necessity-based model that its larger competitors could not easily copy. Why? Because copying it would require those competitors to cannibalize their existing business models. A company like Unibail that has invested billions in luxury flagship malls cannot simultaneously reposition itself around grocery stores and municipal kindergartens without confusing its investor base, alienating its high-end tenants, and destroying its brand identity. Citycon had the freedom to make this pivot precisely because it was smaller, less visible, and operating in a geography where the necessity-based model was culturally organic rather than strategically imposed. The incumbents were stuck; Citycon was free to move.

Now apply Porter's 5 Forces. The Threat of Substitutes is the one that dominates every conversation about retail real estate, and it is genuinely high. E-commerce is not going away. Online grocery delivery is growing, even if slowly in the Nordics. Any honest analysis of Citycon's competitive position must acknowledge that digital commerce represents a permanent, structural headwind to physical retail foot traffic. Citycon's hedge is the grocery anchor: people still overwhelmingly buy fresh food in person, and that behavior is stickier than almost any other retail category. As long as consumers prefer to squeeze their own avocados, the grocery anchor model has a moat. But "as long as" is doing real work in that sentence.

The Bargaining Power of Buyers — in this context, tenants — is where Citycon's model generates a structural advantage that is easy to overlook. Consider the difference between a Zara and a pharmacy. Zara, as a large international fashion retailer, has enormous bargaining power: it can choose among dozens of competing malls, it can threaten to leave, it can demand rent concessions and tenant improvement allowances. A pharmacy or grocery store anchoring a Citycon center has far less leverage. These tenants need to be located where their customers live and commute — which means they need Citycon's specific locations as much as Citycon needs them. A KIWI or Rema 1000 grocery store cannot easily relocate from a metro-integrated center to a random street corner without losing the foot traffic that justifies its lease. This mutual dependency — rather than one-sided landlord power — creates stable, long-duration leasing relationships with limited rent volatility. It is less glamorous than signing a luxury brand at a premium rent, but it is far more predictable.

The Threat of New Entrants is low to negligible. Building a new transit-integrated mixed-use center in a major Nordic city requires years of planning approvals, enormous capital investment, and physical integration with public transit infrastructure that is controlled by municipal authorities. The barriers to entry are not merely financial; they are regulatory, physical, and political. No rational competitor would attempt to build a new Lippulaiva when the process would take a decade and cost hundreds of millions of euros with no guarantee of planning approval.

The Bargaining Power of Suppliers — primarily construction firms and municipal authorities who control zoning — is moderate. Construction costs in the Nordics have risen meaningfully, and planning processes can be slow and unpredictable. This constrains Citycon's ability to develop new projects quickly, but it also constrains every other player in the market, reinforcing the value of existing assets.

Industry Rivalry is moderate within the specific niche that Citycon occupies. The closest strategic peer is Cibus Nordic Real Estate, a pure-play grocery-anchored retail REIT, but Cibus lacks transit integration, municipal tenant relationships, and residential development optionality. Castellum and Sagax, Sweden's other major listed property companies, operate in different asset classes (offices, logistics, industrial) and are not direct competitors. The cautionary tale in the Nordic property space is SBB, which operated nominally "safe" community service properties but destroyed shareholder value through excessive leverage and opaque governance — a reminder that asset quality alone does not protect investors from balance sheet risk.

VIII. Bear vs. Bull Case: The Valuation Narrative

The bear case for Citycon begins with interest rates and ends with governance. This is a capital-intensive business that depends on the spread between rental yields and borrowing costs to generate returns. When Citycon's weighted average interest rate climbed to just over four percent and annual interest expense reached 93.7 million euros in fiscal 2025 — consuming roughly forty-five percent of net rental income — the math got uncomfortable. Total debt stands at 2.39 billion euros against a portfolio valued at approximately 3.8 billion euros, producing a loan-to-value ratio of 44.9 percent. That LTV has improved meaningfully from 47.3 percent in fiscal 2024, but it remains elevated by Nordic REIT standards and leaves limited room for error if property values decline or refinancing costs increase.

The credit rating trajectory is the most visible expression of this risk. Standard and Poor's has downgraded Citycon four times in eighteen months: from BBB- to BB+ in March 2025, then to B+ in November 2025, and again to B in March 2026. Crucially, these downgrades were driven not by operational deterioration — S&P explicitly acknowledges that Citycon operates as an "insulated subsidiary" with independent funding — but by the governance implications of G City's increasing ownership concentration. The rating agency's concern is contagion: that G City's own credit profile and strategic priorities could ultimately compromise Citycon's financial independence. This is not an irrational fear. When a parent company controls 86.4 percent of the equity, the question of whose interests are being served is not academic.

The suspended dividend amplifies the bearish sentiment. For fiscal year 2025, Citycon proposed no dividend — a sharp break from the company's history of paying 1.10 euros per share. A one-time equity repayment of 0.20 euros per share from fiscal 2024 was distributed in January 2026, but the signal to income-seeking investors was clear: cash flow is being redirected toward debt reduction and parent-company priorities rather than shareholder distributions. For a stock that historically attracted investors precisely because of its dividend yield, this represents a fundamental change in the investment thesis.

The "retail is dead" stigma, while increasingly inaccurate as applied to Citycon's specific model, continues to weigh on the stock price. Generalist investors see "shopping center REIT" in the Bloomberg terminal and move on, unable or unwilling to differentiate between a necessity-anchored Nordic urban hub and a dying American mall. This perception gap is real and persistent.

The bull case starts with the most striking number in Citycon's entire financial profile: the discount to net asset value. EPRA Net Reinstatement Value stands at 8.45 euros per share. The stock trades at approximately 3.45 euros. That is a fifty-nine percent discount — meaning the market is pricing Citycon's assets at roughly forty-one cents on the euro. Even accounting for the governance risk, the credit downgrades, and the suspended dividend, buying a portfolio of irreplaceable transit-integrated Nordic real estate at less than half its appraised value is an extraordinary proposition. Either the appraised values are dramatically wrong, or the market is dramatically wrong. Given that Citycon's occupancy rate has held above ninety-five percent, like-for-like net rental income is growing at 5.4 percent, and tenant sales are positive, the case that the assets are fundamentally impaired is difficult to make.

The residential arbitrage is the second pillar of the bull case. Citycon's identified development pipeline of 300,000-plus square meters of residential potential represents a transformation of land value from depressed-retail to premium-residential. The Lippulaiva proof of concept demonstrated that this works — that you can build high-quality apartments on top of a shopping center, fill them with residents, and generate both direct residential rental income and indirect retail foot traffic. If Citycon executes even a fraction of its two-billion-euro development pipeline, the portfolio's value composition shifts materially toward a higher-valued asset class.

The operational performance tells a story of a company that is executing well at the property level regardless of the corporate-level noise. Fiscal year 2025 net profit came in at 94.9 million euros, compared to a loss of 37.9 million euros in the prior year. Fair value gains on investment properties of 51.1 million euros reversed prior write-downs, suggesting that the physical assets are appreciating even as the stock price languishes. Like-for-like net rental income growth of 5.4 percent, with Finland delivering an exceptional 8.4 percent, demonstrates pricing power that is rare in European retail real estate. The company's 2026 outlook indicates that like-for-like growth is expected to exceed 2025 levels.

Citycon has also been actively managing its balance sheet. Over 750 million euros of debt was repaid or tendered during 2025. Assets classified as held for sale totaled 510 million euros at year-end 2025, with management targeting approximately one billion euros in dispositions over the next twenty-four months. The proceeds are being directed toward deleveraging, which — if executed — should bring the LTV ratio toward the low forties and potentially stabilize or reverse the credit rating trajectory. Available liquidity of 278.7 million euros, including a 250-million-euro undrawn revolving credit facility, provides adequate near-term buffer.

The green bond program adds a dimension of capital markets sophistication. A 300-million-euro green bond placed in February 2024 was seven times oversubscribed. A 450-million-euro placement in 2025 drew six times oversubscription. These are not the capital markets of a company in distress — they are the capital markets of a company whose assets generate cash flows that fixed-income investors want to own, even if equity investors remain skeptical.

For investors tracking Citycon's ongoing performance, two KPIs matter above all others. First, the Loan-to-Value ratio, which measures the relationship between debt and asset values and is the single best indicator of whether the balance sheet is improving or deteriorating. At 44.9 percent and trending downward, this metric is moving in the right direction, but it needs to continue declining toward forty percent or below to fully de-risk the equity story. Second, the occupancy rate, which at 95.5 percent confirms that the underlying demand for Citycon's space remains robust. Any sustained decline below ninety-three percent would signal that the necessity-based anchor model is weakening — a development that would undermine the entire investment thesis.

IX. Epilogue: The Future of the "Urban Hub"

Stand in the atrium of Lippulaiva on a weekday morning and watch the flows. Commuters emerging from the metro escalator, splitting left toward the grocery store or right toward the library. Parents dropping children at kindergarten before heading upstairs to apartments or back down to the train. A delivery driver loading click-and-collect orders into a van in the loading dock. A technician checking the geothermal monitoring panel in the basement. What is this place? It is not a mall. It is not an apartment complex. It is not a transit station. It is not a municipal service center. It is all of these things simultaneously — a piece of urban infrastructure that generates rental income as a byproduct of being essential to daily life.

The question that will define Citycon's next decade is whether the company can scale this model across its portfolio while navigating the governance complexities of near-total ownership by G City. The residential development pipeline suggests that management — or, more precisely, G City's management — sees the future clearly: these properties are worth more as mixed-use urban nodes than as standalone retail centers, and the value uplift from residential conversion is substantial enough to justify years of capital investment and construction risk. The target of carbon neutrality across all operations by 2030, backed by science-based targets and a portfolio that is seventy-six percent BREEAM-certified, adds an ESG dimension that institutional investors increasingly require.

But the path from here to there is not smooth. With three CEOs in eighteen months, a credit rating that has fallen from investment grade to single-B, a collapsed free float, and a controlling shareholder whose own strategic priorities may not perfectly align with those of remaining minority investors, Citycon presents a classic case of an exceptional asset portfolio trapped inside a complicated corporate structure. The assets are irreplaceable. The locations are priceless. The tenant mix is resilient. The operational performance is strong. The governance situation is genuinely uncertain.

History will judge whether the Urban Hub model — the idea that a shopping center can evolve into a transit-integrated, necessity-anchored, residential-inclusive piece of city infrastructure — was a genuine strategic innovation or a clever rebrand of a mature business. The evidence from Lippulaiva and the broader Nordic portfolio suggests the former. Grocery-anchored retail in dense, transit-connected, weather-challenged cities is not dying. It is adapting. And the company that owns the best locations for that adaptation — whatever its corporate complications — holds an asset base that the market has not yet figured out how to price.

The "boring is beautiful" philosophy that Chaim Katzman has preached for decades — the idea that the most valuable real estate is the one anchored by the store where people buy bread and milk — finds its purest Nordic expression in Citycon's portfolio. Whether the current corporate structure allows that value to flow to public shareholders, or whether it will be captured entirely by the controlling parent, remains the central question. For investors with the patience and risk tolerance to bet on the asset quality winning out over the governance noise, Citycon offers a proposition that is rare in European real estate: genuinely irreplaceable properties, trading at a fraction of their replacement cost, in markets where necessity never goes out of style.

X. Top Links and Further Reading

- Citycon 2025 Financial Statements Release and Strategy Update

- Analysis of the Lippulaiva "City in a Box" Project and its Geothermal Innovation

- G City Mandatory Tender Offer Documentation and Board Statement (December 2025 - March 2026)

- Nordic REIT Benchmarking: Citycon vs. Castellum vs. Sagax vs. Cibus Nordic

- S&P Global Ratings Reports on Citycon Credit Rating Trajectory (2025-2026)

- Citycon Carbon Neutral by 2030 Sustainability Framework and Science-Based Targets

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube