CTT: The 500-Year-Old Startup

I. Introduction: The Portuguese Paradox

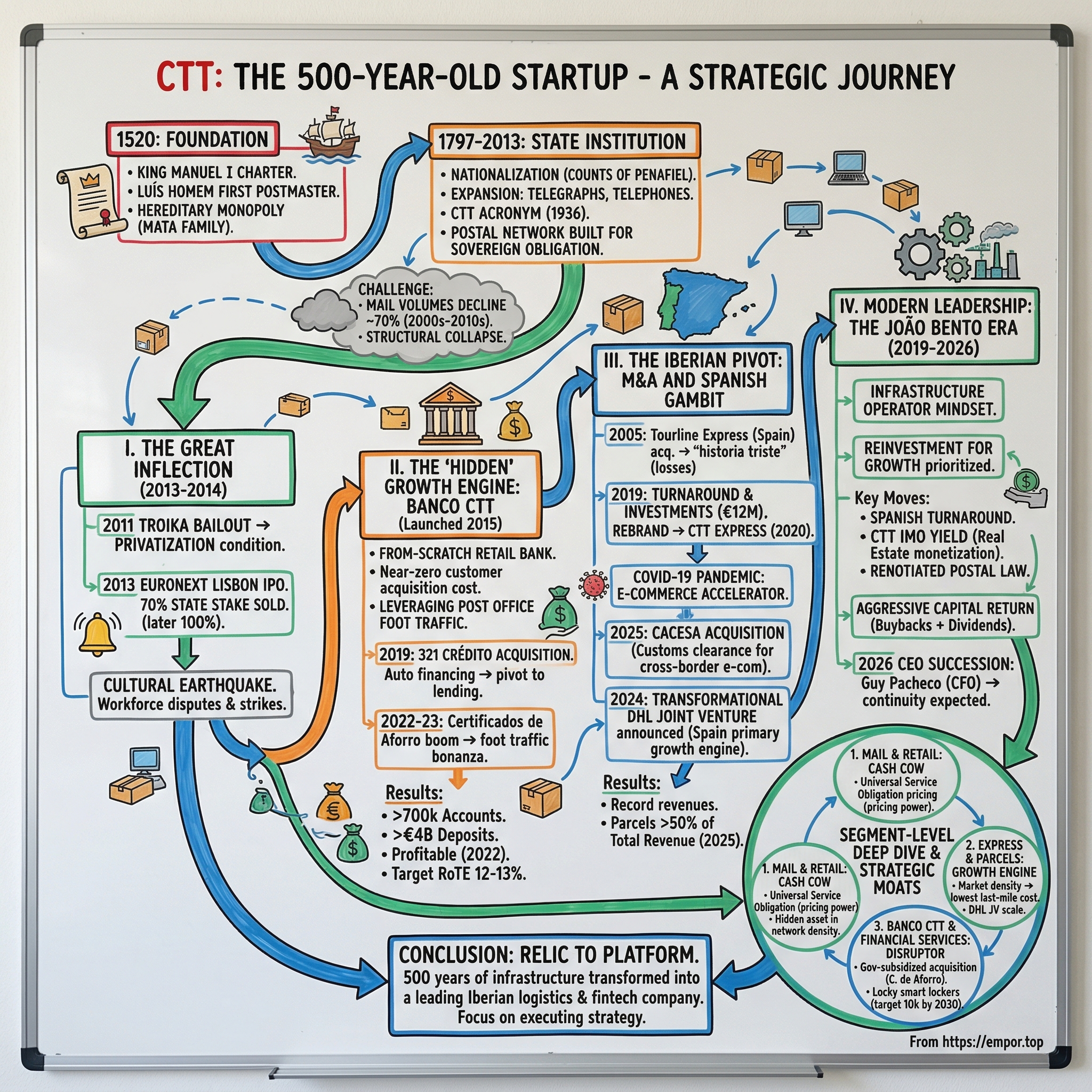

Picture a company born in 1520. Not 1920. Not 1820. The year 1520, when Magellan was still circumnavigating the globe and Martin Luther had just nailed his theses to a church door. Now picture that same company, half a millennium later, posting record revenue growth, running a fast-scaling digital bank, and closing a billion-euro logistics joint venture with DHL. That is CTT — Correios de Portugal.

The question that should immediately occur to any serious investor is: how? How does an institution that predates the steam engine, the telegraph, the telephone, and the internet not only survive but emerge as one of the top-performing mid-cap stories in European logistics and fintech? The answer is not luck, and it is not government life support. It is one of the most deliberate, strategically coherent pivots in modern business history.

Here is the thesis, stated plainly: CTT is not a postal service. It has not been a postal service in any meaningful strategic sense for at least a decade. What CTT actually is, underneath the royal heritage and the red-and-white branding, is a physical network play — a company that owns the densest last-mile logistics infrastructure in Portugal and an increasingly dominant parcel network across the entire Iberian Peninsula, with a high-return-on-equity bank embedded inside it as a bonus. The market, for years, valued CTT like a melting ice cube — a declining mail operator on a single-digit multiple — and largely ignored everything else. That gap between perception and reality is where the story gets interesting.

To understand CTT today requires understanding three inflection points. The first is the 2013 privatization, when Portugal's sovereign debt crisis forced the government to sell the postal service to private investors, creating the conditions for genuine strategic transformation. The second is the 2015 launch of Banco CTT, a from-scratch retail bank that leveraged existing post office foot traffic to achieve near-zero customer acquisition costs and now manages billions in deposits. The third is the COVID-19 pandemic, which turbocharged e-commerce adoption across Iberia and validated what had been a risky, loss-making bet on the Spanish parcel market.

Each of these moments could have gone wrong. The privatization could have produced a cost-cutting zombie. The bank could have been a vanity project. The Spanish expansion could have bled the company dry. Instead, a succession of management teams — most critically under CEO Joao Bento from 2019 to 2026 — turned each of those risks into compounding advantages. The result is a company generating over 1.2 billion euros in annual revenue, with its fastest-growing segment now accounting for more than half of the top line, and a bank that is quietly becoming one of Portugal's most efficient financial institutions.

This is the story of how a 500-year-old institution reinvented itself — not once, but three times — and what it tells us about the economics of physical networks, the power of embedded finance, and the surprisingly high stakes of delivering packages in a country most global investors cannot find on a map.

II. 500 Years in 10 Minutes: The Foundation

On November 6, 1520, in the royal court at Evora, King Manuel I signed a charter that would outlast his dynasty, his empire, and nearly every institution of its era. The charter appointed Luis Homem — a soldier who had served in the Orient and traveled as the king's ambassador to Flanders — as Portugal's first Correio-Mor do Reino, the Grand Postmaster of the Kingdom. Homem had observed the famous Thurn und Taxis postal network operating across Central Europe and convinced the king that Portugal needed a system of its own. The timing was not accidental. Portugal was at the zenith of its maritime empire — spices flowing from Goa, gold from West Africa, sugar from Brazil — and the court needed a reliable way to communicate with its merchants, diplomats, and colonial administrators scattered across four continents.

What makes the early history of CTT genuinely unusual is not that a postal system existed — most European powers had one — but that the position of Correio-Mor became hereditary. In 1606, during the Iberian Union when Spain and Portugal shared a crown, King Philip II sold the office to a wealthy nobleman named Luis Gomes da Mata Coronel for 70,000 cruzados. The Mata family would control Portugal's postal system for nearly two hundred years, passing it from father to son like a feudal estate. It was, in effect, one of the world's first hereditary infrastructure monopolies — a family business that happened to be the nervous system of an empire.

The dynasty ended in 1797, when growing complaints about service quality led Queen Maria I's government to nationalize the post, compensating the Mata family with the title "Counts of Penafiel." From that point forward, the postal service was a state institution, evolving through the nineteenth and twentieth centuries in step with Portugal itself: the merger with telegraphs in 1880, the addition of telephones, the formal adoption of the CTT acronym (Correios, Telegrafos e Telefones) in 1936, and the separation of telecommunications into what would become Portugal Telecom in 1992. By then, CTT stood for "Correios de Portugal" — Posts of Portugal — and nothing else.

But here is why the history matters for investors today: those five centuries created something that no competitor can replicate and no amount of capital can buy. CTT's post office network — roughly 600 offices and over 2,300 service points — reaches every single citizen in Portugal, from downtown Lisbon to the most remote village in the Azores. That network was built not for commercial efficiency but for sovereign obligation, which means it covers places no rational private company would ever choose to serve. That apparent disadvantage is, paradoxically, the company's greatest asset. Because when you want to build a bank, or launch a parcel delivery service, or install a network of smart lockers, having a physical presence in every community in the country is not a cost — it is a platform.

The problem, of course, was that by the 2000s the core product flowing through that platform was dying. Email had begun its systematic destruction of letter mail. Between the early 2000s and the 2010s, Portuguese mail volumes declined by approximately seventy percent — a structural, irreversible collapse that mirrored what was happening to postal operators worldwide. As of the IPO filing in 2013, mail collection and delivery still represented nearly sixty-two percent of total revenue. CTT was, in the bluntest terms, a company whose primary product was evaporating, whose cost structure was built for a volume level that would never return, and whose workforce of civil-service-era employees had spent careers in an institution that measured success by coverage, not profit.

The leadership team that ran CTT through the 2000s understood this. They cut operating expenses by an average of six percent annually from 2010 to 2012, trying to right-size the cost base. But cost-cutting alone could not solve the fundamental problem. You cannot shrink your way to growth. What CTT needed was not austerity but transformation — and transformation, for a state-owned monopoly, required something that only an external shock could provide.

III. The Great Inflection: Privatization (2013–2014)

The external shock arrived in April 2011, when Portugal formally requested a bailout from the Troika — the European Commission, the European Central Bank, and the International Monetary Fund. The country received seventy-eight billion euros in emergency financing, and in exchange, the conservative government of Prime Minister Pedro Passos Coelho agreed to a program of fiscal austerity, structural reform, and privatization. The state would sell its crown jewels: EDP, the energy utility, went to China Three Gorges for 2.7 billion euros. REN, the electricity grid operator, was sold to China's State Grid and Oman Oil. ANA, the airport operator, fetched over three billion euros. And CTT, the postal service, would go to the public markets.

The political context was extraordinarily turbulent. In 2013, a wave of cabinet resignations pushed Portuguese government bond yields toward an unsustainable seven percent. Passos Coelho's Social Democrats were hammered in local elections in September. The privatization program was not a strategic choice — it was a condition of survival. The Troika demanded asset sales, and the Portuguese government complied because the alternative was sovereign default.

CTT's IPO launched on December 5, 2013, on Euronext Lisbon. The state, through its holding company Parpublica, sold seventy percent of CTT's shares — 105 million out of 150 million total — at a price of 5.52 euros per share. Institutional investors took eighty percent of the offering, Portuguese retail investors took fifteen percent, and CTT employees received up to five percent. Retail demand was oversubscribed more than nine times — a remarkable show of confidence in a postal operator with declining mail volumes, or perhaps a reflection of just how few investable Portuguese assets were available at the time.

The stock opened at 5.90 euros, a seven percent premium, valuing the company at roughly 885 million euros. In September 2014, the remaining thirty percent state stake was sold in an accelerated bookbuild to institutional investors, completing the full privatization. Total proceeds to the Portuguese Treasury exceeded 900 million euros — a meaningful contribution to a country that desperately needed every cent.

But the IPO was not just a financial transaction. It was a cultural earthquake. CTT had been a state institution for over two centuries, and its workforce reflected that identity. The CGTP, Portugal's most powerful trade union confederation, characterized the privatization as if "the country were under occupation by foreign powers." Workers faced the elimination of holiday bonuses equivalent to two extra monthly salaries, the extension of the workday by half an hour, and cuts to vacation from twenty-five to twenty-two days. In the years that followed, chronic workforce disputes erupted over hiring practices, mail delivery delays, and the replacement of cash food subsidies with meal cards. Multiple strikes followed.

The cultural challenge was real and should not be underestimated. Transforming an institution that had served as a pillar of the Portuguese state for nearly five hundred years — with deep roots in national identity, universal service obligations, and civil service expectations — into a commercially driven, shareholder-accountable entity is one of the hardest things in business. Most privatizations of this kind produce either stagnant bureaucracies or stripped-down cost-cutting vehicles. What happened at CTT was neither. The first CEO of the private era, Francisco de Lacerda, who had been appointed in 2012 just before the IPO, laid out three strategic pillars: operational transformation, expansion of the parcels and e-commerce business, and — most audaciously — the creation of a bank from scratch. That third pillar, Banco CTT, would prove to be the most consequential strategic decision in the company's modern history.

IV. The "Hidden" Growth Engine: Banco CTT

To appreciate the genius of Banco CTT, you need to understand the state of Portuguese banking in 2015. The sector had just endured its own near-death experience. Banco Espirito Santo, one of Portugal's oldest and most prestigious financial institutions, had spectacularly collapsed in 2014, wiped out by fraud, mismanagement, and exposure to the family's crumbling business empire. The wreckage was carved into Novo Banco, a "bridge bank" eventually sold to the American distressed-debt fund Lone Star. Millennium BCP, the largest private bank, had been bailed out and was now controlled by China's Fosun International and Angola's Sonangol. Caixa Geral de Depositos, the state bank, required a massive recapitalization. In total, over sixty percent of Portugal's banking system had fallen into foreign hands.

The top five banks controlled approximately ninety percent of total banking assets. Fees were high, service was often poor, and public trust was in the gutter. Portuguese consumers, burned by the BES collapse and the broader financial crisis, were deeply suspicious of incumbent banks. Into this environment, CTT proposed something that sounded almost absurdly simple: open a bank inside the post offices.

Banco CTT was registered on August 24, 2015, as a wholly owned subsidiary. It opened its first branches in November 2015, then made a dramatic statement by launching fifty-one branches simultaneously across eighteen districts in March 2016 — the largest single-day branch opening in Portuguese banking history. The technology stack was built from scratch on Finastra's core banking platform, designed to be lean and modern rather than burdened by legacy systems. The product offering was deliberately simple: current accounts, savings products, basic credit. No investment banking, no complex derivatives, no corporate lending. Just straightforward retail banking for Portuguese families and small businesses.

The strategic logic was elegant. CTT already had the most extensive branch network in Portugal — over six hundred post offices and thousands of service points. Millions of Portuguese citizens were already walking through those doors every month to send letters, pay bills, collect pensions, and — critically — subscribe to Certificados de Aforro, the government's retail savings bonds that could only be purchased in person at CTT offices. Every one of those visitors was a potential banking customer, and the marginal cost of offering them a bank account while they were already standing at the counter was close to zero.

This is the concept that the investment community sometimes calls a "cornered resource." CTT did not need to spend millions on branch fit-outs, prime real estate, or marketing campaigns to acquire customers. The customers were already there. The building was already there. The brand — five hundred years of institutional trust — was already there. In an industry where customer acquisition cost is one of the primary drivers of profitability, Banco CTT's structural advantage was enormous.

The growth trajectory confirmed the thesis. From zero in 2015, Banco CTT grew to over 500,000 accounts by around 2020 and reached 701,400 current accounts by the third quarter of 2025, with deposits exceeding four billion euros. The bank is now the eleventh largest in Portugal by total assets at approximately 4.5 billion euros, holding a 1.15 percent market share. That sounds small next to the giants, but it makes Banco CTT the fastest-growing bank in Portugal by percentage terms, and it achieved this position with just 212 branches and roughly 450 dedicated employees — a fraction of what traditional banks require.

The loan book was transformed in 2019 through the acquisition of 321 Credito, a specialist used-car financing company, for approximately 140 million euros. This was a pivotal move: it improved the bank's loan-to-deposit ratio from roughly thirty percent to over seventy percent, turning Banco CTT from a deposit-gathering operation into a genuine lending institution. The car loan book reached nearly 950 million euros by early 2025, while the mortgage portfolio — launched in 2017 — grew to over 850 million euros. A strategic partnership with Generali in late 2022 added insurance distribution to the product suite.

The financial performance has been impressive. After years of startup losses — cumulative net losses of roughly 67 million euros from 2017 through 2020 — the bank reached breakeven in 2021 and turned decisively profitable in 2022, when rising interest rates across Europe dramatically improved net interest margins for all banks. Return on tangible equity reached 12.4 percent in early 2025, with management targeting 12 to 13 percent through 2028. Pre-tax profit hit 26 million euros in 2024, with a target of 40 to 50 million euros by 2028.

There was an unexpected accelerant. In 2022 and 2023, as the European Central Bank aggressively raised rates, the Euribor-linked returns on Certificados de Aforro became extremely attractive — well above what commercial banks were offering on deposits. Portuguese households poured over 20 billion euros into government savings bonds in just over a year, and since these could only be subscribed at CTT post offices, the result was enormous queues at branches nationwide. CTT had to implement an appointment booking system to manage the congestion. But every person standing in line to buy government bonds was exposed to Banco CTT's products. The foot traffic bonanza was a structural, recurring customer acquisition channel that no competitor could replicate.

The reason Banco CTT remains "hidden" in the valuation is straightforward. Most investors and most screening tools categorize CTT as a postal company and slap a low multiple on the entire business. But if you value the bank separately — at even a conservative one times book value on its roughly 270 million euros in equity — that alone represents over thirty percent of CTT's entire market capitalization. The bank is not a side project. It is a high-return, fast-growing financial institution embedded inside a logistics company, and the market has been slow to recognize it.

V. The Iberian Pivot: M&A and the Spanish Gambit

Portugal is a country of roughly ten million people. Spain has forty-seven million. For any Portuguese company with ambitions in logistics, the math is inescapable: you can dominate your home market and still be a small player, or you can cross the border and compete in one of Europe's largest parcel markets. CTT chose the latter, and the journey nearly broke the company before it made it.

The story begins in 2005, when CTT acquired Tourline Express, a Spanish express delivery company founded in 1996, for 28.5 million euros. The strategic rationale was sound — create an integrated Iberian logistics platform by combining CTT's dominant Portuguese network with a Spanish presence. The execution was anything but smooth. Tourline was a mid-tier player in a brutally competitive market, facing off against Correos Express (the Spanish postal incumbent, used by sixty percent of Spanish consumers), SEUR (backed by France's La Poste group, with over ten thousand employees), DHL, GLS, MRW, and the ever-expanding in-house logistics arm of Amazon.

For over a decade, Tourline was what CTT's own CEO would later call a "historia triste" — a sad story. Between 2016 and 2020, the Spanish operations accumulated approximately 25 million euros in operating losses. The business lacked scale, lacked automation, and lacked the kind of focused management attention that a turnaround requires. It was the classic trap of international expansion: the parent company was distracted by its own transformation, the subsidiary was too small to compete effectively, and the temptation to simply sell it and walk away grew stronger with each quarterly loss.

The turnaround began in earnest under Joao Bento's leadership starting in 2019. CTT invested 12 million euros over three years in the Spanish business — sixty percent on warehouse mechanization and new facilities, forty percent on digital systems and operational technology. More than thirty new distribution centers were opened to build a consolidated national network. The company was rebranded from Tourline Express to CTT Express in February 2020, creating a unified Iberian identity. And then, in what can only be described as extraordinary timing, the pandemic hit.

COVID-19 was a catastrophe for many businesses, but for e-commerce logistics operators, it was the great accelerator. Spanish e-commerce adoption surged: by 2024, sixty-one percent of Spanish shoppers were making at least one online purchase per month, up from forty-four percent in 2020. CTT Express was positioned to capture this wave. In the fourth quarter of 2020, the company incorporated Amazon and AliExpress into its distribution operations, delivering an average of 60,000 packages daily from those two platforms alone. Full-year 2020 volumes exceeded 50 million packages across the Iberian Peninsula, with Spanish activity growing seventy percent year-over-year — hitting the company's two-year growth target in just twelve months.

By the first half of 2021, CTT Express reached breakeven in Spain and posted positive operating income in the second quarter. Sales in Iberia grew fifty percent in the first half of 2021 versus the prior year, with Spain specifically growing eighty percent. The turnaround was real.

The numbers since then have been remarkable. Spanish revenue hit a record 186.8 million euros in 2023, then exploded to 305.6 million euros in 2024 — a sixty-four percent year-over-year increase. Parcel volumes in Spain surged nearly 127 percent in 2024. The Express and Parcels segment as a whole posted recurring operating income of 36.1 million euros in 2024, up eighty-three percent from the prior year, with margins expanding from 5.8 to 7.5 percent. By the third quarter of 2025, Express and Parcels represented fifty-two percent of CTT's total revenue — surpassing Mail for the first time in the company's history. Spain alone accounted for nearly sixty-two percent of the segment's revenue.

Two strategic acquisitions cemented the position. In early 2025, CTT completed the acquisition of CACESA, a Spanish international e-commerce customs clearance company, for approximately 104 million euros — roughly 5.5 times operating income. CACESA had doubled in size over the prior two years, generating 92 million euros in revenue and 20 million in operating income in 2023. The acquisition gave CTT the customs clearance capabilities essential for handling cross-border e-commerce volumes — the packages flowing from Chinese marketplaces like Temu and Shein that have become a massive and growing share of European parcel traffic.

Then came the transformative deal. In December 2024, CTT and DHL Group announced a joint venture for Iberian parcel delivery. Under the structure, DHL would purchase a twenty-five percent stake in CTT Expresso (the Portuguese parcel unit) while CTT would acquire twenty-five percent of DHL's parcel business in Iberia. The deal included a 69 million euro cash payment to CTT. Combined, the two operations would generate approximately one billion euros in revenue with daily capacity exceeding one million shipments across the peninsula. The European Commission unconditionally approved the venture in March 2026, and closing was expected in May 2026. Spain, once the "sad story," had become CTT's primary growth engine and the foundation of what management clearly envisions as the leading independent parcel platform in Iberia.

VI. Modern Leadership: The Joao Bento Era

Joao Bento was not an obvious choice to run a postal company. An engineer by training — civil engineering from Instituto Superior Tecnico, a PhD from Imperial College London — he had spent his career in heavy industry and infrastructure. He ran Efacec, the Portuguese industrial equipment manufacturer, from 2011 to 2015. Before that, he spent eleven years on the executive board of Brisa, Portugal's largest motorway concessionaire, overseeing operations, innovation, and business development. He served as vice-chairman and CEO of Gestmin SGPS (now Manuel Champalimaud SGPS), the family holding company of one of Portugal's most prominent business dynasties, from 2015 to 2019. He joined CTT's board as a non-executive director in April 2017 and was appointed CEO on May 22, 2019, succeeding Francisco de Lacerda.

What Bento brought was not postal expertise but something arguably more valuable: the mindset of an infrastructure operator who understood how to extract value from physical networks. At Brisa, he had learned that the motorway itself was just a platform — the real value was in the tolling systems, the service areas, the data, and the concession rights that created recurring, inflation-protected revenue streams. He applied the same lens to CTT.

The shift under Bento was decisive. His predecessor, Lacerda, had launched the bank and begun the parcels expansion, but the late years of Lacerda's tenure were marked by a "dividends at all costs" approach that left the company underinvested. The stock had declined significantly from its post-IPO highs, reflecting both the structural decline in mail and the market's skepticism about the Spanish operations. Bento reversed the priority order: reinvestment for growth first, shareholder returns second — but structured intelligently through buybacks rather than just dividends.

Three strategic moves defined the Bento era. First, the turnaround of the Spanish business, which we have already discussed. Second, the monetization of CTT's real estate portfolio through the creation of CTT IMO Yield in October 2022. This subsidiary was established to manage most of CTT's property holdings — 398 logistics, retail, and mixed-use properties across Portugal, covering 240,000 square meters of gross leasable area with a book value of 105 million euros. CTT sold a twenty-six percent stake in this vehicle for 36 million euros (implying a total portfolio valuation of roughly 137 million euros) to institutional and family office investors, including a 3.6 percent stake to Sonae Sierra, one of Europe's leading real estate specialists. CTT then became the principal tenant under long-term, inflation-linked leases. This was classic capital recycling: unlock the value trapped in property, redeploy it into higher-return logistics and banking investments, and retain operational control of the physical locations.

Third, Bento pushed for and secured a renegotiation of the postal law and the universal service concession contract with ANACOM, Portugal's postal and telecom regulator. The 2026-2028 price convention allowed average annual price increases of 9.1 percent for the basket of universal service products — essential for offsetting continued volume declines in traditional mail and maintaining the viability of the rural post office network.

On capital return, Bento implemented a dual approach: dividends of 0.17 euros per share (a yield of roughly 2.5 percent at current prices) plus aggressive share buybacks. The most recent program, announced in February 2026, authorized 30 million euros in repurchases — three percent of the market capitalization — to be executed by April 2027, with shares to be cancelled. The weighted average shares outstanding declined from roughly 150 million at the time of the IPO to approximately 133 million by 2025, a meaningful reduction that has amplified per-share earnings growth.

The incentive structure under Bento reflected the shift. The Long-Term Incentive Plan, approved at the 2021 general meeting, awarded retained shares to executive directors based on total shareholder return and ESG-linked metrics. Insider ownership remained below one percent — a legitimate concern for governance purists, though the LTIP alignment and the active engagement of major shareholders partially mitigated this.

Bento, having turned sixty-five, announced that he would step down at the annual general meeting on April 30, 2026. His successor, Guy Pacheco, has been CTT's CFO since 2017 and was deeply involved in every major strategic decision of the past decade — the DHL joint venture, the CACESA acquisition, the Banco CTT build-out, and the share buyback programs. The major shareholder consortium backing Pacheco's appointment includes Manuel Champalimaud Group (approximately fifteen percent of shares), Indumenta Pueri (approximately fourteen percent), GreenWood Investors (approximately seven percent), and Grupo Sousa. GreenWood Investors, led by Steven Wood who serves as a non-executive board member, has been a vocal proponent of CTT since 2018, with a thesis centered on under-penetrated e-commerce, fixable Spanish losses, real estate monetization, and improved capital allocation. CTT was a top contributor to GreenWood's portfolio returns in the first half of 2025.

The continuity of strategy under Pacheco is likely — this is the CFO who built the financial architecture now stepping into the CEO role, not an outsider with a mandate to disrupt.

VII. Segment-Level Deep Dive: The Three Pillars

Understanding CTT requires understanding each of its three business segments as essentially independent companies that happen to share a physical network. Each has its own economics, its own growth trajectory, and its own competitive dynamics. Together, they create a portfolio that is more resilient and more valuable than any single piece.

Mail and Retail: The Cash Cow

Mail remains the highest-margin segment, though it is unambiguously a declining business. Letter volumes have fallen roughly seventy percent from their peak, and the trajectory is not going to reverse — nobody is going to start sending more physical letters because email got boring. What protects this segment, and what makes it more valuable than a simple volume-times-price calculation would suggest, is the Universal Service Obligation. CTT is legally required to maintain postal delivery across all of mainland Portugal, Madeira, and the Azores. In return, it holds approximately seventy-nine percent of Portuguese postal traffic and has pricing protection through the ANACOM-regulated price convention, which allows annual increases that offset much of the volume decline.

The retail network — the six hundred post offices and thousands of service points — is the hidden asset within this segment. Those locations generate foot traffic for Banco CTT, serve as pickup and drop-off points for parcels, host Certificados de Aforro subscriptions, and increasingly function as nodes in the Locky smart locker network. The mail itself may be declining, but the infrastructure it built is the platform on which everything else runs. Think of it like a department store anchor tenant: the mail business is Macy's, generating less excitement every year, but its presence keeps the foot traffic flowing to every other store in the mall.

Revenue from Mail accounted for roughly 42.5 percent of group revenue in 2024, though its share is declining as Express and Parcels grows faster. Margins remain attractive because the cost structure has been systematically right-sized over two decades of decline management.

Express and Parcels: The Growth Engine

This is where the energy is. Express and Parcels generated approximately 460 million euros in revenue in 2024, up over forty percent year-over-year, and reached 52 percent of group revenue by the third quarter of 2025. Spain accounts for nearly sixty-two percent of the segment and is growing at roughly double the rate of the Portuguese operations.

The competitive positioning is strong but not unassailable. In Portugal, CTT holds an estimated thirty percent of the parcel delivery market and benefits from the density of its existing postal network — when you already deliver to every address in the country six days a week, adding a parcel to the route is incrementally cheap. In Spain, CTT Express has captured over fifteen percent of the market following the CACESA acquisition, making it a meaningful player in what remains one of the most fragmented parcel markets in Western Europe, where a long tail of small operators still represents nearly twenty percent of the market.

The margin trajectory is encouraging. Segment recurring operating income nearly doubled from 19.7 million euros in 2023 to 36.1 million in 2024, with margins expanding from 5.8 to 7.5 percent. By the third quarter of 2025, margins had reached 9.5 percent. For context, integrated express operators like DHL and FedEx typically run operating margins in the high single digits to low double digits in their ground networks. CTT is approaching competitive parity while still in a high-growth phase, which suggests further margin expansion as volumes scale and fixed costs are absorbed.

The DHL joint venture, pending its expected May 2026 closing, will be transformative for this segment. Combined daily capacity of over one million shipments across Iberia and combined revenues of approximately one billion euros will create the critical mass needed to compete with the Spanish national incumbent Correos and the global integrators.

Banco CTT and Financial Services: The Disruptor

Banking and financial services contributed approximately 128 million euros in revenue in 2024, with the segment growing over twenty-three percent in the first half of 2025. This is the smallest of the three pillars by revenue but arguably the highest quality in terms of return on capital and strategic optionality.

The Certificados de Aforro dynamic deserves emphasis. These government retail savings bonds, which can only be subscribed at CTT post offices or through a limited online portal, create a structural, government-subsidized customer acquisition channel. When rates are attractive — as they were in 2022 and 2023 — the resulting foot traffic is enormous. Portuguese households applied 5.45 billion euros in Certificados de Aforro in 2025 alone. Every one of those transactions brings a person into a CTT branch, where they encounter Banco CTT's products. The government effectively pays for CTT's customer acquisition.

The bank's 2025-2028 strategic plan targets over one million accounts (from roughly 700,000 today), business volumes of 12 to 14 billion euros (from approximately seven billion), pre-tax profit of 40 to 50 million euros, and sustained return on tangible equity of 12 to 13 percent. The planned annual investment of 15 to 18 million euros for 2026 through 2028 is modest — a testament to the capital-light model enabled by the shared branch network.

Beyond the bank itself, CTT has built two additional capabilities worth watching. Locky, the smart parcel locker network, has grown to approximately 1,200 carrier-agnostic self-service lockers in Portugal and an initial deployment of 60 in Spain, with an expansion target of up to 10,000 across the Iberian Peninsula by 2030. These lockers work with multiple carriers, not just CTT, and are deployed at supermarkets, Galp filling stations, shopping centers, and metro stations. Some include refrigerated compartments for grocery delivery in partnership with 360hyper, a Portuguese online grocery marketplace. Roughly 300,000 consumers have registered for the virtual address service that routes online orders to a preferred Locky location. And 360hyper itself — a marketplace model aggregating products from multiple supermarket chains including Continente and Minipreco — represents an early-stage bet on last-mile grocery logistics, leveraging CTT's delivery infrastructure.

VIII. The Playbook: Strategic Moats and Competitive Forces

Every company claims to have a moat. Few actually do. The question for CTT is whether its advantages are durable or merely temporary, and whether they compound over time or erode. Let us apply two of the most rigorous frameworks in strategy — Hamilton Helmer's Seven Powers and Michael Porter's Five Forces — to find out.

Seven Powers Analysis

Three of Helmer's seven powers apply directly to CTT, and they are among the most potent in the framework.

The first is scale economies, specifically in last-mile logistics. Delivery economics are fundamentally about density: the more packages you deliver per route, the lower the cost per package. CTT already delivers mail to every address in Portugal six days a week. Adding a parcel to an existing route costs far less than a competitor building routes from scratch. In Spain, the DHL joint venture will create the kind of volume density — over one million daily shipments — that makes competing on cost extremely difficult for smaller players. This is a scale advantage that increases with volume, and the e-commerce growth trend is providing that volume year after year.

The second is switching costs, concentrated in Banco CTT. Once a customer has their salary deposited into a Banco CTT account, has their mortgage and car loan serviced there, and has their insurance products linked to it, the cost of switching to another bank is substantial — not in financial penalties, but in the sheer friction of changing direct debits, updating payment information, and re-establishing credit relationships. Banking is one of the stickiest consumer relationships in existence. Portuguese consumers change banks less frequently than they change mobile phone providers.

The third is the cornered resource: the exclusive right to operate the postal retail network under the Universal Service Obligation, combined with the near-exclusive channel for Certificados de Aforro subscriptions. No competitor can replicate this. You cannot build six hundred post offices in every municipality in Portugal, and the government is not going to issue a second universal postal license. This is a legally protected, physically embedded, historically entrenched competitive advantage.

Porter's Five Forces

The threat of substitutes is real but narrower than it appears. Yes, email killed letter mail. That substitution is complete and irreversible. But nothing substitutes for the physical delivery of an iPhone, a pair of shoes, or a bottle of wine ordered online. E-commerce requires atoms, not just bits, to reach the consumer. The last-mile delivery of physical goods is growing, not shrinking, and the more commerce moves online, the more critical — and more valuable — physical delivery networks become. Digital substitution destroyed CTT's old business but is simultaneously fueling its new one.

The bargaining power of buyers is the most significant competitive risk. Amazon is building its own last-mile delivery network across Europe and has already begun reducing its dependence on third-party carriers. If Amazon internalizes enough of its Iberian delivery volume, CTT loses a major customer. However, Spain's market fragmentation works in CTT's favor — Amazon needs partners for rural coverage and peak-season overflow, and CTT's network density in Portugal makes it nearly irreplaceable for Portuguese deliveries. The diversification across thousands of e-commerce merchants, rather than dependence on a single platform, is a deliberate strategic choice.

The bargaining power of suppliers is moderate. CTT's primary "suppliers" are labor (delivery drivers, postal workers, bank employees) and real estate (branch locations, sorting facilities). Labor costs are managed through the ongoing transition from legacy civil-service contracts to more flexible private-sector arrangements, though this remains a source of friction and union opposition. Real estate costs have been partially addressed through the CTT IMO Yield structure, which converted owned properties to leased ones with inflation-linked rent escalators.

The threat of new entrants is low in postal delivery (protected by the USO) and banking (heavily regulated, requires a license) but higher in parcels, where any logistics company with capital can enter the market. The DHL joint venture significantly raises the barrier by creating the kind of scale that new entrants would struggle to match.

Competitive rivalry is intense in parcels — Correos, SEUR, GLS, MRW, DHL, and FedEx all compete aggressively in Spain — but more muted in Portuguese postal services and in retail banking, where Banco CTT occupies a distinct niche as the "simple, trusted, low-cost" alternative to the oligopoly incumbents.

The two key performance indicators that matter most for tracking CTT going forward are these: first, Express and Parcels volume growth and margin expansion — this is the segment that will determine whether CTT successfully transitions from a mail company to a logistics company, and the margin trajectory from 5.8 percent in 2023 to 9.5 percent in the third quarter of 2025 is the single most important operational metric to monitor. Second, Banco CTT's growth in total business volumes (deposits plus loans plus off-balance-sheet savings), which captures the bank's ability to deepen customer relationships and scale its lending operations — the path from seven billion euros today to the twelve-to-fourteen-billion-euro target by 2028 will be the clearest indicator of whether the embedded banking model is compounding.

IX. Bear vs. Bull Case

The Bear Case

Start with the risks that keep skeptics awake at night. The first is regulatory. CTT operates under a Universal Service Obligation that requires it to maintain delivery coverage across all of Portugal, including economically unviable rural areas. The Portuguese government, through ANACOM, controls the pricing framework for these services. If a future government decides to squeeze pricing to benefit consumers, or if the USO is expanded without adequate compensation, CTT's mail segment margins would compress. The 2026-2028 price convention allows annual increases averaging 9.1 percent, which is generous, but there is no guarantee that future conventions will be as favorable. Political risk is inherent in any business that depends on government concessions.

The second risk is the cost of maintaining the physical network. Six hundred post offices, 2,300 service points, and hundreds of logistics facilities represent a massive fixed-cost base. If mail volumes continue declining — and they will — the question is whether parcel volumes and banking traffic can grow fast enough to absorb those costs. The real estate monetization through CTT IMO Yield helped, but it also transformed ownership into a lease obligation with inflation-linked escalators. In a high-inflation environment, those lease costs rise automatically.

The third risk is Spain. The Express and Parcels turnaround has been impressive, but Spain remains one of the most competitive parcel markets in Western Europe. Correos, the national incumbent, has its own e-commerce ambitions and a vastly larger domestic network. Amazon continues to build out its own delivery capacity. SEUR, backed by La Poste, has deep pockets. The DHL joint venture addresses scale, but integration risk is real — joint ventures between competitors are inherently complex, with misaligned incentives always lurking beneath the surface. And CACESA, the customs clearance acquisition, was purchased at 5.5 times operating income on the back of two years of rapid growth driven by the China-to-Europe e-commerce surge. If regulatory changes (new EU customs rules, tariffs on Chinese imports) slow that cross-border flow, the acquisition could look expensive in hindsight.

Management transition adds near-term uncertainty. Bento's departure and Pacheco's elevation represent continuity, but every CEO transition carries execution risk, particularly when the incoming leader must navigate a complex joint venture integration, a banking expansion plan, and an ongoing market share battle in Spain simultaneously.

Insider ownership below one percent is a governance concern. While the LTIP provides some alignment and the major shareholders are engaged, the lack of meaningful direct ownership by management means the interests of executives and shareholders are not perfectly aligned through the simplest and most powerful mechanism — personal wealth at risk.

The Bull Case

The bull case rests on a sum-of-the-parts valuation gap that the market has been slow to close but that cannot persist indefinitely. CTT currently trades at roughly 899 million euros in market capitalization. Break the business into its components.

Banco CTT has approximately 270 million euros in equity, is earning a return on tangible equity above twelve percent, and is growing its business volumes at double-digit rates. A bank with these characteristics, if publicly traded, would command at minimum one to 1.5 times book value. That implies a standalone value for the bank of 270 to 405 million euros — thirty to forty-five percent of CTT's entire market cap.

The Express and Parcels segment generated 36 million euros in recurring operating income in 2024, growing at eighty-three percent year-over-year, with margins still well below peer averages. At a conservative 12 to 15 times operating income — below where comparable logistics businesses trade — this segment is worth 430 to 540 million euros.

Add those two together and you reach 700 million to 945 million euros — which means the market is essentially giving you the Portuguese mail business, the retail network, the Locky locker platform, the real estate portfolio, and the 360hyper optionality for free or close to it.

The share buyback program reinforces the bull case. When management is actively spending 30 million euros to repurchase and cancel shares — reducing the denominator of every per-share metric — it signals confidence that the stock is undervalued. Combined with dividends, the total capital return yield is meaningful.

The DHL joint venture, if it closes as expected in May 2026, is a structural catalyst. Combined revenues of one billion euros and daily capacity of over one million shipments across Iberia will reposition CTT from a mid-tier player to the co-leader of the Iberian parcel market. The 69 million euros in cash from DHL provides additional capital for debt reduction or reinvestment.

Finally, there is the secular tailwind of e-commerce penetration in Iberia, which remains below the European average. As more commerce moves online in Spain and Portugal, the volume flowing through CTT's network grows — and in a density-driven business, incremental volume drops to the bottom line at high margins. Locky's expansion to 10,000 lockers by 2030 adds an out-of-home delivery capability that is increasingly preferred by consumers across Europe and which further reduces per-unit delivery costs.

X. Epilogue and Final Reflections

Joao Bento will walk into the annual general meeting on April 30, 2026, and hand the keys to Guy Pacheco. When he does, he will leave behind a company that is almost unrecognizable from the one he inherited seven years earlier. In 2019, CTT was a declining Portuguese postal operator with a loss-making Spanish subsidiary, a startup bank, and a stock price that had fallen more than fifty percent from its post-IPO highs. In 2026, it is an Iberian logistics platform with a billion-euro joint venture, a growing digital bank with over 700,000 accounts, a smart locker network expanding across two countries, and revenue approaching 1.3 billion euros.

The story of CTT is ultimately a story about path dependency — but not in the way that term is usually used. Path dependency typically describes the negative version: companies trapped by their history, unable to escape legacy systems, legacy costs, and legacy thinking. CTT experienced the positive version. Five hundred years of postal infrastructure created the densest physical network in Portugal. That network, built for letter delivery, became the platform for parcel logistics. The same branch locations became the storefronts for a digital bank. The same universal service obligation that seemed like a burden turned out to be a barrier to entry that no competitor could cross.

None of this was inevitable. The network was an asset, but assets without strategy are just costs. What the last decade of private-sector management contributed was the strategic imagination to see the platform underneath the postal service and the operational discipline to build new businesses on top of it. The bank could have been a gimmick. The Spanish expansion could have been an ego trip. The real estate monetization could have been a one-time cash grab. Instead, each decision was made in service of a coherent long-term vision: transform CTT from a Portuguese postal monopoly into an Iberian logistics and financial services platform.

The question for investors now is whether the market will eventually value CTT for what it has become rather than what it used to be. The company's three segments serve different masters — mail serves regulation and legacy, parcels serve e-commerce growth, and banking serves retail consumers — but they share a physical infrastructure that creates operating leverage across all three. As parcels scale, the network costs are spread across more volume. As the bank grows, the branch network generates higher returns per square meter. As the Locky network expands, delivery costs decline. Each piece reinforces the others.

CTT has survived the Age of Exploration, the fall of the Portuguese Empire, two world wars, a revolution, a sovereign debt crisis, and the death of letter mail. The next chapter — the DHL joint venture, the banking expansion, the push toward ten thousand smart lockers — will determine whether this 500-year-old institution completes its transformation from relic to platform. The infrastructure is in place. The strategy is coherent. The execution, so far, has been better than almost anyone expected.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube