Compass Group PLC: The Invisible Empire of Food

I. Introduction & Episode Roadmap

Think about the last meal you ate that you did not cook or pay a restaurant directly to prepare. Maybe it was a tray of pasta in a corporate cafeteria between meetings. Maybe it was the chicken tenders in a university dining hall, the hot dog in a stadium concourse, the hospital lunch on a plastic tray, or the surprisingly decent curry served 200 kilometres offshore on a drilling platform in the North Sea. There is a very good chance that the food was cooked, plated, and served by a company whose name never appeared on the plate, the napkin, or the receipt.

That company is very often Compass Group PLC. It is the largest contract foodservice company on earth, and almost nobody outside the industry can pick its logo out of a lineup. It is the definition of an invisible giant: a business that touches billions of human meals a year while remaining completely faceless to the people eating them.

The scale is genuinely difficult to hold in your head. In its fiscal year ending September 2025, Compass generated $46.1 billion in underlying revenue, grew operating profit 11.7% to $3.34 billion, and lifted its underlying operating margin to 7.2%.1 It operates in around 40 countries, serves billions of meals a year, and employs more than half a million people, which makes it one of the largest private-sector employers in the world.2 If you wanted a single number to capture the improbability of the thing: a business built on cafeteria trays and sandwich counters is a FTSE 100 blue chip worth tens of billions.

Two recent decisions frame just how far this "British" company has drifted from Britain. First, on 1 October 2023, Compass changed its financial reporting currency from pounds sterling to US dollars, on the logic that the bulk of its earnings are generated in dollars and reporting in sterling was injecting pure noise into its numbers.[^4] Second — and this is the genuinely unusual one — on 1 April 2026, Compass changed the currency in which its ordinary shares actually trade on the London Stock Exchange, from sterling pence to US dollars.3 A FTSE 100 constituent quoting itself in dollars in London is close to unheard of. The reason is blunt: roughly three-quarters of the company's profit comes from North America, so pricing the shares in pounds was, in management's telling, simply mistranslating an American earnings stream for a global investor base.9

This is a story about how a wartime canteen operator became that. It runs through Gerry Robinson's audacious management buy-out, Francis Mackay's invention of "sectorisation," a United Nations bribery scandal that nearly ended the company, the operational turnaround under Richard Cousins that made Compass a market darling, the seaplane tragedy that killed him at the peak of his powers, the near-death experience of COVID-19, the quiet cash machine called Foodbuy, and the post-pandemic land grab management calls "first-time outsourcing." Throughout, the question worth holding onto is the skeptical one: is Compass a genuinely advantaged compounder, or a low-margin labour business that has simply been run unusually well? Let us go find out.

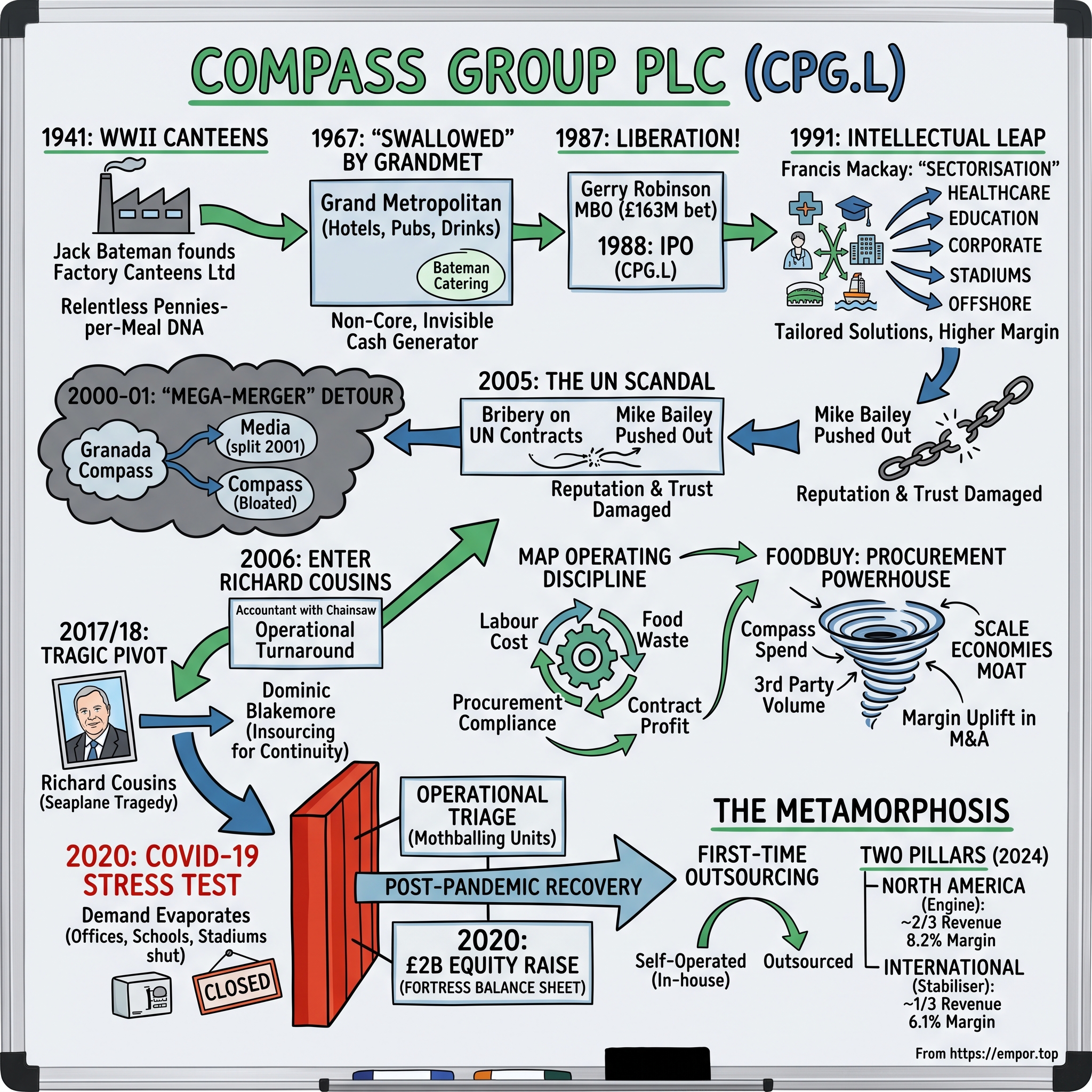

II. From Factory Canteens to Conglomerate Chaos: The Historical Bedrock

The origin is almost too on-the-nose for a British industrial story: it begins in a war. In 1941, with Britain's factories running around the clock to feed the war machine and rationing squeezing every household, a man named Jack Bateman founded Factory Canteens Limited to feed munitions workers who could not go home for lunch.2 There was nothing glamorous about it. Feeding shift workers cheaply, at scale, on tight rations, was a logistics problem dressed up as a catering problem — and that DNA, the relentless management of pennies per meal, never really left the company. Factory Canteens became Bateman Catering, and for a generation it was simply one of several firms doing the unromantic work of feeding people at work.

The next chapter is the corporate equivalent of being swallowed. In 1967, the sprawling conglomerate Grand Metropolitan — better known as GrandMet, a giant of hotels, pubs, and branded drinks — acquired both Bateman Catering and Midland Catering.2 For roughly two decades, contract catering sat inside GrandMet as a non-core division, a rounding error next to the hotels and the Smirnoff bottles. It generated cash and attracted almost no attention. This is a recurring pattern in the Compass story: catering is a wonderful business to own and a boring one to talk about, which means it repeatedly ends up buried inside companies that would rather talk about something else.

The liberation came in 1987. Gerry Robinson, a hard-charging Irish executive who had risen through GrandMet's ranks, led a £163 million management buy-out of the contract catering division and renamed it Compass Group.2 An MBO of this size in 1987 was an act of conviction: the managers were betting their own careers, and a mountain of debt, that they could run the business better untethered than tethered. In 1988, Compass went public on the London Stock Exchange, and the invisible giant had, for the first time, its own ticker.8

The company's intellectual leap came under Francis Mackay, who became chief executive in 1991. Mackay's insight was deceptively simple and turned out to be the strategic foundation of the modern company: feeding a hospital is not the same problem as feeding an investment bank, a school, a stadium, or an offshore rig. So he broke foodservice apart into specialised customer verticals — healthcare, education, business and industry, sports and leisure, defence and offshore — each with its own brand, its own kitchen design, its own menu logic, and its own labour-cost profile. Compass came to call this "sectorisation," and it converted a generic commodity — cooking — into a portfolio of tailored, higher-margin solutions. A caterer that understands the specific rhythms and regulations of hospital food can charge for that expertise in a way that a generalist canteen operator cannot.

Then came the near-fatal detour into empire-building. In 2000, Compass agreed a "mega-merger" with Granada Group, combining catering with hotels and media into a lumbering entity called Granada Compass. On paper it was a conglomerate; in practice it was a culture clash and a distraction, mashing together businesses that shared no logic beyond a spreadsheet. The market's verdict was quick and unforgiving, and within a single year the strategy was reversed: in 2001 the media assets were split off and Compass re-emerged as a standalone, pure-play catering company. But it came out of the experience bloated, loosely controlled, and hungry for growth — a company that had learned it could get big without yet learning how to stay disciplined. That lesson would arrive the hard way.

III. The UN Scandal and the Brink of Ruin

For a while, the growth-at-all-costs approach looked like genius. Under chief executive Mike Bailey, Compass expanded aggressively across the globe, chasing contracts and revenue with the enthusiasm of a company that had just been set free. But rapid international expansion has a way of outrunning a company's controls, and somewhere in the machine, oversight had gone slack. The bill for that came due in 2005, and it very nearly bankrupted the company's reputation.

The scandal centred on Eurest Support Services (ESS), a Compass subsidiary that supplied food to United Nations peacekeeping operations. Investigators uncovered that ESS had bribed a UN procurement officer, Alexander Yakovlev, to steer and rig bids and win contracts to feed peacekeepers in places like Liberia, Burundi, and East Timor.6 Read that back slowly: a British blue-chip caterer had been paying off a UN official to secure the business of feeding peacekeeping forces in some of the world's most fragile regions. It was the kind of story that does not just cost money; it corrodes the thing a services company sells above all else — trust.

The commercial retaliation was ferocious. Rival caterers, including ES-KO and Supreme Foodservice AG, launched enormous lawsuits, invoking the US Racketeer Influenced and Corrupt Organizations (RICO) Act and seeking damages that ran into the hundreds of millions of pounds.6 The UN suspended Compass as a registered vendor, cutting it off from the very contracts at the heart of the affair. Inside the company, the reckoning reached the top: Mike Bailey was pushed out under intense pressure as the scale of the failure became clear.

In October 2006, Compass drew a line under the civil litigation, agreeing to pay up to £40 million — around $75 million at the time — to settle the claims brought by its rivals.6 The cash cost, painful as it was, was almost beside the point. The deeper damage was to credibility. Here was a company carrying meaningful debt, a broken internal culture, weak central controls, and a boardroom that had just fired its CEO. Analysts were sharpening their pens. For a business whose entire proposition is "trust us to run something you'd rather not run yourself," a corruption scandal is close to an existential threat.

What Compass needed was not another visionary with a growth story. It needed someone to walk into the wreckage, count everything, and impose discipline. It found him in an outsider from the building-materials industry — and what followed became one of the most admired operational turnarounds in the modern history of the London market.

IV. Enter Richard Cousins: The Masterclass in Operational Turnaround

Picture the brief handed to the new man in 2006. A sprawling global business with unstandardised contracts, a bruised reputation, a pile of debt, and a portfolio stuffed with assets — airport concessions, motorway service stations, hotel interests — that had little to do with feeding people at work. Into this walked Richard Cousins, a plain-spoken outsider who had run the building-materials company BPB and who arrived with no romance about catering and no tolerance for complexity.7 Cousins was, by all accounts, the opposite of a showman. He was the accountant with a chainsaw, and Compass needed exactly that.

His diagnosis was unsentimental. Compass did not have a demand problem; it had a discipline problem. It was spread too thin across non-core assets and drowning in contracts that were too complex to manage and too often unprofitable. The strategy that followed was almost boringly clear: get back to pure-play contract foodservice, and get very, very good at the unglamorous mechanics of running it.

The first move was subtraction. Cousins sold off the businesses that were not catering — most notably the travel-catering arm SSP and the motorway-services operator Moto — and used the proceeds to pay down debt and rebuild a balance sheet that could survive its own ambitions. Divestment is a strange kind of courage: it means telling the market you are getting smaller on purpose, and trusting that a tighter, cleaner business will be worth more than a bigger, messier one.

The second move was the one that turned Compass into a machine. Cousins imposed a standardised operating discipline the company came to call MAP — a framework for measuring and optimising the things that actually determine whether an individual catering unit makes money: labour cost as a share of revenue, food waste, purchasing compliance, and contract profitability. Contract catering is a game of pennies played millions of times a day; a percentage point of labour or a few points of food waste is the difference between a good contract and a value-destroying one. MAP gave head office a common language and a common set of levers to pull across tens of thousands of kitchens. Alongside it, Cousins pushed relentless procurement standardisation and built out the group's purchasing operation — the seed of what would become Foodbuy — to convert Compass's sheer volume into hard cost advantage.

The results are the reason his name still gets spoken with reverence in the City. Over Cousins' tenure from 2006 to 2017, Compass lifted its operating margin from a weak level around 5% to a sector-leading level above 7%, and it did so while growing.7 Margin expansion in a low-margin labour business is not glamour; it is grinding, unit-by-unit execution repeated across the globe, and it compounds. Compass became, in the language of fund managers, a "quality compounder" — a stock you could own for a decade and forget about — and it delivered multi-bagger returns to patient shareholders.

The honest analytical note is that this kind of advantage lives in the systems and the culture, not in a patent or a network. It can be built, and in principle it can decay if the discipline lapses. Cousins' achievement was not a one-time fix but a way of running the company. Which is exactly why what happened at the end of 2017 was so devastating — not only as a human tragedy, but as a test of whether the machine could run without the man who built it.

V. Tragic Pivot: The Sudden Transition to Dominic Blakemore

By late 2017, Cousins had earned the rarest thing an executive can earn: the right to leave on his own terms, at the top. After an eleven-year run that had turned a scandal-scarred company into a market darling, he announced his intention to retire and named his successor — chief operating officer Dominic Blakemore, an insider with deep financial and operational grounding — with a planned, orderly handover set for 1 April 2018.7 It was the textbook succession: a legendary CEO, a groomed deputy, and a clean date on the calendar.

Then came the news that stopped the company cold. On 31 December 2017, Richard Cousins was killed in a seaplane crash near Sydney, Australia. He died alongside his fiancée, her daughter, his two sons, and the pilot — an entire family, and a company's leader, gone in an instant on a New Year's Eve.7 The obituaries that followed were unusual for a corporate figure in their genuine warmth; Cousins was remembered not as a personality but as a builder, the man who had made a boring business beautiful.

The succession plan that had been drawn up for a spring handover became, overnight, an emergency. Dominic Blakemore was thrust into the chief executive's chair on 1 January 2018, three months early and under the most harrowing circumstances a new CEO could face — stepping into the shoes of a man who had just died, while the entire organisation was in mourning. Whatever else it was, it was a brutal test of institutional resilience: could the framework hold if the framework's author was suddenly gone?

Blakemore's answer, in effect, was to change as little as possible about what worked. He was an insider precisely because Cousins had wanted continuity, and he publicly committed to protecting the MAP operating discipline that was the company's crown jewel, while beginning the slower work of preparing Compass for a more digital, data-driven era.

It is also worth pausing on how the company ties its leaders' incentives to shareholders, because governance is where turnaround discipline either endures or quietly erodes. Under Compass's remuneration policy, the group chief executive is required to build and hold a shareholding worth five times base salary, and to retain a meaningful portion of shares for two years after leaving — a design meant to make executives think like long-term owners rather than short-term optionholders.2 Long-term incentives are tied to return on capital employed, adjusted free cash flow, and relative total shareholder return, with malus and clawback provisions that allow the company to reduce or recover awards if performance later proves illusory or misconduct emerges.2 None of this guarantees good behaviour, and pay frameworks are easy to dress up in investor-friendly language. But the specific choice to anchor incentives on return on capital and cash — rather than on revenue or headline profit — is at least consistent with the discipline Cousins installed. Blakemore would need every bit of that discipline, because barely two years into his tenure, the entire industry's demand would evaporate in a matter of weeks.

VI. The Ultimate Stress Test: COVID-19 and the Capital Raise

For a company whose product is feeding people where they gather, a pandemic that forbids gathering is not a headwind. It is an extinction-level event. In March 2020, the world simultaneously did the one thing Compass's business model could not survive: it stopped gathering. Offices emptied as workers were sent home. Schools and universities shut. Stadiums went dark. In a matter of weeks, a staggering share of Compass's revenue — on the order of half the business — simply disappeared, not because anyone was unhappy with the service, but because the buildings the service fed were locked.2

The financial mechanics of that shock are worth understanding, because they explain the company's response. Catering is a business of high fixed costs relative to its thin margins: kitchens, equipment, and above all labour. When volume collapses but the cost base does not move as fast, margins do not just fall — they can go negative, and cash starts draining out of the business daily. This is the terror of operational leverage working in reverse. A 7% margin business does not have a thick cushion to absorb a 50% revenue hole.

Blakemore's response was fast and, in hindsight, decisive on two fronts. The first was operational triage: furloughing hundreds of thousands of employees where government schemes allowed, mothballing idle units, and renegotiating thousands of contracts to share the pain with clients. The second was the move that separated Compass from weaker rivals. In May 2020, at the depth of the uncertainty, the company raised £2 billion — around $2.5 billion — in fresh equity.2

Raising equity in a crisis is a double-edged decision, and it deserves to be examined rather than applauded reflexively. It was highly dilutive: existing shareholders saw their ownership shrink, and issuing stock near a low is the most expensive form of capital there is. But the alternative calculus was starker. The raise gave Compass a large cash cushion, kept net debt under control, and eliminated any question of refinancing or liquidation risk at a moment when nobody knew how long the shutdown would last. It bought certainty when certainty was the scarcest asset in the market.

The strategic payoff was competitive, not just defensive. With a fortress balance sheet, Compass could keep its supply chain intact, retain the operational capacity to reopen at speed, and stay on the front foot while thinly capitalised, highly leveraged regional competitors were forced into retreat or insolvency. In a fragmented industry, a downturn that kills the weak leaves the survivor with a bigger field to play on when demand returns. The dilution was the price of admission to the recovery — and the recovery, when it came, turned out to carry a structural tailwind almost nobody had priced in.

VII. The Post-Pandemic Metamorphosis: "First-Time Outsourcing" & Regional Reshuffling

When the world reopened, it did not simply return to normal — it returned to a version of normal that was unexpectedly good for Compass. Corporate clients, school districts, and hospital systems came back to a brutal environment: double-digit food inflation, acute labour shortages, and a sudden appreciation of just how hard, expensive, and distracting it is to run a professional kitchen. For an organisation whose core mission is educating students or treating patients, running an in-house canteen through that storm went from a manageable chore to an operational headache nobody wanted.

This is the origin of the tailwind management now talks about constantly: "first-time outsourcing." Historically, roughly half of the global foodservice market has been "self-operated" — run in-house by the school, hospital, or company itself rather than handed to a specialist.2 That self-operated half is the real prize, far larger than the share Compass takes from other caterers. Post-pandemic, a meaningful slice of it began outsourcing for the first time, and Compass, with its scale, its balance sheet, and its purchasing power, was positioned to win an outsized share of those new contracts. On its FY2025 results, the company reported net new business growth of 4.5% — its fourth consecutive year within its 4–5% target range — and client retention above 96%, with new wins securing $3.8 billion of annualised revenue, up 11% at constant currency.1 Those two numbers together — winning new business while keeping almost all the old — are the statistical signature of genuine share gain rather than mere churn.

Alongside chasing this demand, Compass also cleaned up its own footprint, exiting sub-scale, low-margin geographies rather than clinging to flags on a map for their own sake. The structural expression of that focus came on 1 October 2024, when Compass merged its former "Europe" and "Rest of World" reporting segments into a single consolidated "International" segment, leaving the group with a clean two-pillar structure.2

Those two pillars tell you where the value really sits. North America is the engine: in FY2025 it generated roughly $31.4 billion of revenue, around two-thirds of the group, and an operating margin of about 8.2% — the highest-quality, best-run part of the business and the source of the great majority of group profit.1 International is the stabiliser: around $14.7 billion of revenue at a thinner operating margin near 6.1%, a large and improving business but structurally less profitable than the American operation.1 Stitch them together and you get the group's $46.1 billion of underlying revenue, $3.34 billion of operating profit, and a 7.2% underlying margin.1

The analytical takeaway is two-edged. The bull reading is that Compass is winning the exact contracts a structural shift is creating, at high retention, with its most profitable region leading. The bear reading is that this is a company whose fortunes are now overwhelmingly American: when three-quarters of your profit comes from one continent, you are, in effect, a US business with a London listing and an international side-portfolio. Both readings are true at once, and holding them together is the key to understanding the stock. Underpinning both is a piece of machinery most investors never see — the purchasing operation that quietly turns Compass's size into cash.

VIII. The Procurement Powerhouse: Foodbuy

Here is the part of the Compass story that never makes the annual-report cover and yet may be the single most important source of its durability. Every restaurant owner, hospital administrator, and school-district manager who has ever bought food at scale knows the fundamental truth of the business: the person who buys the most, at the best price, wins. Foodbuy is Compass's answer to that truth, and it operates almost entirely out of view.

Foodbuy is not merely Compass's internal purchasing department. It is a distributor-neutral group purchasing organisation, or GPO — a middleman that aggregates the food-buying volume of many organisations to extract better terms from suppliers than any of them could get alone.5 Think of it as a buyers' club with the negotiating leverage of a small nation. It manages an enormous annual purchasing spend — Compass's own food buying combined with billions more in third-party volume from hospitality groups, healthcare operators, and independent restaurants who join precisely to access the pricing that only scale unlocks.5 The aggregate figure runs into the tens of billions of dollars a year, a number so large that suppliers cannot afford to be shut out of it.

The economics work through rebates. Foodbuy negotiates volume rebates with suppliers based on the aggregated purchasing power of its members, passes a portion of those savings back to third-party members, and retains administrative fees and a share of the rebates for itself.5 It is a capital-light toll on a river of food spend: Foodbuy does not have to own trucks or warehouses to profit from the flow. The bigger the flow, the better the terms, the more attractive membership becomes, the bigger the flow — a self-reinforcing loop that is genuinely hard for a smaller player to break into.

Where this becomes strategically vicious is in acquisitions. When Compass buys a mid-sized competitor, one of the first things it does is migrate the target's food procurement onto Foodbuy. Because Foodbuy has already negotiated deeper discounts than the acquired business could ever secure on its own, that migration instantly lifts the target's procurement economics — a margin uplift the acquirer captures more or less on day one, before any of the harder operational integration work is done. It means Compass can pay a fair price for a business and still create value simply by plugging it into the buying machine.

This is the closest thing Compass has to a true structural moat, and it maps cleanly onto what strategist Hamilton Helmer calls "scale economies" power: a benefit that grows with size and that a smaller competitor, by definition, cannot match. A regional caterer or an independent restaurant cannot replicate tens of billions of dollars of aggregated buying volume, so it cannot access the same input costs, so it is permanently disadvantaged on the largest single line of a food business's P&L. The skeptic's caveat is worth stating: rebate-based GPO economics depend on suppliers continuing to tolerate the model, and on Compass passing through enough savings to keep third-party members loyal rather than defecting to a rival club. But as competitive advantages in a low-margin industry go, a permanent cost-position edge is close to the best kind you can own. And it is the engine that makes the company's acquisition strategy work.

IX. The Capital Allocation Engine: Infill M&A & The Share Trading Pivot

If Foodbuy is the moat, capital allocation is the tool that decides whether the moat gets wider or the money gets wasted. Compass has, at least in the post-Cousins era, articulated a disciplined framework, and it is worth laying out because discipline stated is not the same as discipline practised — the test is behaviour over time.

The stated hierarchy runs roughly as follows. First, reinvest in the business at high returns, with capital expenditure running around 3.5% of revenue — a deliberately capital-light model, since Compass typically operates client kitchens rather than building its own real estate. Second, pay an ordinary dividend targeted at around a 50% payout of earnings. Third, pursue acquisitions, but only where the target is expected to earn a return on capital above the company's cost of capital by the end of the second year — a specific, falsifiable hurdle rather than a vague promise to "be disciplined." Fourth, return genuinely excess cash to shareholders through buybacks, which the company restarted after the pandemic and has used to return billions.2 The presence of a two-year ROCE hurdle is the kind of detail that separates a real framework from a slogan; whether every deal actually clears it is the thing an investor should keep checking.

The clearest recent illustration of the M&A playbook is the acquisition of CH&CO, the premium UK and Ireland caterer, agreed in January 2024 for an initial enterprise value of £475 million — around $600 million — plus a two-year earn-out contingent on the acquired business's profit growth.4 CH&CO was not a random purchase. It brought a stable of premium hospitality brands — Gather & Gather, Vacherin, Company of Cooks — roughly £450 million of annual revenue, 10,000 employees, and more than 900 clients across 1,000 locations.4 The strategic logic Compass described was "sub-sectorisation": adding distinct premium brands that let it serve more discerning, higher-value client segments, and then layering those brands onto its existing purchasing and overhead infrastructure to extract synergy.

Read through the Foodbuy lens, the CH&CO deal is the infill playbook in miniature: buy a well-run business with attractive brands at a sensible multiple, migrate its procurement onto the buying machine, fold its back office into an existing overhead base, and let the synergies do the work of making a fair price look cheap. The structure of the deal — a fixed price plus an earn-out tied to profit growth — also shifts execution risk onto the sellers, who only collect the extra consideration if the business actually delivers. That is disciplined deal design, though it is worth noting the earn-out also signals that Compass was not willing to pay the full headline price up front on trust alone.

Which brings us back to the currency revolution that opened this story, because it is fundamentally a capital-markets decision. Having already moved its reporting currency to dollars in 2023, Compass took the far rarer step of shifting the trading currency of its LSE-listed shares from pence to dollars on 1 April 2026, with the London Stock Exchange restating historic share-price data at the 31 March conversion rate.39 The mechanics are almost mundane — the shares' nominal value stays in pence, dividends still default to sterling, FTSE membership and voting rights are untouched.3 The message is not mundane at all. It is an explicit acknowledgment that Compass is, in economic reality, an American earnings compounder that happens to be listed in London, and that pricing its equity in pounds was adding FX noise for no reason while making the stock marginally more awkward for the US institutions that dominate its natural investor base. It is a rational move. It is also, unmistakably, a company quietly admitting where its centre of gravity has moved.

X. Playbook: Durable Business & Investing Lessons

Step back from the chronology and Compass becomes a compact set of investing lessons, each earned the hard way rather than theorised.

The first is the value of pure-play focus over conglomerate bloat, a lesson Compass learned twice. The Granada Compass merger and the pre-2006 sprawl of concessions and motorway services both taught the same thing: a services company that wanders away from its core does not become a diversified powerhouse, it becomes a distracted one. The market rewarded Compass not when it got bigger and broader, but when it got narrower and better. Diworsification is a real cost, and the cleanest chapters of Compass's history are the focused ones.

The second lesson is the moat of shared scale — the GPO model. Foodbuy demonstrates something genuinely counterintuitive: you can build an unassailable procurement advantage by aggregating buying power even from businesses you do not own and, in some cases, would happily compete against. In an industry where input costs are the largest controllable line and inflation is a recurring threat, a permanent cost-position edge functions as armour. The lesson for investors is to look past a company's visible product to the invisible infrastructure that determines its cost base.

The third lesson is unit-level discipline, embodied by the MAP framework. Contract catering is not won with a brilliant strategy conceived once; it is won with a disciplined system applied millions of times, measuring labour, waste, and compliance kitchen by kitchen. This is "process power" in Helmer's language — an advantage embedded in how the organisation operates day to day, hard for a rival to copy because it is cultural as much as technical. The uncomfortable flip side is that process advantages are not permanent; they must be maintained, and a few years of lax execution could erode what took a decade to build.

The fourth lesson is capital allocation discipline, visible in the numbers: the group reported return on capital employed of 18.2% in FY2025.1 A near-18% return on capital in a business often dismissed as "just catering" is the real evidence that something better than a commodity is at work here. It is achieved not by grand, transformational deals but by avoiding overpayment, buying synergistic infill targets, and feeding them into Foodbuy. High returns on capital, sustained, are the closest thing in investing to proof of a moat — and the number to watch is whether that figure holds as the company grows.

Those lessons set up the harder question: how durable is any of this really, when you stress it against the classic frameworks and the competition?

XI. Analysis: Porter's Five Forces & Hamilton Helmer's Seven Powers

War-game the industry structure and Compass looks sturdier than its thin margins suggest — though not invulnerable. Start with Michael Porter's five forces.

The bargaining power of buyers is low to moderate. An individual corporate, hospital, or university client has some leverage at contract-renewal time, and large clients can and do run competitive tenders. But switching caterers is genuinely disruptive — it means new staff, new systems, and the risk of unhappy diners — and the large operators can offer cost savings, chiefly through purchasing scale, that a client simply cannot achieve on its own. That combination of switching friction and cost advantage limits how hard most buyers can push.

The bargaining power of suppliers is very low, and this is the heart of the story. Because of Foodbuy's tens of billions in aggregated purchasing volume, food suppliers have little pricing power against Compass; the volume on offer is too large to walk away from, so suppliers largely accept the rebate terms as the price of access to the distribution.5 This is the mirror image of the buyer analysis — Compass sits in the powerful middle of the value chain, squeezing suppliers while offering buyers savings they cannot self-generate.

The threat of substitutes is moderate. The substitute is not a different caterer; it is the client deciding to self-operate its own kitchen. That option always exists, and in a world of cheap labour and low food inflation it can look attractive. But the post-pandemic reality of wage pressure and operational complexity has made self-operating markedly less appealing — which is precisely the mechanism behind the first-time-outsourcing tailwind. The threat is real but currently pointed in Compass's favour.

The threat of new entrants is low. Entering enterprise contract catering at a competitive cost position requires exactly the scale that takes decades to build; a new entrant cannot match Foodbuy's input costs, and without that it cannot price competitively for large contracts. Competitive rivalry, meanwhile, is low to moderate, concentrated among a top tier of global players — Compass, France's Sodexo, and the US-listed Aramark — who compete rationally at the top while collectively taking share from a long tail of fragmented regional operators.[^9][^14] Sodexo, notably, appointed Thierry Delaporte as chief executive in a governance shake-up that separated its chair and CEO roles, a sign that even Compass's largest peer is still reshaping its own leadership.[^9]

Mapping this onto Hamilton Helmer's seven powers sharpens the picture. Compass's strongest power is scale economies, driven by Foodbuy's procurement volume, as discussed. Its second is switching costs, which are moderate but real: once a caterer has integrated with a client's systems, redesigned its kitchens, and embedded itself in the daily rhythm of a campus or hospital, replacing it is a project nobody undertakes lightly. Its third is process power, the MAP-driven operating discipline that lets Compass run tens of thousands of units at a consistent margin. What Compass conspicuously lacks is any meaningful branding power in the consumer sense — by design, it is invisible — or network economies of the kind that dominate technology platforms. Its advantages are industrial, not viral. That is not a weakness so much as a description: this is a business that wins on cost and execution, not on hype. The question the market has to price is whether cost and execution are enough to justify the premium the stock carries — which is where the bull and bear cases collide.

XII. The Bull & Bear Case

The bull case treats Compass as a compounder in the purest sense — a business that does something unglamorous exceptionally well and can keep doing it for a very long time. The structural core of the argument is the first-time-outsourcing tailwind: with roughly half the global market still self-operated, Compass has a multi-decade runway to convert in-house kitchens to outsourced contracts, and it is currently winning an outsized share of that conversion at high retention.12 Layered on top is Foodbuy's procurement scale acting as inflation armour, a premium North American operation throwing off the bulk of group profit at an 8.2% margin, an 18.2% return on capital, and disciplined buybacks recycling excess cash into fewer shares.1 Put together, the bull says, you have a business whose growth is structurally underwritten and whose economics compound quietly year after year — exactly the profile long-term owners prize.

The bear case does not dispute the quality so much as the fragility beneath it. The first concern is labour intensity. Compass employs more than half a million people, and wages are its single largest cost.2 In a world of rising minimum wages in both the US and UK and periodic labour shortages, margins can be squeezed whenever contract-price adjustments lag cost increases — and in a 7% margin business, that lag hurts fast. Contract structures pass through much of this over time, but "over time" is doing real work in that sentence.

The second bear concern is the changing nature of work itself. A meaningful chunk of Compass's business is corporate — feeding people in offices — and the durable shift to hybrid work means fewer bodies in buildings on any given day, which mechanically reduces meal volumes in the business-and-industry segment. It is not fatal, but it is a structural drag on one of the company's core verticals that did not exist before 2020.

The third, and perhaps sharpest, bear point is concentration. With roughly three-quarters of profit generated in North America, Compass is enormously exposed to a single economy.1 A US recession — with corporate clients cutting headcount, trimming catering budgets, and closing sites — would hit Compass disproportionately, and the recent currency moves, sensible as they are, do nothing to change the underlying earnings concentration; they merely stop pretending it isn't there. Finally, there is valuation: Compass has typically traded at a premium to both Sodexo and Aramark, and a premium multiple is a standing demand for flawless execution.[^9][^14] Any stumble — a margin miss, an integration misfire, a soft patch in North American volumes — is punished harder in a richly valued stock than in a cheap one. The activist-style stress test writes itself: a skeptic would probe whether the premium is truly earned by durable advantage or merely by a long run of good execution that mean-reverts, and whether a business this concentrated and this labour-exposed deserves to be priced for perfection.

The honest synthesis is that both cases are built on the same facts, read with different temperaments. Compass is a genuinely well-run, structurally advantaged business in an unglamorous industry, trading as though the market already knows it. Whether that is opportunity or risk depends entirely on execution from here — which is why the last thing worth doing is naming the handful of numbers that will actually tell you how the story is going.

XIII. Epilogue & Watchlist KPIs

Strip away the drama — the wartime canteens, the UN scandal, the seaplane, the pandemic, the dollar pivot — and what remains is a company that will be judged, quarter after quarter, on a very small number of operating truths. For a long-term investor, three KPIs carry most of the signal.

The first is organic revenue growth, the cleanest read on whether the first-time-outsourcing thesis is real. Compass has guided toward mid-single-digit-plus organic growth, and it delivered 8.7% in FY2025 with net new business of 4.5% and retention above 96%.1 The number to watch is not any single print but the combination: growth that comes from winning genuinely new contracts while keeping the existing book is the fingerprint of share gain; growth that leans on inflationary pricing while retention slips would be a warning that the tailwind is weakening.

The second is the underlying operating margin, currently 7.2%.1 In a business this labour-intensive, margin is the scoreboard for execution — the visible residue of the MAP discipline, Foodbuy synergies, and the mix shift toward higher-value contracts. Steady progression signals that scale and process are still compounding; stagnation or erosion would suggest that wage inflation and hybrid-work headwinds are winning the tug-of-war against efficiency.

The third is return on capital employed, 18.2% in the latest year.1 This is the ultimate test of capital allocation discipline — whether management keeps buying and reinvesting at genuinely high returns or gradually dilutes its own quality chasing growth. A sustained high-teens ROCE is the evidence that the moat is intact and the discipline is holding; a persistent decline would be the first quantitative sign that the machine is losing its edge, long before it showed up in the margin.

Compass Group is, in the end, an extraordinary study in hiding in plain sight: a company almost no diner can name, feeding billions of them a year, run with a level of financial discipline that would flatter far more glamorous industries. It is a low-tech business managed with high-tech rigour, an American earnings engine wearing a London listing, and an invisible empire whose greatest strength — its invisibility — is also the reason so few people appreciate just how formidable it has quietly become. Whether it remains formidable will be written not in headlines but in those three numbers, print after unglamorous print.

References

-

Compass Group FY2025 Preliminary Results Press Release — Compass Group PLC, 2025 ↩↩↩↩↩↩↩↩↩↩↩↩

-

Compass Group Annual Report 2025 — Compass Group PLC, 2025 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Change in trading currency of Compass Group's Ordinary Shares — Compass Group PLC, 2026-04-01 ↩↩↩

-

Compass Group to acquire CH&CO in £475m deal — FoodBev Media, 2024-01-22 ↩↩

-

Foodbuy — Group Purchasing Organization overview — Foodbuy USA ↩↩↩↩

-

Compass settles UN peacekeeper catering lawsuits — Reuters, 2006-10-16 ↩↩↩

-

Richard Cousins obituary and legacy — Financial Times, 2018-01-01 ↩↩↩↩

-

Compass Group PLC listing information — London Stock Exchange ↩

-

Compass Group shifts London share trading from sterling to US dollars — StockTitan, 2026-04-01 ↩↩

-

Compass Group Investor Relations Portal — Compass Group PLC ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube