Cembre S.p.A.: The Electrical Backbone of the Modern World

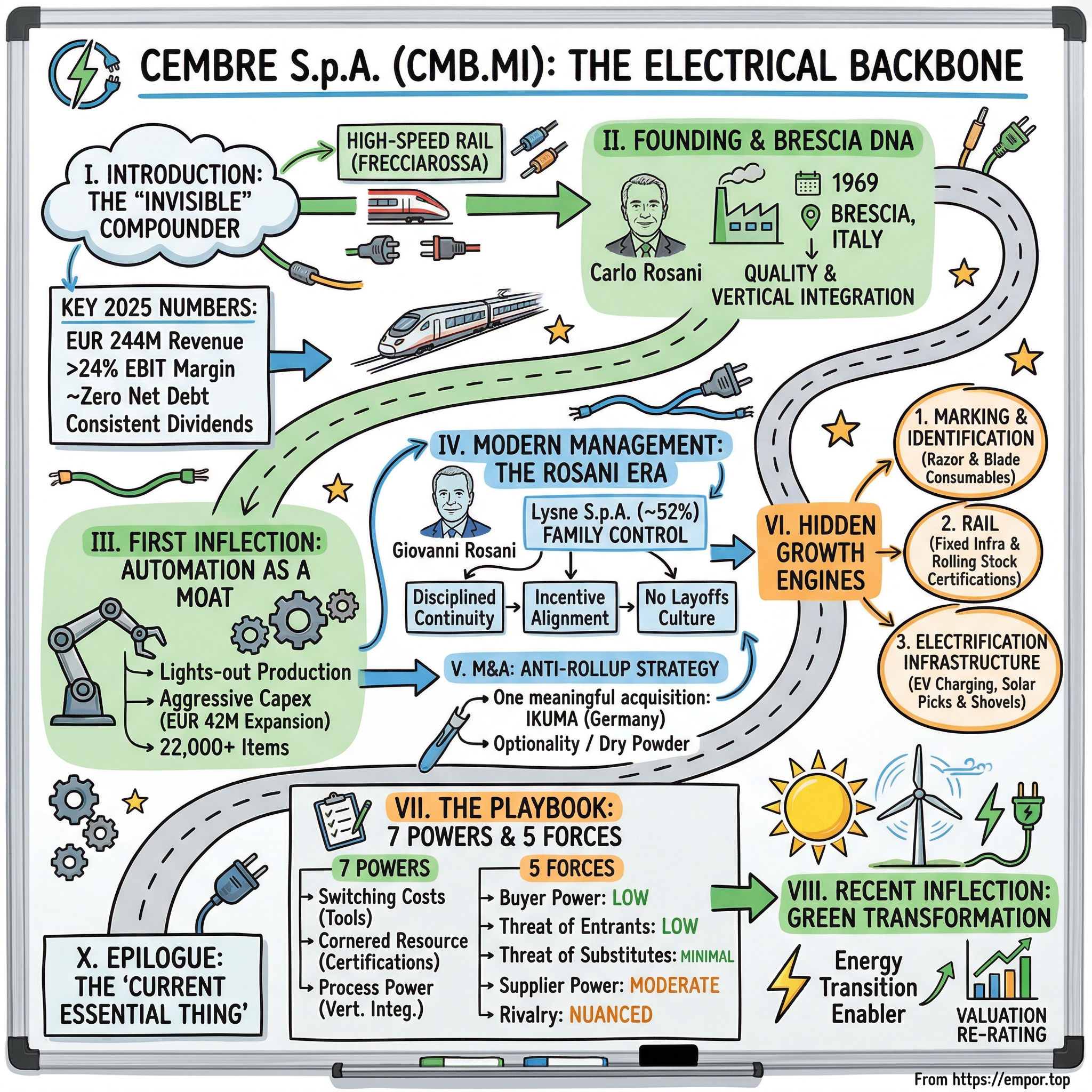

I. Introduction: The "Invisible" Compounder

Picture this: a high-speed Frecciarossa blazing through the Italian countryside at 300 kilometers per hour, carrying hundreds of passengers between Milan and Rome. Beneath the sleek exterior, tens of thousands of electrical connections hold the entire system together — power distribution, signaling, braking, communication. Each one is a small, precision-engineered piece of copper, crimped with a force calibrated to the micron. If even one of those connections loosens, the consequences range from a service disruption to something far worse. Most passengers never think about this. And almost none of them have heard the name Cembre.

Yet Cembre S.p.A. is one of the most efficient manufacturing machines in Italy — and arguably in all of European industrial mid-caps. For the fiscal year 2025, the Brescia-based company reported consolidated revenue of EUR 244 million, an EBIT margin north of 24%, and a balance sheet so clean it would make a Silicon Valley CFO question their life choices: essentially zero net debt, with roughly EUR 20 million in cash sitting against a nearly equivalent debt figure. The company has paid dividends for over twenty consecutive years, raised that payout steadily, and still managed to fund its largest capital investment in history — a EUR 42 million factory expansion — mostly from internal cash flow.

These are not the numbers of a company riding a hype cycle. They are the numbers of a quiet compounder that has been doing the same thing, relentlessly and better, for over half a century. Cembre makes electrical compression connectors — the copper lugs, terminals, and splices that join wires to other wires, wires to machines, and machines to the grid. It also makes the tools to install those connectors, the marking systems to label them, and increasingly, the components that wire the world's renewable energy infrastructure together.

The story of Cembre is the story of how a small workshop in Italy's most industrialized province became a global leader in a category so mundane that most investors have never even considered it. It is a story about the power of vertical integration, the discipline of family ownership, and the quiet tailwind of electrification — from high-speed rail to electric vehicle charging to the massive grid modernization programs now reshaping Europe's energy landscape.

This is a company that has compounded shareholder value not through flashy acquisitions or financial engineering, but through the oldest playbook in capitalism: make something essential, make it better than anyone else, and never stop investing in the factory.

II. Founding and the Brescia DNA

To understand Cembre, you have to understand Brescia. Nestled in Lombardy between Milan and Verona, Brescia has been an industrial city since the Renaissance, when its metalworkers forged armor and weapons that armed half of Europe. By the twentieth century, that tradition had evolved into a dense ecosystem of small and medium manufacturers — steelmakers, toolmakers, mechanical engineers — clustered together in what Italians call a "distretto industriale." If Germany has the Mittelstand, Italy has the Brescia model: family-owned, technically obsessed, export-oriented, and deeply suspicious of debt.

Carlo Rosani was a product of this world. Born in Brescia on November 2, 1926, he studied electronic engineering at the Politecnico di Milano, graduating in 1951 — a moment when post-war Italy was beginning its "Miracolo Economico," the great economic boom that would transform the country from an agrarian society into one of the world's largest industrial economies. After graduation, Rosani spent years in Switzerland and Italy commercializing electrical systems, absorbing the disciplines of both Swiss precision and Italian ingenuity. By his early forties, he had identified the opportunity that would define his life's work.

In March 1969, Rosani founded Costruzioni Elettro-Meccaniche Bresciane — Cembre for short — with a simple thesis: as the world electrified, the humble connection point would become the single most critical element of safety and reliability in any electrical system. A wire can be oversized. A breaker can be replaced. But a bad crimp, a loose lug, or a corroded terminal can cause fires, equipment failure, and loss of life. Rosani's insight was that this market would reward quality above all else — not the lowest price, but the connector that never, ever failed.

The early products were copper compression connectors, manufactured to exacting tolerances using in-house tooling. From the beginning, Rosani insisted on controlling the entire production process — from designing and building the dies and molds, to stamping and forming the copper, to the final chemical tin-plating that protected the connectors from corrosion. This wasn't just operational preference; it was a strategic choice. By doing everything in-house, Cembre could guarantee quality at every step and iterate rapidly. If a customer in the utility sector needed a custom connector for a specific cable gauge, Cembre could design, prototype, and produce it without waiting on outside suppliers.

By 1977, the company had outgrown its original premises and moved to a new site on Via Serenissima in Brescia — the same location that remains its global headquarters today, now sprawling across 121,000 square meters of grounds with 50,000 square meters of buildings. Carlo Rosani ran Cembre with a paternalistic intensity characteristic of the best Brescia industrialists. He never resorted to layoffs or wage reduction schemes — the Italian "cassa integrazione" that many manufacturers relied on during downturns — even during the brutal recessions of the 1970s and 2000s. This built a workforce culture of loyalty and deep technical expertise that persists to this day.

The 1986 founding of Cembre Ltd near Birmingham marked the company's first international move and its only manufacturing operation outside Italy. The UK subsidiary was strategically placed to serve the British rail network, a market that would become one of Cembre's most important growth engines. Over the following decade, Cembre established trading subsidiaries in Spain (1994), France (1998), and the United States (1999), building a distribution network that could get products to customers across Europe and North America quickly and reliably.

The December 1997 IPO on the Milan Stock Exchange gave the company access to public capital while allowing the Rosani family to maintain overwhelming control. It was a classic Italian listing: enough float to provide liquidity and a public market valuation, but not so much that the family risked losing the ability to think in decades rather than quarters. That tension between public accountability and private patience would define Cembre's capital allocation philosophy for the next three decades.

III. The First Major Inflection: Automation as a Moat

In the early 2000s, a tectonic shift swept through European manufacturing. The combination of EU enlargement — bringing low-cost labor markets in Poland, Czech Republic, and Hungary into the single market — and China's entry into the WTO created an irresistible gravitational pull for production capacity. One by one, European manufacturers of commodity industrial products moved their factories east, chasing labor costs that were a fraction of Western European levels. The logic seemed unassailable: why pay a Brescia factory worker EUR 25 an hour when a Polish or Chinese worker could do the same job for EUR 5?

Cembre looked at this calculus and made the opposite bet. Rather than chasing cheap labor, the company invested aggressively in automating its Brescia plant, pushing toward what manufacturers call "lights-out" production — lines that run with minimal human intervention, often overnight and on weekends, guided by robotic arms and computer-controlled quality systems. The reasoning was subtle but profound. A connector that fails in a power substation or a railway junction box doesn't just cost a few cents to replace; it can cause millions of euros in damage and endanger lives. Customers in these markets — utilities, rail operators, industrial OEMs — were not primarily price-sensitive. They were risk-averse. They wanted connectors that were certified, traceable, and produced in a controlled environment with zero defects.

By automating rather than offshoring, Cembre achieved something remarkable: it kept production close to its engineering team, maintaining the feedback loop between R&D and manufacturing that drives continuous improvement. When an engineer noticed a subtle variation in crimp quality on a particular connector line, the fix could be implemented in days, not months. When a customer requested a modification, the turnaround was measured in weeks, not quarters. This responsiveness — paired with a product catalog that eventually grew to over 22,000 items — created a service level that competitors, scattered across multiple countries and time zones, struggled to match.

The "super-factory" model also insulated Cembre from the supply chain disruptions that would later become front-page news. During the 2020 COVID-19 pandemic, companies that had outsourced production to Asia found themselves waiting months for containers that never arrived or factories that remained shuttered. Cembre, with its vertically integrated Brescia operation, continued to ship. During the semiconductor shortage of 2021-2022, which disrupted everything from automotive to industrial automation, Cembre's relatively simple product mix — copper, steel, engineered plastics — meant it was less exposed than competitors with more complex supply chains. The company's revenue surged from EUR 137.6 million in the pandemic-hit 2020 to EUR 199 million by 2022, a 45% increase in just two years.

This isn't to say automation was cheap. Capital expenditure at Cembre has consistently run at levels that would make a "capital-light" investor wince, averaging around EUR 15-20 million annually through the 2010s and rising sharply as the company embarked on its EUR 42 million expansion project in 2023. But the returns speak for themselves: EBIT margins expanded from the high teens to the mid-twenties between 2020 and 2025, even as raw material costs — particularly copper — swung wildly. The factory wasn't just a production facility; it was a competitive weapon.

For investors, the lesson is this: in a market where quality and reliability are non-negotiable, the manufacturer who invests most aggressively in process technology wins — not just on margin, but on customer retention, on service levels, and ultimately on market share. Cembre's Brescia factory is not an overhead burden; it is the company's moat.

IV. Modern Management: The Rosani Era

Carlo Rosani passed away in March 2010 at the age of 83, leaving behind a company with roughly 545 employees across eight entities in seven countries. The succession was smooth — a rarity in Italian family businesses, where founder transitions often trigger years of boardroom warfare. Giovanni Rosani, Carlo's son, stepped into the role of Chairman and Managing Director, the position he holds to this day.

Giovanni had been steeped in the business since his youth, absorbing his father's philosophy of quality-first manufacturing and conservative financial management. Where some second-generation leaders feel the need to prove themselves through dramatic strategic pivots, Giovanni's approach has been characterized by disciplined continuity: the same focus on vertical integration, the same reinvestment in the Brescia factory, the same patient geographic expansion — but with a modern sensibility about energy transition markets and digital manufacturing.

The family's control of Cembre is exercised primarily through Lysne S.p.A., the holding company associated with Anna Maria Onofri — Carlo's widow — which owns approximately 52% of the company's outstanding shares. Giovanni personally holds roughly another 8%, and his sister Sara Rosani sits on the board. Combined, the family controls well over 60% of the equity, ensuring that no activist investor, hostile bidder, or quarterly earnings obsession can divert the company from its long-term trajectory.

This level of family ownership is sometimes viewed skeptically by international investors, who worry about minority shareholder rights, related-party transactions, or empire-building at the expense of returns. At Cembre, the evidence points overwhelmingly in the other direction. Return on equity has consistently hovered around 20%. The balance sheet has been kept in a near-net-cash position for most of the past decade. Dividends have been raised steadily — from EUR 0.90 per share for fiscal year 2020 to EUR 2.06 for fiscal year 2025 — with a payout ratio that has settled around 74%, leaving ample room for reinvestment.

The incentive structure is classically aligned: the Rosani family's wealth is overwhelmingly tied to Cembre's share price and dividend stream. There are no stock option schemes diluting outside shareholders, no aggressive M&A deals justified by "synergies" that never materialize. The family earns money when the share price rises and dividends flow — the same way every other shareholder does.

The corporate culture reflects this alignment. Employee turnover is low by Italian manufacturing standards, and the company's refusal to use layoff schemes — a tradition established by Carlo and maintained by Giovanni — creates a workforce that thinks of Cembre as a career, not a job. The technical expertise that accumulates over decades in a stable workforce is difficult to quantify on a balance sheet but shows up unmistakably in the quality of the product and the efficiency of the operation.

One of the most telling decisions Giovanni has made was the EUR 42 million expansion project approved in January 2023. This was the largest single investment in Cembre's history, funding two new industrial buildings totaling 15,000 square meters at the Brescia headquarters. The new facility, which opened in September 2025, was designed to expand production capacity for electrical connectors while incorporating state-of-the-art photovoltaic systems, intelligent energy management, and low-impact building materials. It was partially funded through Italy's PNRR — the National Recovery and Resilience Plan backed by EU funds — a signal that Cembre is adept at navigating Italy's complex public incentive landscape.

The decision to build at a time when many manufacturers were pulling back — 2023 was a year of widespread industrial caution in Europe, with recession fears dominating headlines — speaks volumes about how the Rosani family thinks about time horizons. They were not building for next quarter's revenue; they were building for the next decade's electrification wave.

V. M&A and Capital Deployment: The Anti-Rollup Strategy

In an era when the private equity playbook of "buy, bolt on, lever up, and flip" has become the default M&A strategy in industrial mid-caps, Cembre's approach to acquisitions is almost quaint in its discipline. The company has made exactly one meaningful acquisition in the past decade: the May 2018 purchase of IKUMA GmbH & Co. KG, a German distributor of cable terminals.

IKUMA was a small operation — 18 employees, EUR 8 million in annual revenue — but it gave Cembre something it had been unable to build organically: a meaningful distribution foothold in Germany, Europe's largest and most competitive market for electrical connectors. Phoenix Contact, Weidmuller, and a host of other German manufacturers dominate their home market with the advantages of proximity, language, and decades of customer relationships. For an Italian company, breaking into that market through organic growth alone would have been a Sisyphean task.

Cembre paid EUR 6.3 million in cash at closing, with an additional EUR 2 million in potential earn-out payments tied to performance milestones — a maximum total consideration of EUR 8.3 million. At roughly one times revenue for a profitable distribution business in a strategically critical market, the price was disciplined by any standard. Compare that to the 12-15x EBITDA multiples that private equity firms routinely pay for industrial distribution businesses, and Cembre's approach looks downright austere.

The integration was characteristically methodical. IKUMA continued to operate under its own brand for two years before being formally merged into Cembre GmbH on July 1, 2020. The strategic logic was clear: IKUMA's relationships with German distributors gave Cembre access to a channel it had never been able to penetrate, while Cembre's vastly broader product catalog gave IKUMA's customers access to 22,000 items they had previously been unable to source from a single supplier.

What's more interesting is the deals Cembre hasn't done. The company has maintained a substantial cash balance for years — often EUR 20-40 million in gross cash — that some investors have criticized as "lazy capital." Why not deploy that cash into additional acquisitions, or return it to shareholders through buybacks?

The answer lies in the company's interpretation of optionality. The energy transition is creating entirely new categories of electrical infrastructure — EV charging, grid-scale battery storage, offshore wind connections, solar farm wiring — each of which requires specialized connectors and tooling. Cembre's cash pile is not idle; it is dry powder for capital expenditure and selective acquisitions as these markets mature. The EUR 42 million factory expansion, funded largely from internal resources, is proof that the cash gets deployed when the right opportunity appears.

The geographic expansion strategy has accelerated recently. In 2024, Cembre established two new subsidiaries: Cembre B.V. in Eindhoven, Netherlands, to serve the Benelux market, and Cembre Electrical Connections Shanghai Limited, its first presence in Asia. Neither is a factory — both are trading and distribution entities — but they represent the company's recognition that its addressable market is growing beyond its traditional European base.

The US operation, Cembre Inc. in Edison, New Jersey, has been a slow build since its 1999 founding. The American market for electrical connectors is enormous but fragmented, dominated by players like Panduit, Burndy (now part of Hubbell), and domestic TE Connectivity operations. Cembre's US presence remains modest, but as American infrastructure spending ramps — driven by the Inflation Reduction Act, the Infrastructure Investment and Jobs Act, and a generational grid modernization cycle — the opportunity for a quality-focused European specialist to gain share is meaningful.

For shareholders, Cembre's capital deployment tells a clear story: this is a company that would rather miss an opportunity than overpay for one. In a world of acquisition-fueled "growth" stories that destroy value, that discipline is worth a premium.

VI. The Hidden Growth Engines

Walk into any industrial panel shop in Europe — the workshops where electricians assemble the control panels that run factories, water treatment plants, and power substations — and you will see two things with Cembre's name on them. The first is obvious: connectors. Rows of copper lugs, ring terminals, and ferrules, crimped onto wire ends with Cembre's battery-powered tools. The second is less obvious but equally important: the labels.

Every wire in an electrical panel must be marked. Every terminal, every relay, every circuit breaker needs an identification tag that tells the maintenance engineer — who might be working at 2 a.m. during a plant emergency — which wire goes where. This is the marking and identification business, and it is arguably Cembre's most underappreciated growth engine.

The business model is beautifully simple. Cembre sells thermal transfer printers — specialized machines designed to print on the tiny plastic tags, heat-shrinkable sleeves, and labels used in industrial wiring. The printers are good but not exceptional; what makes them sticky is the consumable ecosystem. The thermal transfer ribbons, the specialized tag formats, the software that integrates with electrical design programs — these are all Cembre proprietary products. Once an electrician or a panel shop has invested in a Cembre printer and trained their team on the workflow, the switching costs are substantial. Not because the competition is bad, but because the entire process — design, print, apply — is integrated.

This is the classic razor-and-blade model, hidden inside what most investors think of as a "copper connector" company. The margins on consumables are significantly higher than on connectors, the revenue is recurring, and the customer relationship deepens with every box of tags ordered. Cembre claims to offer "the widest range of markers, tags, and legends for industrial applications," a breadth advantage that makes it the default choice for distributors who want a single-source solution.

The second growth engine is rail. Cembre's relationship with Europe's railway networks dates back to the 1986 founding of its UK subsidiary, which was established specifically to serve the British rail market. Today, Cembre supplies connectors and maintenance tools across European rail operators, with products certified for both fixed infrastructure (signaling systems, power substations, track-side equipment) and rolling stock (trains, trams, metro cars).

Rail is a superb market for a quality-obsessed manufacturer. Safety certifications take years to earn and are extremely difficult to replace — a competitor cannot simply show up with a cheaper product and win a contract. Procurement cycles are long but predictable, and the installed base creates decades of aftermarket demand for replacement connectors and tools. As European policy shifts decisively toward rail over short-haul aviation — driven by carbon reduction targets and massive public investment programs — the addressable market is expanding structurally.

Cembre has recently developed aluminum-magnesium connectors as alternatives to traditional copper ones for rail applications, a material science innovation that reduces weight and cost while maintaining the conductivity and durability that rail standards demand. This kind of quiet innovation — unglamorous but technically demanding — is characteristic of how Cembre extends its moat.

The third engine is the newest: electrification infrastructure. Cembre's BIAN.CO EASY is an IEC 61851-compliant wallbox for residential and small commercial EV charging. But the real opportunity isn't in the wallbox itself — it's in all the connectors, cable glands, and wiring accessories that go into every charging station, every grid connection point, every solar array junction box. This is the "picks and shovels" thesis applied to the energy transition. Cembre doesn't need to win the race to build the best EV or the most efficient solar panel; it just needs to be the preferred supplier of the thousands of small copper parts that make those systems work.

The launch of dedicated photovoltaic connectors adds another dimension. Every solar installation requires dozens or hundreds of connection points, each of which must withstand decades of outdoor exposure, thermal cycling, and UV degradation. The performance requirements are stringent, and the installed base is growing explosively across Southern Europe, where solar economics are most favorable — which happens to be Cembre's home turf.

VII. The Playbook: 7 Powers and 5 Forces

To understand why Cembre has sustained margins that would be exceptional in any hardware business — and eye-popping for a manufacturer of commodity-seeming copper parts — it helps to look at the business through two analytical lenses: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces.

Start with switching costs, which are the foundation of Cembre's competitive position. An electrician who uses Cembre's battery-powered crimping tools is locked into Cembre's connector ecosystem. The dies in the tool are engineered for specific Cembre connector geometries. The crimp profile — the precise deformation of the copper barrel around the wire — is calibrated to Cembre's specifications. Using a competitor's connector in a Cembre tool risks an improper crimp, which in safety-critical applications like power distribution or rail signaling could mean a fire, an arc flash, or a system failure. No electrician, no panel shop, no utility procurement manager is going to take that risk to save a few cents per connector. The tool-and-connector system is a closed loop, and once a customer is inside that loop, they stay.

The second power is what Helmer calls a "cornered resource," and in Cembre's case, it manifests as certifications. In the utility and rail sectors, every product that touches the electrical system must be tested, approved, and certified by national and international standards bodies. These certifications are not just paperwork — they involve years of testing, field trials, and documentation. A new entrant cannot simply design a connector and sell it to a European rail operator; they must first spend years and millions of euros navigating a certification gauntlet that the incumbents cleared decades ago. This creates a barrier to entry that is structural, not cyclical.

Process power is Cembre's third source of advantage. The company's vertically integrated manufacturing — from die design through stamping, forming, plating, and assembly — has been refined over five decades of continuous operation. The accumulated knowledge embedded in those production lines — the specific alloy compositions, the plating chemistries, the machine settings that produce zero-defect parts at high speed — is not documented in any textbook. It lives in the institutional memory of the organization and the software that controls the automated lines. A competitor can buy the same stamping presses, but they cannot buy the decades of optimization that make Cembre's lines run at their level of efficiency.

Now apply Porter's Five Forces. Start with the bargaining power of buyers, which in Cembre's markets is remarkably low. A copper connector represents a tiny fraction of a total project's cost — perhaps 0.1% of the bill of materials for a power substation or an industrial control panel. But that connector represents 100% of the safety risk at that junction point. Buyers are not price-sensitive in the traditional sense; they are risk-averse. A procurement manager at a utility company is not going to switch from a proven, certified Cembre connector to a marginally cheaper alternative and risk being the person who signed off on the part that caused a grid failure. This asymmetry between cost share and risk share is the fundamental driver of Cembre's pricing power.

The threat of new entrants is constrained by the same certification barriers discussed above, plus the capital intensity of building a vertically integrated manufacturing operation. A new entrant would need to invest tens of millions in factory equipment, spend years qualifying products, and build a distribution network across multiple countries — all to compete in a market where the incumbents have scale advantages and entrenched customer relationships.

The threat of substitutes is minimal. Electrical connections are governed by physics: wires must be joined to other wires and to equipment, and the most reliable way to do this for permanent, high-current connections remains the compression connector. There is no wireless alternative. There is no software solution. As long as the world uses copper wire to transmit electricity — which will be the case for the foreseeable future — there will be demand for compression connectors.

Supplier power is moderate. Copper is Cembre's primary raw material, and copper prices are set by global commodity markets. Cembre cannot control the price of its input. However, the company has demonstrated a consistent ability to pass copper price increases through to customers — a function of the pricing power described above. When copper prices surged during 2021-2022, Cembre's margins actually expanded, suggesting that the company used the commodity cycle as cover to implement price increases that stuck even after copper retreated.

Rivalry among existing competitors is the most nuanced force. The market is fragmented at the low end — there are hundreds of manufacturers of basic copper connectors worldwide — but concentrated at the high end, where certifications, quality, and breadth of product range matter. Cembre's most relevant competitors are Phoenix Contact, TE Connectivity, and Weidmuller in Europe, along with specialized players in the rail and utility segments. Phoenix Contact and Weidmuller are privately held German companies with deep resources; TE Connectivity is a global giant with over $16 billion in revenue. But none of these competitors is precisely comparable to Cembre. TE is vastly larger and more diversified. Phoenix Contact is focused more on terminal blocks and automation than on compression connectors. Cembre occupies a specific niche — high-quality compression connectors and tools, plus marking systems and rail products — that is large enough to support a EUR 250 million business but specialized enough to discourage head-on competition from the giants.

Two KPIs cut through the complexity for investors tracking Cembre: EBIT margin and organic revenue growth. The EBIT margin reveals whether the company's pricing power and manufacturing efficiency are being maintained or eroded; any sustained decline below 22% would signal competitive pressure or cost absorption problems. Organic revenue growth — excluding currency and acquisitions — shows whether the electrification tailwind is actually translating into market share gains or whether Cembre is merely riding a commodity cycle.

VIII. Recent Inflection: The Green Transformation

Something shifted in Cembre's narrative between 2020 and 2025 — not in what the company does, but in how the world perceives what it does. For decades, Cembre was classified in the minds of investors as an "industrial supplier," a label that consigned it to the low-multiple ghetto alongside valve manufacturers and gasket makers. Then came the European Green Deal, the REPowerEU plan, the explosive growth of solar and wind installations, and the continent-wide push to modernize electrical grids built for an era of centralized fossil fuel generation.

Suddenly, every wind turbine that goes up needs hundreds of high-quality electrical connections. Every solar farm, every battery storage system, every EV charging station, every upgraded substation — all of them require the same unglamorous copper parts that Cembre has been perfecting for half a century. The company didn't change; the world changed around it. Cembre went from being an "industrial supplier" to being an "Energy Transition Enabler," and the valuation re-rating has been dramatic. The stock's trailing price-to-earnings ratio, which spent most of the 2010s in the low teens, has expanded to roughly 27 times earnings as of early April 2026.

The operational story of 2020-2025 is equally compelling. Revenue grew from EUR 137.6 million in the COVID-affected 2020 to EUR 244.3 million in 2025, a compound annual growth rate of approximately 12%. EBIT margins expanded from 18.2% to 24.5% over the same period. The company achieved this while navigating one of the most volatile commodity environments in modern industrial history — copper prices surged from around $5,500 per metric ton in early 2020 to over $10,000 by 2022, before oscillating wildly through 2023 and 2024.

Cembre's ability to manage this volatility without sacrificing margins is a masterclass in pricing discipline. Unlike consumer goods companies, which face immediate backlash when they raise prices, Cembre's customers are commercial and industrial buyers for whom the connector is a trivially small cost relative to the overall project. When Cembre raised prices to offset copper costs, there was no social media outrage, no boycott, no Congressional hearing. There was simply a line-item adjustment on a purchase order that no one scrutinized because the total was still rounding error in the project budget.

The geographic mix of growth has been notable. While Europe — particularly Italy, the UK, Germany, and France — remains the core market, accounting for approximately 88% of revenue, extra-European sales surged by nearly 22% in fiscal 2025. The establishment of new subsidiaries in the Netherlands and China during 2024 signals management's recognition that the electrification wave is global, not just European, and that Cembre's traditional geographic concentration is both a strength (deep customer relationships) and a limitation (market ceiling).

The company also achieved 100% certified renewable energy supply at its Brescia plants — a detail that matters more than it might seem. European industrial customers, particularly in the utility and rail sectors, are increasingly requiring suppliers to demonstrate their own environmental credentials. A connector manufactured using renewable energy, in a factory with low-impact materials and intelligent energy management, is a stronger procurement story than one stamped out in a coal-powered plant overseas. Cembre is effectively turning its sustainability investments into a competitive advantage, layering an ESG moat on top of its existing quality and certification moats.

For fiscal 2026, CEO Giovanni Rosani has guided for "growing consolidated sales volume while maintaining positive economic results" — characteristically understated language from a management team that has consistently under-promised and over-delivered.

IX. The Bear vs. Bull Case

Every investment thesis has two sides, and Cembre — despite its exceptional track record — is no exception. The bear case begins with copper. It is the essential raw material, and Cembre cannot control its price. While the company has demonstrated pricing power through multiple commodity cycles, a sustained spike in copper — driven by, say, a supply disruption in Chile or a speculative surge in futures markets — could temporarily compress margins if customers resist yet another round of price increases. The company does not publicly disclose a hedging strategy, which means this risk is opaque to outside investors.

Succession is a legitimate concern. Giovanni Rosani has led the company capably since 2010, but there is no publicly articulated succession plan. Sara Rosani sits on the board, and the family's control through Lysne ensures continuity of ownership, but the question of who runs the company after Giovanni — and whether that person will maintain the same operational discipline — is unanswered. Italian family businesses have a mixed track record on generational transitions. Some, like the Ferrero family at the eponymous chocolate company, navigate them brilliantly. Others falter. Cembre's track record suggests the former, but it remains a question mark rather than a certainty.

The liquidity trap is structural and likely permanent. With roughly 71% of shares held by the family and related parties, the public free float is only about 29% — approximately 4.8 million shares, trading an average of 5,000-10,000 per day. This makes the stock essentially uninvestable for large institutional funds, which need to build positions of millions of shares without moving the market. The illiquidity works both ways — it discourages selling pressure during downturns (the family doesn't sell), but it also limits the upside from institutional buying during uptrends. The stock can be volatile on modest volume, and anyone building a meaningful position must be patient and accept that exiting quickly is not an option.

The current valuation is itself a risk. At roughly 27 times trailing earnings and 16 times EV/EBITDA, Cembre is priced for continued strong execution. If the electrification narrative cools — whether due to a European recession, a slowdown in renewable installations, or a shift in government subsidy priorities — the multiple could contract even if the underlying business continues to perform.

The bull case starts with the moat. Cembre operates in a market with high switching costs, significant certification barriers, and customers who are structurally risk-averse. These are the conditions that sustain above-average margins over decades, not quarters. The fact that EBIT margins have expanded from the high teens to the mid-twenties over a five-year period, while the company was simultaneously absorbing massive copper price volatility and investing in a EUR 42 million factory expansion, suggests that the margin story is structural, not cyclical.

The electrification tailwind is immense and durable. Europe's installed base of electrical infrastructure — grids, substations, industrial plants, railways — was largely built in the decades following World War II and is now reaching the end of its useful life, requiring wholesale replacement and upgrade. Simultaneously, the energy transition is adding entirely new categories of infrastructure: wind farms, solar arrays, EV charging networks, battery storage systems. Each of these requires electrical connectors. The total addressable market for Cembre's products is not shrinking; it is expanding in every direction.

The marking and identification business is the under-appreciated accelerator. This segment combines the stickiness of a consumable model with the growth dynamics of industrial digitization — as factories and infrastructure become more complex, the demand for precise, durable labeling grows. The margins are higher than the core connector business, and the recurring revenue stream provides visibility that hardware sales alone cannot.

The balance sheet provides resilience and optionality. In a world where many industrial companies are leveraged to optimize returns in the good times and then scramble for survival in the downturns, Cembre's near-zero net debt position means it can weather any reasonable macroeconomic scenario without financial distress. It also means the company can act opportunistically if acquisition targets or capital deployment opportunities arise — as it did with IKUMA and with the Brescia expansion.

Private equity activity in the European industrial connectors space has been notable, with several bolt-on acquisitions by PE-backed platforms in recent years. This validates the attractiveness of the market but also raises the question of whether Cembre itself might eventually become a target. At its current market capitalization of approximately EUR 1.2 billion and with the Rosani family's controlling stake, a hostile takeover is impossible. But the family's willingness to consider a premium offer — should one ever materialize — is unknowable.

One second-layer diligence point worth noting: Cembre's listing on the STAR segment of Borsa Italiana requires enhanced corporate governance standards, including independent directors, a minimum free float, and enhanced disclosure. This provides an additional layer of investor protection relative to a standard Italian listing.

X. Epilogue and Conclusion

There is a particular kind of business that never makes headlines, never disrupts anything, never appears on a magazine cover — and quietly compounds wealth for decades. Cembre is that business. It makes the parts that hold the electrical world together: small, precision-engineered pieces of copper that most people will never see, housed inside panels and junction boxes and rail systems and charging stations across Europe and beyond.

The story is deceptively simple. A Brescia engineer founded a company in 1969 to make the best electrical connectors in the world. His son took over and continued to make the best electrical connectors in the world, while also expanding into marking systems, rail products, and electrification infrastructure. The family kept control, avoided debt, reinvested in the factory, and let compound growth do the work.

But simplicity is not the same as ease. Maintaining 24% EBIT margins in a business that buys copper at market prices requires relentless manufacturing efficiency. Growing from EUR 65 million to EUR 244 million over twenty years without a single dilutive acquisition requires extraordinary capital discipline. Building a product catalog of 22,000 items, each certified and tested for safety-critical applications, requires an organizational capability that cannot be assembled overnight or purchased at any price.

The lesson for investors is not that Cembre is the "next big thing." It is not. It is, and has always been, the "current essential thing" — a business that provides a product the modern world literally cannot function without, produced to a standard that competitors struggle to match, managed by owners whose incentives are perfectly aligned with outside shareholders.

The world is not going to need fewer electrical connections in the decades ahead. It is going to need vastly more of them — in every country, in every sector, in every building. The trains will need them. The solar farms will need them. The data centers will need them. The charging stations will need them. And somewhere in Brescia, in a factory that never stops running, Cembre will be making them.

XI. Top Links and References

- Cembre Investor Relations — Annual reports, earnings presentations, and governance documents are available at cembre.com, reflecting one of the most transparent disclosure practices among Italian mid-caps.

- History of the Brescia Industrial District — The Brescia "distretto industriale" model has been extensively studied by Italian economists, notably by Giacomo Becattini and Arnaldo Bagnasco, as a template for family-driven industrial development.

- IKUMA GmbH & Co. KG Acquisition — The May 2018 acquisition was documented in Cembre's press release and in advisory disclosures by Luther Rechtsanwaltsgesellschaft, providing full transaction details.

- Competitive Landscape — For context on Cembre's market positioning relative to Phoenix Contact, TE Connectivity, and Weidmuller, industry reports from ZVEI (the German Electrical and Electronic Manufacturers' Association) and the European Committee for Electrotechnical Standardization (CENELEC) provide useful frameworks.

- Energy Transition Infrastructure Demand — The European Commission's REPowerEU and Green Deal documentation quantifies the scale of electrical infrastructure investment required across the continent through 2030 and beyond.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube