Clas Ohlson: The Story of the Nordic Omnichannel Handyman

I. Introduction: The Hardware Store That Refused to Die

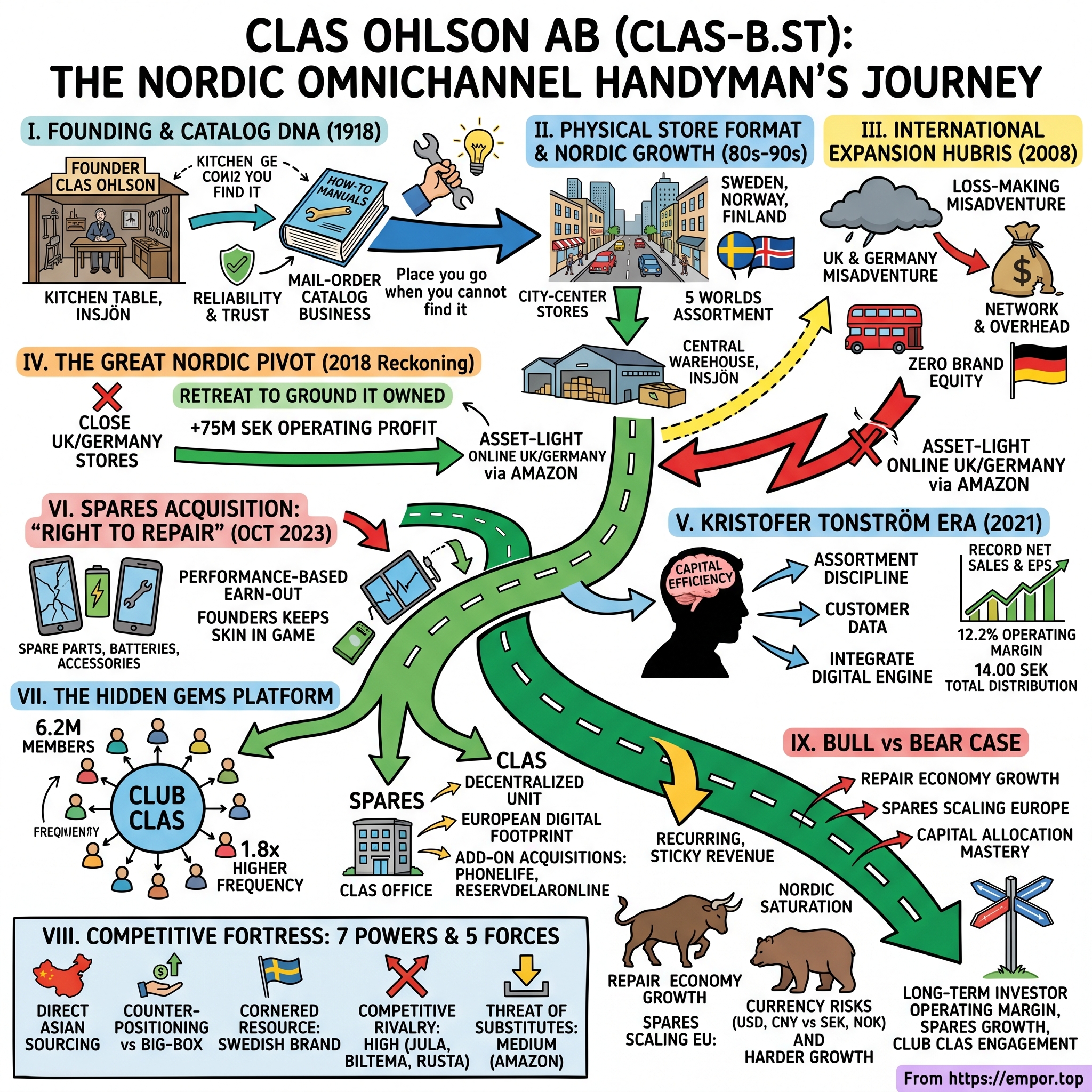

Drive north out of Stockholm for three hours, past the lakes and the birch forests of Dalarna, and you eventually arrive in Insjön — a village of barely a thousand people, the kind of place where the road signs outnumber the traffic. It is not where you would expect to find the headquarters of a company doing more than twelve and a half billion kronor a year in sales. There is no glass tower, no campus. There is a warehouse, a printing legacy, and a town whose identity has been fused with a single surname for more than a century. And yet from this improbable dot on the map, a Swedish retailer has pulled off something that a long parade of regional champions across Europe and North America could not: it has stared down the e-commerce era and come out the other side not merely intact, but stronger than it has ever been.

The numbers tell the story plainly. For the fiscal year ending April 30, 2026, Clas Ohlson AB — listed in Stockholm under the ticker CLAS-B.ST — reported net sales of 12.5 billion SEK, an operating margin of 12.2 percent, and earnings per share of 18.40 SEK, a record on essentially every line.1 The board responded by proposing a total distribution of 14.00 SEK per share — an ordinary dividend of 9.25 SEK topped by an extraordinary dividend of 4.75 SEK — handing back roughly 76 percent of the year's profit to shareholders.1 This is not the financial posture of a company on the defensive. It is the posture of one that has figured something out.

Here is the paradox at the center of this episode. Clas Ohlson spent the first eight decades of its life as a mail-order catalog business — quite literally a company whose flagship product was a thick book of part numbers that landed in Swedish mailboxes once a year. It is exactly the kind of business model that the internet was supposed to vaporize. Catalog retail, physical stores, low-ticket household hardware sold one screwdriver and one plug adapter at a time: every structural feature that made companies like this roadkill in the United States was present here. And yet today the company operates more than 250 physical stores across the Nordics and runs Club Clas, a loyalty program that has swollen to roughly 6.2 million members — an astonishing figure in a home market of only a few tens of millions of people.2

So how did the catalog company become an omnichannel one? The answer is not a single clever pivot. It is three intertwined stories, and they form the spine of this episode.

The first is a story of hubris and its correction — the painful, decade-long cash drain of an international expansion into the United Kingdom and Germany, and the disciplined retreat of 2018 that stopped the bleeding and refocused the company on the ground it actually owned. The second is a story of operational re-engineering under a chief executive, Kristofer Tonström, who arrived in 2021 and rebuilt the business for capital efficiency rather than vanity scale. And the third — the most forward-looking — is a quiet platform play: the October 2023 acquisition of a Nordic spare-parts business called Spares, a bet on the "right to repair" economy that has given an old hardware retailer a genuinely new growth engine.

To understand any of it, you have to start at the kitchen table in Insjön, in 1918.

II. Founding DNA and the Catalog Era

The founder was a young man named Clas Ohlson, and the founding myth is satisfyingly literal: he was a self-taught tinkerer and technical enthusiast who, in 1918, started a mail-order business selling technical and hobby manuals — the kind of "how to wire a radio" and "how to repair a bicycle" instruction booklets that a curious, cash-strapped rural Sweden hungered for.3 This was the tail end of a world in which knowledge itself was a product worth posting. If you lived on a farm in Dalarna and wanted to understand how the new electrical gadgets worked, you could not Google it. You wrote to Insjön.

What turned a pamphlet business into an institution was the realization that the customer who bought the manual also needed the parts. A booklet on radio repair created demand for the specific obscure components the booklet described — the unusual battery, the particular screw, the replacement valve that no general store within fifty kilometers happened to stock. Clas Ohlson became, over the following decades, the place you turned to when you could not find the thing anywhere else. That positioning hardened into a cultural reflex, a phrase Swedes still use: the idea of the company as the universal problem-solver for the everyday handyman. In Swedish households, "ask Clas Ohlson" became shorthand for "someone will have the answer."

The vehicle for that promise was the catalog, and it is hard to overstate what the annual Clas Ohlson catalog meant in twentieth-century Sweden. It was not a marketing flyer; it was a reference work. Thick, dense, organized by a proprietary numbering system that regular customers came to know by heart, it sat in kitchen drawers and workshop benches across the country, dog-eared and annotated. The breadth was the point. A catalog that listed tens of thousands of small, useful, hard-to-source items — and could actually deliver them from one warehouse in Insjön — built a kind of trust that no single product could. The catalog was the brand. The brand was reliability. And reliability, in a category of low-priced functional goods, is worth more than it looks, because nobody wants to drive across town twice for a part that turns out to be wrong.

The leap from catalog to brick-and-mortar came late, and it came carefully. Through the late 1980s and the 1990s, Clas Ohlson took the density of the catalog and translated it into a physical store format, rolling out shops first across Sweden and then into Norway and Finland. The genius of the format was that it inverted the usual hardware-store logic. Rather than the cavernous, out-of-town big-box warehouse that dominated home-improvement retail elsewhere, Clas Ohlson built smaller, densely merchandised stores in city centers and shopping districts — the convenience-store equivalent of a hardware shop. You did not make a special expedition to Clas Ohlson. You popped in on the way home because the lightbulb had blown.

That heritage is not a museum piece; it is the operating system the modern company still runs on. The central warehouse remains in Insjön to this day. The assortment is still anchored in the same five worlds the catalog organized itself around — hardware, electrical, home, multimedia, and leisure — and still skews toward exactly the kind of low-ticket, high-utility items that are genuinely annoying to buy blindly online. You will happily order a book or a phone from Amazon sight unseen. You are far less comfortable ordering a specific plumbing fitting or an obscure fuse without being able to trust that it is the right one. That trust — earned over a century of being the place that has it — is the asset the company has spent the last decade learning to defend. Which is precisely the asset it nearly squandered when it decided, flush with Nordic profits, to conquer the world.

III. The Expansion Hubris: The UK and Germany Misadventure

Success is a dangerous teacher. By the mid-2000s, Clas Ohlson had a problem that looks enviable from the outside and is corrosive from the inside: it was extremely profitable and running out of obvious places to grow. Its Swedish and Norwegian store networks were cash machines, throwing off margins that most retailers can only dream about, in markets where the brand was a household name. The board looked at that cash, looked at a map, and reached the conclusion that almost every dominant regional champion eventually reaches. If the model works this well at home, surely it will travel.

In 2008, Clas Ohlson crossed the North Sea and opened in the United Kingdom, taking expensive, marquee retail space — high-profile locations in places like Croydon and Cardiff — to announce its arrival on the British high street.4 The logic was seductive. Britain had millions of homeowners, a robust DIY culture, and a retail landscape that, to a confident Swede, looked ripe for a better-organized convenience hardware concept. Eight years later, undeterred, the company pushed into Germany as well, opening a cluster of stores anchored in Hamburg as a pilot for continental Europe.

The model broke abroad for reasons that, in hindsight, were visible from the start. The first was brand equity, or rather the total absence of it. In Sweden, "Clas Ohlson" carried a century of accumulated trust; a shopper walking in already knew what the store was for and assumed it would have what they needed. In London or Hamburg, the same sign over the door meant nothing. It was just another unfamiliar shop selling a confusing jumble of cheap household goods, competing for attention against names that locals actually recognized. The single most valuable asset the company owned — that reflexive "ask Clas Ohlson" trust — did not fit in the shipping container. It stayed home.

The second problem was that the company walked into knife fights it had no special advantage in. The UK and German markets were already saturated with hardened competitors: established discounters, enormous big-box home-improvement chains with decades of local scale, and a maturing e-commerce sector led by players who already owned the customer's first click. Clas Ohlson's edge at home came from density and trust built over generations. Abroad, it had neither, and was reduced to competing on the one dimension where it was structurally weakest — being a sub-scale newcomer fighting incumbents on price and convenience simultaneously.

And then there was the overhead. Physical retail is a brutally unforgiving business when the sales do not show up, because the costs show up regardless. Clas Ohlson had signed long-term leases on large, prominent, expensive stores — the kind of commitments that make perfect sense when a location is throwing off Nordic-style margins and become an anchor chained to your ankle when it is not. Every month, rent and staff and fit-out costs landed whether or not enough Londoners wandered in. The marquee locations that were supposed to announce the brand instead quietly converted the company's hard-won Nordic profits into someone else's commercial rent.

The result was a slow bleed that lasted, in the UK, an entire decade. Year after year, the British operation lost money, and the German pilot showed no convincing path to ever turning a profit.4 The losses were never catastrophic enough in any single year to force a crisis — that is what made them so insidious. They were a steady tax on the whole enterprise, a drag that the magnificent Swedish and Norwegian networks were strong enough to absorb but should never have had to. For ten years, the cash cows at home subsidized a vanity project abroad. Eventually, someone in the boardroom had to do the math and say the thing nobody wants to say about their own ambition: this is not going to work, and continuing to fund it is not patience, it is denial.

IV. The Great Inflection: The 2018 Nordic Pivot

The reckoning came in December 2018, and it had the clean, almost surgical quality of a decision that should have been made years earlier. The board announced that Clas Ohlson would close its entire physical store network in both the United Kingdom and Germany and exit brick-and-mortar retail outside the Nordics altogether.5 After a decade of hoping the international stores would turn, management finally accepted that the conditions for profitability simply were not there, and chose the painful certainty of retreat over the comfortable uncertainty of more waiting.

Retreats cost money, and this one came with a bill. The company estimated a one-off settlement and restructuring charge of up to 210 million SEK to unwind the leases, wind down operations, and absorb the human cost of roughly 150 affected employees.56 There was a long tail to the cleanup, too: the company kept a single pilot store open in Reading as it transitioned, and only finally shuttered that last outpost in 2022, taking a final cleanup charge of around 35 million SEK to close the book on the entire physical-international chapter.7 It is worth pausing on that detail, because it captures something about how genuinely hard it is to exit a physical-retail commitment. Even after the strategic decision was made and announced, it took the better part of four more years to fully extract the company from the leases and obligations it had signed in a more optimistic mood.

But here is why the decision was correct, and it is a number worth sitting with. Closing the loss-making network was projected to improve operating profit by approximately 75 million SEK per year, every year, once complete.5 Think about what that ratio implies. The company paid a one-time cost in the low hundreds of millions to permanently remove a structural drag of 75 million annually. That is a payback measured in a small number of years on a benefit that then compounds indefinitely. The retreat was not a write-off of failure so much as the purchase of an annuity — buying back, at a discount, the margin that the foreign adventure had been quietly stealing.

The deeper move, though, was strategic rather than financial, and management gave it a name in spirit if not in slogan: the Nordic pivot. The thesis was a repudiation of the entire logic that had driven the expansion. Instead of spreading capital and attention thin across markets where the company was a sub-scale stranger, Clas Ohlson would concentrate everything on the ground where it possessed what management described as unmatched density and structural brand power — Sweden, Norway, and Finland. This was the transition every disciplined retailer eventually has to make, from chasing the vanity metric of total store count toward the harder, more valuable work of consolidating the profit pool in markets it could actually dominate. Fewer flags on the map; far more profit per flag.

Crucially, the pivot did not mean abandoning the UK and German customers entirely — it meant serving them in a way that put the risk on someone else's balance sheet. Clas Ohlson kept a presence in those markets, but converted it to an asset-light, online-only model, selling through established marketplaces such as Amazon's UK platform rather than its own stores.5 The distinction is the whole point. Owning a store in Croydon means owning the lease, the staff, the inventory, and the empty-Tuesday risk. Listing on a marketplace means renting access to demand and paying only when a sale actually happens. The company had spent a decade learning, the expensive way, that it had no edge in foreign physical retail. The online pivot let it keep whatever residual demand existed while handing the fixed costs and the inventory risk to platforms built to carry them. It was, in retrospect, the moment Clas Ohlson stopped trying to be a global retailer and started becoming a focused Nordic one with optional digital reach — and it set the table for the operator who would arrive to run the refocused company.

V. The Kristofer Tonström Era

A turnaround that has already made its hardest decision still needs someone to build the next chapter on top of it, and in March 2021 Clas Ohlson found that person in Kristofer Tonström.2 He arrived not as a hardware-retail lifer but as a disciplined consumer-goods executive, the kind of operator whose instincts run toward assortment discipline, customer data, and commercial agility rather than grand expansionist visions. After a decade in which the company's defining mistake had been ambition outrunning discipline, that temperament was precisely the corrective the business needed. The era of planting flags was over. The era of optimizing what you already had was beginning.

Tonström's strategic instinct can be summarized as a refusal to be everything to everyone. A century of catalog heritage had left Clas Ohlson with an enormous, sprawling assortment — a virtue when breadth itself was the brand promise, but a liability when every additional slow-moving SKU ties up working capital, clutters the store, and dilutes the data. His approach was to streamline relentlessly, leaning into the high-frequency, consumable, genuinely useful items that bring customers back again and again, while trimming the long tail that looked impressive in a catalog but earned its keep poorly on a shelf. In parallel, he pushed hard on integrating the digital engine — turning the loyalty program and the online channel from bolt-ons into the connective tissue of the whole operation. The result of this patient operational work showed up in the numbers that opened this episode: a company compounding sales and earnings to records while holding a roughly 12 percent operating margin, a level of profitability that most general retailers never touch.1

What makes the leadership story genuinely interesting to a fundamental investor, though, is not the strategy slide. It is the incentive structure, because how a company pays its leaders reveals what it actually wants. Start with ownership. Tonström holds 71,858 Series B shares alongside 15,000 call options, and the detail that matters is where those options came from: they were issued not by the company but directly by the major founding-family shareholders, the descendants of Clas Ohlson himself.8 That is an unusual and telling arrangement. It means the chief executive's upside is tied not to some abstract corporate pool but to the same instrument the long-term family owners hold, aligning him explicitly with their priorities — capital preservation, durable profitability, and the multi-generational health of the business rather than a quarter-to-quarter share-price pop. The chief financial officer, Pernilla Walfridsson, similarly holds 16,724 Series B shares, putting personal capital behind the cost discipline she is responsible for enforcing.8

The variable-pay design reinforces the same philosophy. The short-term incentive is deliberately capped at 60 percent of base salary — a modest ceiling by the standards of executive compensation, signaling that this is not a company trying to mint fortunes on a single good year.9 And the weighting is revealing: at least a quarter of that bonus rides on EBIT and at least another quarter on sales growth, with the remainder tied to sustainability targets and individual milestones.9 In plain language, management is paid roughly equally to grow the top line and to make that growth actually profitable — the two halves of the discipline the company so painfully lacked during its international adventure, now hard-wired into the pay structure.

The long-term incentive looks even further out. The 2025 LTI program vests over three years and keys off three measures: net sales growth, earnings per share, and a sustainability index.9 The inclusion of EPS is the quiet tell. EPS growth cannot be faked with vanity expansion; it rewards profitable growth net of the share count, which is to say it rewards exactly the capital-allocation behavior — disciplined reinvestment, sensible buybacks and dividends, no value-destroying empire-building — that the company learned to value the hard way. A management team paid on EPS over three years is a management team structurally discouraged from repeating the UK mistake. With that alignment in place, the question becomes what management does with the capital the business now reliably generates. And the most consequential answer to that question arrived in the autumn of 2023.

VI. The Spares Acquisition: Buying the Right to Repair

For most of its history, Clas Ohlson grew the way hardware retailers grow — one store, one catalog page, one product line at a time. So when the company made a genuine acquisition of scale in October 2023, it was worth asking what had changed, and whether the discipline that now governed everything else would govern the deal-making too. The target was a business called Spares — operating through Spares Europe AB and its Nordic arm — the leading digital platform in the Nordics for electronics spare parts, batteries, and accessories, running consumer-facing sites such as Teknikdelar.se and Batteriexperten.10 In other words, Clas Ohlson was buying the online version of its own founding identity: the place you go when you need the specific part to fix the thing you already own.

The structure of the deal told you a great deal about how Clas Ohlson now thinks. It acquired approximately 91 percent of Spares, with an initial purchase price of around 430 million SEK, corresponding to an enterprise value of roughly 500 million SEK on a cash- and debt-free basis.10 Layered on top was a performance-based earn-out of up to 225 million SEK, payable only if the business hit growth and profitability targets through the summer of 2024.10 The earn-out is not a financial footnote; it is a philosophy. By making a meaningful slice of the price contingent on the acquired business actually performing, Clas Ohlson protected itself from overpaying for a story while ensuring the sellers had every reason to keep delivering after the ink dried. And the founders and key managers of Spares did more than that — they reinvested to retain roughly a 9 percent stake, keeping their own skin in the game rather than cashing out and walking away.10

Now to the question every acquisition deserves: did they overpay? At the time of the deal, Spares had generated sales of about 820 million SEK over the prior twelve months, with an adjusted EBITA of roughly 49 million SEK — a margin around 6 percent, modest in absolute terms but characteristic of a fast-growing e-commerce business reinvesting in expansion.10 On the initial enterprise value, that works out to a little over 10 times EBITA, rising to a maximum of 10.5 times if the full earn-out were eventually paid.10 To gauge whether that is rich or cheap, you have to look at where comparable assets traded. Fast-growing, digital-native, niche-leading Nordic e-commerce businesses of this profile routinely commanded valuations in the range of 12 to 15 times EBITA in this period. Acquiring the outright category leader in a defensive, structurally growing niche at roughly 10 times was, by that benchmark, a disciplined and even conservative use of capital — exactly the behavior the EPS-linked incentive plan was designed to encourage. The deal was advised on the sell side by Lincoln International and on the buy side by Carnegie, the kind of professional process that tends to push prices up, not down, which makes the modest multiple more notable still.[^11][^12]

The strategic logic was tighter than the price discipline alone would suggest, and it rested on a macroeconomic wave that Clas Ohlson was unusually well-positioned to ride. The "right to repair" movement — part regulatory push, part consumer reaction to inflation and environmental fatigue — has been steadily extending the lifespan of the devices in people's homes. When a phone costs a small fortune and money is tight, you do not replace the cracked screen by buying a new phone; you buy a screen, a battery, a repair kit, and you fix it. Spares sits directly in the path of that behavioral shift, selling precisely the parts and tools that a longer-device-life economy demands. For a company whose entire founding DNA was helping people fix their own stuff, buying the digital pure-play leader of the repair economy was less a diversification than a homecoming — the catalog spirit reborn as an e-commerce platform.

Having established that platform, Clas Ohlson moved to compound it. In November 2025, its Spares unit announced two add-on acquisitions: 70 percent stakes in both Phonelife AB — a fast-growing operator that had itself absorbed the well-known Teknikmagasinet brand in 2024 — and Reservdelaronline Sverige AB, a spare-parts e-commerce specialist, with options to acquire the remaining 30 percent of each after three years.11 Phonelife was forecast to reach net sales of around 207 million SEK in 2025 with adjusted EBITA of roughly 18.4 million SEK, valued at an enterprise value near 184 million SEK — again right around 10 times EBITA, the same disciplined yardstick.11 Reservdelaronline, smaller at about 59 million SEK in forecast sales, was valued near 45 million SEK.11 The point of these tuck-ins was not the headline revenue but the synergy: bolting more volume onto the warehousing, logistics, and digital infrastructure that Spares already operates, so that each incremental brand drops more profit to the bottom line than it could ever earn standalone. This is the platform play in miniature — buy the infrastructure once, then feed it. And it points toward a set of businesses inside Clas Ohlson that the headline retail numbers tend to obscure.

VII. The Hidden Gems: Club Clas, Spares, and Clas Office

Walk into a Clas Ohlson store in central Stockholm and you will see a busy, unremarkable hardware shop. What you will not see are the three businesses that increasingly determine the company's strategic value, because two of them are made of data and software and the third lives in the back offices of small companies. These are the hidden engines, and each one addresses a different structural weakness that has killed lesser retailers.

Start with Club Clas, the loyalty program, which as of mid-2026 counted roughly 6.2 million members.2 Set that against a Nordic population base of a few tens of millions and the density is genuinely striking — this is one of the most penetrated loyalty programs in the region relative to the people it could possibly reach. But membership counts are a vanity metric unless they translate into behavior, and here the behavior is the point. Members purchase markedly more often than non-members — the company points to frequency on the order of 1.8 times higher, alongside larger baskets — which turns the program from a marketing list into a structural advantage.2 The reason it matters so much in 2026 specifically is the economics of customer acquisition. Across retail, the cost of buying attention through search engines and social platforms has climbed relentlessly, and a privacy-first internet has made that bought attention less effective. A retailer with 6.2 million direct, first-party relationships can simply talk to its customers without paying a toll to an advertising intermediary every time. It can target promotions precisely, forecast demand store by store, and tune inventory to local reality. In an era where customer-acquisition cost is the silent killer of online margins, owning the relationship outright is a moat — and one that competitors cannot quickly dig.

The second hidden engine is Spares, which deserves a second look not as an acquisition but as a structural addition to what Clas Ohlson is. Run as a decentralized unit rather than folded into the core retail machine, Spares does two things the legacy business could not. First, it gives Clas Ohlson a true pure-play e-commerce footprint riding the repair wave, growing without the capital intensity of opening and staffing physical stores. Second, and more subtly, it gives the company reach beyond the Nordics — into the broader European market — through a channel that carries none of the fixed-cost, long-lease baggage that made the original international expansion such a disaster. It is, in a sense, the redemption of the failed UK and German strategy: international growth, finally, but asset-light and demand-led rather than lease-heavy and hope-led. The company learned that lesson at a cost of a decade and a few hundred million kronor, and Spares is what it built with the lesson.

The third engine is the quietest: Clas Office, the business-to-business arm aimed at small and medium-sized enterprises. The insight here is about lock-in. Small businesses need a constant trickle of unglamorous supplies — the office consumables, the maintenance and fixing items, the random hardware that keeps a workplace functioning — and procuring it is a low-value chore nobody wants to manage. By integrating B2B accounts across its physical stores and digital portals, Clas Ohlson lets an SME treat it as an outsourced supply closet: one relationship, one account, predictable replenishment. The beauty of this from an investor's perspective is the quality of the resulting revenue. Corporate accounts buy on a recurring, somewhat predictable cadence, they are stickier than fickle retail shoppers, and they tend to carry healthy margins because convenience, not rock-bottom price, is what they are buying. It is the same trust-and-convenience proposition the company has sold to households for a century, repackaged for the back office. Each of these three businesses, in its own way, is a defense against a specific threat — rising ad costs, capital-intensive expansion, and consumer fickleness — which is the natural bridge to the harder analytical question: just how durable is the whole structure?

VIII. The Competitive Fortress: Powers and Forces

To assess durability properly, it helps to run the business through two analytical frameworks — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — not as an academic exercise but as a way of war-gaming where the moat is real and where it is thin.

Begin with what Helmer would call the company's primary power: scale economies, expressed through sourcing. Clas Ohlson sources roughly 70 percent of its products directly from Asia, and it does so through dedicated local infrastructure rather than at arm's length through importers. The company operates a sourcing hub in 上海 Shanghai — 遨盛(上海)贸易有限公司 Clas Ohlson (Shanghai) Co., Ltd., established in 2008 — alongside a quality-assurance and corporate-responsibility operation in 深圳 Shenzhen, set up in 2010.12 The strategic value of owning this sourcing apparatus is layered. By dealing directly with manufacturers, Clas Ohlson bypasses the importer's markup, captures the fat gross margins available on private-label goods, retains the flexibility to switch suppliers when price or quality demands it, and aggregates shipping into its single automated warehouse in Insjön. That combination — direct sourcing plus centralized, automated distribution — is the engine behind the roughly 12 percent operating margin, and it is not something a smaller competitor can easily replicate, because the buying leverage only works at scale.

The second power is a cornered resource, and it is the intangible one: the Clas Ohlson brand in Sweden and Norway. We have already seen what its absence cost the company abroad; at home, its presence is exactly what makes the business defensible. A century of being the reliable problem-solver has made the name synonymous with convenience, and that reputation occupies prime city-center real estate that competitors cannot simply buy their way into. The brand is the reason a shopper walks past three other options to reach the Clas Ohlson sign — and that reflex is not for sale.

The third power is the most forward-looking: counter-positioning, embodied by the Spares repair model. Here Clas Ohlson is structurally positioned against the big-box consumer-electronics retailers — chains like Elgiganten and Power — whose entire business model depends on selling expensive new devices. A retailer that profits from people buying new phones cannot easily pivot to helping them repair old ones, because doing so cannibalizes the core. Clas Ohlson, with no new-device business to protect, can lean fully into repair. That is the textbook counter-positioning trap: the incumbent sees the threat clearly but cannot respond without damaging the franchise that makes it valuable.

Now run Porter's Five Forces over the same business. The bargaining power of suppliers is low, precisely because of the Shanghai and Shenzhen sourcing apparatus — direct relationships and the ability to switch manufacturers keep pricing discipline firmly on Clas Ohlson's side of the table. The bargaining power of buyers is medium-to-high: retail consumers can always shop elsewhere, but the density of the Club Clas ecosystem and the physical proximity of urban stores meaningfully reduce how much of that leakage actually occurs. The threat of substitutes is medium and the most-watched: Amazon and other e-commerce giants are a genuine pressure, but they struggle to replicate the specific value of physical immediacy — the ability to walk into a downtown store and walk out, ten minutes later, with the exact plumbing valve or lightbulb in hand. Same-day desire for a small functional part is the one demand an overnight-delivery model cannot fully satisfy.

The force that bites hardest is competitive rivalry, and it is high. Clas Ohlson operates in a crowded Nordic arena against tough, well-run competitors — Jula, Biltema, and Rusta among them — each fighting for the same household kronor. But notice the strategic differentiation: those rivals largely pursue large, out-of-town warehouse formats, the big-box model on the edge of town. Clas Ohlson deliberately occupies the opposite position — smaller, highly accessible, city-center stores built for the quick convenience trip rather than the weekend expedition. That positioning does not make the rivalry disappear, but it means the company is not fighting head-to-head on its competitors' chosen terrain. It has carved out the convenience corner of the market and defends it with brand, density, and the loyalty data nobody else has. The fortress is real — which does not mean it is impregnable, and a serious investor has to weigh what could bring it down.

IX. Bull, Bear, and What to Watch

Step back from the frameworks and the picture resolves into a set of playbook lessons, then a genuine debate about the future.

The lessons first, because they are the transferable part. The clearest is about the profit pool: international vanity projects can quietly destroy a wonderful home-market business, and the discipline to retreat from the UK and Germany in order to double down on the Nordics is a textbook case of choosing focus over flags. The second lesson is about strategic adjacency in acquisitions — Clas Ohlson did not buy Spares because spare parts were a hot category; it bought Spares because the business was a digital-native expression of the company's own century-old fixing identity, which is why the integration worked rather than diworsifying the core. The third lesson is about the CRM moat: in a privacy-first world where bought attention keeps getting more expensive, owning 6.2 million direct customer relationships is an operational shield against the rising cost of doing business online, and it compounds quietly while competitors keep paying the advertising toll.

The bear case is not hard to construct, and an honest analysis has to take it seriously. The first risk is currency, and it is structural rather than incidental. Clas Ohlson buys the majority of its goods in US dollars and Chinese yuan while selling in Swedish and Norwegian kronor, which leaves the income statement genuinely exposed to exchange-rate swings — a sharp move in the dollar can compress gross margins regardless of how well the stores are run, and the repair businesses have already felt this pull as currency conditions shifted. The second risk is saturation. With more than 250 stores and loyalty penetration that already reaches a large share of the addressable Nordic population, the runway for organic physical expansion at home is approaching its natural limit. The growth that came from simply opening more stores in more Nordic towns is largely behind the company; what comes next has to come from elsewhere, and that is a harder, less certain kind of growth.

The bull case answers the saturation worry directly. The repair economy — Spares and its add-ons in Phonelife, Teknikmagasinet, and Reservdelaronline — represents a digital growth engine that is not capped by the Nordic store map and can, in principle, scale across the rest of Europe without the lease commitments that doomed the first international push. If the right-to-repair wave continues to swell, the company has positioned itself on exactly the right side of it. And underpinning the whole bull thesis is a demonstrated mastery of capital allocation: a business that has settled into a roughly 12 percent operating margin and is comfortable returning the bulk of its profit to shareholders — the 14.00 SEK combined dividend proposed in June 2026 being the latest evidence — is a business that has learned the difference between growth for its own sake and growth that creates value.1 The contrast with the company that bled cash in Croydon for a decade could hardly be sharper.

So what should a long-term investor actually watch? Amid all the numbers, two or three KPIs carry most of the signal. The first is the operating margin itself, sitting near 12 percent — it is the single cleanest readout of whether the sourcing engine, the assortment discipline, and the loyalty-driven marketing efficiency are still working in concert, and it is the metric most exposed to the currency risk the bears worry about. The second is the growth and profitability of the Spares segment, because that is where the company's next chapter is being written; if the repair platform keeps compounding and integrating its add-ons at the disciplined multiples management has paid so far, the saturation argument loses its force. And the third, quieter gauge is Club Clas engagement — not merely the headline member count but the frequency and basket data underneath it, because that is the leading indicator of whether the CRM moat is deepening or merely growing wider and shallower.

The story that began at a kitchen table in Insjön in 1918 turns out to be, at its heart, a story about knowing what you are. Clas Ohlson nearly forgot — it spent a decade and a fortune trying to be a global retailer it was never built to be. What saved it was the discipline to retreat to its own ground, the patience to re-engineer the economics, and the insight to recognize that an old company's founding spirit, the impulse to help people fix their own things, could be reborn as a thoroughly modern platform. Whether that recognition carries the company through the next century, the Insjön warehouse will keep shipping the parts to find out.

References

-

Clas Ohlson Year-end report 2025/26 — Clas Ohlson (Cision), 2026-06 ↩↩↩↩

-

Clas Ohlson Year-end report 2024/25 — Clas Ohlson, 2025 ↩↩↩↩

-

Clas Ohlson Annual and Sustainability Report 2024/25 — Clas Ohlson Investor Relations ↩

-

Clas Ohlson Throws In Towel in U.K., Germany by Closing Stores — Bloomberg, 2018-12-05 ↩↩

-

Clas Ohlson closes shops in UK and Germany — Ecommerce News Europe, 2018-12-05 ↩↩↩↩

-

Clas Ohlson Annual and Sustainability Report 2021/22 — Clas Ohlson Investor Relations ↩

-

Clas Ohlson Corporate Governance — Board and Management Shareholdings — Clas Ohlson ↩↩

-

Clas Ohlson Corporate Governance — Remuneration (STI/LTI) — Clas Ohlson ↩↩↩

-

Clas Ohlson acquires Spares — accelerates presence in accessories and spare parts for electronic products — Clas Ohlson, 2023-10-02 ↩↩↩↩↩↩

-

Clas Ohlson strengthens its offering in technology, accessories and spare parts — acquires Phonelife and Reservdelaronline — Clas Ohlson, 2025-11 ↩↩↩

-

Clas Ohlson Annual and Sustainability Report 2024/25 — Sourcing and Operations — Clas Ohlson ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube