BP: The Great Energy Pivot

I. Introduction: The "Beyond Petroleum" Paradox

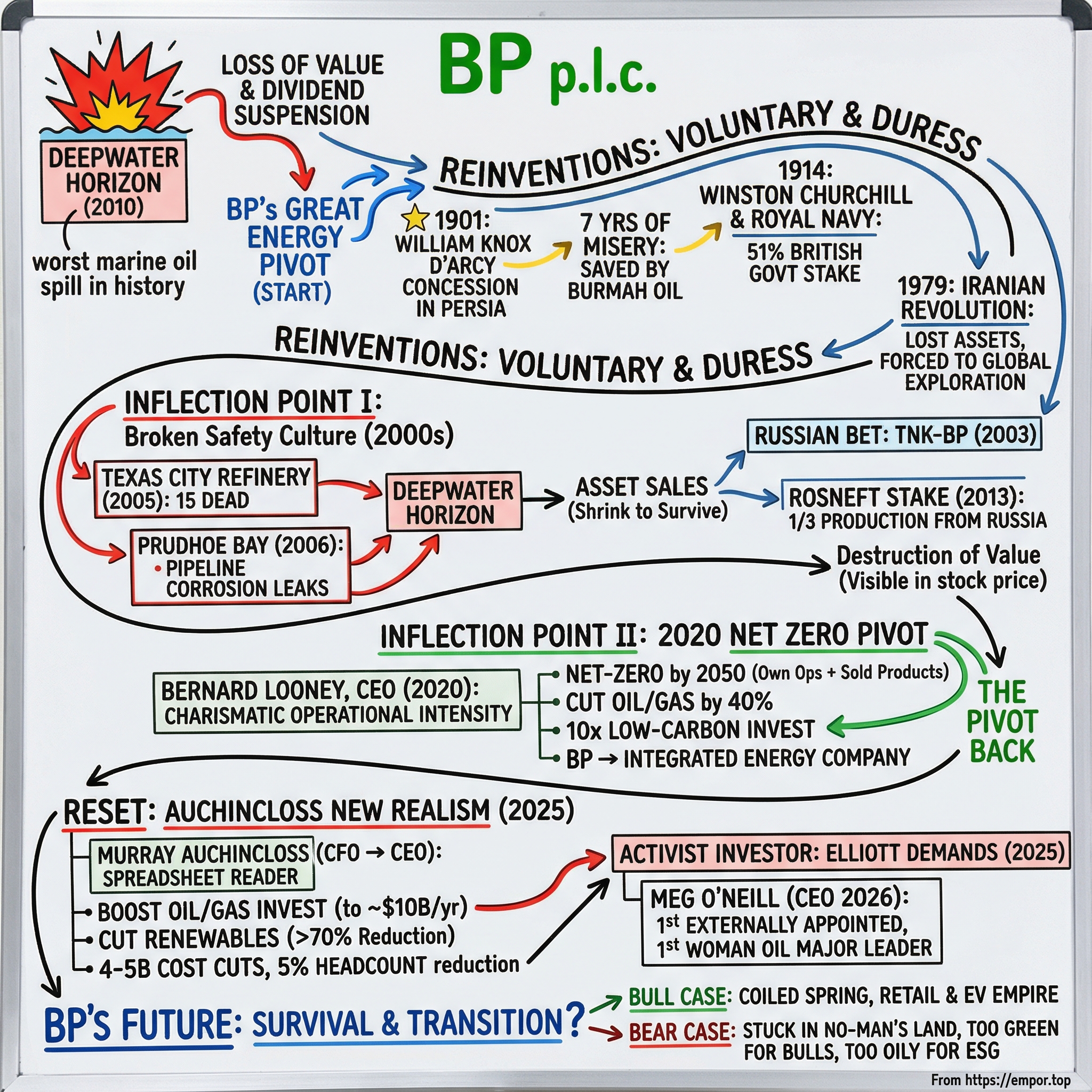

On the night of April 20, 2010, a column of methane gas screamed up through five thousand feet of ocean and exploded on the deck of the Deepwater Horizon drilling rig in the Gulf of Mexico. Eleven men died. The rig burned for two days, capsized, and sank, unleashing the worst marine oil spill in history. Within weeks, BP's market capitalization was cut in half — roughly a hundred billion dollars of shareholder value, gone. The company suspended its dividend for the first time since World War II. In living rooms and congressional hearings across America, BP became shorthand for corporate recklessness.

Fast forward to February 2020. A charismatic new CEO named Bernard Looney stood on a London stage and declared that BP would become a net-zero company by 2050. Oil and gas production would be slashed by forty percent. Investment in low-carbon energy would increase tenfold. The old shield logo was long gone, replaced by a sunburst named Helios — the Greek god of the sun. BP was not merely beyond petroleum. It was, in Looney's telling, reimagining energy itself.

Fast forward again to February 2025. Yet another CEO, Murray Auchincloss, stood before investors and effectively tore up Looney's playbook. Oil and gas investment would jump back to ten billion dollars a year. Renewables spending would be cut by more than seventy percent. The net-zero production targets were quietly shelved. BP had pivoted, and then pivoted back.

This is the story of a company that has been reinventing itself — sometimes voluntarily, sometimes under extraordinary duress — for over a century. It is the story of a British institution born from an Edwardian gambler's bet on Persian oil, midwifed by Winston Churchill's navy, battered by one of the worst industrial disasters in modern history, and now caught between two tectonic forces: the financial imperative to pump hydrocarbons while they are still worth something, and the existential recognition that the world is slowly, unevenly, moving on.

The question that hangs over BP today is deceptively simple: Can a 115-year-old oil company survive the energy transition? And if so, what does it become? As of this writing, BP has a new CEO — Meg O'Neill, the former head of Australia's Woodside Energy, who officially took the reins just nine days ago on April 1, 2026. She is the first externally appointed chief executive in BP's history and the first woman to lead a top-five oil major. She inherits a company with roughly $120 billion in market capitalization, a suspended share buyback, an activist investor breathing down the board's neck, and a strategic identity crisis that has now consumed three CEOs in under four years.

The bull case says BP is a coiled spring — trading at a deep discount to peers, buying back shares at a ferocious pace when it can, and quietly assembling a high-margin retail and EV charging empire that will one day deserve a very different valuation multiple. The bear case says BP is stuck in no-man's land — too green for the oil bulls, too oily for ESG investors, strategically incoherent, and slowly bleeding competitive position to better-capitalized rivals.

The truth, as usual, is more interesting than either cartoon. To understand where BP is going, you have to understand where it came from — and the extraordinary series of crises, gambles, and reinventions that brought it to this moment.

II. Founding & The Persian Legacy

In the spring of 1901, a portly, mustachioed Australian financier named William Knox D'Arcy sat in a London office and signed a document that would reshape the twentieth century. D'Arcy had made his fortune in Queensland gold mining — a classic Victorian-era speculator who understood that outsized returns came from outsized risks. The document was a sixty-year concession from the Shah of Persia, granting D'Arcy exclusive rights to prospect for oil across 480,000 square miles — roughly three-quarters of modern Iran. The price was modest by imperial standards: twenty thousand pounds in cash, another twenty thousand in shares of a company yet to be formed, and sixteen percent of future profits to the Persian crown.

What followed was seven years of misery. D'Arcy dispatched a drilling team under a stubborn British engineer named George Reynolds to the arid foothills of southwestern Persia. The conditions were brutal — scorching heat, malarial swamps, hostile terrain, and local tribes who were understandably suspicious of foreign drillers punching holes in their land. By 1904, D'Arcy had spent one hundred sixty thousand pounds and was nearly bankrupt. His Lloyds Bank overdraft was staggering. The venture looked like a fool's errand.

Salvation came from Burmah Oil Company, which provided rescue financing in exchange for a controlling interest. The drilling moved to a site called Masjed Soleyman, and on May 26, 1908, at four in the morning, Reynolds's team struck oil in commercial quantities. It was the first major petroleum discovery in the Middle East — a find that would redraw the geopolitical map of the entire region for the next hundred years.

The Anglo-Persian Oil Company was incorporated on April 14, 1909. A pipeline was laid to a new refinery at Abadan on the Persian Gulf, which would grow to become the largest refinery in the world. But the company remained fragile and undercapitalized — until a young, ambitious politician intervened.

Winston Churchill, then First Lord of the Admiralty, was engaged in one of the most consequential military decisions of the early twentieth century: converting the Royal Navy from coal to oil. Oil-powered ships were faster, could refuel at sea, and required fewer stokers. But Britain had plenty of coal and almost no oil. Churchill needed a secure, affordable, British-controlled supply — and he was determined not to depend on Standard Oil or Royal Dutch Shell.

On July 7, 1914, Churchill rose in the House of Commons and made his case. The British government would purchase a fifty-one percent controlling stake in the Anglo-Persian Oil Company for two million pounds, along with a thirty-year contract to supply the Royal Navy at preferential rates. The bill passed on August 5, 1914 — one day after Britain entered World War I. The timing was not coincidental. Energy security had become national security, and the precedent Churchill set that summer — a government willing to buy, invest, and fight to control energy supplies — would echo through the next century of BP's history.

For the next six decades, BP (renamed Anglo-Iranian Oil Company in 1935, then British Petroleum in 1954) was one of the fabled "Seven Sisters" — the cartel of Western oil companies that controlled roughly eighty-five percent of the world's petroleum reserves. The cartel's origins traced to a secret agreement at Achnacarry Castle in Scotland in 1928, where the majors agreed to freeze market shares and coordinate pricing. BP's role was anchored in the Middle East: the massive Abadan refinery, the Iraq Petroleum Company consortium, and later, concessions across the Gulf.

This era shaped a corporate DNA that persists in subtle ways to this day. BP learned to operate at the intersection of commerce and statecraft. It learned to manage sovereign relationships, navigate geopolitical risk, and think in decades rather than quarters. It also learned, perhaps too well, to assume that political connections and government backing would provide a safety net when commercial judgment failed. That assumption would prove catastrophic — not once, but twice — in the decades to come.

The Seven Sisters' monopoly was broken in the 1970s by OPEC nationalizations and the 1973 oil embargo. BP lost its Iranian assets entirely after the 1979 revolution. The company that had been born from a Persian concession was suddenly locked out of Persia forever. It was forced to reinvent itself as a global exploration and production company, eventually merging with Amoco in 1998 and ARCO in 2000 to become one of the world's largest integrated oil majors.

But the imperial instinct — the willingness to make enormous, concentrated bets on politically complex geographies — never left BP's bloodstream. It would surface again in Russia, in the deepwater Gulf of Mexico, and in the boardroom debates about the energy transition that continue to this day.

III. Inflection Point I: The Macondo Disaster & The Lost Decade

To understand the Deepwater Horizon catastrophe, you have to understand the culture that produced it. In the early 2000s, BP was led by Lord John Browne, a brilliant, imperious CEO who had transformed the company through a series of mega-mergers — Amoco in 1998, ARCO in 2000, Burmah Castrol in 2000. Browne was lionized by the business press, compared to John D. Rockefeller, and celebrated for his 1997 Stanford speech in which he became the first major oil CEO to acknowledge climate change. He launched the "Beyond Petroleum" rebrand in 2000, replacing the company's historic shield with the Helios sunburst logo at a cost exceeding two hundred million dollars.

But behind the green marketing, Browne was running a relentless cost-cutting machine. BP's capital discipline was the envy of the industry — until it became a cautionary tale. The pressure to squeeze costs percolated down through every level of the organization, and nowhere was the effect more devastating than in process safety.

On March 23, 2005, a hydrocarbon vapor cloud ignited at BP's Texas City refinery in southeast Texas. Fifteen workers were killed and one hundred eighty were injured. It was the deadliest U.S. industrial accident in over a decade. The U.S. Chemical Safety Board's investigation was damning: BP executives had demanded another twenty-five percent budget cut for the facility that very year, maintenance had been deferred, safety equipment was obsolete, and training was inadequate. An independent review panel led by former Secretary of State James Baker concluded that BP had a "broken safety culture" — one that obsessed over slips, trips, and falls (personal safety metrics that looked good in annual reports) while ignoring the kind of process safety failures that cause explosions and kill people.

The following year, 2006, BP's Prudhoe Bay pipeline in Alaska suffered two major corrosion leaks, including the largest oil spill on the North Slope to that date. The pipeline had not been internally inspected for over eight years. BP pleaded guilty to negligent discharge.

These warnings were not heeded. Or rather, they were acknowledged with reforms that proved insufficient. And on April 20, 2010, the consequences arrived with terrible finality.

The Macondo well, located in Mississippi Canyon Block 252 in the Gulf of Mexico, was being drilled by the Transocean-owned Deepwater Horizon rig under BP's direction. At approximately 7:45 PM Central Time, high-pressure methane gas surged up through the marine riser, overwhelmed the blowout preventer, and ignited. The explosion killed eleven workers instantly. The rig burned for thirty-six hours before capsizing and sinking in five thousand feet of water.

What followed was eighty-seven days of uncontrolled oil flow — roughly four million barrels, or 210 million gallons, of crude oil gushing into the Gulf. The environmental damage was staggering: over a thousand miles of coastline contaminated, an estimated one million seabirds killed, and deep-sea ecosystems damaged in ways scientists are still studying. Television cameras trained on the underwater plume broadcast the disaster into American homes twenty-four hours a day, turning BP into the most reviled company in the country.

The financial toll was equally extraordinary. BP's total costs from Deepwater Horizon have exceeded sixty-five billion dollars — a figure that includes a twenty-billion-dollar civil settlement (the largest environmental settlement in U.S. history), four billion in criminal fines, fifteen billion in cleanup costs, and roughly twenty billion in economic damages claims. To put that number in perspective, sixty-five billion dollars was more than BP's entire market capitalization at its post-spill low. It was the corporate equivalent of paying for your own funeral and then being told you still had to go to work on Monday.

To fund the cleanup and legal settlements, BP embarked on a massive program of asset sales, divesting roughly thirty-eight billion dollars' worth of properties over the following years. These were not marginal assets — they were some of BP's best-performing fields and operations, trophy properties that competitors were only too happy to acquire at distressed prices. The fire sale forced BP into what management euphemistically called a "shrink to grow" strategy, but in reality it was shrink to survive. Exxon, Shell, Chevron, and Total did not face this constraint. They could invest for the future while BP was paying for the past.

The Macondo disaster also reshaped BP's geographic strategy in ways that would have profound consequences. With its balance sheet under enormous strain and its deepwater reputation in tatters, BP doubled down on a relationship that had been building for nearly a decade: Russia.

In 2003, BP had created TNK-BP, a fifty-fifty joint venture with a consortium of Russian oligarchs, combining their respective oil assets in Russia and Ukraine. BP contributed eight billion dollars, and for years the venture was highly profitable — giving BP access to vast Siberian reserves at a time when its other exploration frontiers were shrinking. But the partnership was volatile. In 2008, a bitter corporate dispute erupted; BP's on-the-ground CEO, Robert Dudley, was essentially forced to flee Russia after his work visa was revoked amid escalating tensions with the Russian partners.

In 2012, Rosneft — the Russian state oil company — offered to buy out the entire TNK-BP venture for fifty-five billion dollars, the largest oil industry acquisition in history. BP accepted, receiving twelve billion in cash and an 18.5 percent stake in Rosneft itself. The transaction, completed in March 2013, made BP the largest foreign shareholder in Russia's national oil champion. At a stroke, Rosneft came to represent roughly half of BP's oil and gas reserves and a third of its production.

It was a staggering concentration of risk. BP had bet its reserves base — the foundation of any oil company's valuation — on a single, politically fraught counterparty in a country with a track record of expropriating foreign assets. Bob Dudley, who by then had become BP's CEO, argued that the relationship was strategic, that Russia's vast hydrocarbon reserves were irreplaceable, and that the commercial terms were attractive. All of which was true. But so was the fact that BP had essentially made itself hostage to the Kremlin's geopolitical calculations — a vulnerability that would crystallize with devastating speed a decade later.

For investors, the Macondo decade represented a destruction of value that is still visible in BP's stock price today. While Exxon and Chevron rebuilt and expanded through the 2010s, BP spent those years writing checks to the U.S. government, selling assets, and managing a Russian bet that grew more uncomfortable by the year. The company that had been the world's second-largest oil major by market capitalization before the spill never regained that status. The ESG-era discount on BP shares — which would become a central topic in the 2020s — did not begin with Bernard Looney's green pivot. It began on a burning drilling rig in the Gulf of Mexico.

IV. Inflection Point II: The 2020 "Net Zero" Pivot

Bernard Looney was not a typical oil executive. A fast-talking Irishman from County Kerry, he had joined BP as a drilling engineer in 1991 and risen through the upstream ranks with a reputation for charisma, operational intensity, and an unusual (for the industry) willingness to engage with climate activists rather than dismiss them. When he was named CEO in September 2019, effective January 2020, the choice signaled that BP's board wanted a communicator — someone who could articulate a vision for the company's future that would satisfy an increasingly restive investor base.

Looney did not disappoint on the vision front. On February 12, 2020 — barely six weeks into the job — he delivered what may have been the most dramatic strategic announcement in the history of any oil major. BP would become a net-zero company by 2050 or sooner, not just in its own operations, but across the full lifecycle of its products, including the emissions from the oil and gas it sold to customers. The company articulated ten specific aims, backed by quantified targets.

The details, laid out more fully in an August 2020 strategy presentation, were breathtaking. BP would cut oil and gas production by forty percent by 2030 — from 2.6 million barrels of oil equivalent per day to roughly 1.5 million. It would increase low-carbon investment tenfold, to approximately five billion dollars per year. It would develop fifty gigawatts of renewable generating capacity. It would reduce its refining capacity by thirty percent. And it would not explore for oil in any new countries.

No other oil major had gone nearly this far. Shell had made net-zero commitments, but without specific production cut targets. TotalEnergies was investing aggressively in renewables, but framing it as addition rather than substitution. Exxon and Chevron were barely acknowledging the conversation. Looney was betting that BP could win a first-mover advantage by defining what an "Integrated Energy Company" looked like — moving from the old IOC (International Oil Company) model to something genuinely new.

The market's reaction was, to put it mildly, conflicted. Climate-focused investors and ESG-oriented funds applauded. But the traditional oil investor base — yield-hungry institutions that owned BP for its fat dividend and share buybacks — recoiled. If BP was going to voluntarily shrink its most profitable business by forty percent, why own it? The dollars flowing into wind farms and solar panels would earn lower returns than deepwater oil for years, perhaps decades. BP was effectively telling its shareholders: trust us, the transition will eventually create more value than the hydrocarbons we are giving up. It was a version of the classic innovator's dilemma, except that the company was cannibalizing itself not because a competitor was forcing it to, but because it believed the world was changing.

The result was what analysts began calling "the ESG discount." BP's stock persistently underperformed its peers. Between 2020 and 2024, Exxon's market capitalization roughly doubled. BP's barely moved. The company was caught in a valuation trap: ESG-focused funds appreciated the rhetoric but could not overlook that ninety percent of BP's cash flow still came from fossil fuels, while traditional energy investors saw a company voluntarily impairing its own earning power. Neither camp was willing to assign a premium.

Then, on February 27, 2022, Russia invaded Ukraine. Two days later, BP's board convened an emergency meeting and announced that it would exit its 19.75 percent stake in Rosneft — a holding that represented the single largest asset on its balance sheet. The decision was partly ethical, partly practical (Western sanctions made continued ownership untenable), and entirely devastating to BP's financials. The company took a twenty-four-billion-dollar write-down in the first quarter of 2022 — the largest single-company financial hit from the Russia crisis. Roughly thirteen and a half billion reflected the carrying value of the Rosneft shares; another eleven billion was accumulated foreign exchange losses that had been sitting on the balance sheet since 2013, finally crystallized.

The Rosneft exit did not just hurt BP's income statement. It obliterated a significant portion of the reserves and production that underpinned the company's valuation. In one board meeting, BP lost assets that represented roughly half its proved reserves. It was as if Macondo had happened again — not through an explosion, but through a geopolitical shock that made an entire country's worth of oil and gas assets vanish from the books.

And then Looney himself was gone. In September 2023, he resigned abruptly after admitting that he had not been "fully transparent" about past personal relationships with colleagues. An initial board investigation in 2022 had looked at a small number of historical relationships and concluded they did not breach company policy. But new allegations surfaced in late 2023, and Looney acknowledged he should have disclosed more completely. The architect of BP's net-zero vision departed not over strategy, but over a failure of personal candor that left the board with no choice.

The man who replaced him could hardly have been more different in temperament. Murray Auchincloss, a quiet, number-driven Canadian who had served as BP's CFO, was named interim CEO on the day of Looney's departure and confirmed permanently in January 2024. Where Looney was a vision-caster, Auchincloss was a spreadsheet reader. Where Looney spoke of reimagining energy for people and the planet, Auchincloss spoke of free cash flow per share. The era of grand green ambitions was about to collide with the arithmetic of a stressed balance sheet.

V. Current Management: The Auchincloss "New Realism"

Murray Auchincloss is a fourth-generation Canadian oilman. He holds a commerce degree from the University of Calgary and a CFA from West Virginia University. He began his career in 1992 as a tax analyst at Amoco — two years before it merged with BP — and spent the next three decades rising through upstream finance roles with the quiet competence of someone who believes the numbers will always tell you the truth if you read them carefully enough.

When he took over as CEO in September 2023, BP was a company in strategic disarray. Looney's net-zero targets had alienated traditional investors without fully winning over ESG-focused ones. The Rosneft write-down had blown a hole in the balance sheet. The share price was languishing near decade lows relative to peers. And the investor base was fragmented — no one was quite sure what they were buying when they bought BP.

Auchincloss's diagnosis was blunt. In his first major strategy presentation, the "Reset BP" Capital Markets Day in February 2025, he acknowledged that BP had been "too optimistic" and had "chased too much" in the energy transition. The numbers bore him out: low-carbon investments were earning returns well below BP's cost of capital, while the company's core hydrocarbon business — particularly its deepwater Gulf of Mexico assets and its integrated trading operations — was generating the cash that funded everything else.

The reset was sweeping. Oil and gas investment was increased to approximately ten billion dollars per year, twenty percent above prior guidance. Low-carbon and transition spending was slashed to one and a half to two billion dollars annually — more than a seventy percent reduction from the five billion that Looney had targeted. Total capital expenditure was capped at thirteen to fifteen billion per year. BP announced twenty billion dollars in targeted divestments by 2027, including strategic reviews of the Castrol lubricants business and its stake in Lightsource BP, the solar developer. And in a move that cut deepest into the workforce, Auchincloss announced four to five billion dollars in structural cost reductions, including the elimination of roughly 4,700 roles and 3,000 contractor positions — a five percent headcount reduction.

The message to investors was unmistakable: BP is a cash machine that happens to be transitioning, not a transition company that happens to produce cash. The order of priority matters.

But even as Auchincloss was resetting the strategy, the ground was shifting beneath him. In February 2025, Elliott Investment Management — one of the most aggressive activist funds in the world — disclosed that it had been building a stake in BP. By April, the position had grown to approximately five percent of the company, and Elliott's demands were pointed: target twenty billion dollars in annual free cash flow by 2027 (forty percent higher than BP's own target), replace the strategy chief, create separate upstream and downstream business units for better accountability, and implement cost cuts that went far deeper than what Auchincloss had proposed. Elliott viewed the February reset as lacking "urgency and ambition" — an incremental adjustment when radical surgery was needed.

The activist pressure is widely credited as a catalyst for what happened next. In December 2025, BP's board announced that Auchincloss would step down as CEO. His replacement would be Meg O'Neill, the former chief executive of Woodside Energy, Australia's largest independent oil and gas producer. O'Neill was BP's first externally hired CEO and the first woman to lead a top-five Western oil major. She officially took the helm on April 1, 2026.

The choice of O'Neill sent several signals simultaneously. Her Woodside background — a company known for disciplined capital allocation and premium LNG operations — suggested that the board wanted operational rigor. Her outsider status suggested a willingness to break with BP's insular corporate culture. And the fact that she had led a company focused overwhelmingly on hydrocarbons suggested that the board's strategic center of gravity had shifted decisively back toward the core oil and gas business.

Alongside O'Neill, Kate Thomson continues as CFO — a role she assumed when Auchincloss moved up to CEO in late 2023 and was confirmed permanently in February 2024. Thomson, a chartered accountant who joined BP in 2004 after a career in M&A tax at Ernst & Young, is the first woman to serve as CFO in BP's history. Her mandate has been to maintain what she calls a "fortress balance sheet" — managing the tension between shareholder returns, debt reduction, and growth investment. Under her watch, BP suspended its share buyback program in early 2026, redirecting all excess cash to strengthening the balance sheet. The dividend, currently yielding roughly five percent, remains sacrosanct — but the growth rate has been held to a modest four percent per year.

The compensation structure under the current leadership is heavily tilted toward total shareholder return and free cash flow per share — metrics that align management with the value-creation framework that traditional energy investors demand. The "pay for performance" architecture is not subtle: it tells the market that BP's leadership is compensated for generating cash and returning it to shareholders, not for building renewable energy capacity or winning sustainability awards.

As O'Neill settles into the role — she has been CEO for barely nine days as of this writing — the critical question is whether she can chart a coherent strategic course that neither alienates the activist investors pushing for radical upstream focus nor abandons the transition investments that may determine BP's relevance in twenty years. It is, to put it mildly, a difficult needle to thread.

VI. M&A & Capital Deployment: Benchmarking the Bets

If you want to understand a company's real strategy, ignore the press releases and follow the capital. In BP's case, the two most revealing transactions of the Looney-Auchincloss era were not the splashy renewable energy investments that grabbed headlines, but a pair of acquisitions that, taken together, reveal a company betting on the physical infrastructure of the energy transition — the actual land, pipes, and concrete where electrons and molecules will flow.

The first was Archaea Energy. In October 2022, BP announced it would acquire Archaea, a leading U.S. producer of renewable natural gas, for approximately four billion dollars including debt. The price represented a thirty-eight percent premium to Archaea's thirty-day volume-weighted average share price and valued the company at roughly twenty times its projected EBITDA — a rich multiple by any standard.

Renewable natural gas, or RNG, is biogas captured from decomposing organic waste — primarily landfills — and processed to pipeline-quality methane. It is chemically identical to fossil natural gas but carries a different carbon accounting treatment because the methane would have been released into the atmosphere anyway. RNG benefits from federal and state incentive programs, particularly California's Low Carbon Fuel Standard, which creates tradable credits worth significant premiums over conventional gas prices.

Archaea was the market leader, operating a portfolio of RNG production facilities across the United States with a pipeline of development projects. BP's thesis was that Archaea could scale rapidly — the company targeted EBITDA exceeding five hundred million dollars by 2025 and one billion by 2027 — and that BP's balance sheet and engineering capabilities could accelerate that growth.

Did BP overpay? The twenty-times EBITDA multiple was steep relative to conventional energy deals but roughly in line with other "green premium" transactions of the era, such as Chevron's acquisition of Renewable Energy Group. The question is whether those premium multiples were justified by the growth trajectory or whether they reflected a bubble in ESG-adjacent assets that has since deflated. Under Auchincloss's February 2025 reset, BP took a five-billion-dollar write-down on its renewable energy portfolio, suggesting the market's answer has been unkind. However, Archaea's core RNG operations continue to generate cash, and the company launched nine new plants in 2024 alone.

The second acquisition was more conventional in appearance but arguably more strategic in implication. In February 2023, BP announced it would acquire TravelCenters of America for approximately 1.3 billion dollars — an eighty-four percent premium to the company's thirty-day average trading price, though only about six times trailing EBITDA. The deal closed in May 2023.

TravelCenters operated roughly 280 travel center sites across forty-four U.S. states — massive highway complexes with fuel pumps, convenience stores, restaurants, truck maintenance facilities, and parking lots. On the surface, this looked like an old-fashioned fuel distribution play: BP was buying gas stations. But the strategic logic was subtler. Those 280 sites sit on enormous parcels of land along major interstate highways — exactly the kind of real estate that becomes extraordinarily valuable if you want to build out a national network of fast-charging stations for electric trucks and passenger vehicles.

Think of it this way: the hardest part of building an EV charging network is not the chargers themselves — those are commodity hardware. The hard part is securing the real estate, the grid connections, the permitting, and the customer traffic. TravelCenters gave BP all four, packaged in a business that was already generating positive cash flow from its existing fuel and convenience operations. BP was buying the dirt under the trucks, with an embedded option on the EV future.

In the context of capital allocation, these two deals illustrate BP's attempt to position itself at the intersection of the old energy economy and the new one. Archaea captures waste gas that would otherwise be a climate liability and turns it into a revenue stream. TravelCenters provides the physical footprint for a future charging network while generating cash today. Neither bet requires the energy transition to happen on any particular timeline — they work whether the transition is fast or slow — which is precisely the kind of hedge a pragmatic CFO-turned-CEO like Auchincloss would favor.

The broader capital allocation framework tells a similar story. BP's current plan calls for roughly thirteen to thirteen and a half billion dollars in total capital expenditure for 2026, with about ten billion directed to oil and gas and the remainder split between low-carbon investments and maintenance. Divestments of three to four billion are targeted to further reduce debt. The dividend absorbs about five billion per year. Share buybacks, which had been running at roughly 750 million per quarter through 2025, have been suspended to prioritize balance sheet repair — a painful but arguably necessary concession to financial reality.

The question investors are now asking is whether O'Neill will restart buybacks in the second half of 2026 or continue directing cash to debt reduction. The answer will depend on oil prices, divestment proceeds, and whether Elliott Management is satisfied with the pace of change. What is clear is that BP's capital allocation has swung from Looney's "invest for the transition" posture to something closer to "return cash today, invest selectively for tomorrow." Whether that is strategic wisdom or strategic retreat depends entirely on your view of how quickly the energy transition will unfold.

VII. The "Hidden" BP: Segments & High-Growth Engines

Here is something that most casual observers of BP miss entirely: the company is one of the largest convenience retailers on earth. Not a metaphor. Not a side business. A genuine, scaled, global retail operation that generates billions of dollars in earnings and is growing faster than almost any other part of the company.

BP operates roughly two thousand strategic convenience sites worldwide, with a target to exceed three thousand by 2030. In Germany, its Aral brand is the country's largest forecourt operator, with more than 850 sites featuring "REWE To Go" convenience stores — a partnership with the German grocery chain Lekkerland that has turned gas stations into legitimate food retail destinations. In the United Kingdom, BP pioneered the forecourt-grocery partnership model nearly twenty years ago with Marks & Spencer, and M&S Food shops now operate across hundreds of BP stations. In the United States, the acquisition of TravelCenters added 280 highway sites to a portfolio that already included the Thorntons chain — 208 owned convenience locations across six states.

The convenience strategy is not a distraction from the core energy business. It is a deliberate bet on the physics of the energy transition. As vehicles shift from internal combustion to electric, the time required for a "refueling" stop will increase from five minutes at a gas pump to twenty or thirty minutes at a fast charger. That extra dwell time transforms a gas station from a place you want to leave as quickly as possible into a place where you might buy a coffee, a sandwich, groceries, or a meal. The economics of the site flip from selling a commodity (gasoline) at thin margins to selling food and retail at thick margins. BP's goal of generating seven billion dollars in EBITDA from convenience and EV charging by 2030 reflects this logic.

BP Pulse, the company's EV charging network, is the infrastructure play that ties the convenience strategy together. As of early 2026, BP Pulse operates more than 33,900 charging bays globally, with a target of over 100,000 by 2030. The network is concentrated in Germany, the United Kingdom, the United States, and China — the four markets where EV adoption is most advanced. Key partnerships signed in 2025 and 2026 include a deal with Simon Property Group to install ultrafast chargers at seventy-five shopping mall locations across the United States, a partnership with Waffle House for roadside charging stations, and Australia's first airport-scale charging hub.

The "Gigahub" concept — BP's flagship large-format charging station — is designed to replicate the scale and amenity of a traditional highway service area, but for electric vehicles. The idea is that a Gigahub with twenty or thirty ultrafast chargers, a convenience store, a café, and clean restrooms becomes a destination in itself, capturing the high-margin retail revenue that comes with extended dwell time. It is, in essence, a bet that the gas station of the future looks less like a gas station and more like a small shopping center.

Under the February 2025 strategy reset, low-carbon and transition investment was cut to 1.5 to two billion dollars per year, which may slow the pace of BP Pulse's expansion. But the underlying logic of the convenience-plus-charging model remains intact, and BP's competitors — Shell, TotalEnergies — are pursuing similar strategies, suggesting this is not a BP-specific thesis but an industry-wide recognition that the retail interface with consumers is about to be fundamentally redesigned.

Then there is the segment that BP rarely talks about publicly but that may be its single most durable competitive advantage: trading and shipping. BP's Integrated Supply and Trading division, known internally as IST, is one of the largest physical commodity trading operations in the world. It trades over five million barrels per day of oil and refined products — more than many countries produce — along with natural gas, LNG, power, carbon credits, and biofuels. It employs roughly 1,800 traders and operates around the clock from trading floors in London, Chicago, Houston, and Singapore.

What makes IST so valuable is not its size but its integration. Because BP owns upstream production, midstream pipelines and shipping, refineries, and downstream retail outlets, its traders can capture value at every point in the supply chain. They do not just trade paper barrels on a screen; they move physical molecules around the world, optimizing flows between BP's own assets and the open market. In volatile markets — which is to say, most of the time — this physical optionality generates enormous alpha. When oil prices spike, IST can redirect cargoes to the highest-value destination. When refining margins collapse in one region but hold up in another, IST can shift feedstocks accordingly.

The trading division functions, in effect, like an internal hedge fund — one that is permanently long physical infrastructure and can monetize dislocations that purely financial traders cannot access. In 2025, BP's Customers & Products segment, which includes trading, delivered its highest underlying earnings since 2019, with refinery availability consistently above ninety-six percent. Carol Howle, the executive who runs supply, trading, and shipping, was selected as interim CEO during the Auchincloss-to-O'Neill transition — a choice that underscored the trading division's centrality to BP's identity and performance.

The bioenergy and hydrogen businesses are earlier in their development but represent the long-term optionality embedded in BP's portfolio. Archaea's RNG operations provide a near-term revenue stream from waste-to-energy conversion, while BP's hydrogen projects — including a one-gigawatt blue hydrogen facility at Teesside in the UK and a green hydrogen electrolyzer at Lingen in Germany — represent bets on industrial decarbonization that will take years to mature. Under the revised strategy, hydrogen investment has been maintained at a selective level, with five to seven projects targeted globally by 2030.

The common thread connecting these "hidden" businesses is a simple insight: BP's future value may depend less on how much oil it pumps out of the ground and more on how effectively it manages the flow of energy — in all its forms — from source to consumer. The trading floor, the convenience store, the charging bay, and the biogas plant are all expressions of the same capability: integrating complex supply chains and capturing margin at every handoff. Whether this will be enough to justify a re-rating from "cyclical oil major" to "integrated energy platform" is the central question of BP's next decade.

VIII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces

To assess whether BP can sustain returns above its cost of capital over time, it is useful to apply two complementary analytical frameworks: Hamilton Helmer's Seven Powers, which identifies the specific sources of durable competitive advantage, and Michael Porter's Five Forces, which maps the structural attractiveness of the industry in which BP competes.

Starting with Helmer's Seven Powers. The most potent power BP possesses is process power — embodied in its Integrated Supply and Trading division. This is not a technology or a patent but an organizational capability built over decades: the ability to optimize physical commodity flows across a global network of owned and leased assets, generating returns from operational decisions that competitors cannot easily replicate. Process power is inherently difficult to copy because it is embedded in institutional knowledge, relationships, systems, and culture. You cannot acquire it through M&A or reverse-engineer it from a competitor's financial statements. BP's trading operation has been developing this muscle since the company began shipping Persian crude in 1912, and it remains one of the few areas where BP genuinely outperforms larger rivals.

Scale economies provide a secondary advantage, particularly in refining and logistics. BP's refining network — including major facilities at Whiting (Indiana), Gelsenkirchen (Germany), and Rotterdam — spreads fixed costs across enormous throughput volumes. But this advantage is not unique. Shell, Exxon, and Chevron operate refining networks of comparable or greater scale, so while economies of scale exist, they are not a source of differentiation.

Cornered resource is the third relevant power. BP's deepwater Gulf of Mexico acreage — including the Thunder Horse platform (capable of 250,000 barrels per day), Atlantis, and the newer Argos platform — represents some of the highest-quality, lowest-cost barrels in the company's portfolio. The 2025 Bumerangue discovery in Brazil's pre-salt Santos Basin, BP's largest find in twenty-five years, reinforces this position. Access to world-class geological provinces is a genuine competitive advantage, though it is shared with other majors who hold adjacent acreage.

Counter-positioning — the power that arises when an incumbent adopts a business model that competitors cannot copy without damaging their own existing business — was briefly in play during the Looney era. BP's aggressive net-zero commitments could have been a form of counter-positioning against "pure play" oil companies like Exxon: if the world was truly shifting to clean energy, being first to reposition would create enormous value. But the February 2025 reversal effectively abandoned this positioning. BP is no longer trying to be structurally different from its peers; it is trying to be a better version of the same thing. The counter-positioning opportunity, at least for now, has been forfeited.

Network economies, switching costs, and branding are all relatively weak for BP. Oil is a commodity; customers do not exhibit loyalty to a particular barrel of crude. Castrol is a strong consumer brand in lubricants, but it is a small fraction of BP's overall revenue. And network effects — where the value of a product increases as more people use it — are essentially absent in the oil business, though they could emerge in EV charging if BP Pulse achieves sufficient density to make its network meaningfully more convenient than competitors'.

Turning to Porter's Five Forces, the structural picture is challenging. The threat of substitutes is the most important force shaping BP's strategic environment. Renewable energy, battery storage, and electric vehicles are direct substitutes for BP's core products — gasoline, diesel, and natural gas. The substitution is not happening overnight, but the trajectory is clear: global EV sales have grown from roughly three percent of new car sales in 2020 to over twenty percent in 2025, and government mandates in the EU, UK, and California will accelerate the shift. This is the fundamental driver of BP's entire strategic debate: how quickly will demand for its core product decline, and can it build replacement revenue streams fast enough?

Bargaining power of buyers is increasing. As governments mandate EV adoption, regulate emissions, and impose carbon pricing, BP's traditional customers — drivers who pull into a gas station — have less reason to stay loyal to the pump. Industrial buyers of crude oil and refined products, meanwhile, face growing pressure to decarbonize their supply chains, creating demand for lower-carbon alternatives that BP is only beginning to offer at scale.

Bargaining power of suppliers is moderate. BP's key suppliers are oilfield service companies (Schlumberger, Halliburton, Baker Hughes), drilling rig operators, and construction firms. In periods of high activity, these suppliers gain pricing power; in downturns, it shifts back to the operators. The cyclicality is a feature of the industry, not specific to BP.

Threat of new entrants is low in BP's traditional business — the capital requirements, technical expertise, and regulatory barriers to entering deepwater oil production are enormous. But in BP's growth businesses — EV charging, convenience retail, renewable energy — barriers to entry are much lower. Tesla, ChargePoint, and dozens of startups compete aggressively in EV charging. Amazon and established grocery chains compete in convenience. The "moat" around BP's transition businesses is narrower than the moat around its oil and gas operations.

Rivalry among existing competitors is intense and getting more so. Among the oil majors, Exxon has leaned fully into hydrocarbons, betting that peak oil demand is further away than consensus believes. Shell has pursued a moderate transition strategy while maintaining an aggressive buyback program. TotalEnergies has invested heavily in LNG and renewables. Chevron has focused on capital discipline and shareholder returns. BP, having oscillated between green ambition and hydrocarbon pragmatism, risks being perceived as strategically incoherent — a perception that Elliott Management has exploited aggressively.

The net assessment is that BP operates in a structurally challenging industry that is being disrupted by substitution — and its most durable advantages (trading process power, deepwater resource access) are concentrated in the very business segment that faces the most existential long-term threat. The company's growth bets — convenience, EV charging, bioenergy — are in more attractive structural positions but lack the scale and moat to compensate for the core business under a rapid transition scenario.

IX. Bull vs. Bear Case & Epilogue

The bear case for BP is straightforward and uncomfortable. The company is "stuck in the middle" — a phrase that Porter himself would recognize as the most dangerous strategic position a company can occupy. BP is too green for oil bulls, who see Exxon and Chevron as purer plays on sustained hydrocarbon demand, and too oily for ESG investors, who view BP's net-zero reversal as confirmation that the company was never serious about transition. The strategic oscillation — green pivot under Looney, hydrocarbon pivot under Auchincloss, unknown trajectory under O'Neill — has destroyed credibility with both camps.

The numbers support this reading. BP's market capitalization of roughly $120 billion is less than half of Shell's and less than a fifth of Exxon's. Its EV-to-EBITDA multiple of around five times is not a discount driven by hidden value; it reflects the market's judgment that BP's earning power is less durable, its strategic direction less certain, and its balance sheet less robust than those of its peers. The suspended buyback program removes the most powerful near-term catalyst for the stock. And Elliott Management's presence, while potentially value-creating, also introduces the risk of a destabilizing strategic fight that consumes management attention at precisely the moment when focus is most needed.

The bear case also points to BP's M&A track record. The Archaea acquisition, completed at twenty times EBITDA in 2022, has already triggered a write-down as the economics of renewable natural gas proved less favorable than the bull case assumed. The TravelCenters deal, while cheaper in relative terms, added operational complexity in a segment — truck stops — that is capital-intensive and low-margin in its current form. If the EV charging thesis takes longer to play out than expected, BP is left holding expensive real estate that generates modest returns.

The bull case is more nuanced but equally compelling. Start with the buyback math. When a company trading at five times EBITDA buys back its own shares, it is effectively acquiring the cheapest asset in the market — itself. BP repurchased roughly twenty-four billion dollars' worth of shares in 2022 and 2023 alone, shrinking its share count meaningfully. If buybacks resume in the second half of 2026, which several analysts expect, the per-share earnings accretion could be substantial. BP is, in this view, a cash machine temporarily depressed by idiosyncratic factors (Macondo legacy, Russia exit, CEO turnover) that is systematically shrinking its denominator.

Then there is the hidden retail and EV charging business. If BP achieves anything close to its seven billion dollar EBITDA target from convenience and EV charging by 2030, that segment alone would justify a significant portion of BP's current enterprise value — and it would deserve a retail or infrastructure multiple (ten to fifteen times EBITDA) rather than the cyclical oil multiple (four to six times) that the market currently assigns to the whole company. The sum-of-the-parts argument is that the market is valuing BP as if it is just an oil company, when it is increasingly a diversified energy and retail platform.

The trading division is another source of underappreciated value. IST's ability to generate billions in earnings that are partially decoupled from commodity prices — profiting from volatility and physical optionality rather than directional price moves — provides a stability of cash flow that pure-play upstream companies cannot match. In a world of increased energy price volatility, this capability becomes more valuable, not less.

The deepwater portfolio adds a geological foundation. The Bumerangue discovery in Brazil, BP's largest find in a quarter century, provides years of high-return development activity that will generate cash regardless of what happens in the transition debate. The Gulf of Mexico platforms — Thunder Horse, Atlantis, Argos — remain among the most productive deepwater assets in the world, with breakeven costs well below current oil prices.

For investors evaluating BP from here, two key performance indicators matter above all others. The first is free cash flow per share — the metric that captures both the company's ability to generate cash from its operations and the effect of share buybacks on concentrating that cash among remaining shareholders. If free cash flow per share is growing, it means BP is either generating more cash, buying back more shares, or both. This single number encapsulates the "cash machine" thesis better than any other metric.

The second is the trajectory of non-oil EBITDA — specifically, the earnings contribution from convenience retail, EV charging, trading, and bioenergy as a percentage of total EBITDA. If this percentage is rising, it validates the "integrated energy company" thesis and supports the case for a higher valuation multiple. If it stagnates or declines, it means BP's diversification efforts are not scaling and the company remains fundamentally an oil producer dressed in transition clothing.

There is a deeper question beneath the financial arithmetic, and it is one that extends beyond BP to the entire oil industry. Is it possible for a company built to extract, refine, and sell hydrocarbons to transform itself into something fundamentally different — and to do so while continuing to return capital to shareholders, maintain a fortress balance sheet, and manage the decline of its legacy business? Or is the energy transition a challenge that requires new institutions, built from scratch, unencumbered by the physical infrastructure, organizational culture, and shareholder expectations of the old energy world?

BP has now attempted this transformation twice — once as marketing exercise under Lord Browne, once as genuine strategic commitment under Bernard Looney — and reversed course both times. Meg O'Neill inherits a company that is healthier than it was after Macondo, leaner than it was under Looney, and better positioned in deepwater and trading than the market gives it credit for. But she also inherits a credibility deficit that no amount of strategic presentation can erase. The only currency that will buy back trust is execution — delivering the cash flow, demonstrating the growth in non-oil earnings, and proving that BP can be both a disciplined hydrocarbon producer and a credible participant in the energy system of the future.

Whether BP is the canary in the coal mine for the entire oil industry — the first major to attempt the pivot and the first to stumble — or the pioneer whose early mistakes will ultimately prove to be the cost of learning, is a question that will not be answered for years. What can be said with confidence is that the next two to three years, under O'Neill's leadership, will determine which narrative prevails. The Great Energy Pivot is not over. It has barely begun.

X. Recommended "Long Form" Reading

-

Beyond Petroleum — The 2000s branding case study, widely analyzed in business schools as a cautionary tale about the gap between corporate messaging and operational reality.

-

Deepwater: The Gulf Oil Disaster and the Future of Offshore Drilling — The official National Commission report on the Macondo disaster, essential reading for understanding both the technical failures and the regulatory environment that enabled them.

-

The World for Sale by Javier Blas and Jack Farchy — The definitive account of how commodity traders reshaped the global economy, with extensive coverage of BP's trading operations and the culture that makes IST one of the most formidable physical trading desks in the world.

-

BP's 2024 Energy Outlook — The company's annual publication on long-term energy supply and demand scenarios, widely regarded as one of the most rigorous and data-rich forecasts available from any industry source, and essential context for understanding the transition assumptions that underpin BP's strategic planning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube