B&M European Value Retail: The Secret Direct-Sourcing Empire of the West

I. Introduction: The Discount Store That Was Secretly a Logistics Company

Walk into a B&M store on the edge of an English town on a wet Tuesday afternoon — say one of the cavernous, low-slung sheds bolted onto a retail park between a Halfords and a drive-through coffee kiosk — and the first thing that hits you is not a deal. It is a sense of controlled chaos. Pallets of dog food stacked head-high in the aisle. A wall of branded fizzy drinks priced suspiciously below what the corner shop charges. A teetering pyramid of plastic storage boxes, then garden furniture, then a private-label air fryer that looks uncannily like one selling for three times the price in John Lewis. There is no logic to the adjacencies, and that is the point. The industry calls it the "treasure hunt," and it is engineered to make you wander, linger, and toss things into a trolley you never came in for.

Now here is the trick that most shoppers never see. The reason that branded can of cola is cheaper than the corner shop, and the reason that air fryer earns a fat margin, is that B&M is not really competing as a store at all. It is competing as an importer. The genius of the business is that it uses razor-thin, sometimes loss-leading prices on famous grocery brands to drag millions of people through the doors every week — and then quietly makes its profit on container-loads of homewares, toys, and seasonal goods designed in-house and shipped directly from factories in 中国 China, with the wholesalers, agents, and middlemen who clip the supply chain everywhere else simply cut out of the picture.

There is a piece of retail jargon that captures the whole machine in two phrases: "everyday low price" meeting "everyday low cost." Plenty of retailers chase the first — promise shoppers consistently cheap prices rather than a confusing churn of promotions and discounts. Very few build the second underneath it: an obsessively, structurally low cost base that actually lets you afford to be the cheapest and still profit. B&M's founders understood that the price was only the visible tip; the cost was the iceberg. You cannot sustainably out-price your rivals unless you can sustainably out-cost them, and the only way to out-cost them is to own a cheaper supply chain than they do. That is the thesis of this entire episode in a single sentence.

This is a company that took a near-bankrupt regional discounter with twenty-one shops and a turnover of about £50 million and, inside a decade and a half, turned it into a business doing £5.8 billion in annual sales.119 At its peak it carried operating margins of roughly 10 to 11 percent — two to three times what Tesco or Sainsbury's earn on a pound of sales — while selling much of the same stuff.20 For a stretch it was a FTSE 100 constituent worth more than £5 billion. It threw off so much cash it handed shareholders £2.1 billion in ordinary and special dividends over five years.20

And then, in the past eighteen months, the story got complicated — three profit warnings in a single year, a relegation from the FTSE 100, a share price down more than half, a CFO out the door amid an accounting error, and a brand-new Dutch CEO arriving to declare that the company had lost the plot and needed to get "Back to B&M Basics."2818

So the question we want to answer is the one B&M has spent twenty years hiding in plain sight: is this a retailer, or is it a direct-import logistics machine wearing a retailer's costume? Because the answer determines everything — where the margins come from, why the supermarkets can't copy it, who actually holds the keys, and whether the current wobble is a stumble or the first crack in the foundation.

Here is the roadmap. We start in Blackpool with a dying store and two brothers from Manchester who saw something nobody else did. We trace the operational masterstroke — the Far East sourcing engine that is the real beating heart of this company. We follow the private equity owners who institutionalised it and floated it. We benchmark three very different overseas bets — a German disaster, a clever British bolt-on, and a French turnaround that has quietly become the growth engine. We meet the new guard running the place today. And we close with the playbook — Hamilton's 7 Powers and Porter's 5 Forces — and the bull and bear cases for what comes next. Let's begin where every good origin story does: with a business about to die.

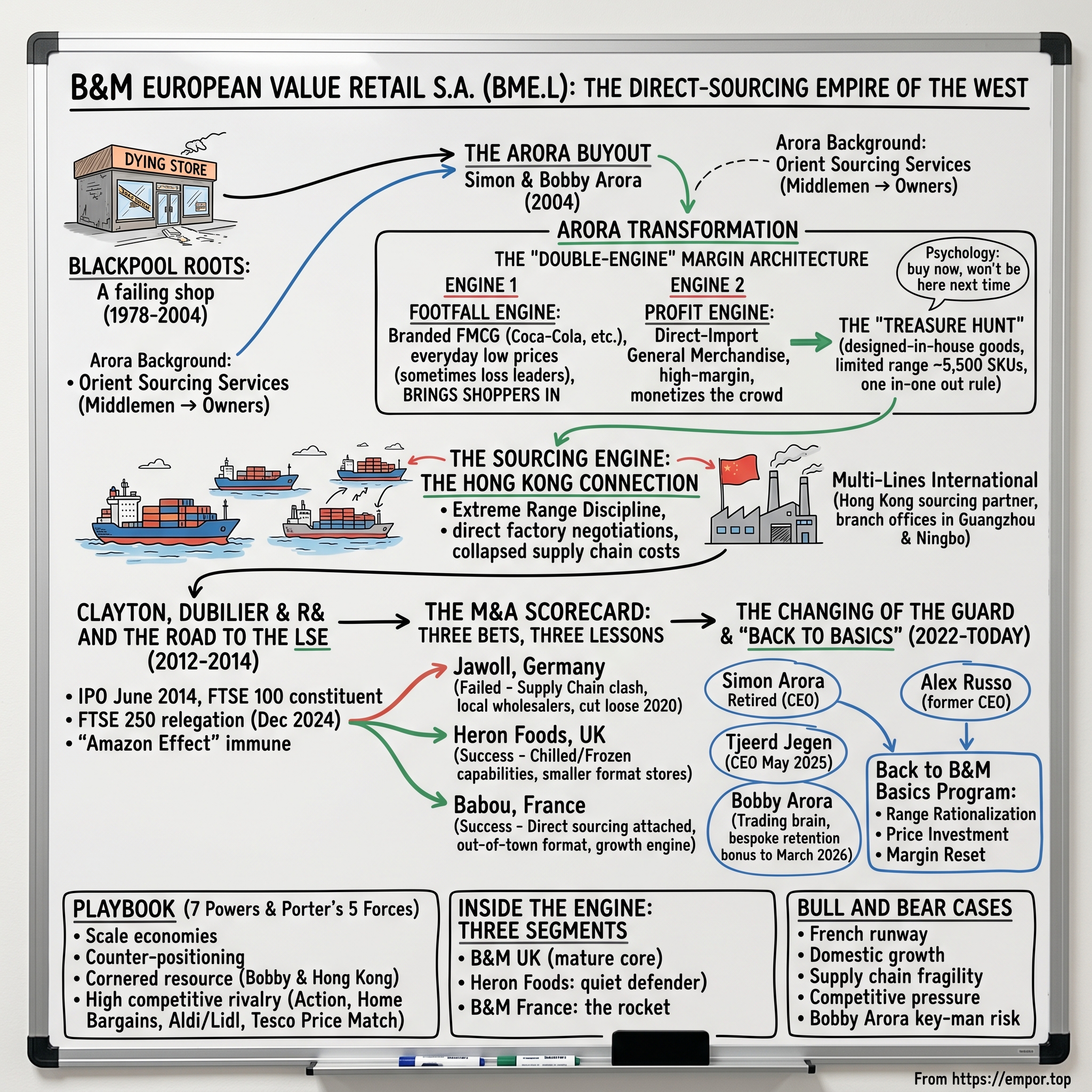

II. Blackpool Roots: From a Failing Shop to the Arora Buyout (1978–2004)

The founding of B&M is almost comically unremarkable, which is exactly why it matters. In March 1978, in Cleveleys, a small seaside town a few miles north of Blackpool on the Lancashire coast, two men named Malcolm Billington and Brian Mayman opened a discount shop and called it, with the unglamorous literalism of the era, "Billington & Mayman."33 The name was quickly shortened to its initials. And for the next quarter-century, B&M did precisely nothing of note.

This is the part of the story we can move through quickly, because the people who built the modern company would be the first to tell you the old company is irrelevant. For twenty-six years B&M was a regional, under-managed, high-street discount grocer of the sort that dotted northern England — the kind of place that sold cut-price tins and household odds and ends, that never found scale, never found a defensible edge, and never grew beyond a cluster of shops in a single corner of the country. By the early 2000s it had limped to a grand total of twenty-one stores.1 It was losing money. Most critically, it was running out of road.

By 2004 the business was, in the plainest terms, weeks from collapse. The man who would eventually run it, Simon Arora, later described the situation with brutal clarity: the chain had a turnover of around £50 million but was loss-making, and "if we hadn't bought it, it was going to run out of cash within six to eight weeks."1 This is the crucial frame for everything that follows. The Aroras did not acquire a going concern with momentum. They acquired a corpse. What they were buying was not a business at all — it was a shell, a brand name nobody loved, and a scattering of cheap retail leases.

So who were they? Simon and Bobby Arora — together with their brother Robin — were the sons of a Punjabi family that had come to the UK from Delhi in 1968 and run a small cash-and-carry warehouse in Manchester.1 They grew up around stock, margins, and the rhythms of buying low and selling on. In 1995, Simon and Bobby had gone into business together and founded Orient Sourcing Services, a wholesale operation that did one thing well: it imported homewares and consumer goods from Asia and sold them on to British retail chains.1 For the better part of a decade, that was the family trade — they were the middlemen, the importers, the people who knew which factory in southern China could make a passable kitchen utensil set at a price that left room for everyone in the chain to make money.

And that, right there, is the insight that turns this from a footnote into a foundation. The Aroras did not buy B&M because they loved discount retail. They bought it because they had spent ten years as wholesalers watching their retail customers mark up the goods they imported, and they realised that if they owned the shops, they could collapse the entire chain — factory to shelf, with no one in between taking a cut. When they bought B&M in December 2004 for the almost trivial sum of £525,000, they were not acquiring a retailer.1 They were acquiring a distribution endpoint for an importing business they already ran.

Everything Malcolm Billington built was, in effect, demolished on day one. The high-street grocery model was scrapped. The reliance on UK wholesalers — the very people the Aroras had been — was severed. The twenty-one stores became a beachhead. The brothers were about to run an experiment that British retail had never quite seen at scale: what happens when an importer, not a shopkeeper, takes over a shop?

III. The Arora Transformation: Building the Machine (2004–2012)

To understand what the Aroras did next, you have to understand the unglamorous economics of how stuff gets onto a British shelf. A traditional discount retailer in 2004 bought its general merchandise — the toys, the kitchenware, the garden tools — from domestic wholesalers and importing agents. Those middlemen had themselves bought from exporters in Asia, who had bought from the factories. Each layer added a markup, often a cumulative 15 to 30 percent, before the product ever reached a buyer's loading bay. It was a chain of comfortable intermediaries, each one perfectly happy with their slice.

The Aroras knew this chain intimately because they had been one of its links. So they did the obvious-in-hindsight, audacious-at-the-time thing: they ripped the middle out of it. Leveraging the relationships built through Orient Sourcing, they sent B&M's buying directly to the source — to the factory floors and trade hubs of southern China, the sprawling wholesale markets of 义乌 Yiwu, the twice-yearly 广交会 Canton Fair where the world's importers come to place container orders. Instead of buying a pre-made assortment from a UK distributor at a 25 percent markup, B&M placed factory-direct orders by the shipping container and captured that entire margin for itself.21

This created what is best understood as a double-engine margin architecture, and it is the single most important thing to grasp about how B&M makes money. The two engines do completely different jobs.

The first engine is footfall. B&M sells branded fast-moving consumer goods — the Coca-Cola, the Cadbury, the laundry detergent, the household names everyone recognises — at margins so thin they are sometimes essentially a loss leader. The job of these products is not to make money. Their job is to be conspicuously, almost suspiciously cheap, so that price-conscious shoppers form the habit of coming to B&M every week to stock up. Branded grocery is the bait.

The second engine is profit. Once those shoppers are inside, wandering the treasure-hunt aisles, B&M sells them general merchandise — the homewares, the seasonal decorations, the garden furniture, the air fryers — much of it designed in-house to evoke premium brands and manufactured direct in Asia at a fraction of the branded cost. This is where the real gross margin lives, well north of what any supermarket earns on a tin of beans. The branded groceries pull the crowd; the imported general merchandise monetises it. Cheap cola pays for itself by selling you a £40 garden chair on the way to the till.

There was a third, quieter masterstroke: real estate. B&M abandoned the expensive high street and the small-format shop entirely, and planted itself in out-of-town retail parks. The logic was layered. Rents and business rates were far lower, which fed straight into the everyday-low-cost discipline. Parking was free and ample, which mattered enormously when you wanted shoppers to buy a flat-pack wardrobe or a barbecue and wheel it to a car. And the sheer floor space — sheds of fifteen to twenty thousand square feet — let B&M stock the bulky, high-margin general merchandise that a cramped high-street unit physically could not hold. The format and the sourcing model were two halves of the same idea.

It is worth pausing on the psychology, because the "treasure hunt" is not an accident of messy merchandising — it is a deliberate weapon. When a shopper cannot predict what will be in the aisle, every visit becomes a small expedition. The seasonal goods rotate. The general-merchandise lines come and go under the one-in-one-out discipline. That cheap garden parasol you saw last week may be gone forever, which manufactures a gentle urgency — buy it now, because it won't be here next time. The effect is to convert a chore into entertainment, and entertainment into impulse purchases at high margin. Aldi and Lidl run a version of the same play with their famous "middle aisle" of random non-food bargains; B&M took that idea and built an entire store around it.

Underneath the theatre sat a culture the company would later codify as "everyday low cost" — an almost monastic hostility to overhead. Stores were restocked pallet-to-shelf, with goods wheeled straight from lorry to shop floor in their shipping packaging rather than being unpacked and merchandised by hand, which slashed in-store labour. Head-office frills were minimal. Marketing spend was a rounding error compared with the supermarkets' television budgets, because the products and the prices did the advertising. Every pound not spent on cost was a pound that could go into a lower shelf price or into the company's own pocket — and in the early years, much of it went into both.

The financial engine this produced was a thing of beauty. Because B&M turned its tightly-curated stock over quickly and paid suppliers on sensible terms, it generated cash faster than it consumed it — the holy grail of retail, negative or near-negative working capital that effectively lets the business grow on its customers' and suppliers' money rather than its own.

The results were the kind that get a business written up in case studies. From twenty-one stores at acquisition, B&M scaled past three hundred by the end of 2012, with annual sales climbing past £1 billion — and crucially, it did almost all of this self-funded, the expansion paid for out of the formidable cash the model generated rather than by piling on debt.2 A dying twenty-one-store chain had, in eight years, become one of the fastest-growing retailers in Britain.

By 2012, the Aroras had built something rare: a high-growth, cash-generative, structurally low-cost retail machine with a sourcing moat that no conventional grocer could easily replicate. Which is precisely the kind of asset that makes the world's most sophisticated private equity firms start sharpening their pencils.

IV. Clayton, Dubilier & Rice and the Road to the LSE (2012–2014)

In December 2012, the Aroras took a phone call that changes the trajectory of any founder-run company. Clayton, Dubilier & Rice — CD&R, one of the most respected private equity houses in the world, a firm whose operating partners have included the likes of former GE and Tesco executives — announced it had agreed to acquire a significant stake in B&M.2 The headline terms were not formally disclosed, but it later emerged that CD&R took roughly 60 percent of the chain ahead of its eventual flotation.3 At the time of the deal, B&M was already a business of over three hundred stores, sales in excess of £1 billion, more than ten thousand employees, and over two million customers a week.2

What did CD&R actually buy, and why does it matter? They bought a founder's hustle and they bet they could institutionalise it without killing it — the eternal private equity gamble. The Aroras had built a brilliant trading machine, but it was still, in many ways, a brilliant trading machine run on instinct. CD&R brought the apparatus of a grown-up corporation: professional finance and reporting systems, a more rigorous and data-driven approach to where and how fast to open new stores, centralised logistics discipline, and the governance scaffolding a public company would need.

It was also CD&R's era that gave the company the slightly mysterious name it carries to this day. To optimise the group's tax and financing structure ahead of a public listing, the holding company was established as B&M European Value Retail S.A. — the "S.A." marking it as a société anonyme, a Luxembourg-incorporated entity. It is why a quintessentially British discounter from the Lancashire coast trades under a continental European corporate banner.

The pay-off came fast. In June 2014, B&M listed on the London Stock Exchange under the ticker BME, pricing its shares at 270p and valuing the group at £2.7 billion.4 The float raised around £1 billion, most of it flowing to the selling shareholders — the Arora family and CD&R cashing in part of their stakes — with about £75 million of fresh capital earmarked for the company itself to fund European expansion.5 The chairman brought in to lend the listing City credibility was Sir Terry Leahy, the legendary former chief executive of Tesco — a powerful signal that this northern discounter now played in the big leagues.

It is worth being clear-eyed about what an IPO like this actually is, because it shapes how you read the company's incentives for the next decade. A float in which the great majority of the money raised goes to existing owners cashing out, rather than into the business, is fundamentally a liquidity event for the founders and the private equity backers — a way to convert paper wealth into real wealth and to begin an orderly exit. There is nothing improper about it; it is how the model is supposed to work. But it tells you that from June 2014 onward, B&M was a company built to return cash to shareholders, not to hoard it. And return cash it did: in the years that followed, B&M became one of the more reliable dividend machines in UK retail, supplementing its ordinary payout with a string of special dividends whenever the balance sheet allowed. In the single year to March 2025 alone it returned roughly £300 million to shareholders, and across the preceding five years it handed back some £2.1 billion in ordinary and special distributions combined — an extraordinary sum for a company of its size, and a direct expression of that cash-generative engine.20 The flip side, which the bears would later seize on, is that a business optimised to pay out rather than reinvest has thinner cushions when trading turns against it.

The public markets fell in love, and the reasons are worth dwelling on because they form the original bull thesis. Here was a retailer growing fast in a mature market, throwing off cash, and — this was the magic phrase analysts kept reaching for — seemingly immune to the "Amazon effect." Its price points were so low and its products so bulky and impulse-driven that home delivery economics simply did not work against it. Nobody was going to pay a courier to bring them a £3 storage box. By staying resolutely offline and out-of-town, B&M had accidentally built a fortress against the very force that was hollowing out the rest of high-street retail. A growth compounder that the internet couldn't touch — in 2014, that was about the most attractive thing a public retailer could be.

But a newly public company with a billion pounds of expansion ambition and a brilliant model needs somewhere to put the growth. And that is where the story gets genuinely instructive — because B&M was about to discover that its magic did not travel quite as easily as the prospectus implied.

V. The M&A Scorecard: Three Bets, Three Lessons

Here is the central question every successful single-market retailer eventually faces: is your edge a model, or is it a place? Can you take what works and export it, or is the magic somehow bound up in your home turf — your supply chain, your property market, your customers' particular habits? B&M answered this question the expensive way, through three acquisitions that produced three radically different outcomes. Taken together, they are a masterclass in why the same playbook wins in one country and loses in another.

Bet one: Jawoll, Germany — the cautionary tale. In March 2014, just before its IPO, B&M made its first move abroad, taking a majority stake (around 80 percent) in Jawoll, a discount chain in northern Germany.67 On paper it looked obvious. Germany is the spiritual home of hard discounting, a vast market, right next door. What could go wrong?

Almost everything, as it turned out. The model that made B&M unbeatable in Britain depended on two things Germany did not offer. First, B&M's edge was its centralised, direct-import supply chain — but Jawoll was wired into Germany's fragmented network of local, higher-cost domestic wholesalers, and B&M could not simply plug its Far East sourcing engine into it. The very thing that generated B&M's margins at home could not be transplanted. Second, the German discount market was already a bloodbath, dominated by the most ruthlessly efficient operators on earth in Aldi and Lidl, and German shoppers showed little appetite for the sprawling out-of-town variety format. B&M had brought a knife to a gunfight, and it was the wrong knife.

The reckoning came in stages. In November 2019, B&M took a £59.5 million impairment charge against Jawoll, and group pre-tax profit for the half fell more than 70 percent, with management blaming distribution problems and poor sales.6 Then, in March 2020, B&M cut it loose entirely, selling the business — by then 89 stores carrying annual losses of around £15 million — for a token €12.5 million, structured as €2.5 million on completion and the rest contingent on trading.7 A business it had bet on as its European bridgehead was offloaded for less than the price of a few new stores. The lesson was seared into the company: the B&M model is not a model in the abstract. It is a model plus a supply chain plus the right real estate. Remove any leg and the stool collapses.

Bet two: Heron Foods, UK — the quiet masterstroke. In August 2017, B&M paid an enterprise value of around £152 million for Heron Foods, a frozen-food specialist founded by the Heuck family in Hull.89 The deal — roughly £112 million in initial cash plus up to £12.8 million deferred — valued Heron at about eight times its EBITDA of £19.1 million on revenue of £274 million.8 To appreciate why this was clever, you have to know that comparable UK grocery and convenience deals at the time routinely cleared at ten to fifteen times earnings. B&M bought a profitable, growing chain at a meaningful discount to the going rate.

But the price was the least interesting part. Heron filled two precise gaps in B&M's armour. The first was cold-chain capability — chilled and frozen logistics that B&M's ambient, general-merchandise-heavy operation simply did not have. The second was format. Heron's stores averaged a compact 2,500 square feet, perfect for the dense urban neighbourhoods and high-street infill sites where a 20,000-square-foot B&M shed could never fit.8 B&M could now reach the customer who didn't have a car and a retail park nearby. The integration logic was elegant: B&M poured its enormous purchasing scale into Heron's ambient buying to lower its costs, and began converting suitable sites to a small-format "B&M Express" fascia.8 It was a bolt-on that bought capabilities, not just revenue — the kind of deal that compounds quietly for years.

Bet three: Babou, France — the deep-value turnaround. In October 2018, B&M acquired Babou, a chain of 95 stores, for an enterprise value of €91.2 million.10 The striking thing was how cheap it was relative to the business it was buying: Babou had revenue of €347 million, meaning B&M paid only around a quarter of one year's sales for it — a fraction of the multiple at which European discount peers changed hands.10 Why so cheap? Because Babou was a problem child. Its big out-of-town stores were stuffed with slow-moving, low-margin apparel and textiles, sitting on a bloated range of roughly 30,000 SKUs.10

But B&M looked at Babou and saw something Jawoll never had: the right bones. These were large, out-of-town stores — exactly the format B&M understood — and France, unlike Germany, was not already saturated with a dominant home-grown variety discounter. So B&M did what it does best. It gutted the underperforming clothing ranges, replaced them with the high-velocity, Far-East-sourced general merchandise and seasonal goods that drive its margins, and progressively rebranded the whole estate to B&M, a conversion completed by the end of 2021. Crucially, this time the supply-chain leg of the stool was attachable: B&M began sourcing French stock through the very same Asian engine that powered the UK. France became the proof that the model could travel — but only when the format and the supply chain travelled with it.

Line the three deals up and a clear decision rule emerges, the kind of pattern that separates disciplined acquirers from empire-builders. The common thread in B&M's two successes and its one failure is not price, geography, or timing — it is supply-chain compatibility. Heron worked because it added a genuinely new capability (cold chain and small-format) that slotted into B&M's existing engine and could be fed by B&M's purchasing scale. Babou worked because, despite being a mess, it had the right physical format and sat in a market where B&M's Asian sourcing advantage could actually be deployed. Jawoll failed because neither of those things was true: the format was wrong, the market was hostile, and — fatally — the local supply chain could not be re-plumbed to the Far East engine. The takeaway for anyone studying B&M is that its acquisition test is really a single question: can we attach this to our sourcing machine? When the answer is yes, the deals compound; when it is no, no purchase price is low enough to save them. Hold that thought, because France is about to become the most important growth story in the entire company.

VI. The Sourcing Engine: The Hong Kong Connection

Strip away the stores, the share price, the boardroom drama, and you arrive at the thing that actually makes B&M B&M: a sourcing operation run, in large part, out of 香港 Hong Kong. This is the engine room, and it is almost invisible to the average shopper, which is exactly how a moat is supposed to work.

The structural anchor is Multi-Lines International Company Limited, a Hong Kong-based sourcing agent through which B&M channels a large share of its general-merchandise buying.22 This is not a generic trading desk. By the company's own account, Multi-Lines operates as B&M's exclusive sourcing partner, headquartered in Hong Kong with branch offices on the Chinese mainland in 广州 Guangzhou and 宁波 Ningbo, running a showroom of some sixty thousand square feet that displays thousands of SKUs, and even holding the rights to put well-known brand names onto B&M's own factory-direct products under licence.23 Roughly 60 percent of B&M's general merchandise is imported, the majority of it from China, and more than half of that flows through this single Hong Kong artery.22 Twenty years of relationships, factory contacts, and quality-control knowledge are bound up in that operation. It is not something a competitor can stand up in a year.

And here is the part that separates B&M from a simple importer of cheap tat: it designs. The company does not merely walk a trade fair and buy whatever generic stock is on offer. It runs a substantial in-house product team — historically described as more than a hundred buyers and designers in the UK working alongside a specialist team of around thirty-five in Hong Kong — that actively designs private-label products, reverse-engineers premium homewares and garden ranges, and then negotiates directly with Chinese factories to manufacture them at a fraction of the branded cost.24 That air fryer that looks like the expensive one isn't a coincidence; it's a design brief executed at the factory gate.

The final piece is the most counter-intuitive, and it is where B&M's buying power really comes from: extreme range discipline. A full-service supermarket might stock 25,000 to 30,000 different items; B&M deliberately caps its range at around 5,500 SKUs and runs a strict "one in, one out" policy to keep it there.24 Think about what that does to bargaining power. Instead of buying modest quantities of tens of thousands of products, B&M buys colossal, container-load volumes of a tightly curated few thousand. To a factory in southern China, an order from B&M isn't an order — it's the whole production run. That concentration is the lever that lets a mid-sized British retailer dictate terms on the factory floor of the world's workshop. Narrowness, counter-intuitively, is the source of the power.

It helps to picture how this actually works at the product level, because it is more sophisticated than "buy cheap from China." Imagine B&M's UK design team spots a high-end ceramic planter selling for £30 in a garden centre. They will study it, strip it down to its essential look and function, and produce a design brief for a near-equivalent that can be made for a fraction of the cost. That brief goes to the Hong Kong team, who know which factory can produce it to an acceptable standard at the right price, and who negotiate the order directly — often a single, enormous run that fills containers. The product arrives months later, branded as B&M's own or under a licensed name, and lands on the shelf at, say, £12. The shopper sees a bargain. What they are actually seeing is the collapsed cost of a supply chain with no exporter, no importer, and no domestic wholesaler taking a cut — value engineered backward from the shelf price to the factory gate. Multiply that across thousands of SKUs and millions of units, and you have the profit engine.

But every strength casts a shadow, and the shadow here is concentration. A model this dependent on Chinese manufacturing and on the long ocean voyage from Asian ports to British and French distribution centres is structurally exposed in ways a domestic retailer is not. When global shipping rates spike — as they did dramatically during the pandemic, and again during periods of Red Sea disruption — the cost of getting that planter from the factory to the shelf can jump severalfold, and because B&M buys so far in advance, it can be locked into elevated freight costs for months before it can react. Add the broader geopolitical temperature around China and the risk of tariffs or trade frictions, and you have a sourcing moat that is also, in a sense, a sourcing dependency. The same narrow, China-centric supply chain that generates the margin is the single biggest variable that can compress it. This is the central tension of the whole business: the moat and the vulnerability are the same wall.

This is the asset that everything else rests on. And it is also the asset most exposed to two specific risks — the cost of shipping a container from Asia to Europe, which we have just met, and the question of who, exactly, holds the relationships. That second risk leads us straight to the people running the company today.

VII. The Changing of the Guard and "Back to B&M Basics" (2022–Today)

For eighteen years, B&M had an answer to the key-man question that didn't need asking, because the key men owned the place. But founders eventually leave, and the manner of their leaving tells you a lot about a company's next chapter.

The first to go was Simon Arora, the public face and chief executive, who retired in April 2022 after eighteen years at the helm, handing the reins to the then-CFO, Alex Russo.13 But the more revealing decision was about the brother who stayed. Bobby Arora remained as Group Trading Director — the man who actually runs the buying, the product strategy, the relationships with the Asian factories. He is, in a real sense, the human embodiment of the sourcing moat described above. And because Bobby sits outside the formal board, he doesn't participate in the standard director long-term incentive plans. So in 2023 the board did something unusual to keep him: it structured a bespoke cash retention bonus of up to £16 million, paid over a three-year period running to March 2026, explicitly to secure the commitment of the company's trading brain.13 When you have to write a £16 million contract to keep one non-board executive, you are telling the market, in the plainest possible language, where the irreplaceable value sits.

The leadership turbulence did not stop there, and the past two years have been genuinely messy. Alex Russo's tenure gave way to a period of instability: an interim chief executive, Mike Schmidt, who had also served as CFO; a CFO who departed amid an accounting error; an interim CFO, Helen Cowing, who herself stepped down after less than five months; and finally, in April 2026, the appointment of Peter Waterhouse as interim CFO — a genuine B&M veteran who had been in the group's finance function since 2013, providing a steady internal bridge through the churn.1514 Overseeing it all from July 2024 was a new chair, Tiffany Hall, appointed at that year's AGM to succeed Peter Bamford, bringing independent governance to a company badly in need of a steady hand.16

Into this came the man now charged with steadying the ship. In May 2025, B&M announced the appointment of Tjeerd Jegen as group chief executive, effective that June.11 Jegen is a heavyweight: a Dutch retail veteran with three decades of international experience, who had run the Dutch value-variety icon HEMA, and before that held senior roles across Tesco's Asian operations, Ahold Delhaize, Metro in Romania, and the supermarkets division of Woolworths in Australia.11 He arrived on a base salary of £928,000, with bonus and long-term incentives that can multiply that several times over.11 What makes Jegen an interesting fit is the shape of his career. HEMA, the chain he ran for years, is in many ways a Dutch cousin of B&M — a value-led, own-brand-heavy variety retailer that lives or dies on sourcing discipline and tight ranges. He has also spent years inside the world's most efficient grocery operators, from Tesco's Asian businesses to Ahold Delhaize, which means he has seen up close both the discount playbook and the supply-chain machinery that B&M needs to professionalise. He is, in other words, neither a pure financier parachuted in to cut costs nor a caretaker — he is an operator who has run almost exactly this kind of business before, in more than one country. That matters enormously for a company whose central challenge is to industrialise a founder's instincts without extinguishing them.

And he did something that bought him instant credibility with the market: within weeks of taking office, he went into the open market and bought around 197,900 B&M shares for roughly £524,000 of his own money.12 At a moment when the share price was on the floor, a new CEO putting half a million pounds of personal capital behind his own turnaround is about the loudest possible statement of conviction. It does not guarantee success, but it aligns him with shareholders from day one, and it signals that he believes the market has overshot to the downside — that this is a fixable operating problem, not a broken model.

It is impossible to talk about who really runs B&M without dwelling a moment longer on Bobby Arora, because he is the rarest kind of executive: the one whose value the board has put a precise price on. While Simon was always the more public, City-facing brother, Bobby was the trader — the one who walked the factory floors, who developed the eye for which £2 product would fly off the shelf and which would gather dust, who built the muscle memory of two decades of buying. That kind of merchant instinct is notoriously hard to teach and harder still to replace; it is closer to a craft than a process. The £16 million the board agreed to pay to keep him through to March 2026 is, in effect, an admission that the company's most important asset is partly housed in one man's judgement.13 For an investor, that is simultaneously reassuring — the asset is locked in for now — and unnerving, because contracts expire and craft does not transfer by memo.

That turnaround has a name — "Back to B&M Basics" — and a diagnosis. Jegen's read, launched as a formal programme in October 2025, was that B&M had quietly betrayed its own founding discipline.27 The range had crept; the legendary tight assortment had bloated with redundant choices, gumming up logistics and slowing stock turnover — the very "SKU creep" the one-in-one-out rule was designed to prevent. So the reset has two prongs. The first is range rationalisation: cutting SKU counts across grocery categories, with pilots removing roughly a third of the lines in test ranges and plans to trim 25 to 35 percent across some two hundred subcategories.18 The second is price: reinvesting margin to cut prices on 35 percent of B&M's key value items, lowering the average price of those lines by 1.8 percent, deliberately widening the price gap against the big supermarkets to protect the all-important footfall engine.17

A word here on the governance wobble, because it is exactly the kind of thing a careful investor flags rather than waves away. A revolving door at chief financial officer is never a good look, and when one of those exits is associated with an accounting error, it deserves scrutiny — it raises questions about the robustness of internal financial controls precisely when the company is under operational strain. The mitigant is that the eventual appointment of a long-serving insider as interim finance chief brings deep institutional memory and continuity to the books at a moment when stability matters more than star power.15 But the episode is a reminder that B&M's historic strengths were trading and sourcing, not necessarily the buttoned-down financial machinery that public-market investors increasingly demand. It is a watch-item, not yet a red flag.

It is also worth noting what the balance sheet has historically looked like underneath all this, because it explains why the market gave B&M the benefit of the doubt for so long. In its better years the company generated returns on capital that most retailers can only dream of — an adjusted return on capital employed north of 30 percent in FY25 — while keeping borrowings modest relative to earnings.20 A business that earns those kinds of returns and turns profit into cash can absorb a bad patch. The question the recent margin slump poses is whether those golden-era returns were a permanent feature of the model or a high-water mark inflated by the pandemic and cost-of-living booms, when shoppers flooded to discounters and B&M could do little wrong.

None of this is free, and the numbers show the pain. Clearing discontinued ranges means heavy discounting, which crushes margins in the short term. Management cut its FY26 adjusted EBITDA guidance to a range of £440 million to £475 million — down from earlier hopes well above £500 million — and the year ultimately landed at £459 million, a fall of around a quarter from the prior year's £620 million.1819 The signal of seriousness came at the half-year, when B&M cut its interim dividend — from 5.3p to 3.5p — a meaningful break for a company whose identity had become bound up with generous, ever-growing payouts.25 For a stock long owned partly for its income, that hurt, and it was part of what drove the share-price capitulation. But it was also the rational move: a board that keeps paying out lavishly while profits are falling and a turnaround is underway is a board in denial. Cutting the dividend to fund the reset and protect the balance sheet was, in the cold logic of capital allocation, the correct call even as it stung the loyalists.

The bet is the classic one: short-term pain to clear the decks, in exchange for cleaner operations, faster stock turn, and a wider price gap that drives renewed like-for-like growth in FY27 and beyond. The encouraging early sign, buried in the FY26 results, was that B&M UK like-for-like sales clawed back to marginal growth in the final quarter as the discontinued ranges cleared — a tentative hint that the medicine might be working.26 Whether that bet pays off across a full year is, in many ways, the entire investment question. But to assess it, you have to look beneath the group numbers at where the growth actually lives.

VIII. Inside the Engine: The Three Segments

B&M today is really three businesses stapled together, and they are at three very different points in their lives. Group revenue reached £5.8 billion in the year to March 2026, up 3.6 percent, but that headline hides a tale of one mature core, one quiet defender, and one genuine rocket.19

The core: B&M UK. This is the cash cow, the original machine, accounting for the large majority of group revenue and profit, and it is the patient currently on the operating table for the "Back to Basics" surgery. By the end of FY26 it ran 799 UK stores, and management still talks about a long-term runway to roughly 1,200 — meaning, on its own estimate, the UK store estate is only about two-thirds built out.19 The near-term story here is not glamorous; like-for-like sales were essentially flat, dipping a fraction over the year before clawing back to marginal growth in the final quarter as the SKU clear-out progressed.26 The bull and bear cases for the whole company largely turn on whether this core can be stabilised and its margins restored.

The defender: Heron Foods. Heron and its B&M Express siblings ended FY26 at 342 stores generating around £544 million of revenue, broadly flat on the year.19 Its strategic job is not to set the world alight but to hold ground — a high-frequency, neighbourhood, convenience footfall driver that gives B&M a foothold in the dense urban grocery spend that its big out-of-town sheds can't reach. It is currently being run through the same margin-optimisation lens as the rest of the group, but its value is defensive: it is the part of the moat that faces the high street.

The rocket: B&M France. This is the segment that quietly justifies the whole international thesis. Built on the bones of the rebranded Babou estate, B&M France ended FY26 at 147 stores, and its sales grew 13.4 percent over the year — multiples of the UK's growth rate.19 In FY25 the division turned over roughly £540 million at a healthy EBITDA margin approaching nine percent.20 France matters out of all proportion to its current size because it is the proof of concept that the B&M model is genuinely exportable when, and only when, the format and the supply chain travel with it. It is now scaling up its own European distribution infrastructure to mirror the centralised UK logistics that make the whole thing work. If the UK is the engine and Heron is the shield, France is the open road ahead.

There is a subtlety in the France story worth drawing out, because it is the crux of the long-term bull case and the place where the company's own framing and reality most need separating. B&M is careful in its formal results not to crown France its "fastest-growing division" as a slogan, but the segment numbers make the case on their own: France's growth rate has run at multiples of the UK core, off a base small enough that it has years of compounding ahead of it.19 The strategic significance is that France is the live experiment testing whether B&M is a British anomaly or a European platform. Every store it opens there, and every point of margin it sustains, is evidence in that experiment. And the company is now doing the unglamorous, capital-intensive work that real exportability requires — building out its own European distribution backbone so that French stores are fed by the same centralised, low-cost logistics that make the UK model hum, rather than relying on patched-together local arrangements. That is the lesson of Jawoll being applied in reverse: this time, the supply chain travels first.

So the segment-level "so what" is this: the boring core is being fixed, the defender is holding, and the real long-term value creation increasingly depends on France compounding for years. It is a reminder that with mature single-market retailers, the interesting question is rarely "how is the whole company doing?" but "which segment is actually the future, and is it big enough yet to matter?" For B&M, the honest answer is that France is the future and is not yet big enough — which is exactly why the next few years are so consequential. Now let's pull back and put the whole thing through the strategic frameworks.

IX. The Playbook: 7 Powers and Five Forces

If you want to know whether a business will still be earning excess returns in a decade, you don't look at last quarter's like-for-likes. You look at the structure. Let's run B&M through Hamilton Helmer's 7 Powers and then Michael Porter's Five Forces, because together they explain both why B&M earns its fat margins and why those margins are now under pressure.

Start with Helmer's framework, which asks: what stops a competitor from simply copying you and competing your profits away?

Scale economies are B&M's primary power, and they work in an unusual way. Most retailers get scale by stocking more — more SKUs, more breadth, more choice. B&M gets scale by stocking less. By concentrating gigantic purchasing volume across a deliberately tiny range of around 5,500 products, it buys at unit costs a broad-line competitor with 30,000 SKUs structurally cannot reach. Layer on a centralised distribution network — by its own account seven UK distribution centres plus one in France — spreading fixed logistics cost over enormous volume, and you have a cost base that is genuinely hard to match.2224

Counter-positioning is the most elegant of B&M's powers. The company runs essentially no e-commerce and no home delivery, and that is a feature, not a bug. By staying offline, it avoids the margin-destroying costs of last-mile delivery, picking, and returns that plague omnichannel grocers. A traditional supermarket cannot simply copy this, because it has already trained its customers to expect online delivery and built the costly infrastructure to provide it; abandoning that would mean cannibalising its own business and breaking a promise to its shoppers. B&M can be cheap because it doesn't do the expensive thing its rivals can't stop doing.

Cornered resource is the Hong Kong sourcing network — those two decades of factory relationships channelled through Multi-Lines — and, just as much, the personal trading genius of Bobby Arora, the value of which the board itself quantified at up to £16 million.13 This is the power most exposed to time, because cornered resources walk on two legs and Bobby's retention runs out in March 2026.

Process power is moderate-to-high: the deeply ingrained "everyday low cost" culture, the pallet-to-shelf restocking that minimises store labour, the out-of-town layouts engineered for rapid replenishment. This is institutional muscle memory, hard to copy but also, as the recent SKU creep showed, something that can erode if discipline slips.

The remaining powers are weak, and honesty demands saying so. Brand is moderate — B&M owns real mindshare for "extreme value," but shoppers feel no loyalty beyond price. Switching costs are essentially nil; there is no loyalty card, no account, nothing to keep you. And network effects are entirely absent. B&M is a cost-and-sourcing story, full stop. It does not have the kind of customer lock-in that defines the great compounders of tech.

Now Porter, which asks about the structure of the industry B&M competes in. The threat of new entrants is low — replicating that Asian supply chain, those factory relationships, and a prime estate of cheap out-of-town sites is a multi-decade undertaking. The bargaining power of suppliers is low for general merchandise, where thousands of Chinese factories compete fiercely for B&M's container orders, and only moderate for branded FMCG, where giants like Unilever and Coca-Cola have pricing power — though B&M counters by offering them prompt cash and zero slotting fees in exchange for the keenest prices. The bargaining power of buyers is a paradox: individual shoppers are intensely price-sensitive, yet during a cost-of-living squeeze that sensitivity makes B&M the destination of choice, not a victim. The threat of substitutes is moderate — digital-native discounters can undercut on individual cheap items but cannot replicate the instant gratification of physical retail or the fresh-and-frozen FMCG draw.

And then there is competitive rivalry, which is high and rising — and this is where the recent wobble starts to make sense. On one flank sits Action, the Dutch variety discounter backed by the private equity firm 3i, which has exploded across continental Europe to several thousand stores and is the single most dangerous competitor to B&M's French ambitions.30 On the home front there is the relentless, privately-owned Home Bargains, and the constant pressure of Aldi and Lidl, which together now command close to a fifth of the UK grocery market.32 When Tesco extends its "Aldi Price Match" deeper into its estate, it is directly attacking B&M's footfall engine by narrowing the price gap on exactly the branded staples B&M uses as bait.34 The moat is real — but the water level is being tested from several directions at once.

There is a cautionary tale sitting right next door that sharpens the point. Poundland — once the most famous name in British single-price discounting — was sold by its owner Pepco in June 2025 for the nominal sum of £1, plus pledged turnaround funding and assumed debt, after years of decline and with significant store closures expected.31 Here was a value retailer that, on the surface, looked a lot like B&M: cheap goods, price-conscious shoppers, a national store estate. Yet it collapsed in value to essentially nothing. The difference is instructive and underlines the entire thesis. Poundland's edge was a price point — the gimmick of everything costing a pound — not a structural cost advantage rooted in owning its supply chain. When inflation made the single price untenable and rivals matched its value, it had no deeper moat to fall back on. B&M's advantage, by contrast, lives in the supply chain rather than on the shelf-edge label, which is precisely why it has proved more durable. The lesson the market should take from Poundland is that not all "value retailers" are the same animal — and the ones built on sourcing tend to outlast the ones built on a slogan.

X. Myth vs Reality, and the Bull and Bear Cases

Before the bull and bear, it is worth puncturing the consensus narrative, because the popular framing of B&M has not kept up with the facts.

Myth: B&M is a £5.5 billion FTSE 100 retail juggernaut. Reality: that was true once, but it isn't now. In December 2024, after a sharp share-price slide, B&M was relegated from the FTSE 100 to the FTSE 250.28 The shares went on to fall more than half from their early-2025 levels, touching record lows around 221p in mid-2025, and the market capitalisation now sits closer to £2 billion than £5 billion.29 The company that the bulls fell in love with in 2014 — the unstoppable, internet-proof compounder — has spent the past two years being repriced as a turnaround. Any honest assessment has to start there.

Myth: B&M is a recession-proof one-way bet because hard times send everyone to the discounter. Reality: the cost-of-living crisis that should have been B&M's golden hour instead exposed its vulnerabilities — three profit warnings in 2025, an accounting error, a revolving door in the C-suite, and margins falling from over 11 percent to around 8 percent.1819 Cheap does not automatically mean resilient. Execution still matters, and recently it slipped.

With the myths cleared, the two cases come into focus.

The bull case rests on three pillars. First, the French runway: if B&M can scale its French estate from under 150 stores toward 300-plus, replicating the UK model in a market without an entrenched variety-discount incumbent, it roughly doubles the company's addressable opportunity — and France is already growing in double digits.19 Second, the reset working: if "Back to B&M Basics" successfully clears the operational bloat, restores stock turn, and drags operating margins back toward their historic 9-to-10 percent, the FY26 trough becomes the springboard for renewed like-for-like growth. Third, the domestic runway: with around 799 of a targeted ~1,200 UK stores open, there is still room to add hundreds more, particularly in the under-penetrated south of England.19 On this reading, today's depressed valuation is the market mistaking a fixable stumble for a broken model.

It is worth war-gaming the single most important competitive collision in that bull case: B&M France versus Action. Action is the elephant in the European variety-discount room — backed by deep-pocketed private equity, operating thousands of stores across the continent, and growing at a ferocious clip with a sourcing operation of genuine scale.30 B&M is entering France's general-merchandise discount space just as Action is consolidating it. The bull's retort is that the French market is large and under-served enough for both to thrive, and that B&M's out-of-town big-box format is differentiated from Action's typically smaller stores. The bear's retort is that Action has a head start, more scale, and an owner willing to fund a land-grab, and that a price war between two sourcing-driven discounters could compress the very margins that make France attractive. How that contest plays out over the next five years is, quite plausibly, the most important external variable for the entire equity story — more important than anything happening on the UK high street.

The bear case is equally coherent and turns on the same moat read in reverse. First, supply-chain fragility: B&M's margins are hostage to the cost of shipping a container from Asia and to geopolitical stability in East Asia; a spike in freight rates or a trade shock hits the general-merchandise profit engine directly, with little B&M can do about it. Second, competitive compression: if Aldi, Lidl, and Tesco's price-matching keep narrowing the gap on branded staples, the footfall engine sputters, and the whole double-engine architecture depends on that engine running. Third, and most acute, key-man risk: Bobby Arora's £16 million retention contract expires in March 2026.13 His departure would not just remove an executive — it would test whether the sourcing moat is an institution or a person. That single question may matter more to the next five years than any line in the income statement.

For the long-term investor trying to cut through the noise, the analysis ultimately collapses to a very short watch-list. The first and most important KPI is B&M UK like-for-like sales growth — the truest test of whether "Back to Basics" is working, because all the store openings in the world don't matter if the existing estate is shrinking. The second is the group operating / adjusted EBITDA margin trajectory — the single number that tells you whether the direct-sourcing advantage is still intact or being competed away, and whether the margin reset is bottoming. And the third, more thematic, is B&M France store growth, the clearest gauge of whether the model truly travels and whether the long-term growth story is real. Track those three, and you are tracking the soul of this company: a low-cost sourcing machine trying to prove that the discipline that built it can also save it.

XI. Epilogue: The Unglamorous Genius

There is a lesson buried in the B&M story that applies far beyond discount retail, and it is this: in retail, the front-end brand is only ever as good as the back-end supply chain. Everything the shopper experiences — the suspiciously cheap cola, the treasure-hunt aisles, the air fryer that costs a third of the brand-name version — is downstream of a single, deeply unglamorous act of optimisation: buying directly from the factory and refusing to let anyone stand in the middle. The Aroras' real insight in 2004 was not that Britain wanted cheaper stuff. Everyone knew that. It was that the cheapest way to sell stuff was to stop being a shopkeeper and start being an importer who happened to own shops.

That insight built a £5 billion-plus revenue business out of a near-corpse, and it remains the source of whatever durable advantage B&M still holds. The irony of the present moment is that the company's troubles stem not from the model failing but from the company drifting away from the discipline the model demands — the range creeping wider, the focus blurring, the founder-trader's instincts diluted by scale and turnover in the executive suite. Tjeerd Jegen's "Back to Basics" is, at its heart, an attempt to make a now-institutional company behave once more like the hungry importer it used to be.

Whether an outsider, however accomplished, can re-instil a founder's obsessive cost discipline — and whether the sourcing genius survives the departure of the man who built it — is the open question on which the next chapter turns. B&M is in the middle of the hardest transition any great company faces: the passage from a brilliant founder-led trading business to a durable, institutionalised global value champion. The machine is still remarkable. The question is whether the people now tending it remember exactly why it was built the way it was.

References

-

Building B&M: speed, strategy and success — Business Leader ↩↩↩↩↩↩

-

Clayton, Dubilier & Rice to acquire significant stake in leading UK variety retailer B&M Retail — CD&R, 2012-12-03 ↩↩↩

-

Private equity firm CD&R sells a further 12% stake in B&M — The Grocer ↩

-

B&M bargain valued at £2.7bn after pricing IPO — The Grocer, 2014-06-12 ↩

-

IPO values retailer B&M at £2.7bn — TheBusinessDesk, 2014-06 ↩

-

B&M profits down 70% as German arm disappoints — Retail Gazette, 2019-11-12 ↩↩

-

City snapshot: B&M sells German business for €12.5m — The Grocer, 2020-03-11 ↩↩

-

B&M acquisition of Heron Foods — investor presentation — B&M European Value Retail, 2017-08-02 ↩↩↩↩

-

B&M acquires convenience retail group Heron for £152m — Retail Gazette, 2017-08-02 ↩

-

City snapshot: B&M acquires French discount chain Babou for €91.2m — The Grocer, 2018-10-22 ↩↩↩

-

Appointment of Tjeerd Jegen as CEO — B&M European Value Retail RNS via Investegate, 2025-05-15 ↩↩↩

-

B&M CEO Tjeerd Jegen buys £500k worth of shares for bargain price — The Grocer, 2025-07 ↩

-

B&M secures Bobby Arora until 2026 — Retail Gazette, 2023-07 ↩↩↩↩↩

-

B&M European Value Retail appoints Peter Waterhouse as interim CFO with immediate effect — Reuters via TradingView, 2026-04 ↩

-

B&M interim CFO steps down after less than five months in role — Retail Gazette, 2026-04 ↩↩

-

B&M shares recovery plan lifts stock 15% as FY26 profits slump — Financial News, 2026-01 ↩↩↩↩

-

FY26 Preliminary Results — B&M European Value Retail RNS via Investegate, 2026-06-03 ↩↩↩↩↩↩↩↩↩↩

-

FY25 Preliminary Results — B&M European Value Retail RNS via Investegate, 2025-06-04 ↩↩↩↩↩

-

Anti-modern-slavery statement — B&M European Value Retail ↩↩↩

-

B&M: The Secret Source in European Value Retailing — Harvard Business School Digital Initiative, 2015-12-07 ↩↩↩

-

FY26 Interim Results — B&M European Value Retail RNS via Investegate, 2025-11-13 ↩

-

FY26 Preliminary Results — B&M European Value Retail RNS via London South East, 2026-06-03 ↩↩

-

B&M profits fall by £200m but turnaround gathers steam — The Grocer, 2026-06-03 ↩

-

FTSE reshuffle: B&M relegated as Frasers promoted — Retail Gazette, 2024-12 ↩↩

-

B&M shares are at record lows — is now the time to consider buying? — Twelfth Magpie, 2025-07-15 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube