Burckhardt Compression: The Invisible Engine of the Energy Transition

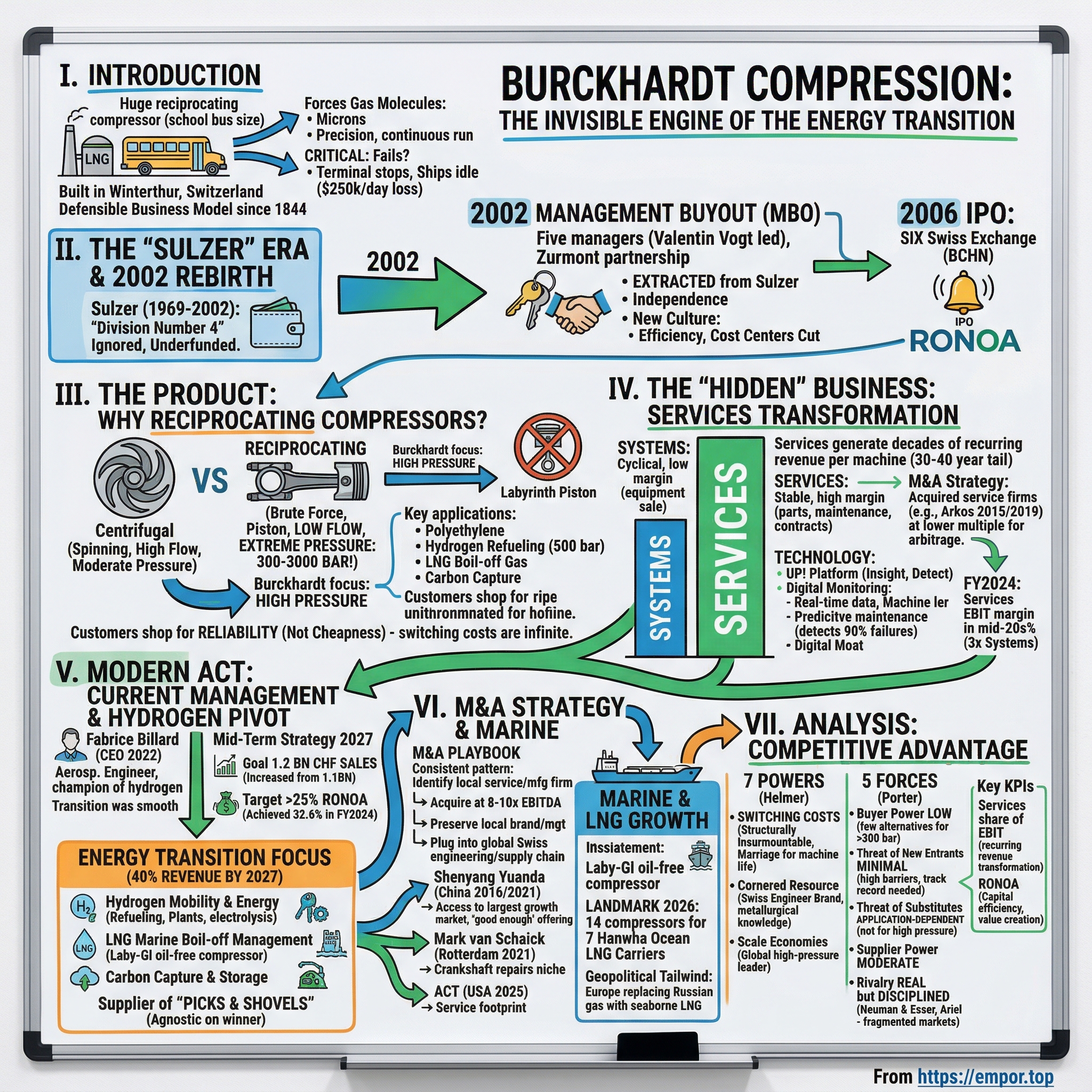

I. Introduction: The Most Important Machine You've Never Seen

Picture a liquefied natural gas terminal on the coast of Qatar at three in the morning. A labyrinth of pipes, valves, and steel vessels stretches across a landscape the size of a small city, all humming with the controlled violence of gas moving at pressures that would crush a submarine hull. Somewhere deep inside this facility, a single reciprocating compressor—roughly the size of a school bus, weighing dozens of tons—is doing what it has done every minute of every day for the past twelve years: forcing gas molecules closer together with mechanical precision measured in microns. If this machine stops, the terminal stops. If the terminal stops, an LNG carrier sits idle in the harbor burning a quarter of a million dollars a day in demurrage fees. If the carrier sits idle long enough, a city somewhere in Asia starts rationing electricity.

That compressor was almost certainly built in Winterthur, Switzerland, by a company most investors have never heard of: Burckhardt Compression.

In a world hypnotized by software margins, semiconductor moats, and AI hype cycles, Burckhardt sits at the opposite end of the industrial spectrum—a maker of enormous, brutally physical machines whose core operating principle has not fundamentally changed since the nineteenth century. And yet this company, founded in 1844 by a Basel mechanic named Franz Burckhardt, has quietly assembled one of the most defensible business models in European industry. Its market capitalization reached over four billion Swiss francs at its peak. Its return on net operating assets exceeds thirty percent. Its services division prints margins north of twenty percent. And its order book now includes compressors designed for hydrogen pressures that would have been considered science fiction a generation ago.

The question worth asking is not "what does Burckhardt Compression do?"—though explaining that will take some time—but rather "why is a 182-year-old company suddenly relevant to the most important energy debates of the twenty-first century?" The answer involves a daring management buyout, a methodical transformation from hardware seller to services platform, and a bet on hydrogen that is quietly reshaping the company's future.

But before any of that, we need to understand how Burckhardt spent decades trapped inside one of Europe's most famous industrial conglomerates—and what happened when five managers decided to break free.

II. The "Sulzer" Era and the 2002 Rebirth

The story of Burckhardt's modern existence begins not with triumph but with institutional neglect. For thirty years, from 1969 to the turn of the millennium, the compressor business that Franz Burckhardt had built sat buried inside Sulzer, the venerable Swiss engineering conglomerate headquartered in Winterthur. Sulzer was—and in some diminished form, still is—a sprawling enterprise with fingers in pumps, turbines, medical implants, surface coatings, and textile machinery. The compressor division was never the star. It was, in corporate strategy parlance, "Division Number Four"—technically profitable, strategically ignored, and perpetually underfunded.

To understand what this meant in practice, consider the late 1990s. Sulzer was in crisis. A hostile takeover attempt by Russian-born financier Viktor Vekselberg's Renova Group was consuming management attention. The textile machinery business was hemorrhaging cash. The medical division needed investment. And the compressor team in Winterthur—engineers who had invented the labyrinth piston compressor back in 1935, who held some of the most specialized metallurgical knowledge in the gas compression industry—was told, essentially, to wait their turn. Capital expenditure requests were deferred. New product development slowed. The Basel production facility, where Franz Burckhardt had originally set up shop, was shut down entirely in 2000 and 2001, with all operations consolidated in Winterthur.

It was, by all accounts, a dispiriting period. But it also created the conditions for one of the more remarkable management buyouts in Swiss industrial history.

In April 2002, a group of five managers—led by Valentin Vogt, who had been running the compressor division since 2000—executed a buyout in partnership with Zurmont, a Zurich-based financial investor. The deal extracted Burckhardt from Sulzer and reconstituted it as an independent company. Vogt, a trained lawyer with an MBA who had spent years at McKinsey before joining Sulzer, was the driving force. He understood something that Sulzer's board apparently did not: the compressor business was not a low-growth hardware operation waiting to be optimized. It was a franchise—a franchise built on an installed base of thousands of machines around the world, each one generating decades of aftermarket revenue.

The five MBO participants collectively held roughly twenty-one percent of the newly independent company's shares. They signed a shareholders' agreement—a Swiss governance mechanism that effectively bound them to act as a coordinated block—and got to work.

The first order of business was cultural. Under Sulzer, decision-making had been slow, bureaucratic, and filtered through layers of conglomerate oversight. Vogt and his team dismantled that apparatus with what people who were there describe as "Swiss efficiency applied to Swiss inefficiency." Cost centers were eliminated. Reporting lines were shortened. Engineers who had spent years writing justification memos for capital they never received suddenly found themselves in direct conversation with the CEO about product development priorities.

The financial discipline was equally striking. The MBO had been financed partly with debt, and the new management team was acutely conscious of leverage. Every franc of capital was scrutinized. The culture that emerged was one of extreme capital discipline—a trait that persists to this day and shows up clearly in the company's return metrics.

Four years after the buyout, on June 26, 2006, Burckhardt Compression listed on the SIX Swiss Exchange under the ticker BCHN. The IPO was not a cash-out event for management—the MBO group retained their twenty-one percent stake—but rather a strategic move to gain what Vogt called "the currency to compete." A public listing meant access to equity markets for acquisitions. It meant visibility with institutional investors. And it meant that the compressor engineers of Winterthur, after decades as a forgotten subsidiary, finally had their name on a stock exchange.

What happened next would prove that the buyout was not merely a financial transaction. It was the foundation for a systematic transformation of how the company made money.

III. The Product: Why Reciprocating Compressors?

Before we can appreciate what Burckhardt built on top of its independence, we need to spend time with the machine itself. This is the part of the story where most financial analysts glaze over—and it is precisely where Burckhardt's competitive advantage lives.

A compressor, at its most basic, is a device that squeezes gas into a smaller volume. Think of a bicycle pump: you push the handle down, the air inside gets compressed, and it flows into the tire at higher pressure than the surrounding atmosphere. Now scale that up by a factor of ten thousand, replace air with methane or hydrogen or ethylene, raise the target pressure to several hundred times atmospheric, demand that the machine run continuously for years without failure, and require that the gas remain absolutely uncontaminated by lubricating oil. That is the world of the reciprocating compressor—or "recip," as the industry calls it.

There are two fundamental approaches to compressing gas industrially. Centrifugal compressors use spinning impellers—think of a jet engine's turbine blades—to accelerate gas outward and convert that velocity into pressure. They are elegant, efficient at high flow rates, and well-suited for applications where you need to move enormous volumes of gas at moderate pressures. Turbo compressors in LNG liquefaction trains, for example, are typically centrifugal machines made by companies like Baker Hughes or Siemens Energy.

Reciprocating compressors take the brute-force approach. A piston moves back and forth inside a cylinder—just like in a car engine, except instead of combusting fuel, it is mechanically compressing gas. What recips sacrifice in flow rate they make up for in pressure capability. When you need gas compressed to three hundred, four hundred, or five hundred bar—pressures where centrifugal technology simply cannot reach—you need a reciprocating compressor. There is no alternative. The physics do not allow it.

This is not a trivial technical distinction. It is the foundation of Burckhardt's entire business model.

Consider the applications. In polyethylene production—the plastic used in everything from grocery bags to medical devices—a "hyper compressor" must push ethylene gas to pressures exceeding three thousand bar. Burckhardt is one of the very few companies on earth that can build these machines. In hydrogen refueling stations, gas must be compressed to five hundred bar or higher before being dispensed into fuel cell vehicles. At LNG terminals, boil-off gas—the natural gas that inevitably evaporates from cryogenic storage tanks—must be recompressed and either reliquefied or fed back into the pipeline. On LNG carrier ships, the same boil-off gas must be compressed to pressures high enough to inject directly into the ship's engines as fuel.

In every one of these applications, the consequences of compressor failure are not merely inconvenient—they are catastrophic. A failed compressor at a refinery or chemical plant does not just mean a maintenance call. It means a production shutdown. Depending on the facility, that shutdown can cost the operator anywhere from hundreds of thousands to several million dollars per day in lost output. In the worst case, a compressor failure involving high-pressure flammable gas can result in an explosion.

This is why the reciprocating compressor market is not a commodity business. Customers are not shopping for the cheapest machine. They are shopping for the machine least likely to fail—and for the company most capable of keeping it running for the next three or four decades. Burckhardt's labyrinth piston compressor, originally developed in 1935, uses a non-contact sealing system that eliminates the need for lubricating oil in the compression chamber. This means the gas remains pure—a critical requirement in applications involving food-grade gases, pharmaceutical processes, or hydrogen, where even trace contamination can be disastrous.

The installed base of Burckhardt compressors around the world numbers in the thousands. Each one is a bespoke or semi-custom machine, designed for specific gas compositions, pressures, temperatures, and flow rates. Each one requires proprietary spare parts. Each one needs periodic maintenance performed by engineers who understand the specific metallurgy, tolerances, and operating characteristics of that particular unit. And each one, once installed in a ten-billion-dollar refinery or chemical plant, is essentially permanent. Nobody rips out a functioning compressor to save a few percent on the replacement. The switching costs are not merely high—they are, for practical purposes, infinite.

This is the "Big Iron" that makes Burckhardt's financial model work. But the machine itself is only half the story. The other half—the half that transformed the company's economics—is what happens after the machine is installed.

IV. The "Hidden" Business: The Services Transformation

In 2010, if you had looked at Burckhardt Compression's income statement, you would have seen what appeared to be a straightforward industrial equipment company. The Systems division—the part that designs, engineers, and manufactures new compressors—generated the majority of revenue. It was prestigious work, technically demanding, and deeply cyclical. When oil prices rose and energy companies expanded capacity, orders flooded in. When oil prices crashed, as they did spectacularly in 2014 and again in 2020, the order book thinned and margins compressed. This is the fundamental problem of selling capital equipment: you are hostage to your customers' capital expenditure cycles.

But there was another line item on the income statement that told a very different story. The Services division—responsible for spare parts, maintenance, repairs, and field service—was smaller in revenue but dramatically more profitable. Where Systems margins fluctuated with the commodity cycle, Services margins were remarkably stable, consistently north of twenty percent at the EBIT level. Where Systems revenue lurched up and down with order intake, Services revenue grew steadily, driven by the simple mathematical reality that the installed base of compressors only gets larger over time. Machines sold in the 1980s still needed parts in 2010. Machines sold in 2010 would still need parts in 2040.

Someone at Burckhardt—and the credit appears to belong to the management team that emerged from the MBO—looked at this dynamic and had an insight that would reshape the company over the next decade. For every compressor they sold, there was a thirty-to-forty-year "tail" of aftermarket revenue. The machine itself was the entry ticket. The real money was in the decades of spare parts, maintenance contracts, diagnostic services, and emergency repairs that followed. This was not a novel insight in industrial circles—Rolls-Royce had long ago figured out that the money in jet engines was in the service contracts, not the hardware. But applying it systematically to the reciprocating compressor market required something most companies lack: the willingness to subordinate short-term equipment margins to long-term aftermarket returns.

The strategy that emerged was methodical. First, Burckhardt invested heavily in expanding its service footprint geographically. The company needed to be physically close to its installed base—you cannot service a compressor in a Texas refinery from a workshop in Winterthur. This meant acquisitions.

The most significant of these was Arkos Field Services, a Houston-based gas compression services provider with more than three hundred employees and roughly seventy-five million dollars in annual revenue, operating from over fifteen service centers across the United States. Burckhardt initially acquired a forty percent stake in December 2015, structured as a partnership that allowed both sides to evaluate the cultural fit. By November 2019, having exercised a call option, Burckhardt owned Arkos outright. The acquisition was a masterclass in what the company calls "Integration without Suffocation"—the Arkos brand was preserved, the local management stayed in place, but the operation was plugged into Burckhardt's global supply chain for proprietary parts and technical knowledge.

The economics of these service acquisitions deserve attention. Burckhardt typically acquired service businesses at valuations in the range of eight to ten times EBITDA—a reasonable multiple for stable, recurring-revenue industrial services firms. But Burckhardt's own stock, at the time, traded at twelve to fifteen times EBITDA. This created what finance professionals call "multiple arbitrage": every dollar of acquired EBITDA was immediately worth more inside Burckhardt than it had been as a standalone business, simply because the public market assigned a higher multiple to the combined entity. This is not alchemy—it works only if the acquirer can actually integrate the target and maintain or improve its margins. But Burckhardt's track record suggests they have done exactly that.

Beyond acquisitions, the Services transformation involved a technological dimension that is easy to overlook. Burckhardt developed a suite of digital diagnostic tools—now branded under the "UP!" platform—that fundamentally changed the service relationship with customers. The flagship product, UP! Insight, is a cloud-based monitoring system that collects real-time operating data from installed compressors, feeds it through machine learning algorithms, and identifies potential component failures before they happen. A companion product, UP! Detect, launched in 2025, adds vibration monitoring to the diagnostic toolkit. The underlying condition monitoring system, PROGNOST-NT, maintains a database of more than two hundred damage patterns specific to reciprocating compressors.

The business implications are profound. Traditional compressor maintenance was reactive—something broke, and the customer called for emergency service, which was expensive and disruptive. Proactive diagnostics flip that model. Burckhardt can now tell a customer that a specific valve or piston ring is showing early signs of degradation and schedule a replacement during a planned maintenance window, avoiding the million-dollar-a-day unplanned shutdown. The company claims its continuous monitoring can detect up to ninety percent of potential component failures at an early stage, reducing response and solution times by approximately seventy-five percent.

This is not just a service improvement—it is a strategic deepening of the customer relationship. A customer running Burckhardt's diagnostic software on their compressors is sharing proprietary operating data with the company, creating an information asymmetry that makes it virtually impossible for a third-party service provider to compete effectively. The diagnostic platform becomes, in effect, a digital moat around the installed base.

By fiscal year 2024, ended March 2025, the results of this transformation were clearly visible in the numbers. Services division EBIT margins reached the mid-twenties—roughly three times the margin of the Systems division. The Services business, while smaller in absolute revenue, contributed a disproportionate share of the company's total profit pool. And the combination of geographic expansion, digital diagnostics, and the ever-growing installed base created a flywheel effect: more machines in the field meant more service revenue, which funded more service acquisitions and digital investment, which improved service quality, which made customers more likely to buy the next machine from Burckhardt.

For investors, the key insight is this: Burckhardt's Systems division is what you see when you look at the company, but the Services division is what you own.

V. The Modern Act: Current Management and the Hydrogen Pivot

On April 1, 2022, Fabrice Billard became CEO of Burckhardt Compression, succeeding Marcel Pawlicek. The transition was not a rupture—Billard had been inside the company since 2016—but it marked a generational shift in ambition and strategic direction.

Billard's background is unusual for the CEO of a Swiss industrial company. Born in 1970, he holds a master's degree in aeronautics and aerospace engineering from the prestigious Ecole Centrale Paris and an executive MBA from Babson College in Massachusetts. His early career took him through Hay Management Consultants and Boston Consulting Group before he joined Sulzer—Burckhardt's former parent—in 2004. At Sulzer, he spent twelve years in progressively senior roles across the hydrocarbon processing and chemical technology divisions, including a period based in Singapore overseeing Asian operations. He understands the oil and gas customer base not as an outsider but as someone who spent years inside the industry's operational machinery.

He joined Burckhardt in 2016 as President of the Systems Division—arriving during what was, by any measure, a difficult period for the capital equipment side of the business. Oil prices had collapsed two years earlier, and the resulting capex drought was still working its way through order books. Billard's task was to turn the Systems division around, which he did through a combination of cost discipline and strategic repositioning toward higher-value applications. But the project that appears to have most defined his pre-CEO years—and that earned him the top job—was the hydrogen initiative.

Billard was the internal champion of what Burckhardt calls its "Hydrogen Mobility and Energy" program. Long before hydrogen became a fashionable investment thesis in public markets, Billard was pushing the company to develop compressor technology for hydrogen applications—refueling stations, liquefaction plants, electrolysis facilities, and power-to-X projects. His argument was straightforward: hydrogen at industrial scale requires compression to extreme pressures—five hundred bar and above for refueling, even higher for certain storage and transport applications. The physics of hydrogen compression are punishing—hydrogen molecules are tiny, leak-prone, and corrosive to many conventional materials. Building reliable compressors for these conditions requires precisely the kind of specialized metallurgical and sealing knowledge that Burckhardt had accumulated over decades with its labyrinth piston technology.

The strategic framework Billard inherited and has since expanded is the Mid-Term Strategy 2027, originally announced with a target of 1.1 billion Swiss francs in annual sales by fiscal year 2027. In June 2024, buoyed by strong order momentum, the company raised that target to 1.2 billion francs, with the Systems Division guidance increased by sixteen percent to 720 million francs and the Services Division targeting 480 million francs. The EBIT margin targets were also lifted by a percentage point for both divisions—to six-to-nine percent for Systems and twenty-three to twenty-six percent for Services.

But the numbers alone do not capture what makes the current strategy distinctive. The real shift is in the composition of revenue. Burckhardt has set a target of generating approximately forty percent of its revenues from applications that support the energy transition by 2027. This includes not just hydrogen but also LNG boil-off gas management, carbon capture and storage compression, and biogas upgrading. The company is, in effect, positioning itself as the "picks and shovels" supplier for the energy transition—agnostic about which green technology ultimately wins, but confident that virtually all of them require gas compression at some point in the value chain.

The management incentive structure reinforces this long-term orientation. Burckhardt uses Performance Share Units tied to RONOA—return on net operating assets—rather than simple revenue growth targets. This is a meaningful choice. RONOA rewards capital efficiency: generating more profit from less invested capital. It penalizes empire-building acquisitions that boost revenue but destroy returns. It encourages asset-light services growth over capital-heavy equipment sales. The target of greater than twenty-five percent RONOA was already being exceeded at 32.6 percent as of fiscal year 2024, suggesting that the incentive structure is working as designed.

Members of the executive board are also required to hold significant multiples of their base salary in Burckhardt shares. The MBO shareholder group—the descendants of the original five managers who bought the company from Sulzer in 2002—still held nearly ten percent of the company as of November 2024, coordinated by Valentin Vogt, who served as CEO for the first decade of independence and continued to influence governance through his board and shareholder roles. This ownership structure means that the people making capital allocation decisions at Burckhardt are making them with a substantial portion of their personal net worth at stake. In corporate governance terms, the alignment between management and shareholders is about as tight as it gets in European industry.

The hydrogen initiative itself has moved well beyond the proof-of-concept stage. Burckhardt has delivered compression systems for Plug Power's hydrogen liquefaction plants in the United States—an order covering twelve large hydrogen refrigeration compressors for six facilities. It has partnered with HRS, a French hydrogen refueling station manufacturer, to jointly develop large-capacity stations capable of dispensing one to two tons of hydrogen per day. It supplies oil-free hydrogen compressors for trailer filling facilities in northwestern Europe. And its diaphragm compressor technology serves smaller hydrogen fueling stations and high-purity gas applications.

The hydrogen market experienced a period of recalibration through 2024 and early 2025, as the initial euphoria around green hydrogen gave way to hard questions about infrastructure costs and policy timelines. But by the second half of 2025, Burckhardt reported signs of recovery in hydrogen-related orders, driven by national industrial decarbonization strategies in Europe and Asia. The company does not separately disclose its hydrogen backlog, but the trajectory is embedded in the forty-percent energy transition revenue target—a number that, if achieved, would represent a fundamental reshaping of the company's end-market exposure.

The transition from a management team that rescued the company from conglomerate obscurity to one that is positioning it at the center of the hydrogen economy has been remarkably smooth. But the vehicle for that positioning—Burckhardt's acquisition strategy—deserves its own examination.

VI. M&A Strategy: The "Swiss Disciplinarian"

If the Services transformation was Burckhardt's strategic masterpiece, the acquisition program was the brush that painted it. Over the past decade, the company has executed a series of deals that, taken together, represent one of the more disciplined M&A campaigns in European industrials.

The pattern is consistent. Burckhardt identifies a service company or a regional compressor manufacturer that either expands its geographic reach, deepens its technical capabilities, or gives it access to a market segment where it is underrepresented. It acquires the target at a reasonable multiple—typically in the range of eight to ten times EBITDA, well below its own trading multiple. It preserves the target's local brand, management, and customer relationships. And then it plugs the target into its global infrastructure: Swiss engineering standards, proprietary spare parts supply chains, and diagnostic technology platforms.

The Shenyang Yuanda acquisition illustrates this approach at its most ambitious. In March 2016, Burckhardt acquired a sixty percent stake in Shenyang Yuanda Compressor, the leading Chinese manufacturer of reciprocating compressors, with approximately 650 employees and annual revenue of roughly one hundred million Swiss francs. The strategic logic was compelling. China represented the world's largest and fastest-growing market for process gas compression, but it was dominated by local manufacturers competing primarily on price. Burckhardt's premium Swiss compressors were too expensive for the mid-market segment. Rather than trying to build a low-cost product line from scratch in Winterthur—a strategy that almost never works for premium European manufacturers—Burckhardt bought the Chinese market leader and positioned it as the "good enough at a good price" offering alongside its own premium brand.

The integration was deliberately light-touch. Shenyang Yuanda continued to operate under its own brand, serving the Chinese mid-market with locally designed and manufactured compressors. But it gained access to Burckhardt's engineering expertise for complex applications and to its global sales network for export opportunities. Meanwhile, Burckhardt gained a credible presence in the Chinese market and a cost-competitive manufacturing base that could serve price-sensitive customers across Asia. In January 2021, Burckhardt acquired the remaining forty percent, bringing Shenyang Yuanda fully into the fold.

The Mark van Schaick acquisition in December 2021 was smaller but strategically significant. This Rotterdam-based firm, with twenty-seven employees and about nine million francs in revenue, specialized in crankshaft repairs—a highly specialized niche within compressor maintenance that requires proprietary machining expertise. For Burckhardt, this was not about revenue scale. It was about capturing a critical link in the service value chain that might otherwise be performed by independent third parties. Every crankshaft repair performed in-house is a customer touchpoint retained, a margin captured, and a competitor shut out.

The most recent acquisition, ACT (Advanced Compressor Technology) in September 2025, followed the same playbook. ACT operates from facilities in Batavia, Illinois and Pasadena, Texas, serving the downstream reciprocating equipment market. Once again, Burckhardt was buying a service footprint—physical proximity to customers and their installed compressors—in the most important hydrocarbon market in the world.

How does this compare to the M&A strategies of Burckhardt's larger peers? Atlas Copco, the Swedish compressor giant, is perhaps the most aggressive industrial acquirer in Europe, completing dozens of deals per year across a broad portfolio. Atlas Copco's approach is more volume-oriented—it acquires widely and integrates tightly into a centralized operating model. Dover Corporation, the American diversified industrial, has historically pursued a more opportunistic M&A strategy, buying businesses across multiple verticals with less emphasis on operational integration. Burckhardt occupies a distinctive middle ground: fewer deals, more targeted, with a level of post-acquisition autonomy that preserves the entrepreneurial energy of the acquired business while extracting the financial synergies of being part of a larger platform.

The marine and LNG segment deserves special attention, both as an M&A beneficiary and as a standalone growth story. Burckhardt's Laby-GI compressor, introduced in 2019 as the world's first completely oil-free reciprocating high-pressure fuel gas compressor, positioned the company as a critical supplier for LNG carriers. These vessels inevitably experience "boil-off"—the gradual evaporation of liquefied natural gas during transport—and the boil-off gas must be managed, either by reliquefying it or by using it as fuel for the ship's engines. Burckhardt's compressors handle the high-pressure injection of this gas into the ship's propulsion system.

Since 2021, the company has sold fifty-eight compressor units for twenty-eight LNG carriers. But the landmark moment came in March 2026, when Burckhardt secured its largest single marine order in company history: fourteen boil-off gas compressors for seven 174,000-cubic-meter LNG carriers being built by Hanwha Ocean in South Korea. These vessels feature next-generation containment systems and operate at 330-bar gas injection pressure. The order was described as a "lighthouse industry reference"—a deal that establishes Burckhardt's new compressor generation as the standard for future LNG carrier construction.

The geopolitical tailwind behind this business is unmistakable. The global LNG trade, already growing rapidly before Russia's invasion of Ukraine in 2022, accelerated dramatically as European nations scrambled to replace Russian pipeline gas with seaborne LNG. Every new LNG carrier that enters the global fleet needs boil-off gas management equipment. And as the fleet grows, so does the installed base of Burckhardt marine compressors—each one generating decades of aftermarket revenue. What was once a niche application has become a geopolitical necessity, and Burckhardt is positioned as the default supplier.

VII. Analysis: 7 Powers and Porter's 5 Forces

To understand why Burckhardt Compression commands premium returns in what appears to be a mature, low-growth industrial niche, it helps to apply the analytical frameworks that investors use to distinguish durable competitive advantages from temporary ones.

Hamilton Helmer's 7 Powers

The most powerful of Helmer's seven powers operating at Burckhardt is switching costs—and the switching costs here are not merely high, they are structurally insurmountable. When a Burckhardt compressor is installed in a ten-billion-dollar refinery, it becomes part of the facility's permanent infrastructure. The machine is custom-engineered for the specific gas composition, pressure requirements, and operating conditions of that particular plant. Its spare parts are proprietary. The maintenance procedures are specific to Burckhardt's design. The foundation it sits on was poured to its dimensions. Replacing it would require not just purchasing a new compressor but re-engineering the surrounding process systems, pouring new foundations, requalifying the installation with regulators, and enduring months of downtime. No rational plant operator would undertake this to save a few percentage points on spare parts costs. The result is that once a Burckhardt compressor is installed, the customer is effectively "married" to the company for the life of the machine—which can easily be thirty to forty years.

This creates a business model with characteristics more commonly associated with software than with industrial machinery. The initial equipment sale is the customer acquisition cost. The decades of aftermarket revenue are the recurring subscription fees. The switching costs ensure retention rates that would make a SaaS company envious.

The second relevant power is what Helmer calls a cornered resource. In Burckhardt's case, this manifests in two forms. First, the "Swiss Engineer" brand—the institutional credibility that comes from 182 years of continuous operation in precision mechanical engineering—is not something a competitor can manufacture. When a customer is selecting a compressor for a mission-critical application involving hydrogen at five hundred bar, they are not just evaluating technical specifications. They are evaluating the probability of catastrophic failure, and they are assigning a risk premium to any supplier that lacks Burckhardt's track record. Second, the specialized metallurgical knowledge required to build reliable compressors for hydrogen, high-pressure ethylene, and corrosive gas applications resides in a relatively small number of engineers worldwide. Many of them work in Winterthur.

A third power worth noting is scale economies. Burckhardt is not large in absolute terms—its annual revenue of roughly 1.1 billion Swiss francs is modest compared to diversified industrial giants. But within the specific niche of high-pressure reciprocating compressors, it is the global leader. This means it can spread its R&D costs—approximately thirty million francs per year, or roughly three percent of revenue—across a larger revenue base than any specialized competitor, allowing it to invest more in product development while maintaining higher margins.

Porter's Five Forces

The bargaining power of buyers is structurally low in Burckhardt's core markets. This is not because the customers are small—Burckhardt's customers include the world's largest oil companies, petrochemical producers, and LNG operators—but because the customers have so few alternatives. For compressor applications requiring pressures above three hundred bar, the number of qualified suppliers on earth can be counted on one hand. Burckhardt, the German privately-held firm Neuman and Esser, and perhaps one or two others represent the entirety of the qualified supply base. When you need a hyper compressor for polyethylene production or a five-hundred-bar hydrogen compressor, you do not have the luxury of running a competitive bidding process with twenty suppliers. You call Burckhardt, and you negotiate—but you negotiate from a position of need, not strength.

The threat of new entrants is minimal. Building reciprocating compressors for extreme-pressure applications requires decades of accumulated engineering knowledge, proprietary metallurgical expertise, a global service infrastructure, and—critically—a reference list of successful installations that potential customers can verify. A new entrant would need to invest hundreds of millions of dollars and wait years to accumulate the track record necessary to win a single major order. The regulatory requirements in industries like LNG, petrochemicals, and hydrogen add another barrier: customers and their insurers demand proven equipment from established suppliers with documented safety records.

The threat of substitutes is application-dependent. For moderate-pressure, high-flow applications, centrifugal compressors are a viable and often superior alternative. But for the high-pressure, low-flow applications where Burckhardt concentrates, centrifugal technology cannot physically compete. The physics of fluid dynamics impose hard limits on the pressure ratios achievable with rotary machinery. This is not a gap that further engineering can close—it is a fundamental constraint of the technology. As long as industrial processes require gas compression above certain pressure thresholds, reciprocating compressors will be necessary, and Burckhardt will be relevant.

Supplier bargaining power is moderate. Burckhardt sources specialty steel, alloys, and precision-machined components from a network of suppliers, some of whom are highly specialized. However, the company's vertical integration in critical areas—its in-house metallurgical capability, its machining operations, its engineering design—limits its exposure to supplier pricing power. The acquisition of firms like Mark van Schaick (crankshaft repairs) further reduces dependence on external suppliers for critical service components.

Competitive rivalry is real but disciplined. The primary competitors—Neuman and Esser, Ariel Corporation, and to a lesser extent Baker Hughes, Atlas Copco, Howden, and Kobelco—compete vigorously for new equipment orders, and price competition can be intense in the Systems business. This is reflected in the Systems division's lower margins. However, the rivalry is significantly less intense in the aftermarket, where proprietary parts and installed-base relationships create strong incumbency advantages. The competitive dynamic is further moderated by the market's fragmentation across applications: Ariel dominates in the North American upstream gas compression market, but Burckhardt leads in high-pressure process gas and marine applications. The competitors are, to some extent, specialists in different corners of the same industry.

Key KPIs for Ongoing Monitoring

For investors tracking Burckhardt's performance over time, two metrics deserve primary attention. First, the Services division's share of total EBIT, which captures the ongoing transformation from a cyclical equipment manufacturer to a recurring-revenue services platform. As this share grows, the company's earnings become more predictable, more resilient to commodity cycles, and more highly valued by the market. The trajectory from roughly a third of EBIT a decade ago to well over half today tells the story of the transformation in a single number.

Second, RONOA—return on net operating assets—which is the metric Burckhardt's own management uses as its primary performance benchmark and compensation driver. RONOA captures both margin expansion and capital efficiency in a single figure. At 32.6 percent as of fiscal year 2024, Burckhardt is generating exceptional returns on its invested capital. Any sustained deterioration in RONOA would signal either margin pressure from competition, poor acquisition discipline, or excessive capital allocation to lower-return projects. It is, in essence, the single number that tells you whether management is creating or destroying value.

VIII. The Playbook: Business and Investing Lessons

Every great business story contains lessons that extend beyond the specific company and industry. Burckhardt Compression offers several that are worth internalizing.

The Installed Base Flywheel

The most powerful idea in Burckhardt's business model is one that sounds almost counterintuitive: the company's most valuable asset is not its factory, its engineering talent, or even its brand. It is the thousands of compressors already sitting in refineries, chemical plants, LNG terminals, and ships around the world. Every machine sold creates a thirty-to-forty-year revenue stream of parts, maintenance, and diagnostic services. The implications for pricing strategy are profound. Burckhardt can afford to be aggressive on initial equipment pricing—not necessarily selling at a loss, but accepting thinner margins than a pure-play equipment manufacturer might demand—because it is not really selling a machine. It is "renting" the right to supply high-margin aftermarket services for decades. This is the razor-and-blade model applied to industrial machinery, and it works precisely because the switching costs make the "blades"—the proprietary spare parts—irreplaceable.

The flywheel effect compounds over time. More machines in the field generate more service revenue. More service revenue funds more acquisitions of service businesses. More service businesses expand the geographic footprint, which improves service quality, which makes customers more likely to buy the next machine from Burckhardt rather than a competitor. The cycle is self-reinforcing, and it accelerates as the installed base grows.

The MBO as Cultural Catalyst

The 2002 management buyout did more than change Burckhardt's ownership structure. It fundamentally altered the company's culture. Under Sulzer, decisions were slow, capital was scarce, and the compressor division existed to serve the conglomerate's priorities. After the MBO, with management holding more than twenty percent of the equity and carrying buyout-related debt, every decision was made through the lens of capital efficiency and long-term value creation. The "conglomerate fat"—the overhead, the bureaucracy, the consensus-driven decision-making—was stripped away in months.

This cultural transformation is arguably the most underappreciated aspect of Burckhardt's success. Companies that emerge from conglomerate structures often carry institutional habits that persist for years. The MBO compressed that process into a single event. The managers who bought the company knew exactly which costs were unnecessary, which processes were redundant, and which investments had been deferred. They had spent years inside the Sulzer bureaucracy, watching good ideas die in committee. When they gained control, they moved with the urgency of people who had been waiting a long time.

Picks and Shovels for the Energy Transition

Perhaps the most relevant lesson for today's investors is how Burckhardt has positioned itself within the energy transition theme. The company is not a hydrogen producer. It is not a fuel cell manufacturer. It is not a renewable energy developer. It does not bear the technology risk, the subsidy risk, or the demand risk that accompanies many "green" investments. Instead, it supplies the critical compression equipment that virtually every form of energy transition infrastructure requires. Hydrogen production needs compressors. Hydrogen distribution needs compressors. Hydrogen refueling needs compressors. LNG—which serves as a transition fuel from coal to renewables—needs compressors. Carbon capture and storage needs compressors. Biogas upgrading needs compressors.

This "picks and shovels" positioning is powerful because it allows Burckhardt to benefit from the energy transition regardless of which specific technology ultimately prevails. If green hydrogen achieves cost parity with gray hydrogen, Burckhardt sells compressors to both. If LNG demand grows faster than expected as Asia transitions away from coal, Burckhardt sells more marine boil-off gas compressors. If carbon capture scales up, Burckhardt has compressor technology suitable for those applications too. The company is, in effect, a diversified call option on the energy transition's physical infrastructure—without the binary risk that characterizes many pure-play green investments.

Myth Versus Reality

One common misconception about Burckhardt is that it is a sleepy, slow-growth Swiss industrial company riding out the clock on legacy oil and gas infrastructure. The reality is considerably more dynamic. Revenue has grown from 650 million Swiss francs in fiscal year 2021 to nearly 1.1 billion in fiscal year 2024—a compound annual growth rate approaching twenty percent. RONOA has expanded from roughly twenty percent to over thirty percent in the same period. The company has executed multiple acquisitions, launched a digital diagnostics platform, and repositioned a significant portion of its business toward energy transition applications.

Another misconception is that reciprocating compressor technology is "old" and therefore vulnerable to disruption. This confuses novelty with obsolescence. The internal combustion engine is old technology too, but it still powers the vast majority of the world's vehicles. Reciprocating compressors endure not because the industry lacks innovation but because the physics of gas compression at extreme pressures have not changed and cannot be circumvented by clever engineering. The laws of thermodynamics are not subject to disruption.

A third misconception concerns Burckhardt's China exposure. The Shenyang Yuanda acquisition gives the company significant revenue and manufacturing presence in China, which some investors view as a geopolitical liability. This risk is real and should not be dismissed. But it is worth noting that Burckhardt's Chinese operations primarily serve the Chinese domestic market—they are not an export platform vulnerable to trade sanctions. The risk is more nuanced than a simple binary of "China exposure good" or "China exposure bad."

IX. Conclusion and Epilogue

Stand at the intersection of two massive, slow-moving global trends—the insatiable demand for natural gas as a bridge fuel and the nascent but accelerating buildout of hydrogen infrastructure—and you will find that both require the same piece of physical technology: a machine that can compress gas to extreme pressures with absolute reliability, day after day, year after year, decade after decade. There are only a handful of companies on earth capable of building that machine to the required specifications. Burckhardt Compression, from its engineering campus in Winterthur, has spent 182 years developing the metallurgical knowledge, the design expertise, and the institutional credibility to be the first name on the list when the stakes are highest.

The bull case is straightforward. Burckhardt is the toll bridge operator for the physical energy transition. Every molecule of hydrogen that gets compressed, every cargo of LNG that crosses an ocean, every ton of carbon dioxide that gets captured and stored—all require compression equipment, and Burckhardt sits at the nexus of supply. The installed base grows every year, generating more recurring service revenue, which funds more acquisitions, which expands the installed base further. The management team has skin in the game, the balance sheet is conservatively managed, and the return metrics—a RONOA exceeding thirty percent, a return on equity above thirty percent—place Burckhardt in the top tier of European industrials.

The bear case is equally worth examining. The Systems division remains cyclical, and a prolonged downturn in energy capital expenditure would compress order intake and margins. The hydrogen economy's timeline is uncertain—government subsidies may be delayed, infrastructure buildout may proceed more slowly than optimists project, and the forty-percent energy transition revenue target by 2027 may prove optimistic. Geopolitical risk in China, where Shenyang Yuanda operates, introduces a tail risk that is difficult to quantify but impossible to ignore. And the share price, which reached a fifty-two-week high of 738 Swiss francs before declining to approximately 520 by early April 2026, suggests that the market is already wrestling with these concerns.

There is also the competitive question. Neuman and Esser, a formidable German competitor, is privately held and therefore unconstrained by public market expectations—a potential advantage in patience-intensive markets. Baker Hughes and Atlas Copco, while less focused on high-pressure reciprocating compressors, have the balance sheets to invest heavily in adjacent technologies if the hydrogen opportunity proves large enough to attract their attention.

But step back from the quarterly noise and the share price fluctuations, and what you see at Burckhardt Compression is something increasingly rare in public markets: a company with a product that the world physically cannot do without, a business model that converts one-time equipment sales into decades of recurring revenue, a management team aligned with shareholders through substantial personal ownership, and a strategic position that benefits from secular trends—LNG trade, hydrogen infrastructure, carbon capture—that will play out over not quarters but decades. The machines Franz Burckhardt first built in Basel in 1844 have been superseded many times over in engineering sophistication. But the fundamental proposition—compressing gas reliably at extreme pressures—has never been more relevant than it is today. Old world engineering, modern capital allocation, and a future that runs on compressed molecules. That is Burckhardt Compression.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube