Bayer: The Aspirin, The Agony, and The Ultimate Turnaround Bet

I. Introduction & Episode Roadmap

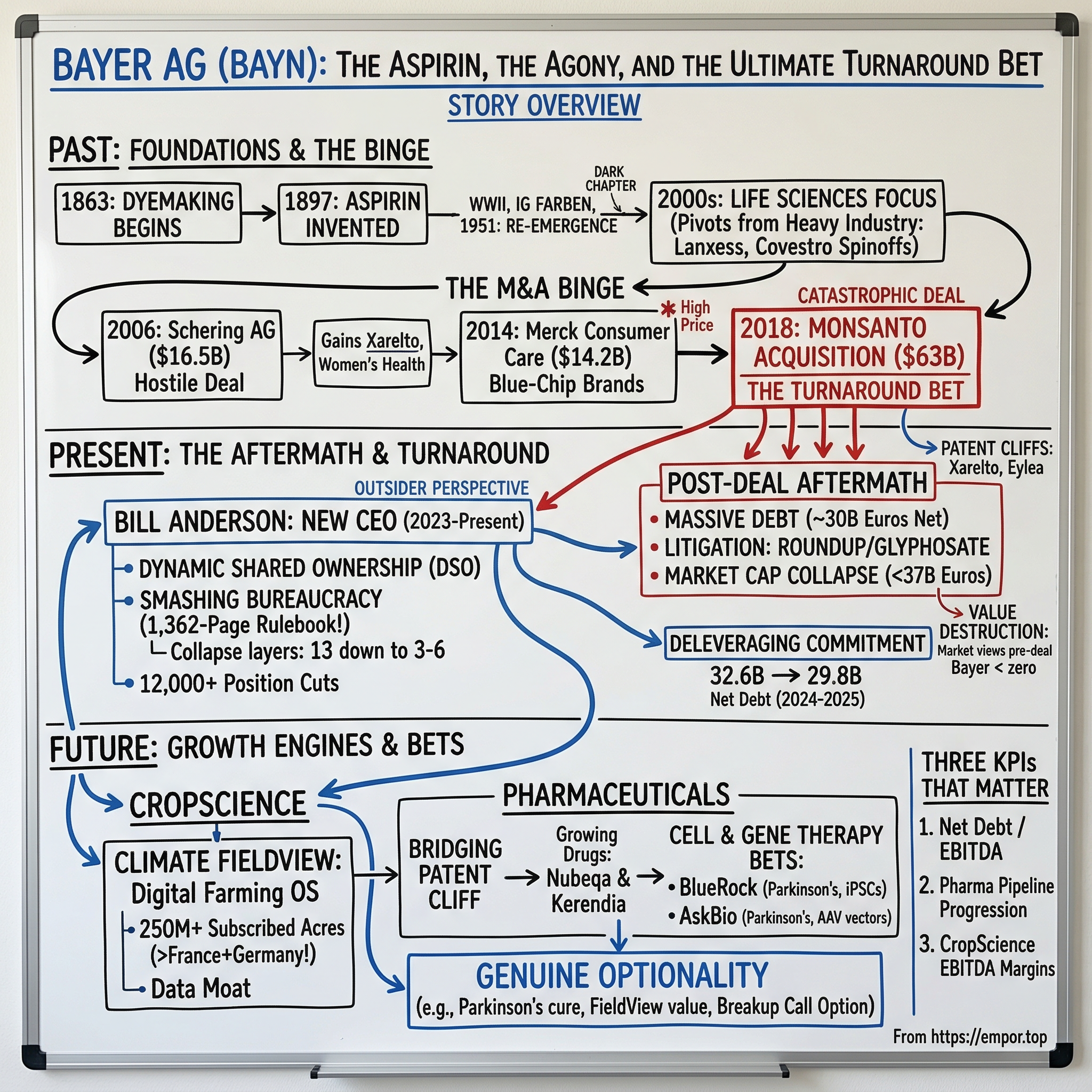

Picture a boardroom in Leverkusen, Germany. The year is 2018. The champagne has barely gone flat from closing the largest all-cash corporate takeover in history. Bayer AG—the 155-year-old colossus that literally invented Aspirin—has just swallowed Monsanto whole for $63 billion. The PowerPoint slides promise transformational synergies, global agricultural dominance, and a new era for the company. Werner Baumann, the CEO who bet the farm (quite literally), tells shareholders this is the deal that will define Bayer for the next century.

He was right about that last part. Just not in the way he imagined.

Fast forward to early 2026. Bayer's market capitalization hovers around 37 billion euros. Read that number again. They paid more for a single acquisition than the entire company is now worth—including the acquisition itself. The public markets have performed a brutal piece of arithmetic: take everything Bayer owned before the Monsanto deal—the pharmaceutical division generating tens of billions in revenue, the consumer health brands sitting in hundreds of millions of medicine cabinets worldwide, 163 years of institutional knowledge, global manufacturing infrastructure, one of the most recognized corporate logos on the planet—and assigned it all a value of less than zero.

That is not a rounding error. That is the market telling you that the liabilities Bayer acquired when it bought Monsanto are worth more than everything else the company owns, combined. It is arguably the most dramatic case of corporate value destruction since AOL merged with Time Warner.

But here is what makes the Bayer story more than a cautionary tale about bad M&A. Underneath the rubble of litigation settlements, crushed shareholder dreams, and a balance sheet groaning under nearly 30 billion euros of net debt, something genuinely interesting is happening.

A rare American outsider—Bill Anderson, the former CEO of Roche's pharmaceutical division—has taken the helm of this most German of institutions. He is systematically dismantling one of the most bureaucratic corporate structures in Europe. He is betting that the same company the market has left for dead contains hidden treasures: a dominant digital farming platform covering more acres than France and Germany combined, a cutting-edge cell and gene therapy pipeline chasing functional cures for Parkinson's disease, and a consumer health portfolio that throws off cash with the reliability of a municipal water utility.

So here is the real question—the one worth spending the next several thousand words exploring: Is Bayer a dying conglomerate suffocated by debt and litigation, destined to be broken up and auctioned for parts? Or is this the ultimate distressed-value play—a generational buying opportunity camouflaged behind the most toxic corporate headline in Europe?

To find the answer, we need to go back to the beginning. Back to a small factory in the Wupper Valley, where two men discovered that the same chemistry that creates a beautiful dye can also create a revolutionary medicine. Then we sprint forward through world wars, forced corporate breakups, a deliberate pivot to life sciences, and a decade of increasingly aggressive deal-making that culminated in the most catastrophic acquisition in modern European corporate history. And finally, we land in the present, where a turnaround CEO is attempting something that has almost never been done: reinventing a 163-year-old German institution from the inside out, while simultaneously fighting a multi-front war against litigation, patent cliffs, and a debt mountain.

This is the story of Bayer. And it is far from over.

II. From Dyes to Drugs: A Succinct History (1863–2000s)

In 1863, in the industrial town of Barmen in Germany's Wupper Valley, a dye salesman named Friedrich Bayer and a master dyer named Johann Friedrich Weskott scraped together their savings and opened a small factory. The Wupper Valley in those days was the Silicon Valley of nineteenth-century chemistry—a dense cluster of competitive, innovative firms, all racing to unlock the commercial potential of synthetic dyes. The river that gave the valley its name reportedly ran a different color every day, depending on which factory upstream was dumping its chemical waste.

Their business plan was elemental: take coal tar—a foul, viscous, black byproduct of the coal-gas industry—and transform it through chemical manipulation into vivid synthetic dyes for the booming global textile trade. Natural dyes, extracted from plants and insects, were expensive, inconsistent, and limited in range. Synthetic dyes were cheap, infinitely reproducible, and available in colors nature had never imagined.

But the truly consequential discovery was not a color. It was a connection. The molecular manipulation required to create synthetic dyes turned out to be strikingly similar to the chemistry needed to create medicines. A dye molecule that binds selectively to a textile fiber is not, at a molecular level, fundamentally different from a drug molecule that binds selectively to a biological receptor. This insight—that the same science that could color a shirt could also cure a headache—was not obvious at the time, but it would become the foundational principle of the modern pharmaceutical industry. By the 1880s and 1890s, Bayer's chemists—the company was one of the first industrial firms anywhere to establish a dedicated research laboratory—were not just creating pigments. They were inventing pharmaceuticals.

In 1897, a young Bayer chemist named Felix Hoffmann synthesized a stable, pure form of acetylsalicylic acid. Willow bark extract, its natural precursor, had been used as a folk remedy for pain since the days of Hippocrates. But previous synthetic versions were harsh on the stomach and wildly inconsistent in potency. Hoffmann's breakthrough was purity and consistency. By 1899, Bayer was selling it under the trademark Aspirin. It became, quite possibly, the most successful consumer pharmaceutical product ever created—more than 125 years later, it remains one of the most widely used medications on the planet, so ubiquitous that in many countries the word itself ceased to be a brand name and became the generic term for the drug.

But the company's early pharmaceutical ambitions included a far darker chapter. One year before Aspirin launched, in 1898, Bayer trademarked another Hoffmann compound: diacetylmorphine. They called it Heroin—from the German "heroisch," meaning heroic—and marketed it aggressively as a non-addictive cough suppressant and, astonishingly, as a cure for morphine addiction. The claims proved catastrophically wrong. The product was quietly phased out by 1913, but not before contributing to one of the earliest modern drug epidemics.

Then came the darkest chapter of all. In 1925, Bayer was absorbed—along with BASF, Hoechst, and several smaller German chemical firms—into IG Farben, a massive conglomerate that would become synonymous with industrial complicity in the Nazi regime. IG Farben produced the Zyklon B gas used in the extermination camps. Its factories operated with an estimated 30,000 slave laborers at Auschwitz alone. After the war, thirteen IG Farben directors were convicted of war crimes at Nuremberg. The conglomerate was broken up by the Allies.

In 1951, Bayer re-emerged as an independent company. But the reputational damage lingered for decades, and the corporate penalty was tangible: Bayer lost the rights to use its own name and the iconic Bayer cross logo in the United States and many other markets. It would not regain those American trademark rights until 1994, when it paid Sterling Drug approximately $1 billion—a staggering sum just to reclaim its own identity.

The post-war decades transformed Bayer into a textbook German industrial conglomerate: profitable, globally respected, sprawling across polymers, specialty chemicals, agricultural products, consumer health, and prescription pharmaceuticals. The organizational culture was characteristically German—hierarchical, process-obsessed, consensus-driven, deeply risk-averse. Decisions percolated upward through layers of committees. Innovation happened, but slowly, carefully, and only with extensive sign-off from multiple stakeholders.

By the 1970s and 1980s, Bayer had evolved into a genuinely global enterprise with operations spanning every inhabited continent. Its product portfolio was staggering in its breadth: polyurethane foams for automotive interiors sat alongside prescription medications for cardiovascular disease, which sat alongside crop protection chemicals for Brazilian soybean farms, which sat alongside Alka-Seltzer tablets in American convenience stores. Its Leverkusen headquarters—a sprawling campus on the Rhine that includes its own hospital, fire department, and even a professional soccer team, Bayer 04 Leverkusen—became a symbol of the kind of paternalistic, cradle-to-grave German industrial enterprise that was both admired and increasingly viewed as anachronistic.

The conglomerate model had real advantages. Diversification smoothed earnings volatility. Internal capital markets allowed management to cross-subsidize R&D investments across divisions. The breadth of the company's scientific capabilities occasionally produced unexpected connections across disciplines. But it also carried a heavy cost: management attention was spread impossibly thin, strategic capital was allocated through political negotiation between division heads rather than through rigorous assessment of returns, and investors struggled to value a company that was simultaneously a pharmaceutical innovator, a chemical manufacturer, a consumer products company, and an agricultural supplier.

By the early 2000s, a new reality was asserting itself in global capital markets. The era of the diversified industrial conglomerate was ending. Investors wanted focus. They wanted to understand, clearly, what they were buying. Financial markets systematically punished companies that tried to do too many things at once with the so-called "conglomerate discount"—the persistent phenomenon where a diversified company's stock trades for less than the sum value of its individual businesses.

Bayer's leadership recognized this shift and made a strategic decision that would reshape the company's identity for the next two decades. They would shed the heavy industrial businesses and reinvent Bayer as a pure-play "Life Sciences" company—focused exclusively on pharmaceuticals, consumer health, and crop science.

In 2004, Bayer carved out its entire specialty chemicals division—rubber, basic chemicals, specialty plastics—into a new company called Lanxess, which began trading on the Frankfurt Stock Exchange in early 2005. Lanxess took with it roughly 19,000 employees, multiple manufacturing plants, and the commodity chemical businesses that had been weighing down Bayer's margins and confusing its equity story.

Eleven years later, in September 2015, Bayer completed the same surgical separation on its high-performance materials and plastics business, spinning it off as Covestro. Where Lanxess had been a relatively straightforward divestiture of commodity chemicals, Covestro was a more strategically significant move—it represented some of Bayer's highest-margin industrial operations, including world-leading positions in polycarbonate plastics and polyurethane precursors used in automotive, construction, and electronics applications. The IPO of Covestro on the Frankfurt exchange was well received, and the company grew into a multi-billion-euro market cap enterprise in its own right, validating the thesis that Bayer's industrial businesses were not underperformers—they were simply misunderstood inside a conglomerate structure.

The strategic logic was elegant. Strip away the cyclical, capital-intensive commodity businesses. Retain only the high-margin, science-driven divisions. Build a balanced three-legged stool: Pharmaceuticals would provide innovation-driven growth and premium margins. Consumer Health—anchored by iconic brands like Aspirin, Bepanthen, Alka-Seltzer, and Canesten—would deliver steady, recession-proof cash flows. And Crop Science would provide global scale plus exposure to the secular mega-trend of feeding a world headed toward nine billion people.

On paper, it was a brilliant strategy. On investor day slides, it was irresistible. But it created a dangerous void: Bayer was now committed to being world-class in three separate, fiercely competitive industries simultaneously. And candidly, it was arguably subscale in all three. The pharma pipeline lacked the depth of a Roche or Novartis. The consumer health business was dwarfed by Johnson & Johnson. The crop science division sat a distant fourth behind Monsanto, Syngenta, and Dow-DuPont.

For decades, the diversified conglomerate model had served the company well enough. But the new Life Sciences identity demanded a level of competitive intensity in each division that the old sprawling structure had never required. Being a respectable fourth in crop science was acceptable when you were also operating profitable plastics and chemicals businesses. Being a respectable fourth in crop science when that is one of only three things you do is an entirely different competitive proposition.

Management's solution was obvious: go shopping. What followed was a decade of deal-making that began brilliantly, escalated recklessly, and ended catastrophically.

III. The M&A Binge & Capital Deployment (2006–2016)

The newly focused Bayer had clarity of identity but a deficit of scale. And in the Life Sciences industries of the 2000s, scale was not just a competitive advantage—it was increasingly an existential requirement.

In pharmaceuticals, the cost of developing a single new drug had soared past $2 billion when you factored in the many failed compounds that never reached the market but still consumed years of research funding. Only companies with massive R&D budgets and diversified pipelines—dozens of drug candidates at various stages of development—could absorb the inevitable clinical trial failures without existential risk. In agriculture, the dynamics were equally brutal. The development timeline for a new genetically modified seed trait stretched to a decade or longer, at costs exceeding $1 billion per trait. And in consumer health, distribution leverage and brand marketing spend meant that the biggest players captured disproportionate shelf space and consumer mindshare.

Bayer's management looked at these dynamics and reached a conclusion that many European corporate boards reached in the same era: organic growth was too slow, too uncertain, and too incremental to close the gap against larger rivals. The fastest path to scale was acquisitions. The investment bankers were only too happy to agree.

Why not invest more in internal R&D? The answer reveals a structural bias in how large pharmaceutical companies allocate capital. Internal drug development is a decade-long commitment with a roughly 90 percent failure rate: for every ten compounds that enter human clinical trials, only one or two will ever receive regulatory approval and reach the market. The other eight or nine represent billions of dollars in sunk costs that generate zero commercial return. An acquisition, by contrast, allows the buyer to purchase proven assets—drugs already on the market, or late-stage candidates with substantial clinical data—thereby compressing a decade of risk into a single transaction. The trade-off, of course, is price: you pay a premium for certainty. And the premiums kept getting larger.

The first major deal was bold, and by any fair measure, it was excellent.

In 2006, Bayer launched an unsolicited bid for Schering AG, the venerable Berlin-based pharmaceutical company. Schering was a prize—a leader in women's healthcare with a dominant franchise in oral contraceptives and hormone therapies, plus a growing presence in specialty areas like multiple sclerosis, diagnostic imaging, and early-stage oncology research.

The complication was that Merck KGaA, a rival German pharma company, had already made a friendly approach to Schering's board. A gentlemanly transaction was in progress. Bayer crashed the engagement party with a hostile counter-bid of 86 euros per share, valuing Schering at approximately 16.5 billion euros. In the polite, consensus-driven world of German corporate M&A—where hostile bids were considered deeply gauche—this was the equivalent of overturning the dinner table.

But it worked. Merck KGaA was financially outgunned and retreated. Bayer absorbed Schering and, in doing so, gained not just the women's health franchise but also a research pipeline that contained what would become one of the most important drugs in the company's history.

That drug was rivaroxaban, commercially branded as Xarelto—a novel oral anticoagulant, or blood thinner, that Bayer would later co-market with Johnson & Johnson. To understand why Xarelto was so valuable, consider the market it addressed. For decades, the standard blood-thinning medication was warfarin, a drug originally developed as rat poison and notoriously difficult to manage—patients needed frequent blood tests, faced dangerous food interactions, and required constant dose adjustments. Xarelto offered a dramatically simpler alternative: a once-daily pill with predictable dosing and no dietary restrictions. It went on to become one of the best-selling pharmaceuticals on earth, generating peak annual global revenues exceeding five billion euros and establishing itself as a standard-of-care treatment for patients at risk of stroke from atrial fibrillation and those with deep vein thrombosis.

In retrospect, the Schering acquisition was a textbook case of excellent strategic M&A. Bayer paid a full price, but the asset it acquired produced a single drug—Xarelto—whose cumulative lifetime revenues far exceeded the total purchase price. If this were a venture capital portfolio, Schering would be the deal that returned the entire fund several times over.

But here is where the narrative takes a dangerous turn. Success in M&A is intoxicating. It validates the deal-makers. It silences the skeptics. And it creates a dangerous institutional muscle memory—a reflex where the boardroom's first response to any strategic gap is to reach for the checkbook rather than the research budget. Why spend a decade and billions of dollars on uncertain R&D when you can simply acquire a company that has already done the hard work?

That logic is seductive. It is also, over a long enough time horizon, almost always destructive. Because each deal requires more debt, and debt is unforgiving—it demands repayment regardless of whether the acquisition delivers on its promises. Each deal raises the bar for what the next deal must achieve, because the cumulative leverage means the company can tolerate fewer mistakes. And each deal reinforces a culture where acquisition-making is the primary expression of strategic leadership, while the quieter, less glamorous work of internal innovation—the laborious, uncertain, decade-long process of building new drugs, new seed traits, and new platforms from scratch—withers from institutional neglect and starved budgets.

In 2014, the pattern repeated. Bayer agreed to acquire Merck & Co.'s consumer care business for $14.2 billion. The portfolio was blue-chip: Claritin, America's leading allergy medication. Coppertone, the nation's most recognized sunscreen brand. Dr. Scholl's foot care products. MiraLAX, the top-selling over-the-counter laxative. Afrin nasal spray. These were recession-resistant consumer brands with deep consumer loyalty and predictable cash flow profiles.

The problem was the price. At approximately 21 times EBITDA, Bayer paid an eye-watering premium—even by the inflated standards of the mid-2010s consumer health M&A boom, when every large pharma company seemed to be scrambling to build consumer-facing revenue streams as prescription drug pricing came under increasing political fire.

For context, consider that when Reckitt Benckiser acquired Mead Johnson Nutrition three years later, in 2017, it paid roughly 19 times EBITDA and was loudly criticized by analysts and shareholders for dramatically overpaying. Bayer had set the high-water mark for consumer health valuations well before that—and at the time, remarkably few voices questioned whether paying 21 times trailing earnings for a basket of cough-medicine and sunscreen brands was a rational use of shareholder capital. It marked the beginning of a dangerous pattern: the institutional confidence that premium prices could always be justified by "strategic value" and that debt taken on to fund acquisitions would be easily serviced by the acquired cash flows.

Neither the Schering deal nor the Merck Consumer Care acquisition was individually ruinous. Schering was a home run. The consumer brands, while purchased at an aggressive valuation, remain solid, cash-generative assets. The danger was never in any single transaction. It was in the pattern—the institutional habit of reaching for acquisitions as the primary growth engine, each one funded with more debt, each one requiring the next deal to be even bigger and more transformative to justify the cumulative leverage.

By 2016, Bayer's management had become convinced that the next deal—the really big one, the transformational play that would catapult them to global leadership in crop science—was not just strategically desirable. It was existentially necessary.

And so they turned their sights to the most controversial, most polarizing, and most consequential target in global agriculture: Monsanto.

IV. The Monsanto Acquisition: A Value Destruction Masterclass (2018)

To understand why Bayer bought Monsanto, you must first understand the tidal wave of consolidation that engulfed the global agricultural industry in the mid-2010s. It happened with a speed and scale that reshaped the entire competitive landscape in under two years—and it terrified every management team in the sector.

In December 2015, Dow Chemical and DuPont—two pillars of American industrial history—announced a blockbuster merger valued at over $130 billion. The combined entity would eventually split into three independent companies, one of which, Corteva Agriscience, would emerge as a dedicated agricultural powerhouse. Just two months later, in February 2016, China National Chemical Corporation—ChemChina—launched a $43 billion takeover bid for Syngenta, the Swiss agrochemical giant. The deal represented a dramatic strategic play by the Chinese state: acquire Western agricultural technology and secure a stronger position in the global food supply chain.

In the span of a few months, an industry that had been structured around six major global players for decades was violently consolidating into four. And Bayer, watching these dominoes fall from its Leverkusen headquarters, knew that its Crop Science division—competent, profitable, and clearly subscale—could not survive long-term in fourth place.

The economics of modern agricultural biotechnology are merciless. Developing a single new seed trait—say, drought tolerance in corn or resistance to a specific insect pest in soybeans—requires roughly a decade of discovery research, followed by years of multi-country field trials, followed by regulatory submissions to authorities in dozens of jurisdictions around the world. The all-in cost per trait routinely exceeds $1 billion. These are the kinds of fixed costs that only massive scale can absorb. If you cannot amortize a billion-dollar R&D program across hundreds of millions of planted acres, the math simply does not work.

Werner Baumann, who assumed the Bayer CEO role in May 2016, made the Monsanto acquisition the defining project of his tenure. Baumann was the opposite of a risk-taker by temperament—a Bayer lifer who had joined the company in 1988, risen methodically through the finance and strategy ranks, and embodied the cautious, deliberate management culture of the German corporate establishment. But his first major strategic move was anything but cautious.

In May 2016—the very month he took office—Bayer made an unsolicited approach to Monsanto at $122 per share. Hugh Grant, Monsanto's Scottish-born CEO who had built the company into the world's dominant force in seeds and agricultural biotechnology, rejected the bid as inadequate. But crucially, he did not slam the door shut.

What followed was a protracted, high-stakes negotiation that played out across the financial press throughout the summer and fall of 2016. Bayer raised its offer repeatedly—from $122 to $125 to $127.50—each increase adding billions to the total deal value and further eroding the financial cushion that was supposed to protect shareholders if things went wrong.

The final agreed price, announced in September 2016, was $128 per share. That represented a staggering 44 percent premium over Monsanto's pre-approach trading price of approximately $89. The total transaction value: roughly $63 billion. All cash. No stock component, no earnouts, no contingency mechanisms, no risk-sharing of any kind. Bayer assumed 100 percent of the financial risk.

The all-cash structure deserves special emphasis. In most large M&A transactions, the acquiring company uses a combination of cash and stock. The stock component serves a dual purpose: it reduces the acquirer's debt burden, and—critically—it aligns the target company's shareholders with the combined entity's future performance. By choosing to pay entirely in cash, Bayer was signaling maximum confidence—but also assuming maximum risk. If anything went wrong, Bayer's shareholders would bear the entirety of the financial consequences. Monsanto's shareholders would be long gone, cashed out at $128 per share.

In retrospect, the all-cash structure looks less like confidence and more like the kind of overcommitment that behavioral economists call the "sunk cost escalation trap." Having publicly committed to the deal, invested months of management time and reputational capital, and staked Baumann's newly begun CEO tenure on the transaction's success, walking away felt psychologically impossible—even as the price kept rising and the risk profile kept deteriorating.

Wall Street analysts published increasingly alarmed notes questioning whether Bayer was suffering from "winner's curse"—the well-documented tendency of the winning bidder in any auction to overpay precisely because they were the most optimistic participant. Environmental advocacy groups mounted public campaigns opposing the merger, warning that the combination of the world's largest seed company with a major chemical manufacturer would create a dangerous concentration of power over the global food supply. Monsanto's own shareholders—many of whom had endured years of reputational controversies around GMOs and aggressive patent enforcement against family farmers—saw the Bayer bid as a golden exit: take the premium, cash out, and let someone else manage the gathering storm.

To finance the deal, Bayer took on an ocean of new debt that pushed the company's leverage ratio to levels that made even the most deal-friendly analysts uncomfortable. The transaction required antitrust approval from over 30 regulatory jurisdictions and took nearly two years to close, finally completing on June 7, 2018. As a condition of regulatory clearance, Bayer was forced to divest approximately $9 billion of crop science assets to BASF—a painful concession that directly reduced the synergies supposed to justify the deal's enormous premium.

The strategic logic of the combination was not insane—and this is an important nuance that often gets lost in the understandable fury over what happened next. Monsanto possessed something genuinely irreplaceable: the world's most comprehensive proprietary germplasm library—the vast, painstakingly assembled collection of plant genetic material from which breeders develop new seed varieties with improved traits. Monsanto's library, accumulated over decades of research investment totaling tens of billions of dollars, contained genetic blueprints for corn, soybean, cotton, and vegetable varieties that would take any competitor a generation to replicate from scratch.

Combining this biological engine with Bayer's strength in chemical crop protection—herbicides, fungicides, insecticides—would, in theory, create the world's most integrated agricultural company, capable of offering farmers a complete solution from seed genetics through chemical protection to harvest optimization. Think of it as an agricultural "full stack"—owning the entire value chain from the DNA inside the seed to the chemical shield protecting the crop above ground. The synergy estimates, while aggressive, were grounded in real operational logic: a farmer who buys Bayer seeds engineered to work optimally with Bayer herbicides is a farmer locked into the Bayer ecosystem, generating recurring revenue year after year.

But Monsanto came with a shadow. A massive, glaring, neon-red shadow that Bayer's board either catastrophically underestimated or willfully ignored.

To understand the magnitude of the risk, you first need to understand Roundup and how thoroughly it had rewired modern agriculture. Glyphosate, the active ingredient, was discovered by Monsanto chemist John Franz in 1970 and commercialized as a herbicide in 1974. It became the most widely used agricultural chemical in human history—applied to hundreds of millions of acres annually, sprayed on lawns and gardens by homeowners, and deployed by municipal workers in schoolyards and public parks. But it was the introduction of Monsanto's "Roundup Ready" genetically modified crops—seeds engineered to tolerate glyphosate, allowing farmers to spray their entire fields to kill weeds without harming the crop—that fundamentally transformed global farming practice. By the time of the Bayer deal, cumulative global glyphosate usage was measured in the billions of gallons. Roundup was not just Monsanto's biggest product; it was the backbone of modern agriculture.

By the time Bayer made its initial approach in 2016, the litigation risk surrounding Roundup was not hidden. It was hiding in plain sight. In March 2015, a full year before Bayer's first bid, the International Agency for Research on Cancer (IARC), a specialized arm of the World Health Organization, had classified glyphosate as "probably carcinogenic to humans." Other regulatory bodies reached different conclusions—the U.S. EPA, the European Food Safety Authority, and Health Canada all found no clear evidence of a cancer link—and the scientific debate remains genuinely contested to this day.

But scientific nuance matters little in an American courtroom. What matters is how a jury feels about the plaintiff versus the defendant. And Monsanto, as a trial defendant, was a catastrophe waiting to happen. Internal company emails, which emerged during legal discovery, suggested that Monsanto had ghostwritten scientific studies favorable to glyphosate's safety and attacked independent researchers who raised concerns.

Bayer's German corporate lawyers, trained in the more predictable European legal tradition—where class actions are rare, punitive damages are virtually nonexistent, and judges rather than juries decide most cases—made a fatal error of legal and cultural imagination. They modeled the glyphosate litigation as a manageable, bounded risk. They ran their probability models and concluded that the exposure was containable. They failed to grasp, at a visceral level, how powerfully the combination of a sympathetic plaintiff, an unsympathetic corporate defendant, damaging internal emails, and the emotional dynamics of an American jury could produce outcomes utterly disconnected from the underlying scientific evidence. The American tort system is not a rational probability machine. It is a human drama, adjudicated by twelve citizens who are asked to decide who deserves sympathy and who deserves punishment. Monsanto, with its corporate arrogance, its ghostwritten studies, and its decades of antagonizing farmers and environmental activists, was perfectly engineered to lose in that theater.

The first verdict arrived on August 10, 2018—less than 65 days after the deal closed. A California state jury awarded Dewayne Johnson, a former school groundskeeper diagnosed with terminal non-Hodgkin lymphoma who had regularly mixed and applied Roundup, $289 million in damages, including $250 million in punitive damages. Johnson was dying. He wept on the witness stand. The jury sided with the groundskeeper in just two-and-a-half days of deliberation.

The award was later reduced to $78 million on appeal. But the symbolic and financial damage to Bayer was instantaneous and devastating. Within days, Bayer's market capitalization dropped by more than 10 billion euros. The stock would never recover.

And the legal floodgates—the very thing that Bayer's due diligence had dismissed as manageable—blew wide open. Plaintiff attorney firms across the United States launched massive advertising campaigns, recruiting new clients through television ads, social media, and direct mail. The message was simple and emotionally powerful: if you used Roundup and developed cancer, you might be entitled to compensation. The pipeline of new cases swelled from thousands to tens of thousands, then to tens of thousands more.

The verdicts kept coming. In March 2019, a federal jury awarded plaintiff Edwin Hardeman $80 million. In May 2019, a state court jury awarded the Pilliod couple $2.055 billion, at the time one of the largest product liability verdicts in U.S. history. In March 2025, a Georgia jury awarded $2.1 billion in the Barnes case. While appellate courts consistently reduced the headline punitive damage numbers, each verdict triggered a fresh wave of plaintiffs and a fresh plunge in Bayer's stock price. At its peak, the litigation docket swelled to over 100,000 pending claims.

In June 2020, Bayer announced a comprehensive settlement framework worth approximately $10.9 billion to resolve the majority of existing claims. It was among the largest product liability settlements in American legal history—comparable in scale to the tobacco settlements of the 1990s. But the litigation proved unkillable.

New cases continued to be filed. Plaintiff attorney marketing campaigns recruited new clients. And even as Bayer paid out billions in settlements, the total number of pending claims remained stubbornly high, with approximately 65,000 outstanding as of late 2025. Bayer's litigation provisions ballooned to 11.8 billion euros, including 9.6 billion specifically for glyphosate-related claims.

In February 2026, Monsanto announced a proposed nationwide class settlement of up to $7.25 billion, to be paid over up to 21 years, designed to resolve both current and future claims in a single comprehensive framework. A U.S. judge granted preliminary approval on March 4, 2026. But even this massive settlement faces opposition—fourteen law firms representing nearly 20,000 plaintiffs asked the court to delay proceedings, arguing that key provisions raise fairness concerns and that the timeline is too compressed.

There is one potential lifeline. On January 16, 2026, the U.S. Supreme Court agreed to hear the Durnell v. Monsanto case, which centers on whether federal pesticide labeling law preempts state failure-to-warn claims. Oral arguments are scheduled for April 2026, with a decision expected by June. The Trump administration filed a brief supporting Bayer's position. A favorable ruling on federal preemption could effectively end most Roundup litigation. A negative one could extend it for another decade.

Here is the number that sears itself into the memory. Bayer's market capitalization peaked above 120 billion euros in mid-2015. By early 2026, it had collapsed to approximately 37 billion euros—a loss of roughly 83 billion euros in shareholder value. The stock, which traded near its all-time highs in the months before the Monsanto announcement, hit a 52-week low of approximately 18 euros per share during its worst stretch. They paid approximately 57 billion euros for Monsanto alone. Add the $9 billion in mandated divestitures, the cumulative litigation costs that have already exceeded $11 billion in actual settlements and damage payments, and the all-in cost of the Monsanto deal rivals or exceeds Bayer's entire current enterprise value.

The market assigned a negative value to everything Bayer owned before the deal. Every pharmaceutical compound. Every consumer brand. Every factory. Every patent. Every employee. All of it, in the market's cold arithmetic, was worth less than nothing once the Monsanto liability was factored in. It is the kind of calculation that, once you see it, you cannot unsee—and it haunts every conversation about Bayer's future.

The deal is now routinely mentioned alongside AOL-Time Warner, Daimler-Chrysler, and Bank of America-Countrywide as one of the most value-destructive corporate acquisitions in modern business history. But unlike those transactions, which involved fundamentally flawed business combinations, the underlying Monsanto agricultural assets were—and remain—genuinely excellent businesses. The destruction came not from the assets themselves, but from the liabilities that traveled alongside them. It is a distinction that matters enormously for understanding Bayer's future potential.

Werner Baumann, the architect of the deal, eventually lost his job—but not before serving as CEO through 2023, nearly five years after the acquisition closed. In the German corporate governance system, where management board contracts typically run for five-year terms and the Supervisory Board must formally vote not to renew, removing an underperforming CEO is a far more cumbersome process than in the American boardroom.

But a CEO change, however overdue, could not undo what had been done. The balance sheet was structurally impaired. The company's strategic flexibility—its ability to invest in R&D, pursue opportunistic acquisitions, or return capital to shareholders—was severely curtailed by debt service obligations. And decades of accumulated shareholder trust, painstakingly built over generations of dividend payments and steady earnings growth, had been shattered in under five years. The German retail investors who had held Bayer stock as a blue-chip bedrock holding—the way American retirees hold shares of Johnson & Johnson or Procter & Gamble—watched their position lose two-thirds of its value and their dividend get slashed. That kind of trust, once broken, takes a generation to rebuild.

V. "Hidden" Businesses & Future Growth Engines

Now comes the pivot in the narrative—from postmortem to prospectus. Because the crucial question for anyone analyzing Bayer today is not "how did they get here?" The question that matters is entirely different: what does Bayer actually own, what is it worth, and can any of it justify the current enterprise value—or suggest that the market has overcorrected?

When you conduct a cold-eyed inventory of the assets inside the portfolio, looking past the headlines—past the litigation, past the debt, past the stock chart—the answer is, perhaps surprisingly, yes. Buried beneath the overhang sit several businesses that, in any other corporate wrapper, would command genuinely premium valuations.

Start with Climate FieldView. This might be the single most underappreciated technology asset hiding inside any European conglomerate.

FieldView is, in simplest terms, the operating system for modern farming. It is a data-driven digital agriculture platform that Bayer acquired as part of the Monsanto deal. Monsanto itself had purchased the platform's predecessor—a startup called the Climate Corporation—back in 2013 for approximately $930 million, at the time considered a wildly aggressive price for a data analytics company with minimal revenue.

Here is how it works, in plain language. A modern commercial farm is essentially an enormous outdoor factory. The production line is thousands of acres of soil. The raw materials are seeds, fertilizer, water, and sunlight. The finished product is a harvest. And like any factory, the difference between mediocrity and excellence comes down to the precision and quality of the data driving decisions.

FieldView integrates information from a dizzying range of sources: satellite and aerial imagery, proprietary weather models, soil composition readings from in-ground sensors, planting density data from GPS-enabled seeding equipment, input application records for fertilizer and crop protection chemicals, and real-time yield measurements from optical sensors mounted on combine harvesters. All of this data feeds into machine-learning algorithms that produce field-level prescriptions—essentially, customized instructions telling a farmer exactly which seed variety to plant in which specific section of which field, how much fertilizer to apply at each point, and when to spray for disease or pests.

Before platforms like FieldView, these decisions were made through a combination of the farmer's hard-won experience and gut instinct. FieldView enables what the industry calls "variable rate" management—precision adjustments at the sub-field level that can boost yields while simultaneously reducing input costs and environmental impact.

As of late 2024, FieldView operates on more than 250 million subscribed acres across 23 countries. To put that scale in context, 250 million acres is roughly equal to the entire combined agricultural area of France and Germany. No competitor is remotely close to this footprint. The platform's moat is a textbook data network effect—the same dynamic that powers Google's search dominance. Each additional farmer generates more data. More data improves the algorithms' predictive accuracy. Better predictions attract more farmers. Every passing growing season compounds the advantage, making the dataset progressively harder for any competitor to replicate.

The platform also creates formidable switching costs. Once a farm operation has uploaded years of field-level records into FieldView—planting histories, yield maps across multiple seasons, soil composition profiles, multi-year weather correlations—the cost of abandoning the platform is the destruction of an irreplaceable institutional memory of the land itself. It is the agricultural equivalent of a Fortune 500 company trying to rip out Salesforce after a decade of accumulated customer records and customized workflows.

The business model is also structurally attractive in ways that the rest of Bayer's portfolio is not. Unlike seeds, which are a seasonal commodity purchase subject to weather and crop-price cycles, and unlike crop protection chemicals, which face generic competition as patents expire, a digital platform generates recurring subscription-like revenue with minimal marginal cost per additional acre. The incremental economics—adding another farmer to the platform—are essentially software economics: near-zero variable cost, high contribution margin, and increasing returns to scale. Competitors exist, but none approaches FieldView's scale. Corteva has its Granular platform. CNH Industrial offers precision agriculture hardware. John Deere has invested heavily in its own data ecosystem. But none has anything close to the 250-million-acre dataset that gives FieldView its algorithmic advantage.

And yet this sticky, high-margin, data-moated software business is effectively invisible to the equity market. It is consolidated into the broader Crop Science reporting segment alongside commodity herbicide sales and cyclical seed revenues. The market assigns it no discernible standalone value. When analysts build sum-of-the-parts models for Bayer, FieldView barely gets a footnote.

Then there is Bayer's ambitious, high-stakes bet on the next frontier of medicine: cell and gene therapy.

Bayer's pharmaceutical leadership recognized that the company had largely missed the first great wave of biotechnology—the monoclonal antibody revolution that produced blockbusters like Humira, Keytruda, and Opdivo. Rather than trying to play catch-up in a race already decided, Bayer chose to leapfrog—to bet on the next wave of medical innovation, one that promises not merely to treat chronic diseases but to functionally cure them by repairing the underlying genetic and cellular damage.

In 2019, Bayer acquired BlueRock Therapeutics for approximately $600 million, with additional milestone payments contingent on clinical progress. BlueRock was born from pioneering research at Memorial Sloan Kettering Cancer Center and the University of Toronto. Its technology platform centers on induced pluripotent stem cells—iPSCs.

To understand why this matters, consider what iPSCs actually are, because the concept is genuinely extraordinary. Take an ordinary adult cell—say, a skin cell from a patient's arm. Through a carefully controlled chemical process discovered by Nobel laureate Shinya Yamanaka in 2006, scientists can reprogram that adult cell backward in time, so to speak, reverting it to a state resembling an embryonic stem cell. In this state, the cell regains the extraordinary ability to develop into virtually any cell type in the human body—heart cells, liver cells, brain cells, anything. Scientists can then guide it forward again, coaxing it to become a specific, functional replacement cell. Need dopamine-producing neurons to replace those destroyed by Parkinson's disease? Grow them in the lab from reprogrammed cells and transplant them into the patient's brain. It is, in effect, biological manufacturing—growing replacement parts for the human body.

BlueRock's lead program, bemdaneprocel, has now advanced to Phase III clinical trials. The first patient was enrolled in the registrational exPDite-2 trial in September 2025, after Phase I data in 12 patients showed good tolerability with no serious drug-related adverse events at 24 months—and importantly, signs that the transplanted cells appeared to survive, integrate, and produce dopamine in patients' brains. The program carries both FDA Regenerative Medicine Advanced Therapy (RMAT) and Fast Track designations, which can meaningfully accelerate the regulatory timeline. If Phase III confirms these results at scale, it would represent not just a new drug but an entirely new category of medicine: a functional cure for a devastating neurodegenerative disease that currently has no disease-modifying treatment.

In 2020, Bayer followed up with the acquisition of AskBio, a gene therapy specialist based in Research Triangle Park, North Carolina, for approximately $2 billion upfront with up to $2 billion more in milestone payments. AskBio's technology uses adeno-associated virus (AAV) vectors as delivery vehicles for therapeutic genes. Think of it as a molecular postal service: scientists take a tiny, harmless virus—one that has been hollowed out so it can no longer replicate—and load it with a corrective gene that can fix a genetic defect inside a patient's cells. AskBio's lead Parkinson's program, AB-1005, entered Phase II trials with the first European participants randomized in September 2025.

In a milestone that went largely unnoticed amid the Roundup headlines, Bayer became the first company in history to simultaneously advance both a cell therapy (bemdaneprocel) and a gene therapy (AB-1005) against the same devastating disease—Parkinson's. BlueRock is also pursuing an iPSC-derived cell therapy (OpCT-001) for primary photoreceptor diseases, which received FDA Fast Track designation in February 2025 and began Phase I testing.

A crucial strategic detail: Bayer deliberately chose to keep both BlueRock and AskBio operationally independent. Rather than absorbing them into the Bayer pharmaceutical organization—with its twelve layers of management and its months-long committee approval cycles—the company maintained them as arm's-length subsidiaries with their own leadership, their own R&D cultures, and their own decision-making autonomy.

This was not altruism. It was hard-won wisdom. The history of large pharmaceutical companies acquiring innovative biotech startups and then suffocating them with corporate process is long and deeply depressing. Roche learned this lesson with Genentech. Pfizer learned it with several acquisitions that lost their innovative edge post-integration. Bayer's decision to preserve the independence of BlueRock and AskBio was an implicit acknowledgment that the entrepreneurial culture of a biotech startup is itself a strategic asset—perhaps the most valuable one—and that integrating these companies into Bayer's traditional structure would not add value. It would destroy the very thing that made them worth acquiring.

There is also a tantalizing theoretical synergy between Bayer's crop science and pharmaceutical divisions that management has occasionally highlighted but has yet to prove in practice. Both businesses increasingly depend on the same foundational sciences—genomics, computational biology, machine learning, and the engineering of biological systems. The algorithms that analyze how a genetic trait expresses itself across thousands of corn varieties are not, computationally, all that different from models predicting how a gene therapy vector will behave in human tissue.

The theoretical logic is compelling: Bayer generates more biological data across more organisms in more environmental conditions than virtually any other company on earth. Its agricultural data spans hundreds of millions of acres across multiple crop species and dozens of climatic zones. Its pharmaceutical data covers human biology from cardiovascular systems to neurological function. Could a unified AI platform, trained on both agricultural and human biological datasets, identify drug targets faster or optimize gene therapy delivery more effectively? It is the kind of cross-divisional synergy that justifies keeping an integrated Life Sciences company together rather than breaking it apart—if it works. So far, concrete commercial results remain elusive. But the theoretical optionality is real, and it is unique to Bayer's combined structure.

None of these hidden businesses solve the near-term problems. FieldView alone cannot service nearly 30 billion euros in debt. The cell and gene therapy bets are years from commercial payoff—if they ever pay off at all. Drug development failure rates are sobering: historically, only about 10 to 15 percent of drugs that enter clinical trials ultimately receive regulatory approval. Novel therapeutic modalities like cell and gene therapy, which push into uncharted biological territory, may face even steeper odds.

But these assets represent something essential to the investment thesis: genuine optionality. In the language of financial options theory, they are out-of-the-money call options on the future. They cost relatively little to maintain—the acquisitions have already been made and the capital deployed—but their potential payoff in a success scenario is transformative. A single approved cell therapy for Parkinson's disease could generate peak annual revenues that would materially alter Bayer's pharmaceutical trajectory. FieldView, properly valued as a standalone data platform, could be worth a meaningful fraction of Bayer's current market capitalization all by itself.

The question—the multi-billion-dollar question—is whether the corporate structure and the balance sheet will allow these hidden businesses to reach their potential, or whether they will remain permanently trapped inside a conglomerate that the market has decided to value as nothing more than the sum of its problems.

VI. The New Era: Bill Anderson & The Turnaround (2023–Present)

By late 2022 and early 2023, Bayer's shareholder base had passed through every stage of grief—denial, anger, bargaining, depression—and arrived at something harder than acceptance: organized revolt.

The stock had lost roughly two-thirds of its peak value. The Roundup litigation showed no signs of final resolution. The pharmaceutical division faced an approaching patent cliff of fearsome proportions, as Xarelto and Eylea—the two blockbuster drugs that together represented the load-bearing pillars of pharmaceutical revenue—marched toward patent expiration. Werner Baumann, who had staked everything on Monsanto, had become a lightning rod for institutional fury.

The activist investors descended in waves. Bluebell Capital Partners, a London-based activist fund, began publicly demanding leadership change in early 2023, issuing detailed open letters to the Supervisory Board arguing that a separation of pharma and crop science could yield 70 percent or more upside. Jeff Ubben's Inclusive Capital Partners called for "speedy regime change." Elliott Management, Paul Singer's formidable New York-based hedge fund, reportedly took a position. Union Investment, one of Germany's largest domestic asset managers, publicly called for a change at the top.

The breadth of this coalition was unprecedented in recent German corporate history. German corporate governance, with its two-tier board structure, codetermination laws that give employee representatives half the Supervisory Board seats, and deeply ingrained cultural resistance to American-style activist campaigns, typically makes it extraordinarily difficult for outside shareholders to force management changes. The German system was designed, in part, to insulate management from short-term market pressures—to allow corporate leaders to think in decades, not quarters. But that same insulation can protect underperforming management long past the point where change is obviously necessary. That the activist coalition succeeded at Bayer—and succeeded relatively swiftly once momentum built—was a measure of just how completely the Monsanto deal had destroyed management credibility.

In February 2023, the dam broke. Bayer's Supervisory Board announced that Baumann's contract would not be renewed. His successor, effective June 1, 2023, sent an unmistakable signal that the era of insider continuity was over.

Bill Anderson was, in almost every conceivable way, the anti-Baumann.

Where Baumann had spent his entire 35-year career inside Bayer's walls, absorbing its hierarchical culture through osmosis, Anderson was a thoroughbred outsider—an American with zero prior connection to Bayer or, for that matter, to the German corporate establishment. His most recent role had been CEO of Roche Pharmaceuticals, the prescription drug division of the Swiss pharmaceutical giant—one of the most commercially successful drug businesses on the planet. At Roche, Anderson had overseen a portfolio of world-leading oncology and immunology drugs and earned a reputation for directness, speed, impatience with organizational bloat, and a willingness to confront entrenched interests head-on.

Critically, Anderson had done this inside a Swiss-German corporate structure, which gave him a rare understanding of how to reform culturally conservative European organizations without destroying the institutional strengths that made them valuable. He knew the terrain. He respected the people. He spoke the cultural language of European industrial management. But he had no loyalty to the bureaucratic traditions, no emotional attachment to the way things had always been done, and no political debts to the internal fiefdoms that had accumulated power over decades.

Anderson arrived with a diagnosis that was both disarmingly simple and profoundly unsettling to the company's old guard. Within his first weeks, he conducted what insiders described as an intensive listening tour—hundreds of one-on-one conversations with employees at every level. What he found was almost comically damning. He would later describe discovering a 1,362-page internal rulebook that all employees were supposed to follow. In another case, a top-20 senior executive had to personally sign off on a 52,000-euro contractor refund. As Anderson later put it: "The problem at Bayer is not the culture—it's the bureaucracy, it's the layers, it's the approvals. You can have all the positive culture you want, but if it takes five signatures to replace a pump in the plant, then the culture is not going to save you."

His assessment, which he communicated with characteristic bluntness to the Supervisory Board and later to the public, was that Bayer's core problems were not primarily strategic. The three business divisions—Crop Science, Pharmaceuticals, Consumer Health—were individually decent businesses with genuine competitive positions, real technological assets, and talented people. The problem was the organism itself—the operating system, so to speak, through which the company's talent and assets were organized and deployed.

Bayer, Anderson argued, had become so encrusted with bureaucratic layers, committee structures, and compliance processes that it had essentially paralyzed itself. A product manager who spotted a market opportunity and wanted to adjust a pricing strategy had to seek approval from as many as twelve layers of management spanning marketing, finance, legal, regulatory, compliance, regional, and global functions. A researcher with a promising pharmaceutical compound could wait six months or more for a steering committee to formally approve advancement to the next development phase—time during which a faster-moving competitor might race ahead.

The system had been built, layer by careful layer, to minimize risk and maximize procedural compliance. In a post-IG-Farben, post-thalidomide, heavily regulated industrial environment, that impulse was understandable. But in practice, it had produced an organization that was catastrophically slow, extravagantly expensive to operate, and institutionally incapable of the kind of agile decision-making that modern competitive markets demand.

Anderson's prescription was radical. He called it Dynamic Shared Ownership, or DSO, and rolled it out beginning in January 2024.

The concept borrows heavily from agile management philosophies—the small, autonomous product teams pioneered by companies like Spotify and Amazon—but adapted, ambitiously and controversially, for a 100,000-person industrial corporation operating in some of the most heavily regulated sectors on earth.

The core structural intervention was simple to describe and extraordinarily difficult to execute: collapse Bayer's organizational pyramid from as many as thirteen management layers down to as few as three in some units, with a target of five to six across most divisions. Eliminate the vast middle-management stratum that existed primarily to review, approve, and escalate decisions rather than to make them. Push decision-making authority downward to small, cross-functional teams of five to fifteen people, each with clear ownership of a specific product, market, or capability. Give these teams the autonomy to make most day-to-day decisions—pricing, resource allocation, development priorities—without running up the chain for approval.

The human cost has been immense, deliberate, and deeply controversial within Germany. Anderson's restructuring has eliminated over 12,000 positions—roughly half of all management roles—reducing Bayer's headcount to approximately 90,000. The cuts fell heavily on middle management: the layers of senior directors, vice presidents, and program managers who populated the approval pipeline. In the German corporate context, where employment stability is treated as nearly sacred and works councils wield powerful legal rights to negotiate layoff terms, executing workforce reductions of this magnitude was a politically and legally fraught undertaking.

The specifics of the cuts reveal Anderson's philosophy. He did not execute a traditional across-the-board headcount reduction—the kind of indiscriminate "salami-slicing" that large companies typically resort to in cost-cutting mode, where every division takes a uniform 10 percent haircut regardless of whether its people are redundant or essential. Instead, he targeted specific organizational layers: the coordinating managers, the portfolio oversight committees, the "chiefs of staff" roles, and the regional approval functions that existed primarily to aggregate information from the people doing the actual work and relay it upward to the people who made the actual decisions. In Anderson's framework, these layers did not add value—they added latency. Every management layer between a frontline team and a final decision was a delay measured in weeks or months that faster-moving competitors did not bear. The goal was not to make Bayer smaller. It was to make it faster.

The target: strip out more than two billion euros per year in structural overhead—not through temporary belt-tightening, but through the permanent removal of organizational complexity that should never have been built in the first place.

The cultural transformation Anderson is attempting runs far deeper than headcount reduction. He has described old Bayer as a culture of "compliance and permission," where employees were implicitly rewarded for following process meticulously and punished for exercising initiative that fell outside established procedures. DSO is designed to build the opposite: a culture of "action and ownership," where empowered teams are expected to make decisions quickly, take calculated risks, and be accountable for results rather than for adherence to procedure.

The debate over whether DSO can actually work at a company like Bayer is one of the most intellectually interesting arguments in global corporate management right now.

The skeptics—and they are numerous—contend that agile management philosophies developed for software companies cannot be transplanted into regulated industrial settings where process is not organizational overhead but legal necessity. A pharmaceutical clinical trial that cuts corners does not just fail commercially—it can kill patients and invite criminal prosecution. An agricultural product that skips a safety review can contaminate water supplies and trigger regulatory shutdowns. The margin for error in Life Sciences is categorically different from the margin for error in shipping a software update.

Anderson's defenders offer a devastating counter: the old system did not prevent catastrophic errors. Bayer bought Monsanto under the twelve-layer system. All those committees, all those approval gates, all that institutional caution—none of it flagged the litigation risk that would destroy more than 80 billion euros in shareholder value. The bureaucracy did not produce better decisions. It produced slower ones.

And in Anderson's view, organizational speed is itself a critical risk-management tool. In pharmaceuticals, getting a drug to market six months faster does not just mean earlier revenue—it means six additional months of patent-protected sales before generic competition arrives. In agriculture, launching a new seed trait one growing season earlier can mean capturing an entire year of farmer adoption that a slower competitor misses. Speed, properly channeled, is not the enemy of quality. It is the enabler of competitive advantage.

Anderson's personal financial alignment with shareholders warrants close attention. His total 2024 compensation was approximately 8.84 million euros, structured with heavy weighting toward performance-based incentives linked to relative Total Shareholder Return against European peer indices over multi-year measurement periods. This is a crucial design choice: Anderson does not cash in simply by cutting costs and boosting near-term EBITDA. The payout structure requires genuine, sustained stock outperformance relative to peers. Further, the company's Share Ownership Guidelines mandate that the CEO personally hold Bayer stock worth at least 200 percent of his base salary—millions of euros of personal wealth tied directly to the stock price.

Anderson also took a pay cut in 2024 as the company kicked off its restructuring—a symbolically important gesture in a German corporate culture that pays close attention to whether leadership is sharing the pain it imposes on the workforce.

In late 2025, Bayer's Supervisory Board rewarded Anderson with a three-year contract extension through March 2029—a nearly six-year runway that signals willingness to give the transformation time to produce results. And in April 2024, Jeff Ubben, the activist investor, formally joined the Supervisory Board itself. The activists are no longer lobbing demands from outside the gates. They are inside the governance structure, with direct oversight and a vote on strategy.

The financial picture beneath Anderson's restructuring tells the story of a company in transition—stabilizing but not yet growing. Full-year 2024 group sales came in at approximately 46.6 billion euros, roughly flat on a currency-adjusted basis. EBITDA before special items declined to approximately 10.1 billion euros, reflecting the early costs of the restructuring and continued pressure on glyphosate pricing. But free cash flow more than doubled to 3.1 billion euros—a critical signal that the cost-cutting was beginning to translate into actual cash generation. In 2025, revenues dipped slightly to approximately 45.6 billion euros as the patent cliff began to bite, EBITDA contracted further to 9.7 billion euros, and free cash flow pulled back to 2.1 billion euros amid heavier litigation payments and restructuring charges. The balance sheet, however, showed tangible improvement: net financial debt fell from 32.6 billion euros at year-end 2024 to 29.8 billion at year-end 2025—an 8.5 percent reduction that demonstrates Anderson's commitment to deleveraging even during a period of revenue pressure.

Meanwhile, the pharmaceutical division is navigating the very patent cliff that investors feared. Xarelto's U.S. patents expired in March 2024, with generic rivaroxaban approved in March 2025. Eylea's composition patent expired in June 2024, with biosimilar competitors entering the market. Combined, these two drugs generated over 6.5 billion euros at their peak. The revenue decline is painful and visible in the numbers—Xarelto revenue dropped from 4.1 billion euros in 2023 to 3.5 billion in 2024, with a further one to 1.5 billion euro decline expected in 2025.

But Anderson's team is not waiting passively. Two newer drugs are growing fast enough to partially offset the cliff. Nubeqa (darolutamide), a prostate cancer treatment, saw sales surge 75 percent to roughly 1.7 billion euros in 2024. Kerendia (finerenone), for chronic kidney disease, grew 72 percent. Together they reached approximately 2 billion euros in 2024, with projections exceeding 2.5 billion in 2025. And in November 2025, the FDA approved elinzanetant, branded as Lynkuet—the first nonhormonal therapy for menopausal vasomotor symptoms, commonly known as hot flashes—opening an entirely new market category for Bayer in women's health, a franchise that traces back to the Schering acquisition two decades earlier. Additionally, acoramidis, a treatment for a form of heart disease called ATTR cardiomyopathy, received a positive opinion from the European medicines regulator in late 2024. The pharma division does not project a return to overall growth until 2027, but the pipeline is no longer a void—it is a collection of meaningful, if individually smaller, growth stories that collectively need to bridge the enormous gap left by the twin blockbusters.

The question every analyst and journalist asks Anderson is the same: will you break up the company? His answer has been consistent and provocative. "Our answer is 'not now'—and this shouldn't be misunderstood as 'never,'" he said in March 2024. His position is that separating Bayer's divisions before the DSO transformation has taken hold would merely create two or three smaller broken companies—each inheriting its share of the dysfunctional culture and none possessing the critical mass to execute meaningful reform independently. Fix the operating model. Repair the balance sheet. Build the muscle memory of agile decision-making. Then evaluate structural options from a position of strength.

It is a coherent strategy, and there is historical precedent for it: Danaher, the American industrial conglomerate widely regarded as the gold standard of operational transformation, famously spent years implementing the Danaher Business System across its portfolio before executing a series of spinoffs that unlocked enormous value. But Danaher had a clean balance sheet and growing earnings during its transformation. Bayer has neither. The comparison is aspirational, not analogous.

Anderson's approach demands patience from a shareholder base that has been patient for a very, very long time—and has nothing to show for it but a stock chart that looks like a ski slope and a dividend that has been cut to a fraction of its former self. Whether that patience holds through two more years of revenue headwinds, litigation uncertainty, and organizational disruption may be the most important variable in the entire Bayer story.

VII. Playbook: Business & Investing Lessons

Step back from the narrative for a moment and consider what Bayer's saga teaches us at a structural level—not just about one company's mistakes, but about recurring patterns in corporate strategy, capital allocation, and competitive positioning that appear again and again across industries and eras.

The Bayer story offers a rich, cautionary, and occasionally illuminating set of lessons for investors and corporate strategists alike. The clearest lens through which to extract them is the dual framework of competitive moat analysis and capital allocation discipline.

Begin with Hamilton Helmer's Seven Powers, the framework that asks a deceptively simple question: what gives a business durable pricing power that competitors cannot erode? For each of Bayer's three divisions, the answer is different—and the differences explain both the company's strengths and its vulnerabilities.

Bayer's most formidable structural power is Scale Economies in Crop Science. Developing a new genetically engineered seed trait requires roughly a decade of laboratory research, greenhouse trials, multi-year field testing across dozens of climatic zones, and regulatory submissions to dozens of national agencies. The fully loaded cost frequently exceeds $1 billion per trait. Only four companies on the planet possess the resources and infrastructure to compete: Bayer (via the legacy Monsanto germplasm), Corteva Agriscience, Syngenta, and BASF. The barriers to entry are not merely high—they are generational. No startup, however well-funded, can replicate a germplasm library that took fifty years to assemble.

In Pharmaceuticals, the relevant Power has historically been Cornered Resources: patent-protected blockbuster drugs that grant what amounts to a temporary legal monopoly on a specific therapeutic mechanism. Xarelto and Eylea were textbook cornered resources, protected by composition-of-matter patents that kept generic competitors at bay for years. But the pharmaceutical model has a built-in self-destruct mechanism: patents expire. When a blockbuster drug goes off patent, generic competitors flood the market within months and the original product's revenues can collapse by 50 to 80 percent in a shockingly brief timeframe. Pharma investors call this the "patent cliff," and it is not a metaphor—it is a literal, vertical, stomach-dropping plunge in revenue. Bayer is standing on this cliff right now.

The third notable Power is Switching Costs, concentrated in the FieldView digital platform. Enterprise software investors instinctively understand this dynamic: it is the same lock-in that keeps companies paying Salesforce license fees for decades. Once a farming operation has loaded years of data into FieldView, migration is not mere technical hassle—it is the destruction of irreplaceable institutional knowledge.

Now shift from Helmer's internal moat analysis to Michael Porter's external competitive framework. The Five Forces squeezing Bayer from multiple directions tell a story of relentless, structural pressure that no amount of internal optimization can fully offset.

The Threat of Substitutes is existential in Pharmaceuticals. The entire generic drug industry—Teva, Sandoz, and dozens of smaller players—exists to do one thing: wait for patent cliffs and flood the market with identical products at dramatically lower prices. For Xarelto and Eylea, this is not a future scenario but a present reality.

Bargaining Power of Buyers is increasing across all three divisions. In pharma, government health systems—the UK's NHS, Germany's statutory insurance system, European formulary committees—negotiate drug prices with increasing aggression, wielding monopsony purchasing power that individual pharmaceutical companies cannot easily resist. In the United States, the Inflation Reduction Act has introduced direct government negotiation of certain drug prices for the first time, further pressuring margins. In agriculture, the consolidation of farm retail chains and the growing sophistication of large-scale farming cooperatives give buyers increasing leverage to squeeze seed and crop protection margins.

Competitive Rivalry in post-consolidation ag-chem is intense but generally disciplined. With four major players controlling the vast majority of global seed genetics and crop protection market share, outright price wars are rare. The industry structure—a tight oligopoly with high barriers to entry—promotes rational pricing behavior, much like the dynamics in global commercial aviation engine manufacturing (GE, Pratt & Whitney, Rolls-Royce) or operating systems (Windows, macOS, iOS, Android). Nobody benefits from a margin-destroying price war when there are only four meaningful competitors.

But innovation competition is fierce and unforgiving. Every major player is racing on multiple fronts simultaneously: developing next-generation biological crop protection products (microbe-based alternatives to synthetic chemicals), deploying CRISPR-based gene-editing technologies (which allow precise genetic modifications without the regulatory baggage of traditional GMO approaches), and building AI-powered digital farming platforms to optimize every aspect of agricultural production. In this kind of innovation race, falling behind in R&D is potentially fatal. You cannot catch up once the data network effects of a competing platform have compounded for several seasons, and you cannot rapidly develop a new seed trait that your competitor started working on a decade ago.

Supplier Power is a nuanced dynamic. In crop science, Bayer is itself the supplier—one of only four companies with the scale to develop new seed genetics and crop protection chemistry. This gives it significant power over its customer base of individual farmers and farm cooperatives, though that power is moderated by the increasing consolidation and sophistication of downstream agricultural retailers. In pharmaceuticals, the company's relationship with the healthcare supply chain is more complex: hospitals and pharmacy benefit managers increasingly wield significant power to negotiate rebates and formulary positioning, while governments exercise direct pricing authority in many markets outside the United States.

New Entrants remain largely a non-threat in seeds and crop protection given the billion-dollar, decade-long development timelines. But there is a notable wildcard: technology companies entering digital agriculture from adjacent industries. Companies like John Deere, with its massive installed base of connected farm equipment, and even Amazon Web Services, which has launched agricultural data initiatives, could theoretically challenge FieldView's dominance—not by replicating the data, but by controlling the hardware and cloud infrastructure through which the data flows.

The capital allocation lesson at the heart of the Bayer story deserves to be written in bold letters on the wall of every boardroom: FOMO—Fear Of Missing Out—is the most destructive emotion in corporate M&A.

Bayer did not buy Monsanto because a rigorous, dispassionate analysis concluded the deal offered uniquely attractive risk-adjusted returns. They bought Monsanto because they were terrified—genuinely, viscerally terrified—of being left behind as Dow-DuPont and ChemChina-Syngenta reshaped the agricultural competitive landscape. That fear drove a 44 percent premium at the absolute peak of the agricultural cycle. An all-cash deal structure that maximized balance sheet risk. And a catastrophic failure to properly size litigation exposure rooted in cultural overconfidence about the predictability of the American legal system.

The pattern is universal, and it repeats with depressing regularity in corporate M&A across industries and decades. Acquisitions driven by fear of competitive irrelevance almost always overpay, because the psychological urgency of "we must act now or be left behind" overrides the financial discipline of "this deal must earn a risk-adjusted return above our cost of capital." Fear shortens time horizons, inflates willingness to pay, and suppresses skepticism.

The deeper structural lesson is about the danger of treating acquisitions as a substitute for organic innovation. Each of Bayer's three major deals—Schering, Merck Consumer Care, and Monsanto—was motivated partly by a perceived gap in internal growth capabilities. Rather than spending more on R&D, building new platforms from scratch, or accepting the slower but more controllable path of internal development, Bayer repeatedly chose the faster, more glamorous, more investment-banker-friendly route of buying what it could not build.

The trajectory from Schering (disciplined) to Merck Consumer Care (expensive but defensible) to Monsanto (catastrophic) is the universal arc of the serial acquirer who gradually loses the ability to distinguish strategic ambition from strategic recklessness. It is a pattern visible across industries and eras: Tyco, WorldCom, Valeant Pharmaceuticals, General Electric under Jeff Immelt. The lesson is always the same, and corporate boards always seem to need to learn it fresh: organic capability development is slow and unglamorous, but it does not blow up the balance sheet. M&A is fast and exciting, but the compounding of deal-related risks—debt, cultural integration, hidden liabilities—eventually catches up with even the most confident acquirer. There is no shortcut to building a great company.

VIII. Bear vs. Bull Case & Epilogue

The Bear Case