British American Tobacco: The Great Smoke-Free Pivot

I. Introduction & Episode Roadmap

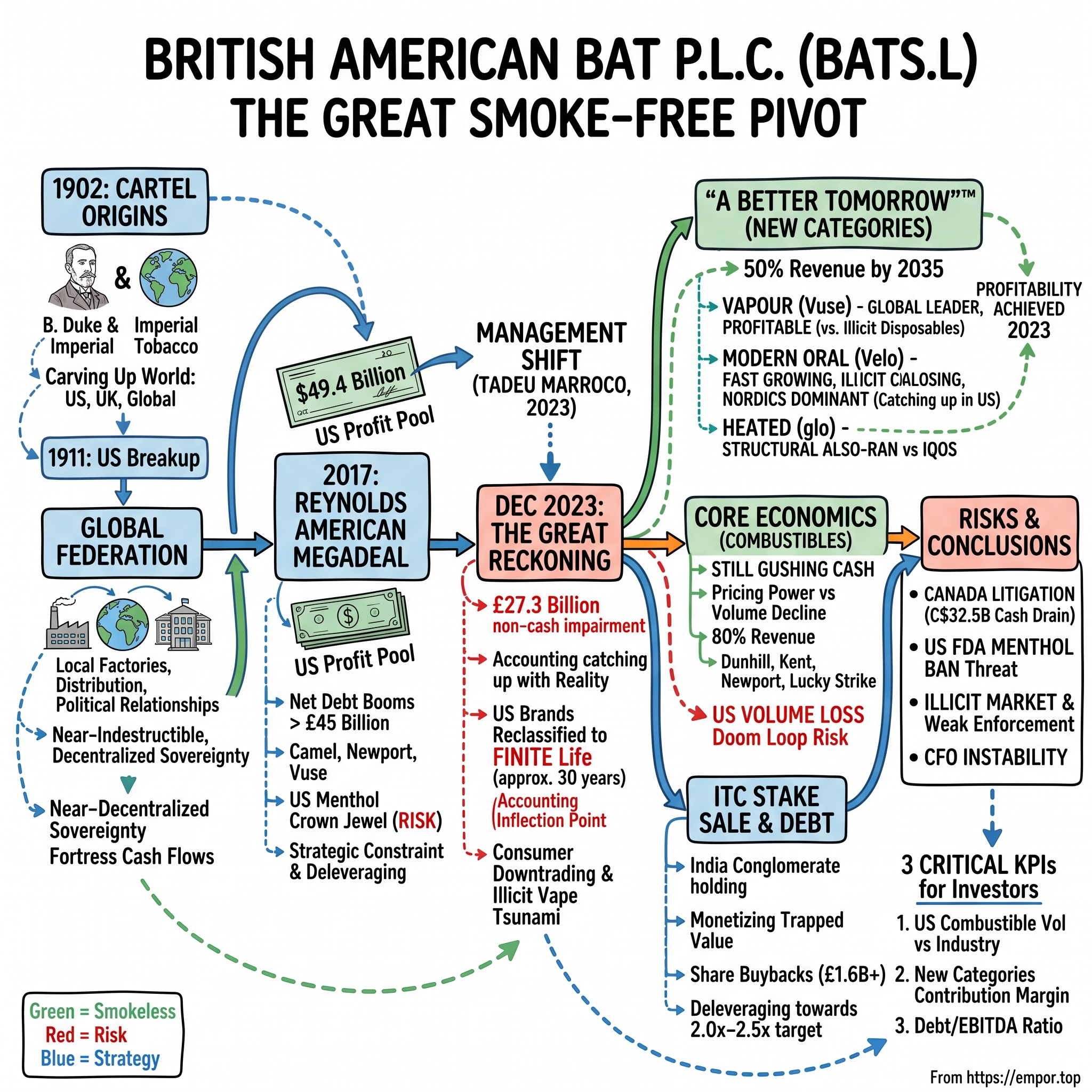

Picture the scene inside a London boardroom in the closing weeks of 2023. A 124-year-old company, one of the last true global oligopolists, is about to do something that no chief executive ever wants to do voluntarily: tell the market that a chunk of its own history is worth far less than the balance sheet claims. The number Tadeu Marroco signed off on was staggering — a £27.3 billion non-cash impairment, roughly $31.5 billion, one of the largest write-downs in British corporate history.1 It was not the result of fraud, a failed factory, or a rogue trader. It was, in Marroco's own framing, simply "accounting catching up with reality."[^2] The reality being caught up with was this: cigarettes, the product that built the modern world's most reliable cash machine, are dying.

That is the paradox at the heart of British American Tobacco p.l.c. (BATS.L, listed on the London Stock Exchange). Here is a business that in 2024 generated £25.87 billion in revenue selling a legal, highly addictive product with formidable pricing power.2 It throws off billions in cash. It pays one of the highest dividend yields in the FTSE 100. And yet for years it has traded at a single-digit price-to-earnings multiple, priced by the market as though it were in a controlled demolition. The share register has been thinned by ESG-driven capital flight, a decade of litigation overhangs, and a slow-motion recognition that the terminal value of a cigarette is, mathematically, zero.

This is the story of how a company born from a cartel treaty tries to reinvent itself before its core product finishes disappearing. It runs from BAT's origins in 1902 — when British and American tobacco barons signed a peace treaty and carved up the planet — through its debt-fuelled $49.4 billion acquisition of Reynolds American in 2017, to the cold-eyed realism of Marroco, a 30-year finance man who took the top job and immediately started telling shareholders uncomfortable truths.3

What makes BAT such a rich case study is that it sits at the intersection of nearly every hard question in modern investing. How do you value a business whose product is being legislated, taxed, and shamed out of existence, yet remains wildly profitable? How should management allocate capital when the core is melting but still gushing cash? Is a cheap stock with a fat dividend a bargain or a trap? Can a legacy incumbent genuinely disrupt itself, or does disruption only ever come from outsiders with nothing to lose? BAT is a live experiment in all of these at once — which is why it deserves to be understood on its own terms, independent of both the industry's boosters and its many, understandable detractors. Our job here is not to defend tobacco or to condemn it, but to understand the machine, the money, and the odds.

Here is the roadmap. We will start with the cartel cartography of BAT's founding. We will benchmark the Reynolds megadeal and ask whether BAT bought a melting ice cube or an essential bridge to the future. We will sit inside the great accounting reckoning of December 2023. We will tour the portfolio — the combustible cash cows (Dunhill, Kent, Newport, Lucky Strike) against the "New Categories" (Vuse, glo, Velo). We will dissect the ITC arbitrage, in which BAT used a giant, non-controlled stake in an Indian conglomerate as a liquid piggy bank to fund buybacks. We will run the business through Hamilton Helmer's 7 Powers and Porter's 5 Forces. And we will stress-test the whole edifice against Canada's C$32.5 billion litigation settlement and the sustainability of that famous dividend. The question underneath all of it: can a company manage the decline of one product fast enough to fund the birth of another — and is management telling you the truth about the odds?

II. The Cartel Origins: Carving up the World

Every empire has a founding myth, and BAT's begins with a man who understood that the real fortune in tobacco was not in growing it or rolling it, but in controlling who could sell it. His name was James Buchanan "Buck" Duke, the son of a North Carolina farmer, and by the 1890s he had done something audacious. When a Virginian named James Bonsack invented a machine that could roll cigarettes far faster than any human, Duke locked up the technology, flooded the market with cheap product, and then used the resulting scale to swallow his rivals. By 1890 he had consolidated the American cigarette industry into a single behemoth: the American Tobacco Company, a trust of such reach that it would eventually control the vast majority of the US market.

There is a detail in Duke's story that tells you everything about the DNA he stamped onto the industry. When he first saw the Bonsack rolling machine demonstrated, most cigarette makers dismissed it — the hand-rollers of the day produced a better, more consistent product, and cigarettes were still a niche indulgence next to pipes, cigars, and chewing tobacco. Duke did the opposite of dismissing it. He reasoned that if he could make cigarettes far cheaper than anyone else, he could create the mass market that didn't yet exist, then own it. He signed exclusive deals for the machines, slashed prices, and poured the savings into a then-radical weapon: advertising. Duke understood before almost anyone that in a commodity product, the brand — not the leaf — was the moat. That single insight, that tobacco is a marketing business wearing an agricultural costume, is the intellectual foundation on which BAT still stands more than a century later.

Duke's ambition did not respect coastlines. In 1901 he sailed to Britain, bought a Liverpool cigarette maker, and effectively declared war on the British trade. The response was pure survival instinct. Britain's fragmented, family-owned tobacco firms — proud, provincial businesses like W.D. & H.O. Wills and John Player & Sons — did something they had never done before: they banded together, forming the Imperial Tobacco Company to repel the American invader. What followed was a brutal, wasteful price war that threatened to bleed both sides dry, with each side subsidising ever-cheaper cigarettes and lavish promotions to buy market share. It was the kind of mutually assured destruction that, in a rational industry, ends in one of two ways: someone dies, or everyone agrees to stop.

Then came the moment that created the company we are discussing. Rather than annihilate each other, the two sides sat down in 1902 and signed a treaty. The terms were elegantly simple and staggeringly anti-competitive by modern standards. American Tobacco would keep the United States. Imperial would keep the United Kingdom. And the rest of the world — Asia, Latin America, Africa, the vast markets beyond either home turf — would be handed to a jointly owned venture, christened the British-American Tobacco Company. Two-thirds American, one-third British, it was less a company than a diplomatic settlement with a share certificate.

History then did BAT a favour. In 1911, the US Supreme Court broke up Duke's American Tobacco trust under antitrust law, forcing it to divest its foreign holdings. BAT was cut loose, became an independent London-listed entity, and inherited a genuinely global map with no American parent looking over its shoulder. What it built on that map is the key to understanding the business even today. BAT never operated as a centralised monolith. It ran as a federation of powerful national subsidiaries — a company in Brazil, a company in India, a company in Nigeria — each with local factories, local leaf, local distribution, and local political relationships. This decentralised sovereignty let it survive tariff walls, revolutions, currency collapses, and two world wars, because in each country it looked and behaved like a domestic champion.

Consider what that decentralised structure meant in practice. When a nationalist government in one country threatened expropriation, BAT could negotiate as a local employer with local jobs at stake rather than as a foreign predator. When a currency collapsed, the damage was ring-fenced to one subsidiary rather than the whole. When wars redrew borders, BAT's factories simply carried on serving whoever now ran the territory. This was not the tidy, centralised multinational of business-school diagrams; it was closer to the British East India Company model — a loose confederation of semi-autonomous fiefdoms sharing a flag and a dividend. The cost was duplication and complexity. The benefit was near-indestructibility. A company organised this way is very hard to kill, which is precisely why BAT has outlived empires, ideologies, and the men who built it.

The economic blueprint underneath was the thing investors should really appreciate. Cigarette manufacturing is astonishingly capital-light: a factory is cheap relative to the ocean of cash it produces. Because retailers and wholesalers pay quickly while excise taxes and suppliers are paid on a lag, the business runs on deeply negative working capital — customers and the taxman effectively finance the company's operations. Add near-total pricing power over an addicted consumer, a product that costs pennies to make and sells for pounds, and distribution networks that took a century to build, and you have a fortress. The barriers to entry were not clever; they were simply insurmountable. No startup could replicate a hundred years of shelf space, brand recall, and regulatory relationships. That fortress generated the kind of returns on capital that make a business look, on a spreadsheet, almost too good to be legal — which, increasingly, is the point. It would eventually become both BAT's greatest asset and, as we will see, the source of its greatest strategic complacency: when your moat has never been breached, you stop imagining what could breach it.

III. The Reynolds American Megadeal: The Battle for the US Profit Pool

For most of the twentieth century, the United States was the one great tobacco market where BAT was an outsider looking in — a consequence of that 1911 breakup. It never fully gave up. By the 2010s, BAT held a 42% non-controlling stake in Reynolds American Inc., the number-two US cigarette maker and home to Camel, Newport, and Natural American Spirit.4 It collected dividends and had board representation, but it did not control the crown jewel of global tobacco pricing power: the American profit pool, the most consolidated and lucrative cigarette market on earth.

In October 2016, under then-CEO Nicandro Durante — an Italian-Brazilian engineer by training who had spent his entire career inside BAT and was known for operational rigour rather than showmanship — BAT decided to buy the whole thing. The first move was rebuffed. BAT's opening approach, valuing Reynolds at around $47 billion, was deemed too low by the Reynolds independent directors, who knew they were sitting on an asset BAT strategically had to own. BAT came back with a sweetened offer, and in January 2017 the two sides agreed: BAT would acquire the 57.8% of Reynolds it did not already own for $59.64 per share in cash and stock — $29.44 in cash plus roughly half a BAT share for each Reynolds share — a package that valued that remaining stake at roughly $49.4 billion and represented a premium of about 26% to Reynolds' undisturbed price.4 The cash half alone, around $24.4 billion, had to be raised in the debt markets.4

It was, at the time, one of the largest consumer deals in history, and it was the culmination of a relationship that stretched back decades — BAT had first taken a Reynolds stake in 2004 when Reynolds merged with BAT's US arm, Brown & Williamson. When the deal closed in mid-2017, BAT had transformed itself from a company with strong emerging-market volumes into the outright owner of the richest cigarette cash flows in the developed world. Durante, on his way toward the exit, had pulled off the acquisition BAT had wanted for a century.

The strategic logic was seductive. Full ownership of Newport handed BAT the leading brand in US menthol, a category with fierce loyalty and premium economics. Camel and Natural American Spirit deepened the portfolio. Crucially — and this is the part the 2017 rationale often understates — the deal also delivered Vuse, Reynolds' small, unglamorous vapour brand that would later become the single most important asset in BAT's transition story. Durante's team was buying today's cash flow, but they accidentally bought a piece of tomorrow too.

So did they overpay? The honest answer depends entirely on which year you ask the question. On the numbers, BAT paid something in the order of 16 times EBITDA for a mature business — a full price for a product category already in structural volume decline, though not an insane one by the standards of consumer-staples M&A at the time, when investors still treated cigarette cash flows as bond-like and eternal. Measured against 2017's assumptions, the deal was defensible. Measured against what actually happened, it was a mistake of historic proportions. The gap between those two verdicts is the story of this company.

The bigger problem was not the multiple but the funding. The transaction loaded BAT with net debt that ballooned past £45 billion, turning a famously cash-rich, lightly geared balance sheet into a leveraged one almost overnight. To put that in human terms: BAT went from a company that could do almost anything it wanted with its cash to one that spent the next decade with a mortgage the size of a small country's GDP. That debt sat on management's shoulders like a rucksack full of bricks, dictating capital allocation, constraining M&A, capping the pace of investment in New Categories, and forcing every subsequent CEO to open every investor call by talking about "deleveraging" rather than growth. The Reynolds deal did not just buy an asset; it bought a decade of strategic constraint.

But the deepest flaw was strategic myopia. BAT — the company whose entire history was built on regulatory navigation — underestimated two regulatory and technological time bombs sitting inside the US market. The first was the rise of cheap, illicit disposable vapes, largely Chinese-manufactured, which would flood American convenience stores in a regulatory grey zone and eat directly into cigarette volumes. The second was the looming threat of an FDA ban on menthol cigarettes, which would strike Newport — the very asset BAT had paid a premium for — at its heart. BAT bought the American profit pool at the top, using the balance sheet as leverage, on the implicit assumption that the terminal value of these brands was durable. Within six years, management would formally admit in writing that this assumption was wrong. That admission is where our story turns.

IV. The Great Reckoning: The £27.3 Billion Write-Down of December 2023

Tadeu Marroco did not arrive in the corner office through charisma or a splashy external hire. He arrived because the board needed a grown-up. In May 2023, BAT abruptly announced that CEO Jack Bowles was stepping down and that Marroco — a Brazilian-born finance lifer who had joined BAT in 1992, run the Europe and North Africa region, and served as Group Finance Director since 2019 — would take over immediately.35 Bowles, a more salesman-like figure who had run the French and Malaysian businesses before rising to the top in 2019, left with the share price languishing and investor trust frayed.6 Marroco's brief was unglamorous but urgent: restore credibility, inject realism, and get the debt down.

Realism arrived seven months later, and it landed like a thunderclap. In its December 2023 trading update, BAT announced a non-cash impairment charge of approximately £27.3 billion, around $31.5 billion, written against the carrying value of its acquired US combustible brands.1 To grasp the scale: this single accounting entry was larger than the entire market capitalisation of many FTSE 100 companies. Much of the value BAT had paid for in the 2017 Reynolds deal was being erased in one line.

The mechanism mattered as much as the number. For years, BAT had carried its big US cigarette brands as "indefinite-lived" intangible assets — an accounting treatment that assumes a brand will generate value forever and therefore is never amortised, only tested for impairment. In December 2023, BAT reclassified these acquired US combustible brands to a finite useful life of roughly 30 years.1 Read that again: the owner of these brands was formally declaring that, on current accounting judgment, traditional cigarettes would cease to have material economic value by around mid-century. This was not a pessimistic analyst's model. It was the company's own auditors and board putting a sell-by date on the product that still generated the overwhelming majority of profit.

Why does the accounting distinction between "indefinite-lived" and "finite-lived" matter so much to an investor? Because it is a window into what management actually believes. An indefinite-lived intangible is the accounting equivalent of saying "this brand is a perpetual-motion machine — it will keep printing cash forever, so we will never write it down against the passage of time." The moment you assign it a 30-year life, you are conceding that the machine has a fuel gauge, and the needle is moving. BAT did not have to make this change in December 2023; auditors and management could have found ways to defend the old treatment for another year or two. Choosing to reset it — and to take the whole £27.3 billion hit at once rather than dribbling it out — was a decision to stop pretending. That is why the number, though non-cash and cosmetically irrelevant to the dividend, carried such a heavy signal.

Two forces drove the reckoning, and both were structural rather than cyclical — which is exactly why they justified a permanent write-down rather than a temporary provision. The first was consumer downtrading. Years of post-pandemic inflation had hollowed out the wallets of BAT's lower-income US smokers, who began abandoning premium brands like Newport for deep-discount alternatives — the fighting brands sold at the bottom of the price ladder. Pricing power, the tobacco industry's sacred moat, works right up until the customer simply cannot afford the premium. For decades that ceiling seemed infinitely high; the 2022–23 inflation shock revealed that it was not, at least not for the marginal American smoker living paycheck to paycheck. The second force was the illicit disposable vape tsunami: thousands of flavoured, synthetic-nicotine disposables, mostly Chinese-made, pouring into US convenience stores outside the FDA enforcement net, sold for a few dollars, and siphoning off exactly the volume — younger, price-sensitive nicotine users — that legal, taxed cigarettes used to convert into lifelong customers. BAT was watching its future customer acquisition funnel get diverted into products it did not sell and could not legally compete with on the same terms.

What is genuinely notable — and worth crediting from a neutral seat — is how Marroco handled the reveal. He could have buried the write-down in a footnote and spun the accompanying trading statement toward the positives. Instead, alongside the impairment, BAT lowered its medium-term revenue growth guidance and reframed the entire strategy around "Building a Smokeless World," making the write-down the centrepiece rather than the fine print.[^2] On the calls and in interviews that followed, Marroco refused to hide behind macroeconomics or blame the weather. Pressed by analysts on whether the US business was structurally broken, he declined the easy outs, acknowledging that the disruption was real and that pricing alone would not save the day. He framed the whole exercise as aligning the balance sheet with reality rather than defending a number.[^2]

For a management team that had spent the Bowles years overpromising and underdelivering — repeatedly guiding to growth rates it then missed — the blunt admission bought something valuable: a floor of credibility. Analysts who had grown weary of tobacco-company spin found, in Marroco, someone willing to say the quiet part out loud. The cynic's counter is equally fair and worth holding in mind: a write-down is non-cash, costs management nothing in the current period, resets the asset base so future return-on-capital ratios look better, and conveniently lowers the bar the new CEO has to clear. A skeptic could call it a "kitchen-sink" quarter — a new boss dumping every possible bad number into one report so that everything afterward looks like improvement. Both readings are true simultaneously. The reckoning told investors, in the company's own words, that the cash machine is finite. The two questions that everything else in this story hangs on are: how fast does it drain, and can the replacement engine be built before it runs dry?

V. Core Business Economics & Segment Breakdown

Strip away the drama and BAT is, first and last, a cash machine — one built to convert an addicted customer base into an almost eerily predictable stream of money. In 2024, the group generated £25.87 billion in total revenue.2 The remarkable thing is not the size but the mix. Even as cigarette volumes decline at a structural 5–8% a year, traditional combustibles still generated roughly £20.7 billion, about 80% of revenue, and an even larger share of operating cash flow.2 The smokeless future is the story; combustibles are still paying for the whole production.

Geography is where the real texture lives. BAT's largest and most profitable engine is the United States, which contributed roughly £11.3 billion of revenue in 2024.2 This is the segment Durante paid so dearly for, and it remains the group's economic heart — extraordinarily high-margin, but also the epicentre of volume decline, downtrading, and the illicit-vape problem. The second region, spanning the Americas and Europe (AME), is a consolidated, mature cash-cow territory — but in 2024 its reported operating profit swung deeply negative, weighed down by the enormous provisions BAT was forced to book against Canadian litigation, a distortion we will return to when we reach the Canadian settlement. The third region, Asia-Pacific, Middle East and Africa (APMEA), is the volume story: enormous smoker populations, growing in some markets, but at far lower margin per pack than the US. It generated several billion pounds of revenue and remained solidly profitable.2

There is a subtle but important point buried in that segment structure. The US, with under half the group's revenue, historically punched far above its weight in profit, because American cigarette pricing and margins dwarf those of most emerging markets. A pack sold in the US throws off multiples of the profit of a pack sold in Nigeria or Indonesia. This is why the US decline hurts so disproportionately: BAT is not just losing volume, it is losing its highest-margin volume, and no amount of growth in low-margin APMEA sticks can fully replace a lost premium American pack. The geographic mix, in other words, means the group's profit pool is more concentrated and more fragile than the revenue split alone suggests.

The competitive map explains why these cash flows are nonetheless so defensible. The US is effectively a duopoly: Altria (owner of the US Marlboro rights) sits at roughly half the cigarette market, with BAT's Reynolds arm the clear number two at around a third. In a two-horse race, neither party has any incentive to start a price war — both would rather raise prices in lockstep and split a shrinking but hugely profitable pie. Globally, the oligopoly splits into recognisable roles — Philip Morris International is the premium leader carrying Marlboro across the rest of the world; 日本たばこ産業 Japan Tobacco is the great volume consolidator, hoovering up brands and markets others exit; and Imperial Brands plays the disciplined regional value hand. Four or five players, entrenched century-old brands, brutal regulatory barriers to new entrants, and a shared understanding that competing on price is collective suicide. This is precisely the industry structure — concentrated, rational, and legally fortified — that produces the pricing power on which the entire business model rests.

And pricing power is the engine of the whole model. The tobacco magic trick, performed annually for decades, is to raise prices 5–10% to more than offset volume declines of 5–8%, so that revenue and profit grow even as fewer cigarettes are sold every year. It is one of the most beautiful pieces of financial physics in all of business: a shrinking business that nonetheless compounds cash. Warren Buffett famously admired the economics — "it costs a penny to make, sell it for a dollar, it's addictive, and there's fantastic brand loyalty" — even as he declined to own the moral and legal baggage.

But it works right up until it doesn't, and the write-down was, in part, an admission that the trick is approaching a physical limit. The mechanism of the breakdown is a doom loop that investors should understand precisely. Each price rise widens the affordability gap and pushes the marginal low-income smoker toward a deep-discount brand or, worse, an untaxed illicit vape. That accelerates volume loss on the premium brands. A faster volume decline means the next price rise has to be even larger to hold total profit flat — but a larger price rise pushes still more smokers away. In a benign environment, price comfortably outruns volume and the loop is virtuous. In a stressed environment, with cheap illicit alternatives everywhere and squeezed consumers, the loop can flip and start eating itself. The math still worked in 2024 — revenue on an organic basis actually edged up.2 The genuine analytical question for a long-term investor is not whether BAT can raise prices next year; it can, and will. It is how many more years the price-volume equation stays positive before the base erodes faster than price can compensate — and whether that crossover arrives before or after the smokeless business is big enough to matter. That ticking clock is exactly why the New Categories are not a nice-to-have but an existential necessity.

VI. "A Better Tomorrow™": The New Categories Battle

If combustibles are the past that pays the bills, "New Categories" are the future BAT is trying to buy with that money. The stated ambition is bold: to derive 50% of revenue from smokeless products by 2035, transforming a cigarette company into a "multi-category consumer goods" business.2 In 2024, New Categories generated £3.43 billion of revenue — real money, but still only about 17.5% of the group total, which tells you how much runway remains.2 The transition is being fought on three fronts, and BAT is winning one, contesting one, and arguably losing one.

The clear win is Vapour, led by Vuse — the brand that came, almost as an afterthought, with the Reynolds deal. Vuse is the global vaping market-share leader and is genuinely profitable in Europe and, increasingly, the US. Think of a vape as a device that heats a nicotine-laced liquid into an inhalable aerosol, no combustion, no tar, no smoke. The unit economics are attractive because the razor-and-blade model works: the device pulls the consumer in, and refills provide recurring, high-margin revenue. Vuse's enemy is not another Big Tobacco brand but the illicit, untaxed Chinese disposables that undercut it on price and flavour while ignoring the rules Vuse must follow — the same grey-market flood that helped trigger the 2023 write-down.

Why does the illicit-disposable problem hurt Vuse so specifically? Because the two products compete for the same customer, but only one of them plays by the rules. Vuse must fund PMTA science, pay excise taxes in many jurisdictions, restrict flavours to what the FDA authorises, and abide by marketing limits. The Chinese disposable ignores all of that — it offers banned flavours, pays no US tax, files no application, and sells for a few dollars. It is competing against a rival that has voluntarily tied one hand behind its back. Vuse can win on brand, quality, and legitimacy where enforcement exists; where it doesn't, price and flavour win, and BAT loses. The health of Vuse is therefore less a story about BAT's product and more a story about whether regulators actually enforce their own rules — a theme that will recur.

The genuinely losing front is Heated Products, led by glo. Here the concept is a device that heats a stick of real tobacco to around 250–350°C — hot enough to release a nicotine-laden vapour but not hot enough to combust the leaf, which is where most of cigarette smoke's harmful compounds come from. The category leader, by a country mile, is Philip Morris International's IQOS, which pioneered heated tobacco, bet the company on it, and commands well over two-thirds of the global market. IQOS is arguably the single most successful reduced-risk product in tobacco history, and it is why PMI now generates a large and rising share of revenue from smokeless products. BAT's glo, which uses induction heating, has fought hard, launched successive device generations, and simply never closed the gap; it remains a structural also-ran in the single most valuable smokeless category. In 2024, glo's stick volumes actually fell around 12%, even as reported revenue edged up on pricing and mix.7 For investors, this is the uncomfortable truth sitting beneath the polished "smokeless world" rhetoric: in the one new category that PMI proved could be enormous and highly profitable, BAT is losing, has been losing for years, and there is no obvious product or distribution catalyst on the horizon that reverses it. A neutral assessment has to treat heated tobacco as a strategic defeat, not a battle still in doubt.

The fast-growing contender is Modern Oral, led by Velo — small white pouches of nicotine tucked under the lip, with no tobacco leaf, no spit, no smoke. This is the category with the most beautiful economics of all: tiny, cheap to make, cheap to ship, and highly addictive to a growing base of younger nicotine users. Velo dominates in the Nordics and is scaling fast; in 2024, BAT's modern-oral volumes jumped 55% and revenue rose to £814 million.7 But in the richest market, the United States, Velo trails badly behind ZYN, the runaway leader owned by Philip Morris via Swedish Match. BAT invented a lead in Europe and is playing catch-up in America.

The unit economics explain why BAT's smokeless portfolio has such uneven prospects, and it is worth pausing on the difference. Modern oral pouches are the dream product: no device, no electronics, no combustion, almost nothing to ship but a tiny tin. The gross margins on a mature nicotine pouch business can approach those of cigarettes themselves, which is why ZYN has been such a monster for PMI and why Velo's Nordic economics are so attractive. Vapour sits in the middle — the device is cheap and the refills recur, a classic razor-and-blade model, but flavour regulation and illicit competition cap the upside. Heated tobacco is the worst of the three from a capital standpoint: it demands heavy, ongoing investment in device hardware, consumer subsidies to seed the installed base, and dedicated manufacturing for the tobacco sticks — all for a category BAT is losing anyway. In effect, BAT's most capital-hungry smokeless bet is also its weakest, while its most capital-light bet (Velo) is where it is playing catch-up in the market that matters most.

The financial turn, however, is real and deserves credit. After years of heavy losses that critics used to mock the whole "A Better Tomorrow" project as an expensive vanity exercise, New Categories reached profitability in 2023 — two years ahead of BAT's own schedule.2 In 2024, the category delivered a positive contribution of £251 million at a 7.1% contribution margin, an improvement of over seven percentage points year on year, while adding millions of net new consumers.27 The neutral reading: BAT has proven these businesses can make money at scale, which was genuinely not obvious three years ago and which distinguishes BAT from the many nicotine startups that never found a path to profit. The unresolved question is the ceiling. A 7% contribution margin is a long way from the 40–50% operating economics of a cigarette, and the path to closing that gap runs almost entirely through Vuse and Velo — because glo, saddled with hardware costs and losing to IQOS, may never carry its weight. The transition is working; it is simply not yet working fast enough, or at high enough margin, to replace what is draining away from the combustible core. Which raises the question that dominates every BAT investor call: where does the money to fund all of this actually come from?

VII. The ITC Stake Sale: Active Capital Allocation

Buried on BAT's balance sheet for decades sat one of the great hidden treasures in global consumer goods: a roughly 29% associate holding in ITC Limited, India's premier consumer conglomerate — a sprawling empire of cigarettes, packaged foods, hotels, and paper.8 ITC is a genuinely wonderful business, and BAT's stake in it was worth many billions of pounds. But it came with a frustrating catch: BAT did not control ITC, could not consolidate its cash flows, and could not simply repatriate its profits beyond receiving dividends. So the market did what markets do with trapped value — it applied a steep conglomerate discount, valuing BAT's ITC holding at far less than its face value.

The history here runs deep. BAT's relationship with ITC dates back to 1910, when ITC was founded as the Imperial Tobacco Company of India — a colonial-era offshoot of the very same Imperial that co-founded BAT. Over a century, ITC diversified far beyond cigarettes into hotels, agribusiness, packaged consumer goods, and paperboard, becoming one of India's most admired and widely held companies, while BAT retained a large equity anchor throughout. For decades, BAT treated the stake as sacred and untouchable — a strategic window into the world's fastest-growing large consumer market, and a source of steadily rising dividends. The idea of selling it would once have been near-heresy inside BAT.

Marroco's team looked at that trapped asset and saw not a heirloom but an opportunity. Here was a highly liquid, publicly traded position that could be converted into cash almost at will, then recycled into BAT's own deeply undervalued shares — effectively arbitraging the gap between the conglomerate discount the market applied to ITC-in-BAT's-hands and the even steeper discount the market applied to BAT itself. If your own stock trades at a single-digit multiple while you hold a liquid asset the market under-credits, selling the asset to buy your own shares is textbook value-accretive capital allocation. In March 2024, BAT executed the first move: a block trade selling about 3.5% of ITC for net proceeds of roughly £1.57 billion.8 The cash went straight into launching a £1.6 billion share buyback, split across 2024 and 2025.8 It was the first time in living memory BAT had treated the ITC stake as a source of funds rather than a monument.

The pattern repeated with discipline. In late May 2025, BAT sold a further 2.5% of ITC through an accelerated bookbuild, raising net proceeds of about INR 121 billion, roughly £1.05 billion, and leaving BAT with a 23.1% holding.9 The proceeds funded a £200 million extension of the 2025 buyback, taking that year's programme to £1.1 billion, while also helping push net debt toward the target leverage corridor.9 Then, in December 2025, BAT monetised a slice of a newly created asset: following ITC's demerger of its hotels arm into the separately listed ITC Hotels, BAT sold a 9% stake in ITC Hotels for roughly ₹3,820 crore, explicitly stating the hotels holding was not strategic and that proceeds would support deleveraging.10

There is a discipline in how these sales were executed that deserves note. BAT did not dump the entire stake in one panic-driven fire sale that would have crushed ITC's share price and destroyed value. It sold in measured tranches through accelerated bookbuilds to institutional buyers, timing each block to market conditions and clearly signalling that it would remain a "significant shareholder" — reassuring the market that a disorderly exit was not coming. Selling roughly 6% of ITC across two years, while retaining around 23%, is the behaviour of a seller managing an asset, not liquidating in distress.9 It is also, notably, subject to Indian regulatory and tax frictions, which is part of why BAT could never simply repatriate ITC's cash flows and had to monetise via equity sales instead.

Step back and the strategy is a clean piece of financial engineering. BAT took a non-controlled, discount-laden Indian associate and steadily converted it into direct, accretive returns for its own shareholders — buying back BAT stock trading at a single-digit multiple with cash raised from an asset the market under-credited anyway. The activist's counter deserves equal airtime, though, and it is not trivial. Selling down ITC means selling one of the highest-quality, fastest-growing assets BAT owns — a compounding stake in an economy that will add hundreds of millions of consumers — to fund buybacks of a business in structural decline. That is, arguably, eating the seed corn: trading tomorrow's growth for today's per-share optics. Each block trade also permanently reduces future dividend income streaming back from ITC and shrinks the strategic optionality of holding a foothold in the world's most populous consumer market — optionality that could matter enormously if BAT ever wanted to build a smokeless presence in India at scale. Whether this is brilliant capital recycling or slow liquidation of the crown jewels depends entirely on your view of BAT's core business and its terminal value. What is not in doubt is that it reveals a management team willing to act decisively, and willing to touch a sacred, century-old asset to do it. That willingness runs directly into the question of who, exactly, these managers are.

VIII. Current Management: Incentives, Credibility, and Governance

The defining feature of the Marroco era is what it is not. Where his predecessors chased transformative M&A — Durante with Reynolds, the broader industry with serial dealmaking — Marroco has run a deliberately boring playbook: pay down debt, cut costs, return cash, and refuse the temptation of a splashy acquisition to paper over the combustible decline. In a sector where "growth by acquisition" has historically masked underlying volume erosion, choosing restraint is itself a strategic statement. For a neutral observer, this is the single most important behavioural fact about current management: they have, so far, matched their disciplined words with disciplined actions.

The alignment is structured to make that discipline personal. BAT requires its CEO to hold shares worth 500% of annual base salary, tying a large portion of Marroco's personal net worth directly to the share price, and post-employment rules force him to retain a major slice of that holding for two years after he leaves — a design meant to discourage short-term share-price games on the way out the door.2 The long-term incentive plan is weighted toward the metrics that actually matter for the transition: New Categories profitability, cash-flow conversion, and relative total shareholder return against a peer group.2 In principle, Marroco only gets rich if the smokeless pivot and the cash generation both work.

Then there is the governance wrinkle no story should skip: the CFO carousel. Soraya Benchikh, a two-decade BAT veteran, rejoined as Chief Financial Officer in May 2024 — and then abruptly stepped down from the role and the board with effect from late August 2025, barely sixteen months later.11 BAT installed Javed Iqbal, its digital and information chief, as interim CFO while it searched.11 In April 2026, the company named Dragos Constantinescu — himself a former sixteen-year BAT executive who had left to run Asahi Europe & International — as permanent CFO, with a start date of September 1, 2026.12 A finance chief lasting less than a year and a half, followed by a long interim gap and a boomerang external-but-familiar hire, is precisely the kind of instability that a skeptical investor should flag. Neither BAT nor Benchikh disclosed a detailed reason for the swift exit, and unexplained C-suite churn at the exact seat responsible for the deleveraging story is a legitimate governance question mark, however capable the eventual successor.

There is also a question of narrative consistency worth applying the diligence lens to. Across the Bowles-to-Marroco transition, BAT's headline ambition shifted subtly but importantly. Bowles championed aggressive New Categories revenue targets — famously a goal of £5 billion of New Categories revenue by 2025 and 50 million non-combustible consumers — that the company later had to soften. Marroco quietly recalibrated the framing away from top-line growth-at-any-cost toward profitability, cash generation, and margin quality. To a charitable reader, that is a mature CEO trading vanity metrics for value metrics. To a skeptic, it is a company that repeatedly set targets it could not hit and then moved the goalposts, which is exactly the pattern a long-term investor should watch for. The most honest characterisation is that BAT's smokeless ambitions have been consistently directionally right and consistently quantitatively optimistic — the strategy has held, the numbers under it have been walked back more than once.

So how does the credibility scorecard read? On the positive side: Marroco confronted the write-down honestly rather than burying it, executed the ITC block trades quickly and exactly as promised, hit the New Categories profitability milestone early, and abandoned the debt-fuelled empire-building reflex that got BAT into trouble. On the negative side: the CFO instability sits awkwardly against a narrative of steady-hands financial discipline, the history of walked-back targets warrants caution on any new guidance, and the true test — whether the smokeless business scales fast enough, at high enough margin, to offset the combustible decline — remains years from resolution. The honest verdict is that this management has earned provisional trust through behaviour, not yet vindication through results. And provisional trust is worth examining against the durability of the competitive moats it is relying on.

IX. Competitive Moats: Hamilton Helmer's 7 Powers

Why does a company selling a declining product still earn fortress-like margins? Run BAT through Hamilton Helmer's 7 Powers and the answer becomes clear — though so do the cracks.

The most counterintuitive power is Cornered Resource, in the form of a regulatory moat. In the United States, any company wanting to sell a legal vape or oral-nicotine product must clear the FDA's Premarket Tobacco Product Application (PMTA) — a process so expensive, scientifically demanding, and legally treacherous that it effectively locks out small and medium players. The very regulation that critics assume hurts Big Tobacco actually protects it, by making the cost of legal entry prohibitive for anyone without a war chest. An FDA marketing order for a product like Vuse is, in effect, a government-issued licence that competitors cannot easily replicate.

The second power is Scale Economies as distribution power. BAT can place Vuse, glo, and Velo into millions of retail outlets worldwide at near-zero incremental cost, riding a distribution network built over a century for cigarettes. When a BAT sales rep visits a corner shop to service the cigarette gantry, adding a Velo display or a Vuse rack to that same visit costs almost nothing. A vape startup, by contrast, has to build shelf access one store at a time, negotiating with each retailer and each distributor from scratch. BAT already owns the shelf, the relationship, and the logistics. This is the same insurmountable-barrier logic from the cartel era, repurposed for the smokeless age — and it is the single biggest structural advantage BAT holds over the pure-play vape companies that briefly threatened to disrupt it.

The third power is genuinely uncomfortable to write about but analytically undeniable: High Switching Costs through addiction dynamics. Nicotine's biological grip creates customer lock-in of a kind most consumer companies can only dream of. Brand switching happens, and downtrading happens, but category abandonment — quitting entirely — is rare and hard. Once a consumer settles into a preferred vapour or oral brand, the neurochemistry does the retention work. The fourth power, Brand Equity, layers on top: the loyalty attached to Newport and Camel, and the growing positioning of Vuse and Velo, are intangible assets competitors cannot buy.

Now run Porter's Five Forces across the business and four of them confirm the fortress while one detonates the tidy picture. Rivalry among the established players is muted by oligopoly discipline — nobody wants a price war. Supplier power is low; tobacco farmers and packaging suppliers are fragmented and price-takers. Buyer power is famously low, because the buyer is an addicted individual consumer with no bargaining leverage and a biological reason to keep purchasing. The threat of substitutes within legality is contained, because BAT itself owns the leading substitutes (vapour, oral, heated). And the threat of new legal entrants is supposedly near zero — that is the whole regulatory-moat thesis.

But here is where the framework breaks. The illicit, synthetic-nicotine grey market has found a way around the moat entirely rather than through it. Chinese disposable-vape makers do not apply for PMTAs, do not pay excise, and do not restrict flavours; they simply ship product into the country and exploit weak enforcement at the border and on the shelf. When that happens, BAT's greatest defensive asset inverts into a liability. The company has spent hundreds of millions complying with rules — funding clinical science, paying taxes, limiting its own product range — while its most damaging competitors bear none of those costs. A high regulatory moat only protects you if the regulator actually patrols the walls. When enforcement collapses, the compliant incumbent is left carrying a cost structure its lawless rivals escape, and the "moat" becomes a self-imposed tax. This is the single biggest crack in an otherwise formidable competitive position, and it is not hypothetical: it is precisely the dynamic that drove volume away from both Newport and Vuse and helped trigger the 2023 write-down. Competitive advantages built on regulation are only ever as strong as the state's willingness to enforce it — and cracks in this industry, as BAT knows better than anyone, tend to arrive alongside lawsuits.

X. Risk Radar & Legal Stress Tests

graph TD

A[BAT Group Cash Flow] --> B(U.S. Combustibles)

A --> C(New Categories)

A --> D(ITC Associate Dividends)

E[Illicit Disposable Vapes] -.->|Volume Cannibalization| B

F[FDA Menthol Ban Threat] -.->|Impairment of Newport| B

G[Canada Litigation Settlement] -.->|C$32.5B Cash Drain| A

H[Glo Failure to scale vs IQOS] -.->|Restricts heated tobacco profits| C

No risk looms larger, or has hung longer, than Canada. The saga began in 2015, when Quebec courts handed down a massive class-action judgment against the country's cigarette makers. In 2019, facing crippling liability, BAT's Canadian subsidiary, Imperial Tobacco Canada (ITCAN), sought protection under the Companies' Creditors Arrangement Act (CCAA) — Canada's equivalent of bankruptcy reorganisation — effectively ring-fencing the Canadian mess from the parent while negotiations dragged on for years.

The resolution finally crystallised in 2024–2025. Canadian courts advanced a proposed pan-Canadian settlement totalling C$32.5 billion to resolve essentially all outstanding tobacco litigation across the industry.13 In March 2025, the Ontario Superior Court sanctioned the CCAA plans, and in August 2025 ITCAN formally exited creditor protection as billions of dollars began flowing to provinces, Quebec class members, other smokers, and a research foundation.14 The structure of the payout is the part investors must understand: rather than one lump sum, ITCAN and its peers are required to hand over the bulk of their available cash and a significant slice of future annual earnings to a settlement trust, for years to come.14 In plain terms, a meaningful portion of BAT's Canadian profits has been effectively nationalised into a compensation stream — cash that can no longer be pulled back to London to service debt or fund the dividend. This is the driver behind that deeply negative reported AME operating result: the provisioning against a liability that will drain real money for two decades.

It is worth being precise about what this means for the money that actually reaches shareholders. BAT is a holding company in London; it pays its dividend and services its debt out of cash that flows up from operating subsidiaries around the world. The Canadian settlement effectively installs a permanent siphon on the Canadian subsidiary's cash before it can travel to London — a portion of Canadian profits is now legally spoken for, for roughly two decades. Canada was never BAT's largest market, so this is not fatal to the dividend on its own. But it is a live example of a broader vulnerability: BAT's dividend depends on the sum of cash flows it can freely repatriate, and litigation, taxation, or capital controls in any major market can quietly reduce that sum. Investors who focus only on group-level EBITDA can miss the distinction between profit a company earns and profit it can actually move to where the dividend is paid.

The second sword hanging over the US is the menthol ban risk. Newport, BAT's US menthol crown jewel, is one of the single largest brand profit-drivers in the entire American portfolio — a disproportionate share of US profit rides on this one mentholated brand. Successive US administrations have floated an FDA ban on menthol combustibles, framed as a public-health measure aimed particularly at the fact that menthol cigarettes are used heavily by certain communities; each time, a combination of political sensitivity, enforcement complexity, and fears of fuelling an illicit menthol market has delayed it. But the threat has not vanished, and it hangs over the stock as a permanent tail risk. A genuine, enforced menthol ban would write off a substantial chunk of BAT's remaining US cash flow — and would very likely trigger yet another impairment against the very Reynolds assets already marked down in 2023. The premium BAT paid in 2017 remains, to this day, hostage to a regulator's pen, and every menthol headline moves the stock precisely because so much value is concentrated in that single line of the portfolio.

The third risk is the one that crystallised most recently, and it cuts against BAT. In March 2026, the US International Trade Commission reversed an earlier administrative-law-judge finding in RJ Reynolds' favour, ruling that key claims of the Reynolds patent asserted against a swarm of disposable-vape importers were invalid and finding no violation of Section 337.15 Reynolds had been trying to use patent law to choke off the illicit Chinese disposables at the border — the enforcement route around the grey market. The ITC's reversal slammed that door, leaving the US market exposed to continued import inflows and confirming, in a courtroom, the very moat-inversion problem described earlier. BAT has since appealed to the Federal Circuit.15 Between Canada draining the past, menthol threatening the present, and disposables undermining the future, the risk radar is unusually crowded — which is exactly why the dividend's sustainability is the question every income investor is really asking.

XI. The Playbook: Key Lessons for Investors & Founders

Strip BAT down to its transferable lessons and it becomes a masterclass — part cautionary tale, part quiet triumph — in a discipline few companies ever have to practise: how to run a business that is supposed to shrink.

The first lesson is the managed decline strategy itself. Most management teams are wired for growth; running a franchise in structural volume decline requires the opposite instincts. BAT's playbook is textbook: standardise the product range, aggressively shrink the manufacturing footprint as volumes fall, and raise prices relentlessly to defend absolute profit even as unit sales drop. The cash harvested from that discipline is then redeployed to fund the next thing. Done well, a "dying" business can generate enormous shareholder value for decades on the way down. Done poorly, it becomes a value trap. The difference is entirely in the capital allocation.

The second lesson is the transition chasm — and it is where the tension in BAT's whole story lives. The company must pivot from a legacy product carrying roughly 40–50% operating margins to a new set of categories that began life deeply loss-making and today earn only single-digit contribution margins. Crossing that chasm means voluntarily diluting near-term profitability to invest in a future that is not guaranteed to arrive at the same scale. Every quarter, management faces the temptation to under-invest in New Categories to flatter combustible margins — and every quarter it must resist, because under-investing is how you fall into the chasm. The 2023 profitability milestone was the first real evidence BAT is crossing rather than falling. It is evidence, not proof.

The third lesson is the value of non-consolidated assets. The ITC stake — trapped, discounted, non-controlled — turned out to be a strategic insurance policy of the highest order: a multi-billion-pound reserve of liquid value that BAT could tap on its own timetable to fund buybacks and deleveraging without touching the operating business. For any company facing a major transformation, the lesson is that an "inefficient" holding of a great asset can be worth more than its accounting discount implies, precisely because it provides optionality when you need cash most.

There is a fifth, more subtle lesson threaded through the others: the discipline of telling the truth to the market. Marroco's write-down, his walked-back-but-honest reframing of targets, and his willingness to name the illicit-vape and downtrading problems rather than blame the macro cycle all point to a management style that treats candour as a strategic asset. In a declining industry, credibility with capital markets is not a soft virtue — it directly affects the cost of debt, the appetite of equity investors, and the multiple the market is willing to pay. A management team that overpromises in a shrinking business eventually loses the benefit of the doubt entirely, at which point the stock de-rates permanently. Paradoxically, the way to earn a higher multiple in a declining industry may be to admit, loudly and early, exactly how the decline works. BAT's recent history suggests management has learned this lesson; whether it keeps applying it under a new CFO and continued pressure is a fair thing to watch.

The fourth lesson is the darkest: the trap of long-lived goodwill. The 2017 Reynolds deal is the case study in what happens when you pay a huge premium for a terminal cash-cow and book the brands as living forever. When technological and regulatory disruption accelerated faster than anyone modelled, that optimism detonated into the largest write-down in the company's history. The warning for acquirers everywhere: the more mature and "safe" the cash flow you are buying, the more skeptical you should be about the terminal value you are capitalising — because safe, mature businesses are exactly the ones disruption ambushes. Those four lessons frame the only debate that matters for the stock: bull or bear.

XII. Bull vs. Bear Case & 3 Critical KPIs

The bull case rests on the resilience of the cash machine. Combustibles still throw off enough cash to cover the interest on the debt, fund the smokeless transition, and pay a dividend yielding in the high single digits — all at a share price that implies the market expects near-liquidation. New Categories have crossed into profitability and are expanding margins, with the £251 million contribution and 7.1% margin of 2024 offered as proof the model works.2 The ITC block trades supply a repeatable template for returning billions to shareholders without wrecking the balance sheet.89 Put simply, the bull argues you are being paid a fat dividend to wait while a genuine transformation quietly compounds, and any success in New Categories is close to free optionality at this valuation.

The bear case attacks each pillar. US combustible volume decline may be accelerating past the point where pricing power can offset it — the exact dynamic that forced the 2023 write-down. In the most valuable smokeless category, heated tobacco, glo has decisively lost to IQOS, shutting BAT out of a huge future profit pool.7 And the twin cash drains of the Canadian settlement and a potential menthol ban threaten the sustainability of the dividend over the next decade — not tomorrow, but on exactly the multi-year horizon a long-term holder cares about.1314 The bear's synthesis: this is a company slowly liquidating a superb legacy asset to fund an uncertain future while lawyers and regulators skim the cash flow, and the cheap multiple is cheap for good reasons.

At the centre of the whole debate sits the dividend, because it is the reason a large share of BAT's investors own the stock at all. BAT has for years been a cornerstone income holding, paying out the majority of its earnings and offering a yield that has at times reached into the high single digits or beyond — a level the market only assigns when it doubts the payout's durability. The bull says the dividend is comfortably covered by combustible cash flow today, is being supplemented by buybacks funded from ITC sales, and sits alongside a genuine deleveraging path. The bear says the combination of the Canadian cash siphon, a possible menthol ban, accelerating US volume decline, and the eventual exhaustion of the ITC piggy bank could, over a decade, squeeze the free cash flow that underwrites both the dividend and the buyback. Neither side disputes that the dividend is safe this year; the entire argument is about the shape of the curve five and ten years out. That is the correct frame for a long-term investor — not "is the yield high" but "what is the trajectory of the repatriable free cash flow that pays it."

Holding both cases against the frameworks already discussed sharpens the judgment. The 7 Powers are real — regulatory cornered resource, scale distribution, addiction-driven switching costs, brand equity — but the Five Forces reveal that weak enforcement against illicit substitutes is quietly dissolving the most important of them at the edges. Against peers, BAT looks like the value player caught between a premium innovator winning the smokeless war (PMI, with IQOS and ZYN) and its own considerable legacy strength in a shrinking core. That competitive positioning is the crux of the entire investment case: BAT is not losing the nicotine business — it remains one of a handful of giants that will dominate legal nicotine for decades — but it is arguably losing the most valuable future parts of it to a better-positioned rival, while defending the most vulnerable legacy parts against regulators and illicit competition.

For an investor who wants to cut through the noise, three KPIs carry most of the signal. First, US combustible volume decline versus the industry average — the cleanest read on whether BAT is merely riding the category down or losing share to deep-discount rivals, which would signal the pricing engine is breaking. Second, New Categories contribution margin expansion — the single most important measure of whether Vuse and Velo can scale toward the economics of a cigarette, or whether the smokeless business is a low-margin consolation prize. Third, the ratio of adjusted net debt to adjusted EBITDA, tracked against management's stated 2.0x–2.5x target corridor — the direct gauge of whether the Reynolds debt is finally being tamed and whether the balance sheet can absorb the Canadian drain while defending the dividend.9 Watch those three numbers over time and you will know, well before the headlines do, whether the great smoke-free pivot is working.

XIII. Epilogue & Outro

British American Tobacco is, in the end, the purest case study in modern markets of a question every enduring business eventually faces: what do you do when the thing that made you rich starts to die? BAT's answer has been neither denial nor panic, but a cold, deliberate management of decline — harvesting a century-old cash machine at full tilt, recycling a discounted Indian treasure into its own shares, and betting the proceeds on a smokeless future it does not yet dominate. Marroco's great contribution has been to stop pretending — to let accounting catch up with reality, and to ask investors to judge the company on cash and discipline rather than on the fiction that cigarettes last forever.

Whether that pivot succeeds will not be settled for years. The combustible engine still runs, the debt is still heavy, the lawyers in Canada are still collecting, and glo is still losing to IQOS. But the transition has crossed from theory into a profitable, if small, reality, and the capital discipline is, for now, real. The lesson for the sophisticated investor is to watch behaviour over rhetoric, to test the moats against the illicit market that is quietly bypassing them, and to keep one eye on those three KPIs. BAT will remain, for the foreseeable future, one of the market's great arguments — a fortress in managed retreat, priced for a funeral, working quietly on a resurrection.

References

-

British American Tobacco Takes $31.5 Billion Hit on US Brands — Reuters, 2023-12-06 ↩↩↩

-

Preliminary results for the year ended 31 December 2024 — British American Tobacco, 2025-02 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

BAT announces Tadeu Marroco as Chief Executive — British American Tobacco, 2023-05-15 ↩↩

-

BAT announces agreement to acquire Reynolds — British American Tobacco, 2017-01-17 ↩↩↩

-

BAT Appoints Tadeu Marroco as CEO — Tobacco Reporter, 2023-05-15 ↩

-

BAT 2024 Results Summary: New Business Earnings Growth Despite 5.2% Revenue Decline — 2Firsts, 2025-02 ↩↩↩↩

-

British American Tobacco to Sell up to 3.5% Stake in India's ITC — Reuters, 2024-03-12 ↩↩↩↩

-

Completion of Block Trade of ITC Shares — British American Tobacco, 2025-05-28 ↩↩↩↩↩

-

British American Tobacco sells 9% stake in ITC Hotels for ₹3,820 crore — Business Standard, 2025-12-05 ↩

-

British American Tobacco brings back company alum for CFO — CFO Dive, 2026-04 ↩↩

-

British American Tobacco picks Dragos Constantinescu as permanent CFO — AJ Bell, 2026-04-14 ↩

-

Canadian Courts Proposed C$32.5 Billion Tobacco Settlement Plan — Reuters, 2024-10-18 ↩↩

-

Historic Tobacco Industry CCAA Plans Implemented — Davies Ward Phillips & Vineberg, 2025 ↩↩↩

-

ITC Rules 'No Violation' in RJR Complaint — Tobacco Reporter, 2026-03-11 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube