Barclays PLC: The Dual Identity and the Quest for Balance

I. Introduction & Episode Roadmap

Picture a single share of Barclays trading on the London Stock Exchange in early 2023. On paper, that share is backed by a slice of one of the most defensive, profitable retail banking franchises in Europe — a business that clears a meaningful fraction of every pound that moves through the British economy, that issued the country's first credit card, and that installed the world's first cash machine. And yet, for years, the market priced that share at roughly half of its tangible book value. Investors were being told, in effect, that a pound of Barclays' net assets was worth about fifty pence. That is the number that hangs over this entire story, and understanding why it was so low is the whole game.

This is the Barclays paradox. It is a 336-year-old high-street institution with Quaker roots, and it is simultaneously the last European bank still standing in the ring with Wall Street's investment banking oligopoly — the only non-American firm that consistently ranks among the global top handful in fixed-income trading and debt underwriting.1 Those two identities do not sit comfortably together. One is a low-risk, high-return utility that turns cheap deposits into mortgages. The other is a capital-hungry, cyclical trading machine bolted on in the wreckage of the 2008 financial crisis. For fifteen years, the market looked at the combined entity and applied what analysts call a conglomerate discount — the penalty a stock pays when investors suspect the sum of the parts is being dragged down by an unloved whole.

The proximate cause of that discount has a name: Lehman Brothers. When Barclays scooped up Lehman's North American operations out of bankruptcy in September 2008, it acquired a top-tier US franchise at a fire-sale price. It also inherited an appetite for risk-weighted assets that would, for the next decade and a half, quietly starve the higher-returning UK businesses of capital and expose group earnings to the violent mood swings of global markets.2

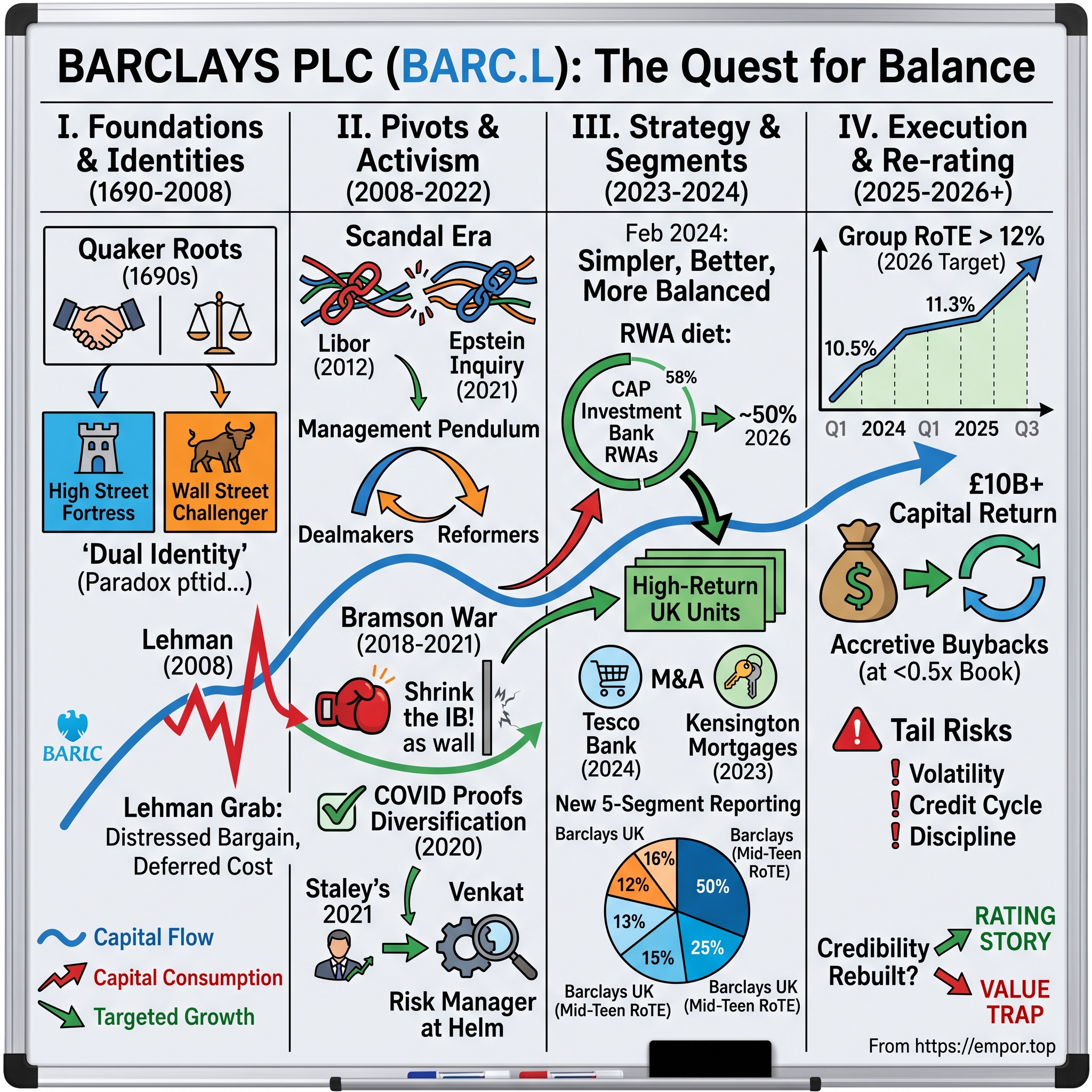

The turning point this episode builds toward arrived on February 20, 2024. That morning, group chief executive C.S. Venkatakrishnan — universally known as "Venkat" — stood in front of investors and unveiled a plan branded "Simpler, Better, More Balanced."3 It was not a revolution. Venkat refused to do what activists had demanded for years and sell the investment bank. Instead, he proposed something more subtle and, arguably, more disciplined: put the investment bank on a strict capital diet, freeze its growth, and redirect every marginal pound of capital into the parts of Barclays that actually earn their cost of equity. The goal — a group return on tangible equity, or RoTE, of above 12% by 2026 — became the single most important number the company had ever committed to publicly.

RoTE is the metric to hold in your head for the next several hours. It measures how much profit the bank generates for every pound of tangible shareholder equity it employs. A bank that earns above its cost of equity — call it roughly 10–12% — creates value and deserves to trade at or above book. A bank that earns below it destroys value and gets punished with a discount. Barclays spent most of the post-Lehman era stuck in the danger zone. The entire "Simpler, Better, More Balanced" thesis is a bet that the bank can climb decisively above the line and stay there.

There is a deeper reason the Barclays story is worth two hours of anyone's attention, and it is not really about Barclays at all. It is about the central, unresolved question of European finance: can a bank headquartered outside the United States credibly compete with JPMorgan, Goldman Sachs, Morgan Stanley, Bank of America, and Citi in the businesses that require the most capital and the steadiest nerve? Deutsche Bank tried and largely retreated. Credit Suisse tried, stumbled from scandal to scandal, and was ultimately swallowed by UBS in 2023. UBS itself chose wealth management over the trading floor. Barclays is the last European name that still shows up, year after year, in the top tier of the global fixed-income and debt-underwriting league tables. Whether that persistence is a source of enduring advantage or a slow, expensive act of denial is a question the market has never fully resolved — and it is the question underneath every chapter that follows.

A note on what this episode is and is not. This is not an investor-relations retelling. Barclays' own materials will tell you the strategy is working and the future is bright; our job is to ask what the evidence actually supports, to separate management's claims from proven facts, and to name the ways the thesis could break. When Barclays says it will re-rate, we will ask what would have to be true, and what would prove it wrong.

Our roadmap runs from Quaker goldsmiths on Lombard Street in the 1690s, through the audacious Lehman grab of 2008, the Libor scandal that toppled a swashbuckling CEO, the bruising activist war waged by Edward Bramson, and finally into the modern execution sprint — where the question is no longer "what is the strategy?" but "can they actually deliver it, quarter after quarter, without the investment bank blowing a hole in the plan?" By the time we reach the end, Barclays will have posted an 11.3% RoTE for 2025 and raised its ambition again.4 Whether that makes it a rerating story or a value trap is the debate we will stress-test throughout.

II. The 300-Year Heritage & The High Street Foundation

To understand why the market treats Barclays' UK retail arm as a fortress, you have to go back to a world without limited liability, without a central bank as we know it, and without any meaningful distinction between a jeweller and a banker. In 1690, two Quaker goldsmith-bankers, John Freame and Thomas Gould, set up shop on Lombard Street in the City of London.5 Goldsmiths were the proto-bankers of the age: people trusted them to hold gold safely, and the receipts they issued for that gold began to circulate as money. The Quaker angle mattered more than it might sound. Barred by their faith from many professions and from the universities, English Quakers poured their energy into commerce and finance, and they brought to it a reputation for plain dealing, sobriety, and keeping their word. In an industry where the entire product is trust, that reputation was the original moat.

The Barclays name entered the picture through marriage — James Barclay joined the family firm in the 1730s — and for the next century and a half the bank grew the way English private banks grew: slowly, through partnerships, kinship, and the quiet accumulation of provincial deposits. It is worth lingering on how unusual that Quaker commercial network was. Because the Quakers were a small, tight-knit, and often persecuted community, they married within it, banked with one another, and extended credit on the strength of personal reputation. A Quaker banker who cheated a counterparty did not merely lose a deal; he lost his standing in a community that was also his customer base, his supply chain, and his family. That social architecture produced an early form of what economists would now call a reputation-based credit system — and it is no accident that several of Britain's most enduring financial names, from Barclays to Lloyds to the confectioners Cadbury and Rowntree, trace back to Quaker families. Trust was not a marketing slogan; it was the collateral.

The pivotal structural moment came in 1896, when twenty private banking houses — a web of interrelated Quaker families including Barclay, Bevan, Tritton, Ransom, and Gurney — amalgamated into a single joint-stock bank, Barclay and Company.5 This was not empire-building for its own sake; it was defensive consolidation. The great joint-stock banks were rising, and a scattering of small family banks could not compete on scale or safety. By merging, the Quaker houses turned a cottage industry into a national institution almost overnight, while keeping the family DNA in the boardroom. It is a pattern worth noting because it recurs across Barclays' entire history: the bank consolidates defensively when a new competitive threat appears — provincial banks in 1896, deregulated global rivals after 1986, distressed Wall Street franchises in 2008, and specialist and supermarket lenders in the 2020s. Barclays has almost always grown by absorbing, not by inventing.

The twentieth century turned that institution into a high-street behemoth. Barclays absorbed rivals — the London, Provincial and South Western Bank in 1918 was a landmark — and stitched together a branch network that reached into virtually every British town.5 But the two innovations that define the retail legacy came in the 1960s, and they reveal a bank that, for all its Quaker caution, had a genuine streak of technological daring. In 1966, Barclays launched Barclaycard, the first credit card in the United Kingdom, importing a piece of American consumer-finance machinery and planting it in British wallets.5 A year later, in June 1967, at a branch in Enfield, north London, Barclays unveiled the world's first cash machine — the automated teller machine — dispensing banknotes to customers using paper vouchers because the plastic debit card had not yet been invented.5

Why dwell on hardware that now feels quaint? Because these were not gadgets; they were customer-acquisition and habit-forming engines. A credit card and a cash machine both do the same strategic thing: they wrap the customer's daily financial life around the bank and make leaving inconvenient. Every current account, every card, every ATM interaction deepened a relationship that the customer had little incentive to unwind. The economic payoff of all that habit is a vast, sticky, low-cost pool of deposits — money that ordinary people leave sitting in current accounts earning little or no interest.

Here is the crucial mechanism, explained plainly, because the rest of this story leans on it. A bank makes money on the spread between what it pays for funding and what it earns lending that funding out. Cheap, stable deposits are the raw material of a profitable bank the way cheap crude is the raw material of a profitable refinery. Barclays UK's deposit base is exactly that: enormous, low-beta (meaning it does not flee the moment a competitor offers a slightly better rate), and largely insensitive to interest rates. When the Bank of England raised rates aggressively in 2022 and 2023 to fight inflation, the yield Barclays earned on its assets jumped while the cost of much of its deposit base stayed low. That is why the UK retail arm can generate returns on tangible equity in the mid-to-high teens — the kind of number the investment bank could only dream of.3

It helps to make this concrete with a simple picture. Imagine millions of customers each leaving a few hundred or few thousand pounds in a current account that pays little or no interest. Individually, those balances are trivial; in aggregate, they are tens of billions of pounds of near-free funding that sits on the bank's books month after month, year after year, because people are busy and switching feels like a chore. The bank takes that near-free money and lends it out as mortgages, credit-card balances, and business loans at much higher rates. The gap between the two is net interest income, and it is the beating heart of retail banking economics. The genius — and the fragility — of the model is that it depends entirely on customers not optimising. The moment depositors become rate-hungry and start chasing the best savings account every few months, the cheap funding gets more expensive and the spread narrows. Three centuries of brand and habit are, in the end, a bet on customer inertia.

There is a second, subtler layer worth understanding, because Barclays talks about it constantly on earnings calls: the structural hedge. Because so much of the deposit base pays a rate that barely moves, the bank is effectively sitting on a huge pool of fixed-cost funding. To convert that into stable income regardless of where short-term rates go, Barclays invests a portion of those balances in a laddered portfolio of medium-term instruments — imagine a rolling series of investments, a slice maturing and being reinvested each quarter. When rates rise, new money rolls into higher yields; when rates fall, the older, higher-yielding tranches keep paying for years. The effect is to smooth the earnings impact of the rate cycle, turning what would be a volatile, rate-sensitive income stream into a more predictable one that grinds upward over time. It is unglamorous financial plumbing, but in a falling-rate environment it is one of the most important reasons Barclays UK's income has proved more durable than a simple "rates are coming down, margins will collapse" story would suggest.4

So the strategic bedrock is this: three centuries of Quaker trust-building produced a funding machine that quietly subsidises the entire group. The tragedy of the modern era — and the seed of the discount — is that this crown jewel spent years hidden inside a conglomerate whose glamorous, volatile other half kept stealing the spotlight and the capital. To understand how that happened, we have to leave the high street and walk onto the trading floor.

III. The Wall Street Seduction & The Lehman Gamble

The seduction began with deregulation. On October 27, 1986, London's financial markets underwent the "Big Bang" — a sweeping liberalisation that abolished fixed commissions, tore down the wall between stockbrokers and market-makers, and threw the clubby, gentlemanly City open to global competition. For a deposit-rich commercial bank like Barclays, Big Bang was an invitation to build an investment bank from scratch by buying the expertise it lacked. It moved quickly, acquiring the stockjobber Wedd Durlacher and the stockbroker de Zoete and Bevan and fusing them into Barclays de Zoete Wedd — BZW.6

BZW was an ambition ahead of its execution. Through the 1990s it struggled to break into the bulge bracket, and in 1997 Barclays largely dismembered it, selling the equities and advisory arms and keeping the debt business. Out of that remnant, a single relationship-driven American executive built something formidable. Bob Diamond, a Massachusetts-born former Morgan Stanley and Credit Suisse First Boston banker with a taste for risk and a genius for hiring, took the surviving fixed-income unit and rebranded it Barclays Capital — "BarCap."6 Diamond's insight was that a bank sitting on Barclays' funding base and balance sheet could dominate debt markets — bond underwriting, interest-rate and credit trading — without needing the ego-driven equities and M&A businesses. Through the early 2000s, BarCap grew into one of the world's premier fixed-income houses. But Diamond wanted the full bulge bracket. He wanted equities. He wanted advisory. He wanted America.

He got all three in a single weekend of chaos. To understand the drama, set the scene. The weekend of September 13–14, 2008, is one of the most storied in modern financial history: US Treasury Secretary Hank Paulson and New York Fed President Tim Geithner had summoned the heads of Wall Street to the Federal Reserve's downtown Manhattan fortress to find a buyer for the dying Lehman Brothers before Monday's market open. Barclays was the leading bidder for the whole firm. Diamond and chairman Marcus Agius wanted it. The deal was, by several accounts, within touching distance — and then it died on a regulatory technicality. Britain's Financial Services Authority would not waive the requirement for a Barclays shareholder vote to guarantee Lehman's trading obligations, and the US authorities would not backstop the gap. Without a guarantee, no deal. Lehman filed for bankruptcy in the early hours of Monday, September 15, 2008, triggering the most violent phase of the global financial crisis.

And that failure turned out to be Barclays' opportunity. In mid-September 2008, Lehman Brothers — the 158-year-old fourth-largest US investment bank — collapsed into the largest bankruptcy in American history. Because Barclays had walked away from the whole company, it could now come back and cherry-pick the good parts from the bankruptcy estate, free of the liabilities that had scared the regulators off days earlier. On September 16–17, 2008, Diamond and his team negotiated the purchase of Lehman's North American investment banking and capital markets business out of bankruptcy for roughly $1.75 billion — a price that included Lehman's gleaming midtown Manhattan headquarters at 745 Seventh Avenue and its trading operations, but left the toxic assets behind in the bankrupt estate.7 The deal was struck in a matter of days, closed within a week, and by the following Monday Barclays' name was going up over a Wall Street tower that had, seven days earlier, belonged to one of its fiercest rivals.

Think about what that price represented. Barclays acquired a top-tier US equities platform, a coveted mergers-and-acquisitions advisory franchise, and a fixed-income operation — plus about 10,000 employees and a trophy skyscraper — for less than the cost of the building alone in a normal market. It was, on the surface, one of the great opportunistic bargains in banking history: a distressed buyer stepping into a once-in-a-generation dislocation. Diamond had, in a single stroke, catapulted Barclays into the bulge-bracket elite in the world's deepest capital market. The strategic logic was seductive and, in a vacuum, sound.

But the deal was not free — it just deferred the bill. Integrating and capitalising a Wall Street investment bank in the teeth of the worst financial crisis since the Depression required capital, and Barclays faced a fateful choice. Its UK peers, Royal Bank of Scotland and Lloyds, were taking government bailouts and effective nationalisation. Barclays' leadership was determined to stay out of state hands and keep its strategic freedom. So instead of the Treasury, it turned to the Gulf. In a series of emergency fundraisings in 2008, Barclays raised billions — ultimately more than £7 billion in the pivotal autumn round — from Qatari and Abu Dhabi sovereign investors, on terms so expensive (fat coupons, warrants, and fees) that they would later become the subject of years of litigation and criminal proceedings over whether the arrangements had been properly disclosed.8

That decision to avoid nationalisation is one of the defining forks in this entire history, and it is worth weighing both sides honestly. On one hand, it preserved Barclays' independence and its investment-banking ambitions — the very things RBS and Lloyds were forced to surrender when the UK government took majority stakes. Barclays kept its own board, its own strategy, and the freedom to build on the Lehman prize while its bailed-out rivals spent the next decade shrinking under state supervision. On the other hand, the Gulf fundraising carried a long tail of legal risk. For years afterward, the UK's Serious Fraud Office pursued criminal charges over whether Barclays had properly disclosed the fees and side-arrangements — including advisory payments to Qatari entities — attached to the capital raises. The corporate charges were ultimately dismissed and individual defendants acquitted, but the episode consumed management attention and reputation for the better part of a decade, and it is a reminder that "avoiding the government" was not the free lunch it looked like in the autumn of 2008.8

More consequentially, the decision locked in a strategic commitment to Wall Street at the precise moment the regulatory world was turning against exactly that kind of risk-taking. In the years after 2008, Basel III and its successors would demand that banks hold far more capital against trading assets — the regulators' post-crisis answer to "too big to fail" was to make big, risky balance sheets expensive to run. The franchise Diamond had bought for a song would prove ravenous for that capital, and the returns it could generate on that swollen capital base would, for years, disappoint. The identity crisis was born. Inside one holding company now lived a high-return, low-risk British utility and a low-return, high-risk American trading house, feeding from the same balance sheet and forever competing for the same scarce capital. The next fifteen years would be a war over which one won — and the first shots would be fired not by an activist or a regulator, but by a scandal buried in the plumbing of the interest-rate market.

IV. Scandals, Activism, and the Staley-Bramson War

The reckoning came for Bob Diamond first, and it came from an obscure corner of the plumbing of global finance. To grasp why Libor mattered, you have to know what it was. The London Interbank Offered Rate was a single number, published each day, that purported to measure the interest rate at which big banks could borrow from one another. It sounds technical and it was — but that number sat underneath an estimated hundreds of trillions of dollars of contracts worldwide: adjustable mortgages, corporate loans, student debt, and vast quantities of interest-rate derivatives all reset off Libor. And here was the flaw: Libor was not observed from actual transactions but submitted by a panel of banks, each reporting where it thought it could borrow. That made it manipulable. In June 2012, regulators in the UK and US revealed that Barclays traders had, for years, nudged those submissions — sometimes to profit their own derivative positions, sometimes, during the crisis, to make the bank look healthier than it was by lowballing its borrowing cost. Barclays was the first bank to settle, agreeing to pay roughly £290 million in fines to UK and US authorities.9

Being first was supposed to earn leniency; instead it made Barclays the face of a scandal that would eventually ensnare more than a dozen global banks. The political firestorm was immediate and ferocious. Emails surfaced in which traders thanked colleagues for favourable submissions with offers of champagne; the phrase became shorthand for a banking culture that had lost its ethical bearings. Within days Diamond — the highest-profile, highest-paid banker in Britain, the American who had built BarCap and bagged Lehman and come to symbolise the industry's swagger — was hauled before a parliamentary committee and then forced to resign. The man who had spent two decades arguing that Barclays could beat Wall Street at its own game was gone, undone not by a trading loss but by a culture problem that ran straight through the franchise he had built.

What followed was a violent swing of the pendulum toward contrition. The board installed Antony Jenkins, a career retail banker who had run Barclaycard and the UK consumer business — a man so associated with ethical rehabilitation that the press nicknamed him "Saint Antony." From 2012 to 2015, Jenkins preached cultural reform, cut costs, shrank parts of the investment bank, and tried to rebuild trust. But the board grew impatient. Jenkins was seen as the right leader for the apology and the wrong leader for the recovery; his instincts ran against the trading business that still generated much of the group's revenue. In 2015 he was pushed out, and Barclays reached, once again, for a Wall Street heavyweight.

Jes Staley arrived in December 2015 carrying more than three decades of JPMorgan pedigree. He had run JPMorgan's investment bank and its asset-management arm, and he arrived at Barclays as a man who had spent his career inside the American universal-banking model that Jamie Dimon had perfected — a model where a fortress balance sheet, a giant consumer bank, and a world-beating trading and advisory operation reinforced one another. Staley did not merely tolerate Barclays' investment bank; he believed in it with the conviction of a convert defending the true faith. His entire strategic thesis was that a diversified bank spanning retail, cards, corporate, and a full-service investment bank is stronger than the sum of its parts, because the pieces zig when others zag — retail earnings are steady when markets are calm, and trading earnings spike when markets are chaotic, so the group's returns are smoother than either business alone.

He spent his tenure defending the investment bank against a chorus of critics who wanted it gone, arguing that trading and advisory were not a distraction from the retail franchise but its natural complement. It was a coherent thesis, and Staley pursued it with a stubbornness that would define his tenure — reinvesting in the trading business, resisting pressure to shrink it, and staking his credibility on the claim that a British-headquartered bank could hold its own in the American-dominated bulge bracket. The problem was that the numbers, for most of his tenure, refused to cooperate: the investment bank kept consuming capital and kept returning less on it than the retail arm, and the stock kept trading below book. Into that gap of underperformance stepped exactly the kind of investor who lives to exploit it.

That conviction was about to be tested by one of the most persistent activist campaigns in British corporate history. In 2018, Edward Bramson — a low-profile, hard-nosed activist investor running a vehicle called Sherborne Investors — began building a stake in Barclays that would reach around 5–6%, making him one of the largest shareholders.10 Bramson's thesis was the mirror image of Staley's, and it was brutally simple. The investment bank, he argued, was a capital-devouring black hole: it consumed the majority of the group's risk-weighted assets while generating a return on equity far below what the retail and cards businesses earned. Every pound trapped in the trading business was a pound not being returned to shareholders or deployed in higher-returning lending. That misallocation, Bramson insisted, was the entire reason the stock languished below tangible book value. His prescription: shrink the investment bank dramatically, or spin it off, and let the market re-rate the high-quality remainder.

Bramson was not a headline-grabbing activist in the Carl Icahn mould. He was quiet, secretive, and patient — an investor who built positions carefully and pressed his case in private letters and boardroom meetings rather than in the financial press. That style made him harder to dismiss, because he was not performing for an audience; he genuinely believed he had spotted a structural mispricing that Barclays' own board was too conflicted or too sentimental to fix. His demand was specific: shrink the investment bank's capital consumption dramatically, and the freed-up capital would flow to shareholders and to the higher-returning businesses, and the stock would re-rate. It was, in essence, a bet that the whole was worth less than the parts — the classic sum-of-the-parts activist play.

For three years, the two men fought a slow-motion war of proxy fights, letters, and boardroom lobbying. Bramson sought a seat on the board and was rebuffed by shareholders, who — crucially — sided with management and declined to force the break-up. Staley dug in. And then, in 2020, reality delivered its verdict — though not the one Bramson expected. When the COVID-19 pandemic hit and the global economy locked down, the retail and cards businesses had to set aside enormous provisions against the wave of loan losses everyone assumed was coming, exactly as a downturn would predict. But the investment bank, far from being a liability, exploded higher: central banks flooded markets with liquidity, companies rushed to raise debt and equity, and volatility sent trading volumes soaring. The very cyclicality of the trading business that Bramson decried became the shock absorber that offset the retail provisions, and group earnings held up when a pure-play retail bank's would have cratered.

It was, for Staley, a live and almost theatrically well-timed demonstration of the diversification thesis he had staked his career on. In May 2021, Bramson threw in the towel and sold his roughly 6% stake, reportedly at a loss on the multi-year campaign.10 The universal-bank defenders had, for the moment, won the argument — the diversification worked exactly when it was supposed to. But here is the subtlety that the modern strategy would later exploit: winning the argument that the investment bank is useful is not the same as winning the argument that it earns an adequate return on the capital it ties up. Bramson lost the battle over whether to keep the investment bank. He did not really lose the war over whether it was allocating capital efficiently — that critique would survive his exit and quietly shape everything Venkat did next.

The victory was hollow. Just six months later, in November 2021, Staley abruptly resigned. The trigger had nothing to do with strategy: the UK's Financial Conduct Authority and Prudential Regulation Authority had been investigating how Staley characterised his historical relationship with the convicted sex offender Jeffrey Epstein to the Barclays board, and the preliminary findings were damaging enough that his position became untenable.11 In one of the more consequential accidents of succession in modern banking, the board turned to the sitting group chief risk officer — a quiet, mathematically-minded former JPMorgan colleague of Staley's named C.S. Venkatakrishnan. Barclays had spent a decade oscillating between flamboyant dealmakers and penitent reformers. Now it handed the wheel to a risk manager. The tonal shift could not have been sharper, and it would define everything that came next.

V. Inside the Machine: Segment Analysis & The Profit Engine

For years, Barclays reported itself in a way that made the Bramson debate almost impossible to adjudicate from the outside. Its old structure lumped businesses into a few broad segments that blurred the very economics investors most wanted to see: which parts earned their cost of capital and which parts destroyed value. On February 20, 2024, Venkat changed that. He blew up the old model and re-cut the group into five reporting divisions, each with its own disclosed returns, so that anyone could finally see the machine's internals.3 This was as much a governance act as an accounting one — you cannot hold managers accountable for capital discipline in businesses whose returns are hidden inside a blended average.

The first and most important division is Barclays UK — the ring-fenced retail bank, the direct descendant of those Lombard Street goldsmiths. This is the defensive engine: current accounts, savings, UK mortgages, and Barclaycard consumer lending, sitting on that deep, cheap deposit base. It is the highest-quality business in the group, capable of returns on tangible equity in the mid-to-high teens, and it benefited enormously from higher interest rates. Its vulnerability is the reverse of its strength: as fixed-rate mortgages roll over and competition on deposits intensifies, the net interest margin — the spread the bank earns — can compress. Barclays manages this partly through a "structural hedge," a portfolio of interest-rate positions that smooths the earnings impact of rate moves over several years, so that even if rates fall, the income rolls down gradually rather than falling off a cliff.4

Second is Barclays UK Corporate Bank, serving mid-market and larger UK companies with lending, transaction banking, deposits, and treasury services. Its appeal is capital efficiency and stickiness: corporate treasury relationships are notoriously hard to move once a company has wired its payroll, payments, and cash management through a bank's plumbing. Third is Barclays Private Bank and Wealth Management, a capital-light, fee-driven business serving wealthy clients. It earns high returns precisely because it consumes little balance sheet — but here honesty requires noting the ceiling: Barclays' wealth arm is subscale next to the Swiss and American giants that dominate global private banking, and it has not been the group's growth story.

Fourth is Barclays US Consumer Bank, the credit-card business built around partnerships — co-branded cards with American brands such as American Airlines, JetBlue, and Gap. The model is elegant in theory: piggyback on a partner's customers and brand to acquire cardholders cheaply, then earn high yields on the balances. There is a genuine irony here, because this business is itself a legacy of the Lehman-era American expansion — a beachhead in US consumer finance that Barclays has kept and grown even as it debates the rest of its American footprint. But it is a tough neighbourhood. US card lending is fiercely competitive, dominated by domestic giants like JPMorgan Chase, Capital One, and Synchrony, and structurally exposed to the charge-off cycle — when the economy weakens, delinquencies and write-offs on unsecured card debt rise fast, and a partnership book can swing from profit to pain. It is also a business where the partner holds real negotiating leverage at renewal time, and where the economics of any single co-brand deal depend on how the rewards, fees, and loss-sharing are carved up. In the group's five-box scorecard, this is the division whose returns are most hostage to the American consumer's balance sheet.

Fifth is the Barclays Investment Bank — the capital guzzler, the inheritance of Diamond and Lehman, and the reason for the entire discount. At the time of the 2024 overhaul, the investment bank consumed roughly 58% of the group's risk-weighted assets while generating returns on tangible equity that hovered in the high single digits — often below the group's cost of equity.3 Risk-weighted assets, or RWAs, are the regulator's measure of how much risk a bank's assets carry; the more RWAs a business uses, the more expensive capital it must hold against them. The investment bank's problem, in one sentence, was that it used more than half the group's scarce capital to earn some of the group's lowest returns.

And yet — and this is the nuance Bramson's thesis underweighted — the investment bank is not a bad business; it is a low-return, high-optionality business with genuine scale. In fixed income, currencies and commodities trading (FICC) and in debt underwriting, Barclays is the only non-American bank to consistently rank among the global top six, a scale position that competitors cannot easily replicate and that becomes extraordinarily valuable in exactly the moments — market dislocations, volatility spikes — when everything else is going wrong.1

So here is the core economic tension that this entire company has been organised around: a single, capital-hungry division with mediocre average returns and enormous scale was cannibalising the capital that the mid-to-high-teens UK businesses could have used to grow. The market, unable to give the good businesses full credit while they were shackled to the capital hog, applied its discount to the whole. Venkat's five-division disclosure did not solve that tension — but by exposing it, line by line, it set up the only plausible solution: change how capital is allocated among these five boxes. That is the subject of the next chapter.

VI. Capital Allocation, Strategic Pivots & UK M&A

Venkat's answer to the Bramson dilemma was neither surrender nor amputation. It was a diet. Rather than sell the investment bank — which would have meant giving up genuine scale at a cyclical low and crystallising the discount as a permanent loss — he chose to cap it. The commitment announced in February 2024 was to hold the investment bank's risk-weighted assets broadly flat in absolute terms while the rest of the group grew, mechanically shrinking the investment bank's share of group RWAs from around 58% toward roughly 50% by 2026.3 Every marginal pound of capital the group generated would be steered away from the trading floor and toward the higher-returning UK consumer and corporate businesses.

This is a genuinely clever piece of capital allocation, and it is worth pausing on why. It does not require Barclays to shrink the investment bank or forgo its optionality; the trading business keeps its scale and its ability to feast in volatile markets. What changes is the marginal decision: growth capital flows to where returns are highest. Over time, that arithmetic alone lifts the group's blended return, because a rising share of equity sits in mid-teens businesses rather than high-single-digit ones. It is the financial equivalent of steering a supertanker by adjusting only the new water it displaces — slow, but inexorable if you hold the line.

The elegance also contains the plan's central vulnerability, and an honest analysis has to sit with it. Holding the investment bank's absolute RWAs flat is easy to promise in a deck and hard to honour in the wild. Trading balance sheets breathe with market conditions; a surge in client activity or a spike in volatility can inflate risk-weighted assets almost mechanically, and the temptation to let them run — to "just this once" capture the revenue a hot market is offering — is exactly the temptation that produced the bloated investment bank in the first place. So the RWA glide-path is not merely an accounting target; it is a behavioural commitment, and it will be tested precisely when it is most lucrative to break. This is why the investment bank's share of RWAs is one of the KPIs to watch: it is the single cleanest read on whether the diet is real or rhetorical.

To feed the UK-tilt, Barclays turned to acquisitions, and two deals show the strategy in miniature. The first was Kensington Mortgages, the specialist UK residential lender Barclays agreed to buy from Blackstone and Sixth Street, completing the roughly £2.4 billion acquisition in March 2023.[^12] Kensington's expertise is lending to borrowers the mainstream mortgage machine handles poorly — the self-employed, people with complex or multiple income streams. That is a higher-yielding niche, and crucially it let Barclays lean into better-priced mortgage lending without simply chasing volume in the cut-throat prime market. It was a considered way to buy yield and capability rather than just balance sheet.

The second deal was the more revealing bargain. In November 2024, Barclays completed its acquisition of the retail banking business of Tesco Bank for around £600 million.12 Look at what that £600 million bought: roughly £8.3 billion of deposits, about £4.2 billion of credit-card balances, and around £4.2 billion of unsecured personal loans, together with an exclusive ten-year partnership to market financial products under the trusted Tesco brand to the supermarket's vast customer base.1213 The economics are the whole point. Barclays acquired a high-yielding, deposit-funded consumer book — precisely the kind of low-cost-funded, high-return asset that sits in the sweet spot of Barclays UK — and it paid a price that looks modest against the book's earning power. The deposits alone are strategically valuable: cheap, sticky funding is the scarcest resource in banking. In one transaction, Barclays did exactly what the whole strategy demanded — it added scale to the high-returning UK consumer bank and tilted the group's capital mix toward the profitable end.

A skeptical investor should still ask the hard questions. Bank M&A is where value goes to die more often than it is created; integration is messy, and the Tesco and Kensington books both concentrate exposure to the UK consumer at a moment when higher interest rates were testing household budgets. The bull answer is that both deals were small relative to the group, priced conservatively, and directly on-strategy rather than empire-building. So far, that is the more persuasive reading — but it is a claim about execution that only time and the credit cycle can fully validate.

Underpinning all of this is the capital-return promise, which is where the discount becomes an asset rather than a liability. Barclays committed to return at least £10 billion to shareholders over 2024–2026 through dividends and, above all, buybacks.3 Here the sub-book valuation flips from insult to opportunity, and the mechanism is worth spelling out because it is the quiet engine of the bull case. Tangible book value per share is simply the bank's net tangible assets divided by the number of shares outstanding. When a company buys back its own stock at roughly half of tangible book value, it spends fifty pence of cash to retire a pound of net assets — which means the assets left behind are now spread over fewer shares, and the tangible book value per remaining share goes up. Do that consistently, quarter after quarter, and every long-term holder's claim on the bank's assets compounds, entirely independent of what the share price does. A buyback executed above book value destroys per-share value; a buyback executed at half of book is one of the most accretive things a management team can do with a pound. Barclays has been doing it at scale.

The bank delivered £3.0 billion of distributions for 2024 and stepped that up to £3.7 billion for 2025 — the latter comprising £1.2 billion of dividends and £2.5 billion of buybacks — keeping the three-year, at-least-£10-billion plan firmly on track.144 The skew toward buybacks over dividends is itself a statement: it says management believes the stock is cheap enough that repurchasing it is a better use of capital than simply handing cash back. The clearest evidence that management believes its own re-rating thesis, in other words, is not what it says on the calls — it is that it has been aggressively shrinking the share count while the stock trades below book. Actions here are more credible than words, and the action has been consistent.

VII. Current Management & Credibility Audit

C.S. Venkatakrishnan is, by temperament and training, the anti-Diamond. Where Bob Diamond was a relationship-driven dealmaker who bought a Wall Street franchise in a weekend, and Jes Staley was a charismatic universal-banking evangelist, Venkat is a mathematician and a risk manager. Born in India and educated as an engineer before earning a doctorate in electrical engineering and computer science at MIT, he came to finance through the quantitative side — the world of models, risk factors, and probability distributions rather than client dinners and league tables. He spent much of his career at JPMorgan, where he ran the models-and-analytics function and later served in senior risk roles, before following Staley to Barclays and rising to group chief risk officer. When Staley abruptly departed, the board handed Venkat the top job in the scramble that followed.11

He is precise, low-key, and analytical — the kind of executive who talks in terms of return distributions and capital allocation rather than trophy deals, and who is temperamentally suited to a plan whose whole logic is disciplined, incremental capital re-allocation rather than a single bold stroke. There is a neat symbolism here. The two crises that most damaged Barclays — the Lehman-era risk appetite and the Libor culture — were failures of risk management dressed up as ambition. For a bank with that pathology, installing the risk officer as chief executive was either poetic justice or exactly the medicine required. The market's initial reaction was skeptical — Venkat was an unknown quantity with no CEO track record and, within months of taking over, a serious cancer diagnosis to manage — which arguably makes the subsequent delivery record all the more consequential for his credibility.

Personal credibility for Venkat is complicated by health: in 2022 he disclosed a diagnosis of non-Hodgkin lymphoma and continued to run the bank through treatment, later confirming his recovery. That candour, and his continuity through it, arguably reinforced rather than undermined confidence in the plan. On compensation, Venkat's total pay for 2024 was disclosed at £10.53 million — comprising a base salary of around £2.9 million, an annual bonus of roughly £2.2 million, and long-term incentive awards of about £5.1 million — with the incentive structure explicitly tied to hitting the RoTE target and cost-efficiency goals.15 Aligning the bulk of pay to a hard RoTE hurdle is the right design in principle; the fair critique is that RoTE can be flattered in the short run by buybacks and by a benign credit environment, so the quality of the returns matters as much as the headline number.

The real test of any management team is not the strategy deck — anyone can draw a bridge to 12% RoTE — but whether it does what it said it would do, on time, quarter after quarter. On this measure, the Venkat era has so far built a genuine track record. For 2024, Barclays delivered a 10.5% RoTE against a target of "greater than 10%," and reported a CET1 capital ratio of 13.6%, comfortably inside its 13–14% target range.14 For 2025, it went further: group RoTE reached 11.3%, ahead of an upgraded target of around 11%, on total income of £29.1 billion (up 9%) and profit before tax of £9.1 billion (up 13%), with the cost-to-income ratio improving to 61% and the CET1 ratio strengthening to 14.3%.4 Meeting or modestly beating guidance two years running, after a decade in which the bank's promises were routinely overtaken by scandals and strategy reversals, is precisely how credibility is rebuilt: not with rhetoric, but with a boring, repeated pattern of hitting the number.

It is worth listening to how management narrates this on the calls themselves, because tone is evidence. Across the 2024 and 2025 results presentations, the striking thing about Venkat and finance chief Anna Cross is how deliberately unexciting they are. They talk in terms of the plan's specific milestones, the structural hedge's contribution to income, and the mechanics of the RWA glide-path — not in the sweeping, visionary register that Diamond and Staley favoured. When analysts press on the softer spots — a quarter where investment-bank revenue lagged US peers, or where a revenue line missed consensus even as profit beat — the answers tend to be concrete and framed against the multi-year targets rather than deflected. That consistency of language across successive calls is itself a credibility signal: management is telling the same story in the same terms it told a year earlier, and then pointing to the delivered numbers. The contrast with the Barclays of the 2010s, whose narrative lurched with each new CEO and each new scandal, is the whole point.

There is one narrative wrinkle worth flagging honestly. The February 2024 plan leaned heavily on cost efficiency, and management set out gross cost-savings ambitions (on the order of around £2 billion of gross efficiency savings across the 2024–2026 plan) as a core lever.3 The clean, verifiable evidence of progress is the falling cost-to-income ratio and the positive "jaws" (income growing faster than costs) the bank reported — a more reliable signal than any single gross-savings figure, which can be obscured by reinvestment and inflation.4 The honest analytical posture is to watch the ratio, not the press-release adjective.

That brings us to the trust-damaging pattern investors should keep watching. Barclays' history is littered with moments when the board's appetite for investment-banking scale overrode capital discipline — the Lehman grab, the defence of the trading business against Bramson, the recurring temptation to chase Wall Street league-table glory. The single most important behavioural question for the years ahead is whether management holds the capital diet if global dealmaking and trading volumes surge. A booming market is precisely when it is hardest to keep the investment bank's RWAs flat, because every extra pound of trading capital looks, in the moment, like free money. Discipline in a bull market, not in a downturn, is the real test of whether this leadership team is different from its predecessors.

VIII. The Playbook: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Strip away the narrative and ask the cold question a strategist would: what, if anything, structurally protects Barclays' profits from competition? Two frameworks help — Hamilton Helmer's 7 Powers, which catalogues the sources of durable advantage, and Michael Porter's Five Forces, which maps the competitive pressures on an industry.

Start with Helmer's scale economies, the clearest of Barclays' powers. In UK clearing and payments, Barclays operates at a size that spreads enormous fixed costs — regulatory, technology, branch and compliance infrastructure — across a vast base of accounts and transactions. That scale is what makes the deposit base cheap, and cheap funding is a cost advantage a smaller competitor structurally cannot match. In the investment bank, scale works differently but no less powerfully: in global debt and equity capital markets, Barclays functions as a high-volume clearing hub, and in flow trading, the firm that sees the most order flow prices risk best and earns the tightest spreads. A sub-scale trading desk simply cannot compete on either price or the ability to warehouse large risk — which is precisely why so many European rivals retreated from Wall Street and Barclays did not.

Second is switching costs, Helmer's power of the sticky customer. A corporate treasury account, once wired into a bank's cash-management, payments, and lending relationships, is painful and risky to move — the finance team has better things to do than re-plumb the company's entire money flow to save a few basis points. Retail current accounts are stickier still; despite years of regulators trying to make switching frictionless, most Britons never move their primary account. These switching costs are what keep the deposit base interest-rate-insensitive, and therefore cheap, and therefore profitable.

Third, and most interesting, is counter-positioning, which the Tesco partnership illustrates well. By marketing cards and loans under a dominant retailer's brand, Barclays captures high-margin unsecured lending yield without building or maintaining the branch network and marketing apparatus a traditional bank would need to acquire those customers. An incumbent competitor cannot easily copy this without cannibalising its own direct-to-consumer economics — the essence of counter-positioning, where the challenger's model is one the incumbent is structurally reluctant to imitate.

Now Porter, focused on the UK retail and corporate arena where Barclays' best economics live. The threat of new entrants is low, and this is the underappreciated moat. Ring-fencing rules (which legally wall off UK retail operations), stringent Basel capital requirements, and the sheer friction of gathering sticky deposits form a formidable barrier. The much-hyped digital challengers — Monzo, Revolut, Starling — have won current accounts and dazzled on user experience, but they have struggled to take meaningful share in the profitable, long-duration, capital-intensive businesses of mortgage and corporate lending, where balance-sheet strength and regulatory capital, not app design, decide the winner.

Rivalry among competitors is high, and it is the force that most directly squeezes returns. The UK "Big Four" — Barclays alongside Lloyds, NatWest, and HSBC — compete fiercely, above all on mortgage pricing, and that price competition compresses net interest margins for everyone. This is why UK retail banking, for all its defensiveness, is not a fat-margin oligopoly but a grinding, share-conscious contest. Finally, the bargaining power of customers rises in high-rate environments: when savings rates climb, depositors wake up and shift idle current-account balances into higher-yielding accounts, forcing banks to "pay away" more of their margin to retain funding. The stickiness of the deposit base slows this migration but does not stop it — which is the standing caveat on the "cheap funding forever" story.

The net read is that Barclays' moat is real but uneven: genuinely strong in scale and switching costs on the UK side, more contestable in the investment bank (where returns are a function of the cycle and league-table position rather than any durable pricing power), and everywhere subject to the intense rivalry of a mature market. That mixed picture is exactly what sets up the bull-bear debate.

IX. Analysis: Bull vs. Bear Case & Key KPIs

The bull case is, at its heart, a re-rating story, and it is refreshingly concrete. If Venkat delivers the above-12% RoTE for 2026 and holds the investment bank near half of group RWAs, the logical consequence is that a growing share of Barclays' equity will be earning mid-teens returns, and a bank that consistently earns comfortably above its cost of equity has no business trading at half of tangible book. The comparison that animates bulls is Lloyds — a cleaner, more retail-focused UK bank that has traded closer to, or above, tangible book value. If Barclays can demonstrate that its blended returns are approaching pure-play quality, the argument goes, the conglomerate discount should narrow toward peer multiples. And while investors wait, the buybacks do compounding work: retiring stock at roughly half of book is one of the most mechanically value-accretive uses of capital available to any company, quietly lifting per-share book value with every quarter the discount persists.

The bear case is equally concrete, and it clusters around the same word that has haunted this story throughout: volatility. The investment bank remains more than half of group RWAs, and its earnings are hostage to markets. A severe global correction or a credit freeze could hollow out trading and underwriting revenue in a single bad quarter and drag group returns back below the cost-of-capital line — undoing years of narrative repair. That is the tail risk the whole diversification argument is supposed to manage, but "supposed to" is doing heavy lifting: 2020 showed the hedge working, but no two crises are alike. Layer on credit-cycle risk: the same higher interest rates that fattened net interest income also strain borrowers, and rising defaults in US co-branded cards or in the specialist Kensington and consumer books could feed straight into loan-loss provisions. The US card book is the sharpest edge here — high-yield, high-charge-off, and fiercely competitive — and a delinquency spike there could neutralise a meaningful slice of UK profitability. The activist stress-test that Bramson articulated has not been retired so much as deferred: a skeptic can still argue that a bank this complex, straddling a British utility and an American trading house, will always carry a structural discount for the sheer difficulty of valuing and governing the two together.

It is worth naming the competitive backdrop explicitly, because Barclays does not operate in a vacuum. Against the US bulge bracket, Barclays is a scale player but not a leader — its investment bank competes for the same mandates as firms with deeper US corporate relationships and, in many years, higher returns. Against its UK peers, the picture inverts: Lloyds is a purer, simpler bet on the British consumer and mortgage market; NatWest is a similar domestic story that spent years working off government ownership; HSBC is a fundamentally different animal, a pan-Asian trade-finance giant whose fortunes track China and global commerce more than the British high street. Barclays is the only one of the four that straddles both a genuine UK retail franchise and a genuine Wall Street trading house — which is exactly why it is the hardest of the four to value and the one that carries the most persistent discount. The bull case is that this straddle is a misunderstood strength; the bear case is that it is a permanent conglomerate penalty that no amount of execution fully cures.

Myth versus reality. Three consensus narratives deserve a fact-check before the KPIs. The first myth is that "the investment bank is dead weight that should be sold." Reality: 2020 demonstrated it can be a genuine stabiliser, and its top-six scale in FICC and debt underwriting is a real, hard-to-replicate asset — the honest critique is not that it should be sold but that its returns on capital have lagged, which is a different and more fixable problem. The second myth is that "Barclays is a cheap UK retail bank in disguise, and the re-rating is just a matter of time." Reality: more than half of group risk lives in a cyclical trading business, so the discount is not purely irrational — it partly prices genuine earnings volatility that a pure retail bank does not carry. The third myth, popular during the rate-hiking cycle, is that "higher rates are an unambiguous tailwind." Reality: higher rates lifted net interest income but also raised the risk of consumer defaults in the card books and eventually invite deposit competition that erodes the very margin they inflated. Each of these is a case where the bull and the bear are both citing real facts and drawing opposite conclusions — which is exactly why the story is unresolved.

Which case wins is, ultimately, an empirical question, and the beauty of the "Simpler, Better, More Balanced" plan is that it is falsifiable — it lives or dies on a small number of hard numbers. Three KPIs matter above all others, and a long-term investor should track them and little else:

First, Group Return on Tangible Equity. This is the master metric — the single number that determines whether Barclays earns its cost of capital and therefore whether the discount is deserved. The target is above 12% for 2026; the bank posted 11.3% for 2025.4 The gap between those two numbers is the entire remaining bull-bear debate in miniature.

Second, the Investment Bank's share of Group RWAs. This is the cleanest measure of whether management is actually holding the capital diet rather than just talking about it. The target is roughly 50% by 2026, down from about 58% in 2023.3 If this ratio drifts back up in a trading boom, the discipline thesis is broken, regardless of what any given quarter's profit looks like.

Third, the CET1 ratio alongside the pace of capital returns. Barclays has committed to run CET1 in a 13–14% range while returning at least £10 billion to shareholders across 2024–2026.3 Watching capital strength and distributions together tells you whether the returns are being funded by genuine capital generation or by running the balance sheet too thin — the difference between sustainable value creation and financial engineering. At the end of 2025, CET1 stood at 14.3%, the strong end of the range, which is the reassuring reading.4

Everything else — quarterly trading revenue, individual product margins, a single acquisition's integration — is noise around these three signals. Get these three right and the re-rating largely takes care of itself; get them wrong and no amount of narrative will hold the discount closed.

X. Epilogue & Outro

The arc of this story is a bank learning, painfully and over more than a decade, that ambition without discipline destroys value. Barclays spent the post-crisis years as the great striver of European banking — the one firm that refused to retreat from Wall Street, that took Gulf money rather than government money to keep its independence, that defended its trading floor against an activist and a pandemic and its own reputational disasters. All of that produced scale and optionality, and also a half-of-book valuation that told the striver, in the bluntest possible language, that the market did not believe the two halves belonged together.

The "Simpler, Better, More Balanced" plan is best understood not as a grand vision but as a pragmatist's compromise — a settlement of the fifteen-year civil war between the high street and Wall Street. It rejects management's old hubris (that the full investment bank must be preserved at any cost to the rest of the group) and it rejects activist dogma (that the trading business must be amputated at a cyclical low). In their place it offers something less dramatic and more durable: keep the optionality, but stop feeding it; grow the good businesses; buy back cheap stock; and let disciplined capital allocation, compounded over years, do what fifteen years of strategic drama could not.

The evidence through mid-2026 is that this quieter approach is working better than the noisy one it replaced. Two consecutive years of meeting or beating guidance, a rising RoTE, a strengthening capital ratio, and on-strategy acquisitions have begun to rebuild the credibility that Libor, Epstein, and the Bramson war corroded. Tellingly, having hit its 2025 marks, management raised the bar again — pointing beyond the 2026 goalposts toward an above-14% RoTE by 2028 and more than £15 billion of shareholder distributions across 2026–2028.16 That is the sound of a team that believes the machine now runs the way it promised.

But the ultimate lesson of Barclays is that capital allocation inside a global financial giant is never finished. The investment bank still sits at the centre of the balance sheet, cyclical and capital-hungry as ever, and the deepest question — whether this leadership holds its discipline when the next bull market makes indiscipline look like genius — cannot be answered by any deck or any single year's results. It can only be answered by behaviour, over time, through a full cycle. Barclays has re-earned the right to be taken seriously. Whether it has finally learned to say no to itself is the story the next few years will tell.

References

-

Barclays PLC Annual Report 2024 — Barclays PLC, 2025-02-19 ↩↩

-

Barclays Launches Major Overhaul and Capital Return Strategy — Bloomberg, 2024-02-20 ↩↩↩↩↩↩↩↩↩

-

Barclays PLC 2025 Results Announcement — London Stock Exchange, 2026-02-09 ↩↩↩↩↩↩↩↩

-

Barclays Investor Relations Hub (company history) — Barclays PLC ↩↩↩↩↩

-

The death of Bob Diamond's dream for Barclays — Fortune, 2012-07-30 ↩↩

-

The death of Bob Diamond's dream for Barclays (Lehman acquisition) — Fortune, 2012-07-30 ↩

-

Barclays Fined £290 Million Over Libor Manipulations — Reuters, 2012-06-27 ↩

-

Edward Bramson's Sherborne Investors Exits Barclays Campaign — Financial Times, 2021-05-14 ↩↩

-

Barclays CEO Jes Staley Steps Down Over Epstein Inquiry — Financial Times, 2021-11-01 ↩↩

-

Completion of Acquisition of Tesco Bank Business — London Stock Exchange, 2024-11-01 ↩↩

-

Disposal of Tesco Bank Business to Barclays — Tesco PLC, 2024-11-01 ↩

-

Barclays PLC FY 2024 Results and Progress Update — Barclays PLC, 2025-02-13 ↩↩

-

Barclays CEO C.S. Venkatakrishnan FY2024 Remuneration Disclosures — Barclays PLC, 2025-02-19 ↩

-

Barclays Hits All Financial Targets with 11.3% RoTE and Eyes >14% Returns by 2028 — BigGo Finance, 2026-02-10 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube