BAE Systems: The Sovereign Shield and the Compounding Defense Prime

I. Introduction & Episode Roadmap

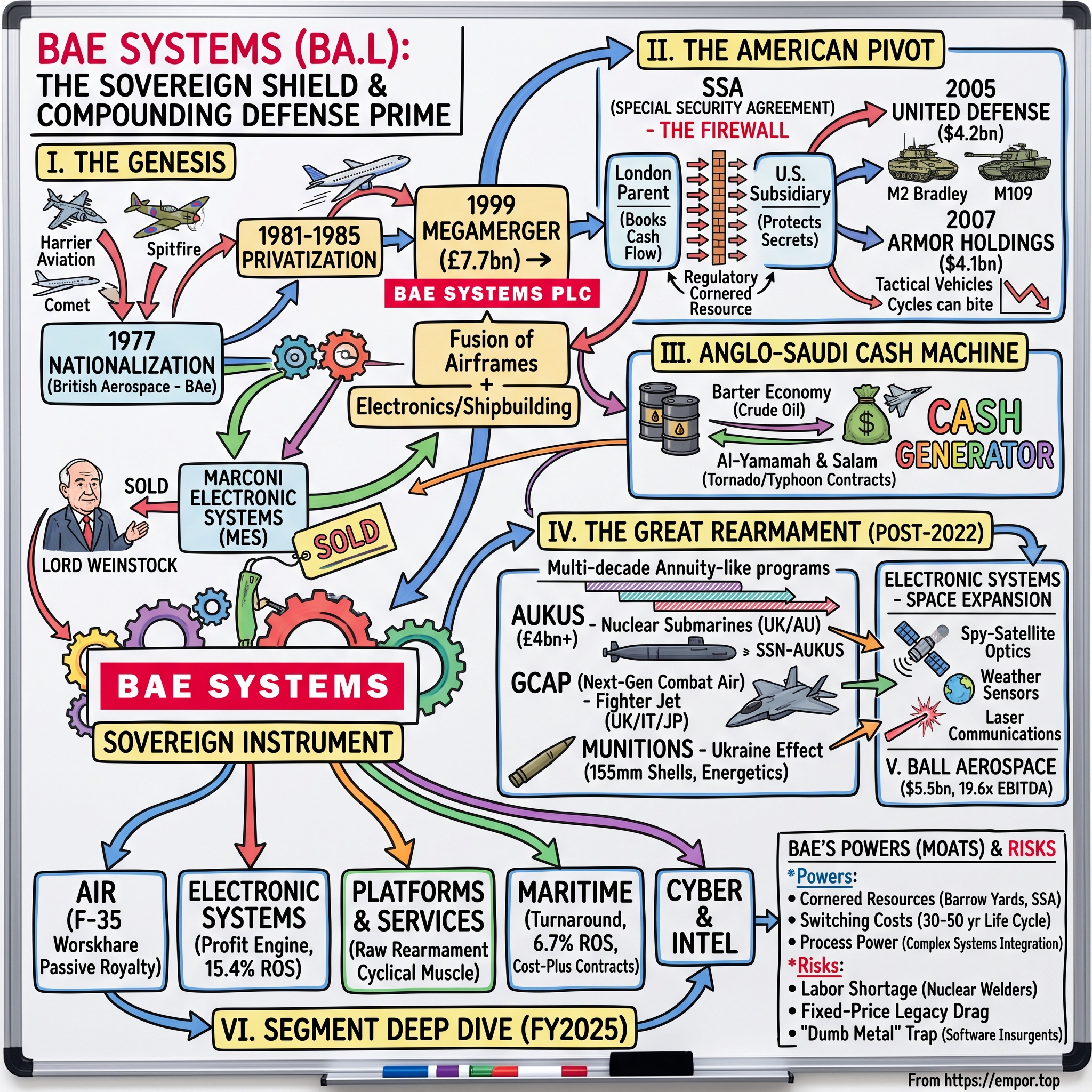

In February 2024, a British company did something that, on paper, should have been impossible. BAE Systems plc — headquartered in Farnborough, England, its board answerable to the London Stock Exchange and, ultimately, to a "golden share" still held by His Majesty's Government — closed a $5.5 billion cash purchase of Ball Aerospace, one of the most sensitive space and intelligence contractors in the United States.1 Ball built spy-satellite optics, weather sensors, and classified payloads for the U.S. intelligence community. It was the kind of asset the Pentagon guards like a crown jewel. And yet Washington waved a foreign buyer through.

How? The answer is a legal instrument most investors have never heard of: the Special Security Agreement, or SSA. Under it, BAE's American arm operates behind a firewall so complete that the British parent is legally walled off from the classified work its own subsidiary performs. The renamed business — Space & Mission Systems, or SMS — was folded straight into the beating heart of the U.S. defense apparatus, and the London parent booked the cash flows without ever seeing the secrets.2 It was the largest acquisition in BAE's history, and a fitting emblem for what this company actually is.

Here is the thesis, stated plainly and then tested for the next 200 minutes: BAE Systems is less a defense contractor than a sovereign instrument — an entity so entangled with the national-security machinery of the UK, the US, Australia, and Saudi Arabia that its fortunes and theirs are difficult to separate. It builds the nuclear submarines that carry Britain's Trident deterrent to sea. It manufactures the aft fuselage of every F-35 Lightning II ever built, anywhere on Earth. It is the UK's only builder of warships that matter. That entanglement is the source of both its extraordinary economics — long-duration, single-source, switching-cost-heavy franchises — and its most serious risks: monopsony buyers who can cancel programs, fixed-price contracts that can bleed margin for a decade, and a labor base of nuclear-certified welders that no amount of capital can conjure overnight.

This is not an investor-relations tour. Where management says BAE will win, we will ask what evidence supports the claim and what would prove it wrong. The company has, at various points, bribed its way to contracts, blown up its own margins on fixed-price warships, and nearly merged itself out of existence with Airbus. It has also compounded shareholder capital through two decades of geopolitical whiplash. Both stories are true.

The roadmap:

- The Genesis — how nationalization and privatization birthed a national champion, ending in the 1999 megamerger that created BAE Systems.

- The American Pivot — the deliberate, decades-long campaign to become a trusted U.S. prime under the SSA.

- The Anglo-Saudi Cash Machine — the economics and the criminal aftermath of Al-Yamamah.

- The Mid-Life Crisis — the failed 2012 EADS merger and the pivot back to defense pure-play.

- The Woodburn Era — operational discipline, plugging the maritime margin leak, the shift from heavy metal to software-defined systems.

- The Great Rearmament — the post-2022 world, AUKUS, GCAP, and the space frontier.

- The Playbook, the Moats, and the Stress Test — monopsony economics, Helmer's 7 Powers, Porter's 5 Forces, and the bear case that could break it all.

Let's start where all sovereign champions start: with a government that decided it could not live without an industry.

II. The Genesis: British Aerospace, Marconi, and the 1999 Megamerger

Picture Britain in the mid-1970s. The empire was gone, the pound was under siege, and the country's aviation industry — once the envy of the world, the industry of the Spitfire and the Comet and the Harrier jump jet — was a fragmented mess of proud, undercapitalized firms bleeding cash on programs none of them could afford alone. Hawker Siddeley, the British Aircraft Corporation, Scottish Aviation: each carried the DNA of legends like de Havilland, Vickers, Bristol, and Supermarine, and each was too small to survive the era of the billion-pound weapons program.

The Labour government's answer in 1977 was blunt: nationalize the lot. The Aircraft and Shipbuilding Industries Act swept the major airframe makers into a single statutory corporation named British Aerospace, or BAe. It was less a company than a state-owned consolidation — a recognition that combat aircraft had become too strategic, and too expensive, to leave to the market.

It helps to understand why the underlying firms had failed. The post-war economics of aviation were merciless in a way that is hard to appreciate now. A single fighter program could cost more than a company's entire market value; a failed one could take the company down with it. Britain had built magnificent aircraft — and lost fortunes doing it, from the ill-starred Comet jetliner to the cancelled TSR-2 strike aircraft, a program so promising and so expensive that its 1965 cancellation became a national trauma for British engineering. The lesson successive governments drew was that no single private firm could carry the risk of frontier military aerospace alone. Consolidation was not ideology; it was actuarial. And once you accept that a country needs one champion to spread that risk, you are most of the way to accepting that the state must have a permanent say in who owns it.

Then the political pendulum swung. Margaret Thatcher's government, ideologically committed to rolling back the state, took BAe public in stages between 1981 and 1985, turning the statutory corporation into a listed plc. But Thatcher's team understood a subtlety that would define the company for the next forty years: you can privatize a national champion, but you cannot let it fall into foreign hands. So the government kept a "golden share" — a special share giving it a veto over any attempt to take control of the company or move it abroad, and capping foreign ownership.3 BAe would be privately owned, market-disciplined, and profit-seeking — but never, ever, foreign-controlled. That single legal artifact is the ancestor of every "sovereign" advantage BAE enjoys today.

For a decade and a half, BAe muddled through — strong in military aircraft (Tornado, Hawk, and a share of the four-nation Eurofighter), weaker in the commercial-jet and regional-aircraft ambitions that repeatedly burned it. What it lacked was electronics: the radars, the sensors, the mission systems that were fast becoming the expensive, high-margin brains of every weapon.

Those brains lived elsewhere — inside the General Electric Company plc, or GEC, the sprawling industrial conglomerate built by the legendarily tight-fisted Lord Weinstock. Weinstock is a character worth pausing on, because his shadow falls across this whole story. For three decades he ran GEC as a cash-hoarding fortress, obsessing over ratios, distrusting grand strategy, and sitting on a legendary pile of cash that came to be known, half-mockingly, as "the GEC cash mountain." His defense electronics arm, Marconi Electronic Systems (MES), was a world-class house of radar, avionics, and — crucially — naval shipbuilding, owning the yards that built Britain's warships and submarines. It was exactly the sort of steady, high-technology, government-underwritten business Weinstock loved.

But by the late 1990s Weinstock had stepped back, and his successor George Simpson had a different, more fashionable vision: reinvent stodgy GEC as a high-flying telecommunications-equipment company for the internet age. Doing that meant selling the defense crown jewels to fund telecom acquisitions. It was, in hindsight, a catastrophic misjudgment — the telecom bet, rebranded Marconi, would collapse spectacularly when the dot-com bubble burst, wiping out one of Britain's great industrial names. But that collapse is a different podcast. What matters here is that in 1998, MES was for sale, and its sale would decide the shape of British defense for a generation.

And here the plot thickened into something close to a national-security thriller. Simpson shopped MES to the Americans (Lockheed Martin) and the Germans (DASA, the Daimler aerospace arm). Either deal would have handed the crown jewels of British defense electronics — and Britain's warship yards — to a foreign owner. That was intolerable to Whitehall. If BAe's airframes and MES's electronics ended up in different, foreign-controlled companies, the UK's entire defense industrial base would be split and hostage.

So BAe moved. On 19 January 1999 it announced it would buy Marconi Electronic Systems, and on 30 November 1999 the deal closed: a £7.7 billion merger that created BAE Systems plc.4 This was not a normal corporate combination. It was a sovereign consolidation — the deliberate fusion of the nation's airframe champion with its electronics-and-shipbuilding champion, engineered to keep both under one British roof.

The strategic legacy was double-edged, and worth sitting with. On the asset side, the merger handed BAE a near-monopoly over UK warship construction — the yards at Govan and Scotstoun on the Clyde, and the sprawling submarine complex at Barrow-in-Furness — plus a dominant position in military aircraft and, now, electronics. On the liability side, it inherited a thicket of long-dated, fixed-price development contracts — deals where BAE had promised to deliver first-of-class ships and jets at a set price, absorbing any cost overruns itself. Those contracts would quietly detonate across the group's margins for the next decade, and learning to defuse them would become the defining operational project of the 2010s. Before that reckoning, though, BAE's leadership turned its attention to a far bigger prize than the shrinking home market. They looked west.

III. The Pivot to America: Building BAE Systems Inc. under the SSA

Do the arithmetic that BAE's board did around the turn of the millennium and the strategy writes itself. The Cold War was over. The "peace dividend" was in full swing, and the UK Ministry of Defence — BAE's anchor customer — was cutting. The entire British defense budget was a rounding error next to the buyer across the Atlantic. The United States accounted for something close to half of all global defense spending. If you wanted to build a compounding defense business rather than manage a genteel decline, there was only one place to do it. You had to win in America.

The problem was that America does not let foreigners near its secrets. The governing concept is FOCI — Foreign Ownership, Control, or Influence — the Pentagon's doctrine for keeping classified work out of foreign hands. A British company trying to export weapons into the U.S. market would run headlong into Buy American rules, ITAR technology-transfer controls, and a procurement culture that instinctively favored domestic primes. Exporting your way into the Pentagon was a dead end.

BAE's insight — and it was genuinely clever — was to stop trying to sell into America and instead become American. Rather than ship UK-built goods across the ocean, BAE would buy U.S. defense companies outright and run them as local firms. The mechanism that made this legal is the Special Security Agreement (SSA). Under an SSA, the U.S. subsidiary — BAE Systems Inc. — is governed by a board of U.S. citizens, typically retired generals, admirals, and intelligence officials, who hold security clearances and are legally obligated to run the company's classified programs independently of the British parent. A group of these "outside directors" and "proxy holders" controls the sensitive work; the London parent gets the economics and the strategic upside but is firewalled from the secrets.

Think of it as a trust arrangement for national security. BAE the shareholder owns the cash flows. American cleared insiders own the decisions. The Pentagon gets a contractor it can treat as domestic, with facility clearances up to Top Secret, bidding on the most sensitive programs as if no Union Jack were anywhere in sight. It is, in Hamilton Helmer's language, a regulatory cornered resource — a legally sanctioned position that a would-be competitor cannot simply buy or build, because the trust that underwrites it took decades to earn.

It is worth dwelling on how unusual this is, because it is central to the whole investment case and easy to underrate. Most cross-border deals in sensitive industries are either blocked outright or hobbled with conditions that strip out the strategic value. The reason BAE could do the opposite — buy sensitive American assets and be welcomed — is that it had spent years demonstrating that the SSA firewall genuinely holds, that its U.S. board really does operate independently, and that no British executive ever reaches through the wall to touch a classified program. Trust of that kind is not a document; it is a reputation accumulated transaction by transaction, and once earned it becomes something close to unassailable. A German or French or Chinese firm attempting the same play today would face a wall of suspicion that BAE spent two decades dismantling. That head start is the moat.

With the structure in place, BAE went shopping — and the shopping list tells you exactly what it was trying to become. In 2005 it acquired United Defense Industries for roughly $4.2 billion, announced in March and closed that June.5 United Defense brought the M2 Bradley infantry fighting vehicle, the M109 Paladin self-propelled howitzer, and U.S. naval gun systems — instantly making BAE a heavyweight in American land systems and armor. Two years later, in 2007, it went further, buying Armor Holdings for about $4.1 billion (around $4.5 billion including debt).6 Armor Holdings was a bet on the signature weapon of the moment: tactical wheeled vehicles and blast-protection armor, in ferocious demand as roadside bombs shredded U.S. convoys in Iraq and Afghanistan.

For a few years, the Armor Holdings bet looked like genius. Vehicle-armor demand was near-insatiable while roadside bombs were the defining threat of two wars, and the business threw off cash. Then it looked like a lesson. When the U.S. surge ended and troops came home, the demand for MRAP-style protected vehicles fell off a cliff — you do not need blast-resistant trucks when the convoys stop rolling — and BAE's U.S. land business went through a brutal cyclical downturn, shedding revenue and forcing painful plant rationalizations. The episode is worth flagging as an analytical fact, not a footnote: BAE bought a wartime peak, and paid for it in the trough. That scar tissue — the memory of over-extending into a cyclical, single-mission product at the top — would inform the more disciplined capital allocation of the following decade, and it is the reason a skeptic should watch closely whenever BAE makes a large acquisition into a hot end-market. The company has made that mistake before.

There is a subtler point buried in the U.S. campaign, too. Notice that BAE deliberately built its American position in the less glamorous corners of defense — land vehicles, electronics, services — rather than the marquee aircraft and shipbuilding primes that were already locked up by Boeing, Lockheed, and General Dynamics. This was not settling for scraps. It reflected a shrewd reading of where a foreign-owned newcomer could actually win: in the fragmented middle tier of the market, where scale and integration skill mattered more than a century of incumbency, and where the Pentagon was happy to have a capable, cleared, competitive supplier to keep the giants honest. BAE would be the specialist the primes could not do without, rather than the rival they would crush.

Strategically, though, the American project worked. BAE deliberately avoided the ego trap of going head-to-head with Boeing or Lockheed Martin as a prime on the marquee fighter programs — the highest-risk, most politically exposed contracts in the business. Instead it positioned itself as the indispensable top-tier subcontractor and niche prime: the electronic-warfare house, the armor specialist, the trusted partner on the F-35. It would be essential without being exposed. That posture — powerful supplier rather than headline prime — is a recurring pattern in how BAE compounds. But the cash that funded the whole American adventure did not come from America at all. It came from the desert.

IV. The Anglo-Saudi Cash Machine & the SFO Storm

For most of BAE's modern life, one contract quietly out-earned almost everything else the company did, and its name was اليمامة Al-Yamamah — "the dove." Signed in 1985 between the British and Saudi governments, with British Aerospace as prime contractor, Al-Yamamah was less an arms sale than a barter economy. Saudi Arabia paid, in substantial part, not in cash but in crude oil — hundreds of thousands of barrels a day, delivered to the UK government, the proceeds funneled to pay for Tornado and Hawk jets, and later Eurofighter Typhoons, along with the training, bases, and decades of support that surround a modern air force.

The economics were staggering. Al-Yamamah, and its later Typhoon-era successor سلام Salam, generated cash on a scale that could swing BAE's entire annual result. It was, for years, the golden goose — funding research, underwriting dividend growth, and, not incidentally, helping bankroll the very U.S. acquisition spree we just watched. When a single customer relationship can move the parent company's profits, it stops being a contract and becomes a dependency. And dependencies, in the arms trade, tend to be built on foundations that do not bear close inspection.

They did not bear it here. Allegations mounted through the early 2000s that the relationship had been lubricated by a systemic architecture of bribery — slush funds, secret commissions, and lavish payments to Saudi intermediaries and officials, all to keep the golden goose alive. The UK's Serious Fraud Office (SFO) opened a major investigation. And then, in December 2006, came one of the most extraordinary interventions in modern British legal history: the government of Prime Minister Tony Blair ordered the SFO to halt its Al-Yamamah inquiry, citing national security and the risk that Riyadh would cut off counter-terrorism cooperation.[^7] The rule of law, it turned out, had a foreign policy exception.

Britain could bury the investigation. The United States could not — or would not. The U.S. Department of Justice, wielding the Foreign Corrupt Practices Act and its jurisdiction over dollar transactions and U.S. operations, kept the pressure on. In 2010 it forced a reckoning. BAE Systems pleaded guilty in U.S. federal court to conspiring to make false statements to the U.S. government about its compliance programs, and agreed to pay a $400 million criminal fine — at the time one of the largest ever in a case touching defense-industry corruption.7 In parallel, BAE settled with the UK SFO, paying £30 million in connection with accounting failures relating to payments in Tanzania.

There is a genuinely uncomfortable investment lesson in this chapter, and it is worth stating without euphemism. For decades, a meaningful share of BAE's profits — and by extension its dividends, its research budget, and the war chest that bought its way into America — was underwritten by a relationship that the company's own guilty plea confirmed was tainted. An investor buying BAE stock in, say, 2003 was, whether they knew it or not, buying a cash flow with a criminal-liability time bomb attached. This is the deep hazard of the defense business: the same government relationships that create the moat also create the corruption risk, because the deals are enormous, opaque, government-to-government, and conducted in jurisdictions where the line between commission and bribe is deliberately blurred. It is a category of risk that never fully disappears in this industry, only recedes when the controls are strong.

For investors, the interesting part is not the scandal itself but what BAE did with it. Rather than treat the settlement as a cost of doing business, the company used it as the forcing function for a genuine governance overhaul. Under the incoming chairmanship of Sir Roger Carr, and prodded by institutional shareholders who had had enough, BAE implemented the recommendations of the independent Woolf Committee — rebuilding its ethics, compliance, and transparency regime from the studs up. The freewheeling, commission-driven model of Cold War arms dealing was dismantled and could not be rebuilt. This matters as an analytical fact about management credibility: the modern BAE's clean-hands reputation is not a marketing claim but a structure erected on the rubble of a criminal plea. Whether that structure holds under future temptation is, of course, untestable in advance — but the behavioral track record since 2010 has been materially cleaner than the two decades before it.

Cleaned up and cashed up, BAE entered the 2010s looking for its next act. What it reached for nearly destroyed the company.

V. The Mid-Life Crisis & the Failed Airbus (EADS) Merger

By 2012, the defense industry's mood had curdled. The financial crisis had given way to austerity; Western governments were slashing military budgets; and the appetite for the wars that had fed the previous decade's armor boom was gone. BAE's leadership, under chief executive Ian King, stared at a shrinking core market and reached for the boldest possible answer: get out of pure defense by merging with the one company that could offer an escape hatch into booming commercial aviation.

That company was EADS — the European Aeronautic Defence and Space Company, the Franco-German-Spanish giant that owned Airbus and would soon rename itself Airbus SE. In September 2012 the two sides confirmed they were in talks over a merger valued at roughly £28 billion (around $45 billion), which would have created the largest aerospace and defense group on Earth, dwarfing Boeing.8 The industrial logic was seductive on a spreadsheet: bolt BAE's high-margin, cash-generative defense franchises onto Airbus's fast-growing commercial-jet business, and ride the global air-travel supercycle while hedging the defense downturn.

But defense mergers are not solved on spreadsheets. They are solved — or killed — in capitals. And this one died in the space of a few weeks, strangled by three governments pulling in incompatible directions. Germany, under Chancellor Angela Merkel, feared being subordinated to France and demanded equal shareholding and a manufacturing and headquarters role to match Paris. France, already a large EADS shareholder through the state, would not simply cede control. Britain wielded its golden share and worried about diluting its sovereign defense supplier into a Continental behemoth. And hovering over all of it was Washington: the U.S. Department of Defense signaled deep unease that BAE's classified American programs, ring-fenced under the SSA, might be exposed to a sprawling European commercial entity. By October 2012 the talks collapsed. No one could agree on who would be in charge.8

At the time it looked like humiliation. In hindsight it was one of the most valuable deals BAE never did. Had the merger gone through, BAE would have diluted its crown-jewel defense economics into the notoriously cyclical, capital-devouring, thin-margin world of commercial aviation — and would have spent the 2020s wrestling with airline order cancellations and narrow-body production ramps instead of harvesting a defense supercycle. Forced to stay a standalone defense pure-play, BAE did the un-glamorous thing instead. It turned inward: simplifying its structure, attacking its own operational inefficiencies, and committing to compound capital organically rather than through a transformational deal. That decision — made under duress, not vision — set up everything that followed. But executing it required a different kind of leader than the deal-makers who had run the company before.

VI. The Charles Woodburn Era: Operation Overlord & Financial Discipline

When BAE named its next chief executive, the surprise was not the man's résumé so much as the industry it came from. Dr. Charles Woodburn took over as CEO on 1 July 2017, and he was not a lifer from the world of fighter jets and defense procurement. He was an oil-services man — a Cambridge-trained engineer with a doctorate, who had spent his career at Schlumberger and then run the oilfield-services firm Expro. He arrived at BAE first as chief operating officer in 2016, then took the top job the following year.

That background matters more than it sounds. Oilfield services is a brutal school of operational execution: you are drilling holes miles underground, on fixed budgets, where a mistake costs a fortune and cash conversion is religion. Woodburn brought that mindset — a fixation on engineering delivery, on turning accounting profit into actual cash, on measuring programs against hard metrics rather than boardroom optimism — into a company that had spent decades treating cost overruns on first-of-class warships as an act of God. In late 2019 he added a like-minded partner, bringing in Brad Greve as group finance director, cementing a duo whose gospel was capital discipline.

There is a management-credibility angle here that a careful investor should weigh. Bringing in an outsider CEO from an unrelated industry is a genuine risk — defense is a clubby, relationship-driven, technically arcane world, and plenty of talented executives have foundered in it because they underestimated how different it is from ordinary manufacturing. BAE's board took that bet deliberately, and the tell that it paid off is not in any single quarter but in the pattern of the years since: a company that had been prone to nasty surprises stopped surprising people. In an industry where the CEO's most important job is arguably credibility with two customers — the shareholders who fund it and the governments who buy from it — a reputation for saying what you will do and then doing it is itself a strategic asset. Woodburn's outsider status, initially a question mark, became part of the pitch: here was a manager who cared about cash and execution rather than the romance of the machines.

Their central operational problem had a name: Maritime. For years, BAE's submarine and warship business had been the group's margin sinkhole. Building a first-of-class nuclear submarine like the Astute, or a new frigate like the Type 26, involves solving thousands of engineering problems for the first time — and when those programs sit under old-style fixed-price contracts, every delay and design change comes straight out of BAE's own pocket. The result was a segment doing enormous, strategically vital revenue at margins that would embarrass a supermarket.

Woodburn's fix was unglamorous and, so far, effective. He ran a program-by-program review, tearing into each troubled contract to understand where the money was actually leaking. He drove a physical modernization of the shipyards — 3D digital modeling, automated welding, and new build halls at Barrow and on the Clyde — to attack the productivity problem at its root. And, critically, he worked with the MoD to change the contracting model itself, shifting developmental, high-uncertainty warship work away from rigid fixed-price deals toward collaborative, risk-sharing arrangements where the customer absorbs some of the unknowns of building something that has never been built before. This is the single most important structural change in BAE's economics over the past decade, and we will see its fingerprints all over the segment margins later.

On incentives, the alignment reads reasonably well on its own terms. Woodburn is required to hold shares worth at least 200% of his base salary and has for years held well above that minimum. Executive pay is anchored to metrics that map onto shareholder value rather than empire-building — return on sales, free-cash-flow conversion, and underlying EPS growth rather than revenue for revenue's sake. And the behavioral record is the part a skeptic should weigh most heavily: across Woodburn's tenure, BAE has built a reputation for setting guidance it then meets or beats, year after year — precisely the boring consistency that was missing during the execution blowups of the early 2010s. The FY2025 results continued the pattern, with the group hitting its raised targets and management issuing a confident 7–9% sales growth outlook for 2026.9 Credibility in this industry is earned in cash conversion, and by that measure the current regime has earned it.

Discipline, though, is easy to praise in a downturn and easy to forget in a boom. And beginning in 2022, BAE was handed the biggest boom its industry had seen in a generation.

VII. The Great Rearmament: Ukraine, GCAP, AUKUS & the Space Expansion

On the morning of 24 February 2022, Russian columns crossed into Ukraine, and thirty years of Western assumptions died with them. The "peace dividend" — the post-Cold War bet that great-power land war in Europe was obsolete and defense budgets could shrink forever — was over. What replaced it was a scramble: to refill artillery stocks emptied in weeks, to rebuild the capacity to make shells and missiles at scale, to rearm air and missile defenses, and, simultaneously, to sprint toward the next generation of digital, autonomous, and space-based warfare. For the first time in a generation, the political constraint on defense spending flipped from "how little can we get away with" to "how fast can industry deliver."

It is worth being precise about what changed, because "defense spending went up" undersells it. The shift was not merely quantitative but structural and durable. NATO members that had spent years failing to hit the alliance's 2%-of-GDP spending target scrambled past it, with several committing to far higher trajectories; Germany announced a special fund to rebuild a military it had allowed to hollow out; Poland embarked on one of the fastest peacetime rearmaments in Europe. Crucially for a company like BAE, governments began signing long-dated commitments — multi-year munitions contracts, decade-plus platform programs — rather than one-off top-ups, because the whole point was to rebuild industrial capacity that had atrophied. For a manufacturer, a ten-year framework contract is worth far more than a single fat year, because it lets you invest in capacity with confidence. The rearmament did not just raise BAE's revenue; it lengthened the duration of that revenue, which is exactly the variable that drives how the market should value it.

For BAE, the rearmament arrived not as a single windfall but as a stack of multi-decade programs that turn its order book into something closer to an annuity. Three deserve real attention.

AUKUS. Under the trilateral security pact between Australia, the UK, and the US, the allies committed to a shared class of nuclear-powered attack submarines — SSN-AUKUS — built around a common UK design and Rolls-Royce reactors. BAE sits at the center of it. In October 2023 the UK government awarded a package of contracts worth around £4 billion to develop the submarine program through 2028, with roughly £3.95 billion going to BAE for design work, infrastructure investment at Barrow, supply-chain build-out, and the recruitment of thousands of new workers.10 BAE is the prime for the UK boats, and its Australian arm, alongside ASC, was selected to build Australia's SSN-AUKUS submarines in Adelaide off the same design.10 The practical meaning: the Barrow-in-Furness shipyard has a credible line of sight to full utilization into the 2060s. There is no comparable backlog visibility anywhere in the broader industrial economy.

GCAP. The Global Combat Air Programme is BAE's bet on the generation of fighter jet after the F-35 and Typhoon. It is a genuinely three-nation effort: the UK, Italy — partnering through Leonardo S.p.A. — and Japan, partnering through 三菱重工業株式会社 Mitsubishi Heavy Industries, Ltd. Together they aim to field a sixth-generation stealth fighter, with BAE leading the UK's share and building the flying demonstrator that will prove the airframe.[^12] The demonstrator was reported to be roughly three-quarters complete by 2025. Strategically, GCAP matters enormously for a reason that is easy to miss: it determines whether BAE remains a genuine airframe prime or slowly slides into being a high-end subcontractor. On the F-35, recall, BAE is a valuable supplier but Lockheed owns the aircraft. On the Eurofighter Typhoon, BAE is a leading partner but the platform is aging and will not be replaced by more Typhoons. GCAP is the program that decides who designs and integrates the West's next front-line fighter — and BAE is positioned to lead the airframe, not merely supply it. Win it well, and BAE carries top-tier combat-air capability, and the decades of support revenue that trail it, into the 2060s and beyond. Fumble it, and BAE's most prestigious franchise ages out without a successor.

The risk is not primarily technical; it is political and managerial, and the EADS collapse is the cautionary tale sitting right there in the company's own history. Three proud nations — Britain, Italy, and Japan — must agree on requirements, workshare, export rules, and cost-sharing across a decades-long program, with each domestic industry and defense ministry protecting its own interests. Japan's participation is especially significant, marking a historic loosening of its long-standing reluctance to co-develop major weapons abroad, but it also adds a partner with its own procurement culture and its own export sensitivities. Multinational fighter programs have a long history of schedule slips and budget blowouts precisely because of this coordination problem — the Eurofighter itself took far longer and cost far more than promised. Whether the GCAP trio can hold together where the EADS merger could not is, on the evidence, a genuinely open question, and one of the more important things to watch over the next decade.

Space. Which brings us back to where this story opened: the Ball Aerospace acquisition, agreed in August 2023 and closed in February 2024, rebranded Space & Mission Systems and stood up as a fourth operating sector.111 Here the numbers deserve a skeptic's eye rather than a cheerleader's. BAE paid $5.55 billion gross, which it framed as roughly $4.8 billion net of the present value of future tax benefits.2 On the seller's disclosed metrics, the gross price worked out to about 19.6x Ball Aerospace's trailing EBITDA — and even on BAE's more flattering net-of-tax, post-synergy math of roughly 13x forward EBITDA, this was not a bargain. Traditional defense acquisitions have historically cleared at something like 12–15x.2

So this was not a distressed purchase or a value play. It was, in plain terms, a land grab — a decision that world-class space capability was strategically scarce enough to justify paying up. The rationale is that space is the new high ground of warfare: whoever owns the sensors, the payloads, and the laser communications in orbit sees and shoots first. Ball handed BAE immediate, credible capability in exactly those areas and turned its highest-margin segment, Electronic Systems, into a space-and-intelligence growth engine. That is the bull framing. The bear framing — that BAE paid a top-of-cycle multiple for an asset whose promised synergies and cross-selling may not materialize — is not refuted by the strategic logic; it is simply deferred to future results. We will return to it in the stress test. First, let's open the hood and see what actually pays the bills.

VIII. Segment-Level Deep Dive & Value Drivers

Strip away the geopolitics and BAE is, at bottom, five businesses under one roof, and the FY2025 results let us weigh each on its own merits. The group did £30.7 billion in sales and £3.32 billion in underlying EBIT, a 10.8% return on sales, up modestly on the prior year — respectable, unspectacular margins that tell you immediately this is a volume-and-visibility story, not a high-margin software story.912 Here is what drives it.

Air — the volume engine. At roughly £9.3 billion of sales and an 11.9% return on sales, Air is the single largest revenue generator in the group.9 Its economics rest on two pillars. The first is the F-35, and it is worth understanding exactly why BAE's slice of it is so valuable. BAE is not the prime contractor — that is Lockheed Martin — but it holds a locked-in workshare on every jet: it builds the aft fuselage and empennage (the rear section and tail structure) and the electronic-warfare system that lets the aircraft detect and defeat enemy radar. Here is the key: this is not a competition BAE has to re-win each year. The workshare was set when the program was designed, and it flows automatically with every aircraft rolling off the line — a jet the U.S. and its allies plan to build in the thousands and operate into the 2070s. BAE earns its cut whether the buyer is American, Japanese, Italian, or British. It is about as close to a passive royalty on a global weapons program as exists in the industry, and it is why Air's cash flows are so predictable. The second is the Eurofighter Typhoon: production tails, upgrades, and the long, lucrative business of supporting fleets already flying. The analytical point is that Air's cash flows are less about winning new competitions than about harvesting installed positions — predictable, long-duration, and hard to dislodge.

Electronic Systems — the profit engine. At about £7.5 billion of sales and the group's fattest margin at 15.4% return on sales, this is the crown jewel.9 It is where BAE's economics look least like a metal-bending contractor and most like a high-IP technology firm: electronic-warfare systems that jam and spoof enemy sensors, cockpit displays, precision-guidance electronics, commercial flight controls, and — since 2024 — the space payloads and intelligence systems of the former Ball business. Margins here are structurally higher because the value is in embedded intellectual property and mission-critical software, not tonnage — a jamming pod or a spy-satellite optic sells for a price set by what it does, not by what it weighs. To make the space piece concrete: the former Ball business builds things like the precision optical instruments that let a satellite resolve fine detail on the ground, the sensors behind U.S. weather and climate satellites, and laser-communication terminals — essentially fiber-optic-speed data links through open space, letting satellites talk to each other and to the ground far faster than old radio links. These are exactly the capabilities modern militaries are scrambling to field as warfare moves into orbit, and they carry the kind of specialized, hard-to-replicate IP that commands premium margins. If the bull case on BAE has a financial center of gravity, it is the mix-shift toward this segment.

Maritime — the turnaround. At roughly £6.8 billion of sales but only a 6.7% return on sales, Maritime is the group's margin laggard — and, paradoxically, one of its most valuable sovereign assets.9 This is the submarine and warship business: Dreadnought and SSN-AUKUS submarines, Type 26 frigates, all built single-source for the UK at Barrow and on the Clyde. The thin margin is not a sign of weakness; it reflects the low-risk, lower-return profile of the newer cost-plus-incentive and risk-sharing contracts Woodburn negotiated to stop the fixed-price bleeding. The investable question is directional: can Maritime margins grind up through 7% and beyond as programs mature past their riskiest development phases? That trajectory, more than any single number, is the tell on whether the operational fix has truly taken.

Platforms & Services — the land-and-munitions muscle. At about £5.0 billion of sales and an 11.4% return on sales, this segment is riding the rawest edge of the rearmament.9 It builds combat vehicles — the AMPV for the U.S. Army, the CV90 fighting vehicle sold across Europe — and, critically, it is the UK's primary sovereign munitions supplier at a moment when Western artillery-shell demand has exploded. The munitions story deserves a beat of its own, because it is one of the clearest strategic reversals of the decade. For years, artillery shells were treated as a low-tech, low-priority commodity; capacity was allowed to wither because no one imagined a war that would burn through them by the hundreds of thousands per month. Ukraine shattered that assumption overnight, exposing how thin Western magazines actually were. Governments responded by pouring money into rebuilding explosives and shell-production capacity — and BAE, as the incumbent UK supplier of energetics and munitions, sits directly in that flow, expanding output of everything from 155mm shells to the propellants and explosives that go inside them. Munitions have a lovely characteristic for a manufacturer: they are consumed, so a war economy converts them into recurring, high-drop-through revenue rather than one-time platform sales. This is the segment where the Ukraine effect shows up most directly and most durably in the P&L — assuming, and it is a real assumption, that the political will to keep the magazines full outlasts the current crisis.

Cyber & Intelligence — the smallest and most contested. At roughly £2.4 billion of sales and a 9.3% return on sales, this is national-security IT services in the US and cyber work in the commercial market.9 It is strategically relevant but structurally the weakest link economically: labor-intensive, competitive, and lacking the switching-cost moats of the hardware franchises. It is also, notably, the segment most exposed to the software-first insurgents we will meet in the bear case.

Put together, the portrait is coherent: BAE volume comes from Air, its margin from Electronic Systems, its sovereign irreplaceability from Maritime, its cyclical upside from Platforms & Services. Now, what are the transferable lessons in how it built and runs this machine?

IX. The Playbook: Business & Investing Lessons

Lesson 1: Local incumbency beats exporting. The single most important strategic decision in BAE's modern history was recognizing that a foreign defense firm cannot win the U.S. market by shipping product across an ocean. Protectionism, security rules, and procurement culture make the export path a trickle. The only way in was to become a domestic player — to buy American companies and run them behind the SSA firewall as a trusted insider, building the multi-decade intimacy with the Pentagon that no amount of export salesmanship could replicate. The generalizable insight for investors: in industries gated by regulation and trust, the winning move is often to acquire your way to legitimate local incumbency rather than to compete as an outsider. The moat is the permission to participate, and BAE bought it.

Lesson 2: Capital allocation as the actual product. Watch BAE's behavior evolve and you see a company that learned capital discipline the hard way — through the Armor Holdings cyclical bust and the near-miss EADS merger — and then codified it. The Woodburn-Greve playbook is deliberately unromantic: fund R&D and targeted capex internally to hold the technology edge; grow the dividend steadily and predictably (raised roughly 10% in both 2024 and 2025, to 36.3p);12 return surplus cash through opportunistic buybacks; and reserve M&A for assets that sit squarely inside secular growth domains with a clear synergy path — the discipline that justified paying up for space capability while passing on lower-conviction deals. The lesson is that in a business with a monopsony customer and limited pricing power, how you allocate the cash is the primary lever of shareholder return. The growth is largely given by the geopolitics; the value creation is in the allocation.

Lesson 3: Managing the monopsony. BAE's customers are governments — often a single government per program, with the legal power to cancel, delay, or renegotiate at will. In theory that is a terrifying position for a supplier. In practice, BAE has turned it into a bilateral dependency. When you are the only firm that can build the nation's nuclear submarines, the relationship inverts: the buyer cannot squeeze you to failure without destroying the very industrial capability it needs. The winning posture is not adversarial price-negotiation but custodianship — positioning yourself as the irreplaceable steward of a sovereign capability, such that the customer's interest and yours converge. It is a collaborative, mutual-hostage model, and it is the deep source of BAE's durability. Which is the perfect segue into a formal look at exactly how defensible this business really is.

X. The Strategic Position: Porter's 5 Forces & Helmer's 7 Powers

Porter's Five Forces

Threat of new entrants — very low, with one asterisk. The barriers here are close to absolute. To build submarines or fighter aircraft you need billions in capital, decades of accumulated tacit engineering knowledge, national-security clearances, ITAR compliance, and — the killer — a government willing to designate you a national champion. You cannot start a nuclear-submarine company. But the asterisk is real and growing: in the software and autonomy niches, well-capitalized insurgents like Anduril and Palantir have entered from the digital side, unburdened by legacy metal-bending, and they threaten precisely the high-margin, high-IP layer BAE most wants to own.

Bargaining power of buyers — high on paper, moderate in practice. Governments are monopsonists and can, in principle, dictate terms or kill programs outright. But as we just saw, single-source status flips the dynamic into a bilateral monopoly. The MoD cannot punish BAE on submarine pricing without endangering Britain's ability to build submarines at all. Power exists on both sides, which in practice means negotiation, not domination.

Threat of substitutes — low. There is no commercial substitute for military deterrence. You cannot outsource a nuclear deterrent to the cloud. The nearest thing to a substitute is a different doctrine — cheaper drones and software replacing exquisite platforms — which is a real long-run threat to specific product lines but not to the existence of the category.

Bargaining power of suppliers — moderate and rising. BAE sits atop a vast supply chain and can dictate terms to most sub-tier vendors. But the chain has choke points that can hold whole programs hostage: solid rocket motors, specialized castings and forgings, and advanced semiconductors. When a single supplier of energetic materials or radiation-hardened chips slips, BAE's schedule — and its fixed-price margins — slip with it. Post-2022, these bottlenecks moved from theoretical to operational.

Rivalry — bifurcated. In the sovereign, single-source domains — UK submarines, UK warships — rivalry is essentially nil. In the export markets it is ferocious: BAE fights Rheinmetall AG tooth and nail for European land-systems and combat-vehicle contracts, and Dassault, Leonardo, and others in air. The Rheinmetall contrast is instructive, because it is the clearest live case study in how the rearmament rewards different strategies. Rheinmetall entered the Ukraine era as a comparatively mid-sized German land-and-ammunition specialist and has ridden the European rearmament — and especially the desperate scramble for artillery shells — into a dramatic re-rating, expanding capacity aggressively and winning share across the Continent. It is, in effect, a purer, higher-beta play on exactly the munitions-and-armor upcycle that BAE captures through its Platforms & Services segment. The comparison cuts both ways: it validates BAE's land-and-munitions exposure as a genuine growth driver, but it also shows that in the contestable parts of the market BAE has no monopoly and faces a hungry, focused rival willing to build capacity faster. The swollen pie has energized every competitor to chase it, and in armored vehicles Rheinmetall has been the most aggressive share-taker of all.

Hamilton Helmer's 7 Powers

Three of Helmer's seven powers apply to BAE with unusual clarity.

Cornered Resource. BAE holds not one but two. The first is physical: the Barrow-in-Furness shipyard is the only facility in Britain licensed and equipped to build nuclear submarines — a legally and practically irreplaceable asset. The second is regulatory: the Special Security Agreement, the trusted-insider status inside the U.S. defense establishment that took two decades and a governance overhaul to earn and that a foreign rival cannot simply purchase. Together they are the hardest parts of BAE's position to copy.

Switching Costs. Once a nation buys a BAE platform — a Typhoon, an F-35 supported through BAE, a CV90 — it is locked in for a 30-to-50-year lifecycle of spares, upgrades, weapons integration, and training. The dirty secret of the defense business is that the sticker price of the platform is often the smaller number; the multi-decade support "tail" is where much of the lifetime value sits, and it accrues almost automatically to the original manufacturer. Think about what switching would actually require: a country that wanted to abandon a BAE fleet mid-life would have to retrain every pilot and technician, re-certify a new supply chain, re-integrate every weapon, and write off billions in sunk infrastructure — all to buy a rival platform that would impose the identical lock-in from year one. The rational choice is almost always to stay, keep paying for upgrades, and stretch the platform's life. This is why defense revenue is stickier than almost any consumer subscription: the switching cost is measured not in monthly fees but in national defense readiness. It is the closest thing in the industry to recurring, contracted, switching-cost-protected revenue, and it is why the installed base matters as much as the order book.

Process Power. Integrating millions of components, thousands of suppliers, and cutting-edge physics into a working nuclear submarine or stealth fighter is a capability that cannot be written down in a manual or bought off a shelf. It is tacit institutional knowledge, accumulated over decades of trial, error, and expensive failure. It is why even a fully funded new entrant could not simply decide to build a submarine — and why BAE's occasional execution stumbles are so closely watched, because process power is the one moat that erodes if the institution forgets how to do the hard thing. That fragility is the doorway to the bear case.

XI. The Bear vs. Bull Case & Skeptical Stress Test

The short-seller's stress test

Put on the skeptic's hat, because the bull case on BAE is now widely held and richly valued, and consensus enthusiasm is exactly where careful investors earn their keep.

The first target is the price paid for Ball. At 19.6x trailing EBITDA, BAE paid a full-cycle multiple for a space asset at a moment of maximum space enthusiasm.2 The deal only works if the promised synergies and the roughly $2 billion of hoped-for cross-selling revenue actually show up, and if national-security space spending keeps climbing. If space budgets normalize, or if the integration underdelivers, this becomes a textbook top-of-market acquisition — and the tell will be an impairment charge some years out. Management's framing that the net multiple is a more reasonable ~13x is accurate but self-serving; it relies on tax benefits and synergies that are, by definition, promises rather than facts. A disciplined observer should treat the Ball multiple as an open question, not a settled win, and watch Electronic Systems' organic space growth for evidence either way.

There is a governance-and-complexity angle an activist might press, too. BAE is a five-segment, four-country conglomerate straddling submarines, fighter aircraft, armored vehicles, space payloads, and IT services — a genuinely sprawling portfolio. A sharp-elbowed investor could argue that some of this belongs in different hands: that the lower-margin Cyber & Intelligence services business, in particular, sits awkwardly next to the exquisite-hardware franchises and might be worth more spun out or sold. The counter-argument is that the breadth is the strategy — that being the one-stop integrator across domains is precisely what makes BAE indispensable to governments buying whole systems rather than parts. Both can be true, and the tension is worth watching: conglomerate breadth that looks like strength in a rearmament boom can look like unfocused "diworsification" if growth slows and the market starts demanding purity.

The second, deeper target is the "dumb metal" trap. This is the most serious intellectual challenge to the entire traditional-prime model. The argument runs: the value in modern warfare is migrating from hardware to software — autonomy, AI-enabled targeting, networked sensing, mass-producible attritable drones — and that value is being captured by software-native firms like Anduril, Palantir, and SpaceX, which move faster and carry none of BAE's legacy cost structure. If that trend runs to its conclusion, the traditional primes get relegated to building the chassis — the "dumb hulls" and "dumb airframes" — while the fat, high-margin software layer is owned by someone else. BAE's own Cyber & Intelligence margins, the softest in the group, hint that it does not yet win convincingly on this turf. This is not a risk to dismiss; it is the central bear thesis, and the honest answer is that the verdict is genuinely undecided.

The bull case

Against that, the bull case rests on three pillars, and it is a strong hand.

First, backlog visibility that has no real peer. BAE closed FY2025 with a record order backlog of £83.6 billion — more than 2.7 times annual sales — after taking in £36.8 billion of new orders against £30.7 billion of revenue, a book-to-bill of roughly 1.2x.912 Crucially, that backlog is stuffed with multi-decade sovereign commitments — AUKUS submarines, GCAP — that are close to recession-proof, because governments do not cancel their nuclear deterrent when GDP dips. Very few companies in any sector can see a decade-plus of demand this clearly.

Second, a margin-expansion runway. As Space & Mission Systems integrates into the high-margin Electronic Systems segment, and as Maritime's newer contracts mature past their loss-making development phases, the group's mix and margins should drift structurally higher — the quiet compounding beneath the headline growth.

Third, capital-allocation consistency. The Woodburn-Greve regime has delivered a bond-like base of steadily growing dividends and buybacks, wrapped around equity-like growth — a total-return profile that, so far, has done what it said it would.

The bear case (execution and bottlenecks)

The bull case can be true and BAE can still stumble, because its two most serious near-term risks are operational, not strategic.

The first is labor, and it is easy to underweight because it does not show up cleanly in any single financial metric. You cannot build a nuclear submarine without nuclear-certified welders, cleared systems engineers, and specialized software developers — and these people are scarce, slow to train, and, in Barrow's case, asked to live and work in a geographically isolated corner of northwest England far from where most skilled young engineers want to build a life. Consider the scale of the ask: AUKUS and the parallel Dreadnought program require BAE to expand its Barrow workforce by many thousands, train them to nuclear-grade standards, and retain them across a program that runs for decades — all while competing for the same scarce technical talent against every other employer in a tight labor market. A submarine is only as fast as the rate at which you can produce certified welds, and there is no software patch for a welder shortage. If BAE cannot recruit and retain fast enough, the grand AUKUS timeline slips, penalty and milestone clauses bite, morale and quality suffer, and the annuity narrative frays at exactly the moment it is supposed to deliver. This is the most concrete constraint on the whole rearmament story, it is the risk management talks about most candidly, and it is not solvable with money alone — which is precisely why it is dangerous.

The second is fixed-price legacy drag. The contracting model has shifted toward risk-sharing, but not every deal in an £83.6 billion backlog is protected. Older fixed-price contracts remain, and if inflation re-accelerates or supply chains fracture again, those contracts turn from fine to loss-making with brutal speed — the very mechanism that gutted Maritime margins a decade ago. The scar is healed, not removed.

Weighing it honestly: BAE's strategic moats — cornered resources, switching costs, process power, monopsony custodianship — are about as durable as they come in public markets. Its risks are real but mostly of a different character: execution, cyclical multiple, and the long-run software-disruption question. That is a materially different risk profile than, say, a consumer company facing demand collapse — which is precisely why the market has come to value BAE the way it does. The job of the investor is not to admire the moats but to track the handful of numbers that would reveal, early, whether the machine is still working.

XII. KPIs, Risk Radar & Epilogue

The three KPIs that actually matter

If you track only a few things on BAE, track these.

1. Book-to-bill (order intake ÷ sales). This is the heartbeat of the entire multi-decade-visibility thesis. As long as new orders keep coming in at or above the rate revenue is recognized — a ratio of 1.0x or higher — the backlog and its annuity narrative stay intact. FY2025's £36.8 billion of intake on £30.7 billion of sales produced an exceptional 1.2x.9 The day this ratio slips durably below 1.0x is the day the growth story needs re-underwriting.

2. Return on sales, especially in Electronic Systems and Maritime. Group margin is the scoreboard for the whole "compounding" thesis. Watch two sub-plots inside it: whether Electronic Systems holds and extends its ~15% margin as it digests the space business, and whether Maritime can claw its way durably above 7%. Those two trajectories, more than the group headline, tell you whether the operational transformation is real.9

3. Free-cash-flow conversion. Cash, not accounting profit, funds the dividend and the buybacks that make up so much of BAE's total return. Management targets conversion above roughly 80% of underlying earnings, and FY2025 delivered strong free cash flow of about £2.16 billion.912 Sustained high conversion is the fuel; if it falters, the capital-return machine stalls regardless of what the order book says.

The risk radar

Three material risks warrant ongoing monitoring, each tied to a concrete business mechanism rather than macro hand-waving. Execution risk on complex ship programs — cost overruns on Type 26 or Dreadnought that echo the old Maritime wounds. Supply-chain fragility — the solid-rocket-motor, explosives, and advanced-semiconductor bottlenecks that can stall deliveries and reopen fixed-price losses. And regulatory and geopolitical veto risk — the possibility that U.S. ITAR export controls, or a fracture among the AUKUS or GCAP partners, chokes the technology transfer on which those flagship programs depend. Each of these is a way the annuity could crack.

Epilogue

BAE Systems began as a state's admission that it could not let its aviation industry die, and it spent the following half-century learning, sometimes disgracefully, how to turn sovereign necessity into a durable business. It bribed its way through the Cold War arms trade and then rebuilt its governance on the wreckage of a criminal plea. It bought a wartime peak in armor and paid for it in the trough. It nearly dissolved itself into Airbus and was saved by the very political walls it had spent decades building. And out of all of that it emerged, under a hard-nosed oilman's operating discipline, as one of the most strategically entrenched industrial franchises on the planet — the builder of Britain's deterrent, a trusted insider in the Pentagon, and now a claimant on the high ground of space.

The story from here is not a foregone conclusion. The moats are real, but the software insurgents are real too; the backlog is enormous, but the welders to work it are scarce; the space bet is bold, but it was bought at a boom-time price. What BAE has that almost nothing else in the public markets possesses is time — a line of sight into demand that stretches past 2060, underwritten by governments that cannot afford to let it fail. Whether it converts that time into compounding returns will come down, as it always has, to execution and capital discipline. On the evidence of the last decade, that is a bet the current management has earned the right to be trusted on — and the next decade is where the trust gets tested.

References

-

BAE Systems completes acquisition of Ball Aerospace — Aerospace Manufacturing and Design, 2024-02 ↩↩

-

BAE Systems agreement to acquire Ball Aerospace — BAE Systems, 2023-08 ↩↩↩↩

-

BAE Systems — British Aerospace & Defense Giant, Britannica Money ↩

-

30 November 1999: BAE Systems formed in £7.7bn merger — MoneyWeek ↩

-

BAE Systems Platforms & Services / United Defense acquisition (2005) — S&P Global Ratings ↩

-

BAE Systems to acquire Armor Holdings for $4.1 billion — Manufacturing.net, 2007-05 ↩

-

BAE Systems plc Pleads Guilty and Ordered to Pay $400 Million Criminal Fine — U.S. Department of Justice, 2010-03-01 ↩

-

BAE and EADS scrap $45 billion merger plan — Reuters, 2012-10-10 ↩↩

-

BAE Systems reports record £30.7 billion sales and £83.6 billion order backlog in 2025 full year results — Defence Industry Europe, 2026-02-18 ↩↩↩↩↩↩↩↩↩↩↩

-

Australia selects BAE to build nuclear powered submarines / UK SSN-AUKUS contracts — UK Defence Journal, 2023-10 ↩↩

-

BAE Systems buys Ball Aerospace for $5.5 billion, expanding defense and space capabilities — GovExec Space Project, 2024-02 ↩

-

BAE Systems Announces 2025 Full Year Results — City A.M., 2026-02-18 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube