B2 Impact: The Arbitrage of Stress

I. Introduction: The Business of Second Chances

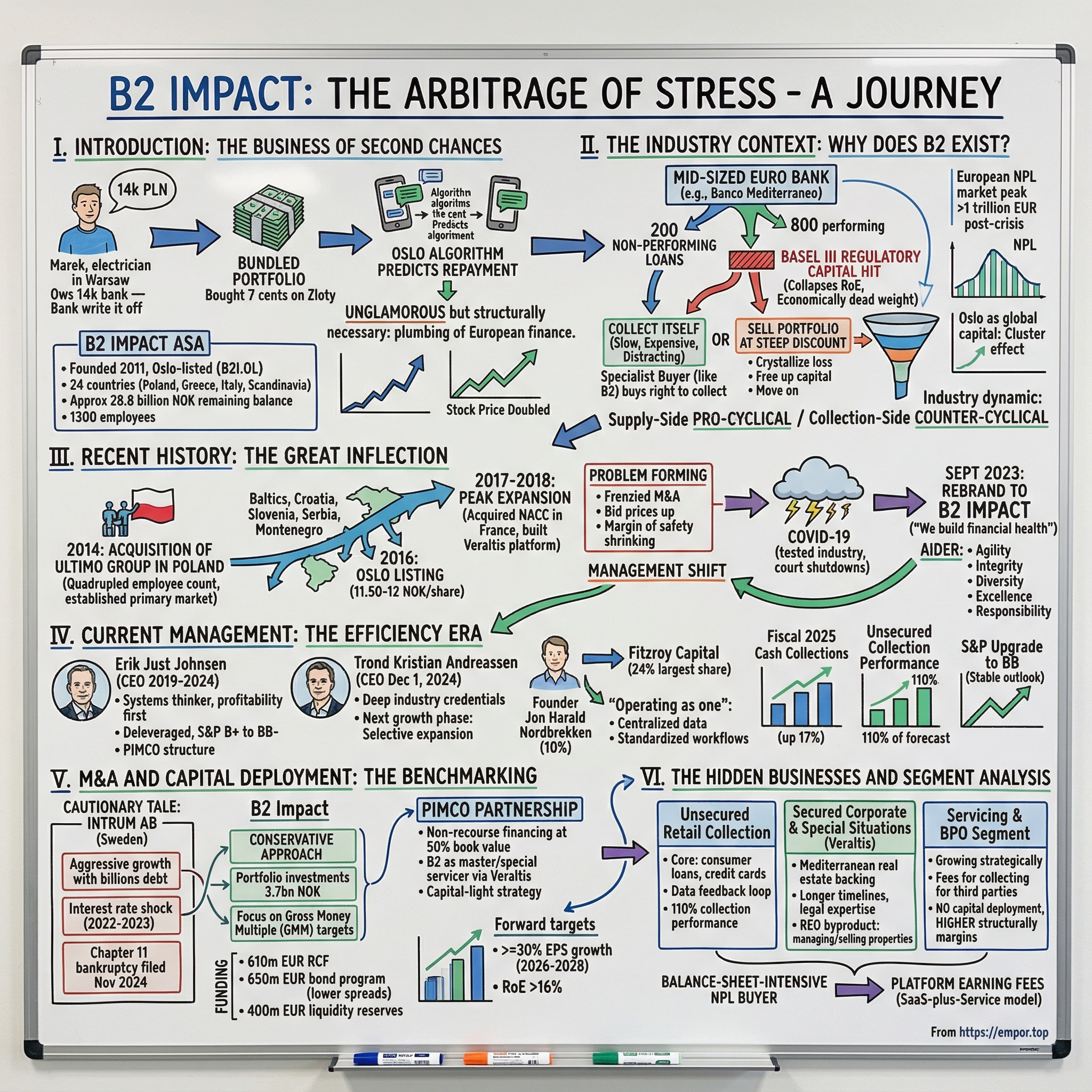

Somewhere in Warsaw right now, a thirty-seven-year-old electrician named Marek owes a bank fourteen thousand zloty on a consumer loan he stopped paying two years ago. The bank has written it off, absorbed the regulatory capital hit, and moved on. But Marek's debt has not disappeared. It has been bundled with tens of thousands of similar obligations into a portfolio, assigned a statistical probability of recovery, and sold at auction to a specialist buyer for roughly seven cents on the zloty. An algorithm in Oslo has already predicted that Marek will eventually repay about eleven hundred zloty over the next thirty months, most likely through a structured payment plan offered via a text message that arrives on his phone three days after payday, worded in a tone calibrated to be firm but not hostile.

This is the business of non-performing loan collection, and it is one of the essential but largely invisible mechanisms that keeps the European banking system from seizing up. When banks hold too many bad loans on their books, regulators force them to set aside capital against those losses — capital that could otherwise fund new lending. The bank's return on equity collapses. Credit markets tighten. Economies stall. The firms that buy these distressed portfolios at a discount, collect what they can, and recycle the recovered cash into the next purchase are performing an unglamorous but structurally necessary function. They are the plumbing of European finance.

B2 Impact ASA — formerly B2Holding, listed on the Oslo Stock Exchange under the ticker B2I — is one of those firms. Headquartered in Oslo, operating across 24 countries with particular strength in Poland, Greece, Italy, and Scandinavia, the company manages an estimated remaining collection balance of approximately 28.8 billion Norwegian kroner. It employs roughly 1,300 people. Its stock has more than doubled over the past year. And its story is, in many ways, the story of the European economy itself: a tale of crisis, recovery, discipline, and the recurring question of what happens when the bills come due.

The company was founded in 2011 by Jon Harald Nordbrekken, a Norwegian serial entrepreneur who had already built and sold two major debt collection businesses before deciding to do it a third time. It went public in 2016. It spent the second half of the 2010s on a rapid acquisition spree across Central and Eastern Europe. It survived a pandemic. It rebranded itself from a "debt collector" to a company that "builds financial health." And under successive management teams, it pivoted from aggressive balance sheet expansion to a capital-light model that increasingly earns fees for managing other people's money rather than deploying its own.

The roadmap of this story runs from the post-2012 European bank deleveraging that created the industry's modern form, through the aggressive M&A of the mid-2010s, to the efficiency-focused strategy of the 2020s. Along the way, B2 Impact watched its largest competitor, Intrum, stumble into Chapter 11 bankruptcy protection under the weight of over five billion dollars in debt — a cautionary tale that B2's own conservative capital deployment helped it avoid. To understand how, you first have to understand why this industry exists at all.

II. The Industry Context: Why Does B2 Exist?

Picture a mid-sized European bank — call it Banco Mediterraneo — that extended a thousand consumer loans during the boom years before 2012. Two hundred of those loans are now non-performing: the borrowers stopped paying more than ninety days ago. Under the Basel III regulatory framework that was phased in after the global financial crisis, the bank must hold capital against those bad loans in proportion to their riskiness. The worse the loan, the more capital must be set aside. Every euro held in reserve against a bad loan is a euro that cannot be lent to a creditworthy borrower or returned to shareholders. The bad loans are not just financial losses. They are economic dead weight that drags down the bank's return on equity and constrains its ability to function.

The bank has a choice. It can try to collect on these loans itself, deploying internal resources to chase delinquent borrowers — a process that is slow, expensive, and operationally distracting for an institution whose core competence is lending, not collections. Or it can sell the entire portfolio to a specialist buyer at a steep discount to face value, crystallize the loss, free up the regulatory capital, and move on. The math almost always favors selling.

This is where the NPL industry enters. Think of it as a secondary market for broken promises. A bank bundles its non-performing loans into a portfolio, hires an investment bank or advisory firm to run an auction, and sells the portfolio to the highest bidder at a fraction of the original balance. The buyer — a firm like B2 Impact — now owns the legal right to collect whatever it can from those borrowers. The difference between the purchase price and the total amount eventually collected, minus operating costs, is the profit.

The mechanics sound simple, but the execution is extraordinarily complex. Each loan is governed by the consumer protection laws of the country where the borrower resides. Collection practices that are legal in Poland may be prohibited in Greece. Payment plan structures that work for Scandinavian consumers may fail entirely with Italian borrowers. The regulatory licensing requirements differ across every jurisdiction. And the fundamental challenge of predicting how much money will actually be recovered from a portfolio of thousands of individual human beings, each with their own financial circumstances, psychological responses, and legal options, requires data models of considerable sophistication.

The European NPL market peaked at over one trillion euros following the sovereign debt crisis, when banks across Southern and Eastern Europe were drowning in bad loans. Regulatory pressure from the European Central Bank, combined with the EU's backstop regulation forcing banks to provision against non-performing exposures on strict timelines, created an unprecedented wave of forced selling. By late 2024, total NPL volumes across European banks had declined to roughly 375 billion euros — still an enormous market, and one that shows signs of growing again as the effects of the post-2022 interest rate hiking cycle work through the economy.

Oslo became the unlikely global capital of this industry through a combination of historical accident and entrepreneurial recycling. Intrum was founded in Stockholm in 1923. Lindorff had Norwegian roots stretching back decades. Aktiv Kapital, founded in Oslo in 1991 by the same Jon Harald Nordbrekken who would later create B2Holding, was among the first European firms to professionalize distressed debt purchasing. When Nordbrekken sold Aktiv Kapital, then built and sold Gothia Financial Group, and then founded B2Holding in 2011, he was drawing on a talent pool of Norwegian executives who had been rotating through the same industry for twenty years. Axactor, another Oslo-listed debt purchaser, was founded in 2015 by alumni of the same ecosystem. The Oslo Stock Exchange became the natural listing venue, and the Norwegian high-yield bond market — the "Norwegian Bond" phenomenon — provided the financing. A cluster effect took hold, and Oslo became to distressed debt what Hartford is to insurance.

For investors, the essential insight about this industry is that it is pro-cyclical on the supply side but counter-cyclical on the collection side. When economies weaken, more loans go bad, and banks sell more portfolios — that is good for the buyer because supply increases and prices tend to improve. But collection rates on existing portfolios may soften because borrowers have less ability to pay. The reverse is also true: in strong economies, supply of new portfolios dries up because fewer loans default, but collections on the existing book improve because borrowers are more solvent. This push-pull dynamic creates a business that is never entirely in or out of favor, and the firms that manage it best are the ones that can price portfolios accurately through the cycle.

Understanding that pricing discipline — the ability to model distress accurately across two dozen borders — is the key to understanding how B2 Impact survived the decade that broke several of its competitors.

III. Recent History: The Great Inflection

In the spring of 2014, B2Holding was a small Norwegian company with a handful of employees and an ambition that vastly outstripped its balance sheet. Jon Harald Nordbrekken, the founder, knew the playbook cold — he had run it twice before with Aktiv Kapital and Gothia Financial Group. The thesis was the same each time: buy distressed loan portfolios in markets where banks are forced sellers, build local collection operations, and generate returns that exceed the cost of funding. The twist this time was geography. Nordbrekken looked east.

The acquisition of the Ultimo Group in Poland from private equity firm Advent International was the transformative deal. It roughly quadrupled B2Holding's employee count overnight and established Poland as the company's single largest market, a position it still holds today. Poland offered a near-ideal combination: a large consumer credit market with high NPL volumes, a legal framework that supported debt recovery, and labor costs significantly below Scandinavian levels. The Ultimo acquisition gave B2 an operational platform — technology, staff, regulatory licenses, banking relationships — that could be used to acquire and service additional Polish portfolios at scale.

From there, the expansion accelerated. B2 Kapital operations were established in Croatia, Slovenia, Serbia, and Montenegro. Acquisitions followed in the Baltics. In 2016, the company listed on the Oslo Stock Exchange at a price in the range of 11.50 to 12 Norwegian kroner per share, raising capital to fuel further growth. Then came 2017 and 2018, the peak of the European NPL expansion era. B2Holding acquired NACC, one of France's leading debt purchasers, for an enterprise value of approximately 90 million euros. It built out the Veraltis platform across eight countries around the Mediterranean — Croatia, Cyprus, France, Greece, Italy, Romania, Bulgaria, and Serbia — focusing on corporate and secured debt. Additional acquisitions in Spain, Lithuania, and Denmark followed.

By late 2018, B2Holding had become a top-ten European debt purchaser with operations spanning more than twenty countries. The growth was exhilarating on the surface, but beneath the headline numbers, a problem was forming. The NPL gold rush of 2016 to 2018 had attracted a flood of capital — private equity funds, hedge funds, new publicly listed vehicles — all chasing the same finite pool of portfolios. Prices were bid up. Gross money multiples, the ratio of total expected collections to purchase price, compressed. Portfolios that might have been purchased at four or five cents on the euro a few years earlier were now trading at seven or eight cents. The margin of safety was shrinking.

Management recognized the danger. The frenzied M&A pace of 2017 and 2018 gave way to a more measured approach. The company began to emphasize collection efficiency on its existing portfolio rather than adding new volume for its own sake. This was the early phase of a philosophical shift that would fully crystallize under subsequent leadership: the move from "empire building" to "efficiency mining."

Then came COVID-19, which tested the debt collection industry in ways that no stress model had anticipated. Courts across Europe shut down, freezing the legal proceedings that debt collectors depend on for secured loan recovery. Collection activity on unsecured portfolios initially declined as borrowers pulled back, governments imposed moratoriums on certain types of debt enforcement, and the operational disruption of remote work hit collection call centers. But the impact was more nuanced than the headlines suggested. B2Holding's diversification across 20-plus countries meant that different markets recovered at different rates, and the unsecured retail book in Poland and Scandinavia proved remarkably resilient. Borrowers who had been on payment plans often continued paying, and the shift to digital collection channels — text messages, online payment portals, email reminders — actually improved efficiency in some markets.

The pandemic also accelerated a strategic reorientation that had been underway since 2019. In September 2023, the company formally rebranded from B2Holding to B2 Impact, adopting a new ticker symbol and a new corporate identity built around the tagline "We build financial health." The name change was more than cosmetic. It reflected a genuine shift in how the company positioned its collection practices, moving away from the confrontational language of "debt recovery" toward a rehabilitation-focused approach emphasizing flexible payment plans, financial counseling, and what management framed as giving borrowers "a new opportunity" to resolve their obligations. The company codified its values under the acronym AIDER — Agility, Integrity, Diversity, Excellence, Responsibility. All core unsecured markets were subsequently rebranded under the B2 Impact name during 2024.

Whether this ESG-inflected narrative represents a substantive change in collection practices or primarily a branding exercise is a matter of debate among industry observers. What is not debatable is that the rebrand coincided with a period of genuine operational improvement, margin expansion, and strategic focus that has transformed the company's financial profile. The question of who drove that transformation leads directly to the management team that took charge as the expansion era ended.

IV. Current Management: The Efficiency Era

Erik Just Johnsen was not the obvious choice for a transformation CEO. An MBA from the University of Chicago in finance, he had joined B2Holding in 2013 as Chief Group Controller — a back-office analytical role far from the deal-making front lines where the company's identity was being forged. He rose to CFO in January 2017, managing the balance sheet through the peak acquisition years. When founding-era CEO Olav Dalen Zahl departed in August 2019, Johnsen stepped into the top role.

The transition from CFO to CEO marked a philosophical shift as much as a personnel change. Where Zahl and the founding team had been builders and deal-makers — people who thought in terms of markets entered, platforms acquired, and portfolios purchased — Johnsen was a systems thinker, someone who looked at the machine and asked whether it was running efficiently. His first public statement as CEO set the tone: the priority would be profitability, return on capital, and value creation, not growth for its own sake.

Under Johnsen, the company deleveraged its balance sheet, negotiated the PIMCO financing structure that became the cornerstone of its capital-light strategy, improved the S&P credit rating from B-plus to BB-minus, and oversaw the rebrand to B2 Impact. He managed through the pandemic, the post-pandemic interest rate shock, and the competitive upheaval caused by Intrum's distress. By December 2024, when he stepped down, B2 Impact was a materially stronger company than the one he had inherited. In his departing statement, he noted that "with the company in a solid position, it is time to hand over the leadership."

His successor, Trond Kristian Andreassen, took the CEO role on December 1, 2024. Andreassen brought deep industry credentials: prior CEO stints at Avida Finans, Gothia Financial Group, and Arvato Financial Solutions across multiple European markets. He had served on B2 Impact's board since May 2020, giving him familiarity with the company's strategy and challenges before taking the operational helm. The board described him as having "solid industry knowledge and experience" for the next growth phase — language that signaled the company was ready to shift from consolidation back toward selective expansion.

The incentive structure under the current leadership reflects the strategic priorities. The Long-Term Incentive Program grants share options tied to performance targets that emphasize return on equity and cash EBITDA rather than portfolio volume or revenue growth. The 2024 LTIP granted 2.7 million options with a strike price of roughly 9.67 kroner, with an annual cap limiting option grants to no more than 0.75 percent of share capital. The structure is designed to reward efficiency and capital discipline, not empire building.

The ownership structure has undergone significant change. Fitzroy Capital recently acquired approximately 24 percent of the company through purchases from Rasmussengruppen and Prioritet Group, making it the largest single shareholder. Founder Jon Harald Nordbrekken retains roughly 10 percent through his investment vehicles. Egil Stenshagen holds about 8 percent. DNB Asset Management holds approximately 5.5 percent. The boardroom also saw turnover: Chairman Harald L. Thorstein stepped down at the May 2025 annual general meeting, replaced by Ole Groterud. These shifts suggest a company in a governance transition that matches its strategic transition — new shareholders, new leadership, new priorities.

The operational culture has shifted from decentralized local autonomy to a more centralized, data-driven model. During the expansion era, each country operation ran largely independently, with local management making pricing, collection strategy, and staffing decisions with limited coordination from Oslo. Under the efficiency era, the company has invested in centralized data infrastructure, standardized collection workflows, and shared technology platforms that allow the Oslo headquarters to set strategy while local teams execute with local knowledge. The goal is what management calls "operating as one" — a unified company that leverages its cross-border data advantage while maintaining the local regulatory expertise and cultural nuance that debt collection requires.

The practical result is visible in the numbers. Cash collections in fiscal year 2025 reached 6.17 billion kroner, up 17 percent year over year. Cash EBITDA hit 4.73 billion kroner. Adjusted net profit rose to 703 million kroner, with adjusted earnings per share of 1.91 kroner. Unsecured collection performance — the ratio of actual cash collected to model forecasts — came in at 110 percent, meaning the company collected significantly more than its own models predicted. The dividend rose to 1.90 kroner per share, up from 1.50 the prior year. And the leverage ratio stood at 2.1 times, comfortably within the company's target of below 2.5 times.

On April 1, 2026, S&P Global Ratings upgraded B2 Impact's credit rating to BB with a stable outlook, the latest step in a multi-year trajectory from B-plus to BB. Credit upgrades in this industry are not just prestige signals — they directly reduce the cost of borrowing, which in a business where funding costs determine the spread between purchase price and collection yield, flows straight to the bottom line.

V. M&A and Capital Deployment: The Benchmarking

The most instructive way to understand B2 Impact's capital allocation philosophy is to compare it to the company that did the opposite. In November 2024, Intrum AB, the Swedish debt purchaser that had been the largest player in Europe, filed for Chapter 11 bankruptcy protection in a Texas court to restructure approximately 5.3 billion dollars in debt. The plan was confirmed on December 31, 2024. Intrum had pursued aggressive growth through the late 2010s, deploying billions in portfolio purchases funded heavily with debt. When interest rates rose sharply in 2022 and 2023, the cost of servicing that debt ballooned while collection yields could not keep pace. The company sold over ten thousand portfolios to Cerberus Capital Management for more than one billion euros in a fire sale to reduce its obligations.

B2 Impact watched this unfold from a position of relative strength — not because it had been prescient about interest rate movements, but because its approach to capital deployment during the critical 2020 to 2023 period was fundamentally more conservative. While other players were chasing volume in an increasingly competitive market, B2 was deliberately restraining its investment pace. Total portfolio investments in fiscal year 2025 were 3.7 billion kroner, roughly in line with the company's capacity but well below the levels that would have strained the balance sheet. The 2022-2023 buying spree that destroyed Intrum was the buying spree that B2 largely sat out, and that discipline proved to be the most important capital allocation decision of the decade.

The Veraltis platform deserves particular attention because it represents a distinct business model within B2. Veraltis Asset Management operates across eight countries around the Mediterranean, specializing in corporate and secured debt — loans backed by real estate, commercial property, or business assets. This is fundamentally different from the unsecured consumer debt that dominates the Polish and Scandinavian operations. Secured debt recovery involves longer timelines, complex legal proceedings, property management, and eventual asset disposition. It requires specialized skills in real estate valuation, legal coordination across multiple jurisdictions, and patient capital. In February 2026, B2 Impact fully absorbed its Romanian Veraltis subsidiary through a merger, simplifying the corporate structure and consolidating the secured asset management operations.

The critical metric for evaluating portfolio purchases in this industry is the Gross Money Multiple — the total amount of cash expected to be collected from a portfolio over its lifetime divided by the purchase price. A GMM of 2.0 means the buyer expects to collect twice what it paid, before operating costs. Higher GMMs indicate either more conservative pricing or higher expected recovery rates. B2 Impact targets GMMs that reflect its priority of returns over volume. When competitors bid more aggressively, pushing GMMs down toward 1.5 or lower, B2 has demonstrated willingness to walk away. This discipline is easier to describe than to practice, because every portfolio not purchased is revenue not earned, and the pressure to deploy capital can override analytical rigor. The Intrum cautionary tale makes the case for why it should not.

The PIMCO partnership, announced in February 2022 and closed in August of that year, represented the clearest structural expression of the capital-light strategy. Under the arrangement, a PIMCO-managed entity provides non-recourse senior financing at approximately 50 percent of the book value of included assets, covering portfolios across most of B2's Central and Eastern European, Southeastern European, French, and Italian markets. B2 Impact serves as the master and special servicer through its Veraltis platform, earning fees for managing the assets while PIMCO bears a significant portion of the balance sheet risk. The structure also allows for co-investments on larger portfolios, giving B2 the ability to participate in deals that would otherwise exceed its standalone capacity.

The funding architecture reinforces the discipline. B2 Impact maintains a 610 million euro senior secured revolving credit facility with DNB, Nordea, and Swedbank, maturing in June 2028 with a one-year extension option. The bond program totals approximately 650 million euros across three series issued between September 2024 and September 2025, all at materially tighter spreads than prior issuances. The September 2025 bond alone generated annual cost savings of 40 million kroner compared to the debt it replaced. Total liquidity reserves stand at roughly 400 million euros, and no major debt maturity comes due until 2027. This is a balance sheet designed for opportunity rather than survival — the kind of positioning that allows management to be selective rather than desperate in portfolio acquisition.

The forward-looking targets announced with the fiscal year 2025 results speak to the ambition of the next phase: at least 30 percent earnings-per-share growth over the 2026 to 2028 period, return on equity above 16 percent, leverage below 2.5 times, and cumulative investments exceeding 10 billion kroner. These are not the targets of a company in defensive mode. They are the targets of a company that believes the competitive landscape has cleared and the supply environment is turning in its favor.

VI. The Hidden Businesses and Segment Analysis

To understand how B2 Impact actually makes money, you need to see past the "debt collector" label and recognize that the company operates what are effectively four distinct businesses, each with different risk profiles, margin structures, and strategic importance. The mix between them reveals where the company is heading.

The first and largest business is unsecured retail collection — the bread and butter of Poland and Scandinavia. This is the high-volume, data-intensive core: consumer loans, credit card balances, telecommunications debts, utility arrears. Individual claim sizes are small, often just a few hundred or a few thousand euros. But the volumes are enormous — hundreds of thousands of individual debtor accounts in a single portfolio. The economics depend entirely on data. Every interaction with every debtor in Poland — every payment, every missed payment, every response to a text message, every payment plan that holds or breaks — generates information that refines B2's pricing models for the next Polish portfolio it considers purchasing. The feedback loop is the business model: collect, learn, price more accurately, buy the next portfolio at a better risk-adjusted return, repeat.

The collection performance metric tells the story of this segment's health. In fiscal year 2025, unsecured collection performance came in at 110 percent of forecast — meaning the company's models predicted it would collect a certain amount, and it actually collected ten percent more. Beating your own model by ten percent is significant. It means either the models were conservative (good discipline) or the collection operations are getting more effective (good execution) or both. Over time, this metric should converge toward 100 percent as models become more accurate. Consistently outperforming forecasts is a sign that the company is erring on the side of caution in its pricing, which is the right kind of error to make in this business.

The second business is secured corporate and special situations — the domain of Veraltis. This is fundamentally different from unsecured retail. The underlying assets are commercial properties, residential developments, corporate real estate, and business assets. The claim sizes are much larger, often running into millions of euros for a single exposure. The recovery process involves legal proceedings that can stretch for years, property valuations that fluctuate with real estate markets, and workout negotiations that require deep local expertise. Greece and Italy are the primary markets.

What makes Veraltis strategically interesting is that it functions as a hidden asset management business within the corporate structure of a debt collector. When B2 Impact buys a portfolio of secured loans backed by Greek commercial real estate, it is not just buying the right to collect cash — it is buying, in economic substance, a claim on physical property. The recovery process often ends with B2 taking ownership of the underlying real estate, managing it, and eventually selling it at what it hopes is a gain. This turns a portion of B2 Impact into something that looks more like a distressed real estate fund than a collections company.

The REO — Real Estate Owned — business is an extension of this dynamic. When the legal process on a secured loan concludes with the creditor taking possession of the collateral, B2 Impact becomes a property owner. It must maintain the property, insure it, market it, and sell it. In Greece and parts of Southern Europe, where real estate markets have been recovering from post-crisis lows, this has occasionally generated windfall gains as properties seized at crisis-era valuations are sold into improving markets. But REO is operationally messy: property management is not a core competence for a debt collection company, and the capital tied up in physical real estate is capital that cannot be deployed into higher-returning NPL portfolios. Management has generally treated REO as a necessary byproduct of the secured business rather than a strategic priority.

The third and most strategically significant hidden business is the servicing and BPO segment. This is where B2 Impact earns fees for collecting debt on behalf of third parties — banks, other financial institutions, or co-investment partners like PIMCO — without deploying its own capital to purchase the underlying portfolios. Think of it as the difference between buying a rental property (NPL purchasing) and managing one for someone else (BPO servicing). The economics are entirely different: servicing fees require no balance sheet commitment, no funding costs, and no portfolio risk. Every euro of servicing income is earned purely on operational capability.

The growth of this segment reflects the capital-light pivot in action. As B2 Impact builds its reputation for collection effectiveness across 24 countries, it becomes increasingly attractive as a servicing partner for institutional investors who want exposure to European NPL returns but lack the operational infrastructure to collect. The PIMCO arrangement is the largest example, but the model is scalable: any institutional investor with an appetite for European distressed debt but no collection platform becomes a potential servicing client. The margin on servicing revenue is structurally higher than on portfolio investment because there is no capital at risk, no funding cost to deduct, and no portfolio impairment to worry about.

The segment mix tells the story of B2 Impact's evolution. In the early years, the company was overwhelmingly a balance-sheet-intensive NPL buyer, deploying its own capital and earning returns on the spread between purchase price and collections. Under the capital-light strategy, the emphasis has shifted toward growing the servicing business as a percentage of total revenue, because it generates returns without consuming capital, and toward maintaining the NPL purchasing business at a scale that supports the data models and partner relationships but does not strain the balance sheet. The ideal B2 Impact of the future looks less like a distressed debt fund and more like a platform that earns fees for applying its collection expertise to capital provided by others — a model that one might describe as "SaaS-plus-Service" for the NPL market.

VII. The Playbook: Hamilton's 7 Powers and Porter's 5 Forces

The debt purchasing industry looks commoditized on the surface. Banks sell loan portfolios. Buyers bid. The highest bidder wins. In this framing, competitive advantages should be minimal, and margins should compress toward zero over time. But the industry's actual dynamics are more nuanced, and applying strategic frameworks reveals why certain players consistently outperform.

Start with Hamilton Helmer's 7 Powers. The primary power B2 Impact possesses is scale economies, but not the conventional manufacturing kind. This is a data scale economy. Every consumer interaction across B2's 24-country footprint generates information: which debtor profiles respond to text messages versus phone calls, which payment plan structures have the highest completion rates in Poland versus Greece, what time of month and what day of week produce the highest contact success rates, how legal enforcement timelines vary by court district in Italy. This information accumulates in B2's pricing models, making every subsequent portfolio bid in those markets statistically more accurate. A smaller competitor entering the Polish market for the first time has no historical dataset to work from. Their pricing models are, by definition, less accurate, which means they will either overpay for portfolios or underbid and miss the market entirely. B2's decade-plus of collection data in Poland is a compounding asset that grows more valuable with each portfolio collected.

The second relevant power is switching costs, but they operate in an unexpected direction. Banks switching between debt purchasers face low switching costs — they can sell their next portfolio to whoever offers the best price. But the regulatory switching costs are high. In many European jurisdictions, debt purchasers and servicers must obtain specific licenses, demonstrate compliance capabilities, and maintain ongoing regulatory relationships with national financial supervisory authorities. B2 Impact holds licenses across 24 countries, has established compliance infrastructures in each, and has built trust with local regulators over years of operating history. A new entrant cannot acquire these relationships overnight. Banks also develop institutional comfort with buyers who have demonstrated the ability to close complex transactions reliably and manage collection operations in compliance with local consumer protection laws. This regulatory and relationship "stickiness" is not absolute, but it creates friction that benefits incumbents.

The third power is what Helmer calls a cornered resource — in B2's case, its proprietary collection platforms. The technology infrastructure built to manage collection workflows across 24 jurisdictions, each with different legal frameworks, consumer protection rules, and communication regulations, represents a substantial and difficult-to-replicate asset. The collection "recipes" — the jurisdiction-specific sequences of contact attempts, payment plan offers, legal actions, and debtor engagement strategies — are embedded in these platforms and have been refined through years of operational trial and error. A self-employed taxi driver in Athens requires a completely different approach than a salaried municipal employee in Stockholm. The accumulated knowledge of what works, encoded in software and standard operating procedures across two dozen markets, is the operational moat.

Now layer on Porter's Five Forces. The bargaining power of suppliers — meaning the banks that sell NPL portfolios — is structurally limited. Banks are not selling NPLs because they want to. They are selling because regulators require them to, because holding non-performing loans on the balance sheet consumes expensive regulatory capital. This creates a structural supply dynamic that operates regardless of market conditions. When the economy weakens and NPL volumes rise, banks must sell more. When the economy strengthens and banks are profitable, they still must comply with minimum NPL ratios. The EU's NPL Directive, adopted in 2021 with a December 2023 transposition deadline, further formalized the framework by creating harmonized licensing and passporting mechanisms for credit servicers across the EU, expanding the cross-border market for authorized players like B2.

Competitive rivalry is the force that most directly threatens margins. The European NPL market includes a diverse set of players: publicly listed specialists (B2 Impact, KRUK, Hoist Finance, Axactor), large servicing platforms (doValue, Intrum post-restructuring), private equity funds (Cerberus, Fortress, Blackstone), and specialty credit funds. When all of these players compete for the same portfolios, prices get bid up and returns compress. B2 Impact's approach to managing rivalry has been geographic selectivity — focusing on niche markets in Southeastern Europe where fewer competitors operate and local knowledge creates barriers to entry — combined with the discipline to withdraw from auctions where pricing exceeds rational thresholds.

The threat of new entrants is moderated by the regulatory licensing requirements, the data scale advantages, and the operational complexity of managing collection infrastructure across multiple jurisdictions. The threat of substitutes is low: banks have limited alternatives to NPL sales for balance sheet cleanup, since internal restructuring is expensive and capital-intensive. Buyer power — the bargaining power of the debtors whose loans B2 purchases — is constrained by the legal framework, though consumer protection regulations continue to expand across Europe, gradually limiting the collection methods available to industry players.

Among publicly listed peers, KRUK of Poland stands out as the most formidable competitor, reporting approximately 21 percent return on equity with strong growth and a Central and Eastern European footprint that overlaps significantly with B2's. Hoist Finance in Sweden benefits from a banking license that provides access to cheaper deposit funding. Axactor, backed by John Fredriksen's Geveran Trading at roughly 44 percent ownership, operates in similar Southern European markets. Each player has a slightly different competitive position, but all are benefiting from the same structural dynamic: the competitive field thinned dramatically after Intrum's restructuring, improving pricing power for the survivors.

VIII. The Bear vs. Bull Case

The bear case against B2 Impact begins with funding risk. The company operates with total debt of approximately 10.5 billion kroner against equity of 5.7 billion — a debt-to-equity ratio of about 1.84. While the leverage ratio of 2.1 times is within management's target, the business model requires continuous access to debt markets at reasonable terms. If interest rates rise further, if credit markets tighten, or if the company's credit rating were to be downgraded rather than upgraded, the cost of funding would increase and the spread between purchase price and collection yield would compress. The recent S&P upgrade to BB is reassuring, but the company remains firmly in sub-investment-grade territory, and the pricing of its bonds reflects the associated risk premium.

Regulatory risk is real and growing. Across Europe, consumer protection regulations governing debt collection practices continue to expand. Restrictions on contact frequency, limitations on digital communication methods, expanded debtor protections in southern European jurisdictions, and the potential for political intervention during economic downturns all represent threats to collection efficiency. Any significant tightening of collection rules in Poland, B2's largest single market, would have an outsized impact on results.

There is also the risk of adverse selection — a term borrowed from insurance that describes the danger of systematically buying the worst loans. In any NPL auction, the seller has more information about the borrowers than the buyer. Banks may retain portfolios with higher recovery prospects and sell those with lower prospects. B2's data models are designed to mitigate this risk, but no model is perfect, and the accounting treatment of NPL portfolios involves significant judgment. The carrying value of portfolios on the balance sheet is based on management's estimates of future cash collections — projections that span years and require assumptions about debtor behavior, economic conditions, and legal outcomes. When those estimates are revised downward, as they were during the pandemic, the impact on reported earnings is immediate.

The concentration of geographic exposure warrants attention. Poland is the largest single market, and any economic downturn in Poland that reduces consumer ability to pay would disproportionately affect the company. Similarly, the secured operations in Greece and Italy are exposed to Mediterranean real estate markets that have historically been volatile.

The bull case rests on the convergence of structural supply growth and reduced competition. The post-2022 interest rate hiking cycle pushed millions of European borrowers into financial stress. Stage 2 loans — the category just above non-performing that serves as a leading indicator of future defaults — were running at 9.5 percent of total European bank lending as of early 2025, an elevated level that signals future NPL inflows. As pandemic-era forbearance programs expire and the accumulated effect of higher rates works through consumer and corporate balance sheets, the volume of distressed debt available for purchase is expected to increase. B2 Impact, with its clean balance sheet, upgraded credit rating, and deployed capital capacity, is positioned to be a primary buyer.

The capital-light transition, if it succeeds fully, fundamentally changes the risk-return profile. Fee income from servicing requires no capital deployment, carries no portfolio risk, and generates high margins on a recurring basis. Every new institutional investor that enters the European NPL space but lacks operational collection capability becomes a potential servicing client. The PIMCO partnership is the proof of concept. If B2 can replicate this model with additional institutional partners, the business transforms from a leveraged balance sheet play into something closer to an asset management platform that earns fees on other people's capital — a structurally higher-multiple business with lower capital requirements.

The competitive landscape has shifted decisively in B2's favor. Intrum's restructuring removed the largest and most aggressive competitor from the market for the foreseeable future. Several private equity funds have reduced European NPL exposure. The number of well-capitalized, operationally ready buyers competing at portfolio auctions has contracted, which should translate into better pricing and more attractive return profiles on new investments.

For investors tracking B2 Impact's ongoing performance, two KPIs matter above all others. The first is collection performance versus forecast on the unsecured portfolio — the ratio that measures whether the company is actually collecting what its models predict. This ratio is the most direct measure of the accuracy of B2's pricing models and the effectiveness of its collection operations. The 110 percent figure for fiscal 2025 is strong, but the trajectory matters more than any single reading. Sustained outperformance above 100 percent indicates conservative pricing and effective operations. A decline toward or below 100 percent would signal either deteriorating debtor conditions or overly aggressive pricing on recent portfolio purchases. The second is return on equity, which management has explicitly targeted at above 16 percent for the 2026 to 2028 period. ROE captures both the profitability of the business and the efficiency of capital deployment. At 11 percent currently, ROE is improving but has meaningful ground to cover before reaching the target, and the trajectory of this metric will reveal whether the capital-light pivot and operational improvements are translating into genuinely superior returns on shareholder capital.

IX. Epilogue

B2 Impact exists because the European financial system produces failure at an industrial scale. Every economic cycle generates a new wave of broken promises — mortgages that cannot be serviced, consumer loans that go unpaid, business debts that exceed the debtor's capacity. The banks that originated these loans need someone to clean up the mess, and the companies that do so occupy a permanent if unglamorous niche in the financial ecosystem.

What makes B2 Impact's story worth studying is not the debt itself but the strategic evolution of the company managing it. In a decade, B2 went from a startup founded by a serial entrepreneur in Oslo to a twenty-four-country operation with nearly seven billion kroner in annual cash collections. It survived a pandemic, watched its largest competitor implode, rebranded itself from a debt collector to a "financial health" company, and pivoted from an aggressive balance sheet model to a capital-light platform strategy. Whether the next decade looks more like "SaaS-plus-Service" — fee income earned on institutional capital, powered by proprietary data and collection technology — or reverts to the old model of leveraged balance sheet arbitrage will depend on whether the current management team can deliver on the ambitious targets they have set.

The European economy does not stop producing distressed debt. The question is always who cleans it up, how efficiently, and at what return. B2 Impact has spent a decade learning the answers.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube