Avolta: The Global Toll Collector of Travel

I. Introduction: The Invisible Giant

Here is a thought experiment. Think about the last time you passed through an airport. Not the flight itself, not the security line, not the gate announcement. Think about the fifteen minutes before boarding, when you drifted into a shop.

Maybe you picked up a bottle of water, a neck pillow, or a box of Swiss chocolates you would never buy at home. Maybe you sat down at a Starbucks or grabbed a burger from Shake Shack. You paid, you moved on, you forgot about it entirely.

You just gave money to Avolta.

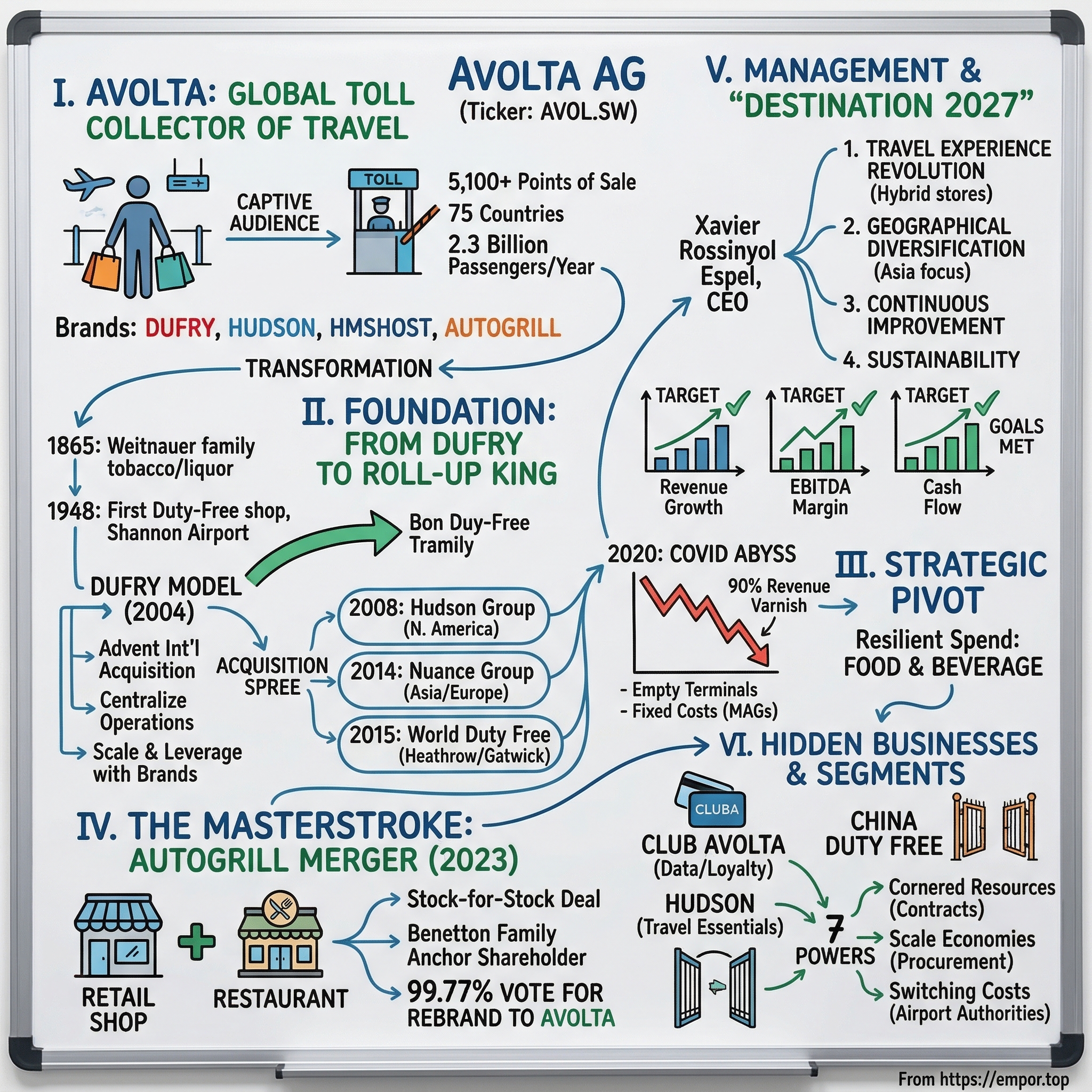

The odds are remarkably high. This Basel-headquartered company operates more than 5,100 points of sale across 75 countries, touching roughly 2.3 billion passengers every year. That is not a typo. Two point three billion. To put that in perspective, if Avolta were a country, its annual "visitors" would represent nearly a third of the world's population.

The company generated over CHF 13.7 billion in revenue in 2024, making it not just the largest travel retailer on the planet, but one of the largest retailers of any kind that most people have never heard of. If you have never encountered the name Avolta, you are not alone. The company operates behind a constellation of brands: Dufry, Hudson, Hudson News, HMSHost, Autogrill, World Duty Free, and dozens of others. The parent company itself is deliberately invisible. It is the holding company behind the holding company, the infrastructure layer beneath the brand you actually recognize.

The thesis behind Avolta is deceptively simple, yet profoundly powerful. Airports are toll booths. Once a traveler clears security, they enter a sealed economic ecosystem where the normal rules of retail competition do not apply. There is no Amazon delivery inside Terminal 5 at Heathrow. There is no walking across the street to find a cheaper coffee. The traveler is, in the most polite sense of the word, a captive audience.

And Avolta is the company that has spent 160 years positioning itself as the toll collector of that captive universe.

What makes the Avolta story truly fascinating is not just its scale, but the audacity of its transformation. This is a company that watched ninety percent of its revenue vanish in the spring of 2020, stared into the abyss of bankruptcy, and then, rather than retreating, made the largest bet in its history.

It swallowed its biggest rival, Autogrill, rebranded itself entirely, and pivoted from being a duty-free shop operator to what it calls the "total travel experience" company. The old Dufry sold perfume and whiskey. The new Avolta wants to own every franc, dollar, and euro a traveler spends from the moment they enter the terminal to the moment they board the plane.

Consider the sheer ambition required. Most companies that survive a ninety-percent revenue decline spend the next decade licking their wounds, paying down debt, and swearing off risk. Avolta did the opposite. It looked at the wreckage of global travel in 2020, decided the business model needed to be fundamentally rebuilt, and then executed the largest merger in the history of travel retail while the industry was still recovering.

Whether this was visionary or reckless may take another decade to fully judge, but the early returns suggest it was closer to the former.

This is the story of how a 160-year-old Swiss company used the worst crisis in aviation history to reinvent itself, and why the result might be one of the most interesting "pick and shovel" plays in global travel.

II. The Foundation: From Dufry to the Roll-up King

Basel, Switzerland, 1865. The Weitnauer family launched a modest tobacco and liquor retail business in a city better known for its pharmaceutical giants than its shopkeepers. Basel was then, as it remains now, the quiet intellectual heart of Switzerland, home to the University of Basel, the chemical and pharmaceutical companies that would become Novartis and Roche, and a merchant class that valued discretion over display.

The Weitnauer firm fit this mold perfectly: a respectable, unflashy business importing and distributing spirits across the Swiss market. For nearly a century, it operated in this mode, building steady relationships with suppliers and customers while the world around it convulsed through two World Wars and a Great Depression.

The pivotal moment came in 1948, when Weitnauer stepped into a business that barely existed yet: duty-free retail. The concept of duty-free shopping had been invented just a year earlier, at Shannon Airport in Ireland, as a way to encourage transatlantic passengers to spend money during refueling stops.

Weitnauer recognized the potential early, and by 1952, it had opened its first continental European duty-free shop in Paris. This was prescient, but premature. International air travel in the 1950s was the province of diplomats, film stars, and the very wealthy. The mass-market airport retail industry that would eventually generate hundreds of billions of dollars in annual revenue was still decades away.

For the next fifty years, Weitnauer grew its duty-free operations gradually, adding locations across Europe and eventually Latin America. But it remained a regional player in what was still a fragmented, localized industry. Each airport operated its own concession process, often awarding contracts to local operators with political connections rather than global scale. The idea that a single company could dominate airport retail worldwide seemed as improbable as the idea that a single airline could fly every route.

The first real transformation came in 2003, when the Weitnauer Group rebranded as Dufry, shedding the family name and signaling a strategic pivot toward pure-play travel retail. The new name, derived from "duty-free," was a declaration of intent: this was no longer a Swiss distribution company that happened to run some airport shops. This was a company whose entire identity was built around travel retail. But the name change was cosmetic compared to what happened next.

In 2004, a consortium led by Advent International, one of the world's most accomplished private equity firms with a particular expertise in retail and consumer businesses, acquired 75 percent of Dufry's outstanding share capital. This was the moment the "Dufry Model" was born.

Advent's playbook was clear and characteristic of the best private equity thinking of the era: strip away everything that was not core to the thesis, centralize operations ruthlessly to create economies of scale, and then use the streamlined platform as an acquisition machine. Dufry divested its wholesale and non-strategic activities, including the legacy Weitnauer Distribution business, and refocused entirely on airport and transit retail.

The company listed on the SIX Swiss Exchange in December 2005, raising capital to fuel the next phase. A separate Dufry Brazil listing followed in 2006, reflecting the importance of Latin America to the growth story. But the real fireworks came in the next decade.

Between 2004 and 2013, Dufry executed a steady drumbeat of acquisitions across Latin America, the Caribbean, and the Mediterranean, building a global footprint one airport at a time.

Each deal followed the same formula: acquire a local operator, plug it into the centralized Dufry procurement and technology platform, strip out redundant overhead, and reinvest the savings into bidding for the next concession.

It was a roll-up strategy, but with a twist that made it more durable than the typical private-equity-fueled consolidation. Unlike most roll-ups, which eventually collapse under the weight of integration complexity or overpayment, Dufry's model actually improved with scale.

The more airports it operated, the more leverage it had with luxury brands like Estee Lauder, Diageo, and Richemont. When you are the single largest buyer of Toblerone chocolate on the planet, the manufacturer will give you a better price per bar than it gives to the operator running a single shop at a regional airport.

The more leverage Dufry had on procurement, the better its margins. The better its margins, the more aggressively it could bid for new concessions while still generating acceptable returns. It was a virtuous cycle, and it was accelerating.

A critical addition came in 2008, when Dufry acquired full control of the Hudson Group for $446 million. Hudson was the dominant operator of newsstands, bookstores, and convenience retail in North American airports and transit hubs, tracing its roots back to its first store at LaGuardia Airport in 1987. The Hudson acquisition gave Dufry something it had never had: a massive position in the world's largest domestic aviation market. While duty-free retail depends on international travelers crossing borders, Hudson sold water, snacks, magazines, and phone chargers to every traveler, domestic or international. This distinction would prove strategically critical in the years ahead.

Then came the shopping spree that changed the industry.

In June 2014, Dufry announced the acquisition of The Nuance Group for CHF 1.55 billion on a debt- and cash-free basis. Nuance was a formidable Swiss competitor, operating approximately 75,000 square meters of retail space across 66 locations in 19 countries, with a concentration in Europe, Asia, and North America. The deal added depth in premium airport locations and, critically, brought significant Asian exposure at a time when Chinese outbound tourism was exploding, growing at double-digit annual rates and creating a wave of luxury-hungry travelers flowing through Asian and European airports. Dufry projected annual pre-tax synergies of approximately CHF 70 million at full run-rate by 2016. The integration was completed ahead of schedule.

Less than a year later, Dufry went even bigger. In March 2015, the company announced the acquisition of a 50.1 percent controlling stake in World Duty Free Group from the Benetton family's Edizione holding company, paying EUR 1.3 billion. A mandatory tender offer for the remaining shares followed at the same price of EUR 10.25 per share. This was a seismic deal. World Duty Free was the second-largest travel retailer in the world, with dominant positions at Heathrow and Gatwick, the crown jewels of European airport retail, and strong operations across Spain and Italy. Expected synergies were up to EUR 100 million annually.

Critics questioned whether Dufry had overpaid. The implied valuation of eight to nine times EV/EBITDA looked expensive by historical travel retail standards. But the critics underestimated what you might call the "Dufry Synergy Machine." By centralizing procurement across an even larger buying volume, consolidating back-office functions and IT systems, and leveraging its newly expanded purchasing power with global luxury brands who now had no choice but to negotiate with Dufry as their primary travel retail channel, the company drove post-synergy multiples down to approximately six times. That was industry-leading. The combined Nuance and World Duty Free acquisitions more than doubled Dufry's turnover and EBITDA, added 17 countries, brought in 836 new retail locations, and grew the employee base from roughly 16,000 to over 31,000.

By 2016, Dufry was the undisputed number one in global travel retail, with roughly 24 percent of the worldwide airport retail market. No competitor was even close. The question was no longer whether Dufry could dominate the industry, but whether a single-product business model, built almost entirely on duty-free luxury goods, could withstand the next downturn. That question was about to be answered in the most brutal way imaginable.

III. The COVID Abyss and The Strategic Pivot

March 2020. The terminals fell silent.

It happened with a speed that defied comprehension. In the first two weeks of March, governments around the world began shutting borders. Airlines grounded their fleets. Airport after airport went dark.

The gleaming retail corridors that normally hummed with the purposeful energy of millions of travelers were reduced to empty, echoing halls lit by the fluorescent glow of unmanned duty-free displays. Bottles of Chanel sat untouched behind glass. Toblerone pyramids gathered dust. The espresso machines fell silent.

For a company like Dufry, whose entire business model depends on the physical presence of travelers walking past its shops, picking up a bottle of perfume, tasting a sample of whiskey, reaching for a bar of chocolate, it was not a slowdown. It was not a recession. It was an extinction-level event.

By April 2020, Dufry's revenue had plunged approximately ninety percent from the prior year. Think about that number for a moment. Not a decline of ninety percent over a year, or a quarter. Ninety percent virtually overnight.

A company generating nearly CHF 9 billion in annual revenue saw its top line collapse to a trickle, while its fixed costs, particularly the concession rents owed to airport authorities around the world, did not disappear.

Dufry's cost structure was designed for a world where 4.5 billion passengers moved through airports annually. Suddenly, the passengers were zero, but the landlords still expected their rent.

This is a crucial point about the economics of concession-based retail that deserves explanation. Airport concession agreements typically include what are called minimum annual guaranteed payments, or MAGs. These are floor-level commitments that the operator must pay to the airport authority regardless of how much revenue the store generates. In normal times, MAGs are a reasonable cost of doing business, typically set well below expected revenue. They give the airport authority confidence that the operator is serious, and they give the operator incentive to maximize sales above the floor. But in a pandemic, when revenue goes to zero, MAGs become financial anvils tied to the operator's ankles. The rent is still due, but there are no customers to pay it.

The full-year 2020 numbers told the story in stark terms. Turnover plunged 71.1 percent year-over-year to CHF 2,561 million, down from CHF 8,856 million in 2019. The adjusted net loss was CHF 1,658 million, a swing of over CHF 2 billion from the prior year's profit.

The company was bleeding cash, and the question facing management was existential: could Dufry survive long enough for travelers to return? And would travelers return in the same numbers, spending on the same luxury goods?

The survival playbook was aggressive, dilutive, and unflinching. In April 2020, Dufry announced a comprehensive capital structure reinforcement that pulled every available lever simultaneously.

On the liquidity side: a new CHF 390 million committed credit facility was secured, with two six-month extension options. The company accessed CHF 142.6 million in COVID-related government-backed loans across its operating jurisdictions. It placed 5 million new shares, generating gross proceeds of CHF 151.3 million, diluting existing shareholders but buying critical liquidity. And it issued CHF 350 million in senior bonds due 2023, conditionally convertible into shares, a structure that prioritized short-term survival over long-term equity value.

On the cost side: management targeted CHF 400 million in recurring fixed cost savings, with CHF 280 million from personnel reductions and CHF 120 million from other operating expenses. Stores were closed. Staff were furloughed or let go. Capital expenditure was frozen.

It was, by any measure, a burn-the-boats moment. The old Dufry that had emerged from the 2014-2015 acquisition spree as a confident, growth-oriented roll-up machine was gone. In its place was a company fighting for survival, making painful choices about headcount, lease renegotiations, and capital structure.

Even 2021 brought only a partial recovery. Revenue climbed to CHF 3,915 million, still less than half of 2019 levels, and the company posted another net loss of CHF 385 million.

The duty-free business was particularly slow to recover because it depended on international travelers, and international borders remained restricted or closed in much of Asia and parts of Europe well into 2021 and 2022. Chinese tourists, who had been the growth engine of global travel retail through the 2010s, were effectively absent from the world stage under China's zero-COVID policy until early 2023. Without the Chinese consumer, the highest-margin duty-free categories, luxury cosmetics, prestige spirits, designer accessories, were operating at a fraction of their potential.

But something else was happening inside the executive suite. The crisis forced a fundamental rethinking of the business model itself.

For years, Dufry had been a one-trick pony: duty-free luxury retail. Perfume, spirits, cosmetics, watches. These categories generated high margins in good times, but they were brutally cyclical and concentrated. When travel stopped, the revenue stopped. When travel resumed, the recovery was uneven, dependent on the return of high-spending international travelers.

A domestic business traveler flying from Dallas to Denver might buy a sandwich and a bottle of water, but they were not going to buy a thousand-dollar bottle of Scotch. And domestic travelers, who make up the bulk of passenger traffic worldwide, had never been Dufry's core customer.

The realization crystallized: Dufry needed what its strategists began calling "resilient spend." It needed categories that were less dependent on international luxury shoppers and more tied to the fundamental act of traveling itself.

Every traveler, whether a business commuter on a domestic shuttle or a family heading to a beach resort, needs to eat. Every traveler needs a coffee, a bottle of water, a sandwich.

Food and beverage was not glamorous like duty-free Chanel, but it was resilient. It was recurring. And it was growing, driven by airports investing billions in terminal upgrades that increasingly prioritized dining experiences alongside traditional retail.

This insight, born from the darkest period in the company's history, would lead directly to the most transformative deal in its existence.

IV. The Masterstroke: The Autogrill Merger

The call came from an unexpected but familiar direction.

Edizione, the Benetton family's investment vehicle, had been part of the Dufry story since 2015, when it sold its controlling stake in World Duty Free Group. The Benetton family had been one of Italy's most prominent business dynasties since the 1960s, building an empire that stretched far beyond the colorful knitwear that made the name famous.

Through Edizione, they controlled Atlantia, the Italian motorway and airport infrastructure giant, several real estate and agricultural businesses, and crucially, Autogrill, the world's largest airport food and beverage operator.

Autogrill's history was quintessentially Italian. Founded in the 1950s to serve travelers on Italy's new autostrada highway system, the company had pioneered the concept of high-quality roadside dining in an era when highway food meant a cold sandwich from a petrol station. If you have ever driven the Italian motorways and marveled at the surprisingly good panini and espresso available at rest stops, you have experienced the Autogrill legacy firsthand.

Over the decades, Autogrill expanded into airports, and in 1999, it made the deal that transformed it into a global player: the acquisition of HMSHost, the dominant airport food and beverage operator in North America. HMSHost had been feeding American travelers since the 1890s, originally as a railroad dining service before pivoting to airports in the postwar era.

It was, in many ways, the food and beverage equivalent of what Hudson was in retail: the incumbent that owned the US market through decades of accumulated concession contracts and institutional relationships.

Now, Edizione held 50.3 percent of Autogrill, and it was thinking about the future. The pandemic had been devastating for Autogrill as well, but the Benetton family was not a distressed seller. They were strategic thinkers, and they saw what Dufry's leadership was beginning to see: that the future of airport commerce was not about retail or dining in isolation, but about the total traveler experience.

A single company that could offer airports both capabilities, from a Chanel counter to a Starbucks, from a luxury liquor collection to a Shake Shack, would be an unbeatable bidder for new concessions and an irreplaceable partner for airport authorities seeking to maximize their commercial revenue.

The logic of combining Dufry and Autogrill was, in hindsight, almost blindingly obvious.

Imagine an airport terminal as a commercial street. On one side, you have the shops: the duty-free boutiques, the electronics stores, the souvenir stands. That was Dufry's world. On the other side, you have the restaurants: the coffee shops, the burger joints, the sit-down dining experiences. That was Autogrill's world.

For decades, these two sides of the terminal had been run by separate companies, competing for the same square footage, negotiating separately with the same airport authorities, and serving the same travelers. It was an obvious inefficiency that no one had been bold enough to fix.

On July 11, 2022, Edizione announced a strategic agreement for the integration of Autogrill into Dufry.

The deal structure was elegant in its complexity and revealed the Benetton family's confidence in the combined entity. Rather than a simple cash acquisition, which would have required Dufry to raise billions in debt or equity at a fragile moment, Edizione transferred its 50.3 percent stake in Autogrill to Dufry in exchange for mandatory convertible non-interest-bearing notes. These notes would convert into 30,663,329 newly issued Dufry shares, at an implied exchange ratio of 0.1581 new Dufry shares per Autogrill share.

Remaining Autogrill minority shareholders were offered the same ratio or a cash alternative of EUR 6.33 per share. The combined entity was valued at approximately $6.7 billion.

The structure accomplished three things simultaneously.

First, it avoided burdening the combined company with additional acquisition debt at a time when leverage was already elevated from the COVID survival measures. This was not a leveraged buyout. This was a stock-for-stock combination.

Second, it aligned Edizione's interests perfectly with those of existing Dufry shareholders, because the Benetton family was receiving Dufry stock, not cash. They were betting on the combined entity succeeding. If Avolta's share price went up, the Benettons would benefit. If it went down, they would suffer alongside every other shareholder. This is the kind of alignment that investors dream about but rarely get.

Third, it gave Edizione a large enough stake in the new company, approximately 25 percent at conversion, to become the anchor shareholder, providing the long-term governance stability that would be essential during a complex multi-year integration. A voting rights cap of 25.1 percent, in effect until June 2029, ensured that Edizione could not unilaterally dominate governance, but its concentrated ownership meant it would be a committed, patient, and engaged partner.

The deal closed on February 3, 2023, with Dufry beginning full consolidation of Autogrill from February 1.

The impact on the financial statements was immediate and dramatic. Revenue leaped from CHF 6.9 billion in 2022 to CHF 12.8 billion in 2023, reflecting the addition of Autogrill's roughly 3,500 food and beverage outlets to Dufry's approximately 1,700 retail locations. On a pro-forma 2019 basis, the combined entity represented approximately CHF 14 billion in turnover, serving 2.3 billion passengers across more than 5,500 outlets in over 75 countries. It was, overnight, the largest travel experience company on earth.

Through Autogrill, Dufry acquired HMSHost, which operated over 1,000 locations in nearly 80 airports across North America, partnering with hundreds of brands from Starbucks and Chick-fil-A to celebrity chef concepts and beloved local restaurants. HMSHost was later recognized as Best Overall Restaurateur at the 2025 AX Awards, a validation of the quality of the asset Avolta had acquired.

Combined with Dufry's existing Hudson subsidiary, the merger gave the new company an unmatched dual presence in North American airports: Hudson on the retail side, HMSHost on the dining side. No other company in the world could walk into an airport authority's office and say: "We can run your entire commercial operation, retail and restaurants, under one contract, with one point of contact, and one integrated strategy."

On November 3, 2023, shareholders voted to rename the company. The vote was 99.77 percent in favor, a near-unanimity that reflected the market's endorsement of the strategy. Dufry AG became Avolta AG, and the new ticker, AVOL, began trading on the SIX Swiss Exchange on November 9. The name was deliberately chosen: "vol" from the Latin for "to fly," referencing the aviation heritage; in Italian, "a volta" means "from time to time," nodding to the Mediterranean roots inherited from Autogrill. There was also an implicit reference to "volt," as in energy, transformation, a jolt of electricity through the old organization.

The rebranding was more than cosmetic. It signaled a fundamental identity shift. The old Dufry was a shop. It sold things. The new Avolta was positioning itself as the architect of the entire traveler experience, from the first coffee after clearing security to the last bottle of whiskey before boarding. The company described this as moving from a "single-engine plane" to a "dual-engine jet," with retail and food and beverage as complementary revenue streams that could cross-sell, co-locate, and share infrastructure.

Was it expensive? The valuation metrics were debated. Dufry paid a meaningful premium for the Benetton family's stake, and the convertible note structure meant significant dilution for existing shareholders. But the strategic rationale was difficult to argue with. No competitor could replicate this combination. Lagardere had travel retail. SSP Group had food and beverage. Only Avolta had both, at global scale, under one roof. And S&P recognized the strategic merit, upgrading the credit rating to BB from BB-minus in July 2023, citing the improved business profile and diversification benefits.

The merger transformed the financial profile in ways that went beyond scale. Food and beverage operates on a fundamentally different economic model than duty-free retail. F&B margins are more predictable, less dependent on the nationality mix of travelers, and more resilient during economic downturns. A family heading on vacation might skip the bottle of Chanel No. 5 when money is tight, but they still need lunch before their flight. This blended model was exactly what the COVID crisis had revealed was needed, and Avolta was now the only company in the world that had built it.

V. Management and The "Destination 2027" Strategy

Xavier Rossinyol Espel was born in 1970 in Spain. He was educated at ESADE in Barcelona with a bachelor's in business administration, completed a joint MBA between ESADE and the University of British Columbia that took him through Spain, Canada, and Hong Kong, and later earned a master's in business law from Universitat Pompeu Fabra.

This is not the profile of a typical retail executive who worked their way up from the shop floor. This is the profile of someone who was built for deal-making, financial engineering, and navigating the legal and cultural complexity of cross-border transactions.

Rossinyol is equally comfortable in a boardroom in Basel, a concession negotiation in Riyadh, and a brand partnership meeting in Milan. He speaks multiple languages, has lived and worked across three continents, and brings a distinctly Mediterranean warmth to a company that, under its Swiss governance structure, could easily become clinical and bureaucratic.

His career arc reads like a carefully plotted novel. From 1995 to 2004, Rossinyol worked at Grupo Areas, a Spanish food services company within the French-listed Elior Group, getting his first taste of the concession-based business model that would define his career. He learned how airport food services worked from the ground up, understanding the unique economics of fixed-rent, high-throughput, captive-audience businesses.

In 2004, the same year Advent International took over Dufry, Rossinyol joined the company as Chief Financial Officer. He was 34 years old, and he was about to spend the next eight years building the financial architecture for one of the most aggressive acquisition campaigns in European retail history. Every deal from the mid-2000s through the early 2010s bore his fingerprints: the financing structures, the synergy models, the integration timelines, the post-deal performance tracking. He was the quiet engine behind the "Dufry Model," turning strategic ambition into executable financial plans.

In 2012, he moved from CFO to Chief Operating Officer for EMEA and Asia, a promotion that took him from the spreadsheet to the shop floor. Running the operational side of the empire he had helped build financially gave him a perspective that few CFOs ever gain: the messy, human reality of managing thousands of retail employees across dozens of countries, each with different labor laws, consumer preferences, and cultural expectations.

Then, in 2015, he left. Rossinyol departed Dufry to become CEO of Gategroup, the Zurich-based airline catering giant that feeds hundreds of millions of airline passengers annually. It was a lateral move within the travel services ecosystem, and it gave him something invaluable: deep operational experience running a food and beverage business at global scale. He was no longer just the financial architect. He was the chief executive, responsible for everything from menu design to supply chain logistics to crisis management. And what a crisis it was: Rossinyol led Gategroup through the pandemic, understanding firsthand how COVID ravaged travel-dependent businesses from the inside.

Then the call came. On February 21, 2022, Dufry announced his appointment as Chief Executive Officer, effective June 1, 2022. He was brought back for a specific reason: to lead the Autogrill integration and execute the company's most ambitious strategic plan. He was, in a sense, the prodigal son, returning to the house he had helped build, but with a decade of additional experience in food services and executive leadership, and a clear mandate for transformation.

The strategic vision he brought back was called "Destination 2027," presented at a Capital Markets Day on September 6, 2022. It was built on four pillars.

The first, and most revolutionary, was what Avolta called the "Travel Experience Revolution": uniting retail and food and beverage under a single offering to deliver seamless, personalized experiences both in-store and digitally.

New-generation stores would allocate 40 to 45 percent of space as flexible activation space, up from just 15 percent previously. This was a radical departure from traditional airport retail, where every square meter was dedicated to fixed product displays. The new approach created stores that could morph, hosting pop-up brand experiences one month, seasonal holiday concepts the next, and critically, integrating food and beverage directly within the retail environment.

A whiskey tasting bar inside a duty-free store. A gelato counter adjacent to the cosmetics aisle. Experiences that made the traveler want to stay, browse, and spend.

The second pillar was geographical diversification, with targeted penetration into high-growth regions, particularly Asia, where rising middle-class populations represented the next wave of global travelers.

The third was continuous improvement, an operational efficiency drive that would extract margin from every corner of the combined business.

The fourth was sustainability, embedded as a core business principle with measurable ESG targets linked to executive compensation.

The financial targets were precise and ambitious: organic revenue growth of five to seven percent per annum, CORE EBITDA margin improvement of 20 to 40 basis points annually, and equity free cash flow conversion improvement of 100 to 150 basis points per year.

These were not aspirational hand-waves. They were measurable commitments tied directly to management compensation through the company's long-term incentive plan. If management missed these targets, their pay would suffer. If they exceeded them, they would be rewarded. This is the kind of explicit, quantified accountability that separates strategic plans that actually drive behavior from glossy investor presentations that sit on a shelf.

This brings us to one of the most important, and underappreciated, aspects of the Avolta story: the alignment of incentives.

The LTIP ties executive compensation to free cash flow per share and total shareholder return relative to the SMI index. Rossinyol's pay is heavily weighted toward outcomes that directly benefit shareholders. Not revenue growth for its own sake. Not EBITDA before lease adjustments. Actual cash flow generation and stock price performance.

The anchor shareholder structure reinforces this alignment. Edizione, the Benetton family's investment vehicle, holds approximately 22 percent of share capital as the largest single shareholder. Alessandro Benetton serves as Honorary Chairman of the board.

The Benetton family thinks in generational timescales. They are not going to pressure management for a short-term exit or a dividend they cannot afford. This is a family that has owned infrastructure assets, from motorways to airports to retail chains, for decades. They understand that the best returns in concession-based businesses come from patience, reinvestment, and compounding.

Advent International, which orchestrated the original 2004 transformation, still holds a position above three percent, alongside notable shareholders including Qatar Holding, Alibaba Group, Richemont, BlackRock, and UBS Fund Management. The top holders collectively represent approximately 55 percent of share capital, a concentrated ownership structure that facilitates decisive strategic action rather than governance paralysis.

Juan Carlos Torres Carretero, the Executive Chairman born in 1949, provides continuity with the pre-merger era and deep institutional knowledge of the concession landscape. The broader management team includes Yves Gerster as CFO, Jordi Martin-Consuegra running North America, Luis Marin Mas Sarda leading EMEA, and Vijay Talwar as Chief Digital and Technology Officer, the person tasked with bringing the data and loyalty strategy to life.

The results, through the first three years of Destination 2027, have validated the strategy.

Fiscal year 2024 delivered revenue growth of 8.9 percent in constant exchange rates, above the top end of the five to seven percent target range. CORE EBITDA margin reached 9.4 percent, with 40 basis points of improvement year-over-year, also at the top of the target range. And equity free cash flow hit CHF 425 million, up 32 percent from the prior year. All three targets were met or exceeded.

Full-year 2025 continued the trajectory. Revenue reached CHF 13.98 billion, with organic growth of 5.4 percent. EBITDA margin expanded to over 10 percent. Net income nearly doubled to CHF 199 million. And equity free cash flow set a new record.

By the nine-month mark of 2025, the deleveraging story had reached a critical milestone: net debt leverage dropped to 1.9 times CORE EBITDA, crossing below the psychologically important two-times threshold for the first time since the Autogrill merger. For a company that many investors had worried was overleveraged, this was a powerful signal. October 2025 organic growth accelerated to 6.0 percent, with North America returning to positive territory.

Dividends were reinstated in 2024 and increased 43 percent to CHF 1.00 per share for fiscal year 2024. A share buyback program was launched, with CHF 129 million repurchased through the first nine months of 2025 and CHF 175 million for the full year. The company was also paying down debt while returning capital, a sign of genuine financial health.

The message was clear: Avolta had transitioned from crisis mode to capital return mode, and the Destination 2027 targets were not just being met but, in most cases, exceeded. The market cap reflected this progress, growing from CHF 3.6 billion at the end of 2022 to approximately CHF 6.3 billion by early 2026.

VI. Hidden Businesses and Segment Analysis

Picture this: a traveler clears security at London Heathrow Terminal 5, the kind of vast, gleaming cathedral of commerce that modern airports have become. She has ninety minutes before her flight.

In the old world, the airport shopping experience was rigidly segregated. The duty-free shop was over there, behind glass walls, organized by brand and category. The food court was over here, a separate cluster of fast-food counters and coffee chains. The two never met.

She might browse the perfume, decide she was not in the mood, walk away, and sit down for a coffee somewhere else entirely. Two separate transactions, two separate companies, two separate experiences, and a total dwell time in the retail zone of perhaps three minutes.

In the Avolta world, the concept is fundamentally different.

She walks into a "hybrid" store, a new-generation retail environment where a curated selection of spirits and cosmetics sits alongside an artisanal coffee bar and a grab-and-go food section. She samples a whiskey at an interactive tasting station, one of the brand activation spaces that now occupy 40 to 45 percent of floor area.

She picks up a latte while browsing. She tries on a fragrance while sipping it, her mood elevated by the experience rather than the transaction. She ends up spending twenty minutes in a space she might have walked past in ten seconds, and her basket at checkout includes items from categories she had no intention of shopping.

The data shows this works. These hybrid formats increase what the industry calls "dwell time," the minutes a traveler spends in a commercial space before moving on. And Avolta has reported that spend-per-head in these formats rises by double digits compared to traditional standalone stores. Double digits. That is the difference between a traveler buying a bottle of water and a traveler buying a bottle of water, a latte, a lipstick, and a box of chocolates.

This hybrid concept is the fastest-growing initiative within the Destination 2027 strategy, and it illustrates why the Autogrill merger was not just about adding a food business to a retail business. It was about creating a format that neither business could have built alone.

Only a company that operates both the coffee machine and the perfume counter can design a space where they reinforce each other. A pure-play retailer proposing to put a coffee bar in its store would need to partner with a separate F&B operator, splitting economics and complicating operations. A pure-play F&B company proposing to add retail would face the same problem in reverse. Avolta faces neither obstacle.

Then there is Hudson, arguably the most underappreciated asset in the entire company.

Hudson operates over 1,000 stores across nearly 90 airports and transportation hubs in the United States and Canada. Its brands include Hudson, Hudson News (the world's largest operator of airport newsstands), Hudson Booksellers, and the newer Evolve by Hudson concept, which modernizes the traditional travel convenience store with upgraded design, digital integration, and a broader product mix.

The company is present in 24 of America's 25 largest airports. Think about that market coverage for a moment. If you fly within the United States with any regularity, Hudson is almost certainly part of your routine, whether you realize it or not.

What makes Hudson strategically important is what it does not sell.

Hudson is not a duty-free operator. It does not depend on international travelers buying luxury goods. Hudson sells what the industry calls "travel essentials": water, snacks, magazines, phone chargers, neck pillows, bestselling paperbacks, last-minute gifts.

These are items that every traveler buys, regardless of whether they are flying from New York to London or from New York to Chicago. Domestic travelers, who represent the vast majority of passenger traffic in the United States, are Hudson's core customer.

This makes Hudson the most resilient part of Avolta's business, relatively immune to the fluctuations in international tourism that drive duty-free volatility. During the pandemic recovery, domestic US travel bounced back far faster than international volumes, and Hudson's revenue recovered accordingly. It was Hudson, not duty-free, that kept the lights on during the darkest days.

Recent contract wins underscore Hudson's competitive position. In late 2024 and into 2025, the company secured 11-plus year contracts for retail and food and beverage concessions at JFK Terminal 8, new dining and retail experiences at JFK Terminal 5 on a seven-year contract, an eight-year retail contract at Salt Lake City International, and a ten-year food and beverage contract at Phoenix Sky Harbor through the HMSHost brand.

These wins are significant not just for their size, but for their structure: increasingly, airport authorities are awarding bundled retail-plus-F&B concessions, which plays directly to Avolta's integrated model and shuts out pure-play competitors who can only bid on one half of the package. This trend, if it continues, could be a structural moat that widens over time.

Perhaps the most intriguing development, and the one with the longest potential runway, is Club Avolta.

Launched globally on September 30, 2024, as a rebrand and expansion of the prior "Red by Dufry" loyalty program, Club Avolta had enrolled over 10 million members by the end of fiscal year 2024. The program operates across 73 countries and all 5,100-plus outlets, with three tiers offering escalating discounts: Silver at five percent, Gold at seven percent, and Platinum at up to ten percent. Food and beverage discounts of five percent apply across all tiers.

But the significance of Club Avolta goes far beyond customer retention and discount programs. It represents Avolta's first serious attempt to build a direct data relationship with its customers.

Historically, travel retailers have operated blind. A traveler walks in, buys something, and leaves. The retailer knows nothing about that person: not their travel patterns, not their preferences, not their upcoming trips.

The airline knows. The hotel knows. The credit card company knows. The retailer did not.

Club Avolta, accessed through a mobile app with QR code scanning at checkout, changes that equation. With data from 2.3 billion annual passengers, Avolta can begin targeting travelers before they even arrive at the airport, through personalized offers, pre-order capabilities, and partner promotions tied to their travel itinerary.

By 2024, the program already accounted for more than five percent of Avolta's annualized revenues, and that figure is growing. The partner ecosystem includes Radisson Rewards for hotel discounts, car rental partnerships, airport lounge access, and lifestyle brand promotions.

This is a playbook borrowed from the airline industry's frequent flyer programs, which have proven to be worth more than the airlines themselves in many cases. Delta's SkyMiles program, for example, was valued at more than twice the market capitalization of the airline itself during the pandemic, because the loyalty data and credit card partnerships generate revenue regardless of whether planes are flying. Avolta's version is in its infancy, but the foundation of 10 million members across 73 countries gives it a reach that no startup loyalty platform could replicate.

In December 2025, Avolta achieved a milestone that underscored its global ambitions: it became the first foreign company to open duty-free shops in Mainland China in 26 years, through its Hudson subsidiary.

China's duty-free market, dominated by state-owned China Duty Free Group, had been effectively closed to foreign operators for decades. Breaking that barrier, even in a limited way, signals that Avolta's scale and government relationships can open doors that remain shut to smaller competitors. It also positions the company for what could eventually be the largest growth market in global travel retail, as China's middle class resumes international travel in the hundreds of millions.

VII. The Seven Powers and Porter's Five Forces

Hamilton Helmer's "7 Powers" framework provides a useful lens for understanding why Avolta's competitive position may be more durable than a superficial analysis suggests. Not all seven powers apply equally, but three stand out with particular force.

The first and most important is what Helmer calls a "cornered resource." In Avolta's case, the cornered resource is the concession contract itself.

Airport retail and food and beverage operate under long-term concession agreements, typically ranging from seven to twelve years, awarded by airport authorities through competitive bidding processes. Once a company wins a concession at a major hub like Heathrow, JFK, or Singapore Changi, no competitor can enter that space until the contract expires.

These are not like retail leases in a shopping mall, where a competitor can open next door if they are willing to pay the rent. These are exclusive operating rights within a physically sealed, security-controlled environment.

Think of it like a government spectrum auction for telecom companies: once you own the license to operate on a particular frequency in a particular geography, no one else can compete with you on that frequency until the license expires. Avolta holds thousands of these "licenses" across 75 countries and approximately 1,200 locations, and the staggered expiry dates create a natural renewal pipeline that provides both revenue visibility and competitive insulation.

The second power is scale economies, and they operate on multiple levels simultaneously.

At the procurement level, Avolta buys more Toblerone, Johnnie Walker, Estee Lauder, and Chanel than almost any other retailer on earth. Its global procurement operation means that its cost on a bottle of gin, a jar of face cream, or a box of chocolates is structurally lower than what a regional competitor pays.

But scale also matters at the bidding level. When an airport authority in, say, Bangkok puts a retail concession out for bid, Avolta can bring to the table not just competitive financial terms, but a proven global track record, established relationships with hundreds of luxury brands, proprietary store design capabilities, digital integration, and now, an integrated F&B offering.

A local operator bidding against Avolta faces a structural disadvantage that has nothing to do with effort or talent and everything to do with the breadth and depth of the platform behind the bid.

The third power is switching costs, but they operate in a counterintuitive direction.

For the consumer, there are effectively zero switching costs. A traveler has no loyalty to the specific operator running the duty-free shop and may not even notice the brand name above the door.

But for the airport authority, switching costs are massive. Replacing an entire airport's retail and food and beverage infrastructure means terminating contracts, removing fixtures, negotiating new brand agreements, hiring and training staff, managing construction in an active terminal, obtaining regulatory approvals, and weathering months of reduced commercial revenue during the transition.

Airport authorities are inherently conservative organizations: they want proven operators who can guarantee revenue shares and minimize operational risk. Avolta's track record across 1,200 locations makes it the "safe choice" for risk-averse authorities, creating a self-reinforcing cycle of contract wins and renewals.

Porter's Five Forces analysis adds additional nuance.

The bargaining power of suppliers, the global luxury and consumer goods brands, is moderate. Brands like Diageo and LVMH have alternatives for reaching consumers, but travel retail is a uniquely valuable channel for them: it reaches affluent, spending-ready customers in an environment free from e-commerce competition, and it serves as a global showroom that builds brand awareness across cultures. Avolta's global reach makes it an essential distribution partner.

The bargaining power of buyers bifurcates sharply.

Airport authorities, the true "landlords," hold significant power. They set the concession terms, demand minimum guaranteed revenue shares that typically consume 25 to 35 percent of operator revenue, and can create competitive tension during bid processes by inviting multiple operators to compete. This is the single biggest structural cost pressure on Avolta's model and the primary reason why margins, despite the captive-audience dynamic, are not higher.

Conversely, the end consumer has almost no bargaining power. They cannot comparison shop across airports. They cannot negotiate prices. They are a captive audience with limited time and limited alternatives within the terminal.

The threat of substitutes is where the story gets more interesting, and potentially more dangerous.

Pre-ordering platforms, where travelers order goods online for airport pickup, are an emerging concept. Several airport e-commerce platforms have launched, and some airlines have begun offering onboard shopping that bypasses the terminal entirely. Airport "delivery" apps that bring food directly to the gate threaten the walk-in traffic model.

These are not yet material threats to Avolta's revenue, but they represent a long-term vector of disruption that bears monitoring. Avolta's response, the Club Avolta loyalty app and digital pre-ordering capabilities, is an attempt to co-opt this disruption rather than be victimized by it.

The threat of new entrants is low in traditional concession-based travel retail, precisely because of the cornered resource dynamic. However, one vector of entry deserves attention: airports building their own in-house retail and F&B operations.

Dubai Duty Free, a government-owned operation generating over $2 billion in annual revenue, proved that airports can successfully internalize the function. Qatar Duty Free and King Power in Thailand represent similar models. If this self-operation trend spreads beyond the Middle East and Southeast Asia to major European or North American hubs, it could erode Avolta's addressable market.

Competitive rivalry is concentrated among a handful of global players. Lagardere Travel Retail is the most direct competitor in travel retail but lacks F&B scale. SSP Group, the UK-listed food and beverage specialist, competes on the dining side but has no retail presence. Gebr. Heinemann, a privately held German company, is strong in European duty-free. Lotte Duty Free, backed by the Korean conglomerate, dominates Asian markets.

None offers the integrated retail-plus-F&B model that Avolta has built, which remains its most distinctive and defensible strategic asset.

VIII. The Playbook: Lessons for Investors

The most useful way to think about Avolta is as a toll booth on global travel.

If you believe, as most macro forecasters do, that international air passenger traffic will grow at three to four percent annually over the coming decade, driven by rising middle-class populations in Asia, Africa, and Latin America, then Avolta is a leveraged bet on that reality. Not leveraged in the financial sense, although the company does carry meaningful debt, but leveraged in the operational sense: every incremental passenger walking through an airport where Avolta operates is another potential customer, and the marginal cost of serving that customer is very low once the concession infrastructure is in place.

The "toll booth" analogy is instructive because it highlights both the opportunity and the risk. A toll booth generates fantastic returns when traffic is flowing. But when traffic stops, as it did in 2020, the fixed costs do not.

Concession contracts typically include minimum annual guaranteed payments to airport authorities, which means Avolta pays rent whether or not customers show up. This creates an asymmetric risk profile: strong operating leverage on the upside, painful cash burn on the downside.

M&A execution deserves special attention because it is genuinely a core competency at Avolta, not just a strategic talking point.

Over the past two decades, the company has integrated more than thirty acquisitions without losing strategic coherence. The playbook is consistent: acquire, integrate onto the global technology and procurement platform, extract synergies on a defined timeline, and reinvest.

The Nuance integration delivered its projected synergies ahead of schedule. The World Duty Free integration delivered EUR 100 million in annual savings. The Autogrill integration has driven consistent margin expansion every quarter since closing.

This track record matters because the travel retail industry remains fragmented, with significant consolidation opportunities in Asia, Latin America, and emerging markets. If Avolta can continue executing acquisitions at historical synergy rates, the growth runway extends well beyond what organic metrics alone would suggest.

The art of concession management is perhaps the least understood aspect of the business, and it is worth dwelling on because it is the fundamental skill that determines success or failure in this industry.

Winning a concession bid is not simply about offering the highest revenue share to the airport authority. It is about presenting a comprehensive proposal that balances financial terms with operational capabilities, brand partnerships, store design concepts, technology integration, digital strategy, and service quality.

Bid too aggressively on the revenue share, and you win the contract but destroy your margins over the ten-year life of the agreement. This is the "winner's curse" that has felled many a concession operator. Bid too conservatively, and you lose to a competitor willing to take less profit for the privilege of operating in a premium location.

Avolta's scale gives it a calibrated advantage: it has enough data from its 5,100-plus outlets to model expected revenue per square meter at virtually any airport in the world, allowing it to price bids with a precision that smaller operators, working from limited data sets and gut instinct, simply cannot match.

There is a myth in the market that Avolta's revenue growth is primarily acquisition-driven, a roll-up story that will eventually run out of targets. The reality is more nuanced.

Organic revenue growth has consistently met or exceeded the five to seven percent target range, driven by a combination of passenger traffic growth, increased spend-per-passenger from the hybrid store format and Club Avolta loyalty program, and new concession wins. The Autogrill merger did provide a step-change in revenue, but the organic engine has proven itself independently.

For investors seeking to monitor Avolta's ongoing performance, two key performance indicators stand above all others.

The first is organic revenue growth in constant exchange rates, which strips out the noise of acquisitions and currency movements to reveal the underlying health of the business. Avolta's Destination 2027 target range of five to seven percent is the benchmark against which every quarterly release should be measured. Sustained performance above the range suggests the hybrid format and loyalty program are working. Performance below suggests either macro headwinds or competitive pressure.

The second, and arguably more important, KPI is equity free cash flow.

This metric matters more than reported net income, and it is essential to understand why. Avolta's profit and loss statement is heavily distorted by approximately CHF 1.9 billion in annual depreciation and amortization, the vast majority of which relates to the capitalization of lease obligations under IFRS 16 accounting standards.

To explain this in plain terms: when Avolta signs a ten-year concession contract with an airport, IFRS 16 requires the company to record the entire future lease obligation as a liability on the balance sheet, and then amortize it as an expense over the contract term. Imagine you sign a ten-year lease on an apartment at CHF 1,000 per month. Under IFRS 16, you would record CHF 120,000 as a liability on day one, and then "depreciate" that liability as a non-cash expense each year. Your cash outflow is still CHF 1,000 per month, but your income statement shows a much larger expense.

This creates a massive non-cash charge that depresses reported net income, making the company look far less profitable than it actually is on a cash basis. Avolta reported net income of CHF 199 million in fiscal year 2025, but equity free cash flow was many times higher.

Equity free cash flow, which the company defines as operating cash flow less capital expenditures, lease payments, and interest costs, reveals the actual cash being generated for shareholders after all real obligations are met. It is the metric most directly tied to management's incentive compensation, and it is the number that matters.

IX. Epilogue: The Bull vs. Bear Case

The bear case against Avolta centers on three interconnected risks that any serious investor must weigh.

First, the Middle Eastern and Asian self-operation threat.

Dubai Duty Free demonstrated that airports can successfully internalize the retail and dining function, building a $2 billion-plus standalone business without a third-party operator. Qatar Duty Free and King Power in Thailand are additional examples.

These are not marginal airports. Dubai International and Hamad International in Doha are among the busiest international hubs in the world, and they have deliberately chosen to capture the retail economics for themselves rather than sharing them with a concession operator.

If this model spreads beyond its current concentration in the Middle East and Southeast Asia to major European or North American hubs, where Avolta's revenue is most concentrated, the addressable market could shrink meaningfully. The counterargument is that self-operation requires deep retail expertise, brand relationships, and operational scale that most airport authorities simply do not possess, and the Middle Eastern examples benefit from unique sovereign wealth dynamics that are not easily replicated elsewhere. But the risk is real and directionally concerning.

Second, the structural evolution of retail.

The "retail apocalypse" narrative that gutted American shopping malls through the 2010s has not yet reached airports in meaningful ways, partly because airports remain walled gardens insulated from e-commerce competition. But that insulation is not guaranteed to be permanent.

Digital pre-ordering platforms that allow travelers to browse, purchase, and have goods delivered to their gate or pickup locker are in early-stage deployment at several major airports. Airlines are experimenting with onboard e-commerce that could shift purchasing from the terminal to the aircraft. And the fundamental question of whether younger generations, who grew up buying everything online, will maintain the impulse-shopping behavior that drives airport retail remains open.

Avolta's digital investments and Club Avolta loyalty program are defensive measures designed to capture the digital traveler rather than lose them, but the threat horizon extends over a decade or more, and the outcome is genuinely uncertain.

Third, the balance sheet.

While Avolta has deleveraged impressively, from 2.6 times net debt to CORE EBITDA at the end of 2023 to 1.9 times by the third quarter of 2025, the absolute level of total liabilities remains substantial.

The total debt figure of approximately CHF 11.5 billion, including roughly CHF 8.5 billion of lease obligations capitalized under IFRS 16, means that in any scenario where travel volumes decline meaningfully, the fixed-cost burden could become painful. Interest expense consumed CHF 634 million in fiscal year 2025, representing more than half of operating income.

A future pandemic, a global recession, or a sustained structural shift away from business travel would test this balance sheet severely. The company survived 2020, but it took massive dilution, government support, and years of painful cost cutting to do so. Shareholders should not assume that the next crisis would be navigated as successfully.

The bull case is built on equally compelling logic.

The structural tailwind behind global travel is powerful and, many argue, represents one of the most durable secular trends in the global economy. The International Air Transport Association projects passenger numbers will reach 8.6 billion by 2040, nearly double the pre-COVID peak.

Emerging market middle classes are traveling internationally for the first time in the hundreds of millions. Low-cost carriers are opening routes to secondary and tertiary cities, creating new travel demand rather than just shifting it. Airport infrastructure investment globally exceeds $200 billion over the coming decade, with virtually every major hub planning terminal expansions that will add commercial space.

Every new terminal, every new route, every new passenger is a potential Avolta customer.

The food and beverage engine provides a margin and resilience profile that the old Dufry never had. F&B is less cyclical, less dependent on luxury spending, and increasingly valued by airport authorities who want to elevate the traveler experience beyond the traditional duty-free model.

The hybrid store format is generating measurably higher revenue per square meter and longer dwell times, and it is still in the early stages of global rollout. If the format works as well in Singapore and Sao Paulo as it has in London and New York, the organic growth story has a long runway ahead.

The Edizione partnership provides a capital structure advantage that is easy to overlook but may be the most important qualitative factor in the entire investment case.

The Benetton family, through Edizione, thinks in generational timescales. They are not going to pressure management for a short-term exit or a dividend they cannot afford. Alessandro Benetton's presence as Honorary Chairman signals a multi-decade commitment. This "forever capital" base gives Avolta the patience to invest in long-term initiatives without the quarter-to-quarter performance pressure that forces many public companies into short-termist decisions.

The valuation tells an interesting story. At roughly 5.8 times EV/EBITDA, Avolta trades at a discount to comparable global concession operators and far cheaper than comparable "toll booth" businesses in infrastructure or transportation.

The price-to-earnings ratio appears elevated at approximately 34 times, but this is almost entirely because reported earnings are depressed by massive non-cash lease amortization that has no bearing on the company's actual cash generation capacity. The equity free cash flow yield, the metric that best captures economic earnings power, tells a very different story.

There is also a regulatory and accounting nuance that investors should flag. The IFRS 16 treatment of lease obligations creates a balance sheet that looks far more leveraged than the economic reality. The CHF 8.5 billion of capitalized lease liabilities represents future rent payments over the remaining terms of thousands of concession contracts. These are real obligations, but they are also matched by the revenue-generating capacity of those same contracts. Comparing Avolta's headline debt-to-equity ratio to that of an asset-light technology company, for instance, would be deeply misleading.

Avolta is, at its core, the ultimate "pick and shovel" play for the 21st-century nomad.

It does not need to predict which airline will win, which destination will trend on social media, or which luxury brand will capture the next generation of travelers. It simply needs people to keep moving through airports. And if the last century of human behavior is any guide, they will.

The question for investors is not whether global travel will grow, but whether Avolta can maintain and extend its position as the dominant commercial infrastructure provider within that growing ecosystem.

The integrated model, the Benetton partnership, the management alignment, and the early results of Destination 2027 suggest the answer may be yes. But the Middle Eastern self-operation trend, the digital disruption risk, and the balance sheet leverage suggest the answer is not without uncertainty.

Top 10 Resources for Further Reading

- Avolta: Destination 2027 Strategy Deck (Corporate Website, avoltaworld.com)

- The History of Autogrill and the Benetton Empire (Edizione S.p.A. corporate publications)

- The Economics of Airport Concessions (ACI World Reports, Airports Council International)

- Xavier Rossinyol on the "Travel Experience" Pivot (Skift Interview)

- Dufry's 2015 World Duty Free Acquisition: A Case Study in Synergies (Moodie Davitt Report)

- The Rise of the "Aerotropolis" by John Kasarda

- Hudson Group: The King of the US Newsstand (Hudson corporate publications)

- Retail in Motion: The Future of Digital Travel Retail (Industry white papers)

- Avolta Annual Report 2024: The First Year of the Merger (avoltaworld.com investor relations)

- 7 Powers: The Foundations of Business Strategy by Hamilton Helmer (Applied to Avolta)

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube