Aviva: The 300-Year-Old Startup Strategy

I. Introduction: The Insurance Giant that Found Its Soul by Shrinking

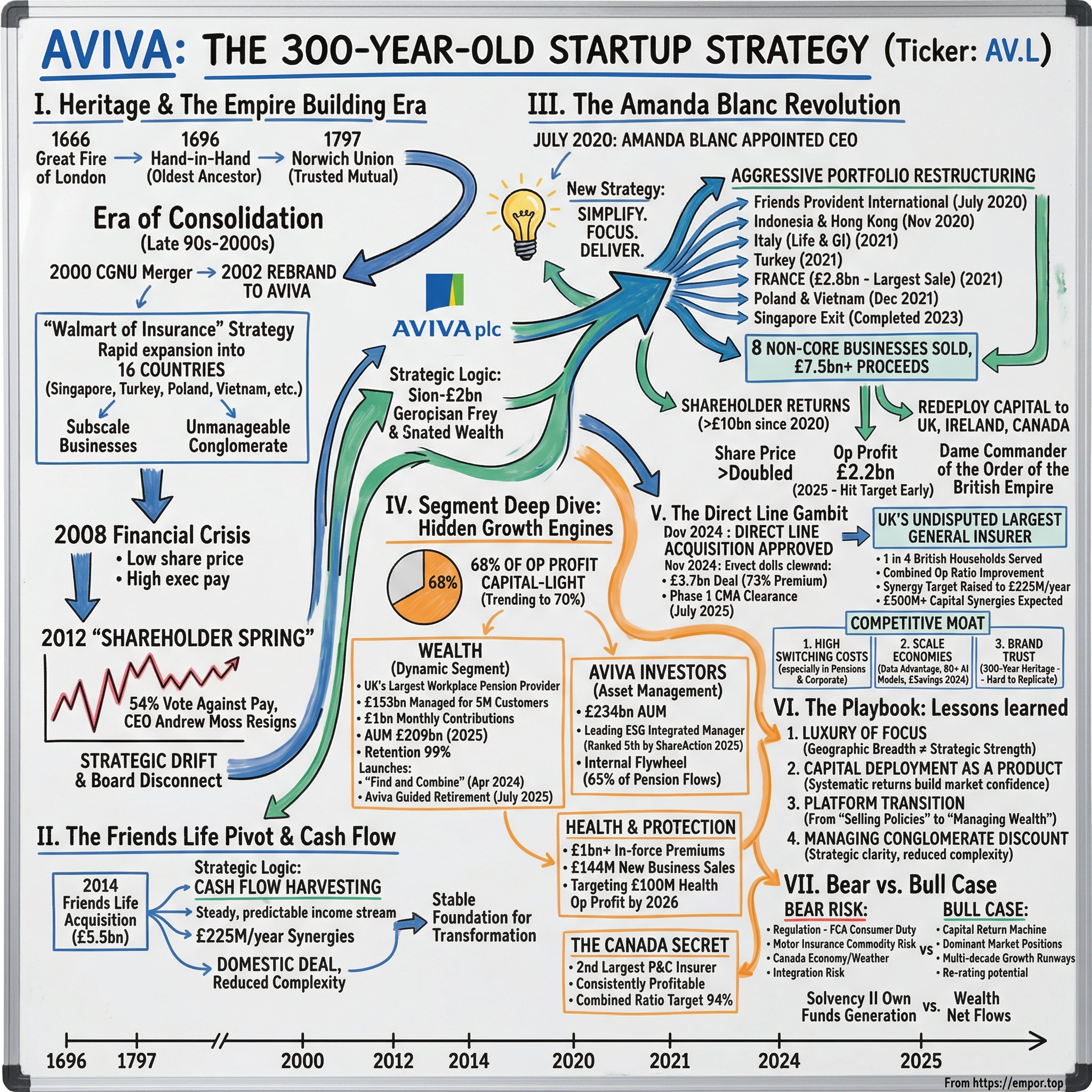

Picture this: it is the summer of 2020, and the world is locked down. Offices are empty. Markets are rattled. And into the corner office at St Helen's in the City of London walks Amanda Blanc, the new chief executive of Aviva plc, one of the oldest and most sprawling financial institutions on the planet. She looks at the empire she has inherited: operations in sixteen countries, a share price that has gone essentially nowhere for a decade, and a board weary from years of strategic drift. Within her first hundred days, she will announce a plan that sounds almost reckless for a company with three centuries of history. She will shrink Aviva, dramatically, by selling off more than half its international footprint. The conventional wisdom in insurance has always been that scale wins. More geographies, more products, more customers. Aviva had spent the better part of two decades chasing that logic, acquiring businesses from Singapore to Turkey, from Poland to Vietnam. By 2020, the company was everywhere and a leader almost nowhere. The stock traded at a persistent discount to peers like Legal & General and Prudential. Analysts had taken to describing it as an "unmanageable conglomerate." Blanc's thesis was the opposite of empire-building. She believed that Aviva's problem was not that it was too small, but that it was too unfocused. The company had extraordinary assets in the United Kingdom, Ireland, and Canada, markets where it held genuine scale advantages, deep customer relationships, and brand trust built over generations. Everything else was a distraction.

The results, five years later, speak for themselves. Aviva's share price has more than doubled since Blanc took over. The company hit its target of two billion pounds in operating profit a full year ahead of schedule. It has returned over ten billion pounds to shareholders through dividends, buybacks, and special distributions. And in the summer of 2025, it completed the acquisition of Direct Line Group, making it the undisputed largest general insurer in the United Kingdom, serving roughly one in four British households.

This is not a story about a startup disrupting an industry. It is something arguably rarer and more instructive: the story of a three-hundred-year-old institution that rediscovered what it was actually good at and had the discipline to shed everything else. It is the ultimate case study in focus versus scale, and why being the category king in a few markets can be far more valuable than being a middling player in many. To understand how Aviva got here, though, we need to go back to where it all began, in the charred aftermath of seventeenth-century London.

II. Heritage and the Empire Building Era

On September 2, 1666, a fire broke out in a bakery on Pudding Lane in the City of London. Over the next four days, the Great Fire consumed thirteen thousand houses, eighty-seven churches, and most of the civic buildings in what was then the commercial heart of the English-speaking world. The devastation was total, and the response was instructive. Within three decades, Londoners had invented an entirely new industry: fire insurance. In 1696, a group of merchants established the "Contributors for Insuring Houses, Chambers or Rooms from Loss by Fire, by Amicable Contribution," later known simply as the Hand-in-Hand Fire and Life Insurance Society. It was one of the first insurance companies in the world, and it is the oldest ancestor of what we now call Aviva.

A century later, in the cathedral city of Norwich, a thirty-six-year-old merchant and banker named Thomas Bignold saw an opportunity. Fire insurance existed, but it was concentrated in London and priced for the wealthy. Bignold believed insurance should be accessible to ordinary people in the provinces. In 1797, he founded the Norwich Union Society for the Insurance of Houses, Stock and Merchandise from Fire, structured as a mutual society owned by its policyholders. A decade later, he established a companion life insurance mutual. Norwich Union would grow to become one of the most recognised and trusted names in British finance, a household brand synonymous with prudent protection. For nearly two centuries, these institutions and dozens of others like them grew organically across the British Isles, serving local communities, underwriting risk conservatively, and building the kind of deep customer trust that only time can create.

Then came the era of consolidation. In the late 1990s, the global insurance industry was gripped by merger fever. The logic seemed irresistible: combine balance sheets for capital efficiency, merge operations to cut costs, and create global platforms that could compete with American and Continental European giants. In 1998, two venerable British insurers, Commercial Union and General Accident, merged to form CGU. Two years later, CGU and Norwich Union consummated a mega-merger, creating CGNU plc, the largest insurance group in the United Kingdom. In 2002, shareholders voted to rebrand the company with an invented name: Aviva, a palindrome derived from the Latin "viva," meaning alive. The idea was to create a single global brand that would work across every market. It sounded elegant in a boardroom presentation. In practice, it was the beginning of a long strategic detour.

Throughout the 2000s, Aviva's leadership pursued what might be called the "Walmart of insurance" strategy. If a market was growing, Aviva wanted to be there. The company expanded into Poland, Turkey, Singapore, Vietnam, Indonesia, Hong Kong, France, Italy, and beyond. At its peak, Aviva operated in more than a dozen countries across multiple product lines. The problem was not that any single market was bad. It was that managing a sprawling portfolio of subscale businesses across vastly different regulatory environments, customer cultures, and competitive dynamics is extraordinarily difficult. Capital was being allocated to markets where Aviva was the fifth or sixth largest player, competing against deeply entrenched local champions who understood their customers far better.

The 2008 financial crisis exposed the fragility of this approach. Insurance companies live and die by their balance sheets, and Aviva's was stretched across too many geographies with too many different risk profiles. The share price, which had traded above 750 pence before the crisis, collapsed. What followed was not a swift recovery but a grinding slog. By 2012, Aviva's stock was hovering around 300 pence, less than half its pre-crisis level, while executive compensation had increased by roughly ninety percent over the same period. The contrast between shareholder pain and boardroom comfort became untenable.

The breaking point came at the 2012 Annual General Meeting, in what the British press dubbed the "Shareholder Spring." Fifty-four percent of shareholders voted against the company's remuneration report, a stinging rebuke that was almost unprecedented for a FTSE 100 company. CEO Andrew Moss had already pre-emptively declined a salary increase in a bid to head off the revolt, but it was not enough. Within days, Moss resigned, becoming the third high-profile British CEO to fall that spring, following similar revolts at Trinity Mirror and AstraZeneca. The shareholder spring was driven partly by broader frustration with executive pay in the wake of the financial crisis, but at Aviva, it carried a more pointed message. Investors were not just angry about pay; they were angry about years of strategic drift, empire-building that enriched managers while destroying shareholder value, and a board that seemed disconnected from the reality of Aviva's competitive position. The company needed more than a new CEO. It needed a fundamentally different strategic direction.

III. The Friends Life Pivot and M&A Benchmarking

By 2014, Aviva had cycled through leadership changes and incremental restructuring, but the fundamental question remained unresolved: what kind of company was Aviva trying to be? The answer began to crystallize with what initially looked like another big acquisition, but was actually something quite different in character. In December 2014, Aviva announced a recommended all-share acquisition of Friends Life Group for approximately five and a half billion pounds. Friends Life shareholders would receive 0.74 Aviva shares for each of their shares, implying a premium of about fifteen percent to the undisturbed share price.

To understand why this deal mattered, you need to understand what Friends Life actually was. It was not a fast-growing insurance startup or a glamorous international expansion. Friends Life was, at its core, an enormous "back book," a portfolio of millions of existing life insurance and pension policies that had been accumulated through years of consolidation. These policies generated steady, predictable cash flows as policyholders paid premiums and the company earned investment returns on the reserves. The policies were "closed" to new business in many cases, meaning no new customers were being added, but the existing book would continue generating cash for decades as policies matured. This is the insurance equivalent of owning a toll bridge. The traffic is predictable, maintenance costs are manageable, and the cash just keeps flowing.

The strategic logic of Friends Life was therefore fundamentally different from Aviva's prior international acquisitions. This was not about planting a flag in a new geography and hoping to grow. This was about cash flow harvesting: acquiring a massive, predictable income stream and using Aviva's existing operational infrastructure to manage it at lower cost. The projected synergies were two hundred and twenty-five million pounds per year by the end of 2017, to be achieved principally through combining overlapping back-office operations, removing duplicate management layers, and rationalizing technology platforms. The present value of those synergies was estimated at roughly one point eight billion pounds, meaning that if Aviva could execute on integration, a substantial portion of the purchase price would effectively pay for itself.

The integration costs were projected at three hundred and fifty million pounds, spread over three years. At the time, skeptics questioned whether Aviva could deliver. The company's track record on integration was mixed at best, and the history of insurance mergers is littered with examples where promised synergies evaporated in execution. But Aviva had one thing working in its favour: this was a domestic deal. Both companies operated in the same market, under the same regulator, with similar product sets and overlapping distribution networks. There were none of the cross-border complexities, currency mismatches, or cultural translation challenges that had plagued Aviva's international ventures.

When the deal closed in April 2015, with overwhelming shareholder approval of over ninety-nine percent from Aviva investors and ninety-four percent from Friends Life holders, it represented a philosophical turning point even if it was not recognized as such at the time. For the first time in years, Aviva was making an acquisition designed to strengthen its position in its home market rather than expand its geographic reach. The synergies ultimately came through largely on schedule. More importantly, the Friends Life back book provided a stable foundation of cash generation that would prove crucial in funding the transformation that was still to come.

The verdict on Friends Life, viewed from the perspective of 2026, is that it was the right deal at the right time. It was a domestic consolidation play in a market Aviva already understood deeply, executed with reasonable discipline and achievable synergy targets. It provided the "dry powder," the steady, reliable cash flows, that would give Aviva's future leadership the financial flexibility to make bolder strategic choices. In a sense, Friends Life was the bridge between the old Aviva of unfocused international expansion and the new Aviva that Amanda Blanc would build. But that bridge would take another five years to cross.

IV. The Amanda Blanc Revolution

Amanda Blanc's path to the top of Aviva was anything but conventional. She studied modern history at the University of Liverpool, not exactly the typical breeding ground for insurance executives. She earned her MBA at the University of Leeds and qualified as a Chartered Insurer, but her early career was defined more by restless ambition than by steady corporate ascent. After a graduate role at Commercial Union, which would later become part of Aviva itself, she spent a year as a management consultant at EY before joining AXA in 1999. Over the next two decades, she moved through a series of increasingly senior roles across the British insurance landscape, each move revealing something about her character.

At Towergate, she ran the retail broking division and rose to group deputy CEO. At AXA UK, she became group CEO overseeing commercial lines, health insurance, and the Irish operation. Then came Zurich Insurance, where she was appointed CEO for Europe, the Middle East, and Africa in 2018, one of the most senior positions in global insurance. She left Zurich after roughly a year, reportedly due to clashes with group CEO Mario Greco over strategic direction. It was a revealing episode: Blanc was not someone who would quietly execute a strategy she disagreed with. She would rather walk away than compromise her convictions.

When Aviva's board came calling in early 2020, Blanc was serving on several non-executive boards, including BP, and was widely regarded as one of the most capable executives in British insurance. She joined as a non-executive director in January 2020 and was elevated to Group CEO in July, just as the first wave of the pandemic was reshaping every assumption about how businesses would operate. Her first major public address set the tone with a clarity that was almost startling for a company accustomed to corporate ambiguity. The strategy had three words: Simplify. Focus. Deliver.

What followed was one of the most aggressive portfolio restructurings in recent British corporate history. Within eighteen months, Blanc orchestrated the sale of eight non-core international businesses. Friends Provident International went first, in July 2020, just weeks after she took over. The Indonesia and Hong Kong operations followed in November. Italy was sold in multiple tranches, with the general insurance arm going to Allianz for two hundred and eighty-four million pounds and the life business to UBI Banca for approximately four hundred million euros. Turkey went for one hundred and twenty-two million pounds. The jewel of the disposal programme was France, sold to Aema Groupe for three point two billion euros, or roughly two point eight billion pounds, in a deal that represented Aviva's single largest divestiture. Poland and Vietnam were sold in December 2021. The Singapore operations, including the stake in the Singlife joint venture, were unwound over a longer period, with the final exit completed in 2023.

The total proceeds from these eight disposals exceeded seven and a half billion pounds, dramatically surpassing Blanc's original target of five billion. Each sale was a statement: Aviva was not going to be a subscale player in markets where it could not win. The France exit was particularly telling. Aviva France was a profitable business with established distribution and a loyal customer base. Selling it was not about cutting losses; it was about redirecting capital and management attention to markets where Aviva had genuine competitive advantages.

The "un-acquired" strategy, as it might be called, is worth dwelling on because it runs counter to the instincts of most corporate leaders. CEOs are rewarded for growth, for acquisitions, for expanding empires. Shrinking a company, even when it is clearly the right strategic move, requires a different kind of courage. Blanc faced skepticism from analysts who worried she was giving away optionality and from employees in divested markets who felt abandoned. But the financial logic was overwhelming. The international businesses Aviva sold were, in aggregate, subscale operations that consumed management bandwidth, regulatory capital, and corporate overhead disproportionate to their strategic value. By exiting them, Blanc freed up billions in capital that could be returned to shareholders or redeployed into the UK, Ireland, and Canada, the three markets where Aviva held genuine scale.

The incentive structure reinforced this discipline. Blanc's remuneration package was heavily tilted toward Solvency II capital generation and total shareholder return, the metrics that reward focus and cash discipline rather than top-line growth. Her total compensation for 2024 was approximately seven point two million pounds, comprising a base salary, an annual bonus of two point two million, and long-term share awards of three point seven million. More telling was her personal shareholding: roughly eleven million pounds worth of Aviva stock held in her own name. When a CEO has that much of her own wealth tied to the share price, the alignment with long-term shareholders is not theoretical. She was appointed Dame Commander of the Order of the British Empire in recognition of her contributions to financial services and gender equality in British business, a public affirmation of a career defined by both commercial success and institutional reform.

By 2025, the results of the Blanc revolution were undeniable. Aviva's share price had risen more than one hundred and twenty percent since her appointment. Operating profit had grown from roughly one and a half billion pounds in 2023 to two point two billion in 2025, hitting the company's own target of two billion a full year early. Operating earnings per share reached fifty-six pence, up seventeen percent. The Solvency II ratio, a key measure of an insurer's financial resilience, stood at a robust one hundred and eighty percent. Dividends had grown at a compound rate of over eleven percent per year. Total capital returned to shareholders since 2020 exceeded ten billion pounds through a combination of ordinary dividends, special dividends funded by disposal proceeds, and share buybacks. The transformation was not just about cost-cutting or financial engineering. It was about fundamentally redefining what Aviva is: a focused, cash-generative financial services platform anchored in three markets where it can be the best, not just present.

V. Segment Deep Dive: The Hidden Growth Engines

The casual observer might look at Aviva and see a large, mature insurance company. Boring. Predictable. Perhaps worth owning for the dividend, but hardly exciting. This view misses what is actually happening beneath the surface. Aviva in 2026 is not just an insurance company. It is rapidly evolving into a diversified financial services platform with several distinct businesses at very different stages of maturity and growth.

Start with what Blanc calls the "capital-light" businesses, the operations that generate profit primarily from fees and management charges rather than from underwriting risk on the company's balance sheet. As of the 2025 results, sixty-eight percent of Aviva's group operating profit came from capital-light sources, up meaningfully from prior years and tracking toward a stated ambition of seventy percent. This distinction matters enormously for valuation. Capital-heavy insurance businesses, where profits depend on predicting losses accurately and investing reserves wisely, tend to trade at lower multiples because earnings are inherently volatile. Capital-light businesses, particularly those with recurring revenue streams and high customer retention, typically command much higher valuations. Aviva's journey, at its core, is a migration up the valuation spectrum.

The most dynamic segment is the Wealth division, which encompasses workplace pensions, advisor platforms, and individual savings products. Aviva is now the UK's largest workplace pension provider, managing roughly one hundred and fifty-three billion pounds across approximately five million customers. The scale of these numbers is worth pausing on. Five million workers in the United Kingdom have their retirement savings entrusted to Aviva. Every month, approximately one billion pounds in member contributions flows into the platform. Wealth assets under management grew to two hundred and nine billion pounds in 2025, up six percent from one hundred and ninety-eight billion the prior year, with net flows of five point eight billion in the first half alone.

What makes this business so attractive is the structural tailwind. The UK workplace pensions market has grown fourfold over the past decade, driven primarily by auto-enrolment legislation that requires employers to provide pension schemes for their workers. This market is expected to reach four trillion pounds over the next two decades. And the economics are beautifully sticky: once a company selects Aviva as its workplace pension provider, the switching costs are enormous. Migration involves moving millions of individual accounts, updating payroll systems, communicating with thousands of employees, and navigating regulatory requirements. The result is retention rates of approximately ninety-nine percent. Aviva won five hundred and forty-four new pension schemes in 2025, the highest on record, with a win rate of roughly seventy-five percent and cumulative scheme wins over the past three years exceeding fifteen hundred.

In April 2024, Aviva launched a "Find and Combine" service, the first of its kind in the UK, which allows individuals to trace and consolidate their scattered pension pots into a single Aviva account. It is a clever move that simultaneously improves customer experience and increases assets on the platform. In July 2025, the company launched "Aviva Guided Retirement," a flexible drawdown product designed to capture members as they transition from accumulation to decumulation. The wealth division is targeting two hundred and eighty million pounds in operating profit by 2027, and the trajectory suggests that target is achievable.

Then there is Aviva Investors, the group's asset management arm, which manages roughly two hundred and thirty-four billion pounds across real estate, infrastructure, private debt, multi-asset, equities, and fixed income. Aviva Investors has positioned itself as one of the UK's leading ESG-integrated asset managers, with over forty dedicated sustainable investing professionals embedded alongside fund managers and analysts. The firm was ranked fifth out of seventy-six of the world's largest asset managers in ShareAction's "Point of No Returns 2025" report and has committed to decarbonising clients' equity assets to net zero emissions by 2040. Importantly, approximately sixty-five percent of workplace pension net flows were directed into Aviva Investors funds, creating a powerful internal flywheel where the wealth platform feeds the asset manager, which in turn benefits from scale.

Health and Protection has emerged as another growth vector, propelled by structural shifts in how the British public thinks about healthcare. The UK's National Health Service, while beloved, has been under enormous strain, with waiting lists reaching record levels. This has driven a surge in demand for private medical insurance. The overall UK private health insurance market grew nearly fourteen percent in 2024 to reach eight point six billion pounds, with private medical cover now extending to eight point four million people, or roughly twelve percent of the population, the highest penetration since 2008. Aviva has over one point one million health insurance customers and saw health new business sales of one hundred and forty-four million pounds in 2025, up four percent year-on-year. Health operating profit reached seventy-two million pounds, growing nine percent, with in-force premiums surpassing one billion pounds for the first time, up twelve percent. The company is targeting one hundred million pounds in health operating profit by 2026, and the structural tailwinds suggest this is more of a floor than a ceiling.

Finally, there is what might be called "The Canada Secret." Aviva is the second-largest property and casualty insurer in Canada, behind only Intact Financial Corporation, with a market share in the range of eight to nine percent. The Canadian P&C market is attractive for several reasons: it is concentrated, with the top ten groups holding roughly sixty-three percent of the market; it is well-regulated with rational pricing; and it has been consolidating steadily, which favours incumbents with scale. Aviva Canada generated general insurance premiums of approximately four and a half billion pounds in 2025. The combined operating ratio, the key measure of underwriting profitability in general insurance where anything below one hundred percent means the company is making money on its core insurance operations, has been trending toward a target of ninety-four percent. Canada may lack the growth glamour of Aviva's wealth platform, but it is a consistent, profitable business in a market where Aviva has genuine competitive scale.

The combined picture is more compelling than any individual segment suggests. Aviva is not just selling insurance policies. It is managing wealth, running pensions, investing capital, providing healthcare, and underwriting risk across three markets where it holds leadership positions. The mix of high-retention capital-light businesses and profitable underwriting operations creates a financial profile that is increasingly difficult for competitors to replicate.

VI. The Direct Line Gambit and Competitive Moat

If the disposal programme was about subtraction, the acquisition of Direct Line Group was about decisive addition. In November 2024, Aviva made a formal approach for Direct Line, one of the UK's best-known motor and home insurance brands, offering two hundred and fifty pence per share. Direct Line's board rejected it. Aviva came back with two hundred and sixty-one pence. Rejected again. Finally, in December 2024, Aviva tabled a definitive offer of two hundred and seventy-five pence per share, a seventy-three percent premium to Direct Line's undisturbed share price and a forty-nine percent premium to the six-month average. The structure was partly cash, partly shares: each Direct Line shareholder received 0.2867 new Aviva shares plus one hundred and twenty-nine point seven pence in cash, plus up to five pence in pre-completion dividends. The total deal value was approximately three point seven billion pounds.

Direct Line had been struggling. Once the darling of the UK motor insurance market, the company had suffered from underpricing its policies, rising claims costs, and a series of strategic missteps that had eroded profitability and investor confidence. Its board had already embarked on a cost reduction programme, but the market was skeptical that standalone turnaround efforts would be sufficient. Aviva's offer represented both a premium for shareholders and a strategic lifeline.

The Competition and Markets Authority cleared the deal unconditionally in Phase 1 in July 2025, finding no substantial lessening of competition despite the combined group's dominant position. The Financial Conduct Authority and the Prudential Regulation Authority also gave their approvals. The acquisition completed on July 1, 2025, creating the UK's largest motor and home insurer with over twenty percent of the motor insurance market, surpassing Admiral to claim the top position. The combined group now serves approximately twenty million UK customers through a portfolio of brands including Aviva, Direct Line, Churchill, Darwin, Green Flag, and Privilege.

The synergy case evolved upward during the integration process. Initial targets of one hundred and twenty-five million pounds in annual pre-tax cost synergies were raised to two hundred and twenty-five million, incremental to Direct Line's own completed cost reduction programme. Capital synergies of over five hundred million pounds are expected upon regulatory approval, anticipated around the end of 2026, which would improve Aviva's solvency ratio by more than ten percentage points. In its first six months as part of Aviva, Direct Line contributed one hundred and seventy-four million pounds to group operating profit, a meaningful addition that helped push the combined group past the two billion pound profit target.

Now, to understand why this position is defensible, it is worth examining Aviva through the lens of competitive frameworks. Consider switching costs, arguably the most powerful of Hamilton Helmer's seven strategic powers in the context of financial services. When a corporation selects Aviva as its workplace pension provider, that decision becomes deeply embedded in the company's HR infrastructure, payroll systems, and employee communications. Switching to a competitor requires migrating millions of individual accounts, retraining HR staff, and managing regulatory notifications. The practical result is a retention rate of ninety-nine percent. In general insurance, switching costs are lower for individual policyholders, but Aviva's breadth across motor, home, health, and commercial lines creates cross-selling opportunities that increase customer lifetime value and reduce churn.

Scale economies provide the second layer of competitive advantage. As the UK's largest general insurer, Aviva underwrites more policies and processes more claims than any competitor. This generates a data advantage in pricing and underwriting that smaller players simply cannot match. The company has deployed over eighty artificial intelligence models across its operations, reducing liability assessment time for complex claims by twenty-three days, improving claim routing accuracy by thirty percent, and cutting customer complaints by sixty-five percent. These AI-driven efficiencies saved an estimated sixty million pounds in 2024 alone. Scale also matters in distribution: Aviva's direct-to-consumer digital platforms, its broker relationships, and its workplace pension partnerships create multiple channels for reaching customers that would require billions to replicate.

Brand trust, the third element, is particularly significant in insurance, a product category where the customer is essentially buying a promise. That promise, that the company will be there when disaster strikes, is only as credible as the institution behind it. Aviva's three-hundred-year heritage provides a reservoir of trust that no neo-insurer or fintech startup can manufacture. This is not to say that brand is an impenetrable moat; price comparison websites have commoditized much of the retail insurance market, and Aviva must compete on price and service like everyone else. But in corporate markets, workplace pensions, and complex commercial insurance, the Aviva brand carries a weight that takes generations to build.

The threat of new entrants deserves honest assessment. Insurtech companies and digital-first challengers have attracted significant venture capital investment over the past decade, and some, like Lemonade and Root in the United States, have achieved meaningful scale. In the UK, however, the regulatory capital requirements for operating as an insurer create a formidable barrier. The Solvency II framework requires insurers to hold substantial capital reserves against their underwriting liabilities, a requirement that is extremely difficult for thinly capitalized startups to meet. Moreover, Aviva's balance sheet moat, the sheer scale of its reserves and capital base, allows it to absorb catastrophe losses and market volatility in ways that would bankrupt a smaller competitor. The practical result is that while insurtechs may nibble at the edges, particularly in direct-to-consumer distribution, the core of Aviva's business remains well-protected.

VII. The Playbook: Business and Investing Lessons

The Aviva story, particularly the transformation under Amanda Blanc, offers several lessons that extend well beyond the insurance industry.

The first and most fundamental is what might be called the luxury of focus. When Blanc took over, Aviva operated in sixteen countries. By the time she was done selling, it operated in three core markets. The instinct to equate geographic breadth with strategic strength is powerful and deeply ingrained in corporate culture. Senior executives build their reputations and their compensation packages by growing empires. Boards approve international expansions because they look bold and forward-thinking in investor presentations. But the Aviva case demonstrates that reducing your footprint by fifty percent can lead to a doubling or more of strategic intensity. When management no longer has to worry about Turkish regulatory changes, Polish distribution challenges, and Vietnamese market dynamics, every ounce of executive attention can be directed at winning in markets that actually matter. The seven and a half billion pounds in disposal proceeds was important, but the real value was in the hundreds of thousands of management hours that were no longer consumed by subscale international operations. Focus is not a retreat. It is a reallocation of the scarcest resource in any organization: leadership attention.

The second lesson concerns capital deployment as a product. In the era of passive investing and shareholder activism, how a company allocates its capital is not just a financial decision; it is a signal, a form of communication with the market. Aviva's capital return programme, more than ten billion pounds since 2020 through dividends, buybacks, and special distributions, was not simply about being generous to shareholders. It was about systematically dismantling the "uncertainty discount" that had plagued the stock for two decades. When a company has a history of value-destructive acquisitions and strategic drift, investors demand a discount for the risk that management will do something foolish with excess capital. By returning the disposal proceeds to shareholders rather than reinvesting them in the next international adventure, Blanc was sending an unmistakable message: we will be disciplined stewards of your capital. The resumed share buyback of three hundred and fifty million pounds in 2026, larger than the pre-Direct Line programme, reinforced this commitment.

The third lesson is about the platform transition. Aviva is in the middle of a fundamental shift from being a company that "sells policies" to one that "manages wealth." This distinction is crucial for understanding the company's future trajectory. A traditional insurer earns money by underwriting risk: collecting premiums, investing the float, and hoping that claims come in below expectations. It is a volatile, capital-intensive business. A wealth management platform, by contrast, earns fees on assets under management, a revenue stream that is recurring, predictable, and grows automatically as markets rise and new contributions flow in. By building the UK's largest workplace pension platform and directing flows into its own asset management arm, Aviva is creating a capital-light flywheel that should, over time, command a higher valuation multiple than a pure-play insurer. The fact that sixty-eight percent of profits already come from capital-light sources, trending toward seventy percent, suggests this transition is well advanced.

The fourth lesson is about managing a conglomerate discount. For most of the 2010s, Aviva traded at a significant discount to its sum-of-the-parts valuation. Analysts could look at the individual businesses and calculate that they were worth considerably more separately than the market was assigning to the whole. This discount reflected several factors: complexity that made the company hard to analyze, a history of poor capital allocation, and the perception that management was not fully in control of its diverse empire. Blanc has systematically attacked each of these factors. The disposals reduced complexity. The capital returns demonstrated discipline. The simplified structure made the company easier for analysts and investors to understand and value. The Direct Line acquisition, while adding a new business, was additive to this clarity because it strengthened Aviva's position in its core market rather than adding a new dimension of complexity. The lesson is that conglomerate discounts are not immutable facts of nature; they are management problems that can be solved with strategic clarity and execution discipline.

VIII. The Bear vs. Bull Case

Every investment thesis has two sides, and Aviva's is no exception. The bear case and bull case reveal different aspects of the company's positioning and future prospects, and a rigorous analysis requires engaging honestly with both.

The bear case begins with regulation. The UK's Financial Conduct Authority introduced its Consumer Duty framework in 2023, representing the most significant shift in insurance regulation in a generation. The Duty requires firms to demonstrate that their products deliver "good outcomes" for customers, raising the bar on pricing transparency, claims handling, and value for money. For a dominant insurer like Aviva, this creates both compliance costs and potential constraints on pricing. If the FCA determines that certain products or pricing practices are not delivering adequate value, Aviva could face enforced changes that compress margins. The Consumer Duty is still in its early implementation phase, meaning the full impact on profitability remains uncertain.

The commodity risk in motor insurance is another concern. Despite Aviva's scale and the Direct Line acquisition, motor insurance remains a fundamentally price-sensitive market in the UK. Price comparison websites like Compare the Market, GoCompare, and Confused.com have made it trivially easy for consumers to switch insurers at every renewal, driving down loyalty and compressing margins. Aviva can partially offset this through better data and AI-driven underwriting, but the structural pressure from price transparency is unlikely to abate. The UK general insurance market is also expected to see moderating premium growth in 2025 and 2026 after several years of sharp increases, as competition intensifies and claims cost pressures ease. This could create headwinds for Aviva's top line.

Canada, while a strong market, is not without risks. The Canadian economy is exposed to housing market dynamics, and a significant downturn in property values could affect both premium volumes and claims patterns in property insurance. Weather-related catastrophe events, which hit Aviva Canada's 2024 results and pushed the combined operating ratio to ninety-eight point five percent compared to ninety-five percent the prior year, are an ever-present wildcard in an era of climate change. Integration risk from Direct Line also warrants attention. While the early signs are positive, fully integrating a three point seven billion pound acquisition while delivering synergies and maintaining service quality is a multi-year execution challenge. History is littered with insurance mergers that looked compelling on paper but stumbled in practice.

The bull case is anchored in Aviva's position as what might be called a "capital return machine." The dividend yield of over six percent at current prices, supported by eleven percent compound dividend growth and a resumed buyback programme, makes Aviva one of the most attractive income investments in the FTSE 100. The dividend is well covered by operating cash flows, and the Solvency II ratio of one hundred and eighty percent provides a substantial buffer above regulatory minimums. The company's new medium-term targets, announced at its November 2025 investor event, include operating earnings per share growth of eleven percent through 2028, a return on equity exceeding twenty percent by 2028, and cumulative cash remittances of over seven billion pounds from 2026 to 2028. If achieved, these targets imply significant further value creation.

The dominant market position in UK general insurance, now cemented by the Direct Line acquisition, provides pricing power and data advantages that smaller competitors cannot easily replicate. In workplace pensions, the combination of auto-enrolment tailwinds, extreme customer stickiness, and a market expected to quadruple in size over the coming decades creates a multi-decade growth runway. The health and protection business is riding a structural shift in UK healthcare that shows no signs of reversing. And the migration toward capital-light earnings should, over time, justify a re-rating from a traditional insurer multiple to something closer to a wealth management or platform multiple.

When assessing Aviva through the lens of Porter's five forces, the picture is nuanced but broadly favourable. The bargaining power of buyers is high in retail insurance, moderated by switching costs in corporate pensions and commercial insurance. Supplier power is limited, as Aviva's scale gives it leverage in reinsurance markets and technology procurement. The threat of substitutes exists primarily from self-insurance for large corporates and government schemes, but these are niche threats. Rivalry among existing competitors is intense in retail lines but more rational in commercial and corporate markets. And barriers to entry, driven by regulatory capital requirements and the need for actuarial expertise and claims infrastructure, remain formidable.

For investors seeking to track Aviva's ongoing performance, two metrics stand out as the most important indicators. The first is Solvency II Own Funds Generation, the amount of excess capital the business produces each year above regulatory requirements. This is the engine that powers dividends, buybacks, and strategic investment. Aviva hit its target of one point eight billion pounds in 2025, a year early, and the trajectory of this metric will signal whether the company can sustain its capital return commitments. The second is Wealth net flows as a percentage of opening assets under management, which measures the organic growth rate of the platform business. In the first half of 2025, this ran at six percent of opening AUM, a healthy rate that suggests the platform is gaining share. If this metric accelerates, it validates the thesis that Aviva is successfully transitioning from insurer to wealth platform. If it decelerates, it would raise questions about competitive positioning in an increasingly crowded market.

IX. Conclusion

Aviva in 2026 looks almost nothing like the Aviva of 2010. The sprawling, unfocused conglomerate that operated in sixteen countries, suffered a humiliating shareholder revolt, and traded at a persistent discount to its intrinsic value has been replaced by a focused, disciplined financial services platform that dominates its chosen markets. The transformation required an unusual combination of strategic clarity, execution discipline, and the willingness to get smaller in order to get better.

The company's heritage, stretching back to the aftermath of the Great Fire of London, provides a foundation of brand trust and institutional knowledge that cannot be replicated. But heritage alone is not enough; plenty of venerable institutions have been undone by strategic complacency. What distinguishes Aviva's trajectory is the marriage of that heritage with modern strategic thinking about capital allocation, platform economics, and competitive positioning. The Friends Life acquisition provided the cash flow foundation. The disposal programme freed up capital and management attention. The Direct Line deal cemented market leadership. And the quiet build-out of the wealth platform, the health business, and the AI-driven operational improvements are positioning Aviva for a future that looks more like a modern financial services platform than the stodgy insurance company of the past.

Amanda Blanc may ultimately be remembered as the CEO who saved a British icon by having the courage to make it smaller. In an era when corporate leaders are rewarded for growth at almost any cost, she chose focus, discipline, and shareholder alignment. The share price, the dividends, and the operating results suggest that the market has endorsed that choice. Whether Aviva can sustain this trajectory through the inevitable challenges of integration, regulation, and market cycles will determine whether this is a completed turnaround or a story that is still being written. But the chapter authored so far is one of the most compelling strategic transformations in recent British corporate history.

X. Further Reading

-

The History of the Norwich Union by Roger Ryan, a comprehensive account of one of Britain's oldest and most influential insurance institutions.

-

Aviva plc 2025 Full Year Results Announcement (5 March 2026), the definitive source for the company's latest financial performance and strategic outlook.

-

Aviva Capital Markets Day Transcript (November 2025, "In Focus" event), where management laid out medium-term targets including eleven percent operating EPS growth through 2028 and return on equity exceeding twenty percent.

-

CMA Phase 1 Decision: Aviva / Direct Line Merger (August 2025), the Competition and Markets Authority's analysis of why the UK's largest insurance combination did not raise competition concerns.

-

The UK Life and Pensions Consolidation Wave, industry analyses from Lane Clark & Peacock and Hymans Robertson on the structural forces driving workplace pension market growth and consolidation.

-

ShareAction: Point of No Returns 2025, the responsible investment benchmark that ranked Aviva Investors fifth globally among the world's largest asset managers for ESG integration.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube