AutoStore: The Geometry of Efficiency

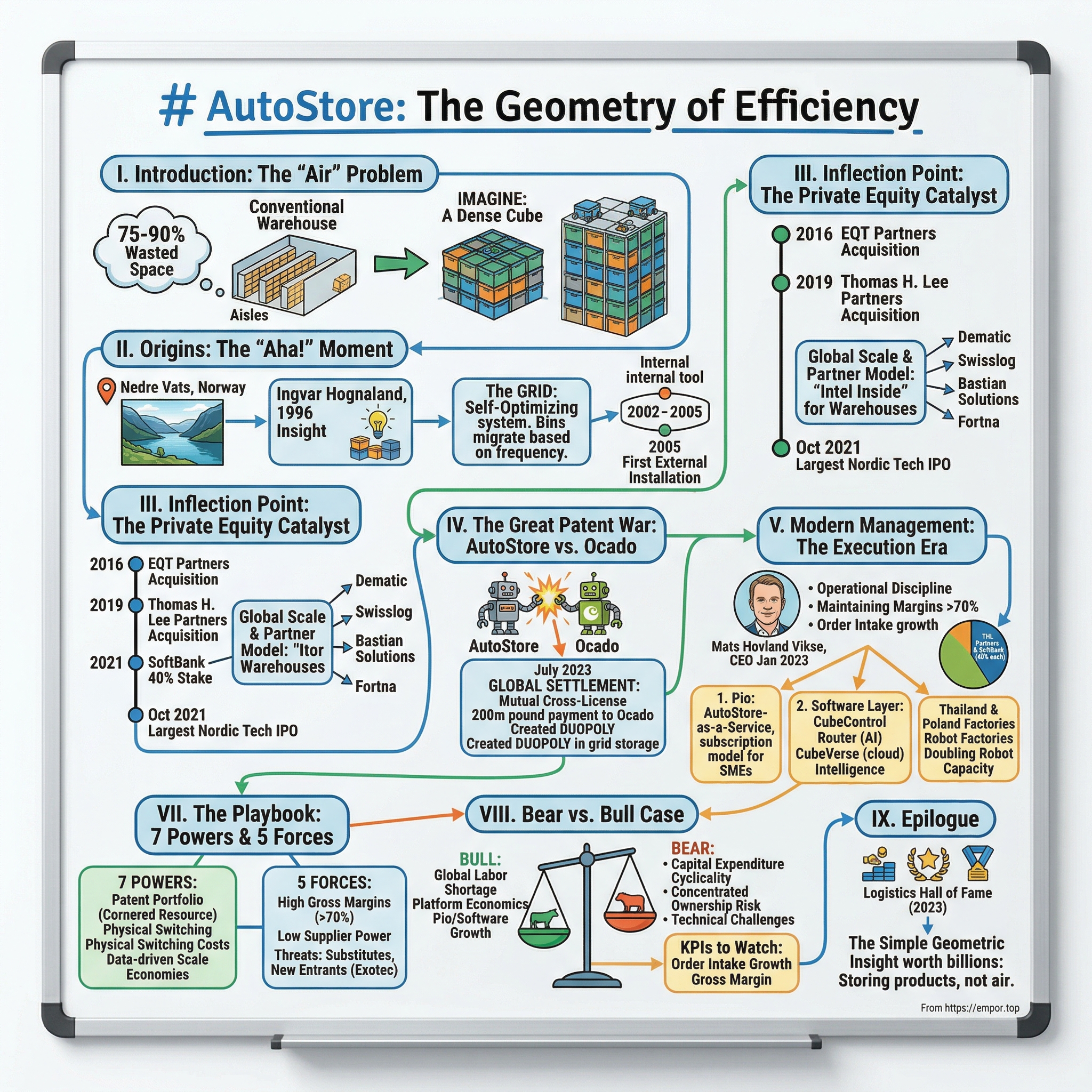

I. Introduction: The "Air" Problem

Walk into a typical warehouse anywhere in the world, and you will notice something absurd. Most of the building is empty. Not just a little empty — roughly 75 to 90 percent of the cubic volume in a conventional warehouse is air. Aisles stretch between towering shelving units so that forklifts can maneuver. Shelves are spaced apart so workers can reach them. Pallets sit half-full because the next shipment might need the remaining space. The entire architecture of modern warehousing was designed around the constraints of human bodies and the turning radius of a forklift, and the result is that companies pay for enormous buildings to store, predominantly, nothing.

Now imagine a different geometry. A dense aluminum grid, like a three-dimensional chessboard, where plastic bins are stacked directly on top of each other with no aisles, no wasted space, and no humans walking the floor. Small robots ride across the top of the grid on rails, dipping down to retrieve bins and delivering them to workstations at the edges. The bins containing the most frequently ordered items naturally migrate to the top of the stack over time — a self-organizing system that gets smarter the more it is used. The footprint of this system is roughly one-quarter the size of a conventional warehouse holding the same inventory. In a world where commercial real estate in logistics hubs costs fifteen to twenty-five dollars per square foot annually, that density advantage is not a novelty. It is an economic weapon.

The company that invented this geometry is AutoStore Holdings Ltd., listed on the Oslo Stock Exchange under the ticker AUTO.OL. It was born not in a Silicon Valley garage or a Tokyo robotics lab, but in a tiny Norwegian coastal village called Nedre Vats, population roughly a thousand, where a regional electronics distributor was running out of warehouse space and one of its engineers had an insight that would reshape global logistics.

AutoStore went public in October 2021 in what was the largest Nordic technology IPO in history, reaching a market capitalization that briefly exceeded twelve billion dollars. Since then, the share price has traveled a turbulent path — buffeted by post-pandemic capital expenditure slowdowns, a bruising multi-jurisdictional patent war, and the broader repricing of high-multiple growth stocks. As of early April 2026, the market cap sits around three billion dollars, a far cry from the IPO euphoria but still reflecting a company with approximately 1,900 installed systems in 65 countries, over 50,000 robots deployed, and adjusted EBITDA margins that most software companies would envy.

This is the story of how a warehouse problem in a Norwegian village became a global logistics standard, how private equity transformed an engineering project into a platform business, and why the geometry of efficiency might be the most underappreciated competitive moat in industrial technology.

II. Origins: The "Aha!" Moment

In the mid-1990s, Jakob Hatteland had a problem that was, ironically, a product of his own success. Hatteland ran one of Northern Europe's largest electronics distribution businesses from Nedre Vats, a village wedged between fjords on Norway's southwestern coast. He had started decades earlier by repairing televisions, then pivoted to distributing electronic components — a business that grew steadily and reliably. But growth meant inventory, and inventory meant space, and space in a fjord village is not something you can conjure from thin air. Hatteland kept building warehouses, and they kept filling up.

His technical director, a quiet engineer named Ingvar Hognaland, spent his days watching workers push carts down long aisles, hunting for parts among shelving units that stretched toward the ceiling but were, in practice, mostly air. The conventional wisdom of warehouse design held that you needed aisles for access and shelves for organization. Hognaland questioned both assumptions. Why, he wondered, do we store things like a library — organized in rows with walking space between them — when we could store them like a Rubik's cube, stacked tight with a mechanism on top to fetch what you need?

The insight sounds simple in retrospect. Most paradigm-shifting ideas do. But Hognaland's 1996 concept was genuinely radical: eliminate the aisles entirely. Stack bins directly on top of each other inside a dense aluminum grid. Build small, lightweight robots that ride on rails across the top of the grid, equipped with gripper mechanisms that can reach down through the stack, grab a specific bin, and bring it to a human operator at a workstation on the edge. No forklifts. No workers walking miles per shift. No wasted vertical or horizontal space.

The physics of the system created an elegant self-optimization loop. Every time a robot retrieves a bin from deep in a stack, it places that bin back on top when finished. Items that are ordered frequently naturally migrate upward, becoming faster to access over time. Items that are rarely needed sink to the bottom, where they occupy space but do not slow down operations. The system learns from its own activity without requiring explicit programming — a kind of emergent intelligence born from simple mechanical rules.

What followed was not a startup sprint but a long, patient, very Norwegian development cycle. Hognaland and the Hatteland team spent the next several years refining the concept, testing prototypes, and iterating on the grid structure, the robot design, and the software that coordinated multiple robots operating simultaneously on the same grid without colliding. The system was used internally at Hatteland's own distribution facility starting around 2002. For nearly a decade, AutoStore existed not as a product but as a proprietary internal tool — a competitive advantage that Hatteland's customers never saw.

The first external installation did not happen until 2005, a full nine years after Hognaland's original insight. In an era when technology startups measure their runway in months and their pivots in weeks, AutoStore's decade of quiet, internal development seems almost quaint. But that patience was strategic, even if it was not always intentional. By the time AutoStore began selling to external customers, the technology had been debugged, refined, and proven in a real-world operating environment — not in a lab, not in a demo, but in a working warehouse shipping real products to real customers every day.

The commercial launch was modest. Early customers were other Norwegian and Scandinavian distributors and manufacturers who had warehouse problems similar to Hatteland's. The team was small. The sales effort was minimal. AutoStore was still very much a division of an electronics distributor, not a standalone technology company with global ambitions. But the fundamental insight — that the geometry of storage could be radically reimagined to eliminate wasted space — was proven. The grid worked. The robots worked. The software worked. What AutoStore needed now was not more engineering. It was capital, commercial infrastructure, and the ambition to scale a Norwegian engineering project into a global platform.

That transformation would arrive in the form of private equity, and it would change everything.

III. Inflection Point: The Private Equity Catalyst

In December 2016, EQT Partners, the Swedish private equity firm, announced the acquisition of AutoStore from Jakob Hatteland Holding and other minority owners. Hatteland had held roughly 67 percent of the company and retained a small stake of around 9 percent post-close. The precise transaction value was not publicly disclosed, but Norwegian media reported that Hatteland received approximately three billion Norwegian kroner. At the time, AutoStore had roughly 500 million kroner in annual revenue and an EBITDA of about 240 million kroner — already a remarkably profitable business with margins that hinted at what was to come.

EQT's arrival marked the transformation from Norwegian engineering project to global platform. The private equity playbook was applied with precision: professionalize the management team, invest in product development, expand geographically, and build the commercial infrastructure to sell the technology worldwide. Under EQT's ownership, AutoStore established a U.S. headquarters, launched the new "Black Line" robot series with enhanced capabilities, quadrupled revenues, and doubled headcount. The sleepy fjord-village invention was being prepared for the global stage.

But the most consequential strategic decision of this era was not a product launch or a geographic expansion. It was the formalization of AutoStore's partner model — a business architecture that would become the foundation of the company's economics and competitive positioning. AutoStore chose not to install its own systems. Instead, it sells its robots, grids, and software to a network of certified system integrators — major logistics firms like Dematic (owned by KION Group), Swisslog (owned by KUKA), Bastian Solutions (owned by Toyota Advanced Logistics), and Fortna. These partners design the warehouse layout, install the grid, integrate AutoStore with the customer's warehouse management software, and provide ongoing service and maintenance.

Think of it like the Intel Inside model applied to warehouses. AutoStore makes the core technology — the high-margin, proprietary components — and lets partners handle the labor-intensive, lower-margin work of installation and integration. This architecture allowed AutoStore to achieve global reach with a remarkably lean organization: even today, the company operates with fewer than a thousand full-time employees. A traditional automation company installing bespoke systems worldwide would need thousands of field engineers, project managers, and service technicians. AutoStore outsourced all of that complexity and kept the economics.

In June 2019, Thomas H. Lee Partners, the Boston-based private equity firm, acquired AutoStore from EQT at a valuation of approximately sixteen billion Norwegian kroner, roughly $1.9 billion. EQT retained a minority stake of around 10 percent. The return for EQT in under three years was extraordinary — a multiple that validated the thesis that cube storage was not a niche curiosity but a category-defining technology.

THL continued the scaling playbook, but the biggest signal of the era came in April 2021, when SoftBank Group acquired a 40 percent stake from THL and other shareholders for $2.8 billion, implying a total enterprise valuation of approximately $7.7 billion. Masayoshi Son's investment thesis was characteristically bold: he viewed AutoStore as "foundational technology" for the future of logistics, a bet on the structural shift toward e-commerce fulfillment and automated warehousing. At $7.7 billion, the valuation was steep — but it was 2021, the world was in the grip of pandemic-era e-commerce acceleration, and the robotics and AI narrative was in full bloom.

Six months later, in October 2021, AutoStore listed on the Oslo Stock Exchange at a price of 31 Norwegian kroner per share, raising approximately 2.7 billion kroner from the sale of treasury shares. The implied market capitalization at the IPO was roughly $12.4 billion, making it the largest Nordic technology listing in history. Shares surged on debut day.

The trajectory from Hatteland's fjord warehouse to a twelve-billion-dollar public company had taken 25 years. The acceleration from a three-billion-kroner EQT buyout to a twelve-billion-dollar IPO had taken five. Private equity had done exactly what it is supposed to do — identify an undervalued asset with platform potential, invest in commercialization, and create the infrastructure for scale. But the IPO came at the peak of a cycle, and what followed would test whether the underlying technology was as defensible as the valuation implied. The most dramatic test would come not from the market, but from a courtroom.

IV. The Great Patent War: AutoStore vs. Ocado

In October 2020, with the IPO still a year away and the business growing rapidly, AutoStore fired the first shot in what would become one of the most consequential intellectual property battles in the history of logistics technology. The company filed suit simultaneously in the United Kingdom's High Court and at the U.S. International Trade Commission, alleging that Ocado Group, the British online grocery technology company, had infringed six AutoStore patents with its "Single Space Robot" grid-based system.

The stakes were existential, not in the financial sense — AutoStore was profitable and growing — but in the architectural sense. If AutoStore could not defend its patents on the fundamental concept of cube storage, the grid design that was the bedrock of its competitive moat would be open to imitation by anyone with the engineering capability to build a similar system. Ocado was not a small startup testing the boundaries; it was a publicly listed company with a market capitalization that at times exceeded ten billion pounds and technology partnerships with major grocery chains worldwide. If Ocado's system was deemed non-infringing, it would signal that the grid concept was either obvious or unpatentable — and AutoStore's premium valuation would be built on sand.

Ocado responded aggressively. In December 2020, the British company filed a defense claiming no infringement and arguing that AutoStore's patents were invalid. By March 2021, Ocado had counter-sued in U.S. District Court in New Hampshire and filed separate infringement claims against AutoStore in German courts in Mannheim and Munich. The battle had gone global, with parallel proceedings across multiple jurisdictions, each with its own procedural timelines and standards for patent validity.

The litigation consumed enormous resources on both sides. Legal teams spanning intellectual property specialists in London, Washington, and continental Europe billed what industry observers estimated were tens of millions of dollars collectively. For AutoStore, which was preparing for its IPO during the early stages of the lawsuit, the litigation cast a shadow over the investment narrative. Patent disputes inject uncertainty, and uncertainty suppresses multiples.

In March 2023, the UK High Court delivered its ruling, and it was not the outcome AutoStore had hoped for. Two of AutoStore's patents were found invalid, and Ocado's products were found not to infringe the remaining patents at issue. AutoStore had already withdrawn claims on two additional patents during the proceedings. Ocado publicly declared "total victory" in the UK proceedings. But the war was far from over. In June 2023, Ocado escalated by filing four new suits against AutoStore at the newly operational Unified Patent Court, targeting local chambers in Dusseldorf, Milan, and the Nordic-Baltic regional division in Stockholm.

The resolution came less than two months later. On July 22, 2023, AutoStore and Ocado announced a comprehensive global settlement. The terms were sobering for AutoStore: the company agreed to pay Ocado approximately 200 million pounds — roughly $257 million — in 24 monthly installments. In exchange, the two companies entered into a mutual global cross-license of each other's pre-2020 patents, allowing both to continue using and marketing all existing products without challenge. AutoStore was prohibited from making or using a single-space cavity robot in jurisdictions where Ocado held patent protection, while Ocado retained exclusive rights to its Single Space Robot design.

For AutoStore, the settlement was financially painful — a quarter-billion dollars paid to the very party it had accused of infringement. In the 2023 fiscal year, the litigation costs and settlement charges contributed to a net loss of $32.6 million despite revenue of $646 million. By early 2026, the installment payments were largely complete, removing the financial drag from the income statement.

But the strategic interpretation was more nuanced than the headline suggested. The cross-license effectively created a duopoly in grid-based cube storage. AutoStore and Ocado each had freedom to operate without infringing the other's intellectual property, while any third party attempting to enter the cube storage market would face the combined patent portfolios of both companies — over 1,500 patents and applications across 270 patent families on AutoStore's side alone. The settlement did not destroy AutoStore's moat. In a counterintuitive way, it formalized it. The grid was now protected not by one patent holder but by two, with a mutual interest in defending the category against newcomers.

The patent war also forced AutoStore to articulate, under legal pressure, exactly what made its technology proprietary and differentiated. That exercise, painful as it was, clarified the intellectual property landscape for investors, partners, and customers in ways that years of marketing presentations never could. When the dust settled, AutoStore's patent portfolio was intact, its market position was unchallenged, and the only company with a credible competing grid technology was contractually bound in a cross-license that prevented further hostilities.

V. Modern Management: The Execution Era

When Mats Hovland Vikse took over as CEO on January 1, 2023, he inherited a company in the middle of a patent war, coming off an IPO peak that had already faded, and facing a macroeconomic environment where rising interest rates were causing corporate customers worldwide to freeze or defer capital expenditure on warehouse automation projects. It was not, by conventional measures, an enviable position.

Vikse had joined AutoStore in 2017 as Chief Strategy Officer, arriving just after the EQT acquisition and helping architect the commercial expansion that followed. He was promoted to Chief Revenue Officer in 2021 as the IPO approached, giving him direct responsibility for the partner relationships and sales pipeline that drove the business. Before AutoStore, he had served as a senior advisor at MHWirth, a Norwegian drilling equipment manufacturer — industrial technology, not consumer tech, not software, not finance. He held degrees from BI Norwegian Business School and the University of Stavanger. His profile was that of a methodical industrial operator, not a charismatic visionary.

This was, by design, the right profile for the moment. AutoStore's preceding CEO, Karl Johan Lier, had guided the company through its transformation from a Hatteland division to a global platform business and through the IPO. Lier, a graduate of NHH (the Norwegian School of Economics), had been with the business since its early days at Hatteland Technology. His departure was described as a planned and orderly succession — a rarity in the world of high-growth tech companies, where CEO transitions are often reactive and disruptive.

Vikse's mandate was not invention or reinvention. It was execution. The technology was proven. The partner network was established. The patent portfolio was secure. What the company needed was operational discipline during a cyclical downturn, continued investment in new products, and a clear communication of the long-term value story to a shareholder base that had watched the stock decline from its IPO heights.

The management team under Vikse holds significant equity, with incentive structures tied to return on invested capital and market expansion metrics rather than simple robot unit sales. This alignment matters in a period where the temptation for a company facing declining revenue might be to chase volume through discounting or premature geographic expansion. Instead, AutoStore under Vikse has maintained gross margins above 70 percent even as revenue contracted — a sign that the company is prioritizing profitability and long-term pricing power over short-term top-line growth.

The ownership structure remains concentrated. THL Partners and SoftBank Group each hold approximately 40 percent of the outstanding shares, leaving a free float of roughly 30 percent. This concentration creates both stability and risk. On the stability side, two large institutional owners with long-term horizons can support management through cyclical downturns without the quarter-to-quarter pressure that dispersed retail ownership creates. On the risk side, the relatively thin free float amplifies stock price volatility, and the eventual monetization of THL's and SoftBank's positions represents a potential overhang that the market has not forgotten. SoftBank, in particular, has a well-documented history of monetizing portfolio holdings to fund other investments, and any signal of selling intention could weigh on the share price.

The financial trajectory under Vikse tells a story of cyclical challenge rather than structural decline. Revenue for fiscal year 2025 came in around $539 million, down roughly 10 percent from fiscal 2024's $601 million, which itself was down from the peak of $646 million in fiscal 2023. The decline reflected the broader capital expenditure slowdown across warehouse automation, not a competitive loss. The critical forward-looking indicator was more encouraging: order intake in the fourth quarter of 2025 reached $194 million, up 35 percent year over year, and the year-end order backlog hit a record $557 million, up nearly 22 percent. Adjusted EBITDA margins held at approximately 42 percent for the full year, with the fourth quarter reaching 43.3 percent. Gross margins actually hit a record 73.1 percent in fiscal 2024 on full-year revenue of $601 million, and remained above 70 percent throughout 2025. The company added 150 new customers during the year and released 11 new products.

The balance sheet remained clean. Net debt stood at roughly $180 million against cash of $90 million, with a net debt to adjusted EBITDA ratio of just 0.8 times — conservative leverage that provides flexibility for investment and acquisitions through the cycle.

VI. Hidden Businesses and High-Growth Segments

The popular narrative around AutoStore centers on robots — the physical machines that ride along the grid, retrieve bins, and deliver them to workstations. It is an appealing image, and AutoStore's marketing leans into it. But the most strategically important developments at the company are happening in three areas that receive far less attention: the Pio product line, the software layer, and micro-fulfillment.

Start with Pio, which AutoStore launched at the National Retail Federation show in New York in January 2023. The name stands for "Product In/Out," and the concept represents a fundamental shift in AutoStore's business model. Traditional AutoStore installations are large, custom-designed projects: a warehouse operator works with one of AutoStore's integration partners to design a grid layout, purchases the hardware, installs the system, and operates it as a capital asset. The upfront cost can run into the millions or tens of millions of dollars, and the sales cycle can stretch twelve to eighteen months. This model works well for large enterprises — the Pumas, the Guccis, the Ahold Delhaizes — but it effectively locks out small and medium-sized businesses that need automation but cannot afford or justify the capital expenditure.

Pio addresses this with a pre-configured, plug-and-play approach. Instead of a bespoke design, Pio offers four standardized configurations — P100, P200, P400, and P600 — scaling from small operations to mid-sized fulfillment centers capable of handling roughly 360 orders per hour. The pricing model shifts from capital expenditure to operating expenditure: customers pay a fee per individual item picked, while the robots, ports, and software remain owned and maintained by Pio. Customers purchase only the bins and grid frames. Think of it as AutoStore-as-a-Service, a subscription model for warehouse automation.

The strategic implications are significant. If AutoStore's traditional business is selling Lego kits to companies that build their own structures, Pio is selling a finished product that plugs into existing operations. It dramatically expands the addressable market by reaching companies that would never have considered a full AutoStore installation. It also creates a recurring revenue stream — per-pick fees that accumulate over time — in a business that has historically been driven by one-time hardware sales. Pio launched in the U.S. market in May 2024 and remains in its early growth phase.

The second hidden engine is the software layer, which is becoming arguably more valuable than the physical robots. AutoStore's core software platform, CubeControl, manages all system operations — directing individual robot movements, coordinating hundreds of robots simultaneously on a single grid, and optimizing bin placement based on order patterns. Within CubeControl sits the "Router," an AI-driven pathfinding engine that continuously calculates optimal routes in real time, anticipates traffic patterns, adjusts to priority changes, and learns from historical data.

In March 2026, AutoStore launched CubeVerse, a new cloud-based platform that extends the software across the full system lifecycle. CubeVerse includes CubeStudio, a shared cloud environment for system design, simulation, and validation that allows integration partners and customers to collaboratively model new installations before a single piece of aluminum is cut. The platform also introduced enhanced warehouse management system integration through a module called VersaPort, which connects AutoStore's software to existing enterprise WMS solutions via standard APIs. Alongside CubeVerse, the company rolled out AutoStore Intelligence, an AI optimization layer that personalizes each grid based on specific operational patterns — analyzing historical data, seasonal demand, and picking patterns to determine optimal routing parameters and what the company calls "robot highways."

The strategic significance of this software evolution is that it shifts the value proposition from "we sell robots that move bins" to "we sell a logistics intelligence platform that happens to use robots." The distinction matters because software scales without factories, creates switching costs through integration, and supports recurring revenue through updates and cloud subscriptions. Hardware competitors can, in theory, build a robot. Replicating a decade of routing algorithm development trained on data from 1,900 installations worldwide is a fundamentally harder problem.

The third hidden growth driver is micro-fulfillment, a category where AutoStore's density advantage creates an almost unassailable position. A micro-fulfillment center — typically about 10,000 square feet, deployed in the back of a grocery store or urban dark store — is designed to handle online grocery orders for rapid delivery. The challenge is space: a grocery store's back room is small, and fitting meaningful inventory into that footprint requires extreme storage density. AutoStore's cube storage architecture, which uses roughly one-quarter the floor space of conventional systems, is uniquely suited to this application.

Major grocery deployments have included Ahold Delhaize in the United States through its Peapod Digital Labs subsidiary, Albertsons for back-of-store micro-fulfillment, Woolworths in Australia, and ASDA in the United Kingdom. A typical micro-fulfillment installation can be deployed in roughly twelve weeks, compared to the months or years required for a full-scale distribution center, and costs in the range of three to four million dollars.

The product hardware itself continues to evolve. AutoStore's main robot lines include the R5, the compact and cost-efficient workhorse designed for most standard applications, and the B1, a roughly twice-as-fast unit designed for high-speed fulfillment environments like e-commerce peak periods and pharmaceutical distribution. Manufacturing has expanded beyond the original contract manufacturing base in Poland, where robots have been produced since 2012, to a new factory in Rayong Province, Thailand, which opened in June 2024, aiming to produce 15,000 robots in eighteen months and doubling total capacity.

VII. The Playbook: 7 Powers and 5 Forces

The most important question about any business with premium margins and a concentrated market position is whether the advantage is durable or temporary. AutoStore's 70-plus percent gross margins and 40-plus percent EBITDA margins are extraordinary, but they only matter to long-term investors if they are defensible. Applying Hamilton Helmer's 7 Powers framework and Michael Porter's 5 Forces reveals a business with multiple reinforcing layers of competitive protection — but also some genuine vulnerabilities.

Start with the 7 Powers. AutoStore's most obvious power is what Helmer calls a cornered resource — in this case, its patent portfolio. With over 1,500 patents and patent applications across 270 patent families, and with the Ocado cross-license settlement effectively creating a duopoly in grid-based cube storage, any new entrant attempting to build a competing grid system faces a formidable intellectual property barrier. Patents expire, of course, and the earliest AutoStore patents from the late 1990s are reaching or have reached the end of their terms. But the company has continuously filed new patents on incremental innovations — robot designs, software algorithms, grid configurations — extending the portfolio's effective life.

The second power is switching costs, and in AutoStore's case, they are almost uniquely physical. When a customer installs an AutoStore grid, they are building a twenty-foot-high steel and aluminum structure into the physical fabric of their warehouse. The grid is bolted to the floor. The bins are custom-fitted. The software is integrated with the customer's warehouse management system. The robots are configured for the specific grid layout. Switching to a competitor would require not just purchasing new technology but physically demolishing and removing the existing grid — a project that would cost millions of dollars, take months, and shut down warehouse operations during the transition. In practice, once a grid is installed, the customer is committed for the fifteen-to-twenty-year lifespan of the system. This creates an extraordinarily sticky installed base and provides a recurring revenue opportunity through spare parts, additional robots, grid expansions, and software upgrades.

The third power is scale economies, though these operate differently from the classic manufacturing context. The more systems AutoStore installs worldwide, the better its software becomes. The Router algorithm is continuously refined based on operational data from 1,900 installations across 65 countries. Each new installation generates data about order patterns, robot traffic management, and bin placement optimization that feeds back into the software for all installations. This is a data-driven scale economy: the marginal cost of improving the algorithm decreases as the installed base grows, while the benefit accrues to every customer. A new competitor starting from scratch would have zero installations generating zero data, making it nearly impossible to match AutoStore's software performance without years of deployment history.

Now apply Porter's 5 Forces to the broader competitive landscape. The threat of substitutes is the most commonly cited concern. Traditional warehouse automation — shuttle systems from companies like Knapp, SSI Schaefer, and Dematic's own non-AutoStore products — uses robotic shuttles traveling along aisles within conventional racking structures. These systems work, but they require roughly four times the floor space for the same storage capacity. In a world of rising real estate costs, this density disadvantage is a significant economic penalty. The more expensive warehouse space becomes, the more compelling AutoStore's density advantage.

The threat of new entrants is real, and the most credible challenger is Exotec, a French unicorn that raised $335 million in 2022 at a $2 billion valuation. Exotec's Skypod system takes a different approach: its robots move in three dimensions, driving horizontally on the warehouse floor and climbing vertically up racking structures up to twelve meters high. The key trade-off is that AutoStore wins on density — more storage per square foot — while Exotec wins on flexibility, offering direct access to any bin without needing to move the bins stacked above it. Exotec is the first genuinely competitive alternative to the grid concept, and its growth is worth monitoring closely. However, Exotec targets a somewhat different customer profile, often competing more directly with traditional shuttle systems than with AutoStore's cube storage approach.

Competitive rivalry within the cube storage niche is currently limited to AutoStore and, through the cross-license, Ocado's technology arm. In the broader warehouse automation market, competition is fierce among Dematic, Swisslog, Honeywell Intelligrated, and others, but AutoStore's partner model means these companies are simultaneously competitors in the broader market and distribution partners for AutoStore's specific technology. This creates an unusual dynamic where the same firms that might develop competing products also have a financial incentive to sell AutoStore systems.

The bargaining power of buyers is moderate. Large customers — global retailers, major logistics providers, pharmaceutical distributors — have significant purchasing power, but the switching costs once a system is installed shift leverage back to AutoStore for expansion and upgrade decisions. Supplier power is low; AutoStore's components — aluminum grid structures, electric motors, sensors — are commodity inputs sourced from multiple suppliers, and robot manufacturing has been diversified across Poland and Thailand.

The competitive moat is layered and reinforcing. The patents create a legal barrier. The installed base creates a physical switching cost. The data network creates a software advantage. The partner model creates distribution reach without proportional cost. And the density advantage creates an economic incentive for customers that intensifies as real estate costs rise. No single layer is impregnable, but the combination creates a defensive position that would take a competitor years and billions of dollars to replicate.

VIII. Bear vs. Bull Case

The bull case for AutoStore rests on a structural thesis: the world is running out of warehouse labor, and the economics of automation are crossing a tipping point that will drive adoption for decades.

The global warehouse labor shortage is not cyclical — it is demographic. Aging populations in developed economies, declining birth rates, and a persistent reluctance among younger workers to take physically demanding warehouse jobs have created a structural deficit that wage increases alone cannot solve. In the United States, the warehouse and storage sector has seen annual employee turnover rates exceeding 40 percent. In Europe and Japan, the labor dynamics are even tighter. Every year that the labor shortage persists, the payback period on a warehouse automation investment shortens, because the cost of the human alternative keeps rising.

AutoStore is, in this framing, a "toll bridge" for the future of commerce. Every package ordered online, every prescription filled at a pharmacy, every auto part delivered to a repair shop passes through a warehouse. As these warehouses automate, AutoStore's grid technology offers the densest, most proven, most partner-supported solution in the market. The 1,900 installed systems represent a tiny fraction of the addressable market — the global warehouse automation market was estimated at roughly $20 billion in 2023 and is projected to approach $41 billion by 2028, growing at approximately 15 percent annually.

The margin profile supports the quality thesis. Gross margins above 70 percent and EBITDA margins above 40 percent are not hardware-company economics — they are platform-company economics. AutoStore designs the core technology and sells it through partners who bear the installation costs. The company operates with fewer than a thousand employees worldwide. Revenue per employee is exceptionally high by industrial standards. If the market begins to value AutoStore on the basis of its actual economic profile — a high-margin, asset-light, recurring-revenue platform — rather than as a cyclical industrial hardware manufacturer, the valuation gap could be significant.

The Pio product line and the software evolution strengthen the bull case further. Pio expands the addressable market to small and medium businesses that were previously uneconomic to serve, while the shift to per-pick pricing creates recurring revenue. The software layer — CubeControl, Router, AutoStore Intelligence, CubeVerse — adds switching costs, supports premium pricing, and opens the door to cloud-based revenue streams that scale without additional hardware sales.

The bear case begins with cyclicality. AutoStore's customers are making large capital expenditure decisions, and those decisions are highly sensitive to interest rates, economic confidence, and the availability of capital. The revenue decline from $646 million in fiscal 2023 to $539 million in fiscal 2025 demonstrated that even a company with structural tailwinds can experience meaningful demand declines when the macroeconomic environment turns unfavorable. If interest rates remain elevated or the global economy enters recession, customers will defer automation projects, and AutoStore's order intake will decline regardless of the long-term demand thesis.

The concentration of ownership creates specific risks. With THL and SoftBank each holding approximately 40 percent and a free float of only about 30 percent, the stock is structurally illiquid relative to its market capitalization. Any indication that either major shareholder intends to reduce its position could trigger significant selling pressure. SoftBank's track record of monetizing portfolio companies to fund its broader investment activities makes this concern more than theoretical.

Competition, while currently limited in the cube storage niche, is evolving. Exotec's three-dimensional approach offers genuine technical advantages in flexibility and direct bin access. If Exotec or another challenger achieves sufficient scale and cost efficiency to compete credibly with AutoStore on density, the premium pricing that supports 70 percent gross margins could come under pressure. The expiration of older patents gradually reduces the legal barrier to entry, placing more weight on the software and data advantages to maintain differentiation.

The EBITDA margin trajectory also warrants monitoring. The decline from 47 percent in fiscal 2024 to 42 percent in fiscal 2025, while still excellent, suggests that margins are not immune to revenue deleverage. If the company invests aggressively in Pio, software development, and geographic expansion during a period of soft demand, margins could compress further before the growth investments pay off.

For investors tracking AutoStore's ongoing performance, two KPIs deserve primary attention. The first is order intake growth, which is the most reliable leading indicator of future revenue. Order intake bottomed during the capital expenditure slowdown and showed strong recovery in the second half of 2025, with the fourth quarter up 35 percent year over year. The trajectory of this metric over coming quarters will signal whether the cyclical recovery is broadening or stalling. The second is gross margin, which captures AutoStore's pricing power and competitive positioning in a single number. Sustained gross margins above 70 percent indicate that the company is not being forced to discount to compete, that the partner model is functioning as designed, and that the technology commands a premium. Any meaningful erosion in gross margin would signal either competitive pressure or a shift in the business mix toward lower-margin products — either of which would require reassessment of the long-term thesis.

IX. Epilogue

The Norwegian secret is no longer a secret. What began as one engineer's frustration with wasted warehouse space in a fjord village has become a global logistics standard with installations on six continents. The journey from Ingvar Hognaland's 1996 insight to a publicly listed company managing 1,900 systems required three rounds of private equity ownership, an IPO, a multi-jurisdictional patent war, a pandemic-era boom, and a post-pandemic correction. It was not fast, not smooth, and not without cost.

The question that remains open is whether AutoStore is a hardware company that happens to have good software, or a software-defined logistics standard that happens to use robots. The answer to that question determines not just the appropriate valuation multiple but the long-term trajectory of the business. Hardware companies grow linearly with unit sales and are constrained by manufacturing capacity, supply chains, and competitive pricing pressure. Software platforms grow with network effects, generate recurring revenue, and compound their advantages through data. The CubeVerse launch, the AutoStore Intelligence rollout, and the Pio subscription model all point toward the software trajectory. Whether that evolution proceeds fast enough to outrun patent expirations and new entrants is the defining strategic question for the decade ahead.

Ingvar Hognaland and Jakob Hatteland were inducted into the International Logistics Hall of Fame in November 2023 — a recognition of the invention that started it all. The grid they conceived in 1996 stores products, not air. In a world where every square foot of warehouse space carries a rising price tag, that simple geometric insight has proven to be worth billions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube