AngloGold Ashanti: Shifting the Golden Anchor

I. Introduction & Episode Roadmap

Picture two maps of the same company, drawn twenty years apart. On the first, dated 2004, almost every dot sits inside a single country: a cluster of ultra-deep shafts strung along South Africa's Witwatersrand, boring more than four kilometres into the oldest, hottest, most seismically violent rock ever mined for profit. On the second, dated 2026, that home country has gone completely dark — not a single producing ounce left inside South Africa's borders — while new dots glow across Egypt, Tanzania, the Democratic Republic of Congo, Ghana, Guinea, Australia, Argentina, Brazil and, most tellingly, the high desert of southern Nevada. The corporate headquarters has migrated from Johannesburg to a glass office park in Greenwood Village, on the southern edge of Denver, Colorado. The primary stock listing has moved from the Johannesburg Stock Exchange to the New York Stock Exchange.4

That is the story in one image: a South African champion that spent two decades methodically dismantling its own origins to escape what the market had priced as a curse.

The hook of this episode is a deceptively simple question. Can a company change its address and thereby change its value? For most businesses the idea is absurd — a mine in Tanzania produces the same gold whether its parent is registered in London or Luanda. And yet AngloGold Ashanti's entire recent history is a multi-billion-dollar wager that geography of incorporation and listing — not just geography of ore — moves the stock price. Management sold the deepest mines on Earth, re-domiciled under the laws of England and Wales, and planted a flag on the NYSE, all to shed what investors had long called the "South African discount" and to be re-rated alongside North American gold majors like Newmont, Barrick and Agnico Eagle.

The current scale suggests the operational half of the strategy is working. In the year ended 31 December 2025, AngloGold Ashanti produced 3.1 million ounces of gold, up 16% year on year, and generated record free cash flow of $2.9 billion — roughly triple the $1.0 billion of a year earlier — helped by a gold price that averaged $3,468 an ounce, up 45%.13 The balance sheet flipped from $567 million of net debt at the end of 2024 to $879 million of net cash a year later, even after paying out a record $1.8 billion in dividends.13 By July 2026 the company carried a market value of roughly $41 billion.21

There is a reason this story matters beyond gold. AngloGold Ashanti is a live experiment in a question that hangs over dozens of emerging-market champions: whether a good business trapped in a bad postcode can buy its way into a better valuation simply by moving house. Naspers wrestled with a version of it; so have Chinese ADRs, Brazilian miners and Middle Eastern nationals eyeing London and New York. Most talk about it. AngloGold actually did it — irreversibly, at the cost of its own founding assets. That makes the company a natural case study in the limits of financial engineering: how much of a valuation discount is an artificial artefact of listing venue that a re-domicile can erase, and how much is a true reflection of where the cash is actually earned, which no ticker change can touch. The answer, as the following sections will show, turns out to be "some of each" — and the boundary between the two is exactly where the investment debate lives.

Three themes run through everything that follows. The first is jurisdictional arbitrage — the deliberate use of corporate migration to attack a valuation gap. The second is an operational pivot — the swap of labour-heavy, capital-devouring deep-reef mining for mechanised open pits and shallow underground ore bodies. The third is an M&A engine that has shifted from defensive African consolidation to aggressive expansion: the takeover of Centamin and its Egyptian crown jewel, and the quiet assembly of an entire new mining district in Nevada. Whether all three add up to a durable competitive edge — or merely a well-timed ride on a historic gold price — is the question a sceptical investor must keep asking. To understand why the migration mattered so much, the story has to begin underground, at the reef that made and nearly broke this company.

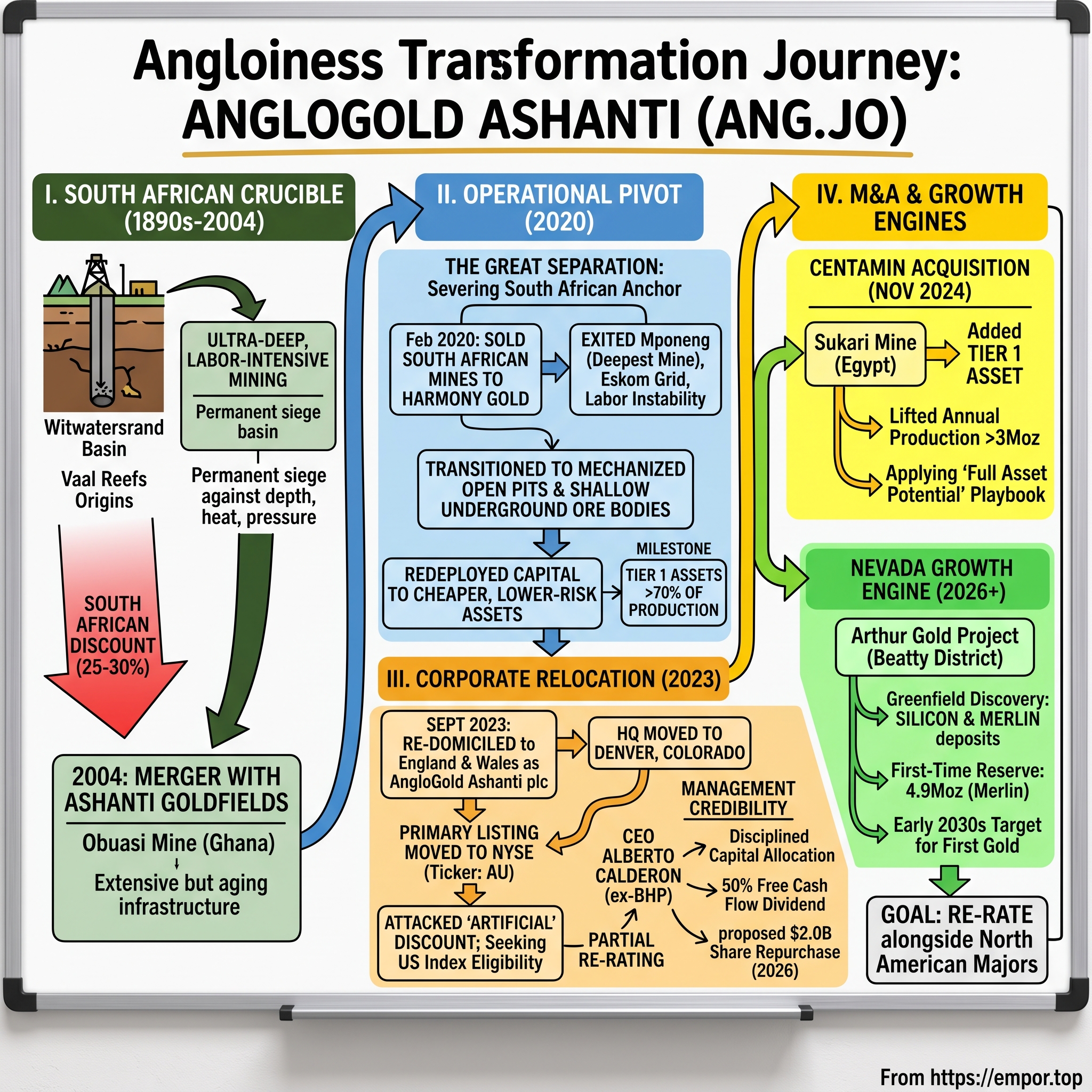

II. The South African Crucible & The Vaal Reefs Origins (1890s–2004)

Some 2.7 billion years ago, an inland sea in what is now the interior of South Africa laid down layer upon layer of sediment laced with gold. Compressed, tilted and buried over aeons, that structure — the Witwatersrand Basin — became the single richest gold deposit in the history of the planet, credited with something on the order of 40% of all the gold humans have ever pulled from the ground.6 When prospectors struck the main reef in 1886, they triggered a rush that built Johannesburg out of open veld in a decade and made South Africa synonymous with gold for the next hundred years.

The catch, written into the geology itself, was that the reef dipped away from the surface at a steep angle. The easy gold near the top was gone within a generation; the rest of it plunged kilometres down, into rock that grew hotter and more dangerous with every metre. Mining the Witwatersrand became less like digging and more like a permanent siege against depth, heat and pressure — a siege that required enormous capital, enormous labour, and a tolerance for risk that would define the industry's culture.

The corporate vehicle at the centre of this story was born inside the empire of Anglo American, the mining and finance house that dominated twentieth-century South Africa. For decades Anglo's gold interests were scattered across a web of separately listed mines. In 1998 the group consolidated them into a single independent company, AngloGold Limited, and listed it in Johannesburg and New York. The legal shell it used had deep roots: the entity had originally been incorporated in 1944 as the Vaal Reefs Exploration and Mining Company, one of the classic Witwatersrand producers.7 AngloGold arrived in the world as the largest gold miner on Earth, but also as a pure expression of South African deep-reef mining — its fortunes chained to a single basin and a single, increasingly troubled, economy.

The company's founders understood that a one-country, one-orebody profile was a strategic weakness, and they went looking for diversification on their own continent. The transformative move came in 2004, when AngloGold merged with Ghana's Ashanti Goldfields Company in a deal worth roughly $1.4 billion, confirmed by the High Court of Ghana in April of that year, and renamed itself AngloGold Ashanti.8 The prize — and the burden — was the Obuasi mine, a Ghanaian ore body worked continuously since 1897, one of the oldest operating gold mines in Africa.8 Obuasi carried extraordinary grade, the kind of rich rock that makes a geologist's heart race, but it also came with more than a century of accumulated developmental baggage: aging infrastructure, a labyrinth of old workings, and its own deep, structurally awkward reefs.

There is a reason Ashanti was available to be acquired at all, and it is a cautionary tale that hangs over the whole industry. Ashanti Goldfields, led for years by the charismatic Ghanaian executive Sam Jonah — knighted in Britain, celebrated as one of corporate Africa's first global statesmen, and the man who took the company onto the New York Stock Exchange in the 1990s — had spent the late 1990s building an enormous derivatives "hedge book" to lock in gold prices. When the gold price spiked sharply in 1999 after European central banks agreed to curb their bullion sales, those hedges turned toxic almost overnight, generating margin calls large enough to threaten the company with insolvency.8 A miner that bets against the price of its own product, and loses, discovers very quickly who really controls its destiny. Financially wounded, Ashanti spent the following years searching for a stronger partner, and AngloGold — outlasting a rival bid from Randgold Resources — was the one that ultimately absorbed it. The lesson embedded in that history would echo two decades later: in a commodity business, financial engineering can destroy a company as surely as a collapsed shaft.

So the company that emerged in 2004 was, on paper, an African champion spanning two of the continent's great goldfields. In practice it was something more precarious: a business anchored to high-risk, labour-intensive, physically dangerous deep-level mining, with a South African cost base and a South African stock listing. The gold was real. The question was whether the market would ever pay a fair price for it. For the next fifteen years, the answer was a stubborn no — and to see why, you have to descend to the bottom of the deepest mine on Earth.

III. The Golden Trap: Deep-Level Economics & The South African Discount (2000s–2010s)

At the bottom of the Mponeng mine, more than four kilometres below the surface, the rock is hot enough to cook a person to death. Left alone, the working faces would sit at around 60°C. To keep miners alive, the operation pumped slurries of ice down the shafts and ran refrigeration plants on a scale more commonly associated with a small city, chilling the air so that human beings could stand — briefly — in a place the Earth never intended them to go.5 Mponeng, at the time part of AngloGold Ashanti's portfolio, was and remains the deepest mine humans have ever operated.5 It is a monument to engineering ambition and, simultaneously, a monument to everything that made South African deep-reef gold a financial trap.

Consider the cost structure that depth imposes. Every extra kilometre of shaft is more rock to hoist, more air to cool, more water to pump, more distance for workers to travel before they even begin their shift. The capital required for refrigeration, ventilation and seismic reinforcement is staggering, and it buys no extra ounce of gold — it merely buys the ability to keep mining at all. Deep-reef mining is, in effect, a business where a large and rising share of spending goes not into production but into holding back the planet.

Then there is labour. Unlike a mechanised open pit, where a handful of operators run house-sized trucks, deep-reef gold mining in South Africa remained overwhelmingly manual, employing tens of thousands of workers in narrow, hot stopes. That workforce sat at the centre of a combustible industrial-relations landscape, with bitter rivalry between the long-established National Union of Mineworkers and the insurgent Association of Mineworkers and Construction Union. Wage disputes, wildcat strikes and, tragically, recurring underground fatalities regularly halted production. Safety was not merely a moral issue; it was an operational and financial one, because a fatal accident could shutter a mine for days or weeks.

To grasp why safety dominates every conversation on this company's earnings calls even today, it helps to sit with what deep-reef mining actually asks of a human being. A worker at the bottom of an ultra-deep mine may spend more than an hour simply travelling — down cages, along tunnels, deeper still — before reaching a working face where the rock radiates heat and the mass of two-and-a-half miles of overlying crust presses in, occasionally releasing that pressure as a "rockburst," a sudden violent failure of the rock that can kill without warning. South Africa's gold sector counted its fatalities in the dozens per year across the industry at its worst, and each incident carried not only human tragedy but regulatory consequence: under South African law, a fatality could trigger a Section 54 safety stoppage that halted an entire operation. For an investor, this translated a moral catastrophe into a financial variable — production you could not forecast, because a mine could go dark for reasons that had nothing to do with the ore and everything to do with the impossibility of the environment. Calderon's later obsession with achieving record-low injury rates is not sentiment; it is the memory of a business model where safety failures were also earnings failures.

Onto this already fragile system came a slow-motion energy catastrophe. South Africa's state power utility, Eskom, entered a long decline, and from the mid-2010s the country endured "load shedding" — scheduled rolling blackouts. For most businesses a blackout is an inconvenience. For a mine with thousands of people working four kilometres underground, dependent on continuous power for hoisting, ventilation and cooling, an unplanned outage is a potential mass-casualty event. Power instability degraded processing efficiency and added a layer of existential operational risk that no amount of good management could fully engineer away.

All of this fed into a number that haunted the company for a decade: the valuation gap. AngloGold Ashanti persistently traded at a discount — often on the order of 25–30% on enterprise-value-to-EBITDA multiples — to North American peers like Newmont, Barrick and Agnico Eagle, even when its individual mines were world class. Part of that gap reflected genuine cost and safety differences. But a large part reflected something more purely financial: the "South African discount." International institutions systematically shied away from JSE-listed miners regardless of where their assets actually sat, wary of the volatile rand, of political and policy uncertainty, of exchange-control rules that complicated moving capital in and out of the country. A mine in Tanzania owned by a Johannesburg-listed parent was, in the market's eyes, somehow worth less than the same mine owned by a Denver- or Toronto-listed one.

It is worth being precise about the mechanism, because "country risk premium" is the kind of phrase that gets used loosely. The discount was not one thing but a stack of them. There was currency risk: a company reporting in rand, whose costs were partly rand-denominated, exposed foreign investors to a currency that could and did swing violently against the dollar. There was policy risk: South Africa's mining charter, its evolving Black Economic Empowerment ownership requirements, and periodic talk of nationalisation all injected uncertainty into any long-dated cash-flow model. There were exchange controls that complicated the free movement of capital across South Africa's borders. And there was the brute mechanical reality of index construction: global and North American equity indices simply did not weight a Johannesburg-primary-listed stock the way they weighted a New York or Toronto one, which meant that a large pool of passive and benchmark-hugging capital was structurally unavailable to the shares no matter how good the underlying mines were. Stack those together and you get a persistent, self-reinforcing gap that no amount of quarterly operational excellence could fully close.

That is the intellectual crux of the entire modern AngloGold story. Management came to believe that a meaningful slice of the discount had nothing to do with rock or engineering and everything to do with the flag on the share certificate. If that belief was right, then the discount was not a fact of nature but a problem to be solved — by changing what the company owned and where it lived. The first, and most radical, step was to cut the anchor chain entirely.

IV. The Great Separation: Severing the South African Anchor (2020)

In February 2020, AngloGold Ashanti did something that would have been unthinkable to its founders: it agreed to sell its last South African gold mines and walk away from the Witwatersrand for good. The buyer was a home-grown rival, Harmony Gold, a company whose entire business model was built around wringing profit from the mature, deep, difficult South African assets that larger miners no longer wanted. Harmony took Mponeng — the deepest mine on Earth — together with the Mine Waste Solutions tailings-retreatment business, and assumed effective control from 1 October 2020.9

The financial terms are worth pausing on, because they became a Rorschach test for how one views the whole strategy. Harmony paid a base cash consideration of roughly $200 million, with additional contingent payments tied to future underground production that could lift the total toward the $300 million range.9 For a set of assets that had once been the beating heart of the world's largest gold miner, that is a strikingly modest sum.

Here the sceptical investor and the strategist part ways. Run the numbers on a pure backward-looking basis — total ounces still in the ground, valued at the gold price that would soon rip to record highs — and it is easy to argue that AngloGold sold enormous deposits far too cheaply, effectively handing Harmony a call option on rising gold. On a reserves-in-the-ground yardstick, this looks like a giveaway, and a short-seller with a spreadsheet could make that case convincingly.

The counter-argument is that the spreadsheet measures the wrong thing. What AngloGold was really selling was not ounces but a risk profile. In one transaction it exited Eskom's grid, the deepest and most safety-intensive mining on the planet, the AMCU–NUM labour battleground, and the open-ended capital sink of keeping ultra-deep shafts alive. Its group-wide cost curve improved simply because the highest-cost, highest-risk operations were gone. Its fatality exposure fell. Its capital could be redeployed into mechanised, shallower, cheaper ore bodies elsewhere. Viewed this way, the low headline price was the whole point: AngloGold was paying — in forgone ounces — to be rid of a structural liability that the market would never reward it for carrying.

The result was one of the more startling facts in modern mining. A company whose very name evoked South African gold, whose corporate DNA traced back to a 1944 Witwatersrand producer, now had exactly zero mining operations in South Africa. It retained a corporate office in Johannesburg, and its shares still traded on the JSE, but the mines — the actual holes in the actual ground — were gone from the country entirely.

That created a peculiar and unstable situation. AngloGold Ashanti had removed the operational reason for the South African discount but still carried the structural one: a primary listing and legal home in Johannesburg. It had, in effect, done the hard, physical, irreversible work of leaving South Africa while still wearing the label that the market penalised. The obvious next question almost asked itself. If the mines were already gone, why was the company still, in the eyes of index funds and screens, a South African stock at all?

V. Shifting the Domicile: The 2023 Corporate Restructuring

The answer to that question arrived in 2023, and it was pure financial engineering — the corporate equivalent of changing not just your house but your passport. The theory being tested was blunt: if a company relocates its legal home and its primary listing to a premium market, will investors value it like the neighbours rather than like the place it came from?

On 25 September 2023, AngloGold Ashanti completed a corporate restructuring that reorganised the entire group under a newly created parent company, AngloGold Ashanti plc, incorporated under the laws of England and Wales and tax-resident in the United Kingdom.4 Simultaneously it moved the primary listing of its shares to the New York Stock Exchange, under the ticker AU, while the Johannesburg listing (ANG) and the Ghana listing were relegated to secondary status.4[^5] Over the following period the group's global headquarters shifted from Johannesburg to the Denver area — specifically Greenwood Village, Colorado — placing the company's leadership in the heart of the North American mining-finance ecosystem, a short flight from the analysts, funds and peers that set the sector's valuation benchmarks.4

The rationale, as management framed it, was about access and comparability. A NYSE primary listing opened the door to the world's deepest pool of capital and, crucially, to eventual eligibility for major US equity indices — the passive money that flows automatically into index constituents. It forced side-by-side comparison with US-listed gold majors rather than JSE-listed ones. Chief executive Alberto Calderon put the logic plainly at the time, describing the move as placing the company "alongside the industry's highest-valued gold companies."4 In other words, if you want to be valued like Newmont, stand next to Newmont on the same exchange.

But the neutral observer has to ask the harder question: did it actually work? And here the honest answer, as of mid-2026, is partly. Liquidity in the shares improved, the shareholder base broadened toward North American institutions, and on the Q4 2025 results call management pointed to "steady progress narrowing the rating gap relative to our North American peers," while conceding it was the product of a multi-year programme rather than a single act.3 What the re-domicile did not do was instantly conjure an Agnico Eagle multiple. Agnico, with its concentration of low-cost mines in Canada and Finland, still commanded a premium that AngloGold had not fully closed.

The share price itself tells the story of a re-rating that is real but incomplete. By mid-July 2026 the stock changed hands around $82, giving the company a market value near $41 billion — a dramatic advance from its lows, but well below the 52-week high above $129 it had touched earlier, and the shares had spent recent months trading below their own 200-day average even as the underlying business posted records.21 Gold equities are volatile and a single price point proves little, but the pattern is a useful corrective to any triumphalist reading: the market has rewarded the transformation, and it has also declined to fully hand over the premium multiple that the whole exercise was meant to unlock. The re-rating is a process with an uncertain endpoint, not an event that has already concluded.

The lesson embedded in that gap is important, and it cuts against the entire jurisdictional-arbitrage thesis if taken too far. Listing location can remove an artificial penalty — the reflexive discount that index rules and mandates slap on a JSE stock. It cannot manufacture the real thing that a premium multiple ultimately rewards: low costs, stable jurisdictions, predictable delivery and margins that hold up when the gold price falls. A New York ticker gets you into the room. It does not, by itself, win the argument. To win that argument, AngloGold needed someone to grind relentlessly on the operational side of the ledger — and in late 2021, that someone had already arrived.

VI. Management Credibility & Capital Allocation under Alberto Calderon

When Alberto Calderon took the chief executive's chair on 1 September 2021, he brought a résumé unusual for a gold company and, arguably, exactly the one the situation demanded.13 A Colombian-born economist with a PhD from Yale, Calderon had spent years in the senior ranks of BHP — running its aluminium, nickel and corporate-development arms and serving as chief commercial officer — before leading Orica, the world's largest maker of commercial explosives, as CEO.13 He was, in short, not a gold lifer steeped in the romance of the reef, but an industrial operator with a reputation for cold-eyed asset optimisation and a diversified-major's discipline about cost and capital.

The situation Calderon inherited was, by the standards of a company its size, unusually unsettled at the top. His predecessor as chief executive had departed abruptly in 2020 after a relatively short tenure, and the chief financial officer, Christine Ramon, had stepped in as interim CEO to steady the ship until a permanent appointment could be made.13 Leadership churn is itself a form of risk in a capital-intensive business where decisions play out over decades, and it had contributed to a perception among investors that the company's strategy could shift with its personnel. Part of Calderon's early mandate, then, was not merely operational but psychological: to convince a sceptical market that AngloGold would now say what it would do and then do it, quarter after quarter, regardless of who was in the chair. That is a harder thing to rebuild than a mine.

That background shaped a management style that comes through vividly on the company's earnings calls. Calderon is almost aggressively un-flashy. "We may become a little bit boring," he told analysts on the February 2026 call. "We are predictable. We want to meet guidance. We keep with full asset potential. We don't have a program of the month every year."3 In an industry notorious for over-promising exploration dreams and then quietly missing production targets, "boring and predictable" is a deliberate, and pointed, brand.

Crucially, the incentive structure was rebuilt to make that discipline personal. Under the group's remuneration framework, the CEO is subject to a Minimum Shareholding Requirement obliging him to build and hold shares worth 300% of net annual base salary throughout his employment — meaning management's own wealth rides on the share price he is trying to re-rate.14 The on-target variable pay is deliberately skewed toward equity rather than cash, with roughly two-thirds of the incentive delivered in shares, and the scorecard is weighted heavily toward the two things management insists it can control: operational delivery and cash generation.14 The design intent is to bolt the executive's fortunes to shareholders' and to blunt the temptation to chase headline growth at the expense of returns.

The capital-allocation record is where those incentives meet reality, and it has become the company's calling card. In early 2025 AngloGold adopted a dividend policy targeting a 50% payout of annual free cash flow, subject to keeping adjusted net debt below 1.0 times adjusted EBITDA — a leverage guardrail designed to protect the balance sheet through the commodity cycle.15 It is a policy management is evidently proud of; Calderon noted, with some satisfaction, that competitors had "copied it exactly," calling the imitation "a sign of flattery."3

In practice the company has paid out even more than the formula requires. For 2025 it declared total dividends of $1.8 billion, equivalent to about 62% of free cash flow, including a Q4 top-up that deliberately drew the year-end net cash position down toward zero.13 Calderon framed that as a statement of confidence — a signal that the business could pay out "substantially all of the cash we generate this year" and still fund its growth.3 The neutral reading is that this is genuinely shareholder-friendly capital allocation, but also that it is happening in the fattest part of the gold cycle, when a 45%-higher gold price is doing enormous heavy lifting; the discipline will be truly tested when prices fall.

Then there is the buyback. For much of 2025 management resisted repurchases, arguing that a $300 million top-up dividend made more sense than a token buyback. But in May 2026 the board changed tack, approving a proposed share-repurchase programme of up to $2.0 billion, funded by a record $1.2 billion of first-quarter free cash flow, and explicitly framed as aligning the company's capital-return toolkit with North American peers.16 Importantly — and contrary to some tellings — this was not part of the 2025 results; it was a 2026 decision, and as of mid-July 2026 it remained subject to a shareholder vote scheduled for 23 July 2026.1617 The signal management intends to send is conviction that the shares are still undervalued. The signal a sceptic hears is a company that spent years promising it would not do buybacks now proposing a very large one at a high gold price — a shift worth watching for consistency.

What ties the Calderon era together is a rebuilding of credibility through repetition: setting guidance, hitting it, and saying the same thing next quarter. On the 2025 scorecard, group gold production and sustaining capital landed within guided ranges, while costs came in only marginally above — and management was careful to attribute that overrun to gold-price-linked royalties rather than to operational slippage.3 Whether that consistency is a durable cultural change or a fair-weather feature of a bull market is the open question. To judge it, we need to open up the machine and look at the assets actually generating the cash.

VII. Inside the Engine Room: Assets & Segment Economics

Strip away the corporate restructuring and the listing venue, and a gold company is only ever as good as its rocks. AngloGold Ashanti's portfolio in 2026 is a study in deliberate rebalancing: an African core that throws off the bulk of the cash, wrapped around smaller, more mature operations in the Americas and Australia. By the end of 2025, management could point to a milestone it had chased for years — Tier 1 assets (its highest-quality, longest-life mines) now accounted for more than 70% of production and 80% of reserves.3

The African core

The anchor of the whole company is Geita in Tanzania, a world-class combination of open-pit and underground mining that produced 483,000 ounces in 2024 and remained one of the group's largest and most profitable single sources of gold.20 Geita's economics are enviable, but it illustrates the central tension of the African portfolio: profitability shadowed by policy risk. Tanzania has a history of abrupt regulatory and fiscal shifts in mining, and a mine this valuable is, by definition, a target for any government looking to capture a larger share of a soaring gold price.

Kibali, straddling the northeast of the Democratic Republic of Congo, is the portfolio's quiet aristocrat. AngloGold holds 45% of it, but does not run it — the mine is operated by Barrick Gold — and in 2024 it delivered 309,000 attributable ounces at costs that place it among the lowest of any Tier 1 mine in the industry.20 The rub is not the mining but the money: getting cash physically out of the DRC has been a persistent administrative grind. On the 2025 call, management noted pointedly that Kibali generated roughly half the free cash flow per ounce of the rehabilitated Obuasi, and welcomed the operator "finally" stepping up growth investment there.3 A superb, non-controlled, hard-to-repatriate asset is a genuine value driver and a genuine frustration at the same time.

Then there is Obuasi — the emotional and strategic heart of the story, and the clearest test of whether this management can actually fix a broken mine. The historic Ghanaian ore body was placed on care and maintenance in 2014 after illegal-mining invasions and structural decay overwhelmed it; a multi-year, multi-hundred-million-dollar redevelopment restarted it in 2020.20 The turnaround has been real but hard-won. In 2025 Obuasi produced 266,000 ounces, up 20% year on year, and generated an eye-catching roughly $1,300 of free cash flow per ounce — double Kibali's — with management guiding to more than 300,000 ounces in 2026 as a new "underhand drift-and-fill" mining method proved itself in the high-grade zones.3 After a decade of Obuasi being a byword for trouble, that is a meaningful reversal, though the technical proof-of-concept is still young enough that execution risk has not vanished.

Rounding out the African engine are Siguiri in Guinea and, since late 2024, Sukari in Egypt — the latter significant enough to warrant its own section below. Siguiri is instructive as a signal of ambition: management told analysts it is evaluating whether combining dormant pits in one block with a ramp-up in another could lift the mine into Tier 1 territory, an example of the "full asset potential" doctrine that runs through the whole portfolio.3 That doctrine is really an operating philosophy imported from Calderon's diversified-major background — the belief that most mines are run below their true capability, and that disciplined, systematic optimisation of throughput, recoveries and maintenance can extract meaningfully more value from assets already owned than from expensive new acquisitions. It is a claim the 2025 results partly substantiated, with management pointing to reserve additions across Geita, Obuasi, Iduapriem, Cuiabá and Kibali that replaced more than three times the year's depletion, at an average finding cost far below what ounces cost on the open market.3

The uncomfortable counterpoint, threaded through every African asset, is that owning great rocks is not the same as banking the cash they produce. Kibali's repatriation friction in the DRC is the sharpest example, but the theme generalises: value trapped behind a border, a tax dispute or an export rule is value an investor cannot spend. The whole African core, for all its low costs and long lives, is a portfolio where the geology is world-class and the jurisdictions are anything but — a tension the company manages continuously and can never fully eliminate.

The Americas and Australia

The secondary segments contribute the remaining slice of group value and, candidly, a good deal of the group's headaches. In Australia, Tropicana provides steady open-pit cash flow but has wrestled with extreme-weather disruption — a 2024 rainfall event dented productivity — and with the grade declines that eventually visit every maturing pit; Sunrise Dam produced below expectations in 2025.3 In Brazil, the historic Cuiabá and Serra Grande underground mines are complex, high-cost legacy assets; management has been actively pruning here, completing the sale of Serra Grande on 1 December 2025 to sharpen the portfolio's focus.3 There is also a genuinely lucrative oddity in Argentina: the Cerro Vanguardia operation, which alongside gold poured 3.7 million ounces of silver in 2025 and which management, after an aborted attempt to sell it, decided to keep because rising precious-metals prices made it too good to let go.3

The through-line across the engine room is a consistent philosophy: concentrate capital and management attention on a handful of large, long-life, mechanised African assets; treat the rest as cash-generative but non-sacred, to be optimised or sold. It is a coherent strategy, and the 2025 numbers suggest it is being executed with unusual discipline. But it also concentrates the company's fortunes in emerging-market jurisdictions — a concentration that the single largest deal of the Calderon era only deepened.

VIII. The $2.5 Billion Bet: The Centamin Acquisition (Nov 2024)

For a management team that talks constantly about discipline and about how hard it is to pay a premium and still add value, the boldest move of the Calderon era was a full-blown takeover. In September 2024, AngloGold Ashanti and Centamin plc announced a recommended acquisition, and on 22 November 2024 the deal closed after approval by the Royal Court of Jersey.1012 The terms offered Centamin shareholders 0.06983 new AngloGold shares plus $0.125 in cash for each Centamin share, a structure that valued the target at roughly $2.5 billion at announcement and settled at a final consideration near $2.2 billion — about $148 million in cash and some $2.08 billion in stock — leaving former Centamin holders owning around 16.4% of the enlarged company.1011 In plain terms, AngloGold diluted its existing owners by roughly a sixth to buy a single mine.

That mine was the point. Sukari, in Egypt's Eastern Desert, is the country's largest and first modern gold mine, a producer of roughly 450,000 ounces a year that had poured more than 5.9 million ounces since production began in 2009.10 Overnight it lifted AngloGold's annual output above three million ounces and added a large, low-cost, cash-generative Tier 1 asset to the African core.10 Strategically, the logic was pure Calderon: rather than gamble on speculative, exploration-stage ounces, buy an asset that is already producing cash today, then apply the group's operating playbook to squeeze more out of it.

Did they overpay? The bull case is that they conspicuously did not. Centamin came with a pristine, effectively debt-free balance sheet and a pile of cash, and the premium over Centamin's recent trading was modest by takeover standards.11 The real test, though, is what the asset does inside the new owner. Here the early evidence has been striking. Sukari delivered a record year in 2025 in its first full year of consolidation, and management claimed that, after stripping out the cash acquired and the proceeds from selling off Centamin's non-core exploration projects, Sukari generated close to a third of its net purchase price in cash in year one alone — with an identified pipeline to expand underground mining from 1.2 million to 2.3 million tonnes of higher-grade ore.3 If those figures hold, this looks less like an overpay and more like a well-timed grab of a mispriced asset.

The integration itself offers a window into how this management thinks. Centamin had been a single-asset company with a scattering of exploration interests, and AngloGold moved quickly to shed what did not fit — selling off Centamin's West African exploration projects, including the ABC and Doropo assets, and using the proceeds, together with the cash that came on Centamin's balance sheet, to shrink the effective purchase price.3 It then turned the "full asset potential" apparatus loose on Sukari, identifying a pipeline of improvements from a larger underground operation to a small heap-leach project and better plant recoveries. The early operating proof was concrete: Sukari produced 246,000 ounces in the first half of 2025, up from the prior year, evidence that the asset's performance was consistent rather than a one-off flattered by a good quarter.22 For a management team whose entire pitch is that it buys cash flow and then improves it, Sukari's first eighteen months were close to a best-case demonstration — which is exactly why the risks deserve equal airtime.

But the neutral ledger has a debit column, and it is labelled concentration. Before Sukari, AngloGold's cash flow already leaned heavily on developing-nation Africa — Tanzania, the DRC, Ghana, Guinea. Adding Egypt piled another emerging-market, single-country dependency onto the stack. Egypt brings its own currency, its own fiscal pressures, and its own political weather. For the conservative North American funds AngloGold is courting with its NYSE listing, every additional emerging-market ounce is a reason to demand a slightly higher risk premium — which is precisely the discount the whole strategy is trying to eliminate. The Centamin deal, in other words, made the operational story stronger and the re-rating story more complicated at the same time. To square that circle, management needed a growth engine in a jurisdiction that North American investors would applaud rather than discount. It found one in the Nevada desert.

IX. The Nevada Growth Engine: The Arthur Gold Project

Every gold executive dreams of the same thing, and Calderon named it out loud on the 2025 results call: "The holy grail for any gold company is a Tier 1 discovery in a low-risk jurisdiction with long life and strong growth potential."3 For AngloGold, that dream has a location — the Beatty district of southern Nevada — and a story that reads like a prospecting fairy tale with a corporate-strategy twist.

It began, as these things do, with an unfashionable idea. Beginning around 2014, in a stretch of Nevada's Walker Lane that the industry largely considered mature and picked-over, a generative exploration effort — a partnership involving Renaissance Gold and Callinan Royalties, with AngloGold executing the targeting and drilling — chased a geological thesis most had dismissed.19 It paid off with the discovery first of the Silicon deposit and then, more importantly, the larger Merlin deposit nearby. In March 2026 the exploration teams behind the find were awarded the Thayer Lindsley Award at the PDAC convention in Toronto — mining's most prestigious recognition for an international discovery — for what the industry judged one of the most significant greenfield gold discoveries in the United States in over a decade.19

Recognising what it had, AngloGold spent several years consolidating the entire district around the find — buying out neighbouring positions from Corvus Gold and Coeur Mining in 2022 and, later, Augusta Gold in 2025 — so that Silicon and Merlin sat inside one contiguous, company-controlled system, now rebranded the Arthur Gold Project.3 Management has been candid that these bolt-ons were the difference between a good deposit and a district: "that really allowed us to consolidate what is probably the most important discovery and land position in Nevada in decades," Calderon told analysts.3

The scale disclosed at the end of 2025 justified some of the excitement. AngloGold declared a first-time Probable Mineral Reserve of 4.9 million ounces at Merlin, calculated conservatively at a $1,950 gold price — 88 million tonnes at 1.75 grams per tonne — with a much larger surrounding resource base still to convert.318 The prefeasibility study envisaged a conventional open-pit mine feeding an oxide mill, producing around 4.5 million ounces over an initial nine-year life at an average of roughly 500,000 ounces a year (and up toward 800,000 ounces in the early years), at cash costs near $780 an ounce and all-in sustaining costs around $950 — well below the group average — for an initial capital outlay of about $3.6 billion.318 Calderon's pitch was that the geology is refreshingly simple: "No autoclaves, no double refractory ore… it's just a very simple project," largely oxide material amenable to conventional processing rather than the technically fraught refractory ores common elsewhere in Nevada.3

Arthur is not, in fact, the first gold AngloGold expects to pour in Nevada. That distinction belongs to the smaller North Bullfrog project, sitting on the same consolidated land package, which management has slotted in as the nearer-term entry point — with construction capital stepping up in 2027 and roughly $320 million earmarked for it that year, ahead of the far larger Arthur build.3 The sequencing matters strategically. North Bullfrog lets the company establish operating infrastructure, permitting relationships and a physical presence in the district on a manageable scale before committing $3.6 billion to Arthur, effectively de-risking the flagship by learning the jurisdiction first. It is a sensible, staged approach — build the on-ramp before the highway — and it says something about a management team that talks incessantly about phasing capital "prudently" rather than betting everything on a single mega-project.

That last point is the crux of the investment case. Nevada is the premier mining jurisdiction on Earth from a country-risk standpoint — exactly the kind of place a North American fund is happy to pay up for. A large, high-grade, low-cost, conventionally processed ore body there is the antidote to the emerging-market concentration that Centamin deepened. It is, potentially, the asset that finally lets AngloGold argue for a peer multiple on its own merits rather than on its listing address.

But the neutral investor must apply a red pen to the timeline, because this is where management rhetoric and management's own caveats diverge from the tidiest version of the story. The prefeasibility economics were released in early 2026, not left as a future promise. Yet the path to production is long and substantially outside the company's control. On the results call, executives declined to commit to permitting dates, saying only that the fuller feasibility study would run through Q4 2027, that federal permitting would begin in Q1 2027, and that they hoped for a construction decision before the end of the decade with first production in the early 2030s.3 Local opposition over water use in the Nevada desert is a live issue that management says it is actively negotiating.3 In short: the reserve is real and the jurisdiction is excellent, but the cash is the better part of a decade away, and any slip in permitting or blowout in that $3.6 billion capital estimate would push it further still. Optionality, not yet delivery. That distinction between what is proven and what is promised is exactly what the strategic frameworks in the next section are built to expose.

X. The Strategic Playbook: Porter's 5 Forces & Hamilton Helmer's 7 Powers

Step back from the individual mines and ask the harder question a long-term investor cares about: does AngloGold Ashanti actually possess a durable competitive advantage, or is it simply a leveraged bet on the gold price with better-than-average management? Two frameworks help stress-test the answer.

Hamilton Helmer's 7 Powers

Helmer's framework asks which of seven structural "powers" a business genuinely holds. For a gold miner, the honest audit is sobering in places and encouraging in others.

The clearest power AngloGold holds is the Cornered Resource. A high-grade ore body in a specific place cannot be replicated by a competitor with more capital or cleverness — there is only one Merlin in the Beatty district, one Sukari in Egypt's Eastern Desert, one Kibali in the DRC. These are geographically unique, scarce assets, and ownership of them is a real and defensible edge. The Arthur discovery is the purest example: a scarce Tier 1 ore body in the world's best mining jurisdiction, assembled into a controlled land position that no rival can now enter.

There is a moderate case for Scale Economies. A three-million-ounce producer buys mining fleets from Caterpillar and Komatsu, and consumables like cyanide, reagents and grinding media, at volumes that command better terms than a junior miner can. It can also afford centralised technical and exploration expertise — and management argues, plausibly, that its in-house exploration team is a genuine differentiator, having added around 23 million ounces of reserves over recent years at an average finding cost near $47 an ounce, far cheaper than buying ounces through M&A.3 That is a real, if bounded, advantage.

And then comes the wall that no gold miner can climb: on the thing that matters most — price — AngloGold has no power at all. Gold is a globally fungible commodity sold into a deep spot market. The company has no pricing power, no switching costs, no ability to charge a premium for its ounces versus anyone else's. It is a pure price-taker. This is the single most important fact about the entire business, and it reframes everything: because AngloGold cannot influence its revenue per ounce, the only variable it controls is cost. In a commodity with no pricing power, competitive advantage is defined almost entirely by position on the cost curve. That is why management's monomania about "full asset potential," cost discipline and Tier 1 mix is not corporate boilerplate — it is, quite literally, the only game available.

Set against its chosen peer group, AngloGold's position comes into sharper relief. Agnico Eagle, the company AngloGold most wants to be valued like, earns its premium the old-fashioned way — a concentration of mines in Canada and Finland, jurisdictions that carry almost no sovereign risk and that investors will pay up for precisely because the cash flow is boringly safe. Newmont, the world's largest producer, offers scale and a spread across the Americas, Africa and Australia. Barrick sits somewhere in between and is, tellingly, AngloGold's partner as well as its rival — it operates the Kibali mine in which AngloGold holds 45%, a reminder that in this industry today's competitor for a Tier 1 deposit is tomorrow's joint-venture operator.20 The strategic gap AngloGold is trying to close is not primarily about size or even cost — its Kibali and Sukari ounces are cost-competitive with anyone's — but about jurisdictional quality. That is why Nevada matters out of all proportion to the ounces it will initially add: it is the one lever that can shift the company's average risk profile toward the developed-market end of the spectrum where the premium multiples live. Everything else being equal, an ounce mined in Nevada is worth more to this company's valuation than an identical ounce mined in Guinea, even if it is not worth more in cash.

Porter's Five Forces

Porter's lens largely reinforces the picture. The threat of new entrants is very low: building a gold major requires billions in capital, decade-long permitting slogs, and the geological luck of finding a Tier 1 deposit in the first place — barriers that protect incumbents handsomely. The threat of substitutes is low but not zero: gold's monetary and safe-haven role has survived the rise of cryptocurrencies, and central-bank and investor demand has, if anything, strengthened, though a sceptic would note that gold's "store of value" status is a matter of collective belief rather than industrial necessity. Buyer power is essentially nil, because there is no negotiation — ounces flow into an infinitely liquid global market at the prevailing price.

The forces that bite are on the supply and rivalry sides. Supplier power is high: specialised equipment makers, chemical suppliers, global diesel and power markets, and skilled (often unionised) mining labour all exert real pressure on input costs — precisely the pressure visible in 2025's cost inflation. And industry rivalry, while absent at the point of sale, is ferocious in the two places that determine long-term survival: the competition to acquire the world's dwindling stock of Tier 1 deposits, and the competition for scarce technical talent. The Centamin takeover and the Beatty land grab are both expressions of that rivalry.

The synthesis for an investor is clean. AngloGold's advantages are real but narrow: cornered resources and some scale, deployed in a business with zero pricing power and high supplier pressure. It cannot win by being clever about price; it can only win by owning better rocks and running them at lower cost than the next miner. Everything in the bull and bear case therefore comes down to whether it can keep doing exactly that — which is where the stress test begins.

XI. The Stress Test: Bull vs. Bear Case & Risks

Having established that AngloGold can only win on cost and asset quality, the investor's job is to war-game the specific ways the case could break — and the specific evidence that it is holding.

The material risk radar

The most immediate pressure is input-cost inflation. Group all-in sustaining costs rose from $1,611 an ounce in 2024 to $1,709 an ounce in 2025, an increase management was careful to attribute largely to factors outside its control — chiefly royalties that rise automatically with the gold price, plus fuel and wage inflation.2 The company's defence is that its controllable cash costs have been essentially flat in real terms since 2021, which, if accurate, would make it the only major to achieve that; on the 2025 call it claimed a fourth consecutive year of cash-cost growth running below inflation-plus-royalties.3 The bear's retort is that royalty-driven cost inflation is still real cash out the door, and that a company enjoying a 45%-higher gold price should be careful about waving away rising costs as merely "uncontrollable."

The second and larger risk is geopolitical and sovereign exposure. With South Africa gone and Nevada years from production, AngloGold's cash flow today depends overwhelmingly on a handful of developing nations — Tanzania, Guinea, the DRC and now Egypt. Each brings the standing threat of tax changes, export restrictions, cash-repatriation friction and outright resource nationalism, especially with gold at record prices tempting every host government to reach for a bigger share. On the call, management acknowledged "constructive conversations" with Ghana over a potential royalty change without pretending the outcome was settled.3 This is the fundamental irony of the whole re-domicile: the company escaped the South African discount only to concentrate its actual operating risk in an even broader set of frontier jurisdictions.

The third is Nevada execution and permitting. The Arthur growth thesis, as established, is real but distant, and it rests on a federal permitting process management repeatedly refused to put dates on, plus a $3.6 billion capital estimate carrying prefeasibility-level margins of error and live local opposition over water.3 Any material delay or overrun directly impairs the growth half of the story.

Myth versus reality

Three consensus narratives deserve a fact-check. The first myth is that the NYSE move "solved" the valuation problem. Reality: it removed a structural, index-driven penalty and improved liquidity, but the residual discount to the highest-rated North American peers persists, and management itself frames the re-rating as an unfinished, multi-year project rather than a completed one.3 Relocation was necessary, not sufficient.

The second myth is that AngloGold is now a "de-risked," developed-market company because it left South Africa and is building in Nevada. Reality: as of 2026 essentially all of its producing cash flow still comes from emerging-market Africa, and Nevada is a promise dated to the early 2030s. On the risk that actually matters — where the money is earned today — the company is arguably more concentrated in frontier jurisdictions than it was when it still had South African production.

The third myth is that the record 2025 numbers prove a structural transformation. Reality: they prove operational competence layered on top of a 45% jump in the gold price, and disentangling the two is the single hardest analytical task in owning this stock. The honest test of the transformation will come not in a bull market but in the next downcycle, when the gold price stops doing the heavy lifting and only the cost curve and the balance sheet remain.

The activist's brief

A short-seller or activist building a bear file would not struggle for material, and a fair-minded investor should hear the argument even while weighing the rebuttals. The capital-allocation critique writes itself: a company that spent years insisting buybacks did not make sense has proposed a $2 billion repurchase at a cycle-high share price, funded by cycle-high cash flows — precisely the pattern of buying high that destroys value if gold reverses. The governance and portfolio critique would flag the sheer jurisdictional complexity — nine or ten assets spread across some of the world's more challenging countries — as inherently hard for outside investors to monitor, and would press on cash trapped in the DRC and the fiscal negotiations underway in Ghana. The narrative-consistency critique would note that a management team selling "boring and predictable" has, in the space of two years, executed a $2.2 billion transformational acquisition, consolidated an entire Nevada district, and reversed course on buybacks — bold moves that are not obviously "boring," however well reasoned each was individually. None of these points is necessarily fatal. But an investor who cannot articulate the bear case has not finished the work.

The three KPIs that actually matter

For all the narrative, an investor tracking this company can watch a very short list of numbers:

- Group all-in sustaining cost per ounce. In a business with no pricing power, AISC is the single truest barometer of competitive health. It is the number that determines whether AngloGold sits comfortably or precariously on the cost curve when gold eventually falls.

- Gold production versus guidance. Not the absolute figure so much as the reliability — whether management keeps delivering inside the ranges it set, because the entire re-rating case rests on rebuilt trust, and a single credibility-shattering miss would undo years of "boring and predictable."

- Free cash flow and the net-cash position. This is the fuel for the 50%-plus dividend and the proposed $2 billion buyback, and the clearest evidence of whether the portfolio is converting a high gold price into real, distributable cash rather than merely accounting profit.

Bull versus bear

The bull case writes itself from the 2025 results: a portfolio delivering record cash, a management team hitting guidance and returning capital aggressively, a rehabilitated Obuasi and a record-breaking Sukari validating the operational playbook, a genuine Tier 1 growth option in Nevada, and a slowly narrowing valuation gap — all levered to a gold price at historic highs. If Nevada comes through and the discount to Agnico and Newmont keeps closing, the re-rating thesis is vindicated.

The bear case is equally coherent, and it lives in the same facts read differently. Much of 2025's brilliance is a gold-price phenomenon that flatters every miner and will reverse; costs are quietly rising; the operating base is a concentrated bet on frontier-market politics; the marquee growth project is expensive, years away and outside the company's control on permitting; and the NYSE listing has not, so far, fully delivered the peer multiple that justified the whole upheaval. An activist reading the same page would question whether a company that promised buyback discipline should be launching a $2 billion repurchase at cycle-high prices, and whether the emerging-market concentration will ever let the discount fully close regardless of where the shares trade.

The truthful conclusion is that both cases are live, and the resolution depends on variables — the gold price, African fiscal policy, Nevada permitting — that management does not control. What management does control, it has so far controlled well. Whether that is enough is the question the epilogue leaves open.

XII. Epilogue & Key Takeaways

Return one last time to those two maps. The distance between them — a South African deep-reef champion in 2004, a Denver-headquartered, NYSE-listed global producer with nothing left in South Africa in 2026 — is the distance a company can travel when it decides that its own origins have become a liability the market will never forgive.

The deeper lesson of AngloGold Ashanti's journey is that a business can be trapped not only by bad assets but by its identity. Its mines in Tanzania and the DRC were never the problem; the flag on its stock certificate and the physics of its home orebody were. Management's response was radical and, on the operational side, largely successful: prune the portfolio down to the deepest liability, sever it, migrate the listing to friendlier capital, and rebuild the growth base in the desert of Nevada rather than the reefs of Johannesburg. That took a kind of institutional courage — a willingness to sell the deepest mine on Earth for a modest sum and to abandon the country in the company's own name — that few incumbents ever muster.

But the story is not finished, and the neutral verdict must stay open. AngloGold has proven it can escape an artificial discount and run good mines with discipline. It has not yet proven that it can manufacture a premium — that listing address and operational competence can fully substitute for the low-cost, low-risk jurisdictional profile that its most admired peers enjoy by geological accident. The gap to Agnico Eagle is narrower than it was, but it is still there, and it is a daily scorecard on whether the entire thesis is right. The next chapter will be written not in boardrooms or on exchanges but underground and in permitting offices — at Obuasi's high-grade zones, in Sukari's expanding decline, and above all in the slow bureaucratic march toward first gold at Arthur. For a company that spent twenty years shifting its golden anchor, the final question is simply whether the new ground holds.

References

-

AngloGold Ashanti Q4 and Year Ended 31 December 2025 Earnings Release and Dividend Declaration — Business Wire, 2026-02-19 ↩↩↩

-

AngloGold Ashanti plc — Form 6-K, Q4 and FY2025 Earnings Release — U.S. Securities and Exchange Commission, 2026-02-20 ↩

-

AngloGold Ashanti Q4 & Full-Year 2025 results and earnings-call commentary — AngloGold Ashanti plc (Form 6-K), 2026-02-20 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

AngloGold Ashanti plc Completes the Primary Listing of Its Ordinary Shares on the NYSE and Commences Trading — Business Wire, 2023-09-25 ↩↩↩↩↩

-

Exploring the World's Top Ten Deepest Mines — Mining Technology ↩↩

-

140 Years of Mining the Witwatersrand Basin — SRK Consulting ↩

-

AngloGold Ashanti Ltd — Form 20-F FY2019 (company history) — U.S. Securities and Exchange Commission, 2020 ↩

-

AngloGold Ltd — Form 6-K FY2004 (Ashanti Goldfields merger) — U.S. Securities and Exchange Commission, 2004 ↩↩↩

-

Harmony increases life of mine and adds quality ounces by acquiring Mponeng and Mine Waste Solutions — Harmony Gold Mining Company, 2020 ↩↩

-

AngloGold Ashanti Gains Jersey Court Approval for Centamin Buyout — Zacks Equity Research, 2024-11-22 ↩↩↩↩

-

Slaughter and May is advising Centamin plc on the recommended acquisition by AngloGold Ashanti plc — Slaughter and May, 2024-09-10 ↩↩

-

Recommended Acquisition of Centamin plc by AngloGold Ashanti — London Stock Exchange, 2024-09-10 ↩

-

AngloGold Ashanti — Form 6-K, appointment of Alberto Calderón as CEO — U.S. Securities and Exchange Commission, 2021-07-06 ↩↩↩

-

AngloGold Ashanti plc — Form 20-F FY2025 (remuneration and minimum shareholding requirement) — U.S. Securities and Exchange Commission, 2026 ↩↩

-

AngloGold upgrades payout policy to 50% of free cash flow — Miningmx, 2025-02-19 ↩

-

AngloGold Ashanti Q1 (31 March 2026) Earnings Release and Dividend Declaration — Business Wire, 2026-05-08 ↩↩

-

AngloGold Ashanti Announces Date for General Meeting of Shareholders in Relation to Proposed Share Repurchase Programme — Business Wire, 2026-06-12 ↩

-

AngloGold Ashanti Builds on Award-Winning Discovery, Advancing Arthur Gold Project in Nevada with First-Time 4.9Moz Mineral Reserve and Robust PFS Economics — Business Wire, 2026-03-26 ↩↩

-

PDAC announces 2026 Awards recipients — Prospectors & Developers Association of Canada, 2025-11-04 ↩↩

-

AngloGold Ashanti plc UK Annual Report 2024 — U.S. Securities and Exchange Commission, 2025 ↩↩↩↩

-

AngloGold Ashanti plc — Form 6-K, Q2 and H1 2025 Earnings Release (Sukari production) — U.S. Securities and Exchange Commission, 2025 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube