Acciona Energías Renovables: Spain's Pure-Play Renewables Pioneer

I. Introduction: The Construction Giant's Clean Energy Metamorphosis

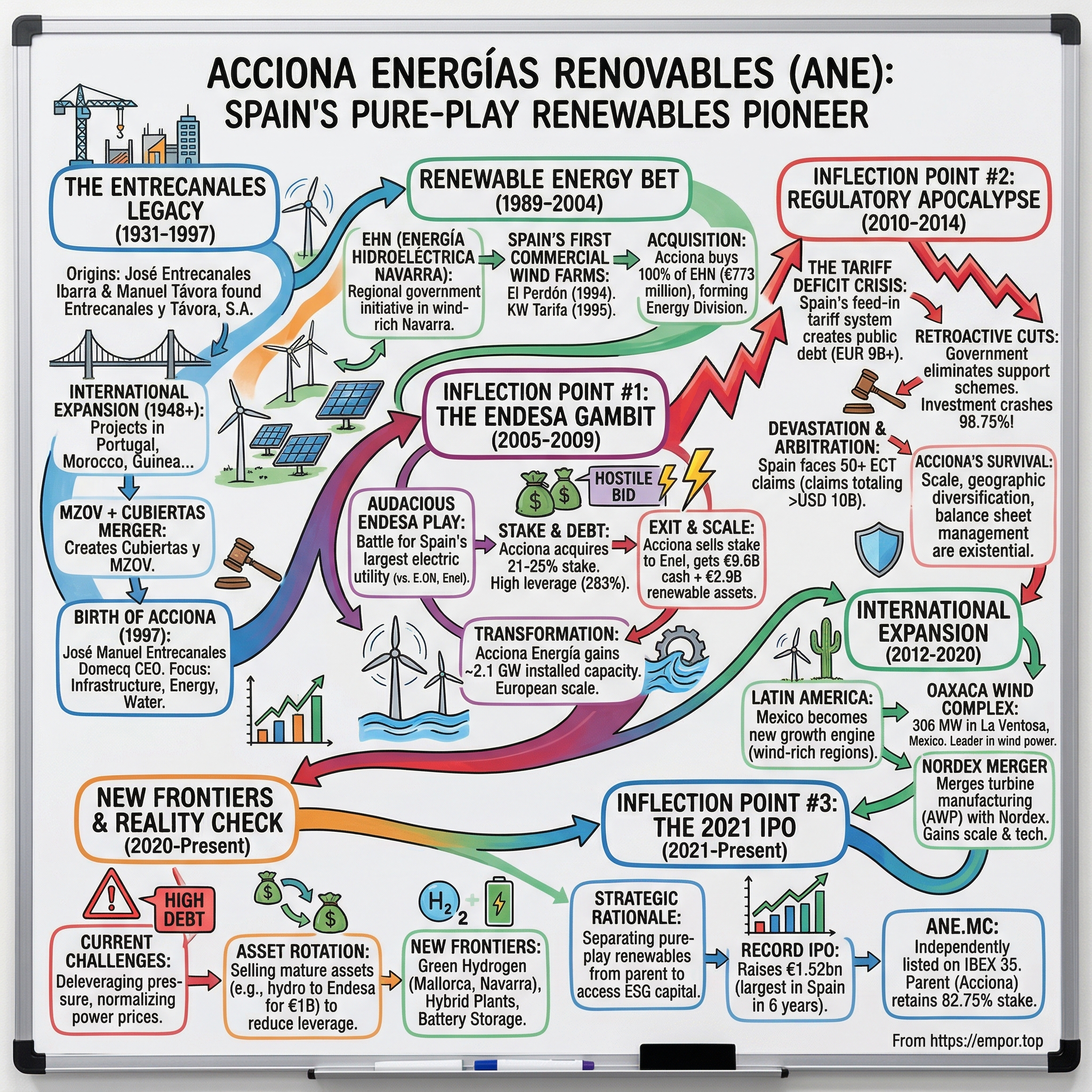

In the summer of 2021, as the world was emerging from pandemic lockdowns and the European Union was finalizing its Green Deal investment plans, something unusual happened on the Madrid Stock Exchange. A renewable energy company with roots in a century-old construction dynasty raised €1.5 billion in Spain's largest IPO in six years—not by selling technology dreams or promising future disruption, but by offering something far more tangible: 10.7 gigawatts of operational wind turbines and solar panels spread across 20 countries.

Corporación Acciona Energías Renovables, trading under the ticker ANE.MC, today commands a market capitalization of approximately €7.7 billion and carries an enterprise value of €12.5 billion. The company sits at an intriguing inflection point—small enough that it flies under the radar of most global investors, yet large enough that it operates one of the most geographically diversified renewable portfolios in Europe.

Acciona Energía specializes in renewable energy as a subsidiary of the ACCIONA Group, focusing exclusively on the development, construction, operation, and maintenance of renewable energy projects without any legacy in fossil fuels. As of the first half of 2025, it manages a total installed capacity of 15.1 GW across wind, solar photovoltaic, hydroelectric, and other technologies, with operations in 24 countries on five continents.

The central question of this analysis: How did a side project of a Spanish construction company become one of Europe's largest pure-play renewable energy platforms? And what does its tumultuous journey through regulatory catastrophe, opportunistic M&A, and strategic spinoff teach us about navigating the energy transition?

The Acciona Energía story unfolds across four pivotal chapters: the Entrecanales family's century-long construction legacy, the discovery of wind energy in Navarra, the audacious Endesa utility battle that transformed the company's scale, and the regulatory apocalypse that nearly destroyed Spain's renewable industry—yet ultimately strengthened those who survived.

This is a case study in regulatory arbitrage (both the rewards and catastrophic risks), family dynasty capitalism, and the art of using public market spinoffs to unlock value trapped inside diversified conglomerates. For investors evaluating the European energy transition, Acciona Energía offers a lens into how local expertise can scale globally—and why geography matters as much as technology in the renewables business.

II. The Entrecanales Legacy: From Civil Engineering to Conglomerates (1931–1997)

Origins: Building Post-War Spain

The story of Acciona Energía begins not with solar panels or wind turbines, but with concrete, steel, and the ambition of a Basque engineer determined to build modern Spain.

José Entrecanales Ibarra was born in Bilbao on December 16, 1899. Son of José Entrecanales Pardo, a pediatric doctor, he moved to Madrid to study civil engineering at the School of Roads, Canals and Ports. The selection process required a difficult entrance exam, which Entrecanales passed after two years of preparation. In 1917, at just 18 years old, he began his engineering studies, which he completed in January 1924 as the top student of his class.

This academic excellence proved foundational to everything that followed. Entrecanales didn't just want to be an engineer—he wanted to build a company that could reshape Spain's infrastructure landscape.

On March 11, 1931, José Entrecanales Ibarra, a civil engineer from Bilbao, and Manuel Távora, an entrepreneur from Seville, founded Entrecanales y Távora, S.A. This company was at the forefront of engineering projects at the time, developing railway lines in the 1940s, works for the Avilés steel plant, the construction of dams in the 1960s (including the Almendra dam, the highest in the world at the time), and nuclear power plants and the Redia road plan in the 1970s.

The company's early projects included the remodeling of the San Telmo Bridge in Seville, designed to preserve the view of the Golden Tower as recommended by King Alfonso XIII, and construction on the Cádiz pier. In 1948, Entrecanales y Távora signed its first contract outside Spain, undertaking projects in Portugal, Morocco, and Equatorial Guinea.

The international expansion was deliberate. Since 1948, the company was setting up operations abroad—first in Morocco and Portugal, then developing such important projects as the EUROLEP Project in France and Switzerland, the Uranium Enrichment Plant in Tricastin (France), bridges over the Paraguay River in Asunción, the Paute Hydroelectric Power Plant in Ecuador, the Metro of Caracas in Venezuela, Reforma Park Center in Mexico City, and the Cairo Thermal Power Plant in Egypt.

The Other Half: MZOV and Cubiertas

The company that would eventually become Acciona was actually a merger of two construction dynasties. Understanding both sides helps explain why the merged entity had the financial firepower and ambition to diversify into renewable energy.

MZOV (Compañía de los Ferrocarriles de Medina del Campo a Zamora y de Orense a Vigo) was a railway company originally covering routes connecting Galicia with central Spain. After being awarded several key railway lines, the company reinvented itself as a leading Spanish construction firm.

Meanwhile, Cubiertas y Tejados, S.A. was founded in 1916 specializing in roofing but expanded into broader industrial construction. Fifty years later, in 1966, it merged with MZOV to become Cubiertas y MZOV, S.A.

José Entrecanales married María de Azcárate Flórez, with whom he had five children: Delfina, Cruz, José María, Juan, and Teresa. On February 12, 1990, at ninety years old, José Entrecanales Ibarra died in Madrid.

He had built an authentic business empire, which he left in the hands of his two sons, José María and Juan Entrecanales de Azcárate, and which today is led by one of his grandsons, José Manuel Entrecanales Domecq.

The Birth of Acciona

The 1997 merger wasn't just consolidation—it was transformation.

José Manuel Entrecanales Domecq, son of José María Entrecanales de Azcárate and grandson of the founder, became President, and Juan Ignacio Entrecanales Franco, son of Juan Entrecanales de Azcárate, became Vice President. Together, they guided the company through a transformation focused on three key pillars: infrastructure, energy, and water.

The new CEO brought a distinctly different background to the family business. José Manuel Entrecanales Domecq, born January 1, 1963, began his career as an investment banker at Merrill Lynch in New York and later London starting in 1985. He studied Economics at the Complutense University of Madrid and moved to Acciona in 1991.

In 2004, he succeeded his late father as chairman and CEO of Acciona. Entrecanales has been highlighted as a key leader of a new generation of Spanish businessmen "shaped by family roots but identifying fully with modernisation."

As CEO of Acciona, José Manuel Entrecanales has transformed the construction and engineering company into a global infrastructure, energy and water services company with over 50,000 employees and presence in 52 countries.

The vision was clear: construction was cyclical and commoditized. Energy and water offered recurring revenue streams and exposure to structural growth themes. But how does a construction company develop renewable energy expertise? The answer lay 400 kilometers north of Madrid, in the wind-swept hills of Navarra.

III. The Renewable Energy Bet: Navarra's Wind Pioneers (1989–2004)

EHN: The Hidden Gem

If you want to understand how Spain became an early renewable energy leader, you need to understand the autonomous region of Navarra. Nestled against the Pyrenees with consistent wind patterns and a regional government obsessed with energy independence, Navarra became the unlikely cradle of Spanish wind power.

Energía Hidroeléctrica Navarra, S.A. (EHN) was founded in 1989, and acquired 15 years later by ACCIONA, forming the foundation of its Energy Division. EHN started out building and acquiring a number of hydro plants in the region of Navarra before expanding into other renewable energy technologies.

The main driving force behind EHN was the regional government's determination to reduce its near full dependency on electricity supplies from outside the region. Just under half of EHN was publicly owned by the regional government's development agency, Sociedad de Desarrollo de Navarra (Sodena), and regional bank Caja de Ahorros de Navarra, with 38% and 10%, respectively.

Navarra's focus on renewable energy sources mushroomed from modest beginnings. In the early 1990s, the regional authorities installed small hydraulic generators along rivers in a region which then did not produce any electricity at all. The regional autonomous government and private shareholders set up Energía Hidroeléctrica de Navarra (EHN), which in 2000 was awarded "world's best renewable energy firm" by the Financial Times.

Think about that for a moment: a regional utility from a Spanish province of 600,000 people was named the world's best renewable energy company. This wasn't just luck—it was execution.

Spain's First Commercial Wind Farms

In December 1994, the first six wind turbines were installed in the El Perdón wind farm, situated on its namesake mountain range, just 12 kilometers from the city of Pamplona. Each turbine had a capacity of 500 kilowatts and a hub height of 40 meters, marking the company's entry into wind energy. Almost at the same time, in early 1995, the KW Tarifa wind farm entered service, the two facilities being the first commercial wind farms in Spain.

Company spokesman José Arrieta recalls how EHN's first step into wind power was to take windforce measurements at 72 points across the region, at altitudes ranging from 700 to 1,100 meters. In 1990, EHN started wind measurements in Navarra. By 1993 these readings had pinpointed such rich wind resources that within a year the company had outlined a 100 MW wind development plan for the region—seen by industry insiders at the time as overly ambitious.

An independent opinion survey carried out in March 1995 by the consultancy company CIES revealed that 85% of the people in Pamplona and the surrounding area had a positive opinion on the wind farm, with only 1% against it. Considerable efforts had previously been made to explain the benefits of wind power to political and social stakeholders and the media, and this played a major role in society's acceptance of an installation built on one of the most popular leisure areas near the capital city of Navarra.

The social license strategy was remarkable for its time. Rather than hiding turbines in remote locations, EHN deliberately placed them near population centers to normalize the technology.

EHN chose Vestas of Denmark to be its turbine supplier for its Navarra plan, but it preferred not to simply import turbines. Instead, the company insisted that the implementation of the plan also have extensive industrial benefits for the region. One of Spain's leading aeronautical manufacturers, Gamesa, was keen to enter the wind industry. EHN's need for turbines was Gamesa's way into the market.

Prior to the installation of the Vestas El Perdón demonstration plant of six 500 kW units, Gamesa Eólica was created to build Vestas wind turbines in Spain. Gamesa dominated the new company with a 51% share, followed by Vestas (40%) and Sodena (9%). Shortly after the first phase of El Perdón came online in December 1994, EHN signed up for 181 Gamesa Eólica turbines worth EUR 72 million, then the world's largest ever single turbine contract.

This partnership catalyzed an entire Spanish wind industry. Gamesa would eventually become one of the world's largest turbine manufacturers before merging with Siemens.

Early Solar Ambitions

EHN wasn't just a wind company. Connected to the grid in 2001, the solar plant near Tudela was the largest in Spain at the time, with a peak capacity of 1.2 MWp.

The company was also building its own turbine manufacturing capability. To manage the entire value chain in the wind energy sector, the company opened its first wind turbine production plant in 2003 in Barásoain (Navarra), using in-house technology. The plant began series production of the AW1500 turbine with a nominal capacity of 1.5 MW.

The Acquisition

The acquisition unfolded in stages. Spanish industrial group Acciona became 100% owner of wind plant developer Corporación Energía Hidroeléctrica de Navarra (EHN) after buying the remaining 10.42% it did not already own. Acciona paid EUR 83.5 million to Caja Navarra, a semi-public savings bank, for the last piece of the formerly independent renewable energy company. It was the third chunk of EHN bought by Acciona since it became 50% owner of the wind company in 2003.

The latest acquisition followed October's purchase of 39.58% of EHN from the regional government's industrial holding company, Sodena. In all, Acciona spent EUR 773 million on buying EHN. The company then operated around 600 MW of wind capacity. In addition to Acciona's shares in other wind concerns—mainly the 180 MW developed and operated by wind affiliate Alabe—the group now owned 842 MW of online wind power plant.

For €773 million, Acciona had acquired not just megawatts, but expertise—the institutional knowledge of building and operating wind farms profitably, relationships with turbine suppliers, and a pipeline of development projects. This capability would prove invaluable when the next opportunity emerged.

IV. Inflection Point #1: Spain's Feed-in Tariff Boom & The Endesa Gambit (2005–2009)

The Golden Age of Spanish Renewables

Spain in the mid-2000s was the Wild West of renewable energy investment. The government's Royal Decree 436/2004 created feed-in tariffs that guaranteed fixed prices for renewable electricity—regardless of wholesale market prices. The economics were too good to ignore.

The Spanish regulatory framework attracted investment from across Europe. While the costs of renewable technologies began to fall, the feed-in tariffs remained in place unchanged, leading to a boom in generation capacity. The feed-in tariffs had been designed to ensure a return of between 5% and 9%, although actual returns were between 10% and 15%.

For Acciona, with its newly acquired EHN platform, the timing was perfect. Every megawatt installed under the feed-in tariff regime was essentially a government-backed annuity.

But José Manuel Entrecanales had a much bolder vision. Why simply build wind farms when you could acquire thousands of megawatts of operational assets at once?

The Audacious Endesa Play

In September 2005, one of the most contentious corporate battles in European history began when Gas Natural made a hostile bid for Endesa, Spain's largest electric utility.

In September 2005, Barcelona-based Gas Natural made a bid for Endesa, whose board unanimously rejected a €23 billion offer. On January 5, 2006, the Competition Court blocked the merger of Gas Natural and Endesa because of what it claimed would be irreversible negative impacts on competition. For most of 2006 and 2007, Endesa was the target of rival takeover bids by Germany's E.ON and the Italian firm Enel. Despite Gas Natural being half the size of Endesa, its bid was championed by the then-Socialist government as an all-Spanish deal, but Gas Natural decided to withdraw its bid after the German firm E.ON offered a higher price.

In 2006, Acciona joined the highly politicized cross-border takeover battle for Spain's largest electric utility, Endesa, by acquiring a 10% stake that it subsequently built up to 21%. Other interested suitors were E.ON and Enel, the largest electric utilities in Germany and Italy, respectively. In March 2007, Acciona's executive chairman José Manuel Entrecanales was considering three strategic alternatives: tendering its shares—and realizing a capital gain of €1.2 billion, 13% of Acciona's market capitalization; holding out as a strategic but minority shareholder in Endesa; or negotiating an agreement with Enel and/or E.ON.

What made this audacious was scale. Acciona was a €9 billion company taking a 25% stake in Spain's largest utility. The debt required was immense. Net financial debt at December 31, 2008 amounted to 17.9 billion euros, giving a gearing of 283%, mainly due to the acquisition of a 25.01% stake in Endesa and the consolidation of 25.01% of its debt.

The percentage of shares controlled by Enel rose to 24.9%, and the other partner opposed to E.ON, Acciona, possessed 21%. Both companies signed an agreement on March 26, 2007 by which they committed to launch a joint offer with a minimum price of 41 euros per share.

Enel and Acciona partnered up in 2007 to take control of Endesa, but have been at odds in recent months over how to manage the company.

The Exit: Massive Capital Infusion

The partnership with Enel was always uncomfortable. Two years later, Entrecanales found his exit.

Under the deal, subject to Spanish and EU regulatory approval, Acciona received €9.6 billion from Enel and €1.5 billion in a dividend from Endesa. Acciona agreed to then buy €2.9 billion in renewable energy assets from Endesa in Spain and Portugal.

Enel paid €11.1 billion for Acciona's stake, including €8.2 billion in cash and roughly €2.9 billion in renewable energy assets that have a capacity to generate 2,104 MW of electricity.

ACCIONA Energía incorporated 2,105 MW of Endesa's renewable assets (wind and hydro power) under an agreement reached between ACCIONA and the Enel group. This was ACCIONA Energía's largest asset acquisition to date, significantly increasing its installed capacity to 6,455 MW by the end of 2009.

The structure was genius. Acciona had effectively used the Endesa takeover battle as a mechanism to: 1. Generate a massive capital gain on its equity stake 2. Acquire over 2 GW of operational renewable assets 3. Exit a partnership that had become contentious 4. Dramatically increase its scale in the renewables sector

ACCIONA Energy contributed 14.1% of ACCIONA's total revenue, with 1.78 billion euros in revenue (63.2% more than in 2007) and an EBITDA of 589 million euros, a year on year increase of 50.3%. Total installed wind capacity rose by 19.4%, to 4,566 MW.

By the end of 2009, Acciona Energía had transformed from a medium-sized Spanish wind developer into one of Europe's largest pure-play renewable energy operators. The €2.9 billion in renewable assets represented roughly 1,400 MW of wind power and 682 MW of conventional hydro assets.

Key Lesson: Entrecanales demonstrated that construction companies don't need to build their way to renewable energy scale. Strategic M&A—even using hostile takeover battles as a mechanism—can be far more effective.

V. Inflection Point #2: The Spanish Regulatory Apocalypse (2010–2014)

The Tariff Deficit Crisis

Just as Acciona Energía reached its new scale, the ground beneath the entire Spanish renewable industry began to crumble.

The 2008 financial crisis exposed a fundamental flaw in Spain's renewable energy framework. A central problem in Spain was the incompatibility of the feed-in tariff with strict limits on how much retail electricity rates could rise. This led to the creation of a public debt to renewable energy producers, which the Spanish government estimated had grown to over EUR 9 billion in 2014. After a very successful year for PV in 2008, the previous Socialist government's solution was to impose retroactive cuts on feed-in tariff levels.

The compensation claims stem from a series of retroactive feed-in tariff cuts that started in 2010 and culminated in the complete eradication of the support scheme in 2014. The cuts saw investments in Spanish renewables dropping from $8 billion to just $100 million over the same period, according to Bloomberg New Energy Finance.

To understand the magnitude: investment collapsed by 98.75% in four years.

Retroactive Cuts: The Nuclear Option

The Spanish Government faced multiple lawsuits over its Royal Decrees which cut the Feed-in Tariff for Solar PV Installations retroactively. These laws were passed in December 2010 as part of the comprehensive review of the Renewable Energy Subsidies by the government.

During a press conference, the European Energy Commissioner, Günter Oettinger, said he refused to support the retroactive cuts to renewable energy subsidies in Spain and the Czech Republic. He said "forward-looking changes may be understandable and necessary, but the European Commission will not accept retroactive amendments. Parliaments in Spain and the Czech Republic have already discussed retroactive changes in order to relieve public budgets, but we consider that this is unacceptable."

The changes came in waves. With the arrival of the crisis, and especially from 2010 onwards, incentives introduced in the previous two decades were phased out. For example, remuneration was cut to set a maximum number of production hours per year. This limit was well below the actual production hours, so the aim was to bring about a reduction in bonuses of around 30%.

Acciona SA has told Bloomberg that the policy will destroy the value of its renewable energy investments in Spain. Spain's renewable energy sector suffered under many attacks, and this latest move by the nation's ruling center-right Popular Party was potentially the most harmful to date.

Industry Devastation and International Arbitration

The retroactive cuts triggered an unprecedented wave of international arbitration. Investors who had deployed capital based on government promises of 20-year fixed returns argued that Spain had violated international investment treaties.

Spain is notoriously the most severely affected state in arbitration proceedings based on the Energy Charter Treaty (ECT), as it is believed to have lost 825 million euros to date, with an aggregated 10,000 million euros sum being sought.

As of 2024, Spain had faced more than 50 intra-EU ECT claims with damages totaling over USD 10 billion. While Spain won early cases like Isolux Infrastructure Netherlands and Charanne B.V., the tide turned decisively against it starting in 2017. Since 2011, Spain has lost 16 disputes before ICSID alone related to the renewable energy sector.

Today, according to ICSID and other international sources, Spain faces more than 52 arbitrations in international courts related to cuts in renewable energy, making the country one of the most sued in the world, along with Argentina, Russia and Venezuela. The total amount of lawsuits filed exceeds 10 billion euros. International courts have ruled in favor of investors in 25 of the 34 lawsuits resolved.

According to the Photovoltaic Industry Association, several hundred photovoltaic plant operators faced bankruptcy. Phil Dominy of Ernst & Young, comparing feed-in tariff reductions in Germany and Italy, said: "Spain stands out as an example of how not to do it."

Acciona's Survival Strategy

Why did Acciona survive when hundreds of smaller players went bankrupt?

Three factors: scale, geographic diversification, and balance sheet management.

First, Acciona's size meant it could spread fixed costs across a larger asset base. Second, its international expansion—accelerated after the regulatory crisis—reduced dependence on Spanish prices. Third, the Endesa transaction had left the company with substantial cash, providing a buffer during the worst years.

But the psychological impact was perhaps more important than the financial impact. The Spanish regulatory crisis burned into Acciona's corporate DNA an almost paranoid focus on geographic diversification. Never again would the company allow itself to be so dependent on a single jurisdiction's political whims.

"Confidence has decreased," said Pietro Radoia, senior analyst at Bloomberg New Energy Finance. "There are a lot of established investors placing considerable amounts of money into new projects, and some are limiting their exposure to Spanish merchant risk."

For Acciona, the lesson was clear: international expansion wasn't just about growth—it was existential insurance.

VI. The International Expansion & Rebound (2012–2020)

Latin America: The New Growth Engine

While Spain's renewable market was imploding, Acciona found opportunity in Latin America—particularly Mexico, which combined strong wind resources with supportive regulatory frameworks.

On March 7, 2012, Mexico's President Felipe Calderón attended the wind farms Oaxaca II, III and IV, operated by Acciona in southern Mexico, to formalize their inauguration. Acciona invested $670 million in a wind farm of 306 megawatts in La Ventosa, in the Mexican state of Oaxaca, the largest wind farm in Latin America.

Oaxaca II, III and IV represent one of the biggest wind power complexes in Latin America with 306 MW of operational capacity. They produce electricity to cover the consumption of 700,000 Mexican homes, avoiding the emission of 670,000 metric tons of CO2. ACCIONA is the leader in wind power in Mexico with 556.5 MW spread across four wind farms.

The Oaxaca complex was built on the Isthmus of Tehuantepec, one of the world's most wind-rich regions. The geography matters: the narrow strip between the Gulf of Mexico and the Pacific Ocean creates a natural wind tunnel with some of the most consistent wind patterns on the planet.

The Eurus Wind Farm is located in Juchitán de Zaragoza, Oaxaca, Mexico. The largest wind farm in Latin America at the time, the partnership between Cemex and Acciona Energia cost US$550 million to build. Its 167 wind turbines combine to generate 250.5 megawatts, sufficient power to supply about half a million people.

Diversifying the Portfolio

Acciona wasn't just building wind farms. The company developed solar capabilities across multiple continents, using projects as learning experiences for increasingly challenging environments.

ACCIONA Energía installed Spain's first grid-connected floating photovoltaic plant on the Sierra Brava reservoir as a demonstration project to explore optimal electricity generation in such installations. The 1.125 MWp plant covers only 0.07% of the reservoir's surface and represents a promising innovation for future energy projects.

Battery Storage Innovation

On September 20, 2017, ACCIONA Energía inaugurated Spain's first battery storage plant for wind farm energy in Barásoain (Navarra), showcasing its leadership in innovative energy solutions for combating climate change and advancing decarbonization. Five years later, the company acquired Texas' largest battery (190MW) and a storage project portfolio exceeding 1GW.

The Nordex Merger: Controlling the Supply Chain

In 2016, Acciona made a strategic move that few renewable developers have replicated: it merged its turbine manufacturing business with a major European OEM.

ACCIONA completed the sale of its wind turbine manufacturing subsidiary, ACCIONA Windpower (AWP), to Nordex of Germany in a cash-and-shares transaction valued at €785 million. The integration of ACCIONA Windpower into the listed German company created a new European powerhouse in wind turbine manufacturing, with combined sales of €3.4 billion in 2015. Following the transaction, ACCIONA became Nordex's principal shareholder with a 29.9% stake.

The two wind turbine manufacturers have complementary technologies and market footprints, with Nordex's strong presence in Europe a good match for ACCIONA Windpower's established position in North and South America. In total, the two companies have installed 18 GW of wind power capacity in more than 25 countries.

The merger generated €657 million in extraordinary earnings from the ACCIONA Windpower (AWP) and Nordex merger, in which ACCIONA became a core shareholder.

This move was controversial. Why would a renewable developer give up control of its turbine manufacturing? The answer lies in scale. "Size today is a must," said AWP CEO José Luis Blanco, a view underpinned by GE's recent takeover of Alstom's energy business, including its wind turbines.

By merging AWP with Nordex, Acciona gained access to better technology (particularly for European markets), diversified manufacturing risk, and crystallized value on its balance sheet—all while maintaining significant influence as the largest shareholder.

As part of ACCIONA's commitment to technological innovation, it develops cutting-edge wind turbines through Nordex, company in which ACCIONA has been the main shareholder since 2016.

VII. Inflection Point #3: The 2021 IPO—Unlocking Value Through Spinoff

Strategic Rationale

By 2020, Acciona found itself in an unusual position. Its renewable energy business had grown to significant scale, yet the stock market seemed to value the parent company as if it were still primarily a construction firm. ESG capital was flooding into pure-play renewable energy companies at premium valuations—capital that diversified conglomerates couldn't access.

Corporación Acciona Energías Renovables ("Acciona Energía" or the Company), a subsidiary of Acciona and one of the leading pure renewable energy companies globally, completed its successful c. €1.52bn IPO on the Spanish stock exchanges on July 1, 2021. The offering represents the largest IPO in Spain in the last 6 years and the largest European renewable energy IPO in the last 5 years.

The logic was straightforward: separate the businesses, give investors a pure-play vehicle, reduce the cost of capital for growth investments, and unlock the valuation premium that ESG-focused investors were willing to pay.

The Mechanics

ACCIONA announced that the non-binding price range for the initial public offering (IPO) of ACCIONA Energía, a leading 100% renewable energy company, would be set between €26.73 and €29.76 per share.

Acciona Energía closed its initial public offering at €26.73 per share, which valued the company at more than €8.8 billion. ACCIONA offered a total of 49,387,588 ordinary shares of ACCIONA Energía, or 15% of the subsidiary's share capital, to which a further 7,408,138 shares, or 2.25%, could be added to cover green shoe allotments.

The pricing at the bottom of the range reflected challenging market conditions for European IPOs in mid-2021. But demand was strong. The demand from institutional investors, for a total of €3.6 billion, was 2.4 times the final offer decided. The book was already covered within the first 24 hours of bookbuilding. The extremely high-quality book consisted of over 220 lines, with allocations skewed over 80% to Long-Only investors.

Market Debut and Index Inclusion

On July 1, 2021, ACCIONA Energía debuted on the Spanish stock exchange in one of the largest IPOs in recent years. This move aimed to support its ambitious growth plan of reaching 20 GW by 2025 and over 30 GW by 2030.

Since July 2021, the renewable energy subsidiary Acciona Energía has been independently listed on the continuous market—it is also part of the IBEX 35 index, with ACCIONA as its majority shareholder.

Following the settlement of the IPO, ACCIONA owned 85% of ACCIONA Energía's capital. ACCIONA's stake would be reduced to 82.75% in the event that the green shoe was fully exercised.

The Investment Thesis at IPO

The IPO prospectus laid out an aggressive growth plan. The company had 10.69 GW of installed capacity at year-end 2020, with 53% in Spain and 47% internationally. Annual production totaled 24,075 gigawatt-hours.

The company had 3 GW under construction or ready to start over the next two years, and targeted annual installations of more than 2 GW from 2023. The geographic priorities were clear: the US (adding 2.7 GW), Australia (2.5 GW), Spain (1.8 GW), and Mexico and Chile (0.7 GW each).

VIII. The New Frontiers: Green Hydrogen & Offshore Wind (2020–Present)

Green Hydrogen Leadership

On March 14, 2022, the first industrial renewable hydrogen plant in Spain was inaugurated in Mallorca, turning the island into the first renewable hydrogen hub in southern Europe. With support of an EU grant of 10 million Euro by the Clean Hydrogen Partnership, the project is part of the Power to Green Hydrogen Mallorca project, led by Enagás and ACCIONA Energía, with the participation of IDAE and CEMEX.

Power to Green Hydrogen Mallorca is Spain's first industrial-sized green hydrogen plant, which will produce at least 300 tonnes per year to serve various energy needs on the Balearic island.

This industrial project is the core element in the European Green Hysland project, in which the European Union has committed 10 million euros through the Clean Hydrogen Partnership to support the deployment of infrastructure to make the renewable hydrogen ecosystem of Mallorca a reality. Mallorca will serve as a model to be replicated in five other island territories (Valentia, Ireland; Ameland, the Netherlands; Tenerife, Spain; Madeira, Portugal, and the Greek Islands).

ACCIONA's Chairman and CEO José Manuel Entrecanales noted that "green hydrogen is an industrial and economic opportunity for Spain and Europe. The public-private partnership in this project and the support of the different administrations is a reference model of how to take advantage of this opportunity. The Mallorca project will allow the maturing of a technology and an economic model based on renewable hydrogen to make a qualitative leap in decarbonisation."

ACCIONA built Spain's first industrial green hydrogen plant in Mallorca and is building a second plant in Navarre, as part of the joint venture created between ACCIONA Energía and US electrolyser manufacturer Plug Power, aimed at the industrial and mobility sectors in Spain and Portugal.

Hybrid Plants and Innovation

ACCIONA Energía has completed its first hybrid renewable energy plant by adding a 29.4MW photovoltaic facility to the existing 36 MW Escepar wind farm, located in the municipalities of Villalba del Rey and Tinajas (Cuenca, Spain).

Hybrid plants—combining wind, solar, and storage on the same grid connection—represent the future of utility-scale renewable energy. They improve grid utilization, reduce interconnection costs, and provide more consistent power output.

IX. Current Challenges & The 2024-2025 Reality Check

Financial Performance Under Pressure

The years 2023-2024 proved challenging for Acciona Energía. After the extraordinary electricity prices of 2022 (driven by the Ukraine war and gas crisis), European power prices normalized—significantly impacting revenues.

ACCIONA Energía achieved an attributable net profit of €357 million (-31.9%) in 2024. Its turnover amounted to €3.05 billion (-14.1%). Of its total revenues, €1.64 billion corresponds to the wholesale generation business and €1.41 billion to marketing activity. ACCIONA Energía's EBITDA for the year was €1.12 billion (-12.6%), comfortably meeting its EBITDA target of €1 billion, thanks to the improvement in electricity prices in Spain during the second half of the year.

In 2024, Acciona Energía added 2 gigawatts of new capacity, mainly due to the development of its own portfolio in countries such as Australia, India, Canada, the US, Spain and Croatia, as well as a one-off acquisition of 297 megawatts of wind power from the Green Pastures complex in Texas. Total installed capacity amounts to 15.35 gigawatts. The company states that 62.75% of its renewable energy fleet is located outside Spain.

Deleveraging Imperative: The Asset Rotation Strategy

With significant debt from its aggressive growth strategy, Acciona Energía embarked on a major asset rotation program—selling mature assets to reduce leverage while maintaining growth investment.

ACCIONA Energía announced the closing of the sale of 626MW hydro assets to Endesa, after receiving the relevant authorizations. The transaction comprises 34 hydroelectric power plants with an annual production of around 1.3 TWh. ACCIONA Energía received approximately €1 billion for the transaction. The plants are located in the Spanish regions of Aragón, Navarra, Soria and Valencia, and operate under long-term concession agreements with an average remaining duration of approximately 30 years.

The Endesa transaction was free of debt and generated estimated capital gains of €620 million. Closing was anticipated in the first half of 2025, following the necessary antitrust and foreign investment clearances.

A central theme of Acciona's presentation was its asset rotation strategy, which is progressing well with approximately €2 billion in proceeds secured from completed or agreed transactions. This represents about 65% of the company's 2024-2025 target. One of the most significant recent transactions was the sale of a 440 MW wind portfolio in Spain to Opdenergy for €530 million.

In 2024, the company completed two hydro deals with proceeds of €1.3 billion (approximately €1.6 million per megawatt) and gains of €680 million, of which €150 million came from impairment provisions' reversal. The Endesa 626MW deal was completed in early 2025 and contributed approximately €450 million in capital gains.

US Market Headwinds

The American market, which was supposed to be Acciona's major growth driver, has become more complicated.

The company is addressing challenges in the US renewable energy market, where tariffs and new FEOC (Foreign Entity of Concern) provisions are limiting access to IRA tax credits. In response, Acciona has paused 0.4 GW of battery energy storage system (BESS) projects in the US while maintaining 1.4 GW of projects with safe harbor provisions.

President Trump signed the One Big Beautiful Bill Act into law on July 4, 2025. The OBBBA introduces accelerated repeal schedules for most renewable energy tax credits, compresses deadlines for certain projects to qualify for such credits, enhances domestic content requirements, eliminates several electric vehicle and residential energy incentives, and implements new foreign entity of concern (FEOC) restrictions barring certain foreign entities from accessing credits.

Wind and solar facilities that begin construction after July 4, 2026 (one year after enactment) are ineligible for the Section 45Y credit if placed in service after December 31, 2027. Facilities that begin construction prior to July 4, 2026 would not be subject to this accelerated placed-in-service deadline.

2025 Recovery Signs

Despite the challenges, the first half of 2025 showed marked improvement.

Spanish multinational Acciona SA presented its H1 2025 results, highlighting substantial financial growth. The company reported revenue increasing 5% year-over-year to €9.23 billion. EBITDA surged 57% to €1.56 billion, while attributable net profit soared 353% to €526 million. The company's EBITDA growth was driven by both operational performance (€1.11 billion) and asset rotation (€443 million).

EBIT stood at €593 million in the first half of 2025, compared to €198 million in the same period last year.

ACCIONA's stake in ACCIONA Energía stood at 90.03% as of June 30, 2025.

X. Playbook: Business & Strategy Lessons

Capital Allocation Mastery

The Acciona Energía story demonstrates sophisticated capital allocation across multiple dimensions:

Using Utility M&A as a Scaling Mechanism: The Endesa transaction remains one of the cleverest moves in European renewable energy history. Rather than building assets one project at a time, Entrecanales used a contested utility takeover to acquire 2+ GW of operational renewable assets while generating billions in cash returns.

IPO Timing for ESG Capital Flows: The 2021 spinoff captured the peak of ESG investor enthusiasm for pure-play renewable vehicles. The timing allowed Acciona to raise €1.5 billion at valuations that diversified conglomerates couldn't access.

Asset Rotation for Balance Sheet Management: The 2024-2025 asset sales demonstrate disciplined portfolio management—selling mature, lower-growth hydro assets at premium valuations to fund growth investments while reducing leverage.

Regulatory Navigation

The Spanish regulatory crisis offers critical lessons:

Geographic Diversification as Insurance: Today, 63% of Acciona's capacity sits outside Spain—a direct response to the trauma of 2010-2014. No single jurisdiction can destroy the company's economics.

Regulatory Risk Assessment: The company now evaluates markets not just on resource quality and returns, but on regulatory stability and rule-of-law track records. The US market's recent policy volatility reinforces this caution.

The Family Business Advantage

The Entrecanales family's multi-generational involvement provides both stability and patient capital. José Manuel Entrecanales, now into his third decade leading the company, can make decisions with a 20-30 year horizon—something most public company CEOs cannot do.

The company controlled by the Entrecanales family owns 55.12% of the share capital.

XI. Bull & Bear Case: Strategic Assessment

The Bull Case

Structural Tailwinds: Europe's energy transition is accelerating, with binding 2030 and 2050 targets creating decades of demand growth. Acciona's geographic diversification captures this trend across multiple markets.

Proven Execution: The company has successfully scaled from 800 MW in 2004 to over 15 GW today—a nearly 20-fold increase in two decades. Management knows how to build, operate, and optimize renewable assets.

Asset Rotation Optionality: The 2024-2025 divestment program demonstrates that Acciona can crystallize value at attractive multiples. The hydro assets sold for €1.6+ million per MW—well above the company's implied market valuation.

Nordex Turnaround: After years of losses, Nordex completed its turnaround in 2024. Nordex has successfully consolidated the turnaround in its financial and operating performance in 2024. Revenues grew by 12.5%, reaching €7,299 million. The EBITDA margin was 4.1%, reaching €296 million in 2024, slightly exceeding the upper guidance range of 3-4%. As the largest shareholder, Acciona benefits from this improvement.

The Bear Case

US Policy Risk: The new FEOC restrictions and accelerated phaseout of IRA tax credits create significant uncertainty for Acciona's American growth plans. Projects without safe harbor provisions face materially worse economics.

Power Price Volatility: Merchant exposure means earnings swing with electricity prices. The 2022-2024 period demonstrated both the upside (2022's record prices) and downside (2024's normalized prices) of this volatility.

Leverage Concerns: Despite the asset rotation program, net debt remains elevated. Net financial debt increased to €7.71 billion as of June 2025, up from €7.13 billion at the end of 2024.

Competition Intensifying: Major oil companies (Shell, BP, TotalEnergies) and utilities are deploying enormous capital into renewables. Technology-focused competitors like Ørsted and Iberdrola bring greater scale.

Porter's Five Forces Analysis

Threat of New Entrants (Medium-High): Low barriers exist for basic wind and solar development, but Acciona's integrated capabilities (development, construction, O&M) create competitive advantages. Scale provides cost advantages in equipment procurement.

Supplier Power (Medium): The Nordex relationship provides some insulation from turbine supplier pricing power, but solar panels remain commoditized with Chinese manufacturers dominating production.

Buyer Power (Medium): Utilities and corporate PPAs provide some pricing stability, but merchant sales are fully exposed to wholesale market dynamics.

Threat of Substitutes (Low-Medium): Nuclear renaissance could provide baseload alternatives, but solar and wind costs continue declining. Battery storage addresses intermittency concerns.

Industry Rivalry (High): Renewable development is increasingly competitive, with multiple well-capitalized players chasing the same opportunities.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Modest scale benefits exist in procurement and O&M, but not transformational. Acciona operates 15 GW versus Iberdrola's 40+ GW of renewable capacity.

Network Effects: Not applicable in renewable energy development.

Counter-Positioning: Limited. Acciona's pure-play status was differentiated in 2021, but competitors have copied the model.

Switching Costs: None for customers buying wholesale electricity.

Branding: Minimal in B2B electricity sales.

Cornered Resource: The Navarra heritage provides institutional knowledge and relationships, particularly in Spain. The 30+ years of operating experience across 24 countries creates hard-to-replicate expertise.

Process Power: Acciona's integrated development-construction-O&M model provides process advantages in project execution. The EHN heritage created processes for community engagement that remain industry-leading.

Assessment: Acciona's competitive advantages stem primarily from institutional knowledge (cornered resource) and integrated capabilities (process power). These are durable but not transformational moats.

XII. Key Metrics for Investors

The Three KPIs That Matter

For investors following Acciona Energía, three metrics capture the essential dynamics:

1. Megawatt-Weighted Average Realized Price (€/MWh)

This metric captures the blended electricity price across the entire portfolio, reflecting both merchant sales and contracted revenues. In 2024, this averaged €68.7/MWh (-20.4% year-over-year). Tracking this metric reveals exposure to power price volatility and effectiveness of hedging strategies.

2. Net Debt to EBITDA Ratio

The company is targeting a net debt to EBITDA ratio from operations of approximately 3.5x and is committed to maintaining financial flexibility. This metric captures balance sheet health and the company's ability to fund growth. Credit rating agencies watch this closely—breaching sustained levels above 4.5x risks downgrades.

3. Capacity Growth Rate (Annual GW Additions)

In 2024, Acciona Energía added 2 gigawatts of new capacity. This metric captures the company's ability to execute its development pipeline. The 2025 target of reaching 20 GW total capacity requires consistent 2+ GW annual additions.

XIII. Looking Forward: The Path Ahead

Current Valuation Context

The company currently trades with a market capitalization of approximately €7.7 billion and an enterprise value of €12.5 billion. The trailing P/E ratio is approximately 10x, with a forward P/E of roughly 30x, and an EV/EBITDA multiple around 7.7x.

The forward multiple expansion reflects analyst expectations for normalized earnings growth as power prices stabilize and asset rotation gains taper off.

Strategic Priorities

Management has outlined clear priorities for 2025-2026:

- Deleveraging: Completing the asset rotation program to achieve ~€3 billion in proceeds

- Selective Growth: Focusing on markets with regulatory stability and strong resource quality

- US Strategy Adaptation: Navigating FEOC restrictions while protecting safe-harbored projects

- Operational Excellence: Improving production efficiency across the existing fleet

Risks to Monitor

Regulatory: Further IRA clawbacks, European permitting bottlenecks, emerging market policy shifts

Financial: Interest rate impacts on project economics, counterparty risk on PPAs, currency volatility

Operational: Extreme weather impacts on production, equipment defects, grid curtailment

The Long View

Acciona Energía represents a particular type of renewable energy investment—one built on decades of operating experience rather than technology disruption. The company won't revolutionize solar cell efficiency or create breakthrough battery chemistry. Instead, it will continue doing what it has done since 1994: identifying wind-rich and sun-rich locations, navigating local permitting and regulatory environments, building projects on time and on budget, and operating assets for maximum efficiency over their 25-30 year lifespans.

For investors with a long-term horizon, the question is whether this execution capability commands a premium in a world where capital increasingly flows to flashier technology stories. The Entrecanales family has been building infrastructure across multiple generations—their time horizon extends well beyond quarterly earnings reports.

The journey from José Entrecanales Ibarra's bridge construction in 1931 Seville to José Manuel Entrecanales Domecq's green hydrogen ambitions in 2025 Mallorca spans nearly a century of family capitalism. Through wars, dictatorships, regulatory crises, and energy transitions, the family has demonstrated an ability to adapt and survive.

Whether that survival instinct translates into market-beating returns depends on factors beyond management's control: power prices, regulatory stability, and the pace of the global energy transition. But for investors seeking exposure to that transition through a company with real assets, real cash flows, and a century of institutional memory, Acciona Energía offers a compelling case study in how patient capital can navigate turbulent markets.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube