Acciona: Spain's Sustainability Pioneer—From Concrete to Clean Energy

Introduction & Episode Roadmap

Picture this: A Spanish family business, ninety years in the making, that bet its future on sustainability before climate change became a boardroom priority. A company that dared to enter one of the most politically charged corporate battles in European history—the €42.5 billion takeover war for Endesa—and emerged not as a utility company, but as the largest 100% renewable energy company in the world with no fossil fuel legacy.

Acciona closed 2024 with a net profit of €422 million, record revenues of €19.19 billion (+12.7%), and gross operating profit (EBITDA) of €2.45 billion (+24%), achieving its targets for the year. In the energy sector, Acciona Energía ended the year with 15.35 GW of installed capacity, following the addition of 2 GW in markets such as Australia, India, Canada, Spain and Croatia.

The central question that defines the Acciona narrative: How does a construction dynasty, built during the Franco era and enriched by Spain's infrastructure boom, transform itself into a global leader in the energy transition?

The Entrecanales family is one of the most successful Spanish business families due to their exclusive ownership of Acciona SA, a conglomerate with a variety of interests, including construction, water, industrial services and renewable energy.

Three themes emerge from this story that every investor should understand:

First, the power of family capitalism and generational succession. The Entrecanales family has controlled this enterprise through three generations, allowing for strategic patience impossible in most public companies. In 2004, José Manuel Entrecanales succeeded his late father as chairman and CEO of Acciona, a global leader company focused on sustainable solutions in infrastructure, renewable energy and water.

Second, the audacious Endesa gamble. In 2006, a construction company with minimal utility experience plunged into a cross-border takeover battle that would transform European energy markets—and emerged with over 2 GW of renewable assets that became the foundation of today's energy empire.

Third, betting on sustainability before it was fashionable. Since 2015 the company has headed the Top 100 Green Utilities ranking, put together by consultancy group Energy Intelligence, which rates one hundred electricity companies based on their CO2 emissions and installed renewables capacity.

The transformation is remarkable. The company has undergone a major transformation in the last decade, diversifying its activity and geographical scope. Acciona has gone from being one of Spain's leading construction companies, specialising in large-scale civil engineering projects, to becoming a world leader in the development, production and management of renewable energy, water and infrastructure.

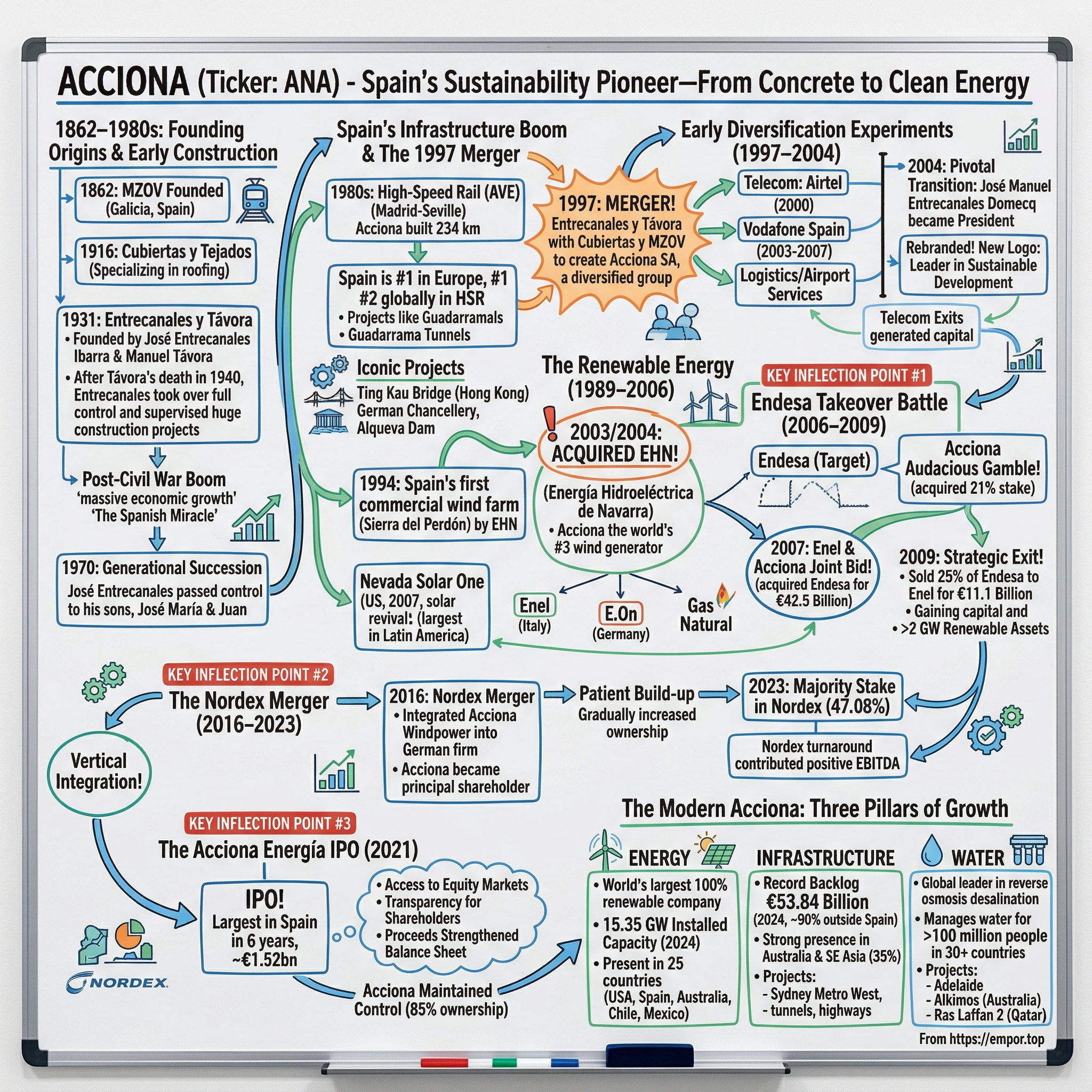

Founding Origins & Early Construction History (1862–1980s)

The origins of Acciona reach back to an era when Spain was transitioning from an agrarian society to an industrial power—or at least trying to. The story begins not with the Entrecanales family, but with a railway company in Galicia.

In 1862, MZOV (Compañía de los Ferrocarriles de Medina del Campo a Zamora y de Orense a Vigo) was founded in northwest Spain. MZOV, the railway company covering the Medina del Campo–Zamora and Orense–Vigo routes, was founded in Galicia, Spain. After being awarded several key lines connecting Galicia with central Spain, the company reinvented itself as a leading Spanish construction firm.

Meanwhile, in 1916, Cubiertas y Tejados, S.A. was founded, specialising in roofing, but also expanding into other forms of industrial construction.

But the family that would eventually control the conglomerate enters the picture in 1931, when the Spanish Republic was still young and the Civil War was still five years away.

José Entrecanales Ibarra, a civil engineer from Bilbao, and Manuel Távora, an entrepreneur from Seville, founded Entrecanales y Távora, S.A. on 11 March 1931.

The partnership was short-lived. The family patriarch is engineer and entrepreneur José Entrecanales Ibarra, who co-founded the engineering company Entrecanales y Távora with partner Manuel Távora in 1931. After Manuel Távora's death in 1940, José took over full control of the company and supervised huge construction projects, such as the extension of the Madrid-Barajas Airport, the construction of the Atazar de Madrid dam and the Bilbao Bank Building in Madrid.

The company was founded in 1931 and grew during the early years of the Franco regime. The timing proved fortuitous. This led to massive economic growth, second only to Japan, that lasted until the mid-1970s, known as the "Spanish miracle." Construction companies that could deliver major infrastructure projects found themselves with extraordinary opportunities.

The post-Civil War period saw Entrecanales y Távora emerge as one of Spain's most capable infrastructure builders. In 1948, Entrecanales y Távora, S.A. signed its first contract outside Spain, undertaking projects in Portugal, Morocco, and Equatorial Guinea. This marked the company's first step towards international expansion.

Over time, the company expanded to various countries in Latin America, Europe, Africa, and Asia, including Egypt, the US, the Philippines, France, Hong Kong, Italy, Jordan, Malaysia, Mexico, and Puerto Rico.

The leadership transition came in 1970 when José Entrecanales Ibarra, having built one of Spain's leading construction firms, decided it was time to pass the torch. In 1970, José Entrecanales Ibarra handed over control of the family business to his sons, José María and Juan Entrecanales de Azcárate.

The brothers saw the company through a booming period of growth and expansion, culminating in the creation of Acciona SA in 1997.

The formation of Cubiertas y MZOV in 1978 through the merger of the two earlier companies created one of Spain's major construction groups. Cubiertas y MZOV, S.A. was established on 2 October 1978 as a result of the merger between MZOV and CYT. The merger capitalised on their complementary businesses, and marked a new era for both companies.

In the 1980s, Entrecanales y Távora, S.A. became primarily known for infrastructure work, but diversification into sectors such as real estate, wine production, urban services, and telecommunications began.

Understanding this history is crucial for investors because it explains the company's DNA. Unlike many renewable energy companies that were born in the green wave of the 2000s, Acciona's roots lie in concrete, steel, and civil engineering. The company knows how to manage complex multi-year projects with massive capital requirements. That operational capability—developed over generations—would prove essential when the company pivoted toward renewable energy.

Spain's Infrastructure Boom & The 1997 Merger

The story of modern Acciona cannot be told without understanding the transformation Spain underwent in the 1980s and 1990s. The country emerged from decades of relative isolation under Franco, joined the European Union in 1986, and embarked on one of the most ambitious infrastructure buildouts in modern European history.

In the 1980s, leading up to Expo 1992, Spain's first high-speed railway between Madrid and Seville was under construction. Acciona played a key role, pioneering the development of an incrementally launched bridge for the high-speed rail line and constructing 234 km of the 472 km track.

The scale of Spain's high-speed rail ambitions was staggering. Spain now ranks first in Europe and second globally (behind China) in terms of high-speed railway infrastructure, with 3,000 km of track. Acciona was involved in building some of the largest projects.

Among the landmark projects: Examples include the Guadarrama tunnels, measuring 14,270 m and 14,000 m in length (the fifth-longest in the world) on the Madrid–Segovia section.

The 1990s saw the Spanish construction sector consolidate, with major players jockeying for position. Into the late 1990s the Spanish construction sector entered a new period of consolidation, with major players, including Dragados, FCC, and others jockeying for position at the top of the market.

In 1997, the strategic logic became irresistible: combine Entrecanales y Távora with Cubiertas y MZOV to create a construction powerhouse capable of competing on the international stage.

In 1997, Acciona was established as a diversified group with José María Entrecanales de Azcárate as President and Juan Entrecanales de Azcárate as Vice President. This marked the creation of an international holding company operating across various sectors.

The company built a formidable portfolio of iconic projects during this era. These included Torre Europa completed in 1985, the Ting Kau Bridge in Hong Kong completed in 1998, the Gare do Oriente in Lisbon completed in 1998, El Museu de les Ciències Príncipe Felipe completed in 2000, the German Chancellery completed in 2001, and the Alqueva Dam completed in 2002.

Entrecanales also increasingly sought business on the international front; in the mid-1990s, for example, the company entered the Asian market, building the Ting Kau Bridge connecting Hong Kong to the Chinese mainland. Begun in 1995, that project was completed by 1998.

The merger created something more than a construction company. It created an international holding structure that could pursue diversification strategies across sectors and geographies. The Entrecanales family maintained control, providing the stable shareholder base that would allow management to pursue long-term strategies impossible for companies with dispersed ownership.

For investors, the 1997 merger represents the moment Acciona gained the scale and structure necessary for its subsequent transformation. The family control, the international experience, and the operational excellence in complex projects—all of these would prove essential when the company later pivoted toward renewable energy and water.

Early Diversification Experiments: Telecom, Logistics & Lessons (1997–2004)

Every great business story includes chapters of experimentation—some successful, others less so. The years following the 1997 merger saw Acciona test various diversification strategies, learning valuable lessons about where its core competencies could create value.

Telecommunications captured the imagination of many Spanish industrial groups in the late 1990s. In 1995, the family business bought a majority share package of a mobile company called Airtel and José Manuel Entrecanales was named CEO in 2000, replacing Juan Abelló. In 2003, Vodafone bought Acciona's shares of Airtel and Entrecanales was the CEO of Vodafone Spain up until October 2007.

The telecom investment demonstrated something important about the Entrecanales family's investment philosophy: they were willing to take major positions in growth sectors, but equally willing to exit when strategic logic demanded. The sale to Vodafone generated significant capital that would later fund renewable energy expansion.

The company also expanded into logistics and airport services. These investments included airport handling and management services, as well as distribution and logistics operations.

Perhaps most significantly for the company's future geographic footprint, Acciona entered the Polish market in 1999 with an acquisition in infrastructure. Poland was preparing to join the European Union in 2004, and Acciona positioned itself to benefit from the country's infrastructure modernization.

The year 2004 marked a pivotal transition. José Manuel Entrecanales Domecq, son of José María Entrecanales de Azcárate and grandson of the founder, became President, and Juan Ignacio Entrecanales Franco, son of Juan Entrecanales de Azcárate, became Vice President. Together, they guided the company through a transformation focused on three key pillars: infrastructure, energy, and water.

José Manuel Entrecanales Domecq was born 1 January 1963 and is a Spanish businessman and former banker. In 2004, he succeeded his late father as chairman and CEO of Acciona.

The new chairman brought a different background. He began his career in 1985 in Merrill Lynch, sharing his time between New York and London. He moved to Acciona in 1991.

José Manuel Entrecanales represents a new generation of Spanish business leaders. Entrecanales has been highlighted as a key leader of a new generation of Spanish businessmen "shaped by family roots but identifying fully with modernisation."

He is a firm advocate of the fight against climate change at a corporate level, which earned him the Order of the Rising Sun, as well as being asked to speak frequently at global forums, including the 2022 UN Climate Change Conference.

When Acciona rebranded in 2004, the company rebranded itself with a new logo, redefining its mission as a leader in sustainable development.

This rebranding was not mere marketing. It signaled a fundamental reorientation of strategy. The telecom exits had generated capital. The infrastructure business provided stable cash flows. Now the question became: where to invest for the next generation of growth?

The answer was already emerging in the Navarra region of Spain, where a small company was quietly building wind farms.

The Renewable Energy Bet: Building Before the Green Wave (1989–2006)

The renewable energy revolution didn't begin with government mandates or ESG pressure. It began with engineers and entrepreneurs who saw potential in the wind.

Milestones in its history include the installation in December 1994 of the first commercial wind farm in Spain on the Sierra del Perdón, next to Pamplona, Navarre, by the Energía Hidroeléctrica de Navarra, S.A. company, acquired by Acciona in 2003 and 2004.

The acquisition of Energía Hidroeléctrica de Navarra (EHN) proved transformational. Founded in 1989, the company had started with hydroelectric assets before expanding into wind power. In 2003, the company paid €383 million to acquire a 50 percent stake in Corporacion Energia Hidroelectrica de Navarra (EHN), a major wind farm operator. As part of that deal, Acciona agreed to transfer its own wind farm holdings to EHN, which then became the world's number three wind power generator. Acciona continued to increase its shareholding in EHN, taking full control by 2004.

Why was this acquisition so significant? Because it happened before renewable energy became fashionable. In 2003 and 2004, climate change was a scientific concern, not yet a boardroom priority. Most investors valued construction companies on infrastructure backlog and margins, not renewable energy capacity.

The EHN acquisition gave Acciona something most construction companies lacked: a technology-driven platform for renewable energy development. The company had pioneered commercial wind power in Spain and understood the full development cycle—from site selection to grid connection.

Jose Manuel Entrecanales Domecq took over direction of the company from his father in 2004. The younger Entrecanales promised to expand the group's renewable energy interests further, as the company adopted a new sustainability platform to underscore its operations.

The US market opened in 2007 with a landmark project. Nevada Solar One, a 64 MW solar thermal plant, represented a technological leap. Acciona led the revival of solar thermal power technology by connecting this plant to the grid.

The company developed its own wind turbine technology through Acciona Windpower, opening its first production facility in Barásoain, Navarre in 2003. The AW1500 platform entered series production in 2005 and subsequent development extended into the 3 MW class.

The Oaxaca wind complex in Mexico showcased the company's ability to execute at scale. Located on the Isthmus of Tehuantepec, one of the world's most wind-rich regions, it became the largest wind power complex in Latin America at the time, generating enough power for 700,000 Mexican households using 204 turbines built with Acciona Windpower technology.

Acciona Energy represents a small but fast-growing part of the overall group. Between 2004 and 2005, that division nearly doubled its total revenues, to more than €500 million.

But the most consequential move was still to come. In 2006, Acciona would enter the most dramatic corporate battle in modern Spanish business history.

Key Inflection Point #1: The Endesa Takeover Battle (2006–2009)

In corporate history, there are transactions and then there are transformational events. The Endesa takeover battle was the latter—a high-stakes drama involving governments, regulators, and some of Europe's largest utilities, with billions of euros and the future of Spain's energy sector hanging in the balance.

Endesa, S.A. is a Spanish multinational electric utility company, the largest in the country. The firm has 10 million customers in Spain.

The battle began in September 2005 when Barcelona-based Gas Natural made a bid for Endesa, whose board unanimously immediately rejected a €23 billion offer.

For most of 2006 and 2007, Endesa was the target of rival takeover bids by Germany's E.On and the Italian firm Enel. Despite Gas Natural being half the size of Endesa, its bid was championed by the then-Socialist government as an all-Spanish deal.

Into this maelstrom stepped Acciona—a construction company with minimal utility experience but with capital, strategic ambition, and the patience that comes from family control.

In 2006, the company joined the highly politicized cross-border takeover battle for Spain's largest electric utility, Endesa, by acquiring a 10% stake that it subsequently built up to 21%. Other interested suitors were E.ON and Enel, the largest electric utilities in Germany and Italy, respectively.

The strategy was audacious. By January 2007, Acciona had become Endesa's largest shareholder. José Manuel Entrecanales announced plans to acquire up to 25 percent—just below the threshold that would have triggered a mandatory automatic bid for all of Endesa.

In March 2007, Acciona's executive chairman Jose Manuel Entrecanales is considering three strategic alternatives: tendering its shares—and realizing a capital gain of €1.2 billion, 13% of Acciona's market capitalization; holding out as a strategic but minority shareholder in Endesa; or negotiating an agreement with Enel and/or E.ON.

The alliance with Enel proved decisive. Acciona and Enel succeeded in their joint bid to acquire Endesa in October 2007 for an estimated €42.5 billion.

E.ON, despite offering €38.75 per share and later raising its offer to €40 per share, ultimately withdrew. Germany's E.ON appears to have failed in its bid to acquire Spanish national energy champion Endesa after Acciona joined Enel in making a rival challenge. In a statement E.ON said it will not execute its takeover bid for a majority stake in Endesa.

The joint venture that emerged was unique. The two companies initially jointly managed Endesa through an Acciona-controlled holding company which held 50.01% of Endesa's share capital.

But the partnership was not destined to last. A partir de ese momento, se inició un periodo de cohabitación entre Enel y Acciona que concluyó el 20 de febrero de 2009. Ese día, el grupo constructor llegó a un acuerdo con la empresa italiana para venderle el 25 % de Endesa por 11.100 millones de euros. (A period of cohabitation between Enel and Acciona began, which concluded on February 20, 2009. That day, the construction group reached an agreement with the Italian company to sell them 25% of Endesa for €11.1 billion.)

The exit was strategic, not forced. In 2009, it acquired more than two GW of renewable assets as part of the operation agreed with the Enel electric group where Acciona stopped participating in Endesa.

What did Acciona gain from this remarkable adventure?

First, capital gains that strengthened the balance sheet. Second, over 2 GW of renewable assets that became the foundation for future growth. Third, invaluable experience operating at the highest levels of the utility industry. Fourth, validation that a construction company could compete in energy markets.

The Endesa episode reveals something essential about the Entrecanales family's approach to capital allocation. They were willing to make bold bets—the original stake represented a massive commitment relative to Acciona's market capitalization. But they were equally willing to exit when the strategic calculus changed, converting a utility investment into the renewable assets that would define the company's future.

Key Inflection Point #2: The Nordex Merger & Vertical Integration (2016–2023)

If the Endesa battle demonstrated Acciona's willingness to play at the highest stakes, the Nordex transaction revealed a more subtle form of strategic genius: the patience to build positions over time, waiting for the right moment to consolidate.

Acciona Windpower had been manufacturing wind turbines since the late 1990s. By 2015, the subsidiary had become a significant player, but it faced the classic dilemma of being too small to compete with industry giants like Vestas and Siemens Gamesa, yet too significant to abandon.

The solution was a merger with Nordex, a German manufacturer with complementary strengths.

The integration of Acciona Windpower into the listed German company creates a new European powerhouse in wind turbine manufacturing, with combined sales of €3.4 billion in 2015. Following the transaction, Acciona will become Nordex's principal shareholder with a 29.9% stake.

The German firm seized the initiative when it agreed to buy Acciona's wind turbine manufacturing arm, Acciona Wind Power (AWP), in October for €785 million, in cash and shares.

The strategic logic was compelling. The two wind turbine manufacturers have complementary technologies and market footprints, with Nordex's strong presence in Europe a good match for Acciona Windpower's established position in North and South America. In total, the two companies have installed 18 GW of wind power capacity in more than 25 countries.

The deal generated significant one-time gains. Acciona obtained €596 million in net profit in the first half of 2016, close to six times the €103 million reported in the first half of 2015, basically as a result of €657 million in extraordinary earnings from the merger of Acciona Windpower and Nordex.

But the real value lay in the stake itself. Acciona maintained its position and gradually increased ownership over the following years.

Acciona will launch a full takeover of Nordex after increasing its majority share in the German turbine manufacturer to 36.27%.

The 2023 consolidation marked the culmination of this patient strategy. Acciona's revenue rose 52% in 2023 compared to 2022 to reach €17.02bn and a net profit of €541m, an increase of 22.6%. The group acquired a majority stake in Nordex, holding a 47.08% stake since 1 April, 2023.

Nordex – the wind turbine manufacturer in which Acciona has held a 47.08% stake since April 1st, 2023 – contributed €5.27 billion, corresponding to the nine months of consolidation, in a year that marks a major turning point for the subsidiary as it contributed a positive gross operating profit.

The news is also positive for Acciona, which holds a 47% stake in Nordex and fully consolidates the company in its financial statements.

The Nordex position gives Acciona something rare in the renewable energy industry: vertical integration. The company can develop projects using its own engineering expertise, install turbines manufactured by a company it controls, and operate the resulting assets for decades. This integration creates competitive advantages in cost management, technology development, and project execution.

The Nordex turnaround has been remarkable. The wind turbine manufacturer now expects a full-year 2025 EBITDA margin between 7.5% and 8.5%, up from its previous forecast of 5.0% to 7.0%.

For investors, the Nordex story illustrates a key aspect of Acciona's strategic approach: the willingness to take minority positions, wait patiently as circumstances evolve, and consolidate when the timing is right. This long-term orientation—enabled by family control—differentiates Acciona from competitors focused on quarterly performance.

Key Inflection Point #3: The Acciona Energía IPO (2021)

The Acciona Energía IPO in July 2021 represented something rarer than a typical equity offering: it was a strategic repositioning that gave the renewable energy business access to capital markets while maintaining family control.

Corporación Acciona Energías Renovables ("Acciona Energía" or the Company), a subsidiary of Acciona and one of the leading pure renewable energy companies globally, has completed its successful c. €1.52bn IPO (assuming exercise of the overallotment option) on the Spanish stock exchanges on 1st July 2021. The offering represents the largest IPO in Spain in the last 6 years and the largest European renewable energy IPO in the last 5 years.

The strategic rationale reflected management's view of global energy markets. The company said green transition programmes around the world were generating record demand for sustainable infrastructure and, in particular, clean energy. Recovery plans following the pandemic had a similar focus, while investor interest in companies meeting strict environmental, social, and governance criteria was growing rapidly.

Acciona Energía, a leading 100% renewable energy company, that will start trading on the Spanish stock exchanges next Thursday July 1st, has closed its initial public offering (IPO) at €26.73 per share, which values the company at more than €8.8 billion.

The execution was impressive. As a result, the book was already covered within the first 24-hours of bookbuilding and ended up 2.4x oversubscribed at the pricing level. The extremely high-quality book consisted of over 220 lines, with allocations skewed over 80% to Long-Only investors.

Following the settlement of the IPO, Acciona will own 85% of Acciona Energía's capital.

The IPO had multiple objectives. First, it gave Acciona Energía access to equity capital markets, supporting ambitious growth plans. The company had announced goals of reaching 20 GW of installed capacity by 2025 and over 30 GW by 2030.

Second, the listing provided independent valuation of the energy business, creating transparency for shareholders.

Third, the offering generated proceeds that strengthened the balance sheet while the parent company maintained controlling ownership.

Since July 1, 2021, Acciona Energía has been listed on the Madrid, Barcelona, Bilbao and Valencia Stock Exchanges.

The post-IPO growth has been substantial. Total revenue in 2021 reached €2,472 million, an increase of 39.8% compared to 2020. By June 2022, the company had joined the Ibex-35, Spain's main stock index.

Acciona's stake in Acciona Energía stood at 90.03% as of 30 June 2025.

The IPO also demonstrated something important about Acciona's governance philosophy. Rather than spinning off the energy business entirely or selling a majority stake to private equity, the family maintained control while accessing public capital. This approach balances the need for growth capital with the long-term orientation that has defined the company's strategy.

The Modern Acciona: Three Pillars of Growth

Today's Acciona operates across three major divisions, each with distinct competitive advantages and growth trajectories.

Energy Division

Acciona Energía is the world's largest 100% renewable energy company. With no fossil fuel legacy in more than 30 years of experience, it has one of the world's leading expert teams in the design of integrated solutions to decarbonise the planet.

Present in 25 countries in 2023, with clean generation from 6 renewable technologies. We are the world's 7th largest wind operator by net installed capacity, second in Spain and leader in Latin America.

Total installed capacity amounts to 15.35 gigawatts.

The geographic distribution reflects decades of strategic expansion: With presence in 24 countries & 15.4 GW of total installed capacity in FY 2024. USA (3.0 GW), Spain (5.7 GW), Australia (1.9 GW), Chile (0.9 GW), Mexico (1.5 GW).

The asset base spans multiple technologies. We are a significant international player in solar photovoltaics, with 2,951 MW of own capacity. In Europe, we pioneered the operation of a solar PV plant plus storage, and in 2020 we commissioned the first floating, grid-connected plant in Spain.

Acciona Energía has solid experience in this technology as it operates assets that are over 100 years old, including an 89 MW pumped-storage plant, which is a high-value storage technology for a back-up system.

Infrastructure Division

Acciona's Infrastructure division posted revenues of €8.15 billion (+5.5%) in 2024, a record figure.

Australia and Southeast Asia (35%) contributed the highest percentage of revenues, followed by Latin America (22%), Spain (20%), Europe, the Middle East and Africa (17%) and North America (6%).

The total aggregate infrastructure backlog once again broke its all-time record and increased to €53.84 billion (+58.1%), with almost 90% outside Spain.

Australia has emerged as a particularly important market. Since 2002, Acciona has grown to become one of the leading players in the Australian infrastructure market. The company has delivered a number of landmark projects such as the Legacy Way tunnels (in Brisbane), a 41-kilometer bypass for the Toowoomba Highway and a desalination plant in Adelaide.

Acciona, in consortium with Ferrovial, has been awarded the contract to build the central section of Sydney Metro West, the new underground rail line that runs through a large part of Australia's largest city. The contract is valued at AU$1.96 billion (€1.24 billion) and is one of the major infrastructure projects under development in the state of New South Wales.

Water Division

Acciona's Water business posted revenues of €1.19 billion euros (-2%) and EBITDA of 93 million euros (-1.7%). Although the lower contribution of projects in the completion phase affected results, the start of new projects such as the Alkimos (Australia) and Ras Laffan 2 (Qatar) desalination plants positions the company for sustained growth in the coming years.

The company is a global leader in the construction of desalination plants using reverse osmosis technology, which is more efficient, less energy intensive and has a smaller carbon footprint than conventional thermal desalination.

Acciona works to ensure water management and universal access to this resource. The company processes, purifies, reuses, desalinates and manages water for over 100 million people in more than 30 countries around the world.

In 2009, the company was awarded one of its most emblematic projects in Australia, the Adelaide desalination plant. The plant has a capacity of 300,000 m³ per day and serves a population of two million.

Recent Financial Performance & Strategic Direction

The 2024 results demonstrated the diversified model's resilience. Acciona closed 2024 with a net profit of €422 million (-22%), record revenues of €19.19 billion (+12.7%) in an environment of lower electricity prices, and gross operating profit (EBITDA) of €2.45 billion (+24%), achieving its targets for the year.

For comparative purposes, the 2023 accounts included a non-recurring positive impact derived mainly from the change in the consolidation method of Nordex. The group's results for 2024 reflect the robust evolution of margins in both Infrastructure (9.4%, +2.3pp) and Nordex (4.1%, +4.1pp), as well as a strong pace of renewable capacity installation (+2GW).

The first half of 2025 showed continued momentum. Acciona posted an attributable net income of €526 million in the first half of 2025 (+353.3%), a profit 4.5 times higher than the same period last year. The company has been boosted by four main factors: the high profitability of the Infrastructure business, the evolution of electricity prices, the successful implementation of Acciona Energía's asset rotation plan, and the growing, solid performance of Nordex.

Acciona's revenues for the first half of 2025 totalled €9,231 million, reflecting growth of 5.2% vs H1 2024, and consolidated EBITDA reached €1,557 million, compared to €990 million in the prior year, an increase of 57.3%. EBITDA from Operations came at €1,113 million, 12% higher than in H1 2024, with all business lines growing year-on-year.

Asset rotation has become a key component of strategy. During the first half of the year, the company closed the sale of 626MW of hydropower assets in Spain for €1 billion. In addition, it reached an agreement for the sale of the 136MW San Juan de Marcona wind farm in Peru for US$253 million (€218 million).

The aggregate Infrastructure backlog rose to almost €57.85 billion (+70.7%), mainly thanks to new contracts awarded in Australia (the Central West Orana transmission network), Brazil (sanitation in Paraná) and the United Arab Emirates (a desalination plant on Saadiyat Island).

Competitive Landscape & Strategic Position

Acciona operates in competitive markets across all three divisions, but its positioning is distinctive.

In renewable energy, the primary competitors are Iberdrola and EDP. Iberdrola's primary competitors include Acciona, Endesa, Naturgy and 10 more.

However, Acciona's positioning as a "pure play" renewable company without fossil fuel legacy creates differentiation. After Acciona, the greenest utilities are Iberdrola (Spain), China General Nuclear, E.On (Germany), Orsted (Denmark), NextEraEnergy (US), China Three Gorges, EDP (Portugal), China National Nuclear Corp and Enel (Italy).

Iberdrola is the largest producer of wind power, and the world's second largest electricity utility by market capitalisation. As of 2023, the company operates a capacity of 62,045 MW, of which 41,246 MW are from renewable sources worldwide.

The scale difference is significant—Iberdrola operates approximately four times the renewable capacity. But Acciona's 100% renewable profile and integrated infrastructure capabilities create a different value proposition.

The company's ESG credentials are exceptional. Acciona and Acciona Energía have reached the top 5% of S&P Global's ESG Score ranking in the S&P Sustainability Yearbook 2023. Acciona Energía, in its first full year of data reporting, is the most sustainable company in the utilities sector in Spain and the second most sustainable one in the world.

Thanks to this long-term approach, in 2024 Acciona Energía was present in the main sustainability ratings, reaching a Tier 1 status in all of them, which places it as an ESG leader in the electricity sector and in the business landscape as a whole.

Bull and Bear Cases

Bull Case

The Family Advantage: The Entrecanales family's controlling stake enables long-term strategic thinking impossible for widely-held competitors. The Endesa adventure, the patient Nordex build-up, and the sustainability pivot all reflect multi-decade time horizons.

Pure-Play Premium: As institutional investors face mounting pressure to decarbonize portfolios, Acciona's 100% renewable profile commands valuation premiums. The company has no stranded asset risk from fossil fuel investments.

Vertical Integration: The combination of renewable development capabilities, Nordex turbine manufacturing, and infrastructure construction creates competitive advantages in project execution and cost management.

Infrastructure Backlog: With €54+ billion in infrastructure backlog, the company has exceptional revenue visibility. This provides stability while the energy business scales.

Geographic Diversification: Presence in 24+ countries reduces regulatory and political risk. The strong position in Australia, a market with ambitious renewable targets, provides growth optionality.

Water Scarcity Theme: The water division is positioned to benefit from one of the defining challenges of climate change. Desalination and water treatment demand are structural growth markets.

Bear Case

Electricity Price Volatility: Energy revenues are sensitive to power prices. Despite prices falling by 29.5% on an annual basis impacted 2024 results. Prolonged price weakness would pressure margins.

Leverage Concerns: The company carries significant debt to fund expansion. Net debt to EBITDA ratio: decreased to 2.9x. While manageable, rising interest rates increase financing costs.

Nordex Execution Risk: The turbine manufacturing business has historically generated volatile margins. Despite recent improvements, the wind turbine industry remains intensely competitive.

Construction Risk: Large infrastructure projects carry execution risk. Cost overruns or delays on major contracts could impact profitability.

Spanish Regulatory Exposure: Despite international diversification, significant assets remain in Spain. Changes to renewable energy policy or power market regulation could affect returns.

Scale Disadvantage: Iberdrola operates four times the renewable capacity. Larger competitors may have advantages in technology development, financing costs, and market access.

Porter's Five Forces Analysis

Competitive Rivalry (Moderate-High): The renewable energy sector is intensely competitive with well-capitalized players like Iberdrola, Orsted, and NextEra. However, Acciona's integrated model and ESG credentials provide differentiation.

Threat of New Entrants (Moderate): Capital requirements and technical expertise create barriers. However, private equity and sovereign wealth funds have entered the sector aggressively.

Buyer Power (Moderate): Power purchase agreements are increasingly competitive, but Acciona's long-term contracts provide price visibility.

Supplier Power (Low-Moderate): The Nordex stake reduces exposure to turbine pricing volatility. The company's scale provides procurement leverage.

Threat of Substitutes (Low): In the energy transition, renewable energy substitutes for fossil fuels, not the reverse. Battery storage and hydrogen present opportunities rather than threats.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Moderate advantages from project scale and operational efficiency.

Network Effects: Limited applicability in current business lines.

Counter-Positioning: Strong. The pure renewable positioning means competitors with fossil assets cannot match Acciona's ESG profile without transformational change.

Switching Costs: Moderate. Long-term PPAs create revenue stickiness.

Branding: Strong in ESG and sustainability markets. The "world's greenest utility" positioning resonates with institutional investors.

Cornered Resource: The Nordex manufacturing capability and integrated development expertise represent difficult-to-replicate assets.

Process Power: The company's track record in complex project execution, developed over 90+ years, creates operational advantages.

Key Metrics to Track

For investors following Acciona, three KPIs merit particular attention:

1. Installed Renewable Capacity Growth (GW): This is the fundamental driver of long-term value in the energy business. The company's target was 20 GW by 2025 and 30 GW by 2030. Current installed capacity of 15.4 GW (as of 2024) against these targets indicates execution progress and growth trajectory.

2. Infrastructure Backlog (€ billions): With €54+ billion in committed work, this metric provides 5+ years of revenue visibility. Watch for the mix between Spain and international markets, as well as the proportion in concessions versus construction-only contracts. The concessions business generates higher-margin recurring revenue.

3. Net Debt / EBITDA Ratio: Currently around 2.9x, this metric indicates balance sheet health and capacity for continued investment. Management targets remaining below 4x. Asset rotation proceeds will be critical to maintaining leverage discipline while funding growth.

Material Legal/Regulatory Considerations

The company operates in heavily regulated markets across multiple jurisdictions. Key regulatory factors include:

Spanish Power Market Reform: The company remains exposed to Spanish electricity market design and pricing mechanisms. Historical regulatory changes have impacted renewable returns.

EU Taxonomy Alignment: Acciona reports high alignment with EU sustainable finance taxonomy requirements, but continued evolution of these standards could affect financing access and costs.

Credit Ratings: The company maintains investment-grade ratings. We expect funds from operations (FFO) net leverage to fall back to its 'BBB-' negative sensitivity of 4.5x by end-2025, following a significant breach in 2024. Rating agency dynamics warrant monitoring.

Australian Market Regulation: Given significant exposure to Australia, changes to renewable energy targets, transmission investment, or capacity market design could impact project economics.

Conclusion: The Sustainability Pioneer's Next Chapter

The Acciona story is fundamentally about reinvention—a family construction business that recognized the energy transition decades before most investors and positioned itself accordingly. The journey from Franco-era dam building to the world's greenest utility required strategic patience, bold capital allocation, and a willingness to transform.

As CEO of Acciona, José Manuel Entrecanales has transformed the construction and engineering company into a global infrastructure, energy and water services company with over 50,000 employees and presence in 52 countries.

What distinguishes Acciona is not just what it does, but how it approaches long-term value creation. The Endesa adventure, the Nordex build-up, the Acciona Energía IPO—each represented calculated risks executed with the patience that family control enables.

The challenges ahead are real. Electricity price volatility, competition from larger rivals, and the complexities of operating across multiple regulated markets all present risks. But Acciona enters this next chapter with €54 billion in infrastructure backlog, 15+ GW of renewable capacity, control of a major turbine manufacturer, and leadership in water infrastructure.

Global leader in the development and management of Infrastructure, Water, Services and Renewable Energies. Family-owned company with more than 100 years of history → Long-term focus & stable shareholder base. From a construction company to a sustainable solutions provider.

For investors seeking exposure to the energy transition through an operator with generational perspective and proven execution capabilities, Acciona offers a distinctive combination: the stability of a century-old family enterprise with the growth potential of clean energy markets.

The concrete foundations laid by José Entrecanales Ibarra in 1931 have evolved into a platform for addressing the defining challenges of the 21st century. Whether that platform can deliver returns commensurate with its ambitions remains the question every investor must answer for themselves.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube