Alm. Brand: Denmark's 233-Year Insurance Reinvention

A Story of Strategic Focus and Nordic Insurance Consolidation

What happens when a 233-year-old company founded to protect Danish farmers from fire decides to completely reinvent itself in the 21st century? The answer lies in Copenhagen's Southern Freeport, where Alm. Brand Group's modernist headquarters—designed by PLH Architects and perched on Middle Pier—stands as a physical metaphor for a company straddling two worlds: an ancient origin in agricultural mutual insurance and a future as one of Scandinavia's most strategically focused non-life insurers.

Alm. Brand A/S was founded in 1792 as a mutual fire insurance company for Danish farmers. Following its acquisition of Codan's Danish operations in 2022, Alm. Brand A/S became the second-largest provider of non-life insurance in Denmark, capturing approximately 18% of the market.

This is a story of strategic focus—how selling a bank, acquiring a competitor, and returning to core insurance roots transformed a 230-year-old company. It's a masterclass in corporate reinvention that holds lessons for any investor studying how legacy businesses can successfully navigate the treacherous waters of industry consolidation and digital disruption.

Alm. Brand's largest shareholder is Alm. Brand af 1792 fmba, which holds 47.8% of the shares in Alm. Brand A/S. This unique ownership structure—with a mutual foundation retaining near-majority control—shapes everything about how the company operates, balancing long-term thinking against modern capital markets pressure.

The Danish Insurance Context: Why This Small Market Matters Enormously

Picture a country of 5.9 million people—smaller than many metropolitan areas—yet hosting one of the world's most sophisticated and highly penetrated insurance markets. Denmark's Nordic welfare state model creates a distinctive backdrop for insurance: comprehensive public healthcare reduces the need for health insurance, but mandatory coverages for property, motor vehicles, and workers' compensation create baseline demand that's remarkably stable.

The insurance sector in Denmark is characterized as highly developed with particularly high penetration and density. Property and casualty insurance in Denmark has shown a favorable underwriting result with relatively low expense ratios. The number of non-life insurance companies has decreased from 113 in 2008 to below 60 in 2020.

That consolidation trend—from 113 companies to below 60 in just over a decade—tells the story of an industry in transformation. Scale economics are driving smaller players out or into the arms of larger acquirers. The Danish non-life insurance market had total gross written premiums of $10.5 billion in 2022, representing a compound annual growth rate (CAGR) of 1.2% between 2017 and 2022. The property segment accounted for the market's largest proportion in 2022, with total gross written premiums of $3.5 billion, equivalent to 33.6% of the market's overall value.

The regulatory environment creates both stability and barriers. The Danish Financial Supervisory Authority (FSA) is responsible for the regulation and supervision of insurance companies. Denmark is primarily a civil law country. The central legislation for insurance in Denmark is the Danish Insurance Contracts Act, which mainly governs the relationship between the insurer and the insured. However, the Insurance Contracts Act is heavily supplemented by case law, and Danish insurance law today is a combination of statutory regulation, case law, and general contracts and tort law.

The competitive landscape remains dominated by a handful of major players. The Danish non-life insurance company Tryg was the leading company on the Danish non-life insurance market as of early 2022. The company had at that point a market share of about 23 percent, followed by Topdanmark, Codan, and Alm. Brand. Tryg Forsikring is one of the largest players in the Danish insurance market with a market share of approximately 24.7%. They offer a wide range of insurance for both private and business.

The market is growing modestly but steadily. The Denmark Life & Non-Life Insurance Market is projected to register a CAGR of 6.5% during the forecast period (2025-2030). For investors, this means a mature market where growth comes primarily from market share gains and disciplined pricing rather than explosive expansion.

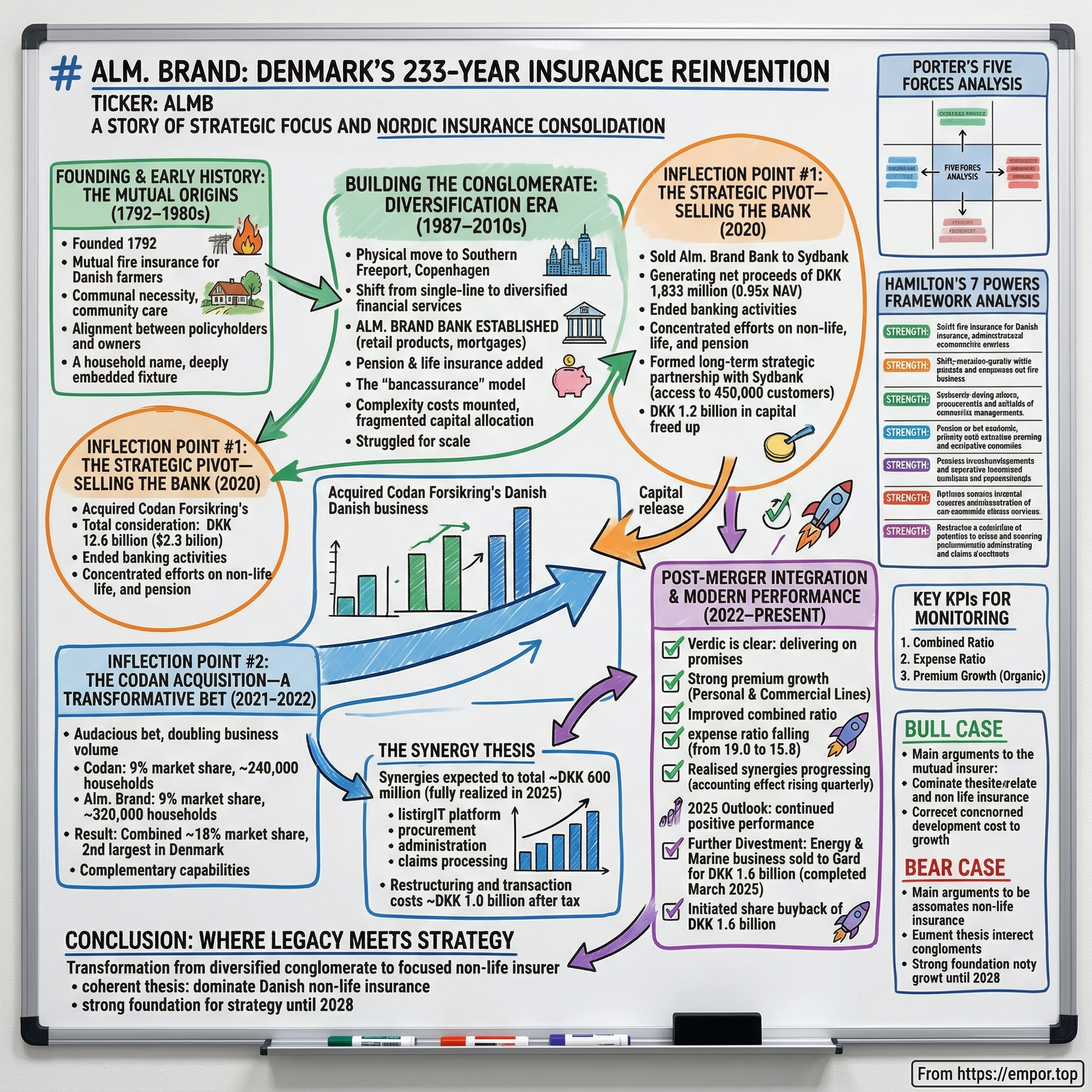

Founding & Early History: The Mutual Origins (1792–1980s)

Imagine Denmark in 1792: a predominantly agricultural nation where a single fire could devastate a farming family's entire livelihood. No government safety net existed for such calamities. Communities relied on each other—and from this communal necessity, Alm. Brand was born.

Alm. Brand af 1792 is a Danish financial services group operating within the markets for non-life, life and pension insurance. The company was founded in 1792 and its activities were originally limited to mutual fire insurance of buildings in rural communities.

Founded in 1792, Alm. Brand began as a mutual insurance company created for the protection of Danish farmers and their property—a mission rooted in community care and sustainability. What began as a national farmers' fire insurance association has since transformed into a dynamic, publicly traded conglomerate that operates in the fields of non-life insurance, life and pension insurance, and banking solutions.

The mutual structure—where policyholders were also owners—created alignment that would prove crucial across centuries of operation. Unlike stock companies driven by quarterly profit demands, mutual insurers could take a generational view, pricing for sustainability rather than maximizing short-term returns.

Alm. Brand A/S holds cultural significance. In the public imagination, the company represents a dependable tradition amidst change. Moreover, it ties modern Danish citizens to their agricultural history, recalling a time when communities came together.

The broader importance of Alm. Brand A/S to Denmark can be interpreted as both historical and contemporary. Historically, it has stood shoulder to shoulder with institutions that helped shape Danish welfare society. In modern times, it continues to adapt and expand, reflecting not just the strength of the company, but the evolving aspirations of the Danish people.

This cultural resonance matters for understanding Alm. Brand's competitive position. Alm. Brand A/S is one of Denmark's oldest surviving corporations, surviving revolutions, economic depressions, world wars, and digital upheavals. This impressive staying power has made Alm. Brand not only a household name but also a deeply embedded fixture in the national economy.

The mutual foundation structure that persists today—Alm. Brand af 1792 fmba—maintains institutional continuity stretching back to these origins, even as the operating company became publicly traded.

Building the Conglomerate: Diversification Era (1987–2010s)

Since 1987, Alm. Brand has been based in Company House on Middle Pier in the Southern Freeport area of Copenhagen. The physical move to Copenhagen's waterfront signaled a transformation in ambition: from rural roots to urban sophistication, from single-line insurer to diversified financial services conglomerate.

What began as a national farmers' fire insurance association has since transformed into a dynamic, publicly traded conglomerate that operates in the fields of non-life insurance, life and pension insurance, and banking solutions.

The diversification thesis seemed compelling at the time. Insurance companies, with their large investment portfolios and extensive customer relationships, appeared natural candidates to expand into banking and asset management. Cross-selling opportunities beckoned. Distribution synergies promised efficiencies. The "bancassurance" model—integrating banking and insurance—was sweeping through European financial services.

Alm. Brand established Alm. Brand Bank, entering a highly competitive Danish banking market. The bank specialized in retail products—mortgages, deposits, personal lending—targeting the same middle-market customers already buying insurance. On paper, the combination made sense: one customer relationship, multiple product categories, shared infrastructure costs.

The pension and life insurance additions followed similar logic. Danish workers needed retirement savings vehicles. Employers needed group insurance programs. Why not keep those premium flows within the Alm. Brand ecosystem?

But complexity costs mounted. Running a bank required different regulatory expertise than running an insurance company. Capital allocation became fragmented. Management attention split across multiple competitive fronts. The bank faced brutal competition from Denmark's larger banking players, struggling to achieve meaningful scale.

By the late 2010s, a reckoning approached. The conglomerate structure that seemed so promising had become a strategic straightjacket.

Inflection Point #1: The Strategic Pivot—Selling the Bank (2020)

Every great corporate transformation has its crossing-the-Rubicon moment. For Alm. Brand, that moment came on October 1, 2020, when CEO Rasmus Werner Nielsen announced the sale of Alm. Brand Bank to Sydbank.

Alm. Brand A/S entered into a conditional agreement with Sydbank A/S on the sale of Alm. Brand Bank A/S, generating net proceeds of DKK 1,833 million, equivalent to 0.95 times the net asset value.

The numbers told a stark story about why the bank had to go. Despite decades of effort, Alm. Brand Bank remained subscale in a market dominated by giants like Danske Bank and Nordea. The price—0.95 times book value—reflected the strategic reality: the business was worth more to a consolidator like Sydbank than as a standalone operation within Alm. Brand.

The divestment marks an end to Alm. Brand's long-standing commitment to banking activities, allowing the group to concentrate all of its efforts on developing an even more customer-oriented and competitive Alm. Brand focused on non-life insurance, life insurance and pension in close interaction with strategic partners.

But here's where the deal got clever: rather than simply walking away, Alm. Brand structured a strategic partnership that preserved distribution access while shedding operational complexity.

At the same time, Alm. Brand formed a long-term strategic partnership with Sydbank that provides access to offering insurance products to Sydbank's approximately 450,000 customers. This partnership will strengthen Alm. Brand's distribution network and support our ambitions for growing the insurance business.

The sale of the bank will reduce the group's capital requirement target by the capital allocated to the bank, approximately DKK 1.2 billion in total, which includes a continued capital requirement of approximately DKK 150 million primarily related to the above-mentioned mortgage deed exposure.

This capital release proved crucial. The DKK 1.2 billion freed up by exiting banking would become ammunition for what came next—the largest acquisition in Alm. Brand's history.

Sydbank A/S completed the acquisition of Alm. Brand Bank A/S from Alm. Brand A/S in 2020.

Inflection Point #2: The Codan Acquisition—A Transformative Bet (2021–2022)

The call came in June 2021. Intact Financial Corporation of Canada and Tryg of Denmark were jointly acquiring RSA Insurance Group. As part of untangling that complex multinational deal, they needed a buyer for Codan's Danish business. Would Alm. Brand be interested?

Alm. Brand is pleased to announce that it has entered into a binding agreement with Intact Financial Corporation and Tryg A/S, through their jointly-owned subsidiary, whereby Alm. Brand will acquire Codan Forsikring A/S's Danish business. The Acquisition is currently expected to complete during the first half of 2022 following the transfer by Intact and Tryg of the Danish business of Codan Forsikring into a Danish legal entity incorporated for such purpose.

Codan DK was acquired by Alm. Brand for a total consideration of DKK 12.6 billion ($2.3 billion), subject to post-closing adjustments. Intact is receiving 50% of the proceeds, commensurate with its stake in Codan DK.

This was not a modest acquisition. At DKK 12.6 billion, it represented an audacious bet for a company of Alm. Brand's size. The deal would fundamentally reshape the Danish insurance landscape.

Chairman of the Board of Directors Jørgen Hesselbjerg Mikkelsen: "With the acquisition of Codan DK, the Board of Directors sets a clear strategic course, significantly enhancing the company's long-term competitive position. We will double our business volume and become one of the largest players in the attractive Danish non-life insurance market with a strong capital position and very exciting development opportunities going forward."

Codan is headquartered in Copenhagen and has approximately 1,000 employees. The company was established in 1916 and is the fourth-largest non-life insurance company in Denmark with a market share of approximately 9%. Codan assists around 240,000 households and 50,000 corporate customers.

The company was established in 1792 and is the third-largest non-life insurance company in Denmark with a market share of approximately 9%. Non-life Insurance assists around 320,000 households and 90,000 corporate customers.

The math was elegant: two companies each with roughly 9% market share combining to create an 18% market share position. Following the Acquisition, Alm. Brand will become the second-largest non-life insurance company in Denmark and the largest non-life insurance company focused entirely on the Danish market with a market share of approximately 18% and a more diversified customer portfolio, estimated at about 700,000 households and corporate customers.

The Synergy Thesis

Every acquisition lives or dies on synergy execution. Alm. Brand laid out an ambitious roadmap.

Alm. Brand still expects to realise substantial synergies and economies of scale from the common IT platform, procurement, administration, lease costs, shared functions and claims processing, thereby improving the profitability and competitive strength of the combined company. Synergies are expected to total around DKK 600 million before tax and to be fully realised in 2025, with an accumulated effect of around DKK 90 million in 2022, DKK 240 million in 2023, DKK 450 million.

With a view to realising the synergies, Alm. Brand expects to incur restructuring and transaction costs of approximately DKK 1.0 billion after tax.

Regulatory Approval

The Danish Competition Council's approval came on April 27, 2022, with an interesting finding that speaks to market structure.

On April 27th 2022 the Danish Competition Council has approved Alm. Brand's acquisition of the Danish activities of Codan Forsikring.

The investigations show among other things that Alm. Brand are focused on small to medium-sized businesses including agricultural businesses, while Codan primarily focuses on bigger businesses including international shipping companies and companies in the field of renewable energy (so-called "Tech Lines").

The Danish Competition and Consumer Authority's preliminary investigations did not give rise to any concerns regarding the competition on this market. The investigations showed that the parties could not be said to be close competitors, and also that neither of the parties can be said to have played an important role for competition before the merger.

The finding that Alm. Brand and Codan were "not close competitors" revealed something crucial: the combination brought genuinely complementary capabilities rather than pure overlap elimination.

The New Structure

Alm. Brand has completed the acquisition of Codan Forsikring's Danish business ("Codan"), thereby creating the second-largest non-life insurance company in Denmark with a more diversified customer portfolio, estimated at about 700,000 households and corporate customers. The new Alm. Brand Group will consist of eight business areas, each headed by an Executive Vice President who will be in charge of managing and developing the business area across the group's brands. Five business areas are directly related to insurance operations and customer service (Industry, Commercial, Private, Bancassurance and Claims Services), while three business areas (Business Development & Technology, Finance and Staff Functions) are key to supporting the group's operations and development.

Alm. Brand is headquartered in Copenhagen and has approximately 1,400 employees. The company was established in 1792 and is the third-largest non-life insurance company in Denmark with a market share of approximately 9% prior to the acquisition of Codan DK. Non-life insurance assists around 320,000 households and 90,000 corporate customers. Following the acquisition Alm. Brand will have approximately 2,400 employees and a market share of approximately 18%, thus making it a number two in the Danish non-life market.

Post-Merger Integration & Modern Performance (2022–Present)

The true test of any transformative acquisition comes in execution. By late 2024 and into 2025, the verdict was becoming clear: Alm. Brand was delivering on its promises.

The strong performance underlines the strength of our large, Denmark-based group. We're entering 2025 in good shape, and we're well on the way to realising the targets we set for the merger of Codan and Alm. Brand.

Synergy Execution

The insurance service result for Q4 2024 was a profit of DKK 440 million (Q4 2023: DKK 287 million), equivalent to a combined ratio of 84.5 (Q4 2023: 89.3), driven by favourable developments both in Personal Lines and Commercial Lines. Insurance revenue grew by 6.2% to DKK 2,845 million (Q4 2023: DKK 2,680 million), driven by sustained strong premium growth of 7.2% in Personal Lines and premium growth of 5.1% in Commercial Lines. The undiscounted underlying claims ratio fell by 1.9 percentage points to 63.8% (Q4 2023: 65.7%), driven by the effects of profitability-enhancing measures in Personal Lines. The expense ratio fell to 18.0 (Q4 2023: 19.0), and the implementation of synergy initiatives generated a positive accounting effect of DKK 138 million in Q4 2024 (Q4 2023: DKK 75 million).

Guidance for the investment result is lifted by DKK 50 million to DKK 300 million. Insurance service result for Q3 2025 was a profit of DKK 535 million (DKK 400 million), equivalent to a combined ratio of 82.2 (85.7). The result was driven by sustained strong premium growth, an improved claims experience and positive developments in the expense ratio. Insurance revenue grew at a highly satisfactory rate of 7.5% to DKK 3,006 million (DKK 2,796 million), driven in particular by premium growth of 9.9% in Personal Lines. The undiscounted underlying claims experience improved by 3.2 percentage points to 61.4, supported by particularly favourable developments in Commercial Lines driven by the implemented profitability-enhancing measures and realised synergies. The expense ratio improved significantly to 15.8 (17.1), reflecting the group's objective of lowering the cost level.

The implementation of synergy initiatives progressed according to plan and generated a positive accounting effect of DKK 158 million in Q3 2025 (DKK 118 million), causing Alm. Brand Group to expect to realise synergies in an amount of more than DKK 600 million in 2025. Satisfactory investment result of DKK 66 million (DKK 133 million), with shares and bonds contributing favourably to the result. The consolidated profit before tax was DKK 452 million (DKK 376 million). High SCR ratio of 254% in Q3 2025 based on PIM approval. CEO Rasmus Werner Nielsen on the Q3 financial results: "We generated robust financial results in the third quarter, reflecting a sustained inflow of new customers to our company and generally satisfactory developments in our business activities."

During the earnings call, CEO Rasmus Werner Nielsen expressed satisfaction with the synergy progress, stating, "Synergies are materializing just as we plan." CFO Andreas reinforced this confidence, saying, "We remain confident that the synergy for the full year will add up to DKK 600 million."

Customer Growth and Claims Processing

As of 2023, the company employs approximately 1,600 people and serves nearly 700,000 private and commercial customers. Thus, confirming its pivotal footprint in both Danish society and the broader financial ecosystem.

CEO Rasmus Werner Nielsen is pleased with the performance: "Seen overall, 2024 was a year in which many people in Denmark needed their insurance company. We helped process claims from more than 430,000 of our customers. In particular, motor-related and travel insurance claims gave rise to many enquiries, whereas weather-related events were not as dramatic as in 2023."

2025 Outlook and Further Divestment

The strategic focus sharpened further with the divestment of the Energy & Marine business.

Alm. Brand today entered into a conditional agreement with Gard on the divestment of its Energy & Marine business for a price of DKK 1.6 billion, equivalent to a cash payment of DKK 1.13 billion combined with the equity freed up in the transaction. The net proceeds including the freed-up equity are expected to be distributed to the shareholders of Alm. Brand A/S after obtaining relevant regulatory approvals. The distribution will be made in the form of extraordinary dividend, share buy-backs or a combination of these.

The divestment of the Energy & Marine business was completed on 3 March 2025. As a result, Alm. Brand Group initiated a share buyback programme for a total amount of DKK 1.6 billion.

After completing the divestment of the Energy & Marine business in March, we're now a fully-focused Danish non-life insurer with a healthy balance between Personal Lines and Commercial Lines. The first quarter also yet again demonstrated that we're on track to meet the ambitious targets we set in connection with the merger of Alm. Brand and Codan.

Alm. Brand Group is set to continue the positive performance in 2025 and expects to report an insurance service result of DKK 1.5-1.7 billion excluding run-off gains or losses. The profit guidance includes synergies in an amount of DKK 600 million.

The expected increase relative to the result realised in 2024 is driven by improved profitability in both Personal Lines and Commercial Lines due to the implementation of profitability-enhancing initiatives. The expense ratio is expected to be about 17% in 2025, and the combined ratio excluding run-offs is expected to be about 85.5-87.5.

The Competitive Landscape

Understanding Alm. Brand requires understanding its competitive context. The Danish non-life market has undergone seismic consolidation, fundamentally reshaping competitive dynamics.

Tryg: The Market Leader

Tryg is the leading non-life insurance company in the Nordic region. We are the largest player in Denmark and the forth-largest in Norway. In Sweden we are the third-largest company in the market.

Tryg's pan-Nordic scale gives it advantages Alm. Brand cannot match. With operations across Denmark, Norway, and Sweden, Tryg can spread technology investments across a much larger premium base.

The Sampo-Topdanmark Deal: Reshaping the Market

In 2024, the Finland-based insurance group, Sampo Group, which already owns the Nordic insurance company If Insurance, also acquired Topdanmark Insurance, making Sampo Group the second-largest insurance group in Denmark after Tryg Insurance.

On 7 August 2024, Sampo plc published the offer document and prospectus for its recommended public exchange offer to acquire all of the outstanding shares in Topdanmark A/S, and on 16 September 2024, Sampo plc announced a successful outcome of the offer, with Sampo plc holding approximately 92.6 percent of the shares in Topdanmark A/S, excluding treasury shares.

Today If has grown to be the largest P&C insurance company in the Nordics and the Baltics. This market leading position will be solidified through the integration of Topdanmark, increasing If's market share in the Nordic market as well as in the Danish market to over 20%. Topdanmark is a successful company and the integration that will be completed during 2025 brings more than 2,000 new, highly skilled colleagues to If.

This transaction fundamentally changes the Danish landscape. What was once a four-player market (Tryg, Topdanmark, Codan, Alm. Brand) has consolidated into effectively three major groups: Tryg, Sampo/If (including Topdanmark), and Alm. Brand (including Codan).

Other Competitive Dynamics

For a long time, there was not much activity on the M&A market in Denmark in relation to insurance companies; however, in recent years, there has been some movement. In 2023, Gjensidige Insurance acquired PenSam Insurance along with its 26,000 customers and 30 employees.

Digital Disruption

One example is the Swedish insurance company Hedvig Försäkring AB, which established a Danish branch in 2021. The company offers home, travel, accident and housing insurance, as well as a separate insurance package for students. Insurance claims are primarily processed through the Hedvig mobile app, which, according to the company, has an average claims processing time of six minutes (the fastest recorded processing time so far is only 195 seconds). Due to the digital nature of the process, this insurance product mostly appeals to a younger demographic. Insurers like Topdanmark, ETU Insurance, Popermo and others have also introduced apps to make their services more accessible to their clients. It seems that a generational shift is well underway in the Danish insurance industry, as it moves away from traditional methods of doing insurance business towards more digital solutions.

The Denmark Life & Non-Life Insurance Market is experiencing notable trends such as an increasing emphasis on digitalization, with companies striving to enhance customer experiences through technology. Additionally, sustainability has become a growing factor, prompting insurers to consider environmental impacts in their offerings.

Porter's Five Forces Analysis

Threat of New Entrants: MODERATE

Entry barriers are substantial but not insurmountable. The number of non-life insurance companies has decreased from 113 in 2008 to below 60 in 2020. This consolidation trend suggests incumbents enjoy advantages that discourage entry.

Denmark is primarily a civil law country. The central legislation for insurance in Denmark is the Danish Insurance Contracts Act. Danish insurance law today is a combination of statutory regulation, case law, and general contracts and tort law.

Capital requirements and regulatory compliance create meaningful barriers. However, digital-first entrants like Hedvig demonstrate that technology can lower barriers in commoditized personal lines. The threat of new entrants is moderate—established brands face protection in complex commercial lines but vulnerability in price-sensitive personal segments.

Bargaining Power of Suppliers: LOW

The reinsurance market is global and competitive. Investment management capabilities can be built in-house. Technology vendors are substitutable. Claims services can be insourced. Supplier power is minimal.

Bargaining Power of Buyers: MODERATE-HIGH

Comparison platforms and price transparency have shifted power toward consumers, particularly in personal lines. Low switching costs compound this pressure. However, commercial and agricultural lines—where Alm. Brand has heritage strength—remain more relationship-driven. Multi-product bundling creates switching friction.

Threat of Substitutes: LOW-MODERATE

There are some statutory insurances for everyone in Denmark. Mandatory coverages provide baseline demand. Government social programs provide some substitution for certain risks, but self-insurance remains impractical for most customers. The threat of substitutes is limited.

Competitive Rivalry: HIGH

Dominance in the Denmark Life & Non-Life Insurance Market lies with a mix of established local companies, reflecting the country's preference for homegrown insurers. The market is moderately consolidated, featuring several key players that balance competitive pressures while ensuring comprehensive service offerings. Data suggest a blend of conglomerates and specialized firms, with local giants like Tryg and PFA Pension among the leaders providing a robust landscape for consumers.

Price competition in commoditized personal lines remains intense. The Sampo-Topdanmark deal intensifies scale dynamics further. Competitive rivalry is high, with the primary battlegrounds being customer acquisition costs, pricing discipline, and claims efficiency.

Hamilton's 7 Powers Framework Analysis

1. Scale Economies: STRONG (Post-Codan)

Alm. Brand still expects to realise substantial synergies and economies of scale from the common IT platform, procurement, administration, lease costs, shared functions and claims processing.

The Codan acquisition fundamentally changed Alm. Brand's scale position. IT platform costs spread across nearly double the premium base. Claims processing efficiency improves with volume. With approximately 18% market share, Alm. Brand now possesses sufficient scale to compete with larger rivals on cost. The expense ratio decline from 19.0 to 15.8 demonstrates this power manifesting in results.

2. Network Economies: MODERATE

Bancassurance partnerships create distribution network effects. The strategic partnership with Sydbank provides access to offering insurance products to Sydbank's approximately 450,000 customers. The multi-brand strategy (Alm. Brand, Codan, Privatsikring) creates segment-specific networks. Network effects are present but not dominant—this is not a winner-take-all business.

3. Counter-Positioning: HISTORICALLY STRONG, NOW EVOLVING

Alm. Brand began as a mutual insurance company for the protection of Danish farmers—a mission rooted in community care and sustainability.

Historically, Alm. Brand's agricultural and rural focus positioned it where urban-focused competitors were weak. The mutual foundation ownership provided legitimacy that pure commercial insurers couldn't match. However, the Codan acquisition moves toward mainstream positioning. Counter-positioning remains relevant in agricultural segments but less distinctive in urban markets.

4. Switching Costs: MODERATE

Multi-product bundling creates switching friction. Agricultural customers have specialized needs creating lock-in. Commercial relationships and claims history create switching costs. Personal lines remain relatively easy to switch, limiting this power in consumer segments.

5. Branding: STRONG

Alm. Brand A/S holds cultural significance. In the public imagination, the company represents a dependable tradition amidst change.

With a legacy deeply rooted in mutual responsibility and community service, the company has adapted to the demands of the modern world without losing sight of its traditional values. Brand A/S proves that legacy and innovation are not mutually exclusive—they are synergistic.

The 233-year heritage creates trust that newer competitors cannot replicate. In insurance—where customers pay premiums for years before potentially making claims—trust is foundational competitive advantage. The multi-brand portfolio (Alm. Brand for agricultural/rural, Codan for urban commercial) allows tailored brand positioning without dilution.

6. Cornered Resource: MODERATE

The mutual foundation's majority control creates unique ownership stability. Alm. Brand's largest shareholder is Alm. Brand af 1792 fmba, which holds 47.8% of the shares in Alm. Brand A/S. This ownership structure provides protection against hostile acquisition while maintaining market discipline through public listing. Agricultural customer relationships spanning generations represent accumulated institutional knowledge.

7. Process Power: EMERGING

Claims processing efficiency, underwriting discipline, and digital transformation represent ongoing process improvements. The synergy realization demonstrates operational execution capability. Process power is emerging but not yet a distinctive competitive advantage.

Key KPIs for Monitoring

For investors tracking Alm. Brand's ongoing performance, three metrics deserve focused attention:

1. Combined Ratio — The ultimate measure of underwriting profitability in non-life insurance. A combined ratio below 100 indicates profitable underwriting; below 90 indicates strong performance. Alm. Brand's trajectory from 89.3 in Q4 2023 to 84.5 in Q4 2024 to 82.2 in Q3 2025 demonstrates improving fundamentals. The 2025 target range of 85.5-87.5 should be tracked quarterly.

2. Expense Ratio — Measures operational efficiency and synergy capture. The decline from 19.0 to 15.8 demonstrates merger synergies flowing to the bottom line. The target of approximately 17% for 2025 reflects integration progress. Sustained improvement indicates scale economies are materializing.

3. Premium Growth (Organic) — With market share already significant, organic growth separates market share gainers from share losers. Personal Lines growth of 9.9% in Q3 2025 demonstrates competitive strength. Premium growth above market rates indicates competitive positioning improvements.

Bull Case

Scale Leadership in a Consolidating Market: The Codan acquisition positioned Alm. Brand as the second-largest Danish non-life insurer at precisely the moment consolidation economics favor scale players. The synergy delivery validates execution capability. The combined ratio guidance for 2025 is set at 84.5-86.5, with an expense ratio target of 17%. The company expects to realize the full DKK 600 million in synergies from the Codan integration by the end of 2025.

Focused Pure-Play Strategy: Selling the bank and divesting Energy & Marine created a focused Danish non-life insurer. Management can allocate 100% of attention to one business in one market. After completing the divestment of the Energy & Marine business in March, we're now a fully-focused Danish non-life insurer with a healthy balance between Personal Lines and Commercial Lines.

Unique Ownership Structure: The mutual foundation provides capital stability while public listing ensures market discipline. This hybrid structure allows long-term thinking without sacrificing accountability.

Heritage Brand Advantage: In a trust-dependent business, 233 years of continuity represents irreplaceable intangible assets. In the public imagination, the company represents a dependable tradition amidst change.

Shareholder Returns: The combination of dividends and share buybacks demonstrates capital discipline. Alm. Brand maintains a strong capital position, with a Solvency Capital Requirement (SCR) ratio of 194%. This robust capital base supports the company's dividend policy, which prescribes a pay-out ratio of at least 80%.

Bear Case

Compressed Market Position: With Sampo/If absorbing Topdanmark, Alm. Brand faces competitors with significantly larger Nordic footprints. Scale disadvantages in technology investment could emerge over time.

Premium Pricing Pressure: The Danish market is competitive and transparent. Intense Competition: The Denmark insurance market is highly competitive, with numerous domestic and international players vying for market share, leading to pricing pressure and reduced profit margins.

Digital Disruption Risk: Insurance claims are primarily processed through the Hedvig mobile app, which, according to the company, has an average claims processing time of six minutes. Digital-native competitors can undercut on cost while providing superior customer experience in commoditized lines.

Weather and Climate Risk: In response to climate change, insurers are looking to set new conditions precedent, especially for house owners in exposed areas, including requirements for climate protection. The Danish "Insurance and Pension" industry organisation has warned that failure to properly implement proper climate protection measures, both at the level of the state and of the individual insured, may lead to a scenario where housing owners in some areas will not be able to insure their homes.

Single Market Concentration: Unlike Tryg or Sampo/If with Nordic diversification, Alm. Brand is concentrated entirely in Denmark. Economic or regulatory changes affecting Denmark would disproportionately impact results.

Integration Risk: While synergies are materializing, merger integrations can encounter late-stage challenges. IT system consolidation remains ongoing.

Material Considerations

Regulatory Environment

The Danish Financial Supervisory Authority (FSA) is responsible for the regulation and supervision of insurance companies. Solvency II requirements shape capital allocation. The FSA's approval was required for both the Codan acquisition and the Energy & Marine divestiture.

Capital Position

High SCR ratio of 254% in Q3 2025 based on PIM approval. The partial internal model approval enhances capital efficiency. This strong solvency position supports the dividend policy and provides cushion for adverse scenarios.

Accounting Judgments

Insurance accounting involves significant estimates around loss reserves. Run-off gains and losses reflect prior period reserving accuracy. The company's consistent positive run-off results suggest conservative reserving practices.

Conclusion: Where Legacy Meets Strategy

Alm. Brand's transformation from diversified financial conglomerate to focused non-life insurer represents a masterclass in strategic clarity. Selling the bank freed capital. Acquiring Codan delivered scale. Divesting Energy & Marine sharpened focus. Each move reinforced a coherent thesis: dominate Danish non-life insurance through disciplined underwriting, operational excellence, and heritage brand strength.

Our interim financial statements also show that we are close to successfully completing the merger of Codan and Alm. Brand and realising our ambitious financial targets for 2025. We owe this achievement to the outstanding commitment and performance of all Alm. Brand Group employees. Our efforts have given us a strong foundation as a fully-focused Danish non-life insurer and a strong platform for launching our strategy for the period until 2028, which we look forward to announcing at our capital markets day in November.

The company's current market capitalization of approximately DKK 25-26 billion reflects the successful transformation. What remains to be seen is whether the strategic moat—scale in a consolidating market, heritage brand, disciplined execution—proves durable against pan-Nordic giants and digital disruptors alike.

For investors seeking exposure to European insurance consolidation with a unique ownership structure and proven execution capability, Alm. Brand presents a compelling case study in how legacy companies can reinvent themselves without abandoning their roots. The Danish farmers who founded this company in 1792 would recognize neither the headquarters nor the technology—but they would understand the fundamental mission: communities protecting each other against life's uncertainties.

That mission, after 233 years, endures.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube