Alma Media: The Marketplace Arbitrage

I. Introduction: The Newspaper Company That Isn't

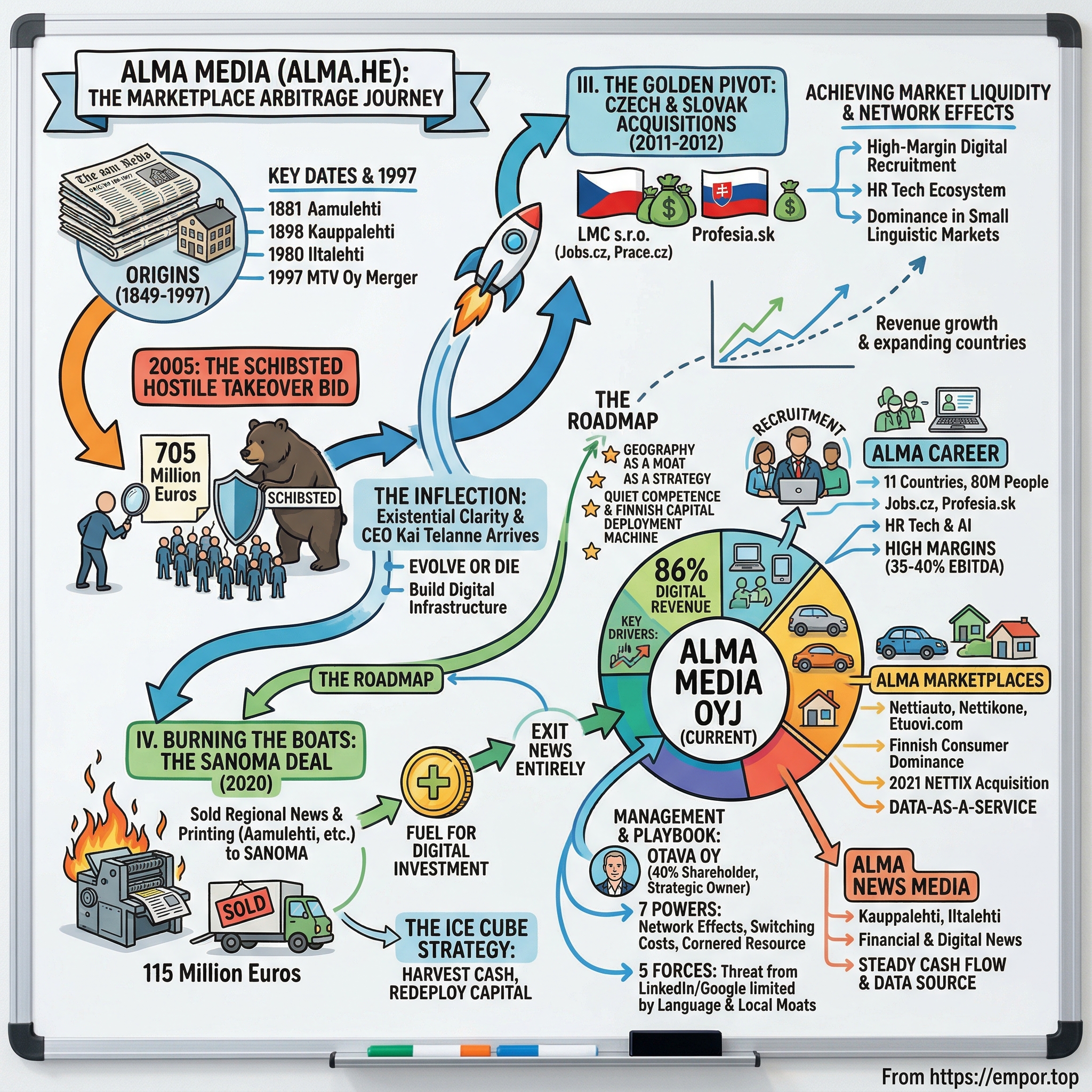

Picture Helsinki in 2005. A modest Finnish media company, barely known outside the Nordics, is fighting for its life. Schibsted, the Norwegian media giant with a war chest and a pan-Scandinavian appetite, has just launched a hostile takeover bid valuing Alma Media at roughly 705 million euros. The headlines write themselves: another legacy newspaper swallowed by a bigger fish. The story, it seemed, was over before it began.

Fast-forward twenty-one years. Alma Media is not dead. It is not a newspaper company. It is not even, in any meaningful sense, a "media" company in the way most people understand the term. It is a high-margin digital recruitment and marketplace machine, pulling in over 327 million euros in annual revenue with an adjusted operating margin north of 25 percent, and nearly 86 percent of that revenue coming from digital sources. The printing presses that once defined its identity now belong to a competitor. The television channels that gave it scale were sold off decades ago. What remains is something far more valuable: a portfolio of dominant online marketplaces across Finland, the Czech Republic, Slovakia, Croatia, and a string of smaller Central European nations.

The thesis here is deceptively simple. Alma Media executed one of the most successful "burning of the boats" transitions in European corporate history. It took a declining asset base of regional newspapers and broadcast licenses, harvested the cash flows, and systematically redeployed that capital into digital recruitment portals and consumer marketplaces in markets where Silicon Valley could not easily follow. The key insight was not technological. It was geographic. In non-English-speaking markets with populations of five to ten million, local network effects create moats that LinkedIn, Google, and Indeed struggle to breach. Alma did not try to out-innovate Big Tech. It out-localized them.

What makes this story worth telling is not just the outcome but the sequence of decisions that produced it. A hostile takeover defense that forced existential clarity. A contrarian acquisition in the Czech Republic that skeptics mocked. A gut-wrenching sale of the company's founding newspaper to fund the digital future. And a CEO who has been in the chair for over two decades, quietly compounding value while flashier European media peers lurched from one crisis to the next.

This is a story about geography as a moat, patience as a strategy, and the rare courage it takes for a century-old institution to sell its soul in order to save its future. The roadmap runs through Helsinki, Prague, and Bratislava, with stops at the intersection of classified advertising, labor economics, and the quiet competence of Finnish capital deployment.

II. Succinct Origins and The Schibsted Inflection

The roots of Alma Media reach back to 1849, when the Finnish Literature Society established a printing company in a country that would not gain independence for another sixty-eight years. The publications that would eventually form the backbone of the company — Aamulehti in 1881, Kauppalehti in 1898, Iltalehti in 1980 — were not just newspapers. They were institutions of Finnish civic life, read at breakfast tables in Tampere and Helsinki for generations. By the late twentieth century, these titles were owned by Aamulehti Corporation, one of Finland's largest publishers, a company that had grown through steady regional consolidation and a deep connection to the industrial heartland around Tampere.

The defining structural event came in April 1997, when Aamulehti Corporation merged with MTV Oy, Finland's leading commercial television company and the operator of MTV3, the country's most-watched commercial channel. The combined entity was christened Alma Media Corporation and began operating on April 1, 1998. On paper, it was a bold convergence play: newspapers, evening tabloids, local papers, radio, television, and early internet properties, all under one roof, with combined turnover approaching half a billion dollars. In practice, it was a classic late-1990s media conglomerate — diversified, complex, and about to be tested by forces nobody fully appreciated.

Then came 2005, and with it, the moment that would define Alma's trajectory for the next two decades.

Schibsted, the Norwegian media powerhouse that had already pioneered online classifieds across Scandinavia with platforms like Finn.no and Blocket, launched a hostile takeover bid for Alma Media. The offer was 11.40 euros per A-share, a 30 percent premium over the previous day's close, valuing the entire company at approximately 705 million euros. Schibsted's CEO, Kjell Aamot, had not contacted Alma's management beforehand. This was a textbook hostile approach, and the strategic logic was clear: Schibsted wanted to consolidate Nordic media, neutralize a competitor, and extend its classified advertising dominance into Finland.

The bid was widely interpreted as a flanking maneuver against Bonnier, the Swedish media dynasty that held a 33 percent stake in Alma and significant positions across Scandinavian broadcasting. The defense that followed was messy, political, and ultimately successful. Finnish regulators, Bonnier's countermoves, and the sheer complexity of Alma's shareholder structure made a clean acquisition impossible. Aamot eventually conceded defeat. But the resolution carried a price: Bonnier and investment firm Proventus ended up purchasing Alma's television division — MTV3, SubTV, Radio Nova, and related broadcasting assets. Alma Media survived, but it survived smaller, stripped of its highest-profile consumer brand.

What looked like a defeat in the moment turned out to be the most important thing that ever happened to the company. The Schibsted fight forced a brutal reckoning. Without television, Alma could no longer pretend to be a diversified media conglomerate. It was a newspaper publisher with some early internet experiments, competing in a small Nordic market where print advertising was already beginning its irreversible decline. The question was existential: evolve or die.

This is where Finnish cultural DNA played an underappreciated role. There is a concept in Finland called "sisu" — a word that resists easy translation but approximates a stubborn, quiet determination to endure hardship and push through adversity. Finnish companies, as a rule, do not panic loudly. They do not pivot with Silicon Valley theatrics. They assess, they plan, and they execute with a kind of grim patience. At Alma Media, the post-Schibsted period produced exactly this response. The new leadership, which would arrive in the form of Kai Telanne taking the CEO role on April 1, 2005 — the same year as the hostile bid — began systematically experimenting with digital classified advertising, recruitment portals, and online marketplaces. While American newspaper companies were still debating whether to put their content behind paywalls, Alma was already building the digital infrastructure that would eventually replace print advertising entirely.

The Schibsted fight did something else, too. It created institutional memory. Every strategic decision Alma made over the following two decades carried the implicit understanding that standing still meant being acquired or made irrelevant. Digital was not an option. It was the only path to independence. That sense of urgency, born from a near-death experience, would prove invaluable when the time came to make truly bold moves.

III. The Golden Pivot: The LMC Acquisition

In December 2011, Alma Media's board approved a transaction that, in retrospect, changed the company's destiny. Alma agreed to acquire LMC s.r.o., a Prague-based company that operated Jobs.cz and Prace.cz — the two leading online recruitment portals in the Czech Republic — along with TopJobs.sk in Slovakia. The enterprise value was 35.4 million euros, paid in cash at closing, with an additional earn-out of up to 3.9 million euros tied to LMC's 2012 financial performance. The deal closed on January 2, 2012.

To understand why this mattered, you have to understand what the Czech Republic looked like as a market at the time. A country of roughly ten million people, recently emerged from the post-communist transition, with a labor market that was rapidly digitizing but still lacked a dominant online recruitment platform with the polish and functionality of Western European equivalents. Jobs.cz had built exactly that dominance. It was the place Czech employers went to find talent, and the place Czech job seekers went to find work. In the language of marketplace economics, it had achieved liquidity — that critical mass where both sides of the market show up because the other side is already there.

The skeptics had a field day. Why was a Finnish newspaper company spending tens of millions of euros on Czech job boards? The cultural distance was vast. Finland and the Czech Republic share no language, limited trade history, and sit on opposite sides of the European continent. The acquisition looked like the kind of random geographic diversification that media companies attempt when their core business is shrinking and they are casting about for growth.

But the skeptics missed the strategic logic entirely. Alma was not buying a Czech company. It was buying a marketplace monopoly in a high-growth labor market, at a price that reflected Central European valuations rather than Western European or American ones. At roughly ten times EBITDA, the LMC deal was cheap by any standard of marketplace economics. Compare that to the valuations that online recruitment and classified platforms commanded in the following decade — StepStone, Scout24, Adevinta — all trading at twenty to forty times EBITDA during peak periods. Alma bought the same type of asset at a fraction of the price, simply because it was in Prague rather than Berlin or Stockholm.

The acquisition was also an arbitrage of operational capability. LMC had the local market knowledge and the user base. Alma brought Finnish operational discipline, technology investment frameworks, and experience scaling digital products. The combination proved potent. Over the following years, LMC did not just maintain its market position — it expanded, deepening its product offering from simple job listings into a broader HR technology ecosystem that included applicant tracking, employer branding tools, and AI-powered candidate matching.

But Alma was not done. The LMC acquisition was the first move in a broader Central European recruitment strategy. In November 2012, Alma acquired Profesia.sk, the dominant online recruitment platform in Slovakia, along with related operations in neighboring markets. The total investment across the Czech Republic, Slovakia, Croatia, and the Baltic states eventually reached approximately 70 million euros. Each acquisition followed the same playbook: find the market leader in a small linguistic market, buy it at reasonable multiples, and integrate it into a shared technology platform while preserving local operational autonomy.

The results were transformative. By the mid-2010s, what Alma internally called its recruitment business — later formalized as the Alma Career segment — was regularly contributing more than half of the group's operating profit. A Finnish newspaper company had, through disciplined M&A in a region most Western European investors ignored, built a high-margin digital recruitment franchise spanning eleven European countries and reaching approximately eighty million people.

The financial profile of these recruitment businesses was extraordinary. Marketplace businesses with dominant positions in small linguistic markets tend to exhibit winner-take-all dynamics. Once all the employers and all the job seekers are on your platform, the cost of switching is enormous — not because of contractual lock-in, but because of network effects. A recruiter at a Czech manufacturing firm does not care about global scale. She cares about whether the platform has the most relevant Czech-speaking candidates. Jobs.cz had them. That was the moat.

For investors, the LMC acquisition illustrated a principle that recurs throughout Alma's history: the willingness to deploy capital into unfashionable markets at attractive prices, combined with the patience to let compound growth do its work. The Czech recruitment market was not a sexy investment thesis in 2012. It was not covered by sell-side analysts in London or New York. It was not discussed at media conferences. It was simply a good business, bought at a fair price, in a market where Alma could add genuine operational value. Sometimes the best investments are the ones nobody is talking about.

IV. Burning the Boats: The Sanoma Deal

On February 11, 2020, Alma Media did something that would have been unthinkable a decade earlier. It signed an agreement to sell Alma Media Kustannus Oy — its regional news media business — and Alma Manu Oy — its printing operations — to Sanoma Media Finland for an enterprise value of 115 million euros. The transaction transferred 365 employees and a portfolio of publications that included Aamulehti, the very newspaper whose parent company had created Alma Media in the first place.

To appreciate the emotional weight of this decision, imagine General Motors selling the Chevrolet brand. Or Coca-Cola divesting its flagship cola. Aamulehti was not just a newspaper. It was the founding asset, the institutional identity, the thing that generations of Alma employees had built their careers around. Regional newspapers in Finland carried civic significance — they were the connective tissue of local communities, the paper that arrived on doorsteps in Tampere and Pori and Jyväskylä every morning. Selling them was not a financial decision in isolation. It was an act of institutional self-reinvention.

The strategic logic, however, was ruthlessly clear. Regional newspapers in Finland were a melting ice cube. Print advertising revenues had been declining for over a decade, accelerated by the shift of local classified advertising — jobs, housing, cars — to the exact type of digital platforms that Alma itself operated. The newspapers still generated cash flow, but the trajectory was unmistakable: declining readership, aging demographics, rising production costs, and competition from free digital news sources. Every euro of management attention spent on slowing the decline of print was a euro not spent on accelerating the growth of digital.

Management, led by Kai Telanne, made the calculation that the 115 million euros from the sale — generating a capital gain of approximately 58 million euros — was worth more as fuel for digital investment than the newspapers were worth as ongoing operations. The Finnish Competition and Consumer Authority approved the deal on March 19, 2020, and the transaction closed on April 30, 2020, just as COVID-19 was reshaping every assumption about media consumption and digital adoption.

The timing was both fortunate and instructive. The pandemic accelerated exactly the trends that justified the sale: digital adoption surged, remote work made online recruitment platforms essential infrastructure, and physical newspaper distribution became logistically challenging. Alma entered the pandemic as a leaner, more digital company, while the regional newspapers it had sold faced the full brunt of advertising collapse during lockdowns.

It is worth pausing to compare Alma's choice with the path taken by other legacy media companies facing the same existential question. The New York Times chose to become a subscription news company, investing heavily in digital journalism and building one of the world's most successful paywalled news products. Axel Springer in Germany chose a hybrid approach, acquiring digital classified companies while maintaining its tabloid and news operations. Schibsted split itself into a marketplace company (Adevinta) and a media company. Each approach reflected different assumptions about where value creation would concentrate.

Alma chose the most radical path: exit news entirely (except for financial and professional media under the Alma Talent umbrella, later renamed Alma News Media) and concentrate capital on marketplaces and recruitment. The implicit bet was that marketplace businesses — with their network effects, high margins, and recurring revenue characteristics — would compound value faster than subscription news businesses, which require continuous editorial investment and face persistent competition from free alternatives. Whether Alma sold too early or just in time is a question that depends on your time horizon, but the financial results since 2020 suggest the decision was vindicated. The capital freed from the newspaper sale was redeployed into digital growth, contributing to the transformation that pushed Alma's digital revenue share from roughly 70 percent at the time of the sale to nearly 86 percent by the end of 2025.

The Sanoma deal also sent an unmistakable signal to the market, to employees, and to potential acquisition targets: Alma Media was a digital company now. The boats were burned. There was no going back to the comfort of print. This clarity of identity, as much as the financial proceeds, may have been the deal's most valuable outcome.

V. Current Management: The Architects of the New Alma

Kai Markus Telanne took over as President and CEO of Alma Media on April 1, 2005 — the same year the company was fighting off Schibsted's hostile bid. Born in 1964, trained as an economist, Telanne had previously served as CEO of Kustannus Oy Aamulehti, the publishing subsidiary, since January 2001. His appointment to lead the entire group came at the moment of maximum uncertainty, and he has held the position ever since — over twenty-one years and counting, making him one of the longest-serving media CEOs anywhere in Europe.

Long CEO tenures carry inherent risks. Leaders can become complacent, wedded to strategies that worked in one era but fail in the next. Boards can lose the willingness to challenge a familiar face. But Telanne's tenure illustrates the upside of stability when paired with genuine strategic evolution. He has presided over the sale of the television business, the acquisition spree in Central European recruitment, the divestiture of the founding newspaper, and the Nettix marketplace acquisition — each representing a fundamental reshaping of the company's portfolio. This is not a CEO who got comfortable. This is a CEO who used the security of a long tenure to make decisions that a shorter-tenured executive, worried about quarterly earnings reactions, might have avoided.

Telanne's compensation structure reflects the digital transformation mandate. His total compensation of approximately 2.49 million euros is weighted roughly 38 percent toward base salary and 62 percent toward performance-linked bonuses and stock-based incentives. Critically, the incentive schemes for Alma's top management have been tied specifically to digital revenue growth and earnings per share — metrics that reward the transition away from print rather than the defense of legacy businesses. When management's personal wealth is directly linked to digital growth, the alignment between shareholder interests and executive decision-making becomes significantly tighter.

Behind Telanne sits the dominant shareholder, Otava Oy. Understanding Otava is essential to understanding why Alma has been able to execute a multi-decade transformation that required patience, capital, and tolerance for short-term disruption. Otava is one of Finland's oldest and largest publishing houses, a family-controlled enterprise with roots stretching back to 1890. It is not a private equity fund with a five-year exit horizon. It is not a public market activist demanding quarterly buybacks. It is a long-term, strategic owner with the temperament and the balance sheet to support bold moves.

Otava's stake in Alma has grown steadily over the years, crossing 10 percent in 2017, reaching roughly 29 percent by 2019, and crossing 30 percent in June 2023 — a threshold that triggered a mandatory tender offer under Finnish securities law. The offer, at 9.10 euros per share, attracted remarkably low acceptance: only about 962,000 shares, or 1.17 percent of the total, were tendered. Minority shareholders overwhelmingly chose to hold, signaling that they viewed the offer price as inadequate and the company's long-term value as substantially higher. The stock has since traded in the 13 to 16 euro range, vindicating the holdouts.

In March 2026, Otava acquired an additional 700,000 shares, pushing its stake to approximately 40 percent — a level that grants effective controlling shareholder status under Finnish regulations and triggered a new mandatory notification to the Finnish Competition and Consumer Authority. The question of what Otava intends to do with its controlling position — maintain the status quo, take the company private, or pursue further strategic transactions — hangs over the stock. But the historical pattern suggests patience rather than aggression. Otava has behaved as a steward, not a raider.

The management philosophy that Telanne has implemented, sometimes referred to internally as the "Alma Way," emphasizes decentralization. The Czech, Slovak, Croatian, and Baltic businesses operate with significant local autonomy — local management, local product decisions, local commercial teams. What they share is a global technology stack, centralized data infrastructure, and group-level strategic direction. This model recognizes a fundamental truth about marketplace businesses in small linguistic markets: local knowledge matters more than global scale. A product manager in Prague understands Czech hiring patterns better than anyone in Helsinki ever could. The role of the center is to provide capital, technology, and strategic guardrails, not to micromanage local operations.

This decentralized structure also serves as a talent retention mechanism. Ambitious managers in Central European subsidiaries are not relegated to executing orders from a distant Finnish headquarters. They run their own businesses with genuine P&L responsibility. This autonomy attracts entrepreneurial talent that might otherwise leave for startups or global tech companies, and it creates a pipeline of tested leaders who understand both local market dynamics and group-level strategic thinking.

VI. The Hidden Engines: Segments and New Initiatives

Walk into the headquarters of LMC in Prague — a modern, open-plan office in one of the Czech capital's renovated commercial districts — and you will find something that looks nothing like a newspaper company. Software engineers cluster around monitors displaying real-time marketplace data. Product managers whiteboard AI matching algorithms. Sales teams work phones and Slack channels, closing deals with Czech, Slovak, and Croatian employers. This is Alma Career, and it is the engine that makes the rest of the company possible.

Alma Career operates online recruitment services across eleven European countries, with its strongest positions in the Czech Republic (Jobs.cz, Prace.cz), Slovakia (Profesia.sk), Croatia (MojPosao.net), and the Baltic states (CV Online). Approximately 800 recruitment professionals serve a network that reaches roughly 80 million people. Full-year 2025 revenue for the segment reached approximately 105.6 million euros, and the margins are the story: Alma Career has historically operated at EBITDA margins in the range of 35 to 40 percent and above, reflecting the inherent economics of a dominant two-sided marketplace where incremental revenue drops almost entirely to the bottom line.

But Alma Career has evolved beyond simple job listings. The business now encompasses a suite of HR technology tools — applicant tracking systems, employer branding solutions, salary benchmarking data, and increasingly, AI-powered candidate matching. The strategic vision is to become not just where employers post jobs, but the operating system for how Central European companies manage their entire recruitment workflow. The deeper these tools integrate into corporate HR processes, the higher the switching costs become. A company that has built its entire hiring pipeline around Jobs.cz does not casually migrate to LinkedIn just because LinkedIn sends a sales email. The integration is too deep, the local candidate pool too essential, the retraining cost too high.

Then there is Alma Marketplaces, the segment that emerged from the 2021 Nettix acquisition and the subsequent reorganization. This is where Alma dominates Finnish consumer marketplaces, particularly in automotive and housing. The crown jewels are Nettiauto — Finland's leading car marketplace, reaching 2.5 million Finns weekly — along with Nettimoto for motorcycles, Nettikone for heavy machinery, and Etuovi.com for residential real estate.

The Nettix acquisition deserves particular scrutiny because it illustrates how Alma thinks about marketplace economics. In March 2021, Alma paid 170 million euros in cash for Nettix Oy, acquired from the Otava Group in a related-party transaction. Nettix's 2020 financials showed revenue of 22.5 million euros and EBITDA of 11.2 million euros — a 50 percent EBITDA margin. That implies a purchase price of roughly fifteen times EBITDA, or about seven and a half times revenue. Expensive? Compare it to global comps. AutoTrader UK was taken private in 2014 at roughly twelve times revenue. Adevinta traded at double-digit revenue multiples before its take-private by Permira. Scout24 in Germany has consistently commanded premium valuations. In the context of dominant marketplace businesses with near-monopoly positions, fifteen times EBITDA for the clear market leader in Finnish automotive classifieds was not unreasonable — particularly given the strategic value.

The strategic logic rested on combining Nettix's dominant auto marketplace with Alma's existing properties, including Autotalli.com and a growing data layer across Finnish consumer markets. Post-acquisition, Alma's Finnish marketplace revenue roughly doubled to around 46 million euros annually. Estimated annual synergies of 1.5 million euros from combining advertising sales, support functions, and IT infrastructure were modest in absolute terms but meaningful on a percentage basis. More importantly, the combination created a near-duopoly with Schibsted in Finnish digital classifieds, with Alma dominant in automotive and Schibsted (through Tori.fi and Oikotie) stronger in generalist and some vertical categories.

The full-year 2025 results highlighted Alma Marketplaces as the company's strongest growth engine, with Q4 2025 organic revenue growth reaching 17.5 percent. Full-year segment revenue hit approximately 121.6 million euros, making it the largest of Alma's three segments. The growth drivers were a combination of increasing digital penetration in Finnish real estate transactions, rising average revenue per listing as Alma introduced premium placement and data-enrichment features, and the secular shift of automotive classifieds from print and offline channels to digital platforms.

The third segment, Alma News Media, encompasses the company's retained media properties: Kauppalehti, Finland's leading financial daily; Iltalehti, the country's largest digital news outlet; and a collection of professional and trade publications including Talouselama, Tekniikka and Talous, and Arvopaperi. This segment also includes business data services, legal information platforms, events, and professional training. Full-year 2025 revenue was approximately 113.2 million euros. While Alma News Media lacks the growth profile of the marketplace and career segments, it serves a strategic function: it generates steady cash flows, provides brand visibility in the Finnish business community, and — crucially — feeds data into the consumer marketplace businesses. Housing market data from Kauppalehti's financial coverage, for example, enriches the analytics layer behind Etuovi.com's property valuations.

New initiatives cluster around data-as-a-service and AI applications. Alma has been building proprietary datasets on Finnish car valuations, property prices, and labor market trends — the kind of structured local data that global tech companies find difficult to replicate. Monetizing this data through analytics products, subscription services, and API access represents an emerging revenue stream that leverages Alma's unique position as the operator of multiple marketplace verticals in a single national market. Additionally, Iltalehti won an international award in 2025 for its AI solution in journalism, signaling that even the traditional media arm is investing in next-generation capabilities.

VII. The Playbook: Hamilton's 7 Powers and Porter's 5 Forces

To understand why Alma Media's competitive position is more durable than its modest international profile might suggest, it helps to examine the business through the lens of strategic frameworks that separate temporary advantages from structural ones.

Start with Hamilton Helmer's 7 Powers, and the most potent force in Alma's arsenal: network effects. In the Czech job market, Jobs.cz achieved a state of near-complete liquidity years ago. Every major Czech employer posts positions there because that is where the candidates are. Every Czech job seeker checks Jobs.cz because that is where the positions are. This is the classic two-sided network effect that characterizes dominant marketplaces, and once established, it is extraordinarily difficult to disrupt. A new entrant — whether a local startup or a global platform like LinkedIn — faces a chicken-and-egg problem of catastrophic proportions. Employers will not pay for listings on a platform with few candidates. Candidates will not visit a platform with few listings. The incumbent holds all the liquidity, and liquidity begets liquidity.

The same dynamic plays out in Alma's Finnish marketplaces. Nettiauto is where Finns go to buy and sell cars. Etuovi.com is the default platform for Finnish home listings. These are not brand preferences that clever marketing can shift. They are deeply embedded behavioral patterns, reinforced by years of accumulated listings data, seller ratings, and pricing history. A Finnish car dealer who lists inventory on Nettiauto gets immediate exposure to the national market. A competitor platform offers a fraction of that audience. The switching cost is not contractual — it is economic.

Speaking of switching costs — Helmer's second power — Alma Career has systematically built these into its corporate recruitment products. When a Czech HR department integrates Alma's applicant tracking system into its hiring workflow, connects it to the company's internal HR information system, and trains its recruiters to use the platform's analytics dashboards, the cost of switching to a competitor goes far beyond the subscription price. It includes retraining costs, data migration risks, workflow disruption, and the loss of historical hiring data that informs future recruitment decisions. These enterprise-grade switching costs create what recurring revenue investors love: sticky, predictable cash flows with low churn rates.

The third relevant power is cornered resource. Alma possesses exclusive datasets on Finnish car valuations, property prices, and professional salary benchmarks that no competitor can replicate. These datasets are generated by the marketplaces themselves — millions of transactions, listings, and price points accumulated over years of market leadership. They are not available for purchase. They cannot be scraped from public sources with equivalent depth. And they become more valuable over time as the historical data series lengthens, enabling more sophisticated analytics, pricing models, and predictive tools. This is data as a structural competitive advantage, not data as a buzzword.

Now turn to Porter's Five Forces, and the question that investors most frequently raise: what about the threat of substitutes? Specifically, can LinkedIn or Google for Jobs kill Alma's recruitment business?

The answer is more nuanced than either bulls or bears typically acknowledge. LinkedIn is a legitimate competitive force in white-collar, English-proficient professional recruitment across all of Alma's markets. A Czech software engineer with strong English skills is just as findable on LinkedIn as on Jobs.cz. But move down the skill spectrum — to Czech-speaking factory supervisors, Slovak retail managers, Croatian logistics coordinators — and LinkedIn's relevance drops sharply. These candidates do not maintain English-language LinkedIn profiles. Their employers do not search for them on a global platform. They exist within local-language labor markets where Alma's platforms are the natural habitat.

Google for Jobs, which aggregates job listings from across the web and presents them in Google search results, represents a different kind of threat: disintermediation. If Google becomes the starting point for job searches, it could theoretically reduce direct traffic to Alma's portals and erode their pricing power. In practice, however, Google for Jobs has struggled to gain deep traction in non-English markets where local platforms have established brand loyalty and habit-based usage patterns. A Czech job seeker does not Google "práce v Praze" and click through to a Google aggregation page. She types "jobs.cz" directly into her browser. That direct-navigation behavior — what marketers call "type-in traffic" — is the most defensible form of web traffic because it bypasses search engines entirely.

The linguistic and cultural barriers that protect Alma's markets deserve emphasis because they are often underappreciated by investors accustomed to thinking about technology companies in global terms. Czech, Slovak, Finnish, Croatian — these are not languages that Silicon Valley product teams prioritize. Building a compelling user experience, localized content, and culturally relevant features for a five-million-person market does not justify the investment for a company like Google or Meta. The return on investment is simply too low relative to addressing English-speaking markets of hundreds of millions. This creates a permanent structural advantage for local specialists like Alma who can amortize their technology investment across multiple small markets while maintaining the local depth that global platforms cannot match.

The competitive rivalry within Alma's markets is real but manageable. In Finland, Schibsted operates Tori.fi and Oikotie, creating an effective duopoly in digital classifieds. The two companies compete in some verticals (generalist marketplace, housing) while Alma dominates others (automotive). In the Czech Republic and Slovakia, local competitors exist but lack the scale and liquidity advantages of the Alma Career platforms. The threat of new entrants is low because marketplace businesses exhibit strong winner-take-most dynamics — the cost of building liquidity from scratch in an established market is prohibitively high.

The bargaining power of suppliers (content creators, data providers) is limited because Alma's platforms are primarily user-generated marketplaces where value comes from the network, not from proprietary content. The bargaining power of buyers (advertisers, employers) is moderate — large corporate recruiters can negotiate volume discounts, but the lack of viable alternatives in most of Alma's markets constrains their leverage.

Taken together, the strategic analysis reveals a business that is structurally better positioned than its market valuation suggests. The combination of network effects, switching costs, and cornered resources creates a durability of competitive advantage that is characteristic of the best marketplace businesses globally. The question is not whether these advantages are real — they clearly are — but whether the market is pricing them appropriately.

VIII. Analysis: Bear vs. Bull Case

The bull case for Alma Media rests on a single, powerful observation: this is a business with the financial characteristics of a technology or SaaS company — high margins, high digital revenue share, strong recurring revenue dynamics — that trades at a valuation more appropriate for a traditional media company. As of early April 2026, the company commands a market capitalization of roughly 1.1 billion euros, implying an enterprise value to adjusted EBITDA multiple in the low double digits. Compare that to publicly traded marketplace peers: Scout24 in Germany trades at twenty-plus times EBITDA, REA Group in Australia at thirty-plus times, and even Adevinta (before its take-private) commanded mid-to-high-teen multiples. If the market were to re-rate Alma Media as a marketplace and HR technology company rather than a Finnish media group, the upside could be substantial.

The bull case is further supported by the company's growth trajectory. Full-year 2025 revenue grew 4.6 percent to 327 million euros, with adjusted operating profit up 6.8 percent to 82 million euros. The strongest growth came from the Alma Marketplaces segment, which posted 17.5 percent organic revenue growth in Q4 2025. Digital revenue now represents 86 percent of the total, up from roughly 70 percent just five years ago. The 2026 guidance calls for revenue roughly in line with 2025 and further adjusted operating profit growth — not explosive, but the kind of steady, profitable growth that compounds meaningfully over five and ten-year horizons.

There is also the Otava wildcard. With Otava now holding approximately 40 percent of Alma and steadily increasing its stake, the question of a potential take-private transaction is never far from investors' minds. The failed 2023 tender offer at 9.10 euros — when the stock now trades around 13.40 — demonstrated that minority shareholders believe the company is worth significantly more than Otava has so far been willing to pay. If Otava were to launch another bid at a meaningful premium, it would represent an immediate catalyst for shareholders. Even without a bid, the presence of a patient, strategic controlling shareholder reduces governance risk and supports the long-term transformation strategy.

The bear case, however, is equally worth examining with rigor.

The most significant risk is cyclical exposure to Central European labor markets. Alma Career derives its revenue from employers paying to advertise job openings, and recruitment advertising is one of the most cyclically sensitive categories in all of media. When the Czech or Slovak economy enters recession, companies freeze hiring, and recruitment revenue drops sharply — potentially by 20 to 30 percent in a severe downturn. The Czech Republic's economy, while dynamic and relatively well-managed, is small and open, heavily dependent on manufacturing exports (particularly automotive), and therefore vulnerable to European industrial downturns. A major recession in Germany — the Czech Republic's largest trading partner — would cascade directly into reduced hiring activity in Prague and Brno.

The second bear concern is competitive evolution. While Alma's local moats are real today, they are not permanently unassailable. LinkedIn continues to invest in non-English markets, improving its local-language capabilities and building sales teams in Central Europe. Indeed has expanded aggressively into Continental European markets. Google for Jobs, while slow to gain traction, could become more impactful as Google improves its localization and AI-powered job matching. The structural protection of small linguistic markets may erode over time as AI-powered translation and localization tools reduce the cost for global platforms to serve these markets with locally relevant products.

The third risk is concentration. Alma Media's profitability is heavily dependent on a small number of marketplace positions in a handful of small countries. The Czech recruitment business alone has historically generated a disproportionate share of group profit. This is simultaneously a strength — deep moats in concentrated positions — and a vulnerability. A regulatory change, a new local competitor backed by deep-pocketed investors, or a technological disruption specific to one market could disproportionately impact group-level results.

The Otava concentration itself cuts both ways. A 40 percent shareholder provides stability and long-term orientation, but it also creates minority shareholder risk. Decisions that benefit Otava — such as the related-party Nettix acquisition — may not always align perfectly with minority shareholder interests, even when they are conducted at arm's length. The low free float resulting from Otava's large stake also reduces liquidity, making the stock less attractive to large institutional investors and potentially contributing to the valuation discount.

For investors seeking to monitor Alma Media's ongoing performance, two metrics deserve particular attention. The first is the digital revenue ratio — currently at 86 percent and trending upward. This metric captures the pace of the company's structural transformation and the extent to which its revenue base has migrated from declining print sources to growing digital platforms. A reversal or stagnation in this ratio would signal that the transformation is losing momentum. The second is adjusted EBITDA margin by segment, particularly for Alma Career. This margin reflects the health of the recruitment marketplace's pricing power, cost discipline, and competitive position. A compression in Alma Career's margins — below, say, 30 percent on a sustained basis — would suggest either competitive pressure or cyclical deterioration that warrants concern.

It is also worth noting a few second-layer diligence points. The related-party dynamics between Alma and Otava, particularly around transactions like the Nettix acquisition, deserve ongoing scrutiny from minority shareholders, even though they have historically been conducted through proper governance processes with independent valuations. The company's gearing ratio of 50.5 percent at end of 2025, while improved from 59.6 percent, is not negligible — in a severe cyclical downturn, deleveraging could constrain the company's ability to pursue opportunistic acquisitions. And the concentration of the shareholder register, with Otava at 40 percent and limited institutional float, creates a structural liquidity constraint that may persist indefinitely.

IX. Epilogue and Lessons

So what is Alma Media? A newspaper company? A media group? A technology company? A marketplace operator? The answer, in 2026, is clear in the financial statements even if the market has been slow to update the label. Nearly nine out of every ten euros of revenue come from digital sources. The highest-margin, fastest-growing businesses are online recruitment platforms and consumer marketplaces — two-sided networks with strong competitive positions in markets where geography and language create durable protection. The newspapers that founded the company were sold six years ago. The television channels were sold two decades ago. What remains is a portfolio of digital marketplace assets assembled through patient, disciplined capital allocation over a fifteen-year period.

The story of Alma Media contains a lesson that is easy to state but extraordinarily difficult to execute: you do not have to be a startup to innovate. You can be a company with roots stretching back to 1849, with printing presses and delivery trucks and unionized workforces, and still have the courage to sell your founding business to fund your future. The critical ingredients were not technological brilliance or Silicon Valley-style disruption. They were clarity of strategic vision, patience in execution, alignment between ownership and management, and the willingness to endure short-term pain — the loss of identity, the criticism of skeptics, the emotional cost of selling institutions that generations of employees had built — in exchange for long-term value creation.

Kai Telanne's two-decade tenure at the helm illustrates something that modern corporate governance orthodoxy often overlooks: the value of management stability in executing a transformation that requires a decade or more to complete. A CEO who serves three to five years, the current median for large public companies, simply does not have enough time to execute the kind of portfolio reshaping that Alma accomplished. The LMC acquisition, the regional newspaper divestiture, the Nettix acquisition — these were not decisions that could be conceived, executed, and validated within a single CEO's typical tenure. They required a leader who was willing to make bets whose payoff would be measured in years, not quarters, and a board and controlling shareholder who were willing to extend that patience.

The geographic-moat strategy — the insight that small linguistic markets provide structural protection against global technology giants — is perhaps the most transferable lesson from Alma's story. In a world where investors obsess over total addressable market size, Alma found value in markets that were too small to attract the full force of Silicon Valley competition but large enough to support highly profitable marketplace businesses. Czech is not a language that Google prioritizes. Finnish car classifieds are not a market that Meta cares about. This indifference, paradoxically, is the source of Alma's competitive advantage.

And then there is the "ice cube" strategy: the disciplined harvesting of cash from a declining business to fund investment in a growing one, without diluting shareholders through equity issuances. Alma funded its digital transformation primarily through operating cash flow and the proceeds of asset sales — the television business, the regional newspapers — rather than through share issuances or excessive leverage. The share count remained stable while the business composition transformed entirely. Existing shareholders participated fully in the value creation, rather than seeing their ownership diluted by capital raises to fund a transformation that primarily benefited future shareholders.

Whether Alma Media is a "category king" in the Acquired sense — a company that defines and dominates a category so thoroughly that competitors are permanently relegated to secondary positions — is a question that depends on how you define the category. In Czech online recruitment, the answer is clearly yes. In Finnish automotive classifieds, also yes. In the broader category of "European digital marketplace conglomerate," Alma is a credible player but not the dominant one — Schibsted and Scout24 are larger, more diversified, and better known internationally.

What Alma Media represents, above all, is the quiet competence of Finnish capital deployment. No flashy press conferences. No celebrity CEO profiles in business magazines. No SPAC mergers or meme-stock moments. Just a methodical, two-decade process of selling what was declining, buying what was growing, and letting compound returns do their work in markets that most global investors cannot even locate on a map. In an era of corporate theatrics and quarterly earnings obsession, there is something deeply compelling about a company that simply did the right thing, slowly, for twenty years, and arrived at a destination that its competitors — burdened by indecision, distracted by diversification, or paralyzed by legacy identity — never reached.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube