Airbus SE: The European Aviation Empire

I. Introduction & Episode Setup

Picture this: It's June 2019 at the Paris Air Show, and Guillaume Faury, newly appointed CEO of Airbus, stands before a sea of reporters. Behind him looms an A350-1000, its carbon fiber fuselage gleaming under the Bourget sun. In his hand, he holds a tablet showing real-time order statistics. For the first time in history, a European aerospace company has definitively overtaken Boeing as the world's largest commercial aircraft manufacturer—not just in orders, but in deliveries, revenue, and market share. The unthinkable has happened: Europe has dethroned America in the one industry that seemed permanently stamped "Made in USA."

How did a consortium of squabbling European nations—countries that couldn't agree on cheese regulations—build an aerospace empire that generates €65 billion in annual revenue and commands over half the global commercial aircraft market? The answer involves political intrigue worthy of a Cold War thriller, engineering gambles that would make venture capitalists blanch, and a peculiarly European form of cooperative capitalism that shouldn't work but somehow does.

This is the story of Airbus SE—a company born from post-war European insecurity, raised on government subsidies and political horse-trading, nearly killed by its own ambition with the A380, and ultimately transformed into a lean, mean, Boeing-beating machine. It's a tale that challenges every assumption about how global champions are built. While Silicon Valley preaches "move fast and break things," Airbus spent decades moving slowly and building things that absolutely cannot break at 40,000 feet.

The narrative arc bends through multiple near-death experiences: the early years when American airlines wouldn't touch European planes with a ten-foot pole; the A380 crisis that nearly tore the company apart along French-German fault lines; the bet-the-company gamble on composite materials for the A350. Yet each crisis somehow strengthened rather than weakened the enterprise.

What makes Airbus particularly fascinating for students of business strategy is how it weaponized its greatest weakness—the Byzantine complexity of European politics—into its greatest strength. Where Boeing optimized for shareholder returns and quarterly earnings, Airbus optimized for something else entirely: industrial sovereignty, technological capability, and the long game. The result? A company that thinks in decades while its competitor thinks in quarters.

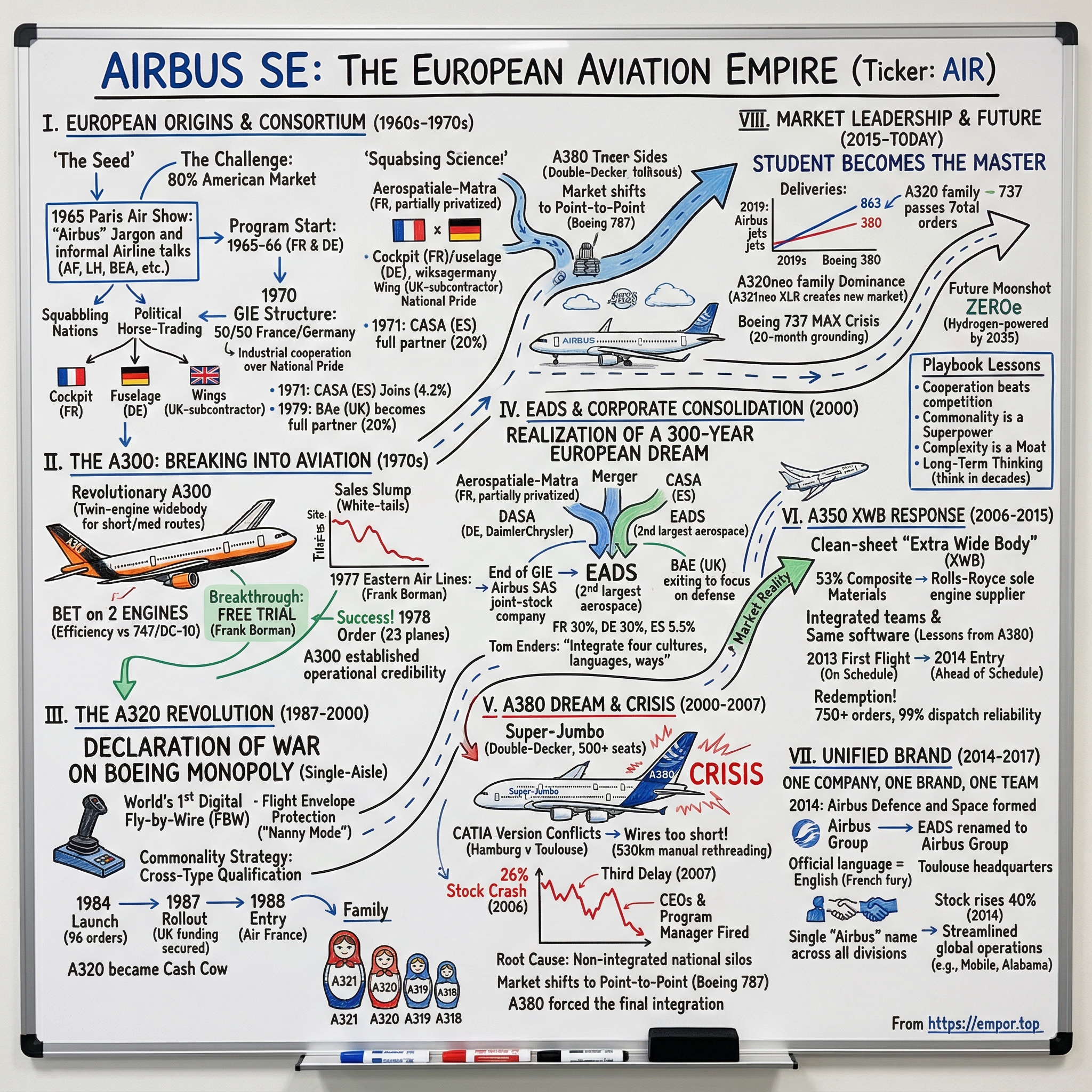

II. European Origins & The Airbus Consortium

The genesis of Airbus begins not in a boardroom or factory floor, but in the rubble of post-World War II Europe. American bombers had reduced European aircraft factories to twisted metal and broken concrete. Meanwhile, across the Atlantic, Boeing, Douglas, and Lockheed emerged from the war with intact facilities, proven designs, and a global market desperate for civilian aircraft. The 1942 Anglo-American agreement—rarely discussed but crucially important—had essentially ceded transport aircraft production to the Americans while Britain focused on fighters. This wartime expedient became peacetime reality: by 1960, American manufacturers controlled 80% of the global commercial aircraft market. The Paris Air Show in June 1965 changed everything. At the 1965 Paris Air Show, major European airlines including Air France, Alitalia, British European Airways (BEA), Lufthansa, Sabena, and SAS informally discussed their requirements for a new "Airbus" capable of transporting 100 or more passengers over short to medium distances at a low cost. The term "Airbus" itself wasn't a company name but industry jargon—a generic expression for a short-to-medium-range, high-capacity aircraft that could handle the growing traffic on busy European routes like London to Paris.

The Airbus program formally began in 1965 when the governments of France and Germany initiated discussions about forming a consortium to build a European high-capacity, short-haul jet transport. By 1966, the pieces started falling into place. French, German, and British officials announced that Sud Aviation (France), Arge Airbus (an informal group of German aerospace companies), and Hawker Siddeley Aviation (Britain) would study the development of a 300-seat airliner for the short-haul sector.

The politics were Byzantine from day one. Each nation wanted the prestigious work—and the jobs that came with it. France insisted on the cockpit and flight controls. Germany demanded the fuselage. Britain, through Hawker Siddeley, claimed the wings—arguably the most complex component. These weren't just industrial decisions; they were matters of national pride wrapped in technical specifications.

On May 29, 1969, at that year's Paris Air Show, French transport minister Jean Chamant and German economics minister Karl Schiller sealed the deal in theatrical fashion: they sat down together in a mock-up of the cabin of a new aircraft destined to reshape the aviation industry. Britain had withdrawn from the partnership just weeks earlier, on April 10, 1969, spooked by the project's ballooning costs. Yet Hawker Siddeley, having already invested heavily in wing design, continued as a subcontractor—a peculiar arrangement that would define Airbus's structure for the next decade.

Airbus Industrie was formally established as a Groupement d'Intérêt Économique (Economic Interest Group or GIE) on 18 December 1970. This wasn't a company in any conventional sense. The GIE structure—a uniquely French legal entity—allowed the partners to pool resources while maintaining their separate identities. Think of it as a permanent joint venture where nobody truly owned anything, yet everyone owned everything. Its initial shareholders were the French company Aérospatiale and the West German company Deutsche Airbus, each owning a 50% share.

The genius of the GIE structure was that it sidestepped the impossible question of which country would "own" Airbus. Instead, each partner company would manufacture its assigned components, deliver them fully finished, and share in the profits (or losses) according to their stake. It was industrial cooperation through creative corporate structuring—a European solution to a European problem.

In October 1971, Spain's CASA joined Airbus with a 4.2% share, bringing its expertise in military transport aircraft and a strategic location on Europe's southwestern edge. The Spanish understood that being inside Europe's aerospace champion, even with a small stake, beat being outside looking in.

The real transformation came in 1979. British Aerospace, which had taken over Hawker Siddeley in 1977, joined Airbus as a true partner with a 20 percent share in 1979. After a decade of awkward subcontracting arrangements, Britain was finally inside the tent. The shareholding structure now reflected the industrial reality: Aérospatiale and Deutsche Airbus each held 37.9%, British Aerospace 20%, and CASA retained its 4.2%.

What emerged from this complex arrangement was something unprecedented: a truly European industrial enterprise that transcended national boundaries while respecting national sensitivities. The consortium structure meant that no single government could dominate, yet all governments had skin in the game. It was messy, inefficient, and politically charged—and it was about to take on Boeing.

III. The A300: Breaking Into Commercial Aviation (1970s–1980s)

October 28, 1972. Toulouse-Blagnac Airport. The morning fog had just lifted, revealing a gleaming white aircraft painted in gaudy orange and black stripes. The A300 prototype first flew on 28 October 1972, with Captain Max Fischl, First Officer Bernard Ziegler, Flight Test Engineers Pierre Caneil and Gunter Scherer, with Romeo Zinzoni as Test Flight Engineer/Mechanic in the cockpit. This maiden flight lasted for one hour and 25 minutes, during which the crew cautiously tested basic systems—a maximum speed of just 185 knots at 14,000 feet.

The A300 was revolutionary yet conservative, audacious yet practical. The first twin-engine widebody airliner, the A300 typically seats 247 passengers in two classes, making it the world's first wide-body twin. Where Boeing's 747 used four engines and the DC-10 and L-1011 used three, Airbus bet everything on two. The lack of a third tail-mounted engine allowed for the wings to be located further forwards and to reduce the size of the vertical stabiliser and elevator, which had the effect of increasing the aircraft's flight performance and fuel efficiency.

The technology was cutting-edge. Airbus partners had employed the latest technology, some of which having been derived from Concorde, on the A300. But the real innovation wasn't just technical—it was philosophical. The A300 introduced what would become Airbus's signature approach: operational commonality. Pilots trained on one variant could fly others with minimal additional training, a concept that would revolutionize airline economics.

Yet for all its innovations, the A300 initially sold about as well as ice to Eskimos. On 15 March 1974, type certificates were granted for the A300 from both German and French authorities, and On 23 May 1974, the first A300 to enter service performed the first commercial flight of the type, flying from Paris to London, for Air France. But Air France's order was essentially a political favor—the French flag carrier couldn't exactly refuse to buy planes from a French-led consortium.

The real problem was credibility. "Most airlines were reticent about a twin-engine widebody carrying so many passengers," Baud says. All widebodies at the time had at least three engines, and the Boeing 747 had four. Even the short- and medium-haul Boeing 727 was a three-engine aircraft. American airlines, in particular, viewed the A300 with deep skepticism. Who were these Europeans to challenge Boeing?

During the first six years of production, Airbus built more A300s than it delivered, parking expensive "white-tails" waiting to be sold and handed over. Between 1974 and 1979, Airbus delivered fewer than 90 aircraft. The low point was 1976; Airbus did not receive a single order between the end of 1975 and mid-1977. Production was reduced to a nominal rate of just 0.5 aircraft per month.

The breakthrough came from an unlikely source: Frank Borman, the former Apollo 8 astronaut who had become CEO of Eastern Air Lines. In September 1973, as part of promotional efforts for the A300, the new aircraft was taken on a six-week tour around North America and South America. Amongst the consequences of this expedition, it had allegedly brought the A300 to the attention of Frank Borman, the CEO of Eastern Airlines, one of the "big four" U.S. airlines.

Borman was a pilot's pilot—pragmatic, numbers-focused, and utterly unsentimental about aircraft. What he saw in the A300 wasn't European sophistication but American-style efficiency. The twin-engine configuration meant lower operating costs. The wide-body capacity meant revenue potential. And Airbus, desperate for American credibility, was willing to make an unprecedented deal.

In 1977, US carrier Eastern Air Lines leased four A300s as an in-service evaluation—essentially a free trial. Airbus was motivated to give Eastern extraordinary terms on the A300s in order to make a breakthrough in the US market. The gamble was enormous. If Eastern rejected the planes after the trial, Airbus might never recover its reputation in America.

December 13, 1977, marked D-Day. Eastern's first A300 entered service on the Miami-New York route. The aircraft performed flawlessly. Passengers loved the wide cabin. Pilots appreciated the advanced systems. Most importantly, Borman's accountants loved the operating economics.

So impressed was the airline's CEO that he placed a US$778 million order for 23 of the type on April 6, 1978. The four already in service would be retained, and EA would purchase 19 more outright. The order was significant for Airbus. Many saw it as the point where the European plane maker was finally recognized as a major competitor to the American behemoths Boeing and McDonnell Douglas.

The Eastern order triggered a cascade. Pan Am followed the EA order shortly afterward with a deal for 13. Asian carriers, particularly those flying over water where twin-engine efficiency mattered most, began placing orders. In September 1974, Korean Air placed an order for four A300B4s with options for two further aircraft; this sale was viewed as significant as it was the first non-European international airline to order Airbus aircraft. Airbus had viewed South-East Asia as a vital market that was ready to be opened up and believed Korean Air to be the 'key'.

By 1979, the tide had turned. By 1979 there were 81 A300 passenger liners in service with 14 airlines, alongside 133 firm orders and 88 options. The ugly duckling had become, if not quite a swan, at least a respectable goose. The A300 would never be a bestseller—eventually reaching a total of 561 delivered aircraft—but it didn't need to be. It had proven that Airbus could build reliable, efficient aircraft that airlines actually wanted to buy.

More importantly, it established the Airbus philosophy that would ultimately conquer the market: commonality, efficiency, and a willingness to challenge conventional wisdom. The same consortium that had nearly collapsed in 1976 was now ready to take on Boeing directly.

IV. The A320 Revolution & Rise to Competition (1987–2000)

On March 2, 1984, Airbus launched the Airbus A320 with 96 orders, with the largest order from Air France. This wasn't just another aircraft launch—it was a declaration of war on Boeing's monopoly of the single-aisle market. Unlike the A300, which had scraped together just 15 orders before its first flight, the A320 had over 400 orders before it first flew, compared to 15 for the A300 in 1972.

The difference was confidence. Airlines weren't buying a promise; they were buying into a revolution. The A320 is the world's first airliner with digital fly-by-wire (FBW) flight control system: input commands through the side-stick are interpreted by flight control computers and transmitted to flight control surfaces within the flight envelope protection. No more cables and pulleys—just electrons and algorithms.

Roger Béteille, then Airbus president, later recalled the gravity of the decision: "Either we were going to be first with new technologies or we could not expect to be in the market." The technology was so radical that Airbus test pilots had been experimenting with fly-by-wire on a modified A300 testbed, essentially using their own widebody as a guinea pig for narrowbody innovation.

February 14, 1987. Toulouse. In the presence of then-French Prime Minister Jacques Chirac and the Prince and Princess of Wales, the first A320 was rolled out of the final assembly line at Toulouse on 14 February 1987. The British royals were there not just for ceremony—BAe had finally secured government funding for its share of the program after years of negotiation. This was Europe showing America that it could build not just competitive aircraft, but revolutionary ones.

Eight days later came the moment of truth. The A320 made its maiden flight on 22 February in 3 hours and 23 minutes. Pierre Baud, Airbus's chief test pilot, emerged from the cockpit with a verdict that would echo through aviation history: "Our A320 is delightfully responsive and reassuringly stable to fly, with qualities which fly-by-wire brings together for the first time in an aircraft."

The A320 was introduced in April 1988 by Air France, making it the world's first commercial aircraft to enter service with full digital fly-by-wire controls. The Airbus A320 began service in 1988 as the first mass-produced airliner with digital fly-by-wire controls. This wasn't just an incremental improvement—it was a paradigm shift.

The fly-by-wire system did more than save weight by eliminating mechanical linkages. It introduced "flight envelope protection"—the aircraft would literally prevent pilots from exceeding safe parameters. Bank too steeply? The computer wouldn't let you. Pull back too hard? The system would intervene. It was controversial—some pilots called it "nanny mode"—but it was undeniably safer.

The cockpit itself was revolutionary. Gone were the traditional control yokes. In their place: side-sticks, borrowed from fighter jets. The A320 retained the dark cockpit (where an indicator is off when its system is running; useful for drawing attention to dysfunctions when an indicator is lit). The philosophy was radical: the plane should almost fly itself, with pilots managing rather than manually controlling.

But the real genius was in what Airbus called "commonality." All following Airbuses have similar human/machine interface and systems control philosophy to facilitate cross-type qualification with minimal training. A pilot certified on the A320 could transition to the A319, A321, or later the A330 with minimal additional training. For airlines, this meant massive savings in training costs and scheduling flexibility.

The family strategy kicked into high gear immediately. The first derivative of the A320 was the Airbus A321, launched on 24 November 1988 after commitments for 183 aircraft from 10 customers were secured. The A319 followed in 1993, and the tiny A318 in 1999. Same cockpit, same systems, different sizes—like Russian dolls, but worth billions.

By the early 1990s, the A320 family was selling faster than Airbus could build them. Production rates climbed from two per month to four, then eight, then higher. The Toulouse final assembly line was joined by Hamburg, then later Tianjin and Mobile. The European experiment had become a global production system.

The numbers told the story. While the A300 had taken six years to reach 100 deliveries, the A320 family hit that milestone in less than three. By 1995, Airbus had captured 30% of the single-aisle market. By 2000, it was approaching parity with Boeing.

What Boeing didn't initially grasp was that Airbus hadn't just built a better mousetrap—they'd redefined what a mousetrap could be. The 737, with its 1960s DNA, suddenly looked antiquated. Boeing would eventually respond with the 737NG and later the MAX, but they were playing catch-up to a competitor that had fundamentally reimagined commercial aviation.

The A320's success also validated Airbus's entire philosophy. Technology could triumph over tradition. European cooperation could match American scale. And most importantly, airlines would pay a premium for innovation if it delivered operational savings.

By 2000, the A320 family had become the cash cow that funded Airbus's next adventures. The profits from single-aisle sales would underwrite the A380 super-jumbo project and the composite A350. The little narrowbody that could had become the foundation of an aerospace empire.

V. EADS Formation & Corporate Consolidation (2000–2006)

July 10, 2000. A date that should be marked in gold letters in European industrial history. On this day, Aerospatiale-Matra, DASA, and CASA merged to form the world's second largest aerospace group, EADS. The merger press conference in Paris featured an unusual sight: French, German, and Spanish executives standing together, speaking in three languages, toasting with champagne. This wasn't just a corporate merger—it was the realization of a 30-year European dream.

The path to EADS had been anything but smooth. Throughout the 1990s, European aerospace companies watched with growing alarm as American giants consolidated. Boeing swallowed McDonnell Douglas in 1997. Lockheed merged with Martin Marietta. The Europeans risked being crushed by sheer American scale unless they could achieve similar consolidation.

The French moved first. In 1999, the French government announced a plan to partially privatize Aerospatiale and combine it with Matra Hautes Technologies. The resulting entity, Aerospatiale-Matra, became the French aerospace national champion, with the government retaining 48% and the Lagardère Group holding 33%. Jean-Luc Lagardère, the flamboyant French industrialist who controlled Matra, saw the merger as just the first step. "The birth of Aerospatiale Matra is just one decisive step in the enormous restructuring movement now taking place in Europe and around the world," he declared.

Meanwhile in Germany, DaimlerChrysler had assembled its own aerospace empire. DASA (Deutsche Aerospace) had absorbed Dornier, MBB, and other German aerospace assets throughout the 1990s. By 1999, DASA was Germany's aerospace champion, but it was still subscale compared to American competitors.

The Spanish played the role of catalyst. CASA, though smaller than its French and German counterparts, controlled valuable military transport aircraft programs and had deep relationships with Latin American markets. More importantly, the Spanish government was willing to be the junior partner that broke the French-German deadlock.

On 14 October 1999 DASA agreed to merge with Aérospatiale-Matra to create the European Aeronautic Defence and Space Company. On December 2, 1999, CASA signed on. The structure was Byzantine but balanced: French interests would hold 30%, Germans 30%, Spanish 5.5%, with the remainder publicly traded. No single nation could dominate, forcing genuine cooperation.

But EADS was only half the transformation. The real revolution came in 2001 when Airbus Industrie GIE was reorganized as Airbus SAS, a simplified joint-stock company. This wasn't just a legal technicality—it was fundamental surgery on Airbus's DNA. The GIE structure, that peculiar French legal construct that had enabled Airbus's birth, had become a straitjacket. Decision-making required consensus among partners. Profits and losses were allocated according to complex formulas. No one truly owned anything.

In January 2001 Airbus Industrie was transformed from an inherently inefficient consortium structure to a formal joint stock company, with legal and tax procedures being finalized on 11 July. Both EADS and BAE transferred ownership of their Airbus factories to the new Airbus SAS in return for 80% and 20% shares in the new company respectively. For the first time, Airbus had real shareholders, a real board, and real accountability.

The British, as usual, charted their own course. BAE Systems, formed from the 1999 merger of British Aerospace and Marconi Electronic Systems, decided to focus on defense rather than commercial aviation. They retained their 20% stake in Airbus but increasingly viewed it as a financial asset rather than a strategic one. The writing was on the wall—the British were heading for the exit.

The transformation wasn't just corporate—it was cultural. The old Airbus had been a United Nations of aerospace, with French engineers arguing with German production managers while Spanish designers looked on in bemusement. The new structure demanded integration. Teams were reorganized along product lines rather than national lines. English became the working language (much to French chagrin). Management processes were standardized.

Tom Enders, a German executive who would later lead the company, captured the challenge: "We had to transform four companies with four cultures, four languages, and four ways of doing business into one company with one culture." It was industrial integration on a scale Europe had never attempted.

The early 2000s were a whirlwind of integration and reorganization. In 2003, EADS acquired BAE's 25% share in Astrium, the satellite manufacturer. Defense units were consolidated. Helicopter divisions were merged. The sprawling empire was slowly being organized into coherent business units.

But the real test of the new structure would come with the A380 program. For the first time, Airbus would develop a major aircraft not as a consortium of national companies but as an integrated corporation. The results would be catastrophic—but that's a story for the next chapter.

What EADS represented was more than corporate consolidation. It was Europe's answer to American aerospace dominance—not through protection or subsidy, but through scale and integration. The company that emerged from this transformation would be leaner, more focused, and more capable of competing globally. The consortium era was over. The corporate era had begun.

VI. The A380 Dream & Crisis (2000–2007)

January 18, 2005. Toulouse-Blagnac Airport. Ten thousand people gathered in the bitter cold to witness history. The first prototype was unveiled in Toulouse, France on 18 January 2005, with Jacques Chirac, Tony Blair, José Luis Rodríguez Zapatero, and Gerhard Schröder in attendance—four leaders of four nations celebrating what they believed would be Europe's triumph over Boeing. The A380 stood before them: 73 meters long, 24 meters high, with a wingspan of almost 80 meters. It was, quite simply, the largest passenger aircraft ever built.

The vision had been germinating since 1988. Airbus studies started in 1988, and the project was announced in 1990 to challenge the dominance of the Boeing 747 in the long-haul market. The logic seemed unassailable. Air traffic was doubling every 15 years. Airports were congested. Airlines needed bigger planes, not more planes. The hub-and-spoke model that dominated international aviation demanded super-jumbos to ferry passengers between major hubs. Boeing's 747 had monopolized this market for 30 years. It was time for Europe to claim the crown.

The then-designated A3XX project was presented in 1994 and Airbus launched the €9.5–billion ($10.7–billion) A380 programme on 19 December 2000. The timing seemed perfect. The dot-com boom was at its peak. Airlines were flush with cash. Orders poured in from Emirates, Singapore Airlines, Qantas—the world's premium carriers all wanted Airbus's new flagship.

The engineering was breathtaking. The A380 could carry up to 853 passengers in an all-economy configuration, though most airlines opted for around 500 seats in a three-class layout. The upper deck stretched the entire length of the fuselage—a true double-decker, not the partial upper deck of the 747. Airlines promised showers, bars, duty-free shops, even casinos. This wasn't just transportation; it was a flying cruise ship.

It then obtained its type certificate from the European Aviation Safety Agency (EASA) and the US Federal Aviation Administration (FAA) on 12 December 2006. But by then, the dream had already turned into a nightmare.

The problems started innocuously enough. Initial production of the A380 was troubled by delays attributed to the 530 km (330 mi) of wiring in each aircraft. Airbus cited as underlying causes the complexity of the cabin wiring (98,000 wires and 40,000 connectors), its concurrent design and production, the high degree of customisation for each airline, and failures of configuration management and change control.

But the real catastrophe was hidden in the software. The German and Spanish Airbus facilities continued to use CATIA version 4, while British and French sites migrated to version 5. CATIA 5 wasn't just an upgrade—it was a complete rewrite, incompatible with version 4. When German engineers in Hamburg designed wiring harnesses using CATIA 4 and sent them to Toulouse for final assembly, where engineers used CATIA 5, the wires didn't fit. They were too short.

Picture the scene: hundreds of German engineers camped out in Toulouse, manually rethreading 530 kilometers of wiring through each aircraft. Each plane required 98,000 individual wires performing 1,150 separate functions. When a wire was too short—and thousands were—it couldn't simply be extended. That would increase electrical resistance. The entire harness had to be ripped out and replaced.

On 13 June 2006, Airbus announced a second delay, with the delivery schedule slipping an additional six to seven months. Although the first delivery was still planned before the end of 2006, deliveries in 2007 would drop to only 9 aircraft, and deliveries by the end of 2009 would be cut to 70–80 aircraft. The announcement caused a 26% drop in the share price of Airbus' parent, EADS, and led to the departure of EADS CEO Paul Dupont, Airbus CEO Gustav Humbert, and A380 programme manager Charles Champion.

The June 2006 announcement was a bombshell. EADS stock crashed 26% in a single day, wiping out €5 billion in market value. But worse was to come. On 3 October 2006, upon completion of a review of the A380 programme, Airbus CEO Christian Streiff announced a third delay, pushing the first delivery to October 2007, to be followed by 13 deliveries in 2008, 25 in 2009, and the full production rate of 45 aircraft per year in 2010.

The human casualties mounted. Paul Dupont, EADS CEO—gone. Gustav Humbert, Airbus CEO—gone. Charles Champion, A380 program manager—gone. The French blamed the Germans for sticking with outdated software. The Germans blamed the French for changing systems mid-program. Both blamed management for allowing the situation to develop.

Tom Enders, who would later become Airbus CEO, revealed the depth of the crisis: "We asked ourselves whether we should terminate the program." This wasn't hyperbole. The development cost of the A380 had grown to €11–14 billion when the first aircraft was completed. In 2000, the projected development cost was €9.5 billion. In 2004, Airbus estimated that €1.5 billion (US$2 billion) would need to be added, totalling the developmental costs to €10.3 billion ($12.7 billion). In 2006, Airbus stopped publishing its reported cost after reaching costs of €10.2 billion and then it provisioned another €4.9 billion, after the difficulties in electric cabling and two years delay for an estimated total of €18 billion.

The root causes went deeper than software incompatibility. The A380 crisis exposed every weakness in Airbus's structure. The French and Germans had never truly integrated their engineering cultures. Hamburg and Toulouse operated as separate fiefdoms, each protecting its turf, each convinced of its superiority. The consortium mentality that had enabled Airbus's birth now threatened to cause its death.

Meanwhile, the market was shifting beneath Airbus's feet. Boeing, rather than building a 747 successor, launched the 787 Dreamliner—a smaller, more efficient plane that could fly point-to-point between secondary cities, bypassing hubs entirely. Low-cost carriers were fragmenting the market. Twin-engine planes could now fly trans-Pacific routes. The hub-and-spoke model that justified the A380 was crumbling.

Due to difficulties with the electrical wiring, the initial production was delayed by two years and the development costs almost doubled. It was first delivered to Singapore Airlines on 15 October 2007 and entered service on 25 October. When Singapore Airlines finally took delivery of the first A380 in October 2007, the celebration was muted. The plane was two years late and billions over budget. The order book, once bursting with promise, had stagnated.

The A380 would fly—beautifully, by all accounts. Passengers loved it. Pilots praised its handling. But the damage was done. The delays had allowed Boeing's 787 to gain momentum. The cost overruns had destroyed the business case. Most fatally, the crisis had exposed Airbus as still, at heart, a collection of national companies pretending to be one.

The great irony was that the A380 crisis forced the integration that should have happened years earlier. Software systems were standardized. Engineering processes were harmonized. Management structures were simplified. The patient nearly died, but the surgery ultimately saved it. The A380 would never recover—production would end in 2021 with just 251 delivered—but Airbus would emerge stronger, leaner, and finally, truly integrated.

VII. The A350 XWB Response & Recovery (2006–2015)

While Airbus was bleeding from the A380 crisis, Boeing landed another blow. At the 2004 Paris Air Show, Boeing launched the 787 Dreamliner with All Nippon Airways committing to 50 aircraft. This wasn't just another airplane—it was a revolution in materials (composites), efficiency (20% better fuel burn), and passenger experience (larger windows, better pressurization). Airbus's initial response was catastrophically inadequate: a warmed-over A330 with new engines, dismissively called the A350.

Airlines revolted. Steven Udvar-Házy, the influential CEO of aircraft lessor ILFC, publicly called Airbus's A350 proposal "a Band-Aid reaction to the 787." In March 2006, Singapore Airlines CEO Chew Choon Seng twisted the knife: "Having gone to the trouble of designing a new wing, tail, and cockpit, why not the fuselage too?"

The message was brutal but clear: half-measures wouldn't work. Airbus has also proposed the A350 XWB to compete with the Boeing 787 Dreamliner, after being under great pressure from airlines to produce a competing model. The XWB—Extra Wide Body—would be a clean-sheet design, not a derivative.

December 1, 2006: Airbus board approved industrial launch of A350-800, -900, and -1000 variants. The timing was surreal. While one team in Toulouse was desperately rewiring A380s, another team down the road was designing the future of Airbus. The company was simultaneously managing its greatest crisis and its most important development program.

The A350 XWB represented everything Airbus had learned from both the A380 disaster and Boeing's 787 strategy. Where the A380 bet on size, the A350 bet on efficiency. Where the A380 used aluminum, the A350 would use 53% composite materials. Where the A380 served hubs, the A350 could profitably serve both hub-and-spoke and point-to-point routes.

The technology leap was enormous. The fuselage would be built from carbon fiber composite panels, not the barrel sections Boeing used for the 787. This allowed for easier customization and repair. The wing would be the most sophisticated ever built, with adaptive camber that changed shape in flight for optimal efficiency.

But the real revolution was in how Airbus developed the plane. No more CATIA version conflicts—everyone used the same software from day one. No more French-German silos—integrated teams worked on systems, not national components. No more concurrent development and customization—the plane would be fully developed before customer configurations began.

The engine strategy was equally clever. Where Boeing had struggled with exclusive engine suppliers on the 787, Airbus selected Rolls-Royce as sole provider but demanded unprecedented guarantees on performance and reliability. The Trent XWB would be the most powerful and efficient engine Rolls-Royce had ever built.

First flight came on June 14, 2013—on schedule, a minor miracle given Airbus's recent history. The test program proceeded flawlessly. When Qatar Airways took delivery of the first A350-900 on December 22, 2014, it was actually two weeks ahead of schedule. For a company that had been synonymous with delays just years earlier, this was redemption.

The numbers validated the strategy. By entry into service, Airbus had accumulated over 750 orders from 40 customers. The A350 was 25% more fuel-efficient than the 777 it competed against. Airlines reported dispatch reliability above 99% from day one—unheard of for a new aircraft type.

More importantly, the A350 proved Airbus could execute. The same company that had bungled the A380 had delivered a technological tour de force on time and on budget. The program would break even by 2019, a remarkable achievement for a clean-sheet aircraft.

The A350 also marked Airbus's philosophical evolution. The A380 had been about European pride—building something bigger than Boeing because they could. The A350 was about market reality—building what airlines actually wanted to buy. The adolescent need to prove itself had given way to mature commercial judgment.

By 2015, the transformation was complete. The A350 was outselling Boeing's 777X before it even flew. The A320neo family was dominating the single-aisle market. The A380, while still losing money, was at least delivering reliably. Airbus had survived its near-death experience and emerged as Boeing's equal—perhaps even its superior.

VIII. Corporate Restructuring & The Airbus Brand (2014–2017)

Tom Enders stood before employees in January 2014 with a simple message: "One company, one brand, one team." After 44 years of complex structures, political compromises, and alphabet soup acronyms, Airbus would finally become just... Airbus.

The restructuring began with defense and space. January 2014: Airbus Defence and Space formed from former EADS divisions Airbus Military, Astrium, and Cassidian. Three separate organizations with overlapping capabilities and competing cultures were forced into a single entity. It was corporate surgery without anesthetic.

EADS NV was renamed Airbus Group NV in 2014 and finally Airbus SE in 2015. The name change was more than cosmetic. EADS—European Aeronautic Defence and Space Company—screamed government consortium. Airbus was a brand customers knew and trusted. If you asked passengers what plane they were flying, they said "Airbus," not "EADS."

May 2015: Company became Societas Europaea (SE); September 2016: Announced merge with largest division Airbus SAS. The SE designation was crucial—it meant Airbus was a truly European company, not French or German or Spanish, but European. No single government could claim ownership or control.

The real revolution came in January 2017: Group reorganized under single "Airbus" brand. Every division, every subsidiary, every business card would carry the same name. Airbus Commercial Aircraft. Airbus Helicopters. Airbus Defence and Space. Simple, clear, unified.

Enders, a German who spoke perfect English and good French, embodied the transformation. Unlike his predecessors who played national politics, Enders played corporate strategy. He moved executive functions to Toulouse, streamlined reporting lines, and most controversially, made English the official working language.

The French were furious. Airbus was headquartered in France, employed thousands of French workers, and received French government support. Making English the official language was seen as Anglo-Saxon colonization. But Enders held firm—a global company needed a global language.

The integration went beyond language. Engineering standards were harmonized. Procurement was centralized. IT systems were unified. For the first time, an engineer in Hamburg used the same processes and systems as one in Toulouse or Madrid or Bristol.

The brand consolidation also simplified the corporate structure that had become byzantine over decades of mergers. Gone were the holding companies, intermediate subsidiaries, and special purpose vehicles. The organization chart, once resembling a plate of spaghetti, became a simple hierarchy.

But the masterstroke was financial. By simplifying the structure, Airbus could finally present clear, consolidated accounts. Investors could understand where money was made and lost. The stock became more liquid and attractive to international investors, particularly Americans who had been confused by the previous structure.

The results were immediate. The stock price rose 40% in 2014 alone. Employee engagement scores improved. Customer satisfaction increased. For the first time, Airbus was winning the talent war, attracting top engineers and managers who previously would have chosen Boeing or Silicon Valley.

The brand unification also enabled global expansion. When Airbus opened its Mobile, Alabama assembly line in 2015, it wasn't EADS or Airbus Americas—it was simply Airbus. The same was true for the innovation centers in Silicon Valley, Beijing, and Bangalore. One company, one brand, worldwide.

By 2017, the transformation was complete. The company that had been cobbled together from national champions, that had nearly collapsed during the A380 crisis, that had been mocked for its bureaucracy and inefficiency, had become a streamlined, global aerospace leader. Revenue reached €67 billion. The commercial aircraft backlog exceeded 7,000 planes. The stock price had tripled in five years.

The corporate restructuring also enabled a cultural transformation. The old Airbus had been defensive, always comparing itself to Boeing, always seeking validation. The new Airbus was confident, setting its own agenda, defining its own success.

This confidence showed in product strategy. The A321neo XLR, launched in 2019, didn't copy Boeing—it created a new market segment. The A220 acquisition from Bombardier in 2018 wasn't reactive—it was opportunistic. The commitment to hydrogen aircraft by 2035 wasn't following—it was leading.

The Airbus brand had become more than a corporate identity. It represented European integration at its best—nations cooperating without surrendering sovereignty, competing globally while maintaining local excellence. In a Europe increasingly fractured by Brexit and nationalism, Airbus stood as proof that European cooperation could work.

IX. Modern Era: Market Leadership & Future Challenges (2015–Today)

The numbers are staggering. In 2019, Airbus displaced Boeing as the largest aerospace company by revenue. For the full year 2019, Boeing delivered 380 aircraft, while Airbus set a new all-time annual record, handing over 863 jets. Boeing had retained a deliveries lead over Airbus since 2012. The student had become the master.

The transformation wasn't sudden—it was the culmination of decades of patient execution. In October 2019, the A320 family became the highest-selling airliner family with 15,193 orders, surpassing the Boeing 737's total of 15,136. By 2023, history was made again: the number of Airbus aircraft in service surpassed Boeing for the first time.

The catalyst for this reversal was Boeing's 737 MAX crisis. Two crashes—Lion Air Flight 610 in October 2018 and Ethiopian Airlines Flight 302 in March 2019—killed 346 people and exposed fundamental flaws in Boeing's development process. The MAX was grounded worldwide for 20 months. Boeing's deliveries collapsed. Its reputation shattered.

But Airbus's ascent wasn't just about Boeing's stumbles. The A320neo family, launched in 2010, had redefined single-aisle economics. With new engines delivering 15-20% better fuel efficiency, the neo wasn't just an upgrade—it was a revolution. Airlines couldn't order them fast enough. For the full year 2019, Airbus handed over 642 A320 family aircraft, of which 551 were A320neos. This compares to a total of 386 A320neo family aircraft delivered in 2018, up from 181 and 68 in 2017 and 2016, respectively.

The production system had been transformed into a global machine. Toulouse and Hamburg were joined by final assembly lines in Tianjin, China (operational since 2009) and Mobile, Alabama (opened 2015). Airbus recently increased the official A320 production rate to 60 aircraft per month and is targeting an additional raise to 63 jets per month from 2021. This wasn't just manufacturing—it was industrial choreography on a planetary scale.

Meanwhile, the A350 had become the profit engine Airbus needed. Airbus delivered a record 112 A350s in 2019, up from 93 and 78 in 2018 and 2017, respectively. Each plane generated healthy margins. Airlines loved its efficiency. Passengers loved its comfort. Boeing's competing 777X was years late and billions over budget.

The financial performance reflected the operational excellence. Airbus SE delivered 863 commercial aircraft to 99 customers in 2019, outpacing its previous output record set in 2018 by eight percent. In the 17th yearly production increase in a row, Airbus progressed on the transition to all NEO variants and by year end Airbus had delivered 173 wide-body aircraft, its highest number in a single year.

But success brought new challenges. Supply chains groaned under the production rates. Engine manufacturers, particularly Pratt & Whitney with its geared turbofan, struggled to deliver on time. Quality issues emerged—nothing like Boeing's problems, but enough to worry customers. The very success of the A320neo had created bottlenecks that threatened future growth.

China loomed as both opportunity and threat. Airbus's Tianjin assembly line had given it unique access to the Chinese market. But China's own COMAC C919, though technologically inferior, represented the first serious challenge to the Airbus-Boeing duopoly. If China could make competitive commercial aircraft, what was Airbus's moat?

Sustainability had become existential. Aviation contributed 2-3% of global CO2 emissions, and that percentage was growing. Airbus committed to a hydrogen-powered aircraft by 2035—a moonshot that would require reimagining everything from fuel systems to airport infrastructure. The ZEROe concept aircraft unveiled in 2020 weren't just designs—they were a bet on the future of aviation.

The competitive landscape with Boeing had also shifted. The old rivalry—Toulouse versus Seattle, Europe versus America—had given way to something more complex. Both companies faced common challenges: sustainable aviation, supply chain resilience, digital transformation. They were less gladiators in an arena and more dancers in a carefully choreographed duet.

Guillaume Faury, who became CEO in 2019, embodied this new era. An engineer by training but a diplomat by temperament, Faury understood that Airbus's future lay not in beating Boeing but in expanding the market. His mantra was "customer focus"—understanding what airlines needed before they knew they needed it.

The COVID-19 pandemic in 2020 tested everything. Air travel collapsed. Airlines canceled orders. Production rates were slashed. But Airbus used the crisis to accelerate transformation. Digital design tools were enhanced. Supply chains were restructured. When demand recovered faster than expected in 2021-2022, Airbus was ready.

By 2024, the numbers told an extraordinary story. The A320 series is poised to overtake its US competitor as the most-delivered commercial airliner in history, according to aviation consultancy Cirium. As of early August, Airbus had winnowed the gap to just 20 units, with 12,155 lifetime A320-family shipments, according to the data. That difference is likely to disappear as soon as next month.

The symbolism was profound. The aircraft family that Boeing had invented—the single-aisle jet—would soon be dominated by Airbus. It wasn't just a commercial victory; it was validation of the European model of patient, collaborative capitalism.

Yet Faury and his team knew that past success guaranteed nothing. Electric vertical takeoff aircraft threatened short-haul routes. High-speed rail was expanding in Europe and Asia. Video conferencing had permanently reduced business travel. The next 50 years would be nothing like the last 50.

X. Playbook: Business & Strategic Lessons

The Airbus story offers a masterclass in strategic patience, but the lessons aren't what MBA textbooks typically teach. This wasn't disruption in the Silicon Valley sense—it was a 50-year grind that required political skill, technical excellence, and an almost Japanese view of time.

Lesson 1: Cooperation Can Beat Competition The conventional wisdom says competition drives innovation. Airbus proves that cooperation can too. Four nations that had spent centuries killing each other figured out how to build planes together. The key wasn't eliminating competition—France and Germany still competed for workshare—but channeling it productively. The consortium structure that everyone mocked as inefficient forced consensus-building that, while slow, produced better long-term decisions than Boeing's quarterly capitalism.

Lesson 2: Strategic Patience Beats Tactical Speed Boeing optimized for shareholder returns. Airbus optimized for market position. Boeing returned cash to shareholders through buybacks. Airbus invested in new programs. Boeing outsourced to reduce costs. Airbus kept capabilities in-house to maintain control. Over five decades, the patient approach won. The A320neo's dominance today stems from investments made in fly-by-wire technology in the 1980s.

Lesson 3: Technology Bets Should Be Binary Airbus's big technology bets—fly-by-wire on the A320, composites on the A350—were make-or-break decisions. There was no hedging, no Plan B. This concentration of risk focused minds wonderfully. When you bet the company, everyone from the CEO to the shop floor understands that failure isn't an option. The A380 failed not because the technology was wrong but because the market bet was wrong—a crucial distinction.

Lesson 4: Commonality Is A Superpower Airbus's obsession with commonality—same cockpit, same systems, same type ratings across aircraft families—created compound advantages. Airlines saved millions in training costs. Pilots could switch between aircraft types. Maintenance was simplified. Boeing, with its disparate aircraft families, couldn't match this. What seemed like a small technical decision in the 1980s became a decisive competitive advantage.

Lesson 5: Crisis Management Requires Brutal Honesty The A380 crisis nearly killed Airbus, but the response saved it. Management was fired. Problems were acknowledged publicly. Fixes were implemented systematically. Compare this to Boeing's response to the 737 MAX crisis—denial, deflection, blame-shifting. Airbus learned that admitting failure quickly and fixing it thoroughly builds more trust than pretending problems don't exist.

Lesson 6: Government Support Is A Tool, Not A Crutch Yes, Airbus received government support. But so did Boeing, through defense contracts and tax breaks. The difference was how it was used. European governments provided patient capital for long-term R&D. They didn't intervene in daily operations. They accepted losses for decades. This wasn't subsidy in the pejorative sense—it was industrial policy that worked.

Lesson 7: Culture Eats Strategy, But Structure Eats Culture Airbus spent decades trying to create a unified culture across four nations. It never fully succeeded. What worked instead was creating structures that forced cooperation. Integrated supply chains meant Hamburg couldn't succeed unless Toulouse did. Common IT systems meant everyone used the same data. Structure shaped behavior more effectively than any culture initiative.

Lesson 8: Market Timing Matters More Than First-Mover Advantage The A380 was a technological marvel that arrived just as the market was moving away from hub-and-spoke to point-to-point. The A320neo was derivative technology that arrived just as airlines desperately needed fuel efficiency. Being first matters less than being right about where the market is heading.

Lesson 9: Complexity Can Be A Moat The complexity of Airbus's structure—multi-national, multi-site, multi-cultural—was supposed to be its weakness. Instead, it became a strength. Chinese and American competitors could copy Airbus's technology but not its ability to manage complexity. In a globalized world, the ability to orchestrate complexity is itself a competitive advantage.

Lesson 10: Long-Term Thinking Requires Long-Term Capital Airbus could think in decades because its shareholders—European governments and patient industrial investors—thought in decades. Boeing's shareholders wanted quarterly returns. This mismatch in time horizons shaped every strategic decision. Airbus could lose money on the A350 for years knowing it would eventually profit. Boeing couldn't.

The meta-lesson is that there's no universal playbook. Airbus succeeded by doing almost everything conventional business wisdom says not to do. It was bureaucratic, political, complex, and slow. It shouldn't have worked. But in industries with 30-year product cycles, decades-long customer relationships, and massive capital requirements, perhaps the Airbus model—patient, collaborative, technically focused—is actually optimal.

The question for other industries is whether similar models could work. Could pharmaceuticals benefit from trans-national R&D cooperation? Could renewable energy scale faster through Airbus-style consortiums? Could even software, with its obsession with speed, learn from Airbus's strategic patience?

XI. Analysis & Bear vs. Bull Case

The Bull Case: Structural Dominance

The optimistic view sees Airbus as virtually unassailable. Start with the order backlog: over 8,000 aircraft worth roughly €1 trillion at list prices. Even at a 50% discount, that's €500 billion in future revenue—about seven years of current sales. The backlog isn't just big; it's diverse, spread across hundreds of customers globally. No single customer or region can tank the business.

The A320neo family has achieved something rare in industrial history: a monopoly-like position in a duopoly market. With over 60% market share in new orders, it's become the default choice for airlines. The switching costs are enormous—pilot training, maintenance procedures, spare parts inventories. Once an airline commits to Airbus, switching to Boeing costs hundreds of millions.

Production capacity is the real moat. Airbus's four final assembly lines across three continents can produce 75 single-aisle aircraft monthly by 2025. Replicating this would take a competitor a decade and tens of billions of euros. China's COMAC might have government backing, but they're still struggling to produce 10 aircraft annually.

The financial trajectory is compelling. Operating margins have expanded from 2% in 2010 to over 10% in 2019 (pre-COVID). The A350 has turned profitable. The A320neo generates massive cash flow. Even the A330neo, dismissed as a niche product, found its market. Free cash flow could exceed €5 billion annually by 2025.

Technology leadership extends beyond current products. Airbus's hydrogen aircraft program, while risky, positions it as the sustainability leader. The company's digital twin technology and predictive maintenance capabilities are industry-leading. The Wing of Tomorrow program promises 20% efficiency improvements. Airbus isn't just selling aircraft; it's selling an ecosystem.

The Bear Case: Peak Aerospace

The pessimistic view sees multiple threats converging. Start with the macro picture: business travel, which drives premium revenues, may have permanently declined by 20-30% post-COVID. Environmental pressure is mounting—flight shaming in Europe, potential carbon taxes, regulatory restrictions. The industry's social license to operate is under threat.

Boeing won't stay down forever. The 737 MAX is selling again. The 777X, despite delays, is a formidable competitor. Boeing's balance sheet is wounded but not fatal. More concerning is potential new competition. China's COMAC C919, while inferior today, will improve. If China orders its airlines to buy domestic, that's 25% of global demand potentially lost.

The supply chain is Airbus's Achilles heel. It relies on single sources for critical components. Engine makers are struggling to meet demand. The aerospace supply chain lost skilled workers during COVID who haven't returned. Any disruption—a factory fire, a quality issue, a geopolitical crisis—could halt production.

Technological disruption looms. Electric aircraft could handle short routes by 2035. Supersonic travel might return for premium passengers. Urban air mobility could cannibalize short-haul flights. Hyperloop technology, while speculative, represents another threat. Airbus must defend its core business while investing in multiple uncertain futures.

The financial risks are serious. Aircraft development costs are exploding—the next clean-sheet design could cost €25 billion. Government support is under attack from the WTO and increasingly skeptical taxpayers. Currency fluctuations—Airbus sells in dollars but incurs costs in euros—can swing profits by billions. A major accident involving an Airbus aircraft, especially if linked to design flaws, could be catastrophic.

The Balanced View: Resilient but Vulnerable

The reality likely lies between extremes. Airbus has built formidable competitive advantages that won't disappear quickly. The backlog provides years of revenue visibility. The installed base of 10,000+ aircraft generates steady aftermarket revenues. The technology and production capabilities took decades to build and can't be easily replicated.

But the industry faces structural headwinds. Growth rates will likely slow from the historical 4-5% annually to 2-3%. Margins will be pressured by environmental compliance costs. Competition will intensify as national champions emerge in China, Russia, and potentially India.

The investment case depends on time horizon. Short-term (1-3 years), Airbus looks compelling as travel demand recovers and production ramps up. Medium-term (3-7 years), the story is mixed as competition intensifies and environmental pressures mount. Long-term (7+ years), everything depends on whether Airbus can transition to sustainable aviation.

For investors, Airbus represents a classic "quality at a reasonable price" opportunity. It's not a growth stock—aviation is mature. It's not a value stock—the multiple reflects its market position. It's a compounder—steady growth, strong moat, reasonable valuation. In a world of zero interest rates and meme stocks, that might not excite. But for investors who think in decades, not quarters, Airbus offers something rare: a European industrial champion that actually wins.

The key metrics to watch: monthly production rates (especially A320neo), order intake versus deliveries, margin progression, and free cash flow conversion. The key risks to monitor: Boeing's recovery, Chinese competition, supply chain stress, and regulatory changes.

XII. Epilogue & Future Outlook

Standing at the Toulouse delivery center in 2035, watching the first hydrogen-powered A320 successor roll out, future historians will mark this as either Airbus's finest hour or the beginning of its decline. The next decade will determine whether Airbus remains a symbol of European industrial might or becomes another case study in disruption.

The hydrogen bet is existential. Airbus has committed to zero-emission aircraft by 2035—not hybrid, not electric, but hydrogen. This isn't incremental improvement; it's reimagining aviation from first principles. Hydrogen requires new engines, new fuel systems, new airport infrastructure. It's a €100 billion bet that hydrogen will become economically viable and that Airbus can make it work safely.

The urban air mobility market represents both opportunity and threat. Airbus's CityAirbus program is developing electric vertical takeoff aircraft for urban transportation. But so are hundreds of startups with billions in venture funding. If urban air mobility succeeds, it could cannibalize short-haul flights. If it fails, Airbus will have wasted precious resources.

Digital transformation will determine competitive advantage. The aircraft of 2035 won't just be transportation devices—they'll be data platforms. Predictive maintenance, dynamic routing, personalized passenger experiences—software will differentiate as much as hardware. Airbus's Skywise platform is impressive, but competing with Silicon Valley on software is treacherous territory.

The geopolitical landscape is fracturing. The post-war order that enabled Airbus—European integration, global trade, Western technological dominance—is unraveling. A new cold war between the US and China could force countries to choose sides. Europe's strategic autonomy push could limit Airbus's access to American technology and markets. The company that benefited most from globalization might suffer most from deglobalization.

What would success look like in 2035? Airbus would have delivered its 20,000th aircraft. The hydrogen-powered ZEROe would be entering service with launch customers. The company would have captured 40% of the Chinese market despite COMAC. Urban air mobility would be contributing €5 billion in annual revenue. Most importantly, Airbus would have proven that aviation can be sustainable—economically and environmentally.

What would failure look like? Boeing and COMAC would have caught up in technology and production. Environmental regulations would have killed demand for conventional aircraft before hydrogen alternatives were ready. New entrants—perhaps a Tesla of aviation—would have disrupted the market with radical new designs. Airbus would be manufacturing fewer aircraft in 2035 than in 2025.

The key lessons for entrepreneurs and investors are timeless. First, patience pays—Airbus took 50 years to overtake Boeing. Second, complexity can be a competitive advantage if managed well. Third, government support and private enterprise aren't mutually exclusive. Fourth, technical excellence matters more than financial engineering. Fifth, crises are opportunities if handled correctly.

For Europe, Airbus represents something precious: proof that European cooperation can create world-beating companies. In an era of Brexit, rising nationalism, and EU skepticism, Airbus stands as a monument to what Europe can achieve when united. Its success or failure will influence whether Europe pursues more integration or less.

For the industry, Airbus has proven that monopolies aren't inevitable, that incumbents can be overtaken, that patience and persistence can triumph over size and speed. Every startup founder drawing up plans to disrupt an industry should study how Airbus, starting from nothing, overtook the mighty Boeing.

The story isn't over. Aviation in 2050 might be unrecognizable—hydrogen-powered, autonomous, supersonic, or something we can't yet imagine. Airbus might dominate this new world or be disrupted by companies that don't yet exist. But whatever happens, the company that began as an impossible dream—European nations cooperating to challenge American dominance—has already achieved the impossible.

The final lesson might be the most important: in industries with long time horizons, the race doesn't always go to the swift or the strong, but to those who endure. Airbus endured political infighting, technical failures, financial crises, and competitive assault. It survived them all and emerged stronger.

As Guillaume Faury recently said, "We're not building aircraft for the next quarter or the next year. We're building them for the next generation." In a world obsessed with speed, there's something profound about a company that measures success in decades. Whether that patience will be rewarded or punished, only time will tell.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube