Groupe ADP: Europe's Gateway to the World

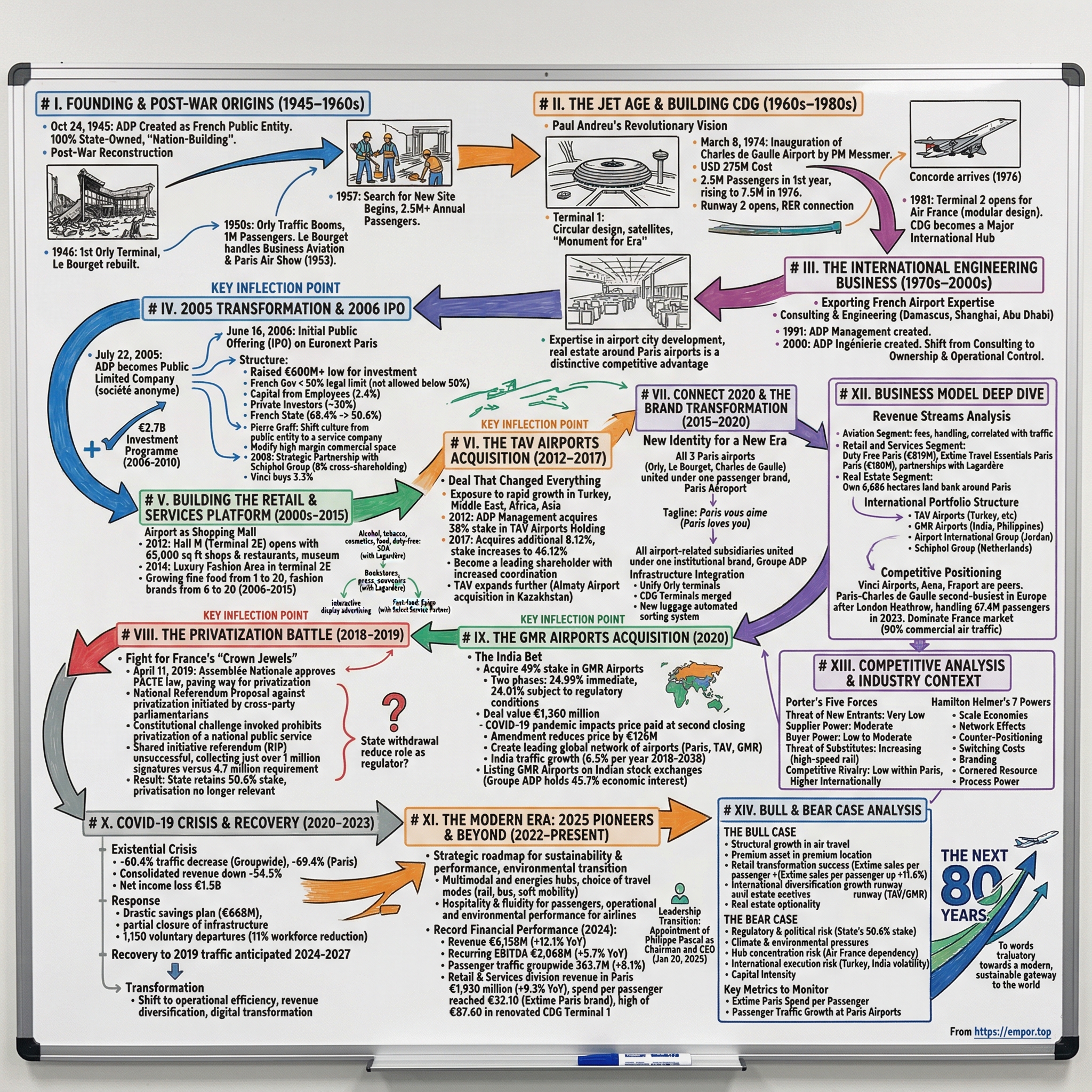

I. Introduction: The Airport Empire Built on French Soil

In the shadow of the Eiffel Tower, approximately 23 kilometers to the northeast, lies one of the world's most remarkable pieces of infrastructure—Paris Charles de Gaulle Airport. Every day, tens of thousands of travelers stream through its iconic circular Terminal 1, many unaware they're walking through a building that helped define modern aviation architecture. Terminal 1 was built in an avant-garde design of a ten-floors-high circular building surrounded by seven satellite buildings, each with six gates allowing sunlight to enter through apertures.

The company behind this gateway—Groupe ADP—represents one of the most fascinating case studies in infrastructure capitalism. Consolidated revenue rose by 12.1% to an all-time high of €6.2 billion in 2024. Recurring EBITDA topped €2 billion for the first time, climbing 5.7% despite the introduction of the long-distance transport infrastructure tax in France. These aren't just numbers on a spreadsheet—they represent the culmination of an 80-year journey from post-war reconstruction to global airport empire.

Passenger traffic groupwide rose by +8.1% to 363.7 million in 2024. To put that in perspective, that's roughly the equivalent of the combined populations of Germany, France, and Italy passing through ADP's airport network in a single year.

The central question for investors: How did a post-war government agency become one of the world's largest airport empires, and what does the unfinished battle over privatization tell us about infrastructure investing? The answer weaves together themes of state capitalism versus privatization, infrastructure as an economic moat, the revolutionary "airport-as-retail-platform" business model, and international expansion through strategic partnerships.

Groupe ADP owns and manages Parisian international airports Charles de Gaulle Airport, Orly Airport and Le Bourget Airport, all gathered under the brand Paris Aéroport since 2016. Groupe ADP operates 26 international airports. It owns 46.1% of TAV Airports Holding, and cross-owns 8% of the Schiphol Group.

The story of Groupe ADP is, in many ways, the story of modern France itself—a narrative of ambitious state planning, gradual privatization, international expansion, and the eternal tension between public infrastructure and private capital. Let's begin at the beginning.

II. Founding & Post-War Origins (1945–1960s)

Rising from the Rubble

Picture Paris in October 1945. The war had ended just months earlier. The Champs-Élysées, once occupied by German soldiers, now hosted victory parades. But France's aviation infrastructure lay in shambles—runways cratered, terminals damaged, and the nation's pride as a pioneer in aviation severely wounded.

Aeroports de Paris, often referred to as ADP, was not established by individual founders but rather as a public industrial and commercial entity by the French government. This governmental initiative took place on October 24, 1945, marking the beginning of its operational history. Aeroports de Paris was created as a public industrial and commercial entity by the French state. Its establishment was a post-war effort to manage critical aviation infrastructure.

At its inception, the ownership of Aeroports de Paris was 100% state-owned. The French government held complete control and equity from the outset. There were no individual founders with equity stakes or shareholdings at the company's inception. Its creation was a direct governmental decision.

This wasn't entrepreneurship in the traditional sense—it was nation-building. The Provisional Government of the French Republic understood that modern air connectivity would be essential to France's economic recovery and its role as a global power. Paris, as the capital of what remained the world's largest colonial empire, needed a world-class aviation hub.

The Orly Era

In 1946, the first provisional terminal at Orly Airport was achieved, as well as the reconstruction of Paris–Le Bourget Airport. Le Bourget, which had hosted Charles Lindbergh's historic landing in 1927, served as Paris's primary airport in the immediate post-war years.

But the real action was happening at Orly. In the 1950s, Orly Airport outgrew Le Bourget's traffic, and became the leading Parisian airport, breaking the 1 million passengers/year milestone. This was a significant achievement—crossing the million-passenger threshold signaled that mass air travel was becoming reality in Europe.

Le Bourget launched the first edition of the Paris Air Show in 1953 and switched to business jet operations in 1976. This decision to specialize Le Bourget in business aviation and air shows rather than commercial traffic proved prescient—the Paris Air Show remains one of the world's premier aerospace events, and Le Bourget's business aviation role provides high-margin services to this day.

The 1950s represented what the French call "Les Trente Glorieuses"—the thirty glorious years of post-war economic boom. After World War II, France experienced an economic boom which lasted almost three decades. This period is often referred to as "Les Trente Glorieuses" or "The Glorious Thirty". During this time growth rates in the country averaged 5% per year. Due to the boom, air travel in the 1950s and 1960s was doubling every five to six years.

By 1957, annual passengers at Paris airports exceeded 2.5 million, with more than 42,000 tons of freight and nearly 112,000 aircraft movements. The numbers were impressive—but ADP's leadership could see they weren't sustainable at the existing facilities.

In 1957, L'aéroport de Paris started to look for a land to build a new Parisian airport.

The need was pressing. Orly, for all its charm and its futuristic Orly-Sud terminal, was hemmed in by suburban development. Expansion was limited, noise complaints were mounting, and the coming jet age would require longer runways and more terminal capacity than Orly could ever provide.

The search for a new site would lead ADP to the wheat fields of Roissy-en-France—and set the stage for one of the most ambitious airport construction projects in history.

III. The Jet Age & Building Charles de Gaulle (1960s–1980s)

A Monument for the Age of Air Travel

The 1960s brought the jet revolution to commercial aviation. Boeing 707s and Douglas DC-8s slashed transatlantic flight times, making international air travel accessible to the growing middle class. Paris's airports strained under the weight of this new demand.

Between 1954 and 1968, the population of the Paris region grew by 25% to 8 million inhabitants. It was projected that by 2000, the population would swell to 14 million. In 1965, Le Bourget and Orly Airport together handled less than 5 million passengers. The demand was forecast to grow eight-fold to 40 million passengers by the mid-1980s, only 20 years away.

Construction began in 1964, at which point the project had the working title of Paris-Nord Airport. However, before opening its name was changed, initially to Roissy Airport, before ultimately opening as Roissy-Charles De Gaulle Airport in honor of the former President of France who had died in 1970 and had been instrumental in getting the airport built. The airport eventually dropped the reference to the nearby town and became known simply as Paris-Charles De Gaulle Airport, the name it still goes by today.

The planning and construction phase of what was known then as Aéroport de Paris Nord began in 1966. On 8 March 1974 the airport, renamed Charles de Gaulle Airport, opened.

Paul Andreu's Revolutionary Vision

Terminal 1 was designed by young avant-garde architect Paul Andreu. March 8th 1974 saw the Inauguration of Terminal 1 at Paris-Charles de Gaulle by Prime Minister Pierre Messmer. It has an annual capacity of 10 million passengers.

After eight years of construction and at a cost of USD 275 million (USD 1.4 billion in 2019) the airport was opened on March 8th, 1974 by Prime Minister Pierre Messmer, during a sober one-hour ceremony with 1,000 spectators in attendance.

The design was unlike anything the aviation world had seen. Newspaper headlines of around the time of opening described the building as "A monument that will mark an era", "a travel machine" and even "Monster"! The fluidity of the routes, by car, on foot, by plane, in the interweaving of curves and in the maze of halls and tunnels, lead many commentators to compare the stay in the airport to a journey. One newspaper wrote: "A worrying construction, brilliant and Kafkaesque, monstrously beautiful and to which it will take getting used to in order to be worthy."

The Hub Takes Shape

Use of the airport grew quickly; it handled 2.5 million passengers in the first year, which had risen to 7.5 million in 1976. The second runway opened that year, as did the RER connection to the city.

Concorde arrived at the airport in 1976. Together with London Heathrow, Paris Charles de Gaulle became one of the first airports to operate commercial Concorde flights. On January 21st, 1976, at 1140, two aircraft took off simultaneously; the Air France one bound from Charles de Gaulle to Rio de Janeiro. Concorde was then a regular sight at the airport until its retirement in 2003.

The airport's design reflected a confidence in France's technological prowess—the same confidence that produced the Concorde, the TGV high-speed train, and the Ariane rocket program. CDG wasn't just an airport; it was a statement about France's place in the modern world.

The 1980s brought continued expansion. Terminal 2 began operations in 1981, designed specifically for Air France and featuring a more modular, linear design that allowed for easier expansion. This symbiotic relationship between ADP and Air France—the national airport authority and the national carrier—would prove crucial to CDG's development as a major international hub.

The TGV station at CDG, opened in 1994, represented a pioneering example of intermodal connectivity, allowing passengers to transfer directly between high-speed rail and international flights. This vision of the airport as a multimodal hub—not just an aviation facility—would later become central to ADP's strategic positioning.

IV. The International Engineering Business (1970s–2000s)

Exporting French Airport Expertise

Even as it built CDG, ADP was developing a parallel business line that would prove crucial to its later transformation: international airport consulting and engineering.

Starting in the 1970s, Aéroports de Paris became an active airport developer in other countries, contributing to the construction of the terminal 1 of the Abu Dhabi International Airport, the terminal 1 of the Shanghai Pudong International Airport, the Mohammed V International Airport, the Damascus International Airport, the Arturo Merino Benítez International Airport.

This wasn't just consulting work—it was building institutional capability and global reputation. When developing nations needed world-class airport infrastructure, they increasingly turned to ADP. The company understood something crucial: airport expertise is highly specialized and difficult to replicate. You can't Google how to build a 10-million-passenger terminal.

Building the Institutional Framework

ADP Management was created as a fully owned subsidiary in 1991 to consolidate the group's growing participations in airports and other industry-related assets.

ADP Ingénierie was created in 2000 as a fully owned subsidiary to provide large-scale engineering for airport-related development projects.

These structural moves signaled a shift in ambition. ADP was no longer content to merely advise on airport development—it wanted ownership stakes and operational control. The engineering work served as a foot in the door, building relationships that could later be converted into equity positions.

By the early 2000s, ADP had accumulated significant international experience and a reputation for delivering complex infrastructure projects. What it lacked was the capital structure to pursue major international investments. That constraint was about to change dramatically.

V. Key Inflection Point #1: The 2005 Transformation & 2006 IPO

The End of an Era—and Beginning of Another

The year 2005 marked the most significant transformation in ADP's 60-year history. A significant transformation occurred on July 22, 2005, when Aeroports de Paris changed its legal status from a public entity to a public limited company (société anonyme), setting the stage for its partial privatization. The company completed its initial public offering on June 16, 2006, listing on the Euronext Paris stock exchange, with the French state retaining a majority stake.

To understand why this mattered, consider the constraints ADP faced as a pure public entity. Capital for expansion came from government budgets competing with healthcare, education, and defense. Decision-making was slow, bureaucratic. International expansion required political approval at every turn.

The ownership structure of Aéroports de Paris (ADP) saw a significant shift with its initial public offering (IPO) in June 2006, which reduced the French government's stake and introduced new investors. This move aimed to provide greater access to capital for the company's development and international ambitions.

Pierre Graff and the Transformation Imperative

Pierre Graff, appointed executive chairman in 2004 to prepare AdP for privatisation, hoped the IPO would accelerate changes he had begun to put in place. ADP has to "modify its culture and create a service company", he says. Since arriving, Mr Graff has restructured the company, giving each airport its own chief executive, with divisional managers and the freedom to develop individual profit centres. The moves have revealed a lack of high margin commercial space in AdP compared with rivals.

The French operator derives only 25 per cent of its 1.9bn ($2.4bn) turnover from commercial activities versus 40 per cent at BAA of the UK. This weakness could explain AdP's feeble margins of 31 per cent, against BAA's estimated 44 per cent. But with debt standing at more than 100 per cent of shareholders' funds, Mr Graff needs money. So the government is selling 30-40 per cent of the group to raise 500m-600m for AdP and up to 800m for itself.

The IPO Structure

Following the airport reform of 2005, the French government proceeded the next year to the partial privatization of the 'Société Anonyme Aéroport de Paris'. This first capital increase raised over 600 million euros. About 30% of the capital was then transferred to private investors, the remainder going to employees of ADP (2.4%) and the French State (68.4%).

Later, the share of the French state diminished twice, once in 2008 (as a result of a strategic partnership with Amsterdam Schiphol) and then again in 2009 (after selling some of the capital to the Strategic Investment Fund). Now, the share of the French state represents only 50.6%.

The IPO was designed to balance multiple objectives: raising capital for investment, modernizing corporate governance, introducing market discipline, while maintaining strategic state control. The airport law of 2005 does not allow the State to go below 50% of the capital of Paris Airport.

The Strategic Partnership with Schiphol

Aéroports de Paris became a public company on 20 April 2005, although the French government retained a majority of the company's shares. In 2008, Aéroports de Paris and Schiphol Group signed a strategic partnership that involved buying 8% of each other's shares to seal the deal. In 2008, French conglomerate Vinci also bought 3.3% of Aéroports de Paris, calling the airport operator "the heart of its strategic aims".

The cross-shareholding with Schiphol was particularly clever. It created alignment between two of Europe's major hub airports, enabling cooperation on issues ranging from slot coordination to retail best practices. It also provided a defense against hostile takeovers—any would-be acquirer would need to negotiate with both Paris and Amsterdam.

The capital increase will give Aéroports de Paris the resources to implement its business plan to become the premier European airport group. The plan is based on a major programme to invest €2.7 billion between 2006 and 2010.

For investors, the 2006 IPO marked the birth of a new type of infrastructure investment opportunity—a chance to own a piece of one of the world's most valuable airport systems, with the regulatory clarity of a modern economic framework and the strategic security of continued state involvement.

VI. Building the Retail & Services Platform (2000s–2015)

The Airport as Shopping Mall

Walk through any major airport today, and you'll be struck by the sheer volume of retail space—luxury boutiques, duty-free shops, restaurants, lounges. This wasn't always the case. The transformation of airports from transit facilities to "retail destinations" represents one of the most significant business model innovations in infrastructure history.

ADP was at the forefront of this transformation. In 2012, Aéroports de Paris and Air France decided to work together towards embellishing the experience in Parisian airports and turn Paris-Charles de Gaulle into a competitive hub for international connections. Aéroports de Paris opened the new Hall M in Terminal 2E in July 2012 (7.8 million passengers/year capacity) which contains 65,000 square feet of shops and restaurants, a museum, and Air France's largest business lounge.

In November 2014, Aéroports de Paris opened a luxury fashion area in terminal 2E, Hall K of the Paris-Charles de Gaulle Airport. From 2006 to 2015, the number of fine food restaurants grew from 1 to 20 in Paris-Charles de Gaulle Airport, and style fashion brands from 6 to 20.

The Joint Venture Model

Rather than operating retail directly, ADP developed a sophisticated joint venture model that leveraged partner expertise while maintaining control.

Société de Distribution Aéroportuaire (Groupe ADP and Lagardère Travel Retail): management of the sales of alcohol, tobacco, cosmetics, food, and duty-free related products in Parisian airports.

Relay@ADP (Groupe ADP and Lagardère): management of bookstores, press and souvenirs stores (travel essentials) in Parisian airports.

In 2011, Aéroports de Paris and French JCDecaux created the joint-venture branded JCDecaux Airport Paris to handle the interactive display advertising system in Parisian airports.

In 2015, Aéroports de Paris and Select Service Partner created the company Epigo to manage fast-food shops in the Charles de Gaulle Airport.

Diversification into Telecommunications

In 2001, Aéroports de Paris created its own telecommunications operator, ADP Telecom, which became Hub Telecom a year later, and finally Hub One in 2012. In 2006, Hub One was involved in the creation of Bolloré telecom, thus holds minority shares in the company. In 2016, Hub One deployed the free guest wifi network across the Parisian airports.

Hub One represented a diversification play—airports generate enormous telecommunications demand (security systems, passenger wifi, cargo tracking), and owning the infrastructure provider creates both operating synergies and additional revenue streams.

The Competitive Advantage

Unlike some competitors who primarily focus on airport management, ADP has diversified its business model to include substantial retail, real estate, and service components, which provide resilience against fluctuations in aeronautical revenues. A distinctive competitive advantage for Groupe ADP is its expertise in airport city development, with significant real estate projects around its Paris airports.

By 2015, ADP had assembled a comprehensive retail and services platform that differentiated it from pure-play airport operators. This capability would prove crucial as ADP sought to expand internationally—it could offer not just airport management expertise, but a complete ecosystem of retail, services, and real estate development capabilities.

VII. Key Inflection Point #2: The TAV Airports Acquisition (2012–2017)

The Deal That Changed Everything

In 2012, ADP made the boldest move in its history as a public company. In 2012, in addition to its existing 8% share, ADP Management acquired 38% of TAV Airports Holding, the leading airport operator in Turkey that used to operate the Istanbul Atatürk International Airport as well as airports in Georgia, Tunisia, North Macedonia, Latvia and Saudi Arabia.

The company embarked on an international expansion strategy in the 2010s, acquiring a 38% stake in TAV Airports in 2012 (later increased to 46.12% in 2017), which operates airports primarily in Turkey and the Middle East. In 2020, ADP completed another significant acquisition by purchasing...

Increasing the Stake

Aéroports de Paris SA, mother company of Groupe ADP, through its subsidiary Tank ÖWA alpha GmbH, entered into a share purchase agreement, signed on 9 June 2017, with Akfen Holding A.Ş. ("Akfen Holding") for the acquisition of Akfen Holding's whole stake in TAV Havalimanları Holding A.Ş. ("TAV Havalimanları Holding" or "TAV Airports"). Groupe ADP has been a 38% shareholder of TAV Airports since 2012. With this transaction, Groupe ADP will acquire an 8.12% stake in TAV Airports, for an amount of USD160 million.

Augustin de Romanet, CEO of Aéroports de Paris SA – Groupe ADP announced: "The reinforcement of Groupe ADP in the capital of TAV Airports is in the continuity of the solid and virtuous partnership in place since 2012. The acquisition of 8.12% of TAV Airports' shares will enable Groupe ADP to bring its stake to 46.12% so that to become a leading shareholder of TAV Airports with an increased involvement in this strategic asset. This operation will allow increased cooperation and coordination between Groupe ADP and TAV Airports. Moreover, this transaction shows the confidence that Groupe ADP has in TAV Airports potential of development, especially for the expansion in the fast growing areas such as the Middle East, Africa and Asia. Groupe ADP also renews its trust in the management of TAV Airports, led by a remarkable entrepreneurial spirit."

TAV's Continued Expansion

TAV itself continued to expand, most notably acquiring Almaty Airport in Kazakhstan. A consortium led by TAV Airports (of which Groupe ADP owns 46.38% of the capital) has signed on May 7th, 2020 a Share Purchase Agreement to acquire 100% of the shares of Almaty Airport and the associated jet fuel activities, which will be delegated to a dedicated operator, and services for an Enterprise Value of $415 million. The share transfer of Almaty Airport took place on April 29th, 2021. Almaty Airport is now fully owned by the consortium of which TAV Airports is an 85% shareholder.

The strategic logic was compelling. Turkey was experiencing rapid economic growth and becoming a major crossroads between Europe, Asia, and the Middle East. Istanbul Atatürk Airport (before its replacement by Istanbul Airport) was emerging as a serious hub competitor to traditional European gateways. Through TAV, ADP gained exposure to this growth while diversifying its geographic risk.

VIII. Connect 2020 & the Brand Transformation (2015–2020)

A New Identity for a New Era

In November 2015, the group's CEO Augustin de Romanet announced ADP's strategic programme Connect 2020. The plan includes a major overhaul of the company's branding organization: All 3 Parisian international airports (Orly, Le Bourget, Charles de Gaulle) are united under one passenger brand, Paris Aéroport. All other airport-related subsidiaries of ADP are united under one institutional brand, Groupe ADP. The rebranding shift became effective in April 2016.

Following the announcement of the Connect 2020 plan, the passenger brand Paris Aéroport was applied to Parisian international airports (Charles de Gaulle, Orly and Le Bourget). The goal is two-fold: Attract more visitors to the Parisian airports, and thus turn Paris Aéroport into a demonstration of Groupe ADP's expertise in airport management worldwide. The Paris Aéroport brand borrows the love effect associated with the French capital to define its airport experience, choosing Paris vous aime (Paris loves you) as its tagline.

While Paris-Charles de Gaulle, Paris-Orly and Paris-Le Bourget airports enjoy wide recognition, our former brand, Aéroports de Paris, was insufficiently known to the general public and no longer in line with our desire to offer world-class customer care and services. We wanted to create a single identity that is modern and representative of this promise, in order to write a new page in the history of the company. This explains a strong two-fold choice: the creation of a Group brand, Groupe ADP, and a traveller brand, Paris Aéroport. This two-pronged identity will enable us to unite our employees and attract new talented people, but also to make us better known to our clients and partners in France and abroad.

Infrastructure Integration

The Connect 2020 also planned to follow through with the project to unify Orly South and West terminals. In Charles de Gaulle, Terminals of the Satellite 1 will be merged, as well as terminal 2B and 2D. A new luggage automated sorting system and conveyor under Terminal 2E Hall L to speed luggage delivery time for airlines operating Paris-Charles de Gaulle's hub. The CDG Express, the direct express rail link from Paris to Charles de Gaulle Airport, is planned for completion by 2027.

The terminal integration strategy addressed a longstanding criticism of Paris airports—the fragmented, confusing passenger experience. By merging previously separate facilities and creating seamless connections, ADP aimed to improve its competitive position against rivals like Amsterdam Schiphol and Frankfurt.

IX. Key Inflection Point #3: The Privatization Battle (2018–2019)

The Fight for France's "Crown Jewels"

In 2018, the Macron government proposed a dramatic acceleration of ADP's privatization—potentially selling the state's entire remaining stake. The battle that ensued offers a masterclass in the politics of infrastructure ownership.

Following growing controversy surrounding the French government's plans to privatize the Aéroports de Paris (ADP) group, Nathalie Roseau looks back at the history of this organization and questions the wisdom of such a reform. On April 11, 2019, France's lower house of parliament, the Assemblée Nationale (National Assembly) approved a law known as PACTE (Plan d'Action pour la Croissance et la Transformation des Entreprises – Action Plan for Growth and Transformation of Enterprises), paving the way for the complete privatization of the Aéroports de Paris (ADP) group, in which the French state is currently the majority shareholder.

On 10 April, a large cross-party group of French parliamentarians gathered enough support to initiate a national referendum proposal against the privatization of Groupe ADP, the operator of Paris's three major international airports, Charles de Gaulle, Orly, and Le Bourget. The lower house of parliament, which is controlled by President Emmanuel Macron's Republic on the Move (Le République En Marche: LREM), had earlier approved the privatization as part of the so-called Pacte Law. The state currently owns 50.6% of ADP, worth an estimated EUR9 billion (USD10 billion).

The Constitutional Challenge

The Conseil constitutionnel has validated several provisions of the PACTE Law, including those authorising the privatization of Aéroports de Paris and La Française des Jeux. Several members of the Parliament submitted a claim before the Conseil constitutionnel in relation to the constitutionality of the provisions of the PACTE law (the Law PACTE), which has just been validated by the French Parliament. Most notably, the members of Parliament requested the cancellation of the provisions of Law PACTE which authorises (i) the privatization of Aéroports de Paris (ADP) and (ii) La Française des Jeux (FDJ). They invoked that ADP and FDJ could not in fact be privatized, in accordance with the Preamble to the 1946's French Constitution, which prohibits the privatization of a company having the character of (a) a de facto monopoly or (b) a national public service.

The Unprecedented Referendum Attempt

This is the first time that opposition deputies have united to force a referendum on proposed legislation. Such a provision - which requires the support of one-fifth of the members of both houses of parliament (185 of 925) - has never been used since it was added to the constitution in 2008 to increase participatory democracy.

The shared initiative referendum (RIP) launched to try to block the privatization of Groupe ADP (Paris Aéroport) was unsuccessful. Its initiators had until March 12 to collect the necessary number of signatures. They did not succeed. While 4.7 million initials representing 10% of the electorate were to be collected, just over 1 million were counted.

If there is a victory, it is only collateral: given the market climate, the privatization of ADP is no longer relevant.

What the Privatization Debate Revealed

This trajectory—simultaneously part of economic globalization and a major contributor to it—questions the role of the state as a shareholder of Paris's airports. While ADP has excelled in making the businesses within its precincts profitable, in order to increase the share of dividends paid out to its shareholders and finance its strategic infrastructures, does this justify the state having to sell its assets to the private sector by accelerating the process of commodification? A total transfer from the state, meaning its withdrawal from the decision-making and management bodies of ADP, would also imply a reduction in its role as a regulator.

The failed privatization attempt left ADP in an interesting position—publicly traded with a 50.6% state stake that legally cannot be reduced below majority ownership. This hybrid model means ADP has access to capital markets while enjoying implicit state backing, a structure that provides both opportunities and constraints.

X. Key Inflection Point #4: The GMR Airports Acquisition (2020)

The India Bet

Even as the privatization debate raged in France, ADP was executing its most ambitious international expansion yet. Aéroports de Paris SA: With the acquisition of 49% of the Indian group GMR Airports, Groupe ADP creates the leading global network of airports. Groupe ADP has signed a share purchase agreement to buy, under certain conditions, a 49% stake in GMR Airports. The operation will unfold in two phases: a first phase will be realized within the coming days for a 24.99% stake. The second phase, for 24.01%, is subject to certain regulatory conditions, notably obtaining the customary regulatory approvals for that type of project, in particular from the Reserve Bank of India. It will be concluded during the upcoming months. Once this operation completed, GMR Airports will be jointly owned with GMR Infrastructure Limited ("GIL"), listed entity of GMR Group, which will keep a 51% stake and retain control over the company. Groupe ADP will be granted highly extended governance rights.

The total purchase price for the 49 per cent stake is 107.8 billion INR (around €1,360 million).

GMR Airports' portfolio incorporates seven airports in India, the Philippines and Greece. These include India's Delhi International Airport and Hyderabad International Airport, which are carbon neutral, and the Philippines' Mactan-Cebu Airport. The other four airports include Goa Airport in India and Heraklion in Greece, which are currently under construction. In addition, the company won the bidding process for airports in Nagpur and Bhogapuram, India.

COVID-19 Impact on the Deal

In order to take into account the pandemic impact linked to the Covid-19 on the aviation sector and its medium term perspectives in the airports of GMR Airports, Groupe ADP and GMR have signed, on July 7 2020, an amendment to the share purchase agreement and the shareholders' agreement. As per the amendment, the price paid at second closing is reduced by Rs. 1,060 Crores (126 million euros) compared to the initial purchase price of Rs. 5,532 Crores (658 million euros). The amendment plans, for the second investment phase, to acquire 24.01% in GMR Airports and will now be structured in two parts: A net fixed amount, paid immediately at the second closing, of Rs. 4,472 Crores (532 million euros), including Rs. 1,000 Crores (119 million euros) of capital increase in GMR Airports; An earn-out clause, for a potential amount of up to Rs.

The Strategic Rationale

Driven by a very dynamic economy, air traffic in India is expected to rise by 6.5% per year on average between 2018 and 2038.

The financial operation includes a strategic industrial partnership with GMR regarding business development in aviation, retail, IT, hospitality, innovation and engineering. This operation also prepares Groupe ADP's future growth, with the existing assets, with the expected air traffic growth, the long run horizon of their concessions and the large capacity reserves, as well as the future acquisitions. With three major development platforms – Groupe ADP, TAV Airports and GMR Airports – this operation gives birth to the leading global network of airports.

Creating a Listed Indian Entity

The Boards of Directors of Aéroports de Paris (Groupe ADP) and GMR Airports Infrastructure Ltd (GIL), both listed companies and co-shareholders of a respectively 49% and 51%-stake in the airport holding GMR Airports Ltd (GAL), have approved the execution of a Framework Agreement initiating the process aiming at a merger between GIL and GAL in the first half of 2024 ("New GIL"). The contemplated merger, will allow Groupe ADP to become shareholder of an airport company listed on BSE Limited and National Stock Exchange of India Limited ("Indian Stock Exchanges"), as contemplated when acquiring its stake in GAL in 2020. This operation will: Simplify and clarify the capital structure of the airport holding company; Fully reveal the value of GAL and provide liquidity to the stake held by Groupe ADP; Make New GIL a more agile development platform to capture new opportunities in India and South-East Asia.

With our partner GMR Group, we have finalized the operation making GMR Airports a company listed directly on the Indian financial markets, in which Groupe ADP holds a 45.7% economic interest.

XI. COVID-19 Crisis & Recovery (2020–2023)

The Existential Crisis

The COVID-19 pandemic represented the most severe crisis in aviation history. Groupe ADP traffic: decrease by -60.4%, at 96.3 million passengers (excluding traffic at Istanbul Atatürk and excluding GMR Airports platforms in 2019); Paris Aéroport traffic (Paris-Charles de Gaulle and Paris-Orly): -69.4% at 33.1 million passengers; Consolidated revenue down by -54.5%, at 2,137 million, due to the important impact of the Covid-19 pandemic on the revenue from aviation and retail activities in Paris as well as from TAV Airports and AIG on the international level; Positive EBITDA at +€168 million, down by -€1,604 million (-90.5%).

The net income stood at -€1,516 million over 2020. Taking into account all these items, the net result attributable to the Group was down by €1,757 million, at -€1,169 million.

This is the first time in 50 years that air traffic has experienced a downturn this abrupt and it is established that the recovery will be very gradual: a return to the 2019 traffic level in Paris is anticipated between 2024 and 2027.

The Response

2020 results "Bear the traces of a brutal and unprecedented crisis", But "Also record the exceptional efforts of the group" to face it, mentioning the deployment of a drastic savings plan of 668 million euros. This plan, including a partial closure of infrastructure, including some passenger terminals, has helped maintain a positive gross operating surplus, at 168 million euros.

ADP announced the signing in December of a collective contractual termination agreement setting at 1,150 the maximum number of voluntary departures – of which 700 will not be replaced – and making it possible to avoid forced departures. In total, the group, of which the State is the majority shareholder, will part with 11% of its pre-crisis workforce.

Recovery and Transformation

The competitive landscape has evolved significantly following the COVID-19 pandemic, with airport operators focusing on operational efficiency, diversification of revenue streams, and digital transformation. Groupe ADP has responded with its "2025 Pioneers" strategic plan, emphasizing sustainability, innovation, and service quality. The company has invested heavily in contactless technologies, biometrics, and artificial intelligence to enhance passenger experience and operational efficiency.

XII. The Modern Era: 2025 Pioneers & Beyond (2022–Present)

The New Strategic Vision

Groupe ADP has adopted a 2022-2025 strategic roadmap to build the foundation of a new airport model geared towards sustainability and performance, in line with societal and environmental expectations. This strategic roadmap is associated to a financial trajectory.

In this long-term vision, the group wishes to make its airports multimodal and energy hubs designed and operated in a sustainable way. It aims at excellence in hospitality and fluidity for its passenger customers and operational and environmental performance for its airline customers. Finally, it develops a multi-local approach to a culture of innovation and responsibility by placing its action at the heart of the regions in which it operates. The "2025 Pioneers" strategic roadmap is a first step in this long-term transformation by defining the priority projects and actions for the period 2022-2025.

At the heart of the industrial transformation initiated for 2025 Pioneers is the evolution of airports towards multimodal and energies hubs: which will no longer be a place to fly, but a place where one benefits from renewed connectivity, offering them a choice between different modes of travel (long and short-distance rail, bus, soft mobility, etc.), and where rail-air connections will account for a growing share of the development of Groupe ADP's hubs.

Record Financial Performance

Group revenue hit a record high of €6,158 million, up +12.1% year-on-year, with recurring EBITDA up +5.7% at €2,068 million, ahead of target and aided by the performance of TAV Airports. Passenger traffic groupwide rose by +8.1% to 363.7 million.

Groupe ADP has reported solid financial results for 2024, with Retail and Services division revenue at its Paris airports climbing by +9.3% year-on-year to €1,930 million. This outstripped the +3.7% rise in passenger traffic to 103.4 million at Paris Charles de Gaulle and Orly airports.

Spend per passenger at the group's retail and hospitality outlets (under the Extime Paris brand) grew +4.9% year-on-year to €32.10, and reached an impressive high of €87.60 in the renovated CDG Terminal 1.

Leadership Transition

Appointment of Mr. Philippe PASCAL as Chairman and Chief Executive Officer (CEO) of Groupe ADP. In accordance with the wishes expressed by the President of the French Republic in a press release dated January 20th, 2025, and following his hearings by the relevant parliamentary commissions, following a meeting of the Board of Directors held today, Mr. Philippe Pascal was appointed Chairman and CEO of the company with effect from today.

Mr. Philippe Pascal, Inspector General of Finances, has been Deputy Executive Officer of the company in charge of finance, strategy and administration since May 2016. Born in 1971, he joined Groupe ADP in February 2013 as Director of Financial Operations and Participations, then Director of finance, management and strategy.

The foundation laid by the Pioneers 2025 strategic roadmap should now enable us to accelerate the Group's transformation. We intend to increase our investment in infrastructure, underpinned by a long-term vision.

XIII. Business Model Deep Dive

Revenue Streams Analysis

Groupe ADP operates through three primary business segments: Aviation, Retail and Services, and Real Estate. This diversification provides meaningful revenue stability and cross-selling opportunities.

Aviation Segment The aviation segment includes airport fees (landing fees, parking fees, passenger fees), ground handling income, and related services. This segment is directly correlated with passenger traffic and aircraft movements—when planes land and passengers travel, ADP earns fees.

Retail and Services Segment Within the commercial performance, revenue from Extime Duty Free Paris increased by +8.3% to €819 million, with Extime Travel Essentials Paris up +52.5% to €180 million. Both are ADP partnerships with Lagardère Travel Retail. Higher footfall and new store openings played a part, said ADP. EBITDA within Retail and Services slipped by -5.5% to €735 million.

The Extime brand represents ADP's integrated approach to airport hospitality and retail. Rather than simply leasing space to third-party retailers, ADP actively manages the retail experience through joint ventures, sharing in the upside while maintaining quality control.

Real Estate Segment Real estate: Groupe ADP owns 6,686 hectares of land, including 4,601 hectares for its aviation activities and 1,310 hectares for real estate purposes. Those assets are managed through several subsidiaries including Cœur d'Orly Investissement and Roissy Continental Square.

This land bank represents a substantial hidden asset—6,686 hectares of land around one of the world's most expensive cities, with development rights that extend over decades.

The International Portfolio Structure

Groupe ADP's international operations now contribute significantly to group results:

- TAV Airports (46.1% stake): Turkey, Georgia, Tunisia, North Macedonia, Latvia, Saudi Arabia, Kazakhstan

- GMR Airports (45.7% economic interest): India, Philippines (Delhi, Hyderabad, Goa, Mactan-Cebu)

- Airport International Group (51% stake): Jordan (Queen Alia International Airport)

- Schiphol Group (8% cross-shareholding): Netherlands

Competitive Positioning

The main listed airport operators in Europe are Aena, Groupe ADP and Fraport. In Europe, VINCI Airports operates 10 airports in Portugal (69.2 million passengers), 12 airports in France (18.9 million passengers) including Lyon-Saint Exupéry (10.5 million passengers), and Belgrade airport in Serbia (8.4 million passengers), and took over operations at Budapest airport in Hungary (17.5 million passengers) in June 2024.

In terms of passenger traffic, Groupe ADP's Paris-Charles de Gaulle Airport ranks as the second-busiest airport in Europe after London Heathrow (operated by Heathrow Airport Holdings), handling 67.4 million passengers in 2023 compared to Heathrow's 79.2 million. Within France, ADP holds a dominant position, with its Paris airports handling approximately 90% of the country's commercial air traffic.

XIV. Competitive Analysis & Industry Context

Porter's Five Forces Analysis

Threat of New Entrants: Very Low Airport infrastructure represents one of the highest barriers to entry in any industry. Building a new major airport requires billions in capital, decades of planning, and government approval that is extraordinarily difficult to obtain. Around major metropolitan areas like Paris, there simply is no available land for competitive airport development. ADP's position in the Paris market is effectively unassailable.

Supplier Power: Moderate ADP's key suppliers include construction contractors, technology providers, and various service companies. While switching costs exist, ADP's scale gives it significant bargaining leverage. The more concerning supplier dynamic is with airlines—major carriers like Air France can exert pressure on fees and terms.

Buyer Power: Low to Moderate Passengers have limited choice when flying into a major city—if you want to go to Paris, you're using ADP airports. Airlines have more leverage, particularly major hub carriers, but even they have limited alternatives given the importance of the Paris market.

Threat of Substitutes: Increasing High-speed rail represents the primary substitution threat. The Paris-Lyon TGV effectively eliminated short-haul air traffic on that route. The expansion of rail networks across Europe continues to cannibalize some short-haul demand. However, for international and intercontinental travel, there is no substitute for air.

Competitive Rivalry: Low within Paris, Higher Internationally Within the Paris market, ADP faces essentially no direct competition. Internationally, airport operators compete for concessions and acquisitions. The major listed operators—Aena, Fraport, and Groupe ADP—compete for airport privatizations globally.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Present but not dominant. Airport operating costs don't decline dramatically with scale, though there are benefits in procurement and corporate overhead.

Network Effects: Limited direct network effects, though airline hub status creates indirect effects—a larger hub attracts more connecting traffic, which attracts more airlines, creating a virtuous cycle.

Counter-Positioning: ADP's hybrid public-private model and integrated retail approach represent counter-positioning versus purely private operators or government agencies.

Switching Costs: Extremely high. Airlines that have built hub operations at CDG cannot easily relocate to another airport.

Branding: The Paris Aéroport brand benefits from association with the city. Paris as a destination provides inherent brand value.

Cornered Resource: ADP's 6,686 hectares of land around Paris represents a cornered resource that cannot be replicated.

Process Power: ADP's decades of experience in airport design, construction, and operations represent accumulated process knowledge that competitors cannot easily match.

XV. Bull & Bear Case Analysis

The Bull Case

Structural Growth in Air Travel Global air travel continues to grow at roughly GDP+ rates, driven by rising middle-class populations in emerging markets and increasing globalization. India, where ADP holds significant exposure through GMR, represents one of the fastest-growing aviation markets globally.

Premium Asset in Premium Location Paris is consistently ranked among the world's top tourist destinations. The city's cultural, business, and diplomatic importance provides resilient demand regardless of economic cycles. CDG's role as Air France's hub creates natural advantages for connecting traffic.

Retail Transformation Working In Paris, the success of the new Extime hospitality brand materializes into an outstanding retail performance: Extime Paris sales per passenger reached a record level of 30.6 euros, an increase of +11.6% compared to 2022.

The Extime strategy demonstrates ADP's ability to extract more value per passenger—a lever that can drive growth even with modest traffic increases.

International Diversification Provides Growth Runway TAV and GMR provide exposure to faster-growing markets while diversifying risk. The successful execution of the GMR listing creates a liquid, transparent vehicle for the India investment.

Real Estate Optionality The development potential of ADP's land holdings around Paris airports represents substantial optionality not fully reflected in current valuations.

The Bear Case

Regulatory and Political Risk The failed privatization attempt demonstrates the political sensitivity around ADP. The state's 50.6% stake creates potential for government intervention in pricing, investment decisions, and strategy.

Climate and Environmental Pressures Aviation faces increasing environmental scrutiny. France has already banned short-haul flights where rail alternatives exist. Carbon taxes and sustainable aviation fuel mandates could increase costs and dampen demand.

Hub Concentration Risk Dependence on Air France as the primary hub carrier creates concentration risk. Airline industry consolidation or competitive shifts could affect CDG's hub status.

International Execution Risk The GMR and TAV investments involve operating in jurisdictions with different regulatory frameworks, political risks, and currency exposures. Turkey's economic volatility and India's complex regulatory environment present ongoing challenges.

Capital Intensity Airports require continuous capital investment for maintenance, expansion, and modernization. The CDG Express project and ongoing terminal renovations represent substantial commitments.

Key Metrics to Monitor

For investors tracking Groupe ADP, two KPIs stand out as most critical:

-

Extime Paris Spend per Passenger: This metric captures the retail monetization efficiency and reflects the success of the Extime brand transformation. The target trajectory toward €32+ represents meaningful incremental value creation.

-

Passenger Traffic Growth at Paris Airports: While group traffic includes international operations, Paris airport traffic drives the majority of high-margin revenue. Monitoring the pace of recovery and growth at CDG and Orly provides the best leading indicator of financial performance.

XVI. Conclusion: The Next 80 Years

2025 marks 80 years since the Company was founded.

From the rubble of post-war France to the largest airport network in Europe, Groupe ADP's journey represents a masterclass in patient infrastructure development. The company that began as a government rebuilding effort has transformed into a sophisticated, publicly-traded operator with global reach and diversified revenue streams.

The investment case rests on several structural advantages: irreplaceable Parisian assets with near-monopoly characteristics, proven capability in retail and hospitality, international growth options through TAV and GMR, and substantial real estate optionality. Against these strengths, investors must weigh political and regulatory risks, environmental pressures on aviation, and execution challenges in international markets.

Groupe ADP's ambition is to continue its transformation and become a global reference in terms of attractiveness and hospitality, while serving as a model for environmental transition for the entire aviation industry.

What Groupe ADP demonstrates is that world-class infrastructure can generate attractive returns over extended time horizons. The company's evolution from pure-play airport operator to integrated airport-retail-real estate platform shows how infrastructure businesses can adapt and create value across market cycles.

For long-term investors seeking exposure to global mobility trends, premium real assets, and sophisticated management of complex infrastructure, Groupe ADP represents a distinctive opportunity—one that combines the stability of essential infrastructure with the growth potential of emerging market aviation and the value creation opportunities of retail transformation.

The next 80 years will bring challenges that today's management can scarcely imagine—perhaps hydrogen-powered aircraft, perhaps revolutionary changes in mobility, perhaps shifts in global travel patterns we cannot foresee. What seems certain is that as long as people want to visit Paris, to connect through its airports, to experience one of the world's great cities, Groupe ADP will remain at the heart of that movement—Europe's enduring gateway to the world.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube